Embed Size (px)

Citation preview

Minnesota Adoption of the Green Book

April 16, 2015Jo KaneInternal Control & Accountability Specialist

History of Internal Control Legislation

• Included in the Governor’s 2010-2011 budget recommendations

• Passed by the Legislature in the 2009 session (Minn. Statute Section 16A.057)

• Originally budgeted for up to 6 staff

MS 16A.057 Responsibilities

• Adopt statewide internal control standards and policies

• Coordinate agency training and assistance• Share internal audit resources• Monitor Office of the Legislative Auditor

reports• Report biennially on the executive branch

system of internal controls and internal audit

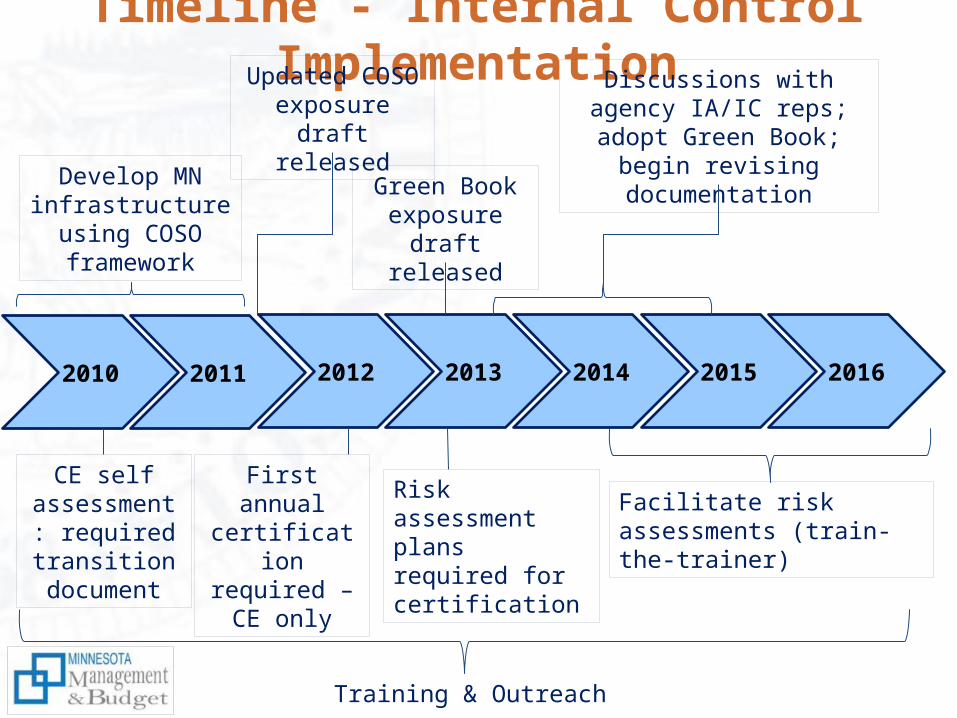

Timeline - Internal Control Implementation

2010 2011 2012 2013 2014 2015 2016

Develop MN infrastructure using COSO framework

Training & Outreach

First annual certification required –

CE only

Risk assessment plans required for certification

Green Book exposure draft

released

Facilitate risk assessments (train-the-trainer)

Updated COSO exposure draft

released

Discussions with agency IA/IC reps; adopt Green

Book; begin revising documentation

CE self assessment:

required transition document

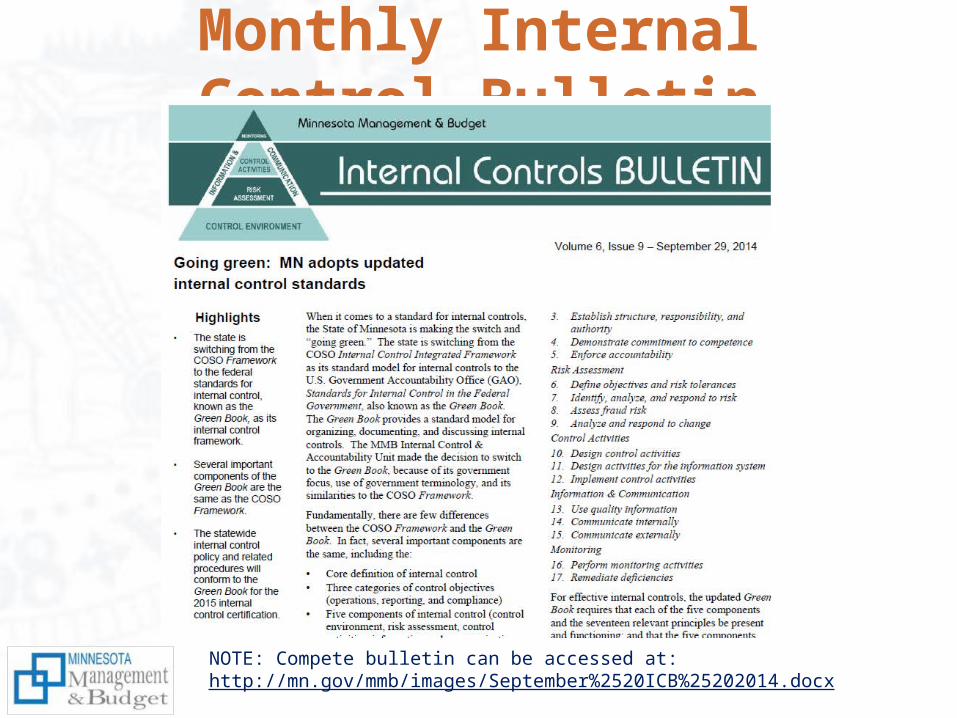

Monthly Internal Control Bulletin

NOTE: Compete bulletin can be accessed at: http://mn.gov/mmb/images/September%2520ICB%25202014.docx

Agency Head Responsibilities“The head of each executive agency must annually certify that the agency head has reviewed the agency’s internal control systems, and that these systems are in compliance with standards and policies established by the commissioner [of Minnesota Management and Budget].”

We began the certification process in 2012 by requiring each agency head to certify that he/she had assess the agency’s control environment using the control environment self-assessment tool.

Control Environment – Green Book Implications

• Revised (i.e. tweaked) our guidance to conform to the 5 Green Book CE principles1. Demonstrate Commitment to Integrity and

Ethical Values2. Exercise Oversight Responsibility3. Establish Structure, Responsibility and Authority4. Demonstrate Commitment to Competence5. Enforce Accountability

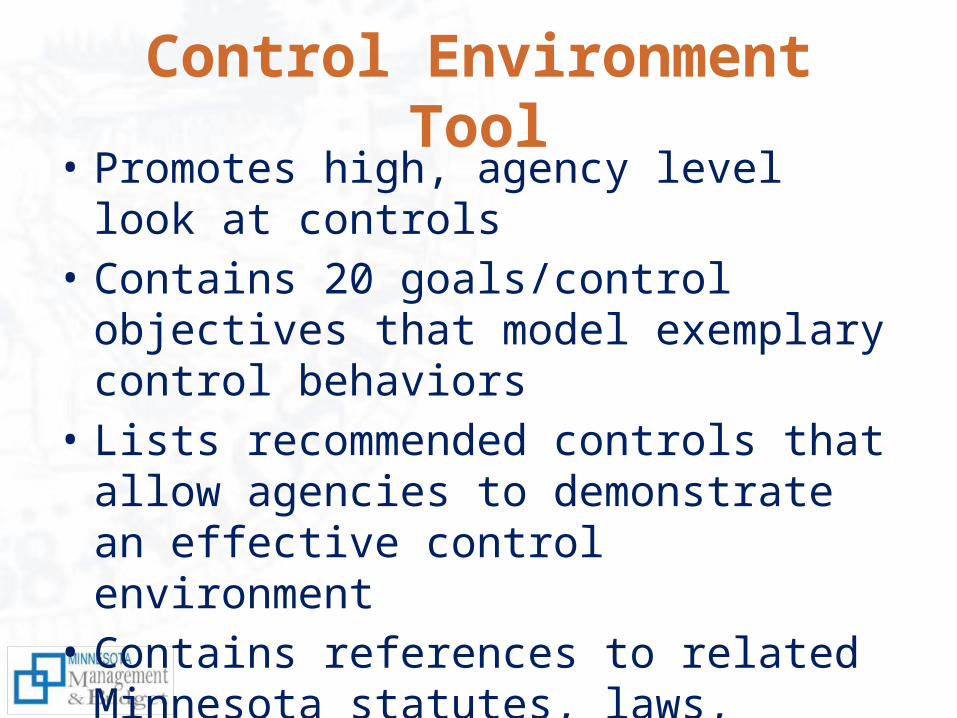

Control Environment Tool• Promotes high, agency level look at controls• Contains 20 goals/control objectives that

model exemplary control behaviors• Lists recommended controls that allow

agencies to demonstrate an effective control environment

• Contains references to related Minnesota statutes, laws, rules, and policies

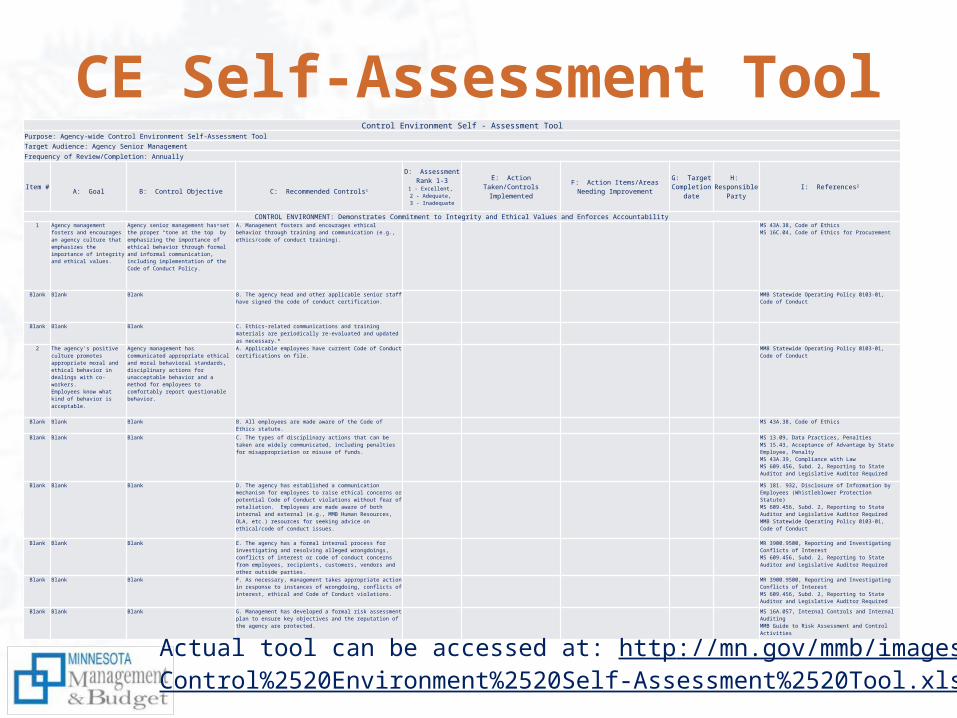

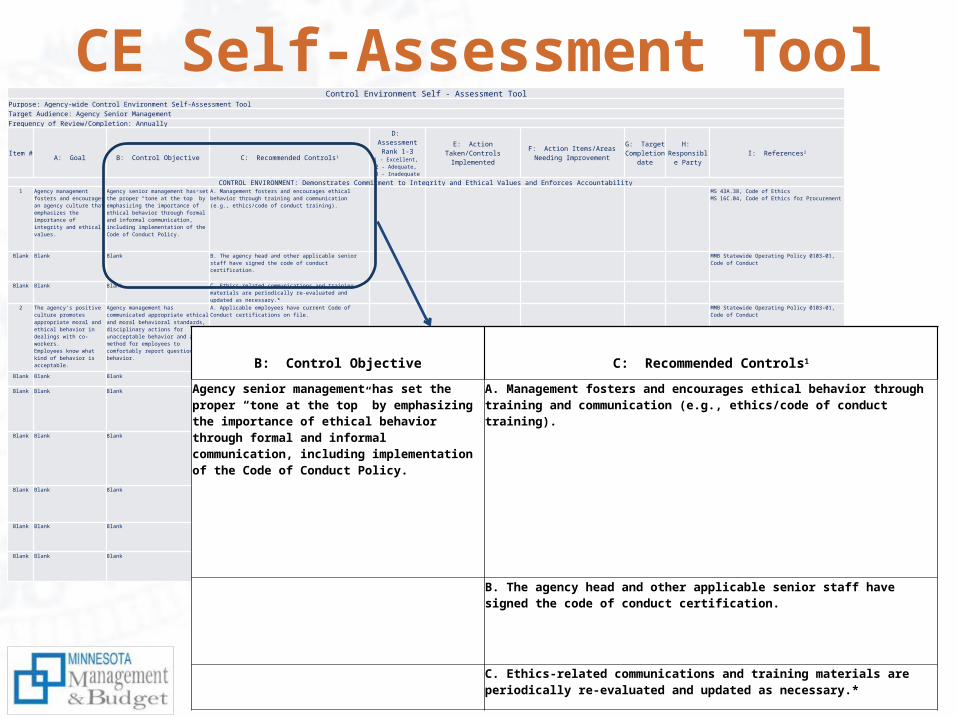

CE Self-Assessment ToolControl Environment Self - Assessment Tool

Purpose: Agency-wide Control Environment Self-Assessment ToolTarget Audience: Agency Senior Management

Frequency of Review/Completion: Annually

Item # A: Goal B: Control Objective C: Recommended Controls1

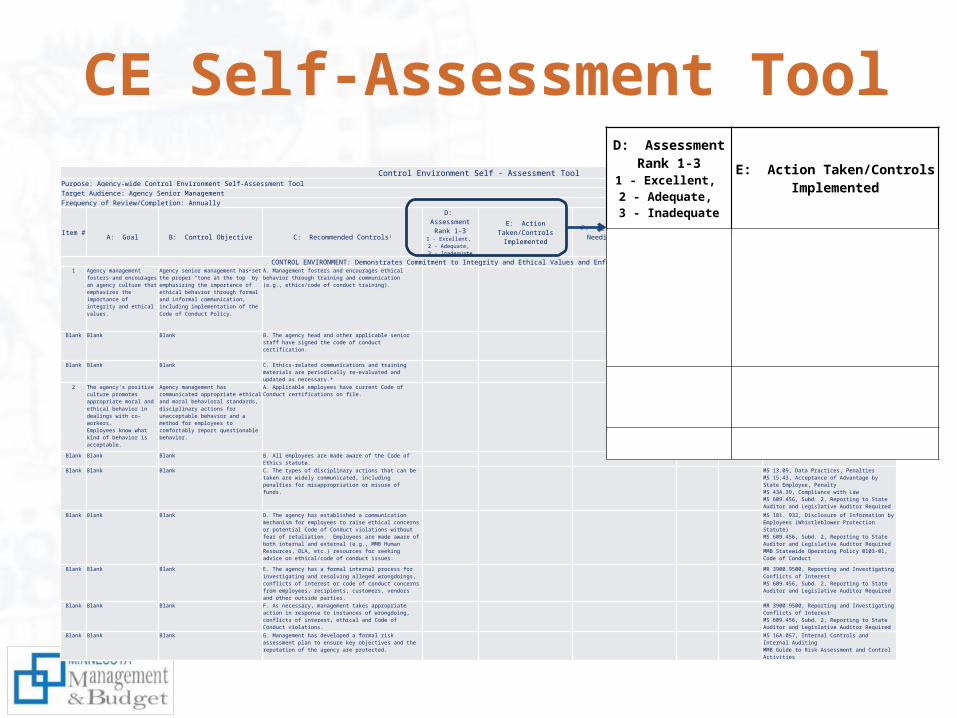

D: Assessment Rank 1-3

1 - Excellent, 2 - Adequate, 3 - Inadequate

E: Action Taken/Controls Implemented

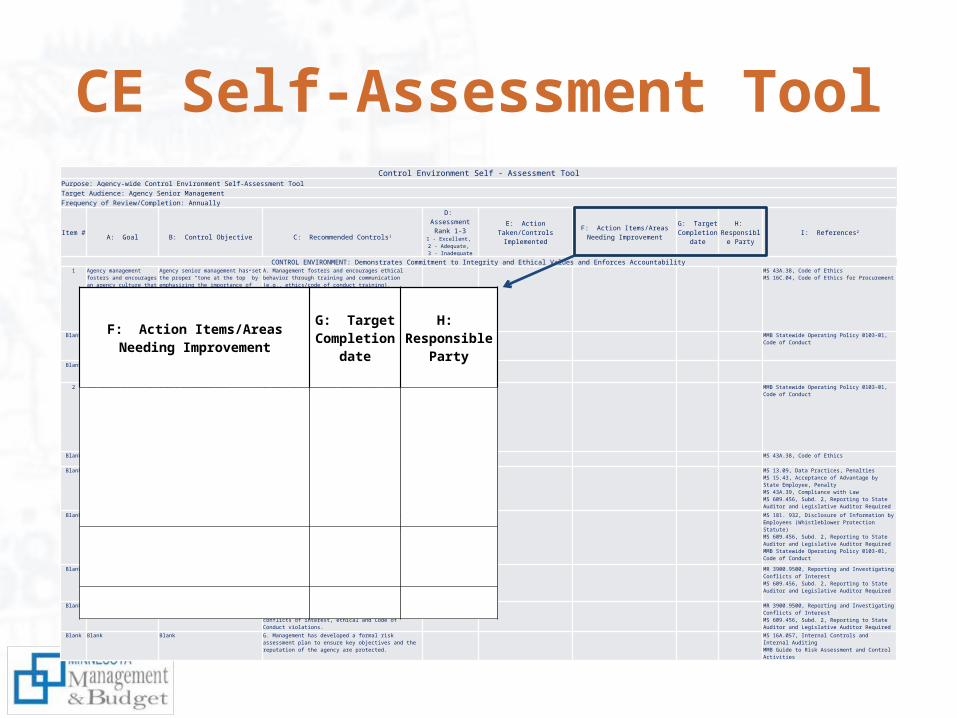

F: Action Items/Areas Needing Improvement

G: Target Completion

date

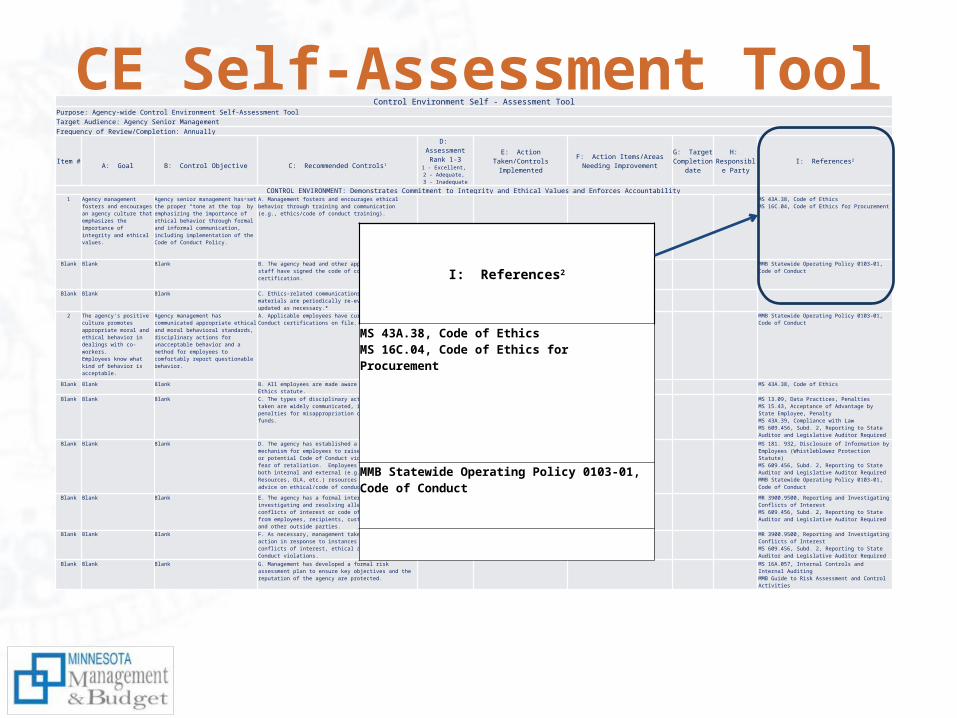

H: Responsible Party I: References2

CONTROL ENVIRONMENT: Demonstrates Commitment to Integrity and Ethical Values and Enforces Accountability1 Agency management fosters and

encourages an agency culture that emphasizes the importance of integrity and ethical values.

Agency senior management has set the proper “tone at the top” by emphasizing the importance of ethical behavior through formal and informal communication, including implementation of the Code of Conduct Policy.

A. Management fosters and encourages ethical behavior through training and communication (e.g., ethics/code of conduct training).

MS 43A.38, Code of EthicsMS 16C.04, Code of Ethics for Procurement

Blank Blank Blank B. The agency head and other applicable senior staff have signed the code of conduct certification.

MMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank C. Ethics-related communications and training materials are periodically re-evaluated and updated as necessary.*

2 The agency's positive culture promotes appropriate moral and ethical behavior in dealings with co-workers.Employees know what kind of behavior is acceptable.

Agency management has communicated appropriate ethical and moral behavioral standards, disciplinary actions for unacceptable behavior and a method for employees to comfortably report questionable behavior.

A. Applicable employees have current Code of Conduct certifications on file.

MMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank B. All employees are made aware of the Code of Ethics statute.

MS 43A.38, Code of Ethics

Blank Blank Blank C. The types of disciplinary actions that can be taken are widely communicated, including penalties for misappropriation or misuse of funds.

MS 13.09, Data Practices, PenaltiesMS 15.43, Acceptance of Advantage by State Employee, PenaltyMS 43A.39, Compliance with LawMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank D. The agency has established a communication mechanism for employees to raise ethical concerns or potential Code of Conduct violations without fear of retaliation. Employees are made aware of both internal and external (e.g., MMB Human Resources, OLA, etc.) resources for seeking advice on ethical/code of conduct issues.

MS 181. 932, Disclosure of Information by Employees (Whistleblower Protection Statute)MS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor RequiredMMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank E. The agency has a formal internal process for investigating and resolving alleged wrongdoings, conflicts of interest or code of conduct concerns from employees, recipients, customers, vendors and other outside parties.

MR 3900.9500, Reporting and Investigating Conflicts of InterestMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank F. As necessary, management takes appropriate action in response to instances of wrongdoing, conflicts of interest, ethical and Code of Conduct violations.

MR 3900.9500, Reporting and Investigating Conflicts of InterestMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank G. Management has developed a formal risk assessment plan to ensure key objectives and the reputation of the agency are protected.

MS 16A.057, Internal Controls and Internal Auditing MMB Guide to Risk Assessment and Control Activities

Actual tool can be accessed at: http://mn.gov/mmb/images/Control%2520Environment%2520Self-Assessment%2520Tool.xlsx

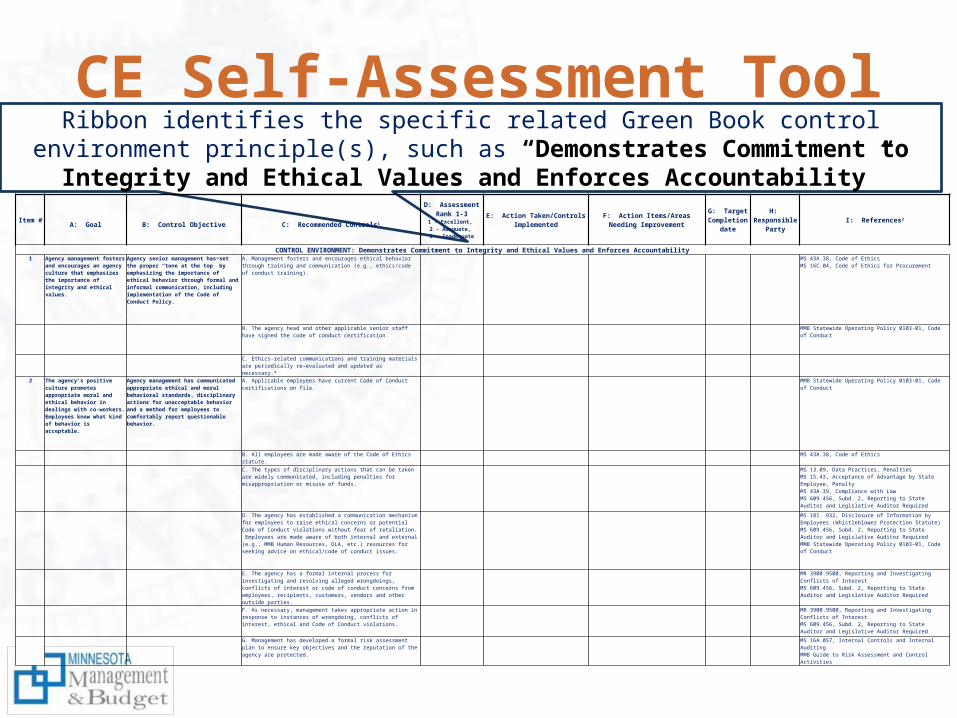

CE Self-Assessment ToolRibbon identifies the specific related Green Book control environment principle(s), such as “Demonstrates Commitment to Integrity and Ethical Values and Enforces Accountability”

Item #A: Goal B: Control Objective C: Recommended Controls1

D: Assessment Rank 1-3

1 - Excellent, 2 - Adequate, 3 - Inadequate

E: Action Taken/Controls Implemented

F: Action Items/Areas Needing Improvement

G: Target Completion

date

H: Responsible

PartyI: References2

CONTROL ENVIRONMENT: Demonstrates Commitment to Integrity and Ethical Values and Enforces Accountability1 Agency management fosters

and encourages an agency culture that emphasizes the importance of integrity and ethical values.

Agency senior management has set the proper “tone at the top” by emphasizing the importance of ethical behavior through formal and informal communication, including implementation of the Code of Conduct Policy.

A. Management fosters and encourages ethical behavior through training and communication (e.g., ethics/code of conduct training).

MS 43A.38, Code of EthicsMS 16C.04, Code of Ethics for Procurement

Blank Blank Blank B. The agency head and other applicable senior staff have signed the code of conduct certification.

MMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank C. Ethics-related communications and training materials are periodically re-evaluated and updated as necessary.*

2 The agency's positive culture promotes appropriate moral and ethical behavior in dealings with co-workers.Employees know what kind of behavior is acceptable.

Agency management has communicated appropriate ethical and moral behavioral standards, disciplinary actions for unacceptable behavior and a method for employees to comfortably report questionable behavior.

A. Applicable employees have current Code of Conduct certifications on file.

MMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank B. All employees are made aware of the Code of Ethics statute.

MS 43A.38, Code of Ethics

Blank Blank Blank C. The types of disciplinary actions that can be taken are widely communicated, including penalties for misappropriation or misuse of funds.

MS 13.09, Data Practices, PenaltiesMS 15.43, Acceptance of Advantage by State Employee, PenaltyMS 43A.39, Compliance with LawMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank D. The agency has established a communication mechanism for employees to raise ethical concerns or potential Code of Conduct violations without fear of retaliation. Employees are made aware of both internal and external (e.g., MMB Human Resources, OLA, etc.) resources for seeking advice on ethical/code of conduct issues.

MS 181. 932, Disclosure of Information by Employees (Whistleblower Protection Statute)MS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor RequiredMMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank E. The agency has a formal internal process for investigating and resolving alleged wrongdoings, conflicts of interest or code of conduct concerns from employees, recipients, customers, vendors and other outside parties.

MR 3900.9500, Reporting and Investigating Conflicts of InterestMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank F. As necessary, management takes appropriate action in response to instances of wrongdoing, conflicts of interest, ethical and Code of Conduct violations.

MR 3900.9500, Reporting and Investigating Conflicts of InterestMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank G. Management has developed a formal risk assessment plan to ensure key objectives and the reputation of the agency are protected.

MS 16A.057, Internal Controls and Internal Auditing MMB Guide to Risk Assessment and Control Activities

CE Self-Assessment Tool

Control Environment Self - Assessment ToolPurpose: Agency-wide Control Environment Self-Assessment ToolTarget Audience: Agency Senior ManagementFrequency of Review/Completion: Annually

Item # A: Goal B: Control Objective C: Recommended Controls1

D: Assessment Rank 1-3

1 - Excellent, 2 - Adequate, 3 - Inadequate

E: Action Taken/Controls Implemented

F: Action Items/Areas Needing Improvement

G: Target Completion

date

H: Responsible Party I: References2

CONTROL ENVIRONMENT: Demonstrates Commitment to Integrity and Ethical Values and Enforces Accountability1 Agency management fosters and

encourages an agency culture that emphasizes the importance of integrity and ethical values.

Agency senior management has set the proper “tone at the top” by emphasizing the importance of ethical behavior through formal and informal communication, including implementation of the Code of Conduct Policy.

A. Management fosters and encourages ethical behavior through training and communication (e.g., ethics/code of conduct training).

MS 43A.38, Code of EthicsMS 16C.04, Code of Ethics for Procurement

Blank Blank Blank B. The agency head and other applicable senior staff have signed the code of conduct certification.

MMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank C. Ethics-related communications and training materials are periodically re-evaluated and updated as necessary.*

2 The agency's positive culture promotes appropriate moral and ethical behavior in dealings with co-workers.Employees know what kind of behavior is acceptable.

Agency management has communicated appropriate ethical and moral behavioral standards, disciplinary actions for unacceptable behavior and a method for employees to comfortably report questionable behavior.

A. Applicable employees have current Code of Conduct certifications on file.

MMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank B. All employees are made aware of the Code of Ethics statute.

MS 43A.38, Code of Ethics

Blank Blank Blank C. The types of disciplinary actions that can be taken are widely communicated, including penalties for misappropriation or misuse of funds.

MS 13.09, Data Practices, PenaltiesMS 15.43, Acceptance of Advantage by State Employee, PenaltyMS 43A.39, Compliance with LawMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank D. The agency has established a communication mechanism for employees to raise ethical concerns or potential Code of Conduct violations without fear of retaliation. Employees are made aware of both internal and external (e.g., MMB Human Resources, OLA, etc.) resources for seeking advice on ethical/code of conduct issues.

MS 181. 932, Disclosure of Information by Employees (Whistleblower Protection Statute)MS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor RequiredMMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank E. The agency has a formal internal process for investigating and resolving alleged wrongdoings, conflicts of interest or code of conduct concerns from employees, recipients, customers, vendors and other outside parties.

MR 3900.9500, Reporting and Investigating Conflicts of InterestMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank F. As necessary, management takes appropriate action in response to instances of wrongdoing, conflicts of interest, ethical and Code of Conduct violations.

MR 3900.9500, Reporting and Investigating Conflicts of InterestMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank G. Management has developed a formal risk assessment plan to ensure key objectives and the reputation of the agency are protected.

MS 16A.057, Internal Controls and Internal Auditing MMB Guide to Risk Assessment and Control Activities

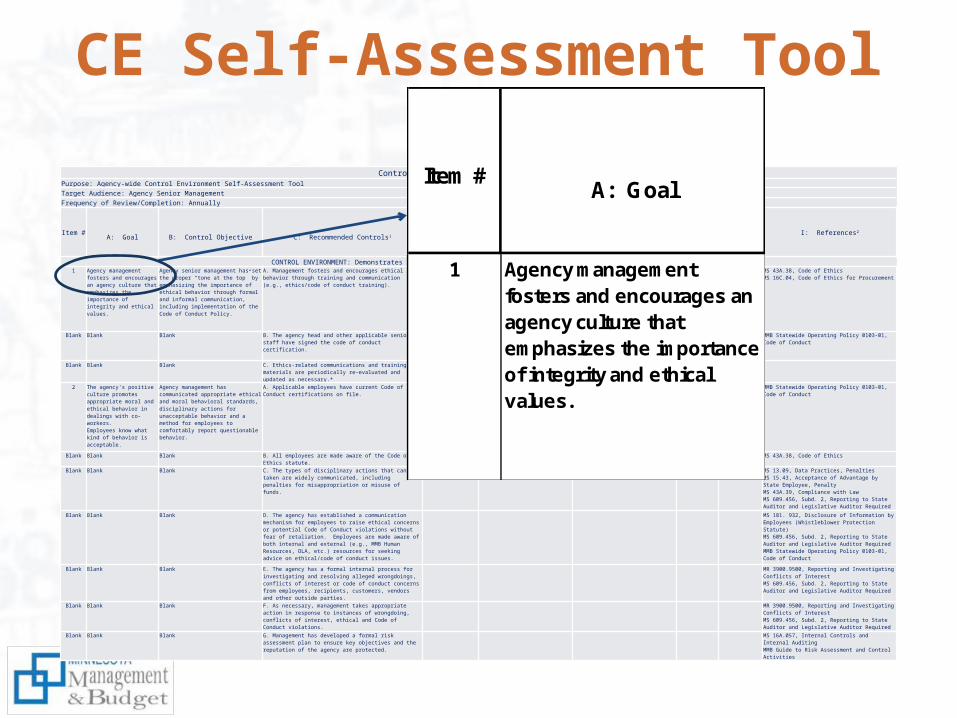

Item #A: Goal

1 Agency management fosters and encourages an agency culture that emphasizes the importance of integrity and ethical values.

CE Self-Assessment ToolControl Environment Self - Assessment Tool

Purpose: Agency-wide Control Environment Self-Assessment ToolTarget Audience: Agency Senior ManagementFrequency of Review/Completion: Annually

Item # A: Goal B: Control Objective C: Recommended Controls1

D: Assessment Rank 1-3

1 - Excellent, 2 - Adequate, 3 - Inadequate

E: Action Taken/Controls Implemented

F: Action Items/Areas Needing Improvement

G: Target Completion

date

H: Responsible Party I: References2

CONTROL ENVIRONMENT: Demonstrates Commitment to Integrity and Ethical Values and Enforces Accountability1 Agency management fosters and

encourages an agency culture that emphasizes the importance of integrity and ethical values.

Agency senior management has set the proper “tone at the top” by emphasizing the importance of ethical behavior through formal and informal communication, including implementation of the Code of Conduct Policy.

A. Management fosters and encourages ethical behavior through training and communication (e.g., ethics/code of conduct training).

MS 43A.38, Code of EthicsMS 16C.04, Code of Ethics for Procurement

Blank Blank Blank B. The agency head and other applicable senior staff have signed the code of conduct certification.

MMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank C. Ethics-related communications and training materials are periodically re-evaluated and updated as necessary.*

2 The agency's positive culture promotes appropriate moral and ethical behavior in dealings with co-workers.Employees know what kind of behavior is acceptable.

Agency management has communicated appropriate ethical and moral behavioral standards, disciplinary actions for unacceptable behavior and a method for employees to comfortably report questionable behavior.

A. Applicable employees have current Code of Conduct certifications on file.

MMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank B. All employees are made aware of the Code of Ethics statute.

MS 43A.38, Code of Ethics

Blank Blank Blank C. The types of disciplinary actions that can be taken are widely communicated, including penalties for misappropriation or misuse of funds.

MS 13.09, Data Practices, PenaltiesMS 15.43, Acceptance of Advantage by State Employee, PenaltyMS 43A.39, Compliance with LawMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank D. The agency has established a communication mechanism for employees to raise ethical concerns or potential Code of Conduct violations without fear of retaliation. Employees are made aware of both internal and external (e.g., MMB Human Resources, OLA, etc.) resources for seeking advice on ethical/code of conduct issues.

MS 181. 932, Disclosure of Information by Employees (Whistleblower Protection Statute)MS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor RequiredMMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank E. The agency has a formal internal process for investigating and resolving alleged wrongdoings, conflicts of interest or code of conduct concerns from employees, recipients, customers, vendors and other outside parties.

MR 3900.9500, Reporting and Investigating Conflicts of InterestMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank F. As necessary, management takes appropriate action in response to instances of wrongdoing, conflicts of interest, ethical and Code of Conduct violations.

MR 3900.9500, Reporting and Investigating Conflicts of InterestMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank G. Management has developed a formal risk assessment plan to ensure key objectives and the reputation of the agency are protected.

MS 16A.057, Internal Controls and Internal Auditing MMB Guide to Risk Assessment and Control Activities

B: Control Objective C: Recommended Controls1

Agency senior management has set the proper “tone at the top” by emphasizing the importance of ethical behavior through formal and informal communication, including implementation of the Code of Conduct Policy.

A. Management fosters and encourages ethical behavior through training and communication (e.g., ethics/code of conduct training).

B. The agency head and other applicable senior staff have signed the code of conduct certification.

C. Ethics-related communications and training materials are periodically re-evaluated and updated as necessary.*

CE Self-Assessment ToolControl Environment Self - Assessment Tool

Purpose: Agency-wide Control Environment Self-Assessment ToolTarget Audience: Agency Senior ManagementFrequency of Review/Completion: Annually

Item # A: Goal B: Control Objective C: Recommended Controls1

D: Assessment Rank 1-3

1 - Excellent, 2 - Adequate, 3 - Inadequate

E: Action Taken/Controls Implemented

F: Action Items/Areas Needing Improvement

G: Target Completion

date

H: Responsible Party I: References2

CONTROL ENVIRONMENT: Demonstrates Commitment to Integrity and Ethical Values and Enforces Accountability1 Agency management fosters and

encourages an agency culture that emphasizes the importance of integrity and ethical values.

Agency senior management has set the proper “tone at the top” by emphasizing the importance of ethical behavior through formal and informal communication, including implementation of the Code of Conduct Policy.

A. Management fosters and encourages ethical behavior through training and communication (e.g., ethics/code of conduct training).

MS 43A.38, Code of EthicsMS 16C.04, Code of Ethics for Procurement

Blank Blank Blank B. The agency head and other applicable senior staff have signed the code of conduct certification.

MMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank C. Ethics-related communications and training materials are periodically re-evaluated and updated as necessary.*

2 The agency's positive culture promotes appropriate moral and ethical behavior in dealings with co-workers.Employees know what kind of behavior is acceptable.

Agency management has communicated appropriate ethical and moral behavioral standards, disciplinary actions for unacceptable behavior and a method for employees to comfortably report questionable behavior.

A. Applicable employees have current Code of Conduct certifications on file.

MMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank B. All employees are made aware of the Code of Ethics statute.

MS 43A.38, Code of Ethics

Blank Blank Blank C. The types of disciplinary actions that can be taken are widely communicated, including penalties for misappropriation or misuse of funds.

MS 13.09, Data Practices, PenaltiesMS 15.43, Acceptance of Advantage by State Employee, PenaltyMS 43A.39, Compliance with LawMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank D. The agency has established a communication mechanism for employees to raise ethical concerns or potential Code of Conduct violations without fear of retaliation. Employees are made aware of both internal and external (e.g., MMB Human Resources, OLA, etc.) resources for seeking advice on ethical/code of conduct issues.

MS 181. 932, Disclosure of Information by Employees (Whistleblower Protection Statute)MS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor RequiredMMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank E. The agency has a formal internal process for investigating and resolving alleged wrongdoings, conflicts of interest or code of conduct concerns from employees, recipients, customers, vendors and other outside parties.

MR 3900.9500, Reporting and Investigating Conflicts of InterestMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank F. As necessary, management takes appropriate action in response to instances of wrongdoing, conflicts of interest, ethical and Code of Conduct violations.

MR 3900.9500, Reporting and Investigating Conflicts of InterestMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank G. Management has developed a formal risk assessment plan to ensure key objectives and the reputation of the agency are protected.

MS 16A.057, Internal Controls and Internal Auditing MMB Guide to Risk Assessment and Control Activities

D: Assessment Rank 1-3

1 - Excellent, 2 - Adequate, 3 - Inadequate

E: Action Taken/Controls Implemented

CE Self-Assessment ToolControl Environment Self - Assessment Tool

Purpose: Agency-wide Control Environment Self-Assessment ToolTarget Audience: Agency Senior ManagementFrequency of Review/Completion: Annually

Item # A: Goal B: Control Objective C: Recommended Controls1

D: Assessment Rank 1-3

1 - Excellent, 2 - Adequate, 3 - Inadequate

E: Action Taken/Controls Implemented

F: Action Items/Areas Needing Improvement

G: Target Completion

date

H: Responsible Party I: References2

CONTROL ENVIRONMENT: Demonstrates Commitment to Integrity and Ethical Values and Enforces Accountability1 Agency management fosters and

encourages an agency culture that emphasizes the importance of integrity and ethical values.

Agency senior management has set the proper “tone at the top” by emphasizing the importance of ethical behavior through formal and informal communication, including implementation of the Code of Conduct Policy.

A. Management fosters and encourages ethical behavior through training and communication (e.g., ethics/code of conduct training).

MS 43A.38, Code of EthicsMS 16C.04, Code of Ethics for Procurement

Blank Blank Blank B. The agency head and other applicable senior staff have signed the code of conduct certification.

MMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank C. Ethics-related communications and training materials are periodically re-evaluated and updated as necessary.*

2 The agency's positive culture promotes appropriate moral and ethical behavior in dealings with co-workers.Employees know what kind of behavior is acceptable.

Agency management has communicated appropriate ethical and moral behavioral standards, disciplinary actions for unacceptable behavior and a method for employees to comfortably report questionable behavior.

A. Applicable employees have current Code of Conduct certifications on file.

MMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank B. All employees are made aware of the Code of Ethics statute.

MS 43A.38, Code of Ethics

Blank Blank Blank C. The types of disciplinary actions that can be taken are widely communicated, including penalties for misappropriation or misuse of funds.

MS 13.09, Data Practices, PenaltiesMS 15.43, Acceptance of Advantage by State Employee, PenaltyMS 43A.39, Compliance with LawMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank D. The agency has established a communication mechanism for employees to raise ethical concerns or potential Code of Conduct violations without fear of retaliation. Employees are made aware of both internal and external (e.g., MMB Human Resources, OLA, etc.) resources for seeking advice on ethical/code of conduct issues.

MS 181. 932, Disclosure of Information by Employees (Whistleblower Protection Statute)MS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor RequiredMMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank E. The agency has a formal internal process for investigating and resolving alleged wrongdoings, conflicts of interest or code of conduct concerns from employees, recipients, customers, vendors and other outside parties.

MR 3900.9500, Reporting and Investigating Conflicts of InterestMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank F. As necessary, management takes appropriate action in response to instances of wrongdoing, conflicts of interest, ethical and Code of Conduct violations.

MR 3900.9500, Reporting and Investigating Conflicts of InterestMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank G. Management has developed a formal risk assessment plan to ensure key objectives and the reputation of the agency are protected.

MS 16A.057, Internal Controls and Internal Auditing MMB Guide to Risk Assessment and Control Activities

F: Action Items/Areas Needing Improvement

G: Target Completion

date

H: Responsible

Party

CE Self-Assessment ToolControl Environment Self - Assessment Tool

Purpose: Agency-wide Control Environment Self-Assessment ToolTarget Audience: Agency Senior ManagementFrequency of Review/Completion: Annually

Item # A: Goal B: Control Objective C: Recommended Controls1

D: Assessment Rank 1-3

1 - Excellent, 2 - Adequate, 3 - Inadequate

E: Action Taken/Controls Implemented

F: Action Items/Areas Needing Improvement

G: Target Completion

date

H: Responsible Party I: References2

CONTROL ENVIRONMENT: Demonstrates Commitment to Integrity and Ethical Values and Enforces Accountability1 Agency management fosters and

encourages an agency culture that emphasizes the importance of integrity and ethical values.

Agency senior management has set the proper “tone at the top” by emphasizing the importance of ethical behavior through formal and informal communication, including implementation of the Code of Conduct Policy.

A. Management fosters and encourages ethical behavior through training and communication (e.g., ethics/code of conduct training).

MS 43A.38, Code of EthicsMS 16C.04, Code of Ethics for Procurement

Blank Blank Blank B. The agency head and other applicable senior staff have signed the code of conduct certification.

MMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank C. Ethics-related communications and training materials are periodically re-evaluated and updated as necessary.*

2 The agency's positive culture promotes appropriate moral and ethical behavior in dealings with co-workers.Employees know what kind of behavior is acceptable.

Agency management has communicated appropriate ethical and moral behavioral standards, disciplinary actions for unacceptable behavior and a method for employees to comfortably report questionable behavior.

A. Applicable employees have current Code of Conduct certifications on file.

MMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank B. All employees are made aware of the Code of Ethics statute.

MS 43A.38, Code of Ethics

Blank Blank Blank C. The types of disciplinary actions that can be taken are widely communicated, including penalties for misappropriation or misuse of funds.

MS 13.09, Data Practices, PenaltiesMS 15.43, Acceptance of Advantage by State Employee, PenaltyMS 43A.39, Compliance with LawMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank D. The agency has established a communication mechanism for employees to raise ethical concerns or potential Code of Conduct violations without fear of retaliation. Employees are made aware of both internal and external (e.g., MMB Human Resources, OLA, etc.) resources for seeking advice on ethical/code of conduct issues.

MS 181. 932, Disclosure of Information by Employees (Whistleblower Protection Statute)MS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor RequiredMMB Statewide Operating Policy 0103-01, Code of Conduct

Blank Blank Blank E. The agency has a formal internal process for investigating and resolving alleged wrongdoings, conflicts of interest or code of conduct concerns from employees, recipients, customers, vendors and other outside parties.

MR 3900.9500, Reporting and Investigating Conflicts of InterestMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank F. As necessary, management takes appropriate action in response to instances of wrongdoing, conflicts of interest, ethical and Code of Conduct violations.

MR 3900.9500, Reporting and Investigating Conflicts of InterestMS 609.456, Subd. 2, Reporting to State Auditor and Legislative Auditor Required

Blank Blank Blank G. Management has developed a formal risk assessment plan to ensure key objectives and the reputation of the agency are protected.

MS 16A.057, Internal Controls and Internal Auditing MMB Guide to Risk Assessment and Control Activities

I: References2

MS 43A.38, Code of EthicsMS 16C.04, Code of Ethics for Procurement

MMB Statewide Operating Policy 0103-01, Code of Conduct

Risk Assessment• Assessment plans required beginning in 2013• Agencies decide which processes need formal

risk assessments, but must consider:– Items material to the CAFR– Major single audit programs– Major sources and uses of funding (financial)– Areas critical to agency mission (operational)

• Risk assessments currently underway in most agencies

Risk Assessment – Green Book Implications

• As of April 2015, we revised the policy, procedures, and guidance to conform to the Green Book principles

– Four risk assessment principles

– Three control activities principles

Risk Assessment/Control Activities Potential Issues

• Biggest sticking point is Principle 11, due to Minnesota’s recent IT consolidation– Principle 11 – Management should design control

activities for the entity’s information system• Other principles being discussed

– Principle 6 – Management should define objectives clearly … and define risk tolerances

– Principle 8 – Management should consider the potential for fraud

Other Green Book Components

• Information and Communication– Embedded in all other components– Must make this component implicit in all guidance

• Monitoring– Still to be determined

Questions?Minnesota Management and Budget (MMB) Internal Control and Accountability Unit• [email protected]• http://mn.gov/mmb/internalcontrol/