Embed Size (px)

Citation preview

Engaging Youth at Your Credit Union

Minnesota Family Involvement Council

Young adult membership is a top priority Attracting 18-35 age group is critical – Gen Y Where to start?

What we’ll chat about today Overview of 6 key components identified

from our 2014 scholarship applicants for CUs reaching out to young adults

Young Adult Membership Growth Guide Facilitated panel discussion of Young Adults

Young Adult Membership

The Essay Question

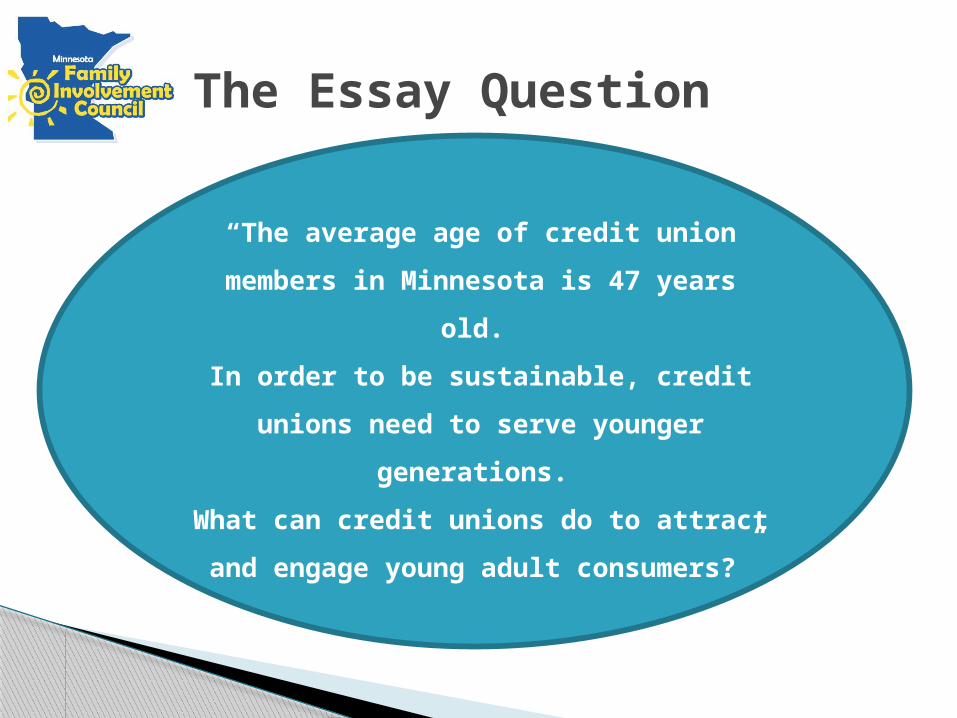

“The average age of credit union

members in Minnesota is 47 years old.

In order to be sustainable, credit

unions need to serve younger

generations.

What can credit unions do to attract

and engage young adult consumers?”

1: Social Media, Websites, Technology

2: Events, Education

3: Targeted Marketing

4: Specialized Products & Services

5: Member Access

6: Member Service

6 Concepts Identified

Social Media◦ Educate youth through all social media channels - Facebook, Twitter,

Google +, YouTube, Instagram, Pinterest

◦ Blogs for topics of interest for young people

◦ Use the 3:1 ratio – For every 1 post marketing a new product or service, there should be 3 human interest posts

Website◦ Financial literacy games online

◦ Use QR codes that direct to specific website pages; create a QR code game where youth find various items on the website and gain education on various topics

Technology◦ Text messages alerts about account activity

◦ Emails to parents urging teens to join the CU

◦ Smartphone apps that are youth-oriented

Tip: Be sure to use humor!

1: Social Media, Websites, Technology

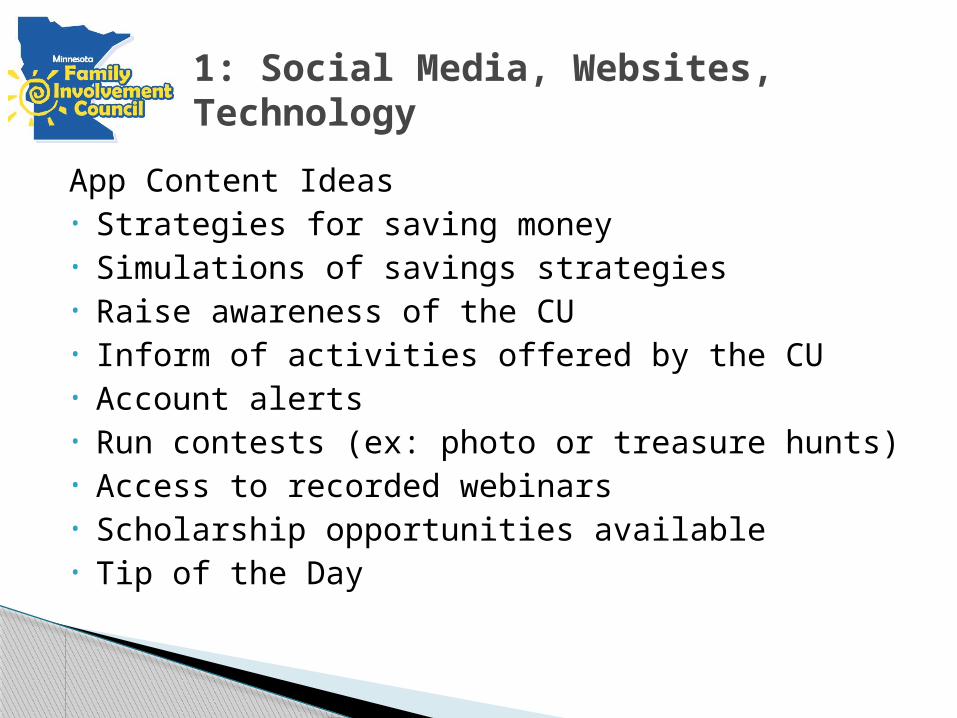

App Content Ideas• Strategies for saving money• Simulations of savings strategies• Raise awareness of the CU • Inform of activities offered by the CU• Account alerts• Run contests (ex: photo or treasure hunts)• Access to recorded webinars• Scholarship opportunities available • Tip of the Day

1: Social Media, Websites, Technology

“Instead of lagging behind other

institutions, credit unions need to be

aggressively using new technology as it

emerges.”

“The younger generation

loves having different options.”

“Technology is demanded; it offers instant solutions and varied options for anything imaginable. This is where

credit unions need to focus, otherwise they will continue to

be ignored and deemed inaccessible.”

“A boring

website

reflects a

tedious Credit

Union.”

2: Events, Education Events

◦ Family events & get-togethers at the CU◦ Show community support involvement by donating to local charity

or sponsoring a HS sporting event◦ The best place for credit unions to get noticed is at school events:

sponsor class parties; support a team booster club; advertise in noticeable locations at schools

◦ Host a college fair, or participate in college fairs◦ Promote social responsibility in the community – give-back

Education◦ Provide free education for youth and parents, either in high

schools, colleges or at the credit union◦ Offer young people a tour of your place of business for a day so

they know what happens behind the scenes◦ Turn young employees into ambassadors (ex: youth board

member) “Our schools do not do enough to prepare young people for the reality of fiscal independence.”

“If you asked this generation what a credit union is, less

than 5% would know.”

College planning/budgeting FASFA seminars – what is it, how to fill it out, tips Transitioning to college life Job interview preparation Fraud/identity theft Money management Opening a checking account and how to balance Getting a car loan How to pay off loans and get out of debt Buying a home The importance of establishing and maintaining a good credit score Make banking easy to understand; offer a step-by-step process or app

with the different options Financial/retirement planning Offer a series of seminars that cater specifically to groups of recent

college graduates and help them create financial strategies and goals The differences between banks and credit unions

2: Education Content Ideas

“Work with colleges like

TCF Bank does.”

“Have representatives at high schools for seniors to consult about

different strategies for

personal finance.”

“Education resolves

most dilemmas.

”

“Young people

love free food!”

3: Targeted Marketing Use exciting & relevant money facts Refer-a-friend programs Have a Youth Advisory Board and a youth spokesperson that is

engaging to the target market Have information readily available and displayed throughout

each branch Use local personalities/celebrities in advertising – partner with

local companies Monthly incentives or drawings as rewards for saving money:

win tickets to Vikings, Twins, Wild games; iPods; trips/travel; and giveaways such as iTunes cards; fast food restaurant gift cards

Use pop culture and interesting advertisements Use focus groups to learn more about your member and your

target audience and modify marketing strategies accordingly Utilize sourcing techniques

“Doing business with the younger generation is

all about staying

relevant.”

1. Identify: Scrub your database for the desired demographics.

2. Product: The product you are marketing and how much you know about it can help shape your strategy through the rest of the steps in the process.

3. Place: Where are you advertising or choosing to directly reach out to your market?

4. Price: What is your product pricing, and how does it compare in the marketplace?

5. Promotion: It’s easy to make assumptions about what work and what won’t. Identify niche media outlets for relaying your message.

3: Targeted Marketing: Sourcing Techniques

“Young adults want rewards, like dorm room

gifts or gift cards.”

“Have a savings challenge… Survive and

Thrive”

“Image is everything”

"I couldn't pinpoint the name of a single credit

union before my parents became members of one.

Banks advertise everywhere; are seen everywhere. Credit

Unions need to tell young adults why they are

better."

Design products for life transitions Offer Incentive Programs

◦ Rewards checking with rewards debit card that can be personalized

◦ Credit cards with financial rewards – cash back

◦ Connect parent and youth accounts for easy transfers and inquires or offer an incentive for parents and children to both be members, encouraging growth of the family membership

Youth investment/retirement accounts Personal financial management tools Emergency loan program: a small loan for sudden

things that happen in life

4: Specialized Products & Services

• Have separate rate and fee structures for the youth market• Lighter penalties for overdrafts

• No ATM fees

• Lower interest rates on loans and flexible repayment plan options

• A loan program with shrinking interest rates based on the youth’s performance of financially- responsible task

• Offer higher savings/Certificate rates and/or incentives for younger members to encourage savings – based on making monthly deposits, attending seminars on financial literacy

• Offer scholarship programs

4: Specialized Products & Services

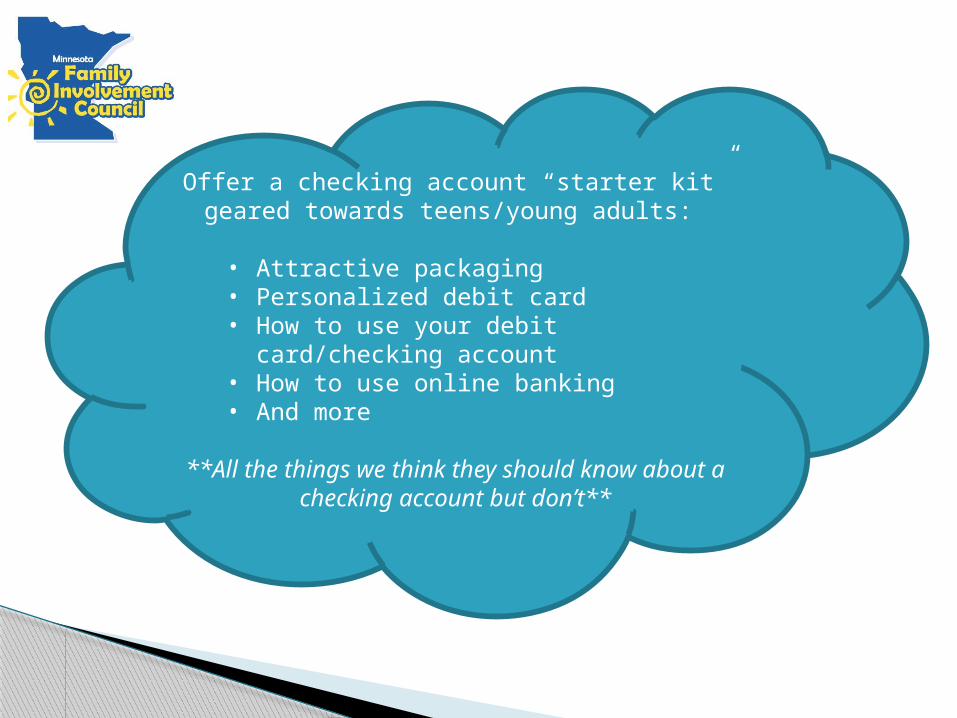

Offer a checking account “starter kit” geared towards teens/young adults:

• Attractive packaging• Personalized debit card• How to use your debit card/checking

account• How to use online banking• And more

**All the things we think they should know about a checking account but don’t**

Multiple and convenient branch locations and later hours

Free access to ATMs Convenience, simplicity, and technology (ex:

mobile deposit) Excellent online banking features Expanded membership access Branches within colleges and high schools Skype access Live chat service Easy check cashing

5: Member Access

“Be a hang out… have a comfortable lobby where people will want to hang

out. ““Young people want free

everything – free shipping, free returns,

free checking , free savings – major for-profit banks have hidden fees just about everywhere.”

“Millennials like money and hate

fees. Why should I have to pay to access my own

money?”

6: Member Service

Credit Union staff should…. Take time to listen and understand the member’s

needs Show young adults equality and support Create trust and loyalty Develop personal relationships with members Always cultivate that credit unions are “local” and

they “care” about you Develop personalized relationships with online

contact as well as interactive services that will keep the youth market feeling safe and secure when making purchases and banking decisions

Young Adult Membership Growth Guide

Source: World Council of Credit Unions

Focus Group Questions

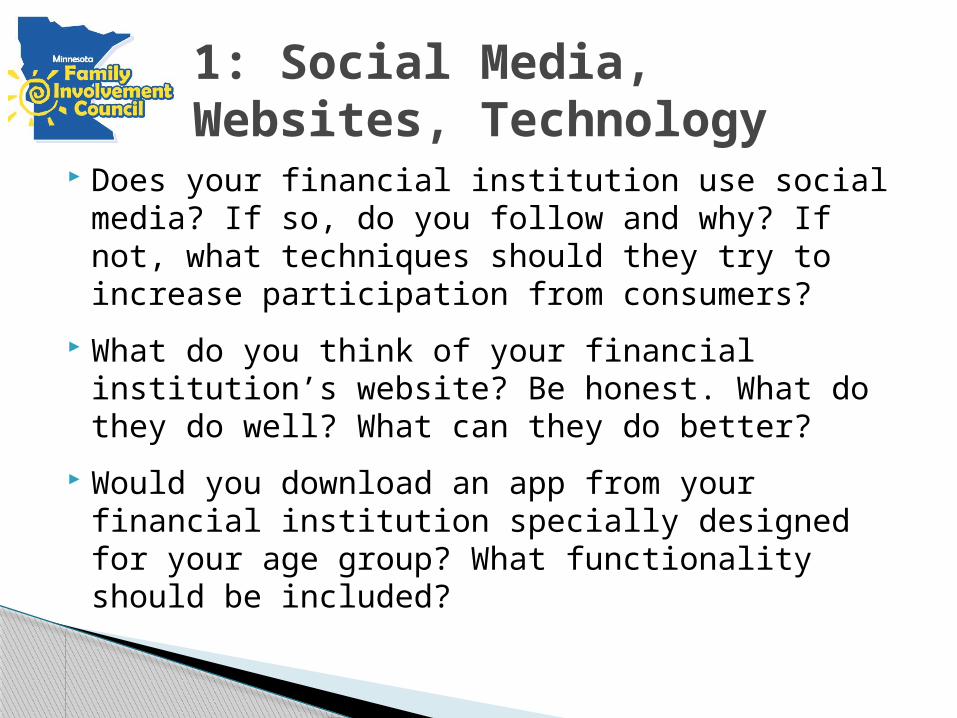

Does your financial institution use social media? If so, do you follow and why? If not, what techniques should they try to increase participation from consumers?

What do you think of your financial institution’s website? Be honest. What do they do well? What can they do better?

Would you download an app from your financial institution specially designed for your age group? What functionality should be included?

1: Social Media, Websites, Technology

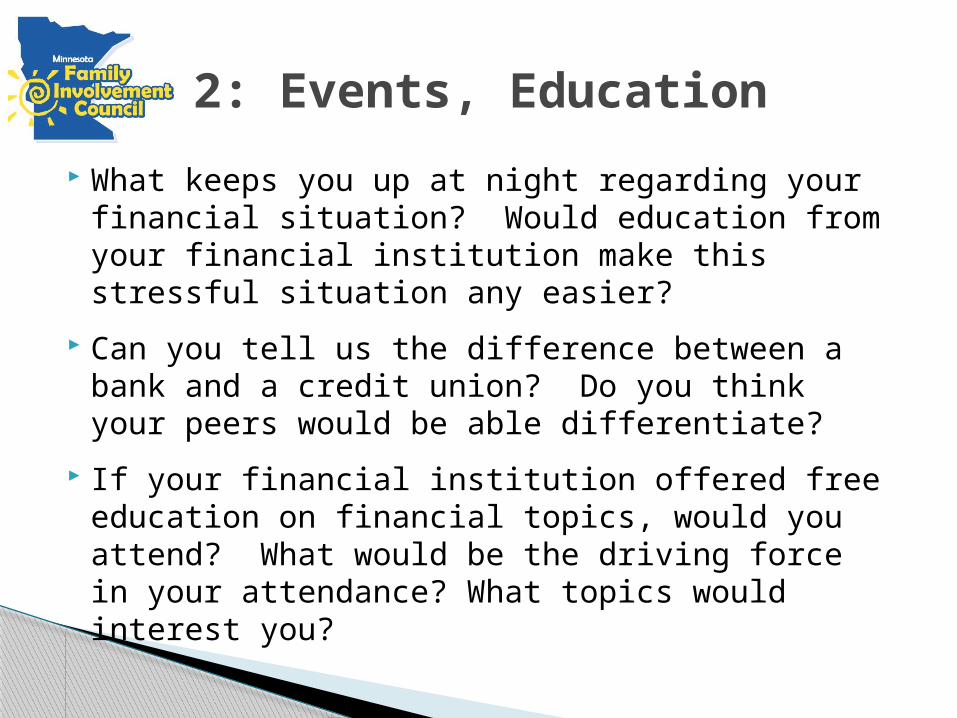

What keeps you up at night regarding your financial situation? Would education from your financial institution make this stressful situation any easier?

Can you tell us the difference between a bank and a credit union? Do you think your peers would be able differentiate?

If your financial institution offered free education on financial topics, would you attend? What would be the driving force in your attendance? What topics would interest you?

2: Events, Education

Other than social media or online marketing tactics, what other marketing avenues or promotions would grab your attention?

If your credit union offered volunteer leadership positions (such as a Youth Advisory Board) for your age group, would you be interested in participating and what responsibilities would you want to facilitate?

3: Targeted Marketing

Can you see yourself taking advantage of any of the specialized products highlighted in the presentation? i.e. Emergency loans, rewards checking, refer-a-friend incentives, personal financial management tools, etc.

What kinds of incentives could your financial institution offer which would make you want to develop smart financial habits such as budgeting or starting a savings plan?

4: Specialized Products & Services

How do you like to- or would you want to- access your financial institution? In branch, phone, skype, live online chat, ATMs, in-school branches, other? List you top three and why?

Many scholarship applicants indicated they would like “longer hours” at their financial institutions. What hours are appealing to you, through which avenues (branch, live representative, online) and why?

5: Member Access

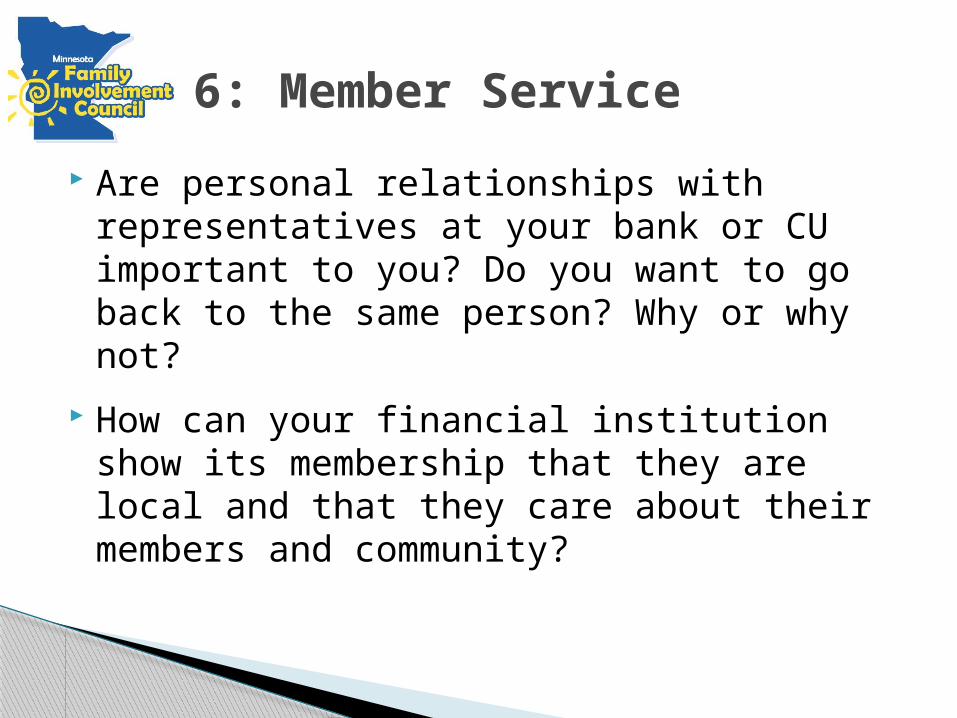

Are personal relationships with representatives at your bank or CU important to you? Do you want to go back to the same person? Why or why not?

How can your financial institution show its membership that they are local and that they care about their members and community?

6: Member Service

What local events could your financial institution support or host that are important to you and/or would make you more likely to do business with them?

Do you have any loans right now? Are they with a credit union or bank? How did you decide where to get your loan?

Other Questions

Our Commitment to Minnesota Credit Unions

The Minnesota Family Involvement Council (FIC) is comprised of a group of credit union volunteers dedicated to providing

Minnesota credit unions the resources needed to provide members with full-family financial education. The FIC

continually works towards fulfilling its mission of being involved and providing support through a variety of

programs, including: Providing financial education resources

Awarding annual scholarships to MN credit union members

Delivering feedback from scholarship essays submitted by credit union members

Thank You For Attending!

All handouts, along with notes from the focus group will be made

available at www.mnfic.org