Embed Size (px)

Citation preview

© 2016 Minnesota Workers’ Compensation Insurers Association, Inc.

Minnesota Workers’ Compensation

State of the Market

State of the Market

Pure Premium

Predictability

Consistent Low Loss

Ratios

Assigned Risk Plan

Depopulation

Significant Payroll

Increases

Permanent Injury

Reductions

Medical Payment

Shifts

Ongoing Net Case

Reserve Reductions

1

Employer Costs

2

-9.0

-7.6-6.3

10.2 10.6

5.3 5.1

8.0

3.7

-6.4

-12.5 -12.3

-3.6

9.610.9

8.3

5.7

4.0

1.4

-.5

-15

-10

-5

0

5

10

15

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Perc

ent C

hang

e (%

)

Calendar Year

Essentially Mirroring National Results through 2016, the 2017 Decrease Was Driven Primarily by Rate Reductions

Minnesota

Countrywide

Source: Direct Written Premium from A.M. Best's Market Share Reports/One Year Premiums and Loss Study

3

838

768706

774

861

931968

10491092

1027

0

100

200

300

400

500

600

700

800

900

1000

1100

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

$ M

illio

ns

Calendar Year

In Spite of the 2017 Decrease, Insured Premium Has Grown over 45% Since 2010

Assigned Risk Plan

Voluntary

Source: Direct Earned Premium from A.M. Best's Market Share Reports/One Year Premiums and Loss Study and Actuarial Advisors

4

42

3532 32

45

5860

62

55

43

5.0% 4.6% 4.5% 4.1% 5.2% 6.2% 6.2% 5.9% 5.0% 4.2%

0

10

20

30

40

50

60

70

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

$ M

illio

ns(M

arke

t Sha

re)

Calendar Year

The Assigned Risk Market Share Has Decreased to a Level Last Seen Six Years Ago

Source: Direct Earned Premium from Actuarial Advisors

5

0.7

4.1

-2.1

6.4

4.2

5.0

3.3

4.4

1.4

3.9

3.2

4.8

-3

-2

-1

0

1

2

3

4

5

6

7

Ratemaking Cycle 2009 to 2016 Ratemaking Cycle 2017 to 2019

Aver

age

Annu

al C

hang

e (%

)After Several Seasons of Decreases, Contracting Payroll Improvement

Has Driven Statewide Growth in Recent Years

Manufacturing Contracting Office & Clerical Goods & Services Miscellaneous Statewide

Source: Unit Statistical Data

6

69

7476

68

6360 60

58

52 52

63

68

75

6568

60 6157

5450

0

10

20

30

40

50

60

70

80

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Perc

ent (

%)

Calendar Year

Comparable to National Results, Loss Ratios Have Decreased 24% Since 2010

MinnesotaCountrywide

Source: A.M. Best's Market Share Reports/One Year Premiums and Loss Study

7

-2.4-1.7

-2.7

-.8-2.0 -2.5

2.0

-12.1

-6.7

1.2

-25.1

-30

-25

-20

-15

-10

-5

0

5

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Perc

ent C

hang

e (%

)

Year

The Average Pure Premium Rate HasDropped 25% over the Last Ten Years

Individual

Cumulative

Source: MWCIA Ratemaking Reports

8

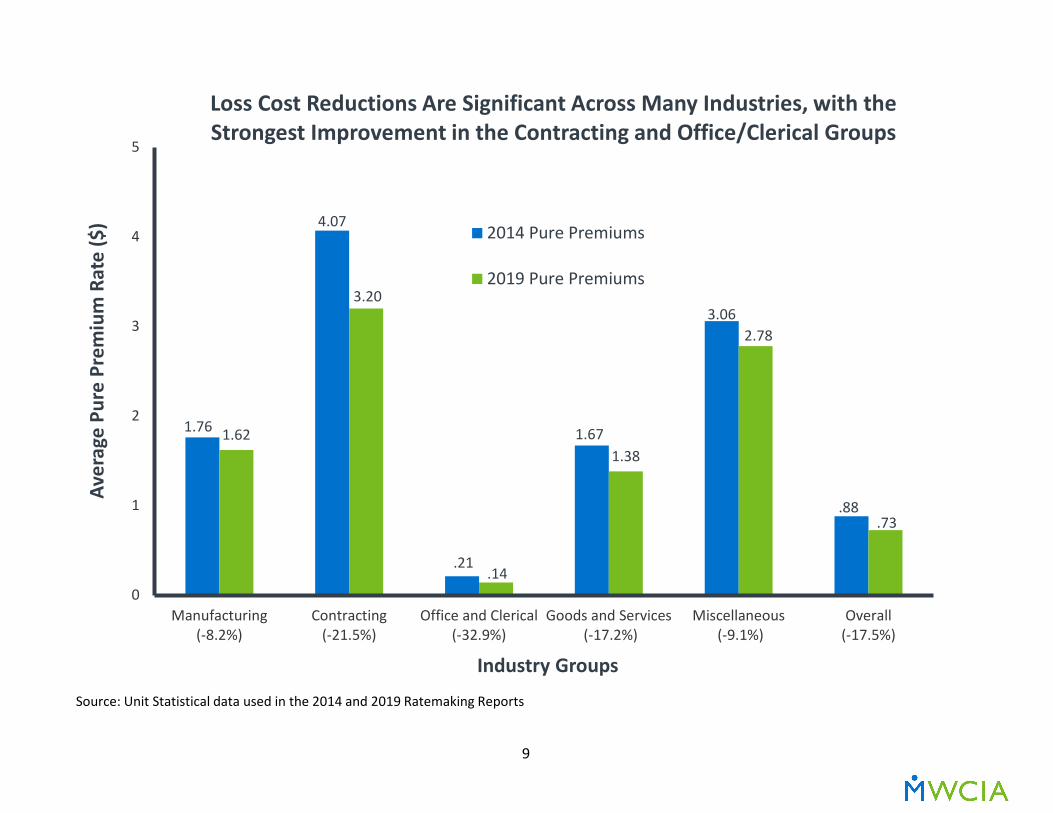

1.76

4.07

.21

1.67

3.06

.88

1.62

3.20

.14

1.38

2.78

.73

0

1

2

3

4

5

Manufacturing(-8.2%)

Contracting(-21.5%)

Office and Clerical(-32.9%)

Goods and Services (-17.2%)

Miscellaneous (-9.1%)

Overall(-17.5%)

Aver

age

Pure

Pre

miu

m R

ate

($)

Industry Groups

Loss Cost Reductions Are Significant Across Many Industries, with the Strongest Improvement in the Contracting and Office/Clerical Groups

2014 Pure Premiums

2019 Pure Premiums

Source: Unit Statistical data used in the 2014 and 2019 Ratemaking Reports

9

Claim Frequency

10

30.232.3 31.9

38.2

35.4 35.933.9

31.7

19.321.2

16.4

23.2

20.5

23.3

20.3 20.0

0

5

10

15

20

25

30

35

40

Metro(-36.2%)

ExtendedMetro

(-34.3%)

Southeast(-48.6%)

Southwest(-39.2%)

Central(-42.2%)

Northeast(-35.2%)

Northwest(-40.1%)

Statewide(-36.9%)

Case

s per

$1M

Pur

e Pr

emiu

m

Region (PY 2006-2015 Change)

There Have Been Dramatic Declines in Indemnity Case Frequency Across All Regions over the Last Ten Years

Policy Year 2006 Policy Year 2015Source: Unit Statistical data

11

.004

.005

.005

.006

.006

.008

.011

.014

.014

.023

.006

.007

.009

.010

.014

.013

.025

.022

.014

.048

Abdomen Including Groin ($16,006)

Foot ($21,312)

Hand ($20,611)

Ankle ($20,668)

Wrist ($23,351)

Finger ($17,173)

Multiple Body Parts ($49,600)

Knee ($25,581)

Shoulder ($39,240)

Low Back Area ($22,002)

.00 .01 .02 .03 .04 .05

Part

of B

ody

Inju

red

(PY

2015

Ann

ual A

vera

ge C

ost P

er C

ase)

Lost-Time Cases/$1M Payroll

The Relative Frequencies of Low Back & Multiple Body Part Injuries Have Been More Than Halved

Policy Year 2006

Policy Year 2015

Source: Unit Statistical Data, First Report Lost-Time Cases Per $1 Million of Payroll

12

.003

.003

.003

.004

.008

.009

.012

.014

.014

.055

.006

.001

.006

.003

.013

.022

.020

.017

.021

.097

Hernia ($16,483)

Concussion ($34,647)

Inflammation ($23,679)

Multiple Physical Injuries Only ($61,064)

Laceration ($14,518)

All Other ($31,841)

Sprain ($25,622)

Contusion ($20,166)

Fracture ($43,432)

Strain ($23,697)

.00 .02 .04 .06 .08 .10

Nat

ure

of In

jury

(PY

2015

Ann

ual A

vera

ge C

ost P

er C

ase)

Lost-Time Cases/$1M Payroll

The Relative Frequencies of Strains & Sprains Have Decreased Markedly

Policy Year 2006

Policy Year 2015

Source: Unit Statistical Data, First Report Lost-Time Cases Per $1 Million of Payroll

13

.004

.004

.005

.006

.006

.007

.007

.009

.012

.021

.006

.005

.008

.012

.005

.010

.016

.012

.021

.039

Falling Or Flying Object ($24,507)

Twisting ($20,395)

From Different Level (Elevation) ($55,162)

Repetitive Motion (strain or injury by) ($28,062)

Ice Or Snow ($28,959)

Fall, Slip, or Trip on Same Level ($27,197)

Strain or Injury by Pushing or Pulling ($26,959)

Fall, Slip, or Trip ($26,898)

Strain or Injury ($25,346)

Strain or Injury by Lifting ($22,416)

.00 .01 .02 .03 .04

Caus

e of

Inju

ry(P

Y 20

15 A

nnua

l Ave

rage

Cos

t Per

Cas

e)

Lost-Time Cases/$1M Payroll

The Relative Frequencies of Injuries Caused by Strains & SprainsHave Also Been Nearly Halved

Policy Year 2006

Policy Year 2015

Source: Unit Statistical Data, First Report Lost-Time Cases Per $1 Million of Payroll

14

.624

.827

.905

.936.956 .963

.622

.851

.922

.951.962 .963

.5

.6

.7

.8

.9

1.0

1st 2nd 3rd 4th 5th 6th

Clos

ed to

Tota

l Los

t-Ti

me

Case

Cou

nts

Report Level(Policy Year Basis)

Claim Closure Improvement is Especially Evident from Second to Fourth Reports of Injury

Valuation Year 2013Valuation Year 2017

Source: MWCIA Financial Call Data

15

Claim Severity

16

18.2 18.5 18.018.8 18.9

19.718.3

19.920.9

21.222.1 22.2 21.6 21.8 21.6 22.3 22.6 22.8

23.424.4

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017p

$ T

hous

ands

Accident Year

Indemnity Case-Incurred Severities HaveGrown by a Modest 1.7% Per Year Since 2008

Minnesota

NCCI States

Source: MWCIA Financial Call Data valued as of 12/31/2017, Losses and Claim Counts Developed to Ultimate ReportNCCI State of the Market Report presented at 2018 Annual Issues Symposium

17

0%

20%

40%

60%

80%

100%

120%

Cum

ulat

ive

Chan

ge

Accident Year

Changes in Indemnity Severity Have Fallen Below Changes in the Statewide Average Weekly Wage Over the Past Eight Years

Indemnity Severity

SAWW

Source: MWCIA Financial Data Valued as of 12/31/2017, Minnesota Department of Labor and Industry

Annual Average Change (2007-2017p)Indemnity Severity: +1.9%

SAWW: +2.4%

Annual Average Change (1997-2007)Indemnity Severity: +7.4%

SAWW: +3.9%

18

23.8 23.2 23.2 24.0 23.6

26.2

23.0 23.7 24.425.6

24.225.2 25.2 25.8 26.0 26.5

27.4 27.2

28.829.9

0

5

10

15

20

25

30

35

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017p

$ T

hous

ands

Accident Year

Lost-Time Medical Case-Incurred Severities Have Grown an Annual Average of 0.8% Since 2008, Well below NCCI-State Results

MinnesotaNCCI States

Source: MWCIA Financial Call Data valued as of 12/31/2017, Losses and Claim Counts Developed to Ultimate ReportNCCI State of the Market Report presented at 2018 Annual Issues Symposium

19

0%

20%

40%

60%

80%

100%

120%

Cum

ulat

ive

Chan

ge

Accident Year

Annual Changes in Both Lost-Time Medical Claim Severity and Countrywide Medicare Care Prices Have

Slowed Down Considerably Over the Past Ten Years

Lost-Time Medical Severity

Chain-Weighted PHC Index

Source: MWCIA Financial Data Valued as of 12/31/2017 Countrywide Chain-Weighted Personal Health Care (CW-PHC) Price Index from Centers for Medicare & Medicaid Services

Annual Average Change (1997-2007)Lost-Time Medical Severity: +8.2%Chain-Weighted PHC Index: +3.0%

Annual Average Change (2007-2017)Lost-Time Medical Severity: +2.0%Chain-Weighted PHC Index: +1.8%

20

55.5% 56.2%58.3%

59.7%62.9%

64.6%62.2%

68.6%

0%

10%

20%

30%

40%

50%

60%

70%

2012 2013 2014 2015 2016 2017 2018 2019Perc

enta

ge o

f Ulti

mat

e M

edic

al L

osse

s Pai

d at

3rd

Rpt

Ratemaking Report Year

The Percentage of Ultimate Medical Costs Paid at Third Reports Has Improved 13% Since 2012

Source: MWCIA Financial Data

21

Cost Distributions

22

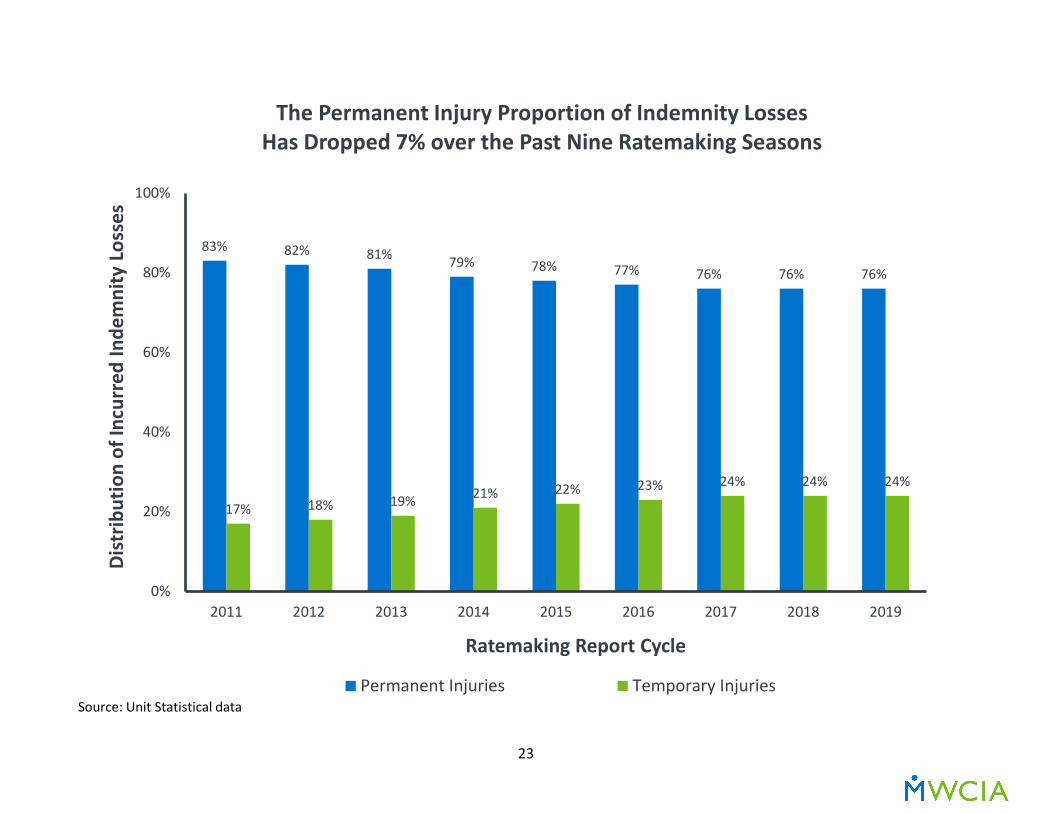

83% 82% 81% 79% 78% 77% 76% 76% 76%

17% 18% 19% 21% 22% 23% 24% 24% 24%

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014 2015 2016 2017 2018 2019

Dist

ribut

ion

of In

curr

ed In

dem

nity

Los

ses

Ratemaking Report Cycle

The Permanent Injury Proportion of Indemnity Losses Has Dropped 7% over the Past Nine Ratemaking Seasons

Permanent Injuries Temporary InjuriesSource: Unit Statistical data

23

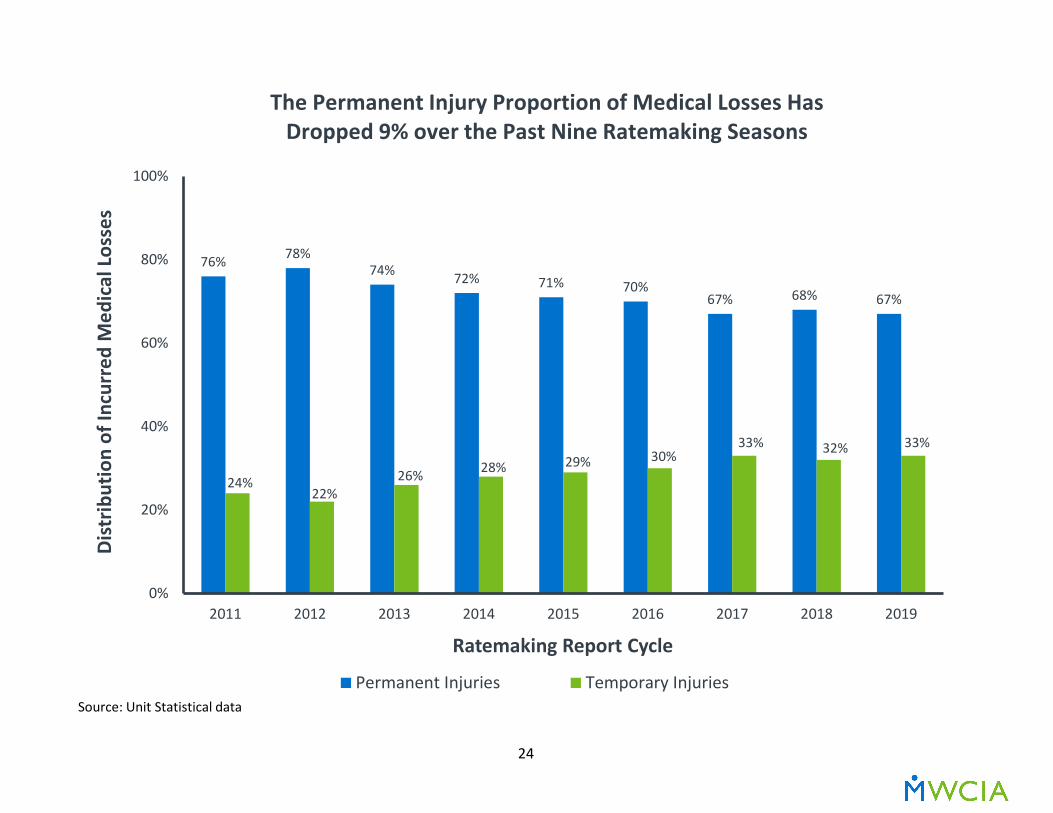

76% 78%74% 72% 71% 70%

67% 68% 67%

24%22%

26% 28% 29% 30%33% 32% 33%

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014 2015 2016 2017 2018 2019

Dist

ribut

ion

of In

curr

ed M

edic

al L

osse

s

Ratemaking Report Cycle

The Permanent Injury Proportion of Medical Losses Has Dropped 9% over the Past Nine Ratemaking Seasons

Permanent Injuries Temporary InjuriesSource: Unit Statistical data

24

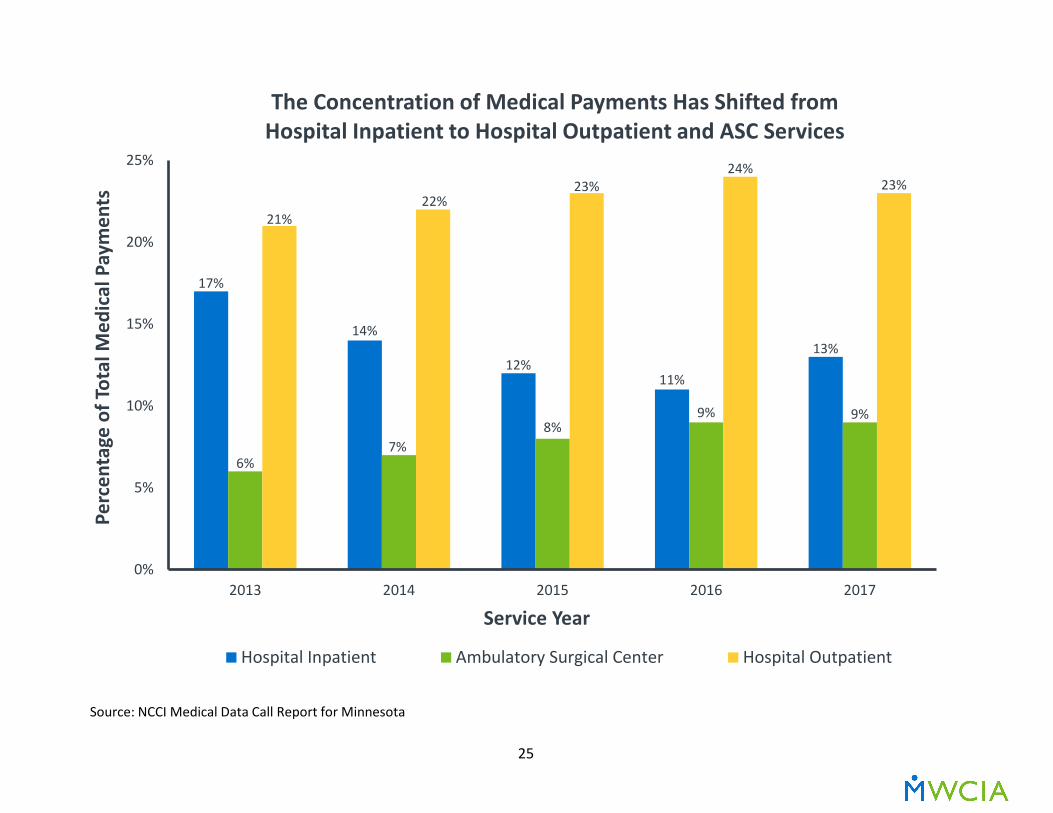

17%

14%

12%11%

13%

6%7%

8%9% 9%

21%22%

23%24%

23%

0%

5%

10%

15%

20%

25%

2013 2014 2015 2016 2017

Perc

enta

ge o

f Tot

al M

edic

al P

aym

ents

Service Year

The Concentration of Medical Payments Has Shifted from Hospital Inpatient to Hospital Outpatient and ASC Services

Hospital Inpatient Ambulatory Surgical Center Hospital Outpatient

Source: NCCI Medical Data Call Report for Minnesota

25

3.4

3.0

2.52.8

2.42.6

4.8

4.2

3.7

2.7 2.72.5

0

1

2

3

4

5

2011 2012 2013 2014 2015 2016

Shar

e of

Cla

ims w

ith In

patie

nt E

piso

des (

%)

Injury Year

Reductions in Inpatient Surgical Episodes Have Led toDecreases in Claims Requiring Inpatient Care

Nonsurgical Inpatient Surgical Inpatient

WCRI CompScope™ Medical Benchmarks for Minnesota, 19th Edition Claims With > 7 Days Of Lost Time At 12 Months Of Experience, Not Adjusted For Injury/Industry Mix

26

13.1

15.2 15.0 15.2 15.1 14.4

24.3

22.4 22.521.5

20.7

19.0

0

5

10

15

20

25

2011 2012 2013 2014 2015 2016

Shar

e of

Cla

ims w

ith F

acili

ty S

ervi

ces (

%)

Injury Year

Increases in ASC Services Have Led to Decreases in Hospital Outpatient Claims

Ambulatory Surgery Center (ASC) Hospital Outpatient

WCRI CompScope™ Medical Benchmarks for Minnesota, 19th Edition Claims With > 7 Days Of Lost Time At 12 Months Of Experience, Not Adjusted For Injury/Industry Mix

27

Case Reserves

28

7159 61 67

76 7263 62 67 72

-90-79

-92 -91 -97-105

-96-84 -85 -86

-150

-100

-50

0

50

100

150

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

$ M

illio

ns

Calendar Year

Net Indemnity Case Reserve Releases from Prior Accident Years Continue to Outstrip Establishment of Current Year Reserves

Latest Accident Year

All Prior Accident Years

Source: MWCIA Financial Call data

29

143

118134 142 143

158 160142

157 157

-60

-87-74

-126 -122 -127 -133 -139-152

-162

-200

-150

-100

-50

0

50

100

150

200

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

$ M

illio

ns

Calendar Year

The Establishment of Case Reserves on New Medical Claims Are Beginning to Be Counterbalanced by Net Reserve Releases from Prior Years

Latest Accident Year

All Prior Accident Years

Source: MWCIA Financial Call data

30

-19 -20

-31

-24 -21

-33 -33

-22-18

-14

83

31

60

1621

3127

3 5

-5

-40

-20

0

20

40

60

80

100

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

$ M

illio

ns

Calendar Year

2017 Saw Both Medical and Total Net Case Reserve Releases for the First Time in Modern History

Indemnity

Medical

Source: MWCIA Financial Call data

31