Embed Size (px)

Citation preview

Appendix 1

6.2 Audit Committee Meeting – 9 June 2020

Minutes of the Audit Committee Meeting held on 9 June 2020

Ordinary Meeting of Council

Thursday 18 June 2020 at 7:00pm

Queenscliff Town Hall 50 Learmonth Street, Queenscliff

Minutes Audit Committee Meeting

Tuesday 9 June 2020 at 3:30 pm

Queenscliff Town Hall 50 Learmonth Street, Queenscliff

Distribution

Members Mr Roland ‘Barney’ Orchard (Chair)

Mr Richard Bull

Mr Graeme Phipps

Ms Helen Butteriss

Cr Ross Ebbels

Cr Bob Merriman

Cr Susan Salter

Officers Martin Gill, Chief Executive Officer

Phillip Carruthers, General Manager Organisational Performance & Community Services

Gihan Kohobange, Manager Financial Services

Invitees

External Audit Provider: Crowe Australasia

Cassandra Gravenall, Associate Partner – Audit and Assurance

Felmer Ealdama, Manager – Audit and Assurance

Internal Audit Provider: HLB Mann Judd

Mark Holloway, Engagement Partner

Kundai Mtsambiwa, Manager Audit & Assurance

Borough of Queenscliffe Minutes for the Audit Committee Meeting 9 June 2020

Page 2 of 22

1. OPENING OF MEETING ..................................................................................................... 4

2. PRESENT & APOLOGIES .................................................................................................... 4

3. PECUNIARY INTEREST & CONFLICT OF INTEREST DISCLOSURES ......................................... 4

4. AUDIT COMMITTEE MEETING – 02 December 2019 .......................................................... 4

4.1 Confirmation of Minutes from Audit Committee Meeting 2 December 2019 ......... 4

4.2 Business Arising from Audit Committee Meeting 2 December 2019 ...................... 5

5. INTERNAL AUDIT .............................................................................................................. 6

5.1 Detailed internal audit reports – April / May 2020 ................................................ 6

5.2 Scope for internal audit review – 2021 to 2023 ..................................................... 9

6. EXTERNAL AUDIT ........................................................................................................... 10

6.1 External Audit strategy for financial year ending 30 June 2020 ............................ 10

6.2 External Audit 2019/20 interim audit management letter ................................... 10

7. REPORTS FROM THE VICTORIAN AUDITOR-GENERAL’S OFFICE (VAGO) ........................... 11

7.1 Other Performance Audits (of which Queenscliffe was not selected for audit) .... 11

7.1.1 Managing Development Contributions—Local Government ............................................ 11

8. REPORTS FROM THE RISK MANAGEMENT COMMITTEE .................................................. 13

9. REVIEW OF COUNCIL POLICIES........................................................................................ 13

9.1 Draft Council Policies for review by Audit Committee ......................................... 13

9.2 Council Policies adopted by Council .................................................................... 14

10. INFORMATION TO NOTE ................................................................................................ 15

10.1 New Accounting Standards ................................................................................. 15

10.2 Financial Impact of COVID 19 .............................................................................. 15

10.3 2019/20 Quarterly Financial Report as at 31 March 2020 .................................... 17

10.4 Draft Implementation Plan 2020/21 ................................................................... 17

10.5 Draft Budget 2020/21 (including Strategic Resource Plan and Long Term Financial Plan) .................................................................................................................. 17

10.6 The Victorian Auditor-General’s Office (VAGO) – Results of Local Government Audits 2018/19 ................................................................................................... 18

11. AUDIT COMMITTEE MEMBERSHIP .................................................................................. 20

11.1 Audit and Risk Committee Charter ...................................................................... 20

12. GENERAL BUSINESS ........................................................................................................ 21

13. DATES OF FUTURE AUDIT COMMITTEE MEETINGS .......................................................... 21

14. CONFIDENTIAL ITEMS ..................................................................................................... 22

15. CLOSE OF MEETING ........................................................................................................ 22

Borough of Queenscliffe Minutes for the Audit Committee Meeting 9 June 2020

Page 3 of 22

Appendices

Appendix 1 Agenda Item 4.1 Minutes of the Audit Committee Meeting 2 December 2019

Issued 20 December 2019

Appendix 2

Agenda Item 4.2 Internal Audit Report - Review of Payroll (updated)

Under separate cover

Appendix 3

Agenda Item 5.1 Detailed Internal Audit Reports – April / May 2020

Under separate cover

Appendix 4

Agenda Item 5.1 Follow-Up Review Report

Under separate cover

Appendix 5 Agenda Item 5.1 ICT Penetration Test Reports

Under separate cover

Appendix 6 Agenda Item 5.2 Proposed Internal Audit Review Topics 2021 – 2023

Under separate cover

Appendix 7

Agenda Item 6.1 External Audit Strategy for Financial Year Ending 30 June 2020

Under separate cover

Appendix 8 Agenda Item 6.2 External Audit 2019/20, Draft Interim Audit Management Letter

Under separate cover

Appendix 9 Agenda Item 8 Minutes of Compliance Committee (meetings held between December 2019 to May 2020)

Under separate cover

Appendix 10 Agenda Item 8 Updated Risk Register

Under separate cover

Appendix 11 Agenda Item 9.1 Revised Council Policy CP013: Procurement Revised Council Policy CP033: Creditor Management

Under separate cover

Appendix 12 Agenda Item 9.1 Standard Operating Procedures

Under separate cover

Appendix 13 Agenda Item 9.2 CP036: Fixed Assets CP025: Public Interest Disclosures CP049: Social Media Policy CP048: COVID-19 Financial Hardship Policy

Under separate cover

Appendix 14 Agenda Item 10.1 New Accounting Standards Position Paper

Under separate cover

Appendix 15 Agenda Item 10.3 2019/20 Quarterly Financial Report as at 31 March 2020

Under separate cover

Appendix 16 Agenda Item 11.1 Revised Audit and Risk Committee Charter

Under separate cover

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 4 of 22

1. OPENING OF MEETING

The Chair, Mr Roland ‘Barney’ Orchard, opened the meeting at 3:43pm.

2. PRESENT & APOLOGIES Present:

Mr Roland ‘Barney’ Orchard (Chair)

Mr Richard Bull

Ms Helen Butteriss

Mr Graeme Phipps

Cr Ross Ebbels

Cr Bob Merriman

Cr Susan Salter

Martin Gill, Chief Executive Officer

Phillip Carruthers, General Manager Organisational Performance & Community Services

Gihan Kohobange, Manager Financial Services

Cassandra Gravenall, Associate Partner – Audit and Assurance, Crowe Australasia (external audit provider) (via videoconference until 4:50pm)

Mark Holloway, Engagement Partner, HLB Mann Judd (internal audit provider) (until 4:35pm)

Jenni Walker, Executive Assistant & HR and Corporate Governance Coordinator (minutes)

Apologies:

Nil

3. PECUNIARY INTEREST & CONFLICT OF INTEREST DISCLOSURES Independent Members: Nil

Councillors: Nil

Officers: Nil

4. AUDIT COMMITTEE MEETING – 02 December 2019 4.1 Confirmation of Minutes from Audit Committee Meeting 2 December 2019 (Appendix 1) Moved: Graeme Phipps / Seconded: Richard Bull That the Minutes of the Audit Committee Meeting held on Monday 2 December 2019, as included at Appendix 1, be confirmed.

Carried

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 5 of 22

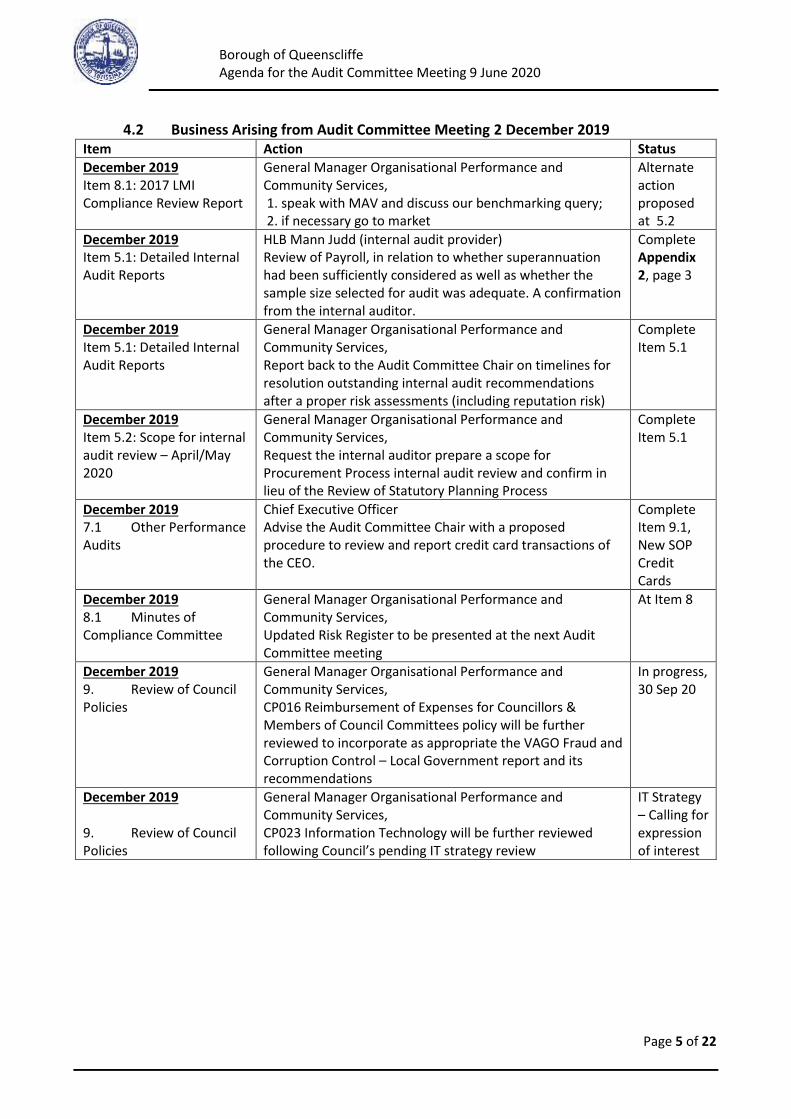

4.2 Business Arising from Audit Committee Meeting 2 December 2019 Item Action Status

December 2019 Item 8.1: 2017 LMI Compliance Review Report

General Manager Organisational Performance and Community Services, 1. speak with MAV and discuss our benchmarking query; 2. if necessary go to market

Alternate action proposed at 5.2

December 2019 Item 5.1: Detailed Internal Audit Reports

HLB Mann Judd (internal audit provider) Review of Payroll, in relation to whether superannuation had been sufficiently considered as well as whether the sample size selected for audit was adequate. A confirmation from the internal auditor.

Complete Appendix 2, page 3

December 2019 Item 5.1: Detailed Internal Audit Reports

General Manager Organisational Performance and Community Services, Report back to the Audit Committee Chair on timelines for resolution outstanding internal audit recommendations after a proper risk assessments (including reputation risk)

Complete Item 5.1

December 2019 Item 5.2: Scope for internal audit review – April/May 2020

General Manager Organisational Performance and Community Services, Request the internal auditor prepare a scope for Procurement Process internal audit review and confirm in lieu of the Review of Statutory Planning Process

Complete Item 5.1

December 2019 7.1 Other Performance Audits

Chief Executive Officer Advise the Audit Committee Chair with a proposed procedure to review and report credit card transactions of the CEO.

Complete Item 9.1, New SOP Credit Cards

December 2019 8.1 Minutes of Compliance Committee

General Manager Organisational Performance and Community Services, Updated Risk Register to be presented at the next Audit Committee meeting

At Item 8

December 2019 9. Review of Council Policies

General Manager Organisational Performance and Community Services, CP016 Reimbursement of Expenses for Councillors & Members of Council Committees policy will be further reviewed to incorporate as appropriate the VAGO Fraud and Corruption Control – Local Government report and its recommendations

In progress, 30 Sep 20

December 2019 9. Review of Council Policies

General Manager Organisational Performance and Community Services, CP023 Information Technology will be further reviewed following Council’s pending IT strategy review

IT Strategy – Calling for expression of interest

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 6 of 22

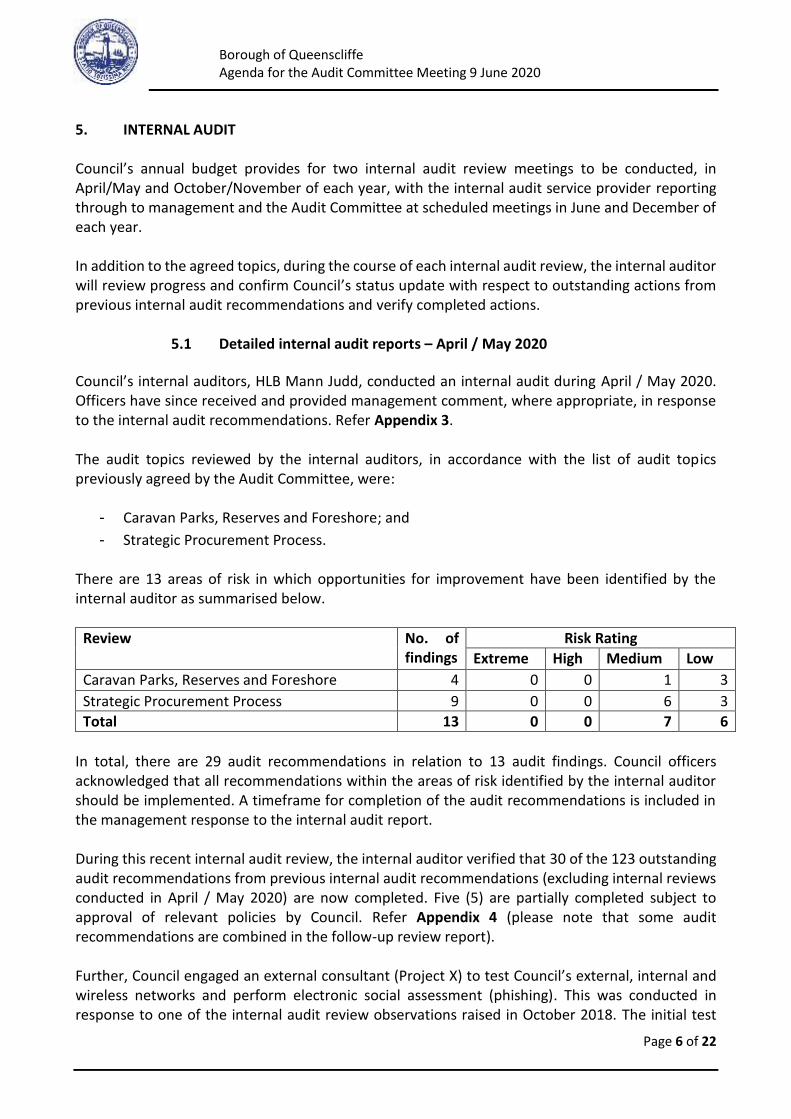

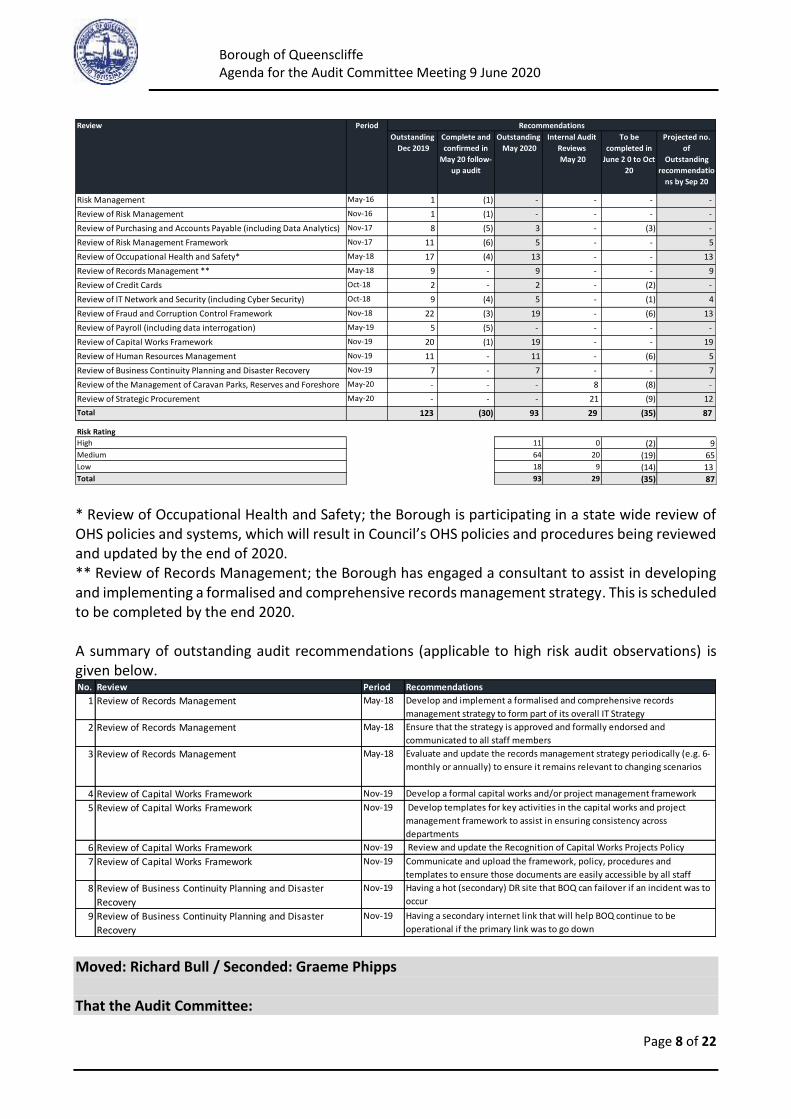

5. INTERNAL AUDIT Council’s annual budget provides for two internal audit review meetings to be conducted, in April/May and October/November of each year, with the internal audit service provider reporting through to management and the Audit Committee at scheduled meetings in June and December of each year. In addition to the agreed topics, during the course of each internal audit review, the internal auditor will review progress and confirm Council’s status update with respect to outstanding actions from previous internal audit recommendations and verify completed actions.

5.1 Detailed internal audit reports – April / May 2020

Council’s internal auditors, HLB Mann Judd, conducted an internal audit during April / May 2020. Officers have since received and provided management comment, where appropriate, in response to the internal audit recommendations. Refer Appendix 3. The audit topics reviewed by the internal auditors, in accordance with the list of audit topics previously agreed by the Audit Committee, were:

- Caravan Parks, Reserves and Foreshore; and

- Strategic Procurement Process. There are 13 areas of risk in which opportunities for improvement have been identified by the internal auditor as summarised below.

Review No. of findings

Risk Rating

Extreme High Medium Low

Caravan Parks, Reserves and Foreshore 4 0 0 1 3

Strategic Procurement Process 9 0 0 6 3

Total 13 0 0 7 6

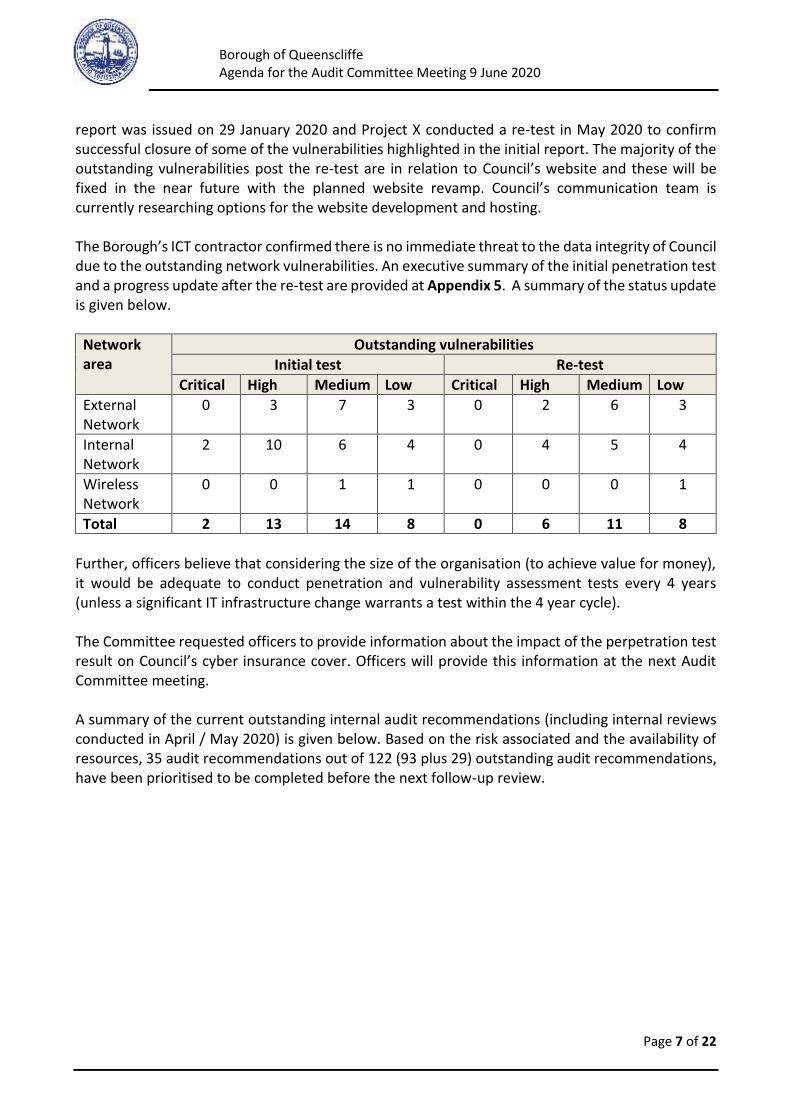

In total, there are 29 audit recommendations in relation to 13 audit findings. Council officers acknowledged that all recommendations within the areas of risk identified by the internal auditor should be implemented. A timeframe for completion of the audit recommendations is included in the management response to the internal audit report. During this recent internal audit review, the internal auditor verified that 30 of the 123 outstanding audit recommendations from previous internal audit recommendations (excluding internal reviews conducted in April / May 2020) are now completed. Five (5) are partially completed subject to approval of relevant policies by Council. Refer Appendix 4 (please note that some audit recommendations are combined in the follow-up review report). Further, Council engaged an external consultant (Project X) to test Council’s external, internal and wireless networks and perform electronic social assessment (phishing). This was conducted in response to one of the internal audit review observations raised in October 2018. The initial test

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 7 of 22

report was issued on 29 January 2020 and Project X conducted a re-test in May 2020 to confirm successful closure of some of the vulnerabilities highlighted in the initial report. The majority of the outstanding vulnerabilities post the re-test are in relation to Council’s website and these will be fixed in the near future with the planned website revamp. Council’s communication team is currently researching options for the website development and hosting. The Borough’s ICT contractor confirmed there is no immediate threat to the data integrity of Council due to the outstanding network vulnerabilities. An executive summary of the initial penetration test and a progress update after the re-test are provided at Appendix 5. A summary of the status update is given below.

Network area

Outstanding vulnerabilities

Initial test Re-test

Critical High Medium Low Critical High Medium Low

External Network

0 3 7 3 0 2 6 3

Internal Network

2 10 6 4 0 4 5 4

Wireless Network

0 0 1 1 0 0 0 1

Total 2 13 14 8 0 6 11 8

Further, officers believe that considering the size of the organisation (to achieve value for money), it would be adequate to conduct penetration and vulnerability assessment tests every 4 years (unless a significant IT infrastructure change warrants a test within the 4 year cycle). The Committee requested officers to provide information about the impact of the perpetration test result on Council’s cyber insurance cover. Officers will provide this information at the next Audit Committee meeting. A summary of the current outstanding internal audit recommendations (including internal reviews conducted in April / May 2020) is given below. Based on the risk associated and the availability of resources, 35 audit recommendations out of 122 (93 plus 29) outstanding audit recommendations, have been prioritised to be completed before the next follow-up review.

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 8 of 22

* Review of Occupational Health and Safety; the Borough is participating in a state wide review of OHS policies and systems, which will result in Council’s OHS policies and procedures being reviewed and updated by the end of 2020. ** Review of Records Management; the Borough has engaged a consultant to assist in developing and implementing a formalised and comprehensive records management strategy. This is scheduled to be completed by the end 2020. A summary of outstanding audit recommendations (applicable to high risk audit observations) is given below.

Moved: Richard Bull / Seconded: Graeme Phipps That the Audit Committee:

Outstanding

Dec 2019

Complete and

confirmed in

May 20 follow-

up audit

Outstanding

May 2020

Internal Audit

Reviews

May 20

To be

completed in

June 2 0 to Oct

20

Projected no.

of

Outstanding

recommendatio

ns by Sep 20

Risk Management May-16 1 (1) - - - -

Review of Risk Management Nov-16 1 (1) - - - -

Review of Purchasing and Accounts Payable (including Data Analytics) Nov-17 8 (5) 3 - (3) -

Review of Risk Management Framework Nov-17 11 (6) 5 - - 5

Review of Occupational Health and Safety* May-18 17 (4) 13 - - 13

Review of Records Management ** May-18 9 - 9 - - 9

Review of Credit Cards Oct-18 2 - 2 - (2) -

Review of IT Network and Security (including Cyber Security) Oct-18 9 (4) 5 - (1) 4

Review of Fraud and Corruption Control Framework Nov-18 22 (3) 19 - (6) 13

Review of Payroll (including data interrogation) May-19 5 (5) - - - -

Review of Capital Works Framework Nov-19 20 (1) 19 - - 19

Review of Human Resources Management Nov-19 11 - 11 - (6) 5

Review of Business Continuity Planning and Disaster Recovery Nov-19 7 - 7 - - 7

Review of the Management of Caravan Parks, Reserves and Foreshore May-20 - - - 8 (8) -

Review of Strategic Procurement May-20 - - - 21 (9) 12

Total 123 (30) 93 29 (35) 87

Risk Rating

High 11 0 (2) 9Medium 64 20 (19) 65Low 18 9 (14) 13 Total 93 29 (35) 87

Review Period Recommendations

No. Review Period Recommendations

1 Review of Records Management May-18 Develop and implement a formalised and comprehensive records

management strategy to form part of its overall IT Strategy

2 Review of Records Management May-18 Ensure that the strategy is approved and formally endorsed and

communicated to all staff members

3 Review of Records Management May-18 Evaluate and update the records management strategy periodically (e.g. 6-

monthly or annually) to ensure it remains relevant to changing scenarios

4 Review of Capital Works Framework Nov-19 Develop a formal capital works and/or project management framework

5 Review of Capital Works Framework Nov-19 Develop templates for key activities in the capital works and project

management framework to assist in ensuring consistency across

departments

6 Review of Capital Works Framework Nov-19 Review and update the Recognition of Capital Works Projects Policy

7 Review of Capital Works Framework Nov-19 Communicate and upload the framework, policy, procedures and

templates to ensure those documents are easily accessible by all staff

8 Review of Business Continuity Planning and Disaster

Recovery

Nov-19 Having a hot (secondary) DR site that BOQ can failover if an incident was to

occur

9 Review of Business Continuity Planning and Disaster

Recovery

Nov-19 Having a secondary internet link that will help BOQ continue to be

operational if the primary link was to go down

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 9 of 22

a) Confirm and accept the internal audit reports, including management comment, as provided at Appendix 3;

b) Confirm the previous audit recommendations, now verified by the internal auditor as completed (as provided at Appendix 4), be removed from the set of outstanding recommendations; and

c) Note that the penetration and vulnerability assessments test to be conducted in every four year unless an early test is required due to significant changes to the Borough’s IT infrastructure.

Carried

5.2 Scope for internal audit review – 2021 to 2023

The current contract for the provision of internal audit services with HLB Mann Judd expires in August 2020. However, there is an option of an additional two-year extension to the period of the contract at Council’s discretion and subject to a successful performance review of the Internal Audit Service Provider by the Audit Committee. A new strategic internal audit plan will be finalised based on the outcome of the performance review of the current internal audit service provider, presented as a confidential item. In the past, on average four internal audit reviews have been conducted within a financial year. However, that has proved to be ineffective considering the number of current outstanding internal audit recommendations.

Section 54 (5) of the Local Government Act 2020 requires the Audit and Risk Committee to prepare a biannual audit and risk report that describes the activities of the Audit and Risk Committee including its findings and recommendations.

Considering the staff resources available within the organisations, officers suggest only two internal audit reviews per financial year in addition to a follow-up review of the outstanding audit recommendations. Further, a staggered approached is proposed to ensure effective participation of the staff in internal audit reviews. Due to the limited staff resources, the same staff members are involved in facilitating most of the internal reviews. Such a staggered approach will help the Audit Committee as well in their biannual audit and risk reporting.

A summary of the internal audit reviews conducted since 2011 and internal audit review proposed for 2021 – 2023 are included at Appendix 6.

Officers would seek advice from the Audit Committee regarding the scope and topics for future internal audit reviews.

Recommendation: That the Audit Committee confirms: a) Only two internal audit reviews per financial year are conducted in addition to a follow-up

review of the outstanding audit recommendations ; and b) The proposed internal audit review topics for 2021 – 2023 as provided at Appendix 6.

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 10 of 22

Moved: Richard Bull / Seconded: Graeme Phipps That the Audit Committee notes and supports: a) That only two internal audit reviews per financial year will be conducted in addition to a

follow-up review of the outstanding audit recommendations and this approach will be reviewed after 12 months; and

b) The proposed internal audit review topics for 2021 – 2023 as provided at Appendix 6. Carried

6. EXTERNAL AUDIT

Council’s annual budget provides for two external audit reviews to be conducted each year, to meet all legislative requirements with respect to the annual financial and performance reports.

An interim audit is conducted in April/May each year, which includes a review of policies and processes.

A final audit of Council’s annual financial statements (including financial report and performance statement) is completed in August of each year, with the external auditor reporting through to management and the Audit Committee at a scheduled meeting in September of each year.

6.1 External Audit strategy for financial year ending 30 June 2020

Council’s external auditor, Crowe Australasia, has provided Council with the audit strategy for the 2019/20 year-end audit approach which will be undertaken by the Victorian Auditor General’s Office (VAGO) and its agents in auditing local government accounts. Refer Appendix 7.

New items for 2019/20, as included in the external audit strategy, are as follows:

- New accounting standards (more details are provided at Agenda item 10.1) o AASB 15 Revenue from Contracts with Customers and AASB 1058 Income of Not-for-

Profit Entities o AASB 16 Leases (replaces AASB 117 Leases)

- COVID-19 Pandemic (more details are provided at Agenda item 10.2)

Moved: Richard Bull / Seconded: Helen Butteriss That the external audit strategy for financial year ending 30 June 2020, included at Appendix 7, be received.

Carried

6.2 External Audit 2019/20 interim audit management letter

Council’s external auditor, Crowe Australasia, conducted an interim audit for the 2019/20 year-end accounts in May 2020. Officers have since received and provided management comment, where appropriate, in response to the external audit recommendations. Refer Appendix 8.

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 11 of 22

The audit identified one finding in relation to accounting for Work In Progress (WIP). One key interim audit area (shell accounts) was outstanding as at the date of the draft interim audit management letter which has now been finalised. Moved: Richard Bull / Seconded: Graeme Phipps That the draft interim audit management letter including management comment, included at Appendix 8, be noted.

Carried

7. REPORTS FROM THE VICTORIAN AUDITOR-GENERAL’S OFFICE (VAGO) The Victorian Auditor-General’s Office (VAGO) provides in its Annual Plan for a range of performance audits to be conducted each financial year. These performance reports typically include state government departments as well as a sample of local councils selected for audit. The Borough of Queenscliffe was included in the performance audit conducted in 2018/19 in relation to Reporting on Local Government Performance.

7.1 Other Performance Audits (of which Queenscliffe was not selected for audit)

7.1.1 Managing Development Contributions—Local Government The Victorian Auditor-General’s Office (VAGO) has tabled the following reports with Parliament in March 2020: https://www.audit.vic.gov.au/report/managing-development-contributions?section=33453--audit-overview&show-sections=1#audit-overview

Background VAGO assessed whether development contributions provide required infrastructure to new and growing communities. VAGO has examined the following programs,

The Growth Areas Infrastructure Contributions program, or GAIC, allow the state government to obtain funds from developers to help deliver state infrastructure in Melbourne’s fringe suburbs.

The Development Contributions Plans program, or DCP, allow councils to obtain funds from developers to help deliver community or transport infrastructure.

Then, instead of using a DCP, seven councils in growth areas can use the Infrastructure Contributions Plans program, or ICPs, to support infrastructure delivery. ICPs are meant to be simpler and cheaper than DCPs. The state government is still implementing the ICP program and plans to expand it to more councils.

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 12 of 22

In addition to DCPs and ICPs, councils can also enter voluntary agreements with developers on a project-by-project basis.

VAGO conclusion drawn from this audit “Overall, we found that Victoria’s development contributions are not delivering the infrastructure that growing communities need to support their quality of life. This is largely because state agencies have not managed development contributions tools strategically to maximise their value and impact. State agencies have set up development contributions programs with little consideration of how they interact, or their collective aims and impact. As a result, Victoria now has a patchwork of overlapping programs that operate in isolation. Without an overarching strategy or coordination, state agency management of development contributions tools will remain inefficient and not consider how contributions could best meet community needs.”

VAGO Overall Recommendation Department of Environment, Land, Water and Planning to create an overarching development contributions framework that establishes a strategic direction, overall accountability, and clear guidance. VAGO Recommendations directly applicable to councils “We recommend that that the Department of Environment, Land, Water and Planning and the Victorian Planning Authority, in consultation with councils: Complete outstanding work to implement the Infrastructure Contributions Plan program, including:

defining Strategic Development Areas and Regional Greenfield Growth areas

recommending to government when the program should expand into Strategic Development Areas and Regional Greenfield Growth areas

recommending to government which parts of Victoria should be included in these categories, using evidence‐based eligibility criteria

recommending to government how to calculate levies for Infrastructure Contributions Plans in new areas

keeping all councils informed about implementation progress and decisions made’’ Relevance for the Borough of Queenscliffe At appendix C of the report, VAGO has identified the Borough as a nil recipient of GAIC and DCP for 2016/17 and 2017/18 financial years. Considering the very limited opportunities for new developments activities within the Borough of Queenscliff, the impact of recommendations mentioned in this report is very minimal for the Borough. Moved: Richard Bull / Seconded: Graeme Phipps That the summary provided by Council officers, with respect to this VAGO Report, be noted.

Carried

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 13 of 22

8. REPORTS FROM THE RISK MANAGEMENT COMMITTEE Risk management committee meetings are held monthly as a part of the Compliance Committee. The minutes of December 2019 to May 2020 Compliance Committee meetings, which incorporates the Risk Committee, are provided at Appendix 9. The updated risk register since the last Audit Committee meeting in December 2019, is provided at Appendix 10. Moved: Helen Butteriss / Seconded: Graeme Phipps That the Audit Committee note: a) the minutes of Compliance Committee meetings held between December 2019 to May 2020;

and b) the updated risk register provided at Appendix 10.

Carried The Chair noted the impressive work and achievements of the Compliance Committee and asked that the Committee’s thanks and appreciation be minuted and passed on to the Compliance Committee. 9. REVIEW OF COUNCIL POLICIES Council policies are reviewed by officers and adopted by Council on a rolling basis, with most policies scheduled for triennial review, noting however that some policies require review every year (e.g. Procurement). It is preferred that policies with a risk management focus be reviewed by the Audit Committee prior to being forwarded to Council for adoption, however this is dependent on the timing of scheduled Audit Committee meetings and the allocation of staff resources to undertake the policy review work. 9.1 Draft Council Policies for review by Audit Committee The following draft Council Policies are provided, at Appendix 11, for review by Audit Committee, prior to being considered by Council for adoption at its Ordinary Meeting on 18 June 2020:

Revised Council Policy CP013: Procurement

Revised Council Policy CP033: Creditor Management

Officers have considered better practices mentioned in the following reports in reviewing and developing the above policies and related Standards Operating Procedures (SOPs):

internal audit review reports;

VAGO, Fraud and Corruption Control—Local Government (June 2019); and

VAGO, Results of Local Government Audits 2018/19. Copies of related SOPs are provided at Appendix 12 for reference.

A summary of the key changes are summarised below:

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 14 of 22

Any purchase in excess of $1,000 requires writing quotations (currently in excess of $5,000). This will minimise the risk exposure of committing for a purchase without a formal quotation from 9% of total material and service to 2%;

Purchase order exemptions to cover fixed term contracts, utility payments and meeting fee approved by Council;

Quotation exemptions to formalise current accepted practices;

New SOP to manage credit cards;

New SOP to govern tender process;

New form to declare conflict of interest;

Introduction of “Creditor Creation / Update Request Form”;

Vetting process for new suppliers; and

Periodic review of supplier master data (data cleansing). Moved: Richard Bull / Seconded: Graeme Phipps That the Audit Committee endorse the draft revisions to Council Policy CP013 and CP033, as included at Appendix 11, and recommend that Council consider adoption of these policies at its Ordinary Meeting on 18 June 2020.

Carried

9.2 Council Policies adopted by Council

Council policies are reviewed by officers and adopted by Council on a rolling basis, with most policies scheduled for triennial review, noting however that some policies require review every year (e.g. Procurement). It is preferred that policies with a risk management focus be reviewed by the Audit Committee prior to being forwarded to Council for adoption, however this is dependent on the timing of scheduled Audit Committee meetings and the allocation of staff resources to undertake the policy review work. Council has adopted the following policies since the last Audit Committee meeting in December 2019 (Appendix 13): Revised Council Policies

1. CP036: Fixed Assets Key changes were (input from the audit committee through the Chair)

Frequency of valuation to synchronise with the frequency of condition assessment and practices within the local government sector.

Introduction of a materiality level to trigger exceptions to proposed frequency of revaluation.

2. CP025: Public Interest Disclosures (was previous policy ”Protected Disclosures’’; minor

changes to reflect correct definitions as per the Act and updated for contact details). New Council Policies

CP049: Social Media Policy

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 15 of 22

CP048: COVID-19 Financial Hardship Policy Moved: Richard Bull / Seconded: Graeme Phipps That the Audit Committee note the policies recently adopted by Council.

Carried

10. INFORMATION TO NOTE 10.1 New Accounting Standards Officers have prepared a position paper provided at Appendix 14, summarising the impact of the new accounting standards on the Borough’s financial statements. Council’s external auditor has performed a preliminary review of the position paper and has agreed in principle with the conclusions drawn. The assessment will be reviewed again before finalising the 2019/20 financial year end. Moved: Graeme Phipps / Seconded: Richard Bull That the Audit Committee note the position paper on new accounting standards provided at Appendix 14.

Carried

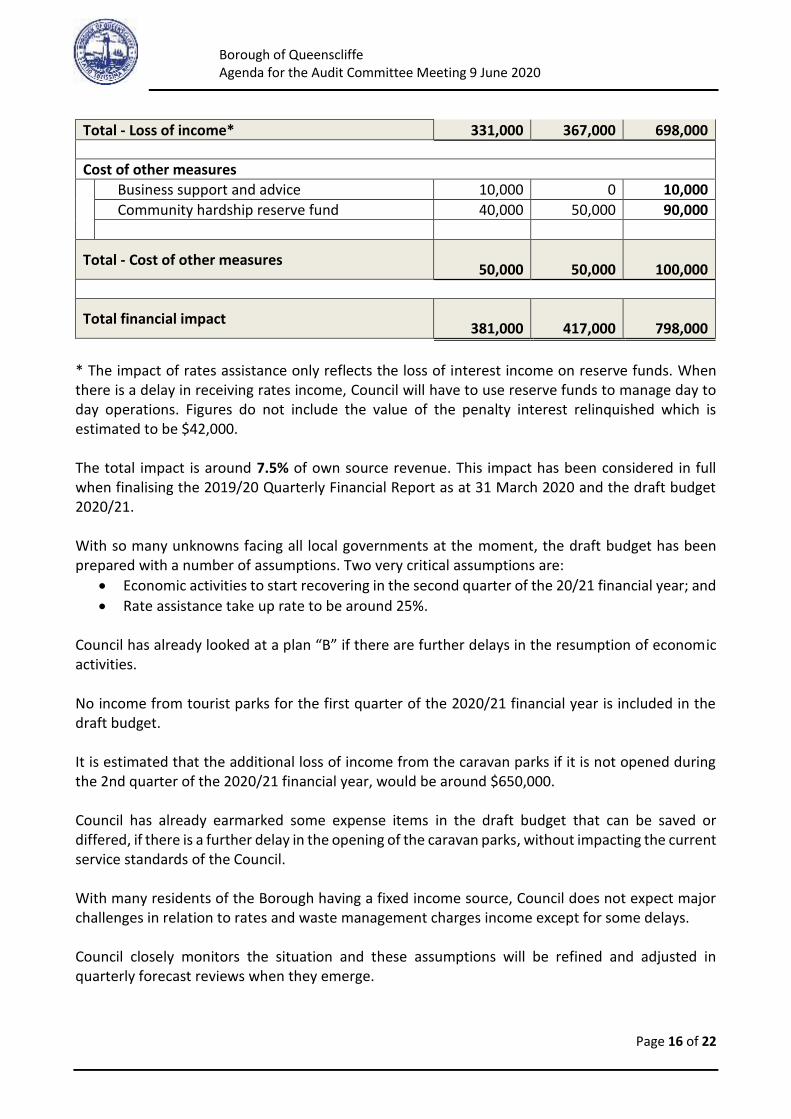

10.2 Financial Impact of COVID 19 A summary of the financial impact of COVID 19, as presented to Council, is provided below. The short term impacts of the coronavirus pandemic are significant and unavoidable. Revenue losses resulting from the closure of caravan parks are difficult to project, but are expected to reach six figures. Additional expenses from Council’s subsidisation of many fees and charges to support our community are necessary stimulus measures. Estimated financial impact to the Borough is summarised in the below table.

Description 2019/20 ($) 2020/21 ($) Total ($) Loss of income

Estimated loss of income from the caravan parks

311,000 179,000 490,000

Loss of income due to subsidisations

- Rates (rebate on waste management charge) - 130,000 130,000

- Lease rental (6 month free) 18,000 18,000 36,000

- Environmental health fees (20/21 free) - 30,000 30,000

- Local law fees (20/21 free) - 8,000 8,000

- Interest income (suspend penalty interest)* 2,000 2,000 4,000

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 16 of 22

Total - Loss of income* 331,000 367,000 698,000

Cost of other measures

Business support and advice 10,000 0 10,000

Community hardship reserve fund 40,000 50,000 90,000

Total - Cost of other measures

50,000

50,000

100,000

Total financial impact

381,000

417,000

798,000

* The impact of rates assistance only reflects the loss of interest income on reserve funds. When there is a delay in receiving rates income, Council will have to use reserve funds to manage day to day operations. Figures do not include the value of the penalty interest relinquished which is estimated to be $42,000. The total impact is around 7.5% of own source revenue. This impact has been considered in full when finalising the 2019/20 Quarterly Financial Report as at 31 March 2020 and the draft budget 2020/21. With so many unknowns facing all local governments at the moment, the draft budget has been prepared with a number of assumptions. Two very critical assumptions are:

Economic activities to start recovering in the second quarter of the 20/21 financial year; and

Rate assistance take up rate to be around 25%. Council has already looked at a plan “B” if there are further delays in the resumption of economic activities. No income from tourist parks for the first quarter of the 2020/21 financial year is included in the draft budget. It is estimated that the additional loss of income from the caravan parks if it is not opened during the 2nd quarter of the 2020/21 financial year, would be around $650,000. Council has already earmarked some expense items in the draft budget that can be saved or differed, if there is a further delay in the opening of the caravan parks, without impacting the current service standards of the Council. With many residents of the Borough having a fixed income source, Council does not expect major challenges in relation to rates and waste management charges income except for some delays. Council closely monitors the situation and these assumptions will be refined and adjusted in quarterly forecast reviews when they emerge.

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 17 of 22

Further, Council is aware of the risk associated in relying heavily on rates and income from caravan parks as own source revenue streams in funding services offered to the community. Moved: Graeme Phipps / Seconded: Richard Bull That the summary provided by Council officers, with respect to financial impact of COVID 19, be noted.

Carried 10.3 2019/20 Quarterly Financial Report as at 31 March 2020

The 31 March 2020 quarterly financial report was issued to Council at its Ordinary Council Meeting on 23 April 2020. This information is provided at Appendix 15. Moved: Helen Butteriss / Seconded: Graeme Phipps That the 2019/20 Quarterly Financial Report as at 31 March 2020, included at Appendix 15, be noted.

Carried

10.4 Draft Implementation Plan 2020/21

The Draft 2020/21 Implementation plan was endorsed by Council at its Ordinary Council Meeting on 23 April 2020. This document was out on exhibition for public comment until the public submission period closed on Monday 25 May 2020. An electronic copy of the Draft Implementation Plan 2020/21 is available to the public on Council’s website and can be accessed via the following link: https://www.queenscliffe.vic.gov.au/images/forms/BoQ_Draft_Implementation_Plan_2020-21_WEB.pdf Moved: Richard Bull / Seconded: Graeme Phipps That the Draft Implementation Plan 2020/21 be noted.

Carried

10.5 Draft Budget 2020/21 (including Strategic Resource Plan and Long Term Financial Plan)

The Draft 2020/21 (including Strategic Resource Plan and Long Term Financial Plan) was endorsed by Council at its Ordinary Council Meeting on 23 April 2020. This document was out on exhibition for public comment until the public submission period closed Monday 25 May 2020.

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 18 of 22

An electronic copy of the Draft Budget 2020/21 (including Strategic Resource Plan and Long Term Financial Plan) is available to the public on Council’s website and can be accessed via the following link: https://www.queenscliffe.vic.gov.au/images/forms/BoQ_Draft_Budget_2020-21_WEB.pdf Moved: Helen Butteriss / Seconded: Graeme Phipps That the Draft Budget 2020/21 (including Strategic Resource Plan and Long Term Financial Plan) be noted.

Carried

10.6 The Victorian Auditor-General’s Office (VAGO) – Results of Local Government Audits 2018/19

The Victorian Auditor-General’s Office (VAGO) tabled this report with Parliament on 27 November 2019. The Borough of Queenscliffe received a clear audit opinion on each of the general purpose financial statements and performance statement, for the 2018/19 financial year. A full copy of the VAGO report is available by accessing the following web link: https://www.audit.vic.gov.au/sites/default/files/2019-11/20191127-Local-Government-report.pdf The local government dashboard, with respect to the local government audit results, can be accessed via the link below: https://www.audit.vic.gov.au/report/results-2018-19-audits-local-government#chapter-1 A summary of the key findings:

Overall, most Councils assessed themselves as being adequately prepared for the incoming accounting standards and concluded that the impact was minimal;

The sector continue to experience internal control weakness surrounding procurement practices, assets management and valuation process, and with management oversight and monitoring of its outsourced service providers; and

Sustainability assessments broadly found no significant concerns with the sector’s short-term indicators. However, some longer-term capital replacement indicators were a little weaker in the regional and rural councils, but were not considered a high risk.

The summary report given below was provided by officers to Council, at its meeting on 27 February 2020, with respect to the VAGO report on Local Government audit outcomes for the 2018/19 financial year including a five-year average and short term forecasts.

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 19 of 22

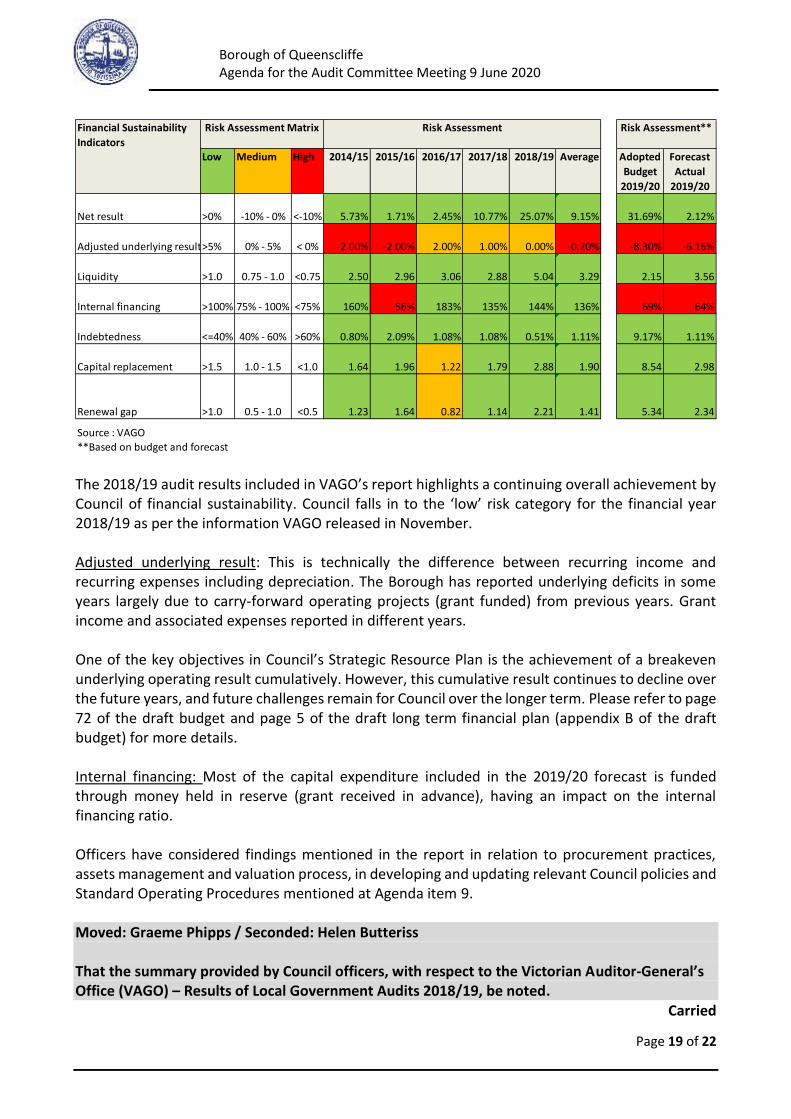

The 2018/19 audit results included in VAGO’s report highlights a continuing overall achievement by Council of financial sustainability. Council falls in to the ‘low’ risk category for the financial year 2018/19 as per the information VAGO released in November. Adjusted underlying result: This is technically the difference between recurring income and recurring expenses including depreciation. The Borough has reported underlying deficits in some years largely due to carry-forward operating projects (grant funded) from previous years. Grant income and associated expenses reported in different years. One of the key objectives in Council’s Strategic Resource Plan is the achievement of a breakeven underlying operating result cumulatively. However, this cumulative result continues to decline over the future years, and future challenges remain for Council over the longer term. Please refer to page 72 of the draft budget and page 5 of the draft long term financial plan (appendix B of the draft budget) for more details. Internal financing: Most of the capital expenditure included in the 2019/20 forecast is funded through money held in reserve (grant received in advance), having an impact on the internal financing ratio. Officers have considered findings mentioned in the report in relation to procurement practices, assets management and valuation process, in developing and updating relevant Council policies and Standard Operating Procedures mentioned at Agenda item 9. Moved: Graeme Phipps / Seconded: Helen Butteriss That the summary provided by Council officers, with respect to the Victorian Auditor-General’s Office (VAGO) – Results of Local Government Audits 2018/19, be noted.

Carried

Low Medium High 2014/15 2015/16 2016/17 2017/18 2018/19 Average Adopted

Budget

2019/20

Forecast

Actual

2019/20

Net result >0% -10% - 0% <-10% 5.73% 1.71% 2.45% 10.77% 25.07% 9.15% 31.69% 2.12%

Adjusted underlying result>5% 0% - 5% < 0% -2.00% -2.00% 2.00% 1.00% 0.00% -0.20% -8.30% -6.16%

Liquidity >1.0 0.75 - 1.0 <0.75 2.50 2.96 3.06 2.88 5.04 3.29 2.15 3.56

Internal financing >100% 75% - 100% <75% 160% 56% 183% 135% 144% 136% 69% 64%

Indebtedness <=40% 40% - 60% >60% 0.80% 2.09% 1.08% 1.08% 0.51% 1.11% 9.17% 1.11%

Capital replacement >1.5 1.0 - 1.5 <1.0 1.64 1.96 1.22 1.79 2.88 1.90 8.54 2.98

Renewal gap >1.0 0.5 - 1.0 <0.5 1.23 1.64 0.82 1.14 2.21 1.41 5.34 2.34

Source : VAGO**Based on budget and forecast

Risk Assessment Risk Assessment**Risk Assessment MatrixFinancial Sustainability

Indicators

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 20 of 22

11. AUDIT COMMITTEE MEMBERSHIP Council’s Audit Committee membership comprises Councillors nominated by Council and up to four independent members. 11.1 Audit and Risk Committee Charter The Local Government Act 2020 (the Act) expands the scope of audit committees, including support for the committee to assume a broader risk management role over and above financial auditing. Under the new arrangements, councils must adopt a charter for the Audit and Risk Committee that satisfies a number of requirements listed in the Act. Membership of the committee also varies from previous requirements for Audit Committees. There are five new requirements that Audit and Risk Committees must meet:

1. Audit and Risk Charter The council must prepare and approve a committee charter and establish the committee (appoint members) by 1 September 2020.

2. Reporting to council The committee must report to council twice yearly; the report must include the committee’s findings and recommendations.

3. Membership A majority of committee members must be independent of council; the chair must not be a councillor and members of council staff must not be committee members. Collectively, the committee must have expertise in financial and risk management and experience in public sector management.

4. Self-assessment The committee must undertake an annual assessment of its own performance against the charter and report on this to council.

5. Workplan The committee must adopt an annual workplan.

As per the section 54 of the Act, the committee charter must specify the functions and responsibilities of the committee, and must include the following functions:

1. monitor the compliance of council policies and procedures with the overarching governance principles and the Act and any regulations and Ministerial directions;

2. monitor council financial and performance reporting; 3. monitor and provide advice on risk management and fraud prevention systems and controls;

and 4. oversee internal and external audit functions.

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 21 of 22

Section 54 of the Act also describes the work an Audit and Risk committee must undertake and administrative instructions. While section 139 of the previous Act (1989) has already been repealed, the new Act (2020) specifically allows for the continued operation of an audit committee established under that section (prior to the repeal) to operate until the new committee is established. In addition to its responsibilities under the Act, Council have resolved ‘to ensure the Charter acknowledges that climate change governance is integral to the Audit Committee’s review of Council activities”. Officers have recently reviewed the Charter, in light of the changes proposed. The revised Charter is given at Appendix 16.

Recommendation: That the revised Audit and Risk Committee Charter (including Terms of Reference), at Appendix 16, be accepted and forwarded to Council for consideration at its next Ordinary Council Meeting.

The Committee deferred consideration of this matter and requested that Officers provide them with a model Charter and the relevant sections of the Local Government Act 2020. The four independent members of the Committee will then review the revised Charter as tabled (Appendix 16) and provide feedback through the Chair by 30 June 2020.

12. GENERAL BUSINESS

13. DATES OF FUTURE AUDIT COMMITTEE MEETINGS

Audit Committee meetings are scheduled to occur at least one week prior to an Ordinary Council Meeting, in order for the Minutes of the Audit Committee meeting to be finalised and included in the Agenda for the Ordinary Council Meeting, for acceptance by Council. All meetings of the Audit Committee will commence at 3:30pm. The September meeting of Audit Committee each year is for the specific purpose of reviewing the draft financial statements and recommending that Council consider adoption of the financial statements, in principle, at its Ordinary Council Meeting in September.

Audit Committee Meeting Ordinary Council Meeting

Monday 7 September 2020 Thursday 17 September 2020

Monday 7 December 2020 Thursday 17 December 2020

Borough of Queenscliffe Agenda for the Audit Committee Meeting 9 June 2020

Page 22 of 22

14. CONFIDENTIAL ITEMS A confidential matter to be circulated later.

Moved: Helen Butteriss / Seconded: Graeme Phipps That the Audit Committee confirm the performance review of the current internal audit service provider is successful.

Carried 15. CLOSE OF MEETING Meeting closed at 6:06pm.