Embed Size (px)

Citation preview

1

Mixed General MeetingApril 29, 2005

2

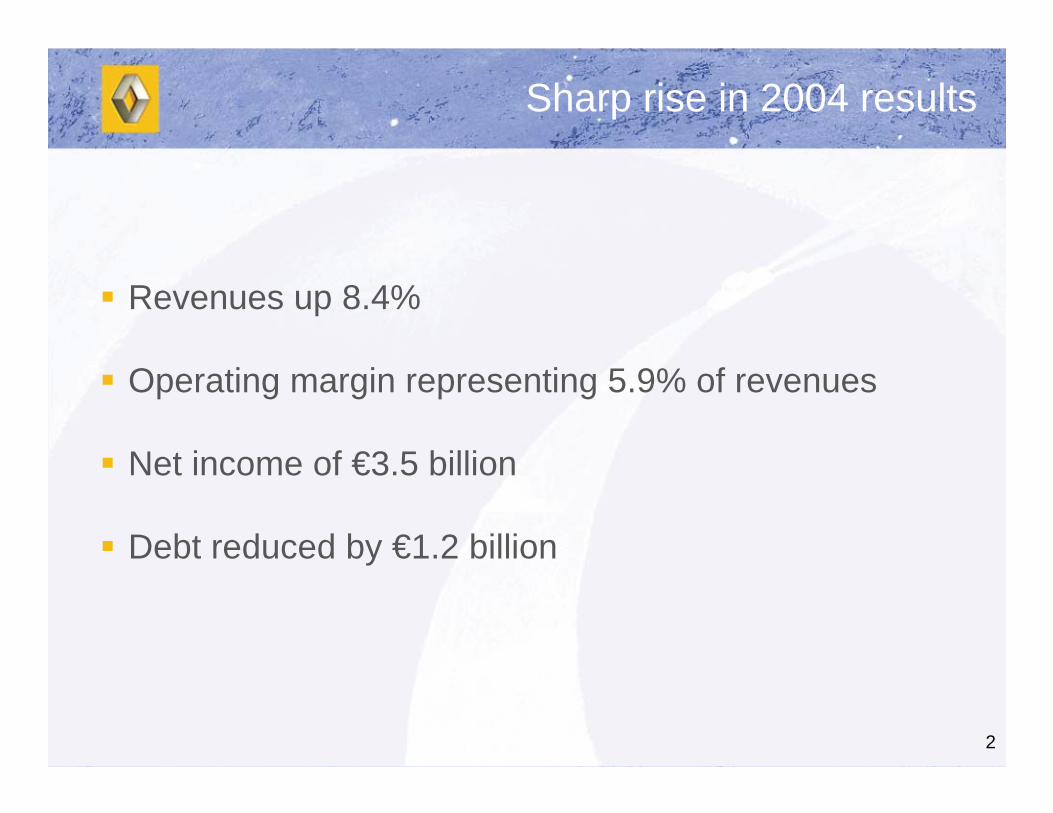

Sharp rise in 2004 results

! Revenues up 8.4%

! Operating margin representing 5.9% of revenues

! Net income of €3.5 billion

! Debt reduced by €1.2 billion

3

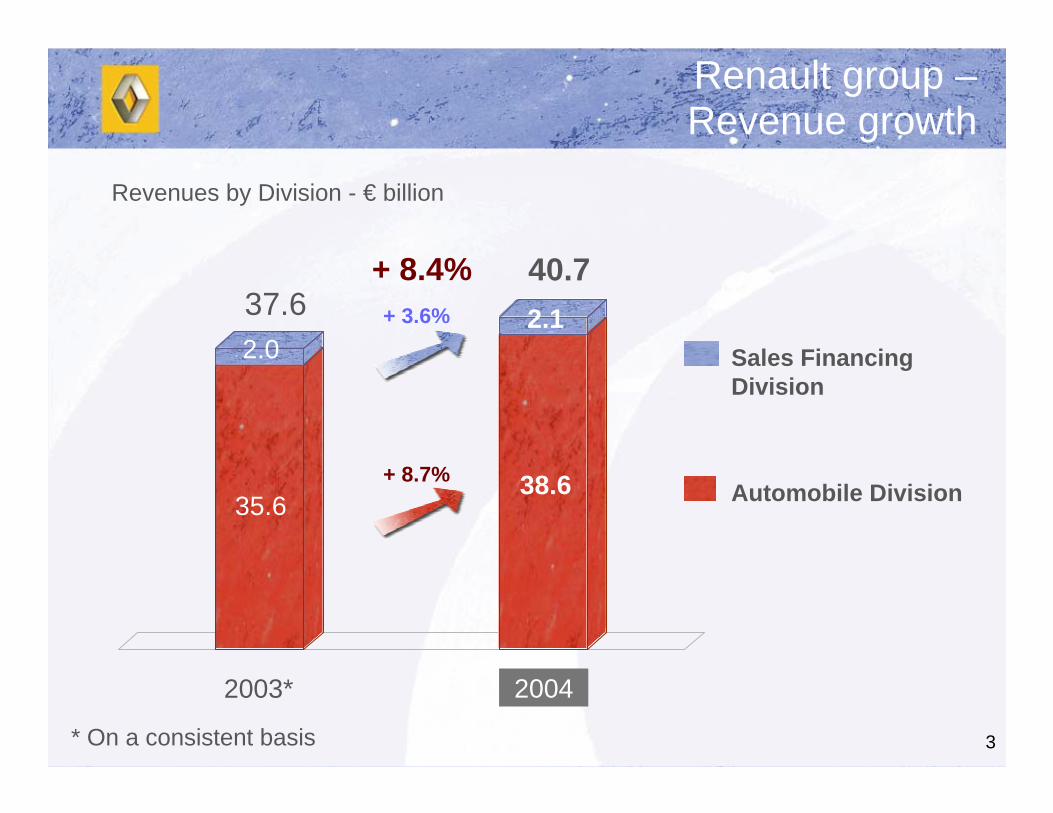

Renault group –Revenue growth

* On a consistent basis

35.6

2.02.1

Revenues by Division - € billion

37.640.7+ 8.4%

38.6

20042003*

Sales FinancingDivision

Automobile Division

+ 3.6%

+ 8.7%

4

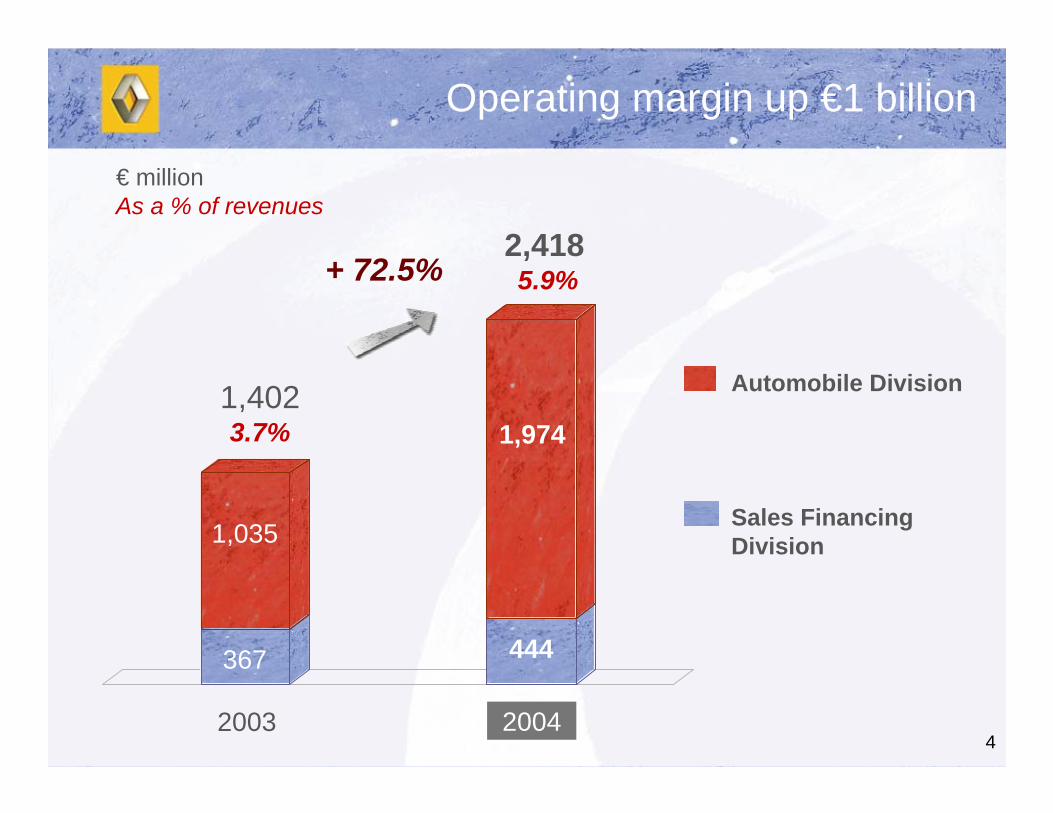

1,035

367

1,974

444

€ millionAs a % of revenues

Operating margin up €1 billion

Sales FinancingDivision

Automobile Division

20042003

+ 72.5%2,4185.9%

1,4023.7%

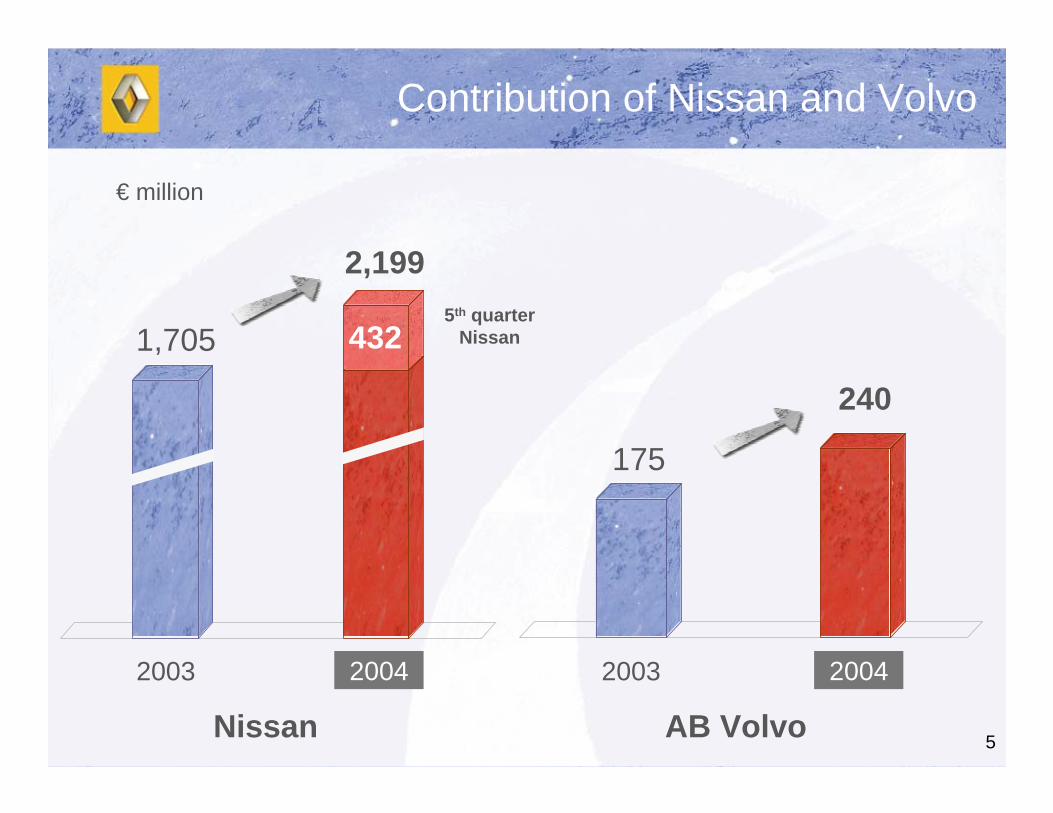

5

Contribution of Nissan and Volvo

1,705

2,199

175

240

Nissan AB Volvo

5th quarter Nissan432

2004200320042003

€ million

6

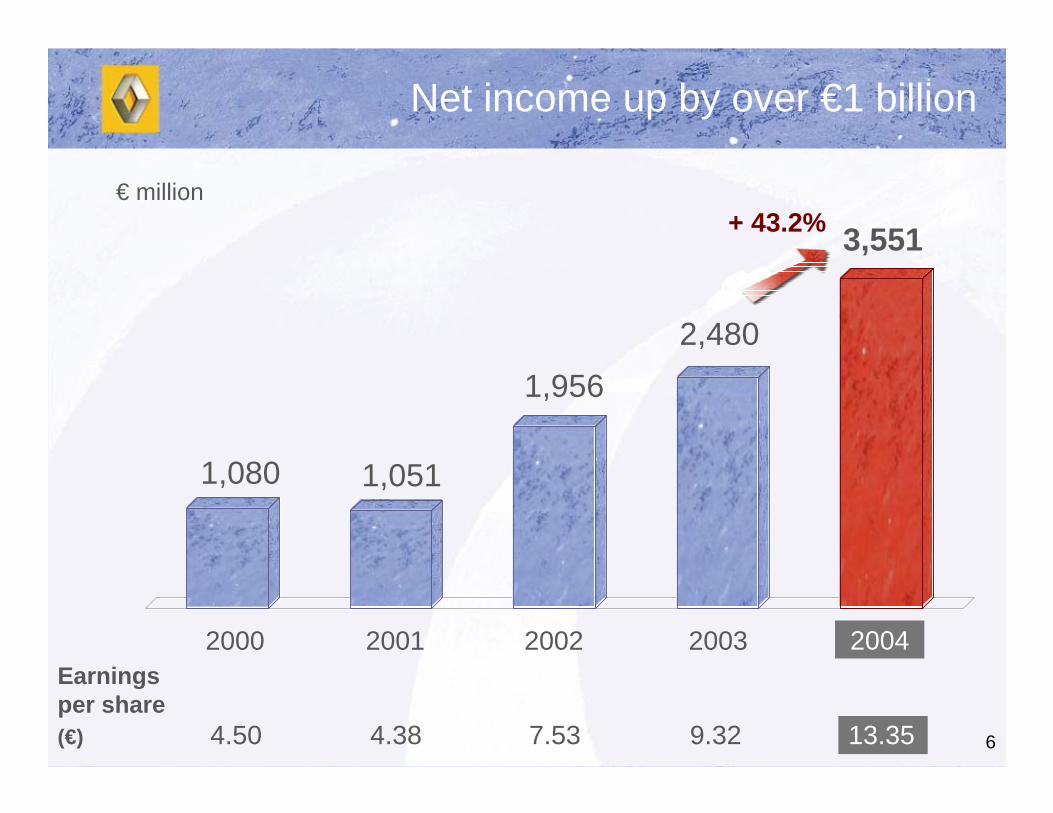

1,9562,480

1,080 1,051

Earningsper share(€) 4.50 4.38 7.53 9.32 13.35

+ 43.2% 3,551

Net income up by over €1 billion

20042003200220012000

€ million

7

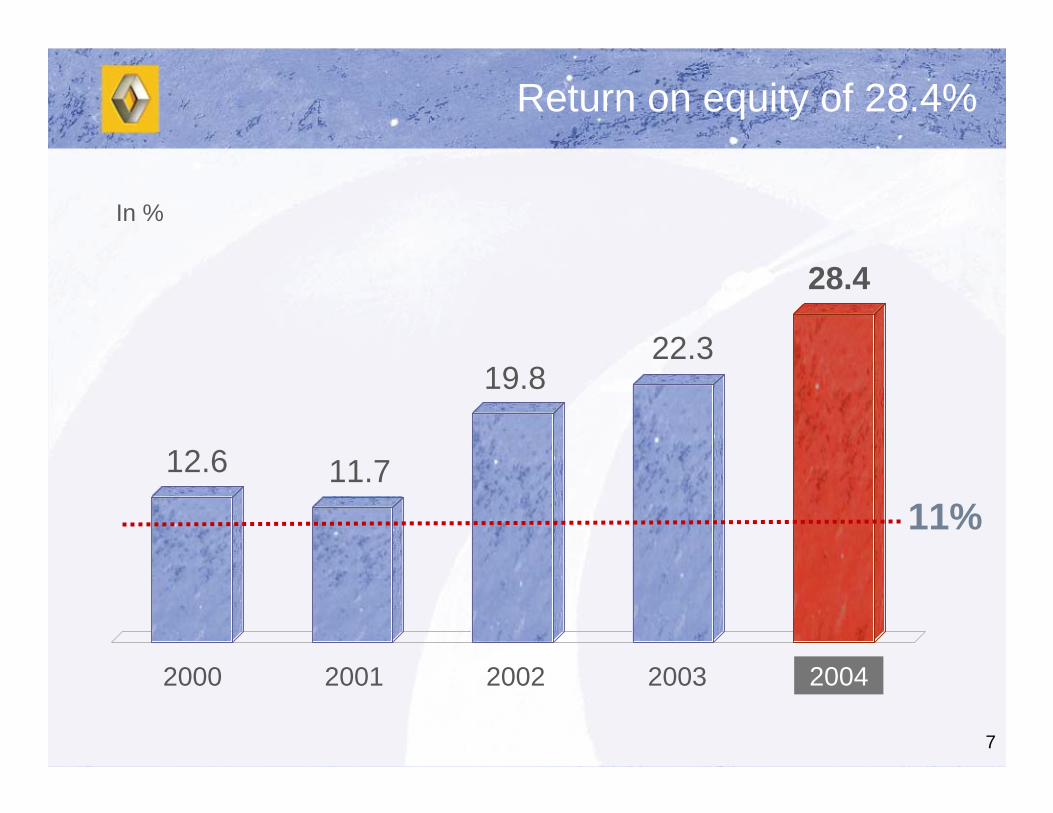

19.8

11.712.6

22.3

11%

28.4

Return on equity of 28.4%

In %

20042003200220012000

8

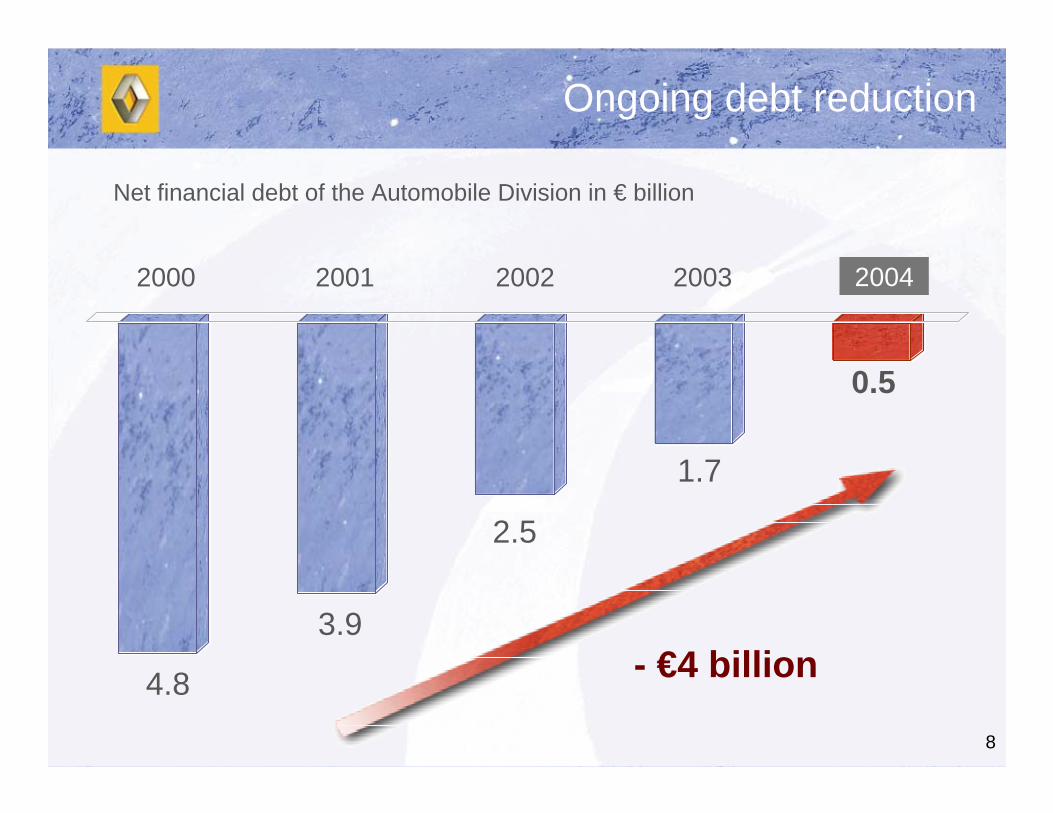

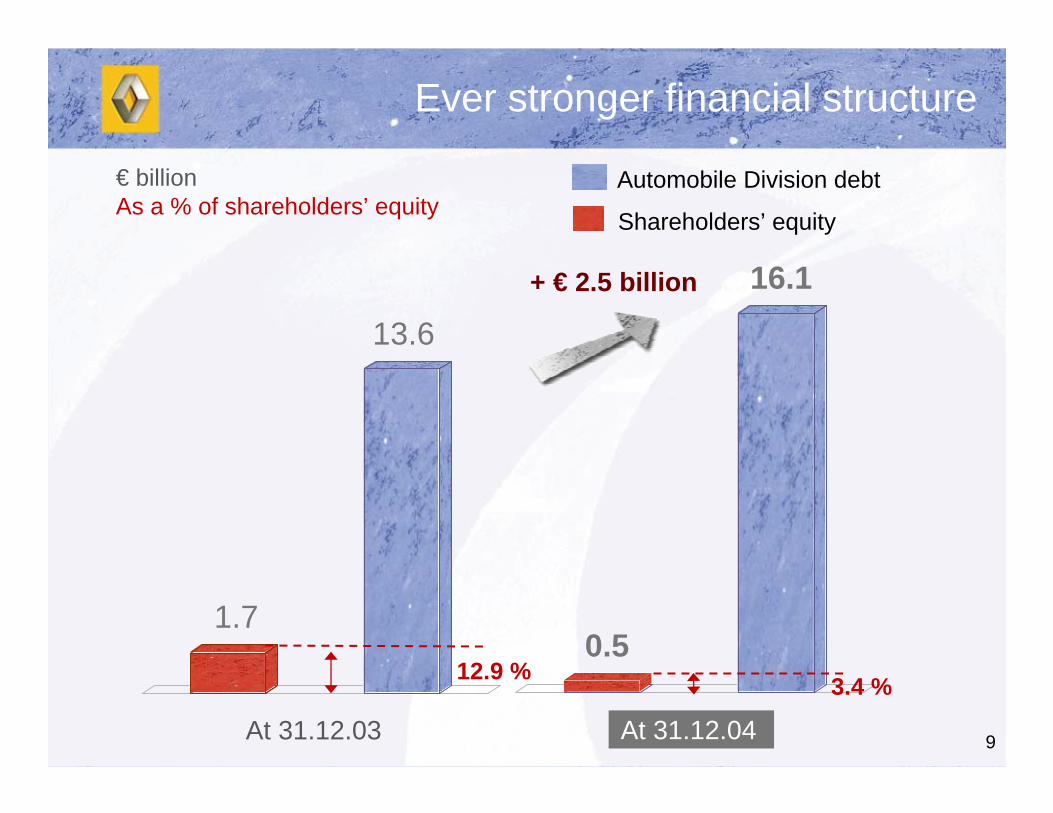

Net financial debt of the Automobile Division in € billion

2.5

1.7

4.8

0.5

Ongoing debt reduction

20042003200220012000

3.9- €4 billion

9At 31.12.03

13.6

16.1

1.70.5

12.9 %

Automobile Division debt

Shareholders’ equity

€ billionAs a % of shareholders’ equity

+ € 2.5 billion

Ever stronger financial structure

At 31.12.04

3.4 %

10

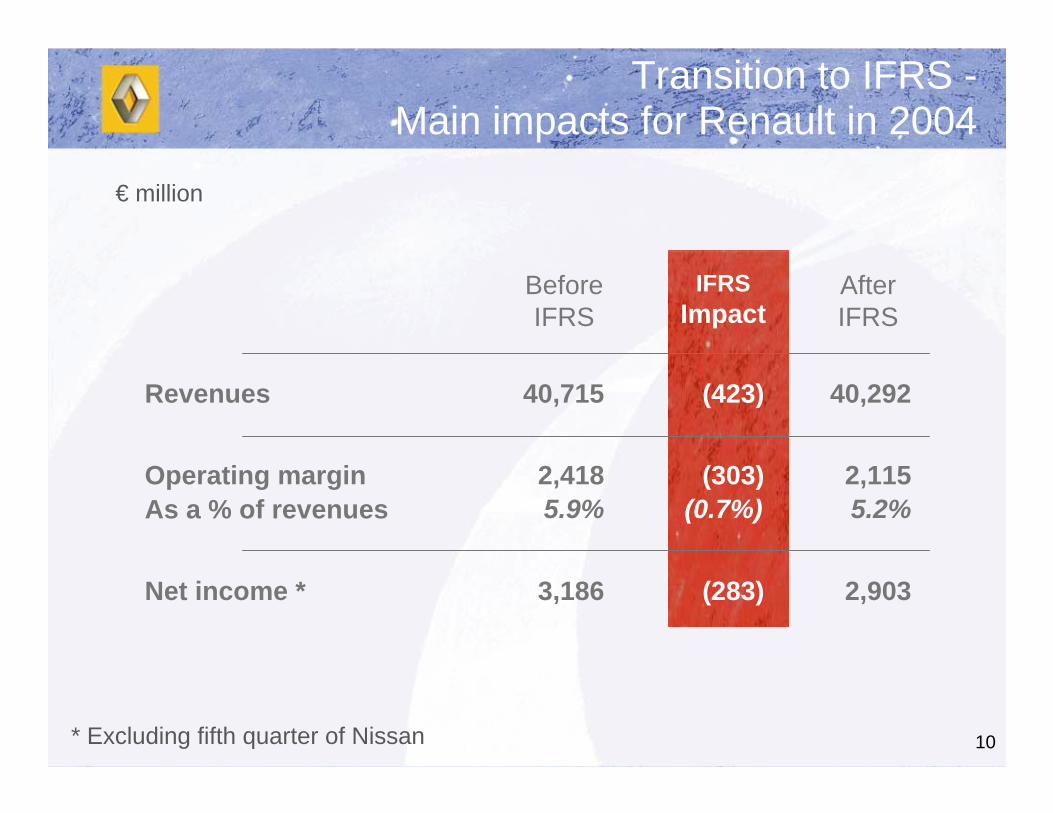

Transition to IFRS -Main impacts for Renault in 2004

IFRSImpact

BeforeIFRS

After IFRS

€ million

(423)40,715 40,292Revenues

(283)3,186 2,903Net income *

* Excluding fifth quarter of Nissan

5.2%5.9%As a % of revenues(303)2,418 2,115Operating margin

(0.7%)

11

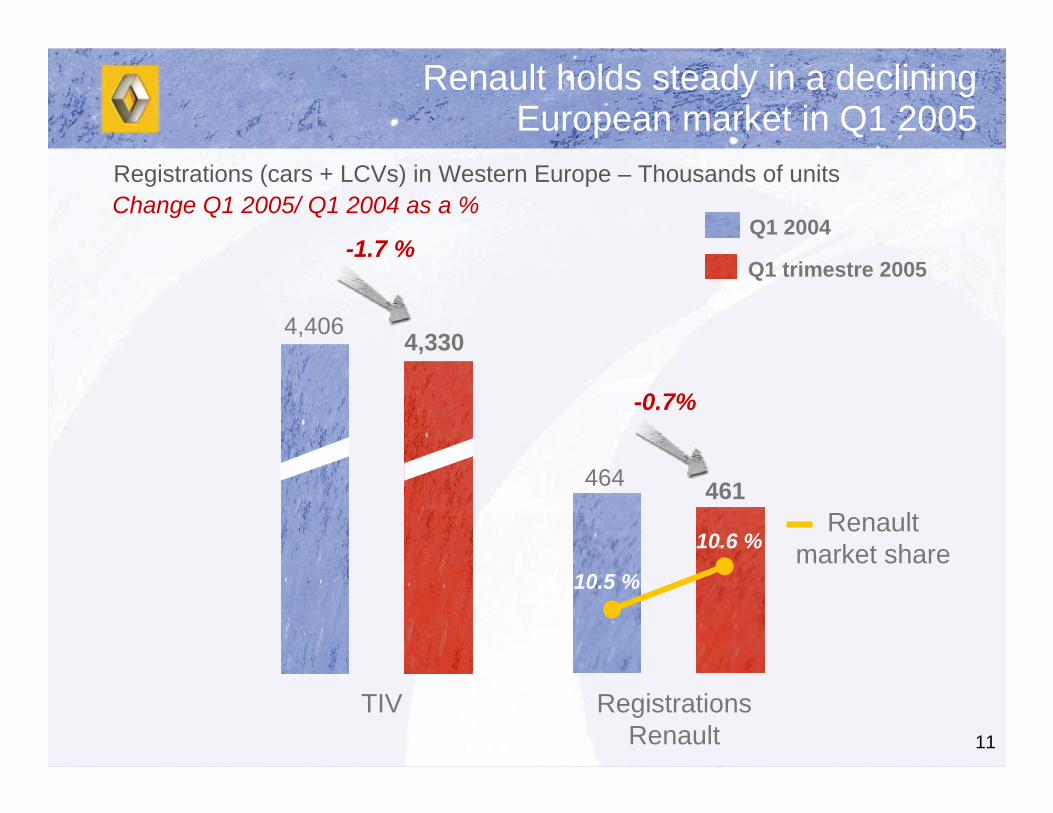

Registrations (cars + LCVs) in Western Europe – Thousands of units

Q1 2004

Q1 trimestre 2005

Change Q1 2005/ Q1 2004 as a %

Renault holds steady in a decliningEuropean market in Q1 2005

TIV

Renaultmarket share

RegistrationsRenault

-1.7 %

4,406 4,330

464 461

10.5 %

10.6 %

-0.7%

12

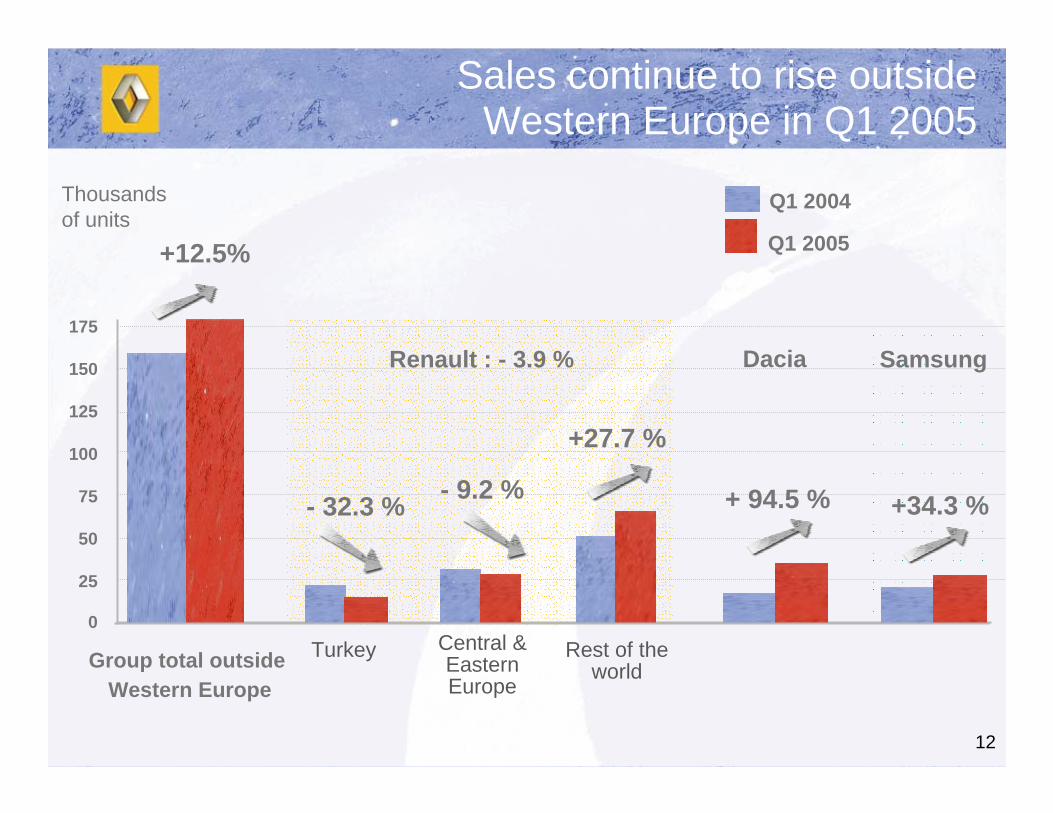

Thousandsof units

Sales continue to rise outsideWestern Europe in Q1 2005

Q1 2004

Q1 2005

+27.7 %

- 32.3 % + 94.5 % +34.3 %

Renault : - 3.9 % Dacia

100

75

50

25

125

150

175

- 9.2 %

0

+12.5%

Group total outsideWestern Europe

Rest of the world

Turkey Central & Eastern Europe

Samsung

13

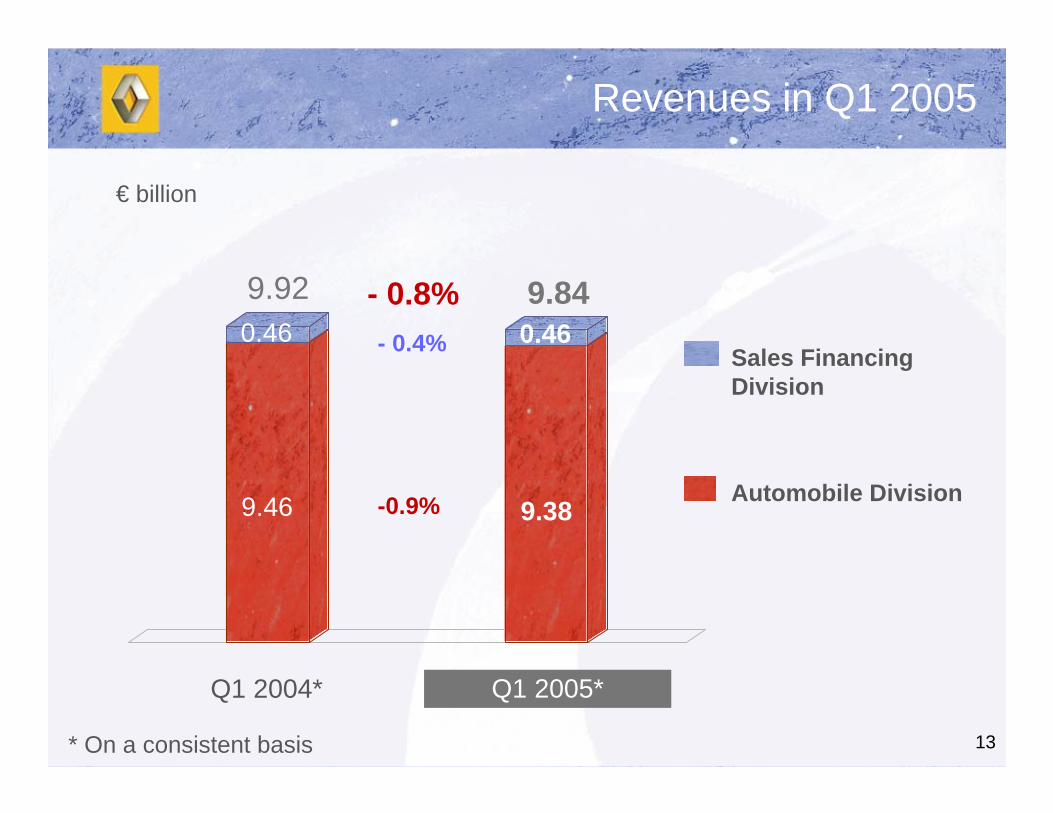

€ billion

* On a consistent basis

9.46

0.46 0.469.92 9.84- 0.8%

9.38

- 0.4%

-0.9%

Revenues in Q1 2005

Sales FinancingDivision

Automobile Division

Q1 2005*Q1 2004*

14

Automobile markets in 2005

! Stability in Western Europe

! International growth (except in Turkey)

15

Outlook for 2005

! Ongoing growth in worldwide sales

! Operating margin higher than 4% of revenues under IFRS

16

Profitable growth strategy

! Build recognition for our brand identity

! Be the most competitive manufacturer on our markets in terms of quality, costs and delivery times

! Extend our international reach

! Develop Renault’s core values

! Translate success into financial performance

Five strategic goals:

17

Electronics and safety

Airbags

18

A young, distinctive range

19

A young, distinctive range

20

A young, distinctive range

21

! Control development times and costs of projects

! Guarantee plant flexibility and productivity

! Rigorously control structural expenses

! Reduce purchasing costs, thanks to RNPO

Goal n°2:

Profitable growth strategy

Be the most competitive manufacturer on our markets in terms of quality, costs and delivery times thanks to the Alliance with Nissan

22

Renault Nissan Purchasing Organization

23

Profitable growth strategy

! Build recognition for our brand identity

! Be the most competitive manufacturer on our markets in terms of quality, costs and delivery times thanks to the Alliance with Nissan

! Extend our international reach

! Develop Renault’s core values

! Translate success into financial performance

Five strategic goals:

24

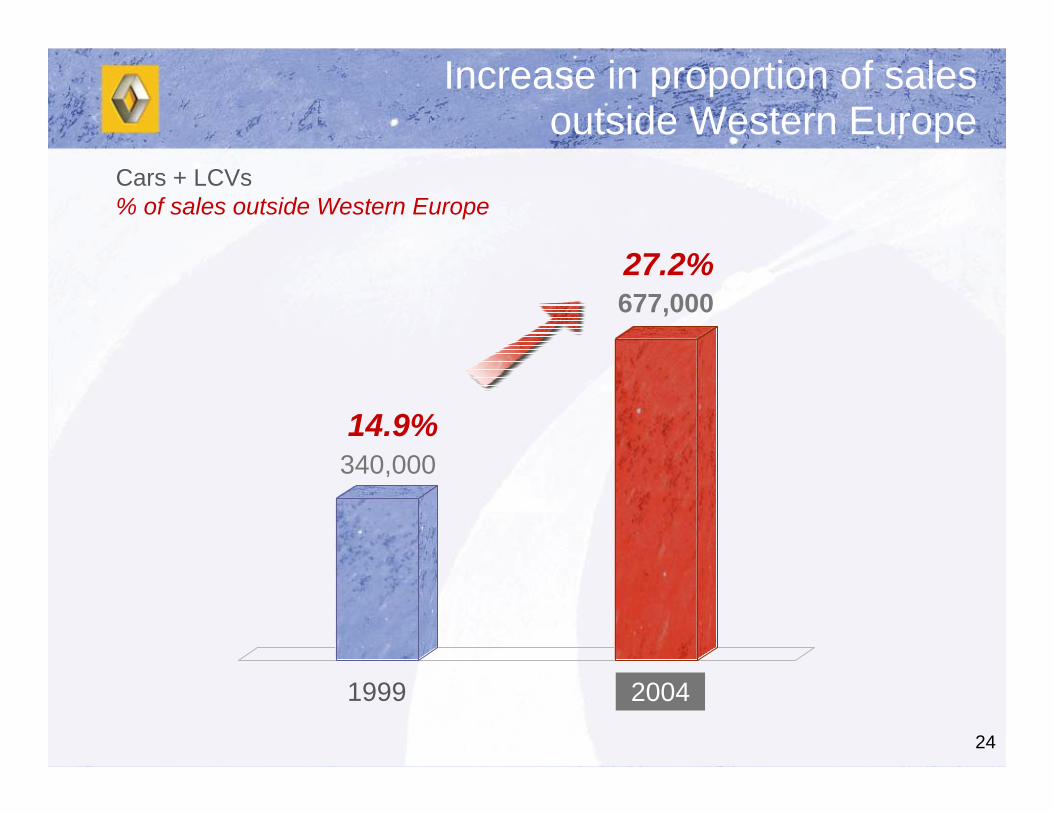

Increase in proportion of salesoutside Western Europe

20041999

Cars + LCVs % of sales outside Western Europe

14.9%

27.2%

340,000

677,000

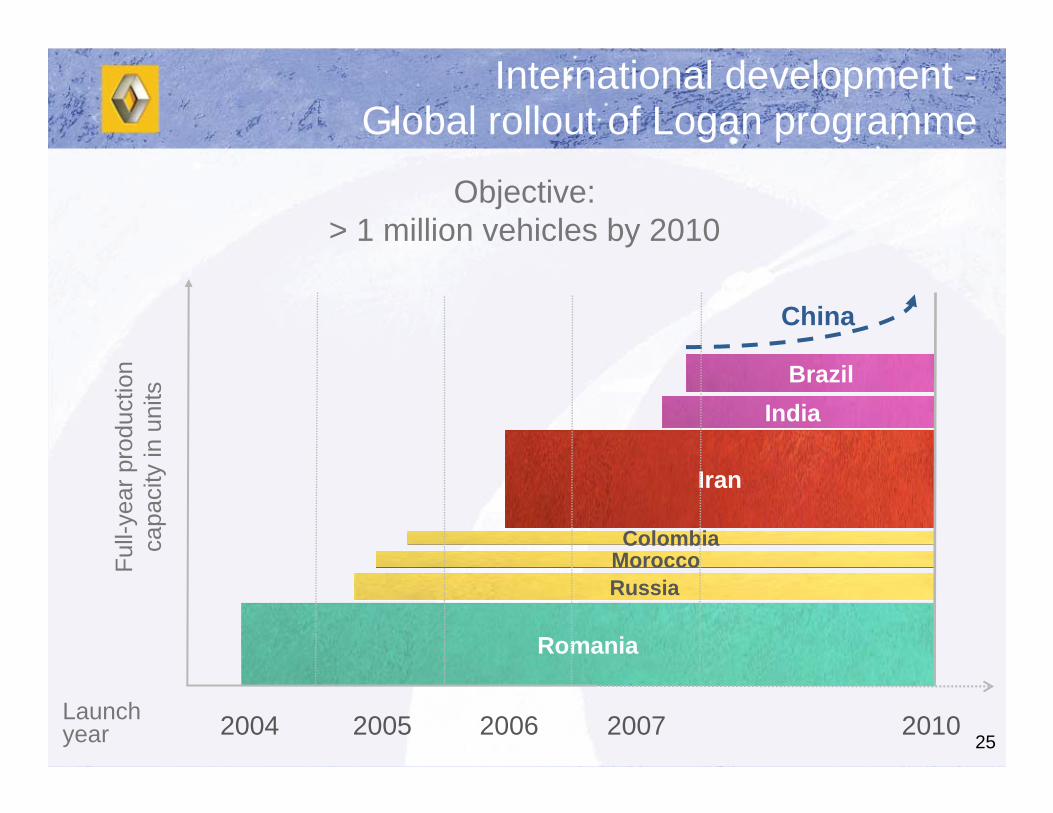

25

Objective:> 1 million vehicles by 2010

2004 2005 2006 2007 2010Launchyear

International development -Global rollout of Logan programme

Full-

year

pro

duct

ion

capa

city

in u

nits

Romania

Russia

Iran

India

Morocco

Brazil

China

Colombia

26

International development -Signing of an agreement in India

27

Renault’s core values –Training

28

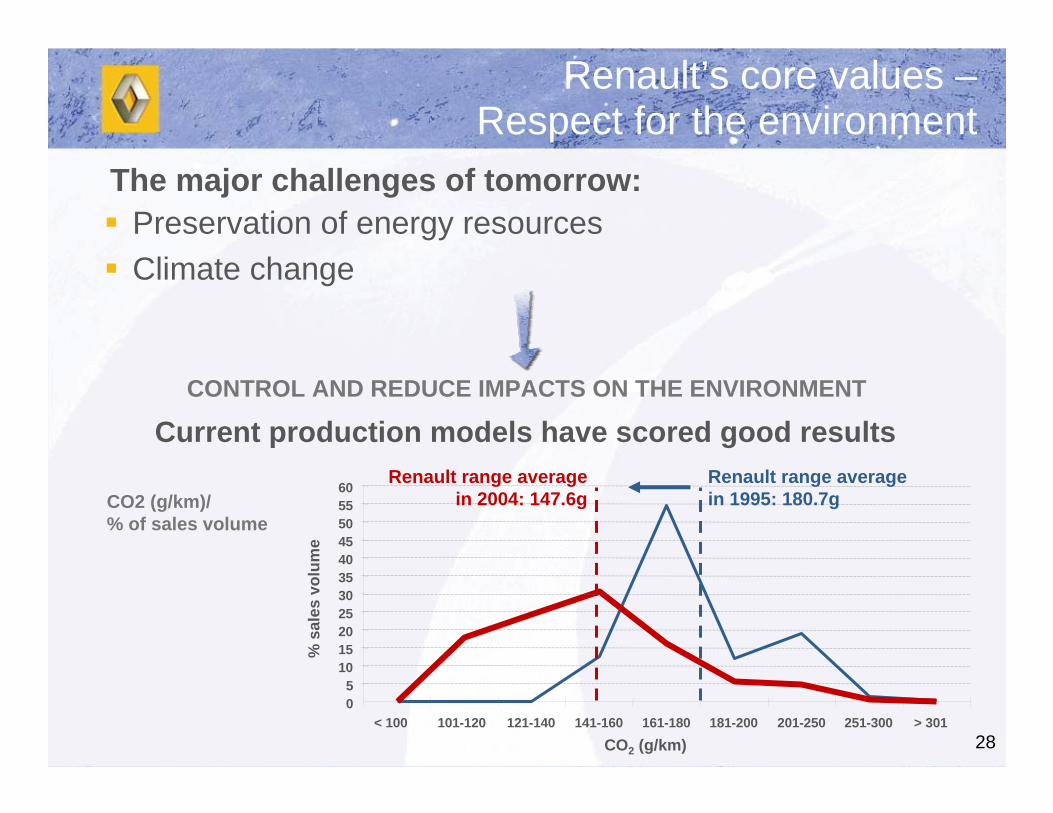

CONTROL AND REDUCE IMPACTS ON THE ENVIRONMENT

Current production models have scored good results

The major challenges of tomorrow:

Renault’s core values –Respect for the environment

! Preservation of energy resources! Climate change

CO2 (g/km)/% of sales volume

% s

ales

vol

ume

CO2 (g/km)

05

1015202530354045505560

< 100 101-120 121-140 141-160 161-180 181-200 201-250 251-300 > 301

Renault range averagein 2004: 147.6g

Renault range averagein 1995: 180.7g

29

Appointments and Remuneration Committee2004

2005

Accounts and Audit Committee

International StrategyCommittee

Remuneration Committee

Appointments and

Governance Committee

Reinforcement of corporategovernance principles

! Specialist committees at Renault

! In-depth evaluation of the composition, organization and operation of the Board of Directors

Accounts and Audit Committee

International StrategyCommittee

30

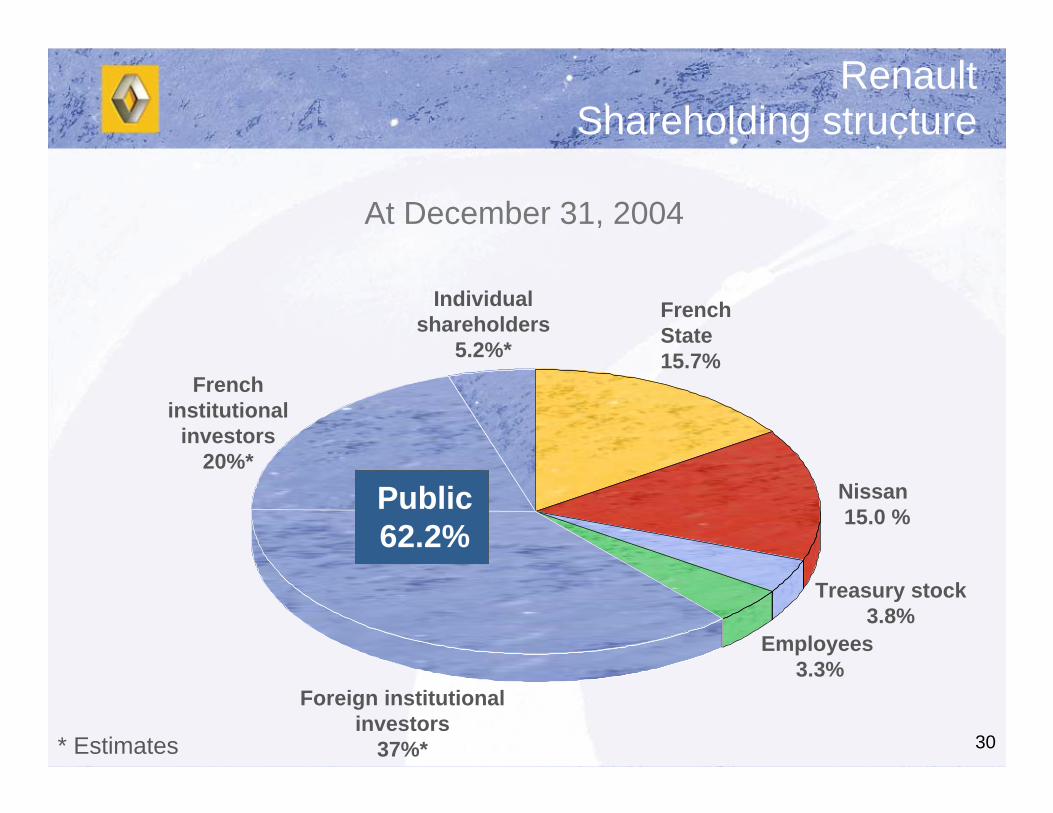

At December 31, 2004

* Estimates

Renault Shareholding structure

Nissan15.0 %

French State 15.7%

Treasury stock 3.8%

Employees 3.3%

Foreign institutional investors

37%*

French institutional

investors20%*

Individual shareholders

5.2%*

Public 62.2%

31

0.921.15

1.40

+ 95.7% 1.80

Dividend doubled in three years

2004200320022001

Net dividend per share in €

+ 28.6%

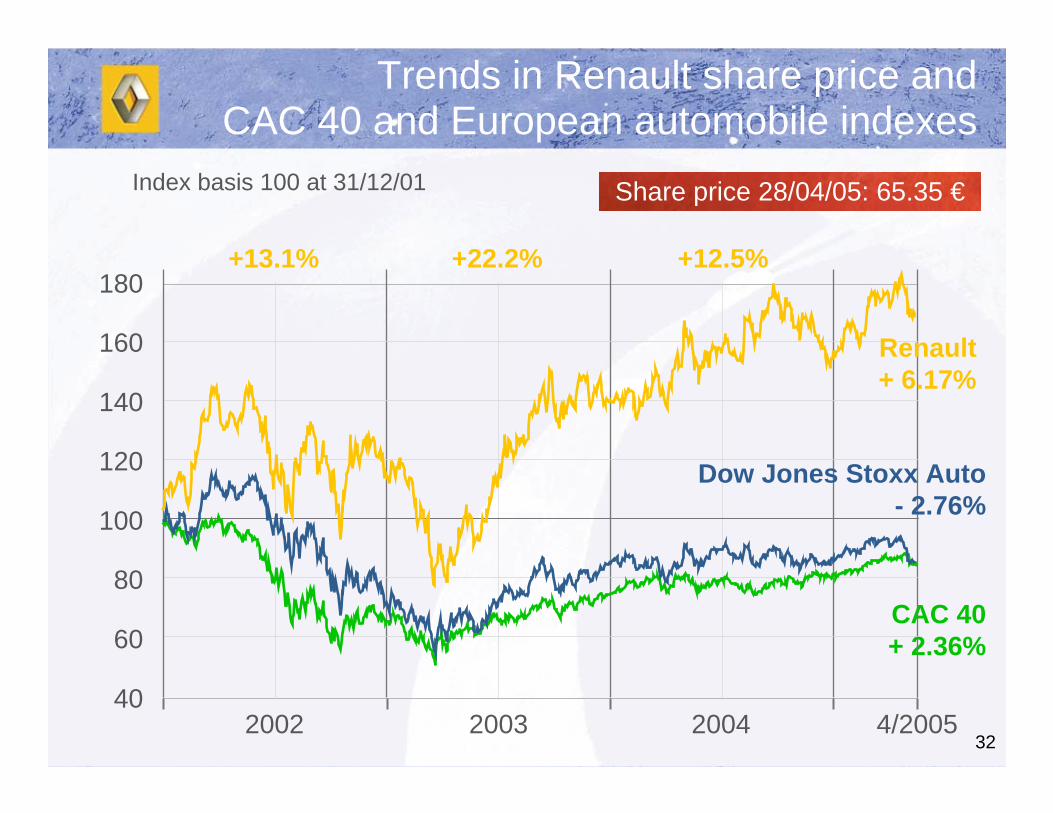

32

Trends in Renault share price and CAC 40 and European automobile indexes

Index basis 100 at 31/12/01 Share price 28/04/05: 65.35 €

+22.2% +12.5%+13.1%

CAC 40+ 2.36%

402002 4/20052003 2004

60

80

100

120

140

160

180

Dow Jones Stoxx Auto - 2.76%

Renault+ 6.17%

33

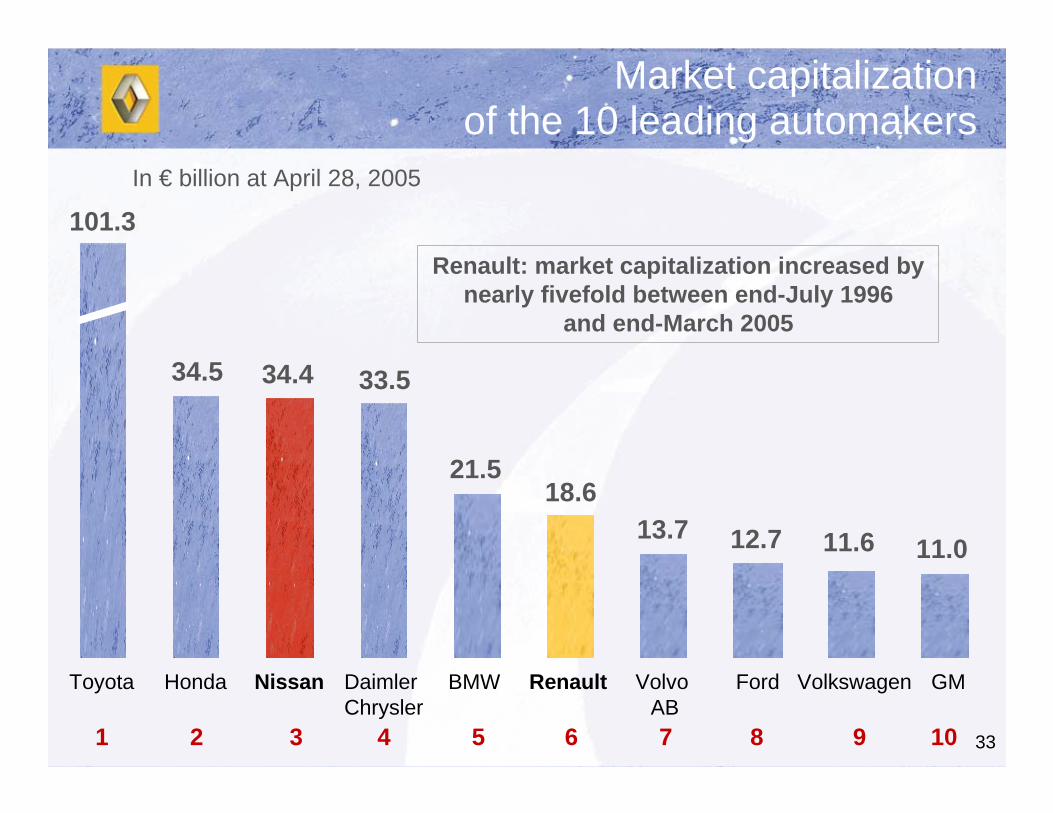

Market capitalization of the 10 leading automakers

In € billion at April 28, 2005

Renault: market capitalization increased by nearly fivefold between end-July 1996

and end-March 2005

Toyota BMWNissan Daimler Chrysler

Honda VolkswagenVolvo AB

FordRenault GM

1 2 3 4 5 6 7 8 9 10

101.3

13.718.6

21.5

33.534.434.5

12.7 11.6 11.0

34

! Performance

! Brand identity

! Efficient international development

Strategic continuity

35

Performance

We owe it to our shareholders,

our customers,

our employees,

our partners,

and society at large.

36

Brand identity

! Irreproachable safety! Product and service quality! State-of-the-art technology! Cost competitiveness

! Design personality! Perceived quality! Driving pleasure! Customer treatment

37

Efficient international development

Develop our presence and succeedin growth markets

38

Three requirements

! Commitment to objectives

! Transparency in operations

! Accountability for results

39

Nissan business plans

! Nissan Revival Plan (2000-2001)

! NISSAN 180 (2002-2004)

! NISSAN Value-Up (2005-2007)

40

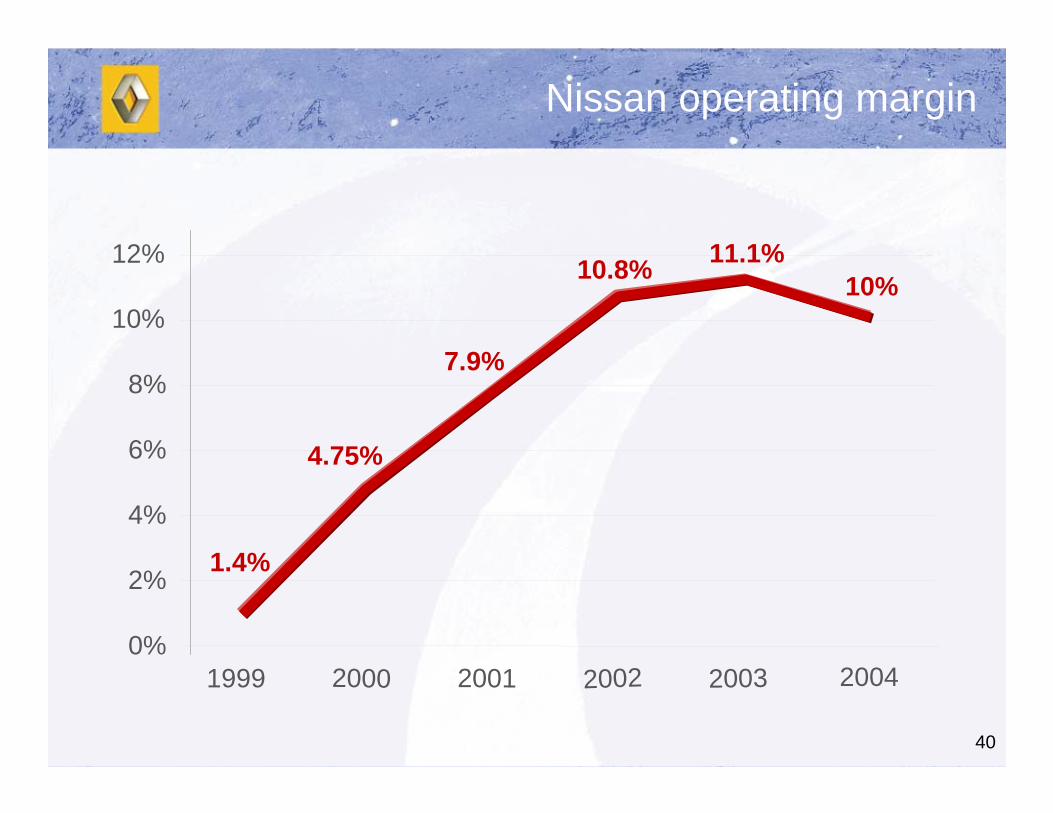

Nissan operating margin

1.4%

4.75%

7.9%

10.8% 11.1%10%

0%

2%

4%

6%

8%

10%

12%

1999 2000 2001 2002 2003 2004

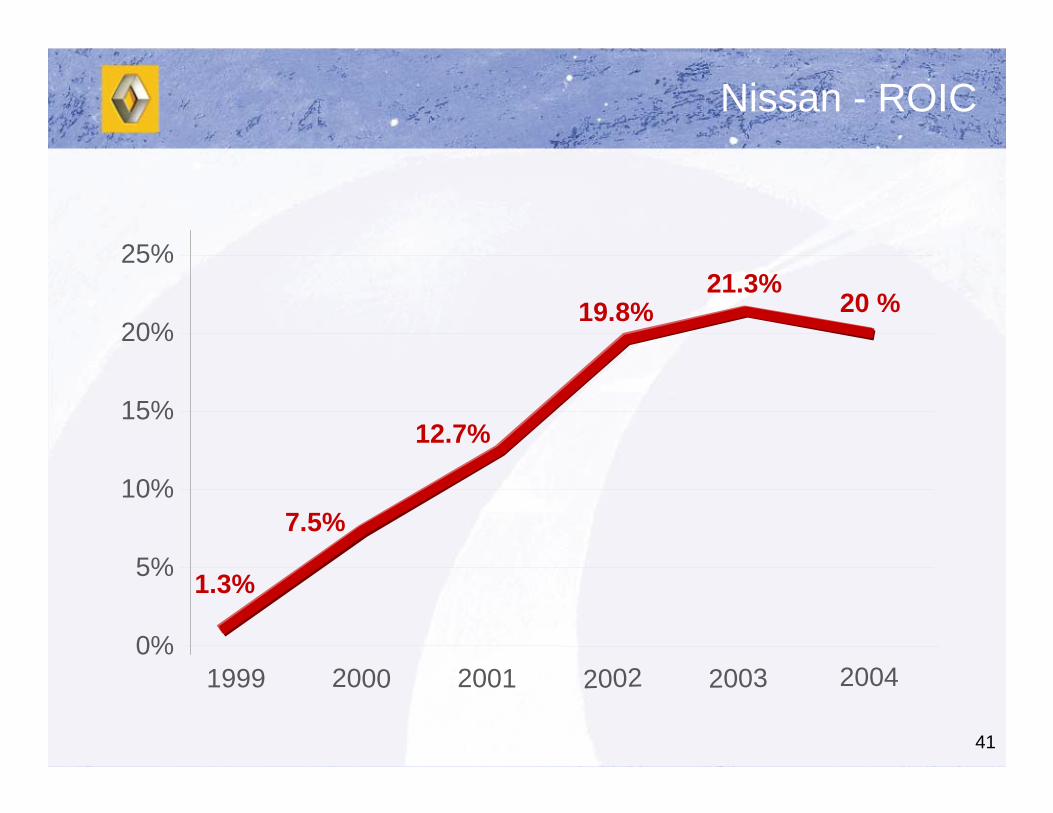

41

Nissan - ROIC

0%

5%

10%

15%

20%

25%

1999 2000 2001 2002 2003 2004

1.3%

12.7%

7.5%

19.8%21.3%

20 %

42

The Alliance

43

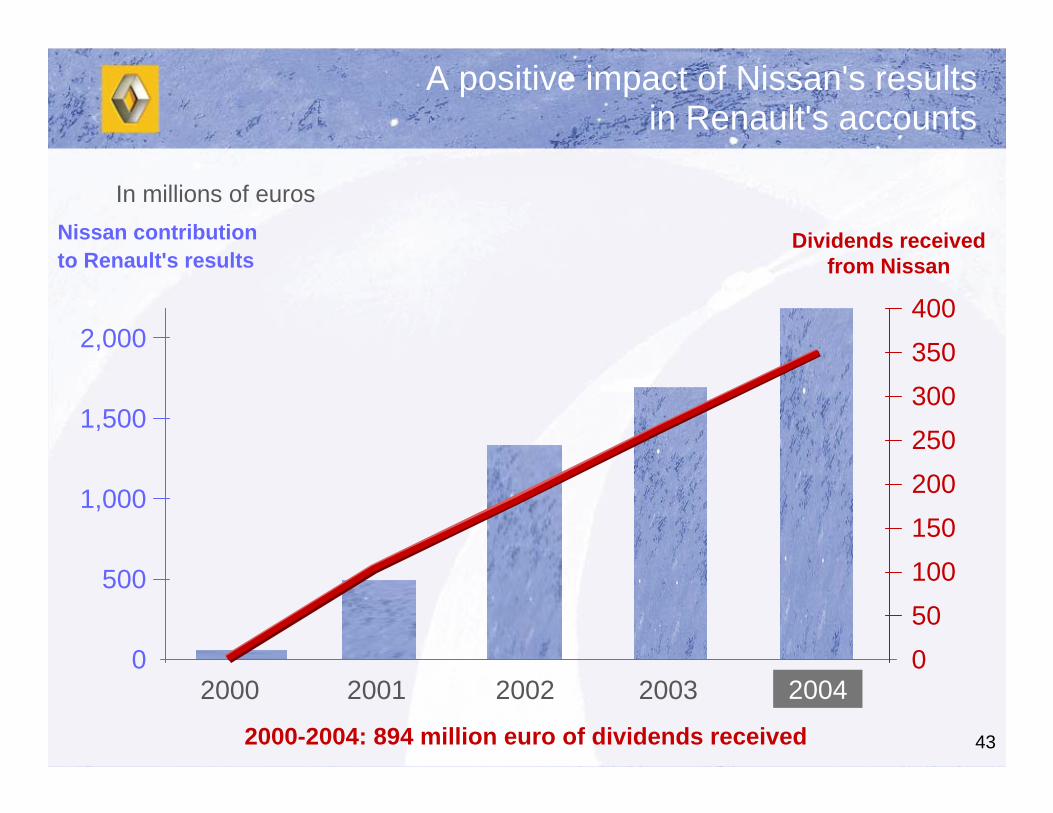

A positive impact of Nissan's resultsin Renault's accounts

Dividends receivedfrom Nissan

Nissan contributionto Renault's results

2000-2004: 894 million euro of dividends received

20042003200220012000

500

100150200250300350400

0

500

1,000

1,500

2,000

In millions of euros

44

The principles of the Alliance

! Develop synergies to boost the performance of Renault and Nissan

! A partnership based on respect for the identity and culture of each company

45

Alliance Vision - Destination

Rank among the world’s top three automotive groups in terms of:

! Quality

! Technology

! Operating profit