Embed Size (px)

Citation preview

mKETs-Pilot lines project The goal of the mKETs-PL project is to prepare and foster

a common understanding and consensus for future actions in Europe focusing on multi-KETs pilot lines

All rights reserved © 2013, mKETs-PL consortium

mKETs-PL working document

Country report Netherlands Date: 09/07/2013 Authors: Govert Gijsbers, Marcel de Heide, Danny Kappen and Frans van der Zee Number of pages: 23 Number of Annexes: 1

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 2 of 23 © 2013

No part of this publication may be reproduced and/or published by print, photo print, microfilm or any other means without the previous written consent of the mKETs-PL consortium. Submitting the report for inspection to parties who have a direct interest is permitted. © mKPL The project partners of the mKETs-PL consortium are:

Netherlands organisation for Applied Scientific Research TNO

Fraunhofer-Gesellschaft

Commissariat à l'énergie atomique et aux énergies alternatives (CEA)

Cambridge University-Cambridge enterprise

VTT

Tecnalia

Technology Partners Foundation

Joanneum Research Austria

D’Appolonia S.p.A

Strauss & Partners

Spark

Noblestreet

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 3 of 23 © 2013

Content 1. Policy perspective ........................................................................................................................................... 4

1.1. Country specific innovation system with emphasis on KETs ................................................................. 4 1.2. Organisation of mKETs policy............................................................................................................... 10 1.3. Main policies for Pilot lines .................................................................................................................. 11

2. Business perspective..................................................................................................................................... 12 2.1. Implementation of multi-KETs pilot lines ............................................................................................ 12 2.2 Evaluation of KET policies .................................................................................................................... 16

3. Conclusions ................................................................................................................................................... 19 3.1. Summary of policy perspective ............................................................................................................ 19 3.2. Summary of business perspective ....................................................................................................... 19 3.3. Recommendations to support pilot lines ............................................................................................. 20

4. References .................................................................................................................................................... 21 4.1. Literature ............................................................................................................................................. 21 4.2. Interviews ............................................................................................................................................ 21

5. Annex: list of pilot lines ................................................................................................................................ 22

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 4 of 23 © 2013

1. Policy perspective This chapter describes the policy initiatives implemented by the Dutch government addressing Key enabling Technologies. The main actors of the Dutch Innovation System (DIS) involved in KETs are describes as well as the policy and corresponding instruments supporting them.

1.1. Country specific innovation system with emphasis on KETs The main stakeholders involved in the process of design and definition of R&D and innovation policies are the Parliament, the Cabinet and the Ministries. There are different coordination mechanisms at this level

A dedicated Cabinet councils called the Economic Affairs, Infrastructure and the Environment Subcommittee (REZIM). It is concerned with issues related to the economy, science and research policy, higher education and innovation, and consists of the ministers most closely involved with these matters.

Its counterpart at ministry level is called the Economic Affairs, Infrastructure and the Environment (CEZIM).

For consultations between Parliament and the Cabinet, the Lower House has a Committee for Education, Culture and Science, while the Upper House has a Committee for Education, Culture and Science Policy. On both levels there is an Economic Committee addressing Innovation.

The most prominent ministries involved in policy design and delivery (as reflected in budget to be allocated) are the Ministry of Education, Culture and Science (OCW) and the Ministry of Economic Affairs (EZ).

The Ministry of Education, Culture and Science has broad political-administrative and financial responsibility for public-sector research in the Netherlands. Most of its budget is in the form of institutional or basic funding. The Ministry finances part of the budget of the major research organisations in the Netherlands and abroad, coordinates the science policy of the national government and contributes to the international science policy (of the EU).

The Ministry of Economic Affairs (EZ) is responsible for facilitating a competitive business climate. As stated as their mission: “The Ministry promotes the Netherlands as a country of enterprise with a strong international competitive position and an eye for sustainability. It is committed to creating an excellent entrepreneurial business climate, by creating the right conditions and giving entrepreneurs room to innovate and grow. By paying attention to nature and the living environment. By encouraging cooperation between Research Institutes and businesses. […]” Intervention by EZ primarily addresses industry-oriented R&D and Innovation.

The process of R&D and Innovation policy formulation in the Netherlands includes consultation of the main actors in the innovation system throughout almost all the phases of the policy cycle (e.g. ,on policy formulation, implementation and evaluation. The involvement of the actors in the innovation system has become more explicit in recent years. But also other Advisory bodies play an important role in the process of research and innovation policy formulation:

The Advisory Council for Science and Technology Policy (AWT) is an independent advisory body that gives solicited and unsolicited advice to government and parliament on science, technology and innovation policy, and on information policy in the fields of science and technology. The twelve members of AWT have various backgrounds (university, industry etc.) and take seat in the Council on the basis of their personal merits.

The Royal Netherlands Academy of Arts and Sciences (KNAW) provides advice to the government on matters of science and technology, especially in the field of basic research.

The Higher Education institutes in the Netherlands play an important role in the innovation system, by providing education and training, and (collaborative) knowledge creation and dissemination. They can be

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 5 of 23 © 2013

clustered in different groups, based on specific tasks within the innovation system, and type of research covered:

1

There are thirteen publicly funded research universities. 2

Their tasks include: providing initial programmes of scientific education; carrying out scientific research (which in practice is focused primarily, but not exclusively, on basic research); training of scientific researchers or technological designers; and disseminating knowledge to society as a whole. These universities are organised in the association of universities in the Netherlands (VSNU).

There are also eight University Medical Centres (UMCs). The core tasks of the UMCs are besides research and innovation, and teaching and training, also treating patients.

An important part of the basic research carried out in the Netherlands by the public research infrastructure is conducted by Research Institutes linked to intermediary organisations involved also in policy delivery. The Royal Netherlands Academy of Arts and Sciences acts as an umbrella organisation for 18 so-called KNAW Institutes.

3 Similarly, the Netherlands Organisation for Scientific Research acts as an umbrella organisation for

nine so-called NWO Institutes.4 These institutes cover specific and strategic research fields, which address also

KETs. Furthermore, there are four Large Technological Institutes (Grote Technologische Instituten (GTIs)) conducting applied research and related activities, such as advising industry and government in specific fields.

5 These

institutes are active in aerospace, water management, hydraulic engineering, maritime research and energy research, and subsequently address KETs.

1 Included are also 41 universities of applied sciences (so-called Hogescholen). These knowledge institutes have

strong traditional relations between education, professional practice and knowledge. The knowledge function of the universities of applied sciences creates a bridge between the educational and professional practice. This function translates new insights and questions from the professional practice to education (the training of the new professionals) and the dissemination of knowledge to this practice. It has the objective to increase the innovativeness of this practice. Research plays an important role. The research function of the universities of applied sciences is anchored in the law on these universities. 2 These include three Universities of Technology (TUs, focussing on S&T / engineering) and one agricultural

university (LU, mainly dedicated to science and technology of food production). Note that there is also a publically funded ‘Open University’, providing initial programmes of scientific education by means of distant learning tools. 3 The KNAW Institutes are: Data Archiving and Networked Services (DANS); Fryske Akademy (FA); Huygens ING;

Internationaal Instituut voor Sociale Geschiedenis (IISG); Koninklijk Instituut voor Taal-, Land- en Volkenkunde (KITLV); Meertens Instituut; NIOD Instituut voor Oorlogs-, Holocaust- en Genocidestudies; Nederlands Interdisciplinair Demografisch Instituut (NIDI); Netherlands Institute for Advanced Study in the Humanities and Social Sciences (NIAS); Centraalbureau voor Schimmelcultures (CBS); Hubrecht Instituut voor Ontwikkelingsbiologie en Stamcelonderzoek; ICIN Netherlands Heart Institute (ICIN); Nederlands Herseninstituut; Nederlands Instituut voor Ecologie (NIOO); Spinoza Centre for Neuroimaging; Rathenau Instituut; Waddenacademie (NIAS). See www.knaw.nl/Pages/DEF/27/128.bGFuZz1FTkc.html.. 4 The NWO Institutes are: Institute for Astronomical Research in the Netherlands (ASTRON); The National

Research Institute for Mathematics and Computer Science (CWI); FOM-Institute for Atomic and Molecular Physics (AMOLF); FOM-Institute for Plasma Physics 'Rijnhuizen' ; The National Institute for Nuclear Physics and High Energy Physics (NIKHEF); Royal Netherlands Institute for Sea Research (NIOZ); Netherlands Institute for the Study of Crime and Law Enforcement (NSCR); Space Research Organisation Netherlands (SRON). See www.nwo.nl/en/about-nwo/organisation/nwo-divisions. 5 The Large Technological Institutes are: (1) ECN, which performs research on nuclear and other forms of

energy; (2) MARIN, involved in research into shipbuilding, offshore technology and oceanography; (3) NLR, engaged in aerospace activities; (4) Deltares resulting from a merge in January 2008 from Geodelft, WL | Delft Hydraulics with parts of TNO Construction and Subsurface and parts of Rijkswaterstaat, resulting in a new and independent institute for applied research and expert advice on water and the subsurface.

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 6 of 23 © 2013

TNO, the Netherlands Organisation for Applied Research, is an independent private non-profit research organisation established by law in 1930, with some 3800 employees.

6 TNO is an umbrella organisation with

several research centres clustered in seven “themes”: (1) Industrial innovation; (2) Healthy living; (3) Energy; (4) Mobility; (5) Built environment; (6) Information society; (7) Defence, Safety and Security. It’s mission is “[…] to connect people and knowledge, in order to innovate with impact.”

7

Other relevant actors in the knowledge infrastructure are for example the agricultural Research Institutes of the DLO Foundation (part of the Wageningen University and Research Centre WUR), which are involved with for example Industrial Biotechnology. The Dutch Innovation system is governed by two dedicated policies addressing R&D and Innovation, described in the corresponding policy documents Quality in diversity - Strategic Agenda for Higher Education, Research, and Science and To the Top - Towards a new enterprise policy. Different ministries play a role in implementing these policies, by means of different instruments and with the help of specific actors in the innovation system. In February 2011 the white paper on industry policy entitled To the Top - Towards a new enterprise policy was presented, which “[…] sets out the key objectives of the government’s new business policy, giving entrepreneurs more scope for their business activities and enabling them to grow. It will allow them to stand out on the world market, profit from growing world trade, exploit opportunities for growth in emerging markets, achieve sustainable economic growth and choose to become top sectors.”

8

Industry-oriented R&D and innovation is part of this enterprise policy, as an integral strategy for innovation driven economic growth. The policy document “[…] explains how, together with businesses and scientists, we can help the Dutch sectors to maintain or achieve a leading position in the world. It is essential that our entrepreneurs are given more scope to do what they do best: business.” The new enterprise policy devotes special attention to nine Top-Sectors of the Dutch economy: High Tech Systems and Materials, Energy, Creative Industry, Logistics, Agro & Food, Horticulture and Propagating Stock, Life Sciences & Health, Water and Chemistry. Head Offices has been added to this as a focal point because it is important that the Netherlands further develop its position as an appealing location for international companies to set up head offices. The selection of the nine sectors was determined by four factors. These are sectors that (1) are knowledge-intensive, (2) export-oriented, (3) usually with (sector-) specific legislation and regulation and that (4) (can) make an important contribution to solving societal issues:

For sectors with a high degree of knowledge intensity, a good, structural connection between publicly funded knowledge institutes and privately financed industrial research is vital. This ensures that areas with the highest economic return become research priorities. Good interaction between companies and educational institutes also reinforces the alignment of education with the labour market.

For internationally-oriented sectors, markets in emerging countries provide great opportunities. These are markets where (foreign) governments have a great deal of influence and which require the targeted use of economic missions and diplomacy to capitalise on international opportunities.

9

Sector-specific legislation and regulation can be decisive for a sector's competitiveness. For example, take network regulation in the case of (sustainable) energy, legislation relating to food security and animal welfare in the case of the agro & food sector, rules surrounding payment for medicines and medical-ethical testing in the case of the life sciences & health sector and the conditions for entering foreign markets (water).

Societal issues such as climate change and scarcity (of water, food, energy), ageing (high tech, life sciences & health) provide opportunities for the Dutch business sector. At the same time, the government bears its own responsibility in these issues because public interests are at stake. There is a great deal of attention in the top sectors to linking

6 See http://www.tno.nl/.

7 PNP is included in GOVERD for the Netherlands.

8 See www.government.nl/documents-and-publications/parliamentary-documents/2011/02/04/to-the-top-

towards-a-new-enterprise-policy.html. 9 See S. Moons and P. van Bergeijk (2011) ´De effectiviteit van economische diplomatie´ [The effectiveness of

economic diplomacy] ESB 96(4616).

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 7 of 23 © 2013

economic opportunities and societal challenges in the form of public-private partnerships. The government, knowledge institutes and business sector are increasingly acting as partners in this.

Box 1: Industry Policy 2011 - present In July 2011 the white paper for Higher Education, Research, and Science entitled “Quality in diversity. Strategic Agenda for Higher Education, Research, and Science” is presented.

10 This policy document sets out the ambitions and intentions of

the Dutch government in the area of Higher Education and science policy, and defines a framework for intervention. This policy has close links to the industry policy as discussed in Box 1. The government defines as its ambition in the agenda: “[…] to equip the Netherlands in order to have a position in the forefront of knowledge economies. The aim is to create a Higher Education system which can compete internationally, performs international outstanding research and to enforce the international position of businesses.” The subsequent future of science and its actors is described as:

The research landscape in 2025 will have a number of distinct, internationally recognised and competing research focus areas, which are able to acquire European funding because they are well embedded in strong European alliances.

Scientific quality and impact are the most important criteria for forming these research focus areas. Within the research focus areas there is close collaboration with companies from the Dutch top sectors and with social organisations for the answers to the big challenges of this century.

The connections between fundamental research, practice-oriented research, applied research, innovations in companies and social renewal will be much stronger and more firmly embedded in 2025. Alongside scientific quality and the criterion of excellence, economic and social impact are central values in the science system.

Key terms of the Strategic Agenda are profiling and impact of research. The aim of profiling is to ensure that universities enhance their academic profile by forming of research focus areas and by collaboration in alliances. The aim is that every university, at least in some areas, belongs to the world's best. Besides, the aim is that the universities contribute to the economic top sectors and "grand challenges". Regarding the impact of research concerns the aim is that new knowledge finds its way towards innovation (innovative products, processes and services). This calls for further public - private partnerships between universities, companies and social institutions.

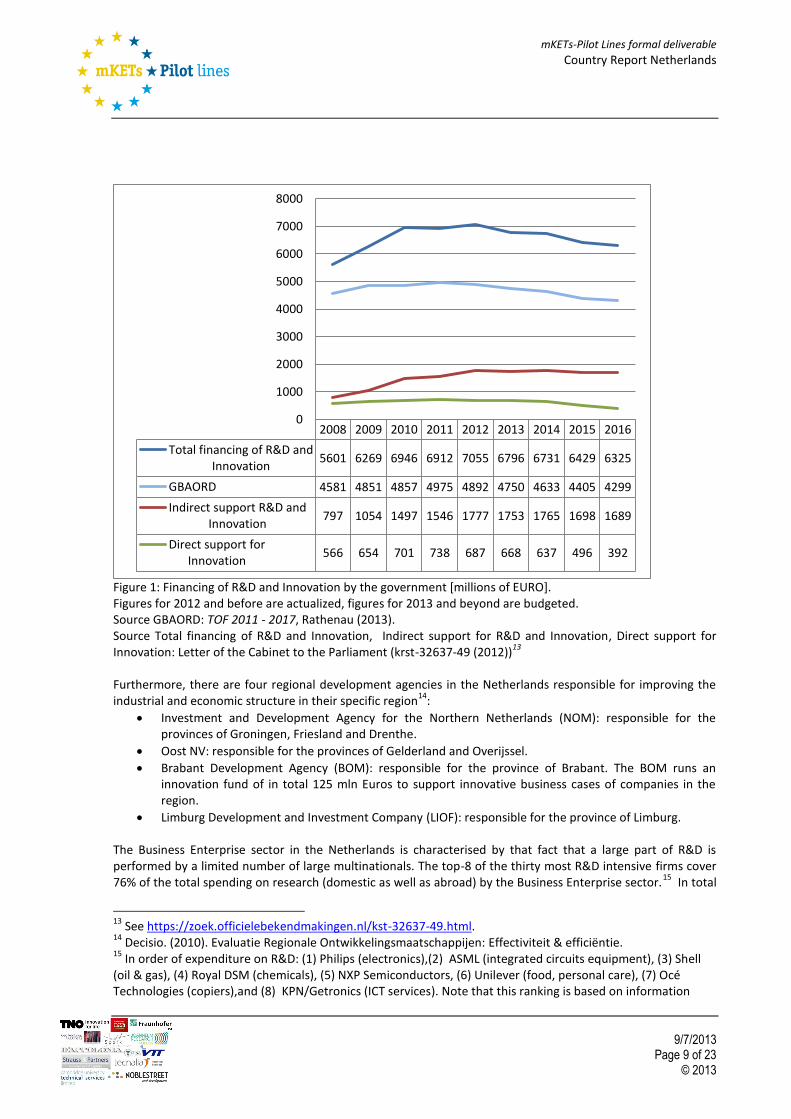

Box 2: Higher Education, Research, and Science Policy 2011 - present KETs are not specifically identified in policy addressing the DIS as described above. But the majority of KETs are covered by the Top-Sectors. The initial plan was to implement an extra governance-structure to coordinate between top sectors and KETs, but this proved to be too bureaucratic and was therefore dismantled. The overall governmental budget allocated for the financing of R&D and Innovation is as described in Figure 1.

11 Part of this is directed towards research and Innovation addressing KETs. The exact budget allocated

however cannot be identified. Important within the framework of this study are the instruments implemented by NL Agency as they could be used for KETs: fiscal tools for industry-oriented R&D and Innovation and direct financial support for innovation (see Figure 1 for total budget). The main fiscal measures implemented by Agency NL addressing R&D and Innovation are:

Research and Development (Promotion) Act (WBSO), implemented already in 1994. Biggest part of the budget involves a reduction of the wage costs associated with research and development,

Research & Development Allowance (RDA), implemented in 2012. This scheme, which supplements the WBSO scheme, is intended for entrepreneurs engaged in R&D. Whereas WBSO is used for staff costs associated with R&D projects, RDA covers the other costs associated with such projects.

The Innovation-Box (since 2010) that allows for a decrease of the total corporate tax for profits resulting from innovation.

10

OCW (2011) Kwaliteit in verscheidenheid. Strategische Agenda Hoger Onderwijs, Onderzoek en Wetenschap, see www.rijksoverheid.nl/documenten-en-publicaties/rapporten/2011/07/01/kwaliteit-in-verscheidenheid.html. 11

Note that this includes for example base funding of the public research infrastructure (i.e. Higher Education institutes and Research Institutes).

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 8 of 23 © 2013

Important direct measures implemented by Agency NL addressing Innovation are:

SME+ Innovation Fund (Innovatiefonds MKB+), implemented in 2012. This scheme consists of 3 pillars: o The Innovation Credit, used to stimulate development projects to which financial risks are attached.

Businesses cannot raise (sufficient) funds in the capital market in order to finance these projects. The Innovation Credit is available for innovative SMEs and SMEs+ that require financing. The minimum project size of the innovation credit is € 150,000.

o The SEED Capital scheme allows emerging technology and creative entrepreneurs to be assisted by investors to convert their knowledge into suitable products or services. The scheme improves the risk-return ratio for investors and increases the financing possibilities for emerging technology and creative entrepreneurs. Emerging entrepreneurs can turn to the investment funds for this.

o The Fund-of-Funds improves the access to the risk capital market for rapidly-growing innovative companies as well. This investment fund is managed by the European Investment Fund in conjunction with the Regional Venture Capital Company for the eastern part of the Netherlands (PPM Oost)

Innovation Performance Contracts (IPC), launched in 2007. This measure provides financial support in the form of a subsidy for multi-annual innovation trajectories of groups of SMEs, under supervision of coordinating organisation that acts for the group, e.g. the sector organisation. The main aims are to increase the innovativeness of SMEs and to increase collaboration and knowledge transfer. The core of the scheme is an agreement (contract) between SMEs and the coordinating organisation about an extra effort in innovation. The scheme is targeted at SMEs that are related (via value chain / sector / region / theme). The SMEs run their own innovation plans, including collective projects with other IPC-participants.

12

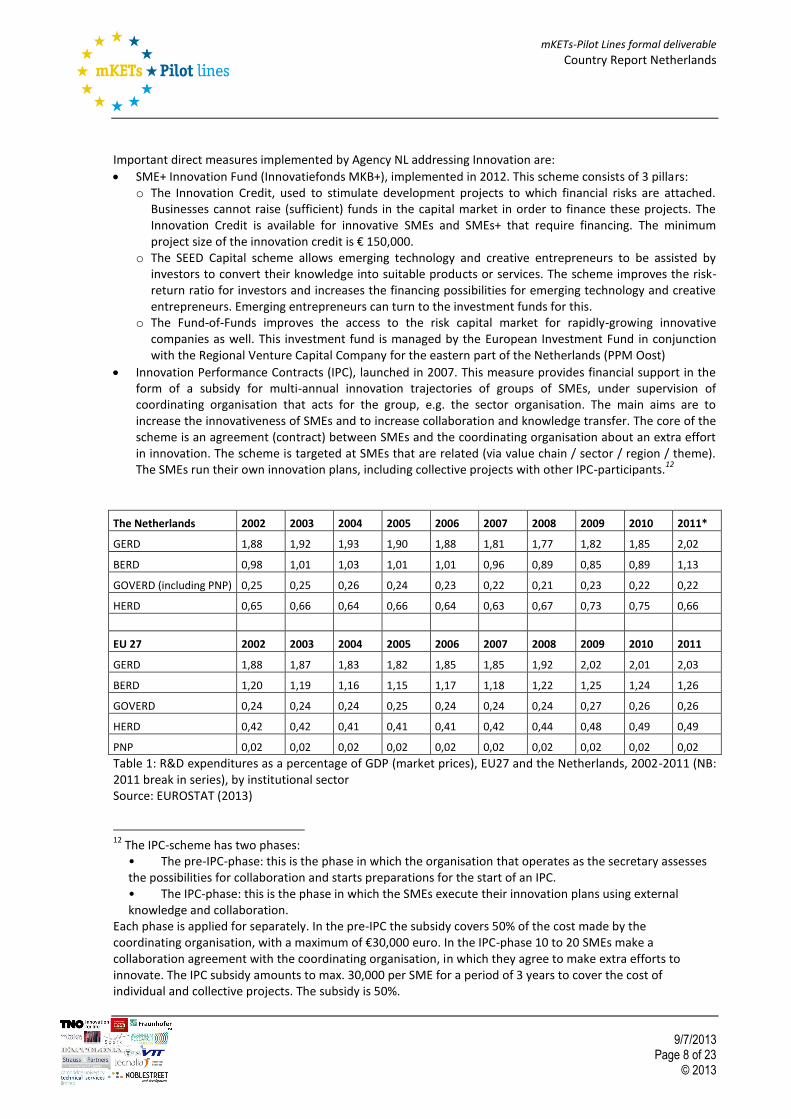

The Netherlands 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

GERD 1,88 1,92 1,93 1,90 1,88 1,81 1,77 1,82 1,85 2,02

BERD 0,98 1,01 1,03 1,01 1,01 0,96 0,89 0,85 0,89 1,13

GOVERD (including PNP) 0,25 0,25 0,26 0,24 0,23 0,22 0,21 0,23 0,22 0,22

HERD 0,65 0,66 0,64 0,66 0,64 0,63 0,67 0,73 0,75 0,66

EU 27 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

GERD 1,88 1,87 1,83 1,82 1,85 1,85 1,92 2,02 2,01 2,03

BERD 1,20 1,19 1,16 1,15 1,17 1,18 1,22 1,25 1,24 1,26

GOVERD 0,24 0,24 0,24 0,25 0,24 0,24 0,24 0,27 0,26 0,26

HERD 0,42 0,42 0,41 0,41 0,41 0,42 0,44 0,48 0,49 0,49

PNP 0,02 0,02 0,02 0,02 0,02 0,02 0,02 0,02 0,02 0,02

Table 1: R&D expenditures as a percentage of GDP (market prices), EU27 and the Netherlands, 2002-2011 (NB: 2011 break in series), by institutional sector Source: EUROSTAT (2013)

12

The IPC-scheme has two phases: • The pre-IPC-phase: this is the phase in which the organisation that operates as the secretary assesses the possibilities for collaboration and starts preparations for the start of an IPC. • The IPC-phase: this is the phase in which the SMEs execute their innovation plans using external knowledge and collaboration.

Each phase is applied for separately. In the pre-IPC the subsidy covers 50% of the cost made by the coordinating organisation, with a maximum of €30,000 euro. In the IPC-phase 10 to 20 SMEs make a collaboration agreement with the coordinating organisation, in which they agree to make extra efforts to innovate. The IPC subsidy amounts to max. 30,000 per SME for a period of 3 years to cover the cost of individual and collective projects. The subsidy is 50%.

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 9 of 23 © 2013

Figure 1: Financing of R&D and Innovation by the government [millions of EURO]. Figures for 2012 and before are actualized, figures for 2013 and beyond are budgeted. Source GBAORD: TOF 2011 - 2017, Rathenau (2013). Source Total financing of R&D and Innovation, Indirect support for R&D and Innovation, Direct support for Innovation: Letter of the Cabinet to the Parliament (krst-32637-49 (2012))

13

Furthermore, there are four regional development agencies in the Netherlands responsible for improving the industrial and economic structure in their specific region

14:

Investment and Development Agency for the Northern Netherlands (NOM): responsible for the provinces of Groningen, Friesland and Drenthe.

Oost NV: responsible for the provinces of Gelderland and Overijssel.

Brabant Development Agency (BOM): responsible for the province of Brabant. The BOM runs an innovation fund of in total 125 mln Euros to support innovative business cases of companies in the region.

Limburg Development and Investment Company (LIOF): responsible for the province of Limburg.

The Business Enterprise sector in the Netherlands is characterised by that fact that a large part of R&D is performed by a limited number of large multinationals. The top-8 of the thirty most R&D intensive firms cover 76% of the total spending on research (domestic as well as abroad) by the Business Enterprise sector.

15 In total

13

See https://zoek.officielebekendmakingen.nl/kst-32637-49.html. 14

Decisio. (2010). Evaluatie Regionale Ontwikkelingsmaatschappijen: Effectiviteit & efficiëntie. 15

In order of expenditure on R&D: (1) Philips (electronics),(2) ASML (integrated circuits equipment), (3) Shell (oil & gas), (4) Royal DSM (chemicals), (5) NXP Semiconductors, (6) Unilever (food, personal care), (7) Océ Technologies (copiers),and (8) KPN/Getronics (ICT services). Note that this ranking is based on information

2008 2009 2010 2011 2012 2013 2014 2015 2016

Total financing of R&D andInnovation

5601 6269 6946 6912 7055 6796 6731 6429 6325

GBAORD 4581 4851 4857 4975 4892 4750 4633 4405 4299

Indirect support R&D andInnovation

797 1054 1497 1546 1777 1753 1765 1698 1689

Direct support forInnovation

566 654 701 738 687 668 637 496 392

0

1000

2000

3000

4000

5000

6000

7000

8000

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 10 of 23 © 2013

41% of their expenditure is allocated within the Netherlands, 59% abroad. The top-14 of them together account for around half of all research spending within the Netherlands (i.e. BERD). It is no surprise that these companies are all involved in KETs. The total expenditure on R&D of the top-8 increased over the period 2000 - 2010 (except for Philips, but that had to do with the split of NXP), but mainly abroad. Total BERD in the Netherlands decreased in that period. In 2010, there were approximately 4600 companies with more than 10 employees that carried out R&D (7% of the total population with more than 10 employees). More than half of that type of firms was involved in innovative activities (either product, process or organisational innovation); a share that is in line with the EU 27 average. In general, expenditure on R&D in the Netherlands is below EU average for the different actors from the DIS (see Table 1).

1.2. Organisation of mKETs policy

Most relevant for the support of mKETS are the interventions resulting from the policy supporting Top-Sectors, as they address cross fertilization of Key Enabling Technologies.

16 The Top-Sectors are each governed by so-

called Top-Teams, representing researchers, entrepreneurs and the government from the specific fields. Each Top-Team formulates an Innovation contract describing how actors from the field they represent will use resources for knowledge and innovation in order to address the specific objective as described above. Each Innovation contract will contain a list of measures addressing basic / fundamental and applied research as well as exploitation of the knowledge created (i.e. valorisation). Corresponding objective is to set-out directions for research programmes of NWO, KNAW, TNO, DLO and GTI’s as well as research by Higher Education institutes. Research with the Top-Sectors, as defined by the Top-Teams in the Innovation contracts is implemented by means of Top-consortiums for Knowledge and Innovation (Topconsortia voor Kennis en Innovatie (TKIs)). Research varies from R&D within dedicated laboratories to building of prototypes. Per sector, one or more TKIs could be implemented.

17 Objective is that in total public and private actors from the sectors allocate 500

million EURO with the help of the TKIs, with 40% financed by the business Enterprise sector. The Top-Sector policy is considered an integral approach, where the whole value chain (horizontal and vertical) is included. Also the innovation chain from TRL 1-9 is to be addressed. The Top-Sectors are trying to link to EU instruments like H2020, JTI’s, JU’s.

18

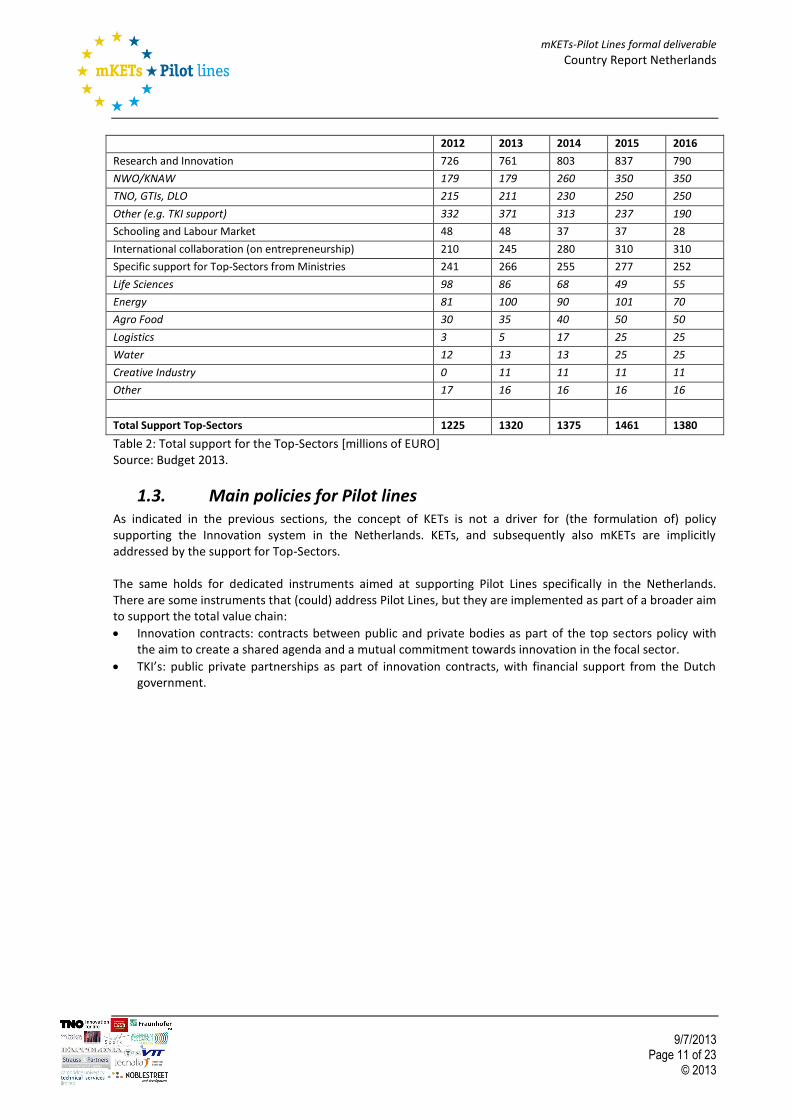

Table 2 provides an overview of the total budgeted financial resources to be allocated to the Top-Sectors. Note that this is a part of the budget described in the previous sections (i.e. Figure 1).

provided by firms on a voluntary basis within the framework of a yearly but unofficial review. Some firms have chosen not to participate in the review, and are subsequently not included in the analysis. 16

Some research areas are considered crosscutting and specific attention is given through organisational structures (separate teams). These are ICT, Nanotech, High tech systems, Biobased economy. 17

TKIs are designed such that they address specific characteristics of their corresponding Top-Sector:

TKIs aim at programming the whole knowledge chain with the help of a multi-annual work programme.

This work programme has a size of at least 5 million EURO, with at least 40% financing by the Business enterprise sector.

Publis financing is designed such that it falls within the scope of the State Aid rules on R&D and Innovation.

By hosting the TKI within the framework of an existing organisation, and by making use of existing infrastructure,

administrative procedures should be simplified as much as possible. 18

Although the EU is given specific attention, also links to other actors / initiatives are considered.

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 11 of 23 © 2013

2012 2013 2014 2015 2016

Research and Innovation 726 761 803 837 790

NWO/KNAW 179 179 260 350 350

TNO, GTIs, DLO 215 211 230 250 250

Other (e.g. TKI support) 332 371 313 237 190

Schooling and Labour Market 48 48 37 37 28

International collaboration (on entrepreneurship) 210 245 280 310 310

Specific support for Top-Sectors from Ministries 241 266 255 277 252

Life Sciences 98 86 68 49 55

Energy 81 100 90 101 70

Agro Food 30 35 40 50 50

Logistics 3 5 17 25 25

Water 12 13 13 25 25

Creative Industry 0 11 11 11 11

Other 17 16 16 16 16

Total Support Top-Sectors 1225 1320 1375 1461 1380

Table 2: Total support for the Top-Sectors [millions of EURO] Source: Budget 2013.

1.3. Main policies for Pilot lines

As indicated in the previous sections, the concept of KETs is not a driver for (the formulation of) policy supporting the Innovation system in the Netherlands. KETs, and subsequently also mKETs are implicitly addressed by the support for Top-Sectors. The same holds for dedicated instruments aimed at supporting Pilot Lines specifically in the Netherlands. There are some instruments that (could) address Pilot Lines, but they are implemented as part of a broader aim to support the total value chain:

Innovation contracts: contracts between public and private bodies as part of the top sectors policy with the aim to create a shared agenda and a mutual commitment towards innovation in the focal sector.

TKI’s: public private partnerships as part of innovation contracts, with financial support from the Dutch government.

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 12 of 23 © 2013

2. Business perspective This chapter discusses the business perspective on pilot lines in The Netherlands. First, the experiences concerning the implementation of pilot lines will be discussed, using the interviews and subsequent desk research as most important input input, followed by a discussion of policy instruments which have a crucial impact on pilot lines.

2.1. Implementation of multi-KETs pilot lines The experiences concerning the implementation of pilot lines will be discussed along three lines. First, the technological aspects of pilot lines will be discussed, focusing on for example the technology readiness levels (TRL) involved, the role of KETs vs. multi-KETs in relation to pilot lines and the role of the process perspective in this respect. Second, the organizational aspects of pilot lines will be discussed, paying attention to the way pilot lines are realized for each KET. This paragraph concludes with an elaboration on the market perspective of pilot lines in the Netherlands, focusing on the connections and interactions between pilot lines and the market. Technological perspective on pilot lines All stakeholders agreed with the European Commission that the valley of death between basic knowledge generation and the subsequent commercialization of this knowledge in marketable products is the most problematic phase in European KET enabled value chains. At the same time, bridging this gap between R&D and commercial production is crucial to address grand challenges and create market impact. Addressing the problems in bridging this gap should therefore be an important element of public policy. However, it became clear that KETs is mainly a policy concept and that the projects and business plans of the industry are not formulated in terms of the KETs involved. The concept of KETs seems to be poorly understood and industry stakeholders have especially difficulties in understanding the difference between the concepts of KETs and multi-KETs. Stakeholders argue that the difference between both is rather arbitrary, two observations seem to be particularly important here.

First, each step in the development process of a new component involves one or more KETs. It seems to depend on the level of analysis if one can speak of a KET or multi-KET project: on the level of the component the project might involve one KET, but if this component is broken down into its components, then each component might involve different KETs. In other words, the more detailed your perspective on pilot lines is, the more KETs will be involved.

Second, in reality it seems that the industry always combines several KETs to form KET based components and products. Some stakeholders even argue that single KET pilot lines do not even exist and that all pilot projects can be characterized as multi-KET, which raises the question what the added value of multi-KETs compared to KETs concept is. Given this observation, it seems that one KET is always dominant in multi-KETs projects, raising the question when one can speak of a single-KET project or a multi-KET project with one dominant KET involved.

Stakeholders agree that in general the six KETs identified constitute important technologies for Europe, yet they argue that the demarcation of the various KETs is somewhat ambiguous. For example, stakeholders argue that the current definition of nanotechnology is very broad and is found in almost any KET enabled product, material or equipment. Furthermore, the stakeholders argue that the several KETs have important differences and that any policy with regard to KETs should respect these differences. Yet the majority of experts believes that there is currently too much focus on the nano-microelectronics or semi-conductors industry and that the majority of technological constructs involved in the KETs discussion are arrived from this industry, although these concepts are not always applicable to other KETs. We will elaborate on this discussion later on in this paragraph. With regard to the technological aspects of the development of pilot lines, industry stakeholders warn for an over emphasis on the product side of the innovation chain. The process perspective is important as well: pilot

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 13 of 23 © 2013

lines are generally used to demonstrate the manufacturability of a breakthrough product, component or material. Manufacturability is clearly an issue when it comes to pilot production. Especially for nano-microelectronics this is important: pilot lines in this sector are used to initiate the first experiences with process development. The importance of such a process perspective becomes eminent when one looks closer at the development of pilot projects. Two observations are particularly important in this respect.

First, according to industry stakeholders, the upscaling of KET based components should not be perceived as a linear cycle in which a company makes a linear progress through several technology readiness levels and ultimately ends up with a component ready for market commercialization. Rather, the development is an iterative process in which a company starts with a design or proof of concept, initiates a pilot project in which it aims to progress towards commercial manufacturing, but experiences unexpected delays or complications in the upscaling process. This initiates an iterative cycle in which a company returns to the drawing board, makes adjustments to the material, component or equipment, and again progresses trough commercialization and up scaling phases. Using several iterative cycles from design to product, the product slowly evolves to the product with the characteristics as identified in the original project plan.

Second, it seems that the experiences concerning development of the manufacturing process can be a reason to return to the design phase of a project and make adjustments in the characteristics of the product or material one wishes to upscale. In other words, experiences with the process can trigger adjustments in the product elements of a pilot project. For example, with advanced materials it is often the case that the composition of a new composite or polymer is not reproducible on a larger scale. In other words, the company cannot guarantee the quality of the output at the level that is required by the end customer. The contrary is true as well: a proposed product with certain unique characteristics usually cannot be manufactured with existing equipment, triggering an iterative cycle in which changes will be made to the process to make upscaling of the product possible and initiate the first experiences with larger scale assembly and manufacturing. In sum, the product and process side of a pilot project are very much intertwined and both seem to be crucial to include in the definition of a pilot project.

Furthermore, it is important that already in the earlier TRLs attention should be paid to the pilot activities. That means that projects focusing on TRLs 1-4 should already be thinking about the necessary steps to be taken to bridge the subsequent TRLs. At the moment, the projects which address different TRLs are too much separated, improving the coherence between these steps increases the speed of development and decreases costs. Organizational perspective on pilot lines A pilot was commonly defined as a facility or activity where the first experiences with new products, equipment or tools are initiated. Such projects are generally referred to as pilot lines

19, yet it seems that especially for

industrial biotechnology and to a lesser extent for advanced materials the notion of a pilot line does not fully capture the scope and experiences of a pilot project. First, it seems that with these KETs the focus is not on the production of components, but on the up scaling of for example new materials or fermentation processes. The notion that “the purpose of the pilot line is to deliver early-stage prototype products through production in low Volumes”

20 might not fully capture the experiences and scope in terms of the upscaling of industrial biotech

based materials and processes. Second, pilot projects in advanced materials and especially industrial biotechnology are better captured through notions such as pilot plants, testing facilities or pilot facility. Several examples of such facilities were found in this country study, to illustrate this observation:

1. Bioprocess Pilot Facility: this facility is located on the DSM site in Delft. The consortium, in which DSM, CSM/Purac and Delft University of Technology collaborate, boasts facilities for upscaling

19

HLG on Key Enabling Technologies (2011): Final Report, European Commission, Brussels. 20

HLG on Key Enabling Technologies. (2011e). Pilot Activities for Jobs and Growth and Advanced Manufacturing in Europe. Working Group 4 Report, Brussels: European Commission. P. 5

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 14 of 23 © 2013

biotechnological processes that can be used for both R&D and educational purposes 21

. The BPF is of key importance for upscaling fermentation and purification processes as well as for the pretreatment of vegetable residues to convert them into fermentation feedstock, for instance as used for second-generation biofuels. The BPF is an open facility in which other companies, universities, institutes, etc. can conduct their upscaling research for bio-processes. Thanks to a joint contribution from the province and municipalities of South Holland the BPF will also be available for use by smaller start-ups.

2. Pilot plants Geleen: two pilot plants are operated by DSM on the Chemelot Campus near Geleen. One pilot plant focuses on the transfer of bio mass into chemical raw materials, another aims on the upscaling of high-performance materials. Both facilities are open to third parties and will closely collaborate with knowledge institutes, government bodies and other companies (including SMEs). The presence on the Chemelot Campus also offers such opportunities for open innovation thanks to the proximity of other (start-up) companies and research and education institutes.

3. Avantium Pilot Plant. This plant is constructed as well on the Chemelot Campus near Geleen in the Netherlands. Avantium has developed a novel and proprietary catalytic process to convert carbohydrates into furanic building blocks under the brand name YXY. The pilot plant will produce these YXY building blocks for making green materials and fuels. The pilot plant will demonstrate the breakthrough process developed in Avantium’s labs at larger scale. Furthermore, it will produce several tons of YXY building blocks per year to support product development. Avantium is collaborating with industrial partners such as NatureWorks (a subsidiary of Cargill) and Teijin Aramid to develop novel materials on basis of its YXY building blocks, the remaining 15 million Euros is raised through additional private funding

22.

Yet there even seem to be considerable differences between these pilot plants for industrial biotechnology, signaling the complexity in defining the concept of pilot lines or pilot activities. For example, whereas the pilot plant operated by Avantium is a single purpose facility focused on the up scaling of YXY building blocks for green materials and fuels and is not open to third parties, other plants operated by DSM offer a wider range of equipment to support the up scaling of for example fermentation and purification processes. Furthermore, these plants are open to third parties, giving research institutes, SMEs and start-ups the possibility to upscale their processes. These facilities are perhaps better captured through the notion of testing facility or pilot facility, to signal the difference with single purpose pilot plants. The notion of pilot lines seems to be better applicable to those projects which focus on the upscaling of photonics, nanotechnology or nano-microelectronics based components. With these KETs the focus is on the upscaling of distinct products, which seems to more in line with the perspective of the High Level Group on KETs

23.

Although there seem to be large differences between the organizational aspects of a pilot activity depending on the KET involved, all industry stakeholders agreed that pilots should be industry led and industry owned. This is crucial to ensure a market uptake of the output of a pilot line and to ensure that this output will feed into the commercialization of new components, equipment or materials. Since the commercialization of this output is the responsibility of industry, stakeholders argue that the organization of a pilot line should also be done by industry, to make sure that the step from pilot to commercialization is coherent. Industry stakeholders explicitly argued that pilot lines should not be led by universities, since universities do not directly benefit from the commercialization of the output of a pilot line and therefore focus on the wrong aspects in upscaling new KET based products. Furthermore, universities are evaluated based on the number of citations, which is generally not a good indicator of the success of a pilot line. In general very few publications emerge from pilot projects.

21

DSM. (2012). DSM invests in knowledge and innovation in the Netherlands. Retrieved from: http://www.dsm.com/en_US/html/dep/news_items/2012-22-5-DSM-invests-knowledge-inno-in-Netherlands.htm 22

Avantium. (2010). Avantium builds YXY pilot plant for green materials and fuels. Retrieved from: http://avantium.com/news/2011-2/Avantium-announces-opening-and-start-up-of-its-YXY-Pilot-Plant.html 23

HLG on Key Enabling Technologies (2011): Final Report, European Commission, Brussels.

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 15 of 23 © 2013

However, pilot lines do not necessarily have to be closed, in fact the majority of stakeholders had positive relevant experience with open facilities or test facilities. The decision to collaborate with such facilities is very much dependent on the equipment that is available at such facilities. If the facility occupies the necessary equipment, then it seems that especially for SMEs such facilities are an excellent opportunity to test or measure the performance of new components, without having to invest large funds in the acquisition of tools and equipment. Market perspective on pilot lines Concerning the reasons to initiate pilot lines, it seems that pilots are mainly initiated to serve an emerging market demand and differentiate from competitors. According to industry stakeholders, pilot projects address a market need and therefore have to be located close to the market. For example, Avantium mentions in its press statement

24 that “With the strong market pull from corporations and consumers for green materials, the

time is right for the scale-up of our technology. We look for industrial partners in the polymer, chemicals, materials and fuels sectors to support our development of YXY based materials and fuels, and help us create a truly green economy”. This means that the market should be in a sufficient mature stadium to persuade companies to invest in pilot activities. If the market is still in an embryonic phase, it seems that the industry in general is not willing to invest in pilot projects. Yet the difficulties experienced in the initiation of pilot lines differ considerably depending on the market and the investments involved. The higher the investments, the more uncertain the market outlook is and the shorter the life cycle, the more problematic the initiation of pilot lines is. Depending on the complexity of a pilot line, the project can take up anything from 3 months to 3 years. These problems are especially severe for SMEs, since they are very much dependent on the market when it comes to the initiation of pilot lines, and it seems that a mature market much more important to SMEs than it is for larger companies. SMEs lack the financial and human resources to organize pilot activities from a technology push perspective, whereas larger companies can afford to experiment with components and materials with a more uncertain market outlook. Industry stakeholders emphasized that SMEs wait for a customer demand before they determine if a pilot line should be initiated. In such cases the demands of a customer are compared with the existing standards, if the demands are any different, changes have to be made to the assembly line or in the composition of the product or material. The goal is always to show to customers if a reproducable number of units can be manufactured with the quality that is requested by the customer. Of course it happens that customers are not satisfied with the sample that is delivered by the SME, sometimes leading to a cancellation of the order. Therefore, there is much risk involved for the SME and in practice it does not always seem to be possible to share this risk with the customer. In some cases it is in the interest of the SME to not to share the risk of a pilot project, since the intellectual property on the developed components or materials rests with the SME. Concerning the position of a pilot activity in the value chain, industry stakeholders argue that such activities are an essential element in the value chain to bridge the gap between R&D and commercial production. However, stakeholders argued that it is not necessary to have the whole value chain for KETs based components, materials or products in Europe. For each step in the value chain, companies determine where it should be located or with which partners they want to collaborate, based on the competences and experience of relevant partners in each region. Whether such partners are located in Europe or not is not important. Furthermore, Collaboration across continents is very often a prerequisite for the successful initiation of pilot lines, since KETs very often involve specific knowledge and capabilities which are not always found in Europe. Therefore, industry stakeholders argued that it is perhaps not a realistic ambition to retain the entire KET value chain in Europe. Rather, it is emphasized that Europe needs to focus on those aspects of the value chain that are crucial to the development of KETs based products and which require high skilled and knowledge intensive labor. It is those steps in the value chain which create value and where Europe really can differentiate from low-wage

24

Avantium. (2010). Avantium builds YXY pilot plant for green materials and fuels. Retrieved from: http://avantium.com/news/2011-2/Avantium-announces-opening-and-start-up-of-its-YXY-Pilot-Plant.html

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 16 of 23 © 2013

countries. Stakeholders argued that there is no need in having the development and production for ‘off the shelf” components in Europe.

2.2 Evaluation of KET policies This paragraph discusses the role of various policy instrument in stimulating KET pilot activities. First, the role of public funds will be discussed, which was emphasized as the most important policy instrument, followed by a discussion of various other policy instrument which can have an impact on pilot activities. This paragraph concludes with an elaboration on the role of national innovation policy on pilot activities from a business perspective. Role of public funding In terms of relevant policy instruments, all stakeholders agreed that funding is the most important policy instrument. All industry stakeholders also have relevant experience with public funding in terms of the initiation and organization of pilot lines. If pilot projects are pre-competitive, not commercial and the product, technology or market is still in an embryonic stage, they argue, then the step from prototype to commercial manufacturing is too large for a company to be taken alone. Public support through funding is crucial in this respect. However, the role of such public funds differs to large extent depending if the SMEs or large conglomerates are the focal point of interest. For SMEs, it seems that public funding is crucial to persuade them to initiate pilot activities and bridge the gap towards commercial manufacturing. Several SMEs examined in this country study had relevant experiences with FP7 programs which explicitly focus on the support of pilot activities for SMEs. In general, such programs are experienced as helpful and useful instruments, yet the process of selecting among projects eligible for funding under Framework Programmes should be faster than is currently the case. At the moment, there is also too much bureaucracy involved in the request for funding under Framework Programmes. The industry perceives that a period of three months is the maximum period between the issuing of a proposal and the selection if this proposal is eligible for funding. Industry stakeholders also argued that when multi-purpose facilities are open to other companies, irrespective if they are independent or operated by a large conglomerate, funds should be available for SMEs to upscale their pilot projects towards commercial manufacturing at such facilities. For larger companies the situation seems to be different. These stakeholders argued that the role of public funding is not so much important because of the funds itself, but rather that public support has an instrumental role in institutionalizing cross-border collaboration. Especially tri-partite approaches such as Joint Technology Initiatives, in which the industry, the Community and EU member states jointly invest in pilot projects through competitive calls for proposals, are highly valued by those organizations that take part in initiatives. Large conglomerates do not only participate in such initiatives because of the public support available, but rather because such support can be a key incentive to bring together a consortium with partners to initiate a pilot project. With regard to such Joint Technology Initiatives, companies emphasized two positive aspects about such initiatives. First, it forces companies to do their best, since the call for proposals is a competitive process with few available funds for many interested companies. It also allows governments to leverage their available funds and it invest in the projects which are most interesting to them. Second, when funds are assigned to certain projects they are immediately available to the consortium, which constitutes a large advantage over other programs such as EUREKA, where funds are not immediately transferred at the start of the project. Concerning the type of funding instrument, industry stakeholders argue that subsidies are the preferred policy instrument. Loans are more relevant when a company progresses through the higher technology readiness levels, for example in the support of KET deployment activities.

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 17 of 23 © 2013

To conclude, the stakeholders emphasized that funding should be focused and targeted to the right areas and industries. In this respect several stakeholders warn for an over emphasis on the micro-nanoelectronics industry. Stakeholders argued that Europe seems to be very afraid of losing this industry and therefore neglects to some extent the industries which are highly relevant as well to Europe. A more balanced approach in terms of funding and attention would be recommendable. Other relevant policy instruments. Next to public funding, several other policy instruments were mentioned by the industry stakeholders which are crucial for the support of KET pilot lines. Public policy should focus on a wider array of policy instruments to support pilot activities. At the moment, the focus is mainly on providing subsidies, whereas industry stakeholders argue that other instruments could be relevant as well.

First, stakeholders advocated the use of innovative public procurement to stimulate KET pilot lines. Due to the funds involved with public procurement, the potential of this policy instrument is large, yet it is difficult to apply for the government in the majority of sectors. The American government uses such procurement tools to stimulate the defense industry, yet this industry is relatively small in Europe compared to US. However, it could be applied to the industrial biotechnology sector, for example by improving the sustainability of procurement and initiating a green procurement policy. For example, government could advocate the use of alternative energy sources. Although the potential seems large, the stakeholders agreed that governments in general and the Dutch government specifically lacks the capabilities to implement an innovative public procurement in a well-organized manner and lacks a vision in this respect.

Second, the harmonization of public policy across EU member states should be improved, at the moment the differences between the countries are too large. Large differences between countries in terms of the regulation associated with KET based products decreases the motivation of countries to invest in pilot activities to upscale components relevant to such products. The investments which are necessary to initiate such pilot activities require that the output can be sold in more than one EU country, otherwise the business case is generally not favorable to the company. In general, obeying the specific national regulations of each EU member states costs a lot of time and effort by the companies. Harmonizing the regulation between the nations to support KET pilot lines is coherent with the perspective that such activities are of European interest and require actions on an EU level.

Third, the EU can help in finding employees and specialists with the right competences. The EU already provides such a facilitating role for PHDs and academia, but should do that for the manufacturing industry as well. The EU can play a role in bringing together the supply and demand of high skilled manufacturing labor. Especially SMEs would benefit from such a facility, since they generally lack financial and human resources to find employees with specific competences themselves.

Finally, stakeholders agreed that a fundamental revision of the state-aid rules is necessary if Europe wants to invest in KET pilot lines. At the moment, financial aid is very much limited to SMEs and countries in the earlier technology readiness levels, the financial support for large scale pilot plants or multi-purpose facilities in Europe led by large conglomerates is currently too much inhibited by the state aid rules. Furthermore, these rules focus to large extent on preventing unfair competition between EU member states, whereas KET pilot activities address the competition between Europe as a whole versus Asia or the USA, due to international character of KETs. The way state-aid rules are currently formulated therefore do not seem to be applicable to the problems associated with KET pilot activities. To conclude, state aid rules limit the contribution of the Community to Joint Undertakings to 10 million euros, inhibiting the support of pilot lines, since the majority of projects requires a contribution which exceeds the sum of 10 million euros.

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 18 of 23 © 2013

Role of national innovation policy At the moment, the Dutch Top Sectors policy is very limited when it comes to the support of KET activities in general or KET pilot lines specifically. Therefore, industry stakeholders benefit only marginally from this Top Sector policy. Three reasons were identified for this. First, stakeholders agreed that the support for KET pilot lines is mainly a European affair and should therefore be organized on a European level. KET projects seem to have an international character by nature, since it involves partners and suppliers from various countries in most cases. Such cross-border collaboration makes a European agenda for KETs much more relevant than a national agenda for KETs. With regard to the Dutch innovation policy, stakeholders argue that especially such an international agenda is lacking. The Top Sectors very much focus on The Netherlands in terms of the support of projects and the organizations involved and it seems that Top sectors therefore first have to determine an international agenda for their sector before the concept of KETs can be incorporated. Second, the Top Sectors are very broad and seem to incorporate the majority of companies, whereas the goals are very broad as well. The Top Sectors policy is not focused and seems to provide little guidance to companies. Third, top sectors focus very much on public private partnerships and especially the collaboration with Research and Technology Organizations. The policy lacks an instrument to support the collaboration between companies as such, without the obligation to include an RTO. Fourth, the support of KET pilot activities requires funds which are generally not available on a national scale, crossing the valley of death through pilot activities can therefore only be done on a European scale. However, the industry emphasized that KETs should be part of national innovation policy, even if KETs have pan-national dimension by definition, due to the fact that the Netherlands benefits to large extent from KETs. Such policy should predominantly focus on an international KET agenda for the various top sectors, the financial support of pilot activities should be left to the European Commission.

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 19 of 23 © 2013

3. Conclusions Based on desk research and the interviews conducted, this report provided insights in the KETs policy in The Netherlands, as well as in the initiatives that the Dutch industry takes to initiate pilot lines. Several conclusions can be drawn based on the experiences of policy makers and industry stakeholders. The next paragraph discusses the conclusions from the policy perspective, followed by the conclusions from a business perspective in the second paragraph.

3.1. Summary of policy perspective The Netherlands has a thematic focus in policy supporting R&D and Innovation, as an integral part of its industry policy. But the selected Top-Sectors do not coincide with KETs. They do however address cross-fertilisation of enabling technologies. No dedicated policy or supporting instruments address Pilot Lines specifically. But they could be addressed by existing measures, as the current policy aims at supporting / sustaining the value chain, and subsequently supports firms also in higher TRL levels.

3.2. Summary of business perspective The experiences concerning the implementation of pilot lines were discussed along the lines of technology, the organization and the market. Concerning the technological perspective the following conclusions can be made:

Industry stakeholders have difficulties delineating between KET pilot lines and multi-KET pilot lines, the multi-KETs concept is not very well understood.

Although the stakeholders agree about the six KETs being important to the competitiveness of Europe, there seems to be issues around the demarcation of the various KETs. At the moment the concept of nanotechnology is for example very broad defined and is found in practically each KET enabled component or material.

Industry stakeholders emphasized the importance of incorporating a process perspective in pilot activities, since the upscaling of KETs is an iterative process in which a company starts with a design or proof of concept, initiates a pilot project in which it aims to progress towards commercial manufacturing, but experiences unexpected delays or complications in the upscaling process. This initiates an iterative cycle in which adjustments are made to the component to make it suitable for mass production.

It is important that already in the earlier TRLs attention should be paid to the pilot activities, the coherence between projects addressing different TRLs should therefore be improved.

With regard to the organizational perspective on pilot lines, the discussion can be summarized as follows:

It seems that there are large differences in terms of the scope and organizational elements of a pilot project, depending on the KETs involved. The notion of pilot lines seems to be better applicable to those projects which focus on the upscaling of photonics, nanotechnology or nano-microelectronics based components, since they focus on the upscaling of distinct products. Pilot projects in advanced materials and especially industrial biotechnology are better captured through notions such as pilot plants, testing facilities or pilot facilities, and should be perceived as small manufacturing facilities focused on the upscaling of certain processes or materials. Yet there even seem to be considerable differences between these pilot plants for industrial biotechnology, whereas some are single purpose facilities with access restricted to the consortium, others can be defined as multi-purpose facilities with a range of fermentation and purification processes and are open to third parties.

All stakeholders agree that pilot activities should be industry led and industry owned to ensure the commercialization of the output of a pilot project. However, pilot activities do not have to be closed or open, in fact the majority of stakeholders had positive experiences with multi-purpose facilities which were open to third parties.

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 20 of 23 © 2013

Depending on the complexity of a pilot line, a pilot activity can take up anything from 3 months to 3 years.

Concerning the market perspective of pilot activities, the following conclusions can be made:

It seems that pilot activities are initiated to serve an emerging market demand. Especially for SMEs the market is very important, since SMEs generally lack the financial and human resources to organize pilot activities from a technology push perspective, whereas larger companies can afford to experiment with components and materials with a more uncertain market outlook.

The higher the investments, the more uncertain the market outlook is and the shorter the life cycle, the more problematic the initiation of a pilot activity is.

The analysis of the policy instruments which have a crucial impact on pilot lines can be summarized as follows:

All stakeholders identified public funding through subsidies as the most important policy instrument to stimulate pilot activities, although the role of such funds seems to differ for large companies versus SMEs. For larger companies, the involvement of public funds is more instrumental in institutionalizing cross-border collaboration, whereas for SMEs public funding is crucial to be able to initiate pilot activities.

Several other policy instruments were identified which can have an impact on pilot activities, among which innovative procurement and the harmonization of regulation across EU member states is most important.

A revision of the state aid rules is necessary, at the moment these rules focus too much on preventing internal competition in Europe and limit the contribution of the Community to Joint Technology Initiatives.

The Dutch innovation policy seems to play only a marginal role in the stimulation of KET pilot lines, since the Top Sectors lack an international agenda and provide little guidance in terms of clear goals or roadmaps.

3.3. Recommendations to support pilot lines Several recommendations can be made based on the interviews and desk research conducted in this country study:

The Dutch policy focusses strongly on the characteristics of the Dutch Innovation System and its actors. Addressing mKETs and Pilot Lines requires intensified attention for international collaboration.

Funding of the later stages of the value chain / higher TRL levels requires a review of the State Aid rules (to allow co-funding of EU programmes).

A periodic review of thematic policy in the EU (KETs) as well as in the Netherlands (Top Sectors) is necessary.

Incorporate a process perspective in the definition of a pilot project. Pilot projects are about manufacturability and attention for the process side of a project is therefore important.

Include the possibility for research in pilot projects. Up scaling is not a linear process, but rather an iterative cycle with companies engaging in research activities to improve manufacturability. This also implies that consortiums should have the opportunity to include universities in the project.

Public policy should differentiate between SMEs and large companies. Policy for large companies should focus on creating favourable framework conditions, whereas policy for SMEs should focus on providing financial support and facilitate the search for qualified labour. An example could be a support scheme which allows access of SMEs to shared facilities.

Target public support to those projects that maximize market output, in terms of for example jobs created and market impact. It should not be required that the whole KET value chain is located in Europe.

Optimize policy delivery: e.g. faster selection of projects in view of the increased speed to market that is required for pilot projects.

Further analysis of public procurement in relation to the initiation of pilot lines is required.

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 21 of 23 © 2013

4. References

4.1. Literature Avantium. (2010). Avantium builds YXY pilot plant for green materials and fuels. Retrieved from:

http://avantium.com/news/2011-2/Avantium-announces-opening-and-start-up-of-its-YXY-Pilot-Plant.html

DSM. (2012). DSM invests in knowledge and innovation in the Netherlands. Retrieved from: http://www.dsm.com/en_US/html/dep/news_items/2012-22-5-DSM-invests-knowledge-inno-in-Netherlands.htm

HLG on Key Enabling Technologies (2011): Final Report. Brussels: European Commission.

HLG on Key Enabling Technologies. (2011e). Pilot Activities for Jobs and Growth and Advanced Manufacturing in Europe. Working Group 4 Report, Brussels: European Commission. P. 5

KNAW. (2013). Academic Institutes. Retrieved from: www.knaw.nl/Pages/DEF/27/128.bGFuZz1FTkc.html.

Ministry of Economic Affairs (2013). Kamerstuk: Bedrijfslevenbeleid. Den Haag: Tweede kamer der Staten Generaal. Retrieved from: https://zoek.officielebekendmakingen.nl/kst-32637-49.html.

Ministry of Economic Affairs, Agriculture and Innovation. (2011). To the Top: Towards a New Enterprise Policy. Den Haag: Tweede Kamer der Staten Generaal

Moons, S. and P. van Bergeijk (2011). ´De effectiviteit van economische diplomatie´ [The effectiveness of economic diplomacy] ESB 96(4616).

NWO. (2013). NWO divisions. Retrieved from: www.nwo.nl/en/about-nwo/organisation/nwo-divisions.

OCW (2011) Kwaliteit in verscheidenheid. Strategische Agenda Hoger Onderwijs, Onderzoek en Wetenschap. Retrieved from: www.rijksoverheid.nl/documenten-en-publicaties/rapporten/2011/07/01/kwaliteit-in-verscheidenheid.html.

4.2. Interviews

Ben Ruck [email protected]

NL representative CATRENE Agentschap NL

Marcel Wubbolts [email protected] CTO DSM

Koen Demeyer [email protected]

Manager Innovations & IP Anteryon

Fred van Roosmalen [email protected] Director Top Sector HTSM, NXP

Hans Geelen [email protected] Vice President R&D Océ

Theo Flipsen [email protected] CEO Polyvation

Gerold Alberga [email protected] Project Coordinator ASML

Karin Jongkind [email protected] Project Leader Ministery of Economic Affairs

Dick De Jager [email protected] Program Manager Business Development

Brabantse Ontwikkelings Maatschappij

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 22 of 23 © 2013

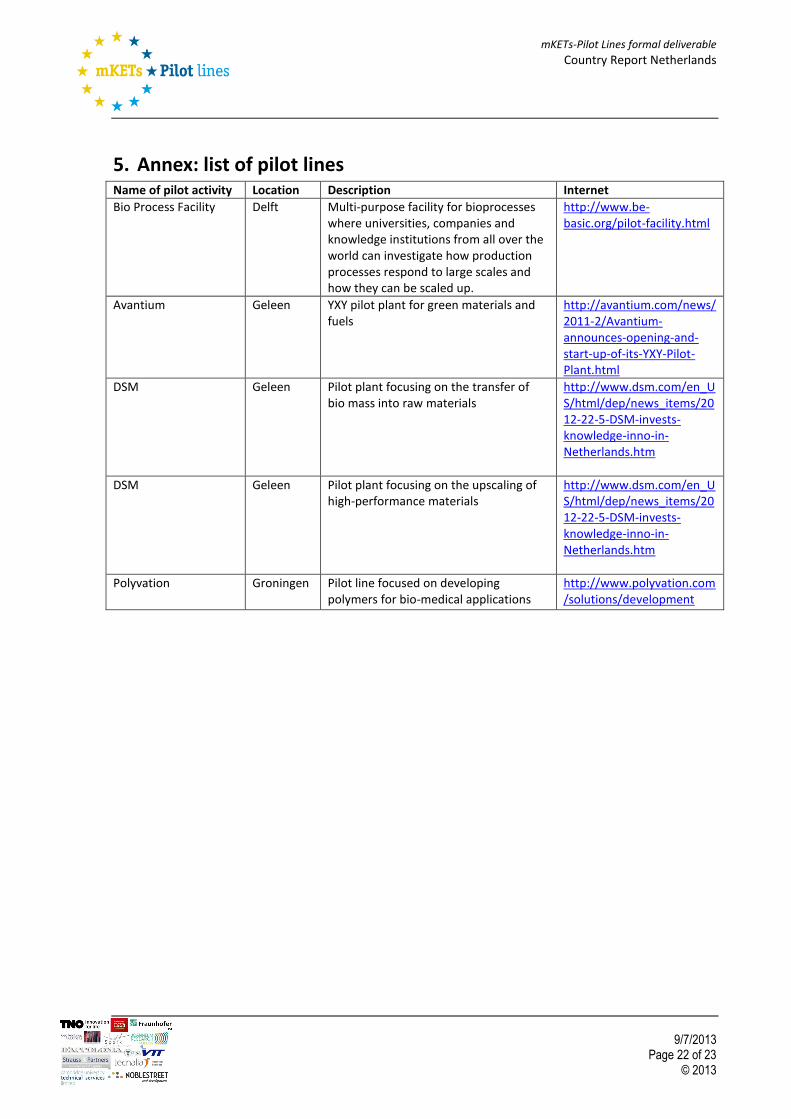

5. Annex: list of pilot lines Name of pilot activity Location Description Internet

Bio Process Facility Delft Multi-purpose facility for bioprocesses where universities, companies and knowledge institutions from all over the world can investigate how production processes respond to large scales and how they can be scaled up.

http://www.be-basic.org/pilot-facility.html

Avantium Geleen YXY pilot plant for green materials and fuels

http://avantium.com/news/2011-2/Avantium-announces-opening-and-start-up-of-its-YXY-Pilot-Plant.html

DSM Geleen Pilot plant focusing on the transfer of bio mass into raw materials

http://www.dsm.com/en_US/html/dep/news_items/2012-22-5-DSM-invests-knowledge-inno-in-Netherlands.htm

DSM Geleen Pilot plant focusing on the upscaling of high-performance materials

http://www.dsm.com/en_US/html/dep/news_items/2012-22-5-DSM-invests-knowledge-inno-in-Netherlands.htm

Polyvation Groningen Pilot line focused on developing polymers for bio-medical applications

http://www.polyvation.com/solutions/development

mKETs-Pilot Lines formal deliverable

Country Report Netherlands

9/7/2013

Page 23 of 23 © 2013

Contact information

mKETs-PL consortium Overall project management Ruud Baartmans, Maurits Butter P.O.Box 49 NL-2600 AA Delft The Netherlands : +31 888668517 : [email protected] Other partners Fraunhofer-Gesellschaft, Axel Thielmann CEA, Laurant Herault CU/Cambridge enterprise, Finbarr Liveley VTT, Torsti Loikkanen Tecnalia, Mirari Zaldua TPF, Tomasz Kosmider JR Austria, Christian Hartmann D’Appolonia S.p.A, Stefano Carosio Strauss & Partners, Roland Strauss Spark, Marc de Vries Noblestreet, Arnoud Goudsmit