Embed Size (px)

Citation preview

H1 2014 Results - Analyst & Investor Presentation

Mobistar always in touch*

2

This presentation contains forward-looking statements about Mobistar, inparticular for 2014. Although Mobistar believes these statements are based onreasonable assumptions, these forward-looking statements are subject tonumerous risks and uncertainties, including matters not yet known to us or notcurrently considered material by us, and there can be no assurance thatanticipated events will occur or that the objectives set out will actually beachieved. Important factors that could cause actual results to differ materiallyfrom the results anticipated in the forward-looking statements include, amongothers, the impact of the price adjustments on the customer base resulting fromthe competitive pressure, the evolution of the customer base, the economicsituation in Belgium, the realization of the net savings of the cost base of Mobistarof 50 million euro net in 2014, the effectiveness of Mobistar convergent strategyincluding the success and market acceptance of the voice and data abundanceplans, the Mobistar TV and broadband offers, the Mobistar brand and otherstrategic, operating and financial initiatives, Mobistar’s ability to adapt to the on-going transformation of the telecommunications industry, regulatorydevelopments and constraints and the outcome of legal proceedings, risks anduncertainties related to business activity.

3

Mobistar’s Transformation:Accelerating Momentum

4

Agenda

• Key Highlights

• Operational Update

• Financial Review

• Financial Outlook 2014

Jean Marc HarionJean Marc HarionJean Marc HarionJean Marc HarionChief Executive Officer

Siddy JobeSiddy JobeSiddy JobeSiddy JobeDirector Investor Relations

& Corporate Finance

Ludovic PechLudovic PechLudovic PechLudovic PechChief Financial Officer

5

‘Mobistar’s progress confirms our path is right and we remain reasonably optimistic going forward’

Key HighlightsJean-Marc Harion

6

Delivering on

Transformation

Financial & KPI’s in line with guidance

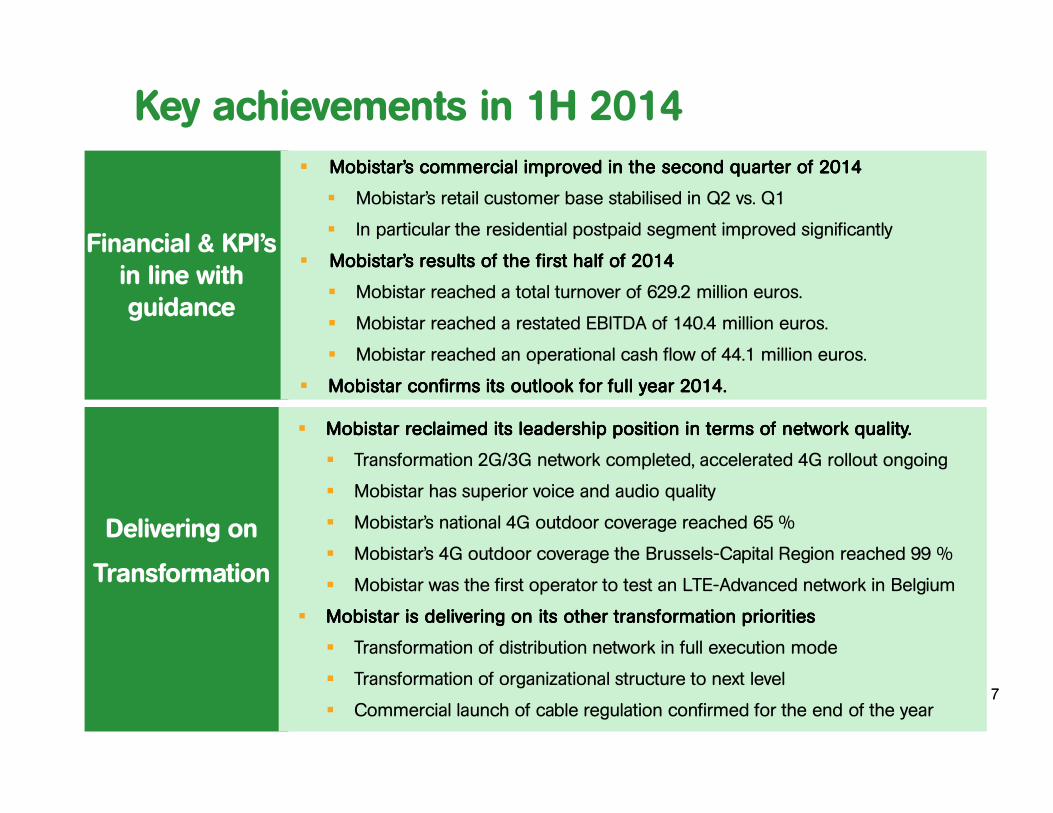

� Mobistar’s commercial improved in the second quarter of 2014Mobistar’s commercial improved in the second quarter of 2014Mobistar’s commercial improved in the second quarter of 2014Mobistar’s commercial improved in the second quarter of 2014

� Mobistar’s retail customer base stabilised in Q2 vs. Q1

� In particular the residential postpaid segment improved significantly

� Mobistar’s results of the first half of 2014 Mobistar’s results of the first half of 2014 Mobistar’s results of the first half of 2014 Mobistar’s results of the first half of 2014

� Mobistar reached a total turnover of 629.2 million euros.

� Mobistar reached a restated EBITDA of 140.4 million euros.

� Mobistar reached an operational cash flow of 44.1 million euros.

� Mobistar confirms its outlook for full year 2014.Mobistar confirms its outlook for full year 2014.Mobistar confirms its outlook for full year 2014.Mobistar confirms its outlook for full year 2014.

� Mobistar reclaimed its leadership position in terms of network quality.Mobistar reclaimed its leadership position in terms of network quality.Mobistar reclaimed its leadership position in terms of network quality.Mobistar reclaimed its leadership position in terms of network quality.

� Transformation 2G/3G network completed, accelerated 4G rollout ongoing

� Mobistar has superior voice and audio quality

� Mobistar’s national 4G outdoor coverage reached 65 %

� Mobistar’s 4G outdoor coverage the Brussels-Capital Region reached 99 %

� Mobistar was the first operator to test an LTE-Advanced network in Belgium

� Mobistar is delivering on its other transformation prioritiesMobistar is delivering on its other transformation prioritiesMobistar is delivering on its other transformation prioritiesMobistar is delivering on its other transformation priorities

� Transformation of distribution network in full execution mode

� Transformation of organizational structure to next level

� Commercial launch of cable regulation confirmed for the end of the year

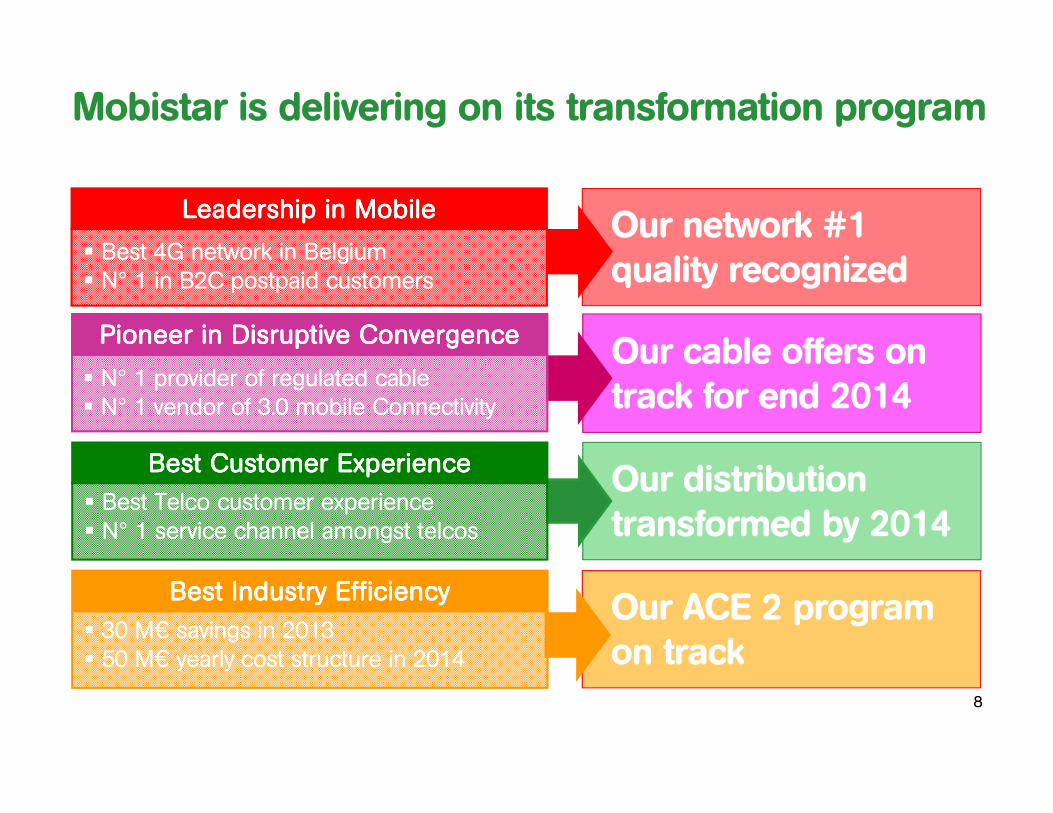

Key achievements in 1H 2014

7

Our distribution transformed by 2014

Our cable offers on track for end 2014

Our network #1 quality recognized

Leadership in MobileLeadership in MobileLeadership in MobileLeadership in Mobile

� Best 4G network in Belgium� N° 1 in B2C postpaid customers

Best Customer ExperienceBest Customer ExperienceBest Customer ExperienceBest Customer Experience

� Best Telco customer experience� N° 1 service channel amongst telcos

Pioneer in Disruptive ConvergencePioneer in Disruptive ConvergencePioneer in Disruptive ConvergencePioneer in Disruptive Convergence

� N° 1 provider of regulated cable� N° 1 vendor of 3.0 mobile Connectivity

Best Industry EfficiencyBest Industry EfficiencyBest Industry EfficiencyBest Industry Efficiency

� 30 M€ savings in 2013� 50 M€ yearly cost structure in 2014

Our ACE 2 program on track

Mobistar is delivering on its transformation program

8

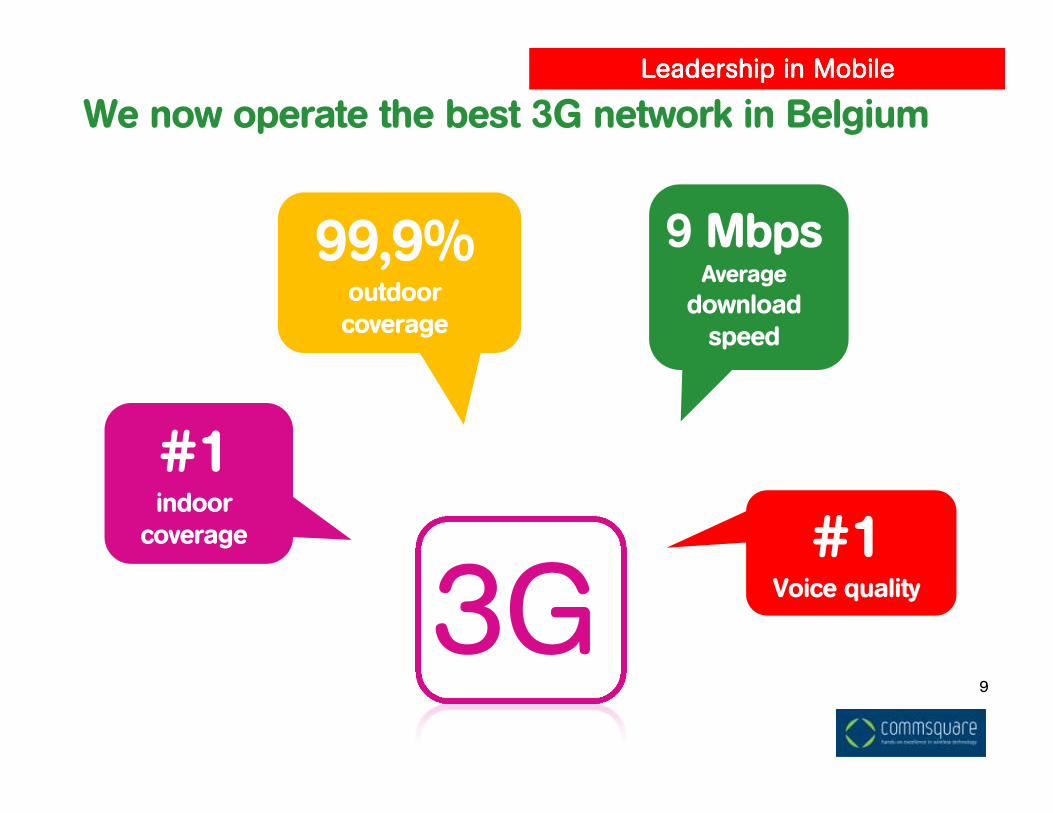

3G

99,9%outdoorcoverage

#1indoor

coverage

Leadership in MobileLeadership in MobileLeadership in MobileLeadership in Mobile

9 MbpsAverage

download speed

#1Voice quality

We now operate the best 3G network in Belgium

9

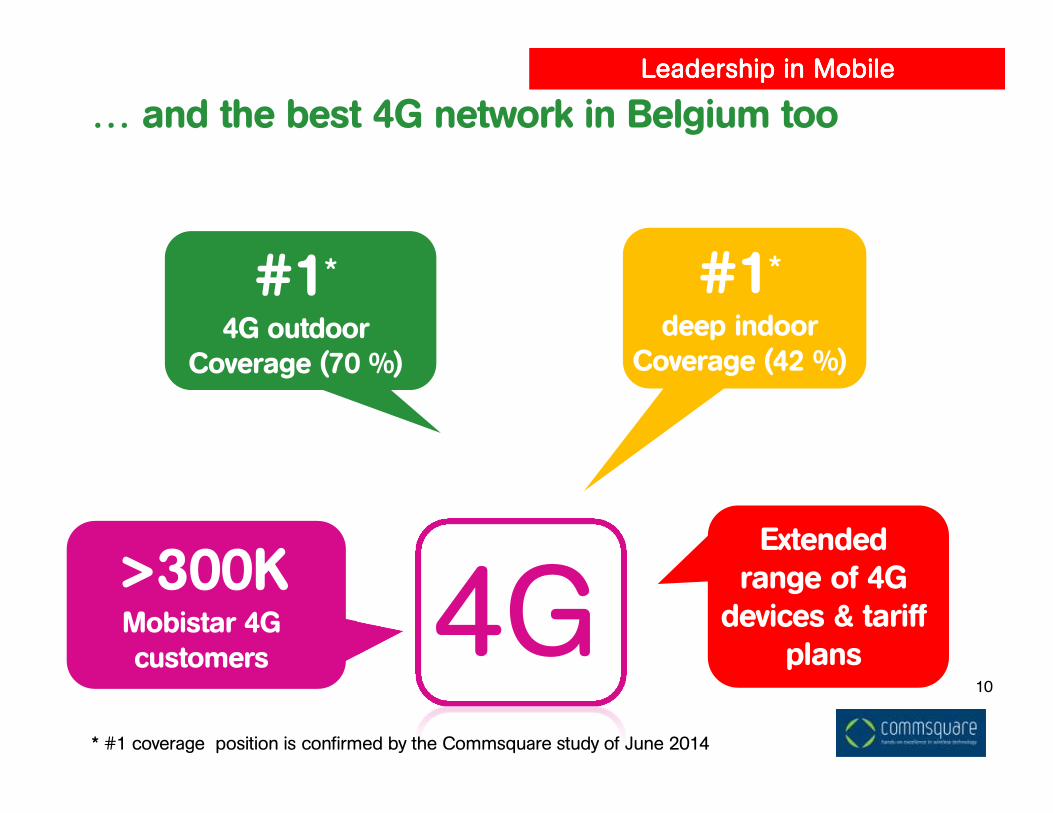

>300KMobistar 4G customers

#1*

4G outdoorCoverage (70 %)

4G

Leadership in MobileLeadership in MobileLeadership in MobileLeadership in Mobile

#1*

deep indoorCoverage (42 %)

… and the best 4G network in Belgium too

Extended range of 4G

devices & tariff plans

10

* #1 coverage position is confirmed by the Commsquare study of June 2014

4Gindoor

coverage =2G

indoor coverage

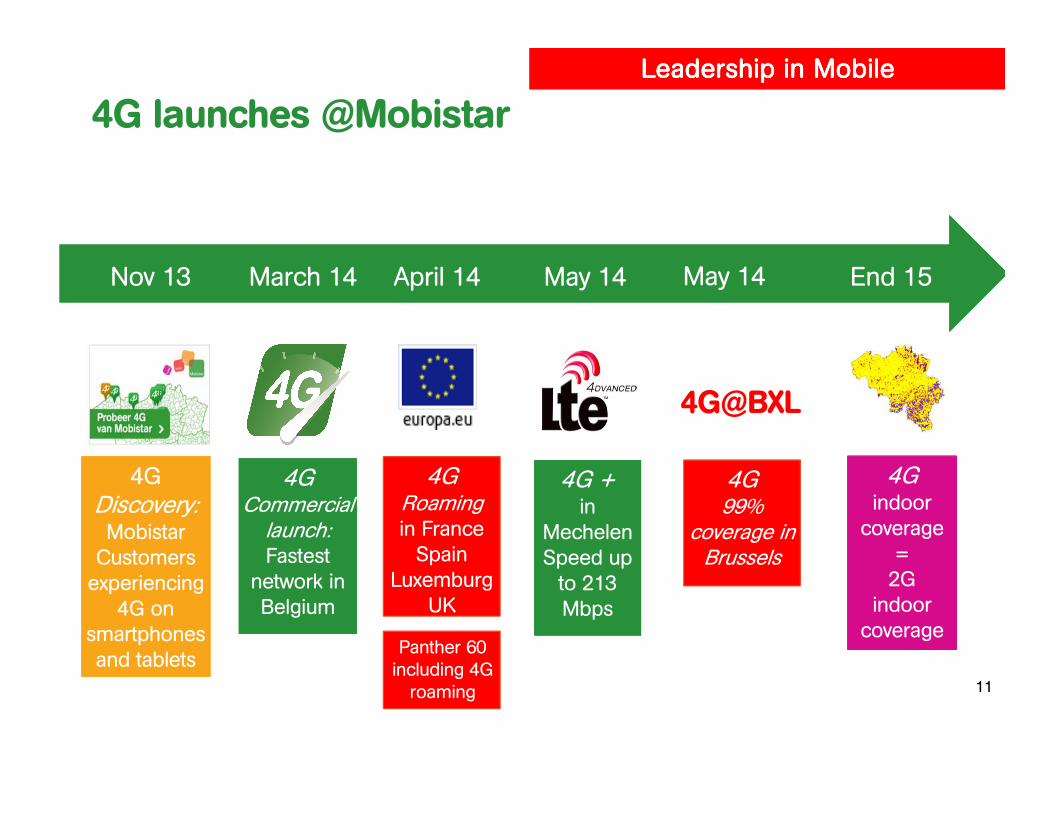

Nov 13

experiencing

smartphones

4G Discovery: MobistarCustomers experiencing

4G on smartphones and tablets

March 14 End 15

4GCommercial launch: Fastest

network in Belgium

4GCommercial launch: Fastest

network in Belgium

April 14

UK

4GRoaming in France Spain

LuxemburgUK

Panther 60 including 4G roaming

4G + in

MechelenSpeed up to 213 Mbps

4G + in

MechelenSpeed up to 213 Mbps

May 14

coverage in

4G99%

coverage in Brussels

May 14

4G@BXL

Leadership in MobileLeadership in MobileLeadership in MobileLeadership in Mobile

4G launches @Mobistar

11

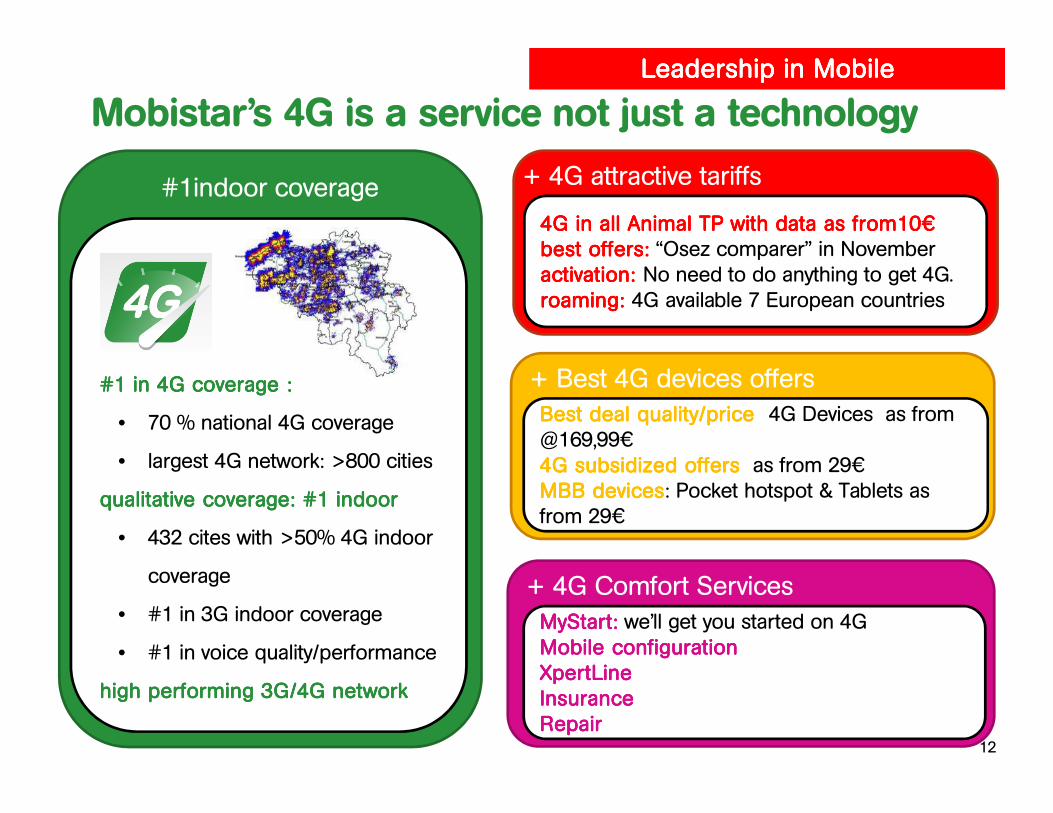

#1indoor coverage

#1 in 4G coverage : #1 in 4G coverage : #1 in 4G coverage : #1 in 4G coverage :

• 70 % national 4G coverage

• largest 4G network: >800 cities

qualitative coverage: #1 indoor qualitative coverage: #1 indoor qualitative coverage: #1 indoor qualitative coverage: #1 indoor

• 432 cites with >50% 4G indoor

coverage

• #1 in 3G indoor coverage

• #1 in voice quality/performance

high performing 3G/4G networkhigh performing 3G/4G networkhigh performing 3G/4G networkhigh performing 3G/4G network

Mobistar’s 4G is a service not just a technology

Leadership in MobileLeadership in MobileLeadership in MobileLeadership in Mobile

12

+ 4G attractive tariffs

4G in all Animal TP with data as from104G in all Animal TP with data as from104G in all Animal TP with data as from104G in all Animal TP with data as from10€€€€best offers:best offers:best offers:best offers: “Osez comparer” in Novemberactivation: activation: activation: activation: No need to do anything to get 4G.roaming: roaming: roaming: roaming: 4G available 7 European countries

+ Best 4G devices offers

Best deal quality/price Best deal quality/price Best deal quality/price Best deal quality/price 4G Devices as from @169,99€4G subsidized offers 4G subsidized offers 4G subsidized offers 4G subsidized offers as from 29€MBB devicesMBB devicesMBB devicesMBB devices: Pocket hotspot & Tablets as from 29€

+ 4G Comfort Services

MyStartMyStartMyStartMyStart:::: we’ll get you started on 4GMobile configurationMobile configurationMobile configurationMobile configurationXpertLineXpertLineXpertLineXpertLineInsuranceInsuranceInsuranceInsuranceRepairRepairRepairRepair

99% of Brussels population covered

96% of Brusselspopulation covered

56% of Brusselspopulation covered

Leadership in MobileLeadership in MobileLeadership in MobileLeadership in Mobile

1st to provide 99% 4G coverage in Brussels

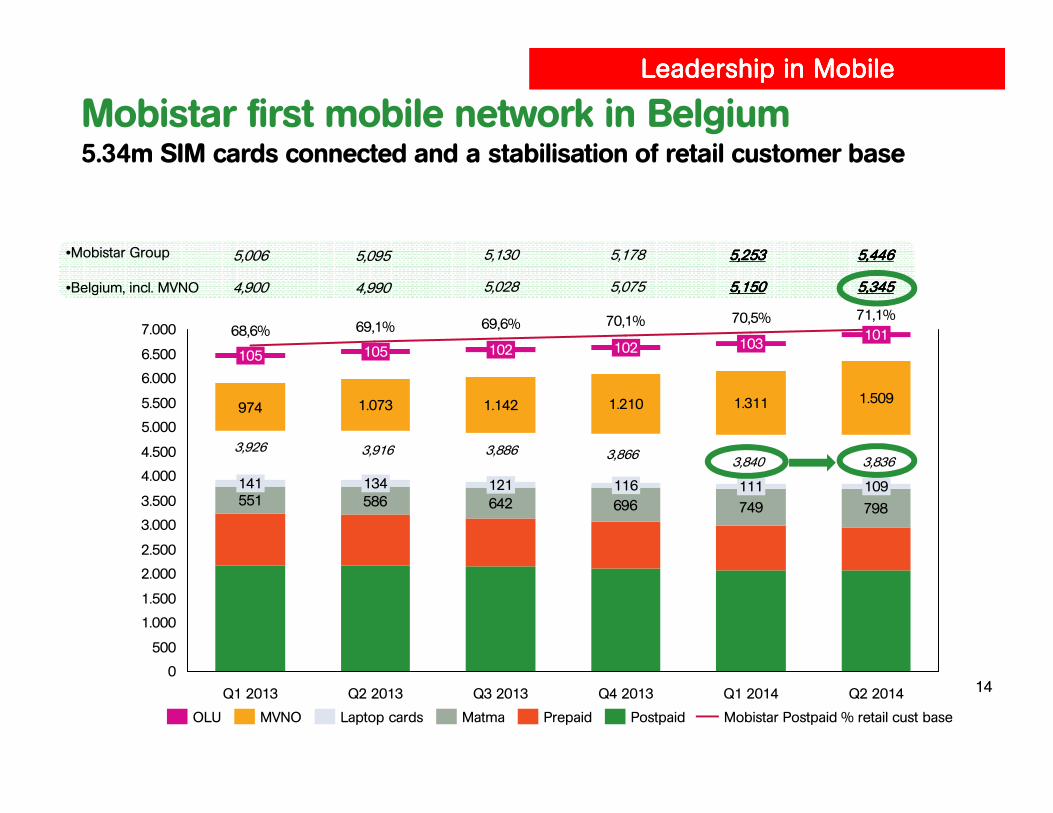

551 586 642 696 749 798

974

4.500

7.000

6.500

4.000

3.500

3.000

6.000

5.500

5.000

2.500

2.000

1.500

1.000

500

0

Q1 2014

70,5%

111

1.311

103

Q4 2013

70,1%

116

1.210

102

Q3 2013

69,6%

121

1.142

102

Q2 2013

69,1%

134

1.073

105

Q1 2013

68,6%

141

105

Q2 2014

109

1.509

101

71,1%

3,926 3,916

5,006 5,095 5,130

3,886

Prepaid Mobistar Postpaid % retail cust baseMatmaLaptop cardsMVNOOLU Postpaid

5,178

3,866

5,2535,2535,2535,253

3,840

14

•Mobistar Group

•Belgium, incl. MVNO 4,900 4,990 5,028 5,075 5,1505,1505,1505,150

3,836

5,4465,4465,4465,446

5,3455,3455,3455,345

Mobistar first mobile network in Belgium5.34m SIM cards connected and a stabilisation of retail customer base

Leadership in MobileLeadership in MobileLeadership in MobileLeadership in Mobile

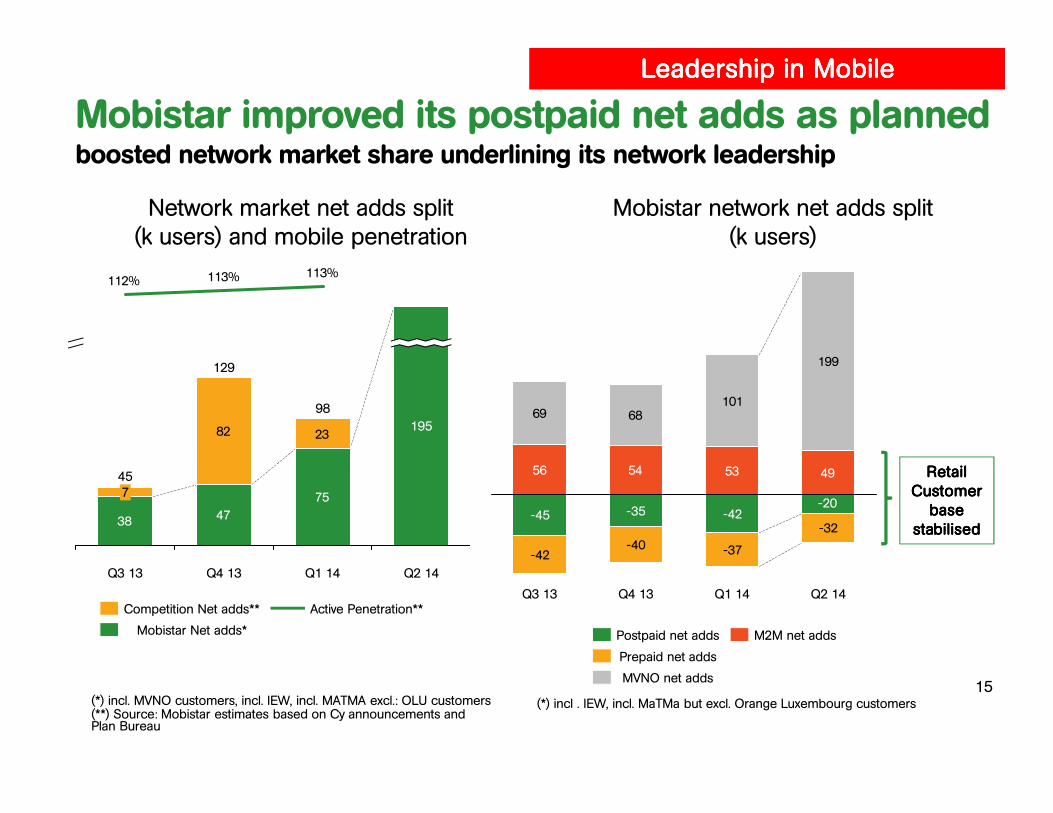

Mobistar improved its postpaid net adds as plannedboosted network market share underlining its network leadership

15

38 47

75

82 23

113%113%112%

Q2 14

195

Q1 14

98

Q4 13

129

Q3 13

457

Active Penetration**

Mobistar Net adds*

Competition Net adds**

-45 -35 -42

-42-40

-32

56 54 49

69 68101

199

-20

-37

53

Q1 14 Q2 14Q4 13Q3 13

M2M net adds

MVNO net adds

Prepaid net adds

Postpaid net adds

(*) incl. MVNO customers, incl. IEW, incl. MATMA excl.: OLU customers(**) Source: Mobistar estimates based on Cy announcements and Plan Bureau

(*) incl . IEW, incl. MaTMa but excl. Orange Luxembourg customers

Network market net adds split(k users) and mobile penetration

Mobistar network net adds split(k users)

Retail Retail Retail Retail Customer Customer Customer Customer

base base base base stabilisedstabilisedstabilisedstabilised

Leadership in MobileLeadership in MobileLeadership in MobileLeadership in Mobile

Panther 60 for international commuterspreempting change in European roaming

• 5% of Postpaid activations after a few weeks

• exclusive 4G roaming included in 7 EU-countries

Leadership in MobileLeadership in MobileLeadership in MobileLeadership in Mobile

16

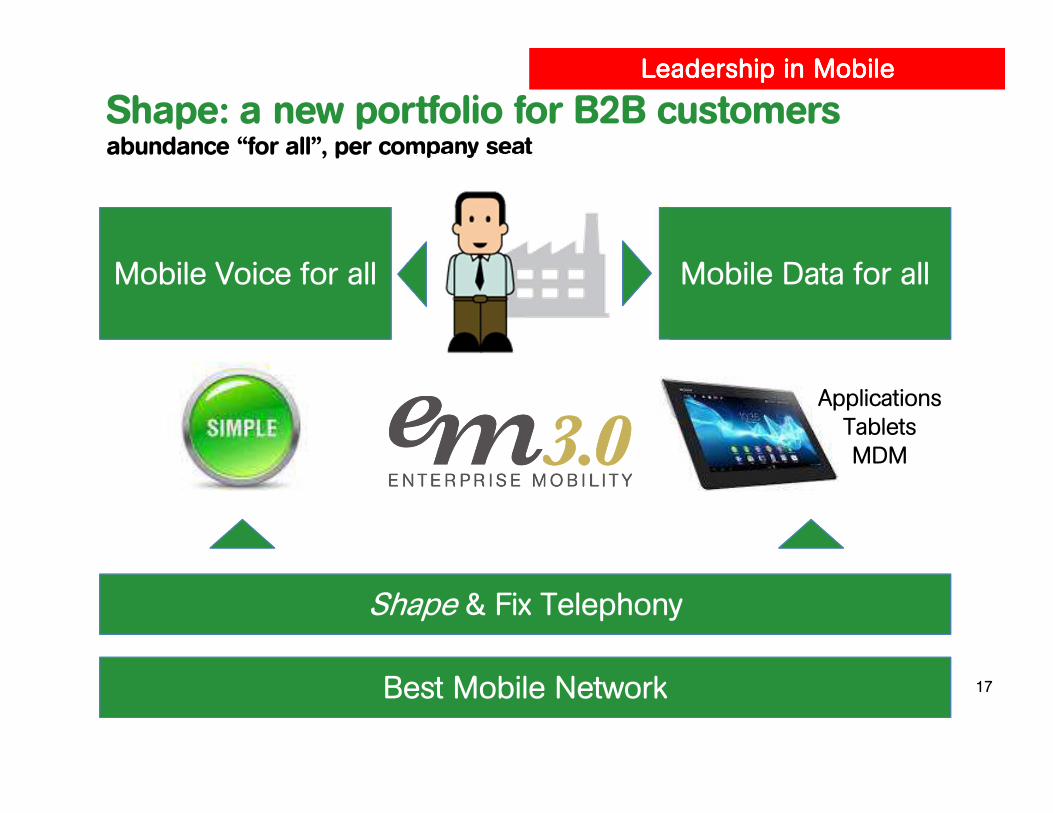

Shape & Fix Telephony

Best Mobile Network

Leadership in MobileLeadership in MobileLeadership in MobileLeadership in Mobile

Shape: a new portfolio for B2B customersabundance “for all”, per company seat

Mobile Voice for all Mobile Data for all

ApplicationsTabletsMDM

17

Have a nice day:our customers are special, let’s surprise them!

Best Customer ExperienceBest Customer ExperienceBest Customer ExperienceBest Customer Experience

18

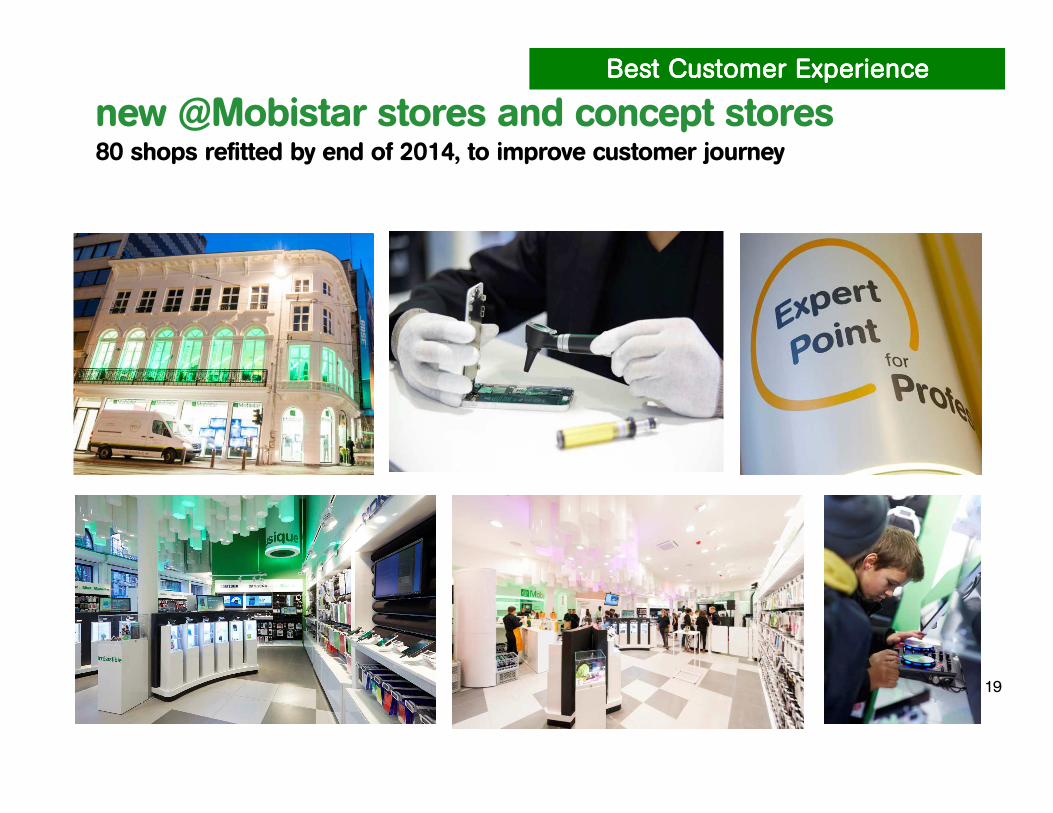

new @Mobistar stores and concept stores80 shops refitted by end of 2014, to improve customer journey

Best Customer ExperienceBest Customer ExperienceBest Customer ExperienceBest Customer Experience

19

.be

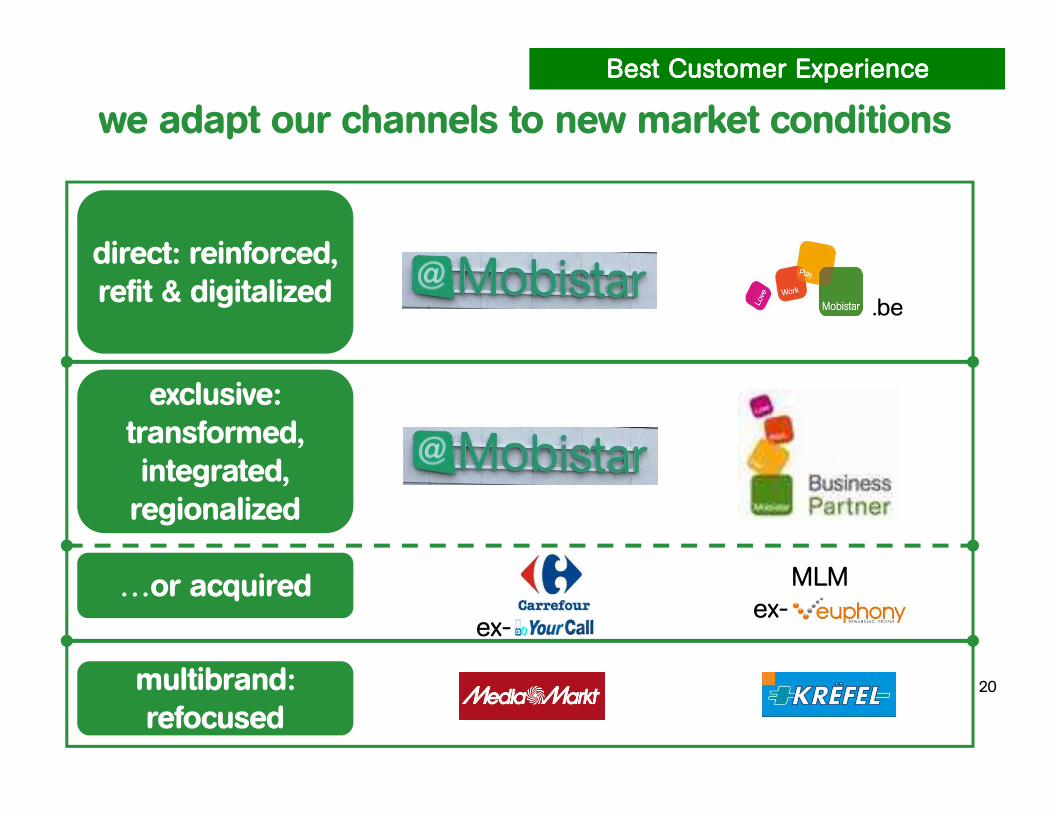

direct: reinforced, refit & digitalized

exclusive: transformed, integrated, regionalized

multibrand: refocused

MLMex-

we adapt our channels to new market conditions

ex-

…or acquired

Best Customer ExperienceBest Customer ExperienceBest Customer ExperienceBest Customer Experience

20

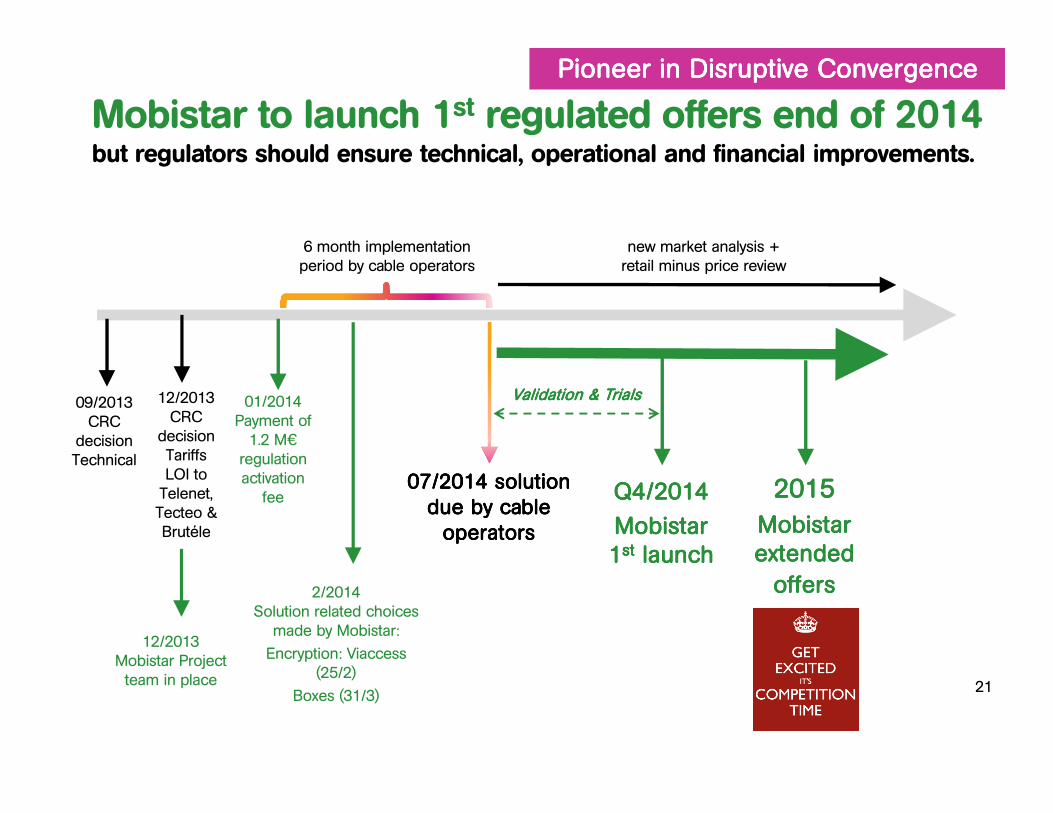

6 month implementation period by cable operators

09/2013CRC

decisionTechnical

07/2014 solution 07/2014 solution 07/2014 solution 07/2014 solution due by cable due by cable due by cable due by cable operatorsoperatorsoperatorsoperators

12/2013CRC

decisionTariffs LOI to Telenet, Tecteo & Brutéle

Q4/2014Q4/2014Q4/2014Q4/2014

MobistarMobistarMobistarMobistar1111stststst launchlaunchlaunchlaunch

12/2013Mobistar Projectteam in place

2/2014Solution related choices

made by Mobistar:

Encryption: Viaccess (25/2)

Boxes (31/3)

01/2014Payment of 1.2 M€

regulation activation

fee

Mobistar to launch 1st regulated offers end of 2014but regulators should ensure technical, operational and financial improvements.

Pioneer in Disruptive ConvergencePioneer in Disruptive ConvergencePioneer in Disruptive ConvergencePioneer in Disruptive Convergence

2015201520152015

Mobistar Mobistar Mobistar Mobistar extendedextendedextendedextended

offers offers offers offers

Validation & TrialsValidation & TrialsValidation & TrialsValidation & Trials

new market analysis + retail minus price review

21

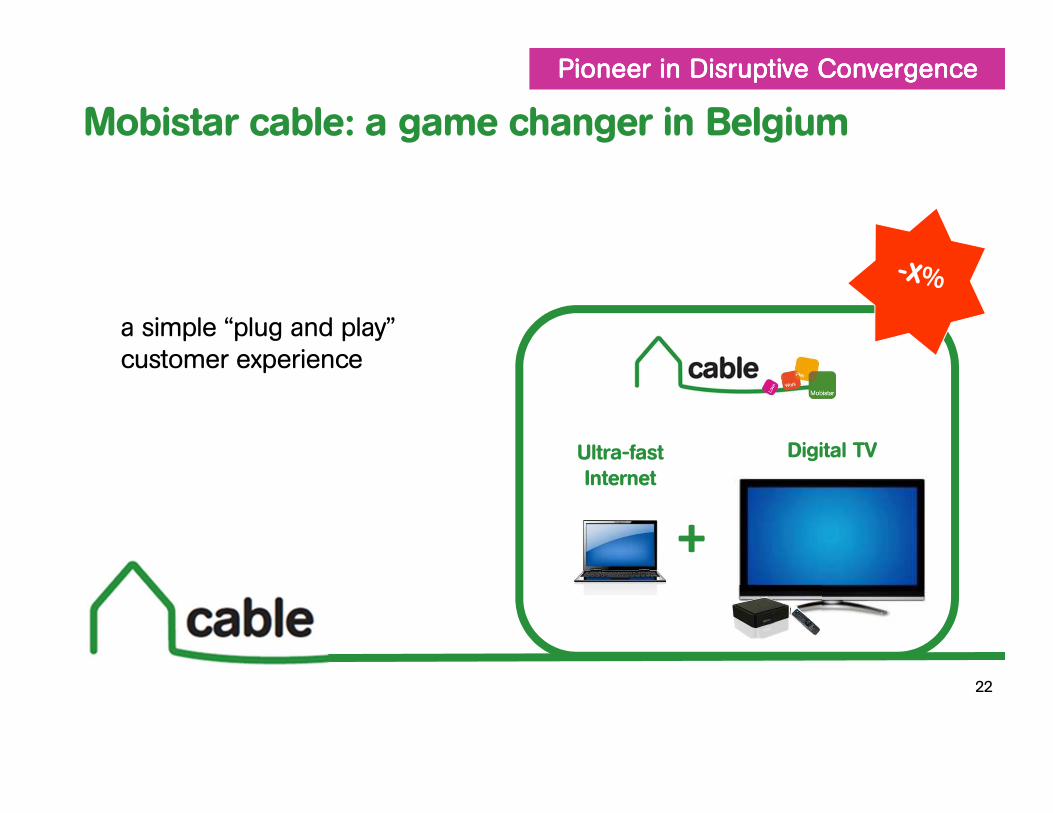

Mobistar cable: a game changer in Belgium

Pioneer in Disruptive ConvergencePioneer in Disruptive ConvergencePioneer in Disruptive ConvergencePioneer in Disruptive Convergence

a simple “plug and play”customer experience

Ultra-fast Internet

Digital TV

+

22

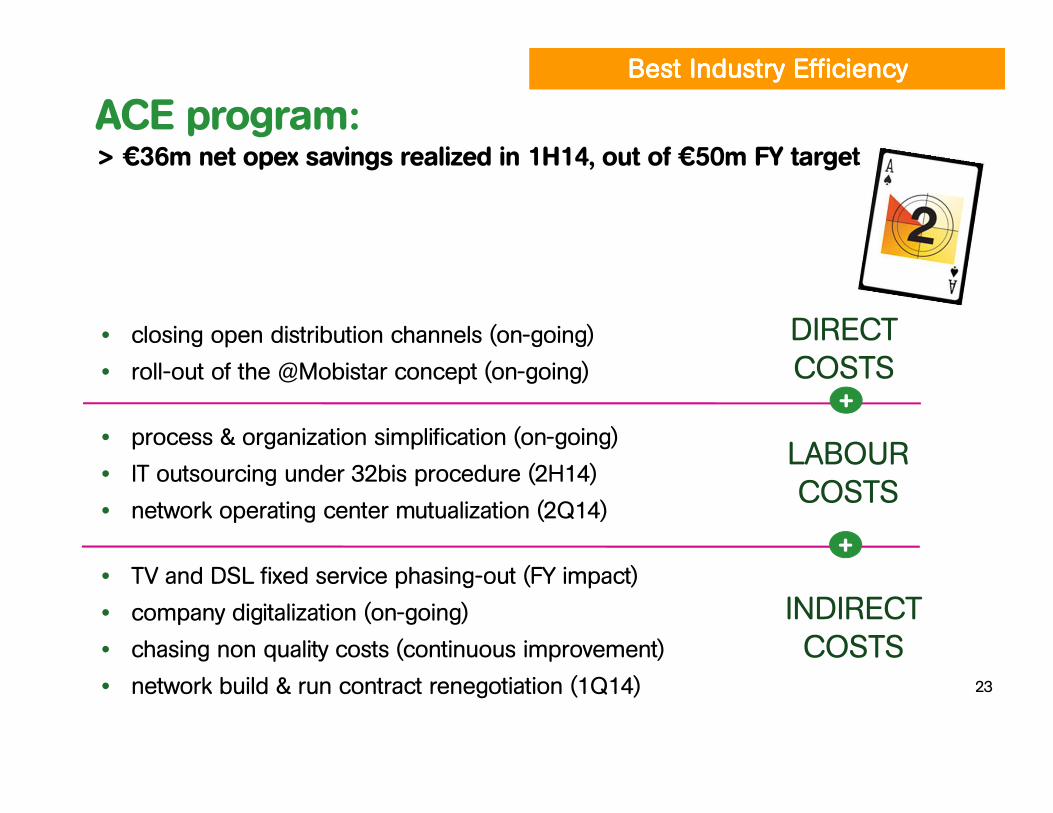

Best Industry EfficiencyBest Industry EfficiencyBest Industry EfficiencyBest Industry Efficiency

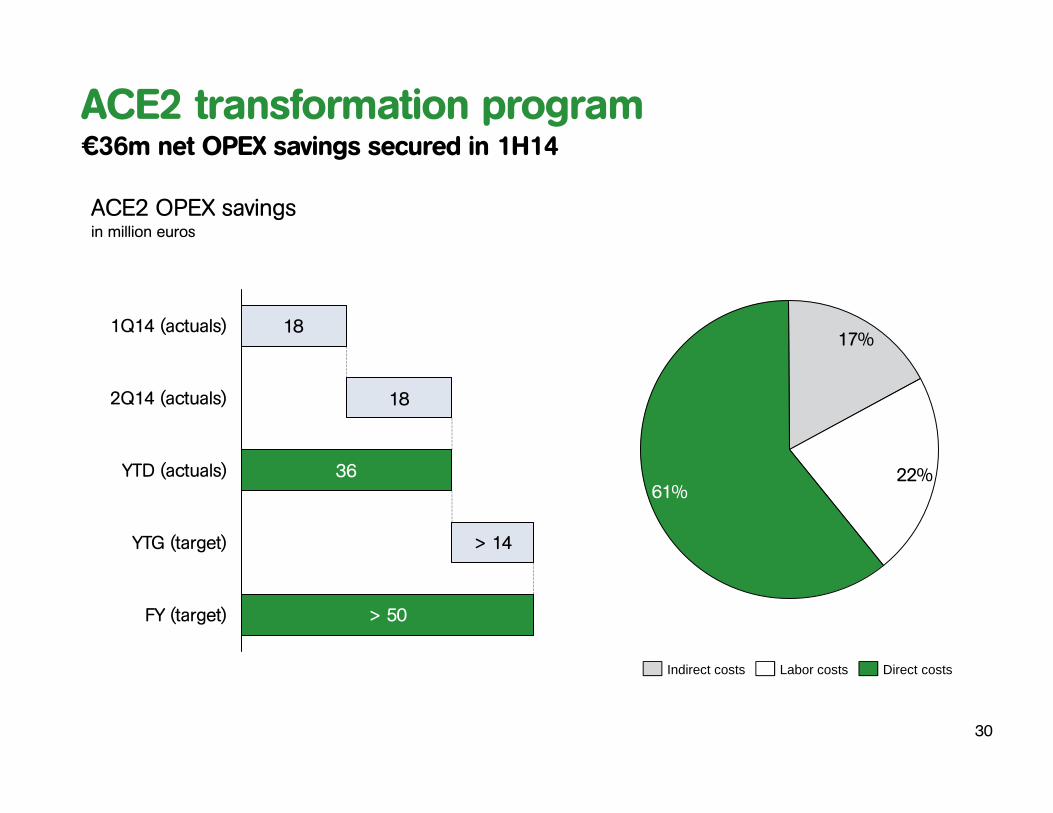

ACE program:> €36m net opex savings realized in 1H14, out of €50m FY target

• closing open distribution channels (on-going)

• roll-out of the @Mobistar concept (on-going)

• process & organization simplification (on-going)

• IT outsourcing under 32bis procedure (2H14)

• network operating center mutualization (2Q14)

• TV and DSL fixed service phasing-out (FY impact)

• company digitalization (on-going)

• chasing non quality costs (continuous improvement)

• network build & run contract renegotiation (1Q14)

DIRECTCOSTS

LABOURCOSTS

INDIRECTCOSTS

+

+

23

‘We will carry on our determined work to

fundamentally transform this company and its cost

structure’

Financial Review Ludovic Pech

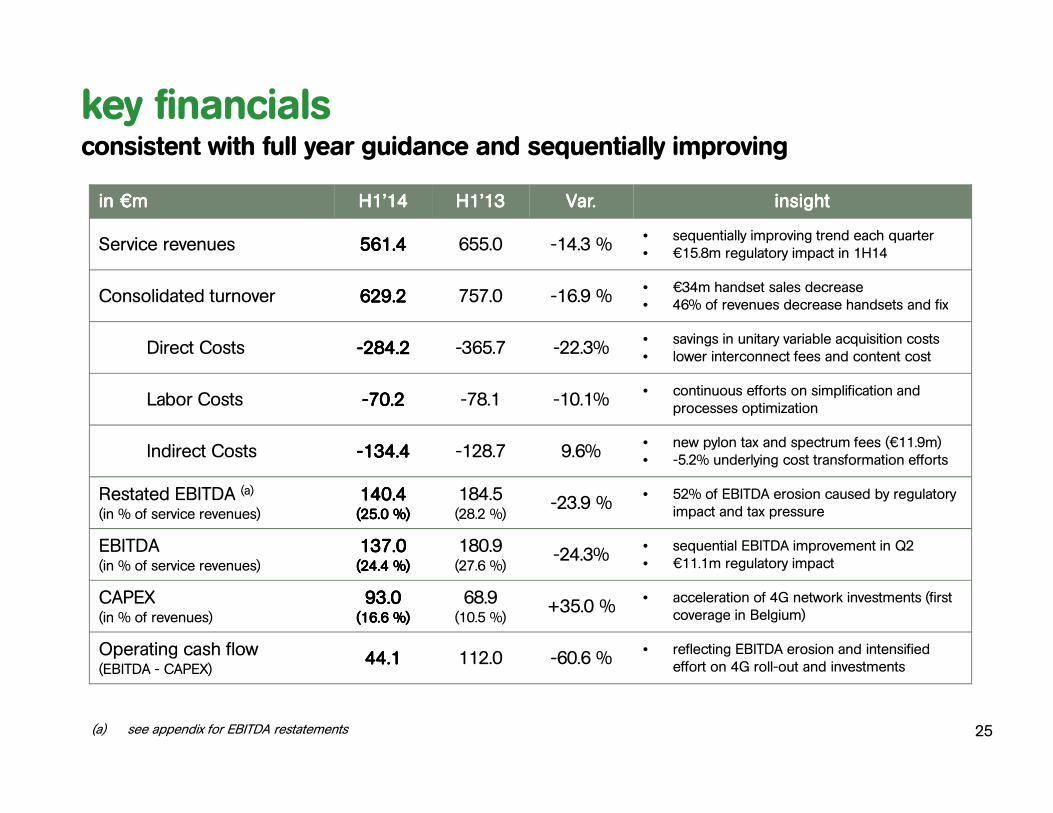

in in in in €€€€mmmm H1’14H1’14H1’14H1’14 H1’13H1’13H1’13H1’13 Var.Var.Var.Var. insightinsightinsightinsight

Service revenues 561.4561.4561.4561.4 655.0 -14.3 %• sequentially improving trend each quarter• €15.8m regulatory impact in 1H14

Consolidated turnover 629.2629.2629.2629.2 757.0 -16.9 %• €34m handset sales decrease• 46% of revenues decrease handsets and fix

Direct Costs ----284.2284.2284.2284.2 -365.7 -22.3%• savings in unitary variable acquisition costs • lower interconnect fees and content cost

Labor Costs ----70.270.270.270.2 -78.1 -10.1%• continuous efforts on simplification and

processes optimization

Indirect Costs ----134.4134.4134.4134.4 -128.7 9.6%• new pylon tax and spectrum fees (€11.9m)• -5.2% underlying cost transformation efforts

Restated EBITDA (a)

(in % of service revenues)

140.4140.4140.4140.4(25.0 %)(25.0 %)(25.0 %)(25.0 %)

184.5(28.2 %)

-23.9 %• 52% of EBITDA erosion caused by regulatory

impact and tax pressure

EBITDA (in % of service revenues)

137.0137.0137.0137.0(24.4 %)(24.4 %)(24.4 %)(24.4 %)

180.9(27.6 %)

-24.3%• sequential EBITDA improvement in Q2• €11.1m regulatory impact

CAPEX(in % of revenues)

93.093.093.093.0(16.6 %)(16.6 %)(16.6 %)(16.6 %)

68.9(10.5 %)

+35.0 %• acceleration of 4G network investments (first

coverage in Belgium)

Operating cash flow(EBITDA - CAPEX)

44.144.144.144.1 112.0 -60.6 %• reflecting EBITDA erosion and intensified

effort on 4G roll-out and investments

key financialsconsistent with full year guidance and sequentially improving

(a) see appendix for EBITDA restatements 25

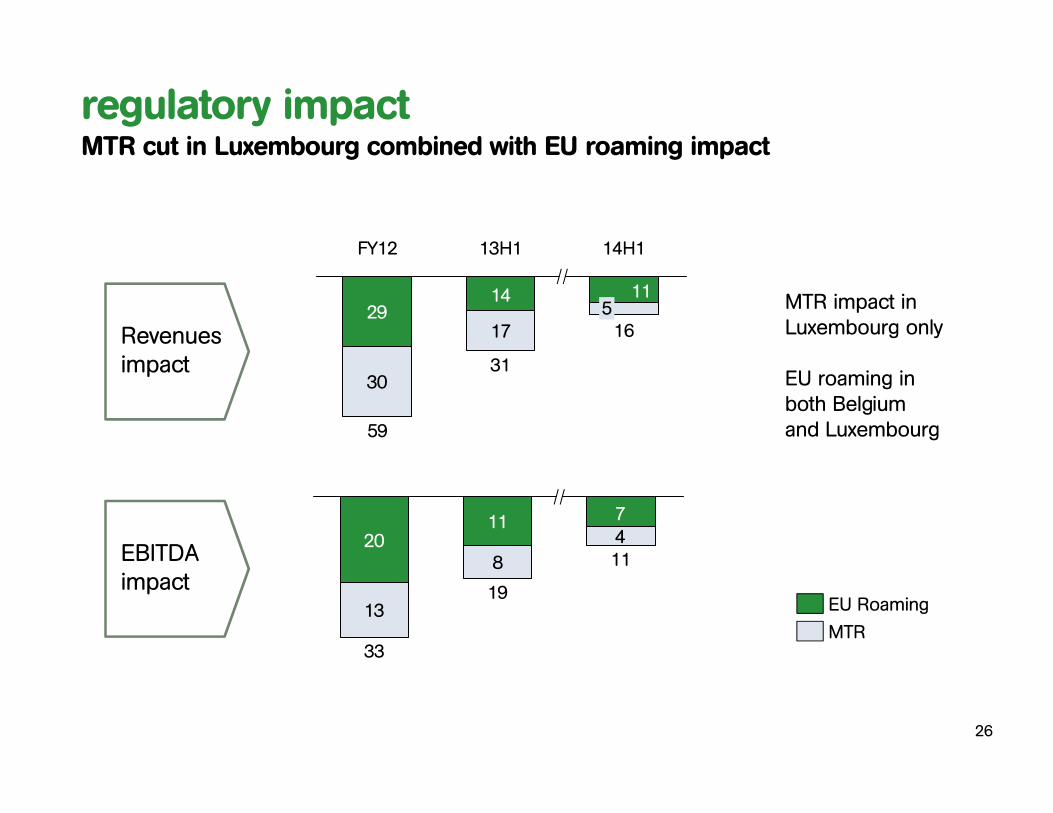

Revenuesimpact

EBITDAimpact

29

30

17

1114

13H1 14H1

16

31

59

5

FY12

2011

13

8

47

33

11

19

MTR

EU Roaming

regulatory impactMTR cut in Luxembourg combined with EU roaming impact

MTR impact in Luxembourg only

EU roaming in both Belgium and Luxembourg

26

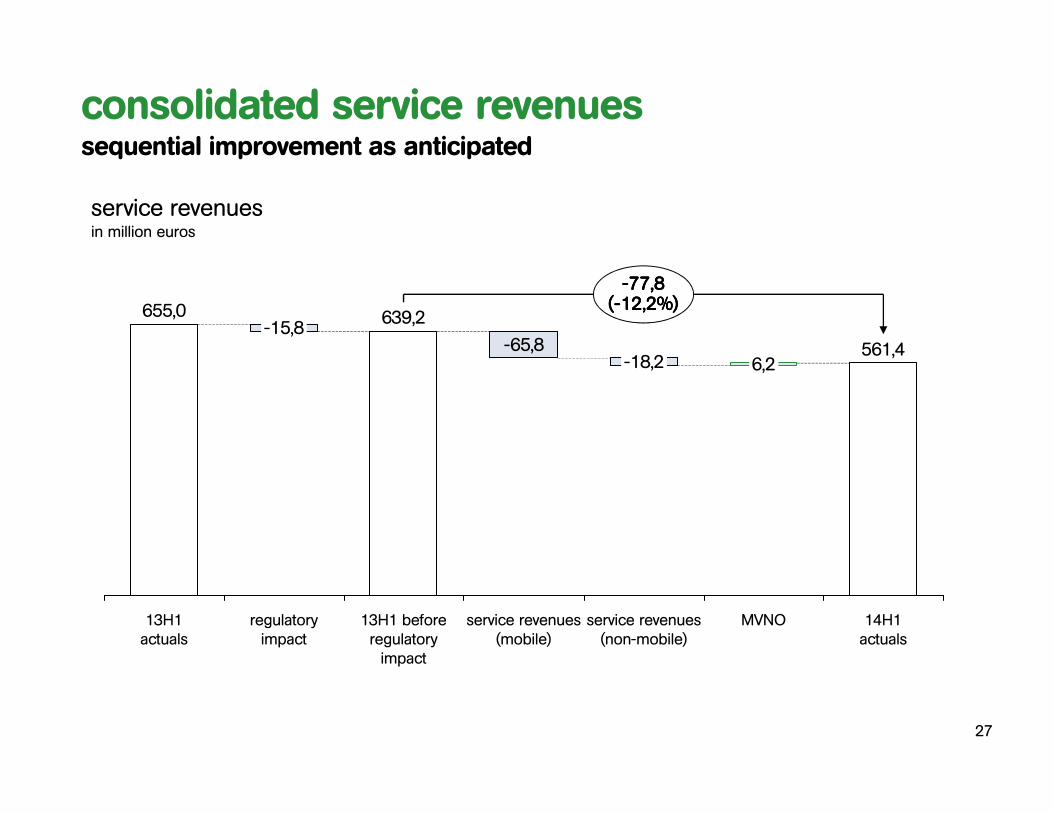

655,0

561,4

----77,877,877,877,8((((----12,2%12,2%12,2%12,2%))))

14H1actuals

-18,2

MVNO

6,2

service revenues (non-mobile)

-65,8

service revenues (mobile)

13H1 beforeregulatory impact

639,2

regulatory impact

-15,8

13H1actuals

service revenuesin million euros

consolidated service revenuessequential improvement as anticipated

27

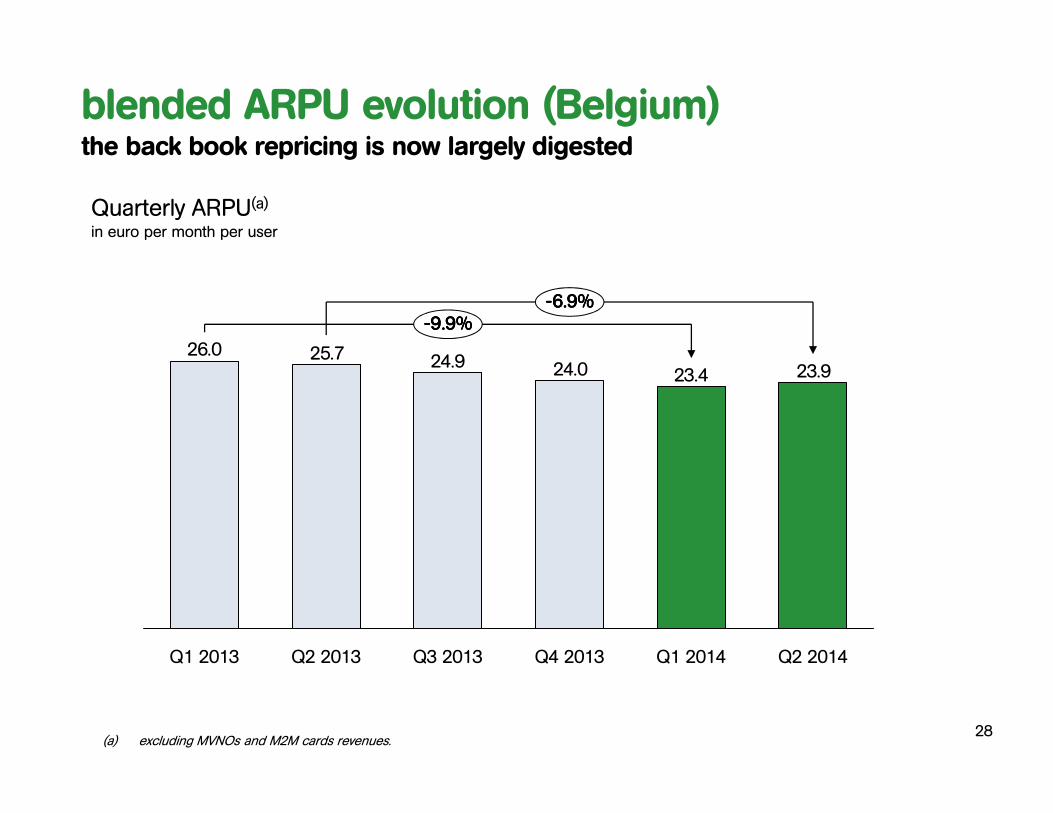

23.923.424.024.925.726.0

----9.9%9.9%9.9%9.9%----6.9%6.9%6.9%6.9%

Q2 2014Q1 2014Q4 2013Q1 2013 Q3 2013Q2 2013

(a) excluding MVNOs and M2M cards revenues.

blended ARPU evolution (Belgium)the back book repricing is now largely digested

28

Quarterly ARPU(a)

in euro per month per user

(a) see appendix for EBITDA restatements and one-offs 29

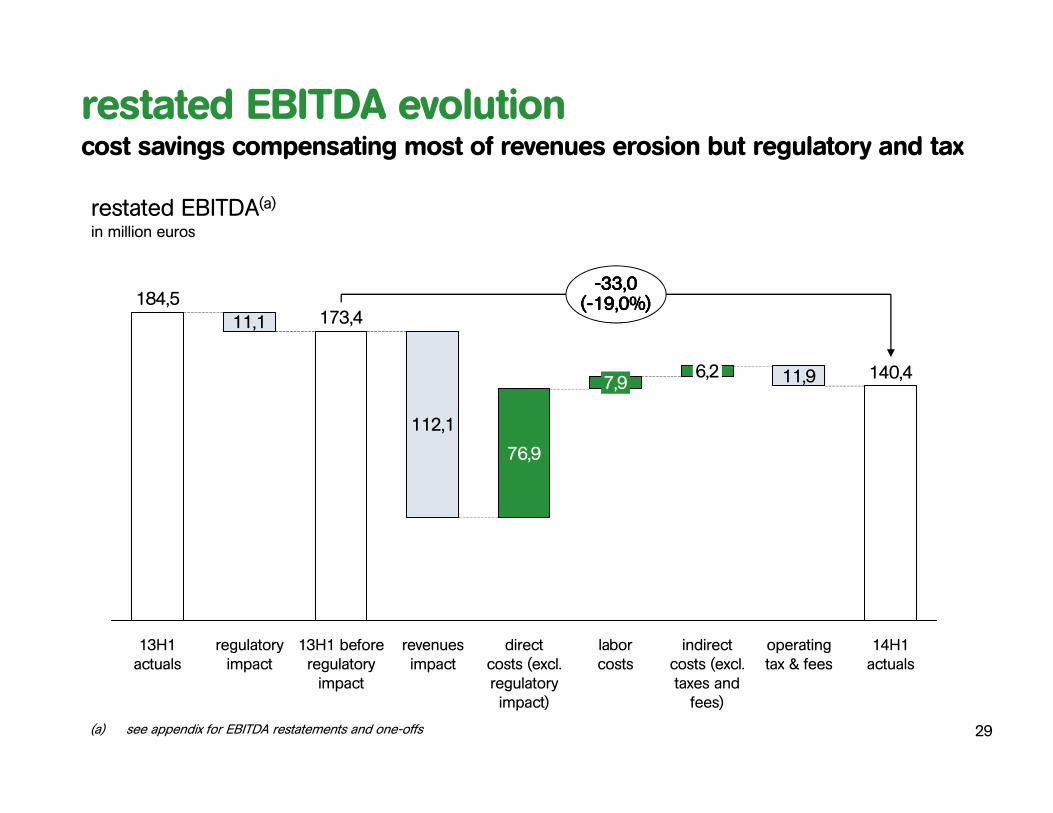

restated EBITDA evolutioncost savings compensating most of revenues erosion but regulatory and tax

----33,033,033,033,0((((----19,0%19,0%19,0%19,0%))))

14H1actuals

140,4

operating tax & fees

11,9

indirect costs (excl. taxes and fees)

6,2

laborcosts

7,9

direct costs (excl. regulatory impact)

76,9

revenues impact

112,1

13H1 before regulatory impact

173,4

regulatory impact

11,1

13H1actuals

184,5

restated EBITDA(a)in million euros

30

ACE2 transformation program€36m net OPEX savings secured in 1H14

ACE2 OPEX savingsin million euros

18

18

36

> 14

> 50FY (target)

YTD (actuals)

1Q14 (actuals)

2Q14 (actuals)

YTG (target)

22%61%

17%

Labor costsIndirect costs Direct costs

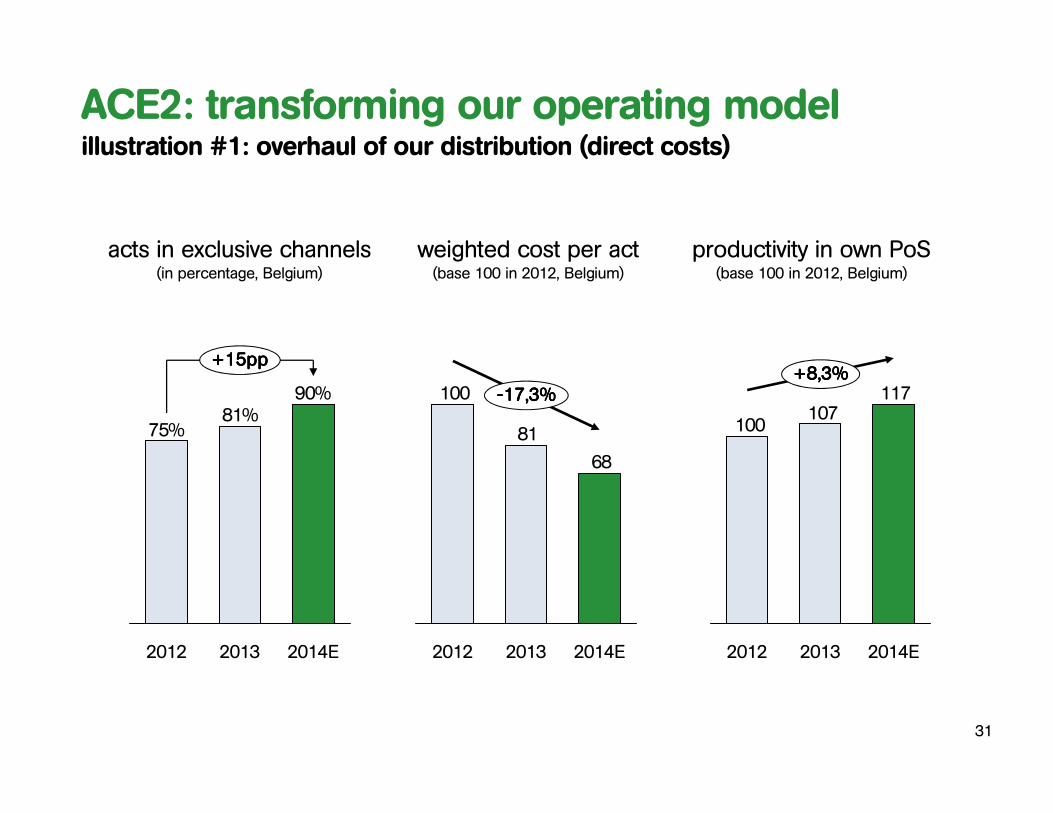

90%81%

75%

+15+15+15+15pppppppp

20132012 2014E

acts in exclusive channels(in percentage, Belgium)

productivity in own PoS(base 100 in 2012, Belgium)

weighted cost per act(base 100 in 2012, Belgium)

ACE2: transforming our operating modelillustration #1: overhaul of our distribution (direct costs)

31

68

81

100

2014E2013

----17,3%17,3%17,3%17,3%

2012

117107

100

2014E2013

+8,3%+8,3%+8,3%+8,3%

2012

billing costs(in euros, Belgium)

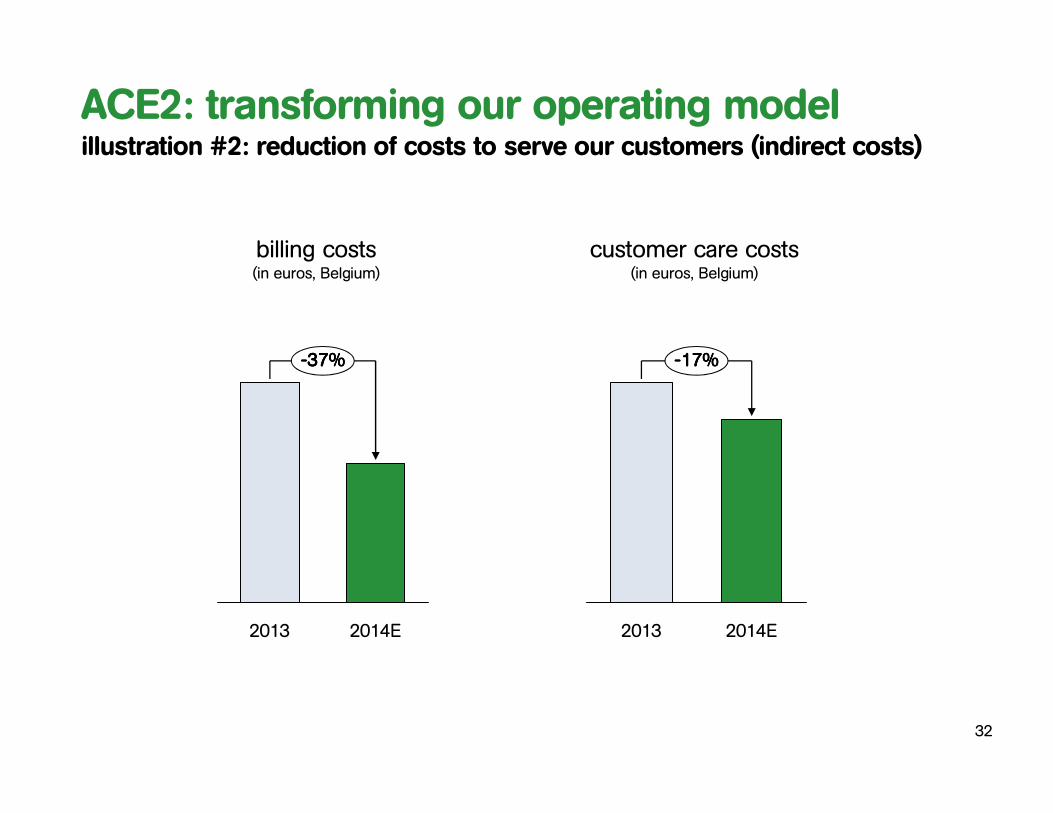

ACE2: transforming our operating modelillustration #2: reduction of costs to serve our customers (indirect costs)

32

2013 2014E

----37%37%37%37%

2013 2014E

----17%17%17%17%

customer care costs(in euros, Belgium)

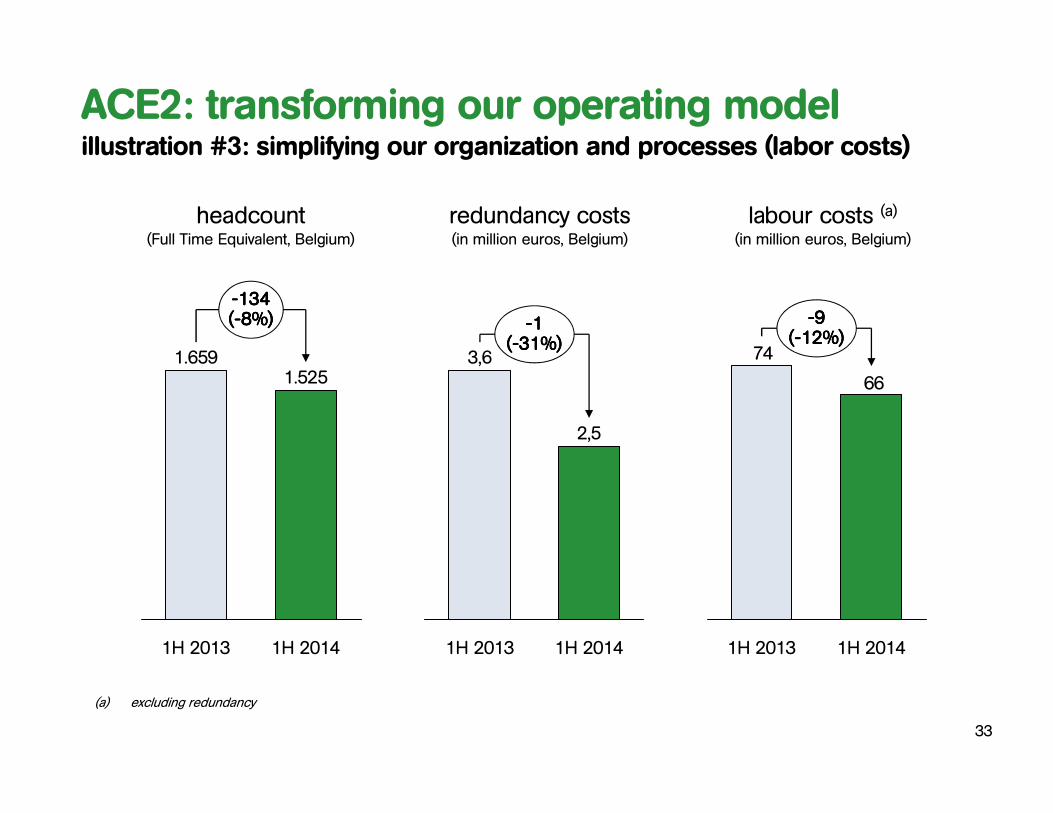

----134134134134((((----8%8%8%8%))))

1H 2014

1.659

1H 2013

1.525

headcount(Full Time Equivalent, Belgium)

labour costs (a)(in million euros, Belgium)

redundancy costs(in million euros, Belgium)

----1111((((----31%31%31%31%))))

1H 20141H 2013

2,5

3,6

ACE2: transforming our operating modelillustration #3: simplifying our organization and processes (labor costs)

(a) excluding redundancy

66

74

1H 2014

----9999((((----12%12%12%12%))))

1H 2013

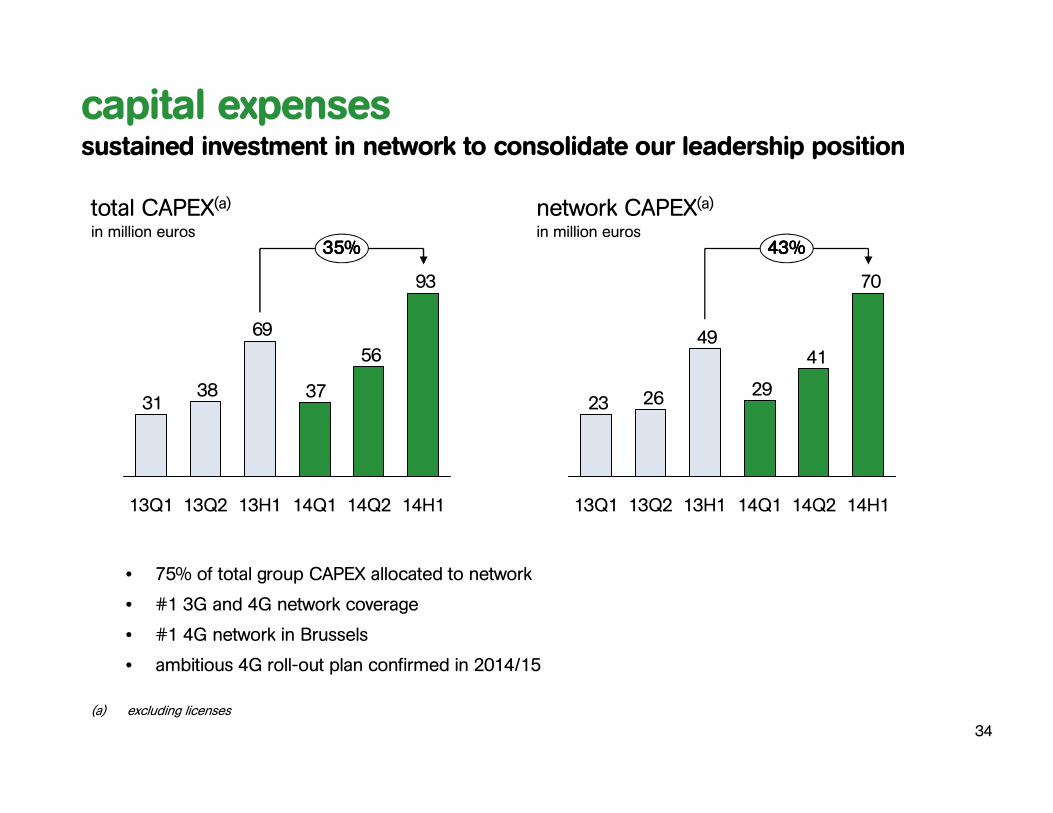

33

93

56

37

69

3831

35%35%35%35%

14Q214Q113H113Q213Q1 14H1

70

41

29

49

2623

14H114Q214Q113H113Q213Q1

43%43%43%43%

capital expensessustained investment in network to consolidate our leadership position

(a) excluding licenses

• 75% of total group CAPEX allocated to network

• #1 3G and 4G network coverage

• #1 4G network in Brussels

• ambitious 4G roll-out plan confirmed in 2014/15

34

total CAPEX(a)in million euros

network CAPEX(a)in million euros

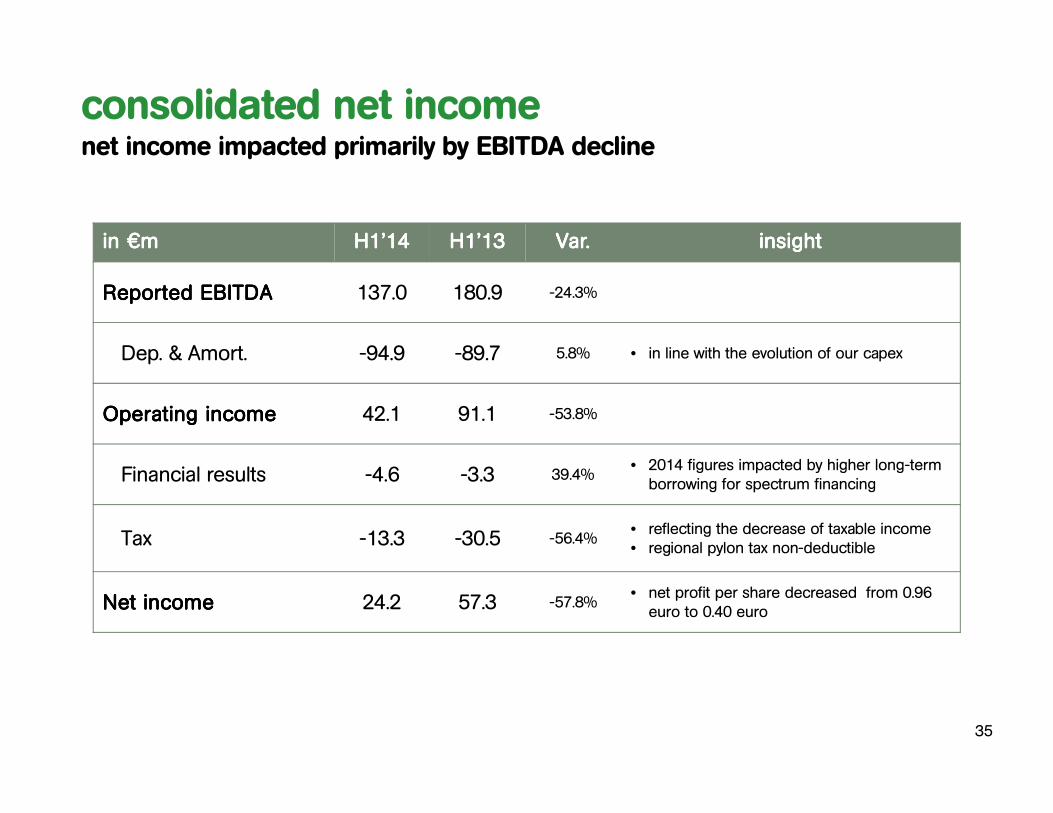

consolidated net incomenet income impacted primarily by EBITDA decline

in in in in €€€€mmmm H1’14H1’14H1’14H1’14 H1’13H1’13H1’13H1’13 Var.Var.Var.Var. insightinsightinsightinsight

Reported EBITDAReported EBITDAReported EBITDAReported EBITDA 137.0 180.9 -24.3%

Dep. & Amort. -94.9 -89.7 5.8% • in line with the evolution of our capex

Operating incomeOperating incomeOperating incomeOperating income 42.1 91.1 -53.8%

Financial results -4.6 -3.3 39.4%• 2014 figures impacted by higher long-term

borrowing for spectrum financing

Tax -13.3 -30.5 -56.4%• reflecting the decrease of taxable income• regional pylon tax non-deductible

Net incomeNet incomeNet incomeNet income 24.2 57.3 -57.8%• net profit per share decreased from 0.96

euro to 0.40 euro

35

in in in in €€€€mmmm H1’14H1’14H1’14H1’14 H1’13H1’13H1’13H1’13 Var.Var.Var.Var. insightinsightinsightinsight

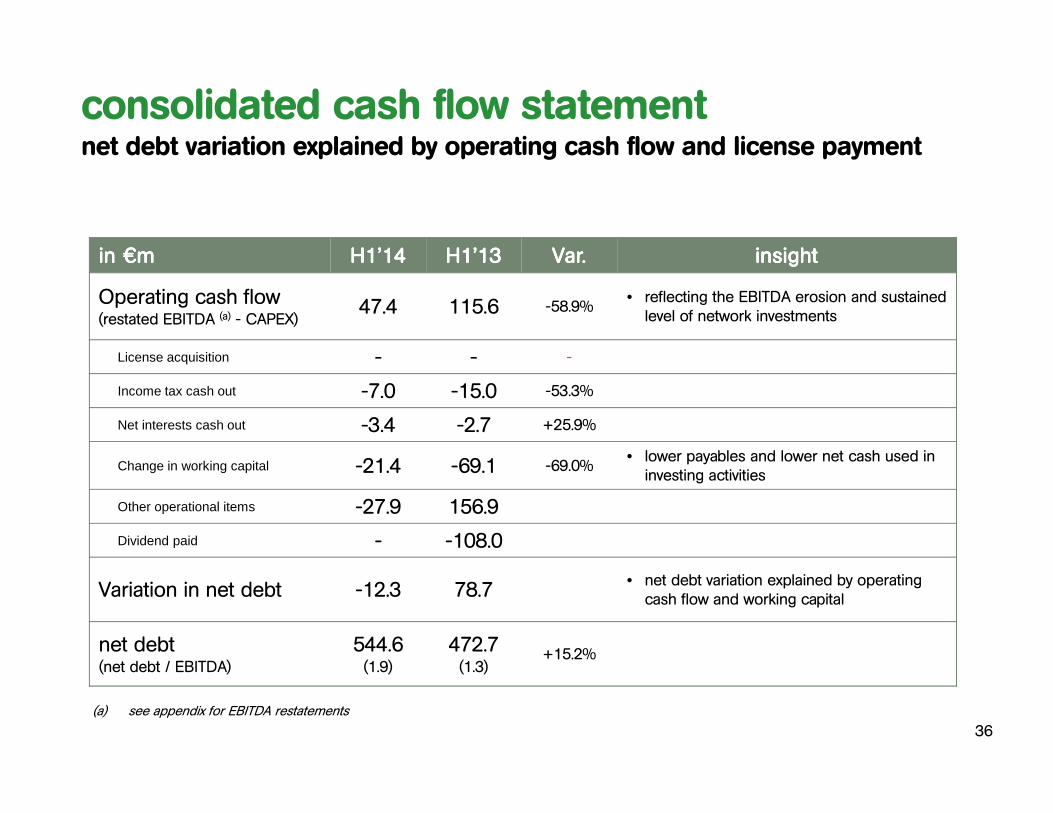

Operating cash flow(restated EBITDA (a) - CAPEX)

47.4 115.6 -58.9%• reflecting the EBITDA erosion and sustained

level of network investments

License acquisition - - -

Income tax cash out -7.0 -15.0 -53.3%

Net interests cash out -3.4 -2.7 +25.9%

Change in working capital -21.4 -69.1 -69.0%• lower payables and lower net cash used in

investing activities

Other operational items -27.9 156.9

Dividend paid - -108.0

Variation in net debt -12.3 78.7• net debt variation explained by operating

cash flow and working capital

net debt(net debt / EBITDA)

544.6(1.9)

472.7(1.3)

+15.2%

(a) see appendix for EBITDA restatements

consolidated cash flow statementnet debt variation explained by operating cash flow and license payment

36

‘The results of the first half of 2014 enabled Mobistar to confirm its outlook as provided in

February 2014’

Financial OutlookJean-Marc Harion

• Before any impact related to the cable opportunity• Operational cash flow = EBITDA – Net Investments

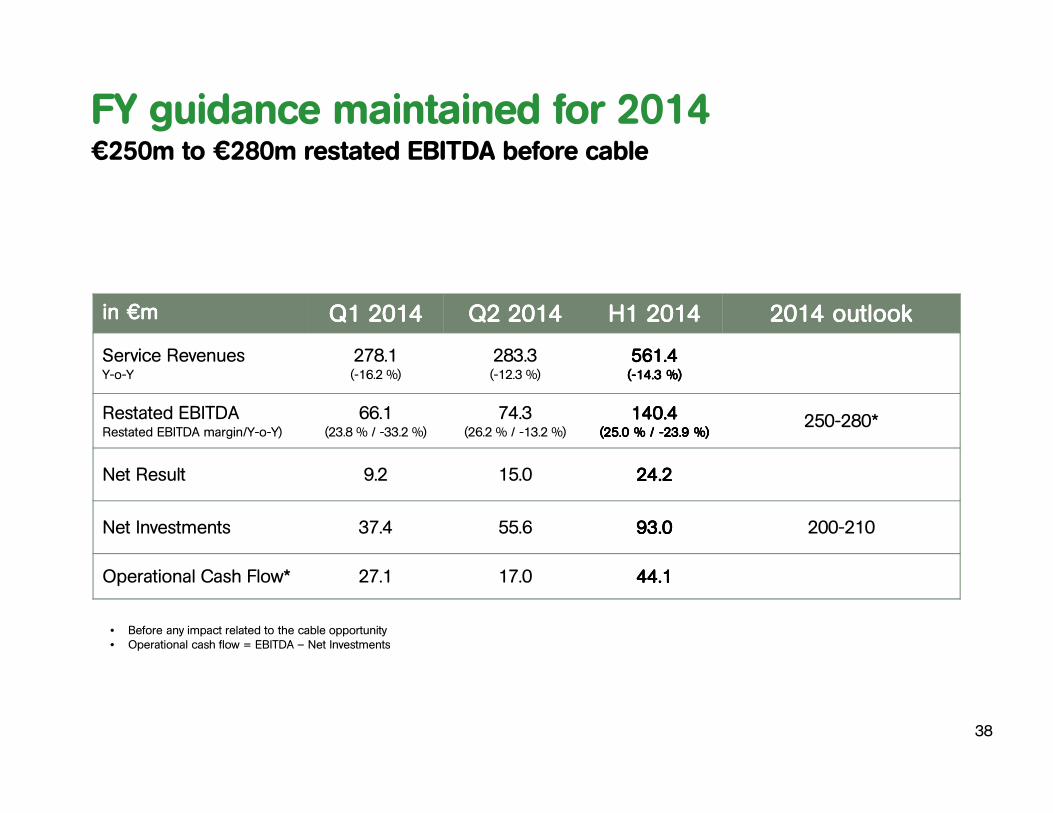

FY guidance maintained for 2014€250m to €280m restated EBITDA before cable

in in in in €€€€mmmm Q1 2014Q1 2014Q1 2014Q1 2014 Q2 2014Q2 2014Q2 2014Q2 2014 H1 2014H1 2014H1 2014H1 2014 2014 outlook2014 outlook2014 outlook2014 outlook

Service RevenuesY-o-Y

278.1(-16.2 %)

283.3(-12.3 %)

561.4561.4561.4561.4((((----14.3 14.3 14.3 14.3 %)%)%)%)

Restated EBITDARestated EBITDA margin/Y-o-Y)

66.1(23.8 % / -33.2 %)

74.3(26.2 % / -13.2 %)

140.4140.4140.4140.4(25.0 % / (25.0 % / (25.0 % / (25.0 % / ----23.9 %)23.9 %)23.9 %)23.9 %)

250-280*

Net Result 9.2 15.0 24.224.224.224.2

Net Investments 37.4 55.6 93.093.093.093.0 200-210

Operational Cash Flow* 27.1 17.0 44.144.144.144.1

38

Appendix

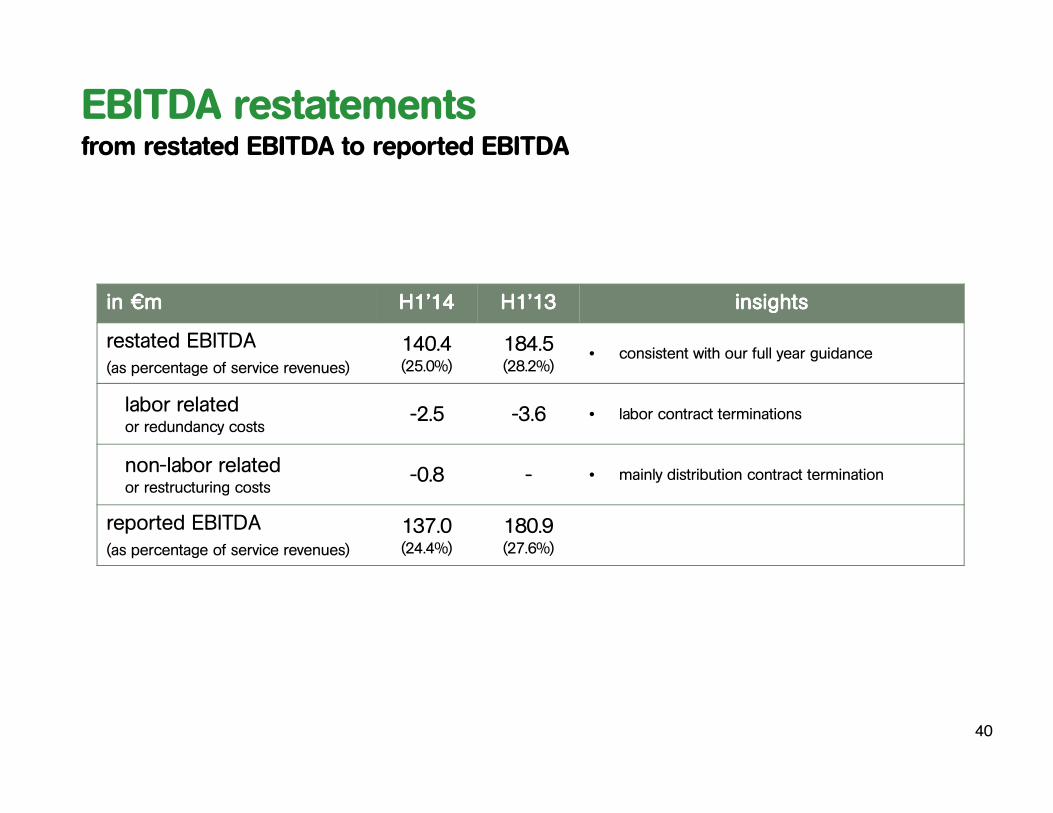

EBITDA restatementsfrom restated EBITDA to reported EBITDA

in in in in €€€€mmmm H1’14H1’14H1’14H1’14 H1’13H1’13H1’13H1’13 insightsinsightsinsightsinsights

restated EBITDA(as percentage of service revenues)

140.4(25.0%)

184.5(28.2%)

• consistent with our full year guidance

labor relatedor redundancy costs

-2.5 -3.6 • labor contract terminations

non-labor relatedor restructuring costs

-0.8 - • mainly distribution contract termination

reported EBITDA(as percentage of service revenues)

137.0(24.4%)

180.9(27.6%)

40

41

50%51%49%48%48%46%

19%18%19%18%15%

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

180

190

Q1 2014

122

62%

33%

4%

Q4 2013

123

63%

33%

4%

Q3 2013

127

60%

36%

4%

Q2 2013

131

63%

33%

3%

Q1 2013

129

66%

30%

4%

Q2 2014

19%

33%

62%

5%

123

SMS

Advanced data as % mobile service rev

Data as % mobile service rev

Mobile Data

MATMA

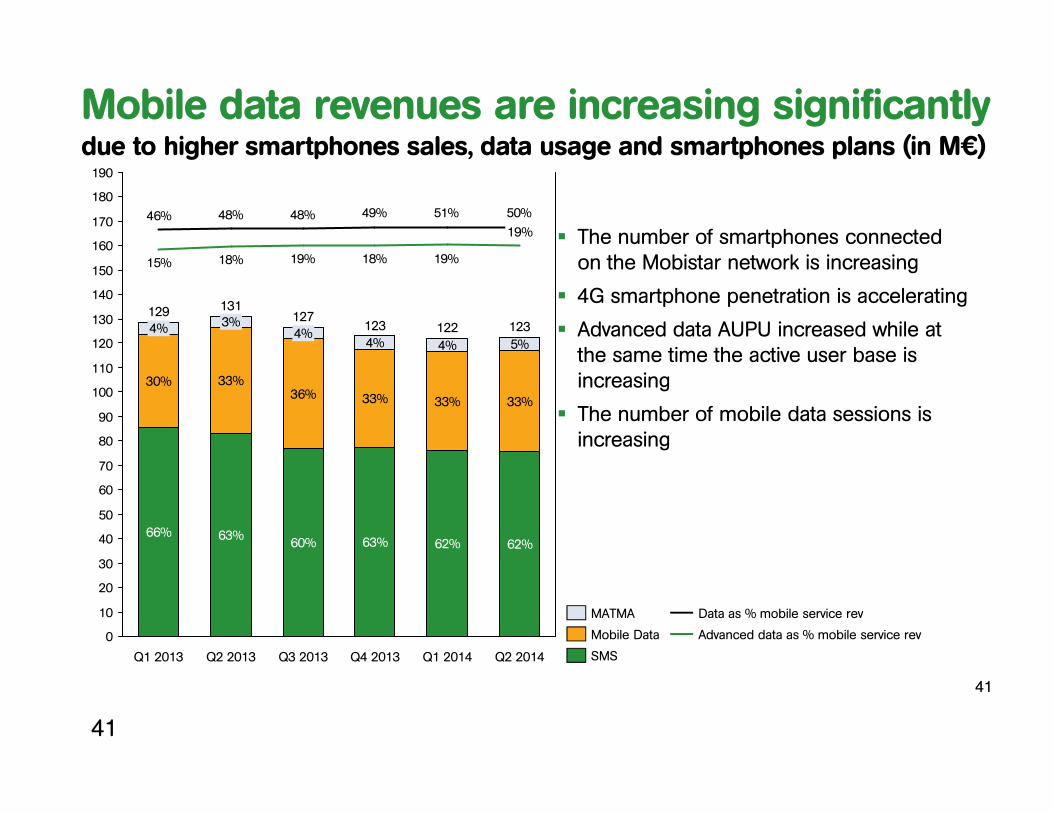

� The number of smartphones connected on the Mobistar network is increasing

� 4G smartphone penetration is accelerating

� Advanced data AUPU increased while at the same time the active user base is increasing

� The number of mobile data sessions is increasing

Mobile data revenues are increasing significantly due to higher smartphones sales, data usage and smartphones plans (in M€)

41

42

17% 17% 17% 19% 19%

13% 16% 16% 10% 12%

7% 7%

51% 51% 49% 50% 49%

4%4%4%4%4%

5%5%5%

31%

2013

1.283

1H 2014

553

3%

1% 1%

1%

2%

Q2 2014

2%

274

2%

1%

3%

2%3%

2%

Q2 2013 1H 2013

1%

1%

2%

3%2%2%

1%

3%

316 659

2%

3%2%

1%

1%

MTR SMS

Visitor Roaming

MTR Voice

Roaming Data

Roaming voice

Roaming SMS

Handsets

MVNO

M2M

Retail billed revenues

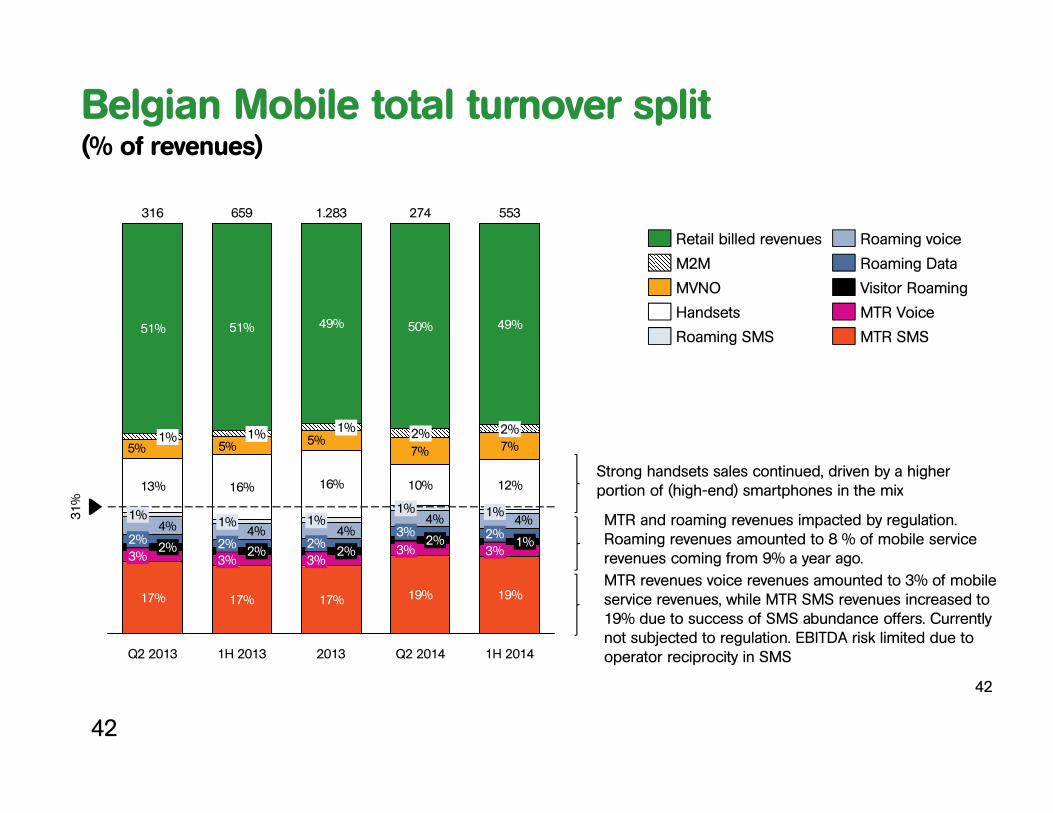

MTR revenues voice revenues amounted to 3% of mobile service revenues, while MTR SMS revenues increased to 19% due to success of SMS abundance offers. Currently not subjected to regulation. EBITDA risk limited due to operator reciprocity in SMS

MTR and roaming revenues impacted by regulation. Roaming revenues amounted to 8 % of mobile service revenues coming from 9% a year ago.

Strong handsets sales continued, driven by a higher portion of (high-end) smartphones in the mix

42

Belgian Mobile total turnover split (% of revenues)

Q&A

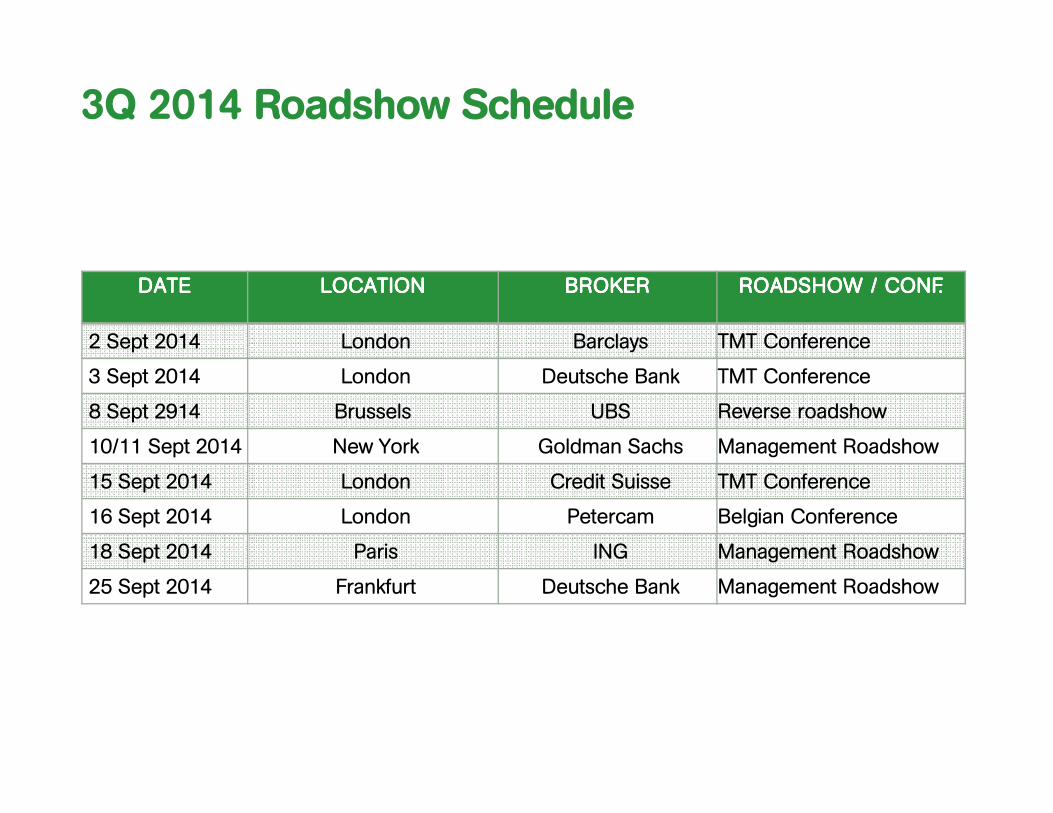

DATEDATEDATEDATE LOCATIONLOCATIONLOCATIONLOCATION BROKERBROKERBROKERBROKER ROADSHOW / ROADSHOW / ROADSHOW / ROADSHOW / CONF.CONF.CONF.CONF.

2 Sept 2014 London Barclays TMT Conference

3 Sept 2014 London Deutsche Bank TMT Conference

8 Sept 2914 Brussels UBS Reverse roadshow

10/11 Sept 2014 New York Goldman Sachs Management Roadshow

15 Sept 2014 London Credit Suisse TMT Conference

16 Sept 2014 London Petercam Belgian Conference

18 Sept 2014 Paris ING Management Roadshow

25 Sept 2014 Frankfurt Deutsche Bank Management Roadshow

3Q 2014 Roadshow Schedule

FURTHER QUESTIONS? PLEASE CONTACT THE IR DEPARTMENT

Investor RelationsPhone: +32 2 745 80 92E-mail: [email protected]

For further information please visit

www.mobistar.be

http://business.mobistar.be

http://corporate.mobistar.be