Embed Size (px)

Citation preview

econstorMake Your Publications Visible.

A Service of

zbwLeibniz-InformationszentrumWirtschaftLeibniz Information Centrefor Economics

Teyssière, Gilles

Working Paper

Modelling exchange rates volatility with multivariatelong-memory ARCH processes

SFB 373 Discussion Paper, No. 1999,5

Provided in Cooperation with:Collaborative Research Center 373: Quantification and Simulation ofEconomic Processes, Humboldt University Berlin

Suggested Citation: Teyssière, Gilles (1999) : Modelling exchange rates volatility withmultivariate long-memory ARCH processes, SFB 373 Discussion Paper, No. 1999,5, HumboldtUniversity of Berlin, Interdisciplinary Research Project 373: Quantification and Simulation ofEconomic Processes, Berlin,http://nbn-resolving.de/urn:nbn:de:kobv:11-10056020

This Version is available at:http://hdl.handle.net/10419/61735

Standard-Nutzungsbedingungen:

Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichenZwecken und zum Privatgebrauch gespeichert und kopiert werden.

Sie dürfen die Dokumente nicht für öffentliche oder kommerzielleZwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglichmachen, vertreiben oder anderweitig nutzen.

Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen(insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten,gelten abweichend von diesen Nutzungsbedingungen die in der dortgenannten Lizenz gewährten Nutzungsrechte.

Terms of use:

Documents in EconStor may be saved and copied for yourpersonal and scholarly purposes.

You are not to copy documents for public or commercialpurposes, to exhibit the documents publicly, to make thempublicly available on the internet, or to distribute or otherwiseuse the documents in public.

If the documents have been made available under an OpenContent Licence (especially Creative Commons Licences), youmay exercise further usage rights as specified in the indicatedlicence.

www.econstor.eu

Modelling Exchange Rates Volatility with

Multivariate Long�Memory ARCH Processes

by Gilles Teyssi�ere�

Humboldt�Universit�at zu Berlin

Institut f�ur Statistik und �Okonometrie

Sonderforschungsbereich ���

� GREQAM� Marseille� France

First version� January ����This revised version� September ���

Abstract

We consider two multivariate long�memory ARCH models� which extend the univariatelong�memory ARCH models� we �rst consider a long�memory extension of the restricted con�stant conditional correlations �CCC� model introduced by Bollerslev ������� and we proposea new unrestricted conditional covariance matrix model which models the conditional covari�ances as long�memory ARCH processes We apply these two models to two daily returns onforeign exchanges �FX� rates series� the Pound�US dollar� and the Deutschmark�US dollarThe estimation results for both models show� �i� that the unrestricted model outperformsthe restricted CCC model� and �ii� that all the elements of the conditional covariance matrixshare the same degree of long�memory for the period April ����January ��� However�this result does not hold for the �oating periods March ����January ��� and September����January ��� This break in the long�term structure may be caused by the EuropeanMonetary System inception in March ���Keywords� Long�memory processes� heteroskedasticity� multivariate long�memory ARCHmod�els� multivariate FIGARCH modelsJEL classi�cation� C� � G��

�This is a revised version of the GREQAM DT ��B�� �October ������ which is available at the followinge�mail address� dtgreqam�ehesscnrs�mrsfrI whish to thank for useful comments Raj Bhansali� Olaf Bunke� Christian Gourieroux� Wolfgang Hardle� HelmutHerwartz� Piotr Kokoszka� Rolf Tschernig� participants to the seminars organized by the Department of Math�ematics� University of Liverpool� May ����� the �th Annual Symposium of the Society for Nonlinear Dynamicsand Econometrics� New York� March ����� the Weierstrass Institute for Applied Analysis and Stochastics� Berlin�April ����� the ESRC Econometric Study Group Annual Conference� Bristol� July ����� the ���� EconometricSociety European Meeting in Berlin I also thank Louis�Andr e G erard�Varet for the research hospitality of GRE�QAM Marseilles while I was on the payroll of another institution This version supersedes previous papers entitled�Modelling Exchange Rates Volatility with Multivariate Long�Memory Skedastic Functions�� and �Modelling Fu�tures Returns with Multivariate FIGARCH Models� The usual caveats applyAddress� Humboldt�Universitat zu Berlin� Institut fur Statistik und Okonometrie� SFB ��� Spandauer Stra�e� ��D������ Berlin GERMANYE�Mail� Teyssier�wiwihu�berlinde� gilles�ehesscnrs�mrsfr

� Introduction

Most of the returns on speculative assets Rt � ln�Pt�Pt���� where Pt denotes the asset price attime t� are characterized by the absence of signi�cant correlation between successive observations�which is a consequence of the martingale property of asset prices� However� their variations areclustered� their conditional variance is predictable� and the power transformations jRtj�� where �is a positive real number� of these series exhibit a signi�cant persistence and dependence betweenvery distant observations called �long�range dependence� or �long�memory���

Four classes of stochastic processes can mimic these properties the long�memory ARCHprocesses introduced in Robinson ����� the long�memory stochastic volatility models proposedby Harvey ����� and Breidt� Crato and de Lima� Mandelbrot s ����� multifractal models� andthe multi�factors models by Gallant� Hsu and Tauchen ������We consider here the class of long�memory GARCH models� Although Ding and Granger

������ and Engle and Lee ����� proposed a mixture of ARCH and IGARCH processes� i�e�� aprocess mixing a transitory and a permanent component� for representing the hyperbolic decayof the autocorrelations of the volatility� these features are more parsimoniously modeled by thestatistical class of long�memory ARCH�GARCH processes��

Long�memory in the class of conditional variance ARCH processes has been considered �rstby Robinson ���� for testing for dynamic conditional heteroskedasticity� Later� several authorshave extended several GARCH�type processes to fractional situations�� In the same way� Dingand Granger ����� have derived a long�memory ARCH model by using an aggregation argument�All these models were concerned with the univariate modeling of time series� Empirical

evidence on futures data�� Intra�Day foreign exchange �FX� rates returns �Henry and Payne������ and stock indexes �Ray and Tsay� ����� suggest that some time series share the same long�memory component in their conditional variance� Since some time series are likely to be in�uencedby the same set of events� it is straightforward to consider long�memory in the conditional secondmoments in a multivariate framework by also modeling the covariation of the series� Furthermore�a common long�range component or �co�persistence in a matrix of conditional variances is ofinterest for long�term forecasts as the relative variations between these covariances are onlytransitory�We �rst consider the extension of the univariate long�memory ARCH models in the restricted

multivariate constant conditional correlations �CCC� framework proposed by Bollerslev ������As we observed that the volatilities and the �co�volatility of some series have a common long�memory component� see p �� we propose a new multivariate unrestricted framework� whichexplicitly models the covariances as long�memory ARCH processes�We apply these classes to the bivariate modeling of two series of FX rates returns at daily

frequency for the periods September ���January ���� March ����January ���� and April����January ��� the Pound�US dollar� and the Deutschmark�US dollar� The e�ects of target

�See Robinson ������ and Beran ������ for a survey on long�memory processes�See Robinson and Za�aroni ������� Ding and Granger ������� Giraitis� Kokoszka and Leipus ������ for a

rigorous demonstration�See Bollerslev and Mikkelsen ������� McCurdy and Michaud ������� and Teyssi�ere �����a��See the ���� version of Teyssi�ere �����b�� and a previous version of this work on futures data As data from

future markets are reliable since ����� the sample sizes were a bit short for analyzing long�memory processes andwe turn to the analysis of FX data

zone systems on the volatility have already been studied by Bollerslev ����� and Engle and Gau����� among others� Our purpose is to analyze the e�ects of the EMS system on the long�termcomponent of the FX rates returns volatilities�This paper is organized as follows� Section � discusses the univariate and multivariate long�

memory ARCH models� Section � presents an application to a bivariate modeling of FX ratesreturns� Section � concludes�

� Multivariate long�memory ARCH models

��� The long�memory property of time series

Let fytg be a stochastic process de�ned by the following autoregressive �AR� representation

�� ��L�� yt � �t �t white noise ��

where ��L� is a lag polynomial� We allow for long�memory in fytg by considering that the orderof ��L� is in�nite� and that its coe�cients �j satisfy

limj��

j�jj � Cj����q� ���

where C is a positive constant and q is a strictly positive real number which represents the long�memory property of the series� This implies that the coe�cients �j have a hyperbolic rate ofdecay� Several polynomials satisfy this property

� The fractional qth di�erence operator� used for de�ning the fractional Gaussian noise I�q�process �Mandelbrot and Van Ness� ���� Granger and Joyeux� ���� Hosking� ����characterized by the real parameter q� called the degree of integration of the series� TheAR representation of the fractional Gaussian noise I�q� is � ��L� � �� L�q� with

�j ����j � q�

���q���j � � � with limj��

�j �����q�j

����q� ���

where ���� denotes the Gamma function�� The Gegenbauer polynomials� �Gray� Zhang and Woodward� ���� Chung� ���a� charac�terized by two parameters q and �� which are respectively the degree of integration of theseries and the cosine of the singularity� The coe�cients of these polynomials are de�ned by

�j �

�j���Xk

���k���q � j � k�����j��k

���q���k � ���j � �k � � ���

with limj��

�j �cos ��j � q�� � �q�����

���q� sin�q�����

j

���q

where ��� indicates integer part� and � � arccos���� When � � � this polynomial reducesto the I��q� polynomial�

�

� The ratio of two Beta functions �Ding and Granger� ����

�j �B�p� j � � q � �

B�p� q�� with lim

j���j �

q��p� q�

��p�j����q� ���

for p� q � ��� If p � q � � this polynomial reduces to an I�q� polynomial� Since thispolynomial is characterized by two parameters� it is more �exible than the polynomial ofthe I�q� process��

The Gegenbauer polynomials capture long�range dependence with persistent component atfrequency �� and are then used for modeling macroeconomic data �see Chung� ���b�� The twoother polynomials� of which coe�cients are always strictly positive� have been used for modelingthe long range dependence of the conditional variance of some �nancial assets� They also satisfy

�Xj�

�j � ���

��� Long�memory in the conditional variance

De�ne a conditional heteroskedasticity model as

Rt �m�Rt� � �t� �t � i�i�d�N��� �t � ���

where m�Rt� denotes the regression function� the conditional variance �t depends on the infor�

mation set It consisting of everything dated t� or earlier� Engle ����� proposed the ARCH�p�skedastic function

�t � � ��L���t ���

where ��L� is a lag polynomial of order p� Robinson ���� has considered the general case ofconditional heteroskedasticity by resorting to long�memory in�nite order lag polynomials� andhas proposed the following long�memory ARCH

�t � � ��Xj�

�j���t�j � �� �

�Xj�

�j��t�j ���

where the coe�cients f�jg�j� of the in�nite order lag polynomial ��L� satisfy equations ��� and���� Thus� equation ��� de�nes a long�memory process in the variance� in which shocks on theerror terms have a persistent e�ect on the conditional variance� We �rst consider for ��L� thepolynomial de�ned by the ratio of two Beta functions� Thus� the long�memory ARCH modelbecomes

�t ��Xj�

B�p� j � � q � �B�p� q�

��t�j ���

which is a particular case of the long�memory ARCH model derived by Ding and Granger �����

�t � �� ��� � ���L���t ��

�If p � �� �� � �� �j � �� �j � ��Ding and Granger ������ report examples of decay of this polynomial for several values of p and q

�

where � is a parameter � ��� �� In our case � � �This long�memory ARCH is very interesting since the coe�cients of ��L� are strictly positive�

there is no restriction for insuring the conditional variance to be strictly positive� provided thatthe ratio of the Beta functions exists� i�e�� p � � and q � �� and at least one of the past errorterms �t is di�erent from zero� which are rather mild constraints� We extend this model byconsidering parameterized real powers for both t and �t� Thus� the long�memory ARCH model��� becomes

�t ��Xj�

B�p� j � � q � �B�p� q�

j�t�j j� ���

We can obviously consider more general forms for equation ��� in which the error terms aretransformed by an asymmetric function for capturing asymmetries�

Long�memory in the conditional variance is also modeled by using the ARMA parameter�ization of some GARCH type processes� and considering fractional unit roots in the AR com�ponent of this ARMA parameterization� We then obtain the class of Fractionally IntegratedGARCH processes� which bridges the gap between GARCH and Integrated GARCH processes��

A FIGARCH�l� q�m� is then de�ned as

�t �

� ����

�� �� �L�� �� L�q

�� ��L��

���t ���

where ��L� and �L� are lag polynomials of respectively �nite order l andm� the roots of ���L�and �L� being outside the unit circle�� This richer parameterization allows a greater �exibilitythan the long�memory ARCH model presented above� The counterpart of this �exibility is amore restrictive set of conditions for insuring the conditional variance to be positive� Whilethe necessary and su�cient conditions for a FIGARCH�� q� �� model are not too constraining� � q � and � �� the su�cient conditions for a FIGARCH�� q� � are more restrictive�

� �� � � q � � ��� q���� q � � �� q���� � �� � � � q� ���

This set of restrictions also applies to the FIAPARCH and FINGARCH models respectivelyproposed by McCurdy and Michaud ����� and Teyssi�ere ����a�� who extended the APARCHmodel of Ding� Granger and Engle ����� and the Engle and Ng ����� NGARCH to fractionalsituations� We alternatively can use a log transformation of the conditional variance� like theFIEGARCH model proposed by Bollerslev and Mikkelsen ������ However� as mentioned byPagan ������ the IEGARCH model is not identi�able by Quasi Maximum Likelihood �QML��thus if q tends to � the same problem is likely to occur for a FIEGARCH�

�See McCurdy and Michaud ������� Teyssi�ere �����a��See Bollerslev and Mikkelsen ������� McCurdy and Michaud �������The link between this FIGARCH model and the previous long�memory ARCH model� with the restriction

p � q � �� is given by the following re�parameterization� � � ��L� � �� � L�q��L����L�� and by assuming that� � ��� ������� is a �nite parameter to be estimated �See Robinson and Za�aroni� �����

�See Bollerslev and Mikkelsen ������ For models of higher orders� the conditions are far more complicate

�

��� Multivariate long�memory skedastic functions

Let Rt be a n�dimensional vector long�memory ARCH process

Rt � m�Rt� � �t� �t � i�i�d�N����t� ���

where m�Rt� denotes the vector regression function� �t is a n�dimensional vector of error termswith conditional covariance matrix �t� We �rst consider a long�memory extension of the con�stant conditional correlations model �CCC� proposed by Bollerslev ������ where the conditionalcovariance matrix �t has as typical element sij�t� with

sii�t � �ii�t ��Xk�

B�pi � k � � qi � �B�pi� qi�

��i�t�k� i � � � � � � n

sij�t � �ijii�tjj�t� i� j � � � � � � n i �� j ���

where �ij � ��� � denotes the conditional correlation which is supposed to be constant� Thisparsimonious diagonal speci�cation insures that the conditional covariance matrix is always pos�itive de�nite� and that the multivariate long�memory ARCH process is stationary if all theunivariate processes in the main diagonal are stationary���

This process can be extended by using a parameterization similar to equation ��� as follows

sii�t � �ii�t� �ii�t ��Xk�

B�pi � k � � qi � �B�pi� qi�

j�i�t�kj� � i � � � � � � n

sij�t � �ijii�tjj�t� i� j � � � � � � n i �� j ���

We also consider the multivariate CCC FIGARCH process

sii�t � �ii�t �i

� �i���

�� �� i�L��� � L�q

� �i�L�

���i�t� i � � � � � � n

sij�t � �ijii�tjj�t� i� j � � � � � � n i �� j ���

Lastly� we propose two alternative unrestricted parameterizations for the conditional covari�ance matrix �t� with typical element sij�t

sij�t ��Xk�

B�pij � k � � qij � �B�pij� qij�

�i�t�k�j�t�k� i� j � � � � � � n ���

and

sij�t �ij

� �ij���

�� �� ij�L��� � L�q

� �ij�L�

��i�t�j�t� i� j � � � � � � n ����

In these cases� there is no analytically tractable set of conditions for insuring �t to bepositive de�nite� and the multivariate process to be stationary� We implement the positivede�niteness constraint in the estimation procedure by resorting to numerical penalty functions�

��See Bollerslev ������� Bera and Higgins ������� Bollerslev� Engle and Nelson ������� Engle and Kroner �������or Pagan ������� for a survey on multivariate ARCH processes

�

The combination of positivity constraints by projection methods and penalty functions makesthe estimation of the multivariate unrestricted FIGARCH more di�cult� However� we will seelater that this model is more apt to represent the conditional covariance of the bivariate seriesof FX rates returns�This unrestricted long�memory ARCH process is stationary provided that �t is a measurable

function on the information set It� and trace��t��t � is �nite almost surely� The latter condition

holds if the moments are bounded� i�e�� E�trace��t��t �

p� is �nite for some p��� As our estimationresults show that the two �rst moments of trace��t

��t � for the unrestricted model are close tothe moments of the diagonal stationary model� we can consider that the process estimated onour data is stationary�Since we are working with data at daily frequency� we can reasonably assume that the error

terms are normally distributed��� Thus� the log�likelihood function of the multivariate long�memory ARCH model is

LT ��� � �nT

�ln���� �

�

TXt�

�ln j�tj� ��t ���t

�t

����

where � and T respectively denote the set of parameters and the sample size� The robustestimators of the variances are given by the heteroskedastic consistent sandwich covariance matrixT��H������I����H������ whereH���� and I���� are respectively the Hessian and the outer�product�of�the�gradient matrices evaluated at the Quasi Maximum Likelihood �QML� estimates ���

� Application to the bivariate modeling of exchange rates

We consider several bivariate long�memory ARCH models for two series at daily frequenciesthe log of returns on the Pound�US dollar� and the Deutschmark�US dollar exchange rates�de�ned by �� ln�Pt�Pt���� where Pt denotes the exchange rate at time t� We consider hereobservations from the �� August ��� after the collapse of the Bretton�Wood �xed exchangerate system� until January ���� A limited variation exchange rates system has been institutedin December ��� the Smithsonian Agreement� but it lasted only � months� and was followedby the ��oating period�� During this �oating period� some European currencies were governedby several mechanisms limiting their relative variations� The �Snake in the Tunnel� mechanismallowed these currencies to vary by a maximum of ��� against each other� the �Snake�� andby a maximum of ���� against the dollar� �the Tunnel�� Belgium� France� Italy� Luxembourg�The Netherlands� and West Germany were the �rst participants� UK joined one month afterand withdrew six weeks afterwards� Later� the reference to the dollar was abandoned� and thenthe system became the �Snake�� in which parities were several times realigned� Later� in March���� the European Monetary System �EMS� replaced the �Snake�� UK joined the EMS in ���and left two years later� A long�memory analysis should� by construction� be una�ected by this

��See Bollerslev� Engle and Nelson ��������The departure to normality does not a�ect the QML results with data at daily frequency However� this

assumption is di�cult to maintain with very high�frequency data� of which leptokurtosis can be captured witht�distributed error terms with t � � or Generalized Exponentially Distributed error terms

�

series of local adjustments and breaks� However� estimation results lead us to consider periodswhich coincide with these events�The most interesting period is the EMS period� April ���� � January ��� ����� observa�

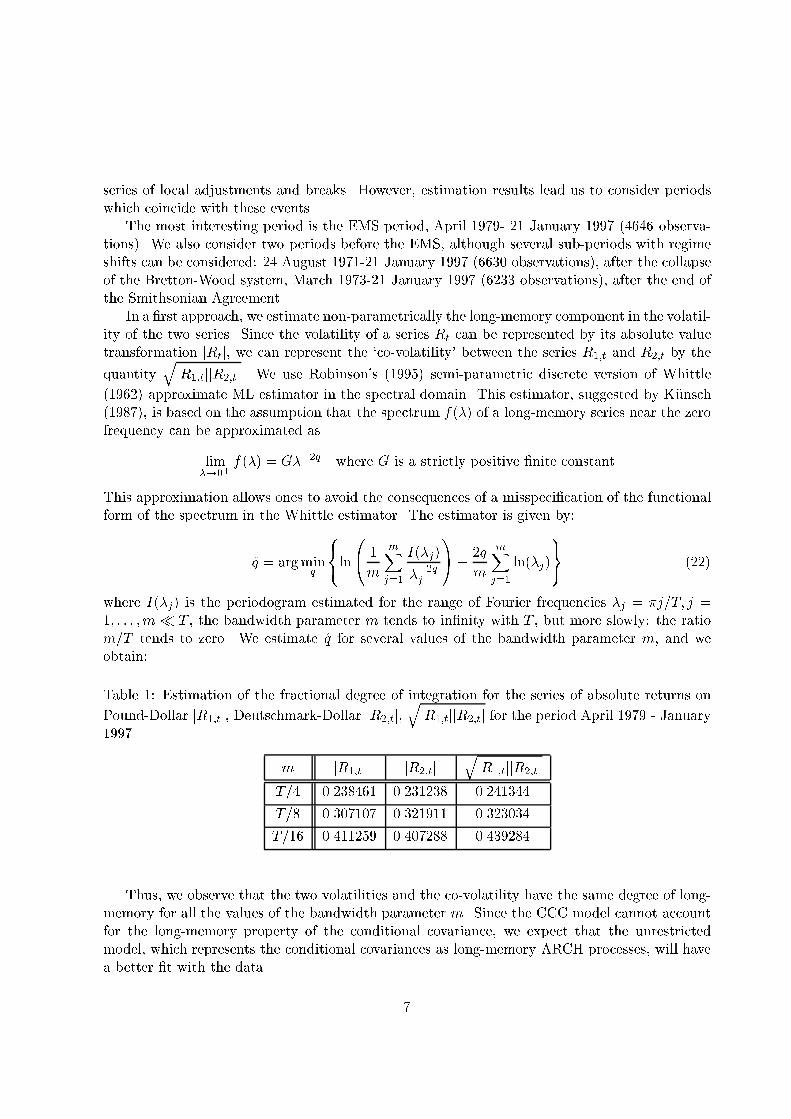

tions�� We also consider two periods before the EMS� although several sub�periods with regimeshifts can be considered �� August ���� January ��� ����� observations�� after the collapseof the Bretton�Wood system� March ����� January ��� ����� observations�� after the end ofthe Smithsonian Agreement�In a �rst approach� we estimate non�parametrically the long�memory component in the volatil�

ity of the two series� Since the volatility of a series Rt can be represented by its absolute valuetransformation jRtj� we can represent the �co�volatility between the series R��t and R��t by the

quantityqjR��tjjR��tj� We use Robinson s ����� semi�parametric discrete version of Whittle

����� approximate ML estimator in the spectral domain� This estimator� suggested by K!unsch������ is based on the assumption that the spectrum f��� of a long�memory series near the zerofrequency can be approximated as

lim��

f��� � G���q where G is a strictly positive �nite constant

This approximation allows ones to avoid the consequences of a misspeci�cation of the functionalform of the spectrum in the Whittle estimator� The estimator is given by

�q � argminq

���ln

m

mXj�

I��j�

���qj

�A� �q

m

mXj�

ln��j�

� � ����

where I��j� is the periodogram estimated for the range of Fourier frequencies �j � �j�T� j �� � � � �m � T � the bandwidth parameter m tends to in�nity with T � but more slowly the ratiom�T tends to zero� We estimate �q for several values of the bandwidth parameter m� and weobtain

Table Estimation of the fractional degree of integration for the series of absolute returns on

Pound�Dollar jR��tj� Deutschmark�Dollar jR��tj�qjR��tjjR��tj for the period April ��� � January

���

m jR��tj jR��tjqjR��tjjR��tj

T�� ������� ������� �������

T�� ������� ����� ��������

T�� ������ �������� ��������

Thus� we observe that the two volatilities and the co�volatility have the same degree of long�memory for all the values of the bandwidth parameter m� Since the CCC model cannot accountfor the long�memory property of the conditional covariance� we expect that the unrestrictedmodel� which represents the conditional covariances as long�memory ARCH processes� will havea better �t with the data�

�

We estimated the following bivariate long�memory ARCH��

�R��t

R��t

��

�����

��

����t���t

�with

����t���t

�� N

����

��

�s���t s���t

s���t s���t

������

where R��t and R��t respectively denote the log of returns on the Pound�Dollar and Deutschmark�Dollar� We consider the �ve alternative multivariate skedastic functions

�A�

B s���t

s���ts���t

�CA �

BBBBBBBBB

�Xj�

B�p� � j � � q� � �B�p�� q��

����t�j

�Xj�

B�p� � j � � q� � �B�p�� q��

����t�j

�ps���t

ps���t

�CCCCCCCCCA

����

�B�

B ����t

����ts���t

�CA �

BBBBBBBBB

�Xj�

B�p� � j � � q� � �B�p�� q��

j���t�j j�

�Xj�

B�p� � j � � q� � �B�p�� q��

j���t�j j�

����t���t

�CCCCCCCCCA

����

�C�

B s���t

s���ts���t

�CA �

BBBBBBB

�

� �����

�� �� �L��� L�q�

� ��L

�����t

�

� �����

�� �� �L��� L�q�

� ��L

�����t

�ps���t

ps���t

�CCCCCCCA

����

�D�

B s���t

s���ts���t

�CA �

BBBBBBBBBBBB

�Xj�

B�p� � j � � q� � �B�p�� q��

����t�j

�Xj�

B�p� � j � � q� � �B�p�� q��

����t�j

�Xj�

B�p� � j � � q� � �B�p�� q��

���t�j���t�j

�CCCCCCCCCCCCA

����

�E�

B s���t

s���ts���t

�CA �

BBBBBBBBB

�

� �����

�� �� �L��� L�q�

� ��L

�����t

�

� �����

�� �� �L��� L�q�

� ��L

�����t

�

� �����

�� �� �L��� L�q�

� ��L

����t���t

�CCCCCCCCCA

����

��We truncate the expansion of the in�nite order polynomial at the order ����

�

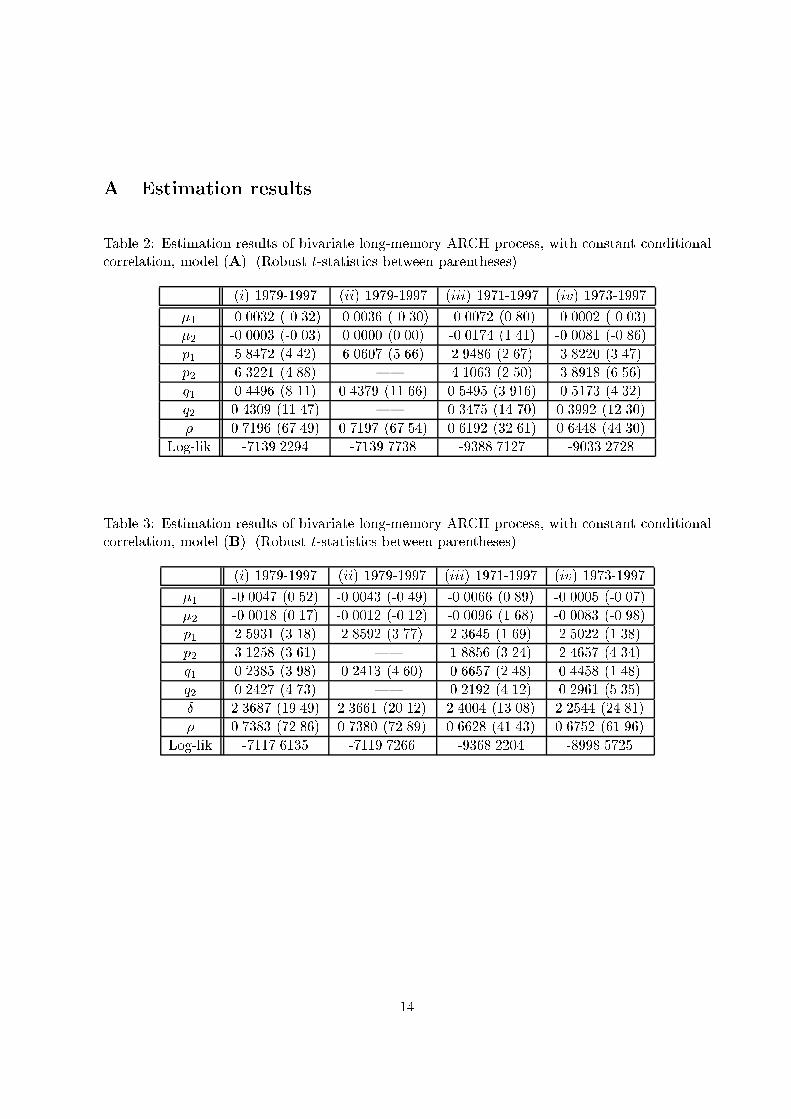

Table � p � reports the QML estimates of the constant conditional variance long�memory ARCHmodel �A� for �i� the period �������� �ii� the same period subject to the constraint that theparameters of the two conditional variances are equal� i�e�� q� � q� and p� � p�� �iii� for theperiod ������� and �iv� the period ��������It clearly appears that for the period �������� the two series share the same degree of

long�memory in the conditional variance� since the estimated values for q� and q� are very close�The constraints q� � q� and p� � p� are accepted by the likelihood ratio �LR� test� and the moreparsimonious constrained model is then preferable� The estimation results for the period ������ are less appealing� The two long�memory parameters largely di�er� This result completesBollerslev s ����� result� which showed� for a multivariate GARCH model on weekly data� adi�erence between these two periods in the estimated parameters explained by the inception ofthe EMS in March ���� The EMS system has modi�ed both the short�term and the long�termvariations of the volatilities of exchange rates returns���

Table � p � reports the QML estimates of the constant conditional variance long�memoryARCH model� model �B�� for �i� the period �������� �ii� the same period with the restrictionsp� � p� and q� � q�� �iii� for the period ������� and �iv� the period �������� The restriction� � � is rejected by the LR test� However� some parameters are instable for the two largersamples this may be due to the misspeci�cation of the model� of which assumption of a constantconditional correlation is too restrictive�Table � p � displays the estimation results for the bivariate CCC FIGARCH model� The

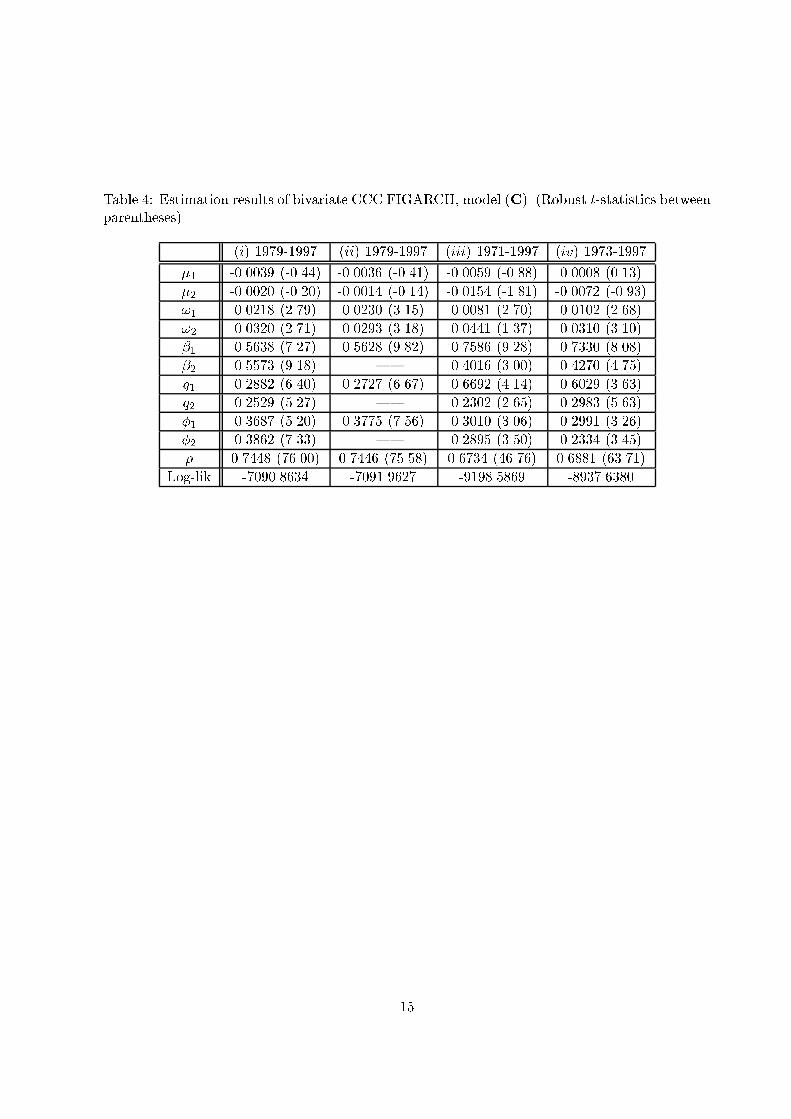

log�likelihood value is higher than the one of the long�memory ARCH model presented above�and the trade�o� between the increase of the value of the likelihood function and the increase ofthe number of parameters leads us to choose the less parsimonious CCC FIGARCH model� Asexpected� the maximization procedure is much slower� As observed above� the degrees of longmemory are the same for the period �������� Furthermore� the LR test accepts the hypothesisof equality of parameters � and for the two conditional variances� We will see later that theequality � � � is likely to be the consequence of the restrictive parameterization of the CCCFIGARCH�Tables � and � p � display the estimation results for respectively the unrestricted models

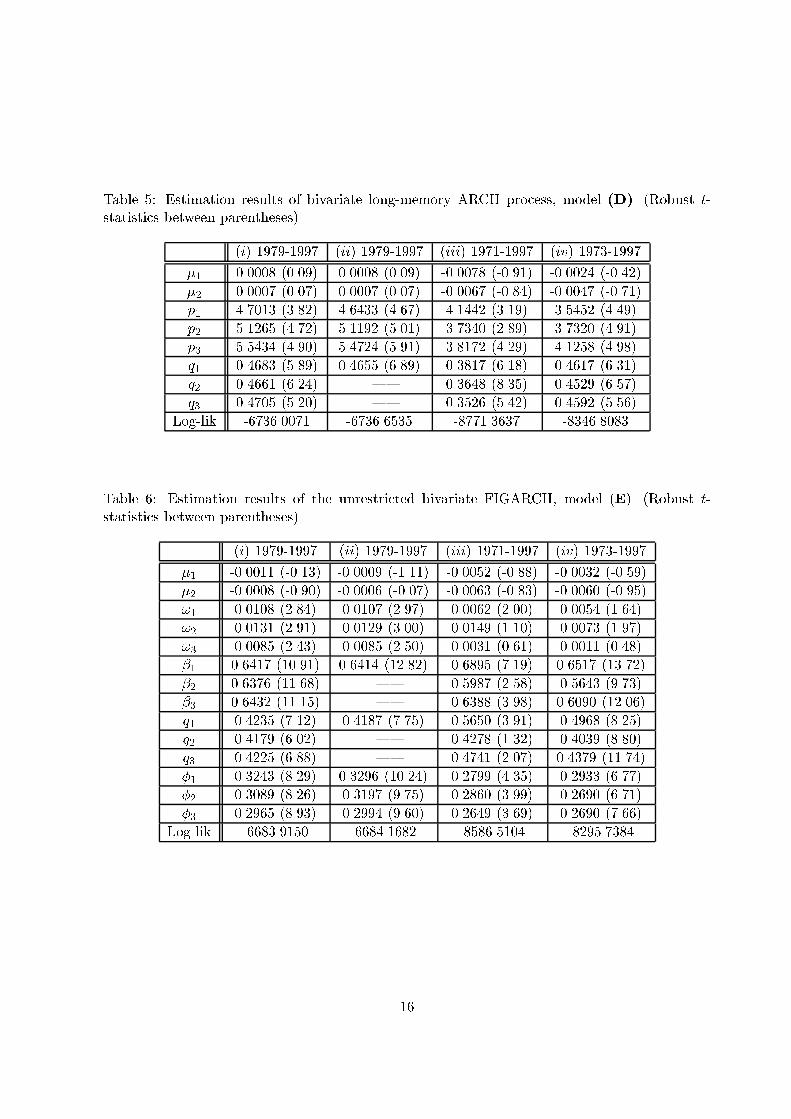

�D�� and �E�� Column �i� contains the QML estimates for the unconstrained model� column �ii�contains the estimates for the model with the restrictions q� � q� � q�� column �iii� containsestimation results for the whole period ������� and column �iv� contains estimation resultsfor the period �������� It clearly appears that the constant conditional correlation assumptionfor the models �A B C� is too strong since the value of the likelihood function is stronglyimproved� We also observe that the multivariate unrestricted FIGARCH model has a better �twith the data than the multivariate unrestricted long�memory ARCH model the log�likelihood isstrongly improved� and any parsimony criteria� e�g�� the Akaike Information Criteria or the BayesInformation Criteria� favors the multivariate unrestricted FIGARCH model��� As expected�

��We have also estimated the models �A� for the period ���������� with two di�erent conditional correlations�the �rst for the period ���������� the second for the period ��������� The LR test rejects the restriction thatthese two parameters are equal� and still rejects the restriction that the two degrees of long�memory are the same

��The statistical properties of the AIC and BIC criteria have not been established for the class of long�memoryARCH process Beran and Bhansali ������ result on the BIC for ARFIMA models casts doubt on the use of theBIC for long�memory volatility models

�

the estimation of the multivariate FIGARCH is more problematic" a sensible choice of startingvalues is necessary� but the model looks well conditioned since we did not encounter too muchproblems��

More interesting� all the elements of the conditional variance matrix� i�e�� the two conditionalvariances and the conditional covariance� display the same degree of long�memory the corre�lations between the estimated parameters are very high� and the restriction q� � q� � q� isaccepted by the LR test for both models �D� and �E� for the EMS period� Furthermore� therestriction �� � �� � �� for model �E� is also accepted by the LR test for the same period�In a standard GARCH framework� the polynomial �L� captures the local variations� while thepolynomial ��L� captures the long�term variations� As we have seen in another paper� Teyssi�ere����a�� this interpretation is less obvious in a long�memory framework as the polynomial �L�enters in the expression of the in�nite order lag polynomial�We estimate the models �D E� with the restriction q� � q� � q� for the periods ������

and �������� This restriction is accepted by the LR test� This result is due to the largerproportion of EMS observations in our sample� since this restriction is rejected respectively forthe �rst ���� and ���� observations� Although� by construction� a test for structural break at agiven time t for the long�memory parameter is meaningless� we can conclude from these resultsthat this equality in the long�memory parameters for the period ������� may be caused by theEMS inception in March ����

� Conclusion

We have proposed two classes of multivariate long�memory ARCH models� One of them� theconstant conditional correlation �CCC� model� requires few constraints in the estimation proce�dure� but a strong restriction on the functional form of the conditional covariance matrix� Thisconstraint appeared to be too strong since the long�memory CCC model is outperformed by theunrestricted long�memory conditional covariance model� We have applied these models to thebivariate modeling of the returns on two exchange rates� and have observed that for the period�������� after the EMS beginning� these two series have the same long�memory component inthe conditional variance� The class of unrestricted conditional covariance models allowed us togo farther by showing that all the elements of the conditional covariance matrix share the samedegree of long�memory�This equality in the long�memory parameter for the same exchange market suggests that this

parameter is linked to the features of the market� This empirical result stimulated further researchfor deriving a structural microeconomic model able to replicate the long�memory property of�nancial time�series� �See Kirman and Teyssi�ere� �����We decided to extend this empirical analysis in another paper� Teyssi�ere ������ with the

new FX rate datasets at ���minute intervals �HFDF��� recently released by Olsen # Associates�A motivation for this paper was the extension of this class of multivariate long�memory ARCHmodels to the framework of double long�memory time series� i�e�� series with a long�memorycomponent in both the conditional mean and the conditional variance developed in Teyssi�ere

��The conditional covariance matrix �t was not always positive de�nite for all t at some steps in the line searchprocedure� but the BFGS algorithm converges to an optimum satisfying the positivity constraint

�

����b�� as these intra�day FX rate returns are anti�persistent�This class of multivariate long�memory models can also be trivially extended by combining

skedastic functions of di�erent type in the conditional covariance matrix�Another issue for future research is the extension of the concept of co�persistence in the

conditional variance� developed by Bollerslev and Engle ������ to the fractional case� althoughthe idea of �fractional cointegration� for conditional variance processes is not yet supported bya theoretical model� �See Pagan� �����

References

�� BERA� A�K� # M�L� HIGGINS ����� �On ARCH Models Properties� Estimation andTesting�� Journal of Economic Surveys� �� ��������

��� BERAN� J� ����� Statistics for Long�Memory Processes� Chapman # Hall�

��� BERAN� J� # R�J� BHANSALI ����� �On Uni�ed Model Selection for Stationary andNonstationary Short� and Long�Memory Autoregressive Processes�� The University of Liv�

erpool mimeo�

��� BOLLERSLEV� T� ����� �Generalized Autoregressive Conditional Heteroskedasticity��Journal of Econometrics� ��� ��������

��� BOLLERSLEV� T� ����� �Modeling the Coherence in Short�run Nominal Exchange RatesA Multivariate Generalized ARCHModel�� Review of Economics and Statistics� ��� ��������

��� BOLLERSLEV� T� # R�F� ENGLE� ����� �Common Persistence in Conditional Vari�ances�� Econometrica� �� ������

��� BOLLERSLEV� T�� ENGLE� R�F� # D�B� NELSON ����� �ARCH Models�� in R�F� EN�GLE # D� McFADDEN editors� Handbook of Econometrics� �� North�Holland� Amsterdam�

��� BOLLERSLEV� T� # H�O� MIKKELSEN ����� �Modeling and Pricing Long�Memory inStock Market Volatility�� Journal of Econometrics� ��� �����

��� BREIDT� F�J�� CRATO� N� # P� de LIMA ����� �On the Detection and Estimation ofLong�Memory in Stochastic Volatility�� Journal of Econometrics� ��� ��������

��� CHUNG� C�F� ����a� �Estimating a Generalized Long�Memory Process�� Journal ofEconometrics� ��� ��������

�� CHUNG� C�F� ����b� �A Generalized Fractionally Integrated ARMA Process�� Journalof Time Series Analysis� to appear�

��� DING� Z�� # C�W�J� GRANGER ����� �Modelling Volatility Persistence of SpeculativeReturns� A New Approach�� Journal of Econometrics� ��� ������

��� DING� Z�� GRANGER� C�W�J� # R�F� ENGLE ����� �A Long Memory Property of StockMarket Returns and a New Model�� Journal of Empirical Finance� �� ������

��� ENGLE� R�F� ����� �Autoregressive Conditional Heteroskedasticity with Estimates of theVariance of U�K� In�ation�� Econometrica� ��� ��������

��� ENGLE� R�F� # G�G�J� LEE ����� �A Permanent and Transitory Component Model ofStock Return Volatility�� University of California� San Diego� DP �����R�

��� ENGLE� R�F� # V�K� NG ����� �Measuring and Testing the Impact of News on Volatility��The Journal of Finance� ��� �������

��� ENGLE� R�F� # K�F� KRONER ����� �Multivariate Simultaneous Generalized ARCH��Econometric Theory� ��� ������

��� ENGLE� R�F� # Y�F� GAU ����� �Conditional Volatility of Exchange Rates under aTarget Zone�� University of California� San Diego� DP ���� �

��� GALLANT� A�R�� HSU� C�T� # G� TAUCHEN ����� �Calibrating Volatility Di�usionsand Extracting Integrated Volatility�� In Proceedings of the Second High Frequency Data in

Finance Conference� HFDF�II� Olsen # Associates� �� April ���� Zurich� Switzerland�

���� GIRAITIS� L�� KOKOSZKA� P�S� # R� LEIPUS ����� �Stationary ARCHModels Depen�dence Structure and Central Limit Theorem�� mimeo LSE � The University of Liverpool�

Department of Mathematics�

��� GRANGER� C�W�J� ����� �Long�Memory Relationships and the Aggregation of DynamicModels�� Journal of Econometrics� ��� ��������

���� GRANGER� C�W�J� # R� JOYEUX ����� �An Introduction to Long�memory Time SeriesModels and Fractional Di�erencing�� Journal of Time Series Analysis� �� �����

���� GRAY� H�L�� ZHANG� N�F� # W�A� WOODWARD ����� �On Generalized FractionalProcesses�� Journal of Time Series Analysis� ��� ��������

���� HARVEY� A�C� ����� �Long�Memory in Stochastic Volatility�� LSE� discussion paper ���SPS�

���� HENRY� M� # R� PAYNE ����� �An Investigation of Long Range Dependence in Intra�Day Foreign Exchange Rate Volatility�� LSE� FMG� DP � �

���� HOSKING� J�R�M� ���� �Fractional Di�erencing�� Biometrika� �� ������

���� KIRMAN� A�P� # G� TEYSSI�ERE ����� �Microeconomic Models for Long�Memory in theVolatility of Financial Time Series�� mimeo GREQAM � Humboldt�Universit�at zu Berlin�

Institut f�ur Statistik und �Okonometrie�

���� K!UNSCH� H�R� ����� �Statistical Aspects of Self�Similar Processes�� In Proceedings of

the First World Congress of the Bernouilli Society�� Yu� Prohorov # V�V� Sazanov editors�VNU Science Press� Utrecht� �� ������

���� MANDELBROT� B� # J� VAN NESS ����� �Fractional Brownian Motion� FractionalNoises and Applications�� S�I�A�M Review� ��� ��������

�

���� MANDELBROT� B�B� FISCHER� A� # L� CALVET ����� �A Multifractal Model of AssetReturns�� Cowles Foundation Discussion Paper �� ��

��� McCURDY� T�H� # P�K� MICHAUD ����� �Capturing Long�Memory in the Volatility ofEquity Returns a Fractionally Integrated Asymmetric Power ARCH Model�� University ofToronto� mimeo�

���� PAGAN� A�R� ����� �The Econometrics of Financial Markets�� Journal of EmpiricalFinance� �� �����

���� RAY� B�K� # R�S� TSAY ����� �Common Long�range Dependence in Daily Stock Volatil�ities�� Graduate School of Business� University of Chicago� mimeo� In Proceedings of the

Second High Frequency Data in Finance Conference� HFDF�II� Olsen # Associates� ��April ���� Zurich� Switzerland�

���� ROBINSON� P�M� ���� �Testing for Strong Serial Correlation and Dynamic ConditionalHeteroskedasticity�� Journal of Econometrics� ��� ������

���� ROBINSON� P�M� ����� �Time Series with Strong Dependence�� In Advances in Econo�

metrics� Sixth World Congress� C�A� Sims Editor� CUP� ������

���� ROBINSON� P�M� ����� �Gaussian Semiparametric Estimation of Long Range Depen�dence�� Annals of Statistics� ��� �������

���� ROBINSON� P�M� # P� ZAFFARONI ����� �Modelling Nonlinearity and Long�Memory inTime Series�� in Nonlinear Dynamics and Time Series� Building a Bridge between the Nat�

ural and Statistical Sciences� C�D� Cutler and D�T� Kaplan editors� American MathematicalSociety�

���� TEYSSI�ERE� G� ����a� �Nonlinear� Semiparametric� and Seminonparametric Long�Memory ARCH Models��� mimeo Humboldt Universit�at zu Berlin� Institut f�ur Statistik und�Okonometrie� and GREQAM�

���� TEYSSI�ERE� G� ����b� �Double Long�Memory Financial Time Series�� GREQAM DT

�B��� Revised January ���� �rst version March ���� Paper presented to the ��� Societyfor Economic Dynamics Conference� and ��� Econometric Society European Meeting�

���� TEYSSI�ERE� G� ����� � Multivariate Long�Memory ARCH Modelling for High FrequencyForeign Exchange Rates�� In Proceedings of the Second High Frequency Data in Finance

Conference� HFDF�II� Olsen # Associates� �� April ���� Zurich� Switzerland�

��� WHITTLE� P� ����� �Gaussian Estimation in Stationary Time Series�� Bulletin of the

International Statistical Institute� ��� ��������

�

A Estimation results

Table � Estimation results of bivariate long�memory ARCH process� with constant conditionalcorrelation� model �A�� �Robust t�statistics between parentheses��

�i� ������� �ii� ������� �iii� ������ �iv� �������

�� ������� ������� ������� ������� ������� ������ ������� �������

�� ������� ������� ������ ������ ������ ���� ������ �������

p� ������ ������ ������ ������ ������ ������ ������ ������

p� ����� ������ $ ����� ������ ����� ������

q� ������ ���� ������ ����� ������ ������ ����� ������

q� ������ ����� $ ������ ������ ������ ������

� ����� ������� ����� ������� ����� ������ ������ �������

Log�lik ��������� ��������� ��������� ����������

Table � Estimation results of bivariate long�memory ARCH process� with constant conditionalcorrelation� model �B�� �Robust t�statistics between parentheses��

�i� ������� �ii� ������� �iii� ������ �iv� �������

�� ������� ������ ������� ������� ������� ������ ������� �������

�� ������ ����� ������ ������ ������� ����� ������� �������

p� ����� ����� ������ ������ ������ ����� ������ �����

p� ����� ����� $ ����� ������ ������ ������

q� ������ ������ ����� ������ ������ ������ ������ �����

q� ������ ������ $ ����� ����� ����� ������

� ������ ������ ����� ������ ������ ������ ������ ������

� ������ ������� ������ ������� ������ ������ ������ ������

Log�lik ������� �������� ���������� ����������

�

Table � Estimation results of bivariate CCC FIGARCH� model �C�� �Robust t�statistics betweenparentheses��

�i� ������� �ii� ������� �iii� ������ �iv� �������

�� ������� ������� ������� ������ ������� ������� ������ �����

�� ������� ������� ������ ������ ������ ����� ������� �������

� ����� ������ ������ ����� ����� ������ ����� ������

� ������ ����� ������ ����� ����� ����� ����� �����

�� ������ ������ ������ ������ ������ ������ ������ ������

�� ������ ����� $ ����� ������ ������ ������

q� ������ ������ ������ ������ ������ ����� ������ ������

q� ������ ������ $ ������ ������ ������ ������

� ������ ������ ������ ������ ����� ������ ����� ������

� ������ ������ $ ������ ������ ������ ������

� ������ ������� ������ ������� ������ ������� ����� ������

Log�lik ���������� ��������� ��������� ����������

�

Table � Estimation results of bivariate long�memory ARCH process� model �D�� �Robust t�statistics between parentheses��

�i� ������� �ii� ������� �iii� ������ �iv� �������

�� ������ ������ ������ ������ ������� ������ ������� �������

�� ������ ������ ������ ������ ������� ������� ������� ������

p� ����� ������ ������ ������ ����� ����� ������ ������

p� ����� ������ ���� ����� ������ ������ ������ �����

p� ������ ������ ������ ����� ����� ������ ����� ������

q� ������ ������ ������ ������ ����� ����� ����� �����

q� ����� ������ $ ������ ������ ������ ������

q� ������ ������ $ ������ ������ ������ ������

Log�lik ��������� ���������� ��������� ����������

Table � Estimation results of the unrestricted bivariate FIGARCH� model �E�� �Robust t�statistics between parentheses��

�i� ������� �ii� ������� �iii� ������ �iv� �������

�� ����� ������ ������� ���� ������� ������� ������� �������

�� ������� ������� ������� ������� ������� ������� ������� �������

� ����� ������ ����� ������ ������ ������ ������ �����

� ���� ����� ����� ������ ����� ���� ������ �����

� ������ ������ ������ ������ ����� ����� ���� ������

�� ����� ����� ����� ������ ������ ����� ����� ������

�� ������ ����� $ ������ ������ ������ ������

�� ������ ���� $ ������ ������ ������ ������

q� ������ ����� ����� ������ ������ ����� ������ ������

q� ����� ������ $ ������ ����� ������ ������

q� ������ ������ $ ����� ������ ������ �����

� ������ ������ ������ ������ ������ ������ ������ ������

� ������ ������ ����� ������ ������ ������ ������ �����

� ������ ������ ������ ������ ������ ������ ������ ������

Log�lik ��������� ��������� ��������� ����������

�