Embed Size (px)

Citation preview

Modelling the Marketin a Risk-averse World(work in progress)

R.J. ThomsonActuarial Society Convention

2008

Modelling the Marketin a Risk-averse World

IntroductionModels of the market portfolioThe parameterisation of the modelsSummary

Introduction

SA data: 1987−2007‘returns’: real annual forces of return‘market portfolio’: listed equity & government bondsConditionally on information at the start of the year:

return on market portfolio normally distributed;market price of risk reasonably greater than 0

Introduction

Purpose of descriptive models: to inform the definition of predictive modelsPurpose of estimation: to derive ex-post estimates of ex-ante parametersRational-expectations hypothesis: applied so far as possibleRisk-free rate not primarily an explanatory variable: primarily to establish a minimum ex-ante expected value of return on market portfolioNot an attempt to obtain ‘the real-world’ model

Models of the market portfolio:the basic model

; ; ;M t I t tg hδ δ σε= + +

; is the risk-free rate;I tδ

. . .~ (0,1).

i i d

t Nε

* 1 and * 0;* 1.2 and * 0; or * 1 and * 0,01

g g h hg h g h

≥ ≥ ≥ ≥= = = =

where:

Models of the market portfolio:the regime-switching model

where:

{ }0,1 ;tS ∈

{ }1 00Pr 0 | 0 ;t tS S p−= = =

{ }1 01 00Pr 1| 0 1 ;t tS S p p−= = = = −

; ;t t t

{ }1 10Pr 0 | 1 ; andt tS S p−= = =

{ }1 11 10Pr 1| 1 1 .t tS S p p−= = = = −

M t S I t S S tg hδ δ σ ε= + +

* *

* *

1 and 0;

1,2 and 0; or * 1 and * 0,01s s s s

s s

g g h h

g h g h

≥ ≥ ≥ ≥

= = = =

Models of the market portfolio:the exponential autoregressive model

( ){ }; ; ; 1 ; 1expM t I t M t I t M tg h gδ δ α δ δ σ ε− −= + − +

Models of the market portfolio:the ARCH model

; ;M t I t tg h zδ δ= + +

where:t t tz σ ε=2 2

1t ta bzσ −= +

The parameterisation of the models

Maximum-likelihood estimates95% confidence limitsAkaike Information Criterion:

Mean market price of risk:

Bias:

2 2A k l= −

ˆˆ

M I

M

R μ δσ

−=

ˆM MB δ μ= −

Parameterisation:basic model

constraints Parameter Details basic g = 1 h = 0

g estimate 1,59 1,76 confidence limits 1; 3,8 1; 2,9h estimate 0,012 0,039 confidence limits 0; 0,14 0; 0,11σM estimate 0,163 0,160 0,159 confidence limits 0,11; 0,21 0,11; 0,21 0,11; 0,20k 3 2 2l 9,28 9,15 9,30A –12,56 –14,30 –14,60R 0,24 0,24 0,22B 0 0 0,004

Parameterisation: basic model:δM:t vs. δI:t

-0,30

-0,20

-0,10

0,00

0,10

0,20

0,30

0,40

0,50

0,00 0,02 0,04 0,06 0,08 0,10 0,12 0,14

dI;t

dM;t

Observed estimate conf limit

Parameterisation:basic model: time series

-0,3

-0,2

-0,1

0,0

0,1

0,2

0,3

0,4

0,5

1987 1990 1993 1996 1999 2002 2005

Year

dM,t dI,t Estimate Conf limit

Parameterisation:basic model: Q-Q plot

-0,3

-0,2

-0,1

0,0

0,1

0,2

0,3

-0,3 -0,2 -0,1 0,0 0,1 0,2 0,3

Parameterisation:regime-switching model

Parameter p00 0p10 0,24g0 2,96h0 0σ0 0,009g1 1,2h1 0,007σ1 0,162l 13,25k 7A –12,50R 0,56B –0,051

Parameterisation: regime-switching model: δM:t vs. δI:t

-0,30

-0,20

-0,10

0,00

0,10

0,20

0,30

0,40

0,50

0,00 0,02 0,04 0,06 0,08 0,10 0,12 0,14

dI;t

dM;t

Observed estimate regime 0 conf limit regime 0estimate regime 1 conf limit regime 1

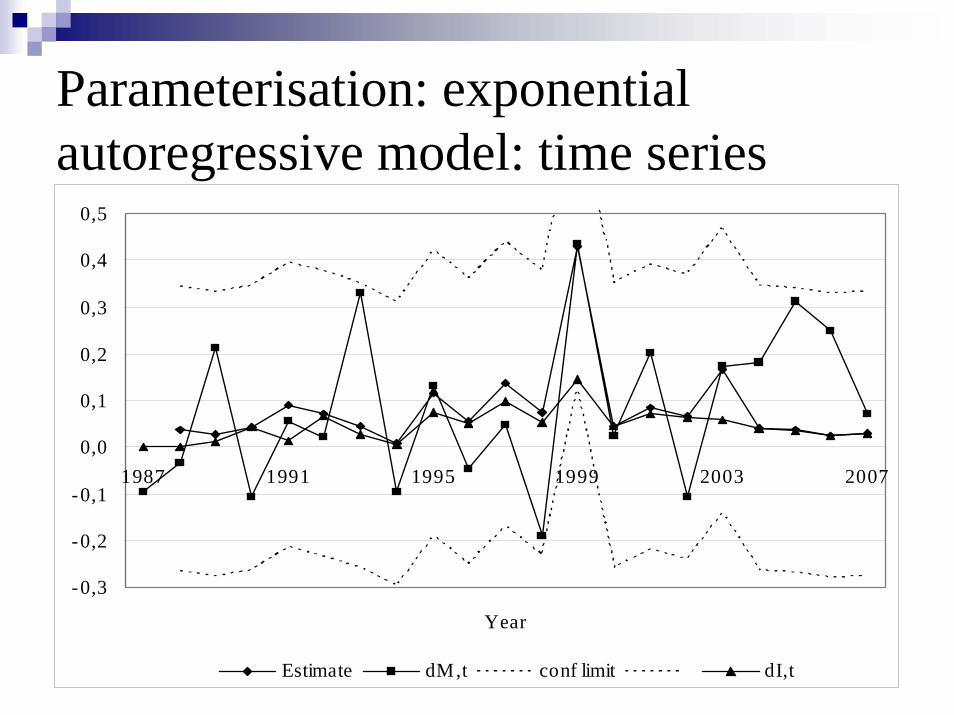

Parameterisation: exponential autoregressive model

Parameter Details α estimate –13,75 confidence limits –16,9; 3,0g estimate 1 confidence limits 1; 2,1h estimate 0,01 confidence limits 0,01; 0,06σM estimate 0,155 confidence limits 0,11; 0,22k 2l 10,34A –16,68R 0,23B 0,003

Parameterisation: exponential autoregressive model: time series

-0,3

-0,2

-0,1

0,0

0,1

0,2

0,3

0,4

0,5

1987 1991 1995 1999 2003 2007

Year

Estimate dM,t conf limit dI,t

Parameterisation: exponential autoregressive model: Q-Q plot

-0,3

-0,2

-0,1

0,0

0,1

0,2

0,3

-0,3 -0,2 -0,1 0,0 0,1 0,2 0,3

Parameterisation: ARCH model

Parameter Details estimate 1,76g confidence limits 1; 2,9

h 0estimate 0,025a confidence limits 0,021; 0,029estimate 0b confidence limits 0; 0,04

k 2l 9,30A –14,60R 0,22B 0,004

Summary

Model Criterion basic regime-switching exponential AR A –14,60 –12,50 –16,68R 0,22 0,56 0,23B 0,004 –0,051 0,003

Problems with the exponential AR model

g = 1; h = 0,01spuriously good fit in 1999inaccuracy of adjustment for different periodconfidence limits of α: −16,9; 3,0allowance for ex-ante means exacerbate the problems

So rather use the basic model

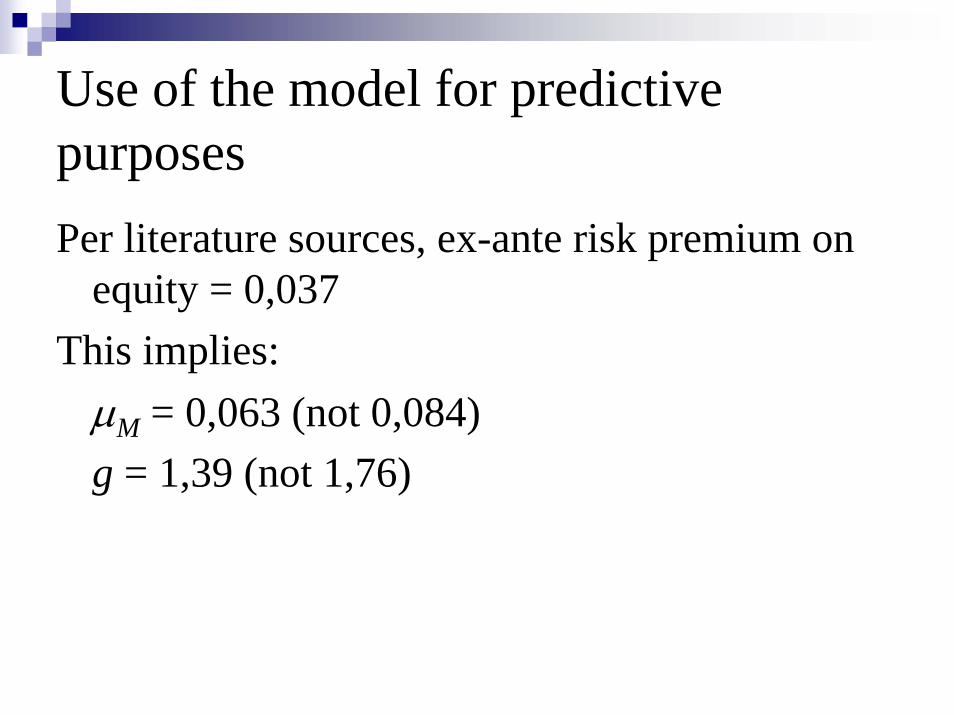

Use of the model for predictive purposesPer literature sources, ex-ante risk premium on

equity = 0,037This implies:

μM = 0,063 (not 0,084)g = 1,39 (not 1,76)

Conclusion

; ;M t I t M tgδ δ σ ε= +

where:

1,39g =

0,159Mσ =

Caveat

Lessons from the global financial crisis:a lower risk premiumhigher volatilitya fatter downside tail

But:governments may bail out the financial institutions