Embed Size (px)

Citation preview

One-year performance (Rel to Sensex)

Source: Capitaline

Mold-Tek Packaging (MTPL)

PRICE: RS.197 RECOMMENDATION: BUYTARGET PRICE: RS.260 FY18E PE: 12.5X

Stock details

BSE code : 533080

NSE code : MOLDTKPAC

Market cap (Rs mn) : 5,423

Free float (%) : 65

52 wk Hi/Lo (Rs) : 217 / 103.8

Avg daily volume (mn) : 60,172

Shares (o/s) (mn) : 27.7

Summary table(Rs mn) FY16 FY17E FY18E

Sales 2,757 3,019 3,812Growth (%) (3.3) 9.5 26.3EBITDA 458 553 754EBITDA margin (%) 16.6 18.3 19.8PBT 368 468 654Net profit 241 314 436Adj EPS (Rs) 8.7 11.3 15.7Growth (%) 42.8 30.1 39.0CEPS (Rs) 11.8 14.5 19.4BV (Rs/share) 47 56 70Dividend / share (Rs) 3.25 3.25 3.50ROE (%) 18.7 20.2 22.6ROCE (%) 18.6 19.9 23.5Net cash (debt) (251) (247) (239)EV/EBITDA (x) 12.5 10.4 7.6EV/Sales (x) 2.1 1.9 1.5P/E (x) 22.6 17.4 12.5P/CEPS (x) 16.7 13.6 10.1P/BV (x) 4.2 3.5 2.8

Source: Company,Kotak Securities - Private Client Research

INITIATING COVERAGEOCTOBER 5, 2016

PRIVATE CLIENT RESEARCH

Shareholding pattern

Source: Capitaline

Jatin [email protected]+91 22 6218 6440

Volume-led-growthMold Tek Packaging stands to gain in the coming years from the increas-ing share of In-Mold labelling (IML) products, backward integration andexpansion in to food and FMCG industry, which would aid profitability.Going ahead, incremental volume is likely to come from IML, therebytaking a proportion of IML in the overall revenue mix to 60% by the endof FY18E from 45% currently. We expect net sales to grow at CAGR of18% during FY16-FY18E supported by 20% growth in sales volume,while EBITDA/KG is likely to increase to Rs31/kg by end of FY18E fromRs27.5/kg in 1QFY17. Large replacement market and better utilisation ofassets make this a good investment opportunity with return ratio ofover 20% in FY17E and FY18E. At CMP, stock trades at 17.4x/12.5x FY17E/FY18E earnings. We initiate coverage with a BUY rating, and a targetprice of Rs260, valuing it at 16.5x FY18E earnings.

Key investment argument

First mover advantage of IML in India: MTPL was the first company tooffer IML technology in 2011, while others were focusing on screen print-ing and heat transfer labelling (HTL). IML is a high margin (300-400bpshigher) technology compared to the traditional methods. Given the higherdurability and better aesthetics of IML products, as compared to screenprinting, majority of the clients are slowly shifting towards IML. Goingahead, with incremental volumes likely to come from lubricants and foodFMCG industry, the share of IML in the overall revenue mix is likely to in-crease to 60% by end of FY18E from 45% in FY16. This would lead to ex-pansion in EBITDA margin to 19.8% by end of FY18E (EBITDA/kg to Rs31) vs16.6% in FY16.

MTPL is a fully integrated player: Mold-Tek Packaging (MTPL) hasemerged as one of the leading manufacturers and suppliers of high qualityairtight and pilfer proof containers/pails in India with an installed capacityof 28,800 tonnes per annum for paints, lubricants, food and FMCG (in-cludes Edible Oil) industries. The company is a pioneer in introducing In-Mold labelling (IML) containers (high margin products) in India. In housetool rooms for mold and robot manufacturing, printing of labels and die-cutting, etc make MTPL a fully integrated player. Infact, Mold-tek is theonly packaging Company in the world to manufacture robots in house. Thecompany has recently developed pails to target Rs12bn edible oil market.In addition, the company has also started focusing more on FMCG industryto increase the share of high margin products (IML), as margin in IML con-tainers in food and FMCG industry is 300-400bps higher than lubricant andpaint industry.

Eyeing FMCG industry to deliver growth: Lubricants and paint industrycontribute nearly 94% of the overall revenue, with Asian paints andCastrol being the largest customers. However, going ahead, incrementalrevenue is likely to come from the food and FMCG industries. The companyhas prepared "square" pails to target Rs12bn (blow mold and tin contain-ers) edible oil industry. To start with, the company is targeting blow moldpackaging (Rs9bn market). Edible oil makers such as Allana, Conagro, andHealthy Hearts, to name a few, have already approved the pails. Thoughtraction on this front is low, management is targetting 6-7% of the market(Rs840 mn) by end of FY18E. In addition, the company has also received

Kotak Securities Limited has two independent equity research groups: Institutional Equities and Private Client Group. This report has been pre-pared by the Private Client Group. The views and opinions expressed in this document may or may not match or may be contrary with the views,estimates, rating, target price of the Institutional Equities Research Group of Kotak Securities Limited.

Promoter35%

FII3%

DI16%

Others46%

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 2

INITIATING COVERAGE October 5, 2016

approval from P&G and Cadbury to supply pails. At the same time, the com-pany is awaiting approval from other FMCG companies. With the growingdemand, the overall contribution from FMCG and Food industry is likely toincrease to 12% by the end of FY18E from 5% currently.

Strategically located: MTPL has 7 manufacturing units in India with an in-stalled capacity of 2,400 tonnes per month. All the units are strategically lo-cated near customer locations, except unit 1 (Hyderabad). Key benefits ofsetting up a plant near customers are i) it helps in saving transportationcosts; and ii) can provide on-time delivery and which also helps the companyto garner 5-8% additional business.

RAK to support earnings: MTPL just commissioned 2500 tonnes capacityof Pails at RAK, UAE with a capex of Rs150 mn. This plant would serve therequirements of paints, lube and the dairy industry in UAE and Iran. With nomajor players in RAK, MTPL is expected to post revenue of Rs300 mn inFY18E. RAK plant has already received orders from Shell, Akzo Nobel, RAKPaints and Dates to name a few. RAK unit would have a superior margincompared to the domestic business due to cheaper raw material cost andexemption of income tax. Management expects RAK unit to have 300bpshigher PAT margin compared to the domestic business.

Investment opportunity with return ratios of over 20%: Volume growthof 20% in last two quarters, coupled with a strong volume guidance in thecoming years and increasing share of IML in the overall revenue mix, makesus believe that company could be a good investment idea with a return ratioof over 20% in the coming years. We expect MTPL to continue deliveringstrong growth in the coming years on the back of integrated facilities andincreasing revenue from the high margin FMCG industry. At CMP, stocktrades at 17.4x/12.5x FY17E/FY18E earnings. We initiate coverage with aBUY rating, and a target price of Rs260, valuing it at 16.5x FY18E earnings.

Key Risks: Slower than expected pick-up in edible oil business; slower thanexpected ramp-up at RAK facilities

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 3

INITIATING COVERAGE October 5, 2016

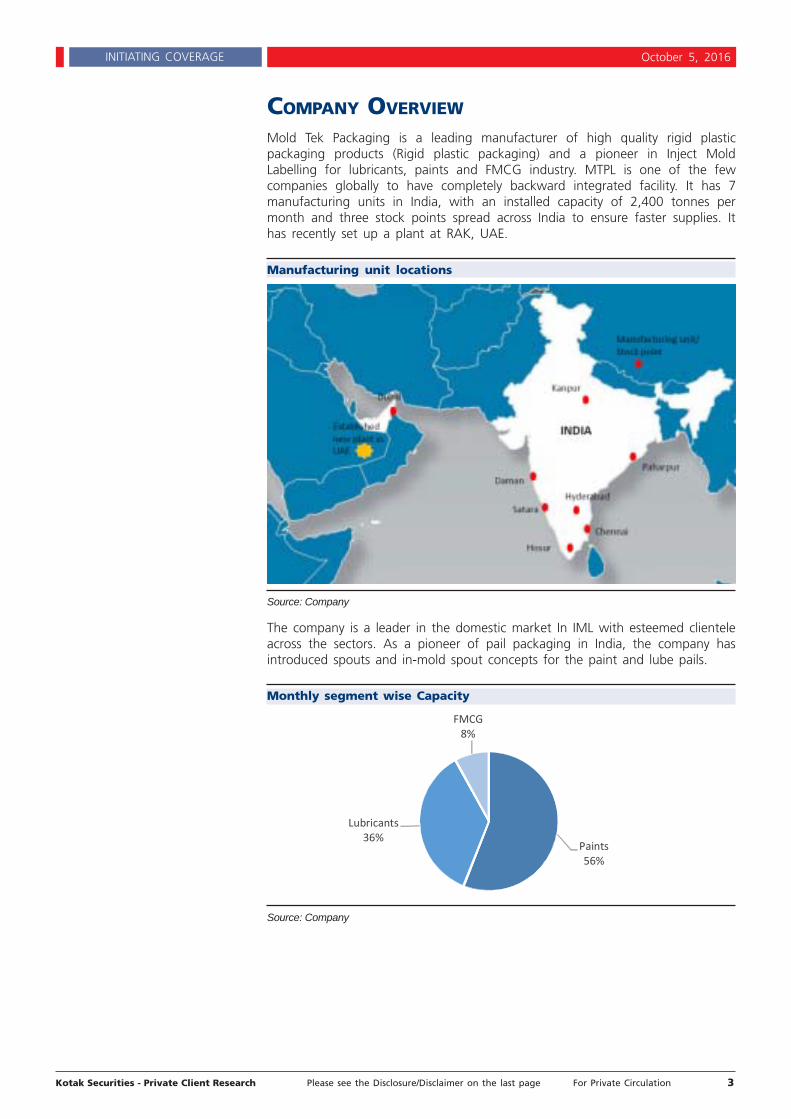

COMPANY OVERVIEW

Mold Tek Packaging is a leading manufacturer of high quality rigid plasticpackaging products (Rigid plastic packaging) and a pioneer in Inject MoldLabelling for lubricants, paints and FMCG industry. MTPL is one of the fewcompanies globally to have completely backward integrated facility. It has 7manufacturing units in India, with an installed capacity of 2,400 tonnes permonth and three stock points spread across India to ensure faster supplies. Ithas recently set up a plant at RAK, UAE.

Manufacturing unit locations

Source: Company

The company is a leader in the domestic market In IML with esteemed clienteleacross the sectors. As a pioneer of pail packaging in India, the company hasintroduced spouts and in-mold spout concepts for the paint and lube pails.

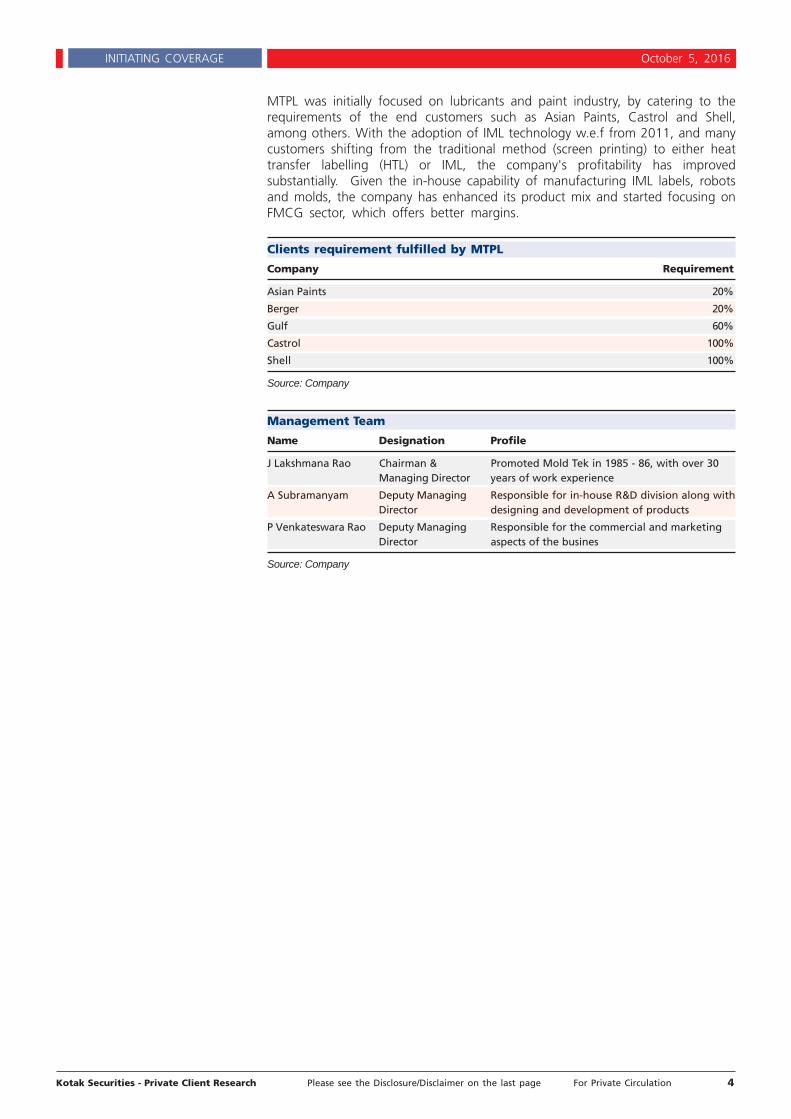

Monthly segment wise Capacity

Source: Company

Paints56%

Lubricants36%

FMCG8%

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 4

INITIATING COVERAGE October 5, 2016

MTPL was initially focused on lubricants and paint industry, by catering to therequirements of the end customers such as Asian Paints, Castrol and Shell,among others. With the adoption of IML technology w.e.f from 2011, and manycustomers shifting from the traditional method (screen printing) to either heattransfer labelling (HTL) or IML, the company's profitability has improvedsubstantially. Given the in-house capability of manufacturing IML labels, robotsand molds, the company has enhanced its product mix and started focusing onFMCG sector, which offers better margins.

Clients requirement fulfilled by MTPL

Company Requirement

Asian Paints 20%

Berger 20%

Gulf 60%

Castrol 100%

Shell 100%

Source: Company

Management Team

Name Designation Profile

J Lakshmana Rao Chairman & Promoted Mold Tek in 1985 - 86, with over 30Managing Director years of work experience

A Subramanyam Deputy Managing Responsible for in-house R&D division along withDirector designing and development of products

P Venkateswara Rao Deputy Managing Responsible for the commercial and marketingDirector aspects of the busines

Source: Company

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 5

INITIATING COVERAGE October 5, 2016

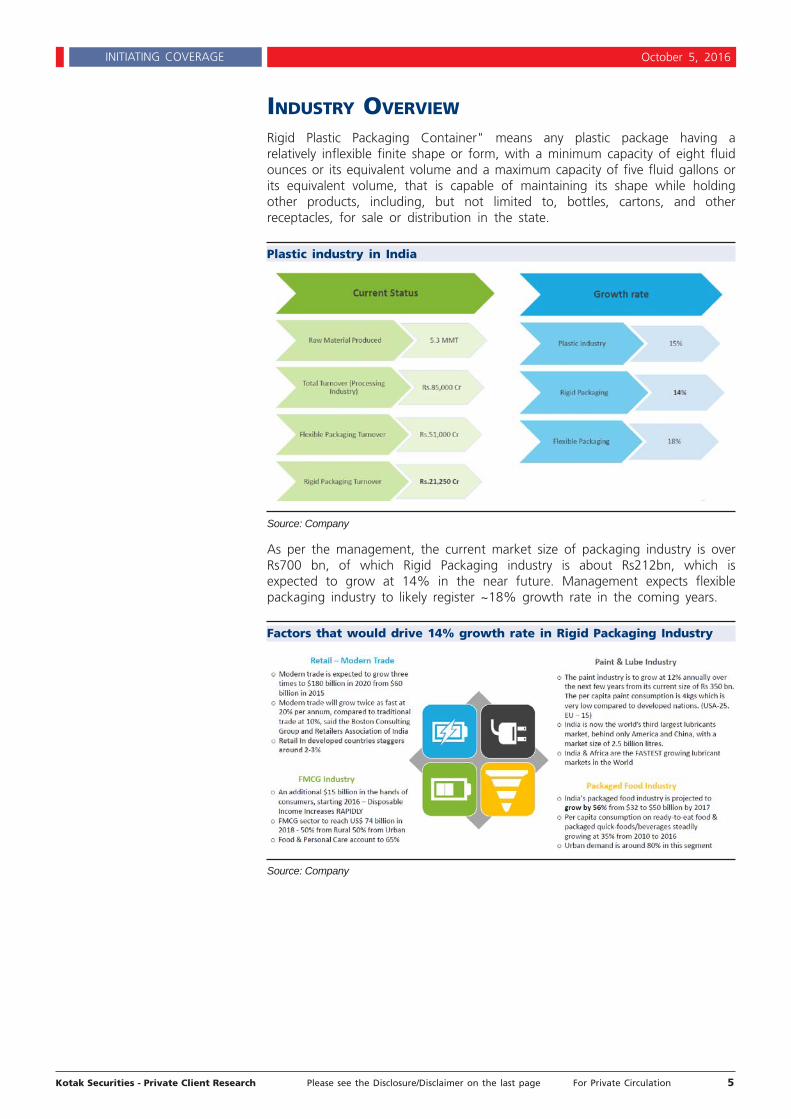

INDUSTRY OVERVIEW

Rigid Plastic Packaging Container" means any plastic package having arelatively inflexible finite shape or form, with a minimum capacity of eight fluidounces or its equivalent volume and a maximum capacity of five fluid gallons orits equivalent volume, that is capable of maintaining its shape while holdingother products, including, but not limited to, bottles, cartons, and otherreceptacles, for sale or distribution in the state.

Plastic industry in India

Source: Company

As per the management, the current market size of packaging industry is overRs700 bn, of which Rigid Packaging industry is about Rs212bn, which isexpected to grow at 14% in the near future. Management expects flexiblepackaging industry to likely register ~18% growth rate in the coming years.

Factors that would drive 14% growth rate in Rigid Packaging Industry

Source: Company

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 6

INITIATING COVERAGE October 5, 2016

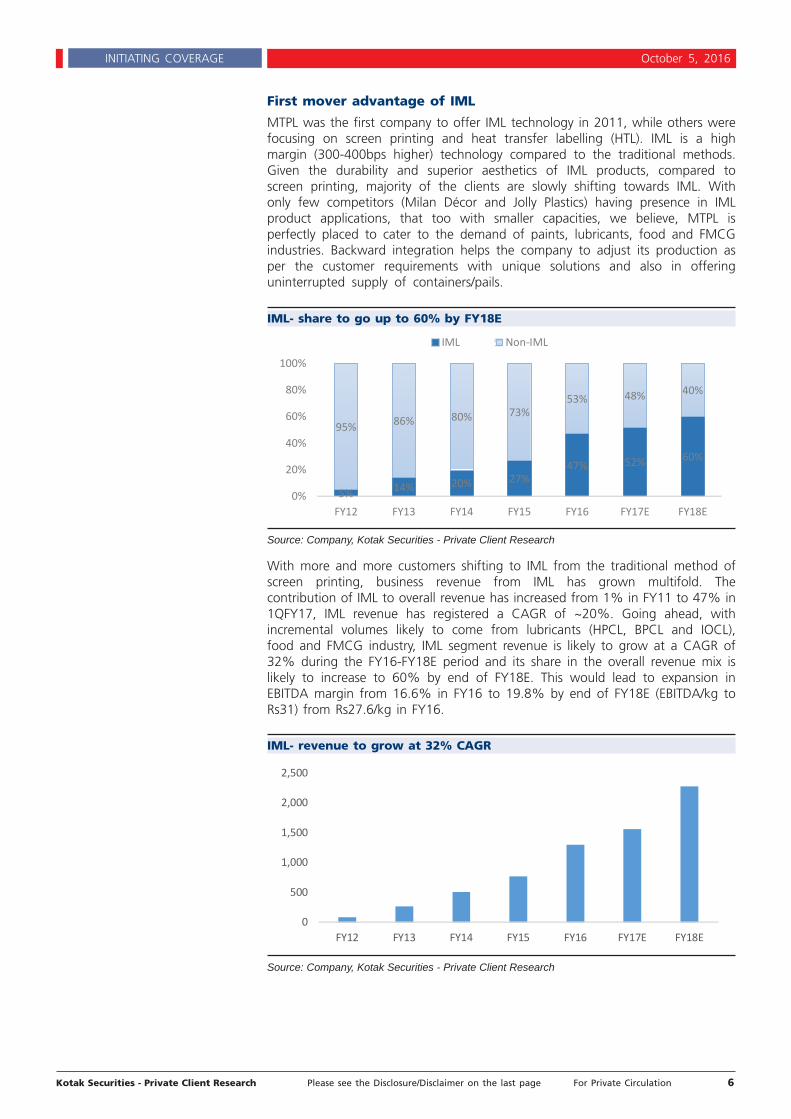

First mover advantage of IML

MTPL was the first company to offer IML technology in 2011, while others werefocusing on screen printing and heat transfer labelling (HTL). IML is a highmargin (300-400bps higher) technology compared to the traditional methods.Given the durability and superior aesthetics of IML products, compared toscreen printing, majority of the clients are slowly shifting towards IML. Withonly few competitors (Milan Décor and Jolly Plastics) having presence in IMLproduct applications, that too with smaller capacities, we believe, MTPL isperfectly placed to cater to the demand of paints, lubricants, food and FMCGindustries. Backward integration helps the company to adjust its production asper the customer requirements with unique solutions and also in offeringuninterrupted supply of containers/pails.

IML- share to go up to 60% by FY18E

Source: Company, Kotak Securities - Private Client Research

With more and more customers shifting to IML from the traditional method ofscreen printing, business revenue from IML has grown multifold. Thecontribution of IML to overall revenue has increased from 1% in FY11 to 47% in1QFY17, IML revenue has registered a CAGR of ~20%. Going ahead, withincremental volumes likely to come from lubricants (HPCL, BPCL and IOCL),food and FMCG industry, IML segment revenue is likely to grow at a CAGR of32% during the FY16-FY18E period and its share in the overall revenue mix islikely to increase to 60% by end of FY18E. This would lead to expansion inEBITDA margin from 16.6% in FY16 to 19.8% by end of FY18E (EBITDA/kg toRs31) from Rs27.6/kg in FY16.

IML- revenue to grow at 32% CAGR

Source: Company, Kotak Securities - Private Client Research

5% 14% 20% 27%47% 52% 60%

95% 86% 80% 73%53% 48% 40%

0%

20%

40%

60%

80%

100%

FY12 FY13 FY14 FY15 FY16 FY17E FY18E

IML Non-IML

0

500

1,000

1,500

2,000

2,500

FY12 FY13 FY14 FY15 FY16 FY17E FY18E

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 7

INITIATING COVERAGE October 5, 2016

MTPL is pioneer in providing IML technology, with in-house manufacturing ofrobots. IML, is the most efficient and effective method of decoration for plasticspackaging, where a printed film PP label (medium for high resolution and photo-realistic image reproduction) is placed on the mold container/pails by robots. Asthe molding and labelling of the product takes place as a single-step process,the hygiene of the pack is assured. The technology and finishing assuredistinguishing a product at the point of sale, with a certainty resulting in salesgrowth of the customer's brand. The key differentiator between IML and screenprinting, heat transfer labelling and shrink sleeving, is that latter technologycovers only 40-70% of the container/pails that too limitation on number ofcolors (Maximum 3-4). While, IML can cover 100%, with the multiple colorsphotographic quality and that too at a faster pace (low lead time) and "nohuman" contact.

IML process

Source: Company

IML product range

Source: Company

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 8

INITIATING COVERAGE October 5, 2016

Backward integration a key strength - only packaging company inthe world to manufacture "ROBOTS".

MTPL is a vertically integrated company with centralized tool room atHyderabad to design, develop and manufacture molds and robots. In addition,the company also has an in-house label making facility. It is the only company inIndia, to make in-house robots with the help of efficient tool rooms andexperienced engineers. MTPL is the only company to give laminated technology.

Having a presence across the value chain, i.e from making a robot to the endproducts, helps MTPL to serve the customer requirements in an efficientmanner. Secondly, it helps the company to develop innovative products to stayahead of the curve, as it operates in a dynamic industry. The company currentlyhas 42 Robots and is developing one more for the FMCG industry.

In-house tool room helps the company, to develop new products at lower costs,quicker maintenance at the time of shutdown and on-time delivery of products.As per management, having an in-house facility helps the company not only todevelop new products but that too at a lower cost compared to the outsourcedmold or a robot or label making. For instance, in-house mold making is almost30% cheaper than imported or outsourced mold, in-house development of robotis 50% cheaper and in-house label making is 30% cheaper.

We believe, in-house facility, helps the company to offer quality product andend-to-end service at competitive prices. Since there are hardly any competitorsin IML, the company enjoys larger share. Couple of unlisted companies fromDaman, have developed IML products and given for testing. Going ahead, webelieve, competition in the IML space would increase, but cost factors would bethe key thing to watch.

Management believes that increase in competition would augur well for thecompany, as competitors would not be as cost effective as MTPL and wouldprice their product at a higher rate. This would give MTPL room to increase itsproduct prices, which would boost its overall profitability.

Vertically integrated business model, coupled with increasing share of IMLproducts, would help the company to report healthy EBITDA margins in thecoming years. We expect EBITDA margin to remain in the range of 19-20% inFY18E.

Exhibit: Toolroom

Source: Company

Exhibit: Robot to produce containers

Source: Company

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 9

INITIATING COVERAGE October 5, 2016

EBITDA Margin to strengthen

Source: Company, Kotak Securities - Private Client Research

FMCG industry to support growth

Lubricants and paint industries contribute nearly 94% of the overall revenue,with Asian paints and Castrol being the largest customer. However, goingahead, the incremental revenue is likely to come from food and FMCGindustries. The company has prepared "square" pails to target Rs12bn (blowmolded and tin containers) edible oil industry. To start with the company istargeting blow mold packaging (Rs 5 bn market). Edible oil makers such asAllana, Conagro, and Healthy Hearts, to name a few have already approved thepails. Though traction on this front is low, management expects to capture 6-7% of the market by end of FY18E. In addition, the company has also receivedapproval from P&G and Cadbury to supply pails. At the same time, the companyis awaiting approval from other FMCG companies. With the growing demand,the overall contribution from FMCG and Food industry is likely to increase to12% by the end of FY18E from 5% currently.

The company has also launched a couple of products for Cadbury recently,which would help the company to garner incremental revenue of Rs120mnannually from Cadbury.

MTPL is also working closely with P&G to develop container/pail for one of theirproducts. If tested successfully and approved by the customer, it would help thecompany garner incremental revenue of Rs50-60mn annually. Besides this, thecompany has given its product concepts for approval to various other FMCGcompanies, which can bring additional revenue of Rs200-250mn annually

New marketing approach - Packaging solutions

Source: Company

0.0

5.0

10.0

15.0

20.0

25.0

0

200

400

600

800

1000

FY14 FY15 FY16 FY17e FY18e

EBITDA (Rs Mn - LHS) EBITDA Margin (% - RHS)

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 10

INITIATING COVERAGE October 5, 2016

Edible oil - can be a game changer

MTPL, has recently developed square shape pails, of 5 & 15 ltr capacityespecially to cater to the edible oil industry (blow mold + tin containers),thereby expanding its presence beyond traditional lubricants and paint industry.To cater to the demand of edible oil industry, which is estimated to be Rs12bnmarket, the company has expanded its capacity by 800 tonnes per annum atHyderabad, Satara and Daman. The edible oil companies using IML products areAdani Wilmar, Conagro and Marico. The company has also given its product fortesting and approval purpose to other companies. The traction in Edible oil isnot as per expected lines and pick up is at a tapid pace.

MTPL has enough head room and facility to cater to incremental demand fromthe edible oil industry. The company, has developed 5ltr and 15ltr square pails tocapture market share from blow mold and tin containers.

Edible Oil - Market Size

5 ltr 15 ltr

Market Size 12 lacs / per month 5 lacs / per month

Current Capacity 5 lacs / per month 2 lacs / per month

Source: Company

Hence the management stated that edible oil industry is Rs12bn market, ofwhich blow mold is Rs4-5bn and remaining is Tin containers. The company isinitially targeting Rs4-5bn market, where they intend to replace blow moldproducts with IML produce square pails. Few edible oil companies have alreadyapproved the products and they might launch them in future. Ghodawat hasalready started taking deliveries of the pails and has given assurance of longterm association with the company. Though traction is currently low, if productsget accepted by the customers, it would entice others to follow suit and bringincremental volume for MTPL. Company is also offering these attractive anduser friendly square pails to other food value added FMCG products.

Lubricant segment to contribute revenue growth in FY17E & FY18E

The company has recently bagged orders from HPCL, BPCL and IOCL to thetune of Rs500mn for supplying IML pails for the period of 3years, starting FY17.The deliveries for the same have started from the month of June 2016. MTPL isthe lone supplier of IML pails to all three PSU's. Given the strong volume growthin the existing business coupled with incremental revenue coming fromlubricants and FMCG industry, we expect revenue to grow at 18% CAGR duringthe FY16-FY18E period.

RAK - growth driver

MTPL has just commissioned 2,500 tonnes capacity of Pails and containers atRAK, UAE with a capex of Rs150mn. This plant would serve the requirements ofpaints, lube and the dairy industry in UAE and Iran. With no major players inRAK, MTPL is expected to post revenue of Rs300mn in FY18E. RAK plants hasalready received order from Shell, Akzo Nobel, RAK Paints and a Dates to namea few. RAK units would have a superior margin compared to the domesticbusiness due to cheaper raw materials cost and exemption of Income Tax.Management expects RAK unit to have 300bps higher PAT margin compared tothe domestic business (due to tax saving). In domestic business, company paystax at the rate of 33-34%, while the income from RAK is tax free.

Square shape pails

Source: Company

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 11

INITIATING COVERAGE October 5, 2016

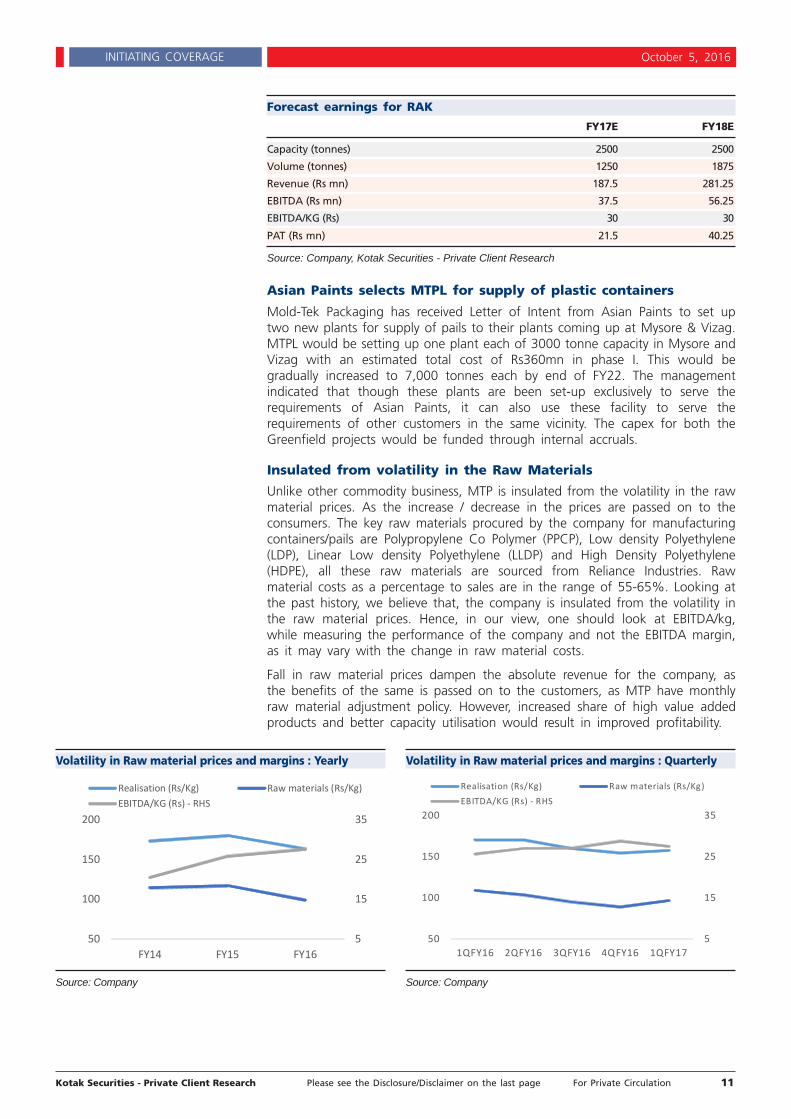

Forecast earnings for RAK

FY17E FY18E

Capacity (tonnes) 2500 2500

Volume (tonnes) 1250 1875

Revenue (Rs mn) 187.5 281.25

EBITDA (Rs mn) 37.5 56.25

EBITDA/KG (Rs) 30 30

PAT (Rs mn) 21.5 40.25

Source: Company, Kotak Securities - Private Client Research

Asian Paints selects MTPL for supply of plastic containers

Mold-Tek Packaging has received Letter of Intent from Asian Paints to set uptwo new plants for supply of pails to their plants coming up at Mysore & Vizag.MTPL would be setting up one plant each of 3000 tonne capacity in Mysore andVizag with an estimated total cost of Rs360mn in phase I. This would begradually increased to 7,000 tonnes each by end of FY22. The managementindicated that though these plants are been set-up exclusively to serve therequirements of Asian Paints, it can also use these facility to serve therequirements of other customers in the same vicinity. The capex for both theGreenfield projects would be funded through internal accruals.

Insulated from volatility in the Raw Materials

Unlike other commodity business, MTP is insulated from the volatility in the rawmaterial prices. As the increase / decrease in the prices are passed on to theconsumers. The key raw materials procured by the company for manufacturingcontainers/pails are Polypropylene Co Polymer (PPCP), Low density Polyethylene(LDP), Linear Low density Polyethylene (LLDP) and High Density Polyethylene(HDPE), all these raw materials are sourced from Reliance Industries. Rawmaterial costs as a percentage to sales are in the range of 55-65%. Looking atthe past history, we believe that, the company is insulated from the volatility inthe raw material prices. Hence, in our view, one should look at EBITDA/kg,while measuring the performance of the company and not the EBITDA margin,as it may vary with the change in raw material costs.

Fall in raw material prices dampen the absolute revenue for the company, asthe benefits of the same is passed on to the customers, as MTP have monthlyraw material adjustment policy. However, increased share of high value addedproducts and better capacity utilisation would result in improved profitability.

Volatility in Raw material prices and margins : Yearly

Source: Company

Volatility in Raw material prices and margins : Quarterly

Source: Company

5

15

25

35

50

100

150

200

FY14 FY15 FY16

Realisation (Rs/Kg) Raw materials (Rs/Kg)EBITDA/KG (Rs) - RHS

5

15

25

35

50

100

150

200

1QFY16 2QFY16 3QFY16 4QFY16 1QFY17

Realisation (Rs/Kg) Raw materials (Rs/Kg)EBITDA/KG (Rs) - RHS

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 12

INITIATING COVERAGE October 5, 2016

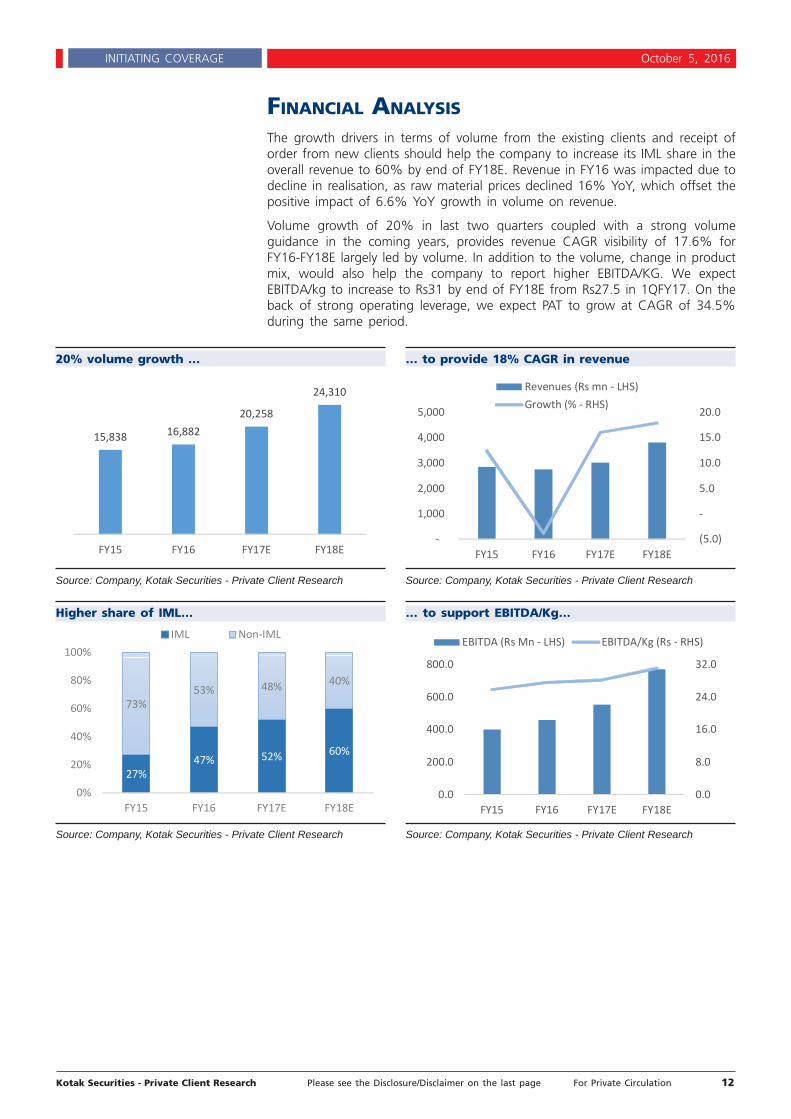

FINANCIAL ANALYSIS

The growth drivers in terms of volume from the existing clients and receipt oforder from new clients should help the company to increase its IML share in theoverall revenue to 60% by end of FY18E. Revenue in FY16 was impacted due todecline in realisation, as raw material prices declined 16% YoY, which offset thepositive impact of 6.6% YoY growth in volume on revenue.

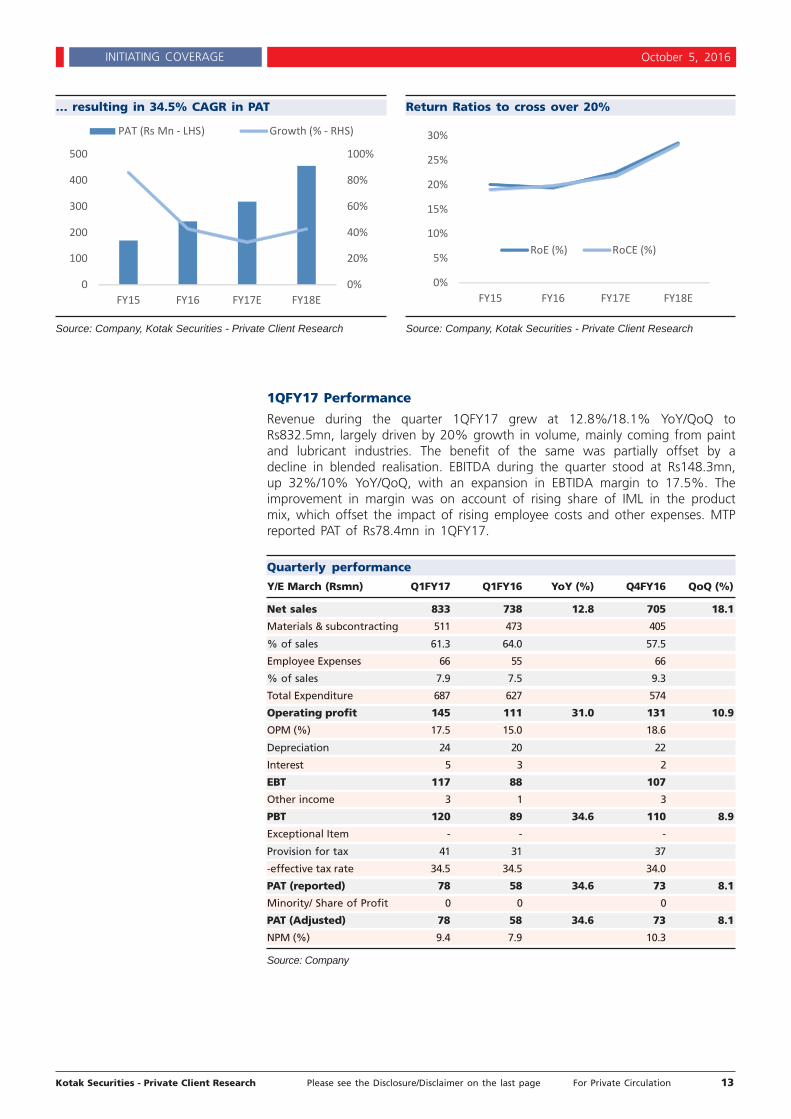

Volume growth of 20% in last two quarters coupled with a strong volumeguidance in the coming years, provides revenue CAGR visibility of 17.6% forFY16-FY18E largely led by volume. In addition to the volume, change in productmix, would also help the company to report higher EBITDA/KG. We expectEBITDA/kg to increase to Rs31 by end of FY18E from Rs27.5 in 1QFY17. On theback of strong operating leverage, we expect PAT to grow at CAGR of 34.5%during the same period.

20% volume growth …

Source: Company, Kotak Securities - Private Client Research

… to provide 18% CAGR in revenue

Source: Company, Kotak Securities - Private Client Research

Higher share of IML…

Source: Company, Kotak Securities - Private Client Research

… to support EBITDA/Kg…

Source: Company, Kotak Securities - Private Client Research

15,838 16,88220,258

24,310

FY15 FY16 FY17E FY18E (5.0)

-

5.0

10.0

15.0

20.0

-

1,000

2,000

3,000

4,000

5,000

FY15 FY16 FY17E FY18E

Revenues (Rs mn - LHS)Growth (% - RHS)

27%47% 52% 60%

73%53% 48% 40%

0%

20%

40%

60%

80%

100%

FY15 FY16 FY17E FY18E

IML Non-IML

0.0

8.0

16.0

24.0

32.0

0.0

200.0

400.0

600.0

800.0

FY15 FY16 FY17E FY18E

EBITDA (Rs Mn - LHS) EBITDA/Kg (Rs - RHS)

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 13

INITIATING COVERAGE October 5, 2016

1QFY17 Performance

Revenue during the quarter 1QFY17 grew at 12.8%/18.1% YoY/QoQ toRs832.5mn, largely driven by 20% growth in volume, mainly coming from paintand lubricant industries. The benefit of the same was partially offset by adecline in blended realisation. EBITDA during the quarter stood at Rs148.3mn,up 32%/10% YoY/QoQ, with an expansion in EBTIDA margin to 17.5%. Theimprovement in margin was on account of rising share of IML in the productmix, which offset the impact of rising employee costs and other expenses. MTPreported PAT of Rs78.4mn in 1QFY17.

Quarterly performance

Y/E March (Rsmn) Q1FY17 Q1FY16 YoY (%) Q4FY16 QoQ (%)

Net sales 833 738 12.8 705 18.1

Materials & subcontracting 511 473 405

% of sales 61.3 64.0 57.5

Employee Expenses 66 55 66

% of sales 7.9 7.5 9.3

Total Expenditure 687 627 574

Operating profit 145 111 31.0 131 10.9

OPM (%) 17.5 15.0 18.6

Depreciation 24 20 22

Interest 5 3 2

EBT 117 88 107

Other income 3 1 3

PBT 120 89 34.6 110 8.9

Exceptional Item - - -

Provision for tax 41 31 37

-effective tax rate 34.5 34.5 34.0

PAT (reported) 78 58 34.6 73 8.1

Minority/ Share of Profit 0 0 0

PAT (Adjusted) 78 58 34.6 73 8.1

NPM (%) 9.4 7.9 10.3

Source: Company

… resulting in 34.5% CAGR in PAT

Source: Company, Kotak Securities - Private Client Research

Return Ratios to cross over 20%

Source: Company, Kotak Securities - Private Client Research

0%

20%

40%

60%

80%

100%

0

100

200

300

400

500

FY15 FY16 FY17E FY18E

PAT (Rs Mn - LHS) Growth (% - RHS)

0%

5%

10%

15%

20%

25%

30%

FY15 FY16 FY17E FY18E

RoE (%) RoCE (%)

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 14

INITIATING COVERAGE October 5, 2016

KEY RISKS

Slow pick up in edible oil business: MTP's recent venture into edible oilsegment has seen positive reviews. However, slower than expected ramp up orflow of order in the segment will affect its revenue going forward, thereby itsprofitability.

Slower than expected Ramp-up at RAK: RAK plant came on stream in themonth of August 2016 and will start contributing from 3QFY17 onwards, as ithas received commercial orders from local markets. However, if the companyfails to bag any new order in the coming quarter or slowdown in the lube, paintand FMCG industry in UAE, will affect its consolidated revenue going forward,thereby its profitability.

Initiate with BUY

MTPL volume growth of 20% in last two quarters coupled with a strong volumeguidance in the coming years and increasing share of IML in the overall revenuemix, makes us believe that company could be a good investment idea with an areturn ratios (RoE) of over 20% in the coming years. We expect MTPL tocontinue to deliver strong growth in the coming years on the back of integratedfacilities and increasing profitability from the high margin FMCG industry. AtCMP, stock trades at 17.4x/12.5x FY17E/FY18E earnings. We initiate coveragewith a BUY rating, and a target price of Rs260, valuing it at 16.5x FY18Eearnings.

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 15

INITIATING COVERAGE October 5, 2016

FINANCIALS

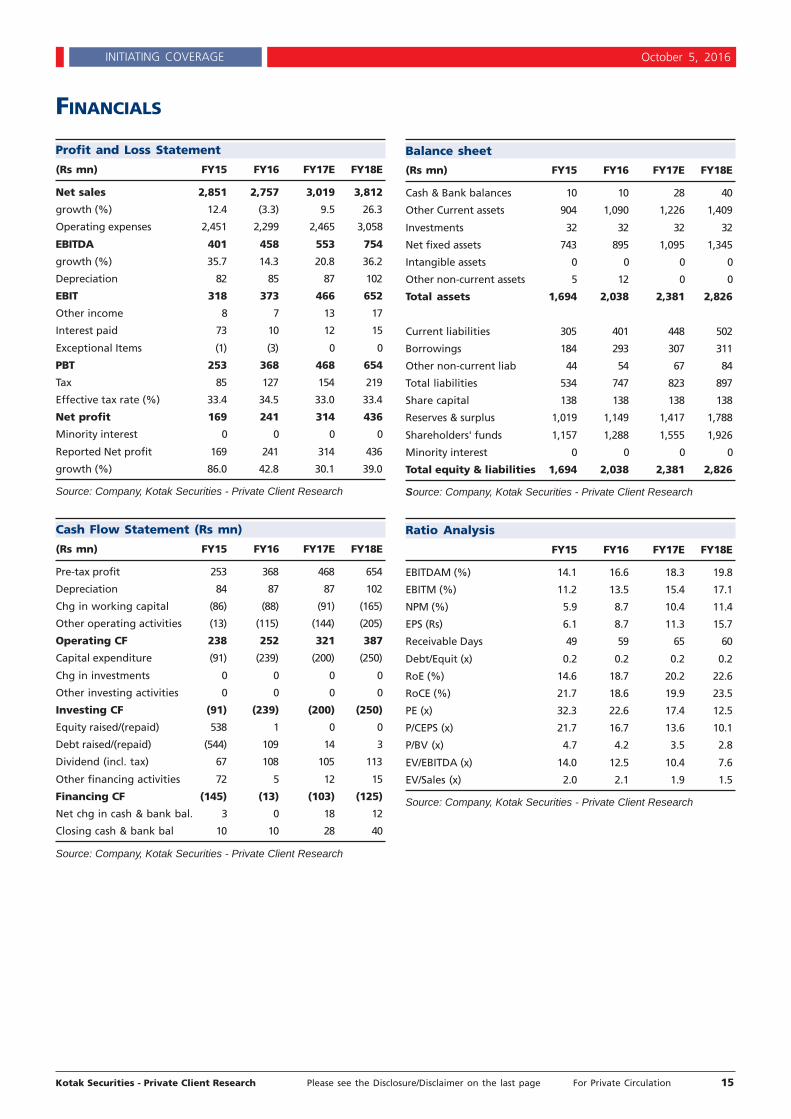

Profit and Loss Statement

(Rs mn) FY15 FY16 FY17E FY18E

Net sales 2,851 2,757 3,019 3,812

growth (%) 12.4 (3.3) 9.5 26.3

Operating expenses 2,451 2,299 2,465 3,058

EBITDA 401 458 553 754

growth (%) 35.7 14.3 20.8 36.2

Depreciation 82 85 87 102

EBIT 318 373 466 652

Other income 8 7 13 17

Interest paid 73 10 12 15

Exceptional Items (1) (3) 0 0

PBT 253 368 468 654

Tax 85 127 154 219

Effective tax rate (%) 33.4 34.5 33.0 33.4

Net profit 169 241 314 436

Minority interest 0 0 0 0

Reported Net profit 169 241 314 436

growth (%) 86.0 42.8 30.1 39.0

Source: Company, Kotak Securities - Private Client Research

Cash Flow Statement (Rs mn)

(Rs mn) FY15 FY16 FY17E FY18E

Pre-tax profit 253 368 468 654

Depreciation 84 87 87 102

Chg in working capital (86) (88) (91) (165)

Other operating activities (13) (115) (144) (205)

Operating CF 238 252 321 387

Capital expenditure (91) (239) (200) (250)

Chg in investments 0 0 0 0

Other investing activities 0 0 0 0

Investing CF (91) (239) (200) (250)

Equity raised/(repaid) 538 1 0 0

Debt raised/(repaid) (544) 109 14 3

Dividend (incl. tax) 67 108 105 113

Other financing activities 72 5 12 15

Financing CF (145) (13) (103) (125)

Net chg in cash & bank bal. 3 0 18 12

Closing cash & bank bal 10 10 28 40

Source: Company, Kotak Securities - Private Client Research

Balance sheet

(Rs mn) FY15 FY16 FY17E FY18E

Cash & Bank balances 10 10 28 40

Other Current assets 904 1,090 1,226 1,409

Investments 32 32 32 32

Net fixed assets 743 895 1,095 1,345

Intangible assets 0 0 0 0

Other non-current assets 5 12 0 0

Total assets 1,694 2,038 2,381 2,826

Current liabilities 305 401 448 502

Borrowings 184 293 307 311

Other non-current liab 44 54 67 84

Total liabilities 534 747 823 897

Share capital 138 138 138 138

Reserves & surplus 1,019 1,149 1,417 1,788

Shareholders' funds 1,157 1,288 1,555 1,926

Minority interest 0 0 0 0

Total equity & liabilities 1,694 2,038 2,381 2,826

Source: Company, Kotak Securities - Private Client Research

Ratio Analysis

FY15 FY16 FY17E FY18E

EBITDAM (%) 14.1 16.6 18.3 19.8

EBITM (%) 11.2 13.5 15.4 17.1

NPM (%) 5.9 8.7 10.4 11.4

EPS (Rs) 6.1 8.7 11.3 15.7

Receivable Days 49 59 65 60

Debt/Equit (x) 0.2 0.2 0.2 0.2

RoE (%) 14.6 18.7 20.2 22.6

RoCE (%) 21.7 18.6 19.9 23.5

PE (x) 32.3 22.6 17.4 12.5

P/CEPS (x) 21.7 16.7 13.6 10.1

P/BV (x) 4.7 4.2 3.5 2.8

EV/EBITDA (x) 14.0 12.5 10.4 7.6

EV/Sales (x) 2.0 2.1 1.9 1.5

Source: Company, Kotak Securities - Private Client Research

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 16

INITIATING COVERAGE October 5, 2016

RATING SCALE

Definitions of ratingsBUY – We expect the stock to deliver more than 12% returns over the next 9 months

ACCUMULATE – We expect the stock to deliver 5% - 12% returns over the next 9 months

REDUCE – We expect the stock to deliver 0% - 5% returns over the next 9 months

SELL – We expect the stock to deliver negative returns over the next 9 months

NR – Not Rated. Kotak Securities is not assigning any rating or price target to the stock. The report has been prepared for information purposesonly.

RS – Rating Suspended. Kotak Securities has suspended the investment rating and price target for this stock, either because there is not asufficient fundamental basis for determining, or there are legal, regulatory or policy constraints around publishing, an investment rating ortarget. The previous investment rating and price target, if any, are no longer in effect for this stock and should not be relied upon.

NA – Not Available or Not Applicable. The information is not available for display or is not applicable

NM – Not Meaningful. The information is not meaningful and is therefore excluded.

NOTE – Our target prices are with a 9-month perspective. Returns stated in the rating scale are our internal benchmark.

Fundamental Research Team

Dipen ShahIT, [email protected]+91 22 6218 5409

Sanjeev ZarbadeCapital Goods, [email protected]+91 22 6218 6424

Teena VirmaniConstruction, [email protected]+91 22 6218 6432

Arun AgarwalAuto & Auto [email protected]+91 22 6218 6443

Ruchir KhareCapital Goods, [email protected]+91 22 6218 6431

Ritwik RaiFMCG, [email protected]+91 22 6218 6426

Sumit PokharnaOil and [email protected]+91 22 6218 6438

Amit AgarwalLogistics, Paints, [email protected]+91 22 6218 6439

Meeta Shetty, [email protected]+91 22 6218 6425

Jatin DamaniaMetals & [email protected]+91 22 6218 6440

Pankaj [email protected]+91 22 6218 6434

Nipun GuptaInformation [email protected]+91 22 6218 6433

Jayesh [email protected]+91 22 6218 5373

K. [email protected]+91 22 6218 6427

Technical Research Team

Shrikant [email protected] 22 6218 5408

Amol [email protected]+91 20 6620 3350

Derivatives Research TeamSahaj [email protected]+91 79 6607 2231

Malay [email protected]+91 22 6218 6420

Prashanth [email protected]+91 22 6218 5497

Kotak Securities - Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 17

INITIATING COVERAGE October 5, 2016

Disclosure/DisclaimerKotak Securities Limited established in 1994, is a subsidiary of Kotak Mahindra Bank Limited. Kotak Securities is one of India's largest brokerage anddistribution house.Kotak Securities Limited is a corporate trading and clearing member of Bombay Stock Exchange Limited (BSE), National Stock Exchange of India Limited (NSE),Metropolitan Stock Exchange of India Limited (MSEI). Our businesses include stock broking, services rendered in connection with distribution of primarymarket issues and financial products like mutual funds and fixed deposits, depository services and Portfolio Management.Kotak Securities Limited is also a depository participant with National Securities Depository Limited (NSDL) and Central Depository Services (India) Limited(CDSL). Kotak Securities Limited is also registered with Insurance Regulatory and Development Authority as Corporate Agent for Kotak Mahindra Old MutualLife Insurance Limited and is also a Mutual Fund Advisor registered with Association of Mutual Funds in India (AMFI). We are registered as a Research Analystunder SEBI (Research Analyst) Regulations, 2014.We hereby declare that our activities were neither suspended nor we have defaulted with any stock exchange authority with whom we are registered in lastfive years. However SEBI, Exchanges and Depositories have conducted the routine inspection and based on their observations have issued advise/warning/deficiency letters/ or levied minor penalty on KSL for certain operational deviations. We have not been debarred from doing business by any Stock Exchange/ SEBI or any other authorities; nor has our certificate of registration been cancelled by SEBI at any point of time.We offer our research services to clients as well as our prospects.This document is not for public distribution and has been furnished to you solely for your information and must not be reproduced or redistributed to any otherperson. Persons into whose possession this document may come are required to observe these restrictions.This material is for the personal information of the authorized recipient, and we are not soliciting any action based upon it. This report is not to be construedas an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It is for the generalinformation of clients of Kotak Securities Ltd. It does not constitute a personal recommendation or take into account the particular investment objectives,financial situations, or needs of individual clients.We have reviewed the report, and in so far as it includes current or historical information, it is believed to be reliable though its accuracy or completenesscannot be guaranteed. Neither Kotak Securities Limited, nor any person connected with it, accepts any liability arising from the use of this document. Therecipients of this material should rely on their own investigations and take their own professional advice. Price and value of the investments referred to in thismaterial may go up or down. Past performance is not a guide for future performance. Certain transactions -including those involving futures, options andother derivatives as well as non-investment grade securities - involve substantial risk and are not suitable for all investors. Reports based on technical analysiscenters on studying charts of a stock's price movement and trading volume, as opposed to focusing on a company's fundamentals and as such, may not matchwith a report on a company's fundamentals.Opinions expressed are our current opinions as of the date appearing on this material only. While we endeavor to update on a reasonable basis theinformation discussed in this material, there may be regulatory, compliance or other reasons that prevent us from doing so. Prospective investors and othersare cautioned that any forward-looking statements are not predictions and may be subject to change without notice. Our proprietary trading and investmentbusinesses may make investment decisions that are inconsistent with the recommendations expressed herein.Kotak Securities Limited has two independent equity research groups: Institutional Equities and Private Client Group. This report has been prepared by thePrivate Client Group. The views and opinions expressed in this document may or may not match or may be contrary with the views, estimates, rating, targetprice of the Institutional Equities Research Group of Kotak Securities Limited.We and our affiliates/associates, officers, directors, and employees, Research Analyst(including relatives) worldwide may: (a) from time to time, have long orshort positions in, and buy or sell the securities thereof, of company (ies) mentioned herein or (b) be engaged in any other transaction involving such securitiesand earn brokerage or other compensation or act as a market maker in the financial instruments of the subject company/company (ies) discussed herein oract as advisor or lender / borrower to such company (ies) or have other potential/material conflict of interest with respect to any recommendation and relatedinformation and opinions at the time of publication of Research Report or at the time of public appearance. Kotak Securities Limited (KSL) may haveproprietary long/short position in the above mentioned scrip(s) and therefore may be considered as interested. The views provided herein are general innature and does not consider risk appetite or investment objective of particular investor; readers are requested to take independent professional advicebefore investing. This should not be construed as invitation or solicitation to do business with KSL. Kotak Securities Limited is also a Portfolio Manager.Portfolio Management Team (PMS) takes its investment decisions independent of the PCG research and accordingly PMS may have positions contrary to thePCG research recommendation. Kotak Securities Limited does not provide any promise or assurance of favourable view for a particular industry or sector orbusiness group in any manner. The investor is requested to take into consideration all the risk factors including their financial condition, suitability to riskreturn profile and take professional advice before investing.The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company orcompanies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations orviews expressed in this report.No part of this material may be duplicated in any form and/or redistributed without Kotak Securities' prior written consent.Details of Associates are available on our website ie www.kotak.comResearch Analyst has served as an officer, director or employee of subject company(ies): NoWe or our associates may have received compensation from the subject company(ies) in the past 12 months. We or our associates may have managed or co-managed public offering of securities for the subject company(ies) in the past 12 months. We or our associates may have received compensation forinvestment banking or merchant banking or brokerage services from the subject company(ies) in the past 12 months. We or our associates may have receivedany compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company(ies) in thepast 12 months. We or our associates may have received compensation or other benefits from the subject company(ies) or third party in connection with theresearch report. Our associates may have financial interest in the subject company(ies).Research Analyst or his/her relative's financial interest in the subject company(ies): NoKotak Securities Limited has financial interest in the subject company(ies): NoOur associates may have actual/beneficial ownership of 1% or more securities of the subject company(ies) at the end of the month immediately precedingthe date of publication of Research Report.Research Analyst or his/her relatives has actual/beneficial ownership of 1% or more securities of the subject company(ies) at the end of the monthimmediately preceding the date of publication of Research Report: NoKotak Securities Limited has actual/beneficial ownership of 1% or more securities of the subject company(ies) at the end of the month immediately precedingthe date of publication of Research Report: No

Subject company(ies) may have been client during twelve months preceding the date of distribution of the research report.

"A graph of daily closing prices of securities is available at www.nseindia.com and http://economictimes.indiatimes.com/markets/stocks/stock-quotes. (Choosea company from the list on the browser and select the "three years" icon in the price chart)."Kotak Securities Limited. Registered Office: 27 BKC, C 27, G Block, Bandra Kurla Complex, Bandra (E), Mumbai 400051. CIN: U99999MH1994PLC134051,Telephone No.: +22 43360000, Fax No.: +22 67132430. Website: www.kotak.com/www.kotaksecurities.com. Correspondence Address: Infinity IT Park, Bldg.No 21, Opp. Film City Road, A K Vaidya Marg, Malad (East), Mumbai 400097. Telephone No: 42856825. SEBI Registration No: NSE INB/INF/INE 230808130, BSEINB 010808153/INF 011133230, MSEI INE 260808130/INB 260808135/INF 260808135, AMFI ARN 0164, PMS INP000000258 and Research AnalystINH000000586. NSDL/CDSL: IN-DP-NSDL-23-97. Our research should not be considered as an advertisement or advice, professional or otherwise. The investoris requested to take into consideration all the risk factors including their financial condition, suitability to risk return profile and the like and take professionaladvice before investing. Investments in securities are subject to market risk; please read the SEBI prescribed Combined Risk Disclosure Document prior toinvesting. Derivatives are a sophisticated investment device. The investor is requested to take into consideration all the risk factors before actually tradingin derivative contracts. Compliance Officer Details: Mr. Manoj Agarwal. Call: 022 - 4285 8484, or Email: [email protected] case you require any clarification or have any concern, kindly write to us at below email ids: Level 1: For Trading related queries, contact our customer service at '[email protected]' and for demat account related queries contact us at

[email protected] or call us on: Online Customers - 30305757 (by using your city STD code as a prefix) or Toll free numbers 18002099191 / 1800222299,Offline Customers - 18002099292

Level 2: If you do not receive a satisfactory response at Level 1 within 3 working days, you may write to us at [email protected] or call us on 022-42858445 and if you feel you are still unheard, write to our customer service HOD at [email protected] or call us on 022-42858208.

Level 3: If you still have not received a satisfactory response at Level 2 within 3 working days, you may contact our Compliance Officer (Name: ManojAgarwal ) at [email protected] or call on 91- (022) 4285 8484.

Level 4: If you have not received a satisfactory response at Level 3 within 7 working days, you may also approach CEO (Mr. Kamlesh Rao) [email protected] or call on 91- (022) 4285 8301.