Embed Size (px)

Citation preview

PUBLIC DISCLOSURE

May 10, 2010

COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

Monarch Bank

2718345

1101 Executive Boulevard

Chesapeake, Virginia 23320

Federal Reserve Bank of Richmond P. O. Box 27622

Richmond, Virginia 23261

NOTE: This document is an evaluation of this institution’s record of meeting the

credit needs of its entire community, including low- and moderate-income neighborhoods, consistent with safe and sound operation of the institution. This evaluation is not, nor should it be construed as, an assessment of the financial condition of this institution. The rating assigned to this institution does not represent an analysis, conclusion or opinion of the Federal financial supervisory agency concerning the safety and soundness of this financial institution.

TABLE OF CONTENTS Institution Rating ............................................................................................................................ 1 Institution Description of Institution .................................................................................................... 1 Scope of Examination ......................................................................................................... 2 Conclusions with Respect to Performance Tests ................................................................ 3 Commonwealth of Virginia Virginia Rating.................................................................................................................... 6 Scope of Examination ......................................................................................................... 6

Description of Institution’s Operations in the Virginia Beach-Norfolk-Newport News, VA-NC MSA Assessment Area.......................................................................................... 6 Conclusions with Respect to Performance Tests ................................................................ 8

State of North Carolina North Carolina Rating ......................................................................................................... 13 Scope of Examination ......................................................................................................... 13 Description of Institution’s Operations in the Dare County Assessment Area .................. 13 Conclusions with Respect to Performance Tests ................................................................ 15

Appendices Appendix A: Scope of Examination ................................................................................... 19 Appendix B: Summary of State and Multistate Metropolitan Area Ratings ...................... 20 Appendix C: Glossary ......................................................................................................... 21

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

1

COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

INSTITUTION'S CRA RATING: This institution is rated: Satisfactory. The Lending Test is rated: Satisfactory The Community Development Test is rated: Satisfactory The major factors supporting this rating include:

The bank’s loan-to-deposit ratio is considered more than reasonable in relation to demand for credit in the bank’s assessment areas.

Given its business model, an adequate percentage of the institution’s loans were originated within the local assessment areas.

Lending to borrowers of different income levels and businesses of different sizes is considered reasonable in Virginia and marginally reasonable in North Carolina. Because the bank’s operations are heavily concentrated in Virginia, the performance in Virginia was given more weight and overall performance is considered reasonable.

Because the bank’s geographic distribution performances are considered reasonable in both Virginia and North Carolina, the bank’s performance overall is also considered reasonable.

The bank’s community development performance demonstrates an adequate responsiveness to the community development needs of the bank’s assessment areas.

DESCRIPTION OF INSTITUTION Monarch Bank (MB) is headquartered in Chesapeake, Virginia, and operates ten full-service branch offices in the Tidewater region of Virginia and the Outer Banks region of North Carolina. The bank also operates a network of 15 residential mortgage loan production offices located in Maryland, Virginia, North Carolina, and South Carolina. The bank is a subsidiary of Monarch Financial Holdings, a single-bank holding company, also headquartered in Chesapeake, Virginia. The bank received a satisfactory rating at its prior CRA evaluation dated May 5, 2008. As of March 31, 2010, the bank reported $704.7 million in assets, of which 89.5% were loans and 1.2% were securities. Various deposit and loan products are available through the institution including loans for residential mortgage, consumer, and business purposes. The composition of the loan portfolio as of March 31, 2010, is represented in the following chart:

$(000s) %

Secured by 1-4 Family dwellings 253,533 39.6

Multifamily 21,756 3.4

Construction and Development 127,217 19.9 Commercial & Industrial/

NonFarm NonResidential

Consumer Loans and Credit Cards 3,696 0.6

Agricultural Loans/ Farmland 0 0.0

All Other 0 0.0

Total 639,505 100.0

Composition of Loan Portfolio

Loan Type 3-31-2010

233,303 36.5

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

2

As indicated in the preceding table, the bank is an active commercial/small business and residential mortgage lender. While the percentages detail the composition of the bank’s existing loan portfolio, they understate, to a large degree, the volume of residential mortgage originations because the bank sells a large portion of their residential mortgage loans to secondary market investors. The bank also continues to offer other loans, such as consumer and farm loans; however, the volume of such lending is relatively small in comparison to the commercial/small business and residential mortgage lending. The bank serves two assessment areas located in Virginia and North Carolina. One of the assessment areas is located within a metropolitan statistical area (MSA) in the Commonwealth of Virginia and the other is located in a nonmetropolitan area of North Carolina. The following table reflects the composition of the bank’s assessment areas.

Assessment Area Names County/City State Census

Tracts

Virginia Beach-Norfolk-Newport News, VA-NC MSA

Chesapeake VA All

Norfolk City VA All

Virginia Beach VA All

Dare County, NC Dare County NC All

During December 2009, the bank opened a second branch in Dare County, North Carolina, located in an upper-income census tract. The opening of the branch did not necessitate any changes to the bank’s existing assessment area. The bank has not closed any branches since the previous evaluation. SCOPE OF EXAMINATION The institution was evaluated using the interagency examination procedures developed by the Federal Financial Institutions Examination Council (FFIEC). MB is required to report certain information regarding its home mortgage lending in accordance with the Home Mortgage Disclosure Act (HMDA). Accordingly, MB’s 2008 and 2009 HMDA loan originations were considered in the evaluation. Additionally, a sample of 136 small business loans randomly selected from a universe of 426 small business loans totaling $88.4 million that were originated during the six-month period ending December 31, 2009, was also included in the analysis. Qualified community development loans and services are considered for activities since the previous evaluation. Qualified investments outstanding as of the date of this evaluation are also considered, regardless of when made. The following table includes the distribution of branch offices, along with deposit and loan volume. The deposit volume includes all bank deposits and is current as of June 30, 2009, while loan volume includes all HMDA and sampled small business loans considered in the evaluation.

Assessment Area Loan Volume Deposit Volume Branches

# % $(000s) % $(000s) % # %

Virginia Beach-Norfolk-Newport

News, VA-NC MSA 2,531 96.8% $616,993 97% $503,968 93.1% 8 80%

Dare County, NC 83 3.2% $19,227 3% $ 37,313 6.9% 2 20%

Totals 2,614 100% $636,220 100% $541,281 100% 10 100%

As indicated in the preceding table, the bank’s operations are heavily concentrated in the Virginia Beach-Norfolk-Newport News, VA-NC MSA assessment area. Accordingly, the bank’s performance in this assessment area is weighted more heavily when considering the bank’s overall performance levels.

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

3

CONCLUSIONS WITH RESPECT TO PERFORMANCE TESTS: When evaluating the bank’s lending performance, consideration is given to its level of lending in relation to relevant demographic data from the 2000 census, aggregate HMDA and small business data from the calendar year 2008, and Dun & Bradstreet (D&B) business demographic data from 2009. Analyses of lending during the review period are discussed in greater detail in subsequent sections of this evaluation. While the HMDA loan data from calendar years 2008 and 2009 were considered in the evaluation, only bank and aggregate data from 2008 are presented in the assessment area analysis tables. Because small business loan data was sampled from the third and fourth quarters of 2009, the small business analysis tables only include small business loan data from 2009. Aggregate HMDA and small business data from 2009 could not be included in the analyses as it is not yet available. In instances where the bank’s residential mortgage (HMDA) lending performance during 2009 varies significantly from the performance during 2008, such variances and corresponding impact on the overall performance are discussed. When evaluating the geographic and borrower distribution for a specific loan category within an assessment area, primary emphasis is placed on the number of loans originated. To arrive at an overall assessment area level conclusion regarding the distribution of lending, performance in each loan category is then weighted by the dollar volume of such loans in the assessment area. The institution’s overall rating is based on the overall performance of each market area, and primary consideration is given to the dollar volume each market contributes to the overall activity considered in the evaluation. Because the bank operates branches in two states, CRA performance ratings are required for each state, as well as for the institution overall. Given that the bank has only one assessment area in each state, the statewide ratings are based solely on the bank’s performance in each assessment area. Based on recent lending activity from the third and fourth quarters of 2009, the bank extends a larger volume of residential mortgage loans (2,197 loans totaling $544.8 million) than small business loans (426 loans totaling $88.4 million). Accordingly, the bank’s residential mortgage lending performance is given more weight than the bank’s small business lending performance when considering the institution’s overall rating. Overall, MB’s lending test performance is rated Satisfactory. This rating considers the bank’s loan-to-deposit ratio, level of lending in its assessment areas, borrower distribution performances, and geographic distribution performances. These components are discussed in the following sections. Loan-To-Deposit Ratio The bank’s quarterly average loan-to-deposit ratio for the eight-quarter period ending March 31, 2010, equaled 108.8% and ranged from 105.2% to 112.4%. As of March 31, 2010, the institution’s loan-to-deposit ratio equaled 106.7%. In comparison, for the seven-quarter period ending December 31, 2009, the average quarterly loan-to-deposit ratios of all banks headquartered in metropolitan areas of Virginia and of a similar asset size to MB ranged from 85% to 88.9%. Since March 31, 2008, loans, deposits, and assets have increased by 29.4%, 26.1%, and 29.7%, respectively. The bank’s loan-to-deposit ratio is considered more than reasonable when considering the ratios of similar sized institutions in the region, the bank’s size, financial condition, and assessment area credit needs. Lending In Assessment Area The institution’s lending volume for HMDA loans from January 1, 2008, through December 31, 2009, and sampled small business loans from the second half of 2009 is represented in the following table.

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

4

A substantial majority of small business loans (89.7%) were extended in the bank’s assessment areas, while less than a majority of HMDA loans (37.2%) were extended inside the bank’s assessment areas. As previously noted, the bank operates a network of residential mortgage loan production offices in a region that includes four contiguous states and is much larger than the bank’s deposit taking branches and corresponding assessment areas in Virginia and North Carolina. The vast majority of residential mortgage loans are originated by the bank and then sold to secondary market investors. In addition, the mortgage department’s operations are funded primarily from warehouse lines of credit rather than local deposits, while the bank’s small business and other portfolio lending is primarily funded from deposit accounts. Given the bank’s business funding model and that a majority of the loans retained within bank’s portfolio are extended within the local market areas, the bank’s overall lending level inside its assessment areas is considered reasonable. Lending To Borrowers of Different Incomes and To Businesses of Different Sizes Within the bank’s market areas, a high level of small business lending activity has been reported by specialized lenders, who often originate small business loans in the form of credit cards. These loans, however, tend to be much smaller in size than traditional small business bank loans, and a substantial majority of such loans do not have revenue data reported. The presence of these lenders is reflected in a smaller market share for traditional lenders and tends to understate the percentage of aggregate lending to businesses with annual revenues of $1 million or less. Consequently, the presence of these lenders was considered as an aspect of performance context when evaluating the level and distribution of bank lending. Therefore, to better gauge performance, MB’s lending is also compared to a peer group of traditional small business lenders that excludes the credit card/specialty lenders. The bank’s borrower distribution performance in Virginia is considered reasonable for both HMDA and small business lending. Within North Carolina, the bank’s small business borrower distribution performance is considered excellent, while the HMDA borrower distribution performance is considered marginally reasonable. The institution’s overall borrower distribution performance is considered reasonable and reflects the reasonable performance level in Virginia where the bank’s operations are concentrated. Geographic Distribution of Loans The bank’s geographic distribution performance is considered reasonable in both Virginia and North Carolina. The bank’s overall geographic distribution performance is considered reasonable.

# % $(000) % # % $(000) %

Home Purchase 1,472 40.9 352,964 39.7 2,128 59.1 535,432 60.3

Home Improvement 10 47.6 1,573 38.7 11 52.4 2,487 61.3

Refinancing 1,007 32.8 254,873 30.9 2,060 67.2 568,823 69.1

Multi-Family Housing 3 75.0 3,375 45.3 1 25.0 4,080 54.7

Total HMDA related 2,492 37.2 612,785 35.6 4,200 62.8 1,110,822 64.4

Small Business* 122 89.7 23,435 89.0 14 10.3 2,886 11.0

TOTAL LOANS 2,614 38.3 636,220 36.4 4,214 61.7 1,113,708 63.6

Comparison of Credit Extended Inside and Outside of Assessment Area(s)

Loan TypeInside Outside

*The number and dollar amount of loans reflects a sample of such loans originated during the evaluation period and does not reflect loan data

collected or reported by the institution.

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

5

Community Development Loans, Investments, and Services During the evaluation period, MB originated six community development loans totaling $3.2 million in the Virginia Beach-Norfolk-Newport News, VA-NC MSA and Dare County assessment areas. Additionally, the bank and its employees provided financial expertise and other support to a number of local organizations that facilitate community development services in the bank’s assessment areas. Detailed discussions of the institution’s community development lending and service activities are included with each assessment area, as applicable. The bank’s overall performance under the community development test is rated satisfactory. FAIR LENDING OR OTHER ILLEGAL CREDIT PRACTICES REVIEW No evidence of discriminatory or other illegal credit practices inconsistent with helping to meet community credit needs was identified. Adequate policies, procedures, and training programs have been developed to support nondiscrimination in lending activities.

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

6

COMMONWEALTH OF VIRGINIA CRA RATING FOR VIRGINIA: Satisfactory The Lending Test is rated: Satisfactory The Community Development Test is rated: Satisfactory Major factors supporting the rating include:

The bank’s borrower distribution performance (lending to low- and moderate-income borrowers and small businesses having annual revenues of $1 million or less) is reasonable for both residential mortgage and small business lending within the assessment area located in the Commonwealth of Virginia.

The bank’s geographic distribution of HMDA loans is considered reasonable while the distribution of small business loans is considered marginally reasonable. Overall, the geographic distribution of loans within this assessment area is considered reasonable.

When considering the availability community development opportunities within the Virginia assessment area and the bank’s current capacity, the bank participated in an adequate level of community development activities.

SCOPE OF EXAMINATION The bank’s operations within Virginia are entirely contained within a portion of the Virginia Beach-Norfolk-Newport News, VA-NC MSA; therefore, the commonwealth’s evaluation is wholly predicated on the evaluation of this assessment area. The evaluation considers the distribution of the bank’s reported HMDA loan originations during 2008 and 2009 and a sample of small business loans originated during the third and fourth quarters of 2009, as well as, the bank’s current and recent community development activities. DESCRIPTION OF INSTITUTION’S OPERATIONS IN VIRGINIA BEACH-NORFOLK-NEWPORT NEWS, VA-NC MSA ASSESSMENT AREA The assessment area, which does not include the entire MSA, is located in the southeast portion of Virginia and has a population of 858,844 and a median housing value of $113,602. The owner-occupancy rate for the market equals 58.6%, which is less than the Commonwealth’s rate (63.3%) but is consistent with the MSA’s rate (58.8%). The percentage of families living below the poverty level in the assessment area (7.8%) exceeds the Commonwealth’s rate (7%) but is lower than the MSA’s rate (8.4%). The 2008 and 2009 median family incomes for the Virginia Beach-Norfolk-Newport News, VA-NC MSA equaled $65,100 and $67,900, respectively. The following table includes pertinent demographic data for the market area.

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

7

The local economy is diverse and employment industries include the military, construction and real estate development, retail and wholesale trade, light manufacturing, shipbuilding and repair, and tourism. Major area employers include the U.S. Department of Defense, Stihl (outdoor power equipment manufacturer), Sentara Healthcare, academic institutions (Old Dominion University, Norfolk State University, and Medical College of Hampton Roads), NORSHIPCO (shipbuilding and repair), Wal-Mart Stores (retail stores), Cox Communications, local school systems, and area municipalities. The following table shows unemployment rates at six-month intervals from May 2008.

# % # % # % # %

15 7.2 9,167 4.2 3,775 41.2 39,192 17.9

57 27.3 45,408 20.8 6,608 14.6 40,570 18.6

72 34.4 82,254 37.6 4,838 5.9 50,421 23.1

64 30.6 81,833 37.4 1,921 2.3 88,479 40.5

1 0.5 0 0.0 0 0.0

209 100.0 218,662 100.0 17,142 7.8 218,662 100.0

# % # % # % # %

3,172 1.6 14,315 4.6 5,756 40.2 60,116 19.4

28,439 14.7 73,189 23.6 11,616 15.9 53,449 17.2

75,402 39.1 113,960 36.7 8,426 7.4 66,324 21.4

85,846 44.5 109,184 35.1 4,637 4.2 130,759 42.1

0 0.0 0 0.0 0 0.0

192,859 100.0 310,648 100.0 30,435 9.8 310,648 100.0

# % # % # % # %

1,113 2.9 966 2.8 95 4.1 52 2.8

7,471 19.6 6,421 18.9 625 26.8 425 23.0

13,627 35.8 12,107 35.7 855 36.6 665 36.0

15,722 41.3 14,318 42.2 717 30.7 687 37.2

150 0.4 89 0.3 41 1.8 20 1.1

38,083 100.0 33,901 100.0 2,333 100.0 1,849 100.0

89.0 6.1 4.9

Total

Assessment Area Demographics

Virginia Beach-Norfolk-Newport News, VA-NC MSA

Income

Categories*

Tract Distribution Families by Tract Families < Poverty as a %

of Families by Tract

Families by Family

Income

Low

Moderate

Middle

Upper

NA

Total

O wner O ccupied Units

by Tract

Households

HHs by Tract HHs < Poverty by Tract HHs by HH Income

Low

Moderate

Middle

Upper

NA

Total Businesses by

Tract

Businesses by Tract and Revenue Size

Less than or = $1 Million O ver $1 Million Revenue not Reported

Percentage of Total Businesses:

*NA-Tracts without household or family income as applicable

Low

Moderate

Middle

Upper

NA

Total

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

8

Geographic Area

Unemployment Rate Trend

May

2008

November

2008

May

2009

November

2008

May

2010

Chesapeake City 3.5% 4.3% 6.2% 6.3% 6.7%

Norfolk City 4.7% 6% 8.2% 8.6% 9.3%

Virginia Beach City 3.3% 4.1% 6% 5.9% 6.3%

Virginia Beach-Norfolk-Newport News, VA-NC MSA 3.7% 4.8% 6.7% 6.8% 7.3%

Virginia 3.6% 4.5% 6.7% 6.5% 6.9%

Area unemployment rates reflect a rising trend over a recent 24-month period. Rising and/or high area employment rates may adversely affect a bank’s ability to extend credit as unemployed applicants often have diminished repayment capacity. A local community development official was contacted during the evaluation to discuss local economic conditions and area credit needs. The contact indicated that local economic conditions have begun to improve, and demand for affordable housing continues to increase in the market area. The contact stated that the cost of developing and/or redeveloping land in Virginia Beach for affordable housing has increased and that affordable housing development opportunities are comparatively more viable in the cities of Norfolk and Chesapeake than in Virginia Beach. The contact also stated that while various local financial institutions have supported community development activities by providing technical expertise, monetary support in the form of grants and loans has declined substantially. CONCLUSIONS WITH RESPECT TO PERFORMANCE TESTS: During the third and fourth quarters of 2009, the bank originated $152.1 million in HMDA loans, and it is estimated that the bank originated $77 million in small business loans during the same time period in this assessment area. Accordingly, the bank’s residential mortgage lending performance is given more weight than the small business lending performance when evaluating overall lending performance. Lending To Borrowers of Different Incomes and To Businesses of Different Sizes Monarch Bank’s borrower distribution performance is reasonable for both residential mortgage and small business lending.

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

9

When considering the bank and aggregate reporter data from 2008, home purchase loans were the bank’s most frequent product extended, while refinancing were extended most frequently by the aggregate reporters. As indicated in the chart, the bank originated only a nominal number of home improvement loans. Accordingly, the bank’s performance associated with home improvement lending is afforded the least weight when considering the bank’s overall performance. The bank’s performance specific to home purchase lending is considered to be at the upper end of the range for reasonable performance, while the bank’s refinance performance is considered to be at low end of the range for reasonable performance. The bank’s home improvement performance is considered excellent. When considering the bank’s performance overall, lending to low-income borrowers (3.8%) lags both the percentage of low-income families in the assessment area (17.9%) and the aggregate lending level to such borrowers (5.1%). The bank’s level of lending to moderate-income borrowers (24%) exceeds both the percentage of moderate-income families living in the assessment area (18.6%) and the aggregate lending level (22.9%). The bank’s performance is considered reasonable and their performance during 2009 was substantially similar.

# % $(000s) % $ # % $(000s) % $

Low 21 3.6 2,510 1.8 359 2.6 44,722 1.3

Moderate 162 27.4 24,198 17.0 3,182 23.4 542,038 16.3

Low 10 3.9 1,267 1.9 1,241 6.6 144,760 3.9

Moderate 40 15.7 7,288 11.1 4,232 22.5 639,262 17.2

Low 1 20.0 113 18.1 184 7.6 10,641 5.2

Moderate 2 40.0 175 28.0 552 22.9 37,049 18.0

Low 0 0.0 0 0.0 0 0.0 0 0.0

Moderate 0 0.0 0 0.0 0 0.0 0 0.0

Low 32 3.8 3,890 1.9 1,784 5.1 200,123 2.8

Moderate 204 24.0 31,661 15.1 7,966 22.9 1,218,349 16.8

Middle 246 28.9 55,844 26.7 10,394 29.8 2,023,293 27.9

Upper 368 43.3 117,597 56.3 14,686 42.2 3,813,898 52.6

Total 850 100.0 208,992 100.0 34,830 100.0 7,255,663 100.0

Unknown 57 20,105 6,206 1,709,831

( ) represents the total number of bank loans for the specific Loan Purpose where income is known

Percentage's (%) are calculated on all loans where incomes are known

(591) Home Purchase (13,626)

Distribution of HMDA Loans by Income Level of Borrower

Virginia Beach-Norfolk-Newport News, VA-NC MSA (2008)

Income

Categories

Bank Aggregate

(0) Multi-Family (0)

HMDA Totals

(254) Refinance (18,790)

(5) Home Improvement (2,414)

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

10

D&B data indicated that 89% of all local businesses have revenues that do not exceed $1 million per year. Aggregate lending data from 2008 is considered as an element of performance context in the analysis because the 2009 aggregate data is not yet available. During 2008, a peer group of traditional bank lenders, which excludes credit card and other specialty lenders, originated 53.2% of the reported small business loans to businesses with annual revenues of $1 million or less. The remaining loans were to businesses with revenues in excess of $1 million per year or revenues were not known. Overall, 61.7% of the sampled small business loans were to businesses with annual revenues of $1 million or less. The bank’s level of lending is considered reasonable. Geographic Distribution of Loans Overall, the bank’s geographic distribution performances for HMDA and small business lending within the assessment area is considered reasonable.

by R evenue # % $(000s) % $ # % $(000s) % $

$1 Million or Less 71 61.7 10,857 47.3 NA NA NA NA

Over $1 Million 44 38.3 12,084 52.7 NA NA NA NA

Unknown 0 0.0 0 0.0 NA NA NA NA

by Loan S ize

$100,000 or less 64 55.7 3,107 13.5 NA NA NA NA

$100,001-$250,000 22 19.1 4,270 18.6 NA NA NA NA

$250,001-$1 Million 29 25.2 15,564 67.8 NA NA NA NA

Total 115 100.0 22,941 100.0 NA NA NA NA

* No data is available for Aggregate loans with Revenues over $1 million and those with Unknown revenues

Distribution of Lending by Loan Amount and Size of Business

Virginia Beach-Norfolk-Newport News, VA-NC MSA (2009)

Bank Aggregate*

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

11

Based on bank and aggregate data, home purchase and refinance loans are the dominate HMDA loan products in the market area. Accordingly, the performances associated with these two products are given the most weight when considering the bank’s performance. The bank’s level of home purchase and refinancings in low- and moderate-income tracts is generally consistent with the proportion of owner-occupied housing units located in such areas (1.6% and 14.7%, respectively) and the aggregate lending level in such areas. Overall, MB’s level of lending in low-income (2.3%) and moderate-income (16.4%) tracts is consistent with the percentage of owner-occupied housing units located in low- and moderate-income census tracts, as well as, the aggregate reporter lending levels (2.1% and 16.7%, respectively). The bank’s geographic distribution performance is considered reasonable and their performance during 2009 is substantially similar.

# % $(000s) % $ # % $(000s) % $

Low 15 2.5 2,524 0.0 334 2.1 75,900 2.0

Moderate 108 18.0 21,253 14.5 2,734 17.5 511,179 13.4

Low 6 2.0 1,768 2.2 469 2.1 84,274 1.8

Moderate 39 13.0 6,855 8.7 3,694 16.2 573,763 12.3

Low 0 0.0 0 0.0 59 2.3 3,435 1.6

Moderate 0 0.0 0 0.0 423 16.4 27,484 12.6

Low 0 0.0 0 0.0 6 9.2 2,343 0.8

Moderate 2 100.0 3,325 100.0 14 21.5 20,147 7.0

Low 21 2.3 4,292 1.9 868 2.1 165,952 1.9

Moderate 149 16.4 31,433 13.7 6,865 16.7 1,132,573 12.6

Middle 337 37.2 71,442 31.2 16,461 40.1 3,309,293 36.9

Upper 400 44.1 121,930 53.2 16,842 41.0 4,357,676 48.6

NA* 0 0.0 0 0.0 0 0.0 0 0.0

Total 907 100.0 229,097 100.0 41,036 100.0 8,965,494 100.0

*NA-Tracts without household or family income as applicable; or a small county

( ) represents the total number of bank loans for the specific Loan Purpose

Loans where the geographic location is unknown are excluded from this table.

(600) Home Purchase (15,590)

Distribution of HMDA Loans by Income Level of Census Tract

Virginia Beach-Norfolk-Newport News, VA-NC MSA (2008)

Income

Categories

Bank Aggregate

(2) Multi-Family (65)

HMDA Totals

(300) Refinance (22,808)

(5) Home Improvement (2,573)

# % $(000s) % $ # % $(000s) % $

Low 1 0.9 5 0.0 NA NA NA NA

Moderate 17 14.8 2,792 12.2 NA NA NA NA

Middle 36 31.3 6,765 29.5 NA NA NA NA

Upper 60 52.2 13,360 58.2 NA NA NA NA

NA* 1 0.9 20 0.1 NA NA NA NA

Total 115 100.0 22,941 100.0 NA NA NA NA

*NA-Tracts without household or family income as applicable; or a small county

Distribution of Small Business Loans by Income Level of Census Tract

Virginia Beach-Norfolk-Newport News, VA-NC MSA (2009)

Income

Categories

Bank Aggregate

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

12

MB’s level of small business lending in low-income (.9%) and moderate-income (14.8%) areas lags the percentage of businesses located in such areas (2.9% and 19.6%, respectively). Aggregate lending data from 2008 is considered as an element of performance context in the analysis because the 2009 aggregate data is not yet available. According to the 2008 aggregate data, 2.1% of small business loans were extended in low-income census tracts, while 16.7% were extended in moderate-income census tracts. The bank’s performance is considered to be marginally reasonable. Community Development Loans, Investments, and Services

Discussions with an individual knowledgeable of the local market area and reviews of the performance evaluations of other financial institutions having a local presence indicate that local community development opportunities are reasonably available in the assessment area. Given its current loan-to-deposit ratio (108.8%), the bank’s capacity for additional lending, including community development lending, is somewhat constrained. Additionally, the bank faces moderate constraints regarding investment activity when considering its balance sheet structure and funding strategies. The bank faces no constraints, however, in providing community development services. Since the previous evaluation in May 2008, the bank originated the following qualified community development loans:

A $1.9 million loan to develop a multifamily affordable housing complex Four loans totaling $764,000 to three local nonprofit organizations that provides community

development services

The bank and its employees provide financial expertise to the following organizations that provide community development services targeted to low-and moderate-income residents, facilitate small business development, and focus on job creation:

Small Business Development Affordable Housing

Small Business Administration Tidewater Mortgage Bankers Association

Virginia Beach Minority Business Council Tidewater Business Financing Corporation

Norfolk Housing and Redevelopment Authority

Community Services Victory Home

VOLUNTEER Hampton Roads Workforce Housing Roundtable

Barry Robinson Center Virginia Housing Development Authority

Virginia Beach CASA First Time Homebuyer Seminars

Horizons – Hampton Roads

Overall, the bank has demonstrated an adequate level of responsiveness to local community development needs through its lending activities and support of area organizations that facilitate community development.

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

13

STATE OF NORTH CAROLINA CRA RATING FOR NORTH CAROLINA: Satisfactory The Lending Test is rated: Satisfactory The Community Development Test is rated: Satisfactory Major factors supporting the rating include:

The bank’s borrower distribution performance varies between poor and excellent by product and by year. Despite the variations in performance, the bank’s overall performance is considered marginally reasonably and is reflective of the performance of bank’s dominate product (HMDA loans) within the market.

While this assessment area does not contain low- and moderate-income tracts, the geographic distribution of HMDA and small business loans is reasonable.

When considering the availability of community development opportunities within the North Carolina assessment area and the bank’s current capacity, the bank has participated in an adequate level of community development activities.

SCOPE OF EXAMINATION The bank’s operations within North Carolina are entirely contained within the Dare County assessment area. Therefore, the state’s evaluation is wholly dependent on the evaluation of this nonmetropolitan assessment area. The evaluation considers the distribution of the bank’s reported HMDA loan originations during 2008 and 2009, a sample of small business loans originated during the third and fourth quarters of 2009, and the bank’s current and recent community development activities. DESCRIPTION OF INSTITUTION’S OPERATIONS IN DARE COUNTY, NORTH CAROLINA Dare County is located in the northeastern coastal region of North Carolina. The market area has a population of 29,967 and a median housing value of $128,583. The owner-occupancy rate for the market equals 35.5%, which is significantly lower than the statewide level (61.6%) as well as the nonmetropolitan areas of North Carolina (62.7%). The low home ownership rate reflects the large volume of area vacation homes. The percentage of families living below the poverty level in the assessment area (5.5%) is lower than the state level of 9% and the nonmetropolitan areas of North Carolina of 11.3%. The 2008 and 2009 median family incomes for the nonmetropolitan areas of North Carolina equaled $48,100 and $49,900, respectively. The following table includes pertinent demographic data for the market area.

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

14

The local economy is heavily based on tourism and other seasonal employment. Major area employers include: the county school system, local government, Carolina Designs Realty, East Carolina Health, Food Lion (grocery store chain), North Carolina Department of Transportation, and Wal-Mart Stores (retail stores). The table below shows unemployment rates at six-month intervals from May 2008.

Geographic Area

Unemployment Rate Trend

May

2008

November

2008

May

2009

November

2008

May

2010

Dare County 4.6% 8.1% 8% 10.1% 8.1%

North Carolina 5.7% 7.4% 10.9% 10.6% 10%

# % # % # % # %

0 0.0 0 0.0 0 0.0 972 11.4

0 0.0 0 0.0 0 0.0 1,353 15.9

3 50.0 4,525 53.2 305 6.7 1,856 21.8

3 50.0 3,979 46.8 163 4.1 4,323 50.8

0 0.0 0 0.0 0 0.0

6 100.0 8,504 100.0 468 5.5 8,504 100.0

# % # % # % # %

0 0.0 0 0.0 0 0.0 1,747 13.8

0 0.0 0 0.0 0 0.0 1,697 13.4

4,995 52.8 6,825 53.8 629 9.2 2,439 19.2

4,459 47.2 5,860 46.2 402 6.9 6,802 53.6

0 0.0 0 0.0 0 0.0

9,454 100.0 12,685 100.0 1,031 8.1 12,685 100.0

# % # % # % # %

0 0.0 0 0.0 0 0.0 0 0.0

0 0.0 0 0.0 0 0.0 0 0.0

1,383 42.5 1,254 42.8 66 42.3 63 37.5

1,871 57.5 1,676 57.2 90 57.7 105 62.5

0 0.0 0 0.0 0 0.0 0 0.0

3,254 100.0 2,930 100.0 156 100.0 168 100.0

90.0 4.8 5.2

Total

Assessment Area Demographics

Dare, NC NonMSA

Income

Categories*

Tract Distribution Families by Tract Families < Poverty as a %

of Families by Tract

Families by Family

Income

Low

Moderate

Middle

Upper

NA

Total

O wner O ccupied Units

by Tract

Households

HHs by Tract HHs < Poverty by Tract HHs by HH Income

Low

Moderate

Middle

Upper

NA

Total Businesses by

Tract

Businesses by Tract and Revenue Size

Less than or = $1 Million O ver $1 Million Revenue not Reported

Percentage of Total Businesses:

*NA-Tracts without household or family income as applicable

Low

Moderate

Middle

Upper

NA

Total

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

15

The Dare County unemployment rates reflect both a rising trend and the effects of seasonal summer employment opportunities over a recent 24-month period. Rising and/or high area employment rates may adversely affect a bank’s ability to extend credit as unemployed applicants often have diminished repayment capacity. A local economic development official was contacted to assist in evaluating the bank’s CRA performance. The contact stated that local economy is heavily influenced by tourism which creates a seasonal employment cycle. Many area residents rely on seasonal jobs as their primary sources of income but seasonal and year-round employment opportunities have decreased during the past three summers as area vacation traffic declined due to poor economic conditions. Additionally, local residents are increasingly having to compete for seasonal jobs with students that come to the beach for the summer. Above average rental vacancies have depressed the housing market and are contributing to an increase in foreclosures. The contact is hopeful that the forecasted increases in vacation traffic and rental occupancies for this summer season will prove accurate. The contact stated that despite difficult economic conditions, local financial institutions are adequately serving the credit needs of the community. CONCLUSIONS WITH RESPECT TO PERFORMANCE TESTS: During the third and fourth quarters of 2009, the bank originated $5.3 million in HMDA loans, and it is estimated that the bank originated $1.6 million in small business loans in this assessment area. Accordingly, the bank’s residential mortgage lending performance is given more weight than the small business lending performance when evaluating overall lending performance. Lending To Borrowers of Different Incomes and To Businesses of Different Sizes The bank’s HMDA borrower distribution performance is considered marginally reasonable, while the bank’s small business lending performance is considered excellent. The bank’s overall borrower distribution performance is considered marginally reasonable. In reaching this conclusion, more weight was placed on the bank’s HMDA lending performance because of the substantially larger dollar volume of such lending within the assessment area.

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

16

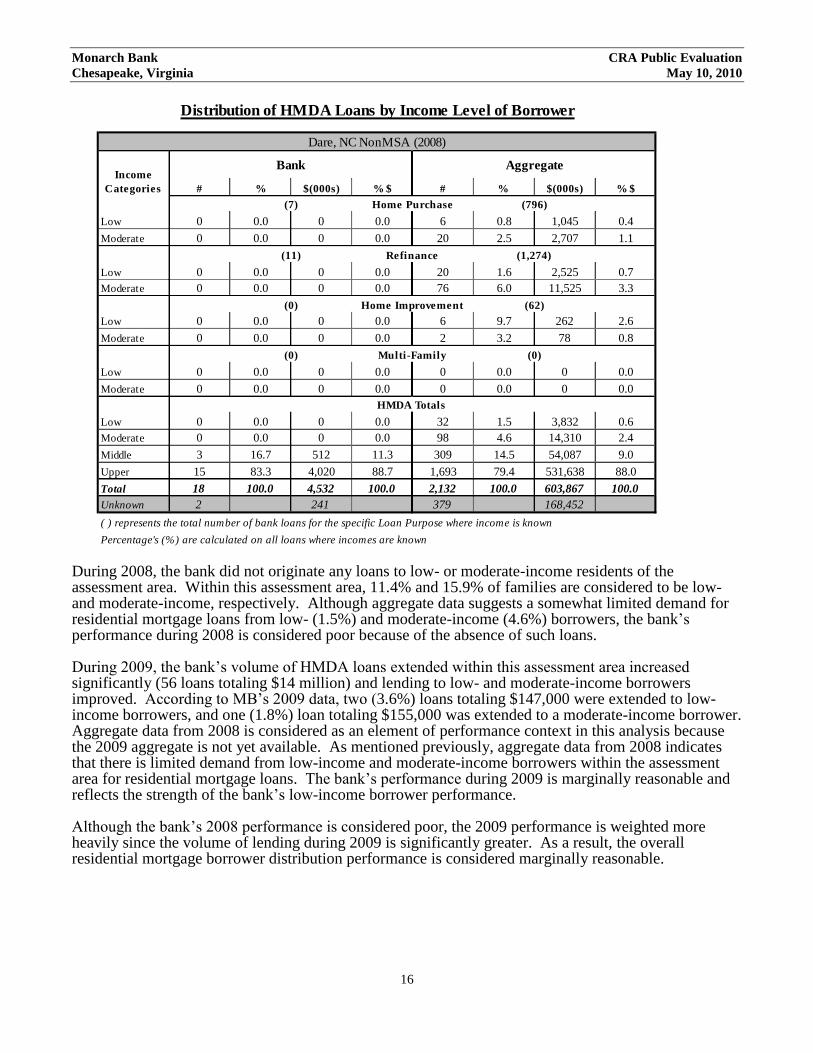

During 2008, the bank did not originate any loans to low- or moderate-income residents of the assessment area. Within this assessment area, 11.4% and 15.9% of families are considered to be low- and moderate-income, respectively. Although aggregate data suggests a somewhat limited demand for residential mortgage loans from low- (1.5%) and moderate-income (4.6%) borrowers, the bank’s performance during 2008 is considered poor because of the absence of such loans. During 2009, the bank’s volume of HMDA loans extended within this assessment area increased significantly (56 loans totaling $14 million) and lending to low- and moderate-income borrowers improved. According to MB’s 2009 data, two (3.6%) loans totaling $147,000 were extended to low-income borrowers, and one (1.8%) loan totaling $155,000 was extended to a moderate-income borrower. Aggregate data from 2008 is considered as an element of performance context in this analysis because the 2009 aggregate is not yet available. As mentioned previously, aggregate data from 2008 indicates that there is limited demand from low-income and moderate-income borrowers within the assessment area for residential mortgage loans. The bank’s performance during 2009 is marginally reasonable and reflects the strength of the bank’s low-income borrower performance. Although the bank’s 2008 performance is considered poor, the 2009 performance is weighted more heavily since the volume of lending during 2009 is significantly greater. As a result, the overall residential mortgage borrower distribution performance is considered marginally reasonable.

# % $(000s) % $ # % $(000s) % $

Low 0 0.0 0 0.0 6 0.8 1,045 0.4

Moderate 0 0.0 0 0.0 20 2.5 2,707 1.1

Low 0 0.0 0 0.0 20 1.6 2,525 0.7

Moderate 0 0.0 0 0.0 76 6.0 11,525 3.3

Low 0 0.0 0 0.0 6 9.7 262 2.6

Moderate 0 0.0 0 0.0 2 3.2 78 0.8

Low 0 0.0 0 0.0 0 0.0 0 0.0

Moderate 0 0.0 0 0.0 0 0.0 0 0.0

Low 0 0.0 0 0.0 32 1.5 3,832 0.6

Moderate 0 0.0 0 0.0 98 4.6 14,310 2.4

Middle 3 16.7 512 11.3 309 14.5 54,087 9.0

Upper 15 83.3 4,020 88.7 1,693 79.4 531,638 88.0

Total 18 100.0 4,532 100.0 2,132 100.0 603,867 100.0

Unknown 2 241 379 168,452

( ) represents the total number of bank loans for the specific Loan Purpose where income is known

Percentage's (%) are calculated on all loans where incomes are known

(7) Home Purchase (796)

Distribution of HMDA Loans by Income Level of Borrower

Dare, NC NonMSA (2008)

Income

Categories

Bank Aggregate

(0) Multi-Family (0)

HMDA Totals

(11) Refinance (1,274)

(0) Home Improvement (62)

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

17

D&B data indicated that 90% of all local businesses have revenues that do not exceed $1 million per year. Aggregate lending data from 2008 is considered as an element of performance context in the analysis because the 2009 aggregate data is not yet available. During 2008, a peer group of traditional bank lenders, which excludes credit card and other specialty lenders, originated 69.8% of the reported small business loans to businesses with annual revenues of $1 million or less. The remaining loans were to businesses with revenues in excess of $1 million per year or revenues were not known. Based on the sample of small business loan, 100% of the bank’s small business loans were to businesses with annual revenues of $1 million or less. The bank’s performance is considered excellent. Geographic Distribution of Loans Although Dare County does not include any low- or moderate-income census tracts, there are three middle- income and three upper-income census tracts within the county. The bank’s geographic distribution performance is considered reasonable for both HMDA and small business lending within the countywide assessment area. During 2008, MB’s level of HMDA lending in middle-income census tracts (15%) lags the percentage of owner-occupied housing units located in middle-income areas (52.8%) and the 2008 aggregate level of lending (39.9%). The bank’s performance, however, improved during 2009. According to MB’s 2009 data, 16 (28.6%) loans totaling $3.2 million were extended to residents of the middle-income census tracts. The bank’s Dare County assessment area is a popular beach vacation destination and includes a large volume of seasonal (non-primary residence) vacation homes as evidenced by the 35.5% owner-occupancy rate. As a mortgage lender, MB provides financing for vacation homes (which are primarily located in upper-income census tracts), as well as traditional owner-occupied primary residences. When considering the effect vacation homes may have on the geographic distribution of lending and the bank’s lending performance for both 2008 and 2009, the geographic distribution for HMDA loans is considered reasonable. The bank’s level of small business lending in middle-income census tracts during 2009 (42.9%) is consistent with the percentage of area businesses located in middle-income areas (42.5%). Overall, MB’s performance is considered reasonable.

by R evenue # % $(000s) % $ # % $(000s) % $

$1 Million or Less 7 100.0 494 100.0 NA NA NA NA

Over $1 Million 0 0.0 0 0.0 NA NA NA NA

Unknown 0 0.0 0 0.0 NA NA NA NA

by Loan S ize

$100,000 or less 6 85.7 270 54.7 NA NA NA NA

$100,001-$250,000 1 14.3 224 45.3 NA NA NA NA

$250,001-$1 Million 0 0.0 0 0.0 NA NA NA NA

Total 7 100.0 494 100.0 NA NA NA NA

* No data is available for Aggregate loans with Revenues over $1 million and those with Unknown revenues

Distribution of Lending by Loan Amount and Size of Business

Dare, NC NonMSA (2009)

Bank Aggregate*

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

18

Community Development Loans, Investments, and Services Discussions with an individual knowledgeable of the local market area and reviews of the performance evaluations of other financial institutions having a local presence indicate that only limited local community development opportunities are available in the assessment area. Given its current loan-to-deposit ratio (108.8%), the bank’s capacity for additional lending, including community development lending, is somewhat constrained. Additionally, the bank faces moderate constraints regarding investment activity when considering its balance sheet structure and funding strategies. The bank faces no constraints, however, in providing community development services. Since the previous evaluation in May 2008, the bank and its employees have participated or provided the following community development activities within the assessment area:

The bank originated a $500,000 multifamily affordable housing loan.

A bank employee participates in the fund raising activities for the benefit of Community Care Clinic of Dare, a local nonprofit entity that provides community services to low- and moderate-income residents.

Overall, the bank has demonstrated an adequate level of responsiveness to local community development needs through its lending as well as support of area organizations that facilitate community development.

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

19

CRA APPENDIX A

SCOPE OF EXAMINATION

ASSESSMENT AREA TYPE OF

EXAMINATION

BRANCHES

VISITED1

Virginia Beach-Norfolk-

Newport News, VA-NC

MSA

Full-Scope

1101 Executive

Boulevard

Chesapeake, Virginia

Greenbrier Office

750 Volvo Parkway

Chesapeake, Virginia

Dare County, North Carolina Full-Scope None

1 There is a statutory requirement that the written evaluation of a multistate institution’s performance must list the individual

branches examined in each state.

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

20

CRA APPENDIX B

SUMMARY OF STATE RATINGS

State Overall State Rating

Virginia Satisfactory

North Carolina Satisfactory

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

21

CRA APPENDIX C

GLOSSARY Aggregate lending: The number of loans originated and purchased by all reporting lenders in specified income categories as a percentage of the aggregate number of loans originated and purchased by all reporting lenders in the metropolitan area/assessment area. Census tract: A small subdivision of metropolitan and other densely populated counties. Census tract boundaries do not cross county lines; however, they may cross the boundaries of metropolitan statistical areas. Census tracts usually have between 2,500 and 8,000 persons, and their physical size varies widely depending upon population density. Census tracts are designed to be homogeneous with respect to population characteristics, economic status, and living conditions to allow for statistical comparisons. Community development: All Agencies have adopted the following language. Affordable housing (including multifamily rental housing) for low- or moderate-income individuals; community services targeted to low- or moderate-income individuals; activities that promote economic development by financing businesses or farms that meet the size eligibility standards of the Small Business Administration’s Development Company or Small Business Investment Company programs (13 CFR 121.301) or have gross annual revenues of $1 million or less; or, activities that revitalize or stabilize low- or moderate-income geographies. Effective September 1, 2005, the Board of Governors of the Federal Reserve System, Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corporation have adopted the following additional language as part of the revitalize or stabilize definition of community development. Activities that revitalize or stabilize-

(i) Low-or moderate-income geographies; (ii) Designated disaster areas; or (iii) Distressed or underserved nonmetropolitan middle-income geographies designated by

the Board, Federal Deposit Insurance Corporation, and Office of the Comptroller of the Currency, based on- a. Rates of poverty, unemployment, and population loss; or b. Population size, density, and dispersion. Activities that revitalize and stabilize

geographies designated based on population size, density, and dispersion if they help to meet essential community needs, including needs of low- and moderate-income individuals.

Consumer loan(s): A loan(s) to one or more individuals for household, family, or other personal expenditures. A consumer loan does not include a home mortgage, small business, or small farm loan. This definition includes the following categories: motor vehicle loans, credit card loans, home equity loans, other secured consumer loans, and other unsecured consumer loans. Family: Includes a householder and one or more other persons living in the same household who are related to the householder by birth, marriage, or adoption. The number of family households always equals the number of families; however, a family household may also include non-relatives living with the family. Families are classified by type as either a married-couple family or other family, which is further classified into ‘male householder’ (a family with a male householder and no wife present) or ‘female householder’ (a family with a female householder and no husband present). Full-scope review: Performance under the Lending and Community Development Tests is analyzed considering performance context, quantitative factors (for example, geographic distribution, borrower distribution, and total number and dollar amount of investments), and qualitative factors (for example, innovativeness, complexity, and responsiveness).

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

22

Geography: A census tract delineated by the United States Bureau of the Census in the most recent decennial census. Home Mortgage Disclosure Act (HMDA): The statute that requires certain mortgage lenders that do business or have banking offices in a metropolitan statistical area to file annual summary reports of their mortgage lending activity. The reports include such data as the race, gender, and the income of applications, the amount of loan requested, and the disposition of the application (for example, approved, denied, and withdrawn). Home mortgage loans: Includes home purchase and home improvement loans as defined in the HMDA regulation. This definition also includes multifamily (five or more families) dwelling loans, loans for the purchase of manufactured homes and refinancings of home improvement and home purchase loans. Household: Includes all persons occupying a housing unit. Persons not living in households are classified as living in group quarters. In 100 percent tabulations, the count of households always equals the count of occupied housing units. Limited-scope review: Performance under the Lending and Community Development Tests is analyzed using only quantitative factors (for example, geographic distribution, borrower distribution, total number and dollar amount of investments, and branch distribution). Low-income: Individual income that is less than 50 percent of the area median income, or a median family income that is less than 50 percent, in the case of a geography. Market share: The number of loans originated and purchased by the institution as a percentage of the aggregate number of loans originated and purchased by all reporting lenders in the metropolitan area/assessment area. Metropolitan area (MA): A metropolitan statistical area (MSA) or a metropolitan division (MD) as defined by the Office of Management and Budget. A MSA is a core area containing at least one urbanized area of 50,000 or more inhabitants, together with adjacent communities having a high degree of economic and social integration with that core. A MD is a division of a MSA based on specific criteria including commuting patterns. Only a MSA that has a population of at least 2.5 million may be divided into MDs. Middle-income: Individual income that is at least 80 percent and less than 120 percent of the area median income, or a median family income that is at least 80 percent and less than 120 percent, in the case of a geography. Moderate-income: Individual income that is at least 50 percent and less than 80 percent of the area median income, or a median family income that is at least 50 percent and less than 80 percent, in the case of a geography. Multifamily: Refers to a residential structure that contains five or more units. Other products: Includes any unreported optional category of loans for which the institution collects and maintains data for consideration during a CRA examination. Examples of such activity include consumer loans and other loan data an institution may provide concerning its lending performance. Owner-occupied units: Includes units occupied by the owner or co-owner, even if the unit has not been fully paid for or is mortgaged.

Monarch Bank CRA Public Evaluation

Chesapeake, Virginia May 10, 2010

23

Qualified investment: A qualified investment is defined as any lawful investment, deposit, membership share, or grant that has as its primary purpose community development. Rated area: A rated area is a state or multistate metropolitan area. For an institution with domestic branches in only one state, the institution’s CRA rating would be the state rating. If an institution maintains domestic branches in more than one state, the institution will receive a rating for each state in which those branches are located. If an institution maintains domestic branches in two or more states within a multistate metropolitan area, the institution will receive a rating for the multistate metropolitan area. Small loan(s) to business(es): A loan included in 'loans to small businesses' as defined in the Consolidated Report of Condition and Income (Call Report) and the Thrift Financial Reporting (TFR) instructions. These loans have original amounts of $1 million or less and typically are either secured by nonfarm or nonresidential real estate or are classified as commercial and industrial loans. However, thrift institutions may also exercise the option to report loans secured by nonfarm residential real estate as "small business loans" if the loans are reported on the TFR as nonmortgage, commercial loans. Small loan(s) to farm(s): A loan included in ‘loans to small farms’ as defined in the instructions for preparation of the Consolidated Report of Condition and Income (Call Report). These loans have original amounts of $500,000 or less and are either secured by farmland, or are classified as loans to finance agricultural production and other loans to farmers. Upper-income: Individual income that is more than 120 percent of the area median income, or a median family income that is more than 120 percent, in the case of a geography.

![Monarch Programmer’s Guide - Product Documentationdocs.datawatch.com/monarch/programmers_guide/Data... · Monarch 14 Programmer's Guide 3 [2] Monarch Properties and Methods This](https://img.pdfslide.net/doc/110x75/5ae7d2b47f8b9acc268f2fe4/monarch-programmers-guide-product-14-programmers-guide-3-2-monarch-properties.jpg)