Embed Size (px)

Citation preview

Monetary EconomicsChapter 8: Money and credit

Prof. Aleksander Berentsen

University of Basel

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 1 / 125

Structure of this chapter

1 Introduction2 Dichotomy between money and credit3 Costly record-keeping4 Strategic complementaries and payments5 Short-term and long-term partnerships6 Money, Credit and Banking7 Conclusion

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 2 / 125

Introduction

Many modes of payments coexist in actual economies:

credit arrangements, where trades are intertemporal by nature andinvolve a future payment;

monetary exchanges, where trades are quid pro quo and do notinvolve future obligations.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 3 / 125

Introduction

One way to explain the coexistence of monetary exchange and creditarrangements is to introduce some heterogeneity among agentsand/or trading matches.

In some markets agents are anonymous, and can therefore only tradewith money, while in others their identities can be veri�ed, andintertemporal contracts can be enforced, and thus agents can resortto credit arrangements.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 4 / 125

Introduction

We �rst consider an environment where there is a technology thatenforces debt contracts in some markets but not in others.

We then assume that the gains from trade vary across matches in thedecentralized market, and that the use of credit involves a costlyrecord-keeping technology.

In the next section, we capture the notion of commitment throughthe reputation that buyers acquire by trading repeatedly with somesellers. We show that the availability of credit depends on the valueof money and monetary policy, and the extent of the trading frictions.

Finally, we will see a model which analyzes the role that banks haveas intermediaries, and the gain in utility they can provide.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 5 / 125

Structure of this chapter

1 Introduction2 Dichotomy between money and credit3 Costly record-keeping4 Strategic complementaries and payments5 Short-term and long-term partnerships6 Money, Credit and Banking7 Conclusion

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 6 / 125

Dichotomy between money and credit

In this section, we divid the day market into two subperiods: amorning (DM1) and an afternoon (DM2).

The morning and afternoon subperiods are similar in terms of agents�preferences and specialization:

buyers can consume in both subperiods but cannot produce,sellers can produce but cannot consume

and in terms of the trading process

buyers and sellers trade in bilateral matches.

The discount factor across periods is β.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 7 / 125

Dichotomy between money and credit

The buyer�s instantaneous utility function is

Ub(q1, q2, x , h) = υ(q1) + u(q2) + x � h,

where q1 is the consumption in the �rst subperiod, q2 is the consumptionin the second subperiod, x is the consumption of the general good in thethird subperiod, and h is the utility cost of producing h units of thegeneral good.

The utility functions υ(q) and u(q) are strictly increasing and concave,with

υ(0) = u(0) = 0,

υ0(0) = u0(0) = +∞,υ0(+∞) = u0(+∞) = 0.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 8 / 125

Dichotomy between money and credit

The utility function of a seller is

Us (q1, q2, x , h) = �ψ(q1)� c(q2) + x � h,

where functions ψ(q) and c(q) are strictly increasing and convex, with

ψ(0) = c (0) = 0,

ψ0(0) = c 0 (0) = 0,

ψ0(+∞) = c 0 (+∞) = 0.

We denote q�1 the solution to υ0(q) = ψ0(q) and q�2 the solution tou0(q) = c 0(q). These are the quantities that maximize the matchsurpluses in the �rst two subperiods.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 9 / 125

Dichotomy between money and credit

MORNING(DM 1)

AFTERNOON(DM 2)

NIGHT(CM)

Utility of consumption:

Disutility of production: )()(

1

1

ψυ

− )()(

2

2

qcqu

− h−

AnonymityRecordkeepingEnforcement

RecordkeepingEnforcement

Figure 8.1: Timing of a representative period

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 10 / 125

Dichotomy between money and credit

Both the DM1 and the DM2 are characterized by search frictions.

A buyer meets a seller in the DM1 with probability σ1 2 [0, 1], and inthe DM2 with probability σ2 2 [0, 1], where σ1 and σ2 areindependent events.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 11 / 125

Dichotomy between money and credit

In the DM1 all agents�identities are known to all other agents.

We assume that any contract written in the DM1 can be (and willbe) enforced at night.

As a result, buyers can get output in the DM1 by using credit� or,equivalently, by issuing an IOU� to be repaid at night.

We will assume that all the IOUs are �one period� in nature in thatthey are repaid in the subsequent competitive night market, CM.

Moreover, the authenticity of the IOUs issued in DM1 cannot beveri�ed in DM2, and hence they cannot be used as medium ofexchange in the afternoon.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 12 / 125

Dichotomy between money and credit

In the DM2 all agents are anonymous.

Since buyers are anonymous in the DM2, bilateral trades cannot bepublicly recorded or enforced.

As a result, sellers do not accept IOUs for output produced in the DM2since buyers would renege on these at night.Because of the anonymity of agents in the DM2, money has anessential role in this environment.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 13 / 125

Dichotomy between money and credit

We assume that the stock of money grows at a constant rateγ � Mt+1/Mt , and that this is accomplished by a lump-sum transfersto buyers in the CM.

We focus on stationary equilibria where real balances and thequantities traded in the di¤erent subperiods are constant over time:φt+1

φt= Mt

Mt+1= γ�1.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 14 / 125

Dichotomy between money and creditBeginning of the CM

Consider a buyer at the beginning of the CM who holds z = φtm units ofreal balances and has issued b units of IOUs in the previous DM1, whereeach unit is normalized to be worth one unit of general good.

The value function for this buyer, W b(z ,�b), is given by

W b(z ,�b) = maxx ,h,z 0

nx � h+ βV b(z 0)

o(8.1)

x + b+ γz 0 = z + h+ T , (8.2)

where V b is the value of a buyer at the beginning of the day market.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 15 / 125

Dichotomy between money and creditBeginning of the CM

Substituting x � h from (8.2) into (8.1), we get

W b(z ,�b) = z � b+ T +maxz 0�0

n�γz 0 + βV b(z 0)

o. (8.3)

As before, the value function is linear in the buyer�s current portfolio, andthe buyer�s choice of real balances is independent of his current portfolio.(Also, recall that sellers do not receive transfers in the CM.)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 16 / 125

Dichotomy between money and creditBeginning of the CM

The value function of a seller holding z units of real balances and b IOUsat the beginning of the CM is given by

W s (z , b) = z + b+ βV s , (8.4)

where V s is the value function of a seller at the beginning of the nextperiod.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 17 / 125

Dichotomy between money and creditBilateral match in the DM2

Consider now a bilateral match in the DM2 between a buyer holdingz units of real balances and a seller.

The buyer is anonymous and cannot use credit.

Hence, he can transfer at most z units of real balances to the seller inexchange for afternoon output.

We assume that the buyer makes a take-it-or-leave-it o¤er.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 18 / 125

Dichotomy between money and creditBilateral match in the DM2

The buyer�s o¤er to the seller is given by the solution to the followingsimple problem,

maxq2,d2

[u(q2)� d2]

s.t. � c(q2) + d2 � 0 and d2 � z ,where the �rst inequality represents the seller�s participation constraintand the second is a feasibility constraint.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 19 / 125

Dichotomy between money and creditBilateral match in the DM2

The solution to this maximization problem is

c(q2) = min [c(q�2 ), z ] , (8.5)

d2 = c(q2), (8.6)

! The buyer purchases the e¢ cient level of output if he has su¢ cient realbalances; otherwise he spends all of his balances on output.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 20 / 125

Dichotomy between money and creditBilateral match in the DM1

Since buyers�identities are known and there is a technology thatenforces contracts at night, they can purchase output with IOUs.

If the buyer defaults on his IOU, he can be subject to an arbitrarilylarge �ne in the CM.

The buyer can also use his money holdings as means of payment inthe morning.

For a given level of real balances, spending money balances in theDM1 is a (weakly) dominated strategy since the buyer might needmoney to trade in the DM2.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 21 / 125

Dichotomy between money and creditBilateral match in the DM1

Suppose then that buyers only use credit to purchase output in the DM1.The buyer makes a take-it-or-leave-it o¤er (q1, b) to the seller so as tomaximize his surplus

υ(q1)� b,subject to the seller�s participation constraint

�ψ(q1) + b � 0.

Thanks to the enforcement technology in the CM, there is no feasibilityconstraint imposed on the transfer of IOUs since the buyer can issue asmuch debt as he wishes.

The solution to the buyer�s problem in the DM1 is

q1 = q�1 (8.7)

b = ψ(q�1 ). (8.8)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 22 / 125

Dichotomy between money and credit

Given the terms of trade established in the DM1 and DM2, the valuefunction of a buyer holding z units of real balances at the beginning of aperiod is

V b(z) = σ1σ2n

υ(q�1 ) + u[q2(z)] +Wb [�b, z � d2(z)]

o+σ1(1� σ2)

nυ(q�1 ) +W

b (�b, z)o

+(1� σ1)σ2nu[q2(z)] +W b [0, z � d2(z)]

o+(1� σ1)(1� σ2)W b (0, z) . (8.9)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 23 / 125

Dichotomy between money and credit

Using the linearity of W b , the beginning-of-period value function can besimpli�ed to

V b(z) = σ1 fυ(q�1 )� ψ(q�1 )g+ σ2 fu[q2(z)]� c [q2(z)]g+z +W b (0, 0) . (8.10)

If we substitute V b(z) from (8.10) into (8.3), then the buyer�s portfolioproblem in the CM can be represented by

maxz�0

f�iz + σ2 fu[q2(z)]� c [q2(z)]gg , (8.11)

where i � γ�ββ . Note that the buyer�s real balances only a¤ects his surplus

in the DM2.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 24 / 125

Dichotomy between money and credit

The �rst-order condition for problem (8.11) is

u0(q2)c 0(q2)

= 1+i

σ2. (8.12)

This expression for the output traded in the DM2 is identical to the onewe derived for the pure monetary economy.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 25 / 125

Dichotomy between money and credit

The allocation is dichotomic in the sense that the output traded in theDM1, q1, is independent of both the quantity traded in the DM2, q2, andthe value of money, φt .

As well, when in�ation increases, q1 is una¤ected and remains at thee¢ cient level, while q2 decreases, see equation (8.12).

So there are no interactions between the DM1 and the DM2.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 26 / 125

Dichotomy between money and credit

In the DM1 a fraction σ1 of the buyers issue debt, while at the same timeholding positive amounts of money. Credit is a preferred means ofpayment because it involves no opportunity cost.

However, credit can only be used in transactions when agents�identitiesare known and debt contracts can be enforced. Buyers will hold money,even though it is more costly than credit, because it allows them toconsume in the DM2 when they are anonymous.

Finally, as the cost of holding money, i , approaches zero, the quantitytraded in the DM2 approaches its e¢ cient level, q�2 . When the cost ofholding money is exactly equal to zero, there is no cost associated withholding real balances, and buyers will be indi¤erent between trading withmoney and credit in the DM1.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 27 / 125

Structure of this chapter

1 Introduction2 Dichotomy between money and credit3 Costly record-keeping4 Strategic complementaries and payments5 Short-term and long-term partnerships6 Money, Credit and Banking7 Conclusion

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 28 / 125

Costly record-keeping

We now consider an environment where money and credit coexist, andmonetary policy a¤ects the composition of monetary and credittransactions.

The model is similar as in Chapter 5, "Divisibility of money", but we add acostly record-keeping technology.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 29 / 125

Costly record-keeping

The instantaneous utility function of a buyer is given by

Ub = εu(q) + x � h,

where ε 2 R+ is a match-speci�c preference shock. The preference shock,ε, is drawn from a cumulative distribution, F (ε), with support [0, εmax].

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 30 / 125

Costly record-keeping

Matched agents in the DM have the option to record a credit transactionat a real cost of ζ > 0. If a credit transaction is recorded in the DM, weassume that its repayment is enforced at night.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 31 / 125

Costly record-keeping

The value functions for buyers and sellers at the beginning of the CM,W b(z ,�b) and W s (z , b), are given by equations (8.3) and (8.4):

W b(z ,�b) = z � b+ T +maxz 0�0

n�γz 0 + βV b(z 0)

o. (8.3)

W s (z , b) = z + b+ βV s , (8.4)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 32 / 125

Costly record-keeping

Consider a match in the DM between a buyer with match speci�cpreference shock ε holding z units of real balances, and a seller. The buyermakes a take-it-or-leave-it o¤er to the seller. The terms of trade, (q, b, d),are given by the solution to

maxq,d ,b

�εu(q)� d � b� ζIfb>0g

�s.t. � c(q) + d + b � 0 and d � z ,

where Ifb>0g = 1 if b > 0 and Ifb>0g = 0, otherwise.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 33 / 125

Costly record-keeping

If the buyer chooses to use credit as a means of payment, he mustincur the �xed cost ζ due to record-keeping.

If the buyer incurs the �xed cost, then the solution is

q = q�ε

with d + b = c(q�ε ), where q�ε solves εu0 (q�ε ) = c

0 (q�ε ).

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 34 / 125

Costly record-keeping

If the buyer does not incur the �xed cost to use credit, then

q = qε(z) = c�1 [min (c(q�ε ), z)]

andd = c(q)

If he has enough real balances, the buyer purchases the e¢ cient levelof output for his particular preference shock; otherwise he spends allof his real balances.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 35 / 125

Costly record-keeping

The buyer�s surplus from a trade match in the DM is

Sb(z , ε) = max fεu(q�ε )� c(q�ε )� ζ , εu [qε(z)]� c [qε(z)]g . (8.13)

Note that Sb(z , ε) is increasing in ε, i.e., both terms in the maximizationproblem increase with ε. We represent each of these terms as a function ofε in Figure 8.2. The slope of the �rst term is u(q�ε ), and the slope of thesecond is u [qε(z)].

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 36 / 125

Costly record-keeping

Let ε̄ denote the value of ε such that c(q�ε̄ ) = z , i.e., ε̄ is a thresholdbelow which the buyer has enough real balances to purchase the e¢ cientlevel of DM output.

For all ε < ε̄, u [qε(z)] = u(q�ε ), which implies that the slopes of the twoterms in the maximization problem (8.13) are equal.

For all ε > ε̄, u [qε(z)] < u(q�ε ), and the slope of the second term in themaximization problem (8.13) is independent of ε and lower than the slopeof the �rst term.

When ε = 0, the �rst term is equal to �ζ, while the second is equal tozero.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 37 / 125

Costly record-keeping

For ε > ε̄ su¢ ciently large,

fεu(q�ε )� c(q�ε )� ζg � fεu [qε(z)]� c [qε(z)]g > 0.

Consequently, there exists a threshold εc > ε̄ above which the buyer usescredit as means of payment and below which he uses money.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 38 / 125

Costly record-keeping

This threshold is given by,

εcu(q�εc )� c(q�εc )� ζ = εcu

�c�1(z)

�� z . (8.14)

Graphically, the �rst term in the maximization problem (8.13) intersectsthe second term from below at ε = εc , see Figure 8.2.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 39 / 125

Costly record-keeping

Buyer’s surplus

Trades with creditTrades with money

ζε εε −− )()( ** qcqu

)()( zqczqu εεε −

cε

Figure 8.2: Credit vs monetary trades

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 40 / 125

Costly record-keeping

It should be emphasized that the value of the threshold, εc , is for a givenlevel of real balances, z . Hence, from (8.14), εc increases with z , i.e.,

dεcdz

=

εcu 0(c�1(z ))c 0(c�1(z )) � 1

u�q�εc�� u (c�1 (z))

> 0,

since q�εc > c�1 (z) for εc > ε̄.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 41 / 125

Costly record-keeping

Graphically, as z increases ε̄ increases and for all ε > ε̄ the second term ofthe maximization problem (8.13) moves upward. Buyers increase theirsurplus by holding more real balances in all trades where they don�t tradethe e¢ cient quantity. Consequently, as buyers hold more real balances thefraction of trades conducted with credit decreases: money and credit arecomplements.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 42 / 125

Costly record-keeping

Using the linearity of W b , the value of being a buyer at the beginning ofthe period, V b(z), is

V b(z) = σZ εmax

0Sb(z , ε)dF (ε) +W b(z). (8.15)

Substituting V b(z) from (8.15) into (8.3), and simplifying, we get

maxz�0

��iz + σ

Z εmax

0Sb(z , ε)dF (ε)

�. (8.16)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 43 / 125

Costly record-keeping

The objective function in (8.16) is continuous and the solution to (8.16)must lie in the interval [0, c(q�εmax)] for all i > 0.

An equilibrium corresponds to a pair (εc , z) that solves (8.14) and (8.16)and can be determined recursively: A value for z is determinedindependently by (8.16), and given this value for z , (8.14) determines aunique εc .

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 44 / 125

Costly record-keepingE¤ects of monetary policy

We now investigate the e¤ects that monetary policy has on the use of �atmoney and credit as means of payment. The �rst-order (necessary but notsu¢ cient) condition associated with (8.16) is

i = σZ εc (z )

ε̄(z )

(εu0�c�1(z)

�c 0 [c�1(z)]

� 1)dF (ε). (8.17)

From (8.17), real balances have a liquidity return when the realization ofthe preference shock is not too low� so that the buyer�s budget constraintin the match is binding� and when the preference shock is not toohigh� so that it is not pro�table for buyers to use credit� i.e., whenε̄ (z) < ε < εc (z).

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 45 / 125

Costly record-keepingE¤ects of monetary policy

Suppose that in�ation and, hence, the cost of holding money, i , increases:

the right side of (8.17) must also increase,

it reduces buyers�real balances and increases the use of costly credit,

As the cost of holding real balances approaches zero, from (8.16):

real balances approach c(q�εmax),

buyers �nd it pro�table to trade with money only.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 46 / 125

Structure of this chapter

1 Introduction2 Dichotomy between money and credit3 Costly record-keeping4 Strategic complementaries and payments5 Short-term and long-term partnerships6 Money, Credit and Banking7 Conclusion

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 47 / 125

Strategic complementarities and payments

In order to be able to accept credit, sellers must invest ex-ante� i.e.,before trades take place� in a record-keeping technology that allowsthe transactions to be recorded and enforced.

Buyers will form rational expectations about sellers�investmentdecisions and choose which means of payment(s) to carry intomeetings.

These decisions made by buyers and sellers create strategiccomplementarities for payment choices and network-like externalities.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 48 / 125

Strategic complementarities and payments

The model with network externalities is similar to that of the previoussection, but modi�ed in the following ways:

All matches are identical, i.e., ε = 1.

It is the seller who invests in the record-keeping technology and thisinvestment is undertaken at the beginning of the DM before matchesare formed.

The cost to invest in this technology is ζ > 0.

The pricing mechanism must be changed from the previous section toone that permits sellers to extract a fraction of the match surplus;otherwise sellers could not recover their ex ante investment costs andwould have no incentive to invest in the record-keeping technology.

Again, the buyer receives a constant share θ 2 [0, 1) of the match surplus,while the seller gets the remaining 1� θ > 0 share.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 49 / 125

Strategic complementarities and paymentsSeller invest in the technology

Consider �rst a match between a buyer holding z units of real balancesand a seller who has invested in the technology. The terms of trade aregiven by the solution to the following problem:

maxq,d ,b

[u(q)� d � b] (8.18)

s.t. � c(q) + d + b � 1� θ

θ[u(q)� d � b] (8.19)

d � z (8.20)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 50 / 125

Strategic complementarities and paymentsSeller invest in the technology

Since b is unconstrained� buyers can borrow as much as they want in theDM� the constraint d � z never constrains the purchase of q.

Because of this, the output produced in the DM will be at the e¢ cientlevel, q = q�, and d + b = (1� θ) u(q�) + θc(q�), i.e., the seller gets thefraction 1� θ of match surplus.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 51 / 125

Strategic complementarities and paymentsSeller does not invest in the technology

Consider next the case where the seller has not invested in therecord-keeping technology. The terms of trade are still determined by theproblem (8.18)-(8.20), but with the added constraint that b = 0. Ifz � (1� θ) u(q�) + θc(q�), then the buyer will have su¢ cient moneybalances to purchase the e¢ cient level of output and q = q�; otherwise,the level of DM output, q(z), will satisfy

z = z(q) � (1� θ) u(q) + θc(q), (8.21)

where q (z) < q�.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 52 / 125

Strategic complementarities and paymentsSeller�s decision

Considering that all buyers hold the same real balances, z , it is optimal fora seller to invest in the technology if

σ(1� θ) [u(q(z))� c(q(z))] � σ(1� θ) [u(q�)� c(q�)]� ζ. (8.22)

From (8.22), the �ow cost to invest in the record-keeping technology mustbe less than the increase in the seller�s expected surplus associated withaccepting credit instead of money.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 53 / 125

Strategic complementarities and paymentsSeller�s decision

The left side of (8.22) is increasing in z :

it equals 0 if z = 0

it equals σ(1� θ) [u(q�)� c(q�)] if z � (1� θ) u(q�) + θc(q�).

Consequently, if ζ < σ(1� θ) [u(q�)� c(q�)], then there exists athreshold zc > 0 for the buyer�s real balances, below which sellers invest inthe record-keeping technology.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 54 / 125

Strategic complementarities and paymentsSeller�s decision

This threshold is given by the solution to

u [q(zc )]� c [q(zc )] = u(q�)� c(q�)�ζ

σ(1� θ). (8.23)

Let Λ be the measure of sellers who invest in the record-keepingtechnology. Then,

Λ =

8<:1

2 [0, 1]0

if z

8<:<=>

zc . (8.24)

The seller�s reaction function is depicted in Figure 8.3. As buyers holdmore money, sellers have less incentives to invest in the costlyrecord-keeping technology.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 55 / 125

Strategic complementarities and paymentsBuyer�s decision

Given the seller�s decision to invest in the record-keeping technology,(8.24), the buyer�s decision problem is given by

maxz�0

f�iz + σ(1�Λ)θ fu[q(z)]� c [q(z)]g+ σΛθ fu(q�)� c(q�)gg .(8.25)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 56 / 125

Strategic complementarities and paymentsBuyer�s decision

The �rst-order condition for problem (8.25) is

[σ(1�Λ)θ � i (1� θ)] u0(q)� [i + σ(1�Λ)] θc 0(q)(1� θ) u0(q) + θc 0(q)

� 0, (8.26)

and holds with an equality if z > 0. If z > 0, and the numerator of (8.26)will equal to zero, and

u0 (q)c 0 (q)

=[i + σ (1�Λ)] θ[i + σ(1�Λ)] θ � i . (8.27)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 57 / 125

Strategic complementarities and paymentsBuyer�s decision

The right side of (8.27) is increasing with Λ, which implies that anincrease in Λ will decrease q, and, hence, z . Therefore, the buyer�s choiceof real balances is decreasing in Λ.

Intuitively, if it is more likely to �nd a seller who accepts credit, thenmoney is needed in a smaller fraction of matches, and since it is costly tohold money buyers will �nd it optimal to hold fewer real balances.

Moreover, there is a critical value for Λ above which buyers hold no realbalances, and this happens when the denominator of equation (8.27) isequal to zero, or when Λc =

σθ�(1�θ)iσθ , where Λc > 0 if i < σθ

1�θ .

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 58 / 125

Strategic complementarities and payments

1

0z

cz

σθθσθ i

c)1( −−

=Λ

Sellers’ reaction function

Buyers’ reaction function

Figure 8.3: Buyers�and sellers�reaction functions

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 59 / 125

Strategic complementarities and paymentsSymmetric equilibrium

A stationary symmetric equilibrium is a pair (z ,Λ) that solves (8.24) and(8.25).

There exists a pure monetary equilibrium with Λ = 0 and z > 0; a purecredit equilibrium, with Λ = 1 and z = 0; and a �mixed�monetaryequilibrium, where buyers use both credit and money, accumulating zc > 0real balances, and a fraction 1�Λ 2 (0, 1) sellers accept only money,while other sellers, Λ 2 (0, 1) of them, are willing to accept both moneyand credit.

The multiplicity of equilibria arises from the strategic complementaritiesbetween the buyers�decisions to hold real balances and the sellers�decisions to invest in the record-keeping technology.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 60 / 125

Strategic complementarities and paymentsSocial welfare

When there are multiple equilibria, which one is preferred from thesociety�s viewpoint? Social welfare is given by

W = σΛ fu(q�)� c(q�)g+ σ(1�Λ) fu [q(z)]� c [q(z)]g �Λζ.

Consider a case where z0 is greater but close to zc :

There is a pure monetary equilibrium with z = z0, Λ = 0, and socialwelfare is W0 = σ fu [q(z0)]� c [q(z0)]g � ζ.

There is also a pure credit equilibrium with Λ = 1 and social welfareis W1 = σ fu(q�)� c(q�)g � ζ.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 61 / 125

Strategic complementarities and paymentsSocial welfare

Given the de�nition of zc in (8.23),

ζ � σ(1� θ) f[u(q�)� c(q�)]� [u(q(z0))� c(q(z0))]g< σ f[u(q�)� c(q�)]� [u(q(z0))� c(q(z0))]g ,

where we get the strict inequality because θ > 0.

In this case, the di¤erence in the surpluses associated with credit andmonetary transactions strictly exceeds the cost of investment in therecord-keeping technology.

Hence, W1 >W0, the pure monetary equilibrium is dominated, from asocial welfare perspective, by the pure credit equilibrium.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 62 / 125

Strategic complementarities and paymentsSocial welfare

However, the socially ine¢ cient monetary equilibrium can prevail becauseof a hold-up externality. If a seller decides to adopt the technology toaccept credit, he incurs the full cost of the technology adoption, but heonly receives a fraction 1� θ < 1 of the increase in the match surplus.

Hence, sellers fail to internalize the e¤ect of the credit technology onbuyers�surpluses, which can lead to excess inertia* in the decision toadopt the record-keeping technology.

*Excess inertia occurs when a particular compatibility switch wouldincrease social welfare, but each player is not willing to initiate it, unsure ifothers will follow.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 63 / 125

Strategic complementarities and paymentsSocial welfare, i close to zero

When i is close to zero, z0 will be close to θc(q�) + (1� θ)u(q�) andq(z0) � q�. Hence, W0 � σ fu(q�)� c(q�)g. Provided that ζ > 0 thepure monetary equilibrium dominates the pure credit equilibrium from asocial welfare perspective.

The resources allocated to the record-keeping technology are �wasted� inthe sense that a monetary equilibrium avoids costs associated withrecord-keeping and provides an allocation that is almost as good as thecredit allocation.

Still, if ζ < σ(1� θ) [u(q�)� c(q�)], agents can end up coordinating onthe inferior (credit) equilibrium because of the strategic complementaritiesbetween the buyers�and sellers�choices.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 64 / 125

Structure of this chapter

1 Introduction2 Dichotomy between money and credit3 Costly record-keeping4 Strategic complementaries and payments5 Short-term and long-term partnerships6 Money, Credit and Banking7 Conclusion

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 65 / 125

Short-term and long-term partnerships

In the next section, we capture the notion of commitment through thereputation that buyers acquire by trading repeatedly with some sellers.

We show that the availability of credit depends on the value of money andmonetary policy, and the extent of the trading frictions.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 66 / 125

Short-term and long-term partnerships

We assume that there is no enforcement technology and buyers cannotcommit to repay their debt.

Debt contracts must be self-enforcing.If there can be repeated interactions with a seller, a buyer will wantto generate a reputation for paying his debts, and the buyer�s desirefor this reputation results in contracts being self enforced.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 67 / 125

Short-term and long-term partnerships

We allow for the possibility of both short-term and long-term partnerships.

A short-term match corresponds to a situation where the buyer andthe seller know they will not meet again in the future.

In a long-term match the buyer and the seller have a chance to staytogether for more than one period.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 68 / 125

Short-term and long-term partnerships

At the beginning of a period, unmatched agents can enter into along-term trade match with probability σ` or a short-term tradematch with probability σs , with 0 < σ` + σs < 1.

A short-term match is destroyed with probability one at the end ofthe day or DM, while a long-term match will be exogenouslydestroyed with probability λ < 1 at the beginning of the CM.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 69 / 125

Short-term and long-term partnerships

In addition, either party to a long-term match that is not exogenouslydestroyed can always choose to terminate the relationship at thebeginning of the DM.

Since the measures of buyers and sellers are equal, there are alsoequal measures of unattached buyers and unattached sellers.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 70 / 125

Short-term and long-term partnerships

DAY NIGHT

A fraction ( )

of unmatched agentsfind a longterm

(shortterm) match.

σl σs Matched sellersproduce

in longterm(shortterm) matches.

q (q )l s

Matched buyersin longterm matches

produce y .l

A fractionof longterm

matchesare destroyed.

λ Agents canreadjust their

money holdings.

Figure 8.4: Timing of a representative period.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 71 / 125

Short-term and long-term partnerships

The night period begins with buyers who are in a long-termpartnership producing the general good for sellers if trade wasmediated by credit in the previous DM.

A fraction λ of buyers in the long-term partnership then realize ashock which dissolves the relationship they have with their currentlymatched seller.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 72 / 125

Short-term and long-term partnerships

This is followed by the opening of the CM, where the general goodand money are traded.

In terms of pricing mechanisms, we assume that buyers maketake-it-or-leave-it o¤ers to sellers in the DM, and that the nightmarket is competitive, where one unit of money trades for φt units ofthe general good.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 73 / 125

Short-term and long-term partnerships

We will restrict our attention to a particular class of equilibria that exhibittwo features.

First, money is valued, but is only used in short-term trade matches.

Second, the buyer�s incentive-compatibility constraint in long-termmatches� that the buyer is willing to produce the general good forthe seller to extinguish his debt obligation� is not binding.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 74 / 125

Short-term and long-term partnerships

This latter assumption implies that a buyer in a long-term partnershipwill be able to purchase the e¢ cient quantity of the DM search good,q�, with credit alone.

So these equilibria will be such that money and credit coexist but areused in di¤erent types of meetings, as in the previous sections, but wedo not need to impose enforcement or commitment.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 75 / 125

Short-term and long-term partnerships

The value of being an unmatched buyer in the CM, W bu (z), is given by

W bu (z) = z + T +max

z 0�0f�γz 0 + βV bu (z

0)g, (8.28)

where V bu (z0) is the value of being an unmatched buyer holding z 0 units of

real balances at the beginning of a period.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 76 / 125

Short-term and long-term partnerships

The value function of an unmatched buyer in the DM who holds z unitsof real balances, V bu (z), is given by

V bu (z) = σ`Vb` (z) + σsV bs (z) + (1� σ` � σs )W b

u (z). (8.29)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 77 / 125

Short-term and long-term partnerships

The expected lifetime utility of an unmatched seller in the CM is

W su (z) = z + βV su , (8.30)

where we take into account that sellers have no incentives to hold realbalances in the DM.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 78 / 125

Short-term and long-term partnerships

In the DM, the value of an unmatched seller is

V su = σ`Vs` + σsV ss + (1� σ` � σs )W s

u (0), (8.31)

where V s` (Vss ) is the value of a seller in a long-term (short-term) match

in the DM.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 79 / 125

Short-term and long-term partnerships

The buyer in a short-term trade match makes a take-it-or-leave-it o¤er,(qs , ds ), to the seller, where qs is the amount of the search good that theseller produces and ds is the amount of real balances transferred from thebuyer to the seller.

The value function of a buyer holding z units of real balances in ashort-term trade match, V bs (z), is given by

V bs (z) = u [qs (z)] +Wbu [z � ds (z)] = u [qs (z)]� ds (z) + z +W b

u (0),(8.32)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 80 / 125

Short-term and long-term partnerships

Similarly, the value function of a seller (with no real balances) in ashort-term trade match is

V ss = �c [qs (z)] + ds (z) +W su (0), (8.33)

where z represents the buyer�s real balances.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 81 / 125

Short-term and long-term partnerships

The take-it-or-leave-it o¤er by the buyer maximizes the buyer�s surplus

u (qs )� ds

subject to the seller�s participation constraint

�c (qs ) + ds � 0

and the feasibility constraintds � z .

It is characterized by either qs (z) = q� and ds (z) = c(q�) if z � c(q�),or qs = c�1(z) if z < c(q�).

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 82 / 125

Short-term and long-term partnerships

Hence, (8.32) becomes

V bs (z) = u [qs (z)]� c [qs (z)] + z +W bu (0) , (8.34)

and, from (8.33), V ss = Wsu (0).

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 83 / 125

Short-term and long-term partnerships

The value function for a buyer in a long-term relationship holding z unitsof real balances at the beginning of the period is

V b` (z) = u [q`(z)] +Wb` [z � d`(z),�y`(z)] , (8.35)

where W b` (z � d`,�y`) is the value of the matched buyer at night holding

z � d` units of real balances, with a promise to produce y` units of thegeneral good for his trade-match partner.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 84 / 125

Short-term and long-term partnerships

Even though we allow the terms of trade (q`, d`, y`) to depend on thebuyer�s real balances, z , in the following we will consider equilibria wherebuyers don�t use money in long-term partnerships, d` = 0 and (q`, y`) isindependent of z .

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 85 / 125

Short-term and long-term partnerships

The value function of a buyer in a long-term partnership at the beginningof the night satis�es

W b` (z ,�y`) = z � y` + T + λmax

z 0�0f�γz 0 + βV bu (z

0)g

+(1� λ)maxz 00�0

n�γz 00 + βV b` (z

00)o. (8.36)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 86 / 125

Short-term and long-term partnerships

The value function for a seller in a long-term relationship at thebeginning of the period is

V s` = �c [q`(z)] +W s` [d`(z), y`(z)] . (8.37)

The value function of the seller at night is

W s` (z , y`) = z + y` + (1� λ)βV s` + λβV su . (8.38)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 87 / 125

Short-term and long-term partnerships

We now turn to the formation of the terms of trade in long-termpartnerships.

We will assume that the buyer makes a take-it-or-leave-if o¤er,(q`, y`, d`).

The o¤er must satisfy the incentive-compatibility constraint accordingto which the buyer is willing to repay his debt at night.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 88 / 125

Short-term and long-term partnerships

The buyer chooses (q`, y`, d`) in order to maximize V b` (z) subject to theseller�s participation constraint

�c (q`) +W s` (d`, y`) � W s

` (0, 0) ,

and the incentive compatibility constraint

W b` (z � d`,�y`) � W b

u (z � d`) .

The incentive-compatibility constraint states that the buyer is better-o¤paying his debt than walking away from his partnership.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 89 / 125

Short-term and long-term partnerships

The buyer�s problem can be expressed as

maxq,y ,d

[u (q)� y � d ] s.t. � c (q) + y + d � 0, d � z , (8.39)

y � W b` (0, 0)�W b

u (0). (8.40)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 90 / 125

Short-term and long-term partnerships

We will focus on equilibria where the incentive-compatibility constraint(8.40) does not bind for all values of z . As a result, q` = q� andy` + d` = c(q�).

So the terms of trade in long-term partnerships are independent of thebuyer�s real balances. With no loss, we can assume that buyers pay withcredit only, d` = 0.

It is also immediate from (8.35) and (8.36) that a buyer in a long-termpartnership at night will not accumulate real balances (in (8.36) z 00 = 0).

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 91 / 125

Short-term and long-term partnerships

Let us consider the choice of real balances by unmatched buyers. From(8.28)-(8.36), the optimal choice of real balances at night, z , for a buyerwho is not in a long-term relationship satis�es

maxz�0

f�iz + σs fu [qs (z)]� c [qs (z)]gg. (8.41)

This leads to the familiar �rst-order condition,

u0(qs )c 0(qs )

= 1+i

σs. (8.42)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 92 / 125

Short-term and long-term partnerships

The last thing we need to check is that the incentive-compatibilitycondition, (8.40), is not binding.

Using that y` = c(q�), (8.40) becomes

c(q�) � W b` (0, 0)�W b

u (0). (8.43)

With the help of equations (8.29)-(8.36), and after some rearranging,inequality (8.43) can be rewritten as

c(q�) � (1� λ)β f(1� σ`)u(q�) + ic(qs )� σs [u(qs )� c(qs )]g ,

(8.44)where qs satis�es (8.42).

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 93 / 125

Short-term and long-term partnerships

If inequality (8.44) holds, then there exists an equilibrium where buyersand sellers in long-term relationships consume and produce q` = q� unitsof the search good during the day and y` = c(q�) units of the generalgood at night, using credit arrangements to implement these trades.

Buyers and sellers in short-term partnerships trade qs units of the searchgood for ys = c(qs ) units of real balances during the day.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 94 / 125

Short-term and long-term partnerships

Perhaps not surprisingly, if σs = 0, then from (8.42), qs = 0 and theincentive condition (8.44) is identical to the one obtained in a modelwhere money was absent and trade in long-term relationships wassupported by reputation.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 95 / 125

Short-term and long-term partnerships

If the frequency of short-term matches, σs , increases, then, from(8.42), agents will increase their real balance holdings; as a result theincentive-constraint (8.44) becomes more di¢ cult to satisfy.

Hence, the availability of monetary exchange in the presence of along-term partnership increases the attractiveness of defaulting onpromised performance.However, if in�ation increases, then, from the envelope theorem, theterm �ic(qs ) + σs [u(qs )� c(qs )] decreases, which relaxes theincentive-constraint (8.44).

Hence, a higher in�ation rate reduces the buyer�s incentive to defaulton this long-term partnership obligations.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 96 / 125

Short-term and long-term partnershipsSummary

The use of credit is not incentive-feasible in short-lived matches, since thebuyer will always default on repaying his obligation.

In contrast, the buyer�s behavior in a long-lived match is disciplined byreputation considerations that will trigger the dissolution of a valuablerelationship following a default.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 97 / 125

Structure of this chapter

1 Introduction2 Dichotomy between money and credit3 Costly record-keeping4 Strategic complementaries and payments5 Short-term and long-term partnerships6 Money, Credit and Banking7 Conclusion

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 98 / 125

Money, Credit and Banking

The following Section has been adapted from the paper:

"Money, Credit and Banking" by Aleksander Berentsen, Gabriele Cameraand Christopher Waller. CESifo Working Paper No. 1617, December 2005.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 99 / 125

Money, Credit and Banking

The economy now has three markets: A banking market, a decentralizedmarket, and a centralized market. Agents lend or borrow in the bankingmarket, and receive interest or pay back loans in the centralized market:

Figure 8.5: The BCW model

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 100 / 125

Money, Credit and Banking

All markets are competitive.

Agents are anonymous in the DM market.

Record keeping of �nancial transactions by banks only.

The nominal price of goods in the DM is p.

i is the nominal interest rate in the Bank market.

φ is the price of money in the CM.

The government makes lump-sum transfert T to agents in CM.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 101 / 125

Money, Credit and Banking

At the beginning of the period, agents learn their type:

buyer with probability 1� n,seller with probability n.

In equilibrium, buyers borrow money and seller deposit money.

We solve the model backwards.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 102 / 125

Money, Credit and Banking

The value function at the beginning of the CM is

V3(m, l) = maxh,x ,m 0

u(x)� h+ βV1(m0) (8.45)

s.t. x + φm0 = h+ φm� φl(1+ i) + T

l : loan (l 7 0)φ: 1

p

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 103 / 125

Money, Credit and Banking

The quantity l can either be positive (to take a loan), or negative (to givesomebody a loan; i.e., a deposit in a bank).

From the constraint:

h = x + φm0 � φm+ φl(1+ i)� T= x + φ[m0 �m+ l(1+ i)]� T

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 104 / 125

Money, Credit and Banking

We can therefore rewrite (8.45):

V3(m, l) = maxx ,m 0

u(x)� x � φ[m0 �m+ l(1+ i)]� T + βV1(m0)

FOC:

x : u0(x) = 1

m0 : φ = βV 01(m0)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 105 / 125

Money, Credit and Banking

The envelope conditions are:

m : Vm3 (m, l) = φ (8.46)

l : V l3(m, l) = �φ(1+ i) (8.47)

Equation (8.46) is the marginal value of money. The negative sign in(8.47) re�ects the disutility that an agent faces when he repays his debt.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 106 / 125

Money, Credit and Banking

The value functions at the beginning of the DM are

V2b(m, l) = maxqbu(qb) + V3(m� pqb , l) s.t. pqb � m (φλq)

V2s (m, l) = maxqs�c(qs ) + V3(m+ pqs , l)

where φλq is the Lagrange multiplier for the buyer�s constraint.

A seller has no constraint, because he can produce as much as he wants to.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 107 / 125

Money, Credit and Banking

The �rst-order conditions are:

For a buyer:

u0(qb)� p � Vm3 � φpλq = u0(qb)� φp � φpλq = 0 (8.48)

For a seller:

�c 0(qs ) + p � Vm3 = �c 0(qs ) + φp = 0 (8.49)

Combining (8.48) and (8.49) yields

u0(qb)c 0(qs )

= 1+ λq (8.50)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 108 / 125

Money, Credit and Banking

The envelope conditions are:

For a buyer:

m : Vm2b = φ+ φλql : V l2b = V

l3 = �φ(1+ i)

For a seller:

m : Vm2s = Vm3 = φ

l : V l2s = Vl3 = �φ(1+ i)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 109 / 125

Money, Credit and Banking

The value function at the beginning of the Banking market is:

V1(m) = (1� n)maxlbV2b(m+ lb , lb)

+nmaxlsV2s (m+ ls , ls )

s.t. lb � l (φλb)

s.t. m+ ls � 0 (φλs )

where l is an exogenous borrowing constraint.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 110 / 125

Money, Credit and Banking

The �rst-order conditions are:

Vm2b + Vl2b � φλb = 0 () φλq � φi � φλb = 0 (8.51)

Vm2s + Vl2s + φλs = 0 () φλs = φi (8.52)

The envelope condition is:

Vm1 = (1� n)Vm2b + n(Vm2s + φλs ) (8.53)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 111 / 125

Money, Credit and Banking

As soon as they know what type of agent they are, the buyer willwant more cash and will be ready to pay for it (interest rate).

The banking market reallocates the cash of sellers (the surplus) topeople who want more money (the buyers).

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 112 / 125

Money, Credit and Banking

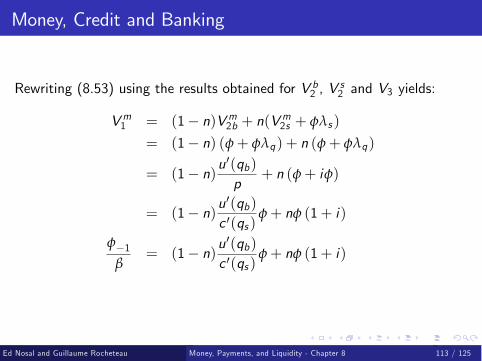

Rewriting (8.53) using the results obtained for V b2 , Vs2 and V3 yields:

Vm1 = (1� n)Vm2b + n(Vm2s + φλs )

= (1� n) (φ+ φλq) + n (φ+ φλq)

= (1� n)u0(qb)p

+ n (φ+ iφ)

= (1� n)u0(qb)c 0(qs )

φ+ nφ (1+ i)

φ�1β

= (1� n)u0(qb)c 0(qs )

φ+ nφ (1+ i)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 113 / 125

Money, Credit and Banking

In a stationary equilibrium, φM = φ�1M�1 ,φ�1

φ = MM�1

= γ , and so:

γ

β= (1� n)u

0(qb)c 0(qs )

+ n(1+ i) (8.54)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 114 / 125

Money, Credit and Banking

We need one more equation that determines i . From Equation (8.48):

u0(qb) = φp + pφλq

= c 0(qs ) + pφ(i + λb)

= c 0(qs ) (1+ i + λb) (8.55)

From Equation (8.55), we can analyze two cases; i.e., when λb is binding,and when it is not.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 115 / 125

Money, Credit and BankingFirst case: not binding

When l is not binding, it means that l is not relevant because people payback and they never reach the exogenous borrowing constraint. Thus,

u0(qb)c 0(qs )

= 1+ i

From (8.54), it follows that

γ

β=u0(qb)c 0(qs )

= 1+ i (8.56)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 116 / 125

Money, Credit and BankingFirst case: not binding

Thus with �nancial intermediation, and from the market clearing condition(1� n) � qb = n � qs , qb solves

γ

β=

u0(qb)

c 0h(1�n)qb

n

i .Without banking, we get

γ

β= (1� n) u0(qb)

c 0h(1�n)qb

n

i + n.Consumption, and hence welfare, is strictly larger with �nancialintermediation than without it.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 117 / 125

Money, Credit and BankingFirst case: not binding

It is easy to see that �nancial intermediation provides a higher utility:�u0(qb)c 0(qs )

� intermediation<

�u0(qb)c 0(qs )

�without intermediationthus:

u(qb)intermediation > u(qb)

without intermediation

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 118 / 125

Money, Credit and BankingFirst case: not binding

Notice that the Fisher equation holds. From (8.56):

γ = 1+ π

β =1

1+ r

and thus(1+ π)(1+ r) = (1+ i), π + r = i (8.57)

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 119 / 125

Money, Credit and BankingSecond case: binding

When the borrowing constraint l is binding, we have

u0(qb)c 0(qs )

= 1+ i + λl

and thusu0(qb)c 0(qs )

> 1+ i

The Fisher equation does not hold. Moreover, the exogenous borrowingconstraint reduces consumption relative to the amount that could beattained without it.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 120 / 125

Money, Credit and BankingWelfare

To analyze welfare, let us sum up the above results, we have:

γ� β

β= (1� n)

�u0(qb)c 0(qs )

� 1�+ ni| {z }

with �nancial intermediation

or:γ� β

β= (1� n)

�u0(qb)c 0(qs )

� 1�

| {z }without �nancial intermediation

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 121 / 125

Money, Credit and BankingWelfare

From these two equations, it is clear that the bene�t of the bankingsystem is that it allows agents to earn interest on "idle" money.

This increases the demand for money and hence it�s value, which allowsagents to consume more.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 122 / 125

Structure of this chapter

1 Introduction2 Dichotomy between money and credit3 Costly record-keeping4 Strategic complementaries and payments5 Short-term and long-term partnerships6 Money, Credit and Banking7 Conclusion

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 123 / 125

Conclusion

In this chapter we considered environments where monetary tradescoexist with credit arrangements.

We �rst examined a model where in some matches, agents�transactions are monitored and debt contracts are enforceable while inother matches, agents are anonymous and debt contracts are notincentive-feasible.

In this benchmark economy, there is a dichotomy between themonetary and credit sectors and monetary policy does not a¤ect theuse of credit.

To break this dichotomy, we extended the model by allowing the gainsfrom trade to vary across matches, and by making the access to arecord-keeping technology costly. We showed that credit is used forlarge transactions and, as in�ation increases, the fraction of credittransactions increases.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 124 / 125

Conclusion

Moreover, if the use of credit requires an ex-ante costly investment bysellers, multiple equilibria can emerge with di¤erent paymentarrangements.

Then, we endogenized the commitment that allows agents to repaytheir debt in an environment where agents can develop bothlong-term and short-term partnerships. In such an environment,self-enforced debt contracts coexist with �at money.

Finally, we developed a model which shows the role of banks asintermediaries and the gain in utility they allow.

Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 8 125 / 125