Embed Size (px)

Citation preview

Peer Reviewed

Richard Gregory [email protected] is an Assistant Professor of Finance and Rafie K. Bhogozian is an Instructor at East Tennessee University.

Abstract

This paper estimates the impact of monetary policy actions on non-financial commercial paper market yields. It uses data from the futures market for the federal funds rate to separate changes in the funds rate into anticipated and unanticipated components in order to provide insight into the efficiency of these markets and the degree to which the yields data supports the expectations hypothesis. It concludes that only the overnight commercial paper yield shows a significant response to changes in Federal Reserve policies, and then they exhibit nearly equivalent responses to both anticipated and unanticipated changes. Longer maturity paper exhibits reaction only to changes in the overnight commercial paper rate.

1

The response of commercial paper rates to Federal Reserve (Fed) actions is a topic of great interest to financial market participants and policymakers alike. In the commercial paper market, holders of commercial paper, such as money market mutual funds, funding corporations, and governments are concerned with the effects of Fed policy on commercial paper rates. Because the first link in the transmission of Federal Reserve policy is from the Fed funds target to other interest rates, this response is important for assessing the effectiveness of monetary policy. Furthermore, as commercial paper is used to fund accounts receivables and the securitization of assets, it is also of importance to corporate financial decisions. Non-Financial commercial paper is an important source of financing holdings of short-term assets, payrolls, and trade credit for companies. Therefore, changes in non-financial commercial paper yields can have an immediate impact upon the real economy.

Economic theory suggests that an increase in the targeted Fed funds rate leads to an increase in commercial paper rates and a decline in paper prices. Evidence for this view is elusive. There are very few studies about commercial paper markets. Downing and Oliner (2004) and Gregory and Word (2006) examine evidence for the expectations hypothesis amongst commercial paper rates and find results that are generally supportive of the hypothesis in both domestic and international commercial paper markets. This means that information on inflation is generally transmitted throughout the maturity structure. This is a result which is supportive of monetary policy affecting rates, but there are no direct measurements or published work on measuring the effects of anticipated and unanticipated changes of policy on rates.

Other research on short term rates suggest mixed support for the expectations

hypothesis in short-term debt markets. Longstaff (2000) uses the term structure of general collateral government repurchase agreement (repo) rates and reports evidence that supports the expectations hypothesis. Della Corte, Sarno, and Thronton (2008) and Brown, Cyree, Griffiths, and Winters (2008) both re-examine the repo market using different data sets and generally find against the expectations hypothesis. Brown, Cyree, Griffiths, and Winters find, however, that the expectations hypothesis holds when rates are less volatile.

Research on the effects of monetary policy on interest rates outside of the commercial paper market is suggestive of the possible effects on the commercial paper market. Cook and Hahn (1989) document a strong response in the 1970s, but regressions using data from the 1980s and 1990s show little, if any, impact of Fed policy. Roley and Sellon (1995) conclude that the empirical relationship is quite variable and time dependent. Kuttner (2001) uses Fed funds futures rates to distinguish between anticipated and unanticipated changes and finds that, while the changes of bond rates are essentially zero to anticipated changes, their response to unanticipated movements

2

is large and highly significant. However, in contrast to the above studies that find support for the expectations hypothesis on the short end of the yield curve, Kuttner finds that surprise policy actions have little effect on near-term expectations of future actions, and this is taken as an explanation of “finding that the expectations hypothesis fails to explain rate structure at the short end of the yield curve”. Radecki and Reinhart (1994) obtain similar results for the 1989–1992 period.

Using a vector autoregression (VAR) Edelberg and Marshall (1996) find a large, significant response of bill rates to policy shocks, but only a small, marginally significant response for bond rates. Other examples of the VAR approach include Evans and Marshall (1998) and Mehra (1996). In an effort to model the discrete nature of target rate changes, Demiralp and Jorda (1999) examines the relationship between policy actions and interest rates using an autoregressive conditional hazard (ACH) model to forecast the timing of changes in the Fed funds target, and an ordered probit to estimate the size of the change. There is some debate as to the reliability of VAR-based measures of policy shocks [e.g., Rudebusch (1998)]. Generally, Rudebusch argues that monetary policy shocks in these models are identified with least squares residuals that show little correlation across various VARs or with fund rate shocks that are derived from forward financial markets. The VAR reaction functions in these models mischaracterize the Federal Reserve Information set (i.e. they use information not available at the time) and can exhibit fragile coefficient estimates.

Using Fed funds futures rates to distinguish expected from unexpected policy

actions, this paper shows that commercial paper rates’ response to the “surprise” component of Fed policy is equal to the response to the change in the target itself; in fact, rates’ response to the anticipated component of policy actions is large and significant for overnight commercial paper rates, but not for longer rates, which is a result inconsistent with the efficient markets hypothesis. However, the significant relationship between the commercial paper rate and the unanticipated portion of the federal funds rate is consistent with the efficient markets hypothesis.

Using Futures Rates to Gauge Policy Expectations

Expectations of Fed policy actions are not directly observable, but Fed funds futures prices are a natural proxy for those expectations. The Fed funds futures market was established in 1989 at the Chicago Board of Trade, and one- through five-month Fed funds contracts are traded, along with a “spot month” contract based on the current month’s funds rate. Krueger and Kuttner (1996) found that funds rate forecasts based on the futures price are efficient, in that the forecast errors are not significantly correlated with other variables known when the contract was priced. Sarno, Thornton,

3

and Valente (2005) find that the current difference between the federal funds rate and its target is the best forecast of future federal funds rates .

Using futures data as a measure of expected Fed policy has a number of advantages over statistical proxies. First, there is no issue of model selection; second, the vintage of the data used to produce the forecast is not an issue; and third, there are no generated regressor problems. The main disadvantage, of course, is that it limits the analysis to the post-1989 period.

As it contains the near-term expectations of the Fed funds rate, the rate from the spot month contract offers a promising way to measure the surprise element of specific Fed actions. Two factors complicate the use of futures data for this. One complication is that the Fed funds futures contract’s settlement price is based on the average of the relevant month’s effective overnight Fed funds rate, rather than the rate. This would be consistent with Thornton (1999), who found that the Cook and Hahn results are attributable to the announcement of a policy change, rather than the action itself. Consequently, the time-averaging must somehow be undone to get a correct measure of the expected funds rate.

A second complication is that the futures contracts are based not on the target Fed funds rate, but on the effective market rate. In monthly averages, the two are very close--usually within a few basis points. At a daily frequency, however, the discrepancy between the market rate and the Fed’s target is often too large to be ignored.

The question, then, is how best to extract a measure of the unexpected change in the target rate on date t, relative to the forecast made on date t-1,

(1)

where is the unexpected change in the target rate on date t, is the target rate,

and is the expected target rate on date t. As noted by Kuttner (2000) computation of the one-day unexpected change can be affected as:

(2)

4

where ms is the number of days in month s, f0s,t is the spot futures rate on day t of month s and t is the date of observation. Equation 2 is used to determine the unanticipated change for all days except at the beginning and the end of the month. When the change comes on the first day of the month, its expectation would have been reflected in the prior month’s spot rate, so the one-month futures rate on the last day of the previous month is used instead. On the last day of the month, as the market Fed funds rate does not change until the day following the target change; so the difference in one-month futures rates are used instead.

Assuming that no further changes are expected within the month, this method is a nearly pure measure of the one-day surprise target change as noted by Kuttner (2001). If the forward premium doesn’t change much from day-to-day, it should be nearly equal to zero. The only other possible sources of error are the day t targeting error and the revision of expectations of future targeting errors. As these errors are occasionally non-trivial, in circumstances where the target rate change occurs within three days of the end of the month, the change in the one-month futures rate is used.

Data and Estimation Results

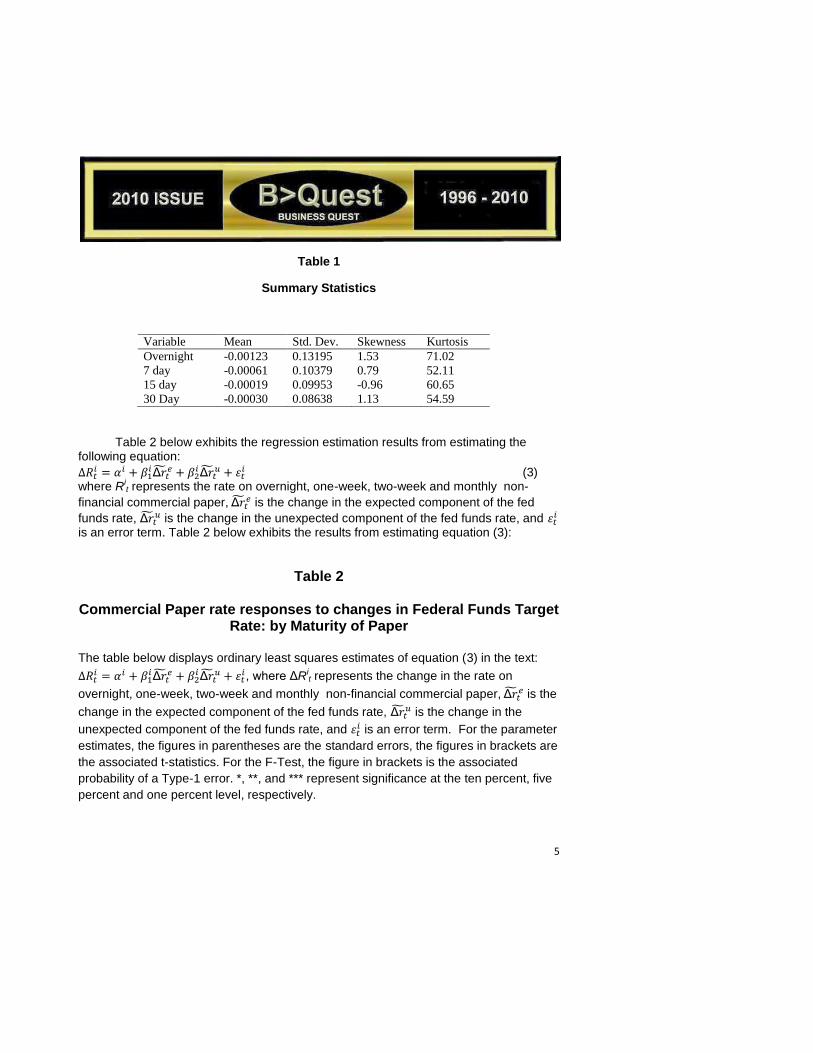

Table 1 below details the descriptive statistics of the data set. The commercial paper rates used are for AA rated non-financial firms for the intervals of overnight to one month. The data on commercial paper rates are from the Federal Reserve Board website at http://www.federalreserve.gov/DataDownload/Choose.aspx?rel=CP. The sample period is from January 5, 1998 through November 14, 2008. The Fed funds futures data are from the Chicago Board of Trade website at http://www.cmegroup.com/market-data/datamine-historical-data/datamine.html. The mean change in the overnight rate is much larger--at least twice the size--of the other commercial paper rates, reflecting in part the greater volume of activity in the US market. All of the variables exhibit leptokurtosis, so regression results need to be interpreted carefully. Violations of normality can compromise the estimation of coefficients and the calculation of confidence intervals. Since parameter estimation is based on the minimization of squared error, a few extreme observations can exert a disproportionate influence on parameter estimates. Calculation of confidence intervals and various significance tests for coefficients are all based on the assumptions of normally distributed errors. If the error distribution is significantly non-normal, confidence intervals may be too wide or too narrow. So coefficients of marginal significance should be interpreted with care.

5

Table 1

Summary Statistics

Variable Mean Std. Dev. Skewness Kurtosis

Overnight -0.00123 0.13195 1.53 71.02

7 day -0.00061 0.10379 0.79 52.11

15 day -0.00019 0.09953 -0.96 60.65

30 Day -0.00030 0.08638 1.13 54.59

Table 2 below exhibits the regression estimation results from estimating the following equation:

(3) where Ri

t represents the rate on overnight, one-week, two-week and monthly non-

financial commercial paper, is the change in the expected component of the fed

funds rate, is the change in the unexpected component of the fed funds rate, and

is an error term. Table 2 below exhibits the results from estimating equation (3):

Table 2

Commercial Paper rate responses to changes in Federal Funds Target Rate: by Maturity of Paper

The table below displays ordinary least squares estimates of equation (3) in the text:

, where Rit represents the change in the rate on

overnight, one-week, two-week and monthly non-financial commercial paper, is the

change in the expected component of the fed funds rate, is the change in the

unexpected component of the fed funds rate, and is an error term. For the parameter

estimates, the figures in parentheses are the standard errors, the figures in brackets are

the associated t-statistics. For the F-Test, the figure in brackets is the associated

probability of a Type-1 error. *, **, and *** represent significance at the ten percent, five

percent and one percent level, respectively.

6

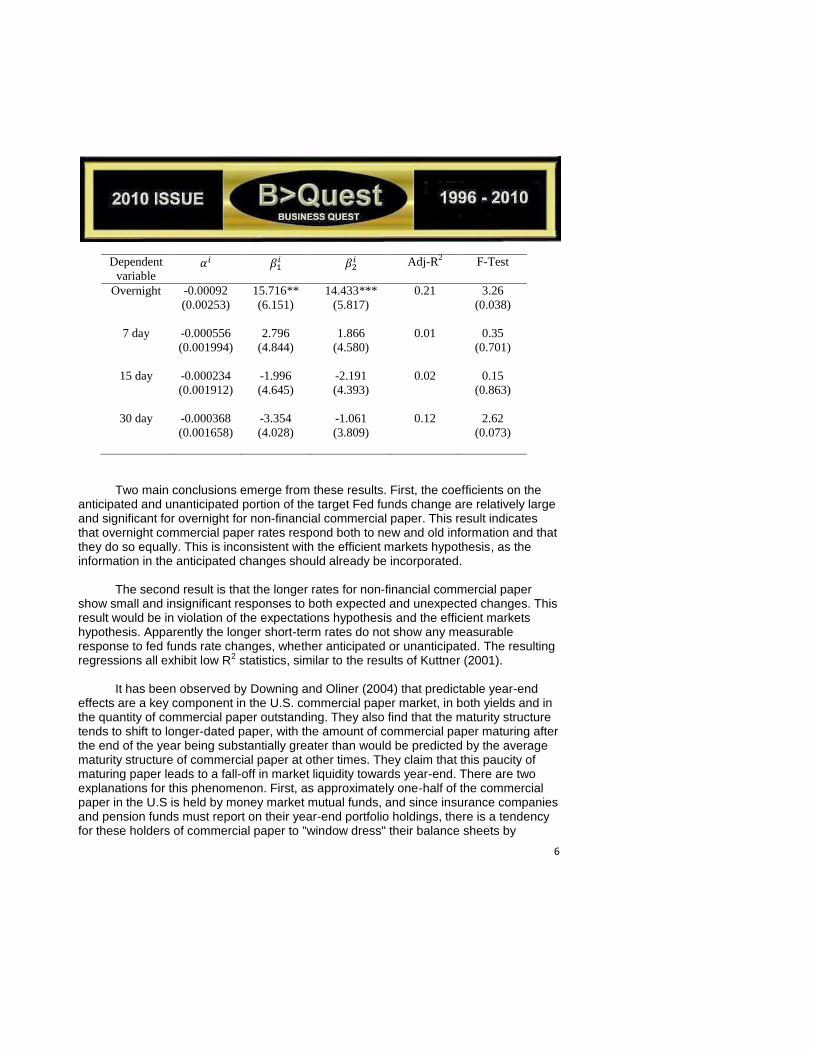

Dependent

variable

Adj-R

2 F-Test

Overnight -0.00092

(0.00253)

15.716**

(6.151)

14.433***

(5.817)

0.21 3.26

(0.038)

7 day -0.000556

(0.001994)

2.796

(4.844)

1.866

(4.580)

0.01 0.35

(0.701)

15 day -0.000234

(0.001912)

-1.996

(4.645)

-2.191

(4.393)

0.02 0.15

(0.863)

30 day -0.000368

(0.001658)

-3.354

(4.028)

-1.061

(3.809)

0.12 2.62

(0.073)

Two main conclusions emerge from these results. First, the coefficients on the anticipated and unanticipated portion of the target Fed funds change are relatively large and significant for overnight for non-financial commercial paper. This result indicates that overnight commercial paper rates respond both to new and old information and that they do so equally. This is inconsistent with the efficient markets hypothesis, as the information in the anticipated changes should already be incorporated. The second result is that the longer rates for non-financial commercial paper show small and insignificant responses to both expected and unexpected changes. This result would be in violation of the expectations hypothesis and the efficient markets hypothesis. Apparently the longer short-term rates do not show any measurable response to fed funds rate changes, whether anticipated or unanticipated. The resulting regressions all exhibit low R2 statistics, similar to the results of Kuttner (2001).

It has been observed by Downing and Oliner (2004) that predictable year-end effects are a key component in the U.S. commercial paper market, in both yields and in the quantity of commercial paper outstanding. They also find that the maturity structure tends to shift to longer-dated paper, with the amount of commercial paper maturing after the end of the year being substantially greater than would be predicted by the average maturity structure of commercial paper at other times. They claim that this paucity of maturing paper leads to a fall-off in market liquidity towards year-end. There are two explanations for this phenomenon. First, as approximately one-half of the commercial paper in the U.S is held by money market mutual funds, and since insurance companies and pension funds must report on their year-end portfolio holdings, there is a tendency for these holders of commercial paper to "window dress" their balance sheets by

7

temporarily substituting higher quality investments for the commercial paper they usually hold. This activity results in a jump in yields since lower quality commercial paper issuers have to offer a premium to sell the paper. Second, overnight interest rates tend to be more volatile towards year-end because of the variable demand for cash by financial institutions, businesses, and individuals. Thus, in order to insure against interest rate risk, firms tend to prefer offering longer term maturities during this time of the year.

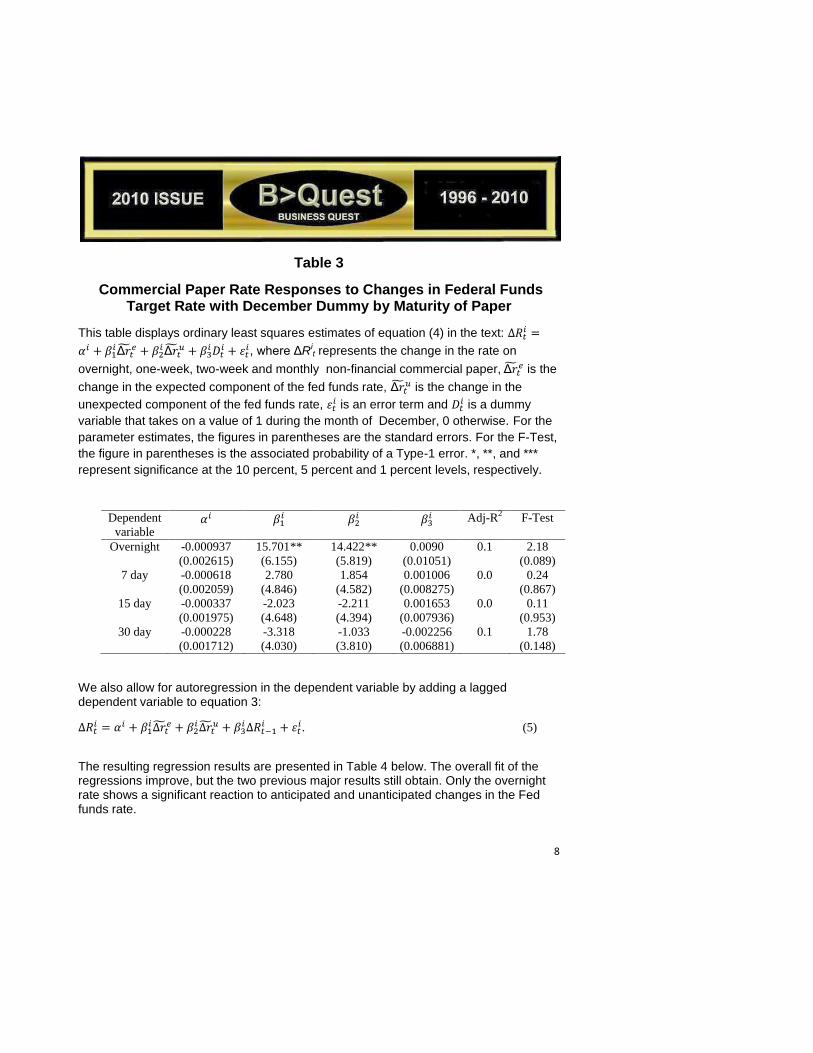

To determine the effects of the year-end phenomenon, we re-run the regressions adding a year-end dummy for the events occurring during the month of December:

(4)

where takes on a value of 1 if the date is in the month of December, 0 otherwise.

These results are displayed in Table 3 below. Despite previous results on the year-end effects, none of the December dummy-variables are significant. The only major change is that the regression R2 statistics are lower and the F-statistics are less significant, indicating that accounting for the year-end effect does not result in superior performance in explaining the effect of monetary policy on commercial paper rates.

8

Table 3

Commercial Paper Rate Responses to Changes in Federal Funds Target Rate with December Dummy by Maturity of Paper

This table displays ordinary least squares estimates of equation (4) in the text:

, where Rit represents the change in the rate on

overnight, one-week, two-week and monthly non-financial commercial paper, is the

change in the expected component of the fed funds rate, is the change in the

unexpected component of the fed funds rate, is an error term and

is a dummy

variable that takes on a value of 1 during the month of December, 0 otherwise. For the

parameter estimates, the figures in parentheses are the standard errors. For the F-Test,

the figure in parentheses is the associated probability of a Type-1 error. *, **, and ***

represent significance at the 10 percent, 5 percent and 1 percent levels, respectively.

Dependent

variable

Adj-R2

F-Test

Overnight -0.000937

(0.002615)

15.701**

(6.155)

14.422**

(5.819)

0.0090

(0.01051)

0.1 2.18

(0.089)

7 day -0.000618

(0.002059)

2.780

(4.846)

1.854

(4.582)

0.001006

(0.008275)

0.0 0.24

(0.867)

15 day -0.000337

(0.001975)

-2.023

(4.648)

-2.211

(4.394)

0.001653

(0.007936)

0.0 0.11

(0.953)

30 day -0.000228

(0.001712)

-3.318

(4.030)

-1.033

(3.810)

-0.002256

(0.006881)

0.1 1.78

(0.148)

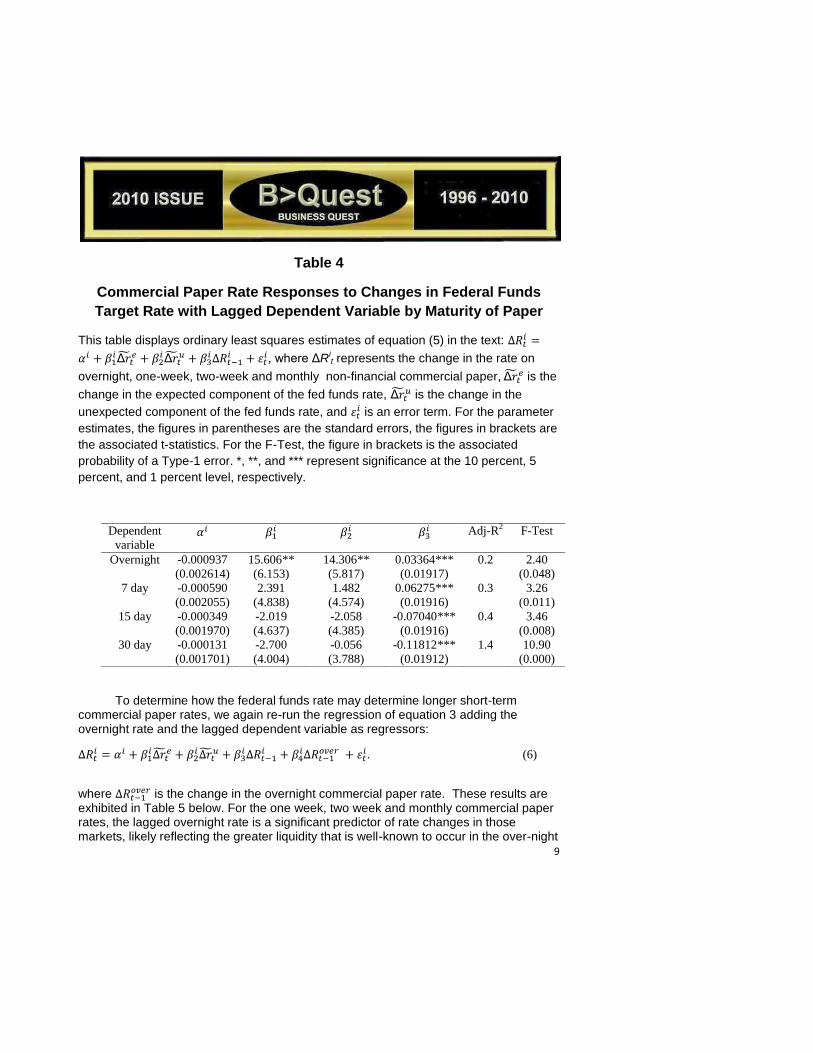

We also allow for autoregression in the dependent variable by adding a lagged dependent variable to equation 3:

. (5)

The resulting regression results are presented in Table 4 below. The overall fit of the regressions improve, but the two previous major results still obtain. Only the overnight rate shows a significant reaction to anticipated and unanticipated changes in the Fed funds rate.

9

Table 4

Commercial Paper Rate Responses to Changes in Federal Funds

Target Rate with Lagged Dependent Variable by Maturity of Paper

This table displays ordinary least squares estimates of equation (5) in the text:

, where Rit represents the change in the rate on

overnight, one-week, two-week and monthly non-financial commercial paper, is the

change in the expected component of the fed funds rate, is the change in the

unexpected component of the fed funds rate, and is an error term. For the parameter

estimates, the figures in parentheses are the standard errors, the figures in brackets are

the associated t-statistics. For the F-Test, the figure in brackets is the associated

probability of a Type-1 error. *, **, and *** represent significance at the 10 percent, 5

percent, and 1 percent level, respectively.

Dependent

variable

Adj-R2

F-Test

Overnight -0.000937

(0.002614)

15.606**

(6.153)

14.306**

(5.817)

0.03364***

(0.01917)

0.2 2.40

(0.048)

7 day -0.000590

(0.002055)

2.391

(4.838)

1.482

(4.574)

0.06275***

(0.01916)

0.3 3.26

(0.011)

15 day -0.000349

(0.001970)

-2.019

(4.637)

-2.058

(4.385)

-0.07040***

(0.01916)

0.4 3.46

(0.008)

30 day -0.000131

(0.001701)

-2.700

(4.004)

-0.056

(3.788)

-0.11812***

(0.01912)

1.4 10.90

(0.000)

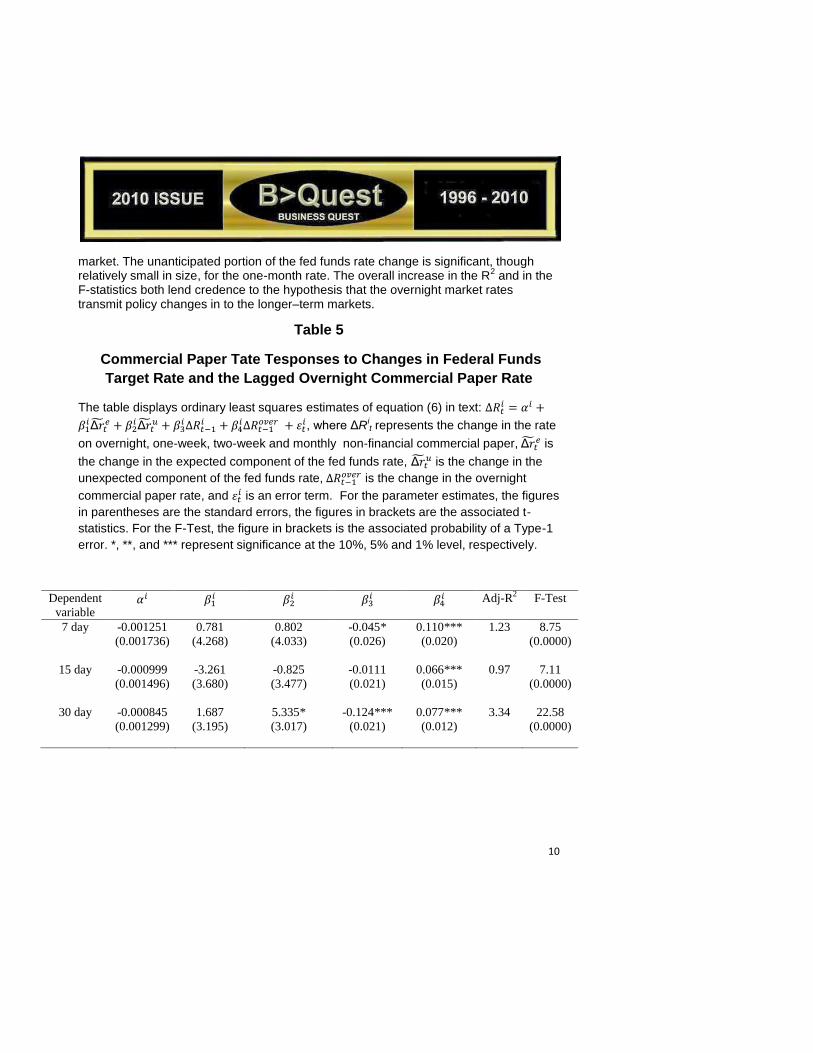

To determine how the federal funds rate may determine longer short-term commercial paper rates, we again re-run the regression of equation 3 adding the overnight rate and the lagged dependent variable as regressors:

. (6)

where is the change in the overnight commercial paper rate. These results are

exhibited in Table 5 below. For the one week, two week and monthly commercial paper rates, the lagged overnight rate is a significant predictor of rate changes in those markets, likely reflecting the greater liquidity that is well-known to occur in the over-night

10

market. The unanticipated portion of the fed funds rate change is significant, though relatively small in size, for the one-month rate. The overall increase in the R2 and in the F-statistics both lend credence to the hypothesis that the overnight market rates transmit policy changes in to the longer–term markets.

Table 5

Commercial Paper Tate Tesponses to Changes in Federal Funds

Target Rate and the Lagged Overnight Commercial Paper Rate

The table displays ordinary least squares estimates of equation (6) in text:

, where Rit represents the change in the rate

on overnight, one-week, two-week and monthly non-financial commercial paper, is

the change in the expected component of the fed funds rate, is the change in the

unexpected component of the fed funds rate, is the change in the overnight

commercial paper rate, and is an error term. For the parameter estimates, the figures

in parentheses are the standard errors, the figures in brackets are the associated t-

statistics. For the F-Test, the figure in brackets is the associated probability of a Type-1

error. *, **, and *** represent significance at the 10%, 5% and 1% level, respectively.

Dependent

variable

Adj-R

2 F-Test

7 day -0.001251

(0.001736)

0.781

(4.268)

0.802

(4.033)

-0.045*

(0.026)

0.110***

(0.020)

1.23 8.75

(0.0000)

15 day -0.000999

(0.001496)

-3.261

(3.680)

-0.825

(3.477)

-0.0111

(0.021)

0.066***

(0.015)

0.97 7.11

(0.0000)

30 day -0.000845

(0.001299)

1.687

(3.195)

5.335*

(3.017)

-0.124***

(0.021)

0.077***

(0.012)

3.34 22.58

(0.0000)

11

Conclusions

Because the commercial paper market is an important source of liquidity to corporations in the United States, the reaction of the yields in commercial paper to changes in Federal Reserve policy should be of interest to practitioners and academics. Violations of market efficiency and the expectations hypothesis implies that corporations and governments that have access to the commercial paper market or have better credit ratings than their peers may be able to earn arbitrage profits by borrowing cheaply in the commercial paper market.

The results of this research indicate that the commercial paper markets show inconsistent conformity with the hypothesis of market efficiency and the expectations hypothesis over the sample period. Only the overnight commercial paper market yields show a significant response to changes in Federal Reserve policies, and then they show nearly equivalent responses to both anticipated and unanticipated changes. A possible explanation for this may be the time span considered. During this time span, there was considerable intervention in the commercial paper market by the Federal Reserve as it attempted to provide liquidity for the market in the wake of the default of Lehman Brothers, an investment bank that had played a role as a market maker in the commercial paper market.

The yields out to one month are found to be dependent upon lagged innovation in the overnight market. This is most likely due to the relative size of the markets, as it is well-known that most of the volume activity in the US commercial paper market takes place in the overnight market. There is some evidence that when controlling for this factor, unanticipated changes in Federal Reserve policies do affect longer-term rates.

There are a number of possible extensions to this research. As noted by Kacperczyk and Schnabl (2010), the commercial paper market underwent a number of crises during the 2007-2008 period, a fact that might have impacted the results reported above. One possible extension suggested by an anonymous reviewer of this paper would be to test for breaks or to use a Markov switching model to see if the results are regime dependent. A further extension would be to make use of measures of market liquidity to understand the effects that liquidity have on the tests of market efficiency and the expectations hypothesis. And, of course, testing by extending the data with commercial paper of financial firms might offer further insights. Achieving this is left to future research.

12

References

Brown, C.R, Cyree, K.B., Griffiths, M.D. and Winters, D.B., "Further Analysis of the Expectations Hypothesis using very Short-term Interest Rates," Journal of Banking and Finance 32, (2008): pp. 600-613.

Cook, T. and Hahn, T. "The Effect of Changes in the Federal Funds Rate Target on Market Interest Rates in the 1970s." Journal of Monetary Economics 24, (1989): 331–351. Della Corte, P., Sarno, L. and Thornton, D. L. "The expectation hypothesis of the term structure of very short-term rates: Statistical tests and economic value." Journal of Financial Economics, vol. 89(1), (2008): pp 158-174. Demiralp, S. and Jorda, O. "The Transmission of Monetary Policy via Announcement Effects" UC Davis Working Paper No. 99-06. (1999)<http://papers.ssrn.com/sol3/papers.cfm?abstract_id=184491> Downing, C. and S. Oliner. "The term structure of commercial paper rates." Journal of Financial Economics Vol. 83 (1), (2007): 59-86.

Edelberg, W. and Marshall, D. "Monetary Policy Shocks and Long-TermInterest Rates." Federal Reserve Bank of Chicago Economic Perspectives 20(2), (1996): 2–17. Evans, C. L. and Marshall, D. 1998. "Monetary Policy and the Term Structure of Nominal Interest Rates: Evidence and Theory." Carnegie-Rochester Conference Volume on Public Policy, 49 (1), (1998): 53-111. Gregory, R. and W. Word. " Do dealer quotes in the euro-commercial paper market conform with the rational expectations hypothesis?" International Journal of Business Disciplines Volume 17, No. 1 Spring/Summer, (2006): pp. 5-18. Kacperczyk, M. and Schnabl, P. "When Safe Proved Risky: Commercial Paper during the Financial Crisis of 2007-2009." Journal of Economic Perspectives 24, (2010): pp. 29-50. Krueger, J. T. and Kuttner, K. N." The Fed Funds Futures Rate as a Predictor of Federal Reserve Policy." Journal of Futures Markets 16(8), (1996): 865–879. Kuttner, K. N. “Monetary Policy Surprises and Interest Rates: Evidence from the Fed Funds Futures Market.” Journal of Monetary Economics 47, (2001): 523-544.

Formatted: Font: Arial, Not Bold

13

Longstaff, F. "The Term Structure of very Short-term Rates: New Evidence for the Expectations Hypothesis." Journal of Financial Economics 58(3), (2000): pp. 397-415. Mehra, Y. P. "Monetary Policy and Long-Term Interest Rates." Federal Reserve Bank of Richmond Economic Quarterly 82(3), (1996): pp. 27–50. Radecki, L. and Reinhart, V. The Financial Linkages in the Transmission of Monetary Policy in the United States. In: National Differences in Interest Rate Transmission. Bank for International Settlements. (1994). Roley, V. V. and Sellon, G. H. "Monetary Policy Actions and Long Term Interest Rates." Federal Reserve Bank of Kansas City Economic Quarterly, 80(4), (1995): pp.77–89. Rudebusch, G. "Do Measures of Monetary Policy in a VAR Make Sense?" International Economic Review 39(4), (1998): pp. 907–931. Sarno, L., Thornton, D. L. and Valente, G. "Federal Funds Rate Pediction," Journal of Money, Credit and Banking. 37(3), (2005): pp. 449-71. Thornton, D. L. "The Feds Influence on the Federal Funds Rate: Is It Open Market or Open Mouth Operations?" Journal of Banking and Finance, 28(3), (2004): pp. 475-498. Note: Title graphic by Carole E. Scott