Embed Size (px)

Citation preview

Money and Stabilization Policy

KW Chapter 31

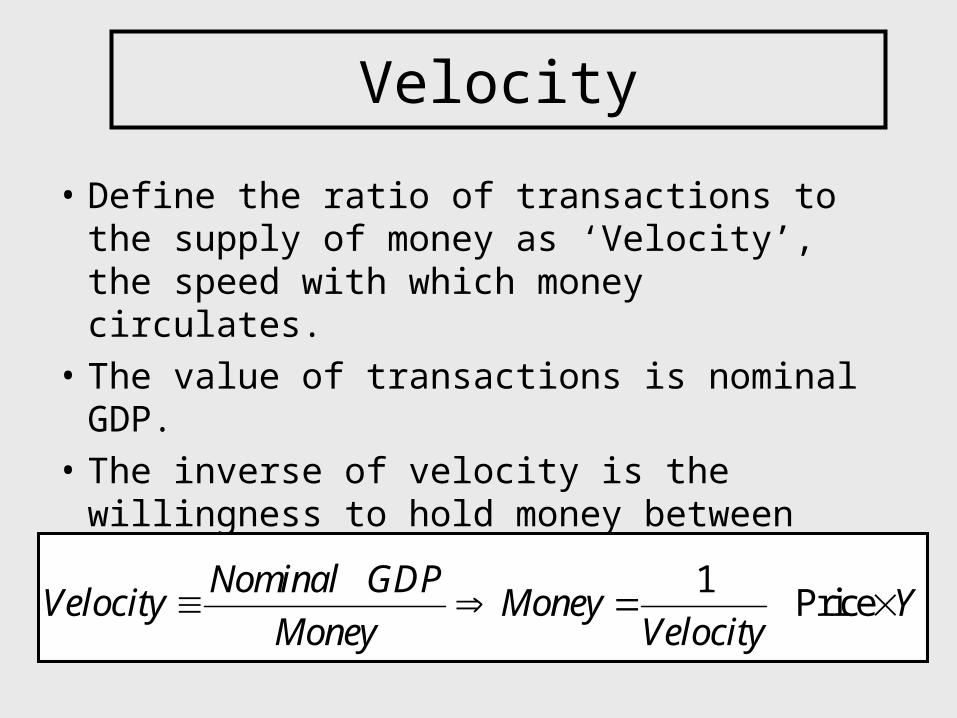

Velocity

• Define the ratio of transactions to the supply of money as ‘Velocity’, the speed with which money circulates.

• The value of transactions is nominal GDP.

• The inverse of velocity is the willingness to hold money between transactions.

1

PriceNominal GDP

Velocity Money YMoney Velocity

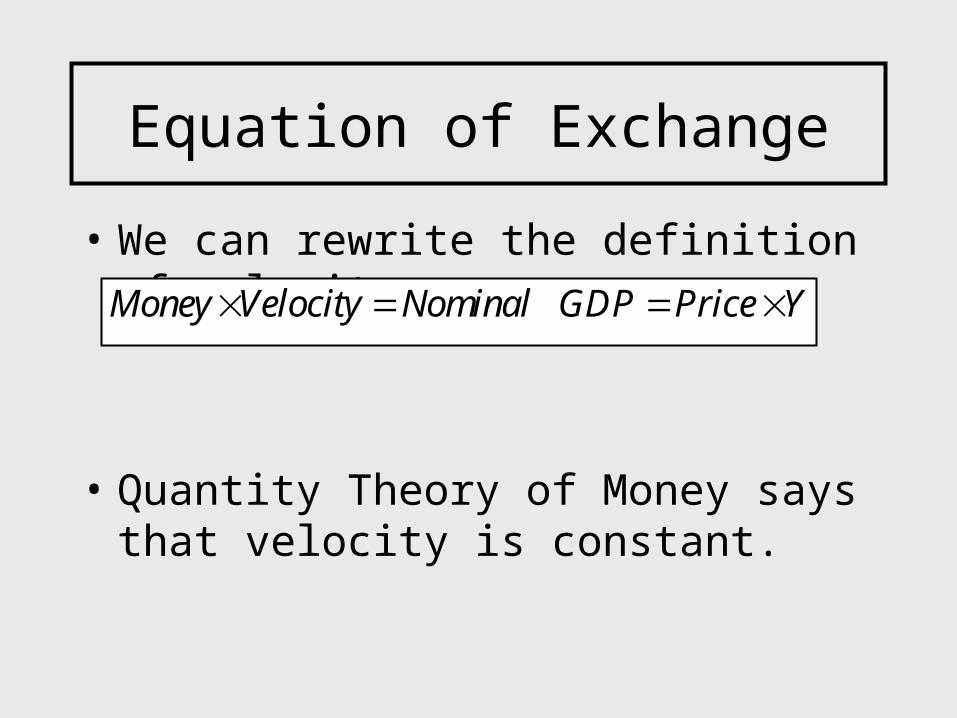

Equation of Exchange

• We can rewrite the definition of velocity as

• Quantity Theory of Money says that velocity is constant.

Money Velocity Nominal GDP Price Y

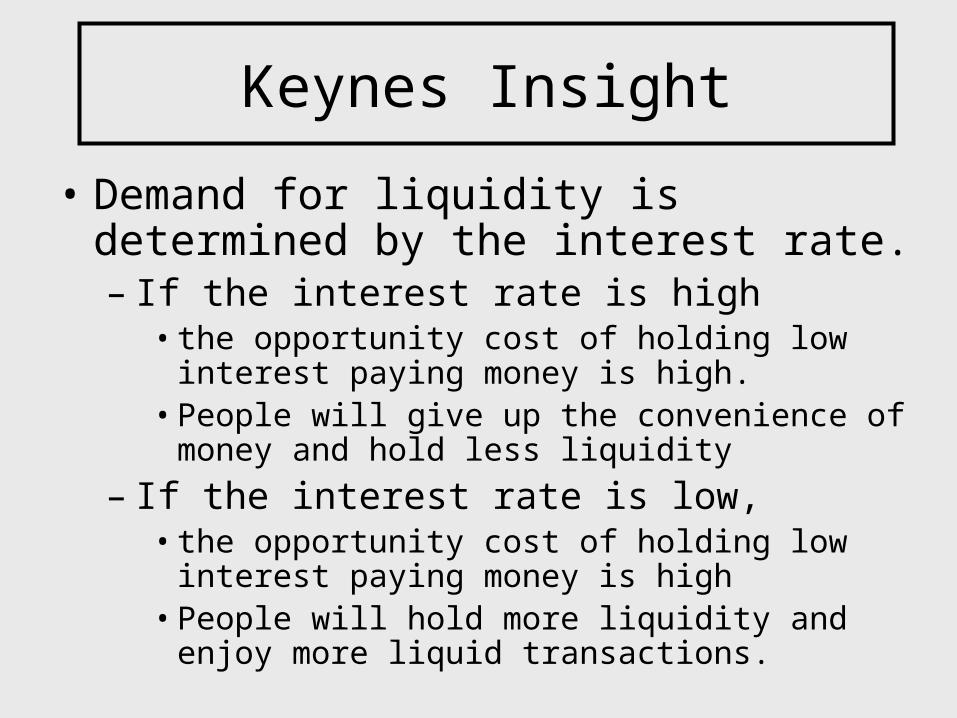

Keynes Insight

• Demand for liquidity is determined by the interest rate. – If the interest rate is high

• the opportunity cost of holding low interest paying money is high.

• People will give up the convenience of money and hold less liquidity

– If the interest rate is low, • the opportunity cost of holding low interest paying

money is high • People will hold more liquidity and enjoy more liquid

transactions.

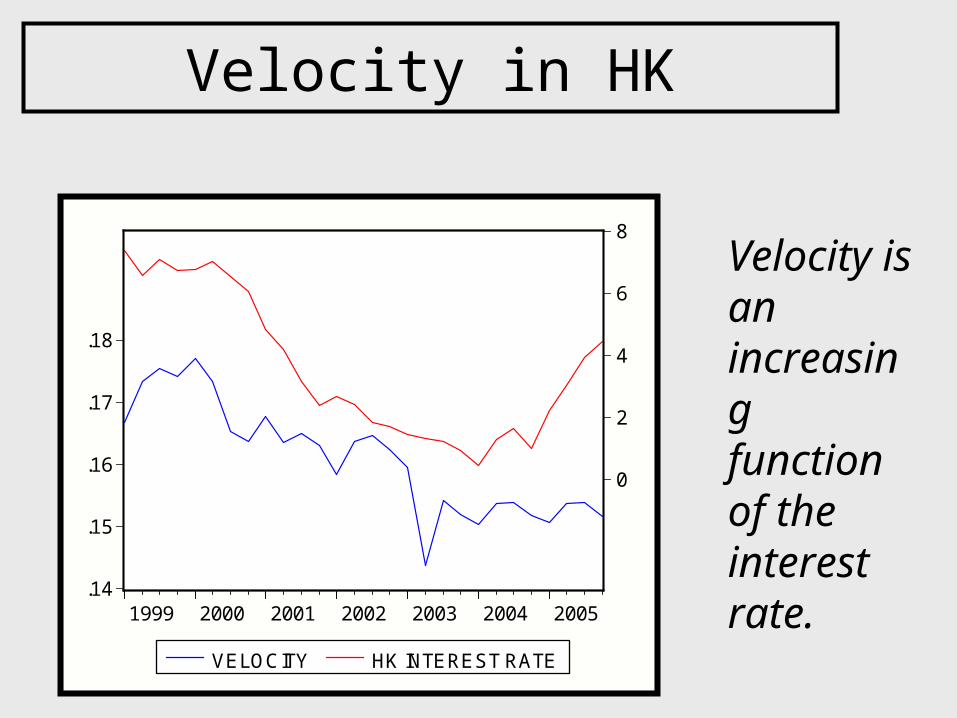

Velocity in HK

.14

.15

.16

.17

.18

0

2

4

6

8

1999 2000 2001 2002 2003 2004 2005

VELOCITY HK INTEREST RATE

Velocity is an increasing function of the interest rate.

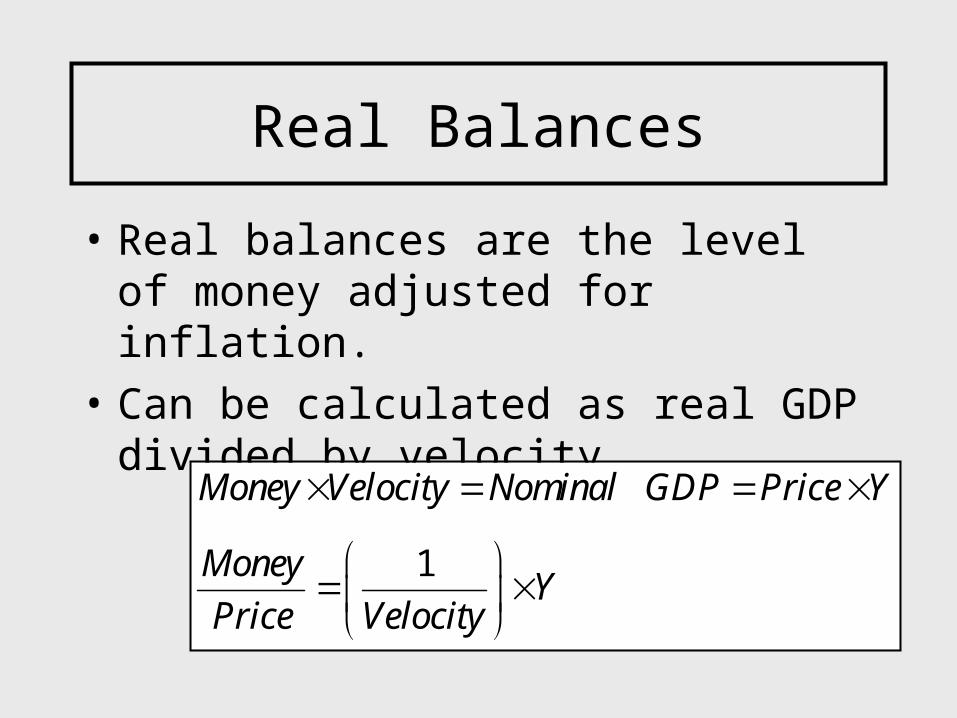

Real Balances

• Real balances are the level of money adjusted for inflation.

• Can be calculated as real GDP divided by velocity

1

Money Velocity Nominal GDP Price Y

MoneyY

Price Velocity

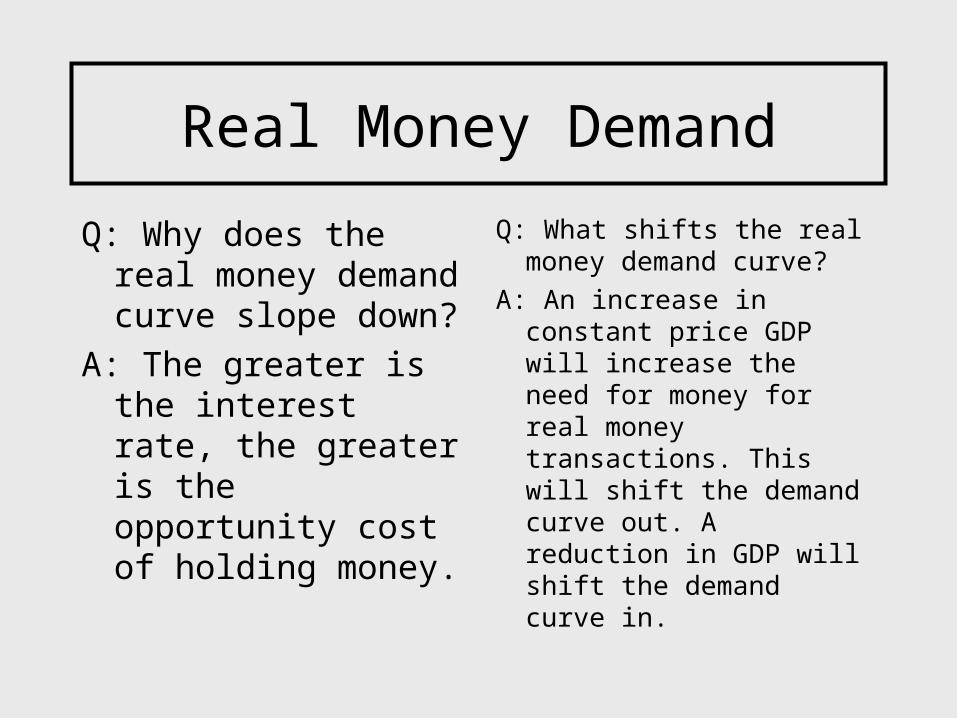

Real Money Demand

Q: Why does the real money demand curve slope down?

A: The greater is the interest rate, the greater is the opportunity cost of holding money.

Q: What shifts the real money demand curve?

A: An increase in constant price GDP will increase the need for money for real money transactions. This will shift the demand curve out. A reduction in GDP will shift the demand curve in.

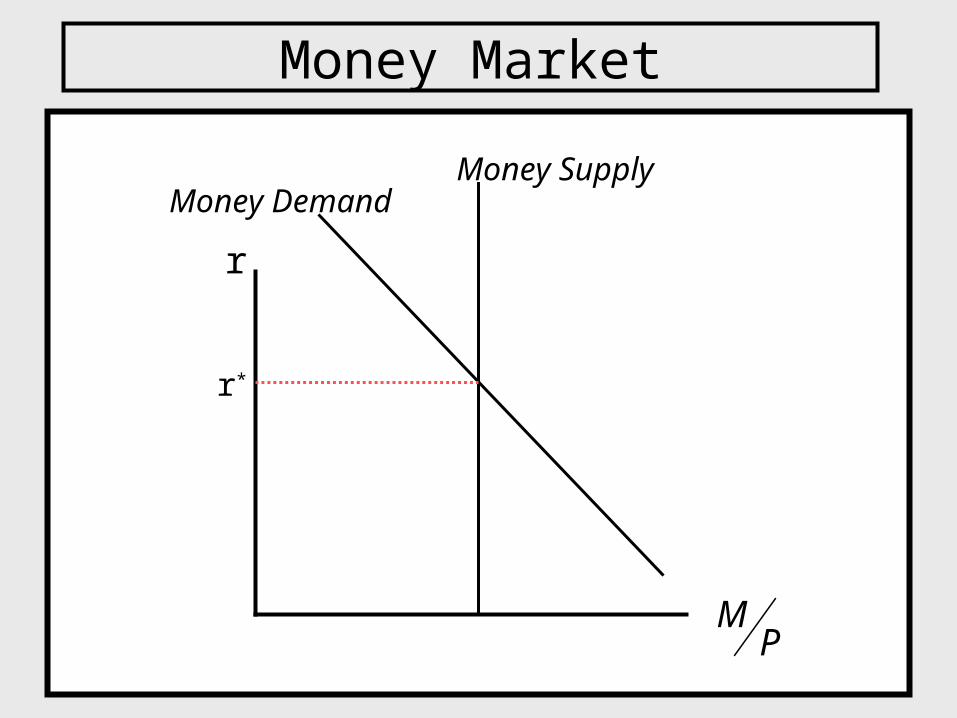

Money Market

r

Money Demand

r*

Money Supply

MP

Equilibrium in the Money Market

• If interest rates are too high, excess supply of money: – people will want to buy interest paying assets like

bank accounts or treasury bills.– Bond dealers and banks can reduce the interest rates

they are willing to offer

• If interest rates are too low, excess demand for money:– people will want to sell interest paying assets like bank

accounts or treasury bills to get more liquidity. – Bond dealers and banks must raise interest rates.

Monetary Policy

• In the US (and Euroland and Japan and most OECD economies), the central bank sets monetary policy by picking a short-run interest rate they would like to prevail.

• In HK, the central bank sets monetary policy by picking a fixed exchange rate.

Channel of Monetary Policy

• When the central bank increases the monetary base, the money supply will increase.

• Banks have excess liquidity which they use to make more loans.

• The supply of liquidity will exceed demand and banks must compete to attract borrowers who will hold this liquidity only at a lower interest rate.

• OECD central banks use their control over the supply of money to set a certain interest rate in the money market.

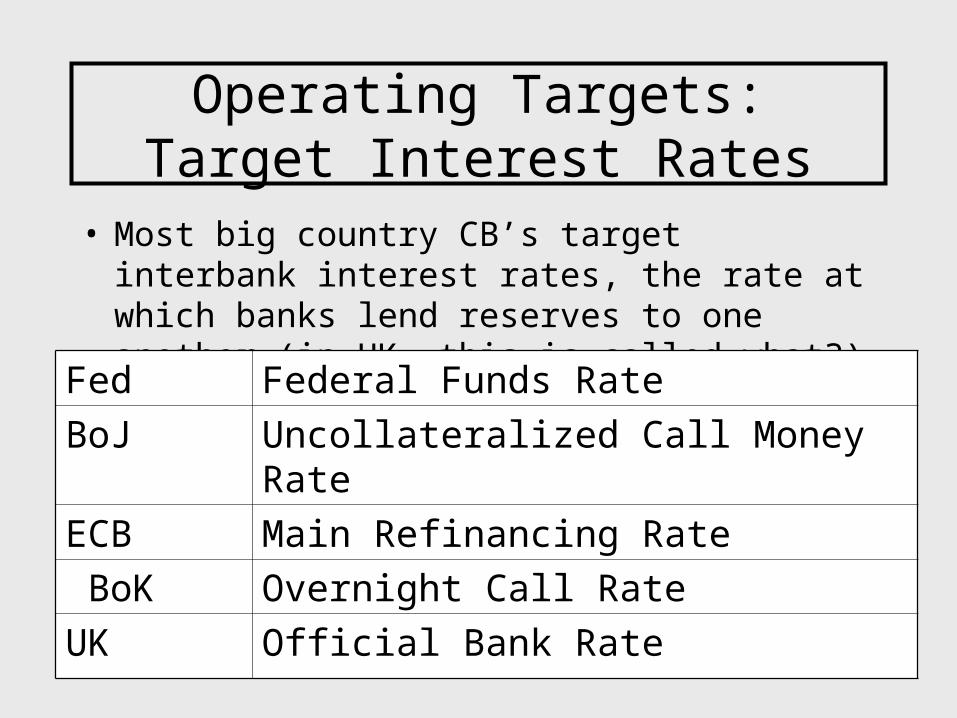

Operating Targets: Target Interest Rates

• Most big country CB’s target interbank interest rates, the rate at which banks lend reserves to one another (in HK, this is called what?)

Fed Federal Funds Rate

BoJ Uncollateralized Call Money Rate

ECB Main Refinancing Rate

BoK Overnight Call Rate

UK Official Bank Rate

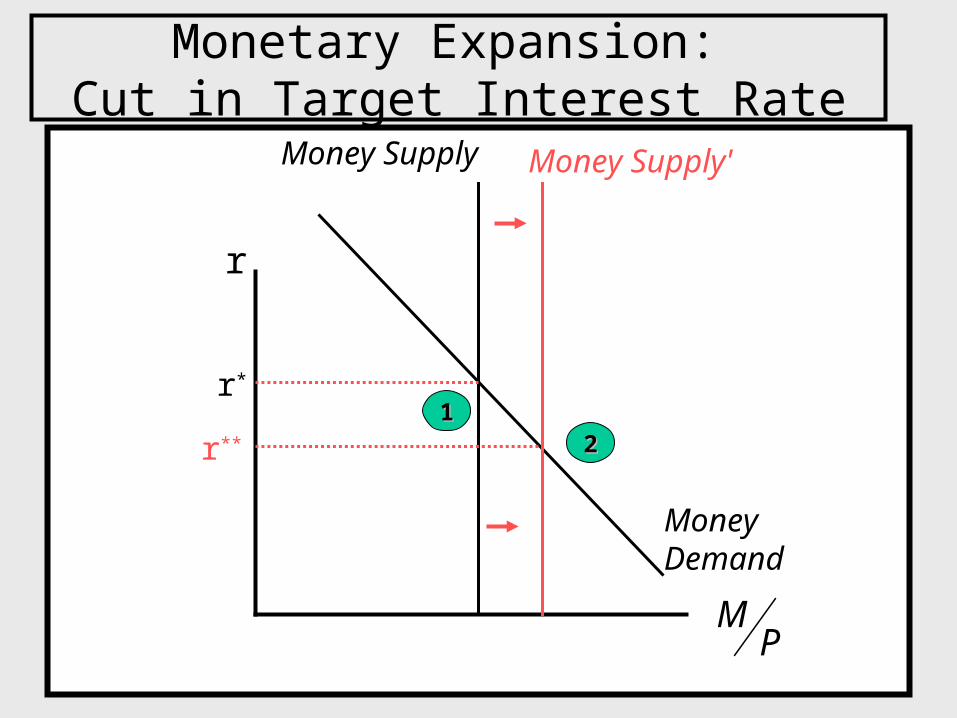

Monetary Expansion: Cut in Target Interest Rate

r

Money Demand

r*

Money Supply

MP

11

Money Supply'

22r**

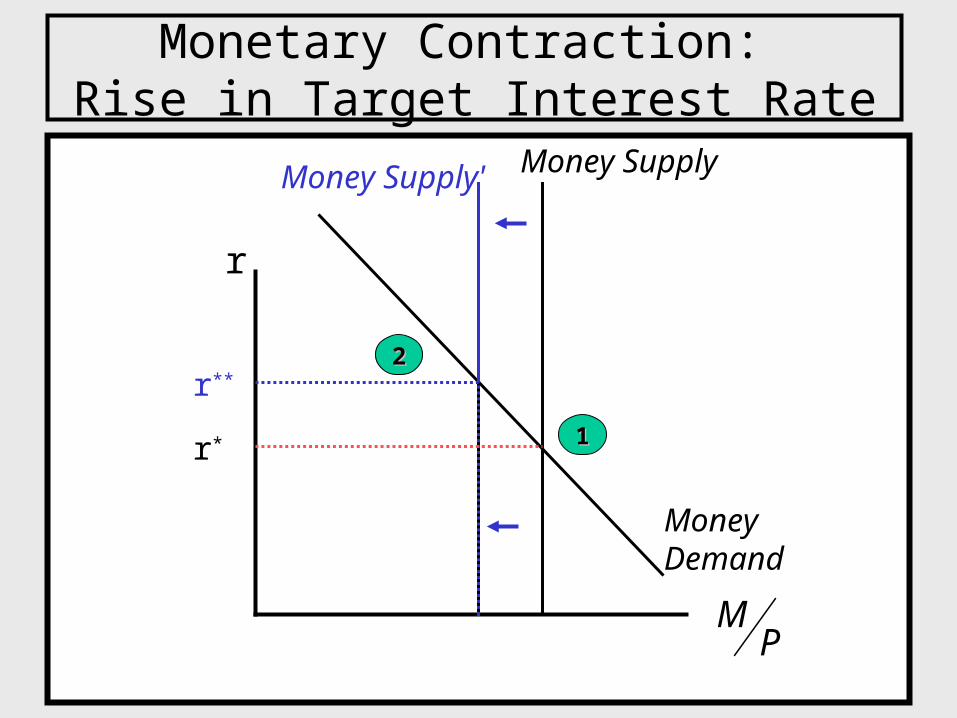

Monetary Contraction: Rise in Target Interest Rate

r

Money Demand

r*

Money Supply

MP

11

Money Supply'

22r**

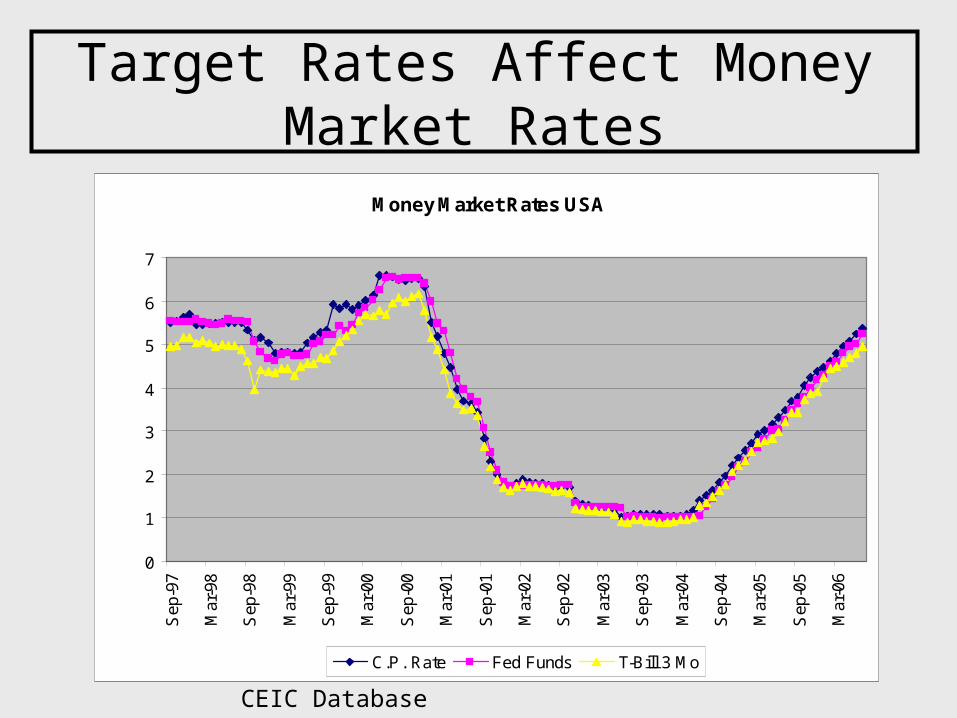

Target Rates Affect Money Market Rates

Money Market Rates USA

0

1

2

3

4

5

6

7

Sep

-97

Mar

-98

Sep

-98

Mar

-99

Sep

-99

Mar

-00

Sep

-00

Mar

-01

Sep

-01

Mar

-02

Sep

-02

Mar

-03

Sep

-03

Mar

-04

Sep

-04

Mar

-05

Sep

-05

Mar

-06

C.P. Rate Fed Funds T-Bill 3 Mo

CEIC Database

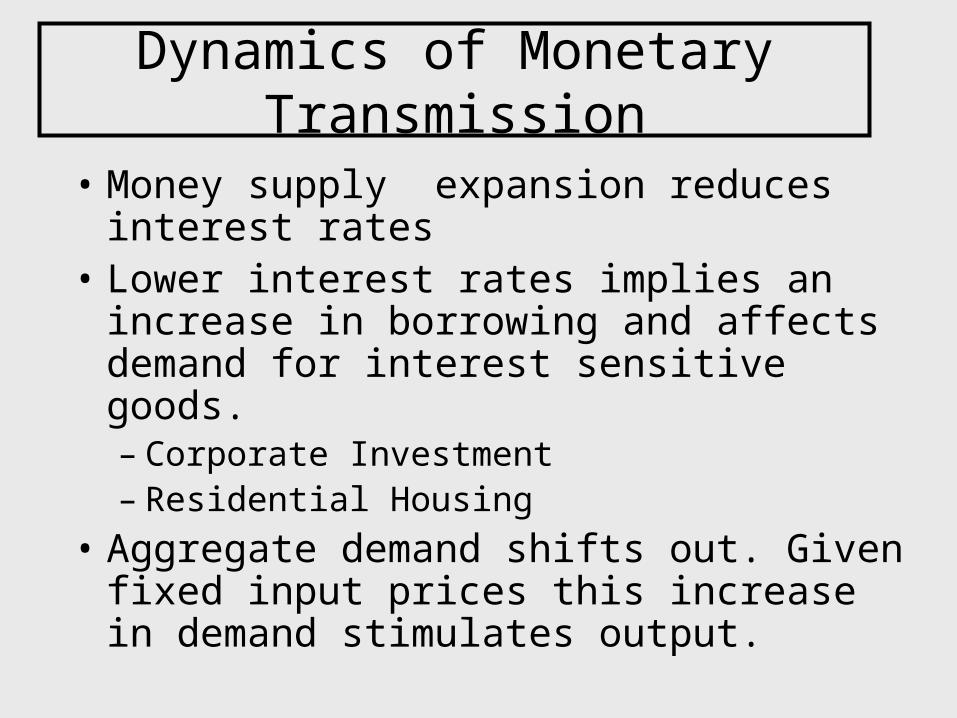

Dynamics of Monetary Transmission

• Money supply expansion reduces interest rates

• Lower interest rates implies an increase in borrowing and affects demand for interest sensitive goods. – Corporate Investment– Residential Housing

• Aggregate demand shifts out. Given fixed input prices this increase in demand stimulates output.

P

YY* AD

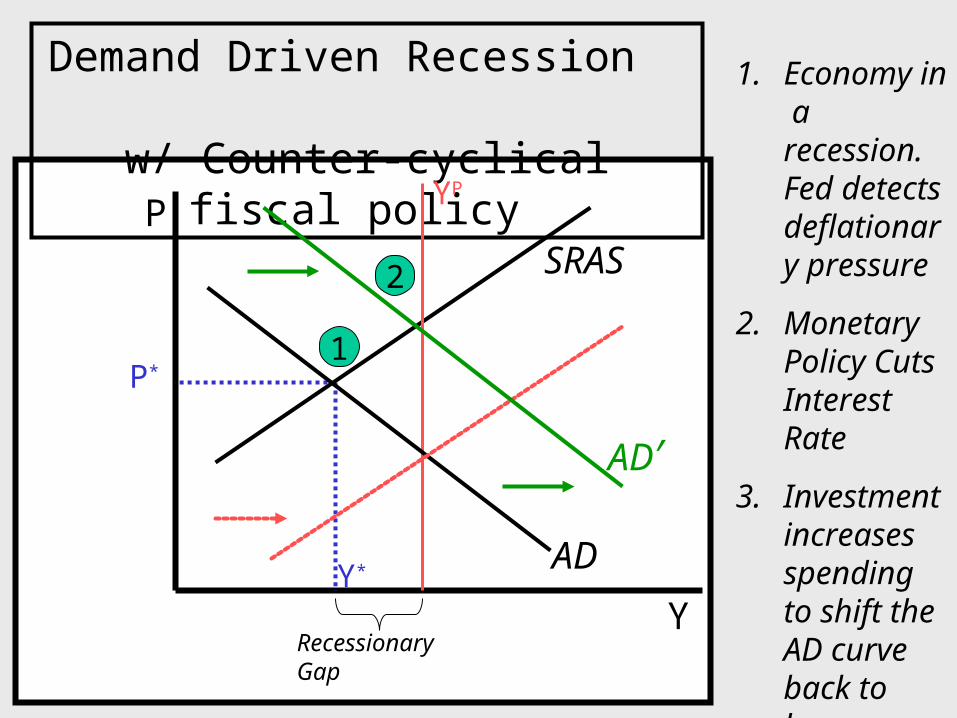

Demand Driven Recession w/ Counter-cyclical fiscal

policy

P*

SRAS

YP

AD′

1

2

1. Economy in a recession. Fed detects deflationary pressure

2. Monetary Policy Cuts Interest Rate

3. Investment increases spending to shift the AD curve back to long run equilibrium Recessionary Gap

P

YAD

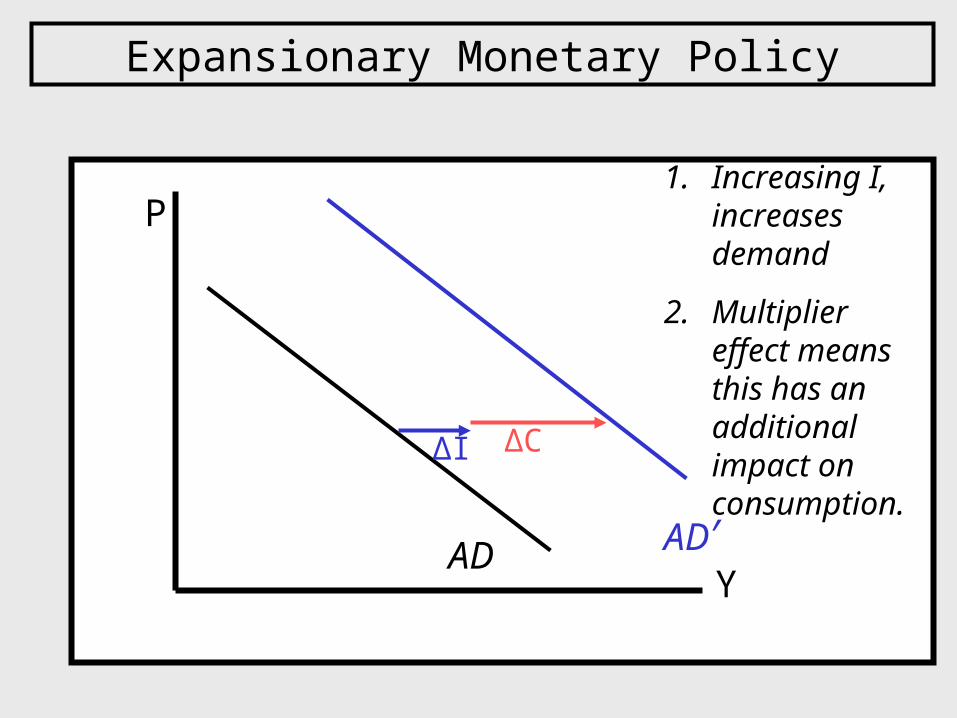

Expansionary Monetary Policy

AD′

1. Increasing I, increases demand

2. Multiplier effect means this has an additional impact on consumption. ΔI ΔC

P

Y

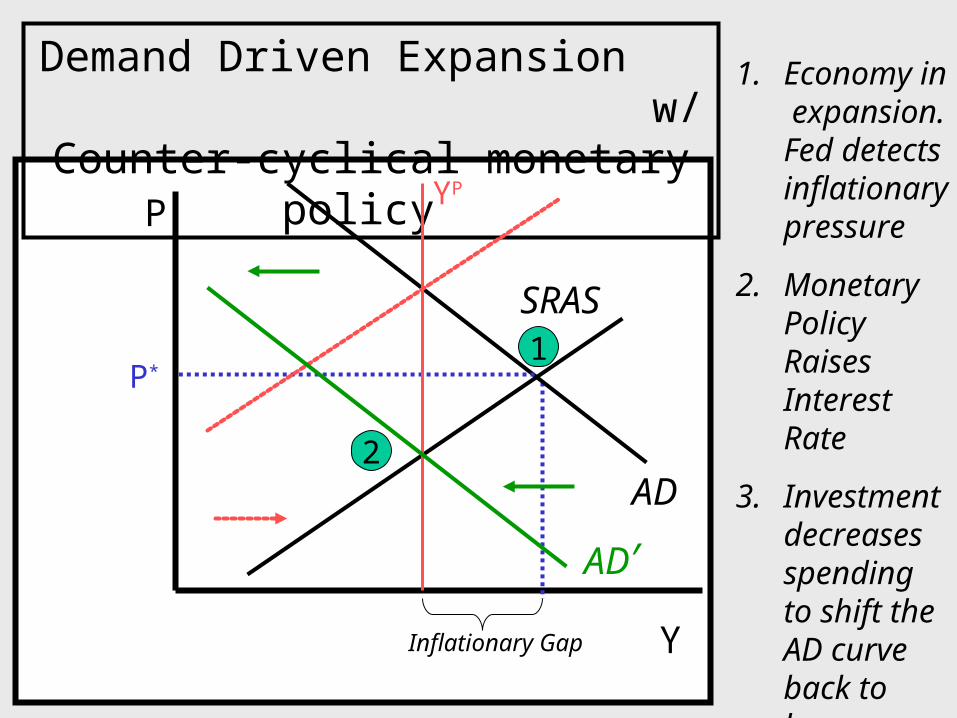

AD

Demand Driven Expansion w/ Counter-cyclical

monetary policy

P*

SRAS

YP

AD′

1

2

Inflationary Gap

1. Economy in expansion. Fed detects inflationary pressure

2. Monetary Policy Raises Interest Rate

3. Investment decreases spending to shift the AD curve back to long run equilibrium

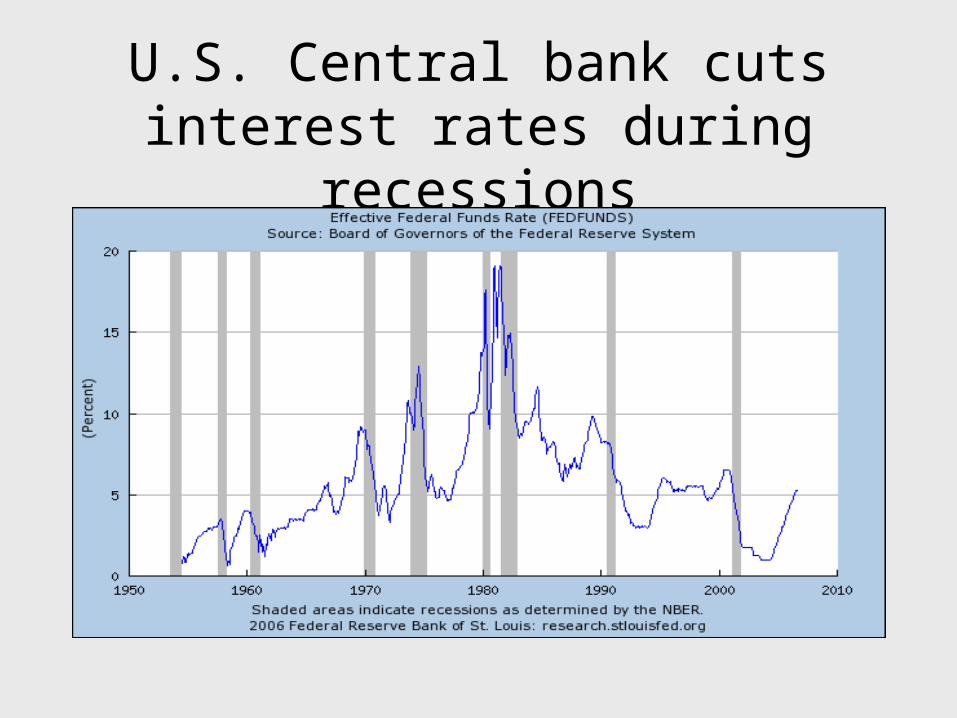

U.S. Central bank cuts interest rates during recessions

Lags, Mistakes and Monetary Shocks

• It is often said that there are long and variable lags in the monetary transmission mechanism in that it might take several quarters for the strongest effects of monetary policy on demand to appear plus it is difficult to predict how long exactly it will take for monetary policy to have its intended effects.

• What happens if a monetary expansion destabilizes the economy?

P

Y

AD

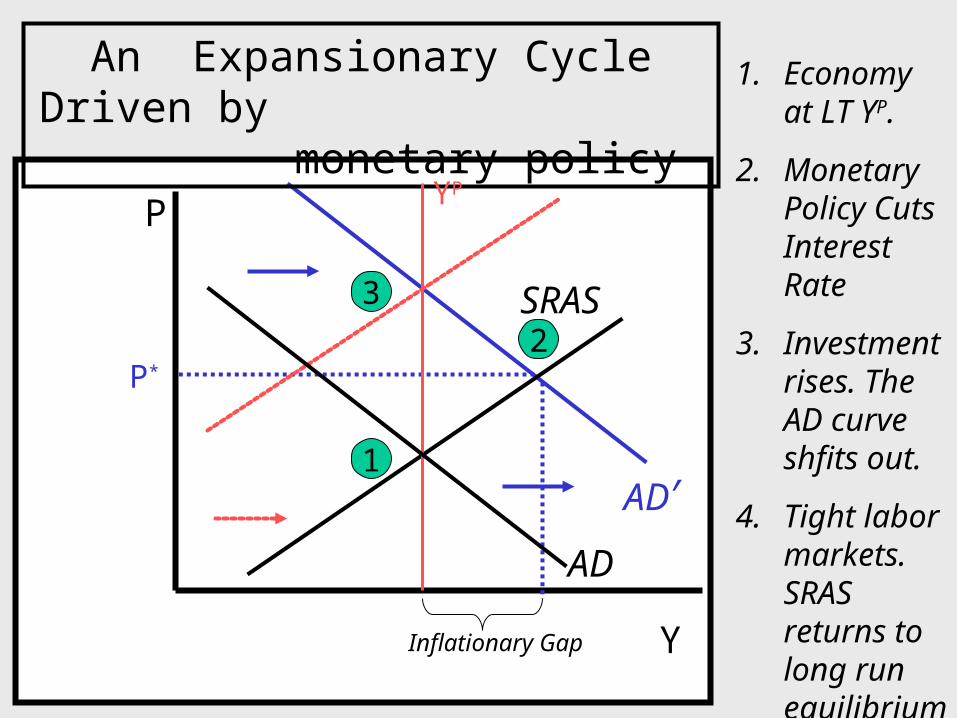

An Expansionary Cycle Driven by monetary policy

P*

SRAS

YP

AD′1

2

Inflationary Gap

1. Economy at LT YP.

2. Monetary Policy Cuts Interest Rate

3. Investment rises. The AD curve shfits out.

4. Tight labor markets. SRAS returns to long run equilibrium

3

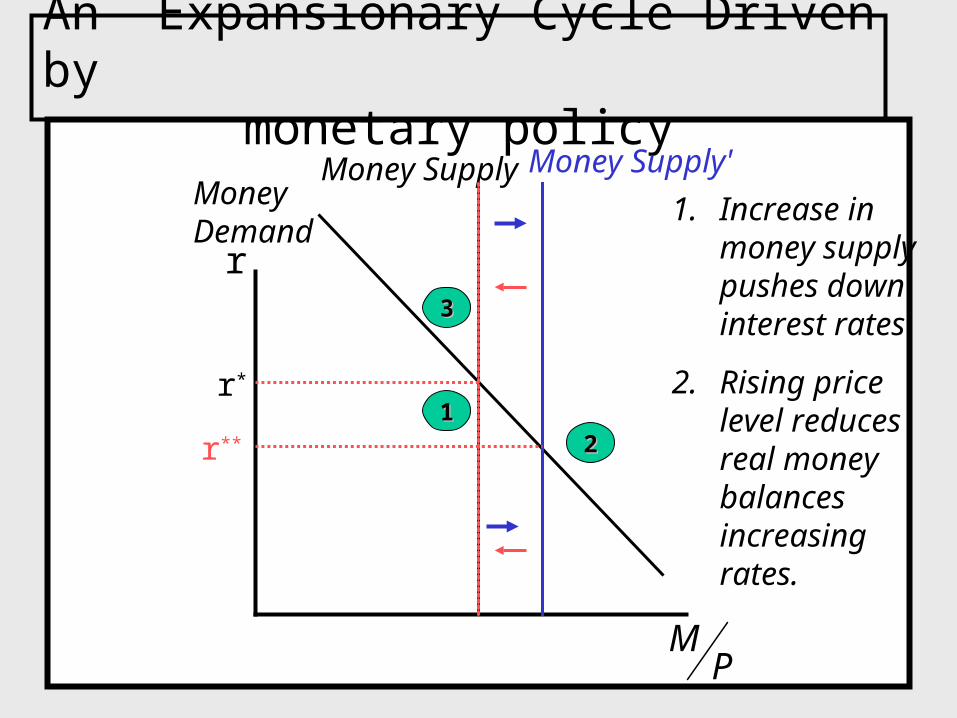

An Expansionary Cycle Driven by monetary policy

r

Money Demand

r*

Money Supply

MP

11

Money Supply'

22r**

1. Increase in money supply pushes down interest rates

2. Rising price level reduces real money balances increasing rates.

33

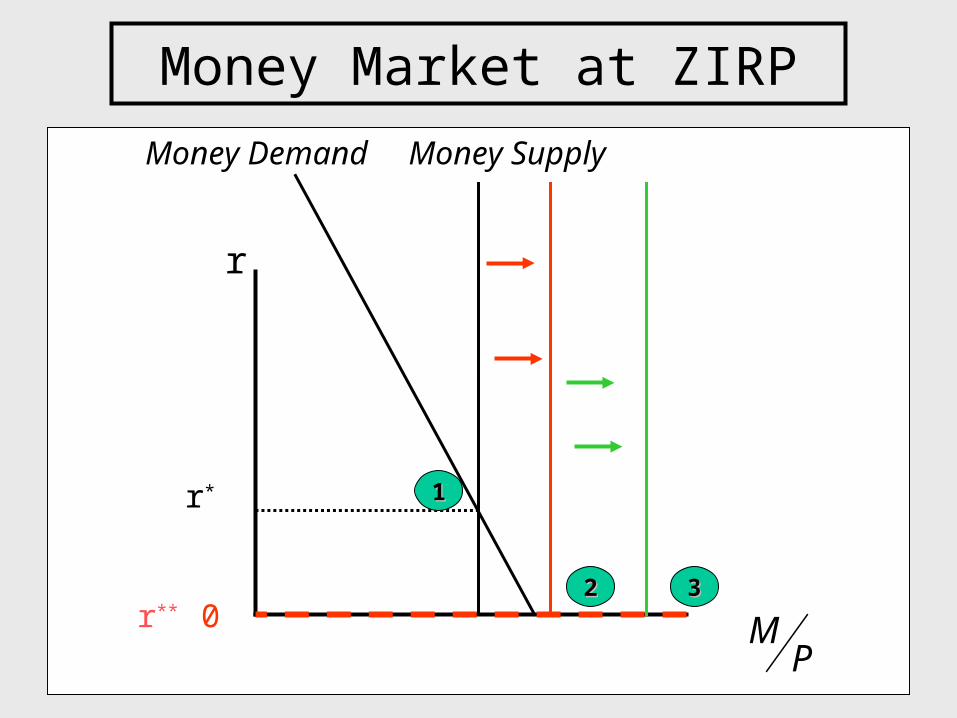

Zero Lower Bound on Interest Rates

• Nominal interest rates cannot go below zero – no one will lend money at an interest rate below that of money itself.

• In Japan, central bank increased money supply to get the economy out of a recession. Pushed the interest rate to zero.

• Once the zero lower bound was reached monetary policy has no effect.

Money Market at ZIRP

Money Demand

Money Supply

0

11

22 33

r

r**

r*

MP

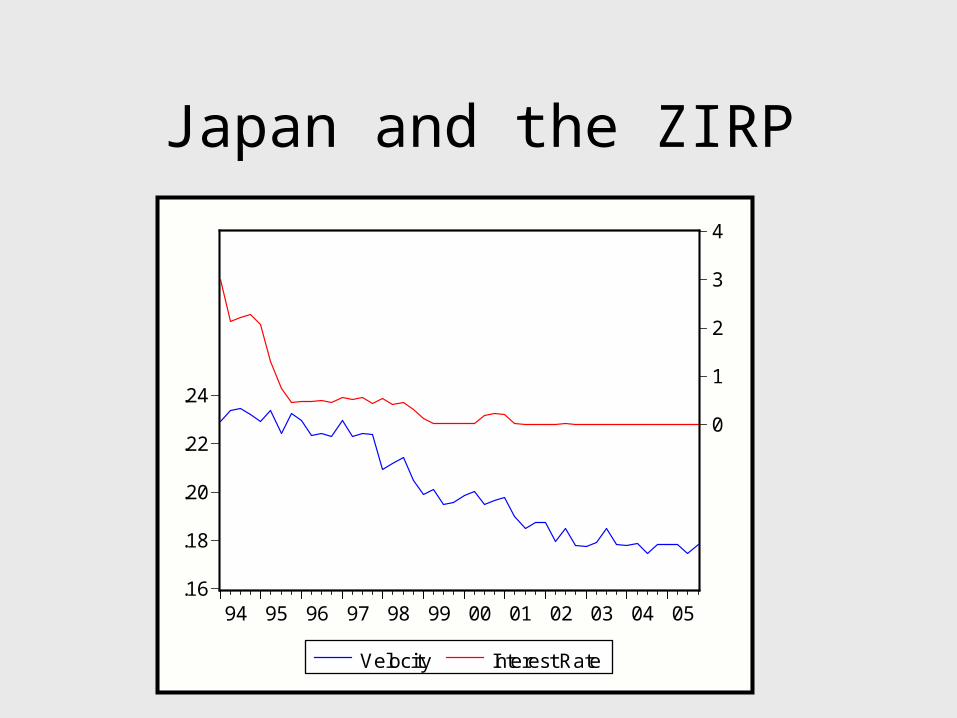

Japan and the ZIRP

.16

.18

.20

.22

.24

0

1

2

3

4

94 95 96 97 98 99 00 01 02 03 04 05

Velocity Interest Rate

US Interest Rates & HK Money Market

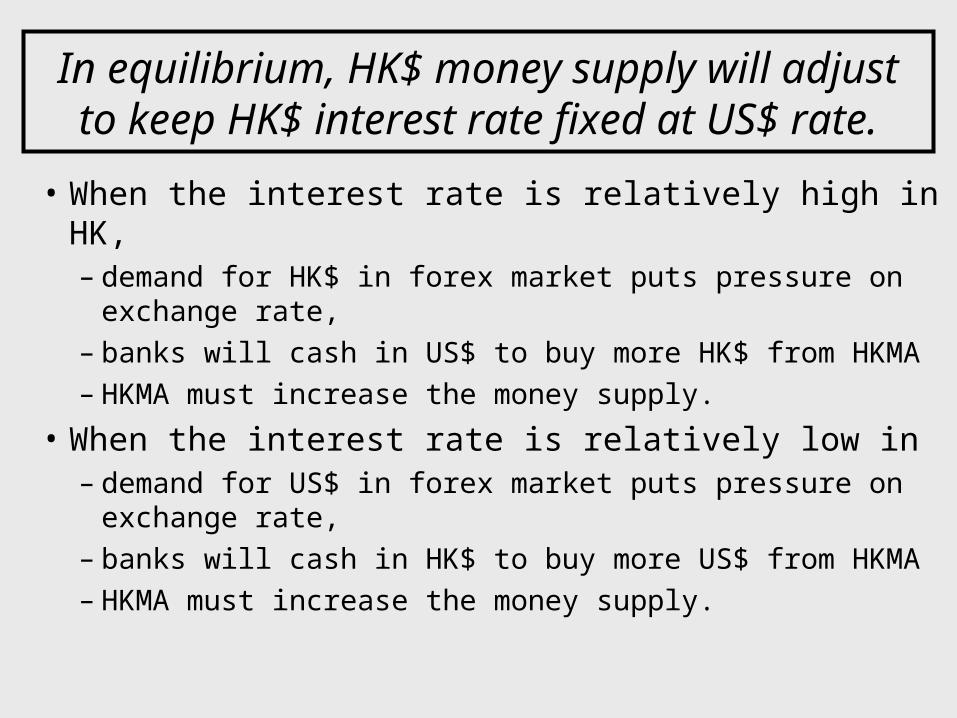

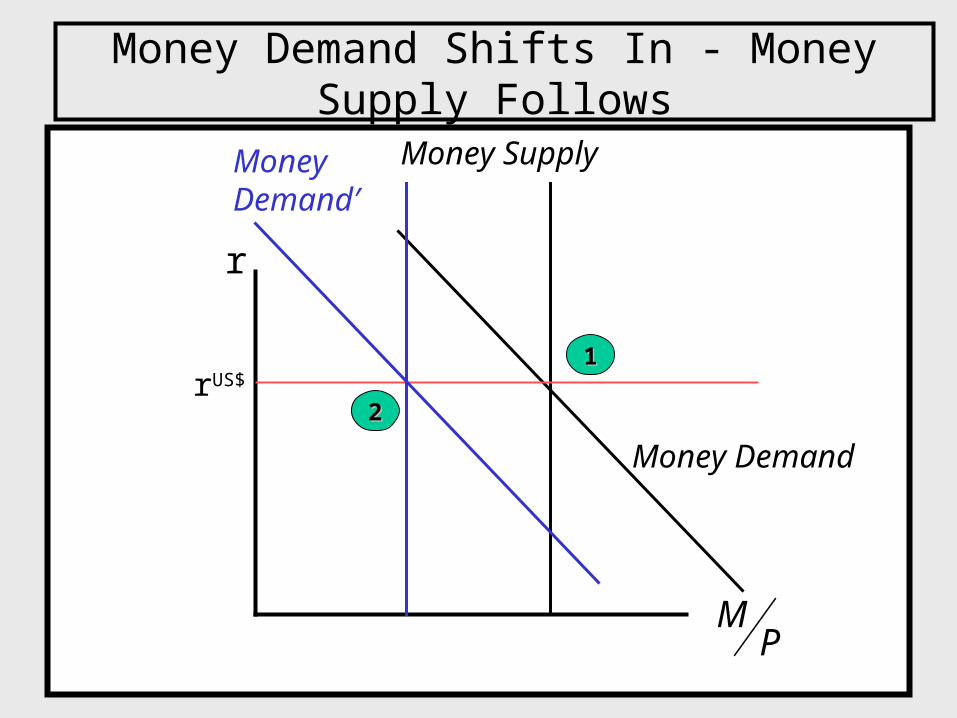

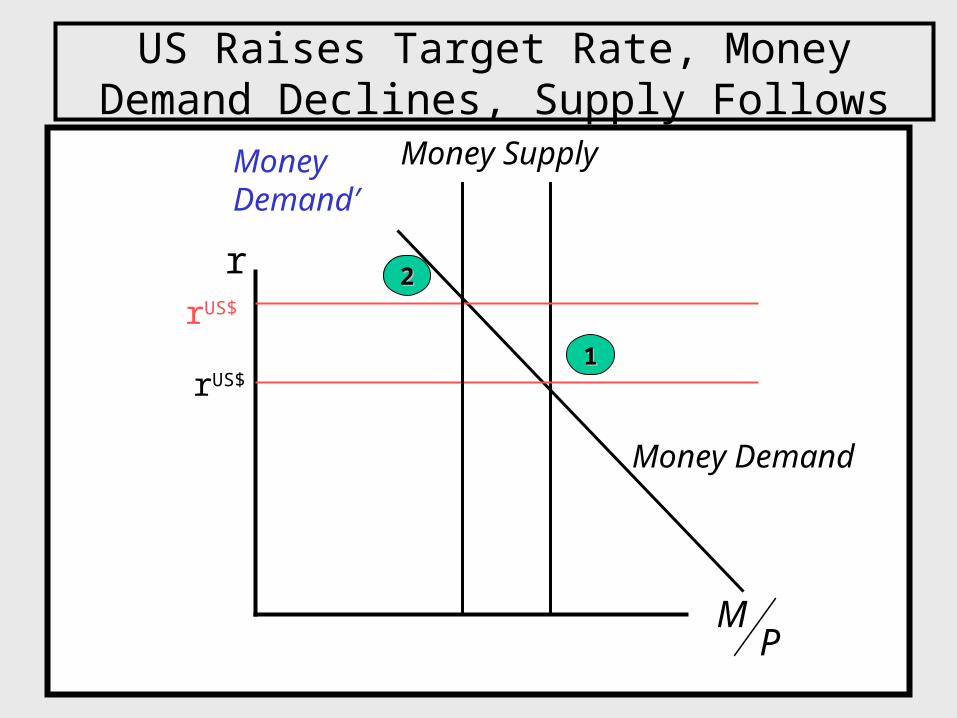

• Under HK’s monetary policy of a fixed exchange rate, HK$ bonds are perfect substitutes for US$ bonds

• Financial market investors will:– buy US$/sell HK$ whenever US$ interest rates are

higher than HK$ interest rate – Sell US$/buy HK$ whenever US$ interest rates are

lower than HK$ interest rate

In equilibrium, HK$ money supply will adjust to keep HK$ interest rate fixed at US$ rate.

• When the interest rate is relatively high in HK, – demand for HK$ in forex market puts pressure on

exchange rate, – banks will cash in US$ to buy more HK$ from HKMA – HKMA must increase the money supply.

• When the interest rate is relatively low in – demand for US$ in forex market puts pressure on

exchange rate, – banks will cash in HK$ to buy more US$ from HKMA – HKMA must increase the money supply.

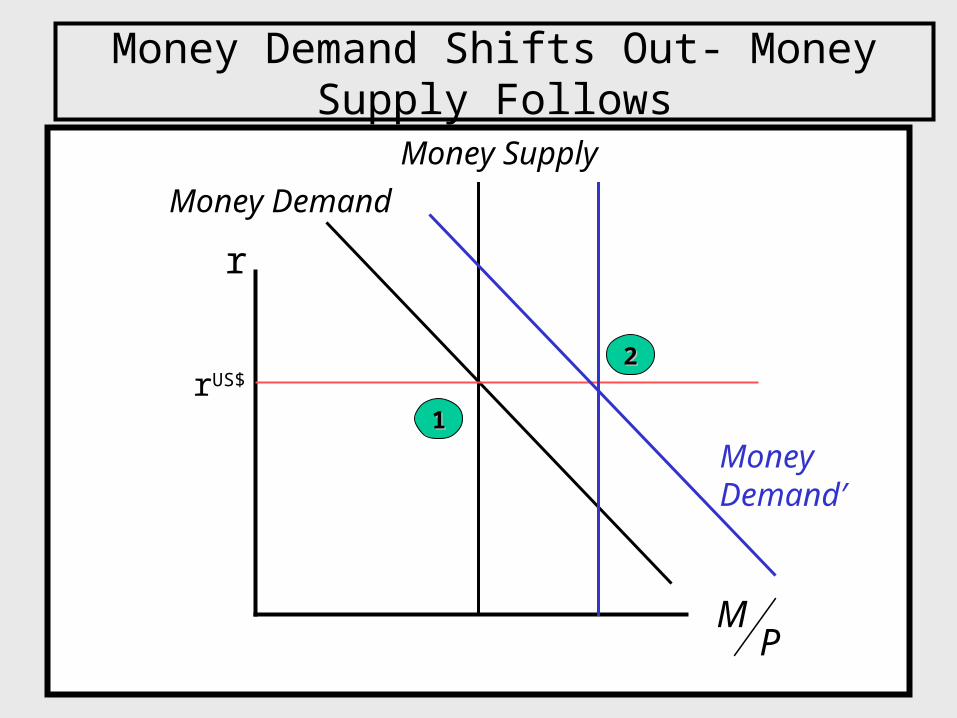

Money Demand Shifts Out- Money Supply Follows

r

Money Demand

rUS$

Money Supply

MP

11

Money Demand′

22

Money Demand Shifts In - Money Supply Follows

r

Money Demand

rUS$

Money Supply

MP

11

Money Demand′

22

US Raises Target Rate, Money Demand Declines, Supply Follows

r

Money Demand

rUS$

Money Supply

MP

11

Money Demand′

22

rUS$

Students should be able to:

• Discuss the determinants of velocity and money demand. Calculate the effects of a change in the interest rate.

• Describe the short-term impact of a counter-cyclical change in monetary policy using graphs and words.

• Describe the long-term and short-term impact of a monetary policy shock using graphs and words.

• Describe the impact of US monetary policy on HK’s monetary policy.

![Velocity-Anti Money Laundering [AML] Solutions Suite …donar.messe.de/exhibitor/cebit/2017/G655382/velocity-aml-solutions... · Velocity-Anti Money Laundering [AML] Solutions Suite](https://img.pdfslide.net/doc/110x75/5b6951b97f8b9a6f778df270/velocity-anti-money-laundering-aml-solutions-suite-donarmessedeexhibitorcebit2017g655382velocity-aml-solutions.jpg)