Embed Size (px)

Citation preview

MONEYMATTERS REPORT

2

Charitable help with money matters

Contents

Foreword . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3by Advocate Rose Colley, Consumer Council Chairman

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Main Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51. Managing our Finances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

2. Where is our Household Income coming from? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

3. Pensions & Savings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

4. Budgeting and Managing your Money . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

5. Financial Shortfalls and Borrowing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

6. Financial Awareness Raising. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Appendices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Appendix 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17Survey Sample

Appendix 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21Cash Only Challenge Report

Appendix 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27‘Karen’ and ‘Richard’ a debt case study

Appendix 4 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29Bad Debt Ghosts

Appendix 5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30Budget Planner

Appendix 6 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .36The Consumer Council and Community Savings

3

Making the Jersey consumer voice heard and making it count

Forewordby Advocate Rose Colley, Consumer Council Chairman

During Spring of this year the Consumer Council and Community Savings, ran a survey to ‘check Islanders’ financial health’ to see what problems people were facing when trying to manage their money, particularly as a result of the recession, and how our two organisations might best help with any issues raised.

‘The results and comments received were heartfelt and illuminating’.

In total we received a good response with 920 surveys returned (23%), which provided a ‘snapshot’ of the respondents’ financial wellbeing and highlighted their own opinions as to how they were managing. I would like to thank those of our randomly selected Islanders who took the time to respond to the survey for being honest and sharing their financial issues. I hope that the results in the Report below will be of interest and that our ’Top Tips’ will be of help to everyone and our Recommendations taken up by the appropriate organisations and individuals.

4

Charitable help with money matters

For easy reading this Report splits the results into a number of sections which reflect the topics upon which questions were asked. In addition, based on the results we have added some ‘Top Tips’ and ‘Recommendations’ under each heading.

It is hoped that the ‘Top Tips’ approach will encourage individuals to take responsibility for their own ‘financial health’ and to seek advice and help for financial worries and difficulties when needed.

Similarly it is intended that the ‘Recommendations’ will be used to help develop the money management and consumer rights awareness raising work already commenced by the Consumer Council, Community Savings and the Citizens Advice Bureau. It is hoped that responsibility for this work can be extended to other agencies to the benefit of as many Islanders as possible.

Executive Summary

Island Ark, a local independent research company, was commissioned to undertake the survey. 4,000 confidential and anonymous Money Matters Survey questionnaires were sent out during February & March to a demographically and statistically robust sample of Jersey households.

The survey results are discussed in this Report with a number of graphs and charts to illustrate them. The results clearly indicate that whilst many Islanders feel in control of their finances many are still struggling to make ends meet. Encouragingly, most take a responsible attitude towards their financial position but results demonstrated how the different age groups face different financial challenges.

Elements of the results raise interesting questions too and some of these are included for readers to reflect upon.

Three key messages emerged from our survey:

y We must all take personal responsibility for our financial health;

y We must all research our facts and ask questions to help us make informed decisions and to better understand the bigger picture of what financial health entails – over the short, medium and long term;

y Most importantly we must NEVER put our head in the sand – financial difficulties escalate not diminish!

5

Making the Jersey consumer voice heard and making it count

Main Report

1. Managing our Finances

Key Finding: The majority of household finances are not a shared responsibility with only 31% of our respondents indicating that finances are shared.

There appears to be a distinct division of labour when it comes to the household finances, with just one family member usually managing the money.

Q: Why don’t we share household finances?

Who manages the household finances?There are both generation and geographical splits. Older respondents appear more likely to have a household with just one person managing the finances whilst those residing in St. Helier are the most likely to have one family member with sole responsibility for holding the family purse strings.

Q: Surely two heads are better than one?

We do have to face the tough reality that in a relationship if only one of us is financially responsible or involved in household money matters and the couple separate for whatever reason (perhaps a relationship ends either acrimoniously or amicably or sadly because of bereavement) if an individual is not financially aware he or she is extremely vulnerable. Adding financial worries and challenges to an already stressful situation is both difficult and frightening.

Interestingly research from the Citizens Advice Bureau indicates that money is a prime reason for divorce.

Q: Is this because we ‘hide’ away from financial truths and fail to talk about money issues?

Q: Or are we too afraid to consider budgeting to cope and plan with tough times?

Me

Someone else

Other

Me, not others personal

Shared

6

Charitable help with money matters

The whole divorce process is usually a huge strain not only on the individuals concerned but on the family finances. Staying in communication may be difficult but it is the key to keeping the overall costs down. Once separating, if couples refuse to communicate other than through lawyer’s letters, the expenses can very quickly rack-up.

Family lawyer Advocate Rose Colley comments that ‘more expenditure is needed to keep the family afloat. It is therefore essential that couples try to share the financial information so that if things go wrong both are far more able to resolve issues and to move forward in a positive way’.

Q: Are you aware of your financial position?

However, whether in a relationship or not an individual’s confidence, wellbeing and personal independence can be adversely affected if they are scared of their relationship with money and the responsibilities that come with it. Having some basic appreciation as to how to manage your money is something that we all need to learn and realising that your personality can affect how you spend or save your money is also important.

Q: Be honest – are you a spendthrift or a natural saver?

: Our ‘Top Tips’

1. Be aware of your financial position

2. If you are not very good at handling your budget, find someone who can help you. There is help available online too

3. Do not bury your head if you foresee a financial hurdle, challenge, or difficulty. Get help and seek impartial advice, see Appendix 5 for a copy of Jersey Consumer Council’s Budget Planner

Recommendations

1. All school students should be helped to develop a positive and organised relationship with money and finances and schools should be supported in their provision of financially based lessons

2. Programmes raising awareness of the importance of how to manage one’s money and make sound financial decisions such as the ‘Money Management’ and ‘Savvy Consumer’ programmes offered by Community Savings and the Consumer Council should be funded sufficiently to make them available widely in the community

3. Clubs, groups, charities and employers should arrange ‘Managing your Finances’ talks and workshops for their members and employees

Take a practical approach to your

finances and budget.

7

Making the Jersey consumer voice heard and making it count

Main sources of household incomeKey Finding: The survey results showed that respondents are relying on a mixture of monetary sources for their income.

In particular wages account for 64%; pensions 19% and government aid 7%. The pie chart (above) and the graph (below) provide the full picture.

2. Where is our Household income coming from?

1.89%7.14%

19.84%

2.86%

3.42%

64.89%

Wages

Investments

Government aid

Business income

Pension

Other

savings

0% 5% 10% 15% 20% 25%

assurance policy

shares or ISAs

other financial investments

private pension

work pension

saving plan

100%

50%

0%

Yes NoEmployed

Unemployed

Homemaker

Retired

How people are drawing from their savings.

Respondents are drawing money from a variety of sourcesHowever to supplement household income we should be aware that our results show that many respondents, in particular the unemployed and the retired, are also regularly drawing significant amounts from their savings, to help ‘stay afloat’ as illustrated in the graph below.

8

Charitable help with money matters

3. Pensions & Savings

Key Finding: The results illustrate that many Islanders are still being prudent saving for their future.

Respondents were asked if they contributed towards a variety of savings schemes.

One third of respondents (33.93%) said they had savings whilst 13% had a savings plan and 22% life assurance schemes.

The chart shows the full results:

: Our ‘Top Tips’

y Try to build up a healthy savings balance throughout your life

y Try and work out a long term financial plan so that you can save accordingly

y Review your budget before drawing from your savings

Recommendations:

y Free workshops on long term financial planning to be made publicly available

y Consumer Council to do a feature on long term financial planning

Savings plan

Savings

(Please note that many respondents may be contributing to one or more investment types).

Private pension

Shares or ISAs

Work pension

Life insurance

Other financial investments

Have a financial plan … short, medium to

long term

9

Making the Jersey consumer voice heard and making it count

Pensions historically have been the way to plan for old age income.It is noticeable that nearly a third of Islanders (30%) have the back up of a work based pension plan to contribute to their future financial well-being whilst 16.93% have private pension arrangements. These results indicate that a high percentage of Islanders still look towards pensions as a sound financial option for retirement years.

However, a word of caution, we now know that pensions do not always fulfil our financial aspirations and plans as the pension funds do not always perform according to original expectations or to the small print.

Financial Advisors urge us to regularly monitor our investments and pensions and to check the charges and estimated maturity values. Craig Wallder at Moore Stephens Financial Management recommends that ….‘To ensure that you are on track to meet your retirement goal, it is important that the funds within your pensions and savings plans are reviewed on a regular basis. The sooner under-performing funds are spotted the less impact they will have on the final fund value. It is also important that the correct blend of investments are chosen; funds that are more growth orientated in the early years and funds that provide capital preservation as you approach retirement. Fees can seriously erode the value of your pensions and investments so it is essential you are aware of the charges that are being deducted each year’.

Financial ProductsThe chart (page 8) shows that Respondents are saving their money in a variety of ways.

However there are many types of financial products and schemes to choose from when investing or saving your money – but markets change.

There are many questions to be asked such as:

y Do people research the products and schemes into which they put their hard earned money and then do they monitor them?

y Is the product the best one for the individual / couple?

y Will the plan pay out as and when the individual / couple need it to and at the intended level?

y Do individuals/ couples review their investments as they progress over time and through to maturity?

Life Assurance policies are an example of a product about which such questions should be asked.

202 (22% of 920) of our respondents are contributing to a Life Assurance policy.There are many types of life insurance available which can be taken out to suit individual circumstances and budgets, such as term assurance or whole of life policies.

The idea is that a suitable policy is for a period long enough to cover the term of a mortgage or provide income protection. It is especially sensible if someone has a joint mortgage for if one person dies it could lead to the surviving partner losing their home if she or he was unable to meet the mortgage payments by themselves. It is important to remember that if you die after your fixed term ends then there won’t be a payout.

‘A life insurance policy will usually be paid out as lump sum in the event of your death, but it can also be paid out over a predetermined length of time to replace lost income. There are also many other beneficial options that you could add to your policy if your budget allows, such as Critical Illness and Income Protection. Some providers also have additional free options such as Children’s Cover or Medical support and advice’ Consumer Council Jersey Issues April 2014.

The survey confirmed that those on higher incomes and respondents in the younger age groups 16 – 24 are more knowledgeable about financial products.

10

Charitable help with money matters

Q: Do you think you know enough about financial products or know where to turn for sound impartial advice?

Q: Do you think that we all understand the reams of paper work we get sent regularly regarding investments and pension funds?

Emergency Back-up FundsOf particular concern in the survey results was the level of back-up emergency funds that some respondents have.

Critically we wanted to know if Islanders are saving enough to cover short-term disasters should the main source of income stop for example because of divorce; illness or loss of a job.

Malcolm Ferey, Chief Executive of the Citizens Advice Bureau says ‘The Bureau recommends holding an emergency fund equal to three months’ wages. Whilst this is easier said, than done, it really does help if you are faced with an unexpected expenditure. If you are unable to save this sum and you are faced with an unexpected bill, do not be tempted by the fast and easy credit adverts and pay day loan companies. Our experience of these operations is that short term ‘fixes’ end up being long term problems.’

Q: How long could you survive financially if you lost your income?

In our survey 43% of respondents had an emergency fund less than Jersey’s Citizen Advice Bureau’s recommended level of 3 months income. Without an adequate emergency back-up fund debts can easily escalate out of control if not managed as the experiences of former Citizens Advice Bureau clients, ‘Karen’ and ‘Richard’ in Appendix 3 of this Report shows.

It is really important for anyone who feels that their finances are spiralling out of their control to seek some help as soon as possible. Most of us do not realise the long term effect that a bad debt record can have on our future finances.

Q: Do you know how your financial record can be affected by your debt record?

In Appendix 4 we give a few examples of how bad debt may affect you – some of which may surprise you.

The Citizen’s Advice Bureau has a Self-Help Advisory Debt Pack on their website which individuals can use or else an appointment can be made with a CAB adviser at their premises at St Paul’s Gate. http://bit.ly/1leN9HW

: Our ‘Top Tips’

1. Seek advice in advance of financial difficulties to help plan and cope

2. Take every opportunity to attend financial awareness seminars and talks

3. Review your savings and investments regularly

4. Make sure you understand your Social Security contributions record

5. Keep saving for the future or that unexpected emergency

6. If possible attend a retirement planning day to understand all about retirement and how to make your financial retirement plans

Recommendations:

y Organisations should run awareness seminars for their staff and members about:– Financial planning for retirement – How to review your savings

y Individuals and families should aim to have dedicated savings accounts, perhaps held in a separate organisation such as Community Savings, to make it less tempting to draw out from savings.

11

Making the Jersey consumer voice heard and making it count

4. Budgeting and Managing your Money

Key Finding: The survey indicates that regardless of our age 74% of us budget on a monthly basis with only a few of us budgeting fortnightly or less.

Do we struggle each month to meet all our household spend commitments?However, despite budgeting, 42% of respondents replied saying that they struggle each month to meet all their domestic financial commitments. Indeed our survey findings are comparable to those of the 2013 Jersey Annual Social Survey, which reported that 45% of respondents had difficulty making ends meet.

But, one of the most important findings of the survey was that 70% of those who budget indicate that they are able to stick to their budgets, albeit many find it hard to do so. The fact that so many were budgeting and not overspending was a re-assuring and important key message from the Money Matters survey.

However, although the results showed that the majority of respondents are prudent savers long term money planning is not a high priority for some as 25% said they do not budget.

‘Two of our key objectives are to make people aware of how important it is to budget and to

save for that unexpected problem,’ says Stuart Stables, Executive Officer at Community Savings ‘I am delighted to see that so many people say they are achieving these goals. However, for those who find it hard we offer free budgeting support to our customers.’

Q: How often do you stick to your planned budget?

Q: Are we just not trained to save and budget as previous generations were brought up to do?

Q: Do some people not budget because they feel unable to plan as they are just about ‘keeping their head above water’?

Are we impulsive spenders?The relationship consumers have with money is pivotal to their spending, saving and understanding of money.

Strongly agree

Neither

Strongly disagreeAgree

Disagree

Always

Sometimes

NeverMostly

Hardly ever

50% of respondents felt that they were not ‘impulsive’ spenders but that they managed their finances prudently and contributed to savings.

However, this does not mean that Islanders are finding it easy at the moment, for, as advised above, 42% of respondents commented that they struggle each month to make ends meet.

12

Charitable help with money matters

Do we impulse buy?The younger we are the more likely we are to be impulsive. However, the results showed that almost half of the ‘under 54’ year olds stated that household finances would not meet commitments. In older age groups respondents report managing better whereas in the middle age groups the %’s are as follows: 42% of 16 - 34 year olds: 36% of 35 - 44 year olds and 37% of 45 to 54 year olds not meeting monthly commitments.

7% of respondents said that they were impulsive spenders but the ease of online shopping and sales can be big traps.

The Jersey Citizens Advice Bureau says ‘Plenty of research has been done to prove that when people deal in cash, they spend less. Try to control your spending in that way or remember this, it’s only a bargain if you can afford it and you need it, otherwise it’s probably unnecessary and frivolous spending.’

Community Savings ran a ‘Cash Only Challenge’ last year to raise awareness of how important it is to budget and save if one can. The volunteers who took part in the Challenge were asked to live off a fixed sum of cash for a week. All noticed how

managing their daily lives using cash only made them far more aware of how much they were spending and how much they spent unnecessarily in normal circumstances e.g. on take-away coffees. Their experiences are recorded in the ‘Cash Only Challenge’ Report attached to this report in Appendix 2.

: Our ‘Top Tips’

y Analyse your spending habits and consider whether your finances would benefit from a few changes

y Try managing on cash, even for a while, to help you spend less

y Try cutting out take aways etc. and see how much you save

y Always try to save even a few pounds each week so as to have some money in reserve from your budget for those unexpected payments

y Budget regularly and stick to it - use a budget planner from the Consumer Council

y Money management is not easy. Plan and do not bury your head if things start to go wrong – see our case in Appendix 3 to highlight how quickly financial issues get out of hand

13

Making the Jersey consumer voice heard and making it count

y Ask budgeting advice from a trusted source such as the Citizens Advice Bureau or Community Savings

y Focus on your real needs rather than have peer pressure decide and shape your spending habits and empty your bank accounts

y Disaster can strike at any time – don’t be ashamed. Seek help if necessary

Recommendations:

y Organisations to promote budget planning sessions for their employees and members

y Budget planners to be made available in central locations e.g. the Library; Social Security

y Employers to supply budget planners or provide online links to the Consumer Council one

y Community Savings to run a savings initiative to promote awareness of the importance of saving and budgeting

5. Financial Shortfalls and Borrowing

Key Finding: The results indicate that generally people seem to be managing, with a healthy approach to managing any debts and borrowings.

The survey revealed that on average only a fifth of respondents have debts or loans - ranging from 34% with a mortgage to 20% with credit card debts. Whether respondents owned their own home, lived in private rental accommodation, or were States tenants this level of debt remained even at 20%.

Respondents reported that hard life experiences are impacting on them yet they also demonstrated an extremely responsible attitude to money. Most respondents would try and help themselves if they got into difficulty with 43% saying that they would attempt to earn extra income; 74% would cut back on living expenses and 83% would cut back on luxuries should money become short or to make ends meet if finances were running low.

Very likely

Not very likely

Don’t knowQuite likely

Not at all

Don’t be lured by ‘keeping up with the

Jones’

14

Charitable help with money matters

Would you rely on credit cards to pay for a large unexpected household cost equivalent to at least one month’s income?If a large unexpected household cost equivalent to at least one month’s income arose 77.88% Islanders would draw on general savings to pay for it. They would not rely on credit cards, an overdraft facility, or take out a loan nor pay a bill.

We were pleased to see that respondents also said that they would reduce spending on luxuries before cutting back on basic foods.

Finally, family support appears to be very strong with 25% of respondents saying that they would approach family for financial support and advice rather than take out loans.

It was also heartening to note that Islanders would take the responsible approach of contacting their own banks or agencies such as Jersey’s Citizens Advice Bureau for help.

‘Although we do not have any commitments apart from rent, I would initially turn to the family for support. However, if this was not possible, I would look to sell personal items such as our laptops and jewellery’

‘Contact mortgage provider and try to come to a sensible solution’

Our survey indicates that people are extremely wary of payday loans with very few taking them out. Of those who did, however, worryingly 50% did not fully understand the terms, conditions and critically the interest rates attached to these short-term loans.

The Jersey Citizens Advice Bureau advises that ‘there is lots of help available for people who have money worries and The Jersey Citizens Advice Bureau and Community Saving are just two

of the main organisations that can help rebuild finances again. Don’t be tempted by credit advice that costs you money, these are very often loan

companies masquerading under another banner. Our services, like those of Community Savings, are FREE and confidential, most importantly; we won’t judge you or your predicament. We’re here to help’.

: Our ‘Top Tips’

y Review your financial position regularly

y If using savings to meet unexpected expenditure – revisit your budget and adjust where possible

y Aim to keep a savings pot of at least 3 months income for a ‘rainy day’

y Always try to pay off your credit card on a monthly basis

y Don’t over extend your spending

y Make sure you understand the ‘real cost’ of any borrowing or loan

Recommendations:

y Consumer Council to run a feature raising awareness of the real cost of borrowing

Budget so that you can always save, even if it is a small amount

15

Making the Jersey consumer voice heard and making it count

6. Financial Awareness Raising

Key Finding: 62.44 % of respondents said that they would have liked more financial education at school.

Young consumers represent significant buying power. The school spending surveys carried out as part of the Consumer Council schools programme reveal that on average Year 10 students (age 14 - 15 years old) spend £20 each when they go out with friends and an average of £18 weekly on the internet on sports, fashion and electronic goods.

We all receive training for the jobs we do but what training are we given to help us manage our money? Yet this is such an important skill we all need to learn to help us throughout our lives. The survey results showed that just over 10% of respondents commented that they lack confidence in managing finances or understand finance products.

However, the reality is that very few of us know how to spend our money wisely by making informed decisions.

The Consumer Council and Community Savings believe that money management and consumer awareness training are ongoing issues. Life moves on, as do options and financial products and we all need to be financially aware in order to make informed financial decisions. Stuart Sables from Community Savings comments ‘It is interesting to note that many would have liked to receive more financial training when at school – a gap that we hope to be filling with the Consumer Council as a result of our joint schools ‘Money Management’ training programme.

: Our ‘Top Tips’

y Consumer Council to keep publishing relevant financial articles for example ‘when you are coming up to retirement’

y It’s never too late to start learning how to manage your money

Recommendations:

y Our agencies will be looking to discuss possibilities to increase financial awareness training programmes for the benefit of all sectors of the community including for the islands youth clubs; centres for the elderly and single parents; those retiring; large employers and church groups as well as schools

y The adoption of a collaborative approach to hosting Money Clinics to help consumers understand financial matters

y Raise awareness of agencies that can help with training on money management and financial products advice

y The practical and important financial life skills programmes in schools offered by Consumer Council; Community Savings; various banks and the Jersey Financial Services Commission to be maintained and further developed

Start your relationship with budgeting and money young, preferably whilst at

school

16

Charitable help with money matters

Appendices

Appendix 1: Survey Sample ............................................................................................................................................. 17

Appendix 2: Cash Only Challenge Report .................................................................................................................21

Appendix 3: Karen and Richard: a debt case study .................................................................................................27

Appendix 4: Bad Debt ‘Ghosts’ .....................................................................................................................................29

Appendix 5: Budget Planner ..........................................................................................................................................30

Appendix 6: The Consumer Council and Community Savings ..........................................................................36

17

Making the Jersey consumer voice heard and making it count

Appendix 1Survey Sample

We would be very grateful if you could spare just 10 to 15 minutes of your time to complete this questionnaire so that we can build a better picture of how people in Jersey organise their finances and to what extent they find their household or personal debt to be manageable. Please be assured that all returned questionnaires will be completely confidential and the identity of any individual responses will never be disclosed to any organisation or individual, and that you will never be followed up with any sales or marketing as a result of completing this questionnaire. The completed questionnaires within the reply-paid envelopes will be returned directly to Island ARK, an independent market research company, who will only report on the depersonalised, consolidated results. The ID number below allows us to identify which recipients responded so that we do not send a reminder unnecessarily. If you choose to respond online, then please use this ID number at the head of the online questionnaire. There are 4 pages in total, but if there are any questions that you cannot or would prefer not to answer, please leave them blank and go on to the next question. Your questionnaire will still be valuable to us. Most of the questions in the survey refer to household finances so please can the most appropriate person complete the survey. When answering household questions, please answer on behalf of you, your partner and any other dependent adults or children.

Thank you very much for your help in this important survey.

6(&7,21���²�+286(+2/'�),1$1&(6�Office use

only

Q1 This questionnaire will be asking about the financial situation of your household, and therefore includes you, as well as any other adults or children living with you. Which of the following best

describes how you organise the finances within your household? (Please tick one response only) 01 { I look after the household finances, as well as the personal expenditure of all the occupants 02 { I look after the household finances, except for the personal expenditure of other occupants 03 { Someone else looks after the household finances, except for my personal expenditure 04 { I share and manage the household finances with my partner and/or others in the household 05 { Some other arrangement Q2 Which of the following would best describe the single main source of your household income? 01 { Wages / salaries 04 { Retirement income / pension 02 { Business income 05 { Government assistance other than pension (e.g. benefits) 03 { Investment income 06 { Other (please state) _______________________________ Q3 Are you and/or your partner currently contributing toward or drawing income from any of the following

to cover your household finances? (Please tick as many as apply in both boxes to the right) Currently contributing Currently drawing my/our income toward my/our income from A savings plan 01 { 01 { A work/company pension 01 { 01 {

A private pension 01 { 01 { A life assurance policy 01 { 01 { Shares or ISA’s 01 { 01 { Other financial investments 01 { 01 { Household or personal savings 01 { 01 { Q4 Do you and/or your partner currently have any of the following debts? (Tick as many as apply) An outstanding property mortgage 01 {

An overdraft on a bank account 01 { A personal loan 01 { Hire purchase agreement (e.g. for a car or household goods) 01 { Outstanding credit card debts (exclude any balances that you will pay off in full this month) 01 { Other outstanding types of loan or financing 01 { I/We have no current outstanding debts 01 {

1

021(<�0$77(56������

,'�1R��

2

3

4

18

Charitable help with money matters

6(&7,21���²�6$9,1*6�$1'�'(%7�0$1$*(0(17�Office use

only

Q5 To what extent do you agree with the following statements?

Strongly

agree Agree

Neither agree nor disagree

Disagree Strongly disagree

I am impulsive and tend to buy things even though I can’t really afford them

01{ 02{ 03{ 04{ 05{�I manage my household finances prudently and make savings for the future

01{ 02{ 03{ 04{ 05{�I am concerned that the household finances will not be sufficient to meet all commitments

01{ 02{ 03{ 04{ 05{�I feel financially secure for the future and have sufficient savings in place

01{ 02{ 03{ 04{ 05{�I am confident in managing my money and finances and feel I understand financial products

01{ 02{ 03{ 04{ 05{�It is a struggle each month to meet all of the household and family spend commitments

01{ 02{ 03{ 04{ 05{�I do not feel sufficiently knowledgeable about financial products in order to make informed decisions

01{ 02{ 03{ 04{ 05{�More education at school on personal finance, money management and debt would have been helpful

01{ 02{ 03{ 04{ 05{�

Q6 If you have savings, are they sufficient to pay for all of your expected household expenditure, including any mortgage or rent? (Please tick one response only) 01 { Yes - for just a month 03 { Yes - for up to 6 months 05 { Yes - for over a year

02 { Yes - for up to 3 months 04 { Yes - for up to a year 06 { No - I/We have no savings Q7a Which of the following best describes how long you generally plan your household budget for? 01 { Weekly 02 { Fortnightly 03 { Monthly 04 { Less frequently 05 { Don’t set a budget Q7b And how often do you generally end up sticking to the budget you set? 01 { Always 02 { Mostly 03 { Sometimes 04 { Hardly ever 05 { Never Q8 If your household had a large unexpected, exceptional cost to cover equivalent to at least one

month’s income, (e.g. a major breakdown, house repairs, a medical fee, professional fees, a vet bill, a major family event) which of the following actions do you think that would you be likely to take?

Very likely

Quite likely

Not very likely

Not at all likely

Don’t know

Rely on family/friends to help out financially 01{ 02{ 03{ 04{ 05{�Draw on general savings 01{ 02{ 03{ 04{ 05{�Pay other bills late / miss payments on other bills 01{ 02{ 03{ 04{ 05{�Use/extend a bank overdraft facility 01{ 02{ 03{ 04{ 05{�Take out an additional loan 01{ 02{ 03{ 04{ 05{�Extend a mortgage arrangement / borrow against property 01{ 02{ 03{ 04{ 05{�Rely on credit cards 01{ 02{ 03{ 04{ 05{�Sell an asset (e.g. stocks, a personal or household item) 01{ 02{ 03{ 04{ 05{�Attempt to earn additional household income 01{ 02{ 03{ 04{ 05{�Cut back on general household living expenses 01{ 02{ 03{ 04{ 05{�Cut back on less essential items (e.g. holiday, eating out) 01{ 02{ 03{ 04{ 05{� Q9a Excluding your main property mortgage and any monthly credit card repayments you will be

settling in full at the end of the month, does your household currently have any outstanding debts on any loans, overdrafts, hire purchase agreements, credit or store cards?

01 { Yes Go to Q9b below 02 { No Go to Q10 on next page Q9b Excluding your main property mortgage, how much money does your household currently owe for

any outstanding debts such as loans, overdrafts, hire purchase agreements, credit or store cards? 01 { Less than £500 05 { £10,000 to £14,999 09 { £30,000 to £39,999 13 { £70,000 to £79,999 02 { £500 to £999 06 { £15,000 to £19,999 10 { £40,000 to £49,999 14 { £80,000 to £89,999

03 { £1,000 to £4,999 07 { £20,000 to £24,999 11 { £50,000 to £59,999 15 { £90,000 to £99,999 04 { £5,000 to £9,999 08 { £25,000 to £29,999 12 { £60,000 to £69,999 16 { £100,000 or more

7a

5

6

8

9b

7b

9a

19

Making the Jersey consumer voice heard and making it count

6(&7,21���²�29(5'5$)76�$1'�/2$16�Office use

only

Q10a In the last 12 months, have you asked for or been refused a bank overdraft? 01 { Yes - have used a bank overdraft facility in the last 12 months

02 { Yes - but have been refused a bank overdraft in the last 12 months

03 { No - Have not needed/requested an overdraft in the last 12 months If No, go to Q11 Q10b Did you fully understand the interest rate and charges on the overdraft facility? 01 { Yes 02 { No Q10c In the last 12 months, have you found yourself unable to pay off an overdraft? 01 { Yes 02 { No Q10d Have you considered taking out another loan to pay off your overdraft? 01 { Yes 02 { No

Q11a In the last 12 months, have you asked for or been refused a loan? 01 { Yes - have taken out a loan in the last 12 months

02 { Yes - but have been refused a loan in the last 12 months

03 { No - Have not needed or requested a loan in the last 12 months If No, go to Q12 For Q11b to Q11f please respond on behalf of the highest loan if you have taken out more than one Q11b What was the main reason for taking out a loan? 01 { To pay off a bank overdraft 05 { To pay for fees (e.g. school fees)

02 { To pay off other outstanding debts 06 { To pay for a car or boat

03 { To pay for household utility/energy bills 07 { To pay for a holiday

04 { To pay for household appliances 08 { Other (Please specify) ____________________ Q11c Did you fully understand the interest rate and charges for the loan? 01 { Yes 02 { No Q11d What was the annual interest rate on the loan? % or 01 { Don’t know

Q11e Have you found yourself unable to fully pay off the loan installments? 01 { Yes 02 { No Q11f Have you considered taking out another loan to pay off your current loan? 01 { Yes 02 { No

Q12a Have you ever heard of or considered using a “pay day loan”? 01 { Have heard of pay day loans but would not consider using one

02 { Have heard of pay day loans and would consider using one, but haven’t used one yet Go to

03 { Have heard of pay day loans but not sure if I would use one Q13

04 { Have not heard of pay day loans

05 { Have previously applied for a pay day loan Go to Q12b Q12b Was your application for a pay day loan successful? 01 { Yes 02 { No Q12c Did you fully understand the interest rate and charges for the pay day loan? 01 { Yes 02 { No

Q12d What was the daily interest rate on the pay day loan? % or 01 { Don’t know

Q12e Have you found yourself unable to pay off the pay day loan? 01 { Yes 02 { No Q12f Have you experienced any problems with pay day lenders? 01 { Yes 02 { No Q12g If yes, please could you briefly describe the problems you experienced below: Q13 If you were unable to pay a minimum repayment for the mortgage, any loans or outstanding credit

or charge cards, what action do you think you would you take?

10a

13

12a

10d

10c

10b

11a

11f

11e

11d

11b

11c

12d

12c

12b

12f

12e

12g

20

Charitable help with money matters

Thank you for taking the time to complete this survey

Office use only

6(&7,21���²�+(/3�:,7+�021(<�0$77(56�

The questions below are to make sure our survey represents the views of all Jersey residents. Q16 What age group are you? (Please tick one response only) 01 { 16 – 24 02 { 25 – 34 03 { 35 – 44 04 { 45 – 54 05 { 55 – 64 06 { 65 or over Q17 Including yourself, how many adults and children under the age of 18 live in your household?

Number of adults: Number of children aged under 18: Q18 Are you currently? (Please tick the one option which is most appropriate to you) 01 { Employed or self-employed 04 { A homemaker (fulltime housewife/husband)

02 { Unemployed, looking for work 05 { Retired

03 { Unable to work due to long-term sickness/disability 06 { In full-time education 07 { Other (please state) ______________________________________ Q19 What type of accommodation do you live in? (Please tick one response only)

01 { Owner-occupied 06 { Staff or service accommodation

02 { States or Parish rent 07 { Lodger in private household

03 { Housing Trust rent 08 { Registered lodging house

04 { Qualified Private rent 09 { Other Non-qualified accommodation

05 { Sheltered or disabled housing

Q20 Which of the following best describes your total annual household income?

01 { Less than £20,000 04 { £40,000 - £49,999 07 { £70,000 - £79,999 02 { £20,000 - £29,999 05 { £50,000 - £59,999 08 { £80,000 - £99,999 03 { £30,000 - £39,999 06 { £60,000 - £69,999 09 { £100,000 or more

Office use only

14

18

15

20

16

19

17a

Q14 Which of the following organisations have you ever heard of or used with regard to providing advice

and help on financial and money matters? (Please tick one response only for Have heard Have heard of Have not each organisation shown below) of and used but not used heard of The Consumer Council 01{� 02{� 03{ Community Savings 01{� 02{� 03{ The Citizens Advice Bureau 01{� 02{� 03{ Jersey Financial Services Commission (JFSC) 01{� 02{� 03{ Q15 If you were to experience financial hardship, how likely would you be to seek advice or support

from the following?

Very likely

Quite likely

Not very likely

Not at all likely

Don’t know

The Consumer Council 01{ 02{ 03{ 04{ 05{�Community Savings 01{ 02{ 03{ 04{ 05{�The Citizens Advice Bureau 01{ 02{ 03{ 04{ 05{�The Jersey Financial Services Commission (JFSC) 01{ 02{ 03{ 04{ 05{�Your own bank 01{ 02{ 03{ 04{ 05{�Another bank or finance company 01{ 02{ 03{ 04{ 05{�A pay day loan company 01{ 02{ 03{ 04{ 05{�Family 01{ 02{ 03{ 04{ 05{�Friends 01{ 02{ 03{ 04{ 05{�Other (Please specify)______________________ 01{ 02{ 03{ 04{ 05{�

6(&7,21���²�$%287�<28�

17b

21

Making the Jersey consumer voice heard and making it count

Appendix 2Cash Only Challenge Report

�

ϭ��

�

³&$6+�21/<�&+$//(1*(´�5(68/76��%XGJHW��%XGJHW��%XGJHW��

�

7KH�&KDOOHQJH�

'XULQJ�1RYHPEHU�HLJKW�YROXQWHHUV�WRRN�XS�WKH�&RPPXQLW\�6DYLQJV�³&DVK�2QO\�&KDOOHQJH´�WR�H[SHULHQFH�OLIH�XVLQJ�FDVK�RQO\�IRU�D�ZHHN�IRU�WKHLU�HYHU\GD\�H[SHQVHV��2XU�YROXQWHHUV�DOO�KDG�GLIIHUHQW�OLIHVW\OHV�DQG�FLUFXPVWDQFHV�DQG�DOO�ZRUN�IRU�RUJDQLVDWLRQV�ZLWK�ZKRP�&RPPXQLW\�6DYLQJV�KDV�D�ZRUNLQJ�UHODWLRQVKLS���

7KH�YROXQWHHUV�ZHUH�DOO�DVNHG�WR�GR�ZKDW�WKH\�QRUPDOO\�GR�GXULQJ�D�ZHHN�DQG�HDFK�ZDV�DVNHG�WR�GUDZ�RXW�IURP�WKHLU�EDQN�D�OXPS�VXP�LQ�FDVK�HTXDWLQJ�WR�����RI�ZKDW�WKH\�ZRXOG�QRUPDOO\�H[SHFW�WR�VSHQG�DQG�WR�PDQDJH�RQ�WKDW���6WDQGLQJ�RUGHUV�DQG�GLUHFW�GHELWV�ZHUH�QRW�WR�EH�LQFOXGHG�EXW�DOO�RWKHU�H[SHQGLWXUH�RQ�LWHPV�VXFK�DV�IRRG��OXQFKHV�FRIIHHV��VWDPSV��QHZVSDSHUV��FORWKLQJ��ODXQGU\��SHWV��VFKRRO�OXQFKHV��WUDQVSRUW�DQG�VSRUWLQJ�DFWLYLWLHV�ZHUH�WR�FRXQW��

)RU�HDFK�RI�WKH�YROXQWHHUV�OLIH�ZLWK�QR�FDUGV�WR�VZLSH�DW�ZLOO��QR�EDQN�DFFRXQW�WR�XVH�DQG�QR�DFFHVV�WR�RQOLQH�VKRSSLQJ�ZDV�JRLQJ�WR�UHYHDO�VRPH�LQWHUHVWLQJ�H[SHULHQFHV��

:K\�GR�LW"�

&RPPXQLW\�6DYLQJV�LV�D�FKDULW\�WKDW�RIIHUV�DFFRXQW�IDFLOLWLHV�DQG�D�PHDQV�RI�VDYLQJ�DQG�ERUURZLQJ�DQG�EXGJHWLQJ�DGYLFH�WR�WKRVH�ZKR��IRU�ZKDWHYHU�UHDVRQ��GR�QRW�ILQG�LW�HDV\�WR�DFFHVV�PDLQVWUHDP�EDQNLQJ�VHUYLFHV�RU�ZKR�DUH�VWUXJJOLQJ�WR�PDQDJH�WKHLU�ILQDQFHV���7KHUH�DUH�VRPH�IRU�ZKRP�OLYLQJ�OLIH�RQ�D�³FDVK�RQO\´�EDVLV�LV�D�UHDOLW\��7KH�³&DVK�2QO\�&KDOOHQJH´�ZDV�ODXQFKHG�WR�UDLVH�DZDUHQHVV�RI�WKH�GLIILFXOWLHV�IDFHG�LQ�WKHVH�FLUFXPVWDQFHV�DQG�WKH�LPSRUWDQFH�RI�EXGJHWLQJ��

6R�KRZ�GLG�WKH�YROXQWHHUV�IHHO�DW�WKH�EHJLQQLQJ�RI�WKH�ZHHN"�

2Q�'D\�2QH��1LQD��PRWKHU�RI�WZR�DQG�D�WHDFKHU�FRPPHQWHG�³7KH�SURVSHFW�RI�XVLQJ�FDVK�ZDV�GDXQWLQJ��,�QHYHU�FDUU\�FDVK��(YHU\WKLQJ�JRHV�RQ�FDUG�DQG�,�GRQ¶W�VHH�WKH�PRQH\��,�GR�D�ORW�RI�RQOLQH�VKRSSLQJ�DQG�WKH�WKRXJKW�RI�QRW�KDYLQJ�WKDW�RSWLRQ�LV�VFDU\�´�

,Q�FRQWUDVW�)UDQFLV��D�VHQLRU�SROLF\�DGYLVHU�DQG�IDWKHU�RI�WZR��IHOW�³FDOP�DQG�FRQILGHQW��:K\�GRHV�HYHU\RQH�VHHP�WR�WKLQN�P\�FRQILGHQFH�LV�PLVSODFHG"´��

%HWK��D�FKDULW\�RIILFHU��WKRXJKW�KHU�FDVK�OXPS�VXP�³ORRNV�OLNH�D�ORW�RI�PRQH\�DQG�,�ZRXOG�EH�GLVDSSRLQWHG�LI�,�VSHQW�LW�DOO´��

0HODQLH��&RPPXQLW\�6DYLQJV�'HYHORSPHQW�2IILFHU�DQG�WKH�PRWKHU�RI�WZR�DGXOW�FKLOGUHQ��³IHOW�YHU\�ZDU\�DV�WR�KRZ�P\�ZHHN�ZRXOG�ZRUN�RXW´���

22

Charitable help with money matters

�

Ϯ��

&ODLUH��D�PDUNHWLQJ�SURIHVVLRQDO�VDLG�³,�VWDUWHG�RII�WKH�ZHHN��ZRUULHG�WKDW�,�ZRXOGQ¶W�VXUYLYH�RQ�FDVK�RQO\��DV�,�DP�WRWDOO\�UHOLDQW�RQ�P\�GHELW�FDUG��EXW�WKHQ�,�UHPHPEHUHG�WKRVH�KDOORZ�GD\V�DW�XQLYHUVLW\�JHWWLQJ�WKURXJK�WKH�GD\�RQ����±�DQG�,�NQHZ�LW�ZRXOG�EH�SRVVLEOH´��

�

$V�WKH�ZHHN�ZHQW�RQ�PRVW�RI�WKH�YROXQWHHUV�IRXQG�WKH�SUHVVXUH�ULVLQJ�«�

5RVH��D�ODZ\HU�DQG�&KDLUPDQ�RI�-HUVH\¶V�&RQVXPHU�&RXQFLO��FRPPHQWHG�³$W�WLPHV�,�IRXQG�LW�UHDOO\�GLIILFXOW�WR�UHPHPEHU�WKDW�XVLQJ�P\�GHELW�FDUG�ZDV�QRW�DQ�RSWLRQ�´�

0HDQZKLOH�'DYLG��D�UHWDLOHU��DQG�IRUPHUO\�3UHVLGHQW�RI�WKH�-HUVH\�&KDPEHU�RI�&RPPHUFH��VSHQW�D�OXPS�VXP�RQ�WKH�ZHHNO\�VKRS�DW�WKH�EHJLQQLQJ�RI�WKH�ZHHN�DQG�FRQFOXGHG�³WKH�GDPDJH�WKLV�KDG�GRQH�RQO\�EHFDPH�DSSDUHQW�DW�WKH�HQG�RI�WKH�ZHHN�ZKHQ�ZH�IRXQG�RXUVHOYHV�FRPLQJ�XS�VKRUW�´�

)RU�%HWK�6DWXUGD\��³��LV�127�JRRG��«��,�JR�WR�WKH�&KULVWPDV�)D\UH�DW�WKH�WRZQ�KDOO�EXW�KDYH�QR�IXQGV�WR�VSHQG��,�DVN�IRU�VRPH�LWHPV�WR�EH�SXW�DVLGH�VR�,�FDQ�SD\�WKH�IROORZLQJ�ZHHN��,�UHWXUQ�KRPH�IRU�D�QLJKW�LQ�WR�VDYH�IXQGV�´�

7RE\��D�MRXUQDOLVW��UHDOLVHG�WKDW��DOWKRXJK�PDQDJLQJ��͞LW�ZDV�DOVR�REYLRXV�WKDW�DQ\�VXUSULVH�FRVWV�ZRXOG�PDNH�SD\PHQW�WULFN\��RU��SXW�SUHVVXUH�RQ�WKH�DPRXQW�VHW�DVLGH�IRU�WKH�ZHHN�´�

%RWK�1LQD�DQG�0HODQLH�IRXQG�VXSHUPDUNHW�VKRSSLQJ�YHU\�UHVWULFWLYH��³)RU�WKH�ILUVW�WLPH�LQ�\HDUV�,�GLGQ¶W�HQMR\�WKH�VKRSSLQJ�WULS��,�ZHQW�LQ�ZLWK�D�OLVW�RI�H[DFWO\�ZKDW�,�QHHGHG�DQG�VWXFN�WR�LW´�ZDV�1LQD¶V�YLHZ�ZKLOVW�0HODQLH�WRR�MXVW�ERXJKW�H[DFWO\�ZKDW�VKH�QHHGHG�DQG�³GLGQ¶W�ORRN�DW�DQ\WKLQJ�HOVH�EHFDXVH�,�GLGQ¶W�NQRZ�KRZ�PXFK�PRQH\�,�PLJKW�QHHG�WLOO�WKH�HQG�RI�WKH�ZHHN�´�

�

6R�ZKDW�SDUWLFXODU�H[SHULHQFHV�GLG�RXU�YROXQWHHUV�KDYH"�

L��7KH�LPSDFW�RI�WKH�FRVW�RI�IRRG�VKRSSLQJ�ZDV�WKH�QXPEHU�RQH�LVVXH�WKDW�VL[�YROXQWHHUV�FRPPHQWHG�RQ��$SDUW�IURP�1LQD�DQG�0HODQLH¶V�FRPPHQWV�DERYH�5RVH�³WULHG�WR�UHGXFH�WKH�DPRXQW�,�QRUPDOO\�VSHQG�RQ�IRRG��7KLV�ZDV�GLIILFXOW��,W�GLG�PHDQ�WKDW�,�ZDV�FDUHIXO�QRW�WR�EX\�WRR�PXFK�DQG�NHSW�DZD\�IURP�06�´�

�'XULQJ�WKH�ZHHN�%HWK�KDG�IULHQGV�IRU�GLQQHU�DQG�³:KHQ�WKH�FDVKLHU�LV�SXWWLQJ�HYHU\WKLQJ�WKURXJK�,�ZRUU\�,�ZRQ¶W�KDYH�HQRXJK�DQG�,�PD\�KDYH�WR�JLYH�VRPHWKLQJ�EDFN��/XFNLO\�P\�PHQWDO�DULWKPHWLF�KDV�EHHQ�FRUUHFW�DQG�ZLWK�P\�KDOI�SULFH�FKLFNHQ�,�OHDYH�ZLWK�MXVW����LQ�P\�ZDOOHW�´��

LL��7KH�DELOLW\�WR�VDYH�PRQH\�FRXOG�EH�DIIHFWHG��:LWK�UHJDUGV�IRRG�1LQD�VDLG�³,W�ZDV�IUXVWUDWLQJ�WKDW�,�ZDVQ¶W�DEOH�WR�EXON�EX\«���,WV�IUXVWUDWLQJ�ZKHQ�WKHUH�DUH�GHDOV�RQ�DQG�ZLWK�D�IDPLO\�,�OLNH�WR�EX\�DKHDG�´�DQG�VKH�IRXQG�WRR�WKDW�KHU�FKLOGUHQ¶V�VZLPPLQJ�OHVVRQV�ZHUH�³FKHDSHU�WR�SD\�PRQWKO\�E\�''�DQG�WKDW�PHDQV�KDYLQJ�D�EDQN�DFFRXQW´���

LLL��6RPH�WKLQJV�\RX�FDQQRW�GR�ZLWKRXW�D�GHELW�FDUG�RU�D�EDQN�DFFRXQW��1HLWKHU�RI�WKH�VSRUWV�FOXEV�DWWHQGHG�E\�1LQD¶V�WZR�FKLOGUHQ�ZRXOG�DFFHSW�IHHV�LQ�FDVK�DQG�)UDQFLV�IRXQG�KLPVHOI�KDYLQJ�WR�XVH�KLV�GHELW�FDUG�WR�SD\�IRU�D�FDU�SDUN��³'XH�WR�WRGD\¶V�UXVK��,�SDUNHG�FORVHVW�WR�P\�ZRUN�QRW�UHDOLVLQJ�WKDW�WKH�FDUN�SDUN�WKDW�LV�WKH�FORVHVW�FDU�SDUN�WR�P\�ZRUN�GRHV�QRW�WDNH�FDVK�DQG�VR�,�KDG�WR�XVH�P\�FDUG�´���LY��)RUJHWWLQJ�\RXU�PRQH\�LV�WLPH�FRQVXPLQJ�DV�%HWK�GLVFRYHUHG��³,�KDYH�WR�VWRS�DW�VKRSV�IRU�HVVHQWLDOV�

23

Making the Jersey consumer voice heard and making it count

�

ϯ��

DQG�PDQDJH�WR�OHDYH�P\�FDVK�DW�KRPH��,�IDFH�WKH�HPEDUUDVVPHQW�DQG�WLPH�ZDVWHG�RI�JRLQJ�EDFN�KRPH�VR�VKDPHIXOO\�SURGXFH�P\�FDUG�WR�SD\���������

Y��/LYLQJ�ZLWK�OXPS�VXPV�RI�FDVK�RQO\�LV�D�ZKROH�GLIIHUHQW�PLQGVHW���³/LYLQJ�RQ�D�ZHHNO\�FDVK�EXGJHW�LV�YHU\�GLIIHUHQW�WR�PDQDJLQJ�ZLWK�D�PRQWKO\�LQFRPH�SDLG�LQWR�D�EDQN�DFFRXQW��<RX�GR�QRW�KDYH�WKH�PHQWDO�VDIHW\�QHW�RI�EXGJHWLQJ�RYHU�D�ORQJHU�SHULRG�DQG�VR�WKH�IRFXV�RQ�\RXU�VSHQGLQJ�LV�FRQVWDQWO\�PRUH�LQWHQVH´�QRWHG�0HODQLH����

YL���+RZ�PXFK�FDVK�GR�\RX�QHHG�WR�FDUU\�ZLWK�\RX"�6HFXULW\�LV�DQ�LVVXH�DV�%HWK�GLVFRYHUHG��³�:DONLQJ�DURXQG�ZLWK�ORWV�RI�FDVK�LQ�\RXU�ZDOOHW�LV�VOLJKWO\�ZRUU\LQJ��HLWKHU�\RX�IRUJHW�\RXU�ZDOOHW�DW�KRPH�RU�\RX�ULVN�ORVLQJ�\RXU�FDVK�VR�,�GHFLGH�WR�VSOLW�P\�FDVK�LQWR�VPDOOHU�VL]HV´��+RZHYHU��\RX�WKHQ�QHHG�WR�EH�DEOH�WR�EXGJHW�DFFXUDWHO\�DV�WR�KRZ�PXFK�\RX�ZLOO�QHHG�HYHU\�GD\�DQG�WKDW�LV�QRW�HDV\���

�YLL��&UHGLW�FDUGV�DQG�GHELW�FDUGV�SURYLGH�ZHOFRPH�IOH[LELOLW\�DQG�PDNH�OLIH�HDVLHU��2XU�YROXQWHHUV�DSSHDUHG�WR�PLVV�WKH�DELOLW\�WR�XVH�WKHLU�GHELW�FDUGV�PRUH�WKDQ�WKHLU�FUHGLW�FDUGV��7KLV�DSSHDUHG�WR�EH�EHFDXVH�GHELW�FDUGV�WHQG�WR�JHW�XVHG�PRUH�IRU�SXUFKDVHV�LQYROYLQJ�VPDOO�VXPV�DQG�IRU�³�QLSSLQJ�WR�WKH�KROH�LQ�WKH�ZDOO´�WR�JHW�D�ELW�PRUH�PRQH\�RXW�ZKHQ�\RX�UXQ�RXW�RI�FDVK�ZKHUHDV�FUHGLW�FDUGV�SD\�IRU�WKH�ELJJHU�RU�XQH[SHFWHG�LWHPV���%HWK�FDOFXODWHG�WKDW�³,�ZRXOG�KDYH�XVHG�P\�FDUG�RYHU����WLPHV�WKURXJKRXW�WKH�ZHHN�KDG�,�QRW�KDG�WKH�FDVK�RQ�PH�DQG�SUREDEO\�PRUH�LI�,�KDG�QRW�EHHQ�VR�FRQVFLRXV�RI�VWLFNLQJ�WR�D�EXGJHW�´��

0HDQZKLOH�'DYLG�IRXQG�WKDW�³D�ELJ�KROH�KDG�EHHQ�SXW�LQWR�RXU�VWDVK�RI�FDVK´�DW�WKH�EHJLQQLQJ�RI�WKH�ZHHN�DIWHU�D�IRRG�VKRS�DQG�)UDQFLV�QRWHG��͞LI�\RX�DUH�RQO\�OLYLQJ�RQ�FDVK�DQG�KDYH�QR�DFFHVV�WR�FUHGLW��XQH[SHFWHG�HYHQWV�FDQ�FDXVH�UHDO�SUREOHPV�´��YLLL��&UHGLW�DQG�GHELW�FDUGV�FDUGV�FDQ�DOVR�PDNH�OLIH�PRUH�H[SHQVLYH�DV�%HWK�DQG�)UDQFLV�ERWK�UHDOLVHG�GXULQJ�WKH�ZHHN��

%HWK��IRU�H[DPSOH��ZDV�H[SRVHG�WR�WHPSWDWLRQ�DW�D�VWRUH¶V�IXQGUDLVLQJ�HYHQW�DQG�GHVFULEHV�KRZ�³�,�ZLOO�EH�VXUURXQGHG�ZLWK�WKH�WUDSSLQJV�RI�FRQVXPHULVP�DQG�WHPSWDWLRQV�RI�����GLVFRXQW�DQG�SRVVLEO\�PRUH�LI�\RX�ZLQ�D�SUL]H��/XFNLO\�,�UHVLVW�DQG�RQO\�VSHQG�D�OLWWOH�RQ�VRPH�VQDFNV�IRU�GLQQHU�´��0HDQZKLOH�)UDQFLV�UHDOLVHG��³,W�LV�YHU\�HDV\�WR�XVH�\RXU�FDUG�WR�SD\�IRU�WKLQJV�KHUH�DQG�WKHUH�DQG�EHIRUH�\RX�NQRZ�LW�\RX�KDYH�DFWXDOO\�VSHQW�TXLWH�D�ORW�RI�PRQH\´�����

YLLL��6SHQGLQJ�VPDOO�XQQHFHVVDU\�DPRXQWV�VRRQ�PRXQWV�XS��&ODLUH�WULHG�WR�EH�GLVFLSOLQHG��³7KURXJKRXW�WKH�ZHHN�,�ZDV�FDUHIXO�VR�DV�WR�QRW�VSHQG�WKRVH�IHZ�VQHDN\�SRXQGV�LQ�WKH�FRUQHU�VKRS�RU�WKH�FR�RS��ZKLFK�\RX�GRQ¶W�WKLQN�DERXW�ZKLOVW�XVLQJ�D�GHELW�FDUG´�ZKLOVW�1LQD�UHDOLVHG�KRZ�PXFK�³RI�P\�LQFRPH�JRHV�RQ�UXEELVK�OLNH�FDQV�RI�GULQN�DQG�VQDFNV�WKDW�,�GRQ¶W�QHHG�´��

2Q�WKH�SRVLWLYH�VLGH��7KH�YROXQWHHUV�WKRXJKW�IDU�PRUH�EHIRUH�VSHQGLQJ�WKHLU�PRQH\�DQG�WKH\�UHDOLVHG�KRZ�PXFK�WKH\�SRWHQWLDOO\�ZDVWHG��

)UDQFLV�QRWHG�WKDW�³8VLQJ�FDVK�LV�D�XVHIXO�ZD\�WR�NHHS�WUDFN�RI�\RXU�PRQH\�DQG�GRHV�HQFRXUDJH�PRUH�GLVFLSOLQH�LQ�\RXU�VSHQGLQJ´���

24

Charitable help with money matters

�

ϰ��

)RU�1LQD�³,W�PDGH�PH�UHDOLVH�KRZ�TXLFNO\�,�FDQ�VSHQG�����D�GD\�RQ�UXEELVK�WKDW�,�GRQ¶W�QHHG��6HHLQJ�LW�LQ�P\�SXUVH�PDGH�PH�PRUH�IUXJDO�DQG�,�WKRXJKW�WZLFH�DERXW�QHHGLQJ�VRPHWKLQJ�´���

)RU�5RVH�³7KH�PRVW�GLIILFXOW�WKLQJ�ZDV�PDNLQJ�VXUH�,�GLGQW�EX\�WRR�PDQ\�VPDOO�&KULVWPDV�WUHH�GHFRUDWLRQV�´��

7RE\�VXUYLYHG�WKH�&KDOOHQJH�EHVW�EXW�KLV�DSSURDFK�GHPRQVWUDWHV�WKH�LPSRUWDQFH�RI�WKH�EXGJHWLQJ�OHVVRQ��³$V�ORQJ�DV�,�NQHZ�URXJKO\�ZKDW�,�ZRXOG�QHHG�PRQH\�IRU�LW�VHHPHG�PDQDJHDEOH�´��

�

6R�GLG�WKH�YROXQWHHUV�PDQDJH�RQ�WKH�PRQH\�WKH\�KDG�RU�ZLWKRXW�XVLQJ�WKHLU�FDUGV�RU�RQOLQH�IDFLOLWLHV"�

7RE\�DQG�&ODLUH�GLG��ZLWK�7RE\�KDYLQJ�WKH�PRVW�VXFFHVVIXO�ZHHN���'HVSLWH�WU\LQJ�WR�PDQDJH�RQ�WKHLU�EXGJHWV�DOO�WKH�RWKHU�YROXQWHHUV�IRXQG�WKHPVHOYHV�KDYLQJ�WR�XVH�WKHLU�GHELW�RU�FUHGLW�FDUGV�RQFH�RU�WZLFH�GXULQJ�WKH�ZHHN�WR�FRYHU�DQ�HYHQW�WKDW�WKH\�KDG�QRW�H[SHFWHG�RU�DOORZHG�IRU��7KH�UXOHV�DOORZHG�SDUWLFLSDQWV�WR�XVH�WKHLU�FDUGV�LI�DQ�HPHUJHQF\�DURVH�EXW�WKH�LQWHUHVWLQJ�UHVXOW�ZDV�WKDW�HYHQ�ZLWK�JRRG�LQWHQWLRQV��RQO\�7RE\�DQG�&ODLUH�PDQDJHG�ZLWKLQ�WKHLU�SHUVRQDO�OLPLWV���

�$�WULS�WR�WKH�YHW��XQDFFRXQWHG�IRU�FKLOG�FDUH�H[SHQVHV��SXWWLQJ�WRR�PXFK�SHWURO�LQ�WKH�FDU��D�EXVLQHVV�WULS���D�ERDW�IDUH��PHPEHUVKLS�WKDW�QHHGHG�UHQHZDO�WR�JHW�D�GLVFRXQW��D�QHFHVVDU\�RQOLQH�SXUFKDVH�DQG�VSRUWV�IHHV�ZHUH�DOO�UHDVRQV�JLYHQ��7ZR�YROXQWHHUV�DOVR�QDUURZO\�HVFDSHG�KDYLQJ�WR�SD\�FDU�UHSDLU�ELOOV�WKDW�ZRXOG�KDYH�WDNHQ�WKHP�RYHU�WKHLU�OLPLWV��

�

&RQFOXVLRQV��

,Q�DGGLWLRQ�WR�WKH�H[SHULHQFHV�TXRWHG�DERYH�ZLWKRXW�H[FHSWLRQ�DOO�WKH�YROXQWHHUV�FRPPHQWHG�RQ���

L�� KRZ�LPSRUWDQW�LW�LV�WR�EXGJHW�LI�RQH�LV�WR�PDQDJH�RQH¶V�PRQH\�WR�WKH�EHVW�DGYDQWDJH�DQG�QRW�ZDVWH�LW�XQQHFHVVDULO\���

LL�� RI�KRZ�VWUHVVIXO�OLIH�ZRXOG�EH�LI�\RX�GLG�QRW�KDYH�WKH�IOH[LELOLW\�RI�EHLQJ�DEOH�WR�XVH�D�GHELW�RU�FUHGLW�FDUG�LI�\RX�ZDQWHG�RU�QHHGHG�WR���DQG�KRZ�VXFK�VWUHVV�FRXOG�HDVLO\�GDPDJH�UHODWLRQVKLSV����

LLL�� KRZ�YLWDO�LW�LV�WR�NHHS�VRPH�PRQH\�LQ�UHVHUYH�IURP�\RXU�EXGJHW�IRU�WKRVH�XQH[SHFWHG�SD\PHQWV��

�

7KHUH��ZHUH�DOVR�VRPH�SHUFHSWLYH�DQG�WKRXJKW�SURYRNLQJ�FRPPHQWV�PDGH�DERXW�WKH�ZD\�RXU�VRFLHW\�QRZ�RSHUDWHV��

�� +DYLQJ�WR�WKLQN�DERXW�PRQH\�DOO�WKH�WLPH�ZRXOG�HDVLO\�EHFRPH�WLULQJ�DQG�VWUHVVIXO��(YHQ�ZKHQ�\RX�KDYH�D�UHDVRQDEOH�DPRXQW�RI�PRQH\�LQ�\RXU�SRFNHW��WKHUH�LV�VWLOO�D�WKRXJKW�LQ�WKH�EDFN�RI�\RXU�PLQG�±�ZKDW�LI�,�VSHQG�WRR�PXFK�DQG�QHHG�PRQH\�ODWHU�RQ"�<RX�HQG�XS�QRW�EHLQJ�DEOH�WR�OLYH�LQ�WKH�PRPHQW�EXW��DOZD\V�ZRUU\LQJ�DERXW�ZKDW�PLJKW�EH�DURXQG�WKH�FRUQHU���)UDQFLV���

25

Making the Jersey consumer voice heard and making it count

�

ϱ��

�� ,�GLG�IHHO�WKRXJK�WKDW�WKH�ODFN�RI�FDVK�PDNHV�\RX�IHHO�YHU\�FRQVWUDLQHG��$�VHQVH�WKDW�\RX�DUH�H[LVWLQJ�UDWKHU�WKDQ�OLYLQJ���'DYLG���

�� 7KLV�ZHHN�UHDOO\�ZRXOG�KDYH�EHHQ�LPSRVVLEOH�DQG�D�JUHDW�VWUXJJOH�KDG�,�KDG�VXFK�D�OLPLWHG�EXGJHW�DQG�QR�RWKHU�PHDQV�WR�SD\�WKDQ�FDVK��«��,W�LV�VRFLDOO\�DFFHSWHG�WKDW�ZH�DOO�KDYH�EDQN�D�F¶V�DQG�EDQN�FDUGV�VR�IRU�WKRVH�ZKR�GRQ¶W�ZH�KDYH�PDGH�RXU�VRFLHW\�DQG�WUDQVDFWLRQV�PRUH�LVRODWLQJ�IRU�WKRVH�ZKR�GR�QRW�DFFHVV�WR�IXQGV�LQ�WKH�VDPH�PDQQHU���%HWK���

�� *RLQJ�RXW�IRU�WHD�ZLWK�IULHQGV�ZDV�HPEDUUDVVLQJ��,�KDG�WR�EX\�D�VHQVLEOH�WHD�DQG�SD\�IRU�H[DFWO\�ZKDW�,�KDG�FRQVXPHG�ZLWK�FDVK��7KLV�ZDV�RN�IRU�WKH�ZHHN�RQ�WKH�FKDOOHQJH�EXW�,�WKLQN�LW�ZRXOG�WDNH�VRPH�YHU\�XQGHUVWDQGLQJ�IULHQGV�ORQJ�WHUP�WR�NHHS�GRLQJ�WKLV��7KHUH�ZDV�QR�URRP�IRU�WLSV�DQG�VSOLWWLQJ�WKH�ELOO�HTXDOO\�ZKLFK�ZH�DOZD\V�GR���1LQD���

�� 7KH�SODVWLF�FDUGV�ZH�VR�RIWHQ�WDNH�IRU�JUDQWHG�DOORZ�IOH[LELOLW\�DQG�IUHHGRP�ZLWK�IXQGV��$QG��ZKLOH�,¶P�VXUH�WKH�JDUDJH�ZRXOG�KDYH�DFFRPPRGDWHG�PH�KDG�,�QRW�EHHQ�DEOH�WR�SD\�RQ�WKH�VSRW��WKH�ZKROH�SURFHVV�ZRXOG�VXUHO\�KDYH�EHHQ�PXFK�PRUH�RI�D�EXUGHQ���7RE\�����,�IHOW�OLNH�WKHUH�ZDV�D�VKDGRZ�ZDWFKLQJ�RYHU�PH�DQG�HYHU\WKLQJ�,�VSHQW�±�,�GLG�QRW�IHHO�OLNH�PH�EHFDXVH�,�ZDV�IHHOLQJ�XQVXUH�DQG�LQVHFXUH�DERXW�P\�ILQDQFLDO�VWDWH�PRVW�RI�WKH�WLPH´��0HODQLH���

�� +RZHYHU��HYHQ�LI�\RX�DUH�FDUHIXO�ZLWK�\RXU�PRQH\��NQRZLQJ�WKDW�\RX�FDQ�XVH�EDQNLQJ�IDFLOLWLHV�JLYHV�\RX�D�SHDFH�RI�PLQG�WKDW�\RX�GR�QRW�KDYH�ZKHQ�\RX�DUH�DOZD\V�ZRUU\LQJ�DERXW�ZKHWKHU�\RX�ZLOO�KDYH�HQRXJK�PRQH\�WR�ODVW�WKH�ZHHN���)UDQFLV���

�� ,�IRXQG�WKH�ZHHN�GLIILFXOW�DW�WLPHV�EHFDXVH�,�GLGQ¶W�KDYH�WKH�XVXDO�FRQYHQLHQFH�RI�KDYLQJ�P\�FDUG��,�FDQ�QRZ�XQGHUVWDQG�KRZ�GLIILFXOW�LW�PXVW�EH�IRU�WKRVH�ZKR�VWUXJJOH�RU�DUH�XQDEOH�WR�JHW�EDQN�DFFRXQWV�DQG�GHELW�FUHGLW�FDUGV���&ODLUH���

�� ,�IRXQG�WKH�ZKROH�H[SHULHQFH�TXLWH�VREHULQJ�DV�LW�GRHV�PDNH�\RX�ZRQGHU�KRZ�\RX�FDQ�NHHS�SHRSOH�ZKR�ILQG�WKHPVHOYHV�LQ�VXFK�GLIILFXOW�FLUFXPVWDQFHV�PRWLYDWHG�WR�DFKLHYH�VRPHWKLQJ�EHWWHU�LQ�OLIH��:LWK�VR�OLWWOH�PRQH\�LW�ZRXOG�EH�YHU\�HDV\�WR�EHFRPH�VRFLDOO\�H[FOXGHG��\RXU�RQO\�IULHQG�EHLQJ�D�UDGLR�RU�79����&RPPXQLW\�6DYLQJV�FOHDUO\�IXOILOV�D�UHDO�QHHG�LQ�RXU�VRFLHW\���,�ZRXOG�WKRXJK�EH�LQWHUHVWHG�WR�KHDU�ZKDW�WKH�QH[W�VWHS�ZDV�IRU�WKRVH�ZKR�ILQG�WKHPVHOYHV�LQ�WKLV�OHYHO�RI�GLIILFXOW\��+DYLQJ�HQRXJK�FDVK�LQ�\RXU�SRFNHW�LV�RQH�WKLQJ��UHLQWHJUDWLQJ�\RXUVHOI�LQWR�VRFLHW\�DQG�EHFRPLQJ�YDOXHG�LV�DQRWKHU���'DYLG���

6R�ZKDW�QH[W"��

6WXDUW�6WDEOHV��([HFXWLYH�2IILFHU�DW�&RPPXQLW\�6DYLQJV�ILUVW�RI�DOO�JDYH�D�KXJH�³7KDQN�<RX´�WR�DOO�WKH�YROXQWHHUV�ZKR�DJUHHG�WR�XQGHUWDNH�WKH�³&DVK�2QO\�&KDOOHQJH�´��

³$V�ZHOO�DV�UDLVLQJ�DZDUHQHVV�RI�WKH�GLIILFXOWLHV�IDFHG�E\�WKRVH�ZKR�GR�QRW�KDYH�HDV\�DFFHVV�WR�PDLQVWUHDP�EDQNLQJ�VHUYLFHV��RXU��YROXQWHHUV¶�H[SHULHQFHV�KDYH�UDLVHG�DZDUHQHVV�RI�VRPH�YDOXDEOH�VRFLDO�TXHVWLRQV�ZKLFK�ZH�VKRXOG�DOO�JLYH�WKRXJKW�WRR´�FRPPHQWV�6WXDUW���

7KH�&KDOOHQJH�UHVXOWV�DOVR�HPSKDVLVHG�WKH�IOH[LELOLW\�RIIHUHG�E\�WKH�DELOLW\�WR�XVH�D�GHELW�RU�FUHGLW�FDUG��7KLV�UHVXOW�VHHPV�WR�EH�ERUQH�RXW�E\�WKH�IROORZLQJ�FRPPHQW�IURP�&ROLQ�0DFOHRG��&KLHI�([HFXWLYH�2IILFHU�

26

Charitable help with money matters

�

ϲ��

RI�WKH�&R�RSHUDWLYH�6RFLHW\�LQ�-HUVH\��DQG�D�GLUHFWRU�RI�&RPPXQLW\�6DYLQJV�/WG���ZKR�DGYLVHV�WKDW�DSSUR[LPDWHO\�����RI�VDOHV�WKURXJKRXW�WKH�FRPSDQ\¶V�VWRUHV�DUH�SDLG�XVLQJ�GHELW�RU�FUHGLW�FDUGV���

³$OWKRXJK�VRPH�RI�RXU�YROXQWHHUV�H[SHULHQFHV�PD\�VHHP�REYLRXV�,�VXJJHVW�WKDW�IRU�PDQ\�WU\LQJ�WKH�&KDOOHQJH�IRU�WKHPVHOYHV�ZRXOG�SURYH�D�ORW�KDUGHU�WKDQ�WKH\�PLJKW�WKLQN´�DGGHG�6WXDUW��³/HDUQLQJ�WR�EXGJHW�DQG�WKH�LPSRUWDQFH�RI�DOZD\V�VDYLQJ�VRPH�PRQH\�IRU�HPHUJHQFLHV�DUH�WZR�NH\�PHVVDJHV�WKDW�&RPPXQLW\�6DYLQJV�LV�DOZD\V�NHHQ�WR�SDVV�RQ�DQG�WKHVH�UHVXOWV�FOHDUO\�VXSSRUW�WKHVH�REMHFWLYHV´��

&XVWRPHUV�RI�&RPPXQLW\�6DYLQJV�DUH�RIIHUHG�EXGJHWLQJ�VXSSRUW�DQG�DOO�DUH�UHTXLUHG�WR�VDYH�D�PLQLPXP�RI����SHU�PRQWK�LQ�WKHLU�DFFRXQWV���

$QRWKHU�LQLWLDWLYH�IRU�ZKLFK�&RPPXQLW\�6DYLQJV�KDV�MXVW�EHHQ�DZDUGHG�D�%DUFOD\V�&RPPXQLW\�$ZDUG��LV�WKHLU�0RQH\�0DQDJHPHQW�SURJUDPPH��7KLV�SURJUDPPH�KDV�EHHQ�GHVLJQHG�IRU�GHOLYHU\�LQ�VFKRROV�DQG�ZLWK�RWKHU�DJHQFLHV�ZKHUH�SHRSOH��SDUWLFXODUO\�\RXQJ�SHRSOH��PLJKW�EHQHILW�IURP�OHDUQLQJ�VRPH��EDVLF�PRQH\�PDQDJHPHQW�VNLOOV�WR�KHOS�WKHP�UXQ�WKHLU�OLYHV��HLWKHU�QRZ�RU�LQ�WKH�IXWXUH��

�³2XU�&KDOOHQJH�UHVXOWV�DSSHDU�WR�IXOO\�VXSSRUW�WKH�YDOXH�RI�WKH�SURJUDPPH´�VD\V�0HODQLH��³�:H�VKRXOG�QRW�IRUJHW�WKDW�PDQ\�RI�XV�FDQ�UHPHPEHU�WKH�GD\V�ZKHQ�GHELW�DQG�FUHGLW�FDUGV�ZHUH�QRW�FRPPRQ�VR�SHRSOH�ZHUH�XVHG�WR�PDQDJLQJ�RQ�FDVK���+RZHYHU��QRZDGD\V�WKH�RSSRVLWH�LV�WUXH�DQG�IRU�PDQ\�OLYLQJ�ZLWK�RQOLQH�VKRSSLQJ��VWRUH�FDUGV��FUHGLW�DQG�GHELW�FDUGV�LV�WKH�QRUP��%XW�LW�LV�VR�LPSRUWDQW�WR�XQGHUVWDQG�WKDW�EXGJHWLQJ�UHPDLQV�D�YLWDO�VNLOO�LI�\RX�DUH�QRW�WR�OHW�\RXU�VSHQGLQJ�UXQ�DZD\�ZLWK�\RX´��

7KURXJK�WKH�VHUYLFHV�LW�RIIHUV�&RPPXQLW\�6DYLQJV�DOUHDG\�VXSSRUWV�PDQ\�ZKR�PLJKW�RWKHUZLVH�EHFRPH�VRFLDOO\�LVRODWHG���7KH�FKDULW\�DOVR�ZRUNV�ZLWK�PDQ\�RWKHU�FKDULWLHV�DQG�6WDWHV�GHSDUWPHQWV�DV�ZHOO�DV�RUJDQLVDWLRQV�VXFK�DV�WKH�&RQVXPHU�&RXQFLO��WKH�&LWL]HQV�$GYLFH�%XUHDX�DQG��PRUH�UHFHQWO\��WKH�-HUVH\�)LQDQFLDO�6HUYLFHV�&RPPLVVLRQ��WR�LQFUHDVH�SHRSOH¶V�DZDUHQHVV�RI�WKH�QHHG�WR�PDQDJH�WKHLU�LQFRPH�FDUHIXOO\�DQG�WR�VDYH�DV�PXFK�DV�WKH\�FDQ��

�³+RZHYHU´�VD\V�6WXDUW��³WKHUH�LV�DOZD\V�PRUH�WR�EH�GRQH�DQG�&RPPXQLW\�6DYLQJV�ZLOO�FRQWLQXH�WR�GHYHORS�RXU�RZQ�OLQNV�ZLWK�RWKHU�DJHQFLHV�DQG�WKH�,VODQG¶V�SROLF\�PDNHUV�WR�DGGUHVV�VRPH�RI�WKH�LVVXHV�UDLVHG��+RZHYHU��,�KRSH�RWKHUV�LQ�WXUQ�ZLOO�OHDUQ�IURP�WKHVH�UHVXOWV�DQG�WDNH�IRUZDUG�WKHLU�RZQ�SURJUDPPHV�WR�HQVXUH�WKDW�PRQH\�PDQDJHPHQW�VNLOOV�DUH�WDXJKW�DW�DOO�DJHV�DQG�WKRVH�ZKR�DUH�VWUXJJOLQJ�ILQDQFLDOO\�DUH�QRW�OHIW�WR�IHHO�RU�EHFRPH�LVRODWHG�´��

�

'DWH�������WK�'HFHPEHU������

�����������������������������������������������������������������������

�

&RQWDFW�GHWDLOV�

2IILFH���� � &RPPXQLW\�6DYLQJV��6HDOH�6WUHHW��6W�+HOLHU��-(���4*�

(PDLO����� � RIILFH�#FRPPXQLW\VDYLQJV�RUJ�MH�

7HO��� �������������������� � :HEVLWH��������ZZZ�FRPPXQLW\VDYLQJV�RUJ�MH��

�

27

Making the Jersey consumer voice heard and making it count

Appendix 3‘Karen’ and ‘Richard’ a debt case study

Debt clients are often portrayed as single parents living in social housing and totally dependent on benefits for their income. Whilst this is often the case and it is always a struggle to make ends meet in the middle for these clients, it is not unusual for us to see people who are accustomed to a good income and lifestyle. A sudden change occurs in their lives such as ill health, relationship breakdown or loss of employment and then they too can find themselves sinking quickly into debt.

Karen and Richard are two such clients and Karen tells of just how miserable it feels to be in this situation. ‘It seemed that we had everything going for us – good jobs, two healthy children, nice home and enough money to buy all that we needed. Credit facilities were readily available for us - we had a family car on HP, as well as laptops for the children to use for homework and we had taken advantage of the low interest rates to take out a loan to clear two of the out- standing credit card balances. This left us with one credit card and a couple of store cards but we always managed to meet their minimum required payments and all was seemingly under control’.

Then disaster struck – Richard’s job became more and more stressful and this seriously affected his health. He finally resigned and for a short time was out of work before finding employment in a very different area with- out the pressure to meet targets, but also with a large drop in salary.

‘At first, we managed to make ends meet by using

the credit and storecards for everyday shopping so that there was enough money to pay the rent and utility bills as well as maintaining the HP and loan repayments. Then the interest started adding up and the payments increased. We used our agreed overdraft to its limit and beyond with all the subsequent interest and charges and eventually returned items. By this time the credit and store cards were ‘maxed out’. We were constantly arguing and this in turn began to affect the children despite our efforts to keep the debt problems out of their hearing. Then the endless letters from creditors demanding immediate payment started to arrive followed by countless calls from the creditors – these were at all times of the day and throughout the evening and many were aggressive and frightening.

We became too scared to open the letters and left the phone to go to answer phone to avoid speaking to our creditors. We felt unable to talk to our friends about our financial problems, and had become isolated from them. We were also too ashamed and embarrassed to discuss our situation with our families. Richard’s health was once again suffering, our relationship was under threat and when there was not enough money to pay the rent, we could see no way out of our situation.’

It was at this point that Karen and Richard were advised by their bank to come to the Citizens Advice Bureau for debt advice. After the initial interview, they were given a ‘debt pack’ to complete in which they had to detail all their

28

Charitable help with money matters

income and outgoings, as well as a list of their creditors, and an appointment was made with a debt adviser. Based on the debt pack, an income and expenditure statement was drawn up and this showed that with careful budgeting there was some money left each month to repay the debts. As the first step towards gaining control over their money Karen and Richard were asked to destroy all their credit and store cards and were also asked not to take out any further credit.

The priority was to keep the roof over the family’s head and the adviser negotiated with the landlord to repay the shortfall over a short period. Then an allowance was made to keep up with the HP agreements which were all due to be paid off within the year, and reduced payments were negotiated with the loan company. A small payment was offered to each of the credit and store cards and now that their outgoings were reduced, the overdraft began to reduce and Karen and Richard felt that they have regained control over their money. Their credit rating has taken a knock and they will have to be careful over their spending, but when the rent is up-to-date and the HP payments finished, they should be able to start work on clearing their other debts until they eventually become debt free.

Karen and Richard both agreed that it had been a great relief just to talk about their debt problems in complete confidence and, whilst the problem hadn’t gone away, the stress and worry was greatly reduced and they realised that at last, with the support of the debt adviser, there was light at the end of the tunnel.

From the Jersey Citizens Advice Bureau

29

Making the Jersey consumer voice heard and making it count

Appendix 4Bad Debt Ghosts

i. Bad debts: can lead to Petty Debts Court Judgements and Arrests on Wages which will be implemented as and when you have any earnings

ii. Any outstanding income tax will remain against your name and be deducted from future earnings

iii. Rental Deposits: If you default on the repayment of a loan for a rental deposit from Income Support you may well be ineligible for a future deposit loan.

iv. Banks may freeze your account or refuse to open an account for you if you have failed to pay into an overdraft.

v. Agencies are likely to check your credit history and if you have a bad credit history it may inhibit your ability to open an account; obtain a loan et)

vi. Banks may not offer you a bank account if you have a bad credit history.

30

Charitable help with money matters

Appendix 5Budget Planner

Where does your money go?

Knowing where and how you spend money can help you save. This can help you pay for unexpected bills and plan for occasions like holidays and Christmas.

To create your Home Budget Planner, gather all the paperwork that you need. For example, electricity; phone and gas bills; grocery receipts; bank/credit card statements and all other spending receipts.

To make this budget planner work, you must work out your total bills, spending, and income either weekly or monthly values and stick to your chosen format throughout the exercise.

Here are two guides on how to work out your budget:

Calculating Monthly What to do

Monthly bills Enter amount in ‘monthly’ column

Quarterly bills (e.g. telephone) ÷ 4

Yearly bills (e.g. Christmas) ÷ 12

Weekly bills (e.g. mobile phone) x 52 then ÷ 12

Calculating Weekly What to do

Weekly bills Enter amount in ‘weekly’ column

Quarterly bills (e.g. telephone) ÷ 13

Yearly bills (e.g. Christmas) ÷ 52

Weekly bills (e.g. mobile phone) x 12 then ÷ 52

Home Budget PlannerThis planner is available in an interactive version at www.jerseyconsumercouncil.org.je

31

Making the Jersey consumer voice heard and making it count

How much do you spend?

Step by step instructions to work out how much you spend.

1. To help you budget, the typical household spend is divided into seven sections.

2. Place your weekly or monthly spend for each item in the box that applies to you.

3. Add up the items in each section and place the totals in the Total box. You should have seven totals at the end of the exercise.

4. Place all seven totals beside the section they apply to in the Spending box.

At different times of the year, you will need to pay annual expenses: e.g. Christmas; summer holidays; an MOT or a rates bill. Write down the bill amount in the yearly column. To work out how much this annual bill is each week or month, divide the annual amount by either 52 for a weekly or by 12 for a monthly total. You will need to put this into your weekly/monthly budget.

5. Add all your totals together to give you an overall total weekly or monthly spend.

Household Bills Each Week Each Month Each Year

Rent/Mortgage/Secured Loan

Electricity

Heating Oil/Gas

Water

TV Licence

Building insurance

Contents insurance

Rates

Other

Total Household

Financial Each Week Each Month Each Year

Car loan/Hire purchase

Credit card

Catalogue/Mail order

Store card

Loan repayments

Life assurance

Pension contribution

University/Collage fees

Savings

Other

Total Financial

1

2

32

Charitable help with money matters

Food/Clothes Each Week Each Month Each Year

Fruit/Vegetables

Bread

Meat

Other groceries

School lunches

Work lunches

Clothes/Shoes/Uniforms

Other

Total Food and Clothes

Other Bills Each Week Each Month Each Year

Telephone

Mobile phone

Home repairs, cleaner, gardener etc

Satellite TV

Child maintenance/Nursery

Vet bills

Computer/Internet

Other

Total Other Bills

Travel Each Week Each Month Each Year

Child Bus/Taxi

Adult Bus/Taxi

Road Tax

Parking

Car insurance

Petrol/Diesel

Car servicing and MOT

Car Wash

Other

Total Travel

3

4

5

33

Making the Jersey consumer voice heard and making it count

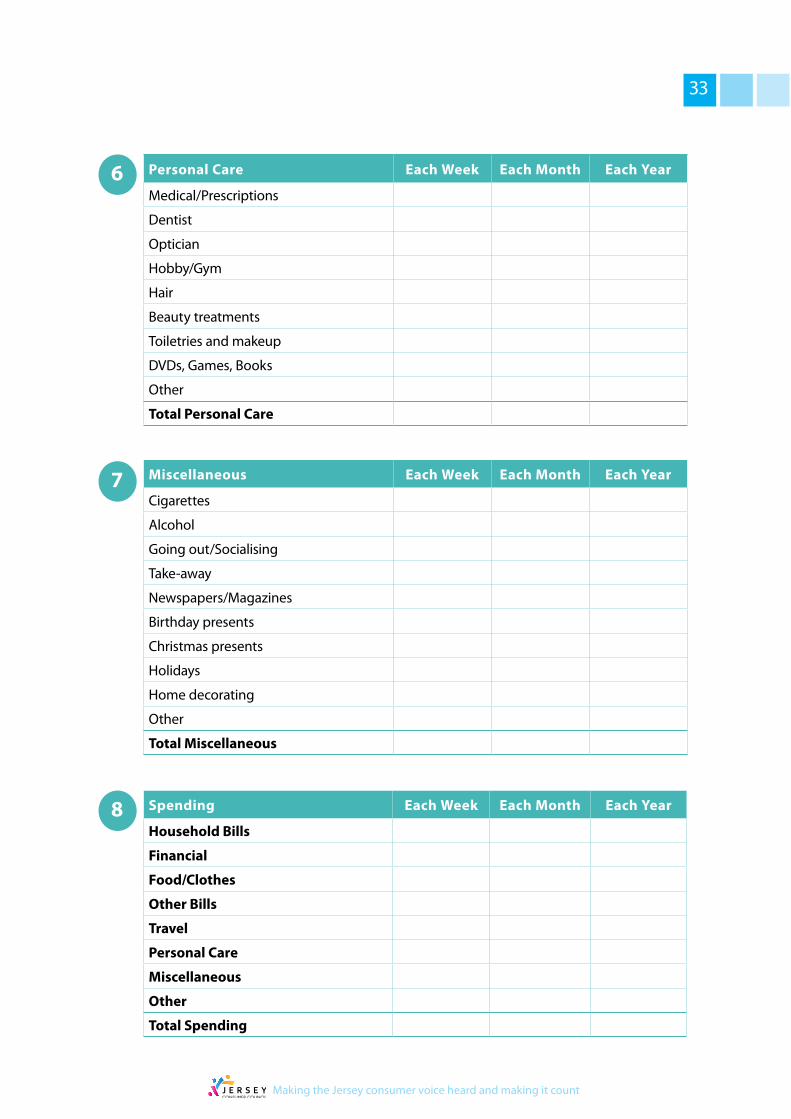

Personal Care Each Week Each Month Each Year

Medical/Prescriptions

Dentist

Optician

Hobby/Gym

Hair

Beauty treatments

Toiletries and makeup

DVDs, Games, Books

Other

Total Personal Care

Miscellaneous Each Week Each Month Each Year

Cigarettes

Alcohol

Going out/Socialising

Take-away

Newspapers/Magazines

Birthday presents

Christmas presents

Holidays

Home decorating

Other

Total Miscellaneous

Spending Each Week Each Month Each Year

Household Bills

Financial

Food/Clothes

Other Bills

Travel

Personal Care

Miscellaneous

Other

Total Spending

6

7

8

34

Charitable help with money matters

Income Each Week Each Month Each Year

Wages/Salary (you/partner and/or other)

States Benefits

Pension

Maintenance/Child Support/Alimony

Contributions from people living with you

Student loan

Other

Total Income

35

Making the Jersey consumer voice heard and making it count

To download a copy of this Budget Planner visit: www.jerseyconsumercouncil.org.je

Overall budget

1. Place your total weekly or monthly income in the total income box below.

2. Place your total weekly or monthly spend in the total spend box below.

3. To find out how much money you have left at the end of each week or month, take your total spending amount away from your total income amount and place it in the Total Left Box.

Totals Each Week Each Month Each Year

Total Income

Total Spending - (minus)

Total Left

You may find that you are spending more than you have coming in. Look carefully at your spending, is there anything you can cut down on? Are there cheaper items available? Try keeping all your receipts (e.g. for one week) this will help you see where you are spending your money.

If you feel you are struggling to make ends meet and need help, please contact a money advisor at one of the following organisations:-

Citizens Advice Bureau 0800 735 0249Community Savings 01534 737 555

36

Charitable help with money matters

Appendix 6About Us

Jersey Consumer Council was established by an Act of the States of Jersey in 1995. It highlights and researches a broad range of subjects to help consumers to make informed purchasing decisions; the Council conducts research to quantify public opinion; raises consumer issues with decision and policy makers; participates in consultations to ensure that the consumer voice is heard and encourages good trading practice.

Community Savings Ltd was established in 2002 to offer account facilities, budgeting and mentoring support and, where appropriate, small loans and emergency funding to those individuals who , for various reasons, cannot access mainstream banking facilities or gain access to emergency funding or support to manage their finances. One of the charity’s objectives is to run awareness campaigns focussing on Money Management and financial literacy issues. The ‘Money Management’ programme is designed to make individuals think about how they feel about money and react to consumer advertising, branding and special offers and the importance of planning (and sticking to) a budget and saving.

Jersey Consumer Council • Liberation Place • St Helier • JE1 1BBTelephone: 01534 611161 • Email: [email protected]

www.jerseyconsumercouncil.org.je

https://twitter.com/@jerseyconsumer

https://www.facebook.com/pages/Jersey-Consumer-Council/523388024389196 http://www.facebook.com/jerseyfuelwatch

Community Savings Ltd • Seale Street • St Helier • JE2 3QGTelephone: 01534 737 555 • Email: [email protected]

www.communitysavings.org.je