Embed Size (px)

Citation preview

© 2014 – Cerved Group Spa – Tutti i diritti riservati – Riproduzione vietata

September 2014

Monitor of Bankruptcies, Insolvency Proceedings and Business Closures

Second Quarter 2014

2 © 2014 – Cerved Group Spa – All rights reserved – Reproduction prohibited

Secondo gli archivi di Cerved, nel terzo trimestre del

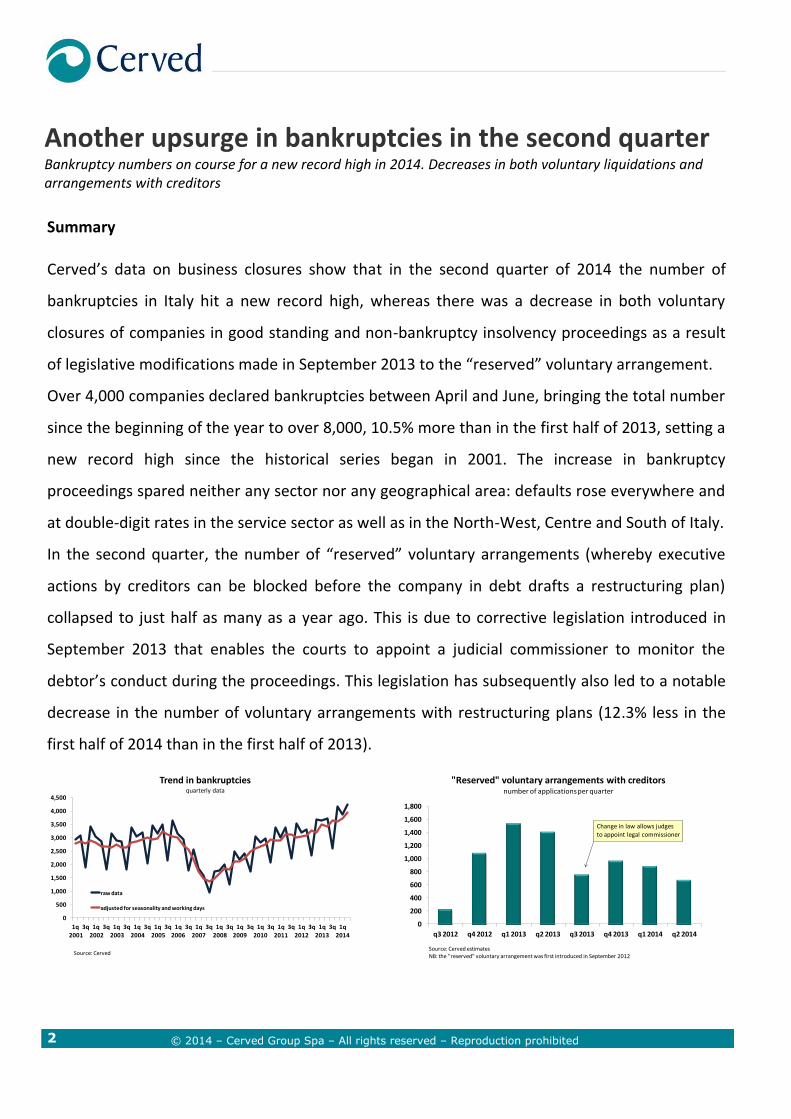

Summary Cerved’s data on business closures show that in the second quarter of 2014 the number of

bankruptcies in Italy hit a new record high, whereas there was a decrease in both voluntary

closures of companies in good standing and non-bankruptcy insolvency proceedings as a result

of legislative modifications made in September 2013 to the “reserved” voluntary arrangement.

Over 4,000 companies declared bankruptcies between April and June, bringing the total number

since the beginning of the year to over 8,000, 10.5% more than in the first half of 2013, setting a

new record high since the historical series began in 2001. The increase in bankruptcy

proceedings spared neither any sector nor any geographical area: defaults rose everywhere and

at double-digit rates in the service sector as well as in the North-West, Centre and South of Italy.

In the second quarter, the number of “reserved” voluntary arrangements (whereby executive

actions by creditors can be blocked before the company in debt drafts a restructuring plan)

collapsed to just half as many as a year ago. This is due to corrective legislation introduced in

September 2013 that enables the courts to appoint a judicial commissioner to monitor the

debtor’s conduct during the proceedings. This legislation has subsequently also led to a notable

decrease in the number of voluntary arrangements with restructuring plans (12.3% less in the

first half of 2014 than in the first half of 2013).

Another upsurge in bankruptcies in the second quarter

Bankruptcy numbers on course for a new record high in 2014. Decreases in both voluntary liquidations and arrangements with creditors

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1q2001

3q 1q2002

3q 1q2003

3q 1q2004

3q 1q2005

3q 1q 2006

3q 1q 2007

3q 1q2008

3q 1q 2009

3q 1q 2010

3q 1q 2011

3q 1q 2012

3q 1q 2013

3q 1q 2014

Trend in bankruptciesquarterly data

raw data

adjusted for seasonality and working days

Source: Cerved

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

q3 2012 q4 2012 q1 2013 q2 2013 q3 2013 q4 2013 q1 2014 q2 2014

"Reserved" voluntary arrangements with creditorsnumber of applications per quarter

Source: Cerved estimatesNB: the "reserved" voluntary arrangement was first introduced in September 2012

Change in law allows judges to appoint legal commissioner

3 © 2014 – Cerved Group Spa – All rights reserved – Reproduction prohibited

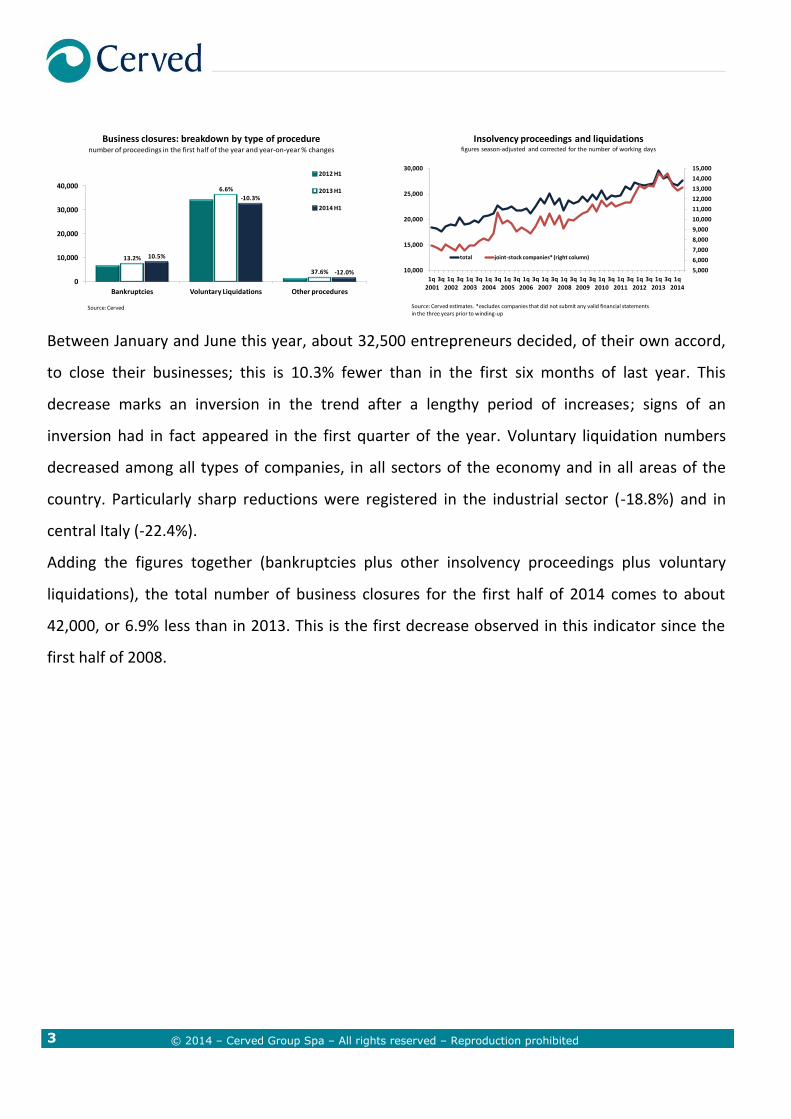

Between January and June this year, about 32,500 entrepreneurs decided, of their own accord,

to close their businesses; this is 10.3% fewer than in the first six months of last year. This

decrease marks an inversion in the trend after a lengthy period of increases; signs of an

inversion had in fact appeared in the first quarter of the year. Voluntary liquidation numbers

decreased among all types of companies, in all sectors of the economy and in all areas of the

country. Particularly sharp reductions were registered in the industrial sector (-18.8%) and in

central Italy (-22.4%).

Adding the figures together (bankruptcies plus other insolvency proceedings plus voluntary

liquidations), the total number of business closures for the first half of 2014 comes to about

42,000, or 6.9% less than in 2013. This is the first decrease observed in this indicator since the

first half of 2008.

13.2%

6.6%

37.6%

10.5%

-10.3%

-12.0%

0

10,000

20,000

30,000

40,000

Bankruptcies Voluntary Liquidations Other procedures

Business closures: breakdown by type of procedurenumber of proceedings in the first half of the year and year-on-year % changes

2012 H1

2013 H1

2014 H1

Source: Cerved

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

10,000

15,000

20,000

25,000

30,000

1q2001

3q 1q2002

3q 1q2003

3q 1q2004

3q 1q2005

3q 1q 2006

3q 1q 2007

3q 1q2008

3q 1q 2009

3q 1q 2010

3q 1q 2011

3q 1q 2012

3q 1q2013

3q 1q 2014

Insolvency proceedings and liquidationsfigures season-adjusted and corrected for the number of working days

total joint-stock companies* (right column)

Source: Cerved estimates. *excludes companies that did not submit any valid financial statementsin the three years prior to winding-up

4 © 2014 – Cerved Group Spa – All rights reserved – Reproduction prohibited

Bankruptcies

Bankruptcy numbers have not stopped

climbing: between April and June, over 4,000

Italian businesses began bankruptcy

proceedings. Having slowed down in the

previous quarter, bankruptcies resumed

double-digit growth (+14.3%), bringing the total

in the first six months of 2014 to over 8,000, up

10.5% from 2013 and the most ever since 2001.

The biggest increase in bankruptcies was

among joint-stock companies, which accounted

for three-fourths of the total. In the first half of

2014, there was a 12.9% increase in

bankruptcies among these companies to over

6,000. Increases were smaller among

partnerships (+5.9%) and businesses of other

legal status (+1.8%).

By macro-sector, the sharpest rise in

bankruptcies was in the service sector

(+15.7%), even faster than the 14.5% growth

seen in the first half of 2013. Bankruptcy

procedure numbers also continued to rise,

although at slower paces, in construction and in

manufacturing: there was an 8.2% increase

among building companies (vs. +12.8% in the

first half of 2013) and a 4.5% increase among

manufacturing companies (vs. +10.5%).

The January-June increase in bankruptcies was

also common to every part of the Boot, and at

double-digit rates everywhere except in the

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1q2001

3q 1q2002

3q 1q2003

3q 1q2004

3q 1q2005

3q 1q 2006

3q 1q 2007

3q 1q2008

3q 1q 2009

3q 1q 2010

3q 1q 2011

3q 1q 2012

3q 1q 2013

3q 1q 2014

Trend in bankruptciesquarterly data

raw data

adjusted for seasonality and working days

Source: Cerved

12.9%

12.8%

10.5%

14.5%

1.2%

8.2%

4.5%

15.7%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

others construction industrial service

Bankruptcies by macro-sector in the first halfnumber of proceedings and year-on-year percent changes

2012 H1

2013 H1

2014 H1

Source: Cerved

14.9%

12.9%

13.5%1.8%

12.9%

5.9%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

other forms joint-stock companies partnerships

Bankruptcies in 1H: breakdown by legal statusnumber of proceedings and year-on-year percent changes

2012 H1

2013 H1

2014 H1

Source: Cerved

5 © 2014 – Cerved Group Spa – All rights reserved – Reproduction prohibited

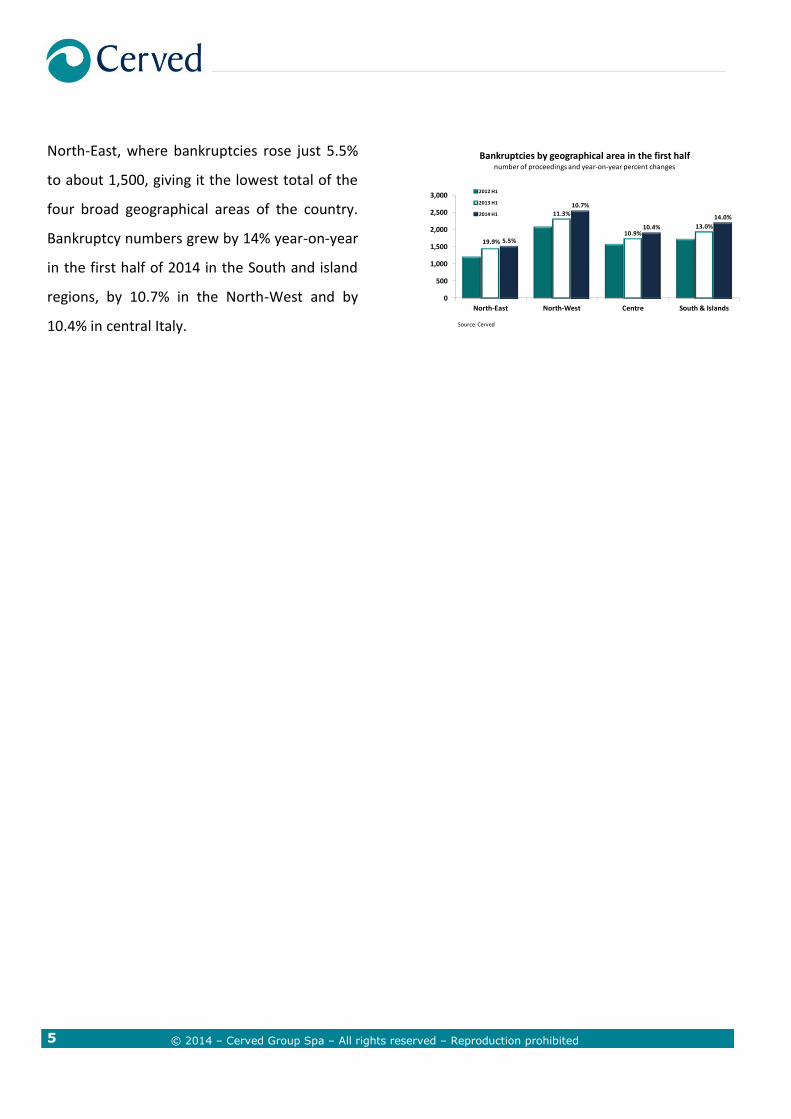

North-East, where bankruptcies rose just 5.5%

to about 1,500, giving it the lowest total of the

four broad geographical areas of the country.

Bankruptcy numbers grew by 14% year-on-year

in the first half of 2014 in the South and island

regions, by 10.7% in the North-West and by

10.4% in central Italy.

19.9%

11.3%

10.9%13.0%

5.5%

10.7%

10.4%

14.0%

0

500

1,000

1,500

2,000

2,500

3,000

North-East North-West Centre South & Islands

Bankruptcies by geographical area in the first halfnumber of proceedings and year-on-year percent changes

2012 H1

2013 H1

2014 H1

Source: Cerved

6 © 2013 – Cerved Group Spa – All rights reserved – Reproduction prohibited

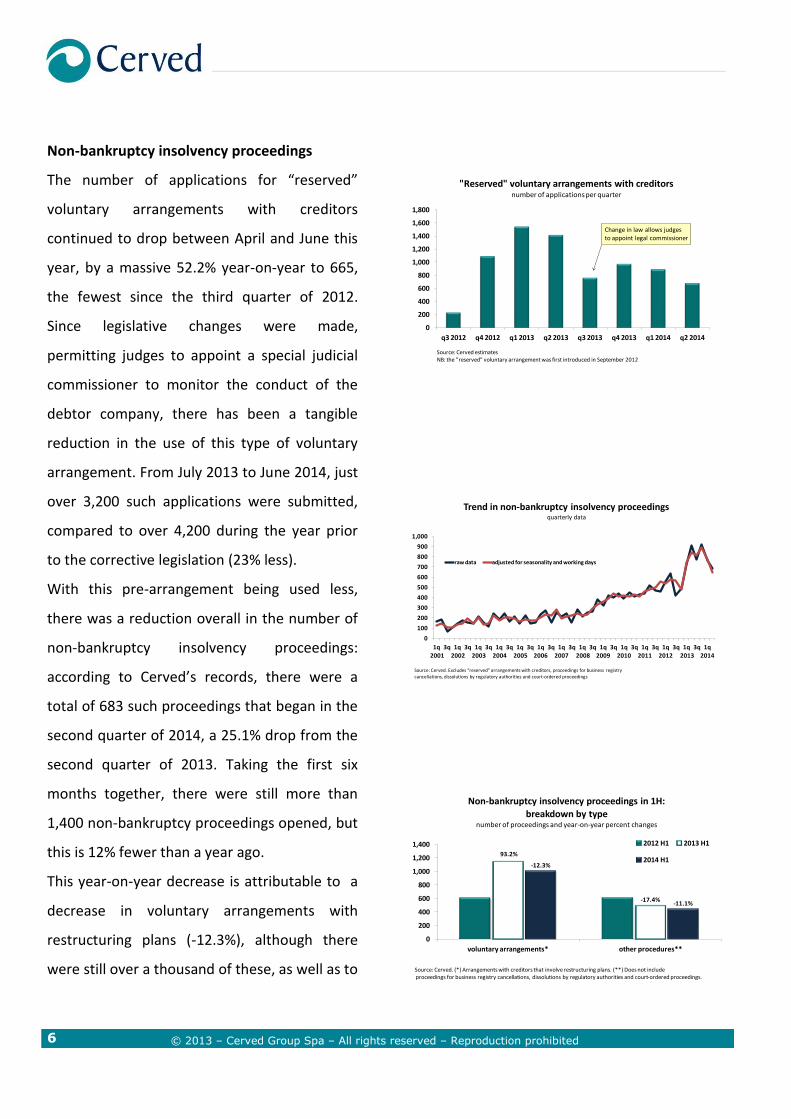

Non-bankruptcy insolvency proceedings

The number of applications for “reserved”

voluntary arrangements with creditors

continued to drop between April and June this

year, by a massive 52.2% year-on-year to 665,

the fewest since the third quarter of 2012.

Since legislative changes were made,

permitting judges to appoint a special judicial

commissioner to monitor the conduct of the

debtor company, there has been a tangible

reduction in the use of this type of voluntary

arrangement. From July 2013 to June 2014, just

over 3,200 such applications were submitted,

compared to over 4,200 during the year prior

to the corrective legislation (23% less).

With this pre-arrangement being used less,

there was a reduction overall in the number of

non-bankruptcy insolvency proceedings:

according to Cerved’s records, there were a

total of 683 such proceedings that began in the

second quarter of 2014, a 25.1% drop from the

second quarter of 2013. Taking the first six

months together, there were still more than

1,400 non-bankruptcy proceedings opened, but

this is 12% fewer than a year ago.

This year-on-year decrease is attributable to a

decrease in voluntary arrangements with

restructuring plans (-12.3%), although there

were still over a thousand of these, as well as to

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

q3 2012 q4 2012 q1 2013 q2 2013 q3 2013 q4 2013 q1 2014 q2 2014

"Reserved" voluntary arrangements with creditorsnumber of applications per quarter

Source: Cerved estimatesNB: the "reserved" voluntary arrangement was first introduced in September 2012

Change in law allows judges to appoint legal commissioner

0

100

200

300

400

500

600

700

800

900

1,000

1q2001

3q 1q2002

3q 1q2003

3q 1q2004

3q 1q2005

3q 1q 2006

3q 1q 2007

3q 1q2008

3q 1q 2009

3q 1q 2010

3q 1q 2011

3q 1q 2012

3q 1q2013

3q 1q 2014

Trend in non-bankruptcy insolvency proceedingsquarterly data

raw data adjusted for seasonality and working days

Source: Cerved. Excludes "reserved" arrangements with creditors, proceedings for business registrycancellations, dissolutions by regulatory authorities and court-ordered proceedings

93.2%

-17.4%

-12.3%

-11.1%

0

200

400

600

800

1,000

1,200

1,400

voluntary arrangements* other procedures**

Non-bankruptcy insolvency proceedings in 1H:

breakdown by typenumber of proceedings and year-on-year percent changes

2012 H1 2013 H1

2014 H1

Source: Cerved. (*) Arrangements with creditors that involve restructuring plans. (**) Does not includeproceedings for business registry cancellations, dissolutions by regulatory authorities and court-ordered proceedings.

7 © 2013 – Cerved Group Spa – All rights reserved – Reproduction prohibited

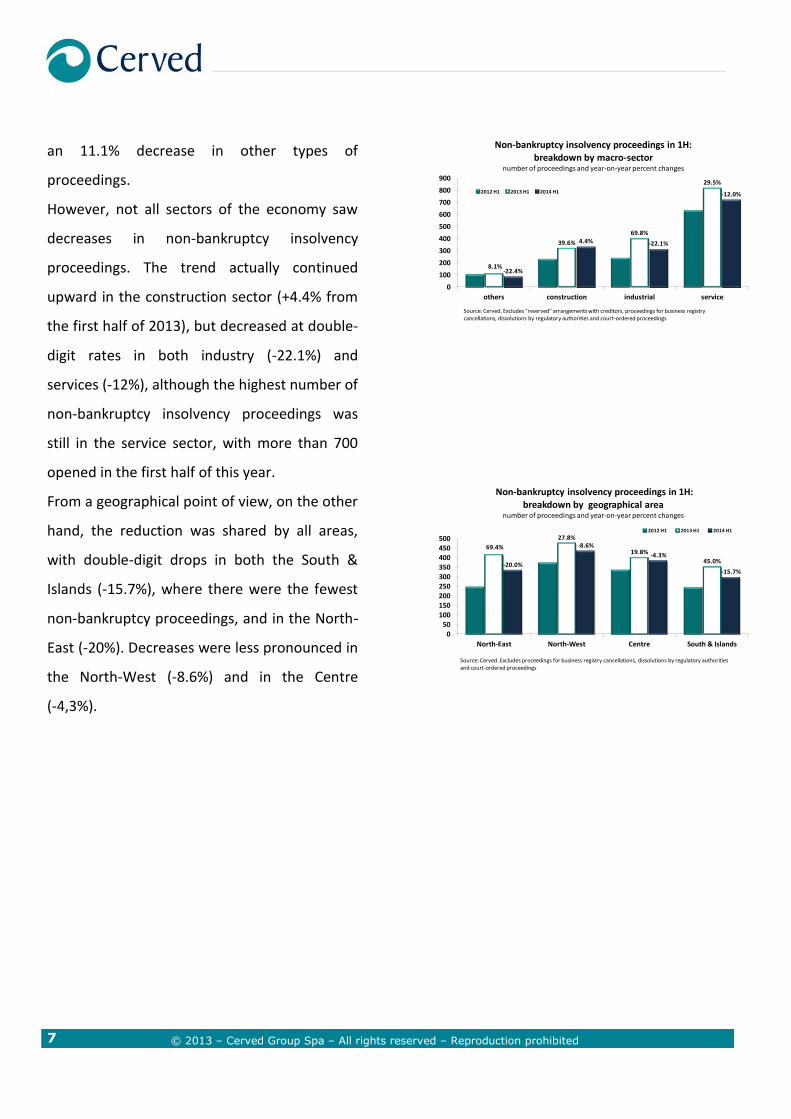

an 11.1% decrease in other types of

proceedings.

However, not all sectors of the economy saw

decreases in non-bankruptcy insolvency

proceedings. The trend actually continued

upward in the construction sector (+4.4% from

the first half of 2013), but decreased at double-

digit rates in both industry (-22.1%) and

services (-12%), although the highest number of

non-bankruptcy insolvency proceedings was

still in the service sector, with more than 700

opened in the first half of this year.

From a geographical point of view, on the other

hand, the reduction was shared by all areas,

with double-digit drops in both the South &

Islands (-15.7%), where there were the fewest

non-bankruptcy proceedings, and in the North-

East (-20%). Decreases were less pronounced in

the North-West (-8.6%) and in the Centre

(-4,3%).

8.1%

39.6%

69.8%

29.5%

-22.4%

4.4% -22.1%

-12.0%

0

100

200

300

400

500

600

700

800

900

others construction industrial service

Non-bankruptcy insolvency proceedings in 1H:

breakdown by macro-sectornumber of proceedings and year-on-year percent changes

2012 H1 2013 H1 2014 H1

Source: Cerved. Excludes "reserved" arrangements with creditors, proceedings for business registrycancellations, dissolutions by regulatory authorities and court-ordered proceedings

69.4%

27.8%

19.8%

45.0%-20.0%

-8.6%

-4.3%

-15.7%

050

100150200250300350400450500

North-East North-West Centre South & Islands

Non-bankruptcy insolvency proceedings in 1H:

breakdown by geographical areanumber of proceedings and year-on-year percent changes

2012 H1 2013 H1 2014 H1

Source: Cerved. Excludes proceedings for business registry cancellations, dissolutions by regulatory authoritiesand court-ordered proceedings

8 © 2013 – Cerved Group Spa – All rights reserved – Reproduction prohibited

Voluntary liquidations

It is estimated1 that about 16,000

entrepreneurs began liquidation proceedings of

their own accord between April and June 2014;

this figure is 3.3% less than in the same period

of 2013. This decrease marks an inversion in

the trend on a six-month basis: after rising for

several years, the number of voluntary

liquidations fell by 10.3% year-on-year in the

first six months of 2014 to about 32,500.

Liquidation numbers went down among all

types of companies: the biggest decrease was

among “truly active” joint-stock companies

(-14.1%), while there was a 7.8% drop in

voluntary liquidations of partnerships and a

2.2% drop among “dormant” companies, that

is, those that had not submitted financial

statements in any of the three years prior to

winding up.

Considering only non-dormant companies,

voluntary liquidations decreased across all

sectors and all geographical areas. The

reduction was in double-digit territory in the

industrial sector (-18.8%) and in the service

sector (-13.9%); the latter is still the macro-

1 Due to delays in Chamber of Commerce database updates,

liquidation figures are estimated for the most recent quarter and then corrected and updated to show the actual number in the subsequent Monitor report. The actual first quarter 2014 number of about 17,000 is lower than the estimate of 19,000 provided in the previous edition of this Monitor.

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

10,000

15,000

20,000

25,000

30,000

1q2001

3q 1q2002

3q 1q2003

3q 1q2004

3q 1q2005

3q 1q 2006

3q 1q 2007

3q 1q2008

3q 1q 2009

3q 1q 2010

3q 1q 2011

3q 1q 2012

3q 1q 2013

q3 1q2014

Trend in voluntary liquidationsfigures season-adjusted and corrected for the number of working days

all businesses joint-stock companies* (right column)

Source: Cerved estimates. *excludes companies that did not submit any valid financial statementsin the three years prior to winding-up

4.4%

73.5%

-0.2%-14.1%

-2.2%

-7.8%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

joint-stock co.* dormant partnerships

Voluntary liquidations in 1H:

breakdown by business status number of proceedings and year-on-year percent changes

2012 H1 2013 H1 2014 H1

Source: Cerved estimates. *excludes companies that did not submit any valid financial statementsin the three years prior to winding-up

6.1%

1.6%0.8%

5.5%

-21.1%

-7.8%-18.8%

-13.9%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

others construction industrial service

Voluntary liquidations of joint-stock companies* in 1H:

breakdown by macro-sectornumber of proceedings and year-on-year percent changes

2012 H1 2013 H1 2014 H1

Source: Cerved estimates. *excludes companies that did not submit any valid financial statementsin the three years prior to winding-up

9 © 2013 – Cerved Group Spa – All rights reserved – Reproduction prohibited

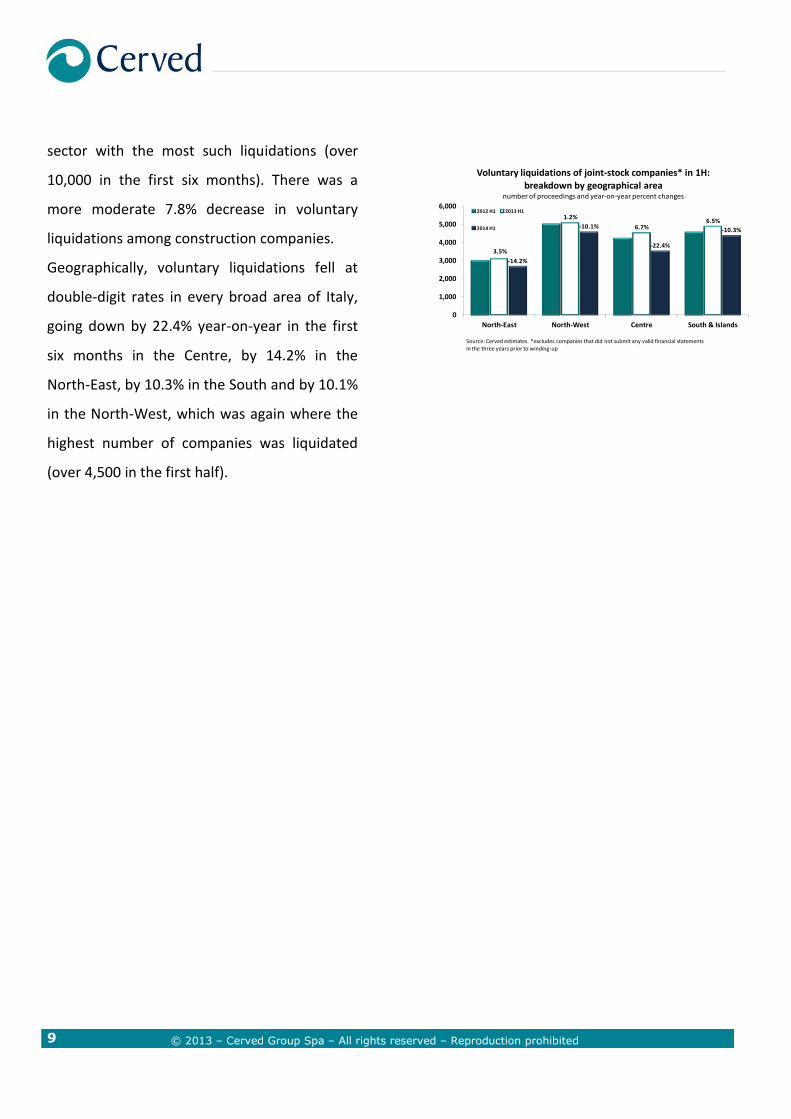

sector with the most such liquidations (over

10,000 in the first six months). There was a

more moderate 7.8% decrease in voluntary

liquidations among construction companies.

Geographically, voluntary liquidations fell at

double-digit rates in every broad area of Italy,

going down by 22.4% year-on-year in the first

six months in the Centre, by 14.2% in the

North-East, by 10.3% in the South and by 10.1%

in the North-West, which was again where the

highest number of companies was liquidated

(over 4,500 in the first half).

3.5%

1.2%

6.7%6.5%

-14.2%

-10.1%

-22.4%

-10.3%

0

1,000

2,000

3,000

4,000

5,000

6,000

North-East North-West Centre South & Islands

Voluntary liquidations of joint-stock companies* in 1H:

breakdown by geographical areanumber of proceedings and year-on-year percent changes

2012 H1 2013 H1

2014 H1

Source: Cerved estimates. *excludes companies that did not submit any valid financial statementsin the three years prior to winding-up