Embed Size (px)

Citation preview

Monthly Cocoa Report

November 2016

Translated from its original source in Portuguese

FUTURES MARKET

Historical cocoa prices in NY (USD/tonne)

3

Source: ICE

Since the beginning of October, the second futures contract for cocoa on the New York

exchange has fallen by 9.8% and is already among 30% of the lowest values from the past 5

years. In addition to the positive outlook for world production in 2016/17, the decline was

triggered by a strong appreciation in the dollar during the first two-weeks of the month

and a decline in commodity prices during the second two weeks.

Seasonality of cocoa prices in NY (USD/tonne)

4

Source: ICE

Historical cocoa prices in London (GBP/tonne)

5

Source: ICE

The decline in cocoa prices was restricted to 5.6% on the London commodity exchange, as

the appreciation of the dollar (and consequent devaluation of the pound sterling) was

bullish for this exchange, where cocoa is denominated in the British currency.

Seasonality of prices in London (GBP/tonne)

6

Source: ICE

Future contracts curve

7

Source: ICE

Funds’ rollover from December/16 positions to March/17 reduced the spread between the

two contracts compared with last month. However this differential has remained

relatively broad, given the expectation that cocoa production for the main African crop

(Oct-Sept) would only result in a greater supply of beans on the market in the new year.

London Arbitrage - New York (USD/tonne)

8

Source: ICE

The gap between the second contract on the London and New York stock exchanges (in

dollars per tonne) continues to fall, as African cocoa exporters are used to setting their

prices on the British commodity market. According to seasonality, this differential should

remain pressured until mid-November.

Position of Funds - ICE

9

Source: ICE, CFTC, INTL FCStone

SPECULATIVES COMMERCIALS

Posi

ção líq

uid

a

Pre

ço

Posi

ção líq

uid

a

Pre

ço

Following the decline in quotes in September, the speculative funds expanded their long

positions in cocoa by 11,174 lots during October, accumulating a total of 82,323 contracts

by November 1st. This has been the longest exposure to long cocoa contracts from the

funds since May, a time when supply fundamentals were much more bullish. This strong

exposure at a time of consolidation of surplus expectations and a possible record in world

production opens the door for intense liquidation movements and with that, a decline in

prices (which was probably the cause of the sudden devaluation in beans between 4th and

7th of November, a period which has not yet considered by CFTC data).

The short position of the funds also advanced, but by 8,732 lots, totaling 64,265 contracts.

Cocoa Correlation v CRB Reuters

10

Source: INTL FCStone, Reuters

The price of cocoa recovered the correlation with the CRB commodity index, in particular

at the end of October and the beginning of November. Among the reasons for the

devaluation of commodity prices during this period are the stronger figures of the US

economy and an increased chance of a rise in the Fed interest rate at the end of the year.

Correlation Cocoa v Euro

11

Source: INTL FCStone, Reuters

Correlation Cocoa v Pound

12

Source: INTL FCStone, Reuters

MARKET FUNDAMENTALS

Fundamentals of the Cocoa Market

14

BEARISH FACTORS

• Favorable weather for the

development of cocoa in Africa and

Indonesia.

• Surplus outlook in the supply and

demand balance for 2016/17 crop.

• Devaluation of Pound Sterling

following "Brexit" and an increased

US and UK interest rate differential.

BULLISH FACTORS

• Demand growth for grinding in

Europe, North America and Asia.

• Grinders project that shortages of

cocoa stocks should persist until the

end of the year.

• 2015/16 has the lowest carryover

stock in 30 years.

• Fourth quarter should see growth in

chocolate consumption.

• Start of harvest slower than

expected in Africa.

Weather - West Africa

15

Rainfall in south of the Ivory Coast and Ghana,

despite delaying harvesting for the first few

months of the main crop, was quite favorable for

the vegetation in West Africa. The VHI of the

cocoa producing regions is good/great, whereas

last year it was regular.

Source: NOAA, MDA

VHI RAINFALL (% average)

Since November, rains have tended to be more

scarce in West Africa with the start of

Harmattan. This year however, we expect less

intensity and a delay for this weather event,

resulting in above average rains in the region.

This may delay the cocoa harvest, but is

favorable for the development of the fruits to be

harvested in the intermediate crop.

* VHI (Vegetation Health Index) is an index which synthesizes soil moisture and temperature conditions. Values below

40 indicate water and thermal stress, while values above 60 give favorable conditions for plant development.

* In the case of rains, values below 90 mm indicate below-average rainfall for the period. Values above 110 mm

correspond to above average rains.

Nov/2016 Nov/2015December January

Ivory

Coast

Ivory

CoastGhana Ghana

Ivory Coast Ivory CoastGhana Ghana

Weather – Indonésia

16

The weather has also been more favorable for the

vegetation health Index for Indonesia in recent

months. In the cocoa growing area, the VHI is

good. In contrast with November of last year,

those same regions had a poor VHI.

Source: NOAA, MDA

VHI RAINS (% of average)

Indonesia's cocoa-producing regions are expected

to continue to record above-average rainfall over

the coming months, which could delay the

process of harvesting and drying of the

commodity.

* VHI (Vegetation Health Index) is an index which synthesizes soil moisture and temperature conditions. Values below

40 indicate water and thermal stress, while values above 60 give favorable conditions for plant development.

* In the case of rains, values below 90 mm indicate below-average rainfall for the period. Values above 110 mm

correspond to above average rains.

December

January

Nov/2016

Nov/2015

Balance of Supply & Demand

17

Source: LMC, USDA, ICCO, FAO, INTL FCStone.

The recovery of production in 2016/17 should bring the balance of demand and supply for

cocoa back to surplus, providing some relief to bean stocks, which are at their lowest levels in

the last 30 years.

Cocoa Final Balance

18

Source: LMC, USDA, ICCO, FAO, Reuters, INTL FCStone.

Relationship between Stocks and Grinding

19

Source: LMC, USDA, ICCO, FAO, INTL FCStone.

World Production

20

Source: LMC, USDA, ICCO, FAO, INTL FCStone.

We estimate that world cocoa production will increase by 11.6% to 4.399 million tonnes in

2016/17. Among the main producers, the largest gains are the Ivory Coast (+12.5%), Ghana

(+9.4%) and Brazil (+49.6%), recovering from the decline caused by El Niño In 2015/16.

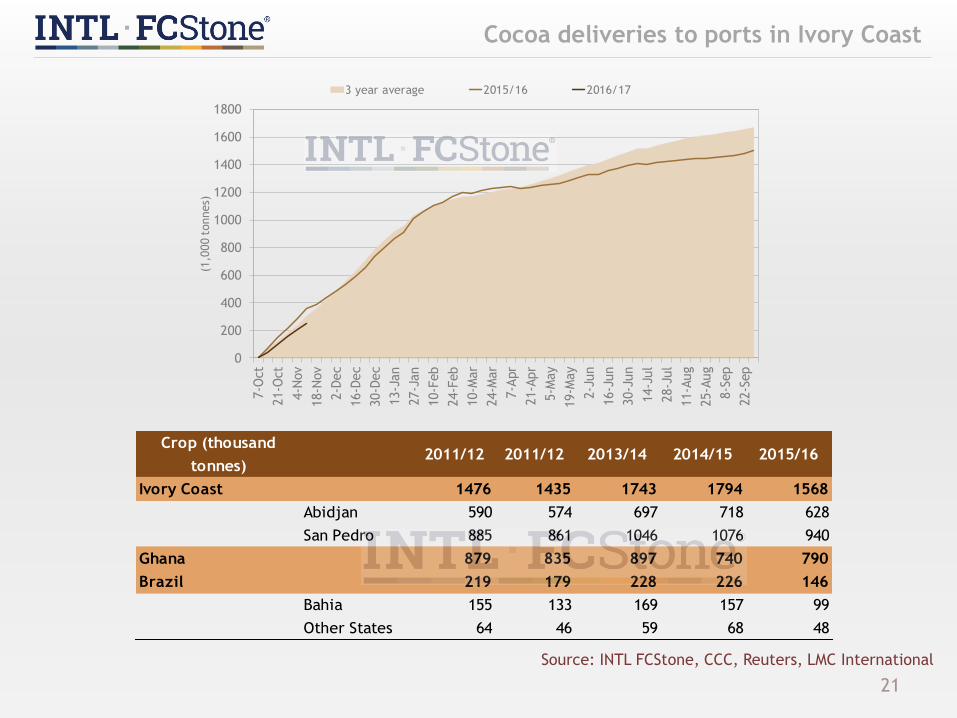

Cocoa deliveries to ports in Ivory Coast

21

Source: INTL FCStone, CCC, Reuters, LMC International

0

200

400

600

800

1000

1200

1400

1600

1800

7-O

ct

21-O

ct

4-N

ov

18-N

ov

2-D

ec

16-D

ec

30-D

ec

13-J

an

27-J

an

10-F

eb

24-F

eb

10-M

ar

24-M

ar

7-A

pr

21-A

pr

5-M

ay

19-M

ay

2-J

un

16-J

un

30-J

un

14-J

ul

28-J

ul

11-A

ug

25-A

ug

8-S

ep

22-S

ep

(1,0

00 t

onnes)

3 year average 2015/16 2016/17

Crop (thousand

tonnes)2011/12 2011/12 2013/14 2014/15 2015/16

Ivory Coast 1476 1435 1743 1794 1568

Abidjan 590 574 697 718 628

San Pedro 885 861 1046 1076 940

Ghana 879 835 897 740 790

Brazil 219 179 228 226 146

Bahia 155 133 169 157 99

Other States 64 46 59 68 48

World Production Calendar

22

Source: ICCO

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Ivory Coast

Ghana

Togo

Camaroon

Nigeria

Indonesia

Malaysia

Costa Rica

Brazil

Mexico

Venezuela

Colombia

Ecuador

Main Crop

Mid Crop

America

Africa

Asia

World Crushing

23

Source: LMC, USDA, ICCO, FAO, INTL FCStone.

After a 0.7% decline between 2014/15 and 2015/16, we estimate that worldwide demand for

cocoa for crushing will increase by 1.8% in 2016/17 to hit 4,231 million tonnes.

Grinding - Europe

24

Source: ECA – European Cocoa Association

Note: ECA accounts for 97% of European cocoa crushers

According to data from the European Cocoa Association (ECA), 343,935 tonnes of cocoa

were processed during the third quarter of 2016, up 2.9% compared with the same period

last year. Accumulated for the 2015/16 crop year (Oct-Sep), European industries processed

1.347 million tonnes of cocoa, their highest volume since 2010/11, and a rise of 3.3%

compared with 2014/15.

Grinding - North America

25

Source: NCA – National Confectioners Association

North American cocoa grinding increased 0.2% during the third quarter of 2012 to 124,412

tonnes. The accumulated total for the 2015/16 crop still showed a slight decrease of 0.5%

relative to the previous one, totaling 486,530 tonnes.

Grinding - Asia

26

Source: CCA – Cocoa Association of Asia

Note: The data reflects the compiling of Malaysia's crushing with the CAA members in Indonesia and Singapore

Grinding in Asia totaled 167,737 tonnes for the quarter, which is a 12.5% increase year-on-

year. Accumulated for the 2015/16 crop, the CAA estimate bean processing totaled

624,228 tonnes, an increase of 8.1% over the previous season and the second best Asian

result, losing out to the 2013/14 crop.

Grinding - Brazil

27

Source: Associação Comercial da Bahia

The low supply and high prices for cocoa in Brazil limited grinding during the third quarter,

where only 54,858 tonnes were added, 4.8% less than the same period last year and its

lowest result since 2009. In total for the 2015/16 crop year, grinding in the country still had

a slight increase of 0.6% compared with 2014/15, giving a total of 224,855 tonnes.

PHYSICAL MARKET

Cocoa prices in Bahia - Brazil (USD/T)

29

Source: Associação Comercial da Bahia, ICE

Cocoa prices in Bahia - Brazil (BRL/T)

30Source: Associação Comercial da Bahia, ICE

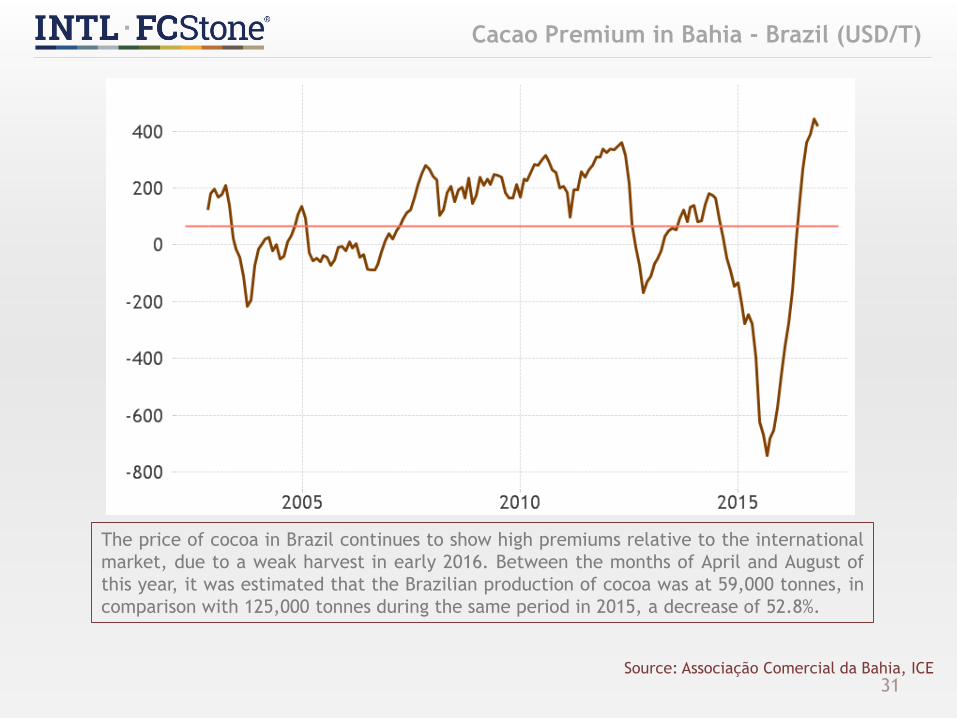

Cacao Premium in Bahia - Brazil (USD/T)

31Source: Associação Comercial da Bahia, ICE

The price of cocoa in Brazil continues to show high premiums relative to the international

market, due to a weak harvest in early 2016. Between the months of April and August of

this year, it was estimated that the Brazilian production of cocoa was at 59,000 tonnes, in

comparison with 125,000 tonnes during the same period in 2015, a decrease of 52.8%.

Cocoa premium in the US - by origin (USD/T)

32

Source: CMAA

COCOA BY-PRODUCTS

By-product ratios - US

34

The values indicate the ratio between the price of the product and the price of cocoa in beans.

The percentages in the product names indicates the amount of butter.

Source: CMAA, Milling and Baking News

Product Oct-16 Sep-16 Change

Butterfat 2,65 2,75 -0,10

Cake 0,79 0,74 0,05

10-12% Natural Powder 0,83 0,81 0,03

16-18% Natural Powder 1,00 0,97 0,03

22-24% Natural Powder 1,04 1,01 0,04

10-12% Alkalized Powder 0,96 0,93 0,03

Red Alkalized Powder 1,00 0,97 0,03

Black Alkalized Powder 1,28 1,23 0,04

Historical Ratio Relationships - US

35Source: INTL FCStone, Milling and Baking News, CMAA

After seven consecutive months of rallies, the butter ratio yielded 1.5% in October, having

reaching 2.71, while the powder ratio increased 7.5% to 0.86. Following the historical

trend, the butter ratio tends to weaken from November, with purchases of product until

the end of the year already having been made. By 2016 however, the product shortage

should keep this ratio high until the end of the year. On the other hand, the powder ratio

should encounter resistance for a rally, given the high supply and high margins of the

grinders.

Historical Ratio Relationships - Brazil

36

Source: INTL FCStone, MDIC, Seagri, Ceplac, Cacauth

Cocoa Butter Ratio - US

37

Source: INTL FCStone, Milling and Baking News, CMAA

Seasonality of the Cocoa Butter Ratio - US

38

Source: INTL FCStone, Milling and Baking News, CMAA

Cocoa Powder Ratio - US

39

Source: INTL FCStone, Milling and Baking News, CMAA

Seasonality of the Cocoa Powder Ratio - US

40

Source: INTL FCStone, Milling and Baking News, CMAA

Grinding margins - US

41

Source: INTL FCStone, Milling and Baking News, CMAA

The combined cocoa product ratio in October was 1,428, its highest since February 2014.

Despite their attractive margins, cocoa processors have low availability of beans after

losses during the 2015/16 crop. The stocks situation is expected to begin to normalize

starting from early 2017.

INTERNATIONAL TRADE

Brazil: Balance of the cocoa trade (tonnes)

43

Source: MDIC

Brazil: Balance of trade balance for butter (tonnes)

44

Source: MDIC

Brazil: powder trade balance (tonnes)

45

Source: MDIC

Butter Exports - Europe and the United States

46

Source: LMC International

0

100

200

300

400

500

2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15

(1,0

00 t

onnes)

United States

UnitedKingdom

Germany

France

Netherlands

2016 Jan-Mar 2016 Apr-Jun

Netherlands 47,48 45,91

France 14,75 15,10

Germany 12,63 10,56

United Kingdom 2,91 3,07

United States 6,43 6,59

Powder Exports - Europe and the United States

47

Source: LMC International

0

100

200

300

400

500

2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15

(1.0

00 t

onnes)

United States

UnitedKingdomGermany

France

Netherlands

2016 Jan-Mar 2016 Apr-Jun

Netherlands 51,72 55,21

France 11,50 11,86

Germany 25,19 23,10

United Kingdom 1,15 0,93

United States 6,90 12,29

Liquor Exports - Europe and the United States

48

Source: LMC International

0

50

100

150

200

250

300

2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15

(1,0

00 t

onnes)

United States

UnitedKingdom

Germany

France

Netherlands

2016 Jan-Mar 2016 Apr-Jun

Netherlands 23,10 21,02

France 9,86 7,90

Germany 15,04 13,55

United Kingdom 0,08 0,07

United States 4,59 5,89

Butter Exports - West Africa

49Source: LMC International

0

20

40

60

80

100

120

140

2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15

(1.0

00 t

onnes)

Nigeria

Cameroon

Ghana

Ivory Coast

2016 Jan-Mar 2016 Apr-Jun

Ivory Coast 14,71 15,65

Ghana 5,26 7,48

Cameroon 2,32 2,53

Nigeria 2,73 2,27

Powder Exports - West Africa

50Source: LMC International

0

10

20

30

40

50

60

70

80

90

100

2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15

(1.0

00 t

onnes)

Ghana

IvoryCoast

2016 Jan-Mar 2016 Apr-Jun

Ivory Coast 16,05 13,86

Ghana 4,63 3,10

Liquor Exports - West Africa

51Source: LMC International

0

50

100

150

200

250

2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15

(1.0

00 t

onnes)

Nigeria

Cameroon

Ghana

Ivory Coast

2016 Jan-Mar 2016 Apr-Jun

Ivory Coast 25,99 25,96

Ghana 6,47 6,01

Cameroon 1,13 1,75

Nigeria 0,02 0,08

Fábio RezendeMarket Intelligence

(55 19) [email protected]

FCStone do Brasil Ltda.Av. José Bonifácio Coutinho Nogueira, 150

Ala Oeste – Sala 203 Jardim MadalenaCampinas-SP 13091-611

33 offices around the world | 1,000 professionals | 20,000 customers in more than 100 countries