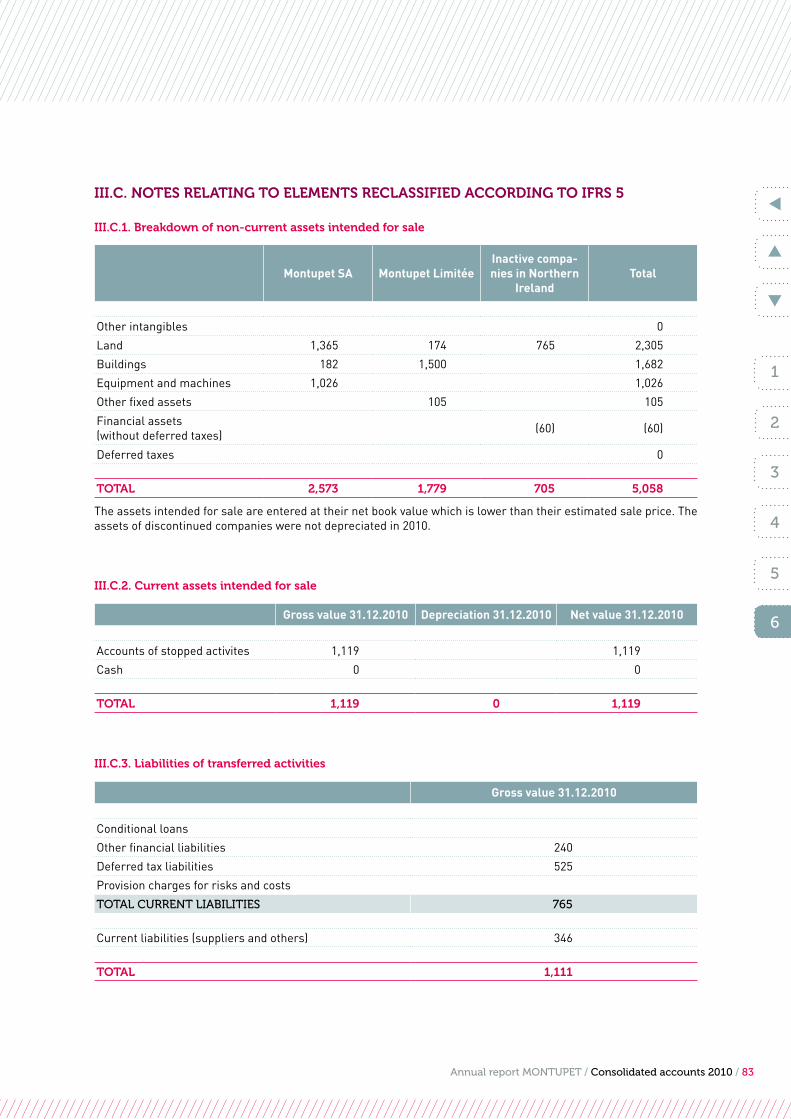

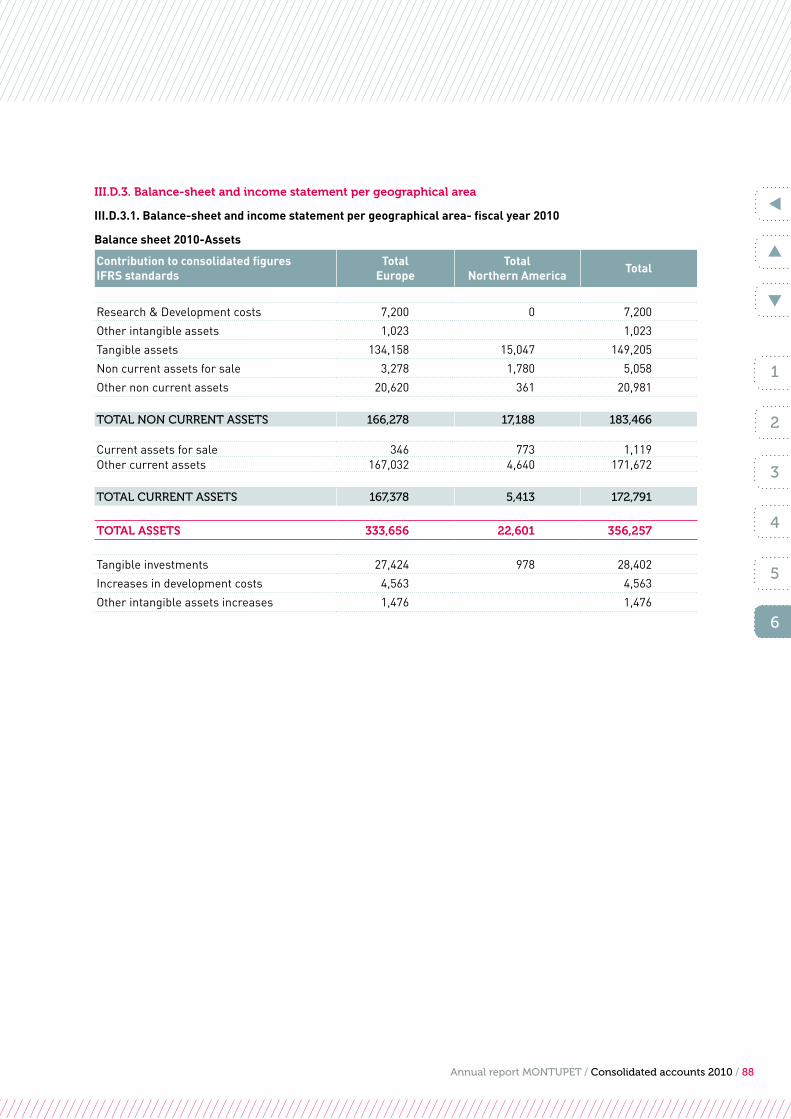

Embed Size (px)

Citation preview

Annual report MONTUPET / 1

MontupetAnnual Report 2010

≥ ≥ ≥ ≥ ≥ ≥ ≥ ≥

2

1

6

5

4

3

Annual report MONTUPET / 3

2

1

6

5

4

3

2

1

6

5

4

3

Shareholders meetingJune 30th 2011

Annual report MONTUPET / 4

2

1

6

5

4

3

Table1. Montupet on line .................................................................................................7

2. Key figures ............................................................................................................9

3. Group profile ......................................................................................................13

3.1. History .................................................................................................................................. 13

3.2. Competitive position ....................................................................................................... 13

3.3. Geographical presence ................................................................................................... 14

4. Board of directors and auditors ......................................................................17

5. Management report ..........................................................................................19

5.1. Results, funding and outlook ........................................................................................ 20

5.1.1. Results ......................................................................................................................................................20

5.1.2. Financing ................................................................................................................................................24

5.1.3. Priorities and outlook .......................................................................................................................25

5.1.4. Risks and uncertainties ....................................................................................................................27

5.1.5. Stock market developments during the financial year 2010 ..........................................30

5.2. Research & Development ............................................................................................... 31

5.3. Legal information concerning the company and its capital ............................... 33

5.3.1. General information on the company ......................................................................................33

5.3.2. Company representatives and board members ..................................................................33

5.3.3. Subsidiaries and holdings ...............................................................................................................37

5.3.4. Share capital and shareholding ....................................................................................................38

5.3.5. Auditors' fees .........................................................................................................................................39

5.3.6. Miscellaneous information .............................................................................................................39

5.4. Social indicators ................................................................................................................ 41

5.5. Environment and sustainable development ............................................................ 47

5.5.1. Environmental appraisal of Montupet SA ................................................................................47

5.5.2. Consolidated elements concerning the Group's environmental impact ................56

Annual report MONTUPET / 5

2

1

6

5

4

3

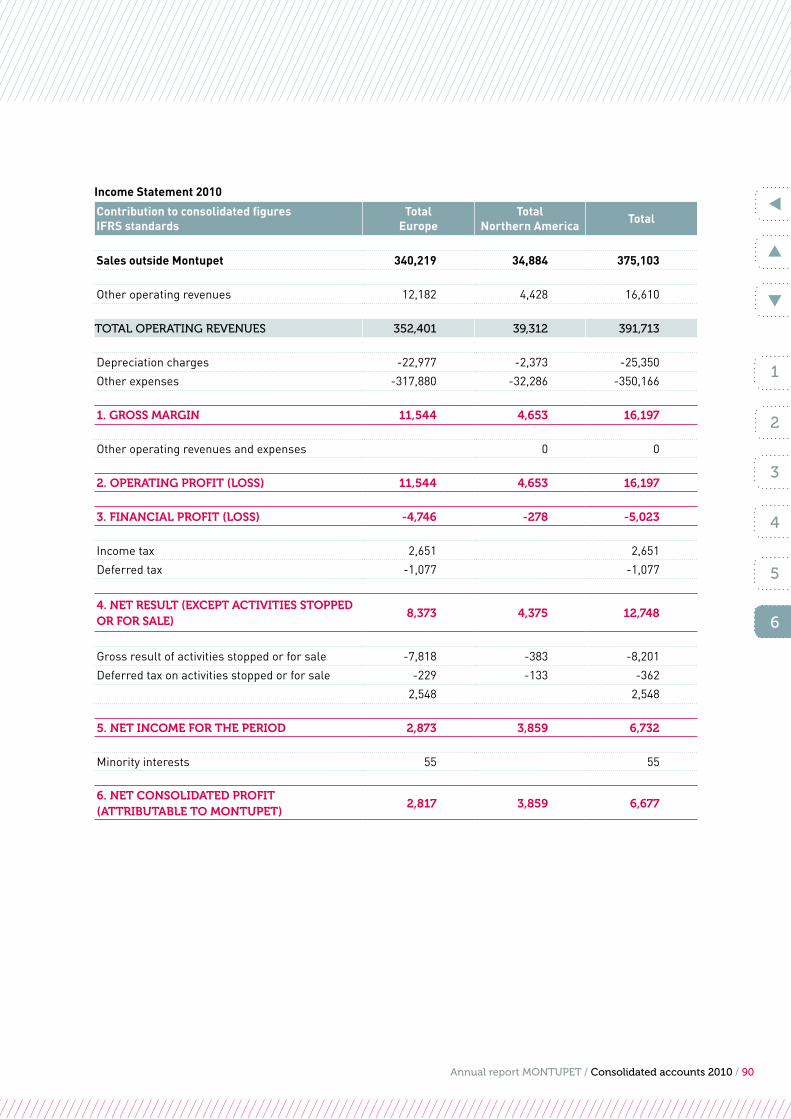

6. Consolidated Accounts ....................................................................................61

6.1. Consolidated balance sheet .........................................................................................62

6.2. Consolidated income statement ................................................................................64

6.3. Changes in equity ...........................................................................................................66

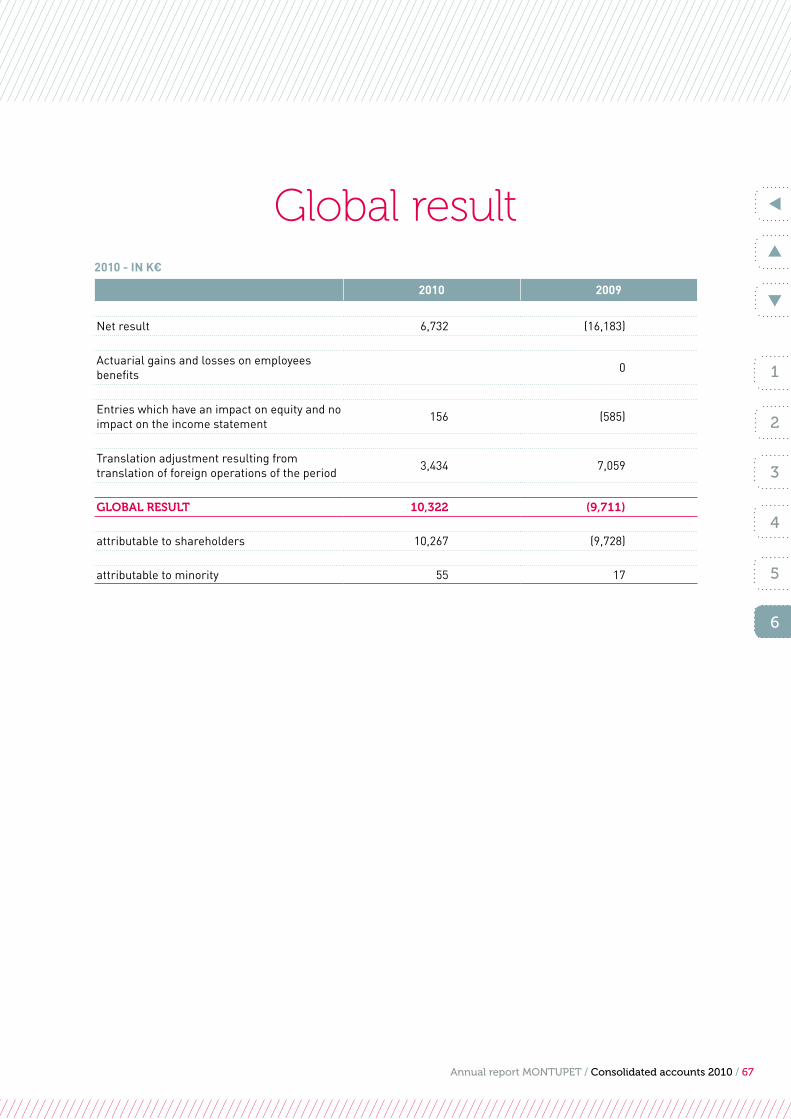

6.4. Global result ......................................................................................................................67

6.5. Consolidated cash flow statement ............................................................................68

6.6. Appendix to the consolidated accounts ..................................................................70

Annual report MONTUPET / 6

2

6

5

4

3

1

Annual report MONTUPET / Montupet on line / 7

2

1

6

5

4

3

Montupet, on lineVisit the Montupet website www.montupet.fr which presents information on the

group (history, financial information, business appraisal), current events, the firm

(customers, products, manufacturing processes, etc.), the corporate strategy, the

production units and a "career" section.

On www.journal-officiel.gouv.fr in the section entitled "advertisements published

in the BALO" (French legal advertisements publication) you can consult the obliga-

tory legal advertisements published by Montupet (quarterly turnovers, half-yearly

accounts, invitations to meetings).

On www.amf-france.org in the sections entitled "issuer area" and "decisions and

financial information" you can consult published information and press releases.

You can consult the value of Montupet SA on the financial sites by entering the code

FR0000037046.

1.

1

6

5

4

3

2

2

1

6

5

4

3

Annual report MONTUPET / Key figures / 9

2

1

6

5

4

3

Montupet, key figures

2.

0

50

100

150

200

250

300

350

400

201020092008

. . .

Consolidated turnover of strategic activities In M€↗

-20

-15

-10

-5

05

10

15

20

25

30

201020092008

-19.6

28.5 16.2

Current operating result of strategic activities In M€↗

Annual report MONTUPET / Key figures / 10

2

1

6

5

4

3

2

1

6

5

4

3

-20

-15

-10

-5

0

5

10

201020092008

-16.2

-0.8

6.7

0

5

10

15

20

25

30

35

40

201020092008

1.9

33.8 36.6

Group net result In M€

Cash flow In M€

↗

↗

2

1

6

5

4

3

Annual report MONTUPET / Key figures / 11

2

1

6

5

4

3

0

30

60

90

120

150

201020092008

135.5103 86 86.5125.8 136.1 Net debtStockholders’ equity

3.56

0

2

4

6

8

10

31 december 201031 december 200931 december 2008

3.13

6.95

Closing price of Montupet shares In €

Net debt & stockholders’ equity In M€↗

↗

Annual report MONTUPET / 12

2

6

5

4

3

1

Annual report MONTUPET / Group profile / 13

1. History

Montupet is a French industrial group established as a limited liability company which specialises in products cast in aluminium alloys for the

automobile industry.

The group was formed in 1977 by the amalgamation of three French foundries: Montupet, Debard became Virax and Fonderie de Précision. After a decade marked by industrial and financial restructuring, the group developed internationally by taking over the Spanish foundry Alumalsa in 1987 and establishing three new foundries in 1988 and 1989 in France, Canada and the United Kingdom. At the same time, Montupet became a producer and supplier of tools with the aim, among other things, of controlling its most technical supplies which constitute one of the strengths of its technology.

After being called into question due to the automobile crisis between 1991 and 1996, expansion resumed from 1997 onwards with the development of existing sites, the establishment of a new foundry in Mexico and the acqui-sition of an existing foundry in Northern Ireland at the request of Ford. In 2008, a new factory began producing in Bulgaria whilst two factories in Northern Ireland and Canada closed down and a planned foundry in China was suspended. On 31 December 2009, the Group acquired the business and assets of the company Fonderie de Poitou Aluminium (in Ingrandes, France). On 30 June 2010, the Group transferred its subsidiary Française de Roues specialising in the wheel business.

The company owns 3 establishments in France:

• The La Martinerie factory in Châteauroux in the de-partment of Indre,

• the Laigneville factory in the department of Oise,• the head offices in Clichy in the department of

Ile-de-France.

It possesses a majority holding in 10 subsidiaries1:

• MFT-Montupet Snc in Brussels, Belgium: coordination centre,

• MFT-Sarl in Clichy, France: metal trading and service provision,

• Alumalsa in Saragossa, Spain: foundry,• Montupet UK in Dunmurry, United Kingdom (and its

subsidiaries): foundry and tools,• Calcast Ltd in Londonderry, United Kingdom: foundry,• Montiac SA de CV in Torreon, Mexico: foundry,• Montupet EOOD, Bulgaria: foundry,• Montupet INC in Livonia, United States: commercial

office,• Montupet Limitée in Rivière-Beaudette, Canada

(inactive),• Montupet Deutschland GmbH, Germany (inactive). And indirectly holds 100% of the company Fonderie du Poitou Aluminium in France.

2. Competitive position

Montupet works in partnership with all European and American automobile manufacturers and specialises in the design and production of two types of cast alumi-nium product:

• untreated or machine-cut parts for engines: cylinder heads, cylinder blocks, induction pipes,

• untreated or machine-cut structural, suspension and braking parts.

Montupet, group profile

2

1

6

5

4

3

1. On 30 June 2010, the Montupet SA group transferred its subsidiary Française de roues SAS in which it had a 100% holding.

3.

Annual report MONTUPET / Group profile / 14

2

1

6

5

4

3

The challenges facing metallurgists are becoming increasingly difficult. This is why the group's reco-gnised skills in this field, particularly as regards cylin-der heads, has enabled it to gain a leading position in Europe and the United-States. Thanks to its large customer base, Montupet is involved in most of the new decade's engine programmes.

In response to environmental regulations and the deve-lopment of electronic functions relating specifically to the automobile sector, manufacturers are showing a strong desire to simplify their vehicles and modernise their drive trains.

Aluminium, and particularly cast aluminium, fulfils these requirements:

• its thermal conductivity is better than that of cast iron and means that more compact, more powerful and less polluting engines can be developed;

• its low density compared with steel or cast iron means that lighter engines and chassis frames can be created.

The processes used in the casting of aluminium also provide a great deal of design flexibility which is bene-ficial for both engineers and designers.

In order to optimise these qualities and propose pro-ducts which comply with the specific requirements of each automobile manufacturer, Montupet has esta-blished a research and innovation policy whose aim is to develop the potential of aluminium and encourage new applications. Montupet is currently developing radical innovations in terms of casting and thermal processing in order to increase the resistance of cylinder heads to thermo-mechanical fatigue and is thus offering moto-rists enhanced design flexibility.

Furthermore, since Montupet's aim is to serve its cus-tomers in the long term, it is important for the firm to control the effects of its business on the environment and to develop the skills of the individuals representing it.

These policies stand alongside the total quality policy of which enables the Group to provide its products and services to Audi, Bosch, Continental-Teves, Fiat, Ford, General Motors, Nissan, PSA, Renault and Volvo.

3. Geographical presence

The local strategy, the synergy between production sites and the international commercial policy of Montupet enable the Group to provide a consistent service and standard quality to customers who possess or are seeking positions all over the world.

r Plants

• Mexico, Torréon• Northern Ireland, Belfast• France, Laigneville• France, Châteauroux• France, Ingrandes• Spain, Saragossa• Bulgaria, Roussé n Commercial presence

• Montupet INC, Livonia, Michigan, USA,• Pechiney UK Ldt, Berkshire, UK,• Montupet SA, head office, Clichy, France,• Alumalsa, Saragossa, Spain,• Esma AB, Spanga-Stockholm & Göteborg, Sweden,• Montupet Eood, Roussé, Bulgaria

2

1

6

5

4

3

Annual report MONTUPET / Group profile / 15

SWEDEN

MEXICO

UNITED STATES

FRANCEBELGIUM

UNITED KINGDOM

NOTHERN IRELAND

SPAINBULGARIA

2

1

6

5

4

3

r Plants n Commercial presence

Annual report MONTUPET / 16

2

6

5

3

1

4

Annual report MONTUPET / Board of directors and auditors / 17

2

1

6

5

4

3

Board of directors and auditors

4.

CHAIRMAn AnD MAnAGInG DIRECTOR

• Stéphane Magnan

DIRECTORS

• Didier Crozet, Director and Executive Managing Director• Marc Majus, Director and Executive Managing Director• Francois Feuillet, Director• Jean Berruyer, Director

REGULAR AUDITORS

• Guilleret & Associés, represented by Marie-José Rochereau• Bellot Mullenbach & Associés, represented by Thierry Bellot

SUBSTITUTE AUDITORS

• Eric Blache• Geneviève Collin-Mansart

Annual report MONTUPET / 18

2

1

6

5

4

3

2

1

6

5

4

3

Annual Report MONTUPET / Management report / 19

2

1

6

5

4

3

Management report5.1. Results, funding and outlook ................................................................................ 20

5.1.1. Results ............................................................................................................................................20

5.1.2. Financing ....................................................................................................................... 24

5.1.3. Priorities and outlook ............................................................................................... 25

5.1.4. Risks and uncertainties ............................................................................................ 27

5.1.5. Stock market developments during the financial year 2010................. 30

5.2. Research & Development ....................................................................................... 31

5.3. Legal information concerning the company and its capital ...................... 33

5.3.1. General information on the company ............................................................. 33

5.3.2. Company representatives and board members .......................................... 33

5.3.3. Subsidiaries and holdings ....................................................................................... 37

5.3.4. Share capital and shareholding ........................................................................... 38

5.3.5. Auditors' fees ................................................................................................................ 39

5.3.6. Miscellaneous information .................................................................................... 39

5.4. Social indicators........................................................................................................ 41

5.5. Environment and sustainable development .................................................... 47

5.5.1. Environmental appraisal of Montupet SA ....................................................... 47

5.5.2. Consolidated elements concerning the Group's environmental

impact ............................................................................................................................ 56

5.

Annual Report MONTUPET / Management report / 20

2

1

6

5

4

3

5.1. Results, funding and outlook

In accordance with regulation n°1606/2002 adopted on 19 July 2002 by the European Parliament and the European Council, these consolidated accounts have been drawn up according to the IFRS reference system adopted by the European Union on 31 December 2010.

Main activities and productsMontupet designs and produces parts and equipment for the automobile industry:

• untreatedormachine-cutpartsforengines:cylinderheads, cylinder blocks, induction pipes,

•machine-cut,paintedwheels(businesstransferredon 30 June 2010)

• untreatedormachine-cutstructural,suspensionandbraking parts,

• someofthetoolsrequiredforproduction.

5.1.1. Results

The consolidated turnover for 2010 amounted to 375 M€ (excludingtransferredactivities),up84%comparedwith 2009.

Thesefiguresconfirmareturntonormalpre-crisisbusiness levels allowing for the optimum use of the capacities of Montupet after restructuring.

Allthesiteshaveseenasignificantincreaseinbusiness:Bulgaria has almost quadrupled its turnover and growth elsewherevariesbetween28%fortheUKsub-groupand71%forMexico.Theturnovergeneratedbythesubsidiary Fonderie du Poitou Aluminium, acquired on 31 December 2009, has enhanced the growth of the French factories.

The current operating result stands at 16.2 M€ compa-red with a loss of 19.6 M€ in 2009.

In 2010, Montupet continued its restructuring activity by selling the wheel unit and the Chinese subsidiary, whichgeneratedanextraordinarylossof8.7M€withoutaffecting the net debt.

The net result amounted to 6.7 M€ compared with -16.2M€in2009.

The Group's industrial mechanism currently consists of threelow-costfactories(Mexico,UnitedKingdomandBulgaria) and four less productive factories in France andSpain.Mostoftheprofitisgeneratedbythelowcost sites with the other units more or less reaching a balance.

Annual Report MONTUPET / Management report / 21

2

1

6

5

4

3

Turnover Operating result

In M€ 2010 2009 Variation

Variation at constant exchange

rate

Variation at constant

metal price and exchange

rate

2010 2009

Strategic Activities

France&Belgium(exceptwheels) 189.0 86.2 119% 120% 112% 3.8 -11.6

UnitedKingdom 71.9 56.4 28% 23% 18% 7.8 -1.4

Mexico 34.9 20.4 71% 63% 38% 4.7 0.6

Spain 55.9 34.9 60% 60% 59% -1.0 -3.6

Bulgaria 23.4 6.5 261% 261% 231% 1.0 -3.5

SUbTOTAL 375.1 204.4 84% 82% 73% 16.2 -19.6

Activities stopped or transferred

Canada 0.0 0 -0.5 -4.6

China -1.8

Calcast(UnitedKingdom) 0.0 1.8 -100% -100% -100% 0.5 -0.9

BSTooling(UnitedKingdom) 0.0 0 -0.1 0

Wheels(FrançaisedeRouesSAS) 31.8 54.4 -42% -42% -42% -5.8 -1.6

SUbTOTAL 31.8 56.2 -43% -43% -44% -7.7 -7.1

ToTal sTRaTegic and sTopped oR TRansfeRRed acTiviTies

406.9 260.6 56% 55% 48% 8.5 -26.7

2. Since the wheel business was transferred on 30.06.2010. its results only relate to the first half of 2010..

5.1.1. Results

• Changes in turnover and consolidated results (2010 v 2009) by business and geographical production area 2

Annual Report MONTUPET / Management report / 22

2

1

6

5

4

3

• Change in consolidated turnover of strategic activities over a 10 year period (M€)In IFRS standards from 2004

• Change in consolidated current operating result of strategic activities over a 10 year period (M€) In IFRS standards from 2004

• Consolidated key figures for the Montupet group on 31 December 2010

In M€ 2010 2009

Consolidated turnover of strategic activities 375.1 204.4

Consolidated turnover of strategic and stopped or transferred activities 406.9 260.6

-atconstantmetalpriceandexchangerate- 386.0 284.5

Operating result of strategic activities 16.2 -19.6

Group net consolidated result 6.7 -16.2

Cashflow 36.6 1.9

Net debt 86.5 86

Stockholders' equity 136.1 125.8

Net debt/ Stockholders' equity 0.64 0.7

0

100

200

300

400

500

20102009200820072006200520042003200220012000

-20-15-10

-505

101520253035

20102009200820072006200520042003200220012000

Annual Report MONTUPET / Management report / 23

2

1

6

5

4

3

• Breakdown of consolidated turnover of strategic activities by customer in 2010

OTHERS 10%

VOLKSWAGEN/ AUDI 7%

RENAULT 42%

PSA 13%

JOHN DEERE 3% HONEYWELL 2%GENERAL MOTORS 3%

FORD 17%

CONTINENTAL TEVES 3%

• Breakdown of consolidated turnover of strategic activities by geographical area in 2010

• Current operating result of strategic activities by geographical area in 2010 (M€)

-1

01

23

45

67

8

BulgariaSpainMexicoUnited KingdomFrance-Belgium

3.8

7.8

4.7

-1

1

Mexico 9%

United Kingdom 19%

Spain 15%

Bulgaria 6%

France-Belgium 51%

Annual Report MONTUPET / Management report / 24

2

1

6

5

4

3

5.1.2. financing

• Change in cash flow for all activities over a 10 year period (M€)In IFRS standards from 2004

0

10

20

30

40

50

60

20102009200820072006200520042003200220012000

• Net debt / stockholders' equity ratio (E/C)

0,0

0,2

0,4

0,6

0,8

1,0

1,2

20102009200820072006200520042003200220012000

1.17

0.86

0.51

0.210.12

0.07

0.247

0.42

0.760.70

0.64

• Net debt and stockholders' equity (M€)

0

50

100

150

200

20102009200820072006200520042003200220012000

■ Net debt ■ Stockholders’ equity

Thecashflowstoodat36.6M€comparedwith1.9M€in2009.Theextremelystrictmanagementoftheincreaseintheworkingcapitalrequirementlimitedthenetdebtto86.5M€comparedwith86M€attheendof2009.Stockholders'equitystoodat136.1M€withgearingthusamountingto0.64.

Annual Report MONTUPET / Management report / 25

2

1

6

5

4

3

5.1.3. priorities and outlook

Sincethesaleofits"wheel"business,91%ofMontupet'sactivity has been in the market for aluminium engine parts. This positioning has enabled the Group to be-comeinvolvedintheworld-widegrowthoftheauto-mobile market as engines "travel" much more easily than bodywork. Since they are less visible, they are less dependent on the model, make and country: they can be assembled in different vehicles, in private cars as wellassmallcommercialvehicles,andareexchangedbetween different makes all over the world.

Thismarketistechnicallyextremelydynamicasitfol-lows the rapid development in mentalities and legis-lation relating to CO2 and particle emissions and fuel consumption. New engines are being developed which requiremorecomplexcylinderhead"architectures",more resistant materials and increased precision in terms of dimensions which Montupet is successfully incorporating in its research and products.

Therefore, in spite of the stagnation in western European markets,Montupetwillthisyearberecordingtwo-figuregrowth due, on the one hand, to the healthy position of current orders and, on the other, on the successful launchoftwonewordersforFord(SigmaEuro5petrolengine)andRenault(K9Euro5dieselengine).

2011willbemarkedbynewproductlaunches(RenaultR9M diesel engine, Nissan R9M diesel engine and Ford Foxpetrolengine,allofwhichhavealreadybeendeve-loped for the Euro6 standard). These new products may initially draw on the Group's resources but will in the future provide growth by gaining new market share.

In addition to "engines", the Group's other products are also developing, particularly suspension parts and turbo safety hoods which currently also equip petrol engines.

The Group's factories are therefore operating in line withtheirinstalledcapacitywiththeexceptionoftheChâtelleraultfactory(FDPA),aswasthecaselastyear.Employee numbers are increasing in a steady, controlled manner both in France and abroad.

Annual Report MONTUPET / Management report / 26

2

1

6

5

4

3

EVENTS AfTEr ThE ClOSE Of ThE fINANCIAl yEAr

• Consolidated turnover for the 1st quarter of 2011(ContributiontotheconsolidatedturnoverinK€)

Montupet's consolidated turnover in the 1st quarter of 2011amountedto121millionEuros,up30%comparedwith 2010 according to the Group forecasts,

2011 2010 adjusted* 2010 published VariationVariation at

constant exchange rate

Strategic Activities on a like-for-like basis by geographical area

France 58,519 50,461 16.0%

Spain 22,221 13,811 60.9%

UnitedKingdom 21,665 17,236 25.7%

Bulgaria 10,334 4,257 142.8%

Mexico 8,594 7,056 21.8%

ToTal 121,334 92,823 97,990 30.7% 31.6%

*: after adjustement of provisions registered in 2009 and charge-back of sales of metal and wheels to Française de Roues

The current outlook for the 2nd quarter is following the same trend.Asfarasfinancingisconcerned,theGrouphasopenednegotiations with its banks with the aim of altering the credit agreement signed in 2009.

Annual Report MONTUPET / Management report / 27

2

1

6

5

4

3

5.1.4. Risks and uncertainties

• risks linked to the Group's business

TheMontupetGroupoperatesexclusivelyintheautomo-bilemarketasaleadingsupplierofseveralworld-widemanufacturers and a secondary supplier of equipment manufacturers(15%ofitssales).Itisthereforesubjectto cyclical and accidental variations in this global market aswitnessedattheendof2008andin2009.

Its current customers, in descending order of turnover, areRenault-Nissan,Ford,PSA,Audi,HTT(HoneywellTurboTechnologies),GM-Daewoo.Thecurrentdefaultrisk for any of these vehicle or equipment manufactu-rersisextremelylow.

The risks linked to the lack of success of a vehicle are reduced by the distribution of turnover between a large number of engine programmes. These engines are ins-talled in several vehicles of the same make, including smallcommercialvehicles,andsomeareexchangedbetween makes, which further reduces the effects of a potential slowdown in the sales of a particular vehicle model.

If, in spite of everything, an engine programme falls below the volume and duration predictions for the esta-blishmentofacylinderheadsaleprice,financialcom-pensationisrequested(andgenerallyobtained)fromthe manufacturer on the basis of an economic study. The ratio maintained in the long term between a limited number of customers and an even smaller number of suppliers is a characteristic of the market for highly sought-aftercastaluminiumpartssuchascylinderheads, braking parts and suspension parts.

The cost of the raw material is passed on to the price ofpartsaccordingtoamathematicalformulaspecificto each customer which protects the Group against increasesinaluminiumprices.However,thisyearweare suffering the effects of an increase in the alloy pre-mium by our suppliers which is being added to the price ofaluminium.Thishascalledforanadjustmentinthemathematical formulae agreed with each customer.

Whilst the supplying of primary alloys is not proving pro-blematic, a certain tension has been noted this year in the supplying of secondary alloys for cylinder heads. We havenotidentifiedanyriskofshortagesinconsumablematerialsforthecurrentfinancialyear.

The competition between manufacturers and between suppliers has led to the acceptance of sale price reduc-tionscheduleswhichthefirmwillhavetocompensatefor by increases in productivity. This productivity stems from various different sources:

• investmentintheautomationoftaskswhenlargeproduction volumes are at stake,

• thecreationofproductionunitsinlowcostareas,particularly in terms of labour,

• profit-makingmethodsinallareaswhosecommonfeatureistoinvolvenotonlyexpertsbutalsotheplayers involved in each of our businesses.

Thankstotheseconstantefforts,thefirmismanagingto satisfy its customers in the long term and gradually gain market share as a result.

• Interest rate risksMontupet is not involved in any hedging and none of its transactions are hedged at present. All the group's loansarespecifiedatvariablerates.

• Exchange rate risks Thegrouprecordedanet foreignexchangelossof-1,345K€in2010(comparedwithaprofitof2,250K€in 2009).

EurO ZONE

MontupetSArecordedanet foreignexchangelossof1,202K€in2010(comparedwithalossof264K€in2009).TheforeignexchangelossesandgainsofMontupet SA stem above all from receivables and de-bts in foreign currency with customers and suppliers. MontupetSAhasalsorecordedaforeignexchangelossof1,666K€asaresultoftheoffsettingofthenetdivi-dendof9,304K€paidbyitssubsidiaryMontupetLimitéewith the loan granted by the latter.

• Mexican pesoMontupet SA pays the operating costs charged by its MexicansubsidiaryMontiacSAdeCVinMexicanpe-sos(MXN)withintheframeworkofits"maquiladora"contractamountingto207,286KMXNaccordingtothecontractin2010(12,467K€).TheexchangerateeffectwasunfavourableforMontupetSAastheMXNhadincreasedby13%attheendofDecember2010com-pared with 2009.

• US DollarMontupetSAhassoldtheproductsofMontiacSAdeCV,whichitowns,inUS$.Theturnoverstoodat34,723K€intheaccounts(19%oftheturnoverofMontupetSA).TheaveragerateoftheUSDincreasedby8%in2010.

• Bulgarian levThereisnoexchangeraterisksincethelevislinkedto the euro.

Annual Report MONTUPET / Management report / 28

2

1

6

5

4

3

NON-EurO ZONE

• Northern IrelandIn2010,MontupetUKsoldapproximately62%ofitsproductioninGBPand38%ineurostoMontupetSA.However,thesalepriceineurostotheendcustomervaries contractually according to the €/GBP parity.

• MexicoStructural equipment is essentially purchased by Montiac inUS$;anincreaseintheMXNthereforeminimises these investments and their deprecia-tion (Montiac'sproductionequipment is ownedbyMontupet SA). Montiac charges Montupet SA for its pro-ductioncostsinMXNandthereforedoesnotincuranyexchangeraterisk,whichispassedontoMontupetSA.

• BulgariaTransactions are conducted in lev or euros and do not generateanyexchangeraterisk.

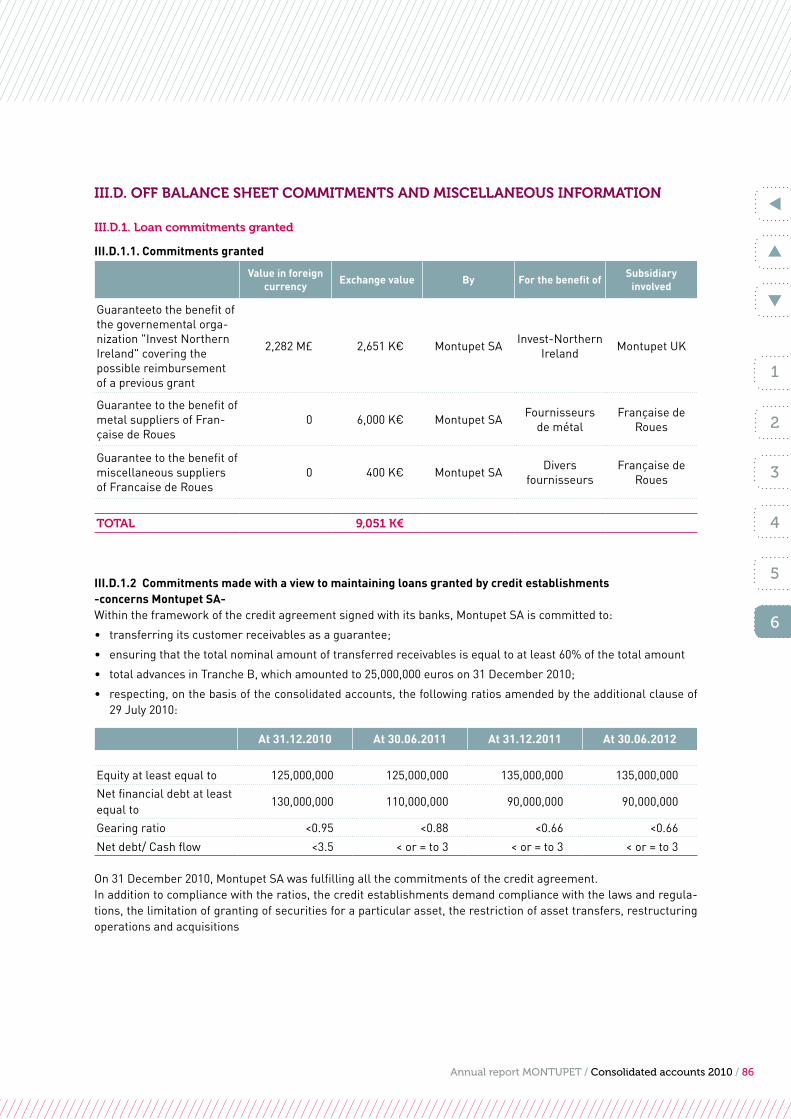

• Credit risksA credit agreement dated 29 July 2009, amended by an additional clause on 29 July 2010, was concluded between Montupet SA and a banking pool in order to guaranteethefinancingofthefirm'sgeneralrequire-ments. Within the framework of this credit agreement, the following credit lines were granted and used on 31 December 2010:

Term credit Section A

revolving creditSection B

OverdraftSection C

Total lines on 31.12.2010 74,385,000 41,900,000 1,000,000

Linesusedon31.12.2010 74,385,000 25,000,000 0

Within the framework of the credit agreement signed with its banks, Montupet SA is committed to:

• transferring its customer receivables as a guarantee;

• ensuring that the total nominal amount of receivables transferredisatleastequalto60%ofthetotalamountof advances in Tranche B, which stood at 25,000,000 euros on 31 December 2010;

• domiciling all its transferred customer receivables to the collection account opened with the BECM;

• respecting, on the basis of the consolidated accounts, the following ratios amended by the additional clause of 29 July 2010:

Annual Report MONTUPET / Management report / 29

2

1

6

5

4

3

On31December2010,MontupetSAwasfulfillingallthecommitmentsofthecreditagreement.

Theaccountsscheduleiscurrentlybeingre-negotiatedwiththelenders'pool.

• Industrial and legal risks linked to the environment

Montupet is concerned to control the environmental effects of industrial sites and the associated risks. The group's activities are governed by traditional systems, declarationsandoperationsspecifictoeachcountry.In addition to the national and local regulations, the different categories of activity may be governed by spe-cificauthorisations.Statutoryconformityismanagedoneachsitebymeansofanon-goingimprovementprocedure.

The risks linked to the environment are those which stem from the use and disposal of mineral oils, chemi-cals(amines,volatilecomponents,solvents,paint,mas-tics and adhesives), the casting of aluminium, air com-pression and radiography workshops. Facilities have beenestablishedfordustandoilremovalfilters,therecyclingofsand,chipsandoilandthermaloxidisers;regular supervision is carried out. A number of sites possess their own water treatment plants. Emergency plansandfirepreventionsystemsexistonallsites.

InFrance,theLaignevillesitewhichMontupetrentsissituated on land which has been polluted by its previous occupant(Desnoyers),whoiscontractuallyresponsiblefor its decontamination.

MontupetSA,andmorespecificallytheLaignevillefactory, received a formal notice on 13 January 2010 concerning the choice of the foundry sand elimination system; the system was changed at the end of February and the formal notice was withdrawn on 15 June 2010.

Comments on the environmental consequences linked to the activity are presented a few pages further.

• Insurance policy

Montupet SA and its subsidiaries are covered by in-surance policies for risks associated with "material damage/operating losses" within the general limits of the guarantee of 250 million euros and for "operating liability" risks up to 50 million euros per claim and "pro-duct liability" up to 50 million euros per year.

At 31.12.2010 At 30.06.2011 At 31.12.2011 At 30.06.2012

Equity at least equal to 125,000,000 125,000,000 135,000,000 135,000,000

Netfinancialdebtatleastequalto 130,000,000 110,000,000 90,000,000 90,000,000

Gearing ratio < 0.95 <0.88 < 0.66 < 0.66

Netdebt/Cashflow < 3.5 < or = to 3 < or = to 3 < or = to 3

Annual Report MONTUPET / Management report / 30

2

1

6

5

4

3

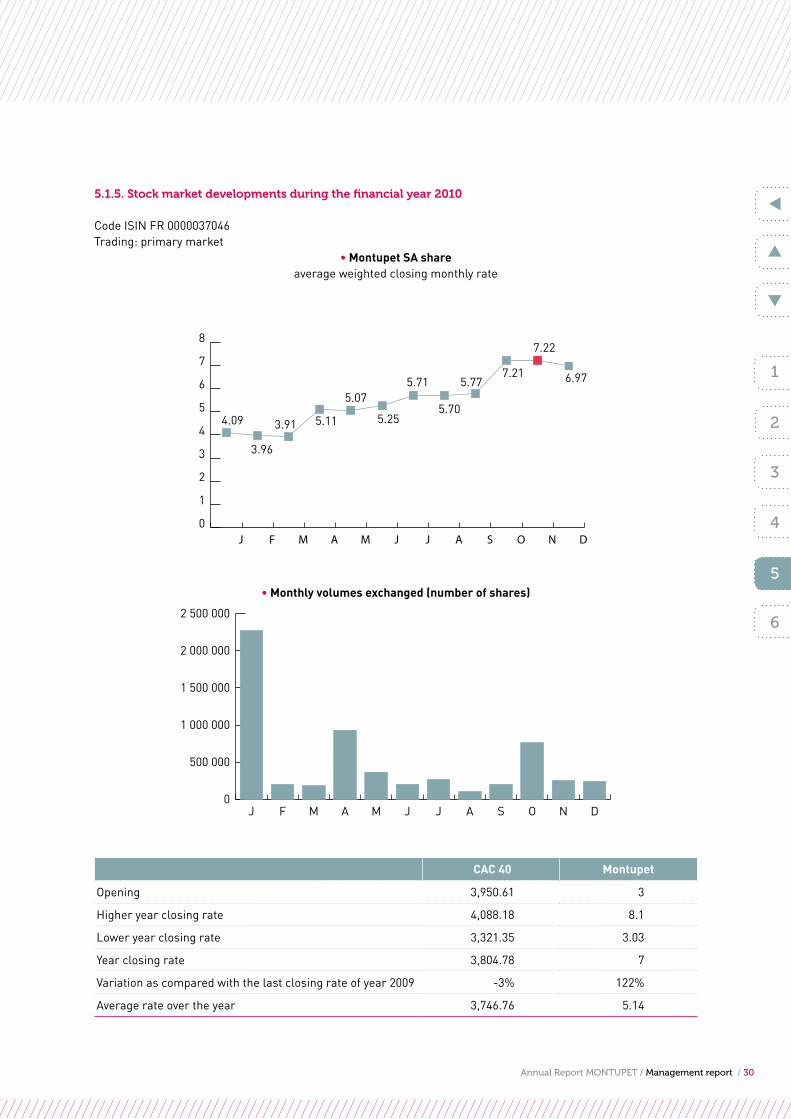

5.1.5. stock market developments during the financial year 2010

CodeISINFR0000037046Trading: primary market

• Montupet SA share average weighted closing monthly rate

0

1

2

3

4

5

6

7

8

DNOSAJJMAMFJ

4.09

3.96

3.91 5.11

5.07

5.25

5.71

5.70

5.777.21

7.22

6.97

• Monthly volumes exchanged (number of shares)

0

500 000

1 000 000

1 500 000

2 000 000

2 500 000

DNOSAJJMAMFJ

CAC 40 Montupet

Opening 3,950.61 3

Higheryearclosingrate 4,088.18 8.1

Loweryearclosingrate 3,321.35 3.03

Year closing rate 3,804.78 7

Variationascomparedwiththelastclosingrateofyear2009 -3% 122%

Average rate over the year 3,746.76 5.14

Annual Report MONTUPET / Management report / 31

2

1

6

5

4

3

5.2. Research & Development

In2010 theR&Dexpensesof theMontupetGroupamountedto24.5M€.Thisamount,whichissignifi-cantlyhigherthanthe2010budget(21.1M€),corres-ponds to the highest level of R&D business in the history of the Group.

This activity illustrates, on the one hand, the intensity of the research efforts made by Montupet in providing its customers with solutions in order to produce more efficientvehicleswhoseenergyconsumptionisreducedand which respect the environment and, on the other, the acceleration of the application of these solutions in customer programmes.

The implementation of European, national and regional financingandinparticulartheuseoftheResearchTaxCredit mechanism, are helping to sustain this effort. The amountofResearchTaxCreditfor2010businesswas2,897K€(comparedwith3,352K€ for 2009 business).

The entire R&D programme focuses on making lighter and more reliable vehicles with a particular focus on the downsizing of engines, or in other words increasing the power per litre of displacement which currently stands at 100 hp per litre for a number of current petrol and diesel models.

The notable elements in 2010 included the following achievements:

rESEArCh

• Materials and thermal processing

Work was carried out in close cooperation with our cus-tomersinthedevelopmentofhighlysought-aftercylin-der heads using new material and thermal processing concepts. The initial customer results have revealed a level of material performance which has never been attained before.

Work on the modelling of residual constraints and microstructure predictions will add to the range of software available from Montupet for the calculation ofpartsirrespectiveoftheircomplexityandconditionsof use.

• ProcessesTheTomographXwaslaunchedinthemiddleof2010atthe“centreV.E.R.T”inLaigneville(GroupcylinderheadR&D sector). This original dual source tool can be used fortheprecisethree-dimensionalreconstitutionoftheexaminedpartsaswellasaquantitativeanalysisofthedimensions and condition of the material.

The information is used for the development of cylin-der heads but also, by comparing the actual situation with digital simulation, to improve the precision and responsespeedofcastingandsolidificationsimulationsoftware. Theaimofthisprogramme(FederTomopic)isalsotodistributetomographyXamonglaboratoriesandfirmsin the Picardy region.

• Development tools

Action has been taken and partnerships established to obtain process and calculation method simulation software which is more powerful than the software cur-rently in use by focusing on highly parallel calculations. Virtualdigitaldevelopmentprovidesaresponsetotherequirements of our customers who are seeking faster developmentofincreasinglycomplexparts.

DevelopMent

Thanks to the establishment in 2010 of a low pressure machinewithsidegate(BPAL),the“centreV.E.R.T.”possesses casting resources which are representative of all the Group's factories including the recently acquired subsidiary,thePoitouAluminiumfoundry.ThisBPALtechnology is particularly suitable for the creation of new engine block structures in aluminium.

ALP"AdvancedLowPressure",anewgenerationoflowpressure casting, has been used on the Ford Puma I5 dieselcylinderheadinLaigneville.Thisprocessallowsforreducedproductioncosts (characteristicof lowpressure) with enhanced mechanical properties in the cylinderheadasawhole(betterthananyotherfoundryprocess).

The tilt casting of cylinder heads has been launched onthesitesofRoussé(Bulgaria)andTorréon(Mexico)withflexibleproductionresourcesrepresentingthenewstandardproductionmodulesofMontupet.Torréonhassuccessfully launched this technology with a Daewoo dieselcylinderheadwhichisalsothefirstMontupetpart to be produced in a batch run with air quenching.

Theteamsfromthe“centreV.E.R.T.”havesupportedthelaunchofproductioninRousséandtakenpartinthetechnical training of staff at this new factory. This team work, which has been upheld in terms of production by staff from different Group factories, resulted in 2010 in the attainment of a high level of autonomy within the Bulgarian factory and internal quality and customer levels comparable with those of the most successful Montupet factories. This performance has been achie-ved with highly technical products, including a BMW

Annual Report MONTUPET / Management report / 32

2

1

6

5

4

3

cylinderhead,whichisoneofthemostsought-afterinthemarket,andV6Audicylinderheadswhosewatercirculation system and sizing and metallurgical requi-rementsarethemostdifficultknowntodate.

The equipment standardisation policy introduced seve-ral years ago is bearing fruit: it has led to a reduction in acquisition costs, the acceleration of production launches,greaterflexibilityinthedistributionofactivi-ties between the different sites and the reuse of equip-ment for new production lines.

The development of the engine market is characte-risedbythelarge-scaleintroductionofsuperchargedengines, for which the factory in Alumalsa develops turbocharger casings.

The development of cylinder head designs is charac-terisedbytheintegrationoffunctions:forexample,thenewgenerationsofdieselenginesuchastheDVlaunchedforPSAinBelfastandthehigh-performanceversionofK9KlaunchedforRenaultinLaignevilleincor-porate the intake manifold in the cylinder head itself.

Some of Montupet's customers frequently use cylinder headswithintegratedexhaustmanifoldswhichallowsfor a further reduction in the number of engine com-ponents, making engines more compact and lighter whilst reducing consumption and emissions to enhance performance. The preparatory work carried out over recent years by Montupet has allowed for numerous developments of this type of cylinder head, which are considerablymoredifficulttocastthanthosewithamore traditional structure, for future production in Roussé,BelfastandTorréon.

In general, the work which has been carried out in recentyearsintheR&Dfieldhasdevelopedsolutionswhichcorrespondexactlytocustomers'requirementsin terms of Euro 5 and Euro 6 generation diesel, petrol and hybrid engines.

Alongside these developments, structural components have been developed for electric vehicles with a view to aproductionlaunchinChâteaurouxin2011.

The 2011 budget remains at a similar level as in 2010 at23.8M€.

Annual Report MONTUPET / Management report / 33

2

1

6

5

4

3

5.3. -Legal information concerning the company and its capital

5.3.1. general information on the company

• Corporate name and addressMontupet SA, 202 Quai de Clichy, 92110 Clichy

• legal form and registrationMontupet, a limited liability company under French law withacapitalof16,389,808.88eurosisenteredinthetrade and companies' register of Nanterre under num-ber:542050794.

• Corporate aimManufacturing of parts and equipment intended for the mechanicalindustry-directorindirectinvolvementinall companies liable to develop social affairs.

• Trading yearThe trading year, which covers a period of 12 months, begins on 1 January and ends on 31 December.

• Montupet stock marketMontupet's shares are listed in compartment C of the EuronextmarketinParis.ISINcode:FR0000037046Mnemo : MON

5.3.2. company representatives and board members

remuneration of company representatives The amounts paid by the company or the companies whichitcontrolsasremunerationandbenefitsforcom-panyrepresentativesduringthefinancialyear2010were:

• forMrStéphaneMagnan,ChairmanandManagingDirector:988,952eurosgross,

• forMrDidierCrozet,ExecutiveManagingDirector:290,896eurosgross,including30,000eurosasremu-nerationforpositionofExecutiveManagingDirectorofMFT-MontupetSNC,

• forMrMarcMajus,ExecutiveManagingDirector:652,364eurosgross,

ThegrossremunerationofMrMagnanisdown0.3%comparedwith2009and thatofMrMajus isdown3%.Thesevariationsareduetothedecreaseinsocialsecurity contributions paid by the Montupet group for theirbenefitwhichstoodat44,567eurosand28,211eurosrespectivelycomparedwith47,302eurosin2009.Their net remuneration paid by the group, from which social security contributions are deducted, remains unchanged.

The gross remuneration of Mr Crozet has increased by 0.1%.

Thesefiguresdonotincludeanyvariableorexceptionalshares. No commitments have been made towards the company representatives apart from the managers' pen-sioncommitmentswhicharenotspecificandwhichareincluded in the pension commitments under liabilities in the consolidated balance sheet.

Duringthefinancialyear2010andthepreviousfinancialyear, no call options or stock options were attributed to the company representatives.

No option or subscription programmes allowed for the taking up of options of this type. No performance shares were attributed and no such shares became available duringthefinancialyear.

Noexceptionalremunerationwasattributed.

Annual Report MONTUPET / Management report / 34

2

1

6

5

4

3

Acquisition of Montupet SA shares by Mr François Feuillet, board member

Date Quantity unit Price Amount including extra costs

09/08/10 6 5.91 € 35.46€

10/08/10 977 5.91 € 5,775.16 €

10/08/10 1,000 5.81€ 5,810.00€

12/08/10 1,000 5.70 € 5,700.00 €

23/08/10 1,000 5.47€ 5,470.00€

Acquisition of Montupet SA shares by Mr Jean Berruyer, board member

Date Quantity unit Price Amount including extra costs

26/03/10 1,000 3.90 € 3,900.00 €

22/10/10 500 7.75 € 3,875.00€

Transfer of Montupet SA shares by Mr Jean Berruyer, board member

Date Quantity unit Price Amount including extra costs

27/04/10 1,000 5.68€ 5,680.00€

28/04/10 1,190 5.68€ 6,759.20 €

• transactions carried out by company managers concerning company securities during the financial year 2010

Annual Report MONTUPET / Management report / 35

2

1

6

5

4

3

• list of mandates carried out by board members during the financial year 2010

Mr sTepHane Magnan France / Within Montupet group (1)MontupetSA aluminiumfoundry,car-partsmanufacturer ChairmanandExecutiveManagingDirector

France / Outside Montupet group Chambre Syndicale de l'Aluminium DirectorGroupeDesIndustriesMétallurgiques(CIM) Director

Abroad / within Montupet group MFT-MontupetSnc(Belgium) serviceswithintheGroup Director(2)MontupetLimitée(Canada) aluminiumfoundry,car-partsmanufacturer ChairmanAlumalsa(Spain) aluminiumfoundry,car-partsmanufacturer Director(2)BSTooling(NorthernIreland) aluminiumfoundry,car-partsmanufacturer DirectorGesfitecLtd(NorthernIreland) holding Director(2)WillaceUKLtd(NorthernIreland) aluminiumfoundry,carpartsmanufacturer DirectorMontiacSAdeCV(Mexico) aluminiumfoundry,carpartsmanufacturer ExecutiveManagingDirectorMontupetInc(USA) commercialrepresentation Director(2)ChangzhouMontupetAutoPartsLtd aluminiumfoundry,carpartsmanufacturer Chairman Mr didieR cRoZeT France / Within Montupet group (1)Montupet SA aluminium foundry, carparts manufacturer DirectorandCo-ExecutiveManaging DirectorFrançaisede Roues aluminium foundry, carparts manufacturer Chairman

Abroad / Within MONTUPET group MontupetUKLtd (NorthernIreland) aluminiumfoundry,carpartsmanufacturer ExecutiveManagingDirector(2)MontupetGmbH(Germany) commercialrepresentation ChairmanMFT-MontupetSnc(Belgium) serviceswithintheGroup DirectorMontupetEOOD(Bulgaria) aluminiumfoundry,carpartsmanufacturer Co-ExecutiveManagingDirectorAlumalsa(Spain) aluminiumfoundry,carpartsmanufacturer Director(2)BSTooling(NorthernIreland) aluminiumfoundry,carpartsmanufacturer DirectorMontupetINC(USA) commercialrepresentation Director Mr MaRc MaJUs France / Within Montupet groups (1)MontupetSA aluminiumfoundry,carpartsmanufacturer DirectorandExecutiveManagingDirector Abroad / Within Montupet group MFT-MontupetSNC(Belgium) serviceswithintheGroup DirectorMontupetEOOD(Bulgaria) aluminiumfoundry,carpartsmanufacturer Co-ExecutiveManagingDirector(2)MontupetLimitée(Canada) aluminiumfoundry,carpartsmanufacturer SecretaryAlumalsa(Spain) aluminiumfoundry,carpartsmanufacturer Director(2)BSTooling(NorthernIreland) aluminiumfoundry,carpartsmanufacturer DirectorandSecretaryGestifecLtd(NorthernIreland) aluminiumfoundry,carpartsmanufacturer DirectorandSecretaryMontupetUKLtd(NorthernIreland) aluminiumfoundry,carpartsmanufacturer Secretary(2)WillaceUKLtd(NorthernIreland) aluminiumfoundry,carpartsmanufacturer DirectorandSecretaryMontiacSAdeCV(Mexico) aluminiumfoundry,carpartsmanufacturer Secretary,TreasurerandViceChairmanMontupetINC(USA) commercialrepresentation DirectorandSecretary(2)CHangzhouMontupetAutoPartsLtd aluminiumfoundry,carpartsmanufacturer Supervisor

Annual Report MONTUPET / Management report / 36

2

1

6

5

4

3

Mr Jean BeRRUYeR France (1)Montupet SA aluminium foundry, carparts manufacturer Director M. fRancois feUilleT France/Trigano group Autostar SAS leisure vehicles manufacturer Chairman CaravanesLaMancelleSARL leisurevehiclesmanufacturer ManagerClairval SAS camping equipment ChairmanCMC France SCP holding Manager Ecim SAS trailers manufacturer ChairmanEuro Accessoires SAS leisure vehicles accessories ChairmanEurop’HolidaysSARL leisurevehiclestrading ManagerLoisirsFinancePublicCywithManagementandSupervisoryBoard leisurevehiclesfinancing BoardMemberMaitre Equipement SAS leisure vehicles accessories ChairmanMecadisSARL trailerstrading ManagerMecanoremSARL trailersmanufacturing ManagerMistercamp SA motor home rental Chairman PerigordVéhiculesdeLoisirsSAS leisurevehiclesmanufacturer ChairmanRivieraFranceSARL leisurevehiclestrading ManagerRulquin SA leisure vehicles accessories Chairman TechwoodSARL carpentryforleisurevehicles Manager(1)TriganoSA Triganogroupmothercompany ChairmanandExecutiveManagingDirectorTrigano Jardin SAS Garden equipment Supervisory Board Member Trigano MDC SAS camping equipment Chairman of Supervisory Board Trigano Remorques SAS trailers manufacturing ChairmanTriganoServiceSARL leisurevehiclesaccessories ManagerTriganoVDLSAS leisurevehiclesmanufacturer ChairmanTroisSoleilsSARL leisurevehiclesrentals Manager

France / Outside Trigano group CICBanqueCIO-BROSA bank DirectorGroupement Foncier Agricole DomaineFrançoisFeuilletGFA vineyard ManagerGroupement Foncier Agricole FrançoisFeuilletGFA vineyard Manager(1)Montupet SA carparts Director SociétéCivileImmobilièreLiliOneSCI realestaterental ManagerSociétéCivileImmobilièreSEVOneSCI realestaterental Manager

Abroad / Trigano group Arca Camper SPA(Italie) leisurevehiclesmanufacturer ChairmanAuto-TrailVRLtd(Grande-Bretagne) leisurevehiclesmanufacturer ChairmanBenimar-OcarsaSA(Espagne) leisurevehiclesmanufacturer ChairmanandDirectorDelwynEnterprisesLtd(Irlande-du-Nord)(PrivateCompany) Garden equipment Director

Annual Report MONTUPET / Management report / 37

2

1

6

5

4

3

DeutscheReisemobilVermietungsGMBH(Germany) leisure vehicles rentals Manager ETRiddiough(Sales)Ltd(UnitedKingdom) leisurevehiclesaccessories DirectorGroveProductsLtd(UnitedKingdom) leisurevehiclesaccessories DirectorPolytexSARL(Tunisia) campingequipment ManagerSorelpolSpzoo(Poland) trailersmanufacturer ManagerTriganoDeutschlandVerwaltungsGMBH(Germany) holding ManagerTrigano GMBH(Germany) leisurevehiclestrading ManagerTrigano SPA(Italy) leisurevehiclesmanufacturer ChairmanTriganoVanSrl(Italy) leisurevehiclesmanufacturer(vans) Chairman

(1) Companies which publicly call upon savings.(2) Inactive companies.

5-3-3-subsidiaries and holdings

On 31 December 2010, the company Montupet SA controlled the following subsidiaries:

MFT Sarl 100% services within the Group France

MFT Montupet Snc 100% services within the Group Belgium

MontupetUKLtdanditssubsidiariesWillaceLTD,BSToolingLTD,GesfitecUKLtd

100% aluminium foundry, carparts manufacturerUnitedKingdom/Northern Ireland

CalcastLtd 100% aluminium foundry, carparts manufacturer Northern Ireland

FDPA(FonderiedePoitouAluminium)(subbranch)

100% aluminium foundry, carparts manufacturer France

MontupetLimitée 100% aluminium foundry, carparts manufacturer Canada /Quebec

Alumalsa 99.67% aluminium foundry, carparts manufacturer Spain

MontiacSAdeCV 100% aluminium foundry, carparts manufacturer Mexico

Montupet INC 100% commercial representation USA

Montupet GMBH 100% commercial representation Germany

Montupet EOOD 100% aluminium foundry, carparts manufacturer Bulgaria

(1) Inactive.

None of the controlled companies holds shares in Montupet SA.

notable events during this financial year: TheChinesesubsidiaryChangzhouMontupetAutopartswastransferredinOctober2010andthecompanyFrançaisedeRouesSASwas transferred on 30 June 2010.

Annual Report MONTUPET / Management report / 38

2

1

6

5

4

3

5.3.4. share capital and shareholding

• Type of capital

ShArES CATEGOryNumber of shares

2009 variation 2010

Shares with a single voting right 6,751,486 96,788 6,848,274

Shares with a double voting right 4,031,283 -96,788 3,934,495

ToTal 10,782,769 - 10,782,769

• Capital holding

NAME Number of shares at

31/12/2010

% Capital at 31/12/2010

Existing voting rights (even not

exercisable if any)

% Existing voting rights

M.StéphaneMagnan 1,172,503 10.87% 2,319,001 15.8%

M.MarcMajus 1,150,016 10.67% 2,285,032 15.5%

M. Didier Crozet 1,053,238 9.77% 2,106,476 14.3%

M. Philippe Mauduit 448,006 4.15% 896,012 6.1%

RichelieuFinanceGestionPrivée 534,173 4.95% 534,173 3.6%

Financièredel'Échiquier 1,077,247 9.99% 1,077,247 7.3%

Financièredel'Échiquier(fondsgérés)

682,411 6.33% 682,411 4.6%

Quaeroq 965,000 8.95% 965,000 6.6%

Orsay Asset Management 537,922 4.99% 537,922 3.7%

Public 3,162,253 29.33% 3,313,990 22.5%

ToTal 10,782,769 100% 14,717,264 100%

• Exceeding the threshold

In a letter received on 30 December 2010, the general partnership Orsay Asset Management, acting on behalf of the funds which it manages, declared:

• inthecontextofanadjustment,thatithadexceededthethresholdof5%ofthecapitalofMontupeton2 November 2010 and that it held on behalf of said fund578,005Montupetsharesrepresentinganequi-valentnumberofvotingrights,amountingto5.36%ofthecapitaland3.93%ofthevotingrightsofthiscompany. This crossing of the threshold is the result of the acquisition of Montupet shares in the market.

• thatithadfallenbelowthethresholdof5%ofthecapital of Montupet on 30 December 2010 and that it held on behalf of said fund 537,922 Montupet shares representing an equivalent number of voting rights, amountingto4.99%ofthecapitaland3.65%ofthevoting rights of this company. This crossing of the threshold is the result of the transfer of Montupet shares in the market.

Annual Report MONTUPET / Management report / 39

2

1

6

5

4

35.3.5. auditors' fees

Auditors fees paid in 2010 Bellot, Mullenbach & Associés Cabinet Guilleret & Associés

216,000 63,000

5.3.6. Miscellaneous information

• use of existing delegations for new equity issues

Thejointgeneralmeetingof29June2010authorisedthe Board of Directors to issue new share capital for amaximumnominalamountof6millioneuros;thisdelegationwastobevalidforaperiodoftwentysixmonths. The Board of Directors has not made use of this delegation to date.

• Tax information

Nontax-deductibleexpenses

In accordance with the provisions of article 223 d of theGeneralTaxCode,weshouldpointoutthatthefollowing amounts were added back for the determi-nationofthetaxableincome:

• surplusdepreciationforcompanyvehiclesamountingto 35,917 euros,

• ataxoncompanyvehiclesamountingto37,190euros.

• Transactions relating to the share capital carried out during the financial year

No transactions relating to the share capital were car-riedoutduringthefinancialyear2010.

• Information on option plans, salaried shareholders, share redemption programmes

• Option plansBy delegation, the board of directors did not grant any options for company representatives or employees of the company or associated companies granting the right to purchase company shares.On 31 December 2010, no option plans were open or liable to be opened as a result of authorisation by a generalmeetingoftheexistingshareholders.

• Salaried shareholdersOn 31 December 2010, the term salaried shareholders asdefinedaccordingtothetermsofarticleL.225-102ofthe Commercial Code was limited to shares held within the framework of the company savings plan and stood at61,750sharesrepresenting0.57%ofthecapital.On31 December 2010, no registered shares which could not be freely transferred were held by the employees. Thefirmisnotawareofanybearersharesheldbytheemployees.

• Transactions carried out by Montupet with its own sharesMontupet did not carry out any transactions with its own sharesduringthefinancialyear2010.

Annual Report MONTUPET / Management report / 40

2

1

6

5

4

3

• Questions on the agenda of the General meeting

Proposed allocation of results The proposed allocation of results has been decided by the board of directors as follows:

- 51,876eurosaslegalreserve,whichincreasesfrom1,587,105eurosto1,638,981euros,

- 1,293,932eurosasdividends, i.eadividendof0.12 euro per share,

- and6,986,244eurosincreasingtheaccumulatedprofit,fromadebitbalanceof2,361,533eurostoacreditbalanceof4,624,711euros.

Other questions on the agenda of the General meeting In addition to the items traditionally put forward at the ordinary general meeting: approval of the company ac-countsandconsolidatedfinancialstatements,ratifica-tion of the regulated agreements, allocation of results, the Board of Directors made the following suggestion at the meeting:

- the allocationof directors' fees amounting to10,000 euros for board members.

• Itemsappendedtothemanagementreport- Tableofresultsforthepastfivefinancialyears,- Chairman'sreportoninternalauditing.

• Amount and tax status of dividends

fiscal year Net dividend Tax relief

2007 0.13 Eligiblefor40%tax

relief

2008 -

2009 -

Asfarasdividendseligibleforthe40%deductionareconcerned, each shareholder may opt for the levy at sourceof19%;thisoptionexcludesthe40%deductionandtheannualdeductionaswellasthetaxcredit.

The option may be partial or total but it is irrevocable andmustbeexercisedwiththecompanybyeachsha-reholder concerned at the latest by the time of the divi-dendpayment.Iftheoptionisexercised,thecompanywillpayadividendreducedby31.3%(19%+12.3%insocial security contributions) and the corresponding amount will be paid directly to the treasury. The sha-reholders are informed that, in the case of a partial option for the levy at source, the dividends for which this option has not been applied would be liable to income taxwithoutthe40%deductionandwithoutbenefitingfromthetaxcredit.

Theoptionforthelevyatsourcedeprivesthebeneficiaryof the possibility of deducting the CSG levied at source for5.8%.Furthermore,fortheincometobetakenintoaccountinthecontextofthe"taxshield",thedividends

subjecttothelevyatsourceareretainedattheirgrossamount without deduction whereas, if this option is not exercised,thecategoricaltaxablenetincomeistakenintoaccountasincomefrommovableassets(thereforeafter deductions).

• Change in stock valuation methodSince 1 January 2010, raw material stocks, supplies, consumables and packaging have been valued accor-dingtothePUMPmethod(weightedaverageunitprice)as Montupet has changed its computer system and optedforanintegratedinformationsystem,SAGEX3,in which the management of stocks at the PUMP is recommended.Stocks were previously valued according to the FIFO method(firstin-firstout).Theeffectonthe2010ac-counts of this change in method

• Information on payment terms The following information is provided in accordance with

articleL.441-6-1oftheCommercialCode:- Thesubsidiariesrepresentmorethan25%ofthe

suppliers'accountsandarepaidwithin45daysfrom the end of the month, 30 days from the end of the month in the case of Montupet EOOD or by cur-rentaccountadjustment(MontupetUK,Montiac,FrançaisedeRouesSAS).

- ThesuppliersfromoutsidetheMontupetgroupcanbe broken down as follows:

<30 days 30 to 60 days >60 days Total TTC

In K€ 2010 2009 2010 2009 2010 2009 2010 2009

Supplier debts outside the group 12,849 3,669 4,769 5,533 1,077 62 18,695 9,264

Accrued invoices 2,936 4,256

ToTal 21,631 13,520

Annual Report MONTUPET / Management report / 41

2

1

6

5

4

3

5.4. Social indicators

The following information concerns Montupet SA.

• Payroll

Thetotalpayrollofthefirmamountedto976employeeson31December2010.Thefirmhired32individualsonfixed-termcontracts(comparedwith9in2009)and17onpermanentcontractsduringtheyear(comparedwith 12 in 2009). Thisyearasin2009,thefirmhasnotmadeanyredun-

dancies on economic grounds but has applied partial unemployment measures. Theproportionofpart-timejobsstoodat1%ofthetotalsalaried employees on 31 December 2010.Employeesagedunder35yearsaccountfor26%ofemployeescomparedwith24%in2009.

• Payroll

0

200

400

600

800

1000

1200

1400

1600

WorkersNon Executives Executives

201020092008

669

104127 100

347 251 256

1,097 616

• Age pyramid

0

50

100

150

200

55 years and +45 to 54 years35 to 44 years25 to 34 years18 to 24 years

249 3

118

5641

173

70

30

194

94

17

107

2713

WorkersNon Executives Executives

Annual Report MONTUPET / Management report / 42

2

1

6

5

4

3

• Seniority pyramid

• Organisation of working hours

• Type of employment

0

50

100

150

200

250

30 years and +25 to 29 years20 to 24 years15 to 19 years10 to 14 years3 to 9 years- 3 years

27 31 30

76

43 35

237

42

1224

10 3

104

58

16

56

32

2

92

40

6

WorkersNon Executives Executives

0

500

1000

1500

2000

201020092008

Day shift2 shifts3 shifts4 shifts

655

156133

627

485

193

342

528

190

258

Permanent contracts Fixed term contracts 0

10

20

30

40

50

60

70

80

ExecutivesNon Executives

Workers ExecutivesNon Executives

Workers ExecutivesNon Executives

Workers

2008 2009 2010

30

38 27

15

14

25

0

0

74

28

1

16

10

12 64

Annual Report MONTUPET / Management report / 43

2

1

6

5

4

3

• Salaries and social security expenses of Montupet SA (in K€)

• Type of departures

• remunerations

The salaries posted in the Montupet SA accounts in 2010(includingprovisionsforpaidholidays)amountedto28,973K€withsocialsecurityexpensesstandingat12,407K€.The"temporaryemployees"itemrepre-sented781.6K€.

TheemployeesbenefitfromaCompanySavingsPlanwithacontributionpaidbythefirm.Onthebasisofatotalindividualisationpolicyforallitsworkers,execu-tivesandnon-executives,thefirmstrivestodeterminethe contributions of each one to the development of business in value terms.

0

100

200

300

400

500

600

201020092008

Transfer to subsidiaries DeathEnd of fixed term contractsOthersEnd of apprentice ship contracts 10Early retirements & pensionsResignationsDismissals - other reasonsRedundancies 0Transfer to Française de Roues

33

5

63 48 8

3023

19

62

2222

24

2723

461

1

10

Salaries Social security expenses 0

10000

20000

30000

40000

50000

201020092008

44,279 18,948 28,110 11,740 28,973 12,407

The2009figureshavebeenreprocessedanddonotincludethesalariesforthe"wheels"activity.

Annual Report MONTUPET / Management report / 44

2

1

6

5

4

3

• Temporary staff expenditure of Montupet SA (in K€)

• Importance of subcontracting

In2010,thesubcontractingcostincurredbythefirmtotalled44,014,491eurosmainlyassociatedwithinter-nal subcontracting within the group. These amounts do not include the production referred to in the "maquila" contractconcludedwiththeMexicansubsidiaryMontiacSAdeCV(representing12,467,018eurosin2010).With regard to the choice of subcontractors and re-lationswiththelatter,thefirmisconcernedtoverifyand guarantee compliance with the provisions of the InternationalLabourOrganisation(ILO)agreements.The countries in which the company and its subsidiaries arebasedrespecttheILOagreements.Thesecountriesare:France,UnitedKingdom,Spain,Bulgaria,Canada,UnitedStatesandMexico.

• Professional relations and collective agreements

An additional clause to the company savings plan regu-lations was signed in 2010 with the aim of:

- supplementingtherangeoffundsproposedintheregulations with a shared return fund,

- definingthemanagementcompanyofsaidsharedreturn fund and supplementing the regulations accordingly,

- supplementingtheregulationswithanappendixproviding details of the characteristics of the sha-red return fund.

0

2000

4000

6000

8000

10000

201020092008

7829,992 110

Annual Report MONTUPET / Management report / 45

2

1

6

5

4

3

• Equal opportunities between men and women

Womenonlyrepresent11.7%ofthestaffofMontupetFrance(factoriesessentiallyemployingmaleworkers)butrepresent25%and14%respectivelyofexecutivesandnon-executivesofthefirm.Salaries are more or less equivalent between men and womenexceptintheexecutivecategoryduetotheexis-

tenceofahighlevelofturn-overamongfemaleexe-cutives in our provincial factories, which reduces their seniority and therefore their scope for development. 2.6% of women are employed on a part-time basis(comparedwith4.3%in2009);theyrepresent21.4%ofpart-timeemployees(comparedwith55.5%).

• Male/female distribution by professional category

• Employment and insertion of handicapped workers

Thefirm'saimistomakeiteasierforhandicappedworkerstoaccessitsjobs.On31December2010,itemployed45handicappedworkers.Thefirmisalsoattemptingtoinvolvefirmswhichemployhandicappedworkersasapriorityandpaysafinancialcontributionprovided for by law to approved organisations.

• health and safety

We are pursuing our policy to increase the involvement of all employees in the prevention of industrial acci-dents.In2010,8accidentsoccurredinthefactoriesofMontupet SA which incurred work stoppages.

• Training

3.2%ofthewagebillwasdedicatedtoprofessionaltraining in2010 (comparedwith2.85 in2009)with720traineesrepresenting74%oftheemployeesofMontupet SA. The most notable efforts were made in thefieldofbusinesstraininginlinewithourdesiretodevelop the skills and employability of employees.

• Social welfare workThe Establishment Committees budget amounted to 311,345euros.

• regional effects of business

Thefirmconductsastudyeachyearonthemanage-ment of skills and employment and their effects on theexternalenvironment.Itispresentedtothetradeunionrepresentativesofthefirminthecontextofanannual report.The establishments take into account the effects of their activities on regional development and local populations both in France and abroad in the following manner:

- prioritisingtherecruitmentofstafffromthelocallabour pool and measurement of the internal stabi-lity rate,

- usinglocalfirmsfortheprovisionofservicesandmonitoring of purchase volumes,

- supportingthelocalcommunityinvariousorgani-sations,

- developingspecialpartnershipswithschoolsanduniversities.

The establishments maintain frequent contacts with government representatives and the main economic and social players in their cities and regions.

0

20

40

60

80

100

WorkersNon Executives

ExecutivesWorkersNon Executives

ExecutivesWorkersNon Executives

Executives

Male Female18 11 7 22 16 8 25 14 9

82 89 93 78 85 92 75 86 91

2008 2009 2010

Annual Report MONTUPET / Management report / 46

2

1

6

5

4

3

• payroll of the Montupet Group on 31 December 2010

0 500 1000 1500 2000 2500 3000 3500

Total

Cumul United Sates

Canada

Mexico

Cumul Europ

Bulgaria

Spain

United Kingdom

France + Belgium 1,479

494

467

356

2,796

352

4

356

3,152

Annual Report MONTUPET / Management report / 47

2

1

6

5

4

3

5.5. -Environment and sustainable development

5.5.1. environmental appraisal of Montupet sa

• Introduction and scope of the report

This report presents the main indicators used to eva-luate the environmental performance of the French factoriesofMontupetSA,namelytheLaignevilleandChâteaurouxfactories,bothofwhicharecategorisedasfacilitiesclassifiedasenvironmentallysensitive.(ICPE).It also presents the type of organisation used on the production sites to deal with environmental challenges and site developments.

In2008and2009,themeasurementinstrumentswerenot able to differentiate between the "wheels" business, which was made into a subsidiary on 30 June 2009 and the main business of manufacturing cylinder heads and suspension parts in terms of consumption at the Châteaurouxfactory.However,thedatarelatingto2010does not take the "wheels" business into account.

The environmental policy of the French factories is structured around three main themes:

1. a statutory conformity commitment with the appli-cable legislation in terms of the environment,

2. the prevention of all pollution risks,

3.anon-goingimprovementprocedurewhichconcernsall areas of the environment : water, air, waste, energy and prevention of pollution risks.

TheLaignevillesitepossessesadevelopmentcentrewhich incorporates environmental protection as one of its operational criteria. The information provided cor-respondstothefinaluseoftheresources.Therefore,energy consumption and emissions relating to the pro-ductionoftheseresources(aluminium,gas,electricity)are not taken into account.

Annual Report MONTUPET / Management report / 48

2

1

6

5

4

3

CONSuMPTION Of rAw MATErIAlS

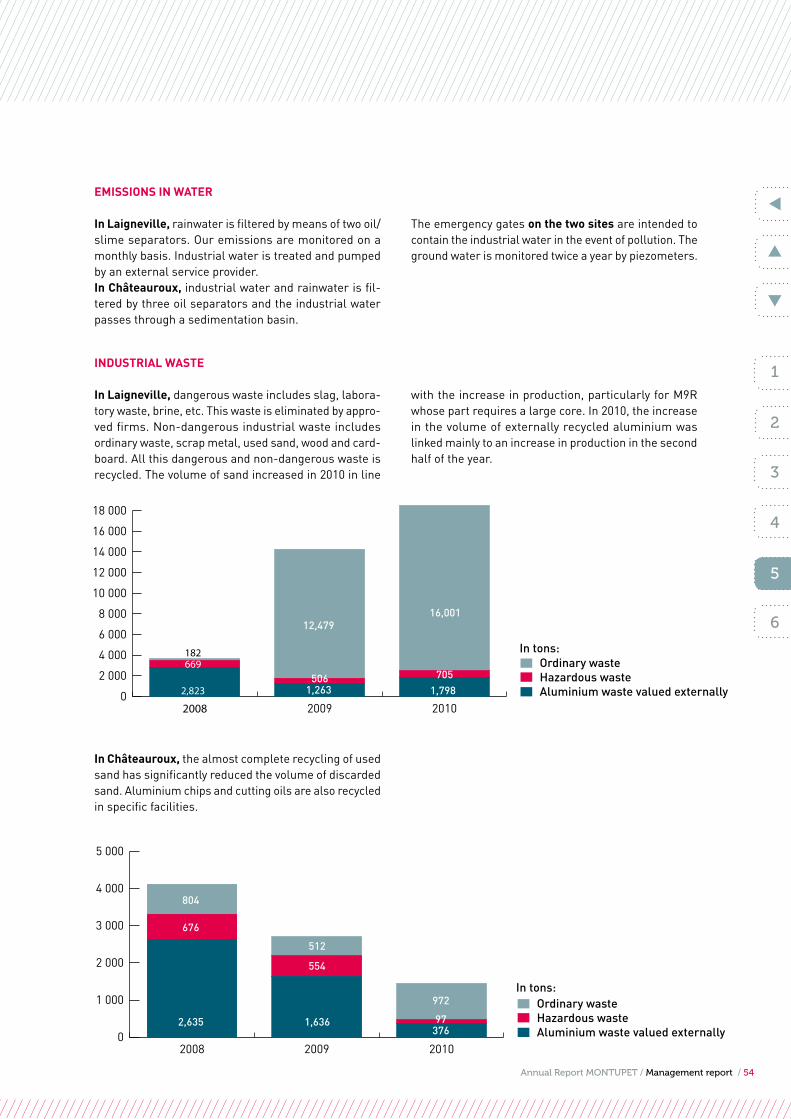

The main raw materials are aluminium and sand.

In laigneville, the consumption of aluminium and sand increasedsignificantlyfollowingtheincreasesinpro-duction during the 2nd half of the year. The used sand isscreenedand94.8%isrecycled.

In Châteauroux, lthe prototypes workshop uses new sand,96.5%ofwhichisrecycledforproductionbyaregeneration facility with a capacity of four tonnes per hourandanuntreatedsandprocessingsystem(non-polymerised sand obtained from the cleaning of shoo-ting heads).

0

5000

10000

15000

20000

25000

201020092008

6,115 Aluminium in tonsSand in tons

13,834 24,812 10,160 10,909 16,576

0

5000

10000

15000

20000

25000

30000

201020092008

20,26928,741 6,760801 260 569 Aluminium in tonsSand in tons

Annual Report MONTUPET / Management report / 49

2

1

6

5

4

3

1,760

Natural Gas consumption in m3 Ratio m3/cast aluminium ton

61,386

28,795

2,5652,465

28,210

0

1000

2000

3000

0

20 000

40 000

60 000

80 000

201020092008

1,150

Electricity consumption in m3 Ratio m3/cast aluminium ton

24,523

18,8171,398

98515,373

0

1 000

2 000

3 000

0

7 000

14 000

21 000

28 000

35 000

201020092008

6,739

Water consumption in m3

Ratio m3/cast aluminium ton

O.4 O.4

O.6

10,991

7,130

0,0

0,2

0,4

0,6

0,8

0

2 000

4 000

6 000

8 000

10 000

12 000

201020092008

ConSUMption of wAter AnD enerGy

In laigneville, water consumption has been reduced by improving the monitoring of consumption during machi-ning and passing a limited number of parts through the traditionalTTH.Asfarasgasconsumptionisconcerned,thereductionintheKWH/tonneofmeltedaluminiumratio is due to the optimum use of the FFC furnace for

large-scaleproduction.Theuseofcheckliststoensurethat lights are switched off when a team goes off duty, the optimisation of equipment opening times and the revision and maintenance of the facilities have improved the electricity consumption ratio.

Annual Report MONTUPET / Management report / 50

2

1

6

5

4

3

In Châteauroux, water is used by cooling towers, furnace hardening basins, surface treatment tunnels, casting platforms and the lubrication centre. Consumption has decreased in the cooling tower and has fallen below 5 m3/tonne and below the limit of 7 m3/tonne set by the order of the prefect. A steering committee meets every month to analyse consumption levels and ratios and to validate the action taken to reduce the latter. In addition, although the ratios for electricity and gas

showed an upward trend between 2009 and 2010 for all activities(FrançaisedeRouesandMontupetSA),theratios linked to the production of cylinder heads and sus-pensionparts(MontupetSA)improvedoverthatperiod.Campaigns have been conducted to eliminate air lea-kages on machines improving the output of air compres-sors. The energy steering committee analyses consump-tion levels and ratios with a view to reducing them.

5,657

Natural Gas consumption in m3 Ratio m3/cast aluminium ton

116,022

38,241

4,150

4,037

84,110

0

2000

4000

6000

0

50 000

100 000

150 000

201020092008

2,467

Electricity consumption in m3 Ratio m3/cast aluminium ton

56,105

1,996

1,952 40,447

0

1000

2000

3000

0

12 000

24 000

36 000

48 000

60 000

201020092008

16,676

26,509 Water consumption in m3

Ratio m3/cast aluminium ton

5 3.9

5143,992

101,122

0

2

4

6

8

0

50000

100000

150000

200000

201020092008

Annual Report MONTUPET / Management report / 51

2

1

6

5

4

3

ConSUMption of toxiC proDUCtS

Themainenvironmentallytoxicproductsusedbytheproduction sites are the phenolic resins used for the core making process. Since 2006, Montupet SA has no longerbeenusingorstockinghighlytoxicsubstancesand liquid preparations referred to in section n°1111.2.b oftheregulationsonfacilitiesclassifiedasenvironmen-tally sensitive. Chemicals are stored in retention contai-ners to prevent the risk of dispersion and in equipped storestopreventtheriskoffire.

In laigneville, the consumption of resin has increased following the increase in production in the second half of 2010.

In Châteauroux, the consumption of resin has increased following the increase in production in 2010.

Phenol in phenolic resins in tons Phenolic resins in tons

0

20

40

60

80

100

120

201020092008

72 68 87

43

4

Phenol in phenolic resins in tons Phenolic resins in tons

0

20

40

60

80

100

120

201020092008

101 53 88

5

3

4

Annual Report MONTUPET / Management report / 52

2

1

6

5

4

3

EMISSIONS IN ThE AIr

Emissionsintheairaresubjecttoregularmonitoringaccording to the regulations in force.

In laigneville,volatileorganiccompounds(VOC)stemmainly from core making and casting operations. The measurementpresentedin2010isbasedonaone-offmeasurementflow.Theflowfor2010amountedto2.5 kg/h compared with 2.2 kg/h in 2009. The change in greenhouse gas emissions is in proportion to that of natural gas consumption.

5 287

SO2 in tonsCO2 in tons

0.04 0.05

5,179

11,270

0.09

0

2 000

4 000

6 000

8 000

10 000

12 000

0,0

0,2

0,4

0,6

0,8

1,0

201020092008

0

5

10

15

20

COV in tonsNO2 in tons

5 12 12 6 16 6

201020092008

Annual Report MONTUPET / Management report / 53

2

1

6

5

4

3

In Châteauroux, emissions of volatile organic com-pounds stem from core making operations, the cas-ting of parts with cores and the application of paint on wheels.In 2006, the DRIRE (Regional Office for Industry,Research and Development) validated the plan for the control of emissions of volatile organic compounds intended to reduce atmospheric emissions from "core making"and"wheelfinishing"workshops.AnadditionalorderbytheprefectsetaspecificlimitforVOCemis-sionsof11.85kgofVOC/tonneofmetalproduced.TheEnvironmental Management System guarantees the statutory conformity of these emissions.

Improvementsintroducedin2008andpursuedinsub-sequentyearshaveledtoasignificantreductionintheseemissionsandconfirmedcompliancewiththeobjectivesetbytheDREAL:

• ThetotaleliminationofthecleaningsolventSOLV60 since January 2006, which represents a 2.6T re-ductioninVOCcomparedwith2000withequivalentproduction levels,

• thetotaleliminationofthereleaseagentKlüberchemsince October 2006, which represents an 11.5T re-ductioninVOCcomparedwith2000withequivalentproduction levels,

• theintroductionofsandeconomisersontheshootingheadsof3newtools(3newproductsplannedin2010on the Montupet site).

• maintainingthecorerejectrate(2009average=7.26%and2010average=7.67%)withincreasedactivity in 2010.

• thetestingofanewresintoreducetheresinintro-ductionpercentage(target-10%for2011)

• thereductionofthecorerejectrateto7%(7.67%achieved in 2010) in order to reduce the consumption of all the products required for core manufacturing,