Embed Size (px)

Citation preview

1 © 2018 Chapman Eastway

AUSTRALIAN GUIDE TO COMPLETING W-8BEN FORMS

CURRENT AS AT 18 OCTOBER 2018

2 © 2018 Chapman Eastway

Disclaimer: The information contained in this booklet is general in nature and does not constitute legal, financial or taxation advice. You should not rely on the information contained in this booklet and it is recommended that you seek independent professional advice relating to your specific circumstances. The information is current at the date of publication only. While we have made every attempt to ensure that the information contained in this booklet has been obtained from reliable sources, Chapman Eastway is not responsible for any errors or omissions, or for the results obtained from the use of this information at the date of publication. In no circumstances will Chapman Eastway be liable to you or anyone else for any decisions made or action taken in reliance on the information contained in the booklet or for any consequential, special or similar damages, even if advised of the possibility of such damages.

This guide is not to be used by US persons

3 © 2018 Chapman Eastway

Introduction

Thank you for choosing Chapman Eastway to assist you in completing your US W-8BEN forms. We are a firm of family and business advisors with a proud 120 plus year history and are delighted to bring you this publication. For an investor who is a non-resident of the US for income tax purposes and who derives certain income (e.g. dividends and interest) from US sources, the US Internal Revenue Service (IRS) requires certain documentation from the ultimate beneficial owner to ensure the appropriate level of tax is withheld in the US. Non-resident investors are subject to withholding tax of 30% on certain income derived from US sources. Where the requisite form is completed and submitted, a reduced withholding tax rate of 15% may apply for Australian income tax residents who derive any such income, in accordance with the Australia/US Double Taxation Agreement (DTA). Generally, a W-8BEN form will remain in effect until 31 December, three years after the date of signing. For example, a form signed on 15 April 2018 will remain in effect until 31 December 2021. However, if a change in circumstances makes any information on the form incorrect, the investor must submit a new W-8BEN form within 30 days of any such change.

Once the form is completed and signed, it should be sent to the requesting financial institution or withholding agent.

Do not send this form to the IRS.

This guide is designed to assist Australian Resident Companies, Trusts, Self Managed Superannuation Funds (SMSFs), Not-for-Profit Companies, Not-for-Profit Trusts and Individuals to complete the necessary US W-8BEN forms. This booklet does not constitute legal, financial or taxation advice. We strongly recommend you obtain professional advice which considers your specific circumstances. If you would like further assistance please contact Chapman Eastway.

4 © 2018 Chapman Eastway

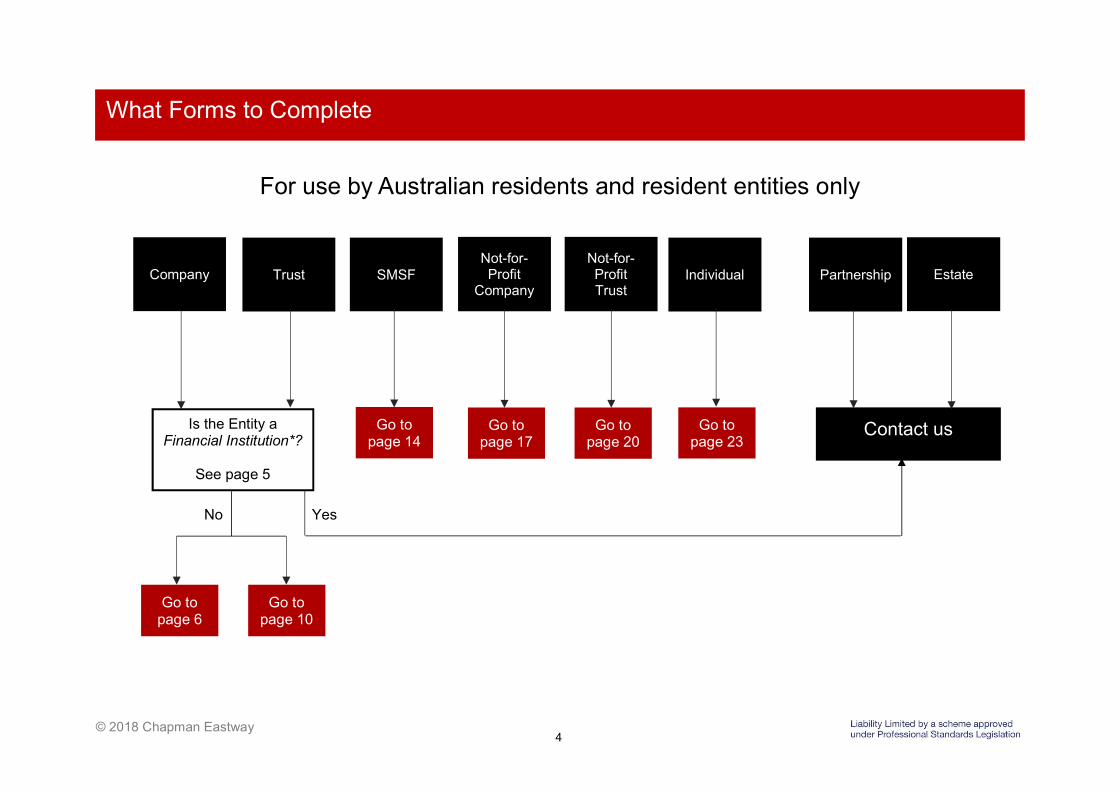

What Forms to Complete

Go to page 6

Go to page 10

Go to page 14

Company Trust SMSF Partnership

Contact us

For use by Australian residents and resident entities only

Go to page 17

Not-for-Profit

Company

Go to page 20

Not-for-Profit Trust

Estate Individual

Go to page 23

Is the Entity a Financial Institution*?

See page 5

No Yes

5 © 2018 Chapman Eastway

What Forms to Complete (continued)

* Financial Institutions include entities which meet the definition of an Investment Entity. The definition of an Investment Entity has the requirement that the trading, investing, administering or managing of financial assets on behalf of other persons is done as a business.

In addition, an entity that is managed by an Investment Entity is deemed to be an Investment Entity.

Company

Companies which are subsidiaries of entities which are Financial Institutions are themselves deemed to be Financial Institutions.

In addition, a company that is managed by an Investment Entity is deemed to be a Financial Institution.

Trust

For trusts, determining whether it is an Investment Entity requires consideration of the entity managing the trust. For example, if the trustee is an Investment Entity, the trust will be an Investment Entity. Also, if the trustee has appointed a professional manager (other than an individual) to manage the trust, the status of both the trustee and professional manager need to be considered.

It is outside the scope of this booklet to consider the reporting requirements for entities that determine they are Financial Institutions.

For more information, please see:

https://www.ato.gov.au/General/International-tax-agreements/In-detail/International-arrangements/Automatic-exchange-of-information---CRS-and-FATCA/

6 © 2018 Chapman Eastway

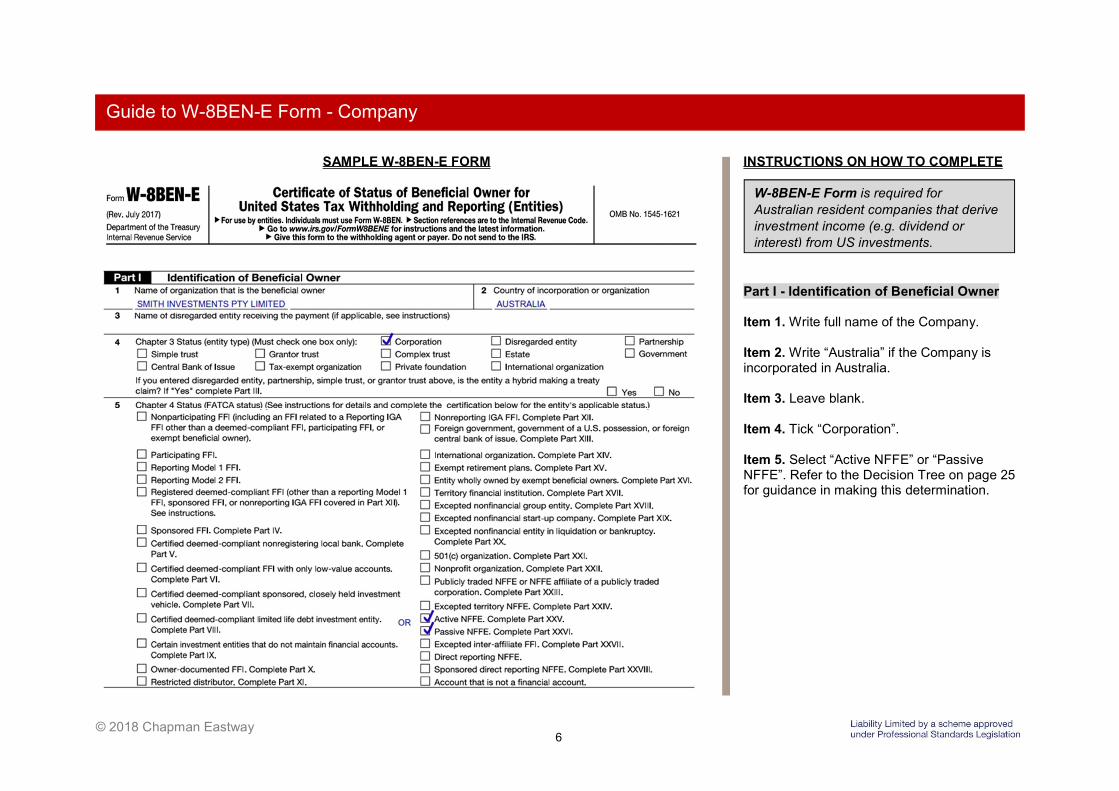

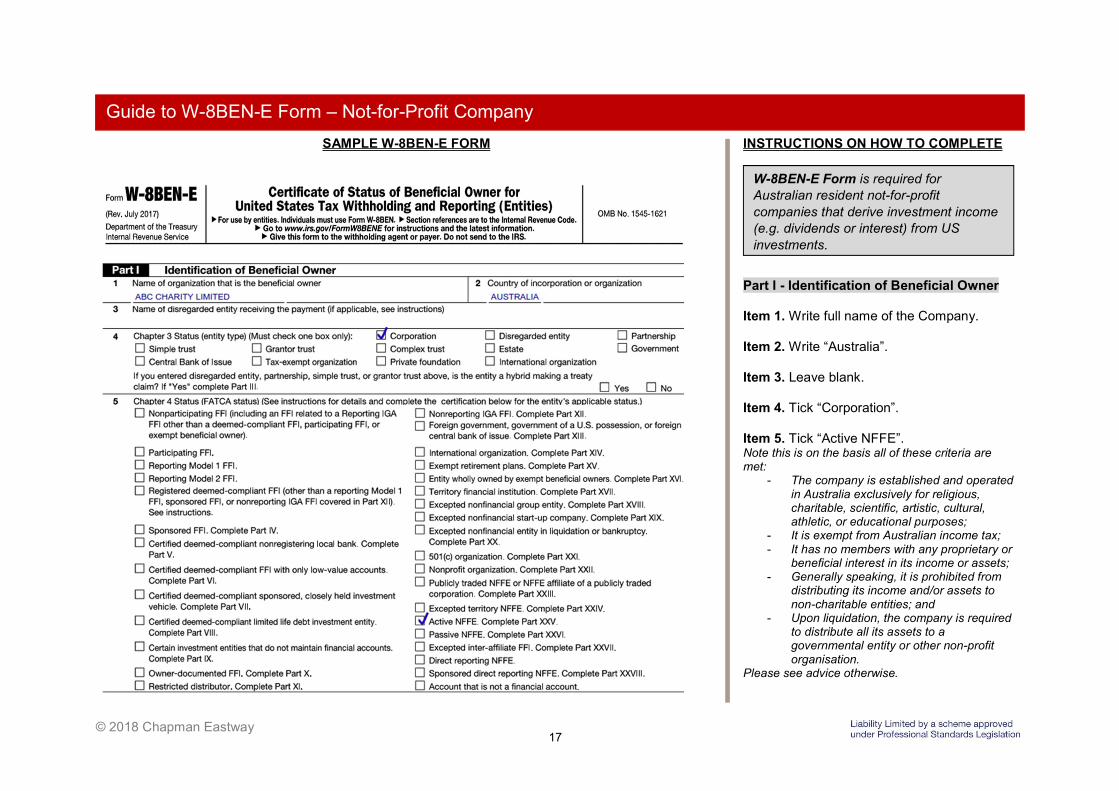

SAMPLE W-8BEN-E FORM INSTRUCTIONS ON HOW TO COMPLETE

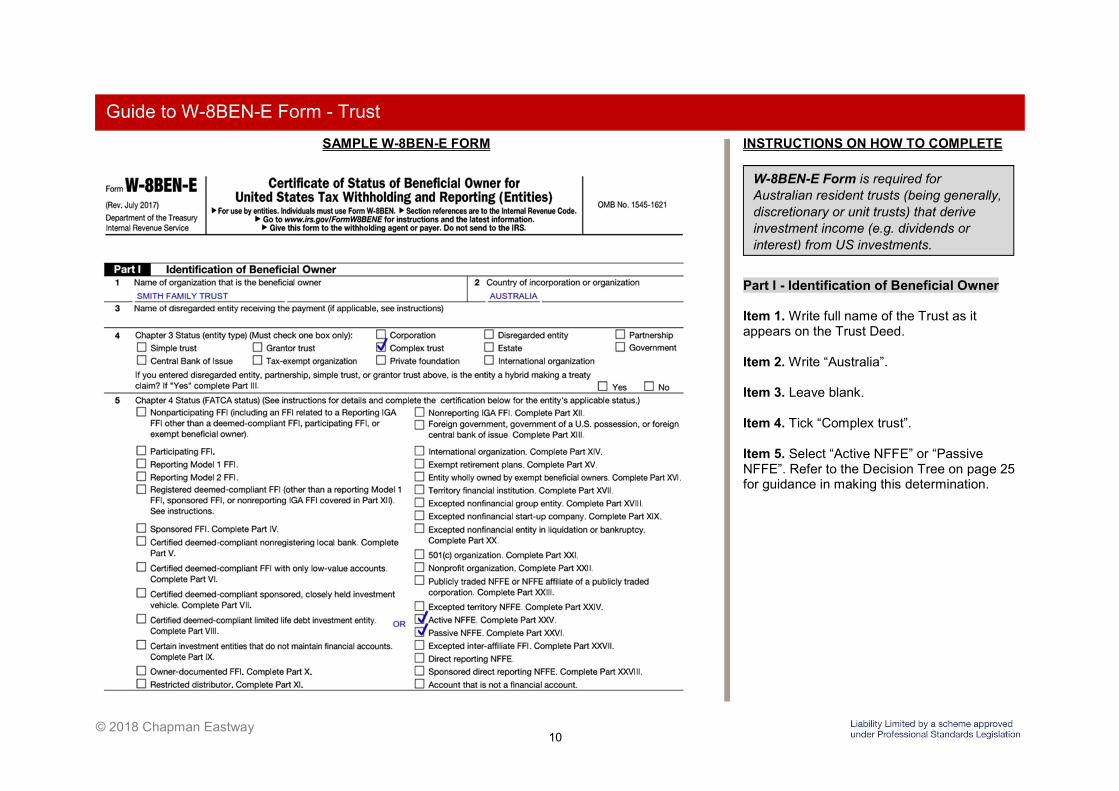

Part I - Identification of Beneficial Owner Item 1. Write full name of the Company. Item 2. Write “Australia” if the Company is incorporated in Australia. Item 3. Leave blank. Item 4. Tick “Corporation”. Item 5. Select “Active NFFE” or “Passive NFFE”. Refer to the Decision Tree on page 25 for guidance in making this determination.

Guide to W-8BEN-E Form - Company

W-8BEN-E Form is required for Australian resident companies that derive investment income (e.g. dividend or interest) from US investments.

7 © 2018 Chapman Eastway

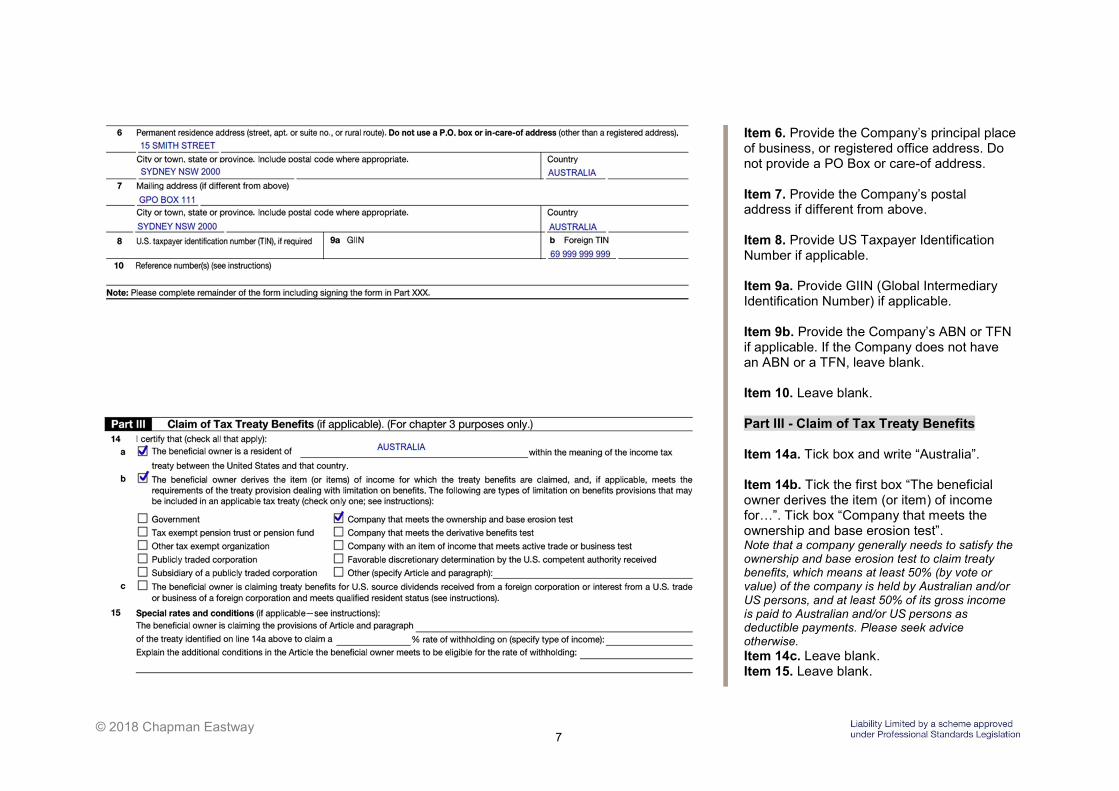

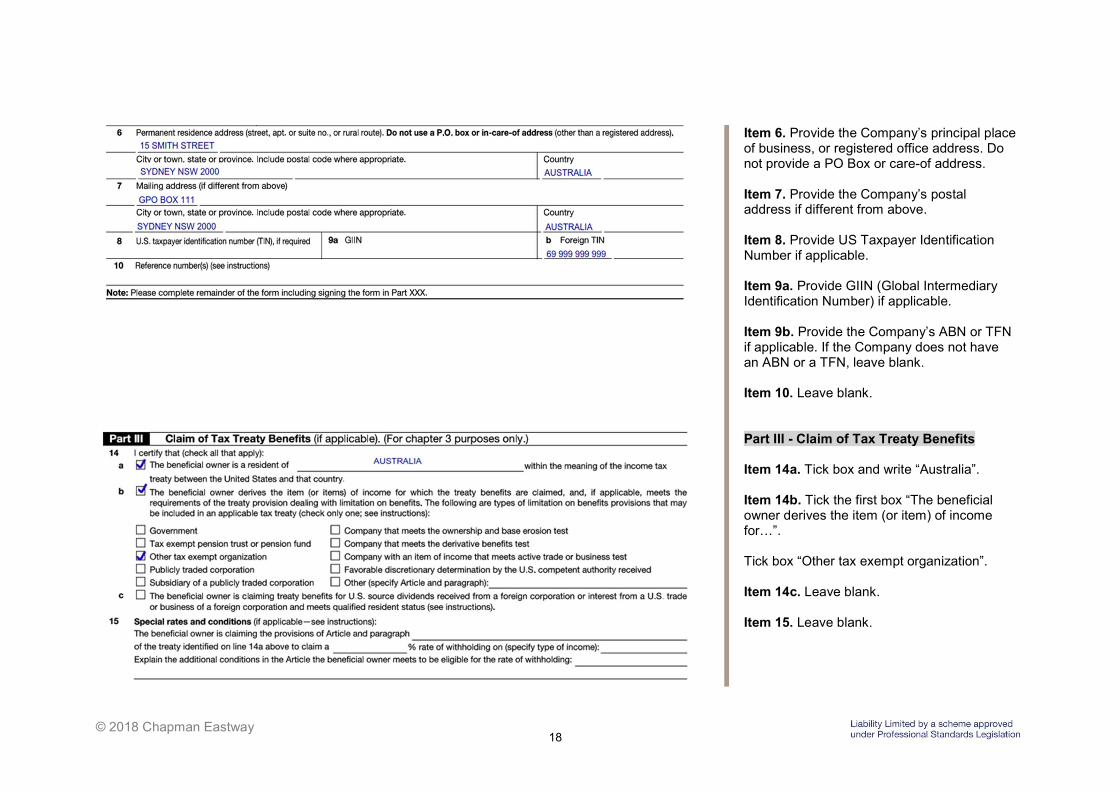

Item 6. Provide the Company’s principal place of business, or registered office address. Do not provide a PO Box or care-of address. Item 7. Provide the Company’s postal address if different from above. Item 8. Provide US Taxpayer Identification Number if applicable. Item 9a. Provide GIIN (Global Intermediary Identification Number) if applicable. Item 9b. Provide the Company’s ABN or TFN if applicable. If the Company does not have an ABN or a TFN, leave blank. Item 10. Leave blank.

Part III - Claim of Tax Treaty Benefits Item 14a. Tick box and write “Australia”. Item 14b. Tick the first box “The beneficial owner derives the item (or item) of income for…”. Tick box “Company that meets the ownership and base erosion test”. Note that a company generally needs to satisfy the ownership and base erosion test to claim treaty benefits, which means at least 50% (by vote or value) of the company is held by Australian and/or US persons, and at least 50% of its gross income is paid to Australian and/or US persons as deductible payments. Please seek advice otherwise. Item 14c. Leave blank. Item 15. Leave blank.

8 © 2018 Chapman Eastway

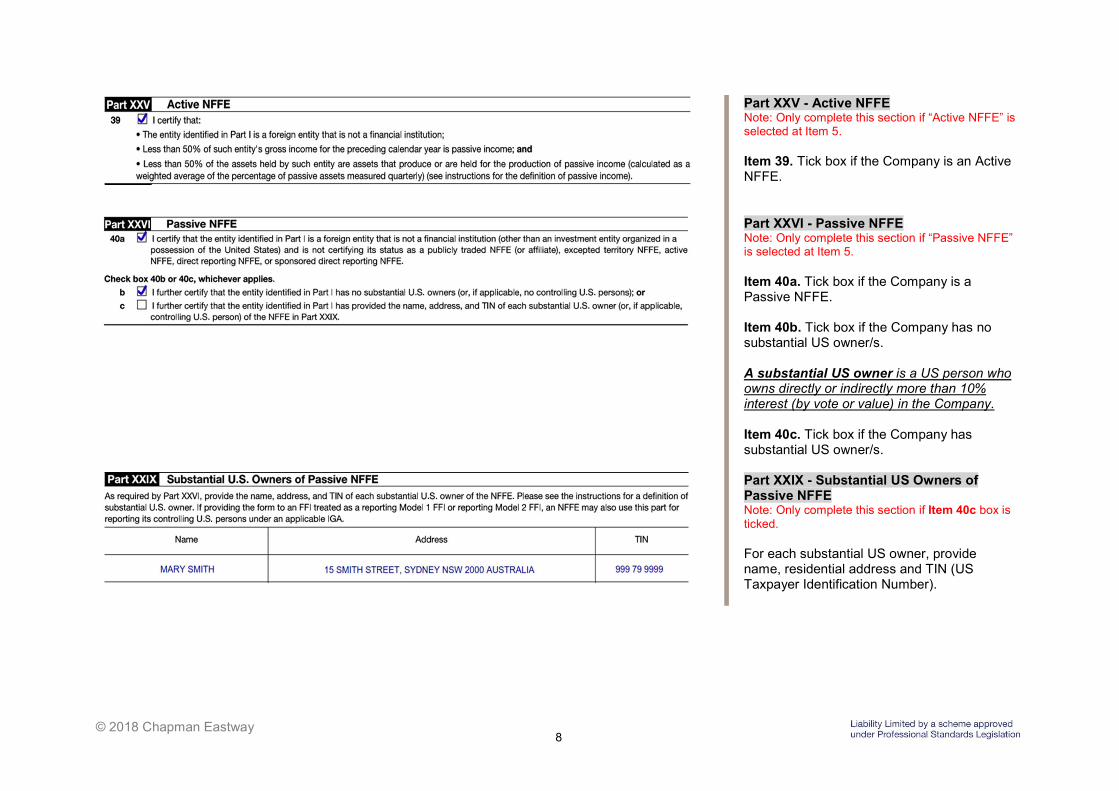

Part XXV - Active NFFE Note: Only complete this section if “Active NFFE” is selected at Item 5. Item 39. Tick box if the Company is an Active NFFE.

Part XXVI - Passive NFFE Note: Only complete this section if “Passive NFFE” is selected at Item 5. Item 40a. Tick box if the Company is a Passive NFFE. Item 40b. Tick box if the Company has no substantial US owner/s. A substantial US owner is a US person who owns directly or indirectly more than 10% interest (by vote or value) in the Company. Item 40c. Tick box if the Company has substantial US owner/s.

Part XXIX - Substantial US Owners of Passive NFFE Note: Only complete this section if Item 40c box is ticked. For each substantial US owner, provide name, residential address and TIN (US Taxpayer Identification Number).

9 © 2018 Chapman Eastway

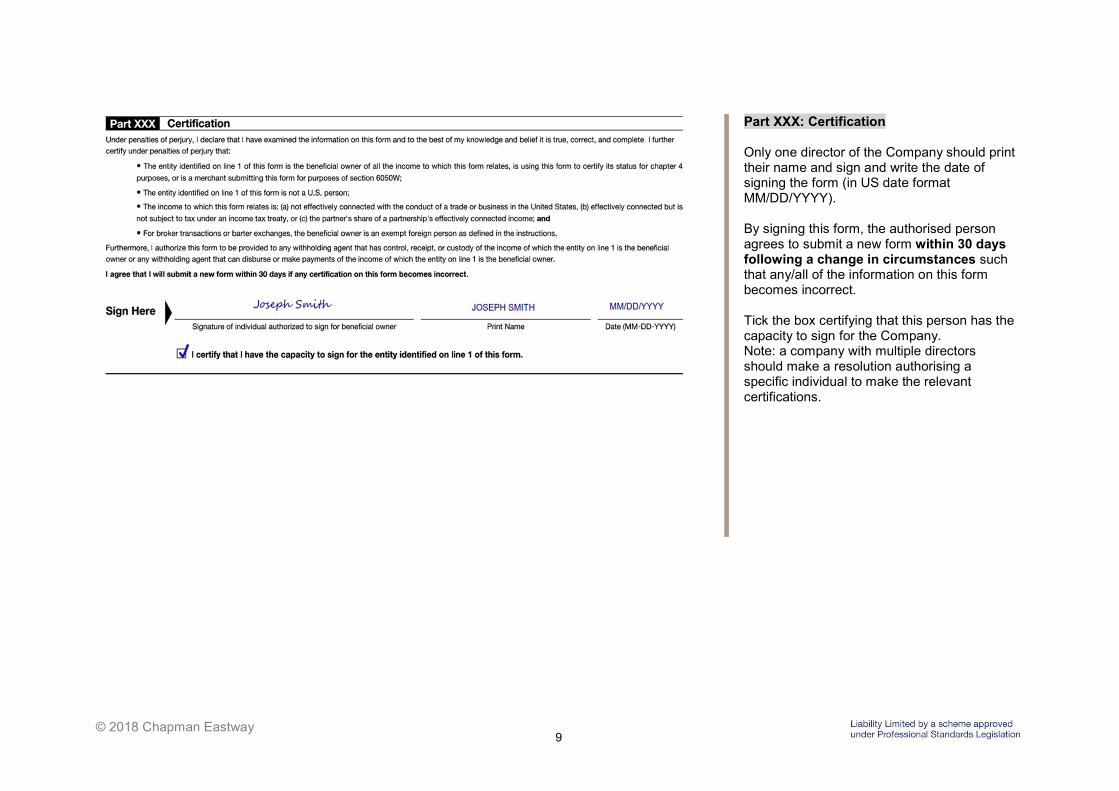

Part XXX: Certification Only one director of the Company should print their name and sign and write the date of signing the form (in US date format MM/DD/YYYY). By signing this form, the authorised person agrees to submit a new form within 30 days following a change in circumstances such that any/all of the information on this form becomes incorrect. Tick the box certifying that this person has the capacity to sign for the Company. Note: a company with multiple directors should make a resolution authorising a specific individual to make the relevant certifications.

10 © 2018 Chapman Eastway

SAMPLE W-8BEN-E FORM INSTRUCTIONS ON HOW TO COMPLETE

Part I - Identification of Beneficial Owner Item 1. Write full name of the Trust as it appears on the Trust Deed. Item 2. Write “Australia”. Item 3. Leave blank. Item 4. Tick “Complex trust”. Item 5. Select “Active NFFE” or “Passive NFFE”. Refer to the Decision Tree on page 25 for guidance in making this determination.

Guide to W-8BEN-E Form - Trust

W-8BEN-E Form is required for Australian resident trusts (being generally, discretionary or unit trusts) that derive investment income (e.g. dividends or interest) from US investments.

11 © 2018 Chapman Eastway

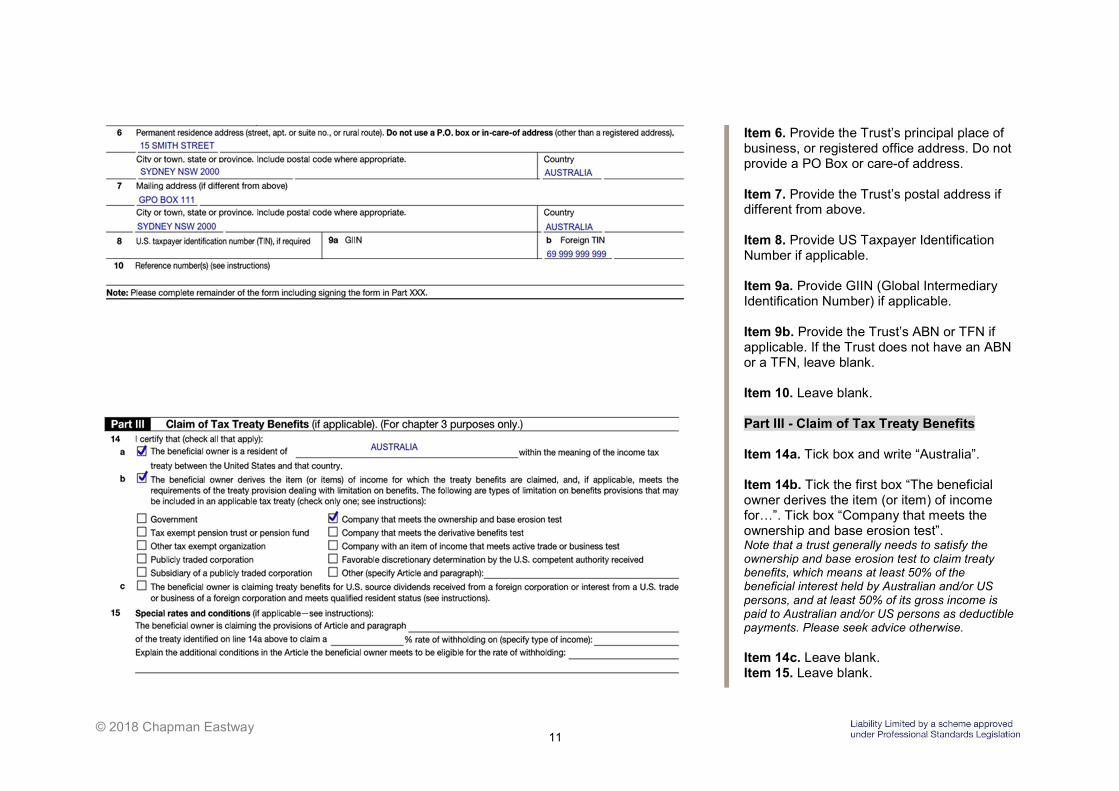

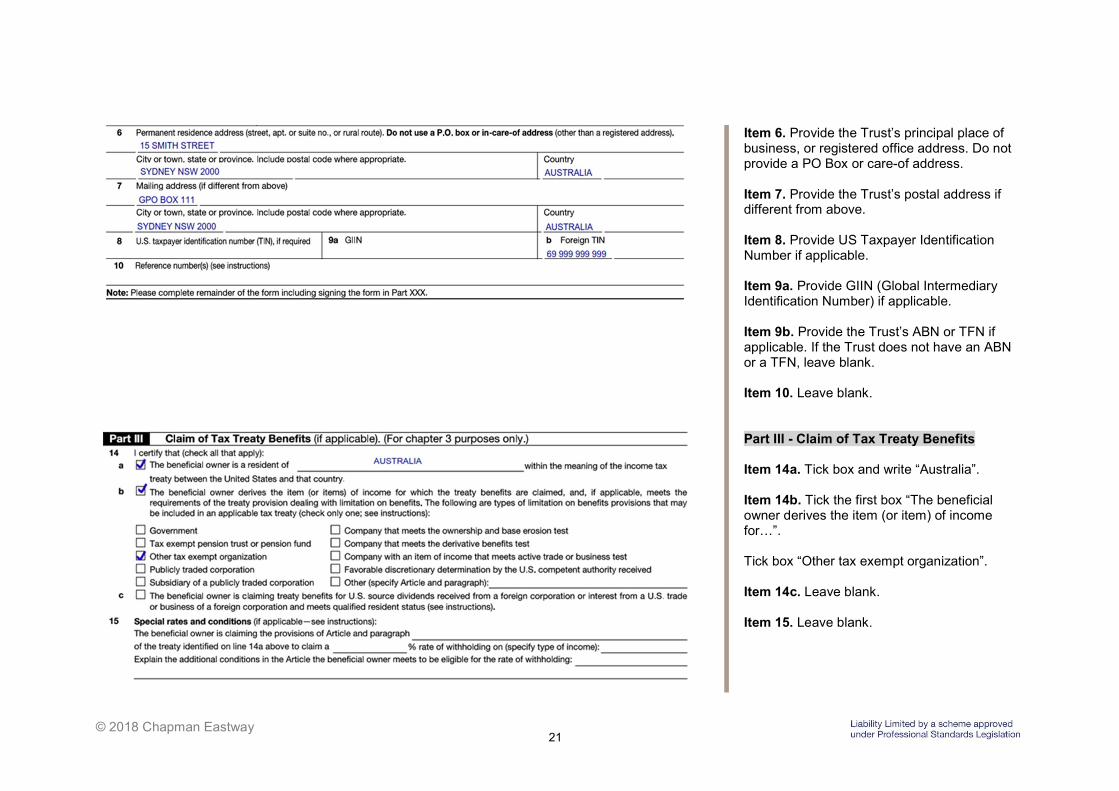

Item 6. Provide the Trust’s principal place of business, or registered office address. Do not provide a PO Box or care-of address. Item 7. Provide the Trust’s postal address if different from above. Item 8. Provide US Taxpayer Identification Number if applicable. Item 9a. Provide GIIN (Global Intermediary Identification Number) if applicable. Item 9b. Provide the Trust’s ABN or TFN if applicable. If the Trust does not have an ABN or a TFN, leave blank. Item 10. Leave blank.

Part III - Claim of Tax Treaty Benefits Item 14a. Tick box and write “Australia”. Item 14b. Tick the first box “The beneficial owner derives the item (or item) of income for…”. Tick box “Company that meets the ownership and base erosion test”. Note that a trust generally needs to satisfy the ownership and base erosion test to claim treaty benefits, which means at least 50% of the beneficial interest held by Australian and/or US persons, and at least 50% of its gross income is paid to Australian and/or US persons as deductible payments. Please seek advice otherwise. Item 14c. Leave blank. Item 15. Leave blank.

12 © 2018 Chapman Eastway

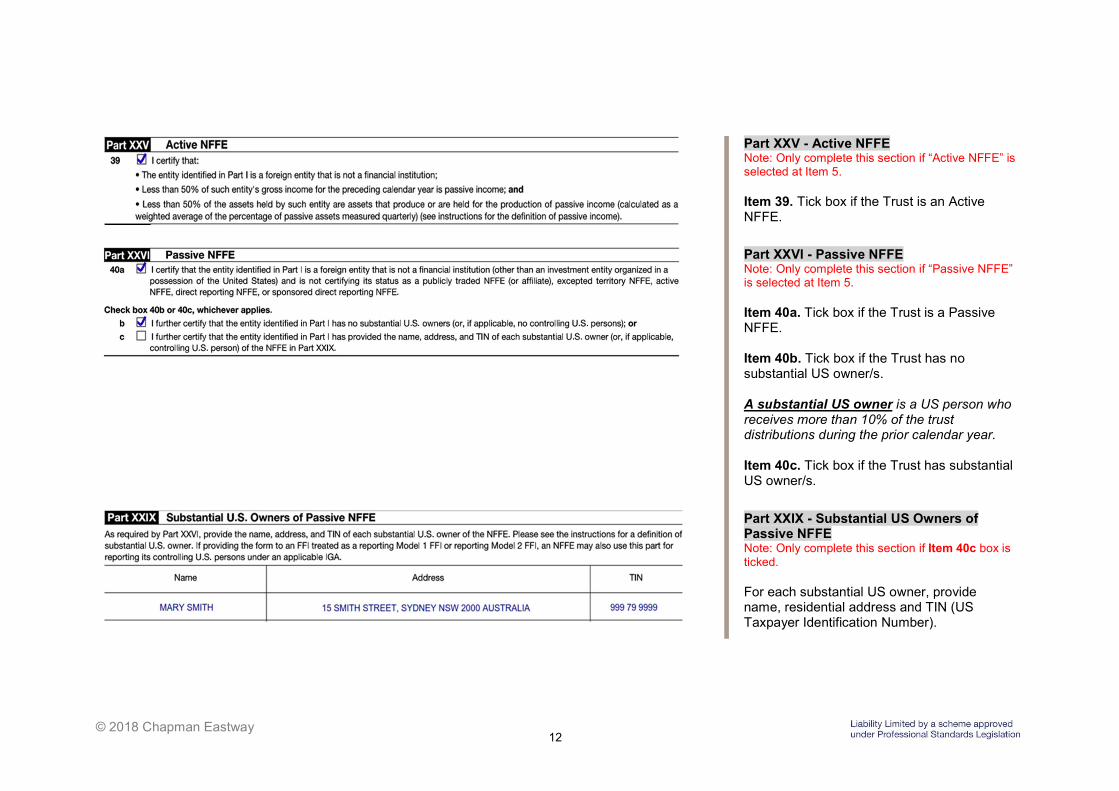

Part XXV - Active NFFE Note: Only complete this section if “Active NFFE” is selected at Item 5. Item 39. Tick box if the Trust is an Active NFFE.

Part XXVI - Passive NFFE Note: Only complete this section if “Passive NFFE” is selected at Item 5. Item 40a. Tick box if the Trust is a Passive NFFE. Item 40b. Tick box if the Trust has no substantial US owner/s. A substantial US owner is a US person who receives more than 10% of the trust distributions during the prior calendar year. Item 40c. Tick box if the Trust has substantial US owner/s.

Part XXIX - Substantial US Owners of Passive NFFE Note: Only complete this section if Item 40c box is ticked. For each substantial US owner, provide name, residential address and TIN (US Taxpayer Identification Number).

13 © 2018 Chapman Eastway

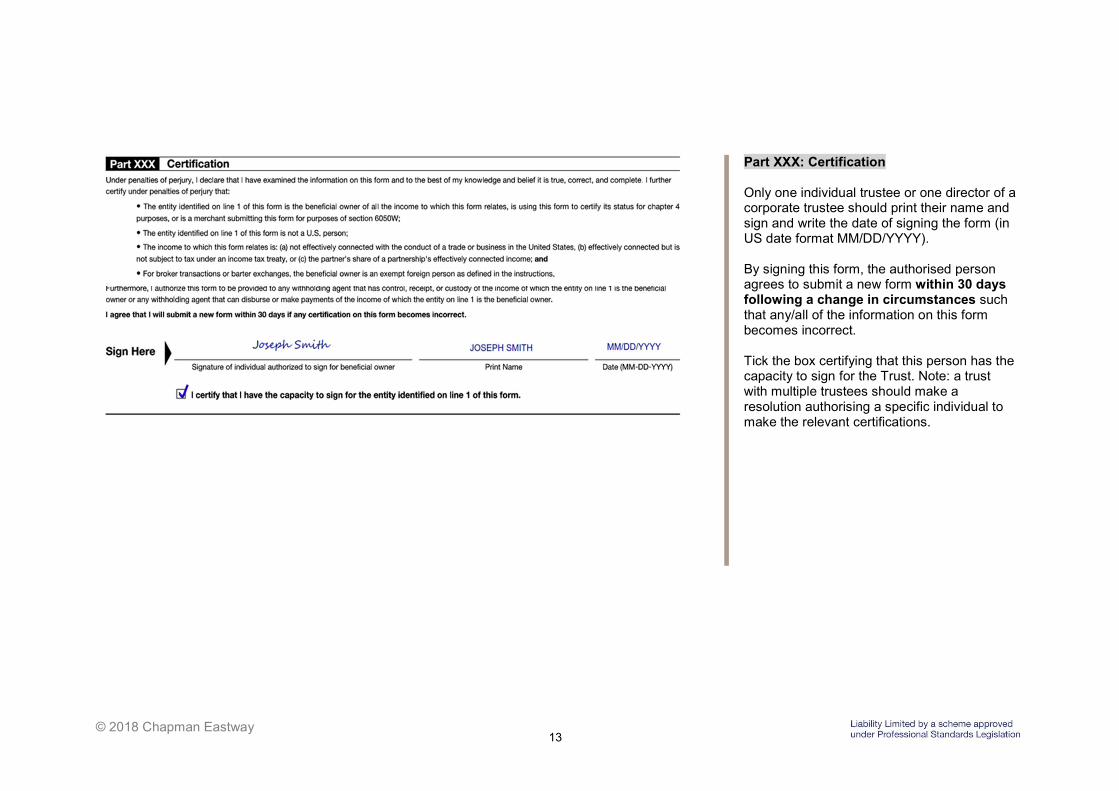

Part XXX: Certification Only one individual trustee or one director of a corporate trustee should print their name and sign and write the date of signing the form (in US date format MM/DD/YYYY). By signing this form, the authorised person agrees to submit a new form within 30 days following a change in circumstances such that any/all of the information on this form becomes incorrect. Tick the box certifying that this person has the capacity to sign for the Trust. Note: a trust with multiple trustees should make a resolution authorising a specific individual to make the relevant certifications.

14 © 2018 Chapman Eastway

SAMPLE W-8BEN-E FORM INSTRUCTIONS ON HOW TO COMPLETE

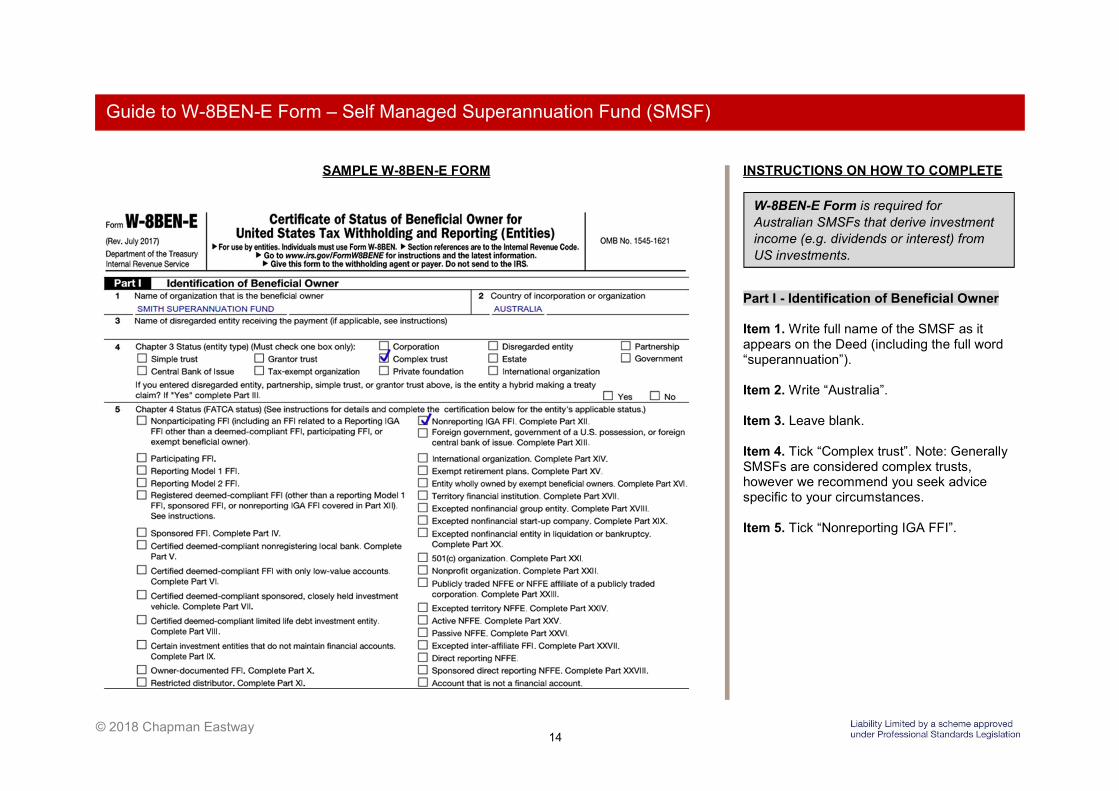

Part I - Identification of Beneficial Owner Item 1. Write full name of the SMSF as it appears on the Deed (including the full word “superannuation”). Item 2. Write “Australia”. Item 3. Leave blank. Item 4. Tick “Complex trust”. Note: Generally SMSFs are considered complex trusts, however we recommend you seek advice specific to your circumstances. Item 5. Tick “Nonreporting IGA FFI”.

Guide to W-8BEN-E Form – Self Managed Superannuation Fund (SMSF)

W-8BEN-E Form is required for Australian SMSFs that derive investment income (e.g. dividends or interest) from US investments.

15 © 2018 Chapman Eastway

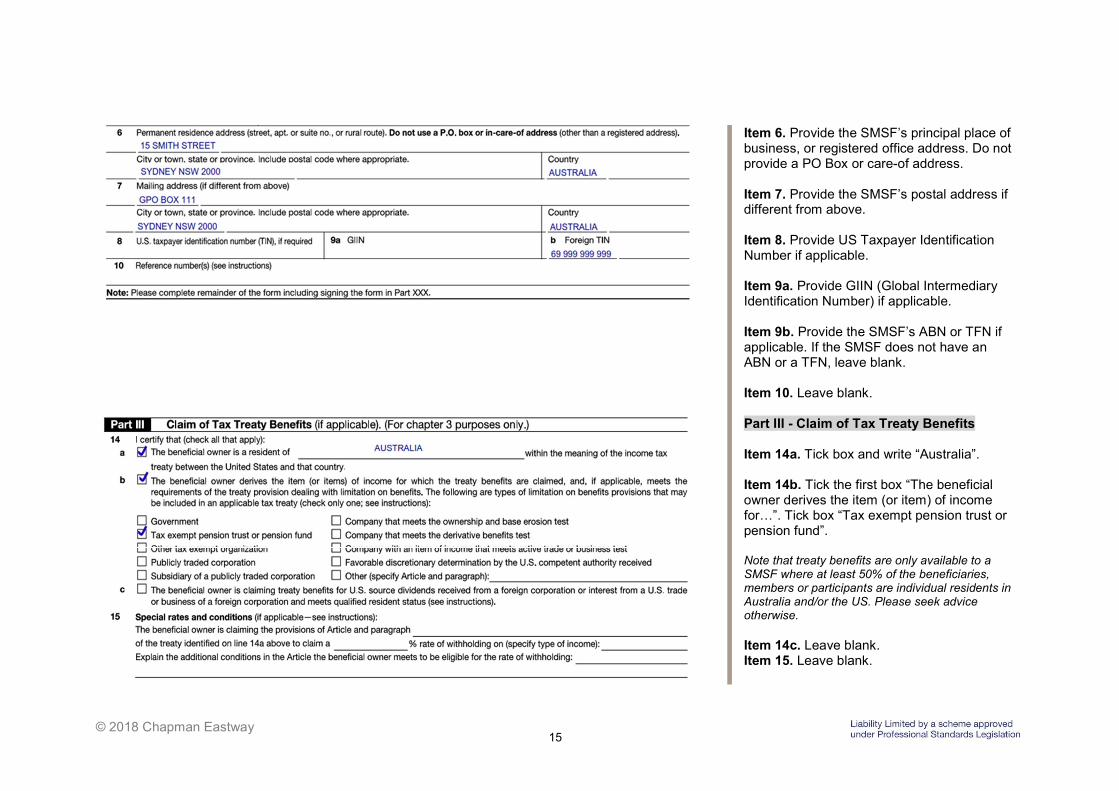

Item 6. Provide the SMSF’s principal place of business, or registered office address. Do not provide a PO Box or care-of address. Item 7. Provide the SMSF’s postal address if different from above. Item 8. Provide US Taxpayer Identification Number if applicable. Item 9a. Provide GIIN (Global Intermediary Identification Number) if applicable. Item 9b. Provide the SMSF’s ABN or TFN if applicable. If the SMSF does not have an ABN or a TFN, leave blank. Item 10. Leave blank.

Part III - Claim of Tax Treaty Benefits Item 14a. Tick box and write “Australia”. Item 14b. Tick the first box “The beneficial owner derives the item (or item) of income for…”. Tick box “Tax exempt pension trust or pension fund”. Note that treaty benefits are only available to a SMSF where at least 50% of the beneficiaries, members or participants are individual residents in Australia and/or the US. Please seek advice otherwise. Item 14c. Leave blank. Item 15. Leave blank.

16 © 2018 Chapman Eastway

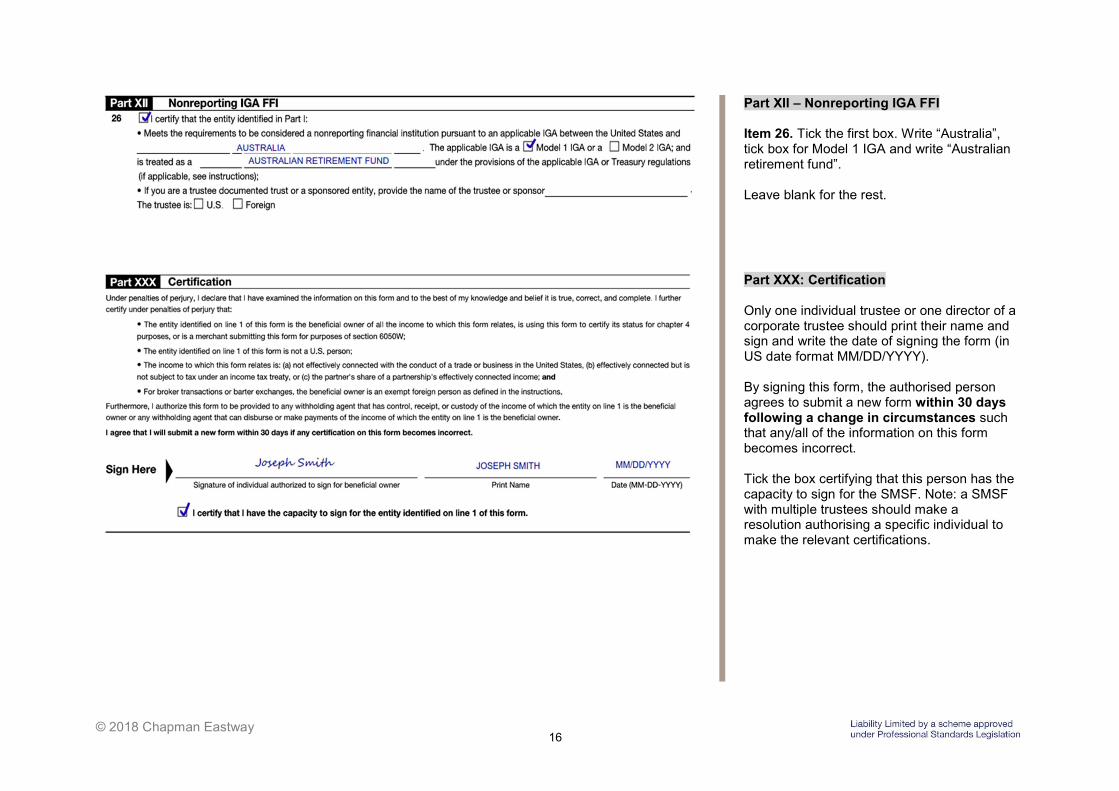

Part XII – Nonreporting IGA FFI Item 26. Tick the first box. Write “Australia”, tick box for Model 1 IGA and write “Australian retirement fund”. Leave blank for the rest.

Part XXX: Certification Only one individual trustee or one director of a corporate trustee should print their name and sign and write the date of signing the form (in US date format MM/DD/YYYY). By signing this form, the authorised person agrees to submit a new form within 30 days following a change in circumstances such that any/all of the information on this form becomes incorrect. Tick the box certifying that this person has the capacity to sign for the SMSF. Note: a SMSF with multiple trustees should make a resolution authorising a specific individual to make the relevant certifications.

17 © 2018 Chapman Eastway

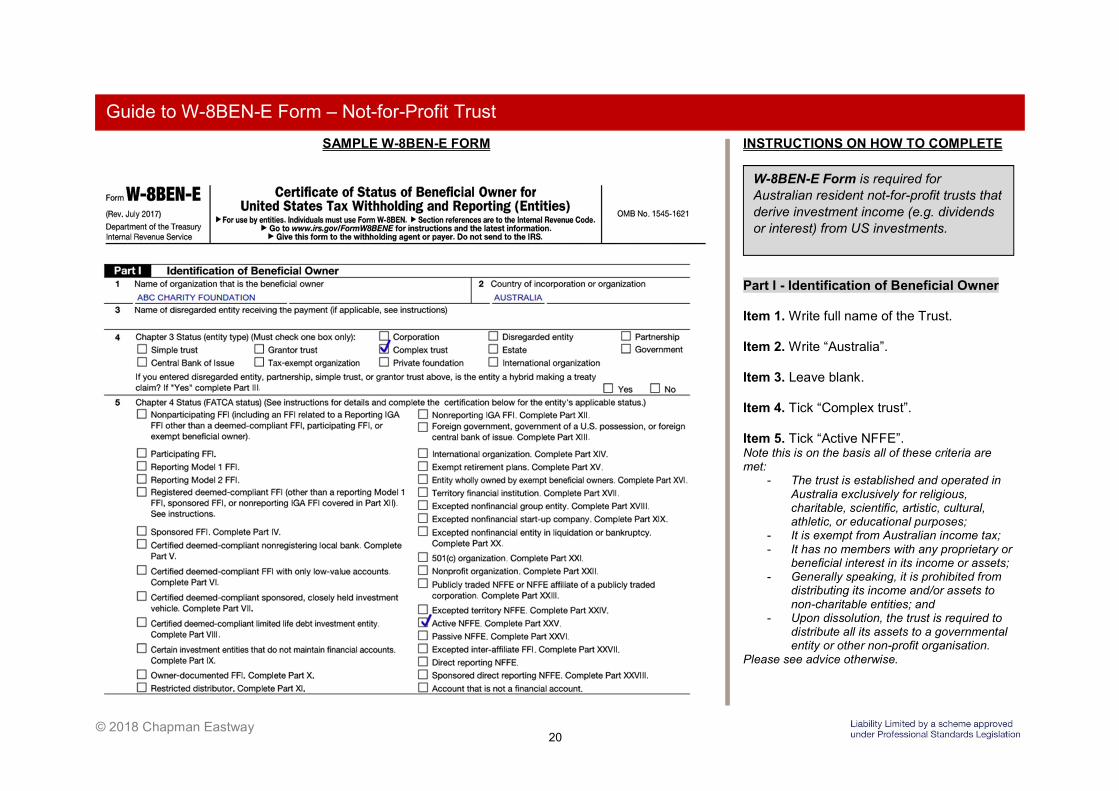

SAMPLE W-8BEN-E FORM INSTRUCTIONS ON HOW TO COMPLETE

Part I - Identification of Beneficial Owner Item 1. Write full name of the Company. Item 2. Write “Australia”. Item 3. Leave blank. Item 4. Tick “Corporation”. Item 5. Tick “Active NFFE”. Note this is on the basis all of these criteria are met:

- The company is established and operated in Australia exclusively for religious, charitable, scientific, artistic, cultural, athletic, or educational purposes;

- It is exempt from Australian income tax; - It has no members with any proprietary or

beneficial interest in its income or assets; - Generally speaking, it is prohibited from

distributing its income and/or assets to non-charitable entities; and

- Upon liquidation, the company is required to distribute all its assets to a governmental entity or other non-profit organisation.

Please see advice otherwise.

Guide to W-8BEN-E Form – Not-for-Profit Company

W-8BEN-E Form is required for Australian resident not-for-profit companies that derive investment income (e.g. dividends or interest) from US investments.

18 © 2018 Chapman Eastway

Item 6. Provide the Company’s principal place of business, or registered office address. Do not provide a PO Box or care-of address. Item 7. Provide the Company’s postal address if different from above. Item 8. Provide US Taxpayer Identification Number if applicable. Item 9a. Provide GIIN (Global Intermediary Identification Number) if applicable. Item 9b. Provide the Company’s ABN or TFN if applicable. If the Company does not have an ABN or a TFN, leave blank. Item 10. Leave blank.

Part III - Claim of Tax Treaty Benefits Item 14a. Tick box and write “Australia”. Item 14b. Tick the first box “The beneficial owner derives the item (or item) of income for…”. Tick box “Other tax exempt organization”. Item 14c. Leave blank. Item 15. Leave blank.

19 © 2018 Chapman Eastway

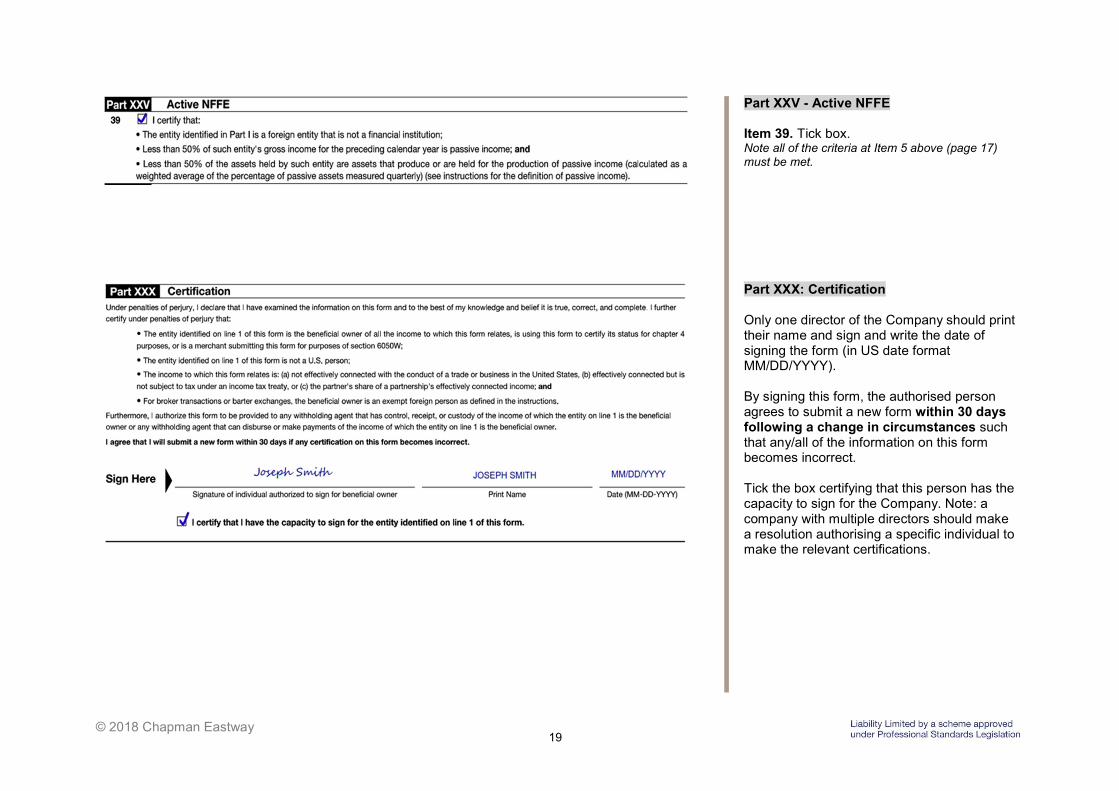

Part XXV - Active NFFE Item 39. Tick box. Note all of the criteria at Item 5 above (page 17) must be met.

Part XXX: Certification Only one director of the Company should print their name and sign and write the date of signing the form (in US date format MM/DD/YYYY). By signing this form, the authorised person agrees to submit a new form within 30 days following a change in circumstances such that any/all of the information on this form becomes incorrect. Tick the box certifying that this person has the capacity to sign for the Company. Note: a company with multiple directors should make a resolution authorising a specific individual to make the relevant certifications.

20 © 2018 Chapman Eastway

SAMPLE W-8BEN-E FORM INSTRUCTIONS ON HOW TO COMPLETE

Part I - Identification of Beneficial Owner Item 1. Write full name of the Trust. Item 2. Write “Australia”. Item 3. Leave blank. Item 4. Tick “Complex trust”. Item 5. Tick “Active NFFE”. Note this is on the basis all of these criteria are met:

- The trust is established and operated in Australia exclusively for religious, charitable, scientific, artistic, cultural, athletic, or educational purposes;

- It is exempt from Australian income tax; - It has no members with any proprietary or

beneficial interest in its income or assets; - Generally speaking, it is prohibited from

distributing its income and/or assets to non-charitable entities; and

- Upon dissolution, the trust is required to distribute all its assets to a governmental entity or other non-profit organisation.

Please see advice otherwise.

Guide to W-8BEN-E Form – Not-for-Profit Trust

W-8BEN-E Form is required for Australian resident not-for-profit trusts that derive investment income (e.g. dividends or interest) from US investments.

21 © 2018 Chapman Eastway

Item 6. Provide the Trust’s principal place of business, or registered office address. Do not provide a PO Box or care-of address. Item 7. Provide the Trust’s postal address if different from above. Item 8. Provide US Taxpayer Identification Number if applicable. Item 9a. Provide GIIN (Global Intermediary Identification Number) if applicable. Item 9b. Provide the Trust’s ABN or TFN if applicable. If the Trust does not have an ABN or a TFN, leave blank. Item 10. Leave blank.

Part III - Claim of Tax Treaty Benefits Item 14a. Tick box and write “Australia”. Item 14b. Tick the first box “The beneficial owner derives the item (or item) of income for…”. Tick box “Other tax exempt organization”. Item 14c. Leave blank. Item 15. Leave blank.

22 © 2018 Chapman Eastway

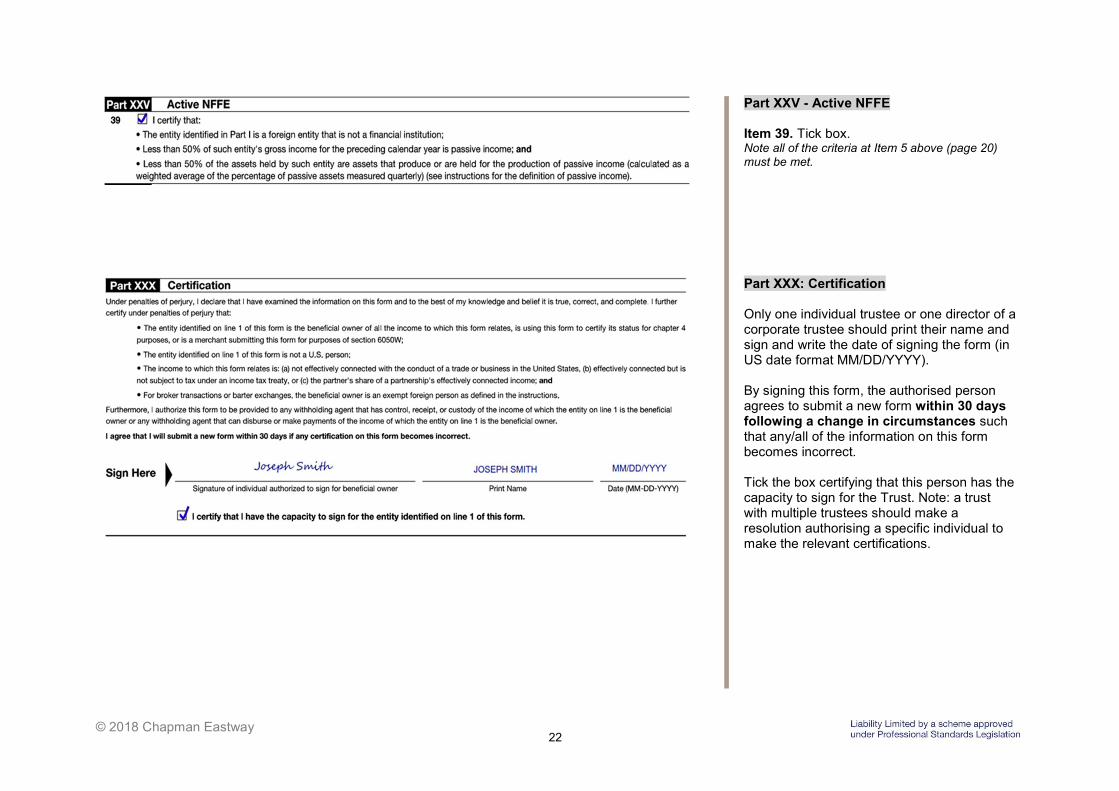

Part XXV - Active NFFE Item 39. Tick box. Note all of the criteria at Item 5 above (page 20) must be met.

Part XXX: Certification Only one individual trustee or one director of a corporate trustee should print their name and sign and write the date of signing the form (in US date format MM/DD/YYYY). By signing this form, the authorised person agrees to submit a new form within 30 days following a change in circumstances such that any/all of the information on this form becomes incorrect. Tick the box certifying that this person has the capacity to sign for the Trust. Note: a trust with multiple trustees should make a resolution authorising a specific individual to make the relevant certifications.

23 © 2018 Chapman Eastway

SAMPLE W-8BEN FORM INSTRUCTIONS ON HOW TO COMPLETE

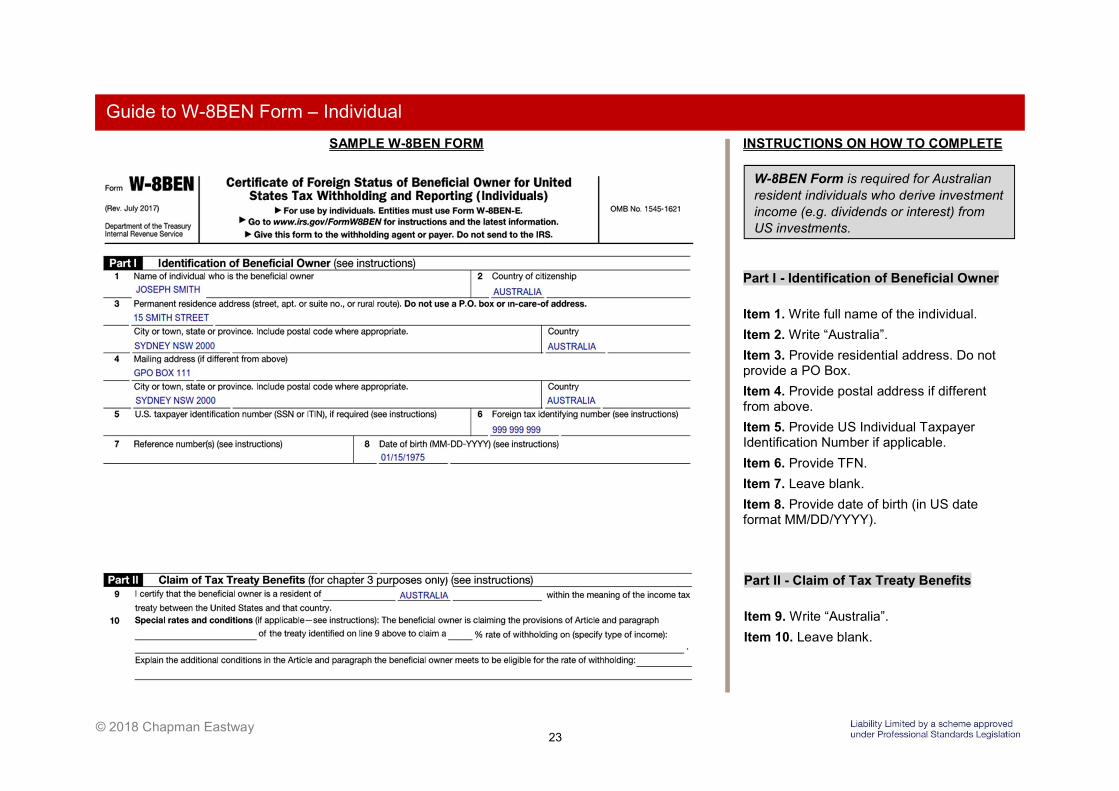

Part I - Identification of Beneficial Owner

Item 1. Write full name of the individual.

Item 2. Write “Australia”.

Item 3. Provide residential address. Do not provide a PO Box.

Item 4. Provide postal address if different from above.

Item 5. Provide US Individual Taxpayer Identification Number if applicable.

Item 6. Provide TFN.

Item 7. Leave blank.

Item 8. Provide date of birth (in US date format MM/DD/YYYY).

Part II - Claim of Tax Treaty Benefits

Item 9. Write “Australia”.

Item 10. Leave blank.

Guide to W-8BEN Form – Individual

W-8BEN Form is required for Australian resident individuals who derive investment income (e.g. dividends or interest) from US investments.

24 © 2018 Chapman Eastway

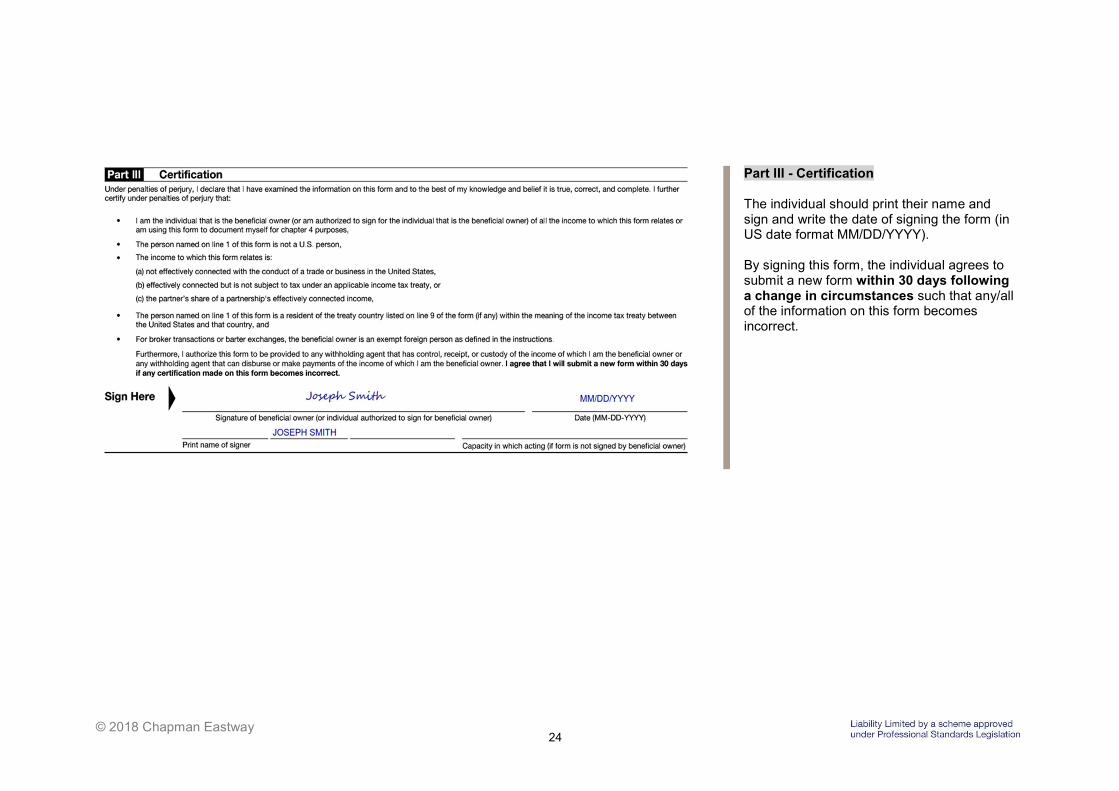

Part III - Certification The individual should print their name and sign and write the date of signing the form (in US date format MM/DD/YYYY). By signing this form, the individual agrees to submit a new form within 30 days following a change in circumstances such that any/all of the information on this form becomes incorrect.

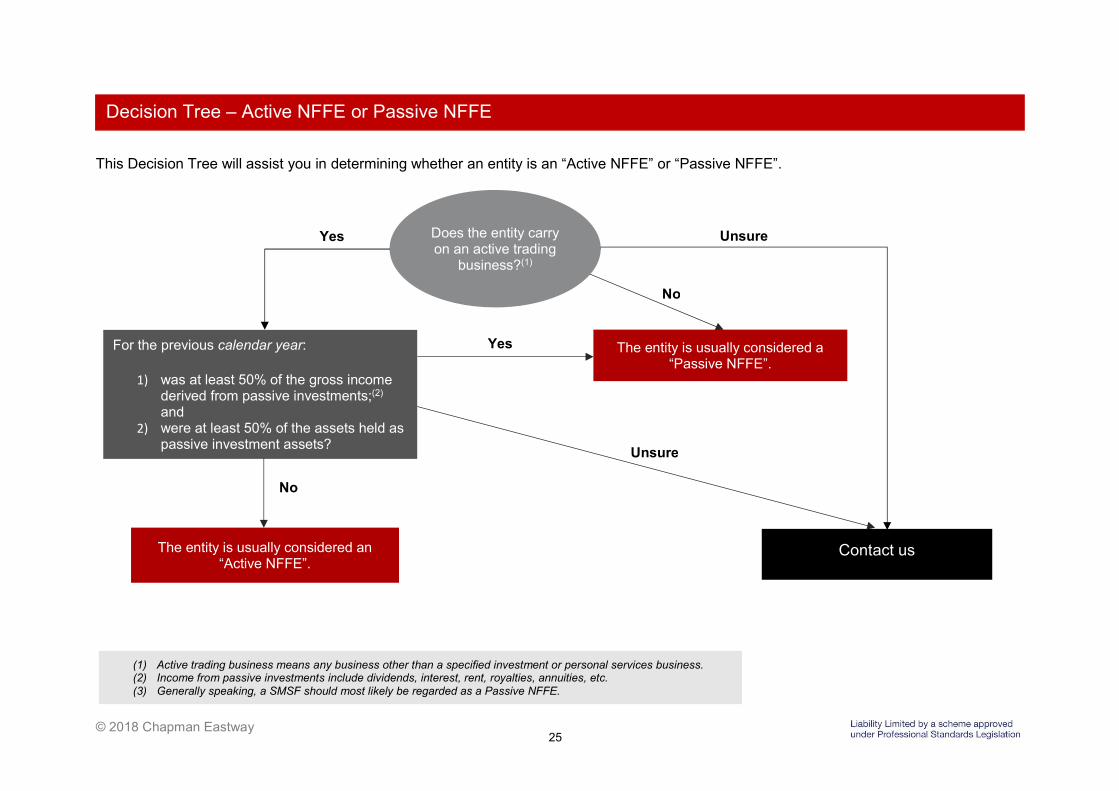

25 © 2018 Chapman Eastway

This Decision Tree will assist you in determining whether an entity is an “Active NFFE” or “Passive NFFE”.

Decision Tree – Active NFFE or Passive NFFE

Contact us

For the previous calendar year:

1) was at least 50% of the gross income derived from passive investments;(2) and

2) were at least 50% of the assets held as passive investment assets?

Unsure Yes

The entity is usually considered a “Passive NFFE”.

Yes

The entity is usually considered an “Active NFFE”.

Unsure

No

Does the entity carry on an active trading

business?(1)

No

(1) Active trading business means any business other than a specified investment or personal services business. (2) Income from passive investments include dividends, interest, rent, royalties, annuities, etc. (3) Generally speaking, a SMSF should most likely be regarded as a Passive NFFE.

26 © 2018 Chapman Eastway

Level 15, 9 Hunter Street Sydney NSW 2000 Telephone: +61 2 9262 4933 Facsimile: +61 2 9262 1619 Email: [email protected] Web: www.chapmaneastway.com.au Mail: GPO Box 979 Sydney NSW 2001 Primary Contacts: Mr Sean Cortis CEO & Principal Mr Anthony Ryan Principal

![Tabel Kontingensi 2x2 (4) ordinal dan eksak fisher PKS/3 Respon Ordinal dan eksak fisher.pdf^ Ç v Æ ^ ^ µ v µ l u v p z ] µ v p d î '$7$ dofrkro ,1387 lwhp lwhp urz fro frxqw](https://img.pdfslide.net/doc/110x75/5e2e570c745c8a6d9a2a21cf/tabel-kontingensi-2x2-4-ordinal-dan-eksak-fisher-pks3-respon-ordinal-dan-eksak.jpg)

![· 2020. 2. 29. · name: edhelper 7klv sx]]oh kdv d odujh qxpehu lq wkh plggoh zklfk lv wkh vxp ri wkh irxu qxpehuv wkdw vxuurxqg lw 6dpsoh lv wkh vxp lv wkh vxp lv wkh vxp ([dpsoh](https://img.pdfslide.net/doc/110x75/5fe294641b710f382d0c50c5/2020-2-29-name-edhelper-7klv-sxoh-kdv-d-odujh-qxpehu-lq-wkh-plggoh-zklfk.jpg)

![25'(5 , %$&.*5281'...wkh\ zhuh hqwlwohg wr uhgxfh %duer]d v dzdug e\ wkh kh uhfhlyhg lq wkh vhwwohphqw ri klv zrunhuv frpshqvdwlrq fodlp ,q plg wkh frxuw judqwhg wkh ghihqgdqwv](https://img.pdfslide.net/doc/110x75/5e7d1d127d832460c10c1ba8/255-5281-wkh-zhuh-hqwlwohg-wr-uhgxfh-duerd-v-dzdug-e-wkh-kh.jpg)

![Promoting Local IT sector Development through Public ... · $ GDVK t LQGLFDWHV WKDW WKH LWHP LV HTXDO WR ]HUR RU LWV YDOXH QHJOLJLEOH ... by BMZ in Bonn in May 2012, including Volker](https://img.pdfslide.net/doc/110x75/5e97465c4a3c7942473c3278/promoting-local-it-sector-development-through-public-gdvk-t-lqglfdwhv-wkdw.jpg)