Embed Size (px)

Citation preview

1

May 5, 2009

MORTGAGE BACKED SECURITIES AN ACTUARIAL APPROACH TO

CASH FLOW ANALYSIS

Kyle S. Mrotek, FCAS, MAAANeal Dihora, ASA, CFA

CAS Spring Meeting

May 5, 2009

2

May 5, 2009

Disclaimer

This presentation contains our views and these views are not necessarily identical to the views of the cosponsors of the program nor the employers or clients of the speakers

3

May 5, 2009

Agenda

Background on the MBS market

Current situation

Actuarial model presentation

4

May 5, 2009

Background

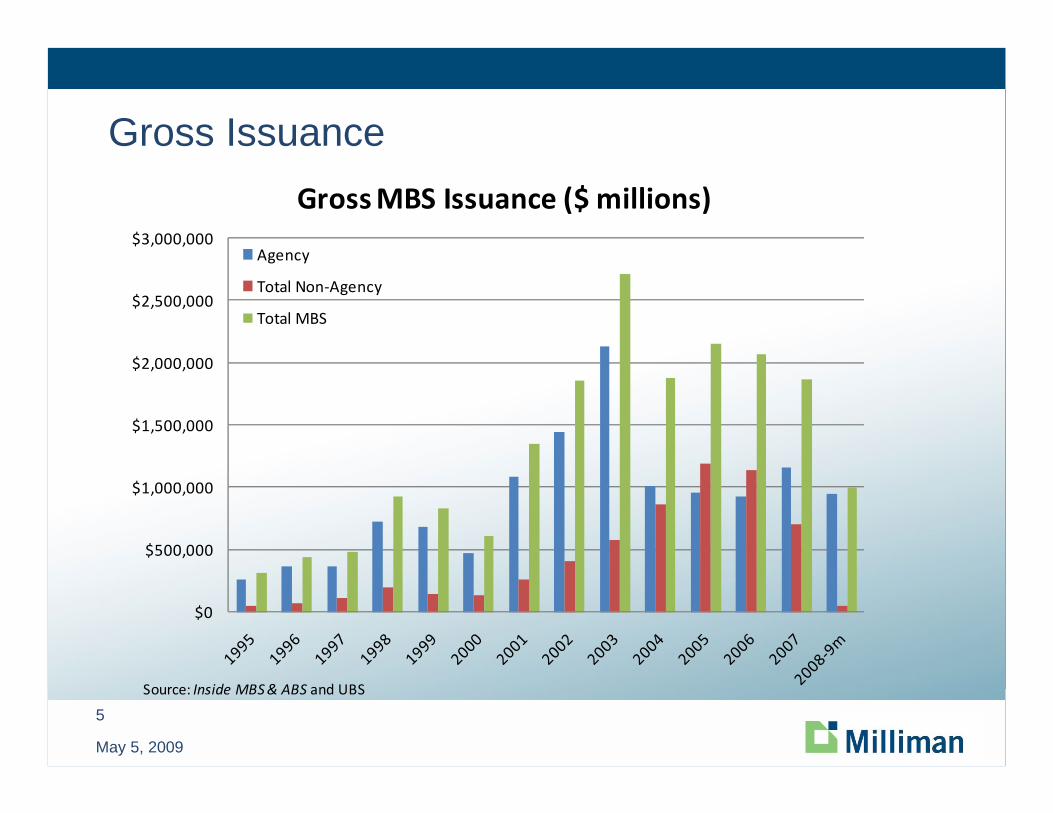

Gross Issuance

Agency vs. Non-Agency Issuance

Split by non-agency type (prime, subprime, alt-a)

5

May 5, 2009

Gross Issuance

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

Gross MBS Issuance ($ millions)

Agency

Total Non‐Agency

Total MBS

Source: Inside MBS & ABS and UBS

6

May 5, 2009

Agency vs. Non-Agency

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Percen

t

MBS Market Share

Agency

Total Non‐Agency

Source: Inside MBS & ABS and UBS

7

May 5, 2009

Non-Agency by Type

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

Non‐Agency Gross MBS Issuance($ millions)

Alt‐A

Jumbo

Subprime

Other

Source: Inside MBS & ABS and UBS

8

May 5, 2009

Non-Agency by Type

0%

5%

10%

15%

20%

25%

Percen

t

Non‐Agency (% of Total MBS Issuance)

Alt‐A

Jumbo

Subprime

Other

Source: Inside MBS & ABS and UBS

9

May 5, 2009

Current Situation

• What happened?• Liquidity evaporated

• Market values eroded

• Why is valuation needed?• GAAP Accounting regulations still require a value (FAS 157)

• Risk quantification• Distribution of assumptions and valuations

10

May 5, 2009

Liquidity Evaporated

Broker/Dealers of non-Agency MBS unwilling to provide liquidity 1

Forced liquidations of MBS set market prices 1

Pricing vendors find it difficult to obtain “real” prices

Bid - Ask spread is 10-30 points depending on collateral and the depth of distress 2

1AD&Co's 16th Annual Conference: The Times They Are A-Changin‘2”Getting Out of the Mess” by Dave Hurt at the Loan Performance Symposium March 11, 2009

11

May 5, 2009

Liquidity Evaporated

100

120

140

160

180

200

220

240

260

280

300

1/9/04

3/9/04

5/9/04

7/9/04

9/9/04

11/9/04

1/9/05

3/9/05

5/9/05

7/9/05

9/9/05

11/9/05

1/9/06

3/9/06

5/9/06

7/9/06

9/9/06

11/9/06

1/9/07

3/9/07

5/9/07

7/9/07

9/9/07

11/9/07

1/9/08

3/9/08

5/9/08

7/9/08

9/9/08

11/9/08

1/9/09

3/9/09

Mortgage Spread (Conventional Mortgage Loan less 10‐year Treasury)

Mortgage SpreadSource: Federal Reserve Board

12

May 5, 2009

Erosion of Market Values

50

75

100

125

150

175

200

225

1890 1910 1930 1950 1970 1990 2010

Real Home Price Index (1890‐2008)

Source: http://www.econ.yale.edu/~shiller/data.htm

13

May 5, 2009

Erosion of Market Values

100

120

140

160

180

200

220

Jan‐00

Apr‐00

Jul‐0

0

Oct‐00

Jan‐01

Apr‐01

Jul‐0

1

Oct‐01

Jan‐02

Apr‐02

Jul‐0

2

Oct‐02

Jan‐03

Apr‐03

Jul‐0

3

Oct‐03

Jan‐04

Apr‐04

Jul‐0

4

Oct‐04

Jan‐05

Apr‐05

Jul‐0

5

Oct‐05

Jan‐06

Apr‐06

Jul‐0

6

Oct‐06

Jan‐07

Apr‐07

Jul‐0

7

Oct‐07

Jan‐08

Apr‐08

Jul‐0

8

Oct‐08

Jan‐09

Case‐Shiller Home Price Index Since January 2000

'Case Shiller 20 City Compsite'Source: Standardand Poor's

Jul06: 206.5

Jan 09: 146.4

Decline: ‐29%

14

May 5, 2009

Erosion of Market Values

0

10

20

30

40

50

60

70

80

Price

ABX HE AAA 2007‐2 Index

Source: Bloomberg

15

May 5, 2009

Erosion of Market Values

ABX HE AAA 2007-2 Index ComponentsACE Securities Corp. Home Equity Loan Trust, Series 2007-HE4Bear Stearns Asset Backed Securities I Trust 2007-HE3Citigroup Mortgage Loan Trust 2007-AMC2CWABS Asset-Backed Certificates Trust 2007-1 First Franklin Mortgage Loan Trust, Series 2007-FF1GSAMP Trust 2007-NC1 Home Equity Asset Trust 2007-2 HSI Asset Securitization Corporation Trust 2007-NC1 J.P. MORGAN MORTGAGE ACQUISITION TRUST 2007-CH3Merrill Lynch First Franklin Mortgage Loan Trust, Series 2007-2 MERRILL LYNCH MORTGAGE INVESTORS TRUST, SERIES 2007-MLN1 Morgan Stanley ABS Capital I Inc. Trust 2007-NC3 Nomura Home Equity Loan, Inc., Home Equity Loan Trust Series 2007-2 NovaStar Mortgage Funding Trust, Series 2007-2 OPTION ONE MORTGAGE LOAN TRUST 2007-5 RASC Series 2007-KS2 Trust Securitized Asset Backed Receivables LLC Trust 2007-BR4 Structured Asset Securities Corporation Mortgage Loan Trust 2007-BC1 SOUNDVIEW HOME LOAN TRUST 2007-OPT1 WaMu Asset-Backed Certificates WaMu Series 2007-HE2

Source: markit.com 3/16/09

16

May 5, 2009

GAAP Valuation Still Needed

Mark to Market – FAS 157 required companies to value holdings

• Level 1 – based on market price– Recent observed prices could be due to forced liquidation

• Level 2 – based on related price (ex. spread to treasuries)– Spreads can reflect lots of different risks (credit, liquidity,…)

• Level 3 – based on model price

Mark to Model pricing developed from loan level data– FASB relaxation of mark-to-market rules – Perhaps an ‘intrinsic value’ based on full range of scenarios

17

May 5, 2009

Risk Quantification

The following table has daily percent changes of DJIA under a Normal Distribution assumption and reality

Percent Move (1916-2003)

Normal Distribution Assumption Reality

<>3.4% 58 1001

<>4.5% 6 366

<>7% 1 in 300,000 years 48

Source: Benoit Mandelbrot, Economist 1/24/2009

18

May 5, 2009

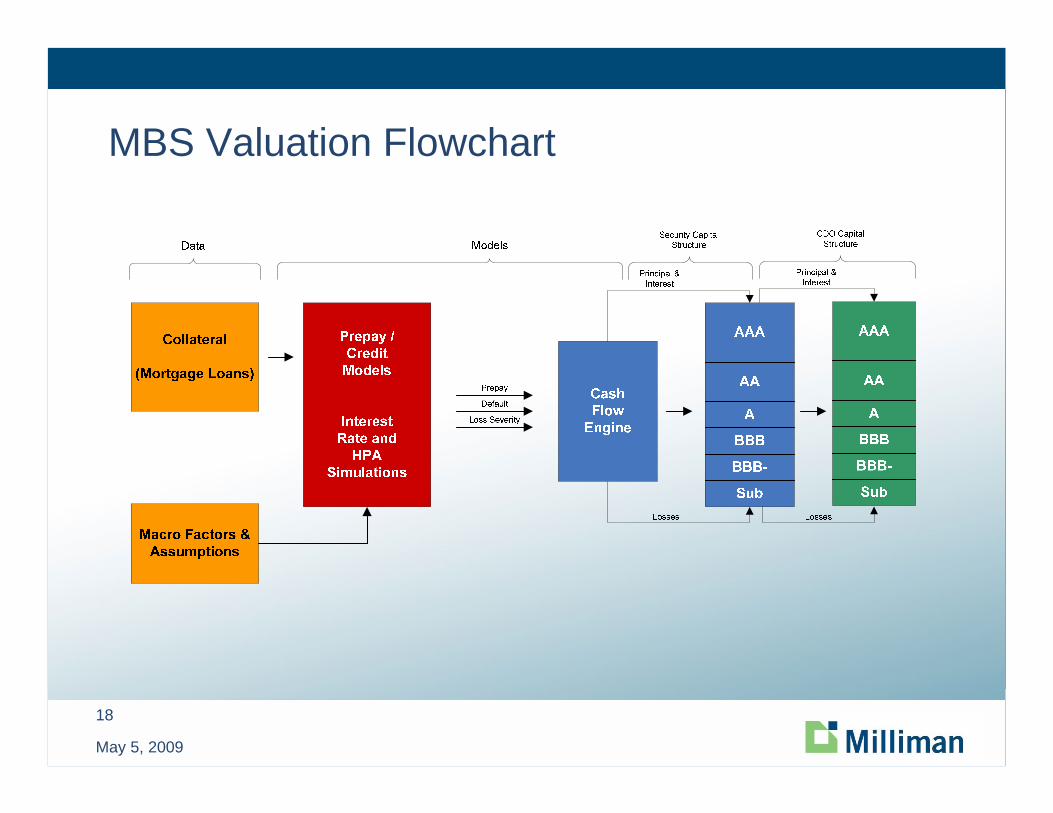

MBS Valuation Flowchart

19

May 5, 2009

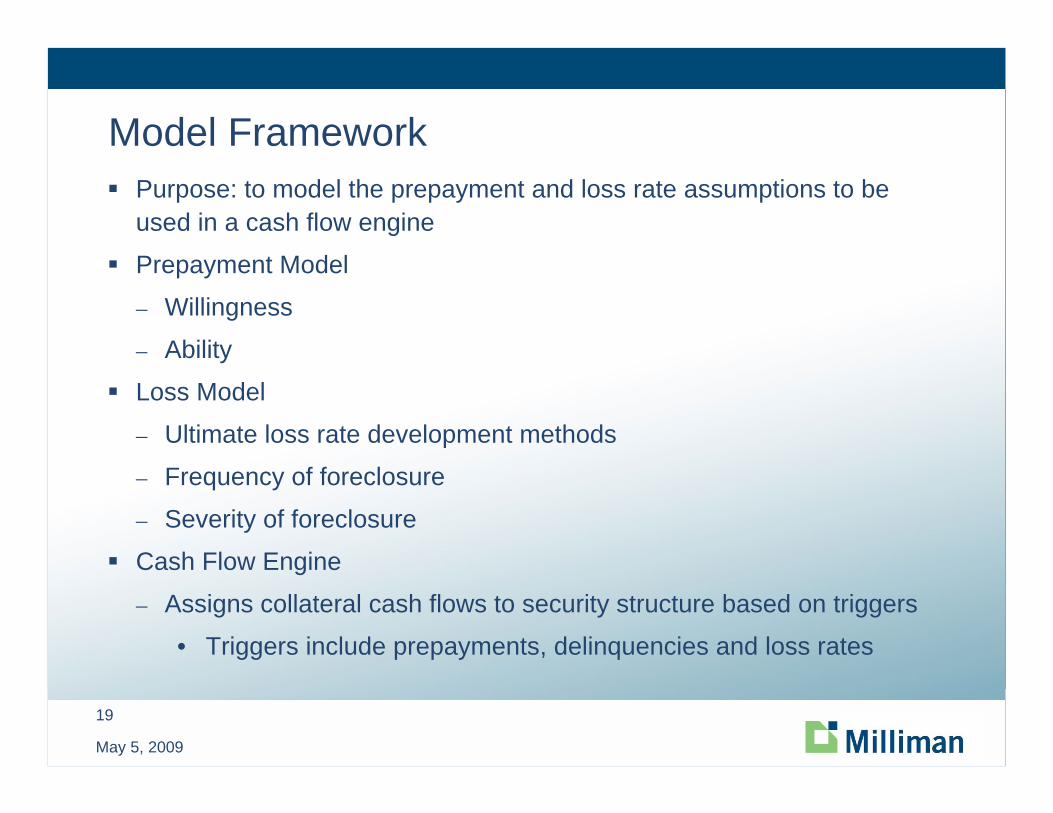

Model FrameworkPurpose: to model the prepayment and loss rate assumptions to beused in a cash flow engine

Prepayment Model

– Willingness

– Ability

Loss Model

– Ultimate loss rate development methods

– Frequency of foreclosure

– Severity of foreclosure

Cash Flow Engine

– Assigns collateral cash flows to security structure based on triggers

• Triggers include prepayments, delinquencies and loss rates

20

May 5, 2009

Model Characteristics

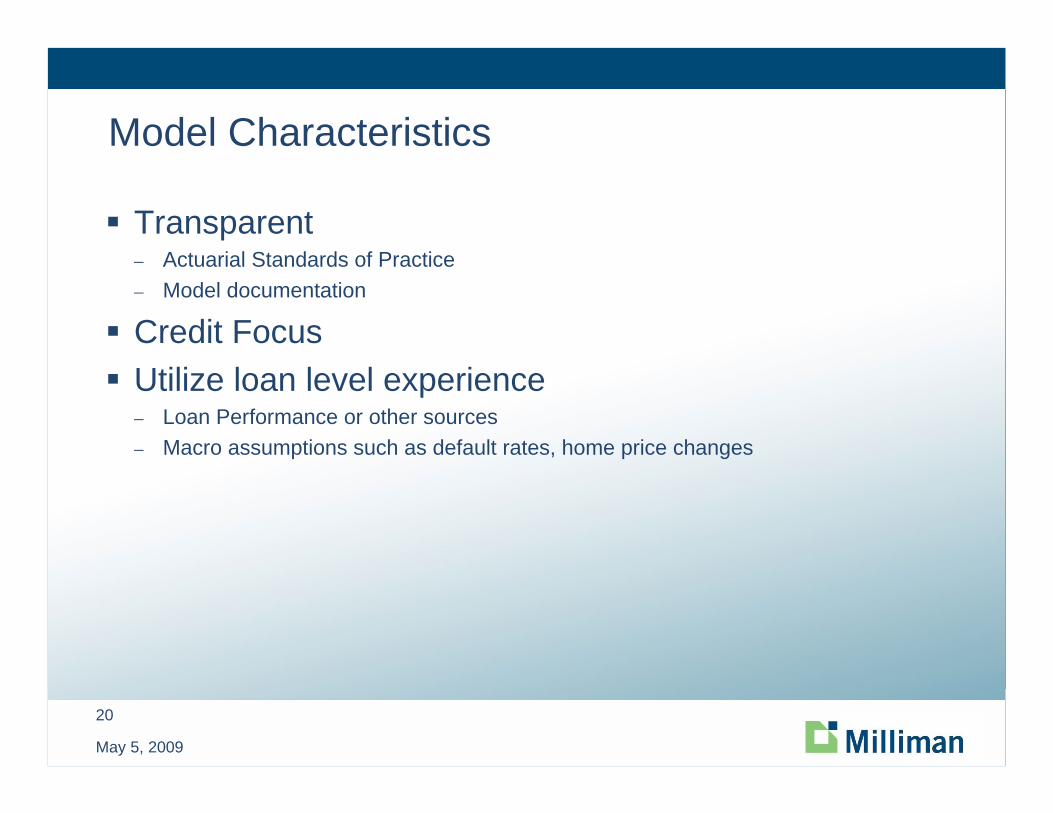

Transparent– Actuarial Standards of Practice– Model documentation

Credit FocusUtilize loan level experience– Loan Performance or other sources– Macro assumptions such as default rates, home price changes

21

May 5, 2009

Prepayment ModelGoal: estimate percentage of loan amounts that will prepay

Willingness– Interest rate differential (refinancing, cash-out)– Loan/Product type– Fixed/Adjustable rate– Seasonality

Ability– Home price changes– FICO scores– LTV – original and current– Lending standards/policies

Federal government initiatives

22

May 5, 2009

Ultimate Loss Rate Development MethodsGoal: estimate percentage of loan amounts that will default and severity of default

‘Paid’ Loss Development Factor (LDF)

‘Incurred’ LDF

A priori ultimate loss rate (ULR) development

Adjusted ‘paid’ BF method

‘Incurred’ BF

23

May 5, 2009

Ultimate Loss Rate ‘Paid’ LDF

‘Paid’ losses to date– Can calculate from loan level data

– Providers such as Bloomberg also provide this data• Receive data from trustees/servicers of loans

Cumulative loss curve by age of loan– Examples on next slide

– What % of the losses should we expect to see at a certain loan age

Ultimate loss = ‘paid’ losses / % expected to be ‘paid’

24

May 5, 2009

Ultimate Loss Rate ‘Paid’ LDF

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0 3 6 9 12 15 18 21 24 27 30 33 36 39 42 45 48 51 54 57 60 63 66 69 72 75 78 81 84 87 90 93 96 99 102

105

108

111

114

117

120

Percen

t

Illustrative Loss Curves ‐Moody's and Fitch

Moody's Alt‐A FRM/ARM First Lien

Fitch Prime/Alt‐A

Fitch Subprime

Moody's Subprime FRM First Lien

Age (months)

25

May 5, 2009

Ultimate Loss Rate “Incurred” LDF

‘Paid’ losses to date

Take current delinquencies to ultimate loss– Roll rate projections (project the % of delinquencies that default)

Severity (% of loan that is not recoverable)

Incurred losses = ‘paid’ losses + estimate of defaults x severity

Utilize incurred loss curves to calculate ultimate loss rate

Challenges/pitfalls

26

May 5, 2009

A Priori ULR Development

• Frequency of foreclosure

• Severity given default

• Unadjusted a priori ultimate loss rate = frequency x severity

• Critical considerations for loan level collateral• Underwriting characteristics (FICO, LTV, documentation, etc.)

• Economic conditions the loan is exposed to

27

May 5, 2009

A Priori Development - Frequency

• Frequency of Foreclosure– Historical data– Specific loan characteristics

– FICO– LTV– Amortization type (fixed, adjustable rate)– Interest only– Loan purpose (refinance, purchase)– Property type (single family, condo) – Occupancy (owner, second home, investor)– Loan documentation (full, low, none)– Loan size (jumbo, conforming)

– Future foreclosure estimates– Take delinquencies to ultimate loss– Economic variables (e.g., home price changes - see chart on slide 32)

28

May 5, 2009

A Priori Development - Frequency

Amortization

FICO‐LTV

Interest Only

Loan Purpose

Property Type

Occupancy

Documentation

Loan Size

Illustrative Loan Characteristics

Prime

Alt‐A

Subprime

29

May 5, 2009

A Priori Development - Frequency

Source: “Negative equity and foreclosure: Theory and evidence”, Christopher L. Foote, Kristopher Gerardi, Paul S. Willen, Journal of Urban Economics 64 (2008), pp. 234‐345

30

May 5, 2009

A Priori Development - Severity

• Severity of Default– Home price changes– Costs of foreclosure (disposal, realtor, legal, upkeep)– Accrued interest– Current economic situation

– Home price depreciation results in higher severity– Government intervention may impact severity

– Bankruptcy law changes– FHA refinancing– Public/private partnerships– Interest claw back from 38% to 31% debt to income– Others…

31

May 5, 2009

A Priori Development - Severity

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55% 60% 65% 70% 75% 80% 85% 90% 95% 100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Loan Level Severity

Illustrative Loan Level Severity Distribution

32

May 5, 2009

Ultimate Loss Rate Adjusted Paid BF

Paid losses to date

A priori persistency adjustment– Actual persistency = unpaid balance / original balance

– A priori persistency = anticipated unpaid balance

– Adjustment needed to allow for more/less losses based on actual vs. anticipated exposure duration

Adjust a priori ultimate loss (frequency x severity) by persistency factor

Use loss curve to estimate % yet to be paid

33

May 5, 2009

Ultimate Loss Rate “Incurred” BF

Utilize incurred loss curve

Take a priori ultimate loss rate (from a priori development) – Utilize incurred loss curves to estimate % yet to be paid

Incurred BF ultimate loss = incurred to date + estimate of yet to be incurred

34

May 5, 2009

Cash Flow Waterfall

Tranche level cash flows based on deal prospectus

Model needs to take into account specifics of the deal

35

May 5, 2009

Cash Flow Waterfall

Illustrative NPV of Cash Flow Waterfall OutputNet Present Value (NPV)

RMBS Tranche Original Rating Scenario 1 Scenario 2 Scenario 3

A AAA 99.71 99.66 99.70

B AAA 77.63 78.52 69.03

C AA 79.09 7.81 1.64

D AA 78.64 9.96 1.66

E A 80.16 2.79 0.70

F BBB 86.83 0.64 0.39

G BBB 85.62 0.49 0.39

H BB 0.94 0.40 0.39

I BB 0.78 0.40 0.39

J Not Rated 5.46 5.34 0.39

K Not Rated 0.40 0.40 0.39

36

May 5, 2009

MORTGAGE BACKED SECURITIES AN ACTUARIAL APPROACH TO

CASH FLOW ANALYSIS

Questions?

[email protected]@Milliman.com