Embed Size (px)

Citation preview

MPR February100210

Figure 1.1. Repo ratePer cent, quarterly averages

-1

0

1

2

3

4

5

6

7

04 05 06 07 08 09 10 11 12 13

-1

0

1

2

3

4

5

6

790%75%50%OutcomeForecast

Source: The Riksbank

Note. The uncertainty band does not take into account the fact that there may be a lower bound for the repo rate. The uncertainty band shows the band within which the repo rate is expected to be with a 50%, 75% and 90% probability. Broken lines represent the Riksbank’s forecast.

Figure 1.2. GDP with uncertainty bandsAnnual percentage change, seasonally-adjusted data

-8

-6

-4

-2

0

2

4

6

04 05 06 07 08 09 10 11 12 13

-8

-6

-4

-2

0

2

4

6

90%

75%

50%

Otcome

Forecast

Sources: Statistics Sweden and the Riksbank

Note.The uncertainty band shows the band within which GDP growth is expected to be with a 50%, 75% and 90% probability. Broken lines represent the Riksbank’s forecast.

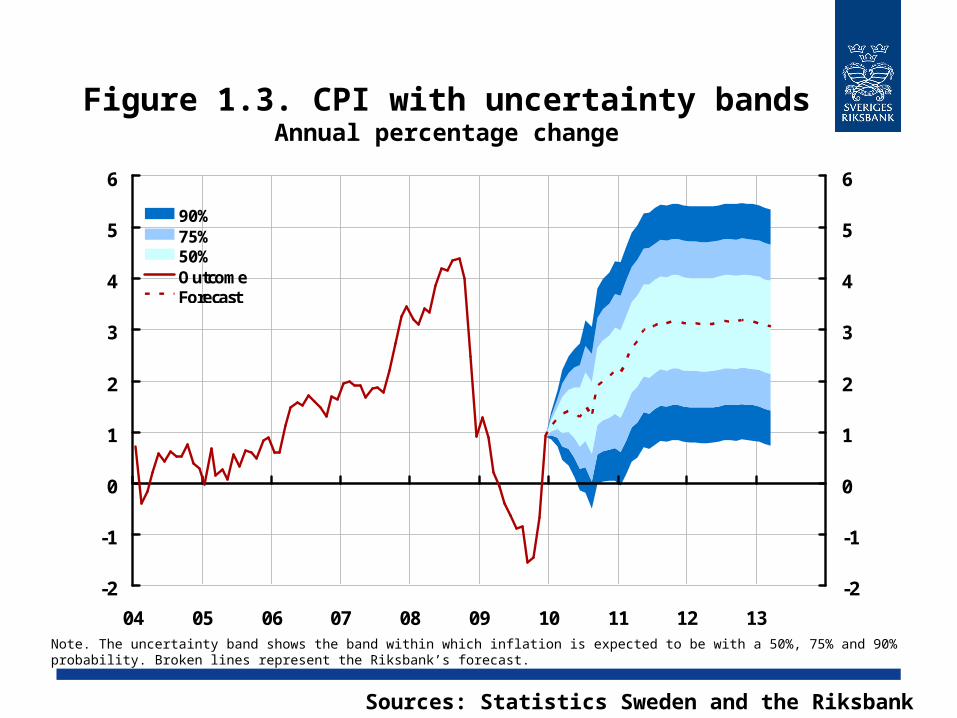

Figure 1.3. CPI with uncertainty bandsAnnual percentage change

-2

-1

0

1

2

3

4

5

6

04 05 06 07 08 09 10 11 12 13

-2

-1

0

1

2

3

4

5

6

90%75%50%OutcomeForecast

Sources: Statistics Sweden and the Riksbank

Note. The uncertainty band shows the band within which inflation is expected to be with a 50%, 75% and 90% probability. Broken lines represent the Riksbank’s forecast.

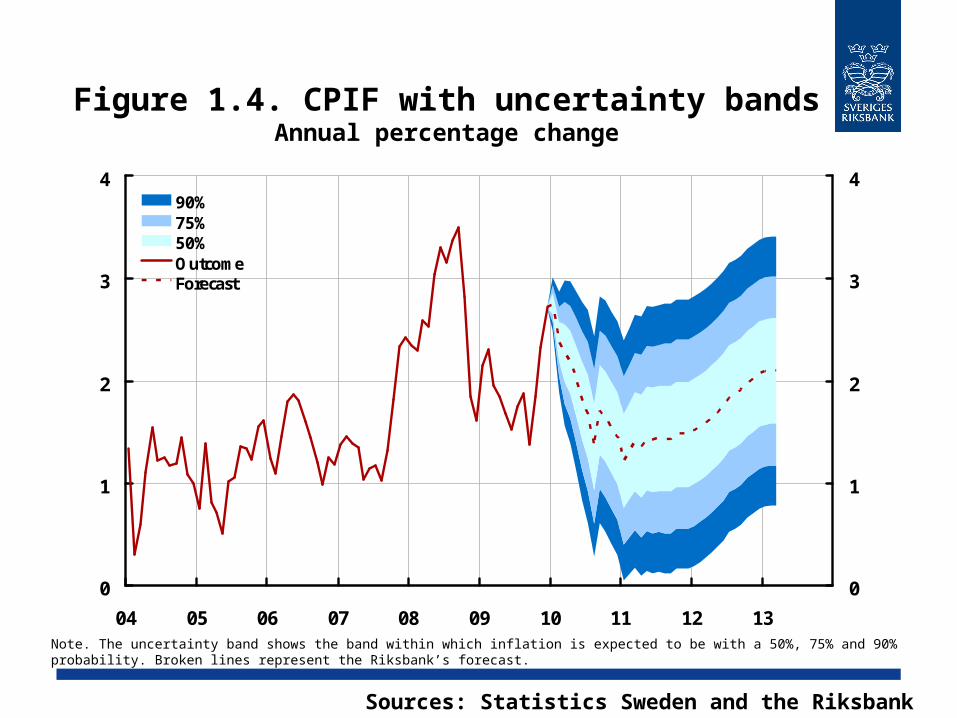

Figure 1.4. CPIF with uncertainty bandsAnnual percentage change

0

1

2

3

4

04 05 06 07 08 09 10 11 12 13

0

1

2

3

490%75%50%OutcomeForecast

Sources: Statistics Sweden and the Riksbank

Note. The uncertainty band shows the band within which inflation is expected to be with a 50%, 75% and 90% probability. Broken lines represent the Riksbank’s forecast.

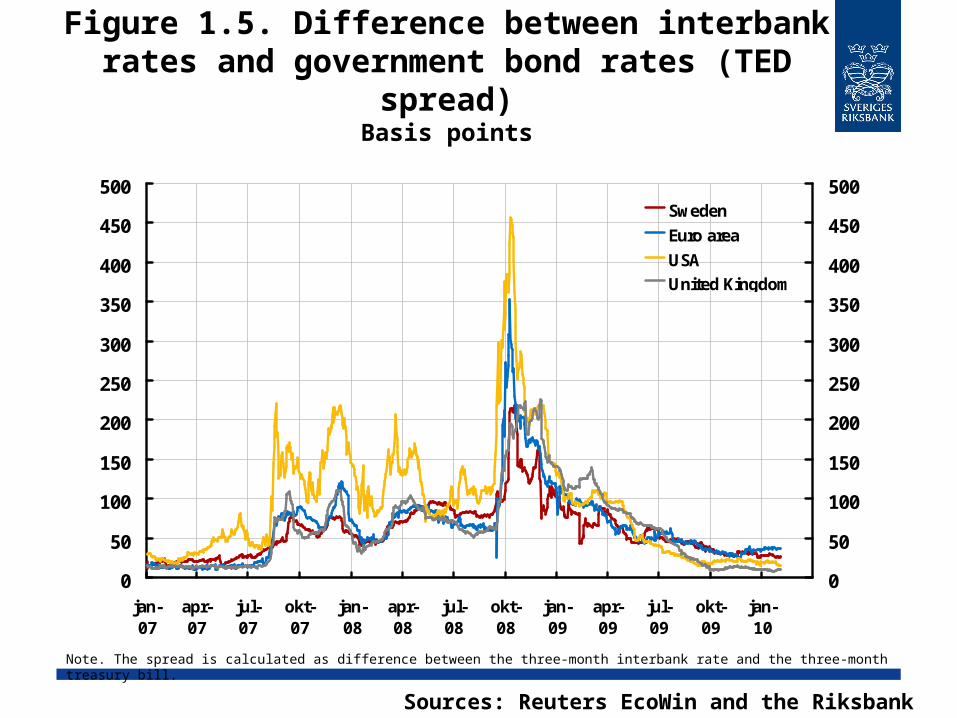

Figure 1.5. Difference between interbank rates and government bond rates (TED

spread)Basis points

0

50

100

150

200

250

300

350

400

450

500

jan-07

apr-07

jul-07

okt-07

jan-08

apr-08

jul-08

okt-08

jan-09

apr-09

jul-09

okt-09

jan-10

0

50

100

150

200

250

300

350

400

450

500Sweden

Euro area

USAUnited Kingdom

Sources: Reuters EcoWin and the Riksbank

Note. The spread is calculated as difference between the three-month interbank rate and the three-month treasury bill.

Figure 1.6. GDP-growth abroadAnnual percentage change

-1

0

1

2

3

4

5

6

7

70 75 80 85 90 95 00 05 10

-1

0

1

2

3

4

5

6

7

Sources: IMF and the RiksbankNote. Striped bars represent the Riksbank’s forecast.

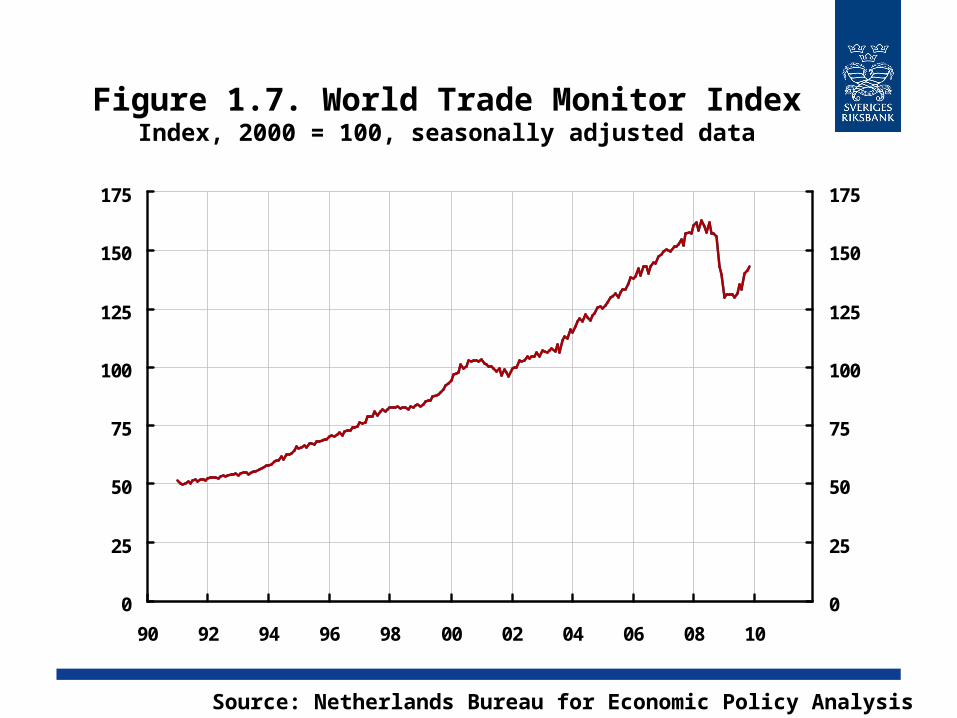

Figure 1.7. World Trade Monitor IndexIndex, 2000 = 100, seasonally adjusted data

0

25

50

75

100

125

150

175

90 92 94 96 98 00 02 04 06 08 10

0

25

50

75

100

125

150

175

Source: Netherlands Bureau for Economic Policy Analysis

Figure 1.8. Oil price, Brent crudeUSD per barrel

0

20

40

60

80

100

120

140

00 01 02 03 04 05 06 07 08 09 10 11 12 13

0

20

40

60

80

100

120

140Outcome

Futures, average up to and including 4 February

Futures, December

Sources: Intercontinental Exchange and the RiksbankNote. Futures are calculated as a 15-day average. Outcomes represent monthly averages of spot prices.

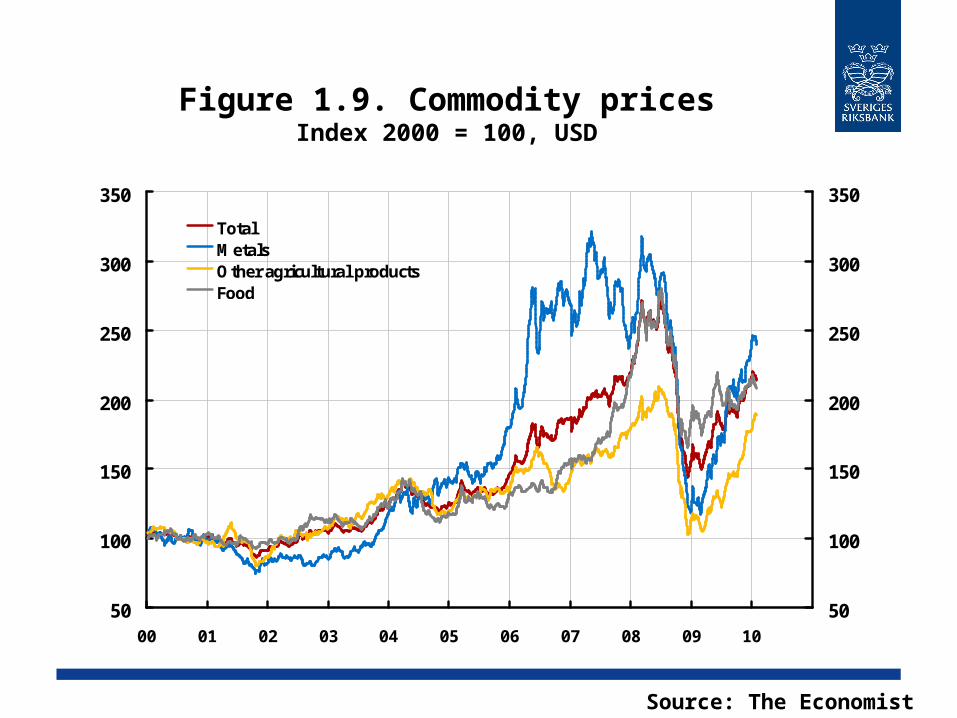

Figure 1.9. Commodity pricesIndex 2000 = 100, USD

50

100

150

200

250

300

350

00 01 02 03 04 05 06 07 08 09 10

50

100

150

200

250

300

350

TotalMetalsOther agricultural productsFood

Source: The Economist

Figure 1.10. Development for GDP in different regions and countries

Quarterly changes in per cent calculated in annualised terms, seasonally-adjusted data

-20

-15

-10

-5

0

5

10

00 01 02 03 04 05 06 07 08 09 10 11 12 13

-20

-15

-10

-5

0

5

10

Sweden

Euro area

USA

Sources: Bureau of Economic Analysis, Eurostat, Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank’s forecast.

Figure 1.11. Public sector net lendingPercentage of GDP

-20

-15

-10

-5

0

5

10

15

20

Swed

en

Euro ar

eaUS

A

Unite

d King

dom

Germ

any

Fran

ceSp

ain

Norw

ay

Icelan

d

Gree

ce

200720092011

Sources: OECD and the RiksbankNote. Striped bars represent forecasts. The forecast for Sweden is the Riksbank's forecast, while for other countries it is the OECD's forecast, December 2009.

Figure 1.12. Comparison of recovery in Sweden, the euro area and USA

GDP-level, index 2007 quarter 4 = 100

Sources: Bureau of Economic Analysis, Eurostat, Statistics Sweden and the Riksbank.

Note. The quarter prior to the recession breaking out in the USA = 100. Broken lines represent the Riksbank's forecast.

94

96

98

100

102

104

106

108

110

07 08 09 10 11 12 13

94

96

98

100

102

104

106

108

110USA

Euro area

Sweden

Figure 1.13. TCW-weighted exchange rate Index, 18.11.92 = 100

Source: The RiksbankNote. Outcome data are daily rates and forecasts are quarterly averages. Broken lines represent the Riksbank’s forecast.

120

125

130

135

140

145

150

155

160

04 05 06 07 08 09 10 11 12 13

120

125

130

135

140

145

150

155

160

February

December

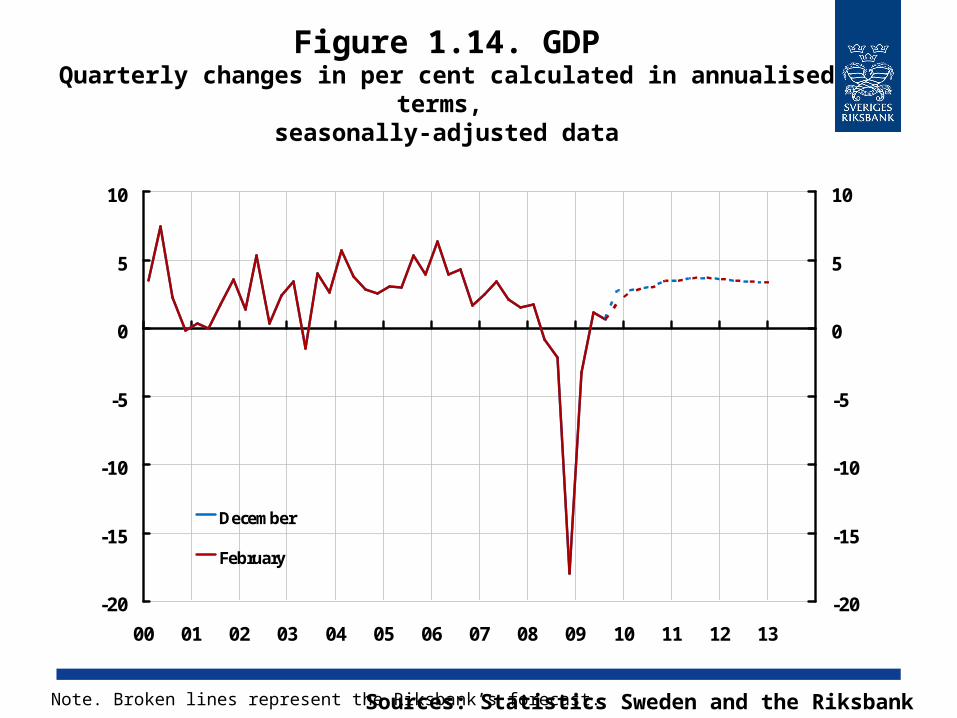

Figure 1.14. GDPQuarterly changes in per cent calculated in annualised

terms, seasonally-adjusted data

-20

-15

-10

-5

0

5

10

00 01 02 03 04 05 06 07 08 09 10 11 12 13

-20

-15

-10

-5

0

5

10

December

February

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank’s forecast.

Figure 1.15. Comparison of recovery following various recessions, GDP Sweden

Index in the quarter preceding the beginning of the recession = 100

92

94

96

98

100

102

104

106

108

110

112

114

116

118

-4 -2 0 2 4 6 8 10 12 14 16 18

92

94

96

98

100

102

104

106

108

110

112

114

116

1181990 Q2

1996 Q1

2000 Q3

2008 Q1

Sources: Statistics Sweden and the Riksbank

Note. Legends denote the quarter in which the index = 100. Broken lines represent the Riksbanks forecast. X-axis relates to quarters.

Figure 1.16. Households’ consumption, disposable incomes

and saving ratio Annual percentage change, fixed prices and percentage of

disposable income

-2

-1

0

1

2

3

4

5

6

7

8

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

-4

-2

0

2

4

6

8

10

12

14

16

Consumption (left scale)Disposable income (left scale)Saving ratio (right scale)

Sources: Statistics Sweden and the RiksbankNote. Broken lines and striped bars represent the Riksbank’s forecast.

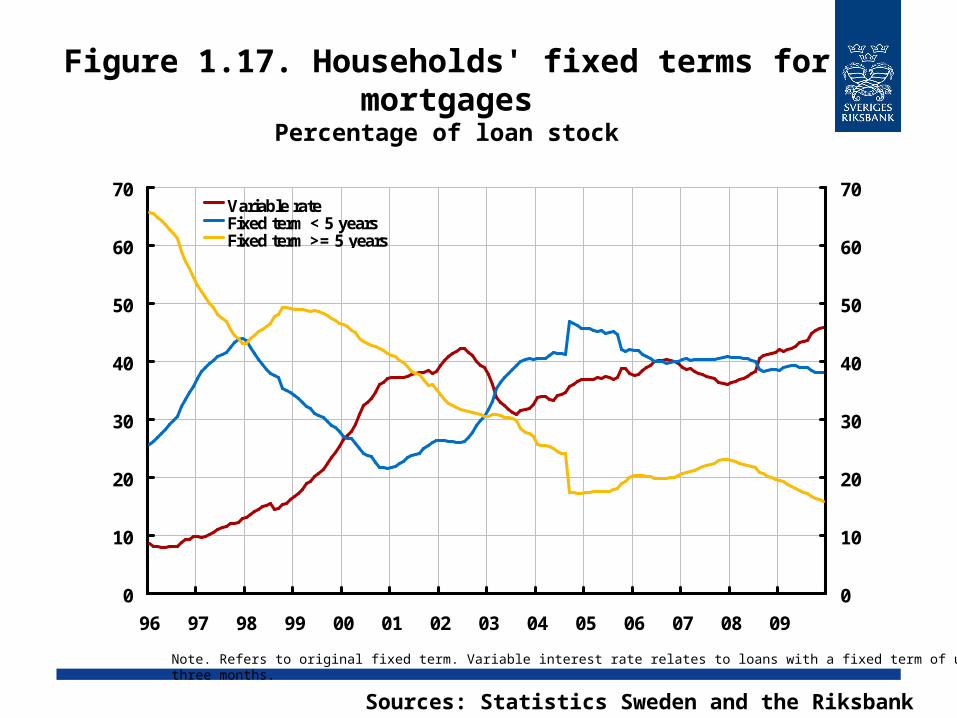

Figure 1.17. Households' fixed terms for mortgages

Percentage of loan stock

Sources: Statistics Sweden and the Riksbank

Note. Refers to original fixed term. Variable interest rate relates to loans with a fixed term of up to three months.

0

10

20

30

40

50

60

70

96 97 98 99 00 01 02 03 04 05 06 07 08 09

0

10

20

30

40

50

60

70Variable rateFixed term < 5 yearsFixed term >= 5 years

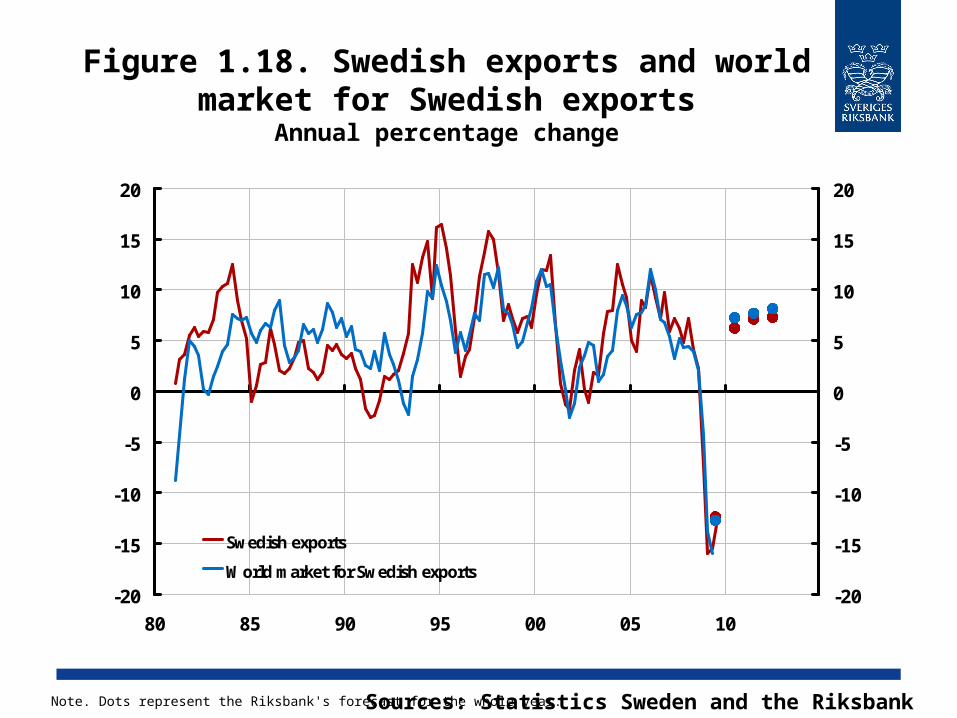

Figure 1.18. Swedish exports and world market for Swedish exports

Annual percentage change

Sources: Statistics Sweden and the RiksbankNote. Dots represent the Riksbank's forecast for the whole year.

-20

-15

-10

-5

0

5

10

15

20

80 85 90 95 00 05 10

-20

-15

-10

-5

0

5

10

15

20

Swedish exports

World market for Swedish exports

Figure 1.19. Gross fixed capital formationQuarterly changes in per cent calculated in annualised

terms, seasonally-adjusted data

-50

-40

-30

-20

-10

0

10

20

04 05 06 07 08 09 10 11 12 13

-50

-40

-30

-20

-10

0

10

20

December

February

Sources: Statistics Sweden and the Riksbank Note. Seasonally adjusted by the Riksbank. Broken lines represent the Riksbank’s forecast.

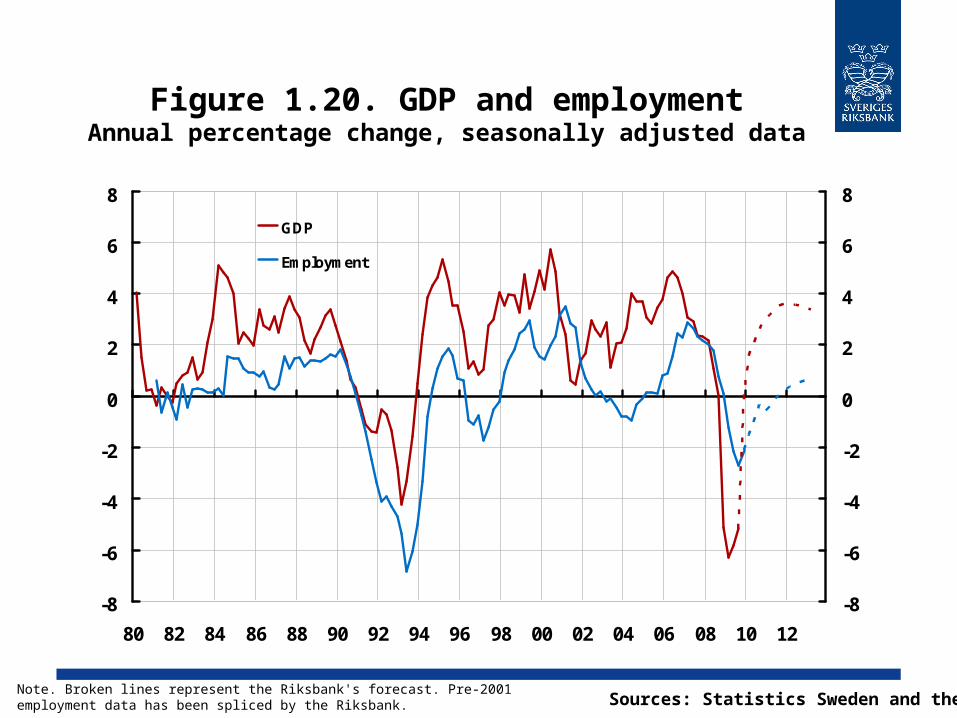

Figure 1.20. GDP and employmentAnnual percentage change, seasonally adjusted data

-8

-6

-4

-2

0

2

4

6

8

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12

-8

-6

-4

-2

0

2

4

6

8

GDP

Employment

Note. Broken lines represent the Riksbank's forecast. Pre-2001 employment data has been spliced by the Riksbank. Sources: Statistics Sweden and the Riksbank

Figure 1.21. Labour force and number of employed

Thousands, seasonally-adjusted data

3800

4000

4200

4400

4600

4800

5000

80 85 90 95 00 05 10

3800

4000

4200

4400

4600

4800

5000Employed, 16-64 years

Employed, 15-74 years

Labour force, 16-64 years

Labour force, 15-74 years

Sources: Statistics Sweden and the Riksbank

Note. Pre-1993 data has been spliced by the Riksbank. Broken lines represent the Riksbank’s forecast, 15-74 year.

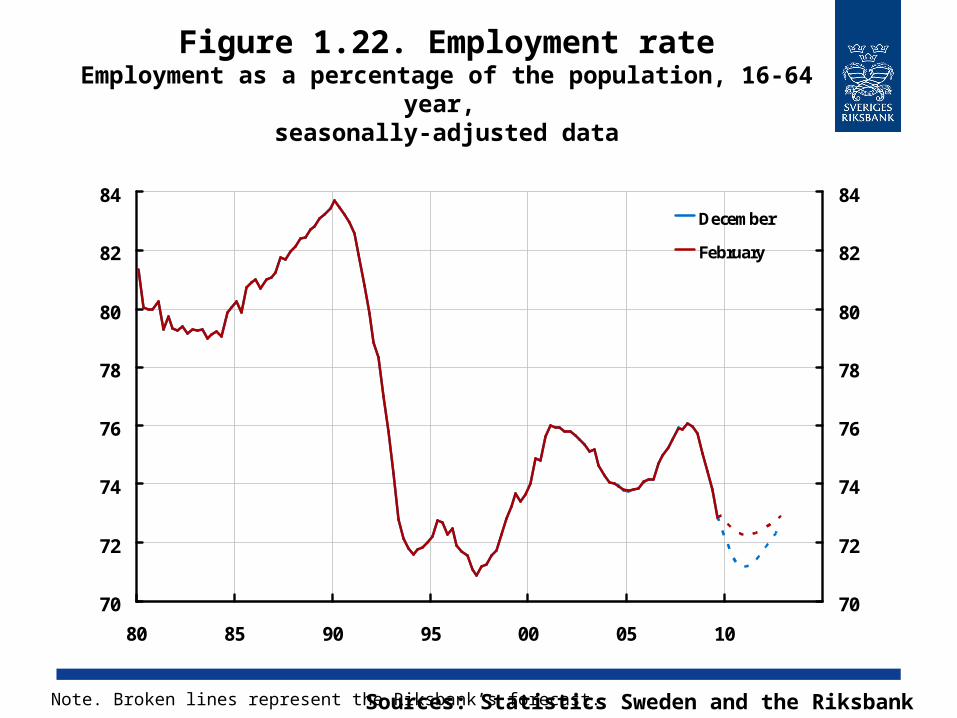

Figure 1.22. Employment rateEmployment as a percentage of the population, 16-64

year, seasonally-adjusted data

70

72

74

76

78

80

82

84

80 85 90 95 00 05 10

70

72

74

76

78

80

82

84December

February

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank’s forecast.

Figure 1.23. UnemploymentPercentage of the labour force, seasonally-adjusted data

0

2

4

6

8

10

12

14

80 85 90 95 00 05 10

0

2

4

6

8

10

12

14

Unemployment, 16-64 years

Unemployment, 15-74 years

February

December

Sources: Statistics Sweden and the Riksbank

Note. Pre-1993 data has been spliced by the Riksbank. Broken lines represent the Riksbank’s forecast, 15-74 years.

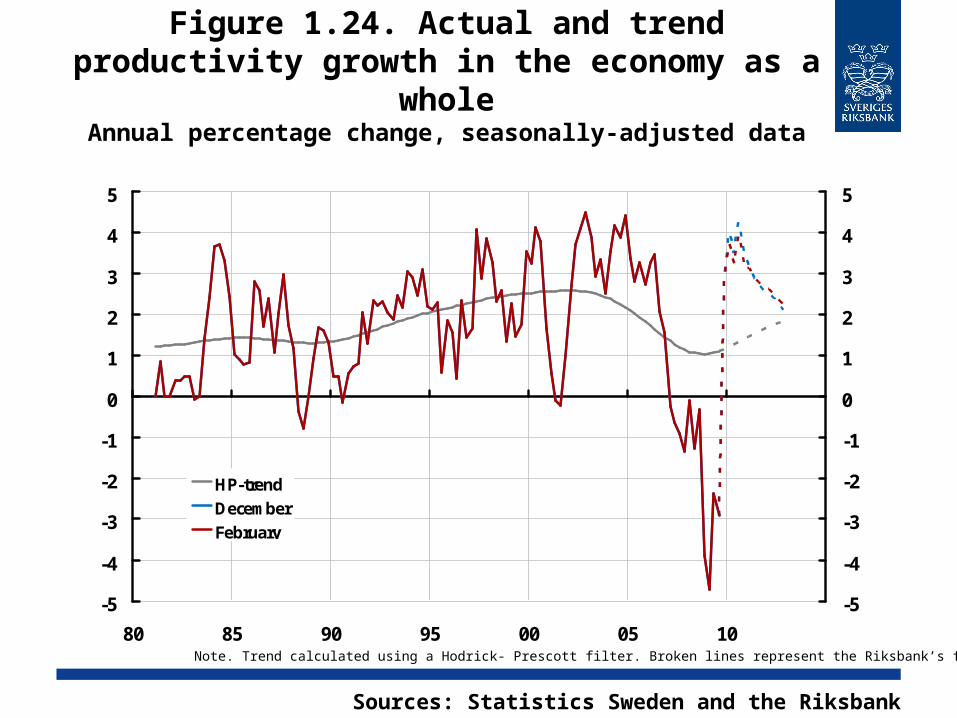

Figure 1.24. Actual and trend productivity growth in the economy as a whole

Annual percentage change, seasonally-adjusted data

-5

-4

-3

-2

-1

0

1

2

3

4

5

80 85 90 95 00 05 10

-5

-4

-3

-2

-1

0

1

2

3

4

5

HP-trendDecemberFebruary

Sources: Statistics Sweden and the Riksbank

Note. Trend calculated using a Hodrick- Prescott filter. Broken lines represent the Riksbank’s forecast.

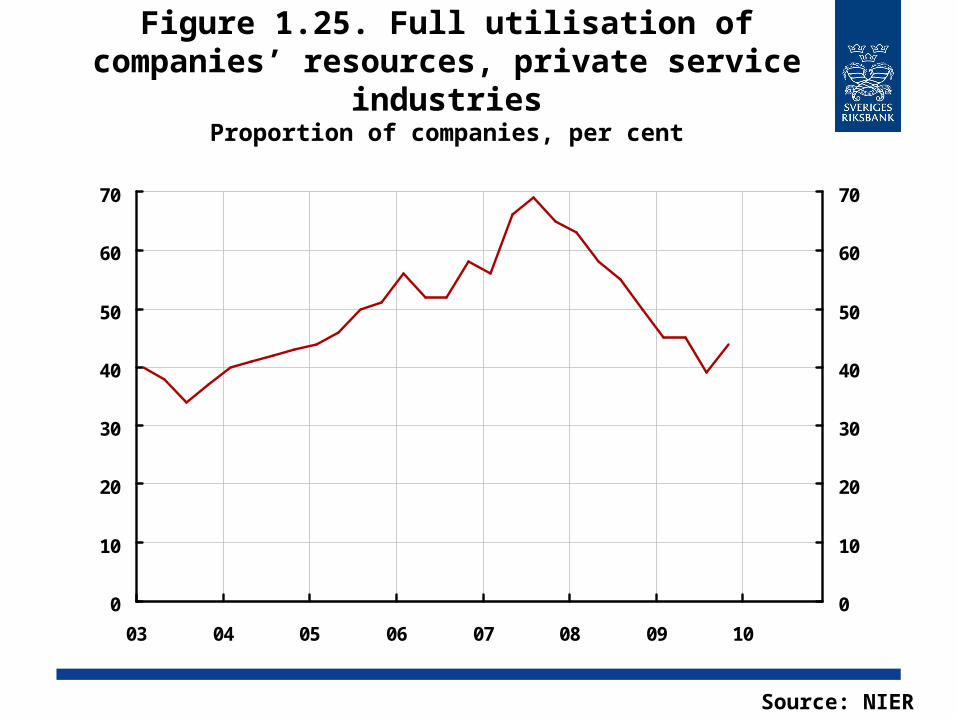

Figure 1.25. Full utilisation of companies’ resources, private service industries

Proportion of companies, per cent

0

10

20

30

40

50

60

70

03 04 05 06 07 08 09 10

0

10

20

30

40

50

60

70

Source: NIER

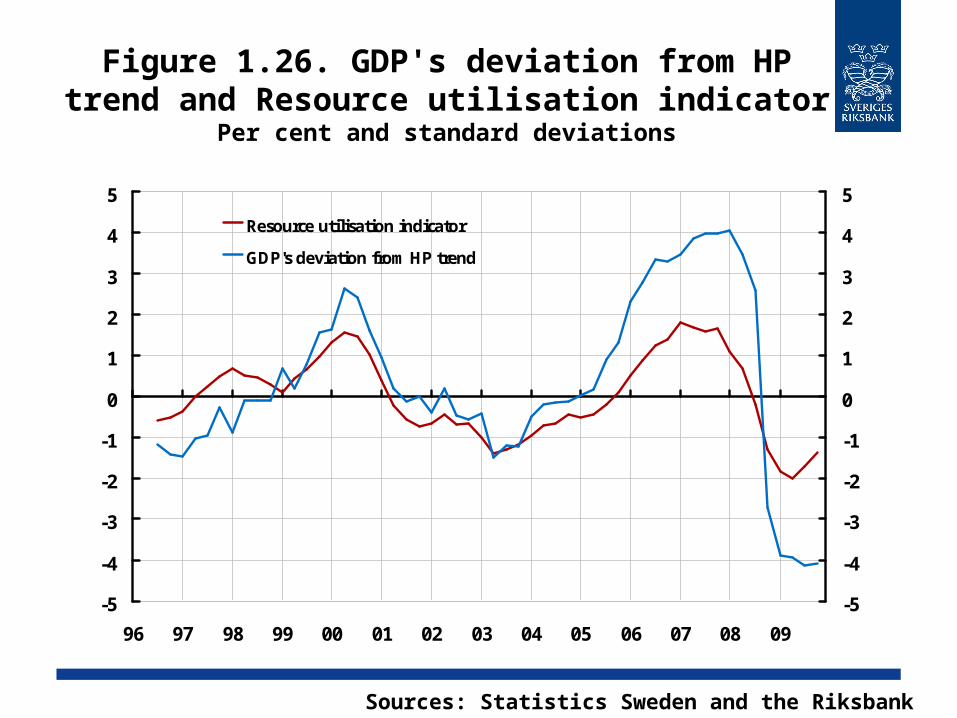

Figure 1.26. GDP's deviation from HP trend and Resource utilisation indicator

Per cent and standard deviations

-5

-4

-3

-2

-1

0

1

2

3

4

5

96 97 98 99 00 01 02 03 04 05 06 07 08 09

-5

-4

-3

-2

-1

0

1

2

3

4

5

Resource utilisation indicator

GDP's deviation from HP trend

Sources: Statistics Sweden and the Riksbank

Figure 1.27. Estimated gapsPercentage deviation from the HP trend

-5

-4

-3

-2

-1

0

1

2

3

4

5

80 85 90 95 00 05 10

-5

-4

-3

-2

-1

0

1

2

3

4

5GDP

Hours worked

Employment

Sources: Statistics Sweden and the Riksbank

Note. These gaps should not necessarily be interpreted as the Riksbank's overall assesment of resource utilisation. Broken lines represent the Riksbank’s forecast.

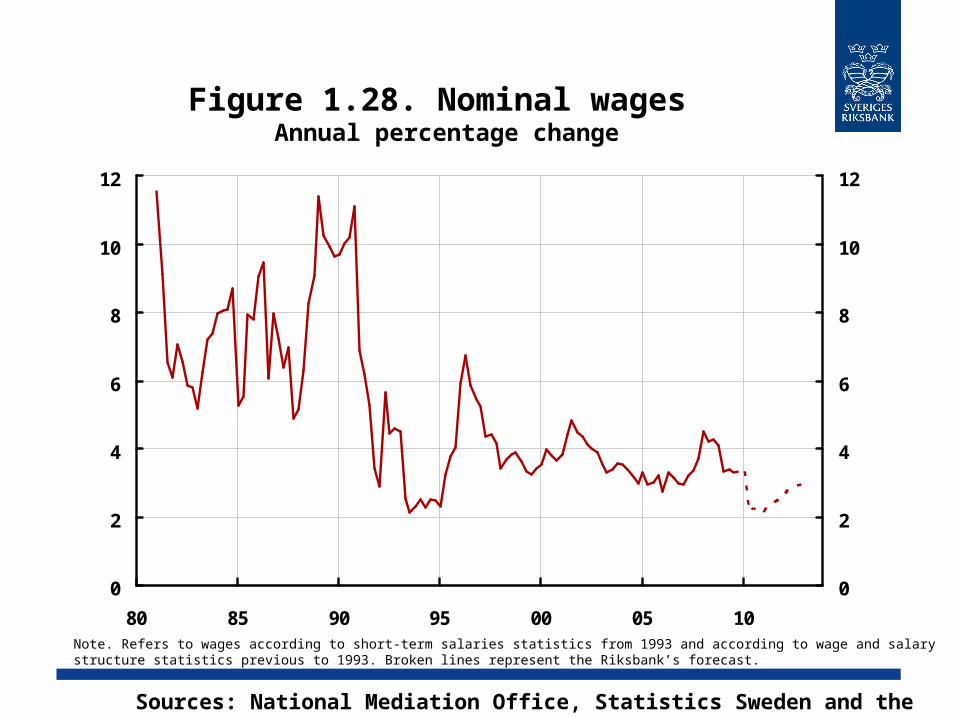

Figure 1.28. Nominal wages Annual percentage change

0

2

4

6

8

10

12

80 85 90 95 00 05 10

0

2

4

6

8

10

12

Sources: National Mediation Office, Statistics Sweden and the Riksbank

Note. Refers to wages according to short-term salaries statistics from 1993 and according to wage and salary structure statistics previous to 1993. Broken lines represent the Riksbank’s forecast.

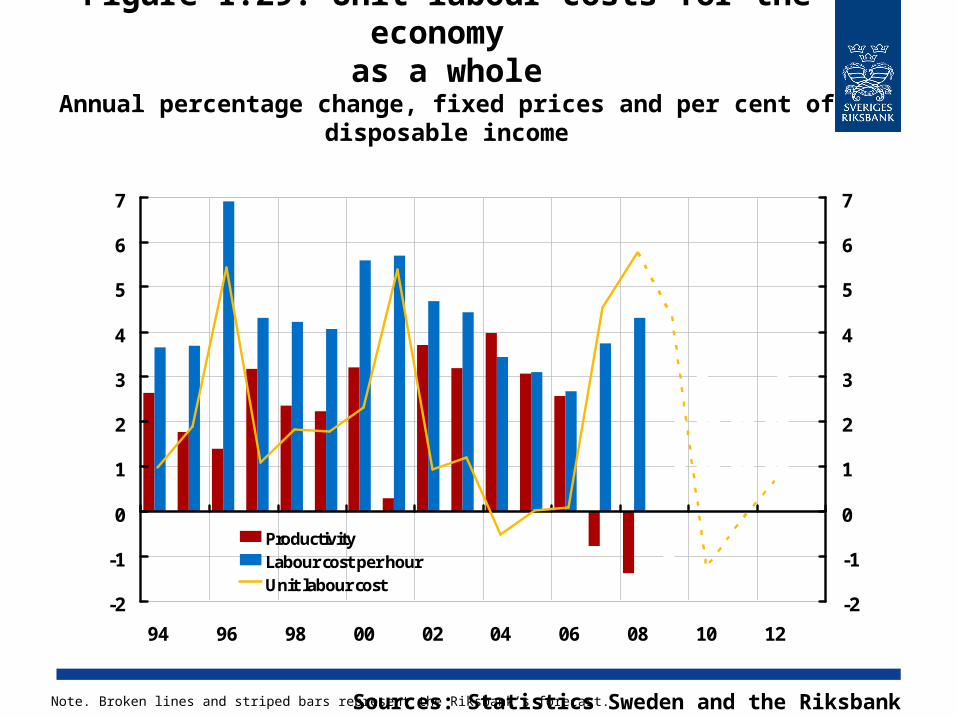

Figure 1.29. Unit labour costs for the economy as a whole

Annual percentage change, fixed prices and per cent of disposable income

-2

-1

0

1

2

3

4

5

6

7

94 96 98 00 02 04 06 08 10 12

-2

-1

0

1

2

3

4

5

6

7

ProductivityLabour cost per hourUnit labour cost

Sources: Statistics Sweden and the Riksbank Note. Broken lines and striped bars represent the Riksbank’s forecast.

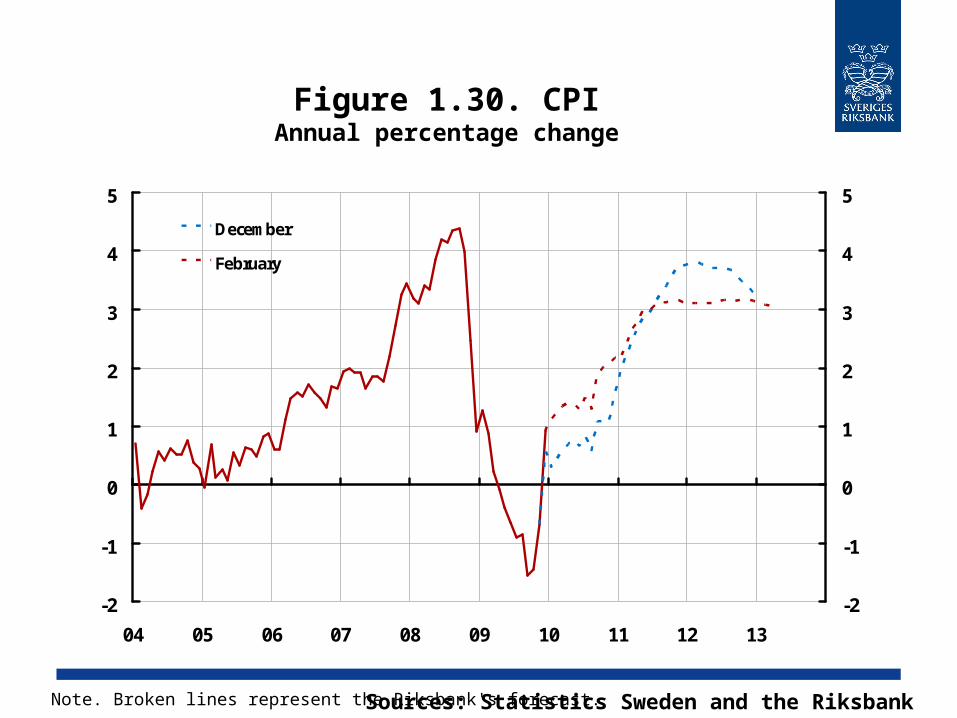

Figure 1.30. CPIAnnual percentage change

-2

-1

0

1

2

3

4

5

04 05 06 07 08 09 10 11 12 13

-2

-1

0

1

2

3

4

5

December

February

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

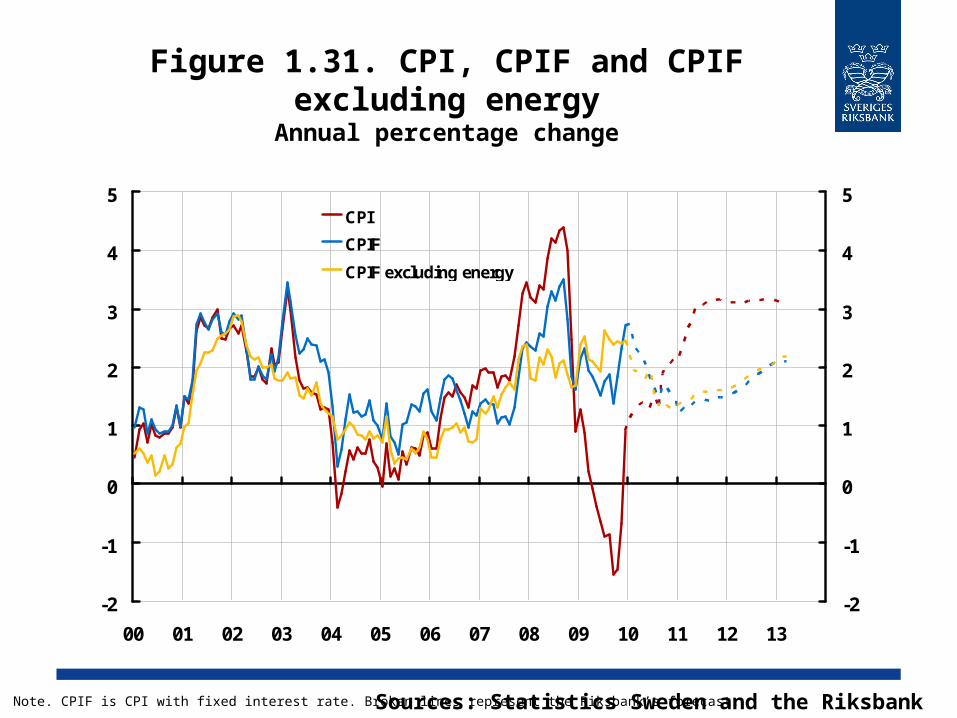

Figure 1.31. CPI, CPIF and CPIF excluding energy

Annual percentage change

-2

-1

0

1

2

3

4

5

00 01 02 03 04 05 06 07 08 09 10 11 12 13

-2

-1

0

1

2

3

4

5CPI

CPIF

CPIF excluding energy

Sources: Statistics Sweden and the Riksbank Note. CPIF is CPI with fixed interest rate. Broken lines represent the Riksbank’s forecast.

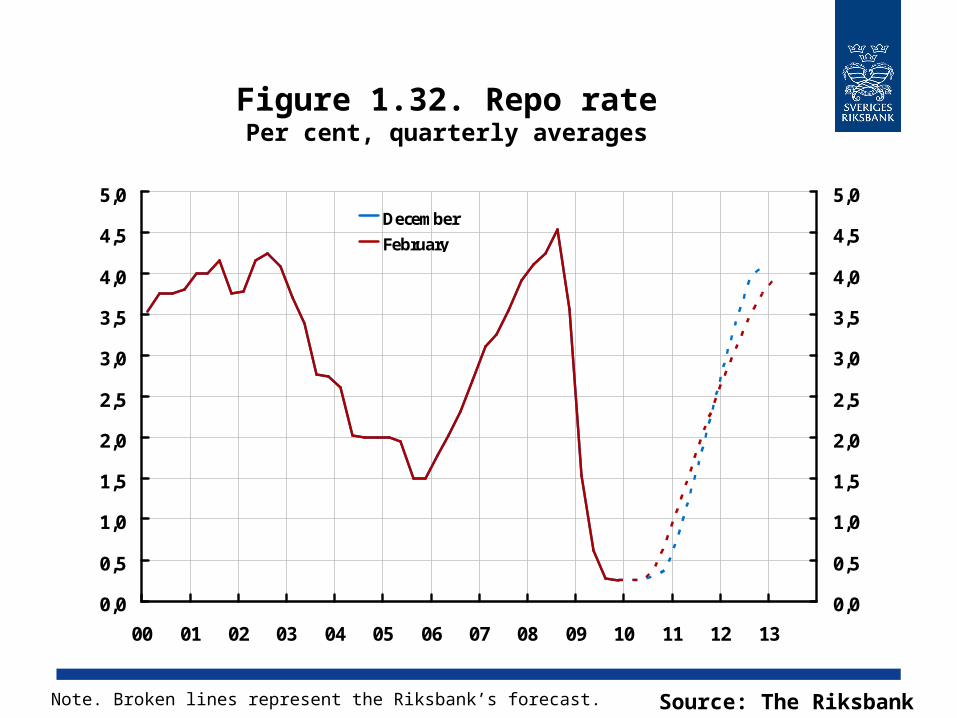

Figure 1.32. Repo ratePer cent, quarterly averages

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

00 01 02 03 04 05 06 07 08 09 10 11 12 13

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0December

February

Source: The RiksbankNote. Broken lines represent the Riksbank’s forecast.

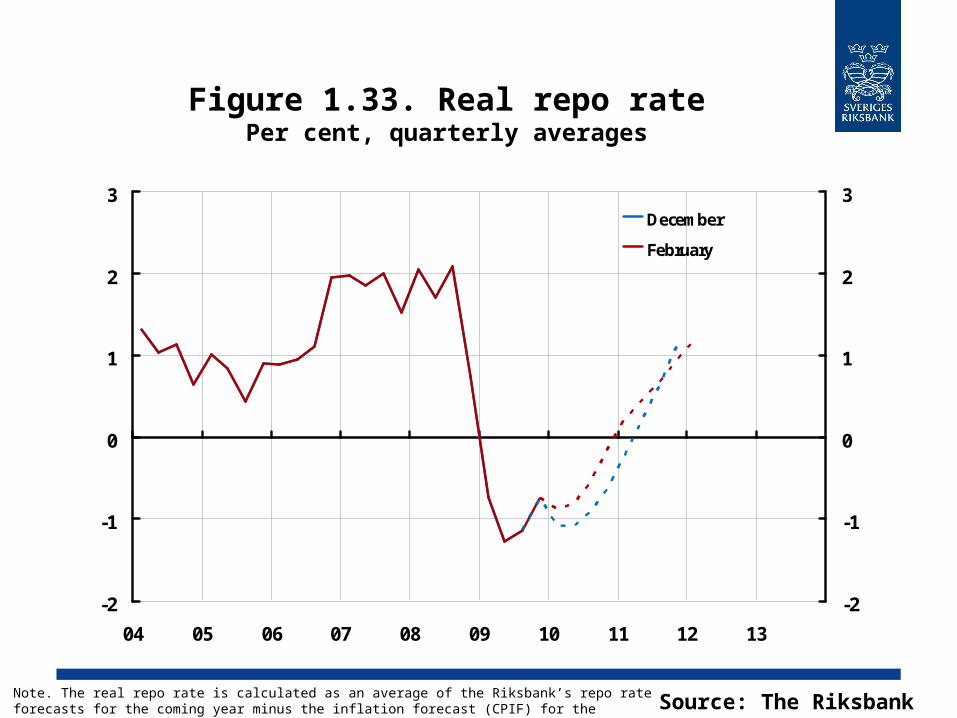

Figure 1.33. Real repo ratePer cent, quarterly averages

-2

-1

0

1

2

3

04 05 06 07 08 09 10 11 12 13

-2

-1

0

1

2

3December

February

Source: The RiksbankNote. The real repo rate is calculated as an average of the Riksbank’s repo rate forecasts for the coming year minus the inflation forecast (CPIF) for the corresponding period. Broken lines represent the Riksbank’s forecast.

Figure 2.1. Hourly labour costAnnual percentage change

0

1

2

3

4

5

04 05 06 07 08 09 10 11 12 13

0

1

2

3

4

5Higher wagesLower wagesMain scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

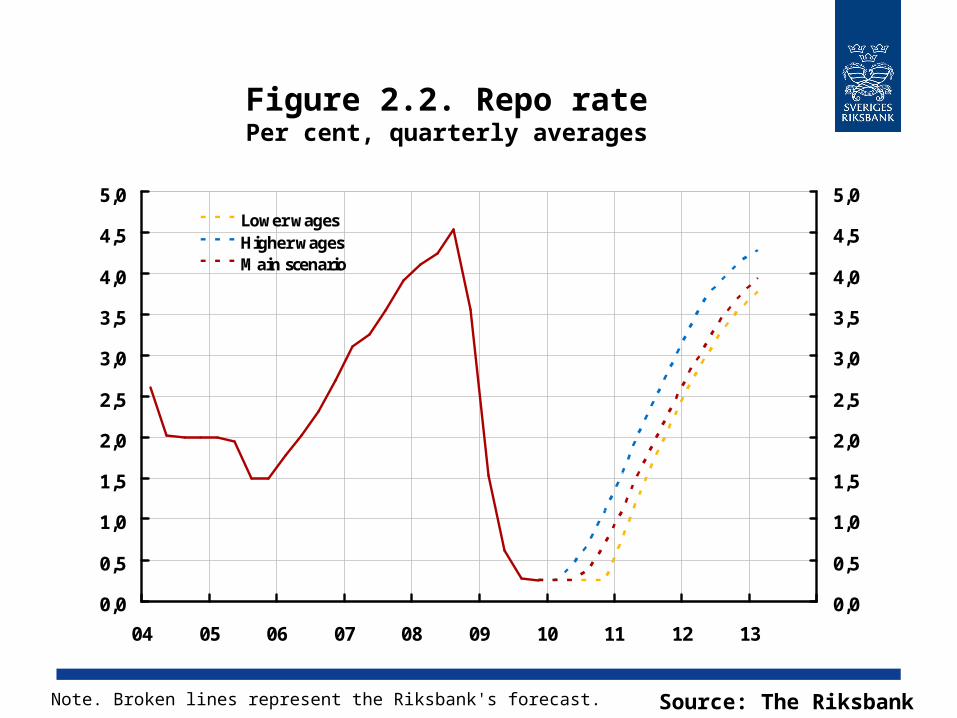

Figure 2.2. Repo ratePer cent, quarterly averages

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

04 05 06 07 08 09 10 11 12 13

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0Lower wagesHigher wagesMain scenario

Source: The RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.3. CPIFAnnual percentage change

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

04 05 06 07 08 09 10 11 12 13

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0Higher wagesLower wagesMain scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.4. Labour market gap (hours worked)

Percentage deviation from the HP trend

-3

-2

-1

0

1

2

3

4

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

-3

-2

-1

0

1

2

3

4

Higher wages

Lower wagesMain scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.5. Hours worked and trendMillions of hours per quarter, seasonally adjusted data

1720

1740

1760

1780

1800

1820

1840

1860

1880

00 01 02 03 04 05 06 07 08 09 10 11 12 13

1720

1740

1760

1780

1800

1820

1840

1860

1880Hours worked

Higher trend

Trend in the main scenario

Gap in main scenario

Gap in alternativescenario

Sources: Statistics Sweden and the RiksbankNote. The last two observations for hours worked refer to the Riksbank's forecast.

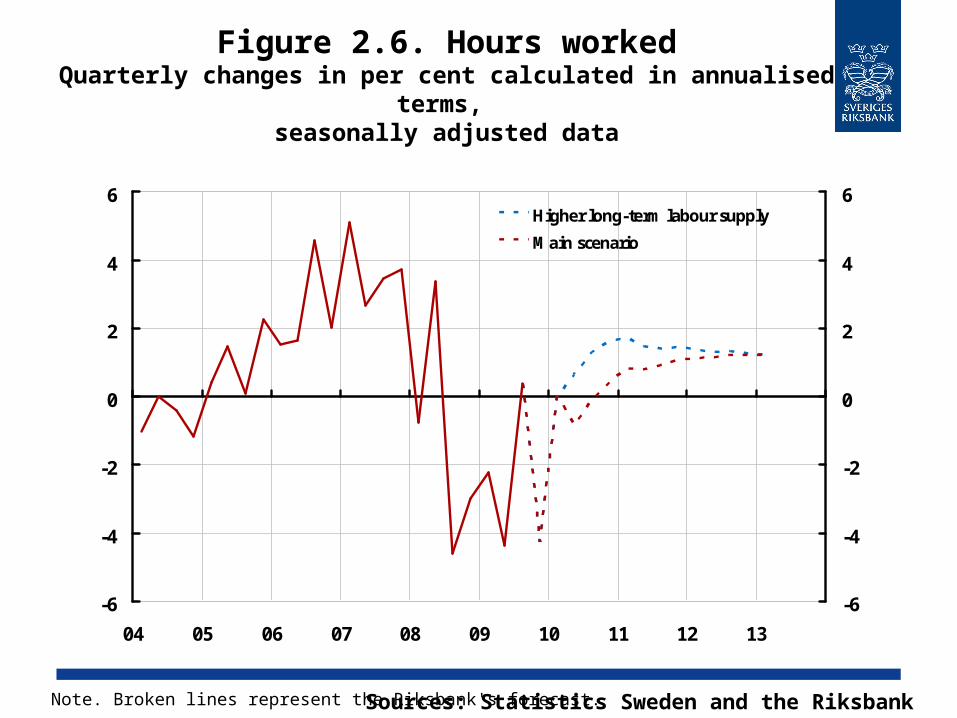

Figure 2.6. Hours workedQuarterly changes in per cent calculated in annualised

terms, seasonally adjusted data

-6

-4

-2

0

2

4

6

04 05 06 07 08 09 10 11 12 13

-6

-4

-2

0

2

4

6Higher long-term labour supply

Main scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.7. Repo ratePer cent, quarterly averages

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

04 05 06 07 08 09 10 11 12 13

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0Main scenarioHigher long-term labour supply

Source: The RiksbankNote. Broken lines represent the Riksbank's forecast.

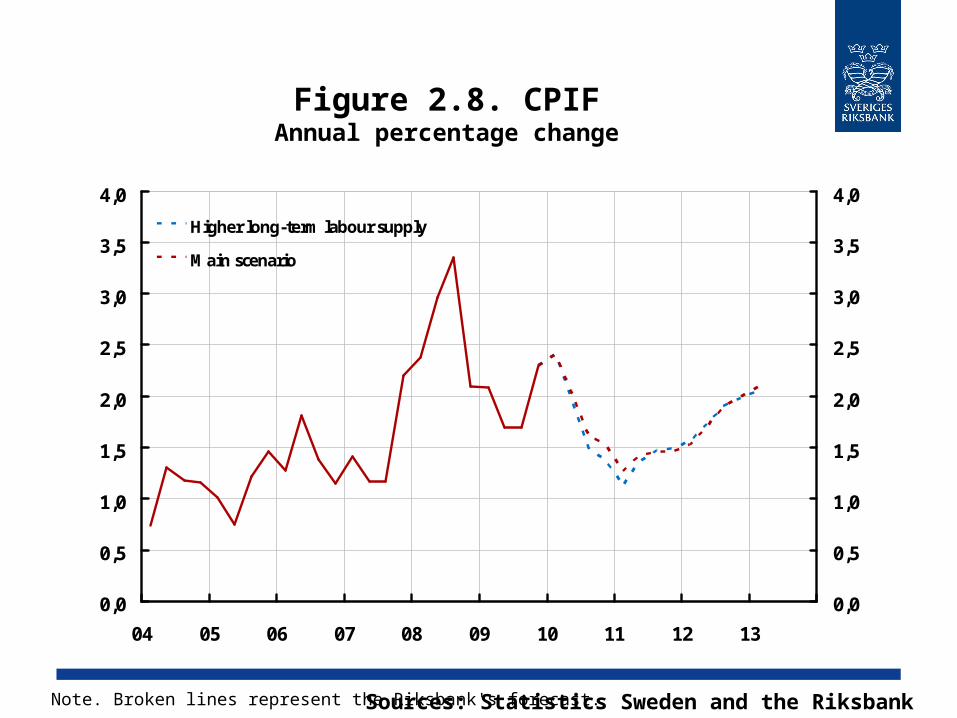

Figure 2.8. CPIFAnnual percentage change

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

04 05 06 07 08 09 10 11 12 13

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

Higher long-term labour supply

Main scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

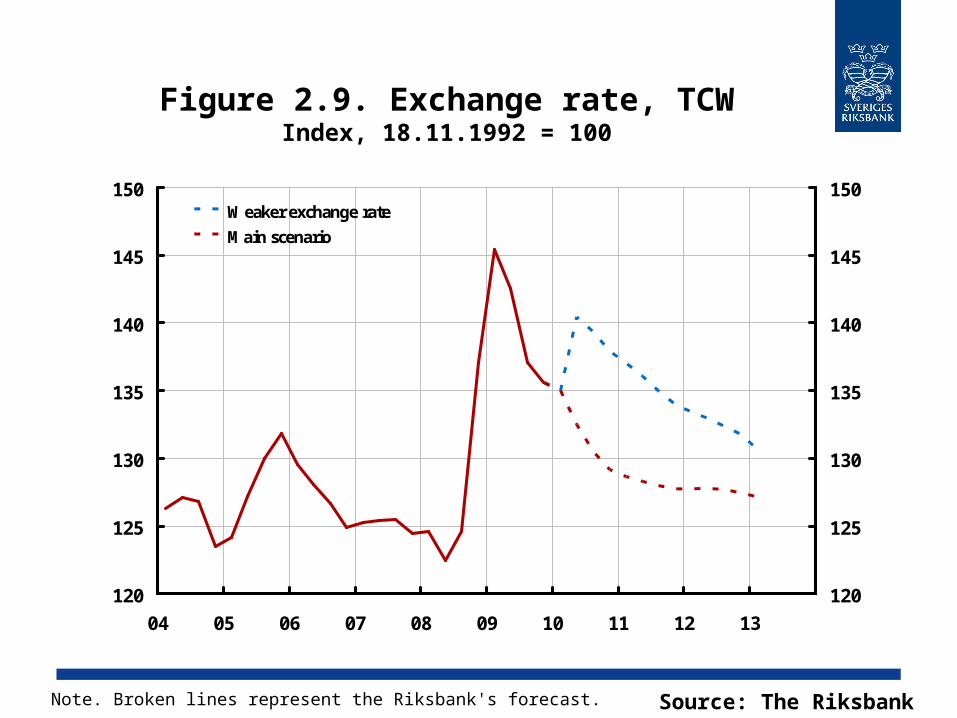

Figure 2.9. Exchange rate, TCWIndex, 18.11.1992 = 100

Source: The RiksbankNote. Broken lines represent the Riksbank's forecast.

120

125

130

135

140

145

150

04 05 06 07 08 09 10 11 12 13

120

125

130

135

140

145

150Weaker exchange rate

Main scenario

Figure 2.10. Labour market gap (hours worked)

Percentage deviation from the HP trend

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

-3

-2

-1

0

1

2

3

4

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

-3

-2

-1

0

1

2

3

4

Weaker exchange rate

Main scenario

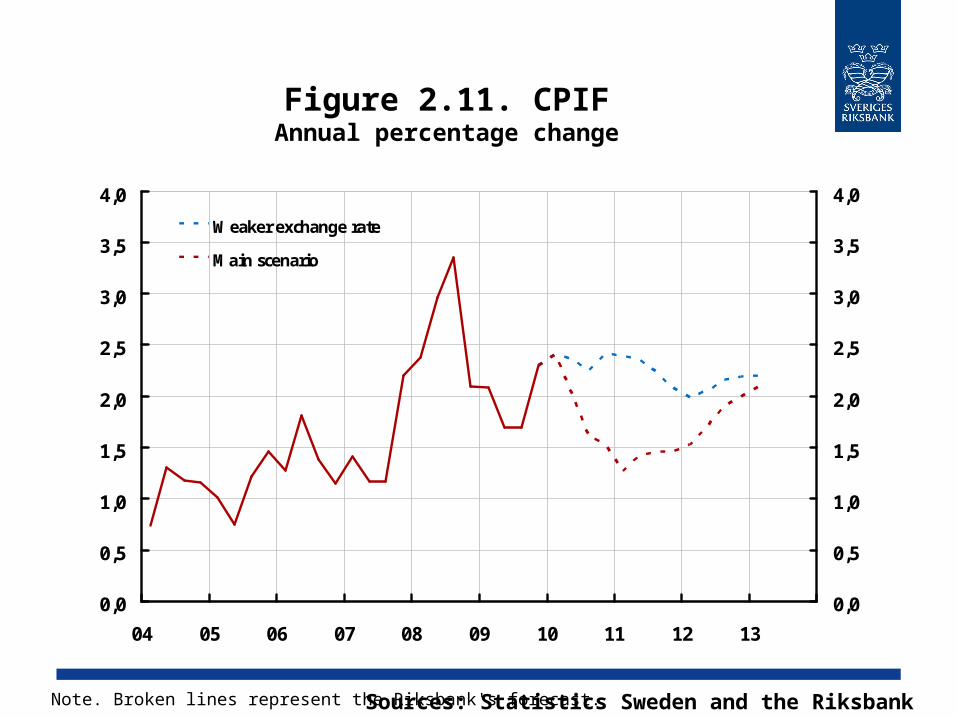

Figure 2.11. CPIFAnnual percentage change

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

04 05 06 07 08 09 10 11 12 13

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

Weaker exchange rate

Main scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.12. Repo ratePer cent, quarterly averages

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

04 05 06 07 08 09 10 11 12 13

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0Main scenarioWeaker exchange rate

Source: The RiksbankNote. Broken lines represent the Riksbank's forecast.

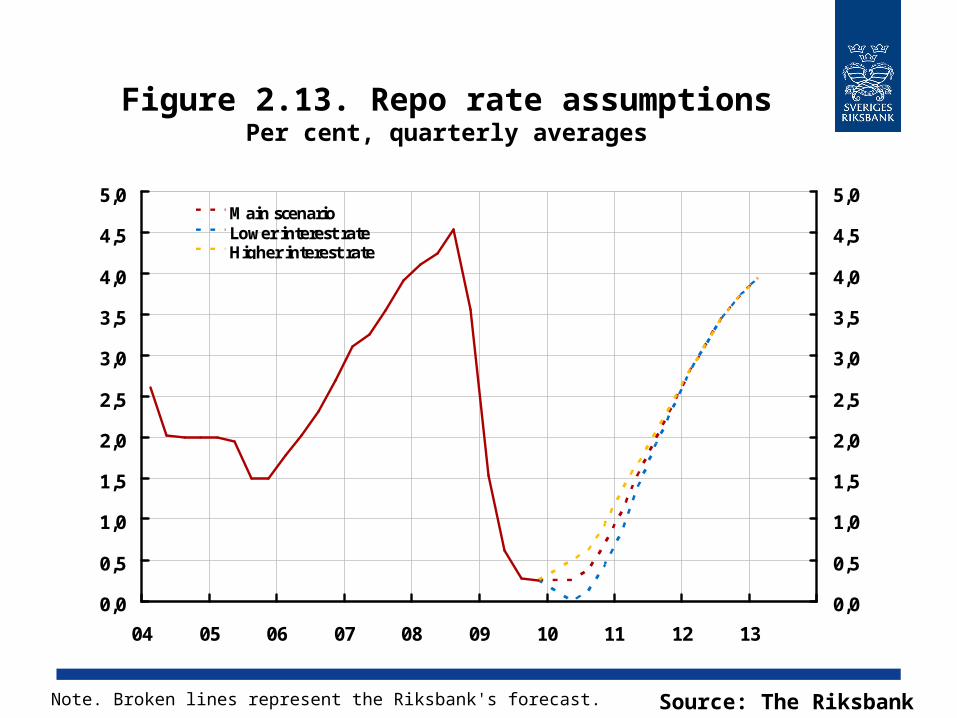

Figure 2.13. Repo rate assumptionsPer cent, quarterly averages

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

04 05 06 07 08 09 10 11 12 13

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0Main scenarioLower interest rateHigher interest rate

Source: The RiksbankNote. Broken lines represent the Riksbank's forecast.

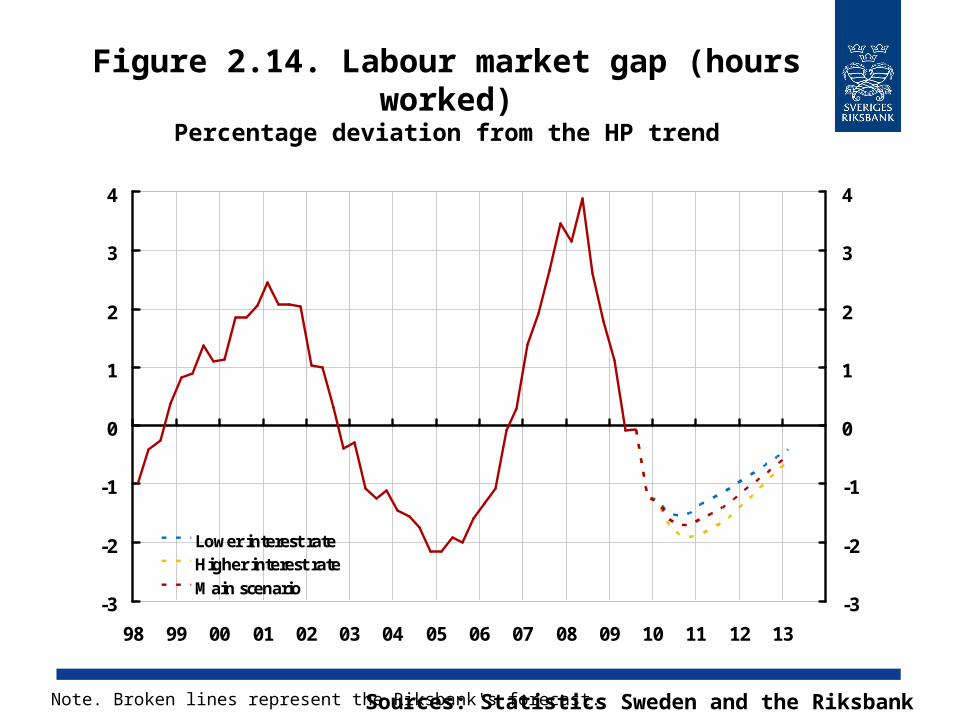

Figure 2.14. Labour market gap (hours worked)

Percentage deviation from the HP trend

-3

-2

-1

0

1

2

3

4

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

-3

-2

-1

0

1

2

3

4

Lower interest rateHigher interest rateMain scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

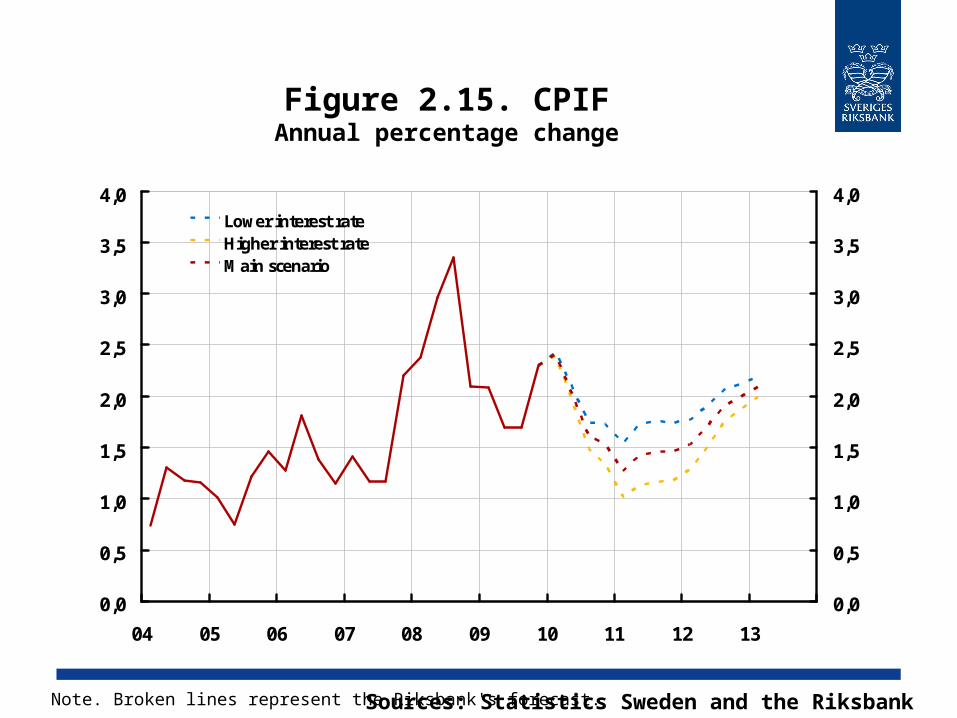

Figure 2.15. CPIFAnnual percentage change

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

04 05 06 07 08 09 10 11 12 13

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0Lower interest rateHigher interest rateMain scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

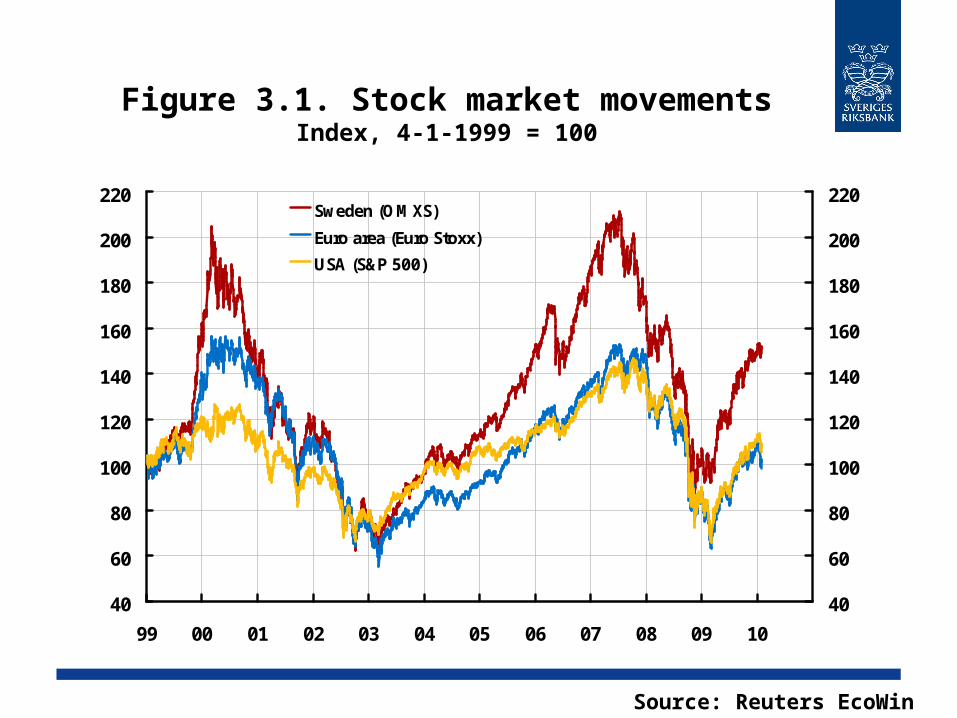

Figure 3.1. Stock market movementsIndex, 4-1-1999 = 100

40

60

80

100

120

140

160

180

200

220

99 00 01 02 03 04 05 06 07 08 09 10

40

60

80

100

120

140

160

180

200

220Sweden (OMXS)

Euro area (Euro Stoxx)

USA (S&P 500)

Source: Reuters EcoWin

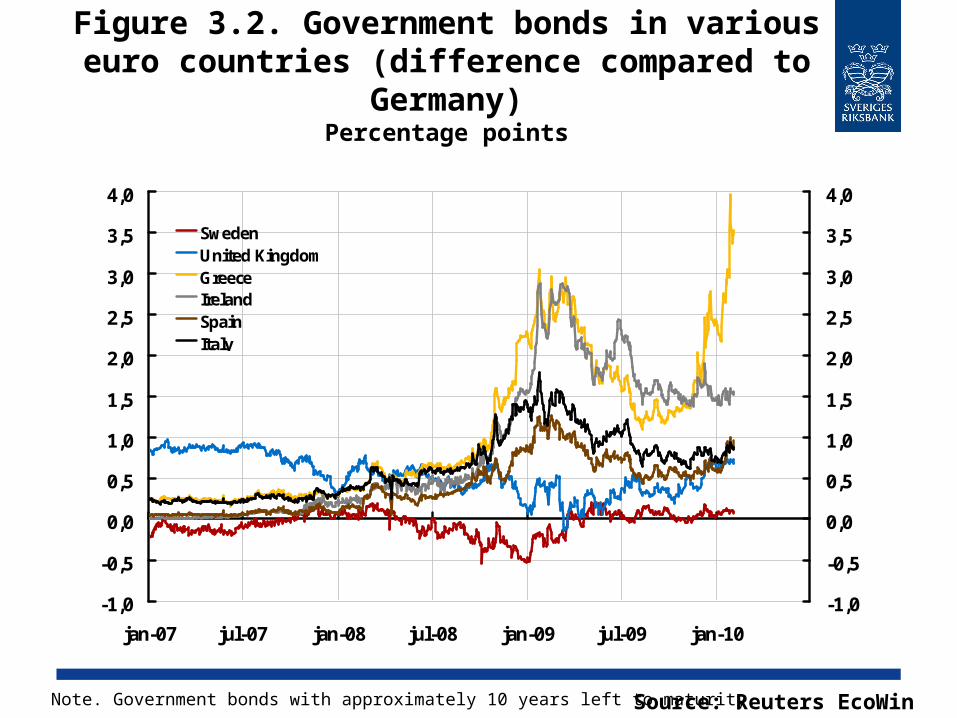

Figure 3.2. Government bonds in various euro countries (difference compared to

Germany)Percentage points

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

jan-07 jul-07 jan-08 jul-08 jan-09 jul-09 jan-10

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

SwedenUnited KingdomGreeceIrelandSpainItaly

Source: Reuters EcoWinNote. Government bonds with approximately 10 years left to maturity.

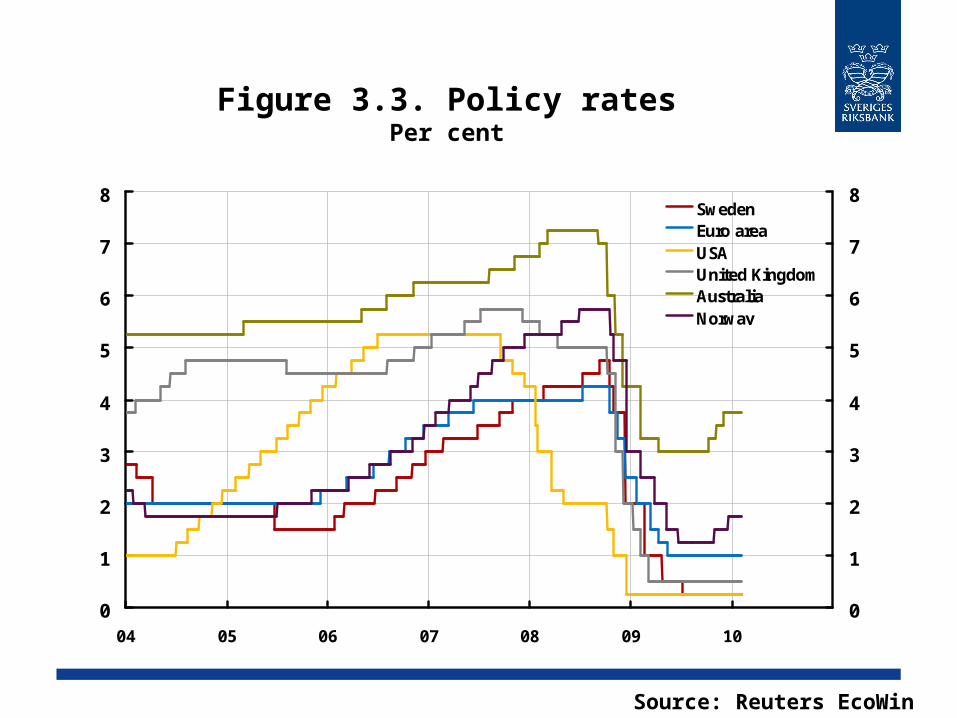

Figure 3.3. Policy ratesPer cent

0

1

2

3

4

5

6

7

8

04 05 06 07 08 09 10

0

1

2

3

4

5

6

7

8SwedenEuro areaUSAUnited KingdomAustraliaNorway

Source: Reuters EcoWin

Figure 3.4. Monetary policy expectations in Sweden according to money market

participants Per cent

0

1

2

3

4

5

6

06 07 08 09 10 11 12 13

0

1

2

3

4

5

6Repo rate

February

Forward rate 2010-02-04

Forward rate 2009-12-16

Survey, Prospera averages, 2010-01-13

Sources: Reuters Ecowin, TNS SIFO Prospera and the Riksbank

Note. Forward rates have been adjusted for risk premiums and describe the expected overnight rate. Broken lines represent the Riksbank's forecast.

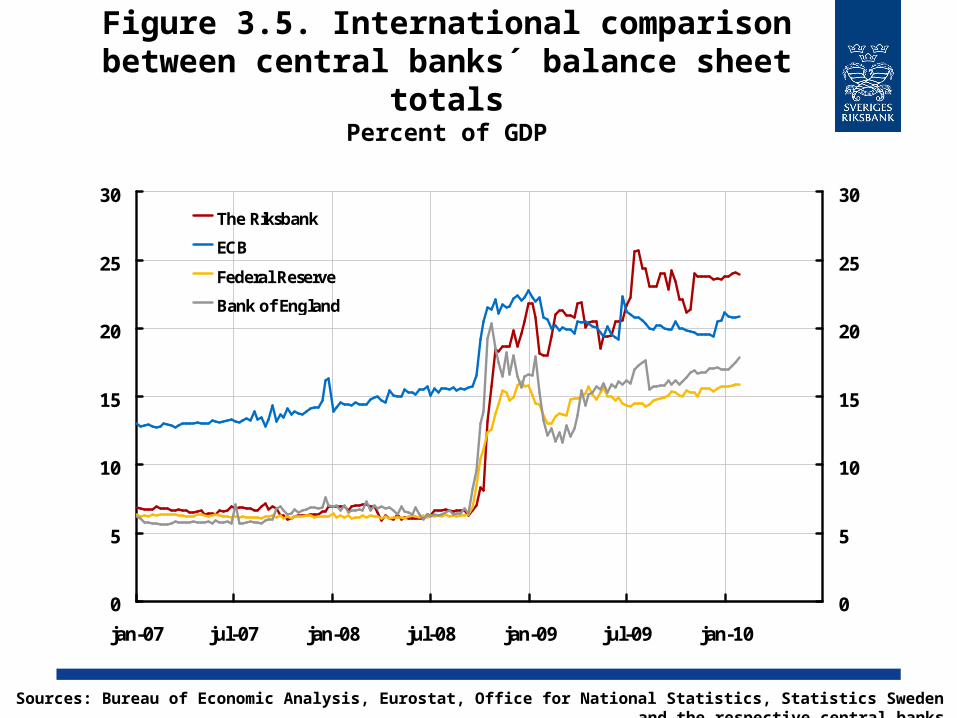

Figure 3.5. International comparison between central banks´ balance sheet

totalsPercent of GDP

0

5

10

15

20

25

30

jan-07 jul-07 jan-08 jul-08 jan-09 jul-09 jan-10

0

5

10

15

20

25

30The Riksbank

ECB

Federal Reserve

Bank of England

Sources: Bureau of Economic Analysis, Eurostat, Office for National Statistics, Statistics Sweden and the respective central banks

Figure 3.6. Housing pricesAnnual percentage change

-6

-4

-2

0

2

4

6

8

10

12

14

00 01 02 03 04 05 06 07 08 09 10

-6

-4

-2

0

2

4

6

8

10

12

14

Property price index

Purchase price coefficient

Source: Statistics SwedenNote. Quarterly observations of property price index and monthly observations of the mean value of the purchase price coefficient (Purchase price/Taxation value).

Figure 3.7. Money SupplyAnnual percentage change

-5

0

5

10

15

20

25

00 01 02 03 04 05 06 07 08 09 10

-5

0

5

10

15

20

25The general public's holding of banknotes and coins

M2

M3

Sources: Statistics Sweden and the Riksbank

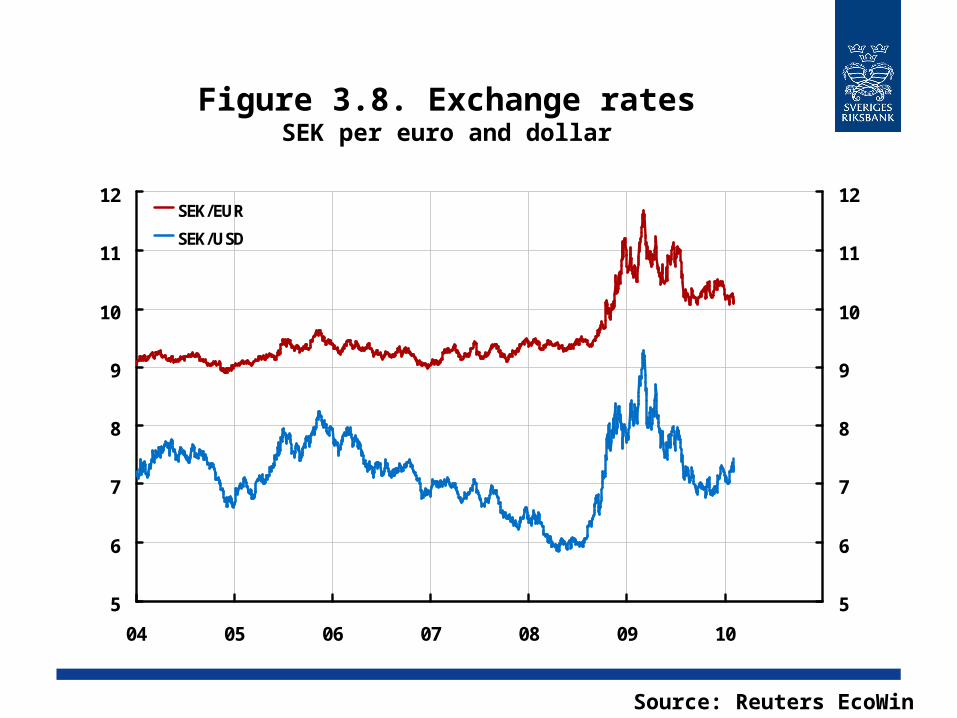

Figure 3.8. Exchange ratesSEK per euro and dollar

5

6

7

8

9

10

11

12

04 05 06 07 08 09 10

5

6

7

8

9

10

11

12SEK/EUR

SEK/USD

Source: Reuters EcoWin

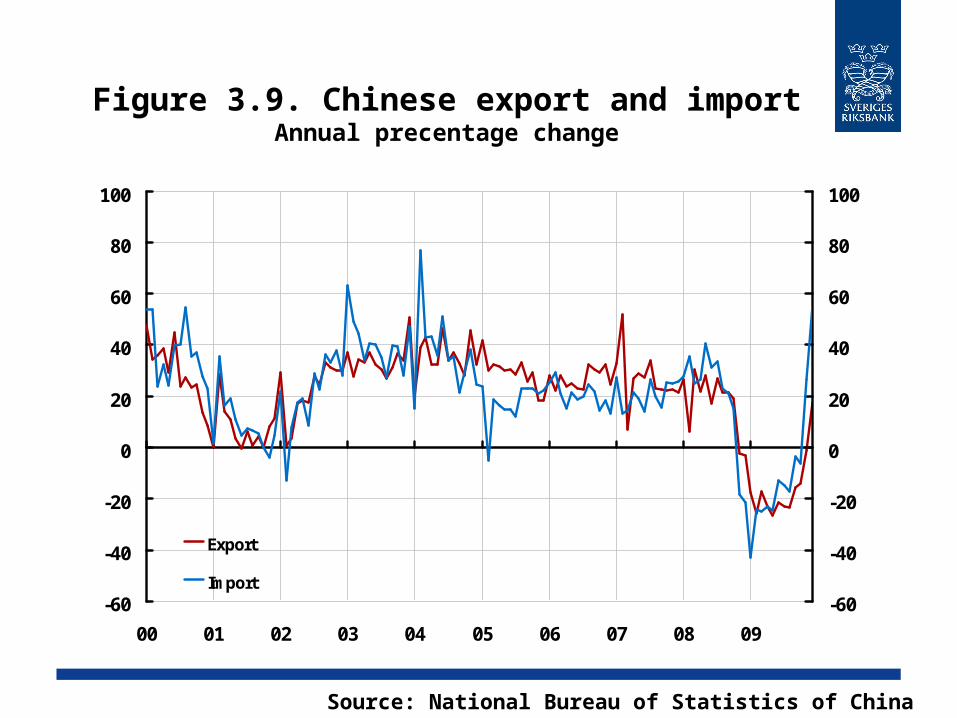

Figure 3.9. Chinese export and importAnnual precentage change

-60

-40

-20

0

20

40

60

80

100

00 01 02 03 04 05 06 07 08 09

-60

-40

-20

0

20

40

60

80

100

Export

Import

Source: National Bureau of Statistics of China

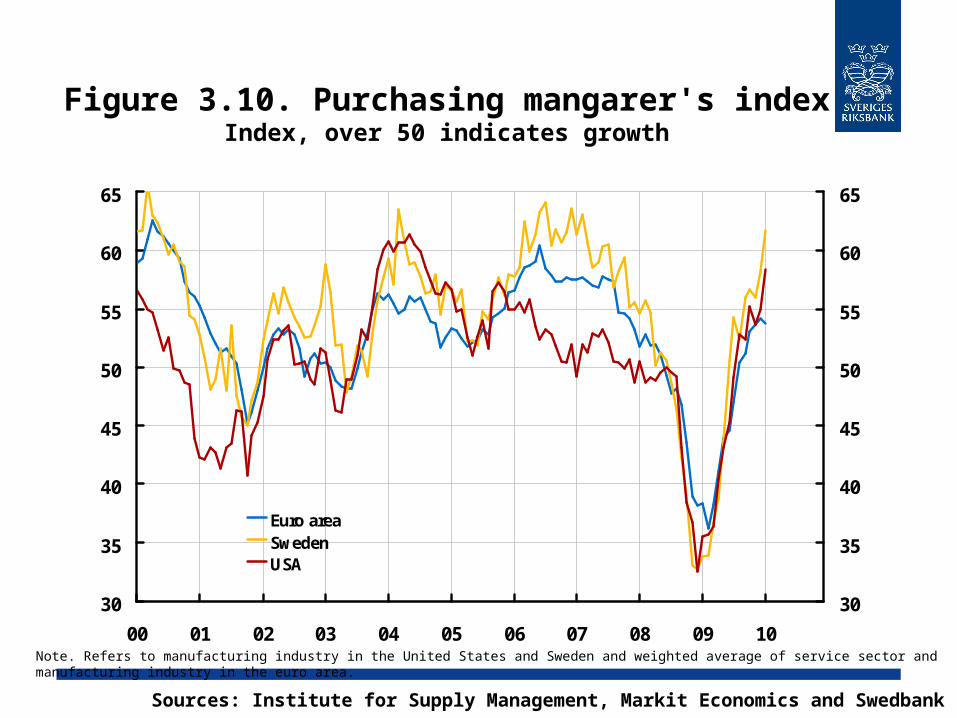

Figure 3.10. Purchasing mangarer's indexIndex, over 50 indicates growth

30

35

40

45

50

55

60

65

00 01 02 03 04 05 06 07 08 09 10

30

35

40

45

50

55

60

65

Euro areaSwedenUSA

Sources: Institute for Supply Management, Markit Economics and Swedbank

Note. Refers to manufacturing industry in the United States and Sweden and weighted average of service sector and manufacturing industry in the euro area.

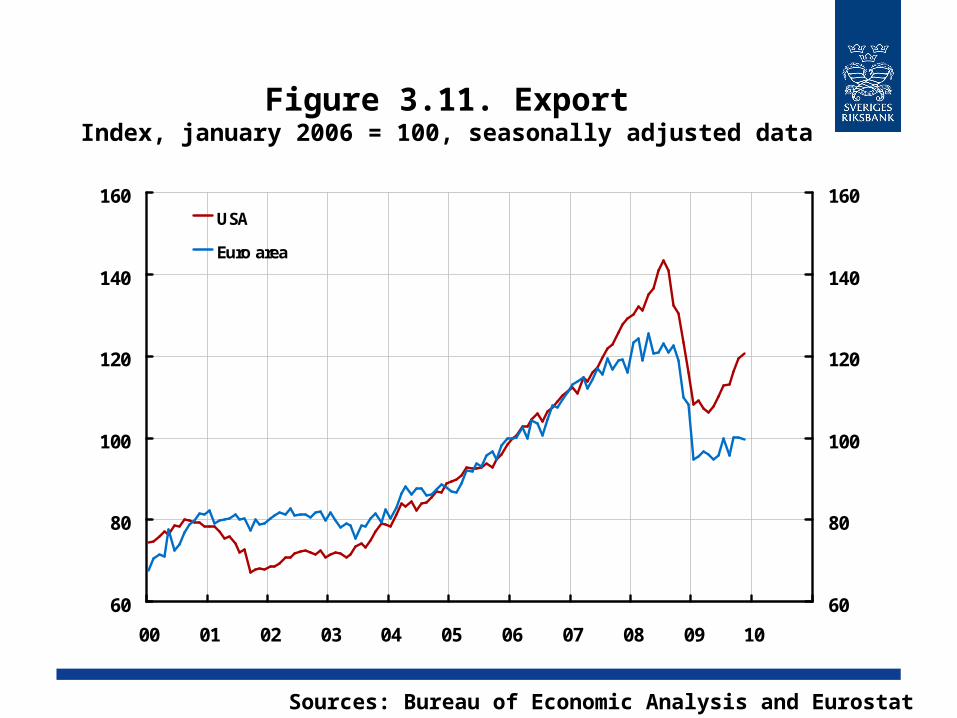

Figure 3.11. ExportIndex, january 2006 = 100, seasonally adjusted data

60

80

100

120

140

160

00 01 02 03 04 05 06 07 08 09 10

60

80

100

120

140

160USA

Euro area

Sources: Bureau of Economic Analysis and Eurostat

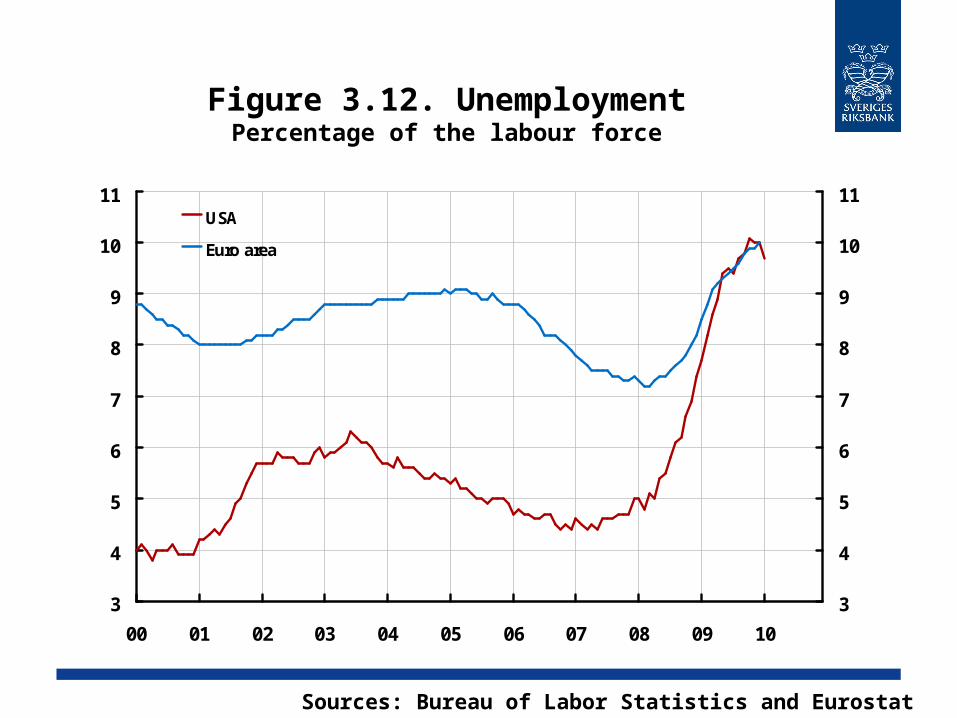

Figure 3.12. UnemploymentPercentage of the labour force

3

4

5

6

7

8

9

10

11

00 01 02 03 04 05 06 07 08 09 10

3

4

5

6

7

8

9

10

11USA

Euro area

Sources: Bureau of Labor Statistics and Eurostat

Figure 3.13. Households confidence indicators

Net values

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

00 01 02 03 04 05 06 07 08 09 10

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

Euro area

Germany

United Kingdom

Source: European Commission

Figure 3.14. HICP for the Euro areaAnnual percentage change

-1

0

1

2

3

4

5

00 01 02 03 04 05 06 07 08 09 10

-1

0

1

2

3

4

5TotalExcluding energy, food, alcohol and tobaccoExcluding energy and unprocessed food

Source: Eurostat

Figure 3.15. The Economic Tendency Indicator

Index, mean = 100

70

75

80

85

90

95

100

105

110

115

120

00 01 02 03 04 05 06 07 08 09 10

70

75

80

85

90

95

100

105

110

115

120The Economic Tendency IndicatorMean+/- one standard deviation

Source: National Institute of Economic Research

Figure 3.16. Industrial production and the production of services

Index, 2005 = 100, seasonally adjusted data

50

60

70

80

90

100

110

120

130

00 01 02 03 04 05 06 07 08 09

50

60

70

80

90

100

110

120

130Industrial production

Production of services

Source: Statistics Sweden

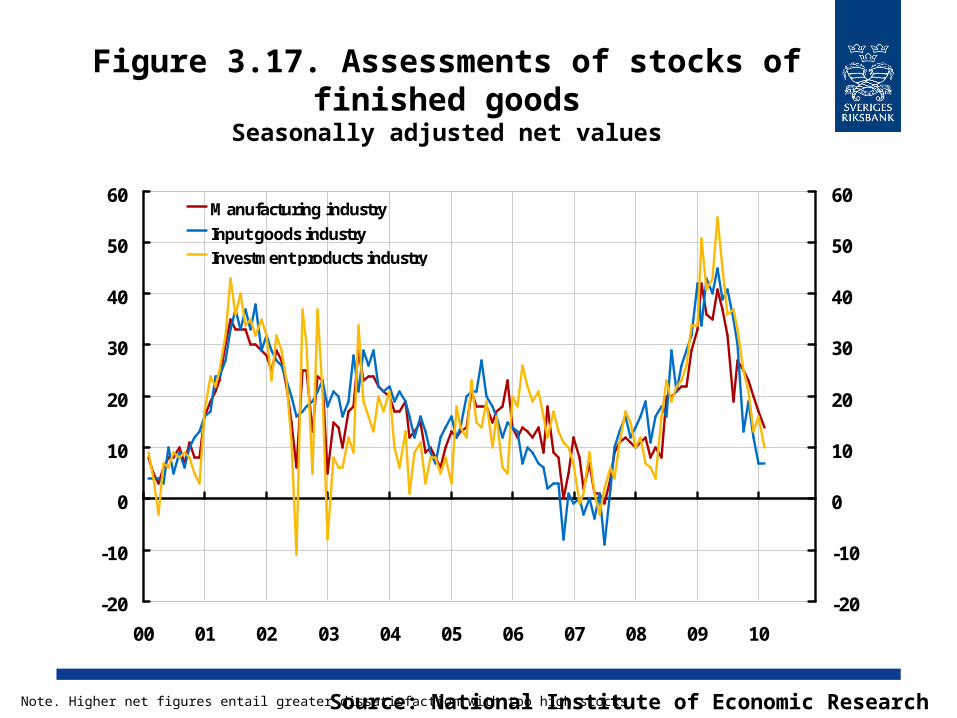

Figure 3.17. Assessments of stocks of finished goods

Seasonally adjusted net values

-20

-10

0

10

20

30

40

50

60

00 01 02 03 04 05 06 07 08 09 10

-20

-10

0

10

20

30

40

50

60Manufacturing industry

Input goods industryInvestment products industry

Source: National Institute of Economic ResearchNote. Higher net figures entail greater dissatisfaction with too high stocks.

Figure 3.18. Households' expectations for the futureNet figures

-90

-75

-60

-45

-30

-15

0

15

30

45

60

75

94 96 98 00 02 04 06 08 10

-90

-75

-60

-45

-30

-15

0

15

30

45

60

75

Unemployment

Confidence Indicator

Source: National Institute of Economic ResearchNote. Unemployment is defined here as the percentage of households that believe unemployment will fall minus the percentage who believe that unemployment will rise.

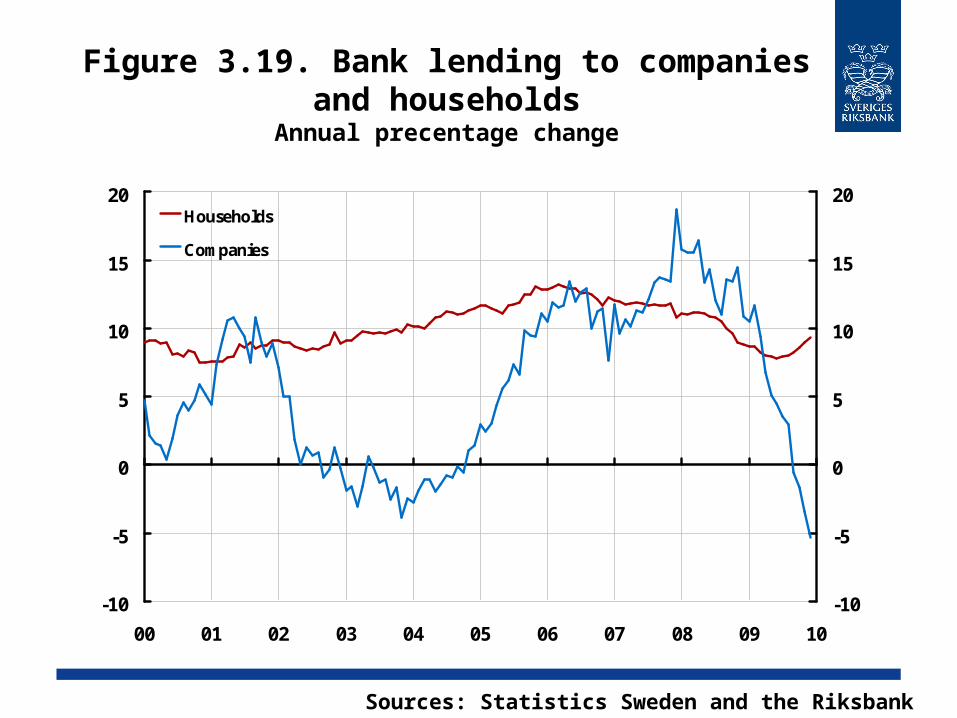

Figure 3.19. Bank lending to companies and households

Annual precentage change

-10

-5

0

5

10

15

20

00 01 02 03 04 05 06 07 08 09 10

-10

-5

0

5

10

15

20Households

Companies

Sources: Statistics Sweden and the Riksbank

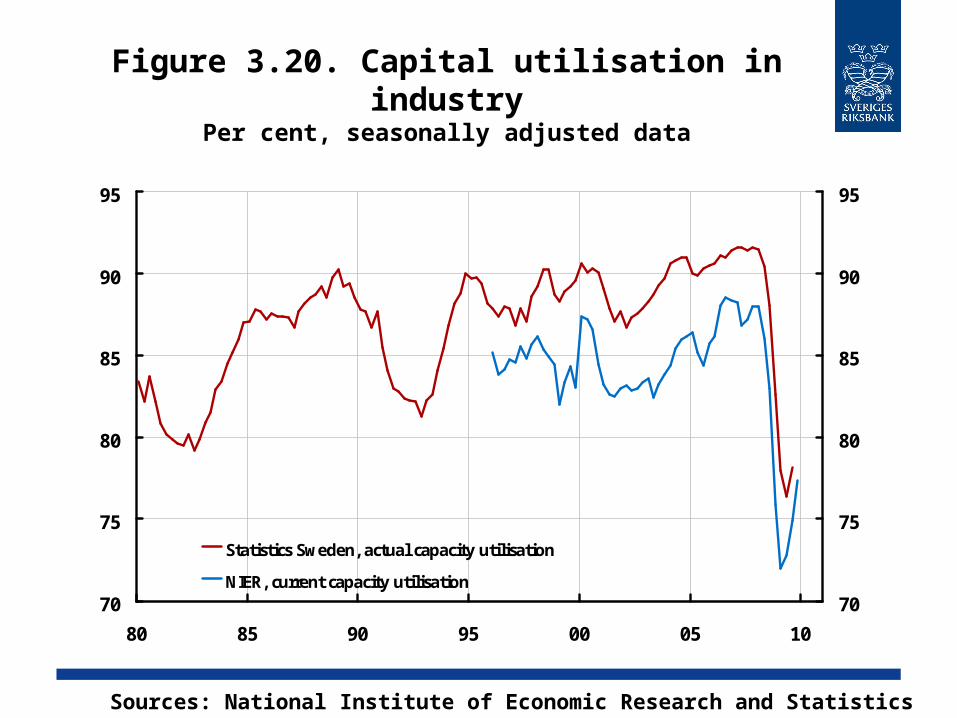

Figure 3.20. Capital utilisation in industryPer cent, seasonally adjusted data

70

75

80

85

90

95

80 85 90 95 00 05 10

70

75

80

85

90

95

Statistics Sweden, actual capacity utilisation

NIER, current capacity utilisation

Sources: National Institute of Economic Research and Statistics Sweden

Figure 3.21. Foreign trade with goods in fixed prices

Index, 2005 = 100, seasonally adjusted data

0

20

40

60

80

100

120

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

0

20

40

60

80

100

120

Export Import

Sources: Statistics Sweden and the RiksbankNote. Three-month moving averages. Fixed prices calculated by the Riksbank.

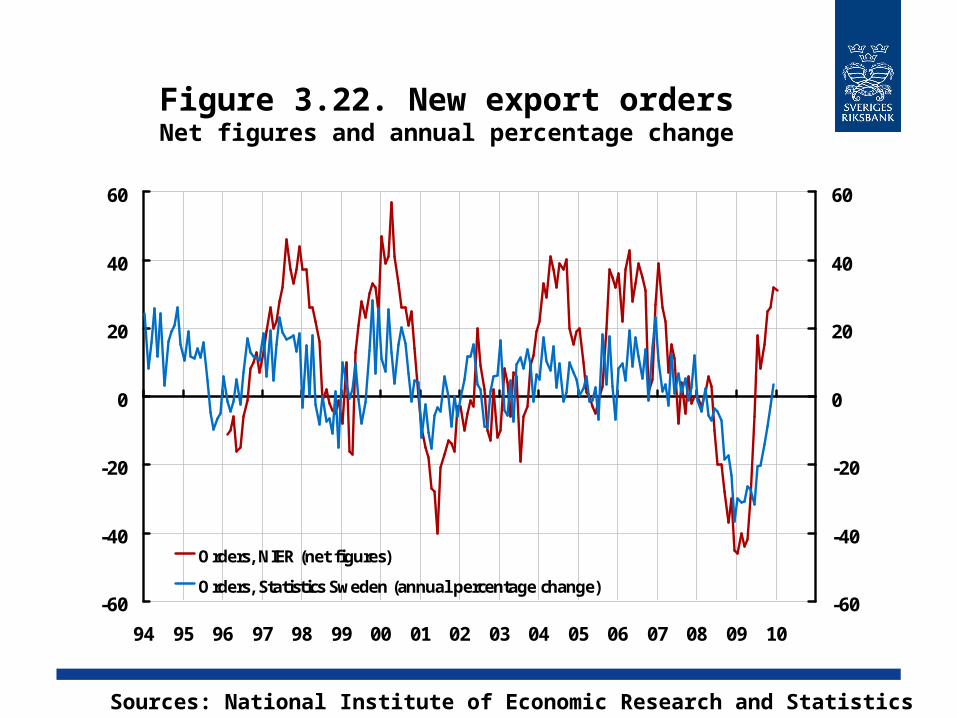

Figure 3.22. New export ordersNet figures and annual percentage change

-60

-40

-20

0

20

40

60

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

-60

-40

-20

0

20

40

60

Orders, NIER (net figures)

Orders, Statistics Sweden (annual percentage change)

Sources: National Institute of Economic Research and Statistics Sweden

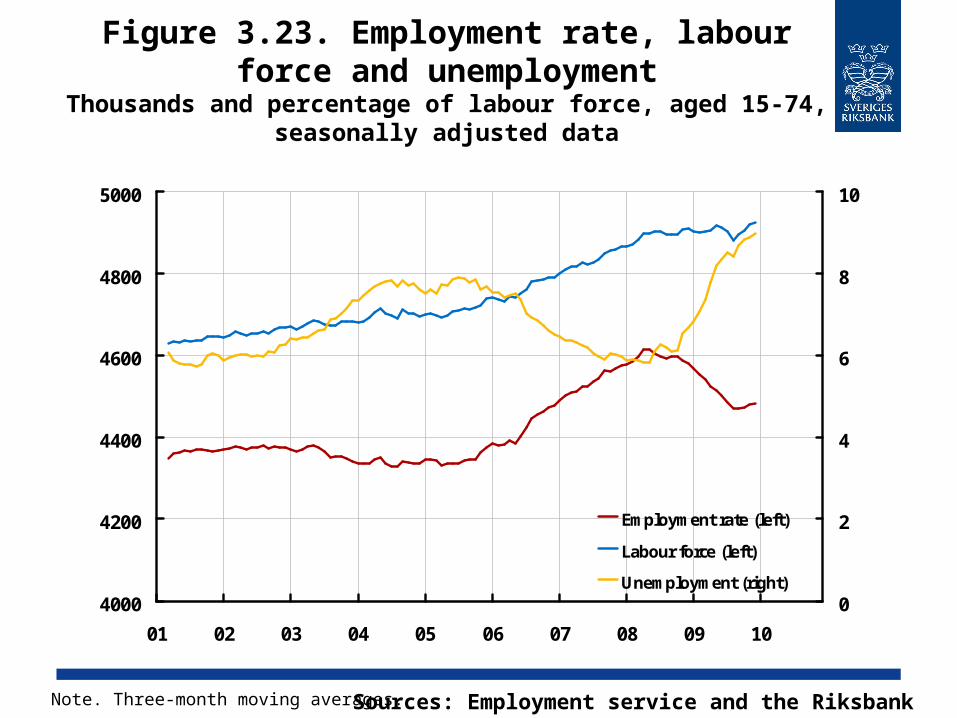

Figure 3.23. Employment rate, labour force and unemployment

Thousands and percentage of labour force, aged 15-74, seasonally adjusted data

4000

4200

4400

4600

4800

5000

01 02 03 04 05 06 07 08 09 10

0

2

4

6

8

10

Employment rate (left)

Labour force (left)

Unemployment (right)

Sources: Employment service and the RiksbankNote. Three-month moving averages.

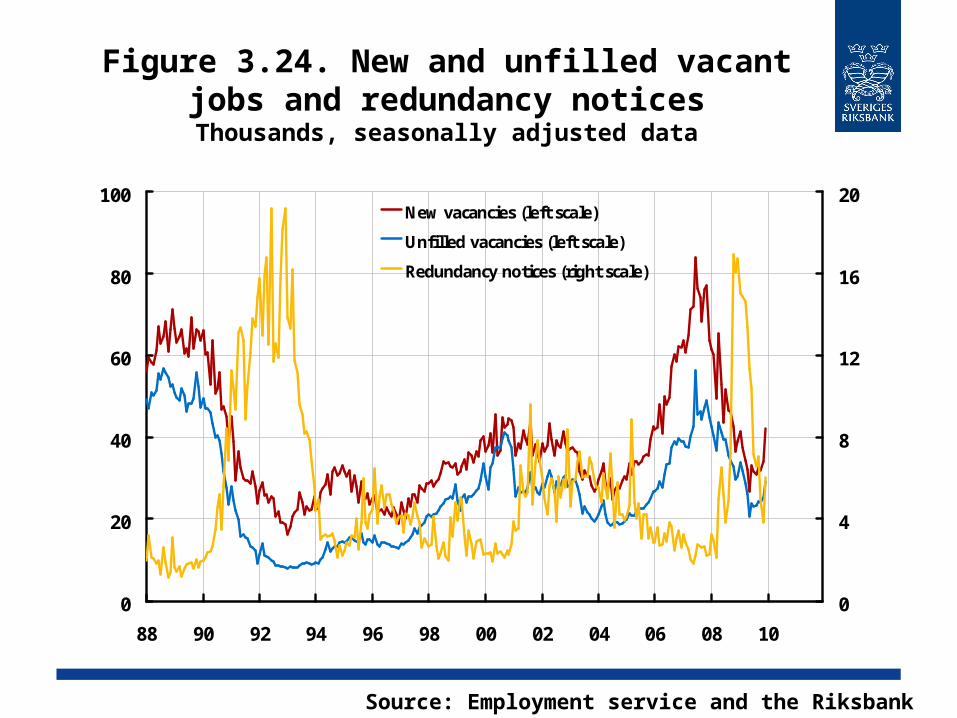

Figure 3.24. New and unfilled vacant jobs and redundancy notices

Thousands, seasonally adjusted data

0

20

40

60

80

100

88 90 92 94 96 98 00 02 04 06 08 10

0

4

8

12

16

20New vacancies (left scale)

Unfilled vacancies (left scale)

Redundancy notices (right scale)

Source: Employment service and the Riksbank

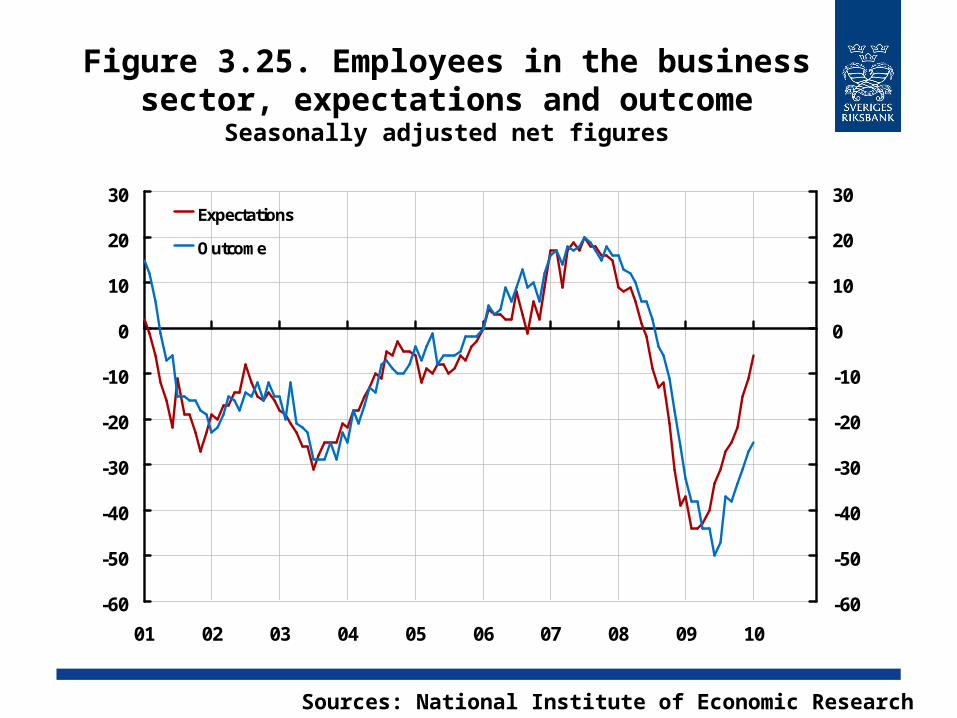

Figure 3.25. Employees in the business sector, expectations and outcome

Seasonally adjusted net figures

-60

-50

-40

-30

-20

-10

0

10

20

30

01 02 03 04 05 06 07 08 09 10

-60

-50

-40

-30

-20

-10

0

10

20

30Expectations

Outcome

Sources: National Institute of Economic Research

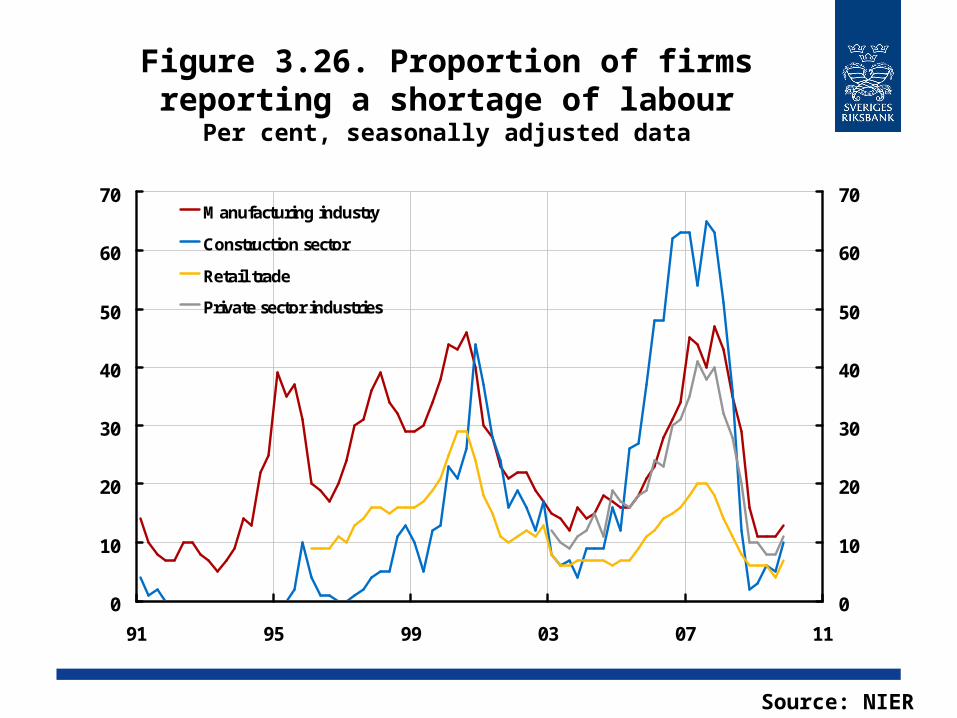

Figure 3.26. Proportion of firms reporting a shortage of labour

Per cent, seasonally adjusted data

0

10

20

30

40

50

60

70

91 95 99 03 07 11

0

10

20

30

40

50

60

70Manufacturing industry

Construction sector

Retail trade

Private sector industries

Source: NIER

Figure 3.27. WagesAnnual percentage change

0

1

2

3

4

5

6

7

8

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

0

1

2

3

4

5

6

7

8Public sector

Business sector

Sources: National Mediation Office and the Riksbank

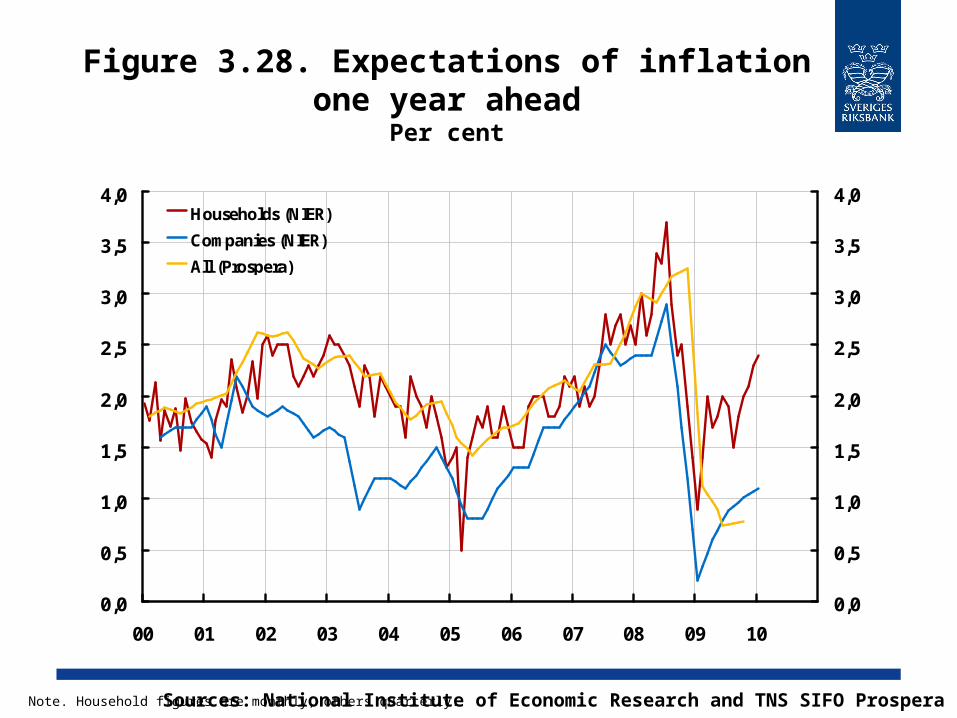

Figure 3.28. Expectations of inflation one year ahead

Per cent

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

00 01 02 03 04 05 06 07 08 09 10

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0Households (NIER)

Companies (NIER)

All (Prospera)

Sources: National Institute of Economic Research and TNS SIFO ProsperaNote. Household figures are monthly, others quarterly.

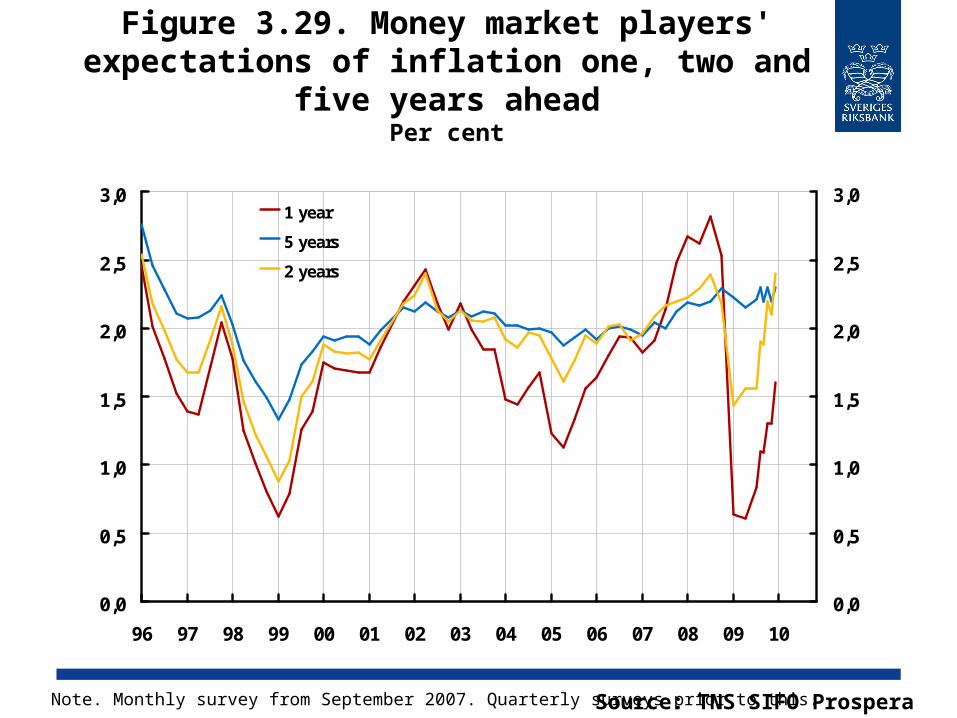

Figure 3.29. Money market players' expectations of inflation one, two and five

years aheadPer cent

0,0

0,5

1,0

1,5

2,0

2,5

3,0

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

0,0

0,5

1,0

1,5

2,0

2,5

3,01 year

5 years

2 years

Source: TNS SIFO ProsperaNote. Monthly survey from September 2007. Quarterly surveys prior to this.

Figure 3.30. The difference between nominal and real five-year rates (break-

even inflation)Percentage points

0,0

0,5

1,0

1,5

2,0

2,5

3,0

00 01 02 03 04 05 06 07 08 09 10

0,0

0,5

1,0

1,5

2,0

2,5

3,0

Source: The Riksbank

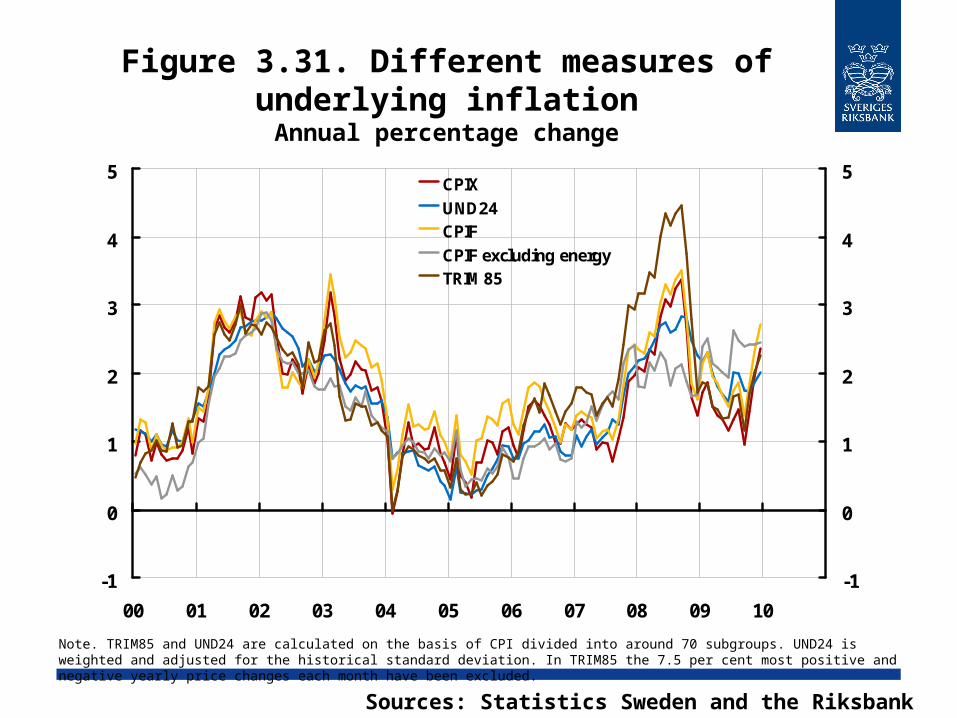

Figure 3.31. Different measures of underlying inflationAnnual percentage change

-1

0

1

2

3

4

5

00 01 02 03 04 05 06 07 08 09 10

-1

0

1

2

3

4

5CPIXUND24CPIFCPIF excluding energyTRIM85

Sources: Statistics Sweden and the Riksbank

Note. TRIM85 and UND24 are calculated on the basis of CPI divided into around 70 subgroups. UND24 is weighted and adjusted for the historical standard deviation. In TRIM85 the 7.5 per cent most positive and negative yearly price changes each month have been excluded.

Figure 3.32. Prices of goods and services in the CPI

Annual percentage change

-3

-2

-1

0

1

2

3

4

00 01 02 03 04 05 06 07 08 09 10

-3

-2

-1

0

1

2

3

4Services (43,5 %)

Goods excluding energy and food (26,3 %)

Source: Statistics SwedenNote. The weight of CPI of the respective components is given in brackets.

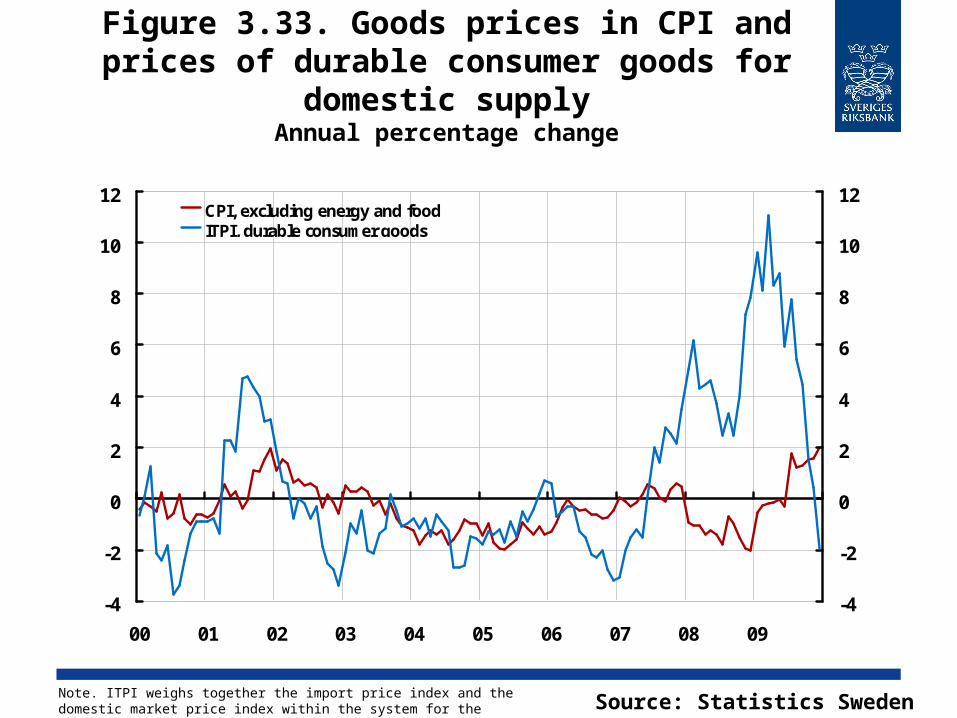

Figure 3.33. Goods prices in CPI and prices of durable consumer goods for domestic

supplyAnnual percentage change

-4

-2

0

2

4

6

8

10

12

00 01 02 03 04 05 06 07 08 09

-4

-2

0

2

4

6

8

10

12CPI, excluding energy and foodITPI, durable consumer goods

Source: Statistics SwedenNote. ITPI weighs together the import price index and the domestic market price index within the system for the producer price index.

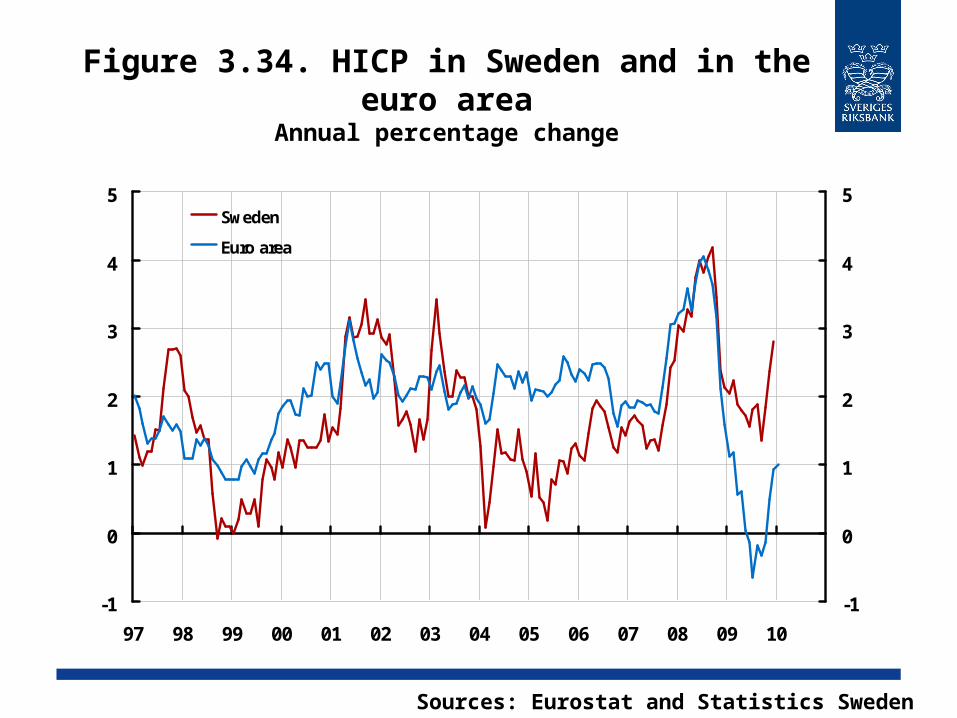

Figure 3.34. HICP in Sweden and in the euro area

Annual percentage change

-1

0

1

2

3

4

5

97 98 99 00 01 02 03 04 05 06 07 08 09 10

-1

0

1

2

3

4

5Sweden

Euro area

Sources: Eurostat and Statistics Sweden

Figure B1. Market agents' expectations of the level of the nominal repo rate in 5 years

Survey responses between June 2005 and end of December 2009, per cent.

0

1

2

3

4

5

6

05 06 07 08 09 10

0

1

2

3

4

5

6

Median

Mean

+- 2 standard deviations

Sources: TNS Prospera AB and the Riksbank

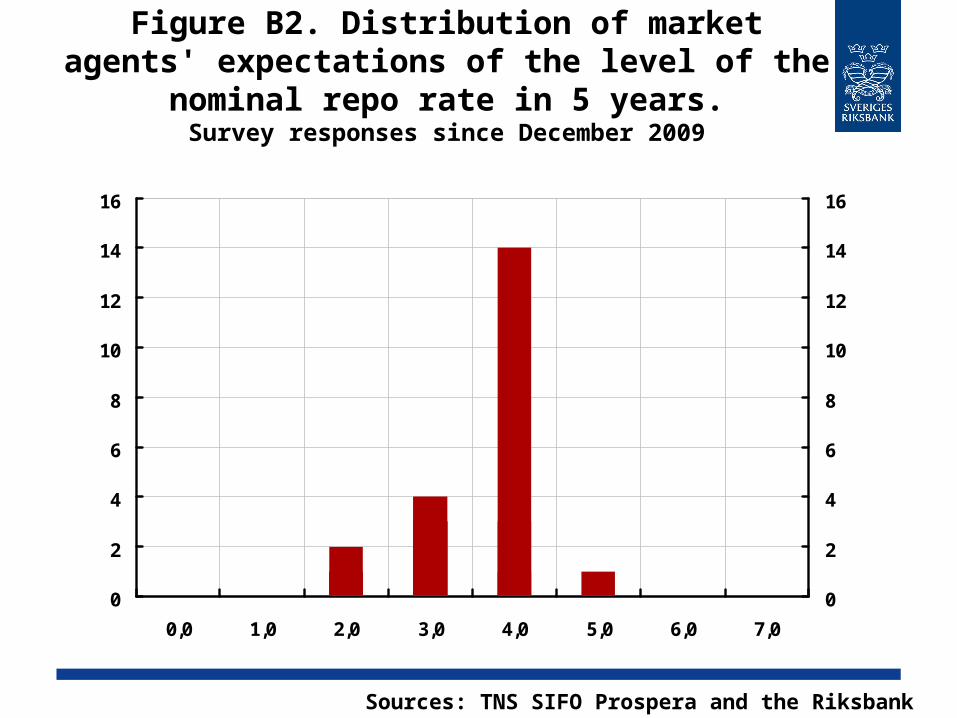

Figure B2. Distribution of market agents' expectations of the level of the nominal

repo rate in 5 years.Survey responses since December 2009

0

2

4

6

8

10

12

14

16

0,0 1,0 2,0 3,0 4,0 5,0 6,0 7,0

0

2

4

6

8

10

12

14

16

Sources: TNS SIFO Prospera and the Riksbank

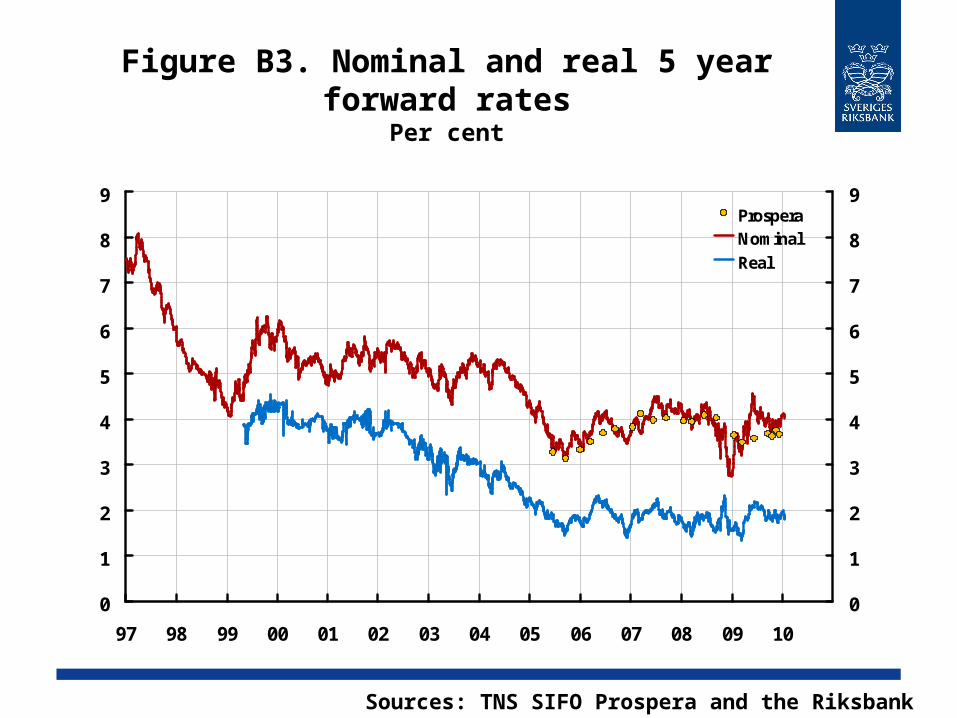

Figure B3. Nominal and real 5 year forward rates

Per cent

0

1

2

3

4

5

6

7

8

9

97 98 99 00 01 02 03 04 05 06 07 08 09 10

0

1

2

3

4

5

6

7

8

9ProsperaNominalReal

Sources: TNS SIFO Prospera and the Riksbank

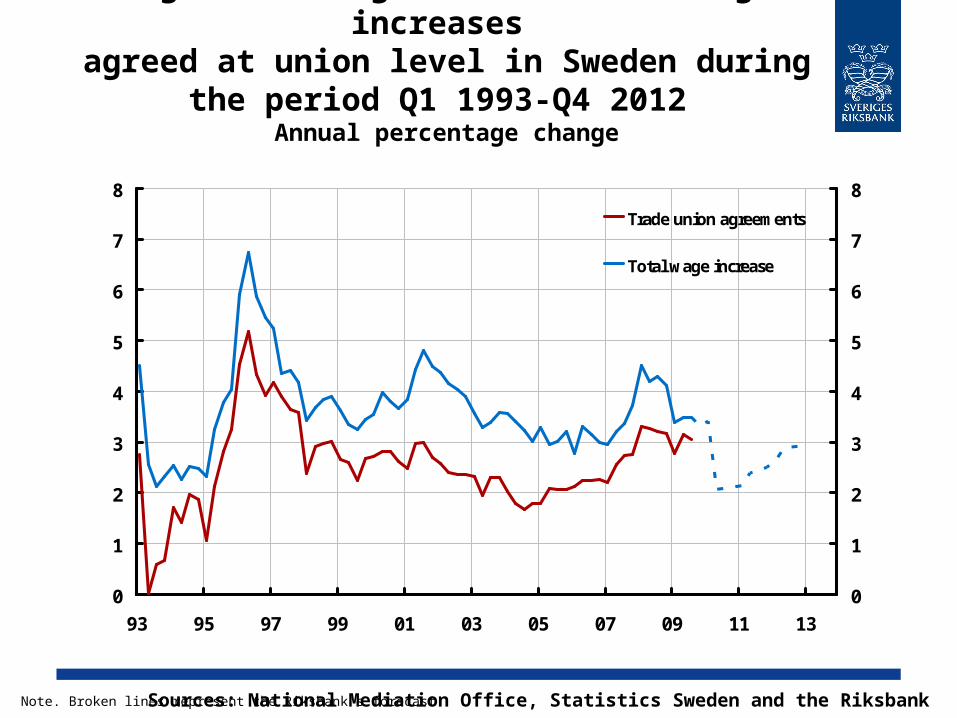

Figure B4. Wage increases and wage increases

agreed at union level in Sweden during the period Q1 1993-Q4 2012

Annual percentage change

Sources: National Mediation Office, Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

0

1

2

3

4

5

6

7

8

93 95 97 99 01 03 05 07 09 11 13

0

1

2

3

4

5

6

7

8

Trade union agreements

Total wage increase

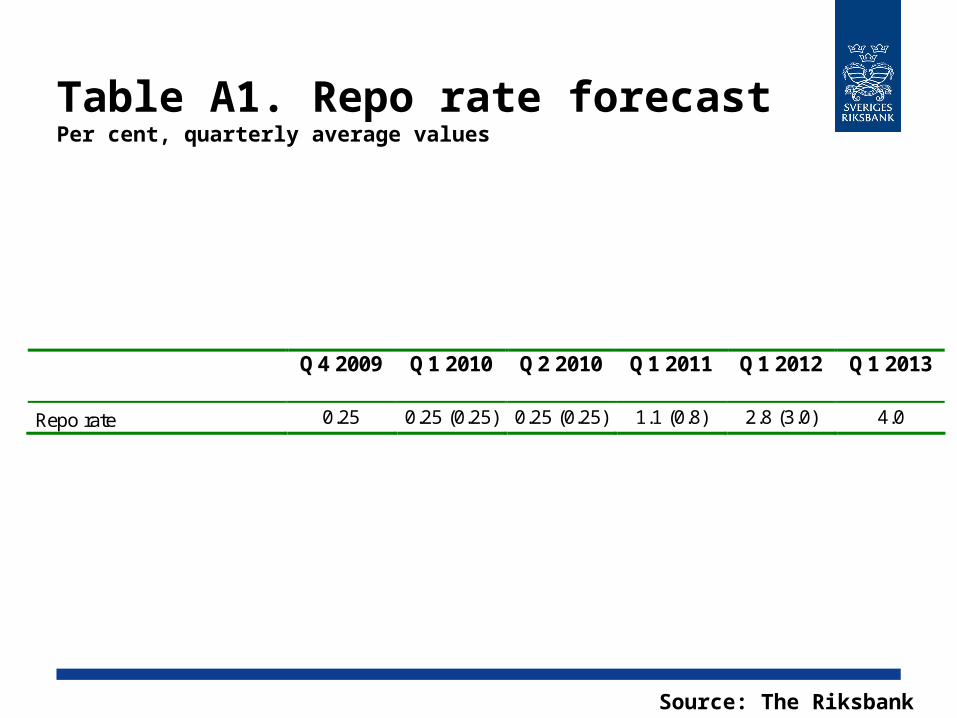

Table A1. Repo rate forecastPer cent, quarterly average values

Source: The Riksbank

Q4 2009 Q1 2010 Q2 2010 Q1 2011 Q1 2012 Q1 2013

Repo rate 0.25 0.25 (0.25) 0.25 (0.25) 1.1 (0.8) 2.8 (3.0) 4.0

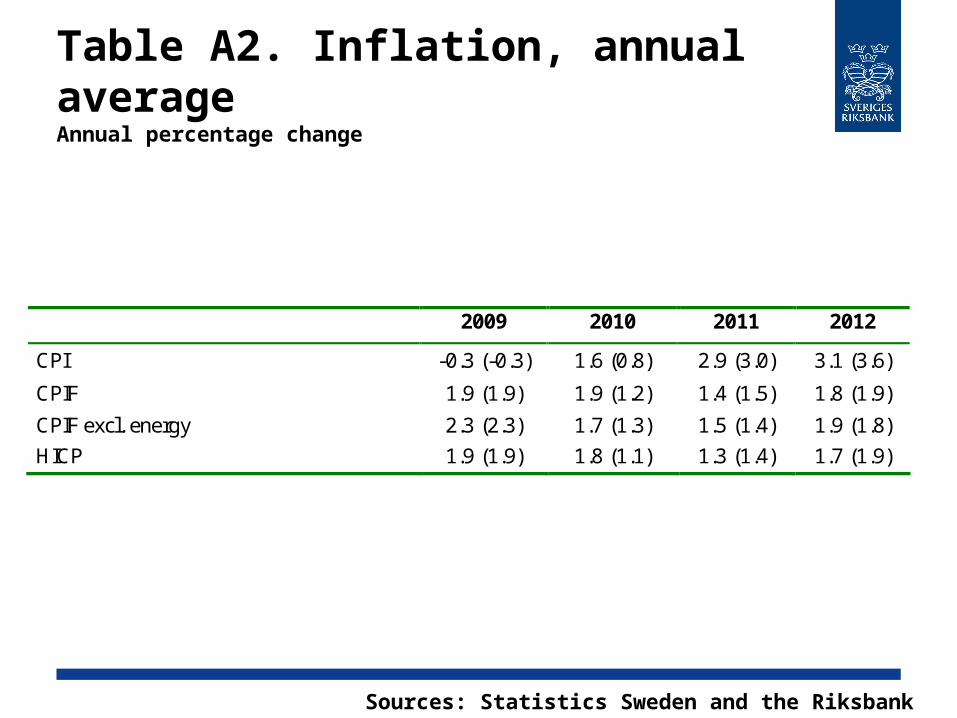

Table A2. Inflation, annual averageAnnual percentage change

Sources: Statistics Sweden and the Riksbank

2009 2010 2011 2012

CPI -0.3 (-0.3) 1.6 (0.8) 2.9 (3.0) 3.1 (3.6)

CPIF 1.9 (1.9) 1.9 (1.2) 1.4 (1.5) 1.8 (1.9)

CPIF excl. energy 2.3 (2.3) 1.7 (1.3) 1.5 (1.4) 1.9 (1.8)

HICP 1.9 (1.9) 1.8 (1.1) 1.3 (1.4) 1.7 (1.9)

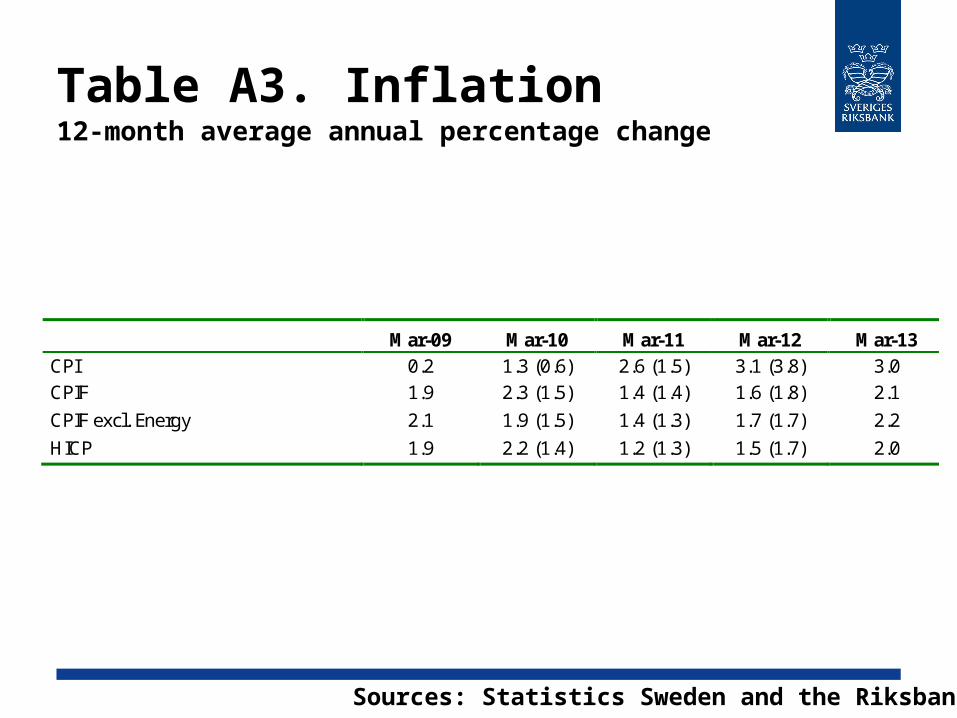

Table A3. Inflation 12-month average annual percentage change

Sources: Statistics Sweden and the Riksbank

Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 CPI 0.2 1.3 (0.6) 2.6 (1.5) 3.1 (3.8) 3.0 CPIF 1.9 2.3 (1.5) 1.4 (1.4) 1.6 (1.8) 2.1

CPIF excl. Energy 2.1 1.9 (1.5) 1.4 (1.3) 1.7 (1.7) 2.2

HICP 1.9 2.2 (1.4) 1.2 (1.3) 1.5 (1.7) 2.0

Table A4. Summary of financial forecasts Annual average, per cent, unless otherwise

specified

Sources: Statistics Sweden and the Riksbank

2009 2010 2011 2012

Repo rate 0.7 (0.7) 0.4 (0.3) 1.8 (1.6) 3.3 (3.6)

10-year rate 3.3 (3.2) 3.6 (3.7) 4.1 (4.2) 4.6 (4.7) Exchange rate, TCW-index, 1992-11-18=100

140.2 (140.0)

131.8 (129.0)

128.2 (127.1)

127.7 (127.3)

General government net lending* -1.5 (-1.9) -1.5 (-2.2) -0.1 (-0.8) 0.7 (0.5)

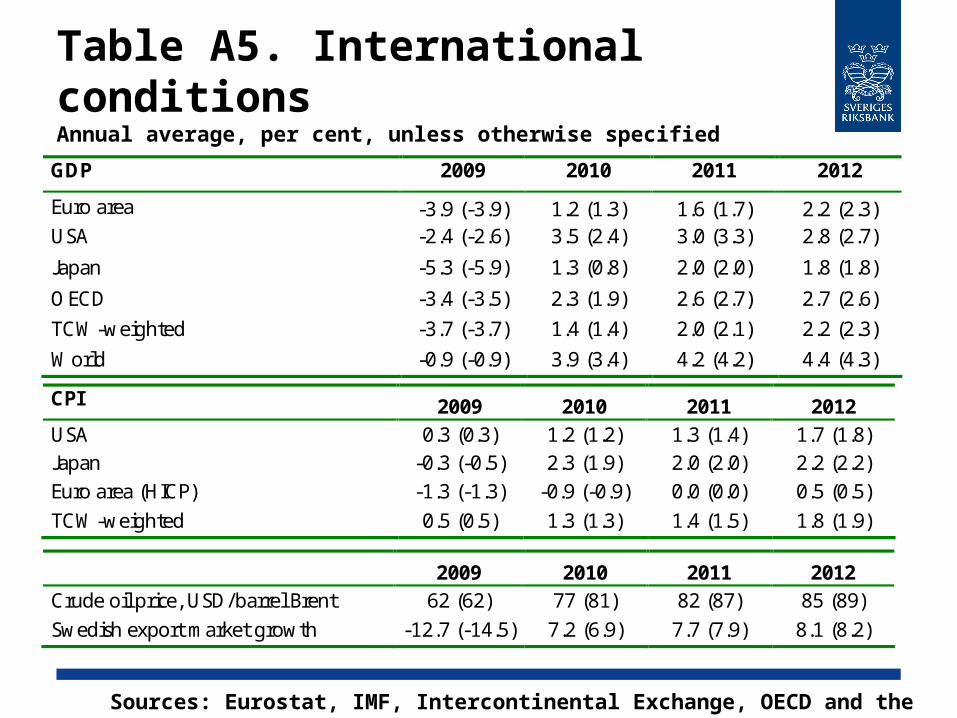

Table A5. International conditions Annual average, per cent, unless otherwise specified

Sources: Eurostat, IMF, Intercontinental Exchange, OECD and the Riksbank

GDP 2009 2010 2011 2012

Euro area -3.9 (-3.9) 1.2 (1.3) 1.6 (1.7) 2.2 (2.3) USA -2.4 (-2.6) 3.5 (2.4) 3.0 (3.3) 2.8 (2.7)

Japan -5.3 (-5.9) 1.3 (0.8) 2.0 (2.0) 1.8 (1.8)

OECD -3.4 (-3.5) 2.3 (1.9) 2.6 (2.7) 2.7 (2.6)

TCW-weighted -3.7 (-3.7) 1.4 (1.4) 2.0 (2.1) 2.2 (2.3)

World -0.9 (-0.9) 3.9 (3.4) 4.2 (4.2) 4.4 (4.3)

CPI 2009 2010 2011 2012 USA 0.3 (0.3) 1.2 (1.2) 1.3 (1.4) 1.7 (1.8) Japan -0.3 (-0.5) 2.3 (1.9) 2.0 (2.0) 2.2 (2.2) Euro area (HICP) -1.3 (-1.3) -0.9 (-0.9) 0.0 (0.0) 0.5 (0.5)

TCW-weighted 0.5 (0.5) 1.3 (1.3) 1.4 (1.5) 1.8 (1.9)

2009 2010 2011 2012 Crude oil price, USD/barrel Brent 62 (62) 77 (81) 82 (87) 85 (89) Swedish export market growth -12.7 (-14.5) 7.2 (6.9) 7.7 (7.9) 8.1 (8.2)

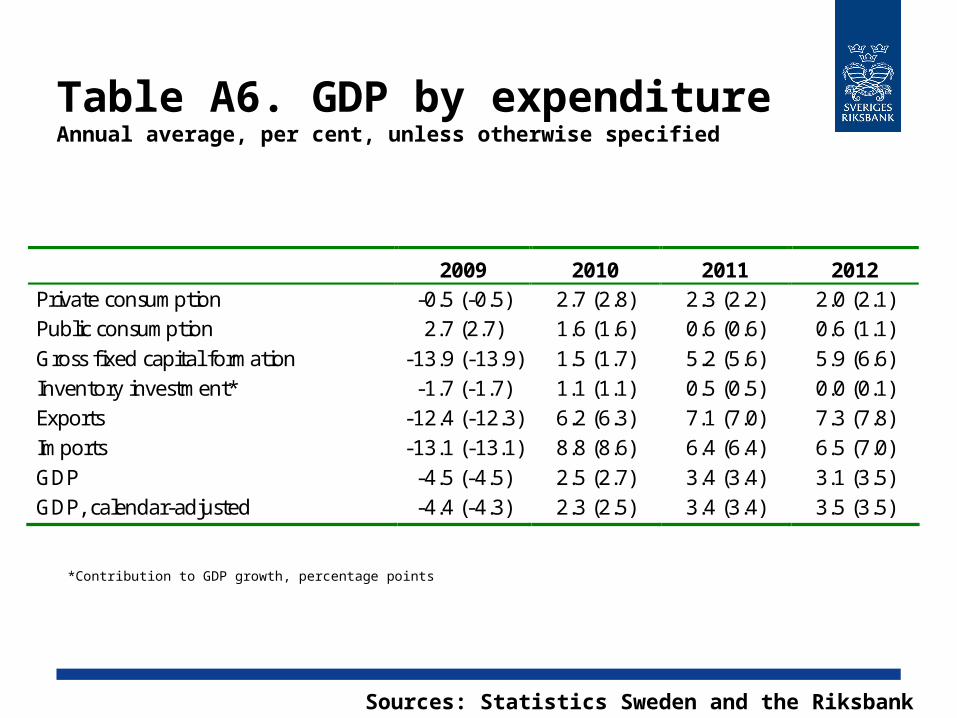

Table A6. GDP by expenditureAnnual average, per cent, unless otherwise specified

Sources: Statistics Sweden and the Riksbank

*Contribution to GDP growth, percentage points

2009 2010 2011 2012 Private consumption -0.5 (-0.5) 2.7 (2.8) 2.3 (2.2) 2.0 (2.1) Public consumption 2.7 (2.7) 1.6 (1.6) 0.6 (0.6) 0.6 (1.1) Gross fixed capital formation -13.9 (-13.9) 1.5 (1.7) 5.2 (5.6) 5.9 (6.6) Inventory investment* -1.7 (-1.7) 1.1 (1.1) 0.5 (0.5) 0.0 (0.1) Exports -12.4 (-12.3) 6.2 (6.3) 7.1 (7.0) 7.3 (7.8) Imports -13.1 (-13.1) 8.8 (8.6) 6.4 (6.4) 6.5 (7.0) GDP -4.5 (-4.5) 2.5 (2.7) 3.4 (3.4) 3.1 (3.5) GDP, calendar-adjusted -4.4 (-4.3) 2.3 (2.5) 3.4 (3.4) 3.5 (3.5)

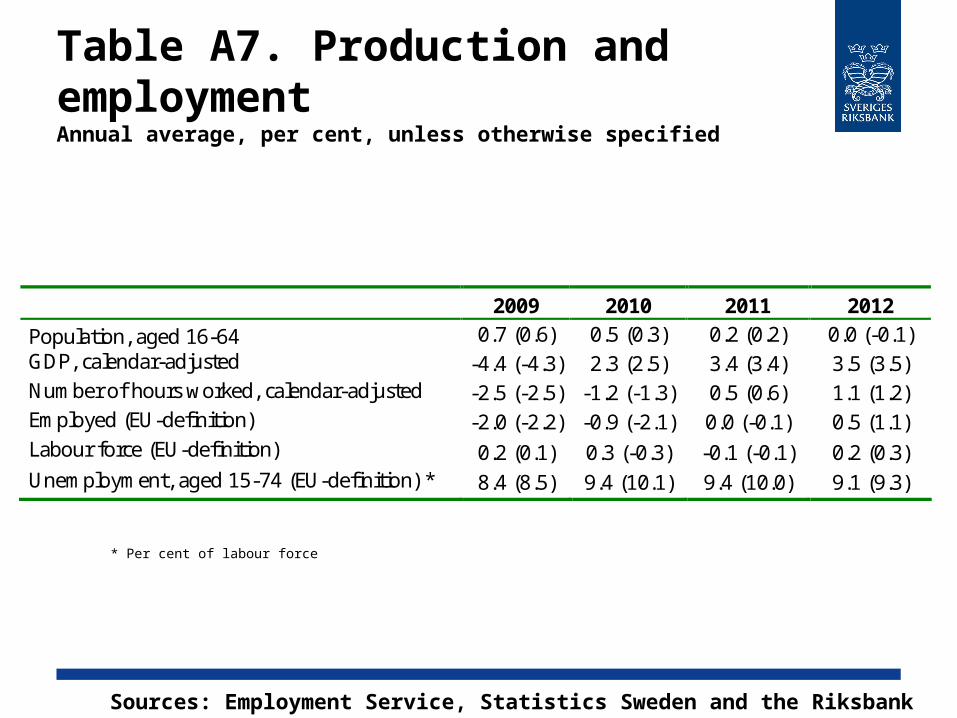

Table A7. Production and employment Annual average, per cent, unless otherwise specified

Sources: Employment Service, Statistics Sweden and the Riksbank

* Per cent of labour force

2009 2010 2011 2012

Population, aged 16-64 0.7 (0.6) 0.5 (0.3) 0.2 (0.2) 0.0 (-0.1) GDP, calendar-adjusted -4.4 (-4.3) 2.3 (2.5) 3.4 (3.4) 3.5 (3.5) Number of hours worked, calendar-adjusted -2.5 (-2.5) -1.2 (-1.3) 0.5 (0.6) 1.1 (1.2) Employed (EU-definition) -2.0 (-2.2) -0.9 (-2.1) 0.0 (-0.1) 0.5 (1.1) Labour force (EU-definition) 0.2 (0.1) 0.3 (-0.3) -0.1 (-0.1) 0.2 (0.3) Unemployment, aged 15-74 (EU-definition) * 8.4 (8.5) 9.4 (10.1) 9.4 (10.0) 9.1 (9.3)

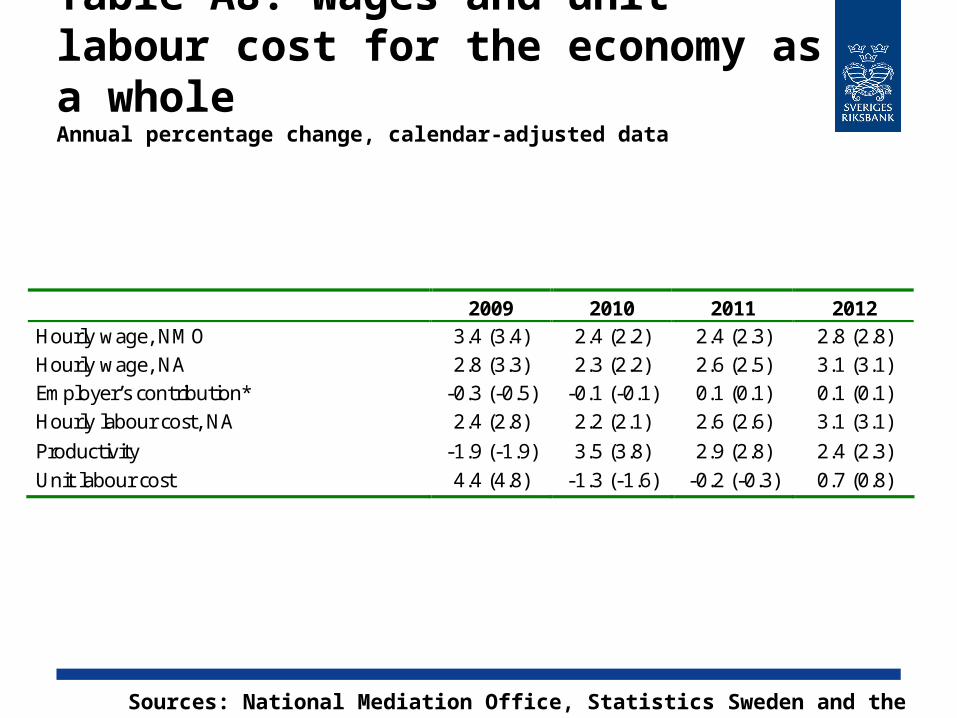

Table A8. Wages and unit labour cost for the economy as a wholeAnnual percentage change, calendar-adjusted data

Sources: National Mediation Office, Statistics Sweden and the Riksbank

2009 2010 2011 2012 Hourly wage, NMO 3.4 (3.4) 2.4 (2.2) 2.4 (2.3) 2.8 (2.8) Hourly wage, NA 2.8 (3.3) 2.3 (2.2) 2.6 (2.5) 3.1 (3.1) Employer’s contribution* -0.3 (-0.5) -0.1 (-0.1) 0.1 (0.1) 0.1 (0.1) Hourly labour cost, NA 2.4 (2.8) 2.2 (2.1) 2.6 (2.6) 3.1 (3.1)

Productivity -1.9 (-1.9) 3.5 (3.8) 2.9 (2.8) 2.4 (2.3) Unit labour cost 4.4 (4.8) -1.3 (-1.6) -0.2 (-0.3) 0.7 (0.8)

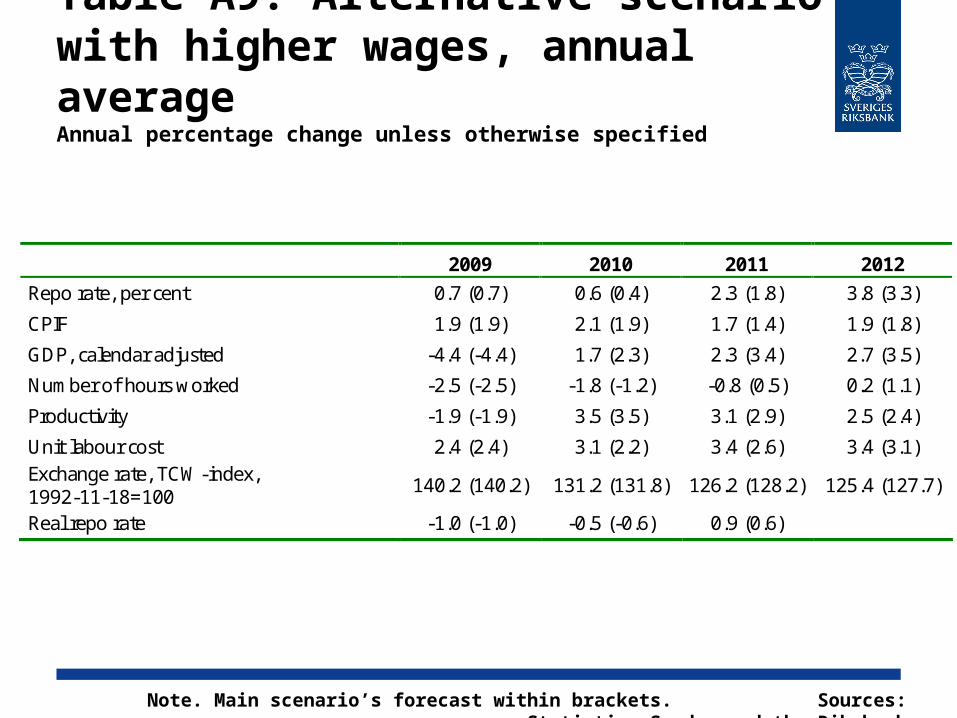

Table A9. Alternative scenario with higher wages, annual averageAnnual percentage change unless otherwise specified

Note. Main scenario’s forecast within brackets. Sources: Statistics Sweden and the Riksbank

2009 2010 2011 2012

Repo rate, per cent 0.7 (0.7) 0.6 (0.4) 2.3 (1.8) 3.8 (3.3)

CPIF 1.9 (1.9) 2.1 (1.9) 1.7 (1.4) 1.9 (1.8)

GDP, calendar adjusted -4.4 (-4.4) 1.7 (2.3) 2.3 (3.4) 2.7 (3.5)

Number of hours worked -2.5 (-2.5) -1.8 (-1.2) -0.8 (0.5) 0.2 (1.1)

Productivity -1.9 (-1.9) 3.5 (3.5) 3.1 (2.9) 2.5 (2.4)

Unit labour cost 2.4 (2.4) 3.1 (2.2) 3.4 (2.6) 3.4 (3.1) Exchange rate, TCW-index, 1992-11-18=100

140.2 (140.2) 131.2 (131.8) 126.2 (128.2) 125.4 (127.7)

Real repo rate -1.0 (-1.0) -0.5 (-0.6) 0.9 (0.6)

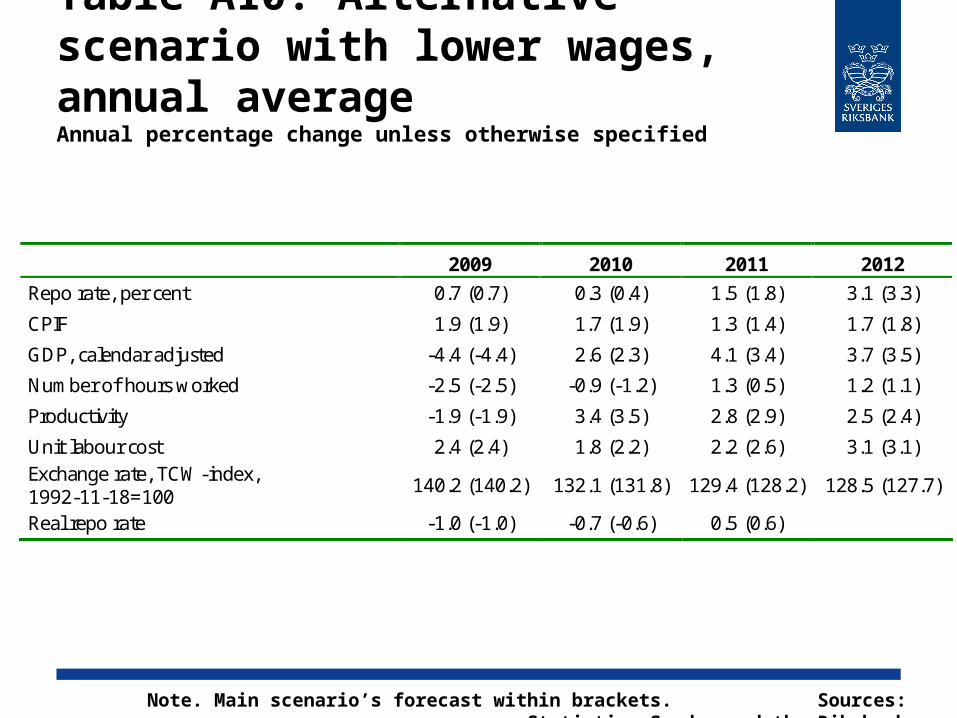

Table A10. Alternative scenario with lower wages, annual averageAnnual percentage change unless otherwise specified

Note. Main scenario’s forecast within brackets. Sources: Statistics Sweden and the Riksbank

2009 2010 2011 2012

Repo rate, per cent 0.7 (0.7) 0.3 (0.4) 1.5 (1.8) 3.1 (3.3)

CPIF 1.9 (1.9) 1.7 (1.9) 1.3 (1.4) 1.7 (1.8)

GDP, calendar adjusted -4.4 (-4.4) 2.6 (2.3) 4.1 (3.4) 3.7 (3.5)

Number of hours worked -2.5 (-2.5) -0.9 (-1.2) 1.3 (0.5) 1.2 (1.1)

Productivity -1.9 (-1.9) 3.4 (3.5) 2.8 (2.9) 2.5 (2.4)

Unit labour cost 2.4 (2.4) 1.8 (2.2) 2.2 (2.6) 3.1 (3.1) Exchange rate, TCW-index, 1992-11-18=100

140.2 (140.2) 132.1 (131.8) 129.4 (128.2) 128.5 (127.7)

Real repo rate -1.0 (-1.0) -0.7 (-0.6) 0.5 (0.6)

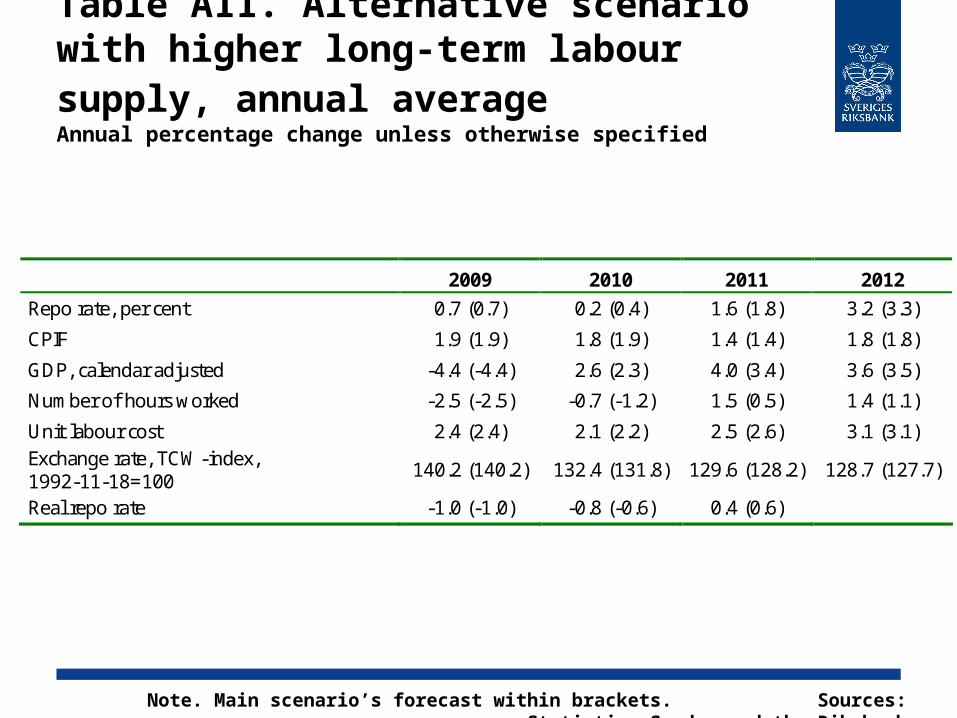

Table A11. Alternative scenario with higher long-term labour supply, annual averageAnnual percentage change unless otherwise specified

Note. Main scenario’s forecast within brackets. Sources: Statistics Sweden and the Riksbank

2009 2010 2011 2012

Repo rate, per cent 0.7 (0.7) 0.2 (0.4) 1.6 (1.8) 3.2 (3.3)

CPIF 1.9 (1.9) 1.8 (1.9) 1.4 (1.4) 1.8 (1.8)

GDP, calendar adjusted -4.4 (-4.4) 2.6 (2.3) 4.0 (3.4) 3.6 (3.5)

Number of hours worked -2.5 (-2.5) -0.7 (-1.2) 1.5 (0.5) 1.4 (1.1)

Unit labour cost 2.4 (2.4) 2.1 (2.2) 2.5 (2.6) 3.1 (3.1) Exchange rate, TCW-index, 1992-11-18=100

140.2 (140.2) 132.4 (131.8) 129.6 (128.2) 128.7 (127.7)

Real repo rate -1.0 (-1.0) -0.8 (-0.6) 0.4 (0.6)

Table A12. Alternative scenario with weaker exchange rate, annual averageAnnual percentage change unless otherwise specified

Note. Main scenario’s forecast within brackets. Sources: Statistics Sweden and the Riksbank

2009 2010 2011 2012

Repo rate, per cent 0.7 (0.7) 0.7 (0.4) 2.3 (1.8) 3.6 (3.3)

CPIF 1.9 (1.9) 2.4 (1.9) 2.3 (1.4) 2.1 (1.8)

GDP, calendar adjusted -4.4 (-4.4) 2.6 (2.3) 3.8 (3.4) 3.6 (3.5)

Number of hours worked -2.5 (-2.5) -0.9 (-1.2) 0.8 (0.5) 1.0 (1.1)

Unit labour cost 2.4 (2.4) 2.3 (2.2) 3.3 (2.6) 3.2 (3.1) Exchange rate, TCW-index, 1992-11-18=100

140.2 (140.2) 138.2 (131.8) 135.5 (128.2) 132.6 (127.7)

Real repo rate -1.0 (-1.0) -0.8 (-0.6) 0.7 (0.6)

Table A13. Alternative scenario with higher repo rate, annual averageAnnual percentage change unless otherwise specified

Note. Main scenario’s forecast within brackets. Sources: Statistics Sweden and the Riksbank

2009 2010 2011 2012

Repo rate, per cent 0.7 (0.7) 0.6 (0.4) 1.9 (1.8) 3.3 (3.3)

CPIF 1.9 (1.9) 1.8 (1.9) 1.1 (1.4) 1.6 (1.8)

GDP, calendar adjusted -4.4 (-4.4) 2.2 (2.3) 3.3 (3.4) 3.6 (3.5)

Labour market gap, per cent -0.1 (-0.1) -1.7 (-1.6) -1.7 (-1.4) -1.0 (-0.9)

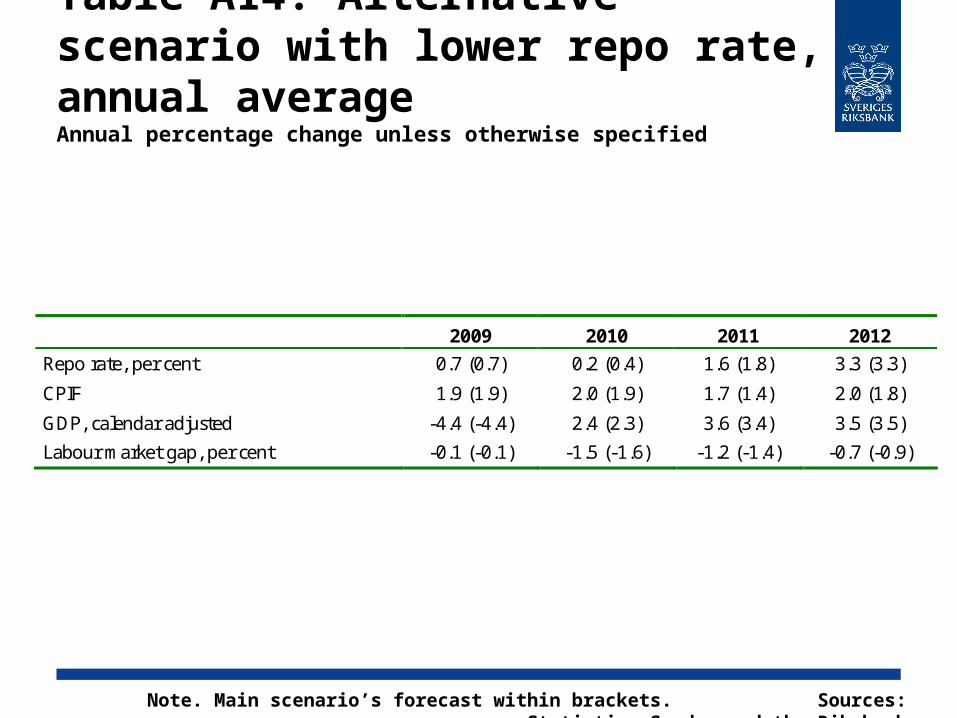

Table A14. Alternative scenario with lower repo rate, annual averageAnnual percentage change unless otherwise specified

Note. Main scenario’s forecast within brackets. Sources: Statistics Sweden and the Riksbank

2009 2010 2011 2012

Repo rate, per cent 0.7 (0.7) 0.2 (0.4) 1.6 (1.8) 3.3 (3.3)

CPIF 1.9 (1.9) 2.0 (1.9) 1.7 (1.4) 2.0 (1.8)

GDP, calendar adjusted -4.4 (-4.4) 2.4 (2.3) 3.6 (3.4) 3.5 (3.5)

Labour market gap, per cent -0.1 (-0.1) -1.5 (-1.6) -1.2 (-1.4) -0.7 (-0.9)

![Cecilia Skingsley: Should the Riksbank issue e-krona? · 1 [10] Should the Riksbank issue e-krona?1 Should the Riksbank issue electronic means of payment in the same way as we now](https://img.pdfslide.net/doc/110x75/5ec82f088662860afc5de461/cecilia-skingsley-should-the-riksbank-issue-e-krona-1-10-should-the-riksbank.jpg)