Embed Size (px)

Citation preview

MR PRICE GROUP LIMITED

INTERIM RESULTS

SEPTEMBER 2004

Market Conditions:

•Interest rates at lowest levels in 22 years

•South African Rand continues to trade well against the US$

•Credit retailers benefiting from increased consumer borrowing

•South African economy appears to be achieving macro inflation targets

Mr Price Group:

•Group remains predominantly cash retailer with 85% of sales for cash

•Financial health of balance sheet provides solid platform to achieve 2007 targets of:

•Turnover R6 billion

•Operating margin 10%

•Group remains committed to expansion and revamp programmes (35 000 sqm added to date)

Group Performance for the Period Ending Sept 2004:

•Revenue from continuing operations up 9% (comp 5.7%) to R2 billion despite deflation of 8%

•Strong unit sales exceed 50 million units, up 19% on prior year

•Costs and expenses grew by only 7%

•Net finance income reach R5m compared to net finance costs of R1.5m reported in the previous year

•Net profit from continuing operations up 45% to R18m

•Interim operating margin from continuing operations increased from 4.6% to 6.1% as a consequence of an improvement in gross profit margins

Headline Earnings per share

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004

Compound growth 60.66% over 5 years

Headline earnings per share up 31% to 33.2 cents per share

3,73,7 3,9 3,9 3,20

2

4

6

8

10

12

2000 2001 2002 2003 2004

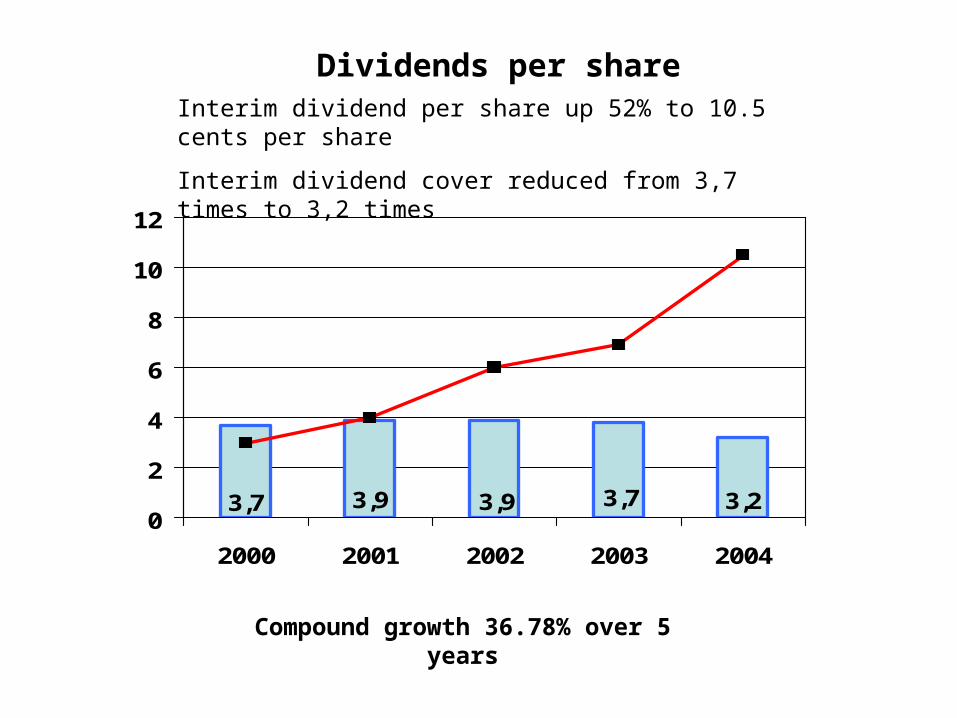

Compound growth 36.78% over 5 years

Dividends per shareInterim dividend per share up 52% to 10.5 cents per share

Interim dividend cover reduced from 3,7 times to 3,2 times

Taxation:•RSS operations sold to management during the period under review (loss on discontinuance of R1m does not impact on HEPS)

•Group tax rate up to 35% from last year 31%•STC•Effective corporate and other tax

•Prior year tax rate impacted by the significant losses uncured by the discontinued Chile operation

Discontinued Operations:

•RSS operations sold to management during the period under review (loss on discontinuance of R1m does not impact on HEPS)

•As reported previously, the business closed the six test stores in Chile in the previous financial period and is attending to the wind-up of the corporate structure

Mr Price Group Turnover Growth

0

0.5

1

1.5

2

2.5

2000 2001 2002 2003 2004

Ra

nd

Bill

ion

s

0

15

30

45

Perc

en

tag

e G

row

th

2000 2001 2002 2003 2004

Strength in Working Capital Management Continues:

Cash:

•Cash balances end on R337m notwithstanding:

•Capital expenditure of R37m

•R95m of short term borrowings repaid (SARS)

•Payment of final F2004 dividend which was 40% up on prior period

Inventory:

•Inventories 3.9% lower at R586m, notwithstanding:

•Sales growth of 9%

•Unit sales growth of 19%

•Stock turn increased from 4.3 times to 4.5 times

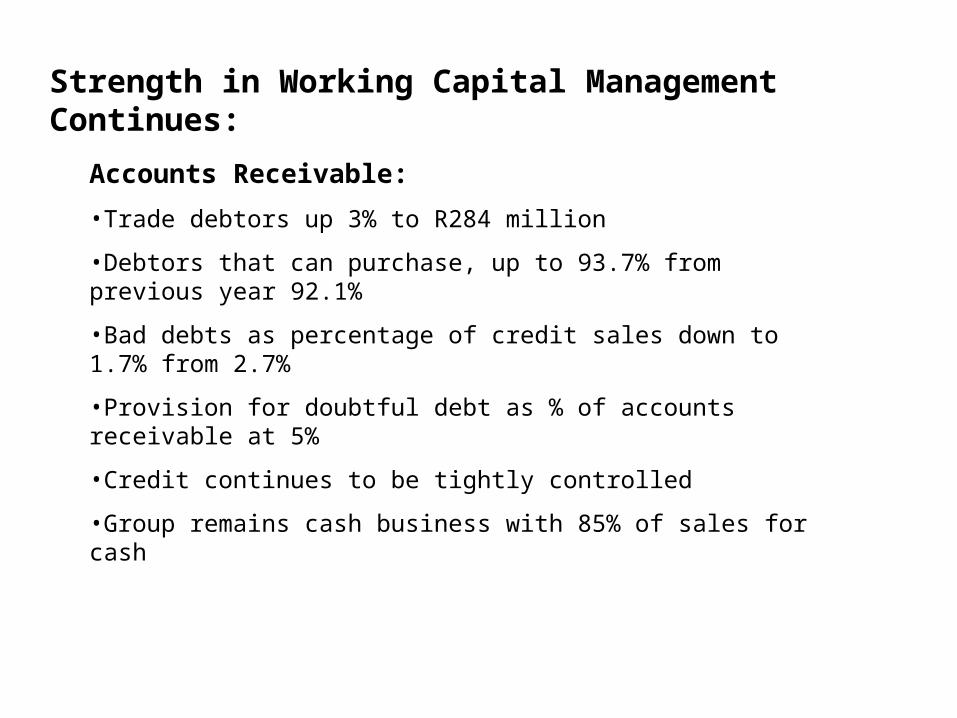

Strength in Working Capital Management Continues:

Accounts Receivable:

•Trade debtors up 3% to R284 million

•Debtors that can purchase, up to 93.7% from previous year 92.1%

•Bad debts as percentage of credit sales down to 1.7% from 2.7%

•Provision for doubtful debt as % of accounts receivable at 5%

•Credit continues to be tightly controlled

•Group remains cash business with 85% of sales for cash

CASH DIVISION: 539 STORES

WEEKEND MATERIAL: 306 stores

Weighted ave sqm up 3.3%

Gross space added 5037 sqm

MR PRICE HOME: 119 stores

Weighted ave sqm1.0%

Gross space added 623 sqm

SHEET STREET: 114 stores

Weighted ave sqm 10.6%

Gross space added 2751 sqm

Cash Division Comprises:•Mr Price Weekend Material

•Mr Price Home

•Sheet Street

•Revenue up 9% (comp 4.7%) to R1.5 billion with deflation of 9%

•Unit sales grew by 20 % to over 42 million

•Weighted average trading space up 4.4%

•Operating profit up 42% at R89 million

•Operating margin increased from 4.7% to 6.1%

•Operating profit up 42% at R89 million

•Operating margin increased from 4.7% to 6.1%

•Weekend Material delivers strong operating margin

•Home chains significant increase in operating profit with deflation of 2%

CREDIT DIVISION: 259 STORES

MILADYS: 160 stores

Weighted ave sqm down 0.3%

Gross space added 183 sqm

THE HUB: 11 STORES

GALAXY & CO: 88 stores

Weighted ave sqm down 7.1%

Gross space removed 473 sqm

Credit Division Comprises:•Miladys

•The Hub

•Galaxy & Co

•Revenue up 9% (comp 8.7%) to R513 million on deflation of 8%

•Unit sales grew by 15 % to over 7 million

•Weighted average trading space down 0.4% Operating profit up 33% at R47 million

•Operating margin increased from 7.5% to 9.3%

Prospects:

•Commitment to expansion and revamp programme

•Investigation of new concepts and potential growth opportunities

•The group anticipates growth in earnings for the full year, despite a far stronger base in the second half

•Credit division: new look for Galaxy tested and new Miladys format to be rolled out within the next few years