Embed Size (px)

Citation preview

Market value accountingfor commercial banks

Thomas Mondschean

IFFOne of the repercussions of thesavings and loan crisis andrecent capital adequacy prob-lems among some commercialbanks and insurance compa-

nies has been a debate about the system ofaccounting used by financial institutions. Theissue is whether the current method of valuingassets and liabilities conveys information accu-rate enough to measure the economic net worthof financial institutions. If it does not, then is itpossible to design a valuation system for whichthe benefits of changing exceed the costs? Thisissue is important to policymakers and taxpay-ers because better information about the eco-nomic net worth of financial institutions couldgive regulators an opportunity to intervenesooner and potentially reduce the cost of clos-ing insolvent institutions. It is important toshareholders because uncertainty about theactual value of an institution makes it harder todecide whether to invest in its stocks. It is alsorelevant for creditors since the value of eco-nomic net worth affects a bank's ability toabsorb future losses and thus is an indication ofits ability to bear risk.

One proposal that has been debated inrecent years is to require banks to use marketvalue accounting (MVA) to compute the valuesof their portfolios. MVA would require banksto adjust the values of assets and liabilitiesperiodically for changes in market prices andconditions. This idea is not new in financialcircles. For example, futures exchanges requirethat all futures contracts be marked to market atthe end of each trading day. For a variety of

reasons, however, marking certain portions of abank's portfolio to market is more difficult.Opponents of MVA focus on these difficultiesand the additional costs a new accounting sys-tem would require and contend that such achange is economically impractical. Propo-nents, on the other hand, emphasize the costs ofnot changing systems. Under the current histor-ical cost accounting system (HCA), banksrecord the value of assets and liabilities at thetime they are acquired, and these values are notsubsequently adjusted until they are sold orwritten down. Proponents of MVA argue thatthe current accounting system diminishes thepublic's confidence in the financial system bynot presenting an accurate enough picture of thecurrent economic health of financial firms.

The purpose of this article is to examinethe costs and benefits of market value account-ing. I focus the discussion on the case of com-mercial banks; however, much of the analysispresented could be applied to other types offinancial intermediaries. Many of the issuesdiscussed here have been examined in greaterdetail in the chapter on market value account-ing in the 1991 U.S. Treasury study on reform-ing the financial system. After a discussion ofthe purposes served by an accounting systemfor banks, I explain how HCA misrepresentsthe true economic value of financial institu-

Thomas Mondschean is a consultant at the FederalReserve Bank of Chicago and assistant professor ofeconomics at DePaul University. The author thanksDavid Allardice, Herb Baer, and David Jones forhelpful comments, and George Rodriguez and JohnMcElravey for research assistance.

16 ECONOMIC PERSPECTIVES

tions. Next, the commercial bank balance sheetis examined in detail both to explain how marketvalue accounting would work and to evaluatethe difficulty of marking to market various bal-ance sheet items. Once it is known which bal-ance sheet items are most difficult to value, it isthen possible to assess how costly the move toMVA would be and whether the cost-benefittradeoff for market value accounting is differentfor large banks than for smaller institutions. Ithen discuss the major criticisms raised aboutMVA. The issues raised by both sides implythat there may be some middle ground, so Iexplore possibilities for improving the system ofreporting that does not require a complete moveto market value accounting. The article con-cludes by making suggestions for improving thequality of information provided by commercialbanks to both bank regulators and the public.

What should an accounting system forbanks achieve?

Any bank accounting system must provideuseful information to both bank regulators andthe public. According to the recent U.S. Trea-sury study on financial reform, useful informa-tion should be: "(a) relevant, timely, and under-standable to users of financial statements; (b)reliable, in the sense of being accurate, objec-tive, and verifiable by outside parties; and (c)reported in a consistent manner to facilitatecomparisons over time and across firms."' Butfor what purposes are accounting data useful?One goal is to assist in ensuring financial con-trol. As Benston (1989) points out, the currentbank accounting system is "... designed to reporton the transactions that occurred between theenterprise and other market participants andamong control and decision units within theenterprise and the people responsible.'" Costaccounting allows banks to trace each dollar asit is acquired or spent, leaving a paper trail thatassists both banks and independent auditors indetecting fraud as well as in finding and correct-ing mistakes. Given the volume of transactionsa typical bank handles every day, whateveraccounting system is in place must allow banksto monitor accurately all transactions as theytake place.

Another purpose of an accounting system isto permit accurate appraisals of the value ofbank net worth or capital. Net worth is definedas the difference between the value of assets andthe value of liabilities. Shareholders need an

accurate measure of accounting net worth inorder to make informed investment decisions.To the bank's uninsured creditors, net worthrepresents the amount a bank could lose andstill pay its debts. From their perspective, it ismore important that the value of net worth notbe overstated than that it be accurate. If networth is understated, uninsured creditors re-ceive additional protection. Appraisals of networth should be timely in the sense that valua-tions of net worth should take into accountchanging economic conditions, so that, forexample, a decline in the value of a bank'sassets, other things equal, would result in adecline in the value of its net worth. The infor-mation provided should also make it possiblefor users of these data to compare the relativeperformance of different banks.

No matter which type of accounting systemis in place, a related issue is whether banksshould be required to disclose more informationto permit the public to reach their own conclu-sions about a bank's net worth. In particular,should banks be required to release the sameinformation to the public as they do to the regu-latory authorities? Some argue that greaterdisclosure of a bank's loan portfolio mightaffect the competitive position of a bank or itscustomers if confidential information valuableto other firms was released. Regulators mustbalance the public's need to learn about bankswith the banks' need to protect confidential orproprietary information. Stockholders anduninsured creditors have a legitimate need toknow the economic value of a bank to protecttheir own interests; however, it may not be inthe best interest of bank managers to releasesuch information. Some market participantscontend that price-earnings ratios for bankholding company stocks might be higher ifbanks disclosed more and better informationabout their portfolios. Thus, the public policyissue is not whether banks should disclose con-fidential or proprietary information but whetherthey should be required to release more infor-mation than they currently do.' It is worthnoting that other financial services industriesdisclose more detailed information about theirportfolios to the public than banks do. Mutualfunds are required by the Securities and Ex-change Commission (SEC) to disclose theircomplete portfolio holdings every quarter. SECregulated broker/dealers and futures commis-sions merchants must report market values.

FEDERAL RESERVE BANK OF CHICAGO

17

Insurance companies are required to disclosetheir complete stock and bond holdings as wellas state-by-state breakdowns of their long termmortgage loans to regulators once a year. 4

Problems with the currentaccounting system

Under HCA rules, a bank records the nom-inal value of the asset or liability at the time itis acquired.' One justification for HCA is thatbanks were presumed to acquire assets andliabilities and hold them until maturity. Aslong as they receive repayment of interest andprincipal at the contracted periods, changes inmarket value were presumed to have no effecton the asset's cash flow. However, this motiva-tion for HCA violates basic economic princi-ples. First, an asset's purchase price does notrepresent the best estimate of what it will beworth in the future because it ignores subse-quent information about changes in marketinterest rates, credit risk, and other variables.Second, the assumption that banks hold all oftheir assets to maturity is outdated. The devel-opment of securitization and other techniquesmeans that many types of loans can be easilysold before maturity. Third, for certain assets,banks can lock in current embedded gains orlimit future economic losses by hedging even ifthe asset is not sold before maturity.

The development and use of generallyaccepted accounting principles (GAAP), whichare based in large part on HCA principles, aredesigned to give all banks a similar set of ruleswith which they report the value of their portfo-lios. However, GAAP allows banks some flexi-bility in determining the timing of valuationchanges. For example, a bank with an unreal-ized gain on a particular asset may choose aparticular time to sell the asset, realize the gain,and use it to offset other losses. Alternatively,a bank may prefer to increase loan loss reservesat discrete intervals rather than taking losses asthey become apparent.' Thus, the book valueof bank capital might understate its economicvalue if a bank has unrealized gains in its port-folio or overstate its economic value if it hasunrealized losses. Because GAAP permits suchbehavior, meaningful comparisons betweenbanks are more difficult. Proponents of MVAbelieve the best way to solve this problem is torequire banks to report changes in values whenthey occur, rather than allowing banks tochoose when to realize them.

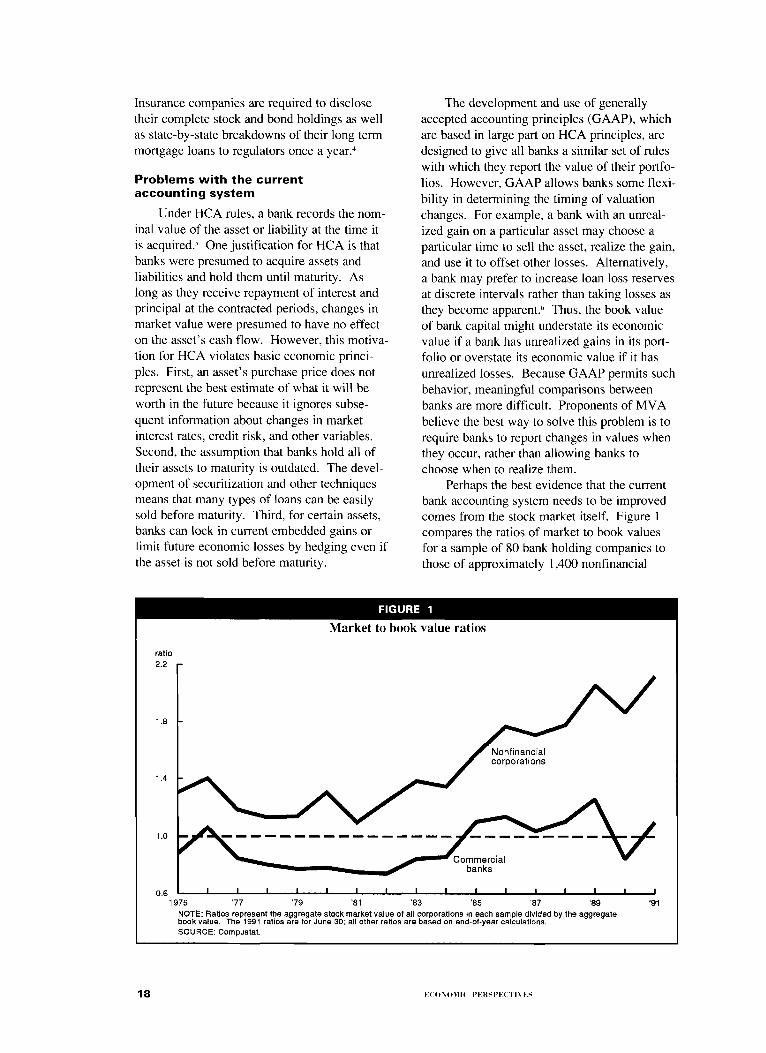

Perhaps the best evidence that the currentbank accounting system needs to be improvedcomes from the stock market itself. Figure 1compares the ratios of market to book valuesfor a sample of 80 bank holding companies tothose of approximately 1,400 nonfinancial

FIGURE 1

Market to book value ratios

ratio

1.8

Nonfinancialcorporations

1.4

1.0

0.6 '89 '91

NOTE: Ratios represent the aggregate stock market value of all corporations in each sample divided by the aggregatebook value. The 1991 ratios are for June 30; all other ratios are based on end-of-year calculations.SOURCE: Compustat.

18 Et1INOMII PERSPECTIN ES

Commercialbanks

Nonfinancialcorporations

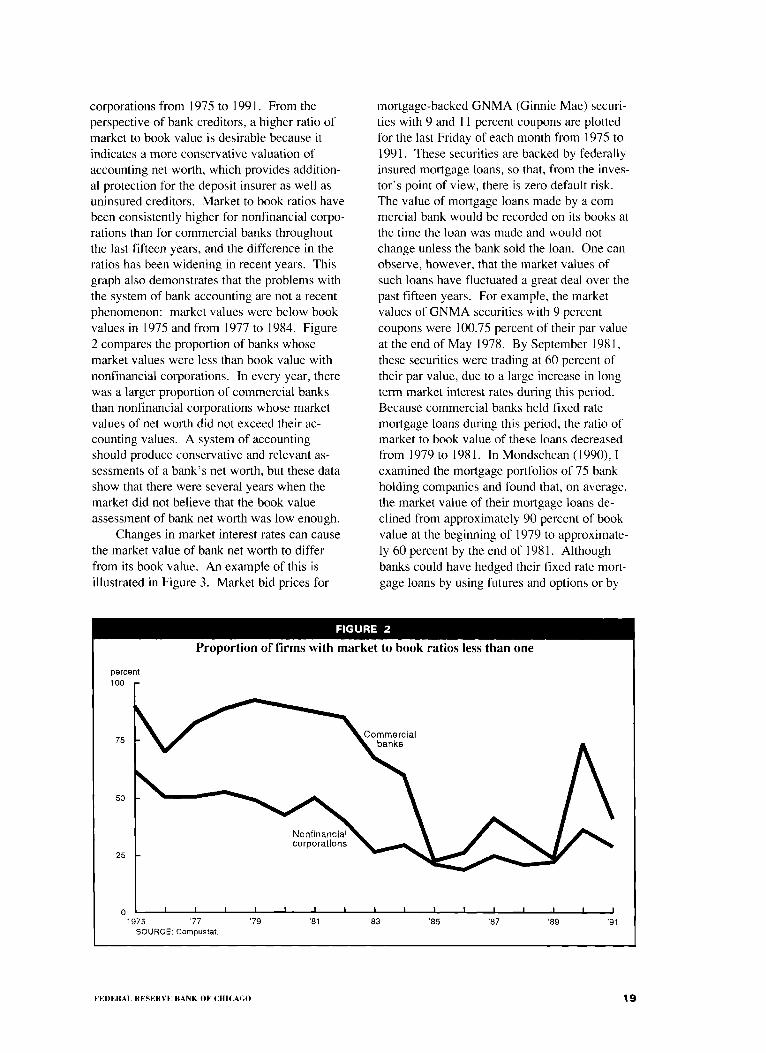

corporations from 1975 to 1991. From theperspective of bank creditors, a higher ratio ofmarket to book value is desirable because itindicates a more conservative valuation ofaccounting net worth, which provides addition-al protection for the deposit insurer as well asuninsured creditors. Market to book ratios havebeen consistently higher for nonfinancial corpo-rations than for commercial banks throughoutthe last fifteen years, and the difference in theratios has been widening in recent years. Thisgraph also demonstrates that the problems withthe system of bank accounting are not a recentphenomenon: market values were below bookvalues in 1975 and from 1977 to 1984. Figure2 compares the proportion of banks whosemarket values were less than book value withnonfinancial corporations. In every year, therewas a larger proportion of commercial banksthan nonfinancial corporations whose marketvalues of net worth did not exceed their ac-counting values. A system of accountingshould produce conservative and relevant as-sessments of a bank's net worth, but these datashow that there were several years when themarket did not believe that the book valueassessment of bank net worth was low enough.

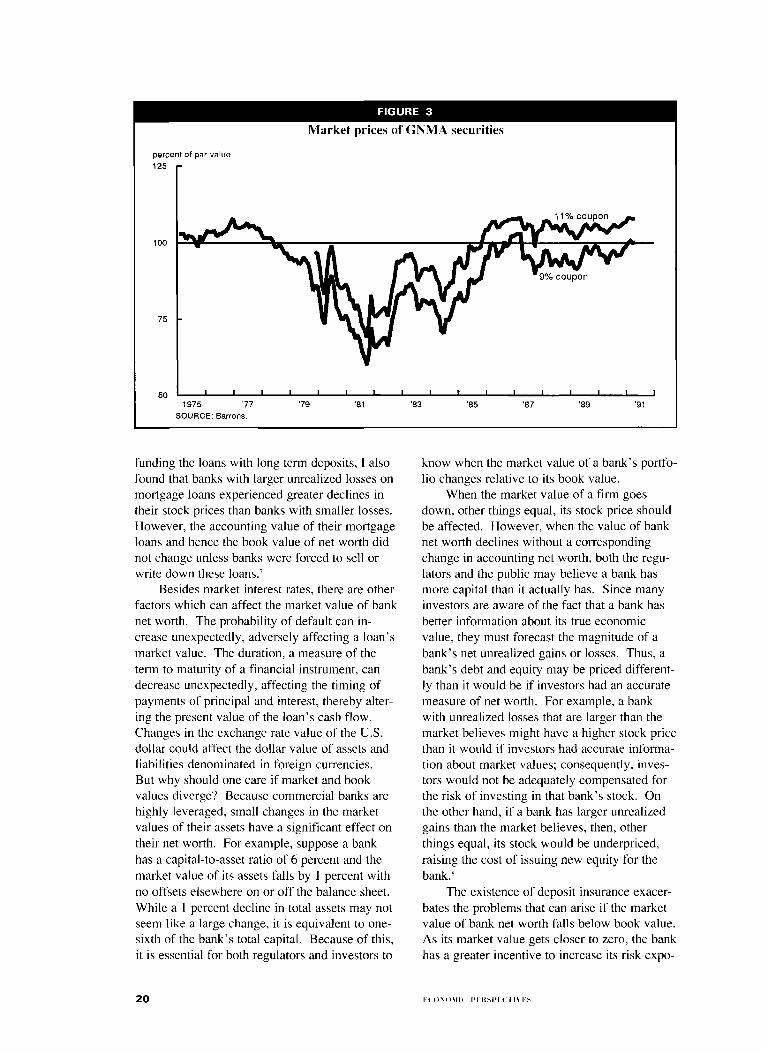

Changes in market interest rates can causethe market value of bank net worth to differfrom its book value. An example of this isillustrated in Figure 3. Market bid prices for

mortgage-backed GNMA (Ginnie Mae) securi-ties with 9 and 11 percent coupons are plottedfor the last Friday of each month from 1975 to1991. These securities are backed by federallyinsured mortgage loans, so that, from the inves-tor's point of view, there is zero default risk.The value of mortgage loans made by a com-mercial bank would be recorded on its books atthe time the loan was made and would notchange unless the bank sold the loan. One canobserve, however, that the market values ofsuch loans have fluctuated a great deal over thepast fifteen years. For example, the marketvalues of GNMA securities with 9 percentcoupons were 100.75 percent of their par valueat the end of May 1978. By September 1981,these securities were trading at 60 percent oftheir par value, due to a large increase in longterm market interest rates during this period.Because commercial banks held fixed ratemortgage loans during this period, the ratio ofmarket to book value of these loans decreasedfrom 1979 to 1981. In Mondschean (1990), Iexamined the mortgage portfolios of 75 bankholding companies and found that, on average,the market value of their mortgage loans de-clined from approximately 90 percent of bookvalue at the beginning of 1979 to approximate-ly 60 percent by the end of 1981. Althoughbanks could have hedged their fixed rate mort-gage loans by using futures and options or by

FIGURE 2

Proportion of firms with market to book ratios less than one

percent100

75

50

25

01975 '77

'79

'81

'83

'85

'87

'89

'91SOURCE: Compustat.

FEDERAL RESERVE BANK OF CHICAGO

19

FIGURE 3

Market prices of GNMA securities

percent of par value125

funding the loans with long term deposits, I alsofound that banks with larger unrealized losses onmortgage loans experienced greater declines intheir stock prices than banks with smaller losses.However, the accounting value of their mortgageloans and hence the book value of net worth didnot change unless banks were forced to sell orwrite down these loans.'

Besides market interest rates, there are otherfactors which can affect the market value of banknet worth. The probability of default can in-crease unexpectedly, adversely affecting a loan'smarket value. The duration, a measure of theterm to maturity of a financial instrument, candecrease unexpectedly, affecting the timing ofpayments of principal and interest, thereby alter-ing the present value of the loan's cash flow.Changes in the exchange rate value of the U.S.dollar could affect the dollar value of assets andliabilities denominated in foreign currencies.But why should one care if market and bookvalues diverge? Because commercial banks arehighly leveraged, small changes in the marketvalues of their assets have a significant effect ontheir net worth. For example, suppose a bankhas a capital-to-asset ratio of 6 percent and themarket value of its assets falls by 1 percent withno offsets elsewhere on or off the balance sheet.While a 1 percent decline in total assets may notseem like a large change, it is equivalent to one-sixth of the bank's total capital. Because of this,it is essential for both regulators and investors to

know when the market value of a bank's portfo-lio changes relative to its book value.

When the market value of a firm goesdown, other things equal, its stock price shouldbe affected. However, when the value of banknet worth declines without a correspondingchange in accounting net worth, both the regu-lators and the public may believe a bank hasmore capital than it actually has. Since manyinvestors are aware of the fact that a bank hasbetter information about its true economicvalue, they must forecast the magnitude of abank's net unrealized gains or losses. Thus, abank's debt and equity may be priced different-ly than it would be if investors had an accuratemeasure of net worth. For example, a bankwith unrealized losses that are larger than themarket believes might have a higher stock pricethan it would if investors had accurate informa-tion about market values; consequently, inves-tors would not be adequately compensated forthe risk of investing in that bank's stock. Onthe other hand, if a bank has larger unrealizedgains than the market believes, then, otherthings equal, its stock would be underpriced,raising the cost of issuing new equity for thebank.'

The existence of deposit insurance exacer-bates the problems that can arise if the marketvalue of bank net worth falls below book value.As its market value gets closer to zero, the bankhas a greater incentive to increase its risk expo-

20 1•14.4 )',1 11414 PEItS1 . 1.:1:1 I'

sure. Since shareholders would receive nothingif the institution is closed, a market value insol-vent bank acting in the best interest of share-holders has a strong incentive to increase risk inthe hope of earning above normal returns. Ifthe institution experiences greater losses, thelosses are borne by the deposit insurer and notby the shareholders, thereby placing the depositinsurance fund at greater risk. This moral haz-ard problem underscores the importance ofproviding accurate market values of bank networth to regulators. Because the current ac-counting system does not guarantee that thiswill be the case, the probability that taxpayerswill be required to absorb part of the cost offuture bank failures is increased. 9

Measurement issues in a market valueaccounting system

Under a system of market value account-ing, banks would be required to adjust all assetsand liabilities for changes in the market valueof those assets and liabilities. Critics of thisapproach argue that market value estimates ofbank net worth would be unreliable due to thedifficulty of measuring the value of various

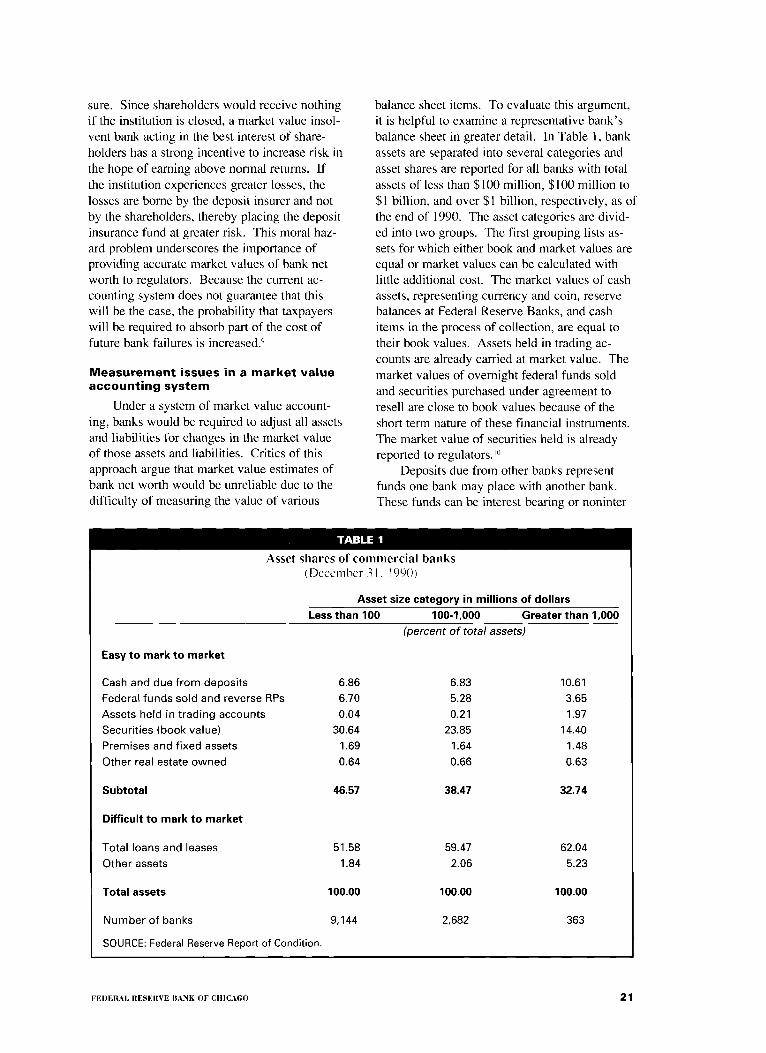

balance sheet items. To evaluate this argument,it is helpful to examine a representative bank'sbalance sheet in greater detail. In Table 1, bankassets are separated into several categories andasset shares are reported for all banks with totalassets of less than $100 million, $100 million to$1 billion, and over $1 billion, respectively, as ofthe end of 1990. The asset categories are divid-ed into two groups. The first grouping lists as-sets for which either book and market values areequal or market values can be calculated withlittle additional cost. The market values of cashassets, representing currency and coin, reservebalances at Federal Reserve Banks, and cashitems in the process of collection, are equal totheir book values. Assets held in trading ac-counts are already carried at market value. Themarket values of overnight federal funds soldand securities purchased under agreement toresell are close to book values because of theshort term nature of these financial instruments.The market value of securities held is alreadyreported to regulators.'°

Deposits due from other banks representfunds one bank may place with another bank.These funds can be interest-bearing or noninter-

TABLE 1

Asset shares of commercial banks(December 31. 1990)

Asset size category in millions of dollars

Less than 100 100-1,000 Greater than 1,000

Easy to mark to market

(percent of total assets)

Cash and due from deposits 6.86 6.83 10.61Federal funds sold and reverse RPs 6.70 5.28 3.65Assets held in trading accounts 0.04 0.21 1.97Securities (book value) 30.64 23.85 14.40Premises and fixed assets 1.69 1.64 1.48Other real estate owned 0.64 0.66 0.63

Subtotal 46.57 38.47 32.74

Difficult to mark to market

Total loans and leases 51.58 59.47 62.04Other assets 1.84 2.06 5.23

Total assets 100.00 100.00 100.00

Number of banks 9,144 2,682 363

SOURCE: Federal Reserve Report of Condition.

FEDERAL RESERVE BANK OF CHICAGO

21

est-bearing. In general, smaller banks having acorrespondent relationship with a larger bankdeposit these funds in exchange for servicesprovided by the larger bank. Since there is agreat deal of competition for this business amonglarge banks, it is believed that the value of ser-vices provided as implicit interest on these bal-ances approximates a market interest rate; hence,the market values of these deposits equal theirbook values.

Computing market values for other realestate owned (OREO) is somewhat less precise.OREO includes all real estate owned or con-trolled by the bank excluding bank premises,such as direct and indirect investments in realestate ventures for investment purposes and realestate acquired through foreclosure. Currently,banks report to regulators the book value ofthese assets less accumulated depreciation,which cannot be greater than fair market value.Fair market values of these assets are generallycalculated by independent appraisers. Theaccuracy of these appraisal reports depends onboth the availability of comparable market infor-mation as well as the judgment of the appraisers.While they may be imprecise, these estimateswould be no less exact under market value ac-counting than under the current system. Sincebanks also record bank premises and fixed assets(computers, furniture, etc.) at book value lessdepreciation, there is no reason why marketappraisals could not be used to value theseassets as well."

Taken as a group, those assets for whichusing MVA would entail little or no additionalcost to banks represent approximately one-thirdof total assets for banks with over $1 billion intotal assets and just under one-half of total assetsfor the 9,144 banks with $100 million or less intotal assets as of the end of 1990.

Proponents of MVA recognize that certaincategories of loans would be difficult to mark tomarket. While some loans, such as one-to-fourfamily mortgage loans and student loans, areactively bought and sold, most types of loansare not actively traded, and so market valuescannot be inferred directly from secondary mar-

kets. 12 Although financial institutions must oftencompute market values of nontraded assets fortheir own purposes, such calculations are inher-ently judgmental and could potentially be ma-nipulated. Opponents of MVA point out thatthe cost of imposing MVA on banks would behigh if every bank loan required such a valua-

tion. Proponents counter that banks already usesuch judgment in determining the appropriatesize of their loan loss reserves.

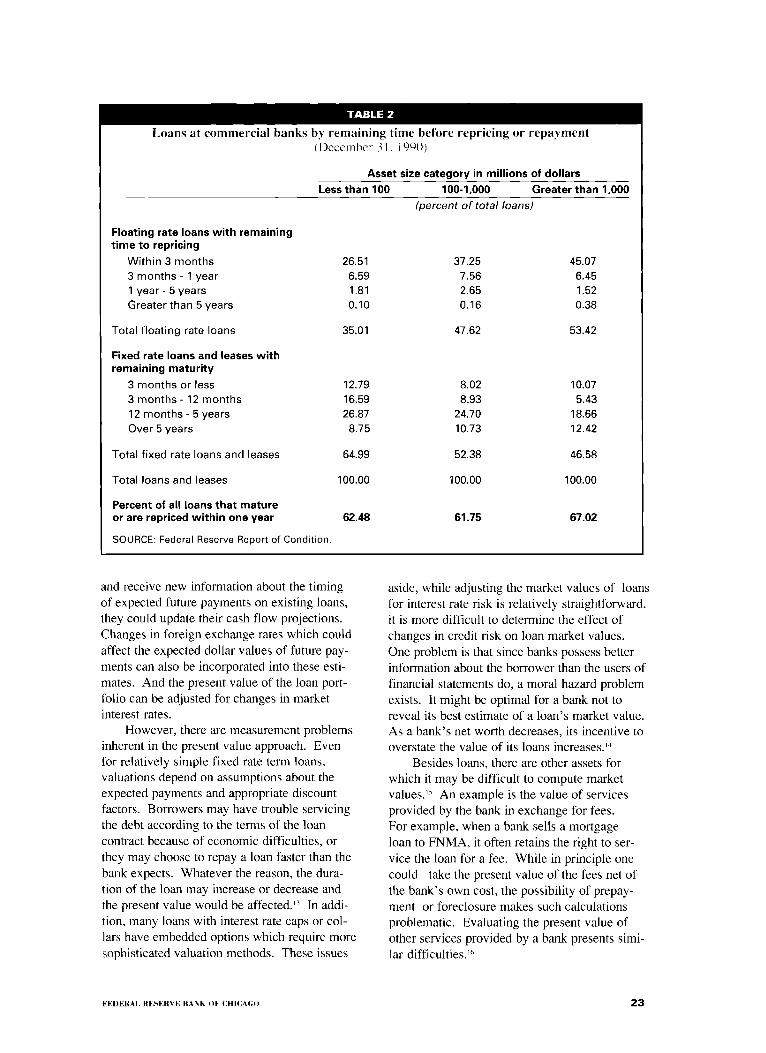

Analyzing the effect of market interest ratechanges on loan market values is a primary ob-jective of MVA. Table 2 classifies loans at com-mercial banks according to the remaining time torepricing or repayment. Floating rate loans areloans whose interest rate is adjusted to reflectmarket interest rate changes. For banks withover $1 billion in total assets, the majority ofloans are made at floating interest rates. Themarket values of these loans can diverge duringthe period between repricing dates; however,once the loan interest rate is adjusted, market andbook values are equal. Thus, the effect of chang-es in market interest rates on the market values ofbank loans depends on the time period beforeeither the loan is repriced or it is repaid. AsTable 2 indicates, for all size classes, the percent-age of loans which are repriced or repaid withinone year is between 60 and 70 percent.

For loans with longer periods before repric-ing or repayment, assuming banks revealed accu-rate cash flow information, market values couldbe inferred using some form of discounted cashflow analysis. The market value of a loan isequated to the present value of the expected flowof payments accruing from the loan. Assuming,for simplicity, that payments are made at the endof each period, the present value of the flow ofpayments as of date 0 can be represented by thefollowing:

PV0 = Co + C i l(1 + r)+ C2/(1 + r2)2 ++ CA1 + r„ )"

where, for example, C, represents the expectedpayment of principal and interest in period 1, r isthe discount rate for period 1, and n is the num-ber of years from today to the date of the finalpayment. The present value of a bank's existingloans can be affected in two ways. First, thetiming of interest and principal payments may bealtered in the event of a rescheduling of repay-ments. Second, the interest rate used to discountfuture payments may change. Using discountedcash flows to derive market values would haveseveral advantages. As long as banks know whenexpected payments of interest and principalwould occur, they could combine loans and re-port the expected cash flow of the entire loanportfolio. Thus, they need not report the marketvalue of each loan. As banks make new loans

22 VE4) \ ONlIE VERSVECTIN ES

TABLE 2

Loans at commercial banks by remaining time before repricing or repayment(December 31, 1990)

Asset size category in millions of dollars

Less than 100 100-1,000 Greater than 1,000

Floating rate loans with remainingtime to repricing

(percent of total loans)

Within 3 months 26.51 37.25 45.073 months - 1 year 6.59 7.56 6.451 year - 5 years 1.81 2.65 1.52Greater than 5 years 0.10 0.16 0.38

Total floating rate loans 35.01 47.62 53.42

Fixed rate loans and leases withremaining maturity

3 months or less 12.79 8.02 10.073 months - 12 months 16.59 8.93 5.4312 months - 5 years 26.87 24.70 18.66Over 5 years 8.75 10.73 12.42

Total fixed rate loans and leases 64.99 52.38 46.58

Total loans and leases 100.00 1 00 .00 100.00

Percent of all loans that matureor are repriced within one year 62.48 61.75 67.02

SOURCE: Federal Reserve Report of Condition.

and receive new information about the timingof expected future payments on existing loans,they could update their cash flow projections.Changes in foreign exchange rates which couldaffect the expected dollar values of future pay-ments can also be incorporated into these esti-mates. And the present value of the loan port-folio can be adjusted for changes in marketinterest rates.

However, there are measurement problemsinherent in the present value approach. Evenfor relatively simple fixed rate term loans,valuations depend on assumptions about theexpected payments and appropriate discountfactors. Borrowers may have trouble servicingthe debt according to the terms of the loancontract because of economic difficulties, orthey may choose to repay a loan faster than thebank expects. Whatever the reason, the dura-tion of the loan may increase or decrease andthe present value would be affected." In addi-tion, many loans with interest rate caps or col-lars have embedded options which require moresophisticated valuation methods. These issues

aside, while adjusting the market values of loansfor interest rate risk is relatively straightforward,it is more difficult to determine the effect ofchanges in credit risk on loan market values.One problem is that since banks possess betterinformation about the borrower than the users offinancial statements do, a moral hazard problemexists. It might be optimal for a bank not toreveal its best estimate of a loan's market value.As a bank's net worth decreases, its incentive tooverstate the value of its loans increases."

Besides loans, there are other assets forwhich it may be difficult to compute marketvalues." An example is the value of servicesprovided by the bank in exchange for fees.For example, when a bank sells a mortgageloan to FNMA, it often retains the right to ser-vice the loan for a fee. While in principle onecould take the present value of the fees net ofthe bank's own cost, the possibility of prepay-ment or foreclosure makes such calculationsproblematic. Evaluating the present value ofother services provided by a bank presents simi-lar difficulties.'€

FEDERAL RESERVE RANK OF CHICAGO

23

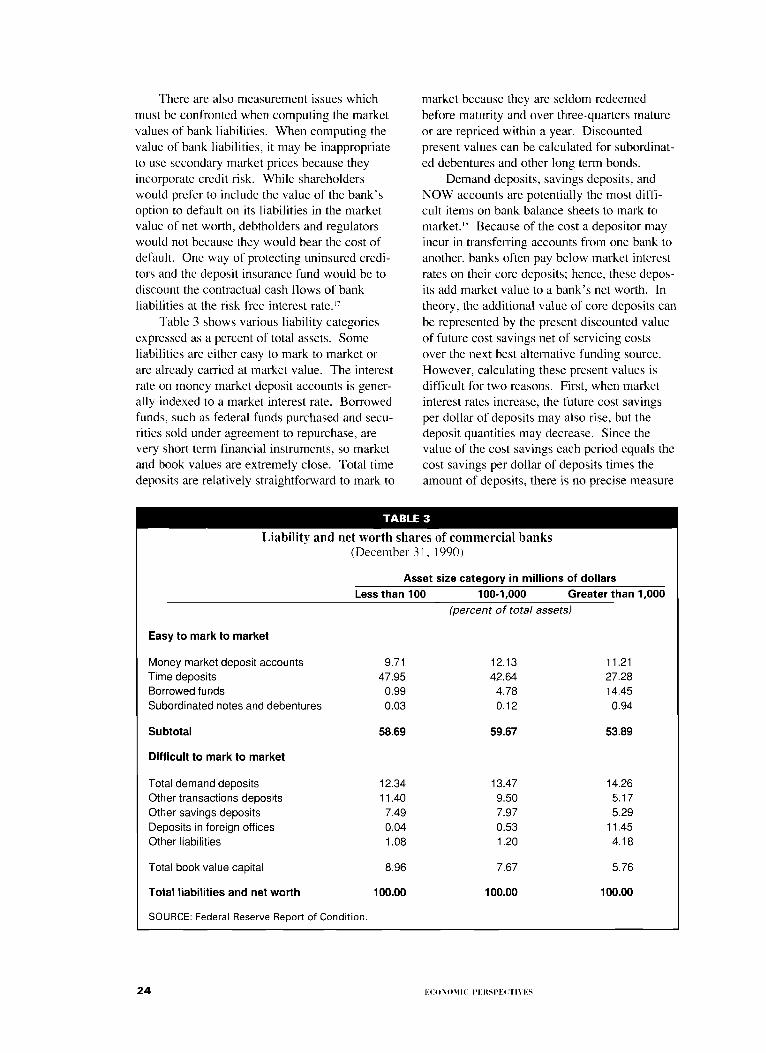

There are also measurement issues whichmust be confronted when computing the marketvalues of bank liabilities. When computing thevalue of bank liabilities, it may be inappropriateto use secondary market prices because theyincorporate credit risk. While shareholderswould prefer to include the value of the bank'soption to default on its liabilities in the marketvalue of net worth, debtholders and regulatorswould not because they would bear the cost ofdefault. One way of protecting uninsured credi-tors and the deposit insurance fund would be todiscount the contractual cash flows of bankliabilities at the risk free interest rate."

Table 3 shows various liability categoriesexpressed as a percent of total assets. Someliabilities are either easy to mark to market orare already carried at market value. The interestrate on money market deposit accounts is gener-ally indexed to a market interest rate. Borrowedfunds, such as federal funds purchased and secu-rities sold under agreement to repurchase, arevery short term financial instruments, so marketand book values are extremely close. Total timedeposits are relatively straightforward to mark to

market because they are seldom redeemedbefore maturity and over three-quarters matureor are repriced within a year. Discountedpresent values can be calculated for subordinat-ed debentures and other long term bonds.

Demand deposits, savings deposits, andNOW accounts are potentially the most diffi-cult items on bank balance sheets to mark tomarket.'' Because of the cost a depositor mayincur in transferring accounts from one bank toanother, banks often pay below market interestrates on their core deposits; hence, these depos-its add market value to a bank's net worth. Intheory, the additional value of core deposits canbe represented by the present discounted valueof future cost savings net of servicing costsover the next best alternative funding source.However, calculating these present values isdifficult for two reasons. First, when marketinterest rates increase, the future cost savingsper dollar of deposits may also rise, but thedeposit quantities may decrease. Since thevalue of the cost savings each period equals thecost savings per dollar of deposits times theamount of deposits, there is no precise measure

TABLE 3

Liability and net worth shares of commercial banks(December 31, 1990)

Asset size category in millions of dollars

Less than 100 100-1,000 Greater than 1,000

Easy to mark to market

(percent of total assets)

Money market deposit accounts 9.71 12.13 11.21Time deposits 47.95 42.64 27.28Borrowed funds 0.99 4.78 14.45Subordinated notes and debentures 0.03 0.12 0.94

Subtotal 58.69 59.67 53.89

Difficult to mark to market

Total demand deposits 12.34 13.47 14.26Other transactions deposits 11.40 9.50 5.17Other savings deposits 7.49 7.97 5.29Deposits in foreign offices 0.04 0.53 11.45Other liabilities 1.08 1.20 4.18

Total book value capital 8.96 7.67 5.76

Total liabilities and net worth 100.00 100.00 100.00

SOURCE: Federal Reserve Report of Condition.

24

ECONOMIC PERSPECTIVES

of the magnitude of these cost savings overtime. Second, because core deposits have nostated maturity, there is no objective method todetermine the duration of these deposits. Thus,any calculation using present values must bebased on assumptions which are difficult toverify. On the other hand, imprecise thoughthey may be, estimated valuations of core de-posits are routinely done by depository institu-tions interested in purchasing core deposit ac-counts from insolvent institutions or whenanalyzing the value of a bank for a prospectivemerger or acquisition.

Deposits in foreign offices, which fundover 10 percent of total assets for banks with $1billion or more in total assets, present similarconceptual difficulties for MVA. Time depos-its would be relatively easy to mark to market,but other types of foreign deposits may be moredifficult. While banks are currently not re-quired to break down their deposits in foreignoffices by type of deposit, we do know thatover 95 percent of these deposits pay explicitinterest. Thus, if foreign deposits were reportedin the same detail as domestic deposits are,accurate market valuations could be made forthe vast majority of these deposits. Requiringforeign deposit holdings to be reported in great-er detail would impose little additional costsince these deposits are concentrated in thelargest banks who need these data for internalpurposes.

Another set of measurement issues ariseswhen accounting for off balance sheet contin-gencies under MVA. Examples of such contin-gencies include interest rate and foreign curren-cy swaps, forward and futures contracts, loancommitments, letters of credit, and guarantees.Since banks are already required to estimate themarket value of interest rate and futures posi-tions for regulators, these pose no additionalproblems under MVA. However, evaluatingthe market value of loan commitments is com-plicated by the possibility that they would be-come loans. The values of loan guaranteesdepend on the probability that they will beexercised, which implies some estimate ofcredit risk is necessary. 19

In summary, while computing accuratemarket values for some bank balance sheetitems is difficult, many proponents of MVAbelieve the extent of the problems is exaggerat-ed since the majority of bank assets and liabili-

ties can be marked to market with little addi-tional cost. Many of the problems are inherentin any accounting system, but others are theresult of assumptions or subjective judgmentswhich must be made in order to provide esti-mates of market values. Proponents of MVAcontend that if banks start valuing their portfoli-os using MVA, the experience will spur ac-counting innovations that can improve thequality of information and reduce measurementerrors. Also, they argue that the questionshould not be whether market value accountingis perfectly accurate, but whether MVA is animprovement over historical cost accounting. IfMVA can reduce the bias (the difference be-tween economic and accounting values) and thevariance of the bias (the tendency for the biasto fluctuate over time) relative to HCA, itwould be an improvement over the currentaccounting system.

Costs imposed by a market valueaccounting system

The banking industry maintains that thecost of implementing a new system designed toreport market values as a basis for GAAP andregulatory reports would be prohibitively ex-pensive. According to this view, MVA requirescostly marking to market of all assets, liabili-ties, and contingent claims it holds using what-ever method—observation of secondary marketprices, appraisals, or discounted cash flowanalysis—is deemed most appropriate. Manydepository institutions claim that MVA wouldrequire additional developmental and othercosts to obtain necessary data, modify or pur-chase computer software, perform complexcalculations, and train personnel. Becausemany of these costs are fixed, smaller bankswould experience even greater burdens on aunit cost basis. Moreover, because many as-sumptions required to compute market valuesare subjective, the cost of auditing banks mayalso rise as verification of a bank's methodswould take longer and be more difficult.

Proponents of MVA respond that the incre-mental cost of adopting MVA is overstated forsmall banks. Smaller banks hold a larger pro-portion of assets which are relatively easy tomark to market, partly because they have ahigher percentage of their assets in securitiesbut also because of the nature of their loanportfolios. Table 4 shows how the average loan

FEDERAL RESERVE RANK OF CHICAGO 25

TABLE 4

Total loans at commercial banks by type of loan(December 31, 1990)

Asset size category in millions of dollars

Less than 100 100-1,000 Greater than 1,000

(percent of total loans)

Loans secured by real estate 50.07 51.10 35.12

Construction and land development 3.50 5.41 6.47Secured by farmland 4.93 1.26 0.21Revolving, open-end loans secured

by one-to-four family properties 1.55 3.34 3.00Mortgage loans-one-to-fourfamily dwellings 26.22 3.26 12.72

Mortgage loans-multifamilydwellings 0.94 1.41 0.88

Nonfarm nonresidential realestate loans 12.93 16.41 10.12

Loans to depository institutions 0.25 0.94 3.06Agricultural loans 9.68 1.81 0.56Commercial and industrial loans 19.33 22.45 32.53Consumer loans-credit cards 1.00 3.78 6.76Consumer loans-other 17.88 17.10 11.33Loans to foreign governments

and official institutions 0.01 0.06 1.65Other loans 3.61 4.71 10.03

Total loans and leases, net ofunearned income 100.00 100.00 100.00

SOURCE: Federal Reserve Report of Condition.

portfolio for smaller banks differs from theirlarger counterparts. The data show that, forbanks with less than $100 million in total assetsat the end of 1990, the proportion of relativelyeasy to value one-to-four family mortgageloans and non-credit-card consumer loans wassignificantly larger than for banks with over $1billion in total assets, and small banks held asmaller proportion of commercial and industrialloans They also have a larger proportion ofloans secured by farmland, for which there is agreat deal of price data. With few exceptions,smaller banks also do not have any foreigndeposits. In other words, because smaller bankshave portfolios which are easier to value, thecosts of adopting MVA per dollar of earningsmay actually be less than for larger banks.

Another point is that it is not necessary tomark individual assets and liabilities to marketin order to obtain the majority of the benefits ofMVA. One could aggregate loans and deposits

into pools with similar characteristics and esti-mate market values for each pool. An advan-tage of such a method is that idiosyncraticdifferences among assets within a pool wouldnot have as great an effect on its overall value,so measurement error may be reduced. Inaddition, while implementation and operatingcosts may be high initially, they would mostlikely decline over time. New products wouldbe created and marketed to make it easier tocollect and process the additional informationrequired for MVA. Economic incentives tolower these costs would lead to the develop-ment of standardized databases and software tocompute market values of complex financialinstruments. The movement toward standard-ization would also make it easier for users ofbank financial statements to compare relativebank performance.

Even if adopting MVA proves to be costly,proponents believe that any incremental cost of

26

E1:0■■41MIC PERSPECTIV t:S

MVA to the banking industry should be com-pared with the gains society derives by havingbetter information. Regulators and taxpayerswould especially benefit by having better andmore timely information about a bank's eco-nomic value. Bank managers could use theinformation derived from MVA to improvetheir management of risk exposure. Investorswould have a better measure of the economicvalue of banks which would allow investors tomake more informed choices about which bankinvestments to hold. Thus, while it may be inan individual bank's interest to oppose MVAbecause its cost of implementation may notexceed the benefits for the bank itself, MVAmay be worthwhile if the total benefit to societyexceeds the total cost to society. Indeed, thedifference between private and social net bene-fits is one of the principal justifications givenfor imposing regulations in general.

Possible economic effects of marketvalue accounting

In assessing the feasibility of changing theaccounting system for banks, it is necessary toevaluate the likely economic effects of such achange. Many researchers have studied theimpact of changes in accounting regulations onmarket values of firms.'" The general conclu-sion of these studies is that changes in account-ing and reporting rules do affect stock marketvalues. While it seems likely that changes inbank accounting rules may affect market valuesof bank securities, this is hardly a reason fornot making needed reforms since firms mustoften adjust to changes in accounting methodsand standards. Thus, a key question is whetherthe use of MVA will improve the safety andsoundness of the banking system. Also, willbanks become more or less competitive relativeto other firms under MVA? A third questionis how will bank portfolio behavior changeunder MVA.

Whether market participants perceivebanks to be safer under MVA than under cur-rent accounting practices depends in part onhow serious the measurement problems are.Opponents of market value accounting arguethat estimates based on subjective and difficultto verify assumptions will increase uncertaintyabout the true economic value of banks. Thiswill undermine public confidence in the banks,raising their costs of capital and borrowed

funds. Also, MVA opponents argue that cur-rent bank earnings will be even more sensitiveto fluctuations in interest and exchange ratesbecause they would have to realize capitalgains and losses sooner. As a result, investorswill demand greater risk premia. Banks maythen be induced to focus more on short runprofits and avoid long term loans that may bemore profitable but also more risky if they mustbe marked to market.

Proponents of MVA respond that requiringgreater disclosure of market values of bankportfolios would allow investors to make betterestimates of the economic or true value of banksecurities. Thus, MVA comes closer than his-torical cost accounting to disclosing the truevalue, and the true risk, of a bank to investorsand regulators. In particular, banks' cost ofcapital will rise under MVA only if banks hadbeen underpaying for capital, deposits, or bor-rowed funds previously by undercompensatinginvestors or depositors for the risk of investingin or lending to banks. Hence, MVA will bene-fit investors and lenders because it insures thatinvestors and lenders will be fairly compensat-ed for the risk of investing in or lending tobanks. Moreover, since MVA would make itmore difficult for banks to overstate their networth, MVA will benefit regulators by allow-ing banks that are having capital adequacyproblems to be identified more quickly. Thiswould improve the safety and soundness of thebanking industry.

The likely consequences of MVA for fu-ture bank behavior are difficult to determine.One concern is that banks may reduce creditavailability during periods of declining assetprices. Since declining market values wouldquickly affect capital positions, banks mightcurtail lending to increase capital-asset ratios.It is also conceivable that if MVA increases thevolatility of reported net worth it may alsoincrease the volatility of credit availability.Due to the growth of commercial paper andother types of direct corporate borrowing, theborrowers that would be most adversely affect-ed by increased credit rationing would be thosewho do not have direct access to capital mar-kets, such as small businesses. Another issue iswhether the optimal capital-asset ratio willincrease under MVA. If reported earningsunder MVA were more volatile and regulatorsand creditors based their actions on these new

FEDERAL RESERVE RANK OF CHICAGO

27

earnings estimates, a bank would increase itsequilibrium capital ratio and reduce hedgeablerisk in order to reassure its customers that itcould withstand shocks that reduced its networth. This behavioral change could mitigatethe need to restrict credit availability whenmarket values are falling, and it may also im-prove safety and soundness.

Alternatives to market valueaccounting

Acknowledging some of the criticisms offull MVA, some have argued that most of theadvantages of MVA can be obtained by modi-fying rather than overhauling the current ac-counting framework. One proposal is to requirethe reporting of values for those instruments forwhich secondary market prices exist. Such astep would not be very costly to banks becausemuch of this information is already reported toregulators. Proponents believe that this wouldrepresent an improvement over the currentsystem and would reduce the degree of mea-surement error that currently exists by usingHCA. Opponents disagree, contending thatmany institutions use securities to offset posi-tions taken elsewhere in the balance sheet. Forexample, a bank might decide to purchase somelong term Treasury securities to offset longterm certificates of deposit. Marking one andnot the other to market would reduce the effec-tiveness of such a hedging position. Moreover,the difficulty of measuring the duration of coredeposits implies that it may be not be easy todetermine whether some banks have positive ornegative gaps (a gap is the difference betweenthe market value of assets and the market valueof liabilities of equal times to repricing or re-payment). In this case, it becomes unclearwhether an increase in interest rates will reducethe market value of net worth. Thus, onlymarking a portion of the balance sheet to mar-ket for changes in interest rates would distort itsmeaning and lead to greater confusion aboutbank net worth, according to MVA opponents.Note that this argument would not hold forcredit risk since it is difficult to hedge againstcredit risk.

Another proposal is to require banks todisclose more information about the perfor-mance of their portfolios in their financial re-ports but not necessarily mark their portfoliosto market. An advantage of disclosure is that itavoids many of the measurement problems

discussed earlier because it would be up to theusers of financial data to determine the effect ofthe additional disclosures on the market value ofnet worth. As a result, the cost of auditing thebank would be less than it would be under fullMVA. Another advantage of disclosure is thatinvestors, depositors, and bank regulators coulduse the information to make decisions. Investorscould respond to disclosure of negative informa-tion by selling a bank's securities, thereby impos-ing greater market discipline on banks.

Disclosure of market value informationwould be a useful transitional step toward fullMVA, because it would give market participantsand regulatory bodies time to assess the useful-ness of market value information and its likelyeconomic effects. The Financial AccountingStandards Board (FASB) appears to agree. State-ment No. 105 requires additional disclosure infinancial statements with off balance sheet riskof accounting loss. It also requires greater dis-closure of "... all significant concentrations ofcredit risk of all financial instruments, whetherfrom an individual counterparty or groups ofcounterparties." A concentration of credit riskexists when the parties have common economiccharacteristics, such as operating in similar in-dustries or locations, which would cause theirability to meet contractual obligations to besimilarly affected by changes in these characteris-tics. For more details, see FASB (1990) andCarlson and Mooney (1991).

A recent statement, FASB (1991), goes evenfurther. It requires that all entities disclose infor-mation about the market value of all financialinstruments, both assets and liabilities on and offthe balance sheet, for which it is practical to doso. For instruments for which it is impractical toestimate market value, the statement requiresdescriptive information that would assist users inestimating market values. The proposed date ofimplementation is for financial statements issuedfor fiscal years ending after December 15, 1992,for entities with $150 million or more in totalassets. For those entities with less than $150million in total assets, the effective starting datewould be three years later.

Conclusion

The savings and loan crisis has focused at-tention on the accounting system used by finan-cial institutions. Many economists and otherresearchers believe that the current system ofaccounting presents a misleading picture of the

28

ECONOMIC l'ElSPECTI

true economic value of commercial banks.They contend this is both raising the cost ofcapital for banks and placing the deposit insur-ance fund at greater risk. Market value ac-counting has been proposed as a better way tomeasure the economic value of banks. Howev-er, MVA has conceptual and measurementdifficulties which need to be addressed. Manyof these problems can be mitigated, but it mustbe recognized that no system of accounting caneliminate the use of judgment in valuations.

Until this debate is resolved, there is still aneed for better information to protect the depos-it insurance fund and ultimately taxpayers fromexcessive risk taking by banks with low marketvalues. Because managers of banks may notwant to voluntarily improve the quality of in-formation submitted to both regulators and thepublic, banks should be required to report theexpected future cash flows (repayment of prin-cipal and interest) on their fixed rate loans andtime deposits as a function of the time whenrepayment is made. Currently, banks are onlyrequired to report the value of assets and liabili-ties which fall into different time periods, asshown in Table 2. To compute present values,one needs the expected future cash flows as afunction of time, not what is currently reported.

Disclosing this information would greatly assistregulators in examining interest rate risk ofcommercial banks. Second, banks should nothave as much discretion to choose the time torealize gains or losses as they currently do. Inparticular, accounting rules for reporting nonper-forming loans and for increasing loan loss re-serves need to be strengthened, and changes incredit risk must be reported sooner to regulators.Third, deposits held in foreign offices should bereported in the same detail as domestic deposits.Finally, greater public disclosure is necessary toenable investors to estimate bank net worth moreaccurately. If investors are more accuratelyinformed, market prices of bank stocks andsubordinated debentures would better reflect theeconomic condition of commercial banks.Healthy banks would benefit as reduced uncer-tainty would raise their stock prices and lowertheir cost of capital. Less well-capitalized bankswould be subject to greater market disciplineand thus have a stronger incentive to improvetheir net worth positions. In the absence ofrequiring market value accounting, I believethese changes would improve the ability of regu-lators and investors to monitor the safety andsoundness of the banking system and to measurebank performance.

FOOTNOTES

'See U.S. Treasury (1991), p. XI-3.

2Benston (1989), p. 549.

3The total value of bank assets which involve truly propri-etary information may be overstated. For example, manybusiness loans are made by groups of banks in whichinformation is shared. Currently, there are approximately$800 billion outstanding in the shared national creditsprogram.

4Insurance companies must also report a breakdown oftheir bond holdings by six quality classes. By contrast,commercial banks only report the aggregate amount ofsecurities for different types (U.S. government, state andlocal government, corporate, foreign, etc.). They do notreport which corporations' securities they are holding nordo they classify their bonds by credit quality.

5There are some exceptions. For example, banks reporttheir securities holdings at par value less amortization ofdiscount or plus accretion of premium. Other exceptionsare discussed in greater detail in the measurement issuessection.

6An example of such behavior was Citicorp's decision toincrease reserves against its Latin American debt by $3.4

billion in the second quarter of 1989. Many large banksfollowed Citicorp's lead with substantial increases in theirown loan loss reserves.

71t is also worth noting that since savings and loan (S&L)associations had over three-quarters of their assets investedin mortgage loans and mortgage-backed securities, the rapidincrease in market interest rates from 1978 to 1981 had aneven larger negative impact on S&L net worth than it did oncommercial banks. It is in part because of this experiencethat the Office of Thrift Supervision has developed a MarketValue Model for adjusting the values of S&L portfolios forchanges in market interest rates.

8 Even if stock prices did accurately reflect unrealized gainsor losses, the holders of debt contracts with covenants con-tingent on accounting values may be arbitrarily penalized.

9Since deposit insurance can be viewed as a call option, amarket value insolvent bank still open for business canincrease its risk exposure and thus the value of its depositinsurance. Since this option is capitalized into the price ofthe bank's stock, such an action can actually raise thestock's value.

"'Even though market price information may be available forall these financial instruments, one must interpret these data

FEDERAL RESERVE BANK OF CHICAGO 29

carefully because of the varying liquidity of the markets in

which these instruments trade. For example, the municipal

bond market is very heterogeneous, so one might simulta-

neously receive different price quotations from dealers. A

bank could use the highest or lowest price quote depending

on whether it is trying to overstate or understate the market

value of its net worth.

"'Requiring banks to carry these assets at lower of cost or

market value (LOCOM) reduces the likelihood that a bank

could use an overestimated appraisal of its real estate

holdings to increase its net worth. On the other hand,

reporting real estate using LOCOM makes it more difficult

for a bank to realize gains on real estate that may have

appreciated in value. In any case, these two asset catego-

ries represent less than three percent of total bank assets.

12 It is possible to get market prices for mortgage loans that

conform to the standards set by the Federal Home Loan

Mortgage Corporation (FHLMC) and the Federal National

Mortgage Association (FNMA). However, it is not possible

to get detailed pricing information for nonconforming

mortgage loans, and there are problems with using FHLMC

and FNMA prices. For more information, see U.S. Trea-

sury (1991), pp. XI-14 and XI-15. In addition to mortgage

loans, there are active secondary markets in loans to less

developed countries (LDCs) and loans for highly leveraged

transactions (HLT). The shared national credit program

can be a source of market value information. Also, market

values of collateral for some loans may be readily avail-

able, such as loans secured by farmland.

"Duration is a measure of the effective maturity of a stream

of future payments, defined as the weighted average matu-

rity of an instrument's future cash flows, with the present

values of the cash flows serving as the weights. A change

in the market interest rate can affect the duration of a loan.

For example, a decrease in market interest rates may induce

borrowers to refinance a loan or pay it off sooner, thereby

altering the duration of the loan.

141n practice, matrix pricing can be used to reduce the

degree of subjectivity involved in determining the risk

premia of discount factors employed in the analysis [see

U.S. Treasury (1991) for more details]. In addition, audi-

tors provide a check on a bank's use of its information

advantage. For a detailed discussion of the incentive

problem inherent in a bank valuing its loan portfolio, see

Berger, King, and O'Brien (1991). These authors stress the

importance of developing some incentive compatible

mechanism for getting banks to report truthfully the market

values of their loans.

15 The category "other assets" in Table 1 includes: (1)

investments in unconsolidated subsidiaries and associated

companies, (2) customers' liability to this bank on accep-

tances outstanding, (3) intangible assets, which includes

loan servicing rights and goodwill, and (4) other assets such

as income earned but not collected on loans, net deferred

income taxes, and miscellaneous items. Investments in

unconsolidated subsidiaries are currently reported to

regulators using the equity method of accounting, where

the asset is carried at cost and adjusted for earnings and

losses of the investee.

16 Another intangible asset is goodwill, which arises in

connection with merger and acquisitions transactions for

which the purchase price exceeds the fair value of the

identifiable net assets that are acquired. Calculating the

market value of goodwill is difficult in any accounting

system. One suggestion, contained in U.S. Treasury

(1991), is "because of the subjective nature of the deter-

mination, goodwill under MVA might be handled in much

the same way as under current GAAP; that is, goodwill

would be recognized only if acquired through arms-length

transactions, and its historical cost would be amortized over

some appropriate period of time."

' 7For details, see U.S. Treasury (1991), pp. XI-18-X1-19.

18The total return on demand deposits and NOW accounts

equals the sum of explicit plus implicit interest. Placing

noninterest-bearing demand deposit balances with banks

represents partial compensation for services provided to the

depositor. For corporations and depository institutions with

a correspondent relationship, the size of these compensat-

ing balances is adjusted for changes in market interest rates.

°The current risk-based capital guidelines do require banks

to hold additional capital based on the extent of their off

balance sheet exposure.

20Examples are for mandatory accounting changes in the oil

and gas industry [Collins, et. al. (1981)], consolidated

reporting requirements [Mian and Smith (1990)], and

translation of foreign currency transactions [Salatka

(1989)]. The effects of regulatory accounting changes in

the savings and loan industry has been studied by Blacco-

niere (1991).

REFERENCES

American Bankers Association, Market ValueAccounting, June 1990, monograph.

Benston, George J., "Market value accounting:Benefits, costs, and incentives," Proceedings ofa Conference on Bank Structure and Competi-tion, Federal Reserve Bank of Chicago, 1989,pp. 547-563.

Berger, Alien N., Kathleen K. King, andJames M. O'Brien, "The limitations of marketvalue accounting and a more realistic alterna-tive," Journal of Banking and Finance, Sep-tember 1991, pp. 753-783.

Blacconiere, Walter G., "Market reactions toaccounting regulations in the savings and loan

30 El:41141111C PIAISPECTIN ES

tion, Federal Reserve Bank of Chicago, 1991,pp. 534-550.

industry," Journal of Accounting and Econom-ics, March 1991, pp. 91-113.

Carlson, Ronald E., and Kate Mooney, "Im-plications of FASB Statement No. 105," Jour-nal of Accountancy, March 1991, pp. 54-58.

Collins, Daniel W., Michael S. Rozeff, andDan S. Dhaliwal, "The economic determinantsof the market reaction to proposed mandatoryaccounting changes in the oil and gas industry,"Journal of Accounting and Economics, March1981, pp. 37-71.

Financial Accounting Standards Board, "Dis-closures of information about financial instru-ments with off-balance-sheet risk and financialinstruments with concentrations of credit risk,"Statement No. 105, reprinted in Journal ofAccountancy, December, 1990, pp. 140-156.

"Disclosures about fair value of financial in-struments," Statement No. 107, 1991.

Houpt, James V., and James A. Ebersit, "Amethod for evaluating interest rate risk in U.S.commercial banks," Federal Reserve Bulletin,August 1991, pp. 625-637.

Jones, Jonathan, Robert Nachtmann, andFred Phillips-Patrick, "Market value account-ing and bank income volatility: Some evidencefrom the investment account," Proceedings of aConference on Bank Structure and Competi-

Mengle, David L., "Market value accountingand the bank balance sheet," ContemporaryPolicy Issues, April 1990, pp. 82-94.

Mengle, David L., and John R. Walter, "Howmarket value accounting would affect banks,"Proceedings of a Conference on Bank Structureand Competition, Federal Reserve Bank ofChicago, 1991, pp. 511-533.

Mian, Shehzad L., and Clifford W. Smith,"Incentives associated with changes in consoli-dated reporting requirements," Journal ofAccounting and Economics, July 1990, pp.249-266.

Mondschean, Thomas H., "Market values ofmortgage loans at large commercial banks—estimates and applications," DePaul University,unpublished manuscript, March 1990.

Office of Thrift Supervision, The OTS MarketValue Model, instruction manual, 1990.

Salatka, William K., "The impact of SFASNo. 8 on equity prices of early and late adopt-ing firms," Journal of Accounting and Econom-ics, February 1989, pp. 35-69.

U.S. Treasury, Modernizing the FinancialSystem: Recommendations for Safer, MoreCompetitive Banks, February 1991.

FEDERAL RESERVE RANK OF CHICAGO 31