Embed Size (px)

Citation preview

MS 3255

BUSINESS TAXATION

CAPITAL ALLOWANCES: PLANT AND

MACHINERY

Table of content

i. Definition of Capital Allowances and Plant & Machinery

ii. Annual Investment Allowance (AIA)iii. First Year Allowance (FYA)iv. Writing down Allowance (WDA)v. Capital Allowance for Motorcarsvi. Sales of Plant and Machineryvii. Impact of private use of asset on capital

allowanceviii. Recognize treatments of short-life assetsix. Treatments of assets included in the special

pool rate

Capital Allowances In General Purpose?

To provide a business tax relief for capital expenditure

Deducted as a trading expense in calculating the tax-adjusted trading income.

Calculated for a trader’s period of account.

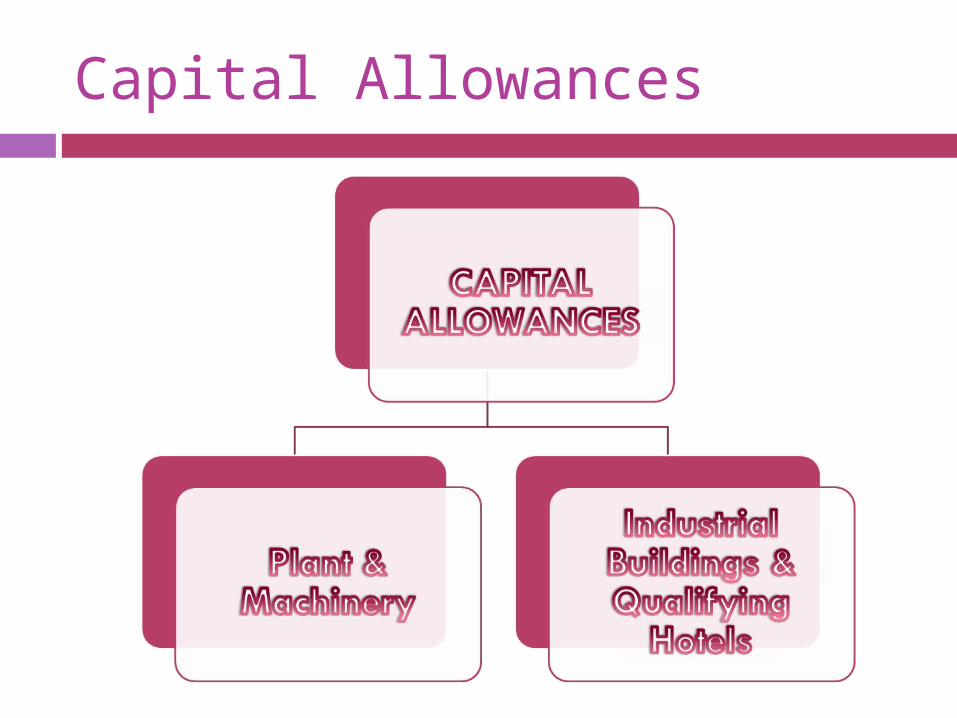

Capital Allowances

Definition Of Plant and Machinery

Machinery has a commonly understood meaning

Plant is not so clearly defined. Thus, HMRC codified some rules to specifically deem certain types of expenditure as plant and machinery.

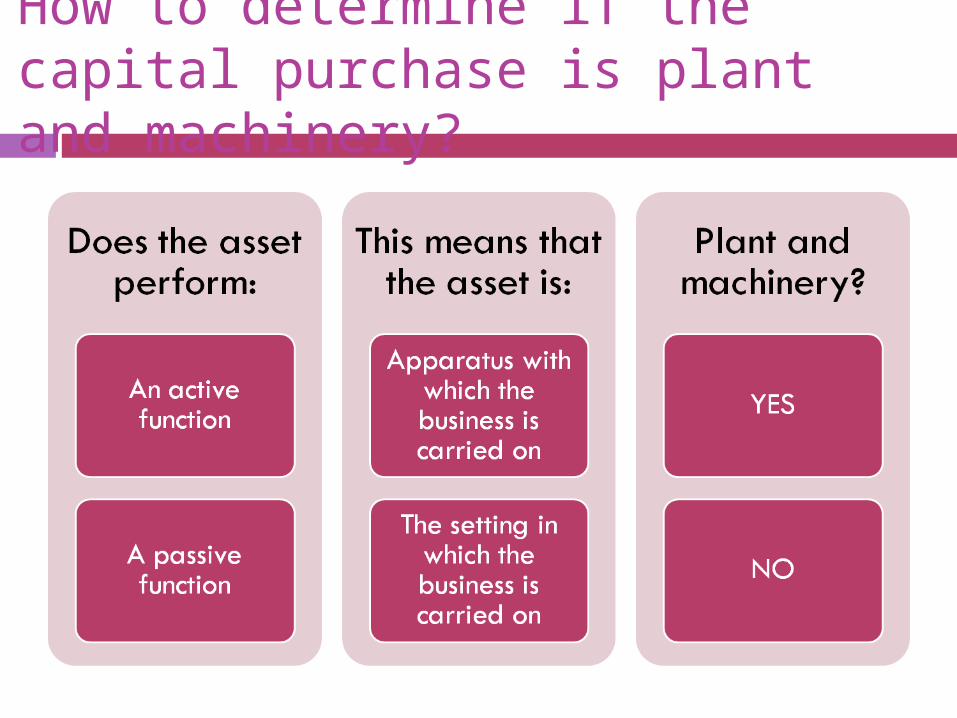

How to determine if the capital purchase is plant and machinery?

However…

Certain types of expenditure not thought to be plant BUT are TREATED as plant by specific legislation. For example,

1. Capital expenditure incurred in complying with fire regulations

2. The cost of alterations to buildings needed for the installation of plant

3. Expenditure on acquiring computer software

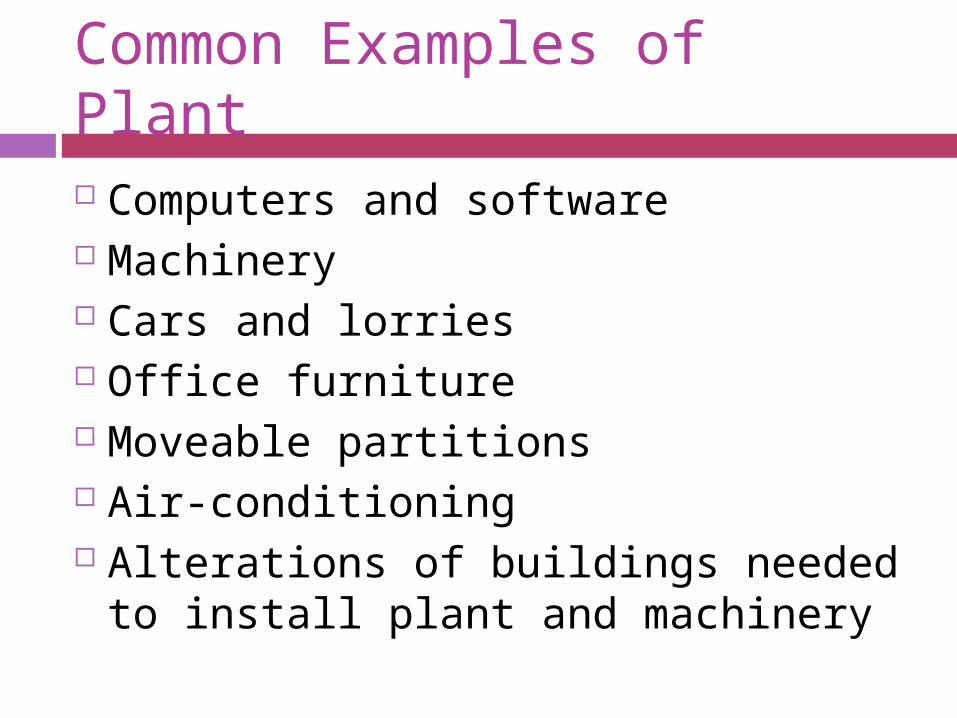

Common Examples of Plant

Computers and software Machinery Cars and lorries Office furniture Moveable partitions Air-conditioning Alterations of buildings needed to

install plant and machinery

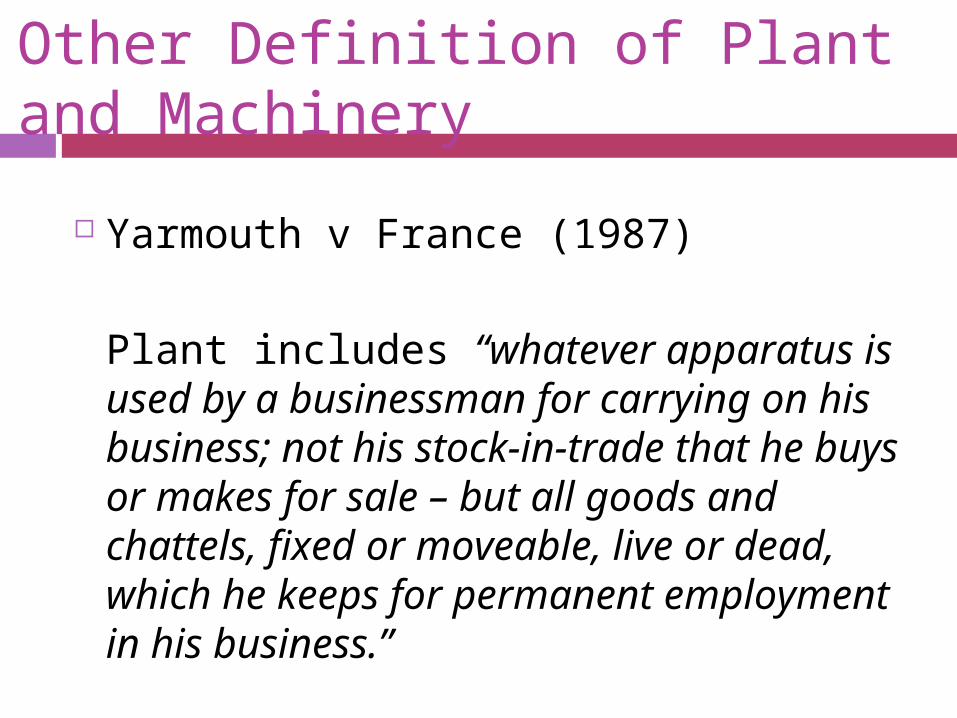

Other Definition of Plant and Machinery

Yarmouth v France (1987)

Plant includes “whatever apparatus is used by a businessman for carrying on his business; not his stock-in-trade that he buys or makes for sale – but all goods and chattels, fixed or moveable, live or dead, which he keeps for permanent employment in his business.”

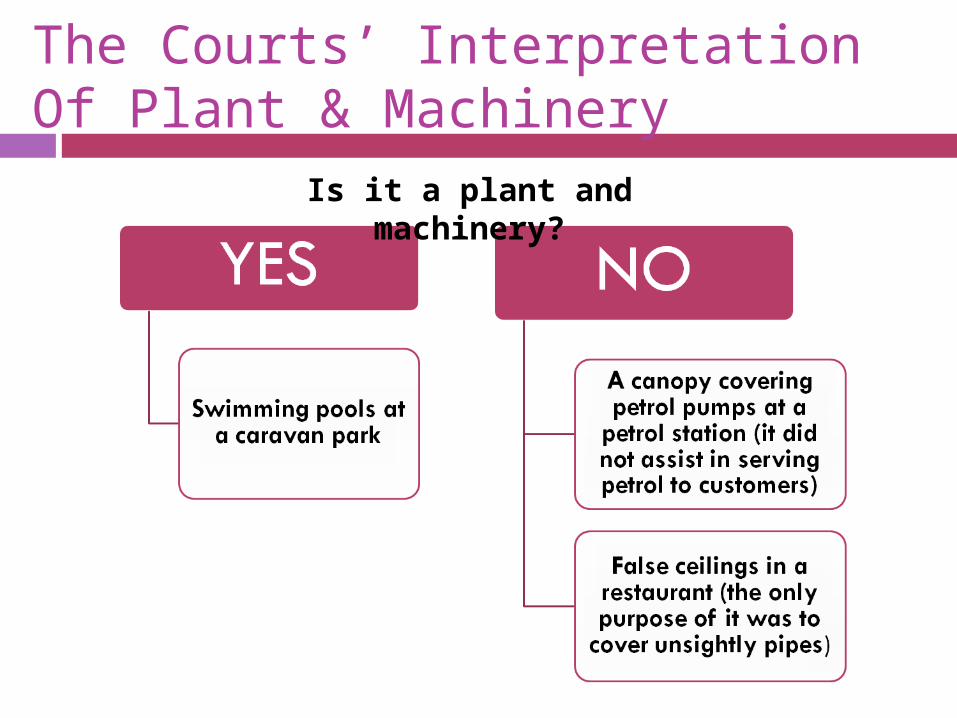

The Courts’ Interpretation Of Plant & Machinery

Is it a plant and machinery?

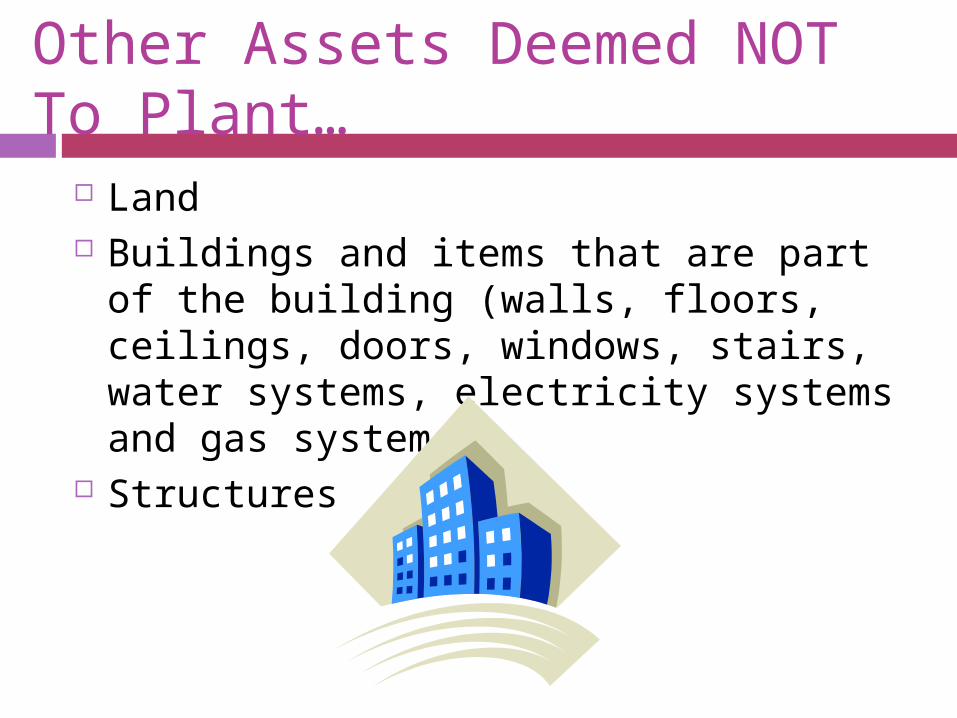

Other Assets Deemed NOT To Plant…

Land Buildings and items that are part of the

building (walls, floors, ceilings, doors, windows, stairs, water systems, electricity systems and gas systems)

Structures

Items within the definition of a building but can still qualify as plant

Electrical, cold water and gas systems provided to meet the particular requirements of the trade.

Water heating systems, systems of water ventilation and air cooling, and any ceiling and floor comprised in such systems.

Manufacturing/processing equipment, storage equipment, display equipment, counters, checkouts.

Items within the definition of a building but can still qualify as plant

Cookers, washing machines, dishwashers, refrigerators

Wash basins, sinks, baths, showers, sanitary ware Furniture and furnishings Lifts, escalators, moving walkways Sprinkler equipment and fire alarm systems Movable partition walls Decorative assets provided in a hotel, restaurant

or similar trade Advertising hoardings, signs and similar displays

What is Annual Investment Allowance?

Annual Investment Allowance (AIA) is a 100% allowance for the first £50,000 of expenditure incurred by a business on plant and machinery (Taxation FA09, ACCA).

AIA is an amount you can write off against taxable profits for purchases of qualifying plant and equipment.

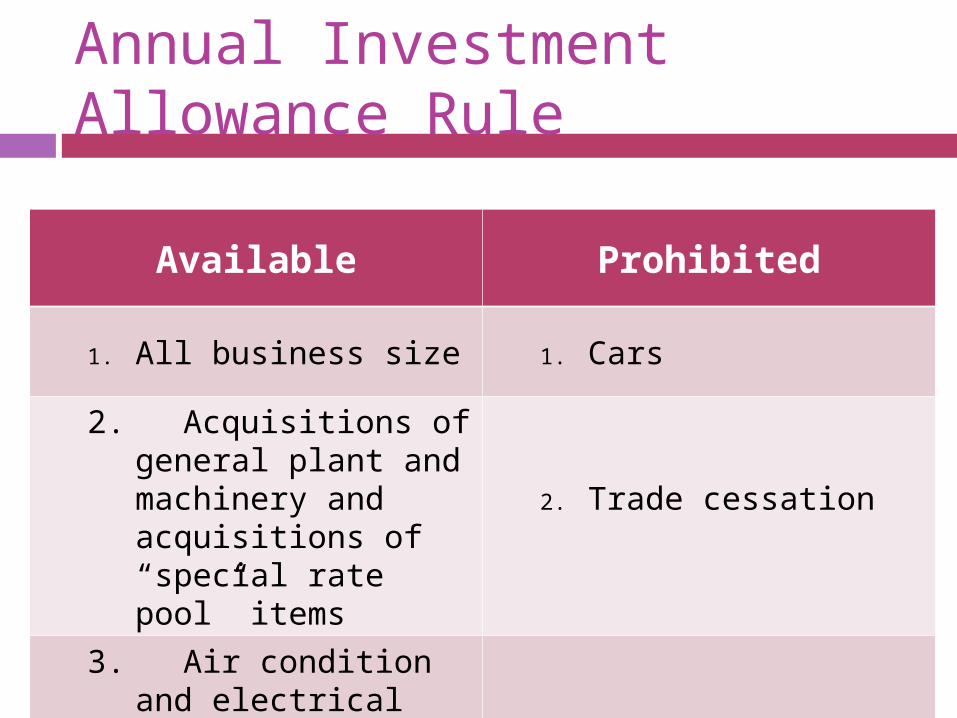

Annual Investment Allowance Rule

Available Prohibited1. All business size 1. Cars

2. Acquisitions of general plant and machinery and acquisitions of “special rate pool” items

2. Trade cessation

3. Air condition and electrical systems

Annual Investment Allowance Rule

In each accounting period of 12 months, it is limited to a maximum of £50,000 expenditure incurred.

The £50,000 allowance is prorated for

long and short accounting periods.

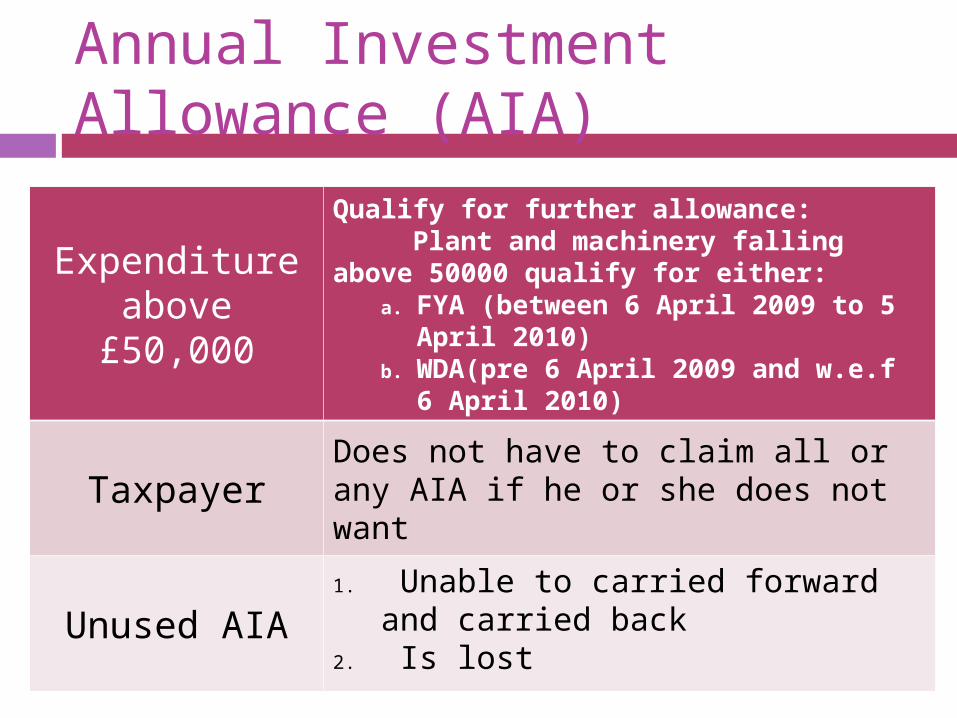

Annual Investment Allowance (AIA)

Expenditure above

£50,000

Qualify for further allowance: Plant and machinery falling above 50000 qualify for either:

a. FYA (between 6 April 2009 to 5 April 2010)

b. WDA(pre 6 April 2009 and w.e.f 6 April 2010)

Taxpayer Does not have to claim all or any AIA if he or she does not want

Unused AIA1. Unable to carried forward and

carried back2. Is lost

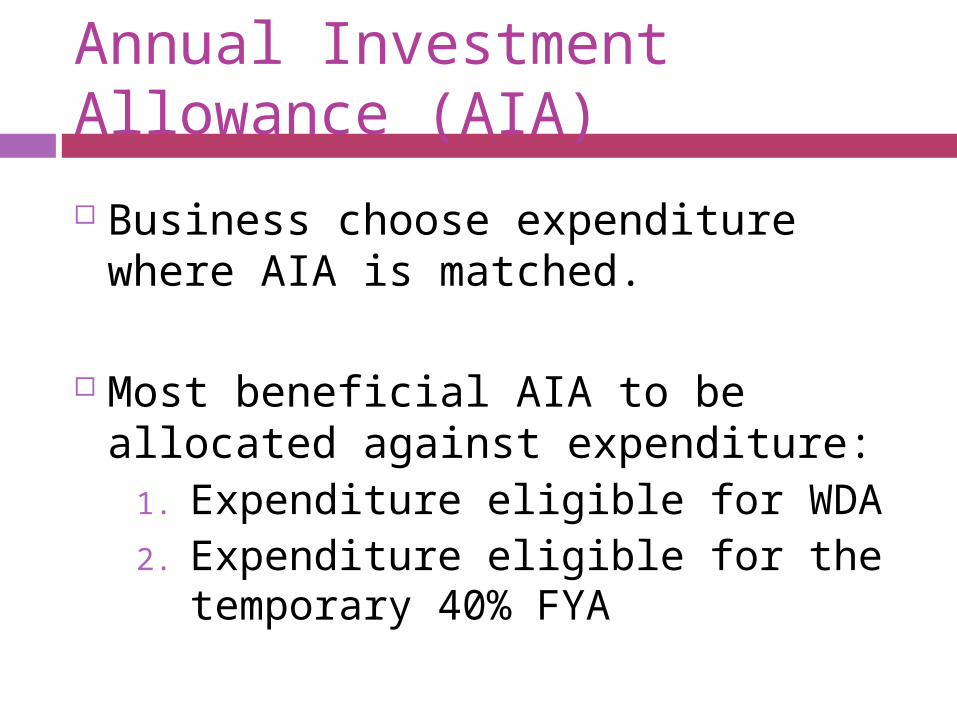

Annual Investment Allowance (AIA)

Business choose expenditure where AIA is matched.

Most beneficial AIA to be allocated against expenditure:

1. Expenditure eligible for WDA2. Expenditure eligible for the

temporary 40% FYA

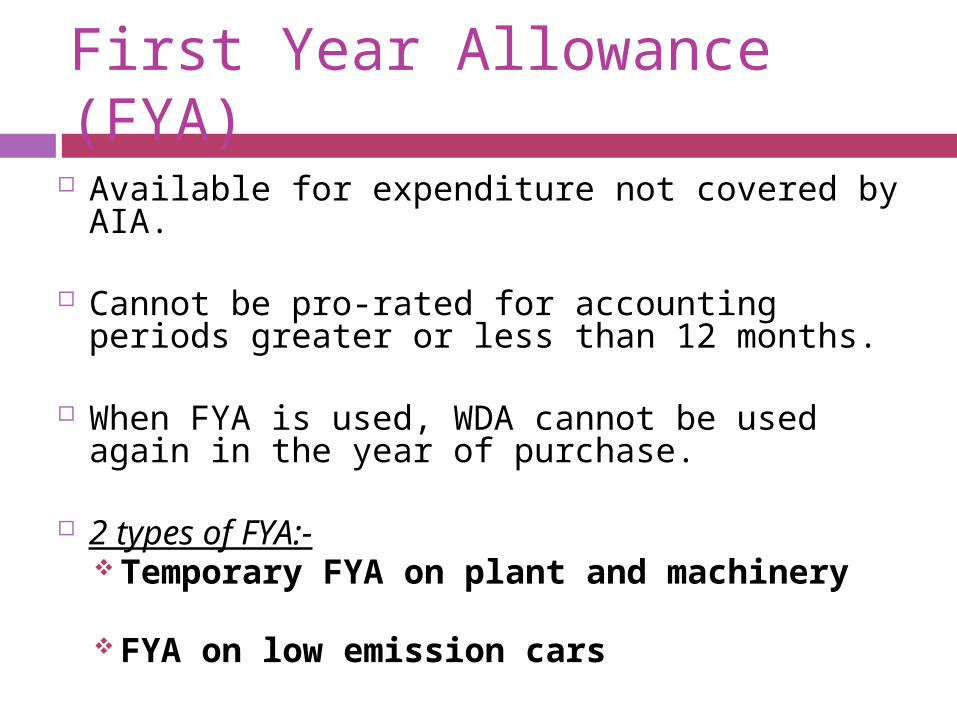

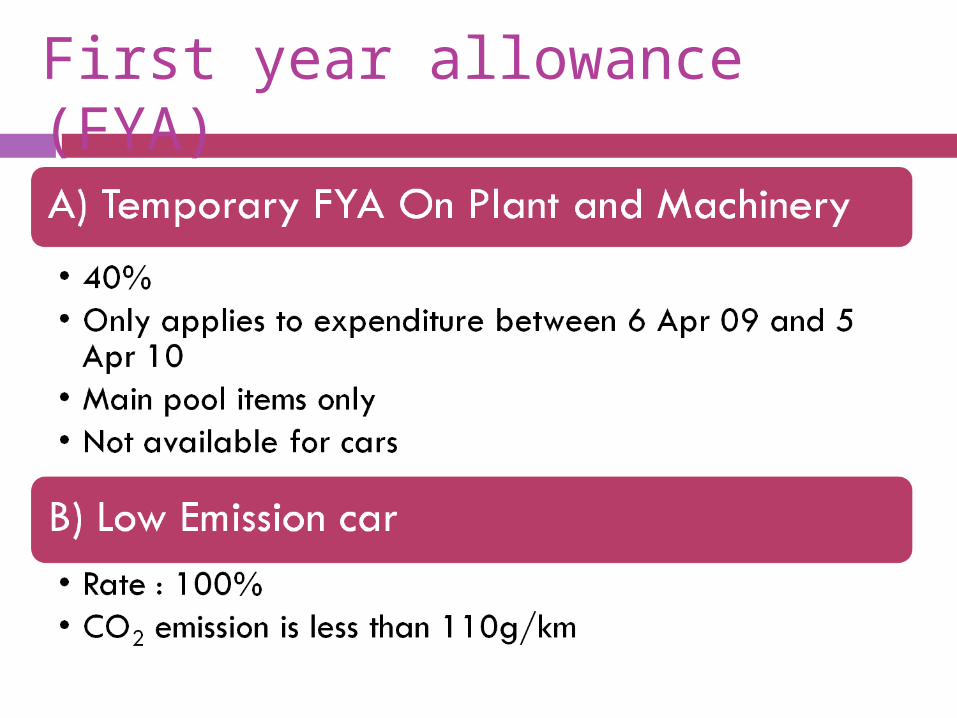

First Year Allowance (FYA)

Available for expenditure not covered by AIA.

Cannot be pro-rated for accounting periods greater or less than 12 months.

When FYA is used, WDA cannot be used again in the year of purchase.

2 types of FYA:-

Temporary FYA on plant and machinery

FYA on low emission cars

First year allowance (FYA)

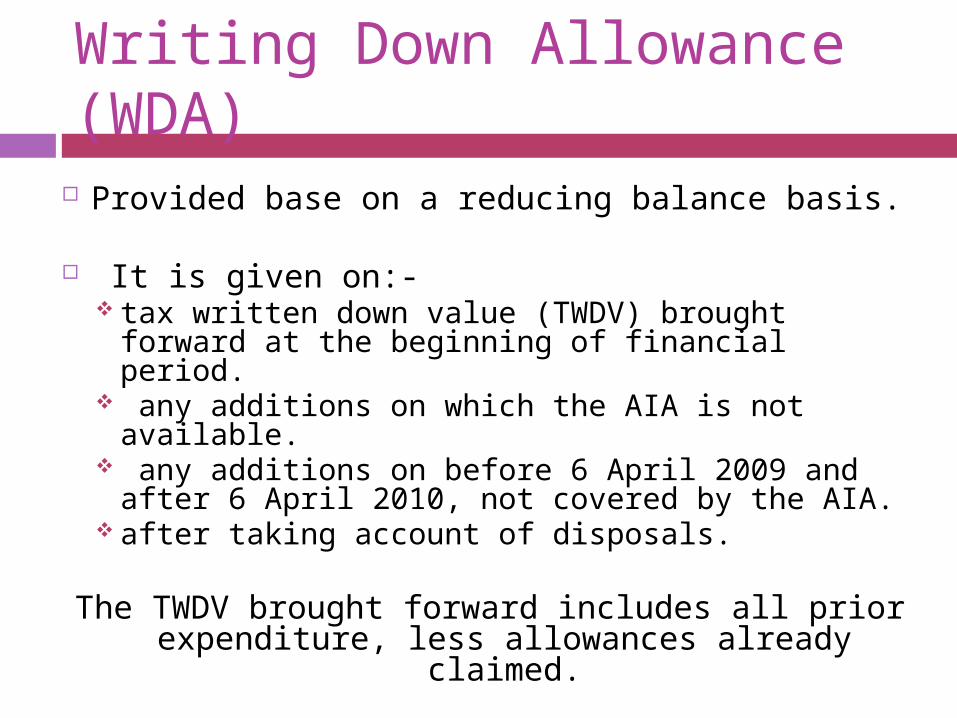

Writing Down Allowance (WDA)

Provided base on a reducing balance basis.

It is given on:- tax written down value (TWDV) brought

forward at the beginning of financial period. any additions on which the AIA is not

available. any additions on before 6 April 2009 and after

6 April 2010, not covered by the AIA. after taking account of disposals.

The TWDV brought forward includes all prior expenditure, less allowances already

claimed.

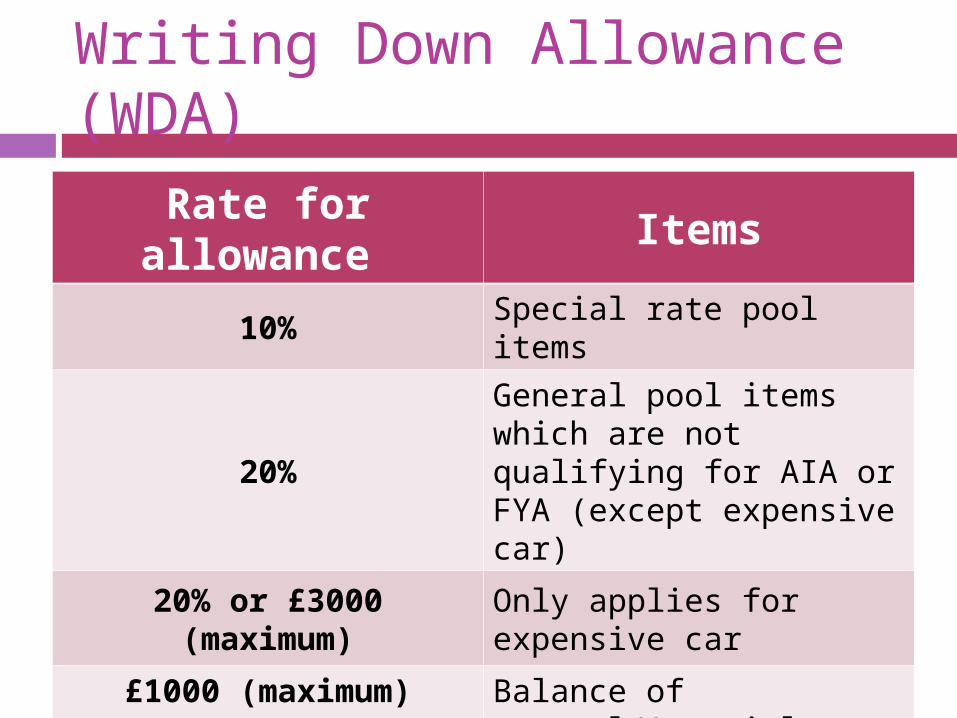

Writing Down Allowance (WDA)

Rate for allowance

Items

10% Special rate pool items

20%

General pool items which are not qualifying for AIA or FYA (except expensive car)

20% or £3000 (maximum)

Only applies for expensive car

£1000 (maximum) Balance of general/’special pool’ items ≤ £1000 before WDA

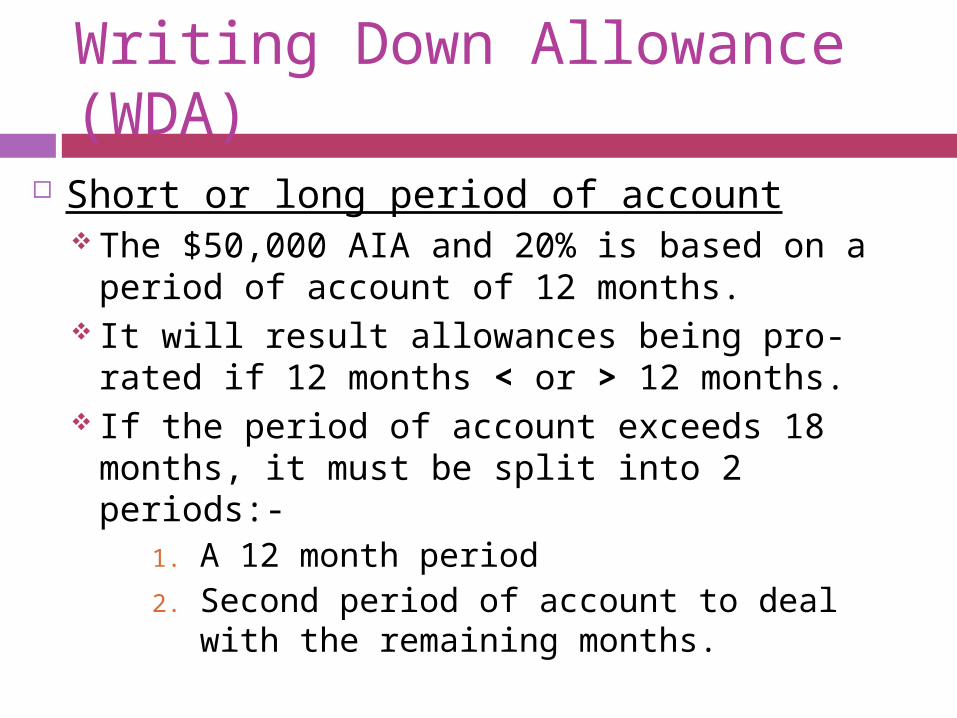

Writing Down Allowance (WDA)

Short or long period of account The $50,000 AIA and 20% is based on a period

of account of 12 months. It will result allowances being pro-rated if 12

months < or > 12 months. If the period of account exceeds 18 months, it

must be split into 2 periods:-1. A 12 month period2. Second period of account to deal with the

remaining months.

Writing Down Allowance (WDA) Length of ownership in the period of

account Never restricted by reference to the length of

ownership of an asset in the period of account. Example:-

If a business prepares accounts for the year ended 31 March 2010, the same WDA is given whether an asset is purchased on 10 April 2009 or on 31 March 2010.

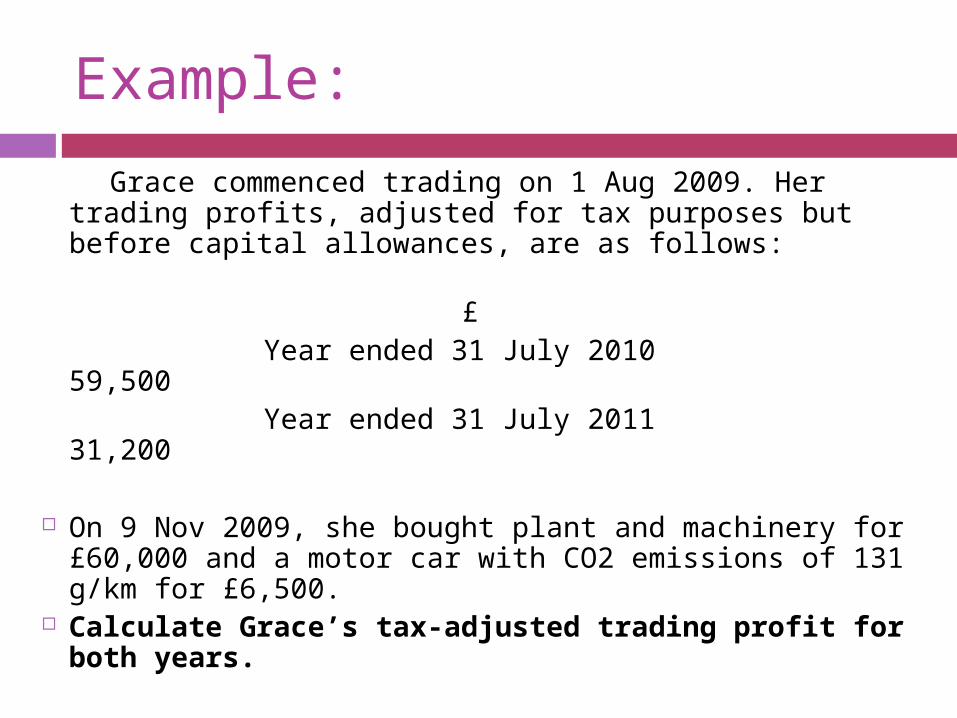

Example:

Grace commenced trading on 1 Aug 2009. Her trading profits, adjusted for tax purposes but before capital allowances, are as follows:

£ Year ended 31 July 2010 59,500 Year ended 31 July 2011 31,200

On 9 Nov 2009, she bought plant and machinery for £60,000 and a motor car with CO2 emissions of 131 g/km for £6,500.

Calculate Grace’s tax-adjusted trading profit for both years.

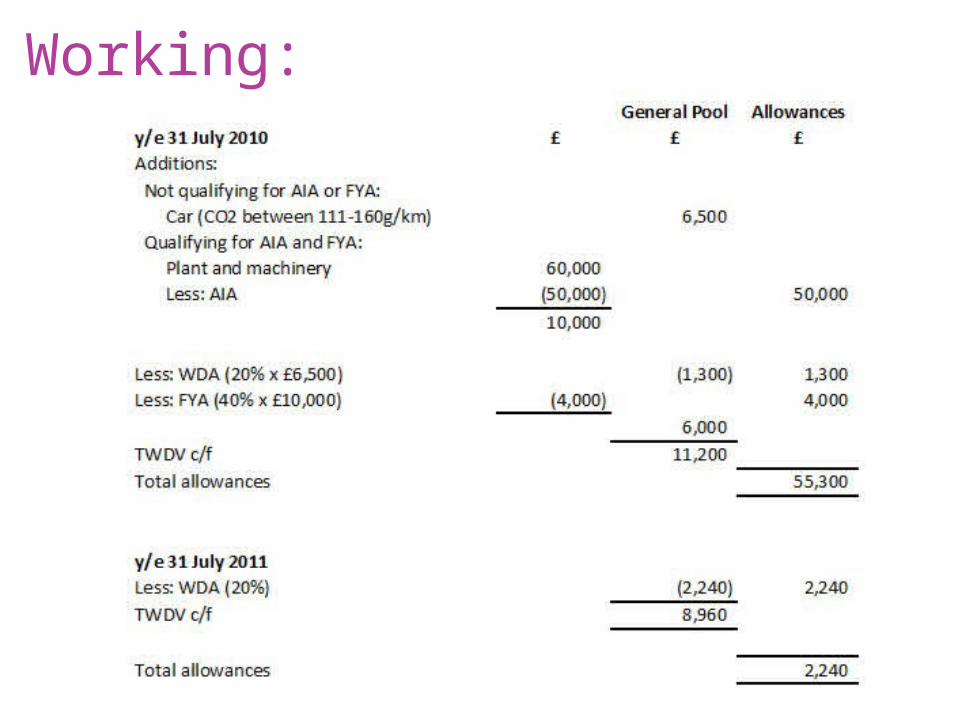

Working:

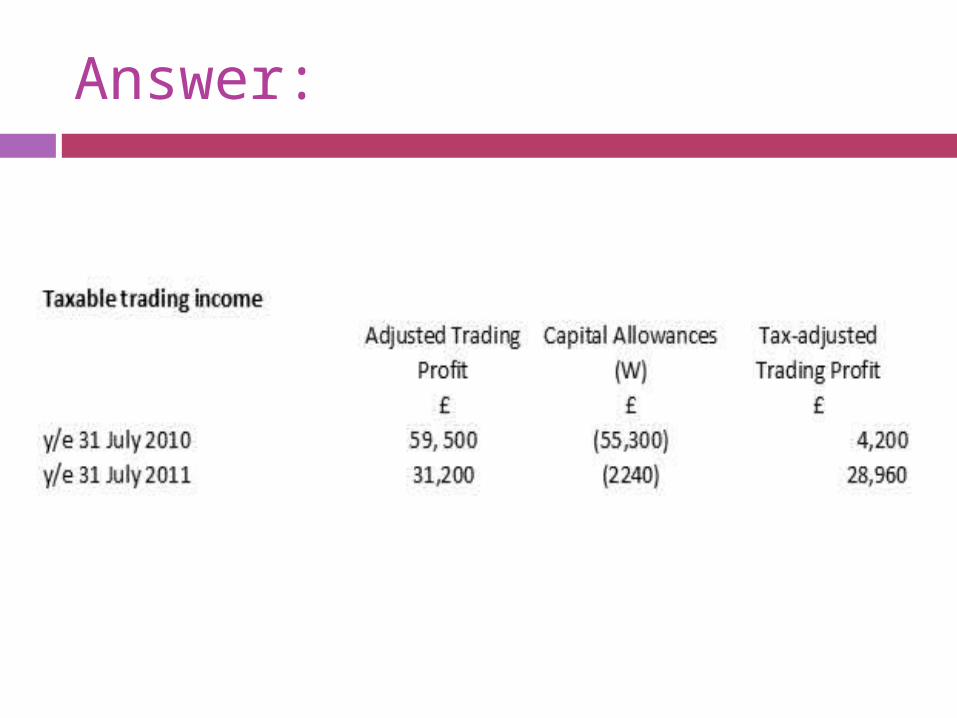

Answer:

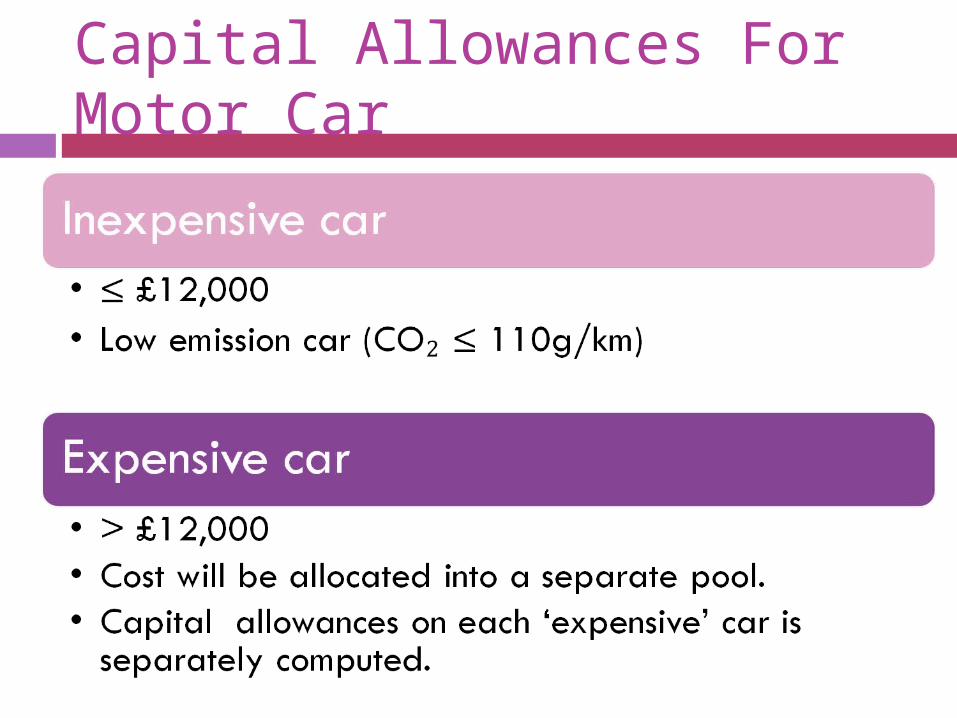

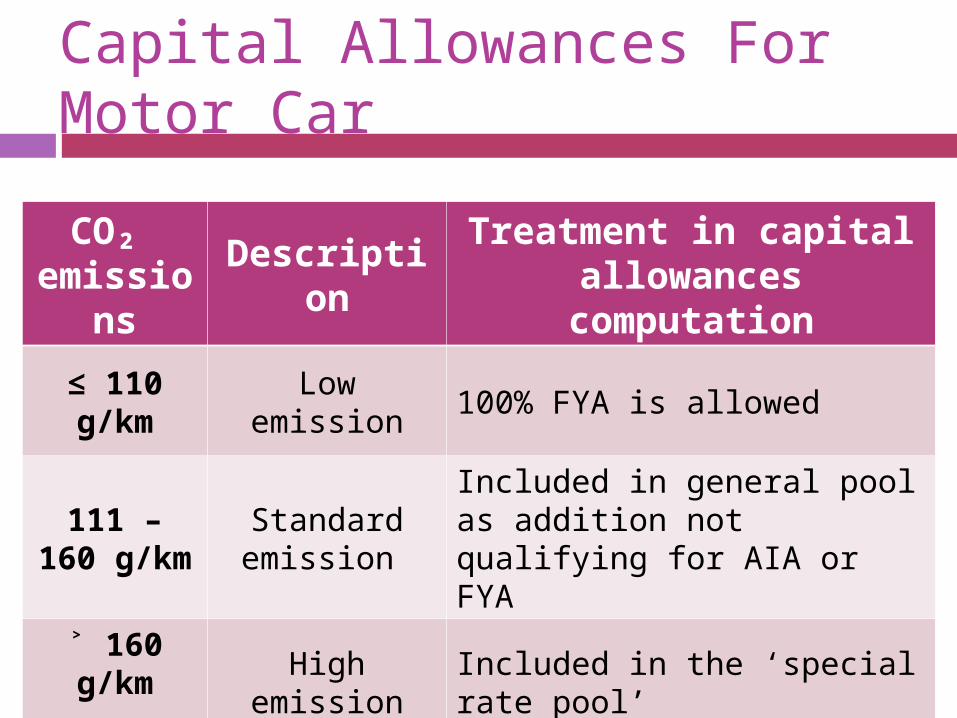

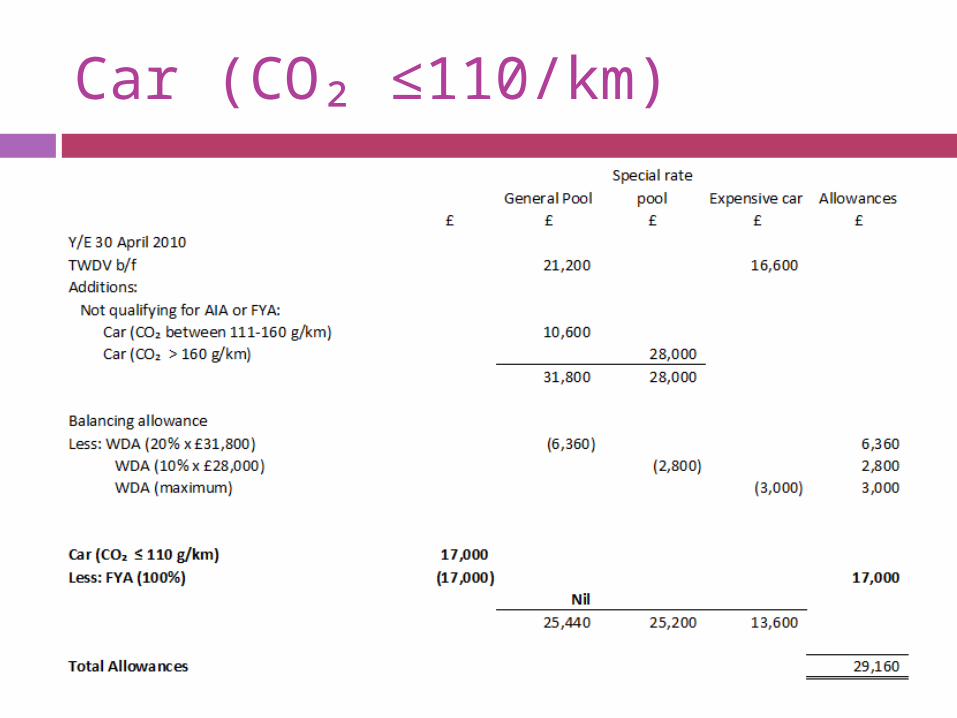

Capital Allowances For Motor Car

Capital Allowances For Motor Car

CO₂ emissio

ns

Description

Treatment in capital allowances

computation≤ 110 g/km

Low emission 100% FYA is allowed

111 – 160

g/km

Standard emission

Included in general pool as addition not qualifying for AIA or FYA

˃ 160 g/km

High emission

Included in the ‘special rate pool’

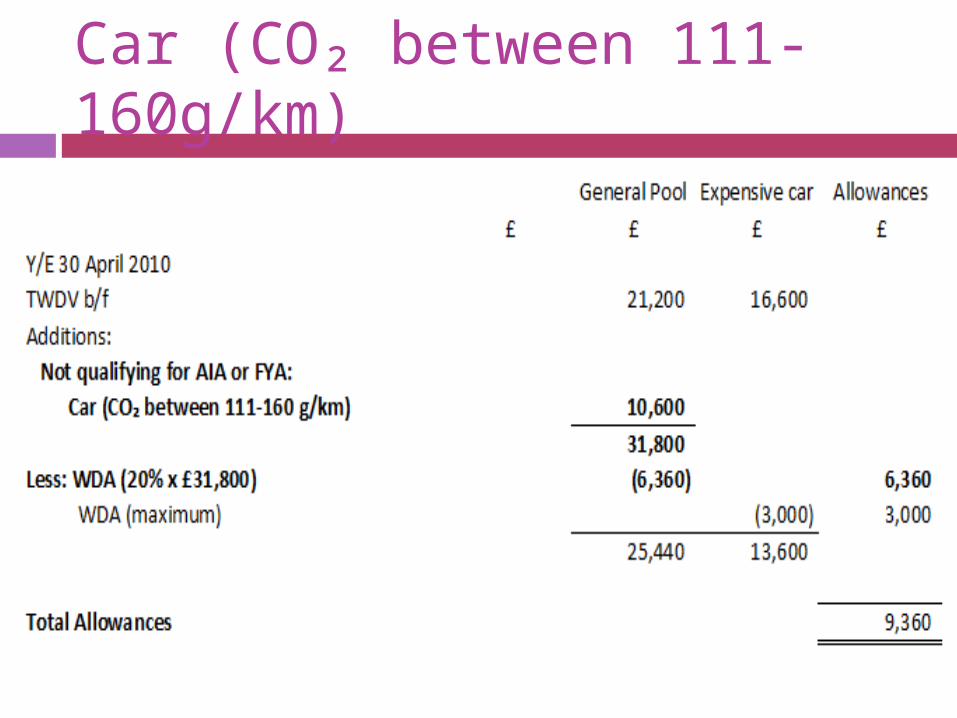

Car (CO₂ between 111-160g/km)

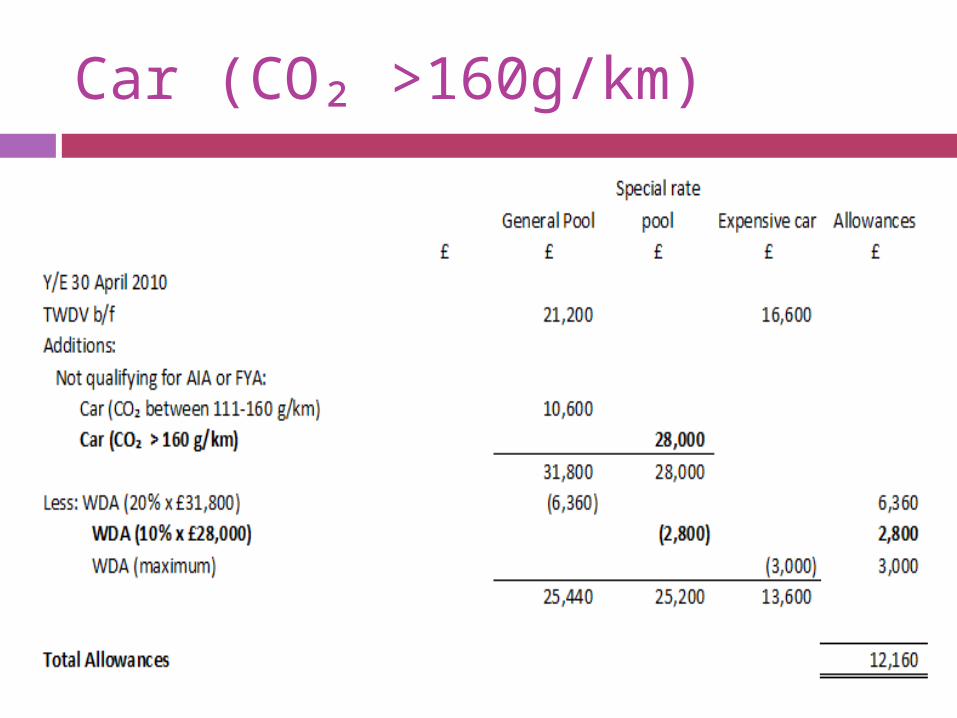

Car (CO₂ >160g/km)

Car (CO₂ ≤110/km)

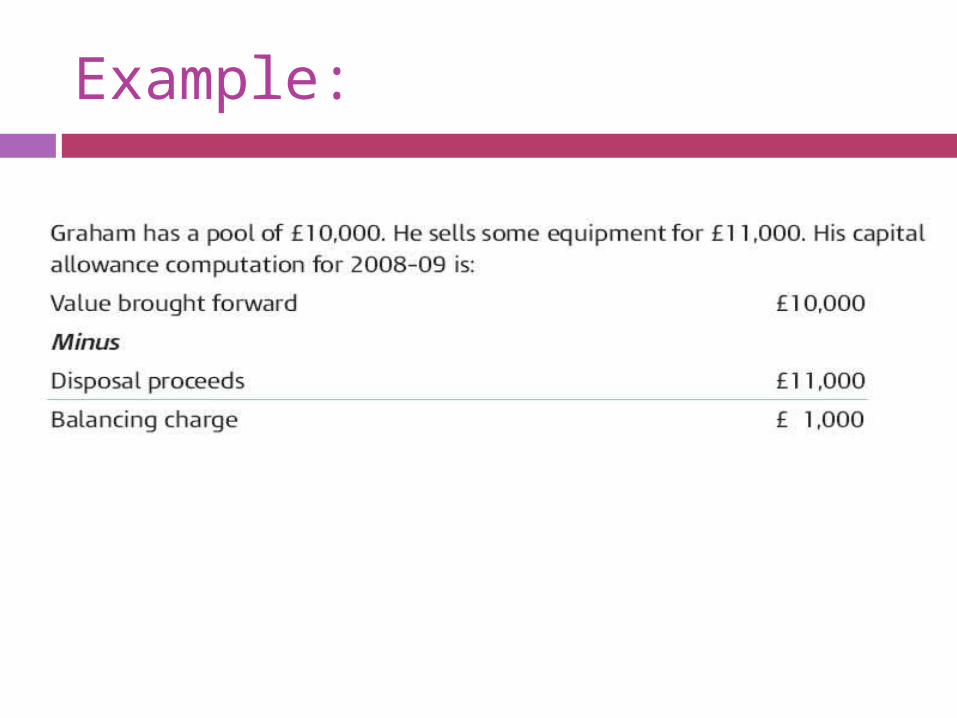

Sale Of Plant And Machinery

Upon the sale of plant and machinery, the following steps are taken before calculating the capital allowances.

The disposal proceeds is deducted from the total of: TWDV brought forward on the pool plus

additions brought into the general pool

Sale Of Plant And Machinery

The WDA for the year is then calculated on the remaining figure, and the temporary FYA is calculated after the WDA is deducted.

However…

o If sale proceeds exceed the original cost of the asset, the sale proceeds deducted from the pool are restricted to the original cost of the asset. An excess of sale proceeds over original cost may then be taxed as a chargeable gain.

o This chargeable gain is known as balancing charge and it will be added to the taxable trading profit.

Example:

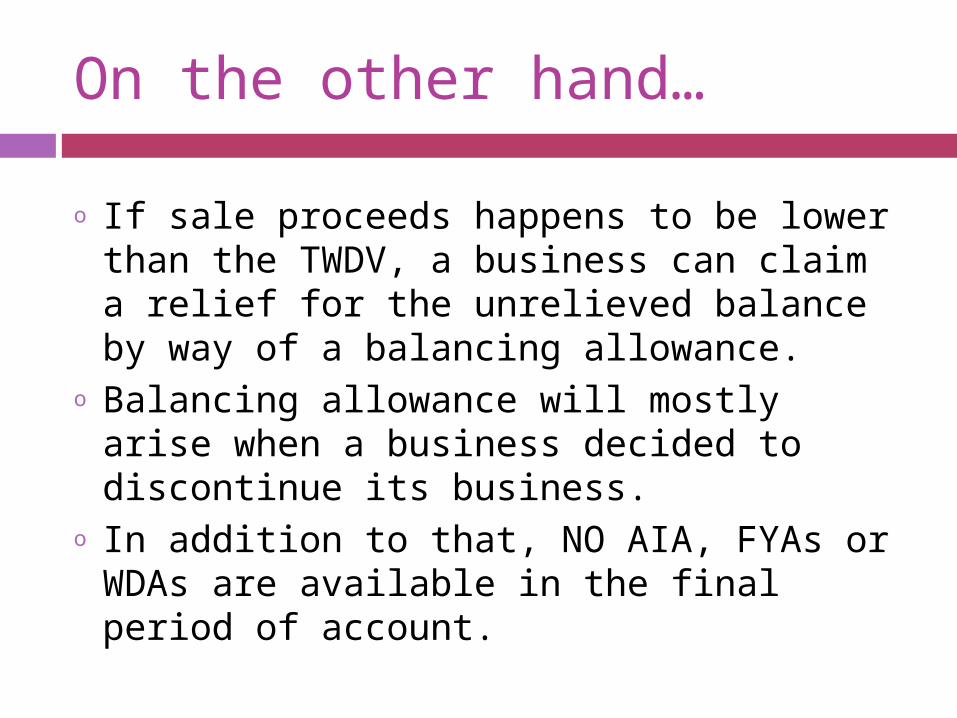

On the other hand…

o If sale proceeds happens to be lower than the TWDV, a business can claim a relief for the unrelieved balance by way of a balancing allowance.

o Balancing allowance will mostly arise when a business decided to discontinue its business.

o In addition to that, NO AIA, FYAs or WDAs are available in the final period of account.

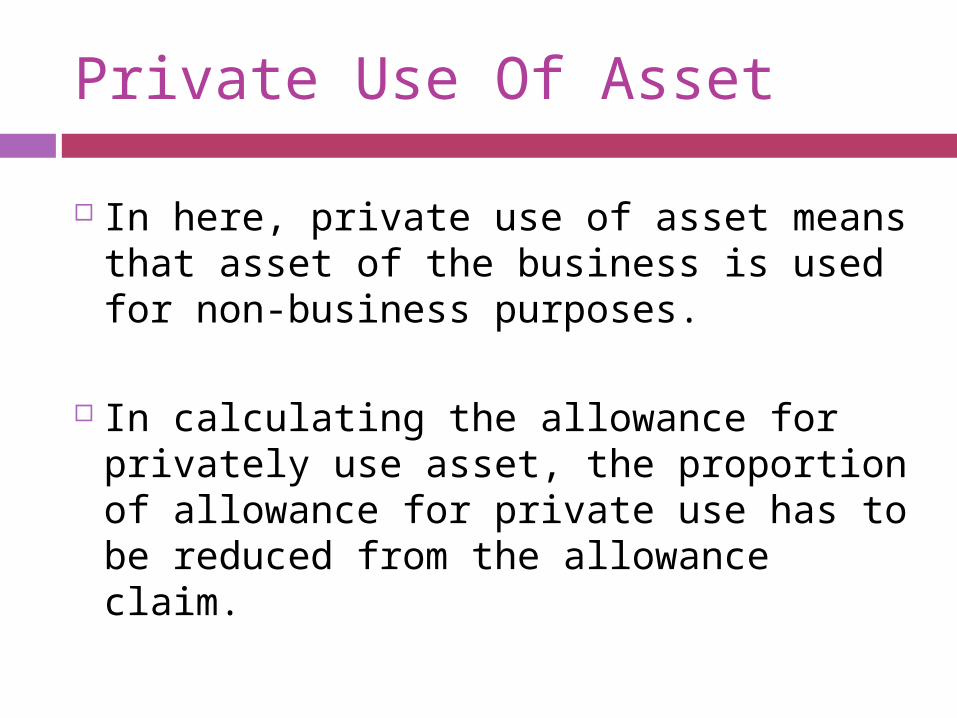

Private Use Of Asset

In here, private use of asset means that asset of the business is used for non-business purposes.

In calculating the allowance for privately use asset, the proportion of allowance for private use has to be reduced from the allowance claim.

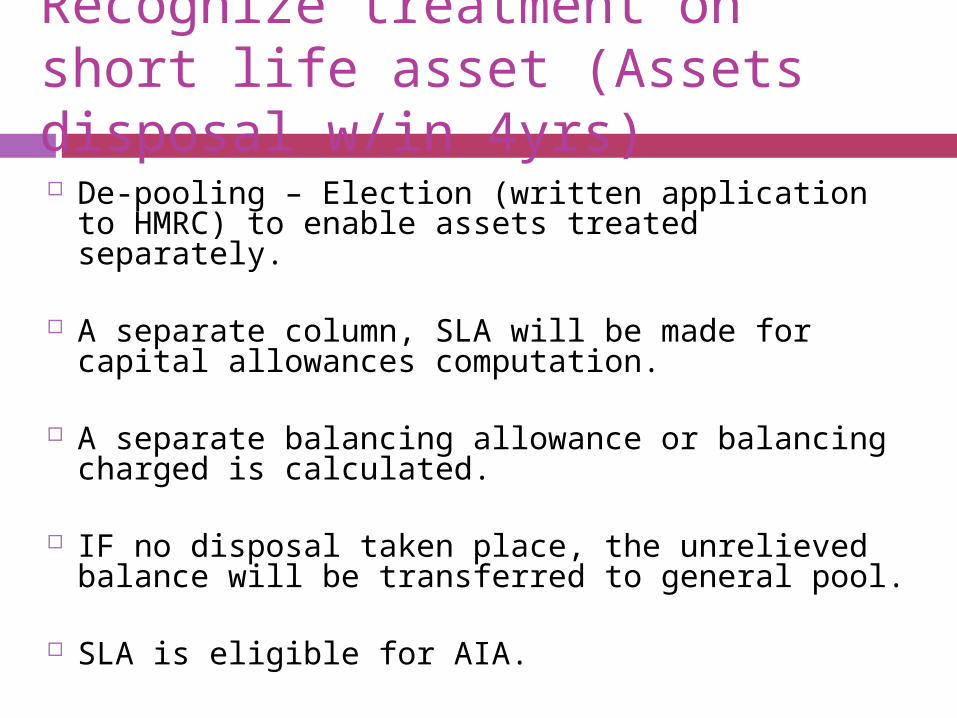

Recognize treatment on short life asset (Assets disposal w/in 4yrs) De-pooling – Election (written application to

HMRC) to enable assets treated separately.

A separate column, SLA will be made for capital allowances computation.

A separate balancing allowance or balancing charged is calculated.

IF no disposal taken place, the unrelieved balance will be transferred to general pool.

SLA is eligible for AIA.

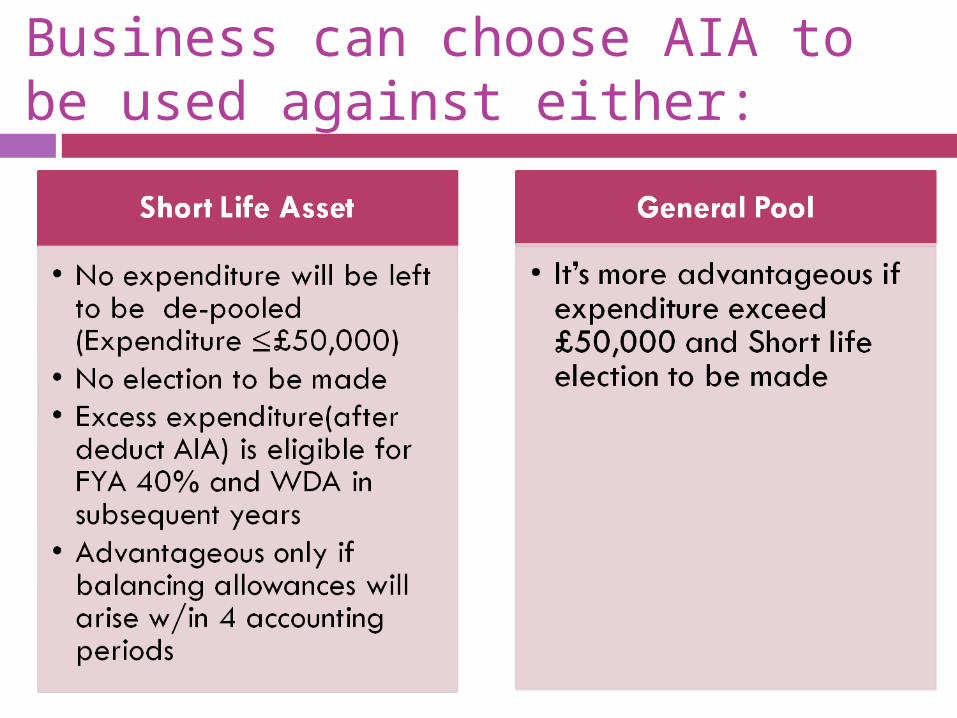

Business can choose AIA to be used against either:

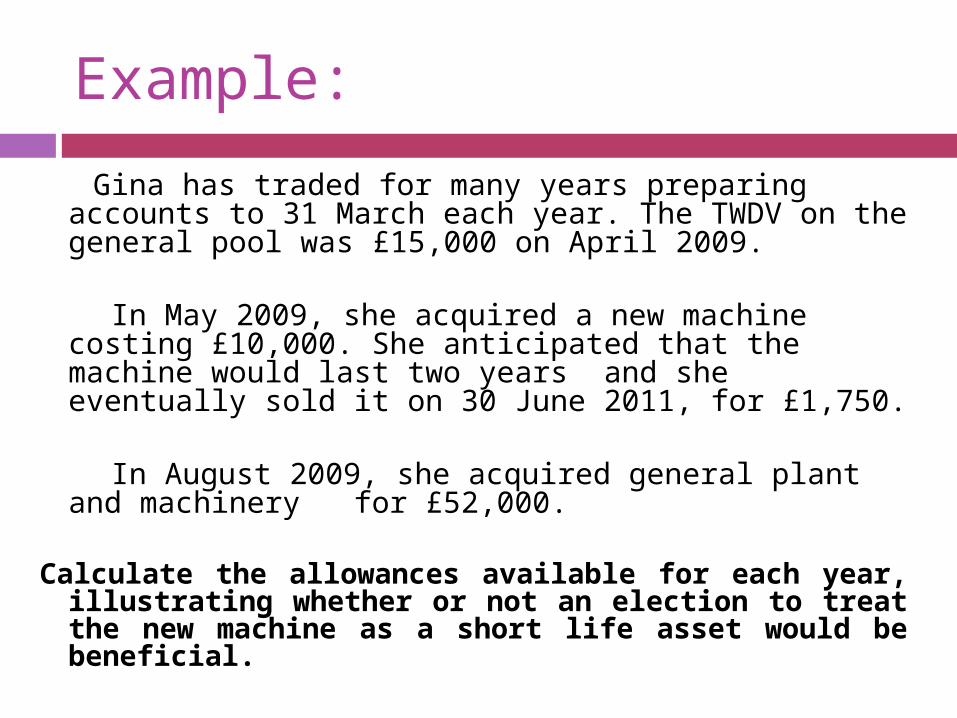

Example:

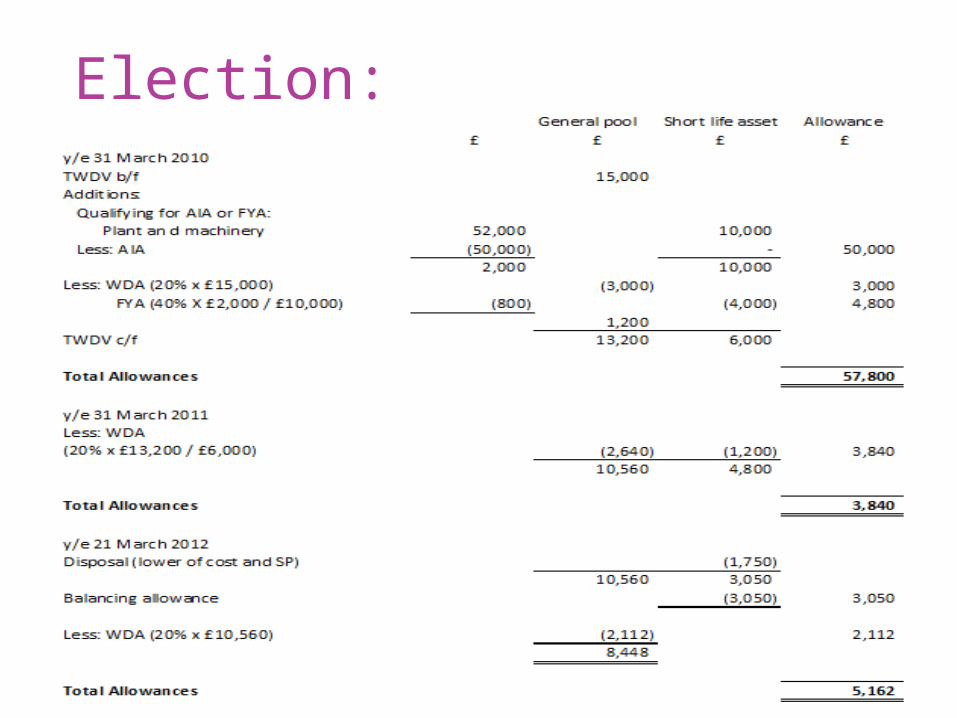

Gina has traded for many years preparing accounts to 31 March each year. The TWDV on the general pool was £15,000 on April 2009.

In May 2009, she acquired a new machine costing £10,000. She anticipated that the machine would last two years and she eventually sold it on 30 June 2011, for £1,750.

In August 2009, she acquired general plant and machinery for £52,000.

Calculate the allowances available for each year, illustrating whether or not an election to treat the new machine as a short life asset would be beneficial.

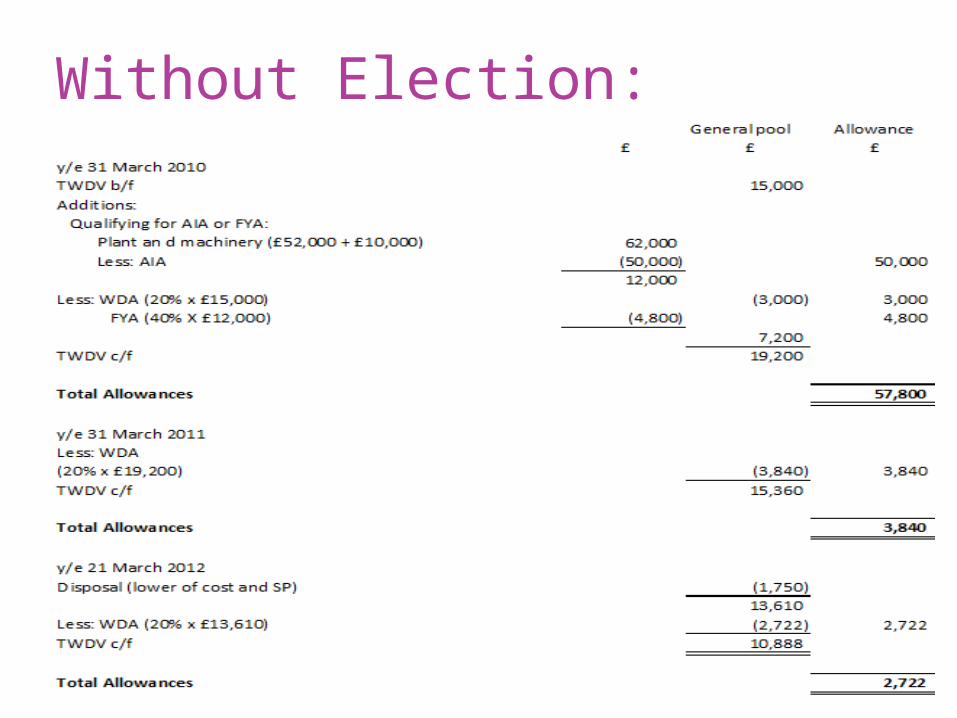

Without Election:

Election:

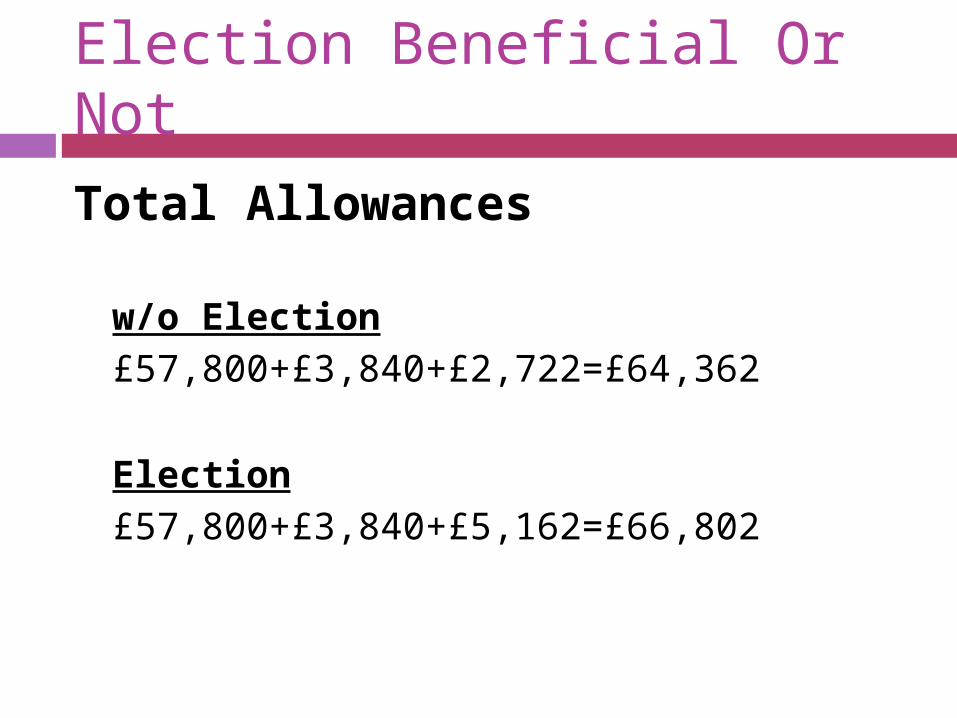

Election Beneficial Or Not

Total Allowances

w/o Election£57,800+£3,840+£2,722=£64,362

Election£57,800+£3,840+£5,162=£66,802

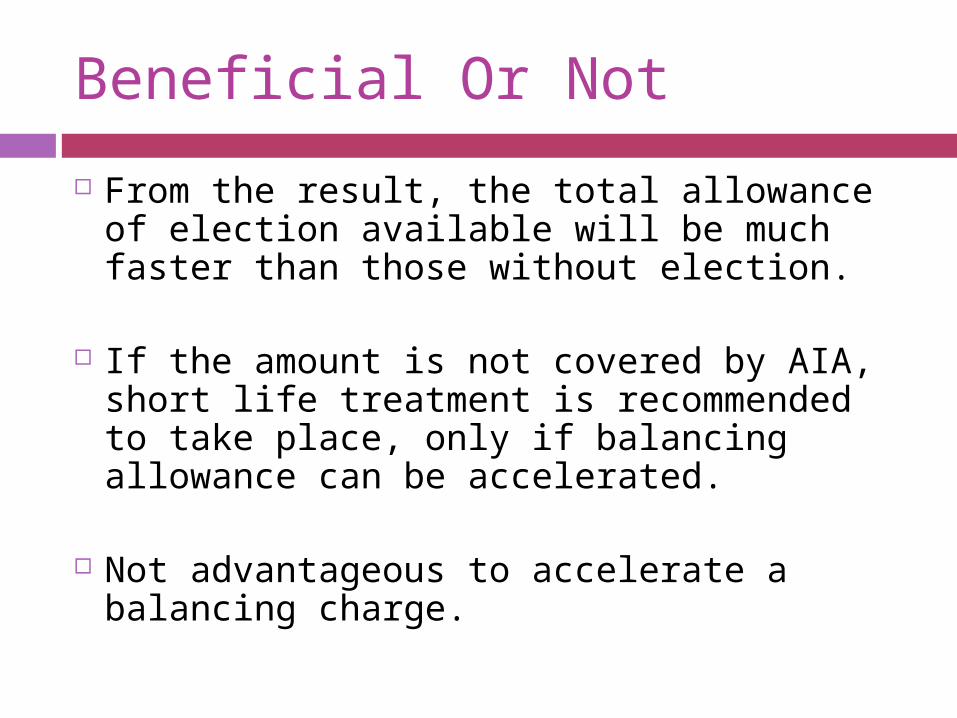

Beneficial Or Not

From the result, the total allowance of election available will be much faster than those without election.

If the amount is not covered by AIA, short life treatment is recommended to take place, only if balancing allowance can be accelerated.

Not advantageous to accelerate a balancing charge.

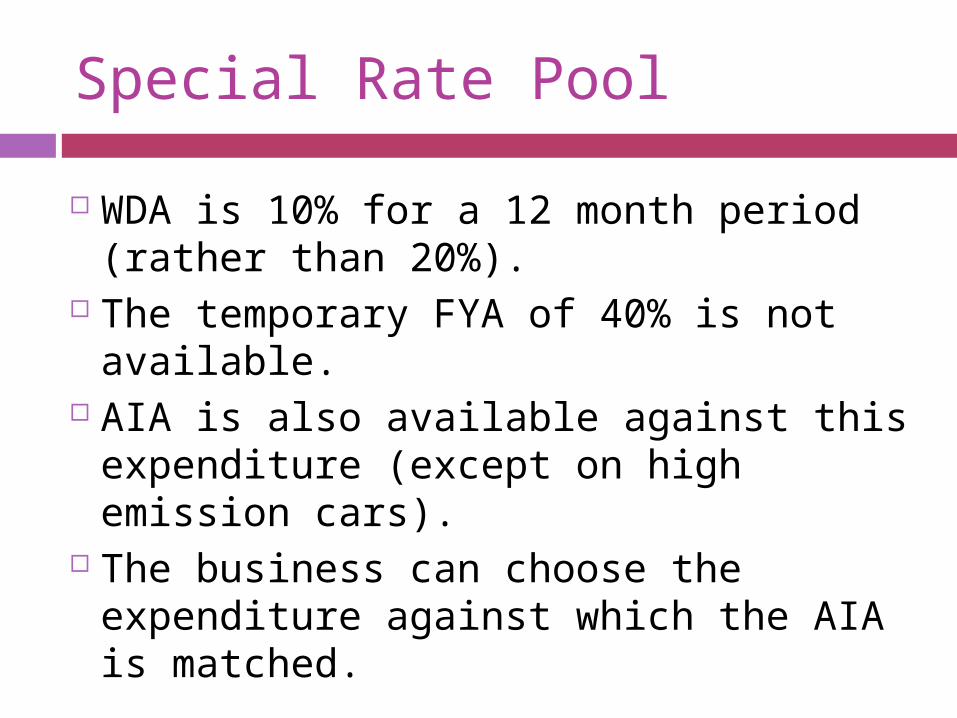

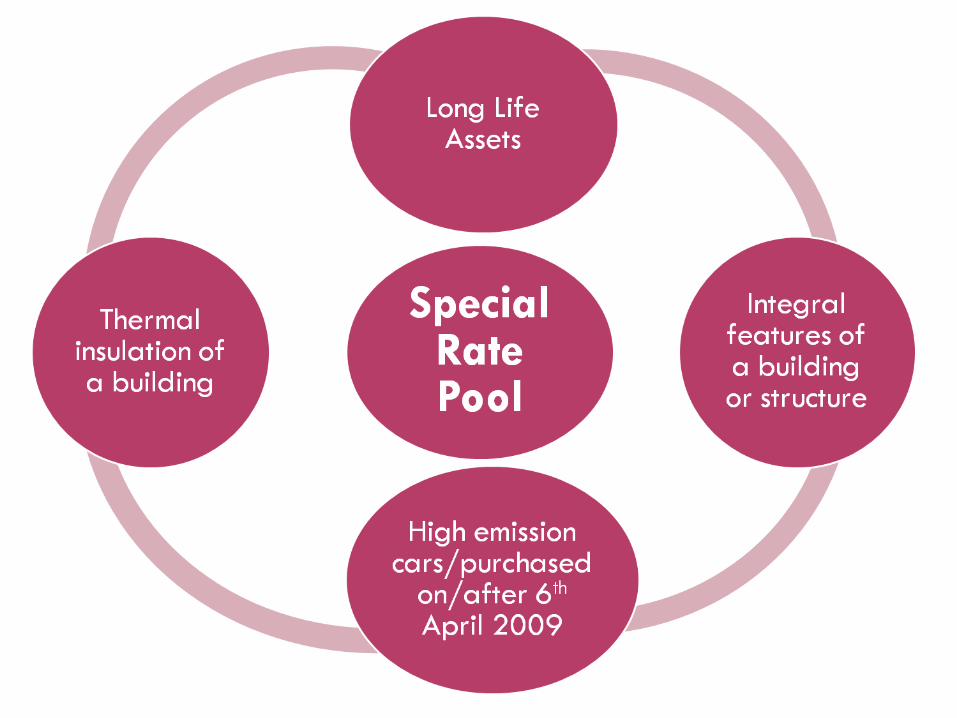

Special Rate Pool

WDA is 10% for a 12 month period (rather than 20%).

The temporary FYA of 40% is not available.

AIA is also available against this expenditure (except on high emission cars).

The business can choose the expenditure against which the AIA is matched.

It will be most beneficial for AIA to be allocated against expenditure in the following order:

The ‘special rate pool’

The general pool

Short life assets

Private use assets

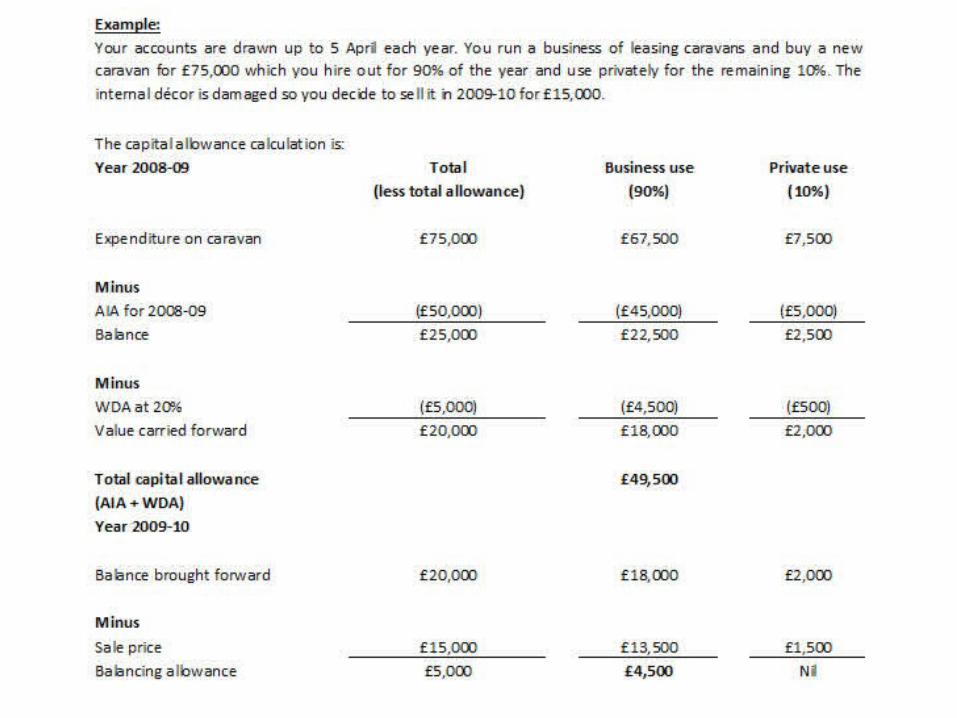

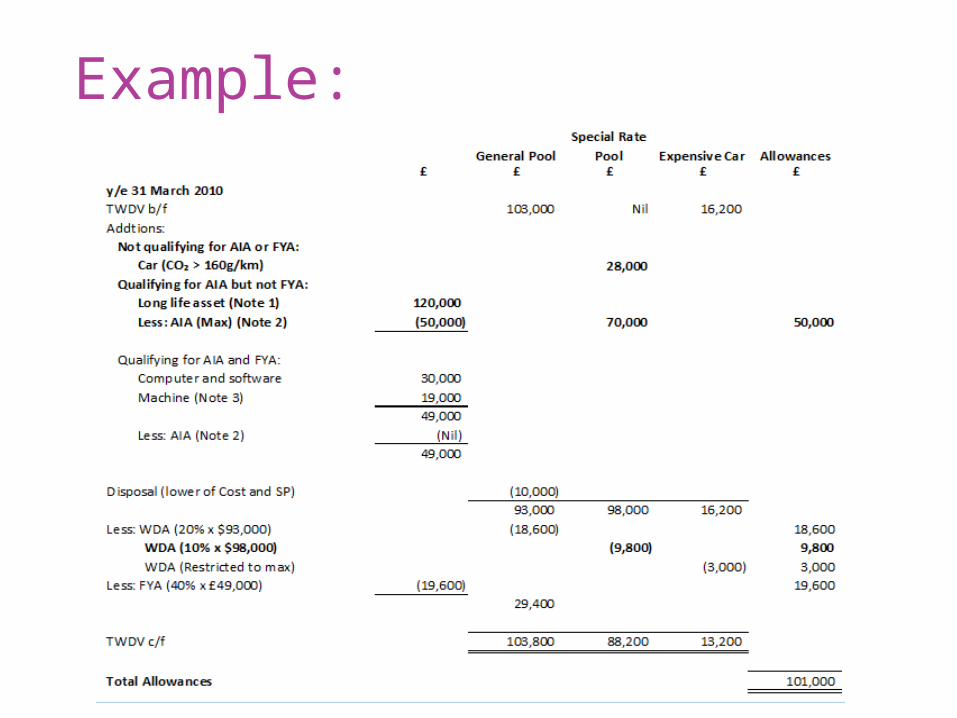

Example:

Reference:

“Capital allowances: Plant and machinery” in ACCA: Paper F6 The Complete Text (2009) (pp.161-211) Kaplan Publishing.

HMRC, Help Sheet 250: Capital allowances and balancing charges in a property rental business (2009). Extracted from: http://www.hmrc.gov.uk/helpsheets/hs250.pdf

Group members:

Jestina Tan anak Fauzi 08B1912 Carmen Chang Chaw Mann 08B1927 Andrew Sung Chee Hau 08B1907 Low Choon Ein 08B1905 Goh Kwang Lian 08B1911 Tan Ai Woon 08B1918