Embed Size (px)

Citation preview

Multinational Capital BudgetingMultinational Capital Budgeting

1414 Chapter Chapter

14 - 2

Chapter Objectives

To compare the capital budgeting analysis of an MNC’s subsidiary with that of its parent;

To demonstrate how multinational capital budgeting can be applied to determine whether an international project should be implemented; and

To explain how the risk of international projects can be assessed.

14 - 3

Subsidiary versus Parent Perspective

• Should the capital budgeting for a multi-national project be conducted from the viewpoint of the subsidiary that will administer the project, or the parent that will provide most of the financing?

• The results may vary with the perspective taken because the net after-tax cash inflows to the parent can differ substantially from those to the subsidiary.

14 - 4

Subsidiary versus Parent Perspective

• Such differences can be due to:

¤ Tax differentialsWhat is the tax rate on remitted funds?

¤ Regulations that restrict remittances

¤ Excessive remittancesThe parent may charge its subsidiary very high administrative fees.

¤ Exchange rate movements

14 - 5

Remitting Subsidiary Earnings to the Parent

Conversion of Fundsto Parent’s Currency

Parent

Cash Flows to Parent

Corporate Taxes Paid to Host Government

Retained Earningsby Subsidiary

After-Tax Cash Flows Remitted by Subsidiary

Withholding Tax Paid to Host Government

Cash Flows Remitted by Subsidiary

After-Tax Cash Flows at Subsidiary

Cash Flows Generated at Subsidiary

14 - 6

• A parent’s perspective is appropriate when evaluating a project, since any project that can create a positive net present value for the parent should enhance the firm’s value.

• However, one exception to this rule occurs when the foreign subsidiary is not wholly owned by the parent.

• So, the way to decide the project to be either subsidiary perspective or Parent perspective is look upon the share holder. If share holders are from subsidiary country, it would be subsidiary perspective unless otherwise.

Subsidiary versus Parent Perspective

14 - 7

Input for MultinationalCapital Budgeting

The following forecasts are usually required:

1.Initial investment2.Consumer demand over time3.Product price over time4.Variable cost over time5.Fixed cost over time6.Project lifetime7.Salvage (liquidation) value

14 - 8

The following forecasts are usually required:

Input for MultinationalCapital Budgeting

9.Tax payments and credits10.Exchange rates11.Required rate of return

8.Restrictions on fund transfers

14 - 9

MultinationalCapital Budgeting Techniques

• Capital budgeting is necessary for all long-term projects that deserve consideration.

• One common method of performing the analysis involves estimating the cash flows and salvage value to be received by the parent, and then computing the net present value (NPV) of the project.

14 - 10

MultinationalCapital Budgeting

• NPV = – initial outlay n

+ cash flow in period t

t =1 (1 + k )t

+ salvage value

(1 + k )n

k = the required rate of return on the projectn = project lifetime in terms of periods

• If NPV > 0, the project can be accepted.

14 - 11

Example

• Spartan, Inc. is considering the development of a subsidiary in Singapore that will manufacture and sell tennis rackets locally.

• Initial investment: 20 million Singapore dollars (S$) which is $10 million at $.50 per Singapore dollar. Project life: 4 years. Price and demand: 1st yr, 2nd, 3rd, 4th yrs price S$ S$ 350, S$ 350, S$ 360, S$ 380 and demand 60000, 60000, 100000,100000 units respectively.

• Costs: Variable cost per unit of 1st ,2nd, 3rd, 4th are S$ 200, S$ 200, S$ 250, S$ 260.The expense of leasing extra office space is S$ 1 million per year and other annual overhead expenses are expected to be S$1 million per year.

• Exchange rate: Spot rate is $.50 which will be assumed same over the years. Host country taxes on income earned by subsidiary: 20 percent tax rate on income. Also have withholding tax of 10%. And the remitted fund will not be taxed further in US. Depreciation: at a maximum rate of 2 million per year. Salvage Value: S$ 12 million. Required rate of return: 15%.

14 - 12

Capital Budgeting Analysis: Spartan, Inc.

14 - 13

Capital Budgeting Analysis: Spartan, Inc.

14 - 14

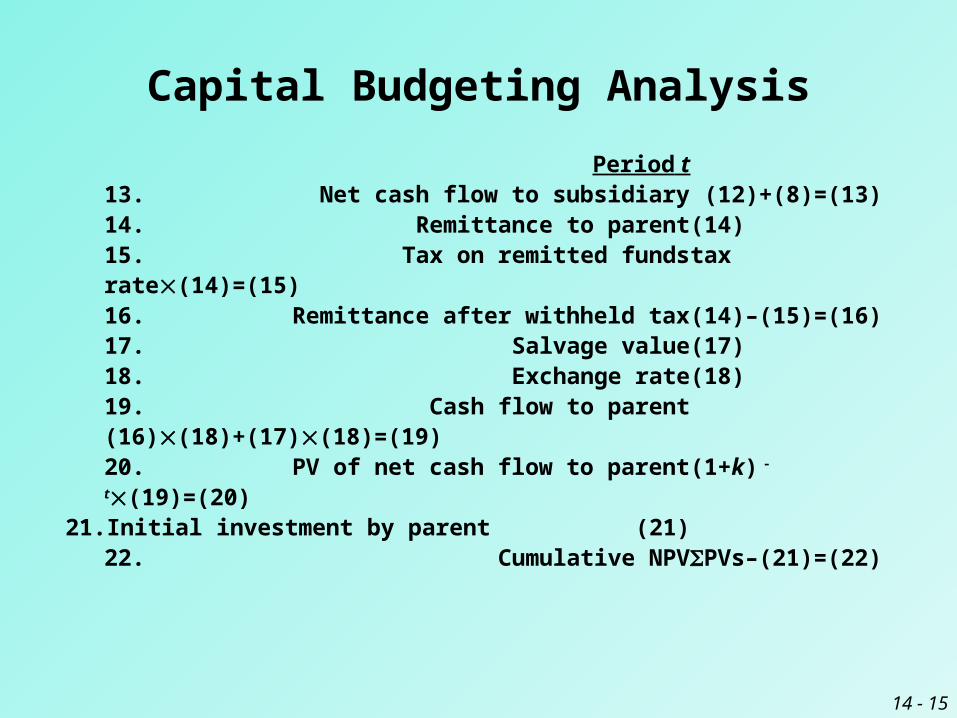

Capital Budgeting Analysis Period t

1.Demand (1)2.Price per unit (2)3.Total revenue (1)(2)=(3)4.Variable cost per unit (4)5.Total variable cost (1)(4)=(5)6.Annual lease expense (6)7.Other fixed annual expenses (7)8.Noncash expense (depreciation) (8)9.Total expenses (5)+(6)+(7)+(8)=(9)10. Before-tax earnings of subsidiary (3)–(9)=(10)11. Host government tax tax rate(10)=(11)12. After-tax earnings of subsidiary (10)–(11)=(12)

14 - 15

Capital Budgeting Analysis Period t

13. Net cash flow to subsidiary (12)+(8)=(13)14. Remittance to parent (14)15. Tax on remitted funds tax rate(14)=(15)16. Remittance after withheld tax (14)–(15)=(16)17. Salvage value (17)18. Exchange rate (18)19. Cash flow to parent(16)(18)+(17)(18)=(19)20. PV of net cash flow to parent (1+k)

-

t(19)=(20)21. Initial investment by parent (21)

22. Cumulative NPV PVs–(21)=(22)

14 - 16

Factors to Consider in Multinational Capital Budgeting

Exchange rate fluctuations

Since it is difficult to accurately forecast exchange rates, different scenarios can be considered together with their probability of occurrence.

14 - 17

Analysis Using Different Exchange Rate Scenarios: Spartan, Inc.

14 - 18

Sensitivity of the Project’s NPV to

Different Exchange Rate

Scenarios: Spartan, Inc.

14 - 19

Factors to Consider in Multinational Capital Budgeting

Inflation

Although price/cost forecasting implicitly considers inflation, inflation can be quite volatile from year to year for some countries.

14 - 20

Factors to Consider in Multinational Capital Budgeting

Financing arrangement

Financing costs are usually captured by the discount rate.

However, when foreign projects are partially financed by foreign subsidiaries, a more accurate approach is to separate the subsidiary investment and explicitly consider foreign loan payments as cash outflows.

14 - 21

Factors to Consider in Multinational Capital Budgeting

Blocked funds

Some countries require that the earnings generated by the subsidiary be reinvested locally for at least a certain period of time before they can be remitted to the parent.

14 - 22

Capital Budgeting with Blocked Funds: Spartan, Inc.Assume that all funds are blocked until the subsidiary is sold.

14 - 23

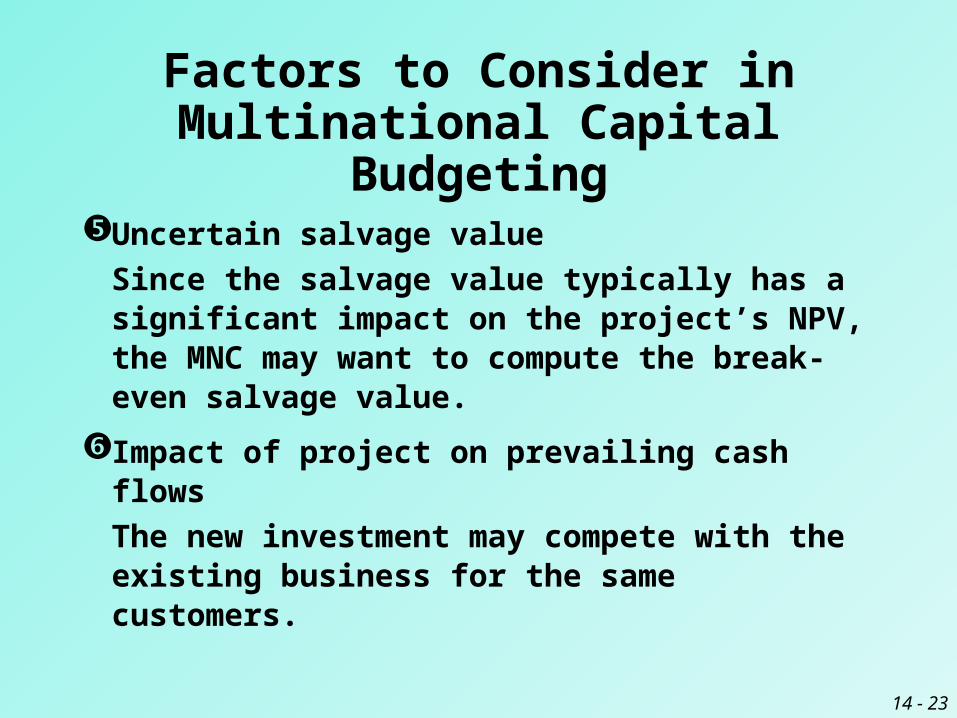

Factors to Consider in Multinational Capital Budgeting

Uncertain salvage value

Since the salvage value typically has a significant impact on the project’s NPV, the MNC may want to compute the break-even salvage value.

Impact of project on prevailing cash flows

The new investment may compete with the existing business for the same customers.

14 - 24

Factors to Consider in Multinational Capital Budgeting

Host government incentives

These should also be incorporated into the analysis.

A low-rate host government loan or a reduced tax rate offered to the subsidiary will enhance periodic cash flow.

If the government subsidizes the initial establishment of the subsidiary, the MNC’s initial investment will be reduced.

14 - 25

Adjusting Project Assessmentfor Risk

• When an MNC is unsure of the estimated cash flows of a proposed project, it needs to incorporate an adjustment for this risk.

• One method is to use a risk-adjusted discount rate. The greater the uncertainty, the larger the discount rate that should be applied to the cash flows.

14 - 26

Adjusting Project Assessmentfor Risk

• An MNC may also perform sensitivity analysis or simulation using computer software packages to adjust its evaluation.

• Sensitivity analysis involves considering alternative estimates for the input variables, while simulation involves repeating the analysis many times using input values randomly drawn from their respective probability distributions.

14 - 27

Problem-1• Brower, Inc., just constructed a manufacturing plant in

Ghana. The construction cost 9 billion Ghanaian cedi. Brower intends to leave the plant open for three years. During the three years of operation ,cedi cash flows are expected to be 3 billion cedi,3 billion cedi and 2 billion cedi, respectively. Operating cash flows will begin one year from today and are remitted back to the parent at the end of each year. At the end of the third year, Brower expects to sell the plant for 5 billion cedi. Brower has a required rate of return of 17%.It currently takes 8700 cedi to buy one US dollar, and the cedi is expected to depreciate by 5 percent per year.a) Determine the NPV for this project .Should Brower build the

plant?b) How would your answer change if the value of the cedi was

expected to remain unchanged from its current value of 8700 cedi per US over the course of the three years? Should Brower construct the plant then?

14 - 28

Problem-2

• A project A project in South Korea requires an initial invvestment of 2 billion South Korean Won. The Project is expected to generate net cash flows to the subsidiary of 3 billion and 4 billion won in the two years of operation,respectively. Thee project has no salvage value. The current value of the won is 1100won per US dollar and the value of the won is expected to remain constant over the next two years.

A) What is the NPV of this project if the required rate of return is 13 percent?

B) Repeat the question, except assume that the value of the won is expected to be 1200 won per US dollar after two yeas. Further assume that the funds are blocked and the parent company will only be able to remit them back to the united states in two years. How does this affect the NPV of the project.