Embed Size (px)

Citation preview

"Multinationals, Nation States andGlobal Value Chains: Mexico’s

Perspective"

Ismael PlascenciaUniversidad Autónoma de Baja California

The Labor Relations CommissionCroke Park Conference Centre

19th june 2008

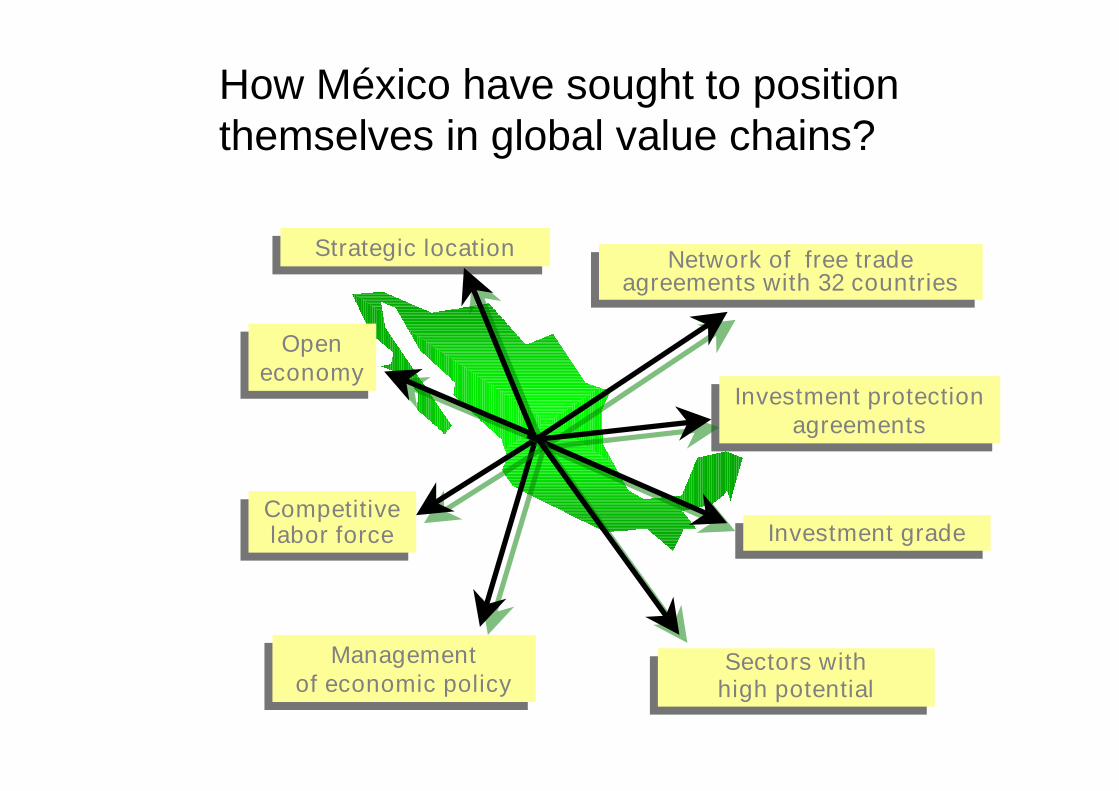

Investment protectionagreements

Investment protectionagreements

Sectors withhigh potential

Sectors withhigh potential

Openeconomy

Openeconomy

Strategic locationStrategic locationNetwork of free trade

agreements with 32 countries

Network of free tradeagreements with 32 countries

Competitivelabor force

Competitivelabor force

Managementof economic policy

Managementof economic policy

Investment gradeInvestment grade

How México have sought to positionthemselves in global value chains?

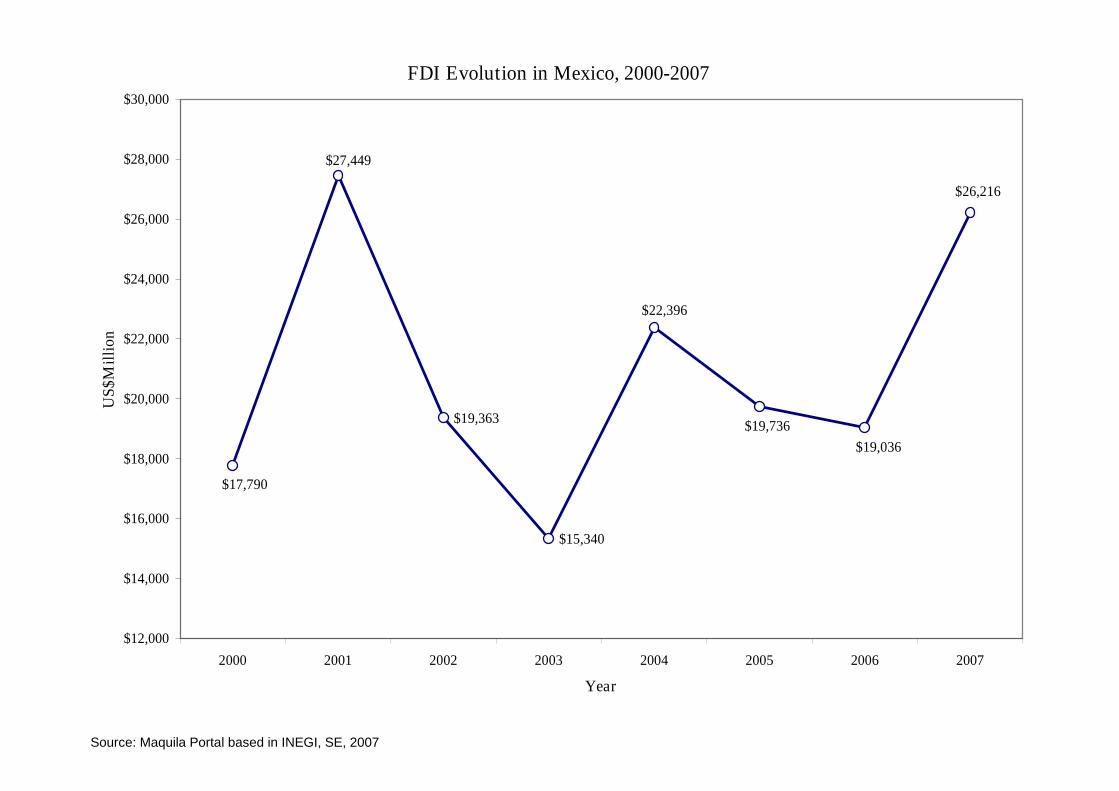

FDI Evolution in Mexico, 2000-2007

$19,363

$15,340

$27,449

$17,790

$26,216

$19,036

$19,736

$22,396

$12,000

$14,000

$16,000

$18,000

$20,000

$22,000

$24,000

$26,000

$28,000

$30,000

2000 2001 2002 2003 2004 2005 2006 2007

Year

US

$M

illi

on

Source: Maquila Portal based in INEGI, SE, 2007

Source: Maquila Portal based in INEGI, SE, 2007

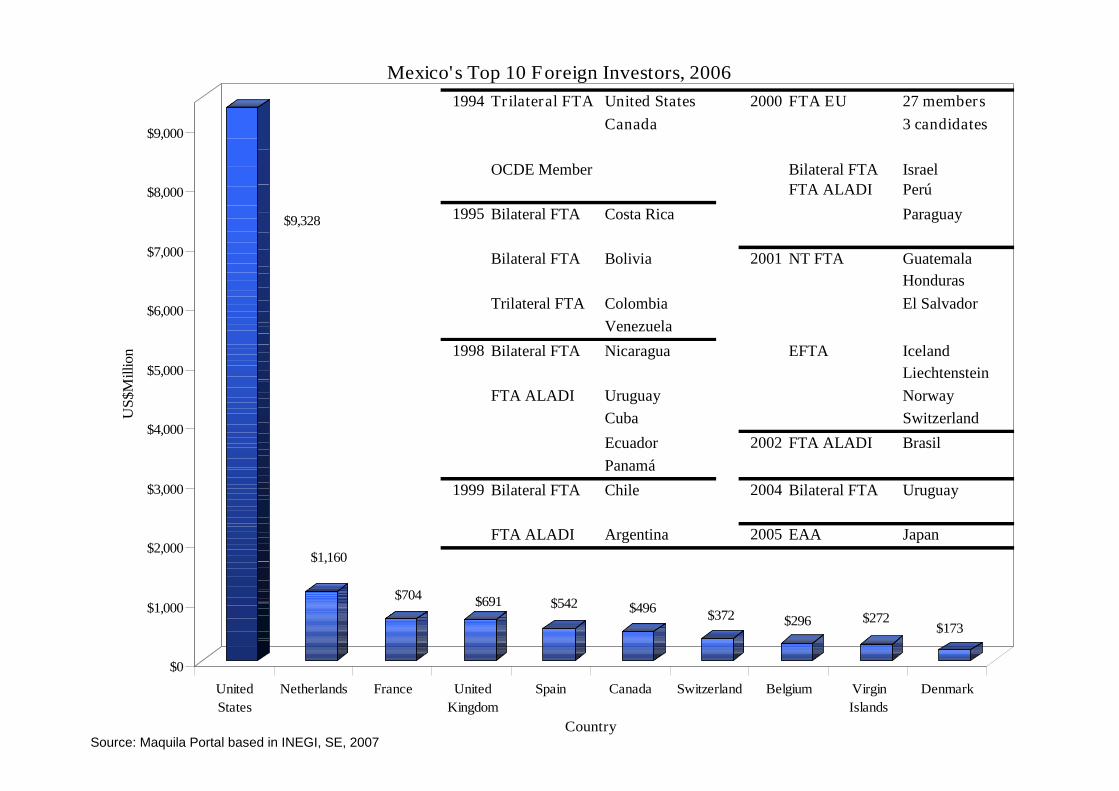

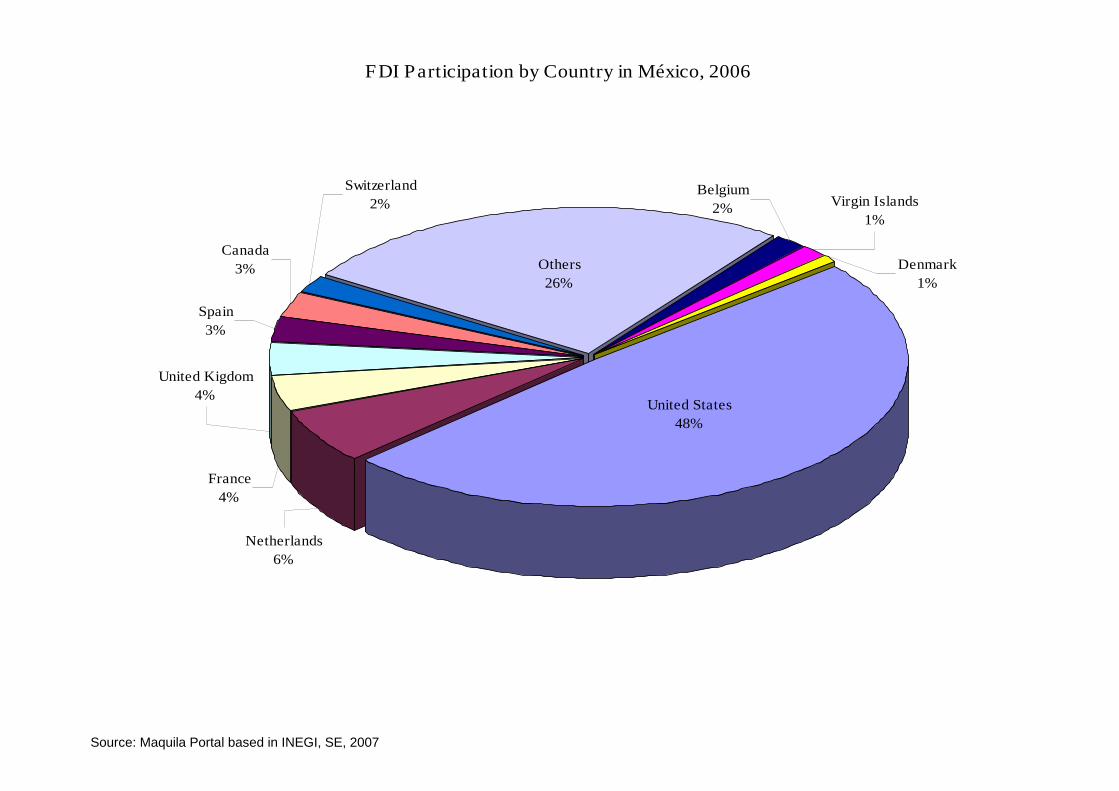

$9,328

$1,160

$704 $691 $542 $496$372 $296 $272

$173

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000U

S$M

illion

United

States

Netherlands France United

Kingdom

Spain Canada Switzerland Belgium Virgin

Islands

Denmark

Country

Mexico's Top 10 Foreign Investors, 2006

1994 Trilateral FTA United States 2000 FTA EU 27 members

Canada 3 candidates

OCDE Member Bilateral FTA IsraelFTA ALADI Perú

1995 Bilateral FTA Costa Rica Paraguay

Bilateral FTA Bolivia 2001 NT FTA Guatemala

Honduras

Trilateral FTA Colombia El Salvador

Venezuela

1998 Bilateral FTA Nicaragua EFTA Iceland

Liechtenstein

FTA ALADI Uruguay Norway

Cuba Switzerland

Ecuador 2002 FTA ALADI Brasil

Panamá

1999 Bilateral FTA Chile 2004 Bilateral FTA Uruguay

FTA ALADI Argentina 2005 EAA Japan

Source: Maquila Portal based in INEGI, SE, 2007

FDI Participation by Country in México, 2006

Denmark

1%

Netherlands

6%

France

4%

United Kigdom

4%

Others

26%

Belgium

2%Virgin Islands

1%

United States

48%

Switzerland

2%

Spain

3%

Canada

3%

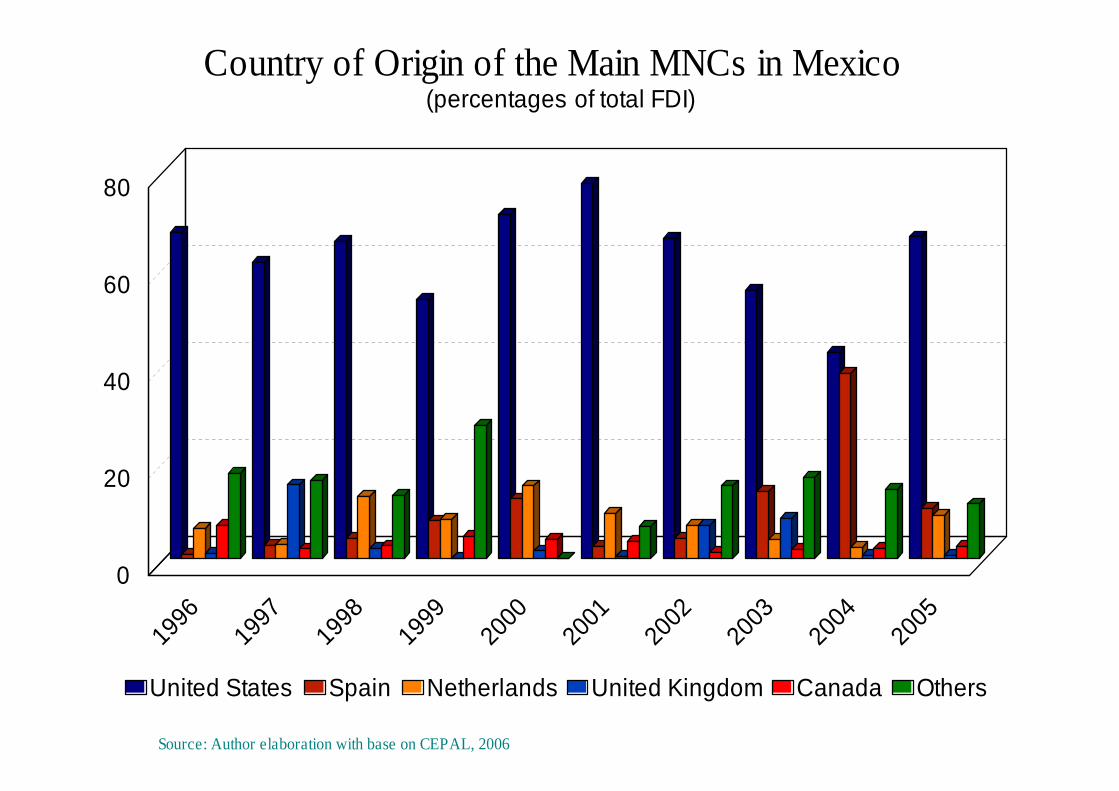

Country of Origin of the Main MNCs in Mexico(percentages of total FDI)

Source: Author elaboration with base on CEPAL, 2006

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

0

20

40

60

80

United States Spain Netherlands United Kingdom Canada Others

Source: Maquila Portal based in INEGI, SE, 2007

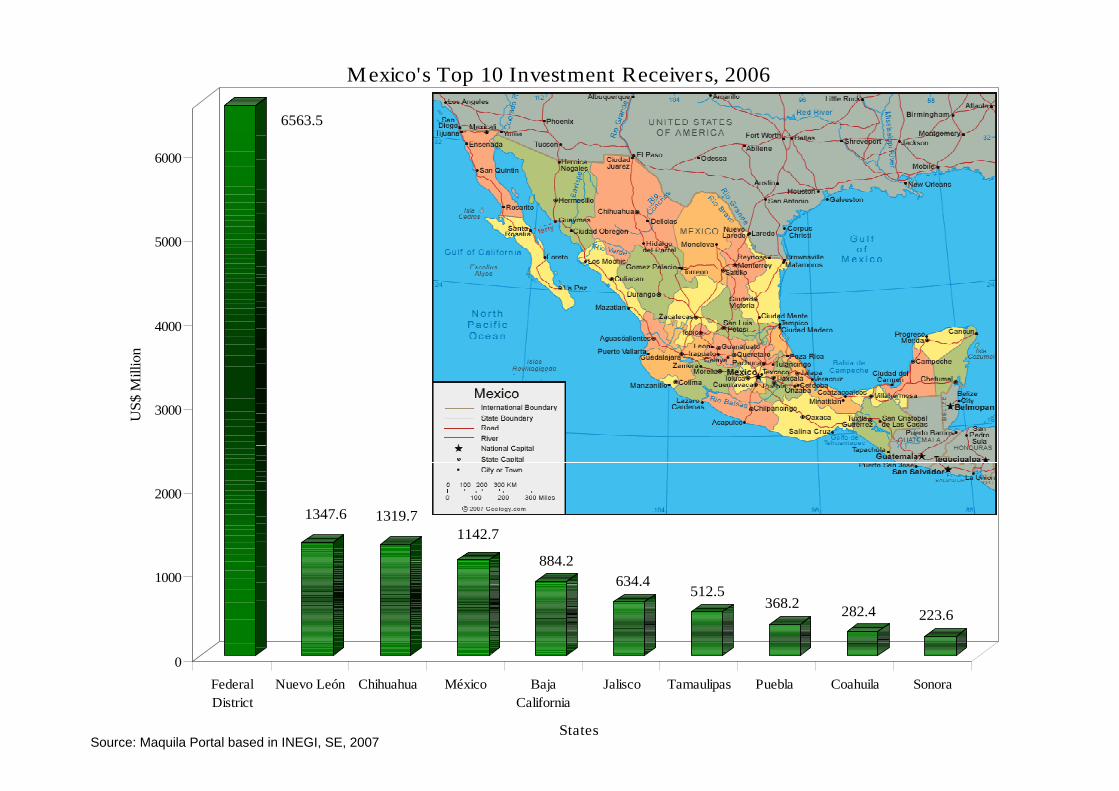

6563.5

1347.6 1319.71142.7

884.2

634.4512.5

368.2282.4 223.6

0

1000

2000

3000

4000

5000

6000

US

$M

illion

Federal

District

Nuevo León Chihuahua México Baja

California

Jalisco Tamaulipas Puebla Coahuila Sonora

States

Mexico's Top 10 Investment Receivers, 2006

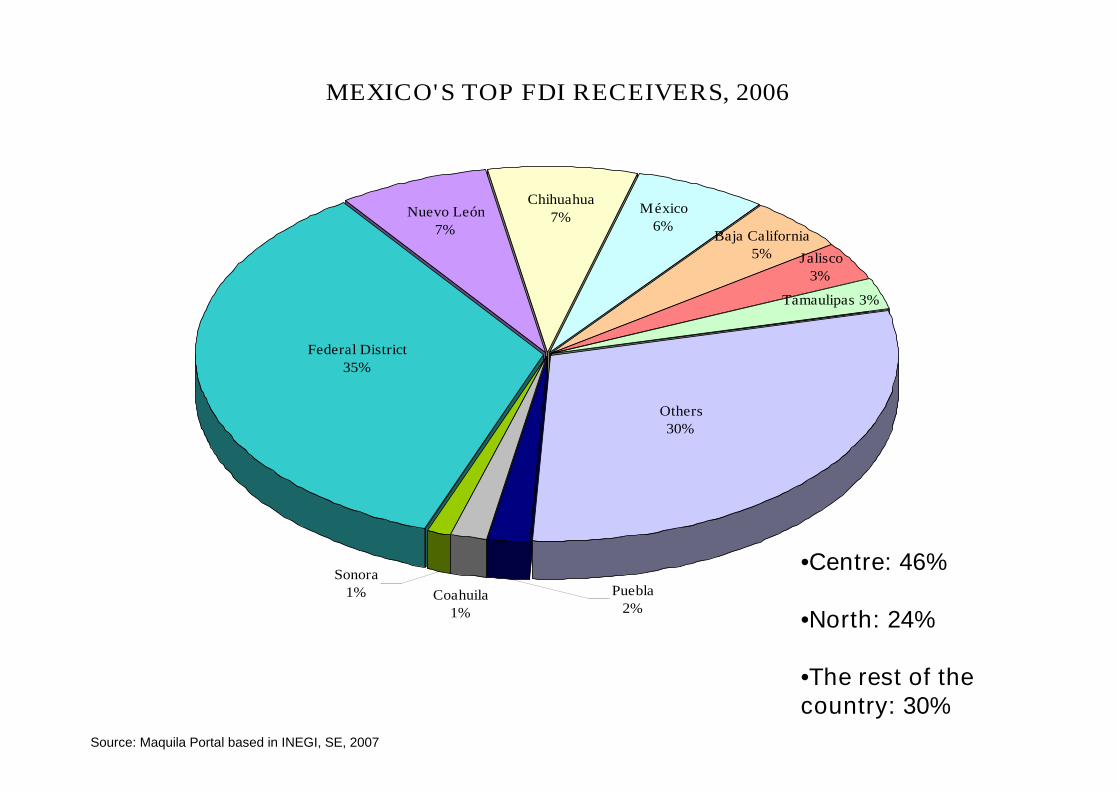

MEXICO'S TOP FDI RECEIVERS, 2006

Tamaulipas 3%

Federal District

35%

Others30%

Puebla2%

Coahuila1%

Sonora1%

Chihuahua

7%México

6%Nuevo León

7% Baja California5% Jalisco

3%

Source: Maquila Portal based in INEGI, SE, 2007

•Centre: 46%

•North: 24%

•The rest of thecountry: 30%

Path dependence of the actual situation

• Natural Resources: Mexico assumed a strong position in defending itsnatural resources in the 1930s with the nationalization of the oil industry.Mexico became a unique case in the history of Latin America.Government needs to privatized the oil extraction and energy sector.

• Manufactures: FDI came with the inward growth model, which gaveinvestors monopolistic profits (through protection). A new round beganwith the opening of the economy and its export oriented approachsince 1983. MNCs became interested in taking advantage of a lowcost area, located geographically close to the largest market in theworld. That’s why this sector its attain to the cyclical economy of theUS: almost 90% of the Mexico’s exports goes to US.

• Services: After the 1994 financial crisis, almost all of the banks weresold to foreign investors. On the other hand, wholesale and retail firms(Walt-Mart, Costco) start operations to take advantage of the Mexicanmarket .

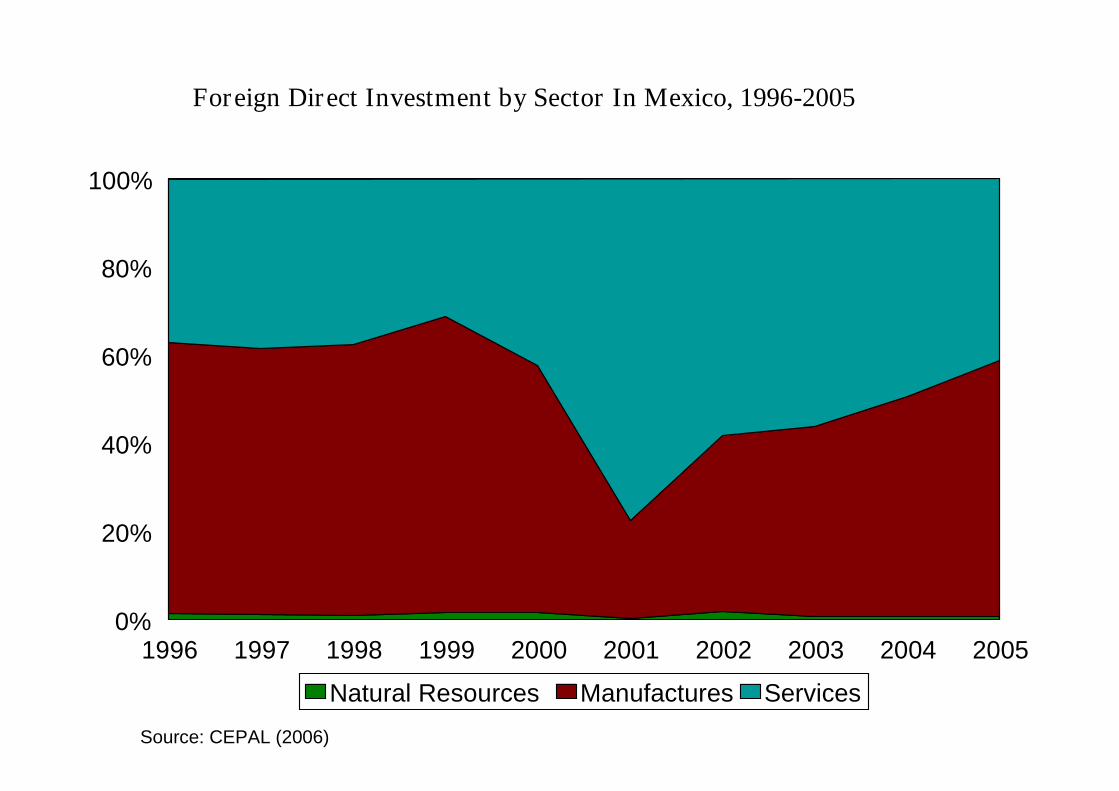

Foreign Direct Investment by Sector In Mexico, 1996-2005

Source: CEPAL (2006)

1996 1997 1998 1999 2000 2001 2002 2003 2004 20050%

20%

40%

60%

80%

100%

Natural Resources Manufactures Services

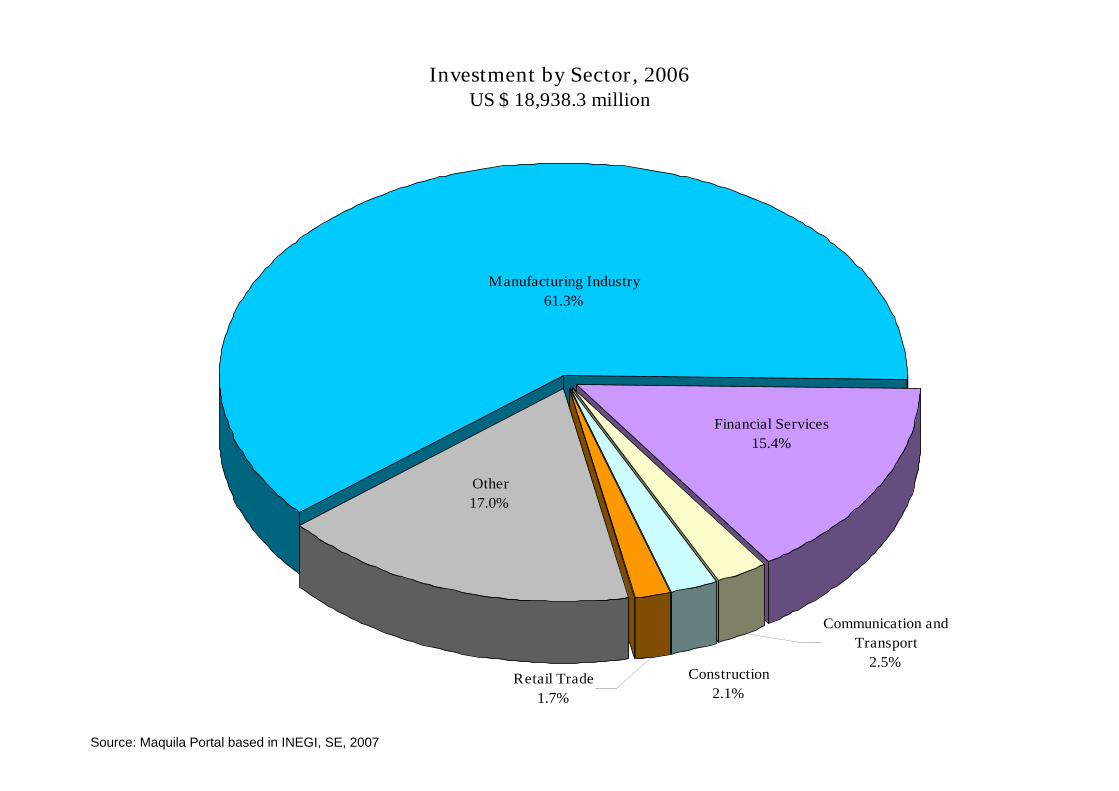

Investment by Sector, 2006US $ 18,938.3 million

Construction

2.1%

Communication and

Transport

2.5%Retail Trade

1.7%

Other

17.0%

Manufacturing Industry

61.3%

Financial Services

15.4%

Source: Maquila Portal based in INEGI, SE, 2007

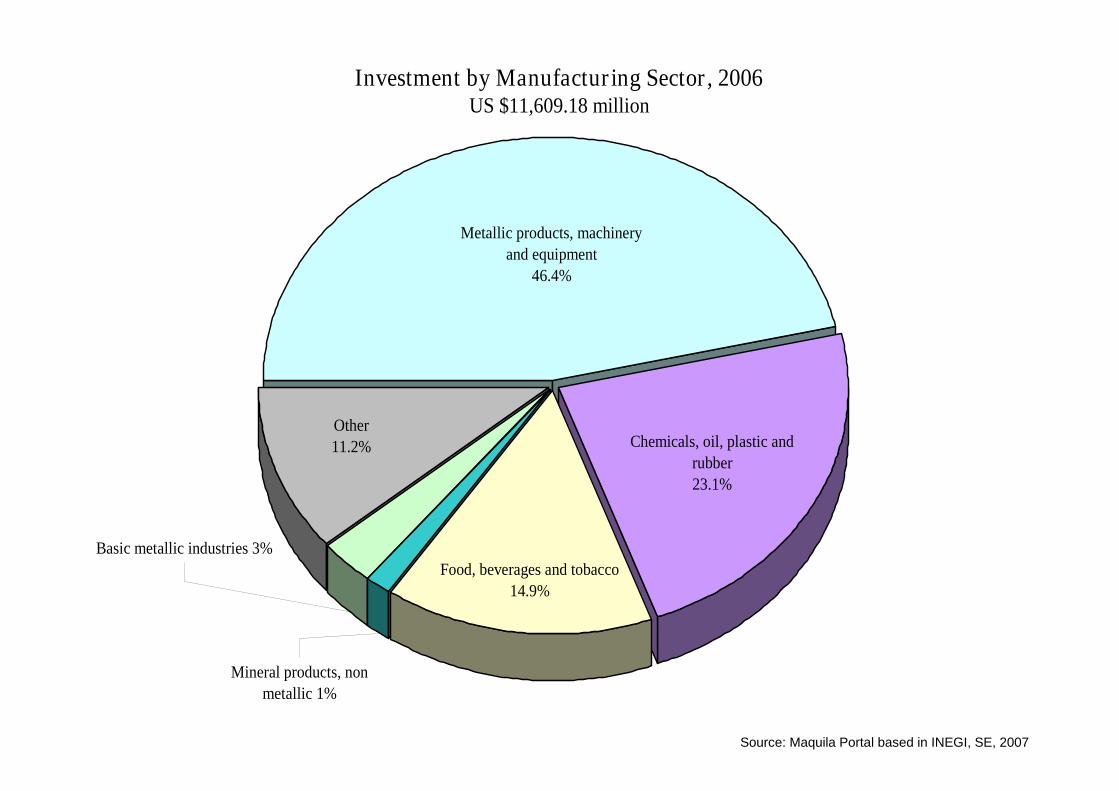

Investment by Manufacturing Sector, 2006US $11,609.18 million

Metallic products, machinery

and equipment

46.4%

Chemicals, oil, plastic and

rubber

23.1%

Food, beverages and tobacco

14.9%

Other

11.2%

Mineral products, non

metallic 1%

Basic metallic industries 3%

Source: Maquila Portal based in INEGI, SE, 2007

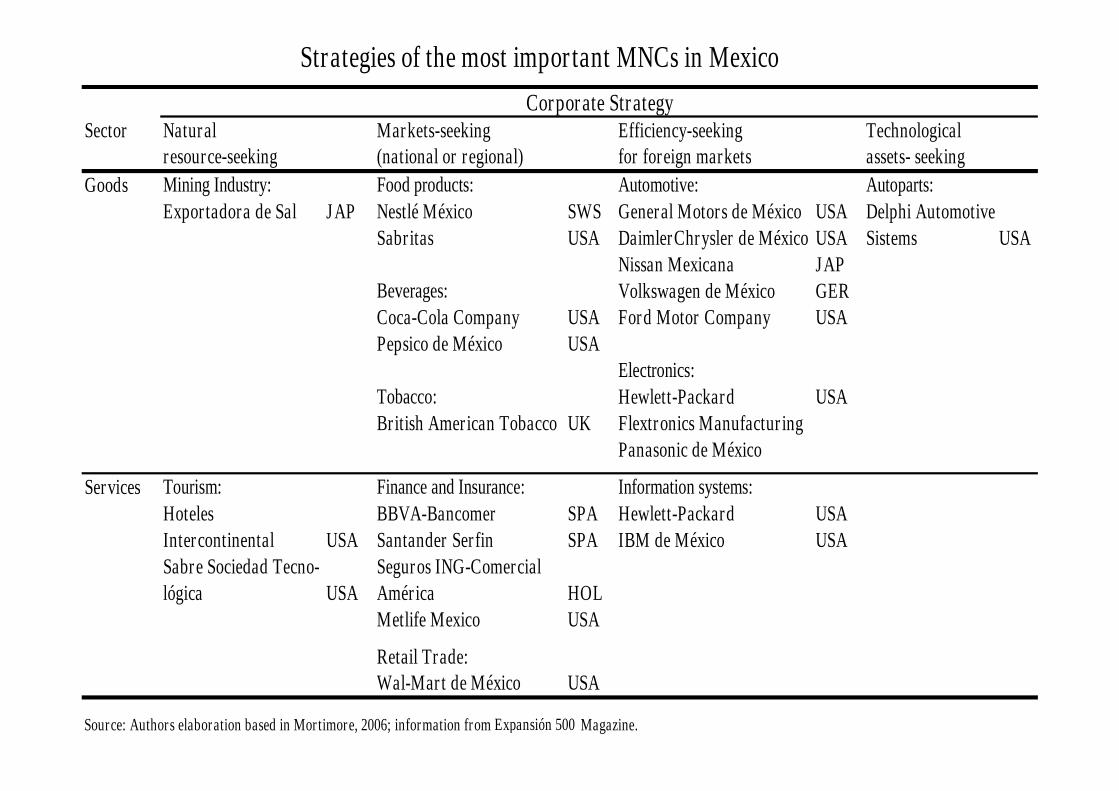

What kinds of MNCs are presentin Mexico?

Sector Natural Markets-seeking Efficiency-seeking Technologicalresource-seeking (national or regional) for foreign markets assets- seeking

Goods Mining Industry: Food products: Automotive: Autoparts:

Exportadora de Sal JAP Nestlé México SWS General Motors de México USA Delphi AutomotiveSabritas USA DaimlerChrysler de México USA Sistems USA

Nissan Mexicana JAPBeverages: Volkswagen de México GERCoca-Cola Company USA Ford Motor Company USAPepsico de México USA

Electronics:Tobacco: Hewlett-Packard USABritish American Tobacco UK Flextronics Manufacturing

Panasonic de México

Services Tourism: Finance and Insurance: Information systems:

Hoteles BBVA-Bancomer SPA Hewlett-Packard USAIntercontinental USA Santander Serfin SPA IBM de México USASabre Sociedad Tecno- Seguros ING-Comerciallógica USA América HOL

Metlife Mexico USA

Retail Trade:Wal-Mart de México USA

Source: Authors elaboration based in Mortimore, 2006; information from Expansión 500 Magazine.

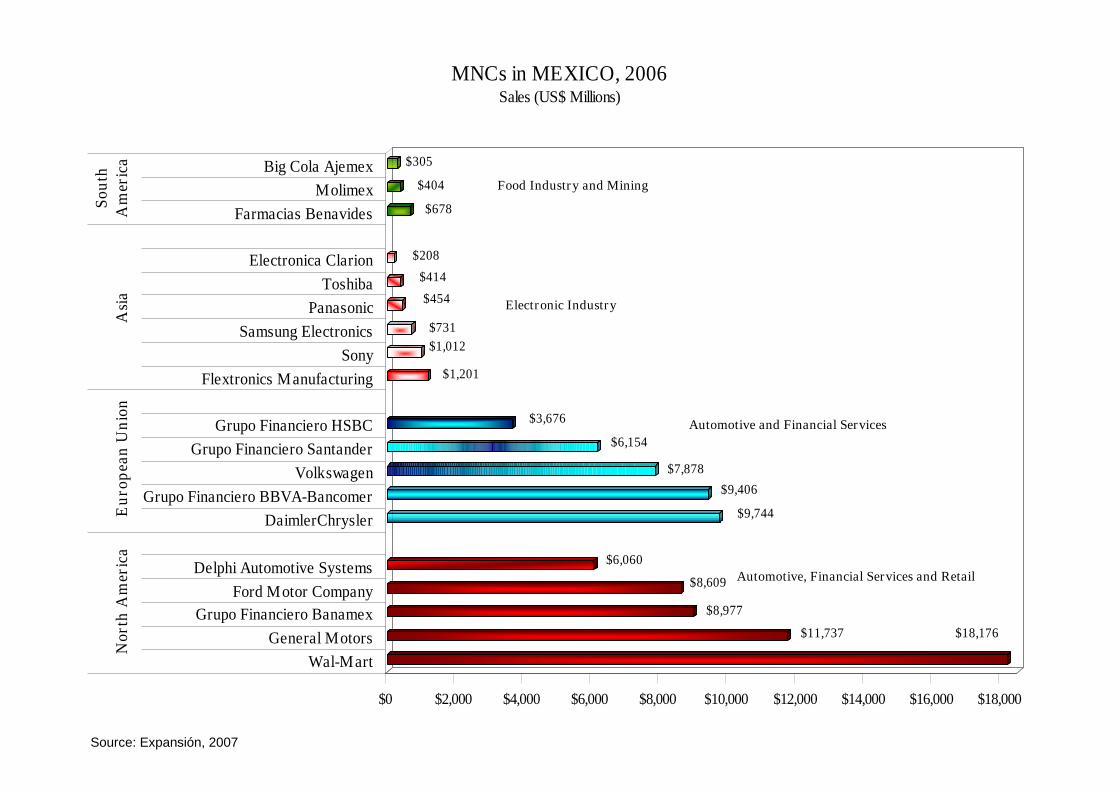

Strategies of the most important MNCs in Mexico

Corporate Strategy

Source: Expansión, 2007

$18,176$11,737

$8,977

$8,609

$6,060

$9,744

$9,406

$7,878

$6,154

$3,676

$1,201

$1,012

$731

$454

$414

$208

$678

$404

$305

$0 $2,000 $4,000 $6,000 $8,000 $10,000 $12,000 $14,000 $16,000 $18,000

Wal-Mart

General Motors

Grupo Financiero Banamex

Ford Motor Company

Delphi Automotive Systems

DaimlerChrysler

Grupo Financiero BBVA-Bancomer

Volkswagen

Grupo Financiero Santander

Grupo Financiero HSBC

Flextronics Manufacturing

Sony

Samsung Electronics

Panasonic

Toshiba

Electronica Clarion

Farmacias Benavides

Molimex

Big Cola Ajemex

No

rth

Am

eric

aE

uro

pea

nU

nio

nA

sia

So

uth

Am

eric

a

MNCs in MEXICO, 2006Sales (US$ Millions)

Food Industry and Mining

Electronic Industry

Automotive and Financial Services

Automotive, Financial Services and Retail

403,244

179,953

76,829

63,022

58,440

25,000

356,840

140,505

80,371

54,635

41,418

39,911

- 50,000 100,000 150,000 200,000 250,000 300,000 350,000 400,000

Total

Walmart

Grupo Financiero Banamex

Delphi Automotive Systems

Grupo Financiero BBVA

Bancomer

General Electric

Total

PEMEX

Grupo Carso

Cemex

América Móvil

Grupo ModeloO

utw

ard

MN

Cs

Mex

ica

nM

NC

s

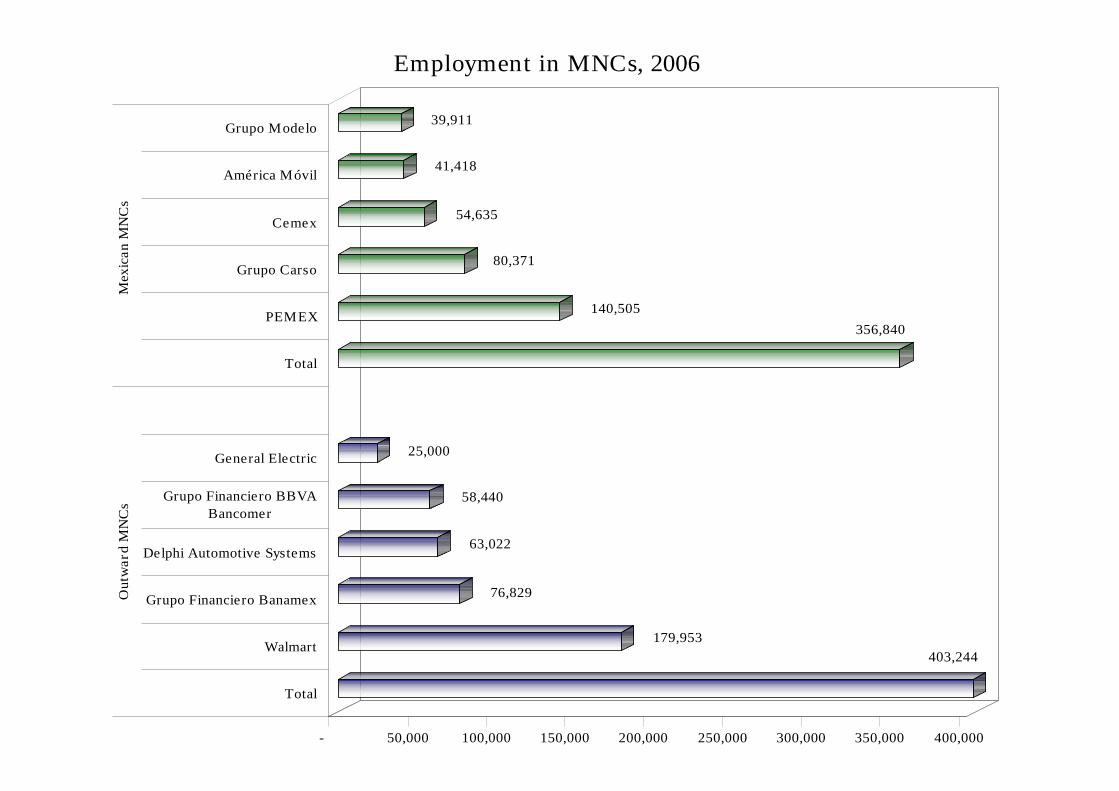

Employment in MNCs, 2006

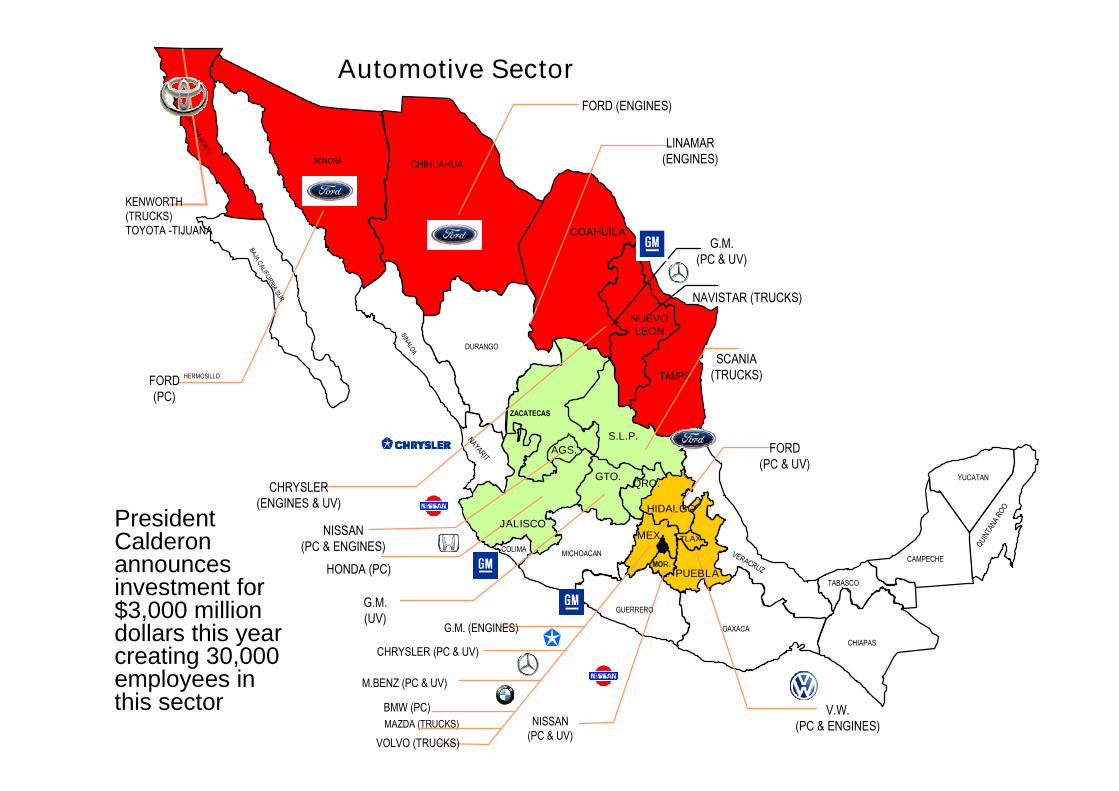

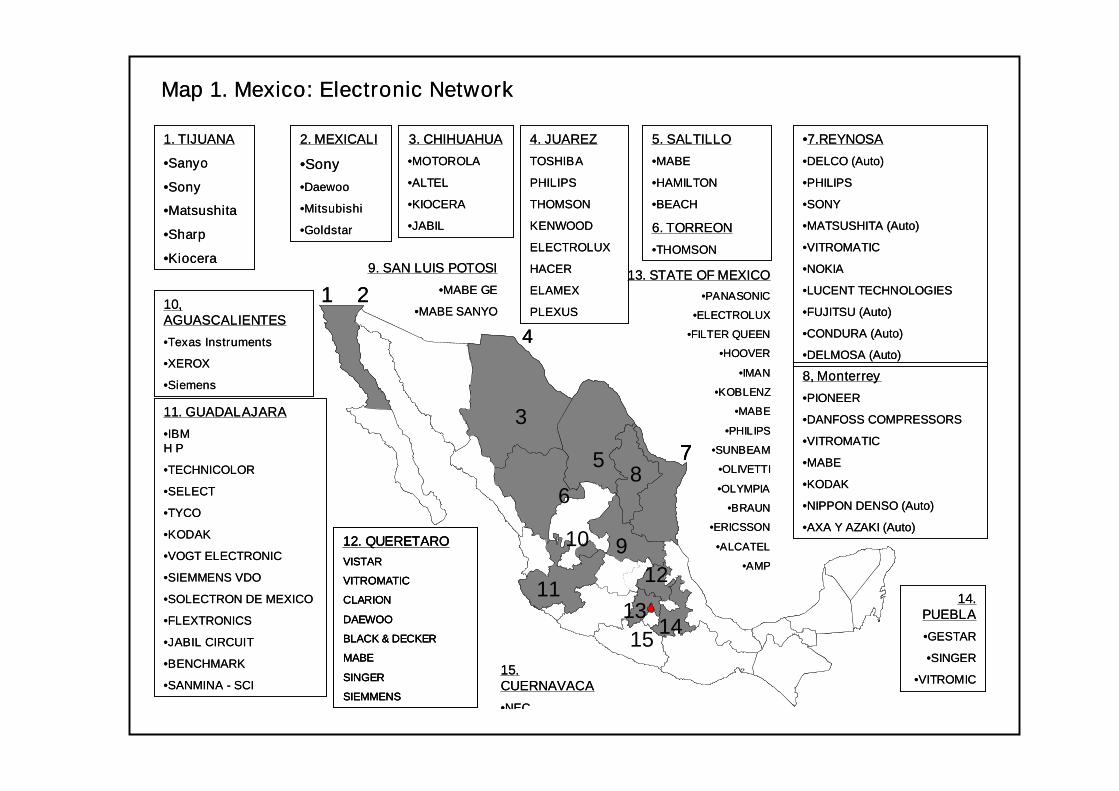

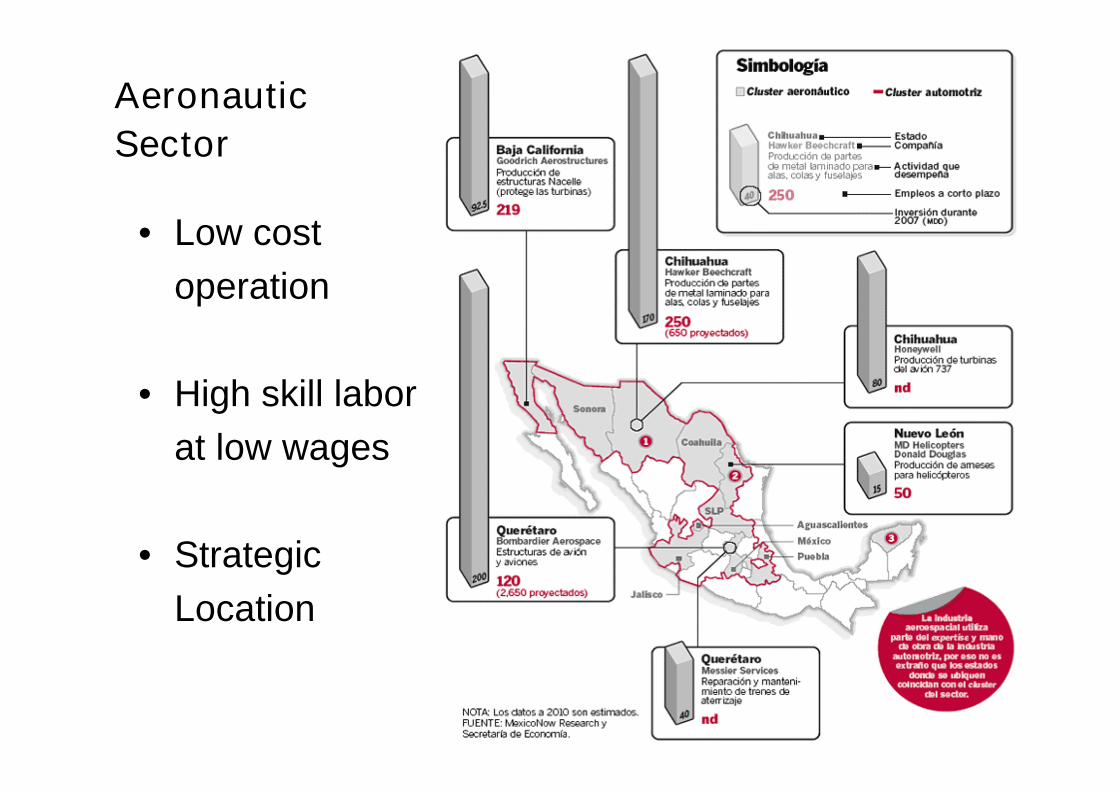

How’s the changing role of localoperations in the global division of

labour of these MNCs?

• MNC’s in Mexico are making andimportant upgrading in their operationsmainly due to process restructuring andchange of operations from US to Mexico.

• The most important sectors areautomotive, electronics and recently theaeronautic sector.

QRO.

COAHUILA

HERMOSILLOFORD(PC)

CHRYSLER(ENGINES & UV)

AGS.

NISSAN(PC & ENGINES)

GTO.

G.M.(UV)

M.BENZ (PC & UV)

V.W.(PC & ENGINES)

HONDA (PC)

SONORA

FORD (ENGINES)

CHIHUAHUA

LINAMAR(ENGINES)

MOR.

NISSAN(PC & UV)

BAJAC

ALIFOR

NIA

NO

RTE

BAJAC

ALIFOR

NIA

SUR

SINALO

A DURANGO

NAYARIT

ZACATECAS

S.L.P.

TAMPS.

VERACRUZ

COLIMAMICHOACAN

GUERRERO

OAXACA

CHIAPAS

TABASCO

CAMPECHE

YUCATAN

QU

INTA

NA

RO

OHIDALGO

TLAX.MEX.

PUEBLA

NUEVOLEON

G.M.(PC & UV)

G.M. (ENGINES)

CHRYSLER (PC & UV)

BMW (PC)

FORD(PC & UV)

MAZDA (TRUCKS)

VOLVO (TRUCKS)

KENWORTH(TRUCKS)TOYOTA -TIJUANA

SCANIA(TRUCKS)

NAVISTAR (TRUCKS)

JALISCO

Automotive Sector

PresidentCalderonannouncesinvestment for$3,000 milliondollars this yearcreating 30,000employees inthis sector

1. TIJUANA

•Sanyo

•Sony

•Matsushita

•Sharp

•Kiocera

10,AGUASCALIENTES

•Texas Instruments

•XEROX

•Siemens

11. GUADALAJARA

•IBMH P

•TECHNICOLOR

•SELECT

•TYCO

•KODAK

•VOGT ELECTRONIC

•SIEMMENS VDO

•SOLECTRON DE MEXICO

•FLEXTRONICS

•JABIL CIRCUIT

•BENCHMARK

•SANMINA - SCI

Map 1. Mexico: Electronic Network

2. MEXICALI

•Sony

•Daewoo

•Mitsubishi

•Goldstar

3. CHIHUAHUA

•MOTOROLA

•ALTEL

•KIOCERA

•JABIL

4. JUAREZ

TOSHIBA

PHILIPS

THOMSON

KENWOOD

ELECTROLUX

HACER

ELAMEX

PLEXUS

5. SALTILLO

•MABE

•HAMILTON

•BEACH

6. TORREON

•THOMSON

•7.REYNOSA

•DELCO (Auto)

•PHILIPS

•SONY

•MATSUSHITA (Auto)

•VITROMATIC

•NOKIA

•LUCENT TECHNOLOGIES

•FUJITSU (Auto)

•CONDURA (Auto)

•DELMOSA (Auto)

8, Monterrey

•PIONEER

•DANFOSS COMPRESSORS

•VITROMATIC

•MABE

•KODAK

•NIPPON DENSO (Auto)

•AXA Y AZAKI (Auto)

13. STATE OF MEXICO

•PANASONIC

•ELECTROLUX

•FILTER QUEEN

•HOOVER

•IMAN

•KOBLENZ

•MABE

•PHILIPS

•SUNBEAM

•OLIVETTI

•OLYMPIA

•BRAUN

•ERICSSON

•ALCATEL

•AMP

9. SAN LUIS POTOSI

•MABE GE

•MABE SANYO

14.PUEBLA

•GESTAR

•SINGER

•VITROMIC

1 2

12. QUERETARO

VISTAR

VITROMATIC

CLARION

DAEWOO

BLACK & DECKER

MABE

SINGER

SIEMMENS

3

4

5

6

7

13

8

11

910

12

14

15.CUERNAVACA

•NEC

15

1. TIJUANA

•Sanyo

•Sony

•Matsushita

•Sharp

•Kiocera

10,AGUASCALIENTES

•Texas Instruments

•XEROX

•Siemens

11. GUADALAJARA

•IBMH P

•TECHNICOLOR

•SELECT

•TYCO

•KODAK

•VOGT ELECTRONIC

•SIEMMENS VDO

•SOLECTRON DE MEXICO

•FLEXTRONICS

•JABIL CIRCUIT

•BENCHMARK

•SANMINA - SCI

Map 1. Mexico: Electronic Network

2. MEXICALI

•Sony

•Daewoo

•Mitsubishi

•Goldstar

3. CHIHUAHUA

•MOTOROLA

•ALTEL

•KIOCERA

•JABIL

4. JUAREZ

TOSHIBA

PHILIPS

THOMSON

KENWOOD

ELECTROLUX

HACER

ELAMEX

PLEXUS

5. SALTILLO

•MABE

•HAMILTON

•BEACH

6. TORREON

•THOMSON

•7.REYNOSA

•DELCO (Auto)

•PHILIPS

•SONY

•MATSUSHITA (Auto)

•VITROMATIC

•NOKIA

•LUCENT TECHNOLOGIES

•FUJITSU (Auto)

•CONDURA (Auto)

•DELMOSA (Auto)

8, Monterrey

•PIONEER

•DANFOSS COMPRESSORS

•VITROMATIC

•MABE

•KODAK

•NIPPON DENSO (Auto)

•AXA Y AZAKI (Auto)

13. STATE OF MEXICO

•PANASONIC

•ELECTROLUX

•FILTER QUEEN

•HOOVER

•IMAN

•KOBLENZ

•MABE

•PHILIPS

•SUNBEAM

•OLIVETTI

•OLYMPIA

•BRAUN

•ERICSSON

•ALCATEL

•AMP

9. SAN LUIS POTOSI

•MABE GE

•MABE SANYO

14.PUEBLA

•GESTAR

•SINGER

•VITROMIC

1 2

12. QUERETARO

VISTAR

VITROMATIC

CLARION

DAEWOO

BLACK & DECKER

MABE

SINGER

SIEMMENS

3

4

5

6

7

13

8

11

910

12

14

12. QUERETARO

VISTAR

VITROMATIC

CLARION

DAEWOO

BLACK & DECKER

MABE

SINGER

SIEMMENS

3

4

5

6

7

13

8

11

910

12

14

15.CUERNAVACA

•NEC

15

• Low cost

operation

• High skill labor

at low wages

• Strategic

Location

Aeronautic

Sector

MNCs from Mexico

• Emerging MNCs (“Trans-Latins”) from Mexicohave become an important phenomenon,particularly since the mid-1990s.

• Outward FDI by Trans-Latins is accounting foran increasing share of total FDI in Latin America.

• Their participation is mainly in basic industries,food and beverage, and services that are takingadvantage of proximity to the US.

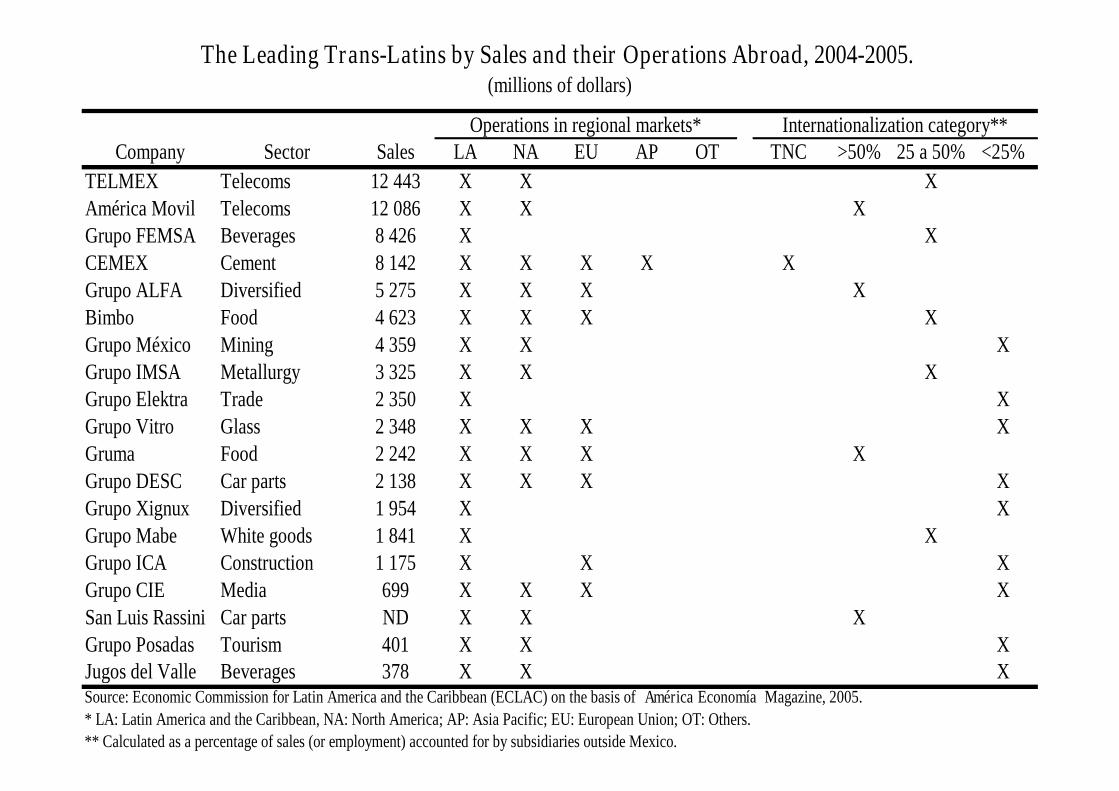

Company Sector Sales LA NA EU AP OT TNC >50% 25 a 50% <25%

TELMEX Telecoms 12 443 X X XAmérica Movil Telecoms 12 086 X X XGrupo FEMSA Beverages 8 426 X XCEMEX Cement 8 142 X X X X XGrupo ALFA Diversified 5 275 X X X XBimbo Food 4 623 X X X XGrupo México Mining 4 359 X X XGrupo IMSA Metallurgy 3 325 X X XGrupo Elektra Trade 2 350 X XGrupo Vitro Glass 2 348 X X X XGruma Food 2 242 X X X XGrupo DESC Car parts 2 138 X X X XGrupo Xignux Diversified 1 954 X XGrupo Mabe White goods 1 841 X XGrupo ICA Construction 1 175 X X XGrupo CIE Media 699 X X X XSan Luis Rassini Car parts ND X X XGrupo Posadas Tourism 401 X X XJugos del Valle Beverages 378 X X X

* LA: Latin America and the Caribbean, NA: North America; AP: Asia Pacific; EU: European Union; OT: Others.

** Calculated as a percentage of sales (or employment) accounted for by subsidiaries outside Mexico.

(millions of dollars)

The Leading Trans-Latins by Sales and their Operations Abroad, 2004-2005.

Operations in regional markets* Internationalization category**

Source: Economic Commission for Latin America and the Caribbean (ECLAC) on the basis of América Economía Magazine, 2005.

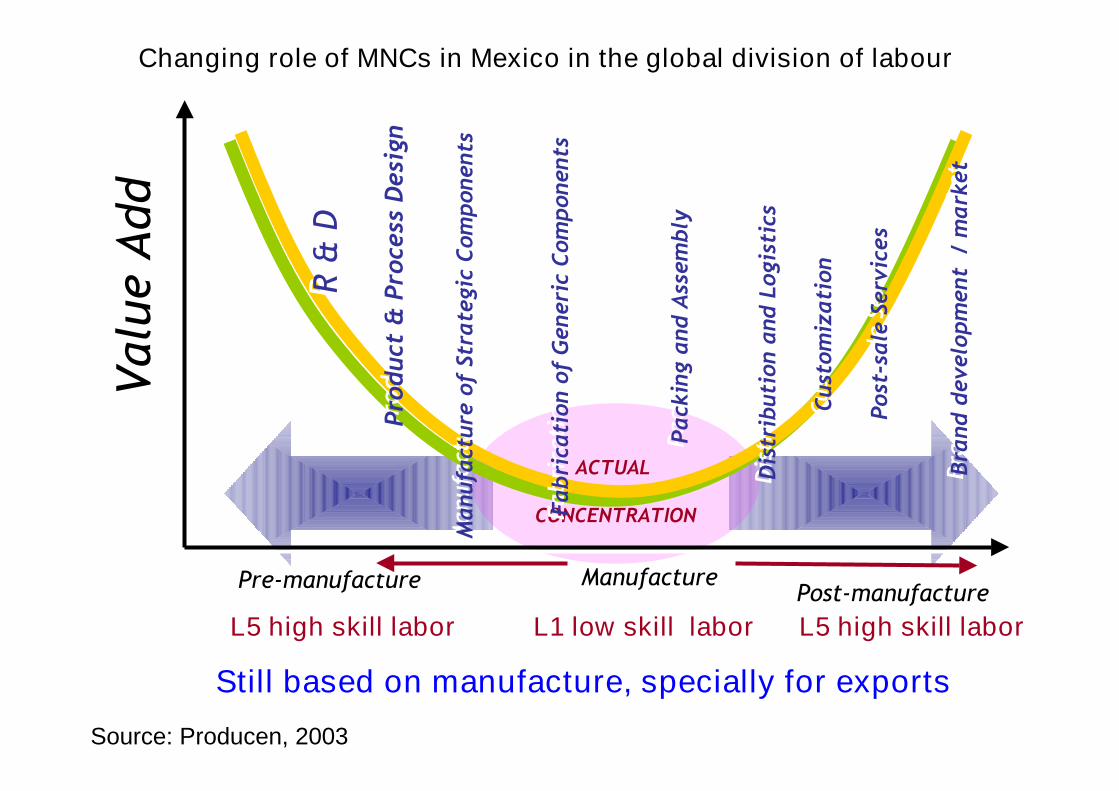

Still based on manufacture, specially for exports

ACTUAL

CONCENTRATION

Valu

eA

dd

Valu

eA

dd

Pre-manufacturePre-manufacture ManufactureManufacturePost-manufacturePost-manufacture

R&

DR

&D

Manufa

cture

of

Str

ate

gic

Com

ponents

Manufa

cture

of

Str

ate

gic

Com

ponents

Fabri

cati

on

of

Generi

cC

om

ponents

Fabri

cati

on

of

Generi

cC

om

ponents

Pro

duct

&Pro

cess

Desi

gn

Pro

duct

&Pro

cess

Desi

gn

Pack

ing

and

Ass

em

bly

Pack

ing

and

Ass

em

bly

Cust

om

izati

on

Cust

om

izati

on

Dis

trib

uti

on

and

Logis

tics

Dis

trib

uti

on

and

Logis

tics

Bra

nd

develo

pm

ent

/m

ark

et

Bra

nd

develo

pm

ent

/m

ark

et

Post

-sale

Serv

ices

Post

-sale

Serv

ices

L1 low skill laborL1 low skill labor L5 high skill laborL5 high skill laborL5 high skill laborL5 high skill labor

Changing role of MNCs in Mexico in the global division of labour

Source: Producen, 2003

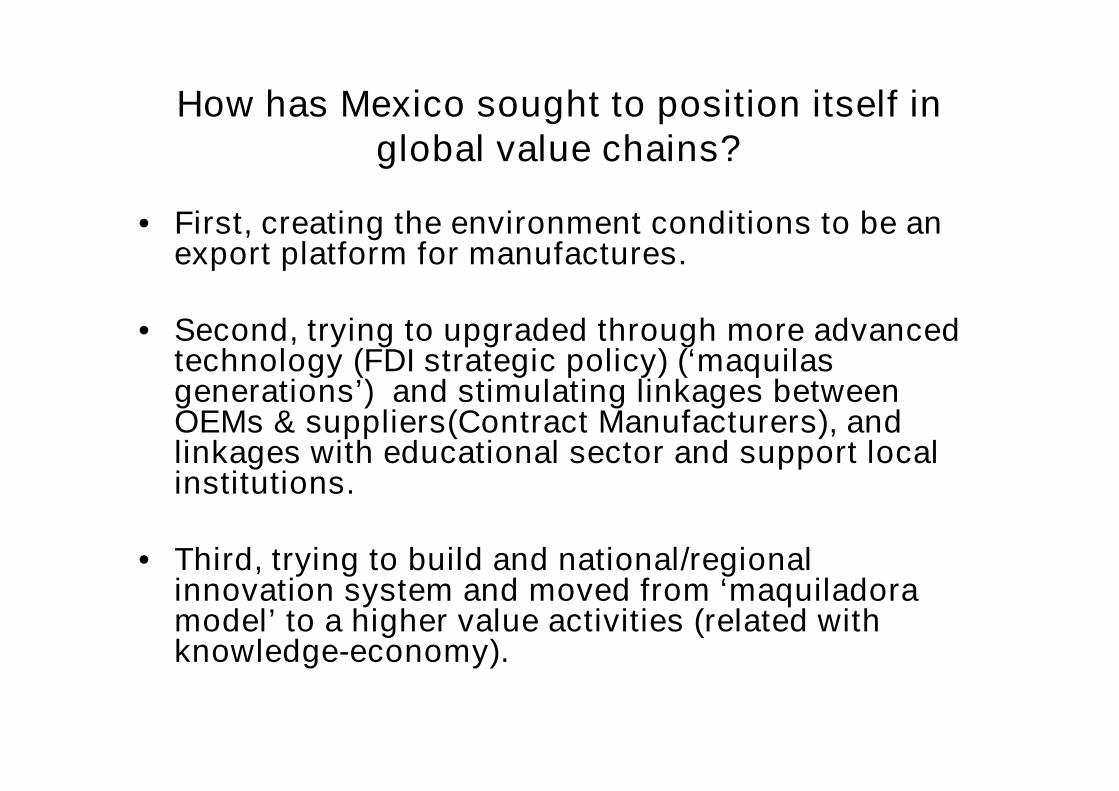

How has Mexico sought to position itself inglobal value chains?

• First, creating the environment conditions to be anexport platform for manufactures.

• Second, trying to upgraded through more advancedtechnology (FDI strategic policy) (‘maquilasgenerations’) and stimulating linkages betweenOEMs & suppliers(Contract Manufacturers), andlinkages with educational sector and support localinstitutions.

• Third, trying to build and national/regionalinnovation system and moved from ‘maquiladoramodel’ to a higher value activities (related withknowledge-economy).

What are the HR, employment and publicpolicy implications of this strategy?

• Volatility in the volume of employment.

• High skill workers

• Labor flexibility

• Cost reduction pressures or Low wagestrategy mainly because of the presuresfrom China

Thank You