Embed Size (px)

Citation preview

Country Profile 2006

Myanmar (Burma) This Country Profile is a reference work, analysing the country�s history, politics, infrastructure and economy. It is revised and updated annually. The Economist Intelligence Unit�s Country Reports analyse current trends and provide a two-year forecast.

The full publishing schedule for Country Profiles is now available on our website at www.eiu.com/schedule The Economist Intelligence Unit 26 Red Lion Square London WC1R 4HQ United Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managing operations across national borders. For over 50 years it has been a source of information on business developments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where the latest analysis is updated daily; through printed subscription products ranging from newsletters to annual reference works; through research reports; and by organising seminars and presentations. The firm is a member of The Economist Group.

London The Economist Intelligence Unit 26 Red Lion Square London WC1R 4HQ United Kingdom Tel: (44.20) 7576 8000 Fax: (44.20) 7576 8500 E-mail: [email protected]

New York The Economist Intelligence Unit The Economist Building 111 West 57th Street New York NY 10019, US Tel: (1.212) 554 0600 Fax: (1.212) 586 0248 E-mail: [email protected]

Hong Kong The Economist Intelligence Unit 60/F, Central Plaza 18 Harbour Road Wanchai Hong Kong Tel: (852) 2585 3888 Fax: (852) 2802 7638 E-mail: [email protected]

Website: www.eiu.com

Electronic delivery This publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, online databases and as direct feeds to corporate intranets. For further information, please contact your nearest Economist Intelligence Unit office

Copyright © 2006 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However, the Economist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 1364-3533

Symbols for tables �n/a� means not available; ��� means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

RANGOON)RANGOON)

MawlamyinMawlamyine (Moulmein)e (Moulmein)MaubinMaubinMartabanMartaban

ThatonThaton

KyaiktoKyaikto

NyaungleNyaunglebinbin

Dawei (TaDawei (Tavoy)voy)

TanintTaninth

YANGON (RANGOON)

MandalayMandalay

PyinmanaPyinmana

Taung-gyiTaung-gyi

KengtungKengtungAmarapuraAmarapura

KyaukseKyaukse

MaymyoMaymyo

Mandalay

Mawlamyine (Moulmein)

HenzadaHenzada Bago (Pegu)Bago (Pegu)Bago (Pegu)

Pathein (Bassein)

Bogale

MaubinMartaban

Thaton

Kyaikto

Nyaunglebin

ToungooToungoo

SagaingSagaing

PromeProme(Pye)(Pye)

MyanaungMyanaung

ChaukChauk

PakokkuPakokku

MeiktilaMeiktila

Toungoo

Pyinmana

Taung-gyi

Kengtung

Mong Yangong YangMong Yang

Amarapura

Lashio

MyitkMyitkyinayina

KathaKatha BhaBhamomo

PutaoPutao

Myitkyina

Katha Bhamo

Putao

Namtu

HsipawHsipawKyaukmeKyaukme

KalKalemyoemyo KalewaKalewa MogokMogok

HsipawHakaHakaHaka

Kyaukme

Sagaing

Kyaukse

Maymyo

Prome(Pye)

Paletwa

Melun

Myanaung

KayaikkaKayaikkami (Amherst)mi (Amherst)Kayaikkami (Amherst)Kungyangon

Henzada

Sandoway

Kyeintali

MyohaungMyohaung

ThayetmyoThayetmyoThayetmyo

MagyichaungSittwe

Myohaung

MinbuMinbuMinbuAyeyarwady R.Ayeyarwady R.(Irrawaddy R.)(Irrawaddy R.)Ayeyarwady R.(Irrawaddy R.)

Ramree Is.

Cheduba Is.

Gulf ofMartaban

YenangyaungYenangyaungYenangyaung

Chauk

PakokkuMyingyanMyingyanMyingyan

Monywa

Shwebo

Kalemyo

Tamu

Kalewa

Mawlaik

Mogok

Meiktila

Dawei (Tavoy)

Mergui

Tanintharyi (Tenasserim)

Ye

MYANMARMYANMAR(BURMA)(BURMA)MYANMAR(BURMA)

THAILAND

VIETNAM

LAOS

INDIA

BHUTAN

CHINA

BANGLADESH

INDIANOCEAN

Bay of Bengal

Andaman Sea

Gulf of ThailandMergui

archipelago

Ayey

arw

ad

yR

.(I

rraw

add

yR

.(I

rraw

add

yR

.

Chin

dwin

R.

Chindwin

R(Salween R.)

Thanlwin R.

Thanlwin R.

Moei R

Kaladan R.

0 km 50 100 150 200

0 miles 50 100

© The Economist Intelligence Unit Limited 2006

November 2006

Main railway

Main road

International boundary

Main airport

Capital

Major town

Other town

Pre-1989 names( )

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Comparative economic indicators, 2005

Gross domestic product(US$ bn)

Sources: Economist Intelligence Unit estimates; national sources.

0 50 100 150 200 250 300

Laos

Cambodia

Myanmar

Vietnam

Singapore

Malaysia

Thailand

Indonesia

0.0 1.0 2.0 3.0 4.0 5.0 6.0

Myanmar

Cambodia

Laos

Vietnam

Indonesia

Thailand

Malaysia

Singapore

0.0 2.0 4.0 6.0 8.0 10.0 12.0

Singapore

Malaysia

Thailand

Cambodia

Laos

Vietnam

Myanmar

Indonesia

0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0

Thailand

Malaysia

Myanmar

Indonesia

Singapore

Laos

Vietnam

Cambodia

Gross domestic product(% change, year on year)

Sources: Economist Intelligence Unit estimates; national sources.

Consumer prices(% change, year on year)

Sources: Economist Intelligence Unit estimates; national sources.

Gross domestic product per head(US$ '000)

Sources: Economist Intelligence Unit estimates; national sources.

26.9

Myanmar (Burma) 1

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Contents

Myanmar (Burma)

3 Basic data

4 Politics 4 Political background 6 Recent political developments 8 Constitution, institutions and administration 10 Political forces 12 International relations and defence

14 Resources and infrastructure 14 Population 16 Education 16 Health 17 Natural resources and the environment 17 Transport, communications and the Internet 19 Energy provision

20 The economy 20 Economic structure 21 Economic policy 24 Economic performance 26 Regional trends

27 Economic sectors 27 Agriculture 29 Mining and semi-processing 30 Manufacturing 31 Construction 31 Financial services 33 Other services

33 The external sector 33 Trade in goods 36 Invisibles and the current account 36 Capital flows and foreign debt 38 Foreign reserves and the exchange rate

39 Regional overview 39 Membership of organisations

41 Appendices 41 Sources of information 42 Reference tables 42 Population estimates 42 Labour force 43 Transport statistics 43 National energy statistics

2 Myanmar (Burma)

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

43 Government tax revenue 44 Money supply, credit and interest rates 44 Gross domestic product 44 Gross domestic product by expenditure 45 Gross domestic product by sector 45 Consumer price index 45 Output of key crops 45 Production of livestock and fish 46 Timber production 46 Minerals production 46 Banking statistics 46 Tourist arrivals 47 Exports 47 Key exports (volume) 48 Imports 48 Merchandise trade balance 48 Main trading partners 49 Balance of payments 49 Foreign direct investment approvals 50 External debt 51 Foreign reserves 51 Exchange rates

Myanmar (Burma) 3

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Myanmar (Burma)

Basic data

676,563 sq km

53.2m (fiscal year 2003/04, Central Statistical Organisation)

Population in �000 (1983 census)

Yangon 2,513 Bago 320 Mandalay 533 Moulmein 220

Note. In the text, places are referred to by their pre-1989 names, apart from Yangon and Myanmar. Pre-1989 names appear in brackets on the map at the beginning of this report

Subtropical

Hottest month, April, 24-36°C; coldest month, January, 18-23°C; driest month, January, 3 mm average rainfall; wettest month, July, 582 mm average rainfall

Burmese; numerous other minority languages are also in use, such as Karen and Shan

Derived from the UK system. Some other units are in use. For example, 0.9842 long or imperial tons=1 metric tonne=1.10231 short tons. Local measures include: 1 lakh=100,000 units; 1 crore=10,000,000 units; 1 viss or peiktha=100 ticles=1.6 kg; 1 basket (paddy)=20.9 kg; 1 basket (rice)=34 kg

1 kyat (Kt)=100 pyas. Average official exchange rate in 2005: Kt5.76:US$1. Average free-market exchange rate in 2005: K1,095:US$1 (based on private estimates). Average free-market exchange rate in October 2006: Kt1,300:US$1

6.5 hours ahead of GMT

April 1st-March 31st

January 4th (Independence Day); February 12th (Union Day); March 2nd (Peasants� Day); March 27th (Armed Forces� Day); April 13th-17th (Thingyan, New Year) May 1st (Workers� Day); July 19th (Martyrs� Day); December 25th (Christmas Day); plus other holidays, the timing of which depends on lunar sightings

Currency

Time

Fiscal year

Public holidays, 2006

Population

Main towns

Climate

Weather in Yangon (altitude 5 metres)

Language

Measures

Land area

4 Myanmar (Burma)

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Politics

Myanmar!s ruling military junta, known as the State Peace and Development Council (SPDC), came to power in 1988 after violently suppressing widespread pro-democracy protests. The main opposition party, the National League for Democracy (NLD), won the last election, which was held in May 1990. However, the junta has never recognised this result and has held on to power. Under intense international pressure, in August 2003 the SPDC outlined plans for limited political reform, including the completion of a new constitution. But progress has been slow, and the junta seems intent on putting into place a constitution that leaves sweeping powers in the hands of the military, ignoring the demands of opposition political and ethnic groups.

Political background

On January 4th 1948 the Union of Burma (as Myanmar was known before the military government changed the name in 1989) gained independence, ending more than 60 years of British rule. The fight for independence was spearheaded by the Anti-Fascist People!s Freedom League (AFPFL), under the leadership of Aung San and U Nu. The AFPFL won a landslide election victory in April 1947. However, in July 1947 Aung San was assassinated, and it was U Nu who became prime minister following independence. The AFPFL won two further elections, and Myanmar enjoyed 12 years of democratic government"interrupted only by a two-year period under a military caretaker government led by the army chief-of-staff, General Ne Win. In March 1962 General Ne Win launched a coup d!état, replacing the government with a military-run revolutionary council, and plunging Myanmar into an era of authoritarian military rule that persists today.

In 1972, in the face of growing discontent, General Ne Win and his senior commanders retired from the army, but remained in control of the government. In 1974 a new constitution declared Myanmar to be a socialist one-party state, ruled by the military!s Burma Socialist Programme Party (BSPP, or Lanzin Party). The BSPP embarked on the so-called Burmese Way to Socialism, of which the central element was economic self-sufficiency. Myanmar was shut off from the outside world, a policy that resulted in economic stagnation.

In October 1987, as the economy deteriorated, student demonstrations were held in the capital, Yangon. Widespread protests began in March 1988, increasingly focused around the leadership of Aung San Suu Kyi, the daughter of the independence era leader, Aung San. In July 1988 General Ne Win resigned as chairman of the BSPP, and was replaced by General Sein Lwin, but the protests gathered strength until on August 8th 1988 troops were ordered to fire on unarmed demonstrators. Several thousand civilians are estimated to have been killed in the ensuing bloodbath.

The demonstrations continued, forcing General Sein Lwin to resign within weeks of coming to power. His successor"a civilian, Maung Maung"lasted less than one month, during which time a multiparty election was planned. On

The pro-democracy movement is crushed in 1988

Myanmar has a long history of military rule

Myanmar (Burma) 5

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

September 18th 1988 the military again formally took power, nominally under the leadership of General Saw Maung"although with General Ne Win!s involvement behind the scenes. The junta formed a military council, called the State Law and Order Restoration Council (SLORC), to rule the country. The junta also dismantled the socialist one-party order and bowed to the demonstrators! demand that an election be held.

More than 200 parties registered for the 1990 election. The main contenders were the National Unity Party (NUP, a renamed BSPP), the NLD and major ethnically based parties. Although Aung San Suu Kyi, the NLD�s leader, was placed under house arrest, her party managed to record a convincing election victory, taking almost 60% of the popular vote. This would have given the NLD 392 seats in the 485-seat legislature, compared with only ten seats won by the pro-junta NUP. But the junta refused to accept the result or to convene parliament, and has remained in power ever since.

Senior General Than Shwe, the commander-in-chief of the army, succeeded General Saw Maung as chairman of the junta!s ruling council in 1992. In November 1997 the junta was reshuffled and renamed the State Peace and Development Council (SPDC), but there was no marked change in its policies, with major decisions being made by the military council. (There is an additional government structure headed by a prime minister, but the government comprises military appointees, and does not act as a check on the powers of the ruling military council.)

General election results, May 1990 % of vote No. of seatsNational League for Democracy 59.9 392

Shan Nationalities' League for Democracy 1.7 23

Arakan League for Democracy 1.2 11

National Unity Party 21.2 10

Mon National Democratic Front 1.0 5

National Democratic Party for Human Rights 0.9 4

Chin National League for Democracy 0.4 3

Party for National Democracy 0.5 3

Union Paoh National Organisation 0.3 3

Kachin State National Congress for Democracy 0.1 3

Others 12.8 28

Total 100.0 485

Source: Press reports.

Throughout the 1990s the junta made every effort to entrench itself and to side-line the NLD. Most political activities were severely restricted, and NLD members and their families were subjected to harassment, including imprison-ment and torture. By the late 1990s most NLD party offices had been forced to close and hundreds of NLD supporters were in jail. Aung San Suu Kyi was released from house arrest in 1995, but was returned to confinement from September 2000 to May 2002. Despite this, the NLD continued to campaign for the result of the 1990 election to be recognised. In September 1998 the NLD formed a ten-member body, known as the Committee Representing the People!s

The junta rejects the result of the 1990 election

The junta entrenches its grip, and sidelines the NLD

6 Myanmar (Burma)

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Parliament (CRPP), to highlight the demands of the NLD and other parties that won seats in 1990.

A number of Myanmar!s many ethnic groups have been struggling for greater autonomy since independence. At times more than 40 ethnic organisations have been engaged in armed conflict with the military regime. In 1989 a series of ceasefires were concluded. However, a number of groups continued their armed struggle. For years the SPDC has used brutal tactics including torture, rape, forced labour, extra-judicial killings and forced relocation on a massive scale in a bid to stamp out ethnic minority opposition movements and to control ethnic populations. International agencies, including the UN, have strongly criticised the atrocities committed by the junta against ethnic minority peoples. As a result of such policies and the continued fighting, there are around 140,000 ethnic-minority refugees in camps in Thailand and an even larger number of ethnic-minority people displaced from their homes within Myanmar.

Recent political developments

After years of impasse, in 2002 the SPDC briefly relaxed restrictions on the NLD. Small groups of NLD political prisoners were released and some party offices were reopened. In May 2002 Aung San Suu Kyi was again released from house arrest and allowed to travel outside Yangon for the first time in many years and large crowds of supporters turned out to welcome her. Alarmed at this show of public support, the SPDC quickly ended the détente. In late May 2003 Aung San Suu Kyi!s motorcade was attacked during a tour of the north of the country and a number of her supporters were killed or injured. Aung San Suu Kyi was subsequently jailed by the military, as were around 70 of her supporters and other senior NLD leaders. Although most were eventually released, Aung San Suu Kyi and the NLD!s vice-chairman, Tin Oo, were moved from jail and once again placed under house arrest in Yangon. Both were still being held in October 2006, despite repeated calls from the UN and regional allies to release political prisoners, including Aung San Suu Kyi.

In August 2003, under intense international pressure, the SPDC announced a road map for political reform. The steps outlined included reconvening the National Convention (NC), which was suspended in 1996, to draft a new constitution; holding a national referendum to approve the new constitution; holding parliamentary elections; and forming a new government. There was nothing new in the road map"the SPDC has been promising for years to hold a fresh election after a new constitution has been completed and progress so far seems to confirm that the SPDC intends to entrench its hold on power.

The NC met for a few weeks in 2004, 2005 and 2006; the latest session began in October 2006. However, the junta placed tight restrictions on debate; delegates were not permitted to question the SPDC!s objectives or challenge the military in any way. The sessions were boycotted by the NLD, partly in protest at such restrictions and partly because the junta continued to detain its top

Ethnic groups are oppressed

A �road map� for political reform moves slowly

The SPDC contains the opposition

Myanmar (Burma) 7

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

leaders. The junta has not given any timetable for completion of the road map, and progress has been slow.

The legacy of years of military dictatorship means that there is no clear process for the transfer of power, and there are faultlines within the SPDC itself. On the whole, the SPDC has been able to keep a fairly united front. However, tensions have increased as the SPDC has struggled to find a way to deal with opposition demands and growing international pressure for political reform, while at the same time attempting to shore up its own grip on power. Factional splits came to a head in October 2004 when General Khin Nyunt (for years one of the most powerful members of the junta, holding the post of SPDC secretary-1 and then prime minister) was ousted from power. Following his fall, the military intelligence body he had helped to set up was dismantled, and hundreds of his supporters have since been investigated or jailed. Khin Nyunt himself is now under house arrest in Yangon, having been given a long jail term on charges of corruption. With Khin Nyunt gone, the ageing head of the junta, Senior General Than Shwe, has sought to secure his legacy through promotion of his allies. But he has had to balance competing factions within the junta. In 2005-06 there were persistent rumours of growing tensions between the SPDC vice-chairman, Deputy Senior General Maung Aye, and a faction surrounding the army chief-of-staff, General Thura Shwe Mann, who appeared to be growing in favour with Senior General Than Shwe.

In 2004 the SPDC was seemingly close to settling one of the country�s longest-running ethnic conflicts, reaching an informal ceasefire with the Karen National Union (KNU), the largest group still in armed conflict with the junta. Following Khin Nyunt�s removal, the SPDC has become even less tolerant of rebel groups, pushing hard for them to disarm. As a result, a number of existing ceasefires have unravelled. The SPDC stepped up military campaigns against rebel groups in 2005 and 2006, continuing widespread human rights abuses against civilians in Karen, Karenni and Shan areas.

Important recent events

May 2002

After being detained since September 2000, Aung San Suu Kyi is released from house arrest and permitted to meet with supporters.

May 2003

Aung San Suu Kyi and other senior National League for Democracy (NLD) leaders are detained and jailed following an attack on NLD supporters orchestrated by the State Peace and Development Council (SPDC).

August 2003

General Khin Nyunt takes over as prime minister but loses his position in the SPDC. Soon after taking the post, he announces a �road map� for political reform, but refuses to commit to a timetable or to discuss a possible role for the NLD.

The SPDC struggles to keep a united front

Ethnic conflict escalates

8 Myanmar (Burma)

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

May 2004

The National Convention (a body tasked with drafting a new constitution) is reopened. The NLD boycotts the convention to protest against the continued detention of its leaders.

October 2004

General Khin Nyunt, who is regarded as one of the three most powerful members of the junta, is sacked, resulting in the dismantling of the military intelligence service that he headed.

May 2005

A series of large bombs explode in a Yangon convention centre and two shopping centres, killing at least 20 people and injuring at least 160. The SPDC initially blamed exiled opposition groups, particularly the National Coalition Government of the Union of Burma, although no group has taken responsibility.

July 2005

Myanmar relinquishes its turn to chair the Association of South-East Asian Nations (ASEAN) as scheduled from late 2006. ASEAN members feared the group!s international credibility would have been damaged if Myanmar had taken the chair.

March 2006

The relocation of the government!s ministries to the country!s newly established administrative capital, Naypyidaw, is completed.

September 2006

The US succeeds in getting sufficient support to put "the situation in Myanmar" on the UN Security Council!s formal agenda for discussion. China and Russia vote against the move.

October 2006

The "88 Generation" of students launches a petition for the release of political prisoners, and according to the petition!s organisers more than half a million people signed up. In a rare mass public gathering, the group holds a vigil at the Shwedagon pagoda in Yangon calling for the release of all political prisoners.

Constitution, institutions and administration

In 1988 the junta suspended the 1974 constitution and abolished all state institutions, including parliament and the civilian courts. The junta claimed (after the event) that the 1990 election had been held in order to elect representatives to the NC. The NC first met in January 1993. However, of its 702 members only 106 (15%) were elected representatives, the rest being appointed by the junta. In November 1995 the NLD was expelled from the convention for protesting against the restrictions on debate. The convention was closed the following year.

In 2003 the junta unveiled its road map for political reform, starting with completion of a draft constitution. The NC was reconvened for short sessions in 2004, and again in 2005 and 2006. However, the SPDC imposed tight restrictions on debate, and the NLD continued to boycott the convention. By

Work on a new constitution continues

Myanmar (Burma) 9

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

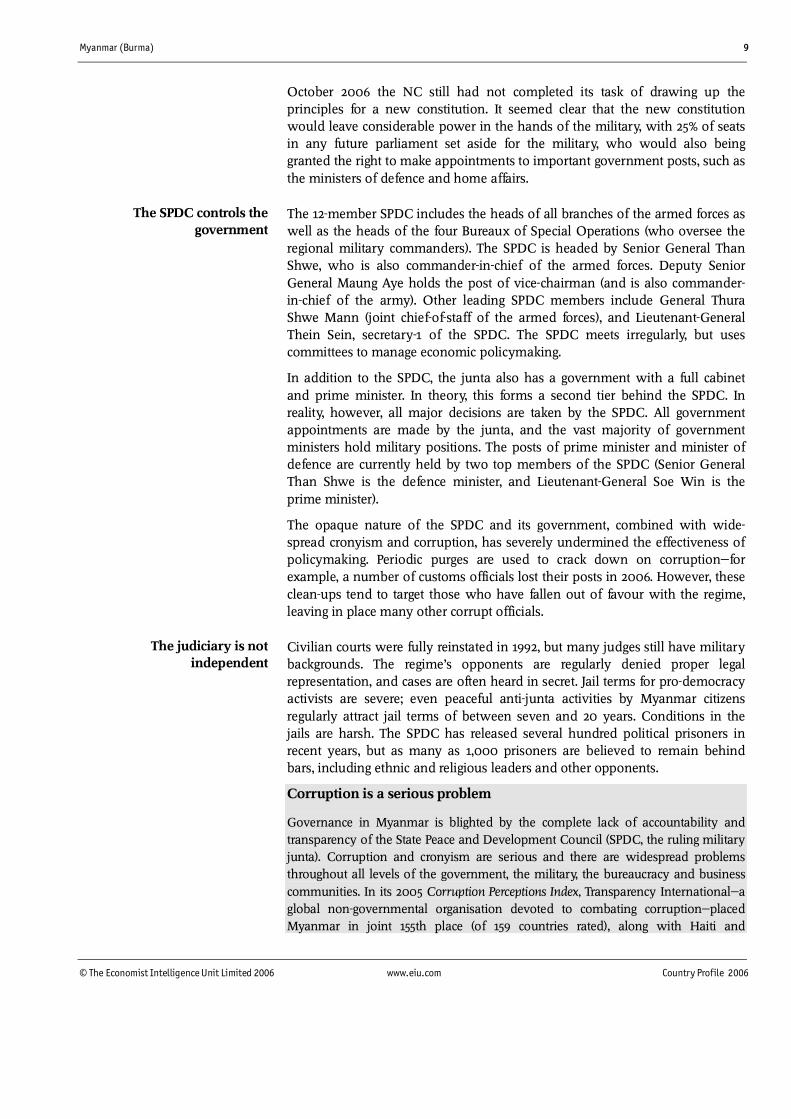

October 2006 the NC still had not completed its task of drawing up the principles for a new constitution. It seemed clear that the new constitution would leave considerable power in the hands of the military, with 25% of seats in any future parliament set aside for the military, who would also being granted the right to make appointments to important government posts, such as the ministers of defence and home affairs.

The 12-member SPDC includes the heads of all branches of the armed forces as well as the heads of the four Bureaux of Special Operations (who oversee the regional military commanders). The SPDC is headed by Senior General Than Shwe, who is also commander-in-chief of the armed forces. Deputy Senior General Maung Aye holds the post of vice-chairman (and is also commander-in-chief of the army). Other leading SPDC members include General Thura Shwe Mann (joint chief-of-staff of the armed forces), and Lieutenant-General Thein Sein, secretary-1 of the SPDC. The SPDC meets irregularly, but uses committees to manage economic policymaking.

In addition to the SPDC, the junta also has a government with a full cabinet and prime minister. In theory, this forms a second tier behind the SPDC. In reality, however, all major decisions are taken by the SPDC. All government appointments are made by the junta, and the vast majority of government ministers hold military positions. The posts of prime minister and minister of defence are currently held by two top members of the SPDC (Senior General Than Shwe is the defence minister, and Lieutenant-General Soe Win is the prime minister).

The opaque nature of the SPDC and its government, combined with wide-spread cronyism and corruption, has severely undermined the effectiveness of policymaking. Periodic purges are used to crack down on corruption"for example, a number of customs officials lost their posts in 2006. However, these clean-ups tend to target those who have fallen out of favour with the regime, leaving in place many other corrupt officials.

Civilian courts were fully reinstated in 1992, but many judges still have military backgrounds. The regime�s opponents are regularly denied proper legal representation, and cases are often heard in secret. Jail terms for pro-democracy activists are severe; even peaceful anti-junta activities by Myanmar citizens regularly attract jail terms of between seven and 20 years. Conditions in the jails are harsh. The SPDC has released several hundred political prisoners in recent years, but as many as 1,000 prisoners are believed to remain behind bars, including ethnic and religious leaders and other opponents.

Corruption is a serious problem

Governance in Myanmar is blighted by the complete lack of accountability and transparency of the State Peace and Development Council (SPDC, the ruling military junta). Corruption and cronyism are serious and there are widespread problems throughout all levels of the government, the military, the bureaucracy and business communities. In its 2005 Corruption Perceptions Index, Transparency International"a global non-governmental organisation devoted to combating corruption"placed Myanmar in joint 155th place (of 159 countries rated), along with Haiti and

The SPDC controls the government

The judiciary is not independent

10 Myanmar (Burma)

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Turkmenistan. Low wages for officials have helped to create a system where rent-seeking has become the norm. Money-laundering, smuggling and other forms of corruption are rife, in part owing to the impact of a huge illegal drug trade"Myanmar is one of the world�s top two producers of opiates (the other being Afghanistan), and a major producer of amphetamines.

Political forces

The SPDC is the dominant political force, and after decades of oppressive military rule it is widely feared and disliked. The current regime has spent heavily on expanding the military. According to the International Institute for Strategic Studies, the armed forces (including the police and militias) expanded from 170,000 in 1988 to 485,000 by 2005, including a regular army of 350,000. Poor pay and conditions may have weakened support for the junta within the rank-and-file of the armed forces, but not sufficiently to prove a serious threat to its grip on power.

The Union Solidarity Development Association (USDA), set up in 1993 to undertake public-works projects, has been groomed as the junta�s political wing. The USDA has frequently taken a quasi-political role (for example, holding large-scale rallies to proclaim support for the SPDC) and in 1997 the junta explicitly recognised the USDA as its political wing. Heavy-handed recruitment tactics"civil servants and high school students are pressured into joining boosted membership of the USDA to an estimated 16m by 2001. Given the pressure tactics used to increase membership, it is likely that real support for the junta within the USDA is limited, thereby making it impossible to predict whether USDA members would vote as directed if the SPDC does decide to risk another election. However, the SPDC does appear to be grooming the USDA to represent it in any future election, intending that USDA support combined with the 25% of seats already set aside for the military would be enough to ensure victory.

Only nine of the parties that contested the May 1990 election are still legally recognised. Of the 485 deputies elected in 1990, the majority have been detained, disqualified, have resigned under pressure or gone into exile. The NLD remains the most important source of political opposition to the junta. However, years of intense harassment by the junta have weakened the party. Most party offices have been forced to close and many party members forced to resign. The years of stalemate resulted in some tensions within the NLD itself, although there seems to be no threat to the core NLD leadership. During a brief thaw in 2001-02, most party offices were able to reopen, and key NLD leaders were able to meet supporters around the country. The massive turnout to some of these gatherings, despite intimidation by the USDA, suggests that popular support for the NLD remains strong.

The USDA takes shape as the military�s political wing

The NLD is the most important source of political opposition

The military remains the main source of power

Myanmar (Burma) 11

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Main political figures

Aung San Suu Kyi

The secretary-general of the National League for Democracy (NLD) and daughter of the independence hero, Aung San, she is extremely charismatic and her personal popularity within Myanmar remains high. She has been held under house arrest for most of the past 15 years; the most recent period of detention began in May 2003.

Senior General Than Shwe

Now in his late 70s, Senior General Than Shwe remains the most powerful man in the country. He heads the armed forces and is the chairman of the ruling military junta, the State Peace and Development Council (SPDC). He is also minister of defence in the government. Despite persistent rumours of ill-health and of tensions between him and Deputy Senior General Maung Aye, he still seems to be calling the shots.

Deputy Senior General Maung Aye

The vice-chairman of the SPDC, deputy commander-in-chief of the armed forces and army commander. He is regarded as a hardline opponent of dialogue with the NLD, and he appears to favour a return to isolationist economic policies. In theory, he is second in line to Senior General Than Shwe, but the SPDC chairman appears to be increasingly favouring General Shwe Mann.

Lieutenant-General Soe Win

Lieutenant-General Soe Win was promoted to secretary-1 in 2003, but lost some influence with his subsequent move to the post of prime minister. He is a patron of the Union Solidarity Development Association (USDA) and is widely believed to have been behind the attacks against NLD members on May 30th 2003.

General Shwe Mann

General Shwe Mann holds the post of joint chief-of-staff of the army, navy and air force. He appears to be gaining in influence owing to his close relationship with Senior General Than Shwe (who was his regional commander in the early 1980s).

Lieutenant-General Thein Sein

Lieutenant-General Thein Sein holds the post of secretary-1 of the SPDC. He also heads the committee in charge of the National Convention (the junta�s constitution-drafting body), and in this position he has been a vocal critic of any opposition to the constitution-drafting process and has been a strong defender of the junta!s plans for reform.

General Khin Nyunt

For many years his roles as head of military intelligence and secretary-1 of the SPDC made him one of the most powerful men in the country. Although he was certainly no reformer, he was perhaps more aware of the need to improve the junta!s image and seek some form of legitimacy. He was removed from office in a spectacular fall from power in October 2004, and is now under house arrest.

12 Myanmar (Burma)

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

A number of important ethnically based political parties performed well in the 1990 election. Most have since been forced to suspend their activities. In addition to the legally registered parties, a number of well-organised ethnic political groups have agreed ceasefires with the SPDC, giving them varying degrees of control over local affairs. Others have continued their armed conflict with the SPDC, demanding greater autonomy for ethnic minority areas and an end to human rights abuses. The latter groups include the KNU and the Karenni National Progressive Party (KNPP), and their armed wings. Low-level conflict continues to destabilise large regions of the country, primarily along the eastern border in Shan State, Karenni State and Karen State.

A number of pro-democracy political groups operate outside of Myanmar. Two prominent groups are the National Coalition Government of the Union of Burma (NCGUB), a government-in-exile comprising parliamentarians elected in 1990, and the All Burma Students Democratic Front (ABSDF), composed of students who fled the country following the 1988 massacres. The ABSDF has formed a political bloc to campaign for change from outside the country. In August 2005 the junta declared both the NCGUB and the ABSDF to be illegal organisations.

International relations and defence

Myanmar was admitted as a full member of the Association of South-East Asian Nations (ASEAN) in July 1997, and for years the group has followed a policy of "constructive engagement" with Myanmar, trying to avoid any overt criticism of the regime. However, ASEAN has become increasingly embarrassed by its newest member. After the SPDC!s attack on the NLD in May 2003, Myanmar!s fellow members of ASEAN departed from their traditional policy of non-interference in domestic affairs, publicly calling on the junta to begin talks with political opposition groups. Myanmar was due to take over the presidency of ASEAN in 2006, but a number of ASEAN members became alarmed at the potential negative impact on the group!s image. Under heavy behind-the-scenes pressure, the junta finally announced in mid-2005 that it would give up its turn to chair the group.

Although ASEAN has continued to present a united front, there are differences in approach to dealings with the junta. Some ASEAN members, notably Indonesia and Malaysia, kept up pressure on the junta in 2006, calling for the release of Aung San Suu Kyi and for faster progress on political reform. Thailand has been more conciliatory, although both the flow of drugs and illegal immigrants from Myanmar have remained contentious issues between the two governments. The newer members of ASEAN, Cambodia and Vietnam, have tended to be reluctant to voice criticism.

The junta has been shunned by many countries and international bodies for failing to recognise the results of the 1990 election, as well as for its extremely poor record on human and labour rights. Most donors"including Japan and the US"suspended aid after the September 1988 coup, and in 1997 the US banned new investment in Myanmar by US companies. After years of stalemate, in the

Ethnic groups are still fighting for autonomy

ASEAN increases behind-the-scenes pressure on the junta

Myanmar remains an international pariah

A number of political groups operate in exile

Myanmar (Burma) 13

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

late 1990s some countries began to look for ways to engage the SPDC. Japan, for example, resumed limited aid. This modest thaw came to an abrupt end in May 2003 when an SPDC-orchestrated attack on pro-NLD supporters and the detention of senior NLD leaders was greeted by international outrage. Since then, both Western and Asian nations have been grappling (so far, unsuccessfully) with how to bring about change in Myanmar.

The US and the EU continue to treat Myanmar as a pariah state. The US has taken a particularly strong stance, banning all imports from Myanmar in 2003. These sanctions, as well as the earlier investment ban, remained in place in 2006. In 2006 the US succeeded in getting Myanmar added to the formal agenda of the UN Security Council, despite resistance from China and Russia. The EU has imposed an arms embargo and other measures.

In a bid to counterbalance pressure from the West and some wavering of support within ASEAN, the junta has concentrated on cementing ties with China, which remains an important ally and a major trading partner, as well as a provider of regular military assistance to the junta. Efforts by Western nations to encourage China to exert some pressure on the junta have so far had little effect. The SPDC has also invested considerable effort into developing its economic and political ties with India and Bangladesh, resulting in a variety of investment projects and agreements to boost crossborder trade.

Security risk in Myanmar

Armed conflict

Parts of several of the border states (including Karen and Shan state) are under the territorial control of armed ethnic groups. In other areas, such as Karenni, ethnic groups control only a small area, but sporadic clashes with the ruling military regime continue outside of this zone. These intractable armed conflicts (some have con-tinued for more than 50 years) could potentially pose a risk to nearby transport and energy projects. The risk is mainly one of general instability rather than specific attacks on infrastructure. Some areas are heavily mined.

Terrorism

Terrorism poses a limited but growing problem. There are periodic bomb attacks in cities, including the capital, Yangon, and border towns. Such attacks have generally been small scale. However, a series of large bombs exploded in Yangon in a convention centre and two shopping centres in May 2005, killing at least 20 people and injuring at least 160. Such attacks do not seem to be targeted at foreign businesses, but they have taken place in busy public areas. The ruling military junta, the State Peace and Development Council (SPDC), generally blames such attacks on political and ethnic opposition groups. Such groups have strongly denied any involvement, and have no history of such attacks.

The junta seeks to promote wider ties

14 Myanmar (Burma)

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Unrest/demonstrations

Demonstrations pose a limited risk to business, with the risk generally that of being caught up in an uprising against the regime. The last major pro-democracy uprising occurred in 1988 and was brutally suppressed by the junta. The junta remains deeply unpopular among numerous segments of the population, including students, monks and ethnic minorities; there currently appears to be a low risk of another mass uprising. Public protests and union activity are not permitted.

Violent crime

Violent crime is a relatively low risk in Myanmar. However, anecdotal evidence suggests that there has been a rise in crime"including burglaries targeting foreign residents"in recent years, linked to the deterioration of the economy.

Organised crime

Organised crime poses a risk to business. There is a huge illegal economy based on the smuggling of goods and drugs. Myanmar is one of the world!s two largest producers of opium, and a major producer of amphetamines. Some armed groups that have reached ceasefires with the SPDC are heavily involved in the drug trade, most notably the United Wa State Army (UWSA), which has a militia numbering an estimated 16,000-20,000 and controls a large area of Shan state. A number of top UWSA leaders have been indicted on charges of drug-trafficking by the US. Money-laundering has contaminated the financial system, and Myanmar has been cited by the US and the multilateral Financial Action Task-Force (FATF) as being of prime money-laundering concern"although improvements in banking regulations allowed Myanmar to be taken off the FATF watchlist in 2006 (see Economic sectors: Financial services). Corruption is also endemic among sections of the government, bureaucracy and military.

Kidnapping/extortion

Kidnapping is a low risk in Myanmar. However, extortion, in the form of corruption by the government and bureaucracy, is widespread.

Resources and infrastructure

Population

According to Myanmar!s Central Statistical Organisation (CSO), the total population reached 53.2m in fiscal year 2003/04 (April-March). However, Myanmar�s population data are not totally reliable. For example, the Asian Development Bank (ADB) estimates that the population reached 55.5m in mid-2005, and the World Bank has a figure of 50.5m for 2005. According to a report by the UN Children!s Fund (UNICEF), an internal evaluation of population data in 1994 found under-reporting of 40% for births and 60% for deaths. Another complicating factor is the flow of refugees and migrant workers (see box: Myanmar!s mobile population). Myanmar has a fairly young population; around 33% was in the 0-14 age group in 2003/04, with only around 8% aged over 60 years.

Population and labour statistics are unreliable

Myanmar (Burma) 15

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Population, 2003/04 (fiscal year Apr-Mar) m % of total

Age group

0-14 17.4 32.7

15-59 31.5 59.2

60+ 4.3 8.1

Gender

Males 26.5 49.8

Females 26.8 50.2

Total population 53.2 100.0

Source: Central Statistical Organisation, Statistical Yearbook 2004.

In 2003/04 Myanmar!s labour force reached 26.4m people, according to ADB estimates. Traditionally, the agricultural sector accounts for over 60% of all employment. Lack of investment in education and repeated closure of the universities in recent years have reduced the number of skilled workers.

Myanmar�s mobile population

Refugees, migrant workers and internally displaced people

A repressive regime, civil conflict and a stagnant economy have resulted in a large flow of workers and refugees from Myanmar to neighbouring countries. Thailand alone has an estimated 1m illegal migrant workers"the majority from Myanmar"as well as around 140,000 refugees from Myanmar housed in border camps. Inside Myanmar, continued fighting in some border regions, and the junta!s harsh policies against ethnic minorities, including forced relocation, have led to many people being displaced from their homes. According to estimates by the Norwegian Refugee Council!s Global Database of Internally Displaced People (IDPs), in 2002 around 270,000 people in Myanmar had been driven into hiding in jungle areas, and a further 365,000 people were living in poor conditions in forced-relocation camps.

Data on the size of Myanmar!s numerous ethnic groups are contentious: no detailed census of ethnic minorities has been attempted since 1931. The 1931 census classified 65% of the population as belonging to the majority Burman group, followed by the Karen (9%), the Shan (7%), the Chin (2%), the Mon (2%), the Kachin (1%) and the Wa (1%). However, these figures may underestimate minority populations. There are many other smaller minority groups, the majority living in border states, although there are also sizeable minority populations living in the Burman-majority areas.

About 89% of the population is Buddhist. An estimated 4% is Christian (including large numbers of Karen, Karenni and Kachin) and a further 4% Muslim, mostly concentrated in Arakan state. A wide range of local languages are spoken among minority groups, but Burmese is the official language and is widely spoken and understood"although less so in the border states.

Buddhism is the main religion

16 Myanmar (Burma)

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Education

Underfunding remains a chronic problem throughout the education system. According to the World Bank, spending by the State Peace and Development Council (SPDC, the ruling military junta) on education totalled 1.3% of GDP in 2002, well below the average of 3.2% of GDP for other low-income countries in Asia. Teachers are poorly paid, and the quality of teaching is often low. According to World Bank data, the adult literacy rate stood at close to 90% in 2004, comparable with rates in Malaysia and Indonesia. However, this may be a considerable overestimate. Many children are taken out of school early either because their parents cannot afford ever-increasing unofficial fees or because falling family incomes mean that children have to start work early. According to World Bank estimates, in 2005 only around 40% of all children at secondary school age were actually enrolled in secondary school, compared with an average of 71% for East Asia and the Pacific.

At the other end of the system, higher education has frequently been disrupted over the past decade. The junta regularly closed down the universities, some-times for years at a time, in an effort to prevent student dissent. The majority of universities were reopened in 2000, but courses were shortened in order to push through the backlog of students.

There has been a rise in private classes in subjects such as English and computing"but these are mainly found in urban areas and are only accessible to the relatively well-off. Traditional monastic schools, which have historically played an important role in education, can only go so far in making up the shortfall left by the junta�s lack of investment in education. As a result of these problems, the overall standard of education in Myanmar, particularly in rural areas, is believed to have declined sharply in recent years.

Health

A UNICEF report has described a "dramatic decline" in spending on healthcare in the 1990s, and IMF figures reveal that spending on health was equivalent to just 0.1% of GDP in the second half of the 1990s. As a result, much of the population has access to only basic healthcare, or none at all. According to the UN Development Programme (UNDP), 35% of children under the age of five in Myanmar were underweight in the period 1995-2002. Border areas suffer the worst, with a higher incidence of diseases such as HIV/AIDS, tuberculosis and malaria. According to the World Bank, national life expectancy was 60.8 years in 2004 compared with an average of 70.3 in East Asia and the Pacific. Infant mortality stood at 76 per 1,000 live births in 2004 compared with an average of 29 in East Asia and the Pacific, with a further 106 children per 1,000 dying before their fifth birthday. Private clinics have emerged, but are relatively expensive and located mainly in urban areas.

The junta's policies have hit education hard

Health indicators paint a gloomy picture

Myanmar (Burma) 17

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

According to UNICEF, an estimated 330,000 people were living with HIV/AIDS in 2003. Migrant workers play a role in spreading the disease to other groups. The junta was initially reluctant to acknowledge the scope of the problem, and public health campaigns have been limited.

Natural resources and the environment

Myanmar has rich natural resources, including fertile agricultural land, a range of minerals and extensive forests. The agricultural sector has great potential. Among the most economically important crops are rice, pulses, oilseeds, timber, rubber, cotton, and many fruits and spices. However, agricultural production is held back by a lack of investment, and the area of land under cultivation remains unusually low. In fiscal year 2003/04 (April-March) only 15.9% of the total land area was cultivated, with a further 9.7% officially classified as "wasteland suitable for cultivation".

Myanmar!s rivers and its 2,832-km coastline provide rich waters for fishing (as well as great hydroelectricity potential). Myanmar also has rich forest resources. The Ministry of Agriculture estimates that in 2004/05 just under 50% of the total land area was forested (of which 22.7% was set aside in forest reserves). According to the Ministry of Forestry, Myanmar has recorded 7,000 plant species, of which 1,070 are endemic. The most economically important forest resources are teak and other hardwoods"Myanmar accounts for around 75% of the world!s remaining teak. Despite bans on logging exports, hardwood cutting continues and over-logging is a serious problem in some areas.

Myanmar has major offshore oil and gas reserves; following large-scale foreign investment, natural gas is now the country�s single largest source of export revenue. Myanmar also has reserves of a wide variety of minerals, ores and gemstones, including copper, gold, nickel, coal, lead, zinc, silver, gemstones, tungsten and tin. A full assessment of these resources has not been undertaken, but some mining specialists believe that Myanmar could be a major producer of several minerals, including tin and copper. However, investment in mining has been limited to date. All minerals and metals belong to the state (in some cases, this right has been all but ceded to regional military commanders). Investors must negotiate a profit- or production-sharing agreement with the state (or one of the state-owned mining companies), or in some cases with the regional military command.

Transport, communications and the Internet

Myanmar is a large country with a poor transport and communication infrastructure. The junta has built a number of new bridges and upgraded some important roads in recent years, which has helped to shorten some journey times. However, roads are poorly maintained (in some areas the junta uses forced labour for repair work). Many roads are unpaved, and during the rainy season some parts of the road network become impassable. Car traffic is limited outside of the main cities, as few people can afford a car. The public

Myanmar is rich in natural resources

Myanmar has abundant mineral and energy resources

The transport network is underfunded and unreliable

18 Myanmar (Burma)

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

transport system includes a limited rail network, as well as local bus services. Much of the rail network has been in place since the colonial era; aged tracks and rolling stock mean that lengthy delays are frequent. However, a number of efficient private coach companies have sprung up to service the main road routes. Domestic air travel is an expensive and unreliable alternative, and there are some concerns over the safety record of the domestic carrier, Myanmar Airways. Myanmar has two international airports located in the capital, Yangon, and in Mandalay, providing limited regional connections.

The poor state of the road and rail networks means that the country!s extensive inland waterways remain the principal means of transporting freight in many areas"waterways carried more freight than the railways (in actual tonnes rather than ton-miles) in 2003/04. Yangon seaport is the largest in the country, handling 90% of seaborne trade, but it cannot accommodate vessels of more than 10,000 tonnes. New seaports are being developed at Thilawa, on the outskirts of Yangon, and Kyaukpyu in Rakhine (Arakan) state.

Telecommunications services remain unreliable and expensive, despite some recent expansion of both the fixed-line and mobile networks. According to the International Telecommunication Union (ITU), in 2005 there were 476,200 land lines in Myanmar, close to double the number in 2000"but still less than one for every 100 people. In 2005 there were 695,600 fixed-line subscribers. In the same year, there were 183,400 mobile-phone subscribers, up from only 13,400 in 2000. The number of mobile-phone subscribers has increased rapidly since the country�s first GSM (Global System for Mobile Communications) mobile-phone service was launched in 2002, but this was from a low base.

The junta has often stated that it wants to improve the country!s telephone network. In August 2004 the Myanma Post and Telecommunications (MPT) announced plans for a Chinese-funded mobile switching centre that would enable the network to handle a further 100,000 connections. However, Myanmar�s poor business climate and high political risk have so far deterred major foreign investment, and the MPT lacks the capital to expand the network significantly on its own. The high price of mobile handsets has also kept a lid on demand.

Internet usage remains in its infancy in Myanmar. Low incomes mean that few people can afford high connection rates, even if they do have access to a telephone and a computer. A handful of private businesses have been granted licences to operate Internet cafes, but the cost remains out of reach for most people. Another problem is that e-mail communications are strictly monitored, and most sites originating outside Myanmar are blocked. These factors have prevented Myanmar from experiencing the boom in Internet usage recorded throughout much of the region. According to the ITU, Myanmar had 78,000 Internet users in 2005, or 0.15 per 100 people, giving it one of the lowest Internet penetration rates in the whole of Asia, lower than in Cambodia (0.3 users per 100 people) and Laos (0.4 users).

The telecommunications infrastructure is poor

The SPDC hampers development of the Internet

Myanmar (Burma) 19

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Myanmar has two Internet service providers, the MPT and Myanmar Teleport (formerly Bagan Cybertech). Myanmar Teleport was set up by Khin Nyunt!s son, Ye Naing Win, but was taken over by the junta after Khin Nyunt�s fall from power in late 2004.

Censorship of telecommunications and the media

Although the State Peace and Development Council (SPDC, the ruling junta) talks about promoting information technology (IT), it remains more concerned about security. In its 2005 �press freedom� index, Reporters Sans Frontières (an international non-governmental organisation that defends press freedom) placed Myanmar in 163rd place, out of 167 countries. All media, including the Internet, TV and print, are censored. The 1996 Computer Science Development Law regulates the use of modems and computers with networking capabilities. These tight regulations are backed by harsh penalties. In recent years the ruling junta has brought in technology to boost its surveillance capabilities, including the monitoring of cellular phones and e-mail. Firewalls ensure that most Internet sites are blocked (including widely used Internet e-mail accounts, such as Yahoo and Hotmail). The SPDC also tightly controls print and broadcast media. A range of privately run newspapers and magazines do exist alongside state-owned media, but all are heavily censored. Local-language radio broadcasts from foreign news organisations remain popular; many people rely on such broadcasts to hear any real news.

Energy provision

In February 2006 total installed electricity capacity by the state-owned Myanma Electric Power Enterprise (MEPE) was 1,775 mw, according to CSO data. The current electricity power supply is inadequate, and ageing power stations and heavy transmission losses result in frequent and lengthy power cuts, even in major cities. Many towns and villages are not yet connected to the national grid. According to a 1997 survey by the CSO, only 37% of all households had access to electricity for lighting (71.6% in urban areas and 17.7% in rural areas).

Natural gas accounts for 53% of electricity output, followed by hydropower (43%), thermal sources (3%) and diesel (less than 1%). Significant offshore natural-gas reserves have been discovered in recent years, but this has not helped the energy shortfall, as the majority of natural gas is exported (see Economic sectors: Mining and semi-processing). Instead, the Ministry of Electric Power�s long-term strategy to improve electricity supply is to invest in hydropower. A number of new hydropower plants are expected to come on stream over the next few years, producing energy for export and for domestic consumption. For example, hydropower projects are being developed on the Salween River in a series of joint ventures with Chinese and Thai firms. Environmental and local ethnic groups are deeply concerned at the expected serious social and environmental impact of the projects, which could displace large numbers of ethnic minority people and flood large areas.

The power supply is inadequate

20 Myanmar (Burma)

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

The economy

Economic structure Main economic indicators, 2005 Real GDP growth (output basis; %)a 13.8

Consumer price inflation (av; %) 9.4Current-account balance (US$ m)b 111.5

Foreign debt (US$ bn)b 7.2Official exchange rate (Kt:US$1) 5.8Free-market exchange rate (Kt:US$1)c 1,095

a Fiscal year 2003/04, official estimate. b 2004. c Economist Intelligence Unit estimate, annualaverage.

Sources: IMF, International Financial Statistics; World Bank, Global Development Finance.

Myanmar!s official economic statistics are unreliable, a situation that is not helped by the fact that Myanmar has a large informal sector and a massive extralegal economy, including illegal logging and widespread smuggling. These factors make it difficult to assess accurately the size and structure of the economy. However, according to the available official data, agriculture (including forestry and fishing) remains by far the biggest sector, accounting for 50.6% of current-price GDP in fiscal year 2003/04 (April-March), and employing close to 63% of the workforce in 1997/98 (latest data available). Overall, the industrial sector (including manufacturing, energy, mining and construction) remains relatively undeveloped, accounting for only 14.3% of GDP in 2003/04. Of the various industrial sectors, the energy sector is growing in importance as major natural-gas projects have come on stream. Myanmar has also developed a small manufacturing sector, accounting for 9.8% of current-price GDP in 2003/04, which is dominated by food processing and garment manufacturing. Among services sectors, the trade sector accounted for 22.6% of GDP in 2003/04, and transport and communications totalled just over 10% of GDP.

The huge disparity between the official exchange rate and the free-market rate makes regional comparisons difficult. Nevertheless, Myanmar counts among the world!s lowest-income countries by any measure. In 2003/04, based on official estimates, GDP per head stood at only US$162 at the free-market exchange rate. A survey undertaken in 1997 indicated that 23% of Myanmar!s population lived below the poverty line. This is a relatively small percentage compared with other countries of a similar level of income per head. However, other indicators, such as high rates of child malnutrition, suggest that the real incidence of poverty is far higher. In recent years, high inflation for even basic staples has severely reduced most people!s purchasing power, from already low levels.

Agriculture remains dominant

Myanmar is one of the world�s lowest-income countries

Myanmar (Burma) 21

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Comparative economic indicators, 2005

Myanmara Indonesiab Malaysia a Thailandb Vietnama

GDP (US$ bn) 8.9 281.3 130.6 b 176.6 52.8b

GDP per head (US$) 176 1,162a 4,997 2,697a 631b

GDP per head (US$ at PPP) 730 3,505a 10,776 8,450a 2,993

Consumer price inflation (av; %) 9.4b 10.5 3.0 b 4.5 8.3b

Current-account balance (US$ bn) 1.1 0.9 19.4 -3.7 0.3

Current-account balance (% of GDP) 12.1 0.3 14.9 -2.1 0.5

Exports of goods fob (US$ bn) 4.6 86.2 141.1 109.2 32.5

Imports of goods fob (US$ bn) -1.7 -63.9 -108.1 -106.1 -33.3

External debt (US$ bn) 6.8 138.6a 52.2 51.9a 20.2

Debt-service ratio, paid (%) 2.5 15.4a 5.6 8.5a 2.6

a Economist Intelligence Unit estimates. b Actual.

Source: Economist Intelligence Unit, CountryData.

A modest privatisation programme has stalled and the state sector!s share of GDP has remained steady at around 20% of constant-price GDP in recent years. The state totally dominates some sectors, including mining and power, and state-owned firms have an important role in transport, trade and manu-facturing. The military is heavily involved in business in sectors including gems and logging, through military-backed companies such as Union of Myanmar Economic Holdings (UMEH, sometimes referred to as Myanmar Economic Holdings) and Myanmar Economic Corporation (MEC). The Union Solidarity Development Association (USDA), a mass-membership group set up by the ruling junta, the State Peace and Development Council (SPDC), is also extensively involved in business.

The government accounted for over 80% of all domestic credit in the first quarter of 2006. It also controls exports of many important commodities, and in the first 11 months of 2005/06 was responsible for 54.2% of all exports (in kyat terms).

Economic policy

The SPDC is running a huge public-sector deficit. In 1999/2000, the latest actual data available, the public-sector deficit totaled nearly Kt110bn (US$17.4bn at the prevailing official rate or about US$322m at the free-market exchange rate), equivalent to around 5% of that year!s current-price GDP. The bloated state sector accounted for 65.6% of the total deficit, with the central government accounting for the remainder. The public-sector budget deficit appears to have swollen further in recent years. According to the Asian Development Bank (ADB), the total public-sector deficit surged to around 6% of GDP in 2004/05.

The deficit is the result of both weak revenue collection and a failure to control spending. Central government tax revenue is low, at around 5% of current-price GDP in 1999/2000. The SPDC has limited ability to boost tax revenue; the huge "grey" economy is untaxed, and tax evasion is rife. Factors including rising customs revenue have helped to boost central government

The state still crowds out the private sector

Fiscal policies are lax

22 Myanmar (Burma)

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

revenue in nominal terms in recent years. However, although the SPDC has slashed spending on healthcare and education, it has failed to curb high levels of military spending or subsidies to state-owned enterprises.

As the SPDC does not publish regular or timely budget data, it is difficult to assess recent fiscal performance. Although tax revenue has been rising over the past few years, the central government!s budget position is unlikely to have improved, as the government has continued to borrow heavily from the Central Bank. The relocation from late 2005 of many government offices to a huge new administrative capital, Naypyidaw, around 320 km north of the capital, Yangon, has imposed heavy costs. In addition, in April 2006 the junta raised salaries for around 1m civil servants and military officers by between 500% and 1,200%. The SPDC has introduced some revenue-raising measures, including adjusting the exchange rate used to calculate customs duties in mid-2006"in effect raising import duties"in addition to reducing electricity subsidies in October 2005 and raising electricity prices in May 2006. The junta also made some efforts to tighten up on tax evasion with a crackdown on corrupt customs officials in mid-2006. However, such efforts are unlikely to have been sufficient to bring down the budget deficit.

The junta has no coherent monetary policy and rarely adjusts interest rates, even during periods of high inflation. The SPDC relies on the Central Bank to print money to cover its budget deficit, and monetising the deficit in this way has kept upward pressure on inflation (although official data understate inflation rates). With interest rates often negative in real terms, the SPDC tends to rely on a mix of controls and subsidies to keep a lid on price increases.

In April 2006 the Central Bank and commercial banks raised interest rates"the first increase in around five years. The Central Bank rate was raised by 2 percentage points to 12%, and commercial banks raised interest rates to 17% from 15% for loans to state-owned enterprises (SOEs). The interest rate on savings accounts was raised from 9.5% to 12%. The increase was probably intended to dampen inflationary pressures following the huge pay increase for civil servants, effective from April 1st.

The junta maintains a confusing multiple exchange-rate system. The little used official rate remains fixed, while licensed traders are allowed to trade using a more realistic �free-market� rate. There is now a huge disparity between the two rates; the official rate averaged nearly Kt6:US$1 in 2005, compared with around Kt1,095:US$1 for the free-market rate. This distorted multiple exchange-rate system provides hidden subsidies to SOEs.

Despite the rapid GDP growth rates claimed by the SPDC for the past few years, incomes remain extremely low. There are high levels of child malnutrition and low life expectancy (see Resources and infrastructure: Health). The SPDC lacks a coherent policy to address poverty, or to tackle the country!s severe macroeconomic imbalances, and has ignored calls from the IMF, World Bank and Asian Development Bank (ADB) to begin economic reforms. The junta has started a limited privatisation programme, but progress has been sluggish.

Myanmar remains in need of wide-ranging economic reform

Monetary policy is incoherent

Myanmar (Burma) 23

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

The SPDC!s main policy focus is on boosting output of important domestic staples (primarily rice) and export-oriented crops (such as pulses) by means of a land reclamation plan. More land has come into use, but a lack of inputs (such as fertiliser) has limited gains in yields and output. Another policy focus has been on import substitution in sectors such as edible oils and paper products. The SPDC also wants to see diversification of the limited manu-facturing sector. However, the junta has done little to support these policy goals. State support is largely directed towards SOEs, which benefit from subsidised access to foreign exchange and easier access to credit. Widespread cronyism benefits military-backed enterprises and others with links to the generals.

Little effort is made to encourage private domestic or foreign investment, even in priority sectors. Instead, the business climate remains extremely difficult. Businesses are hampered by a range of factors, including poor infrastructure and distribution networks, widespread corruption, shortages of capital, restrictions on repatriation of foreign exchange and erratic policymaking.

Key changes in economic policy

Agriculture

The ruling junta has made some effort to liberalise the agricultural sector, but progress has been patchy. Since 1987 farmers have been allowed to sell most of their output, except rice, on the domestic market at market prices. However, the junta has continued to force farmers to sell a portion of their rice crop to the state at below-market prices"despite several attempts to phase out this policy. Private traders are also restricted from exporting some important commodities. These export restrictions were eased in 2003, only to be reimposed in early 2004 when the junta imposed a six-month ban on all exports of rice, onions, beans, maize and sesame, in a bid to control domestic prices.

Trade

The State Peace and Development Council (SPDC, the ruling junta) has opened up trade with neighbouring countries by opening a number of check-points along its borders. In theory, the junta is also committed to reducing tariffs to 0-5% by 2008 under the common effective preferential tariff (CEPT) scheme of the Association of South-East Asian Nations (ASEAN) Free-Trade Area (AFTA). The SPDC did cut tariffs on several hundred items in mid-2004, but it has also increased some tariffs and taxes. In 2004 the junta imposed a flat 25% commercial tax on a range of imported items, including televisions and construction materials (some items such as foodstuffs and fertiliser were exempt). The new rate replaced a previous raft of taxes at rates ranging from 2% to 20%. The junta has also reduced the exchange rate used to calculate the value of customs duties on imported goods, in effect imposing a further increase in the rate of duty to be paid in kyat. In 1996 the rate was reduced from Kt6:US$1 to Kt100:US$1; it was then cut again in 2004 to Kt450:US$1, and again in mid-2006 to Kt850:US$1. The SPDC has also imposed various non-tariff restrictions on imports. In March 1998, faced with dwindling foreign-exchange reserves, the SPDC announced that import licences would only be issued for items on one of two �priority lists". Then in late

24 Myanmar (Burma)

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

2000 the SPDC imposed further tight limits on the value of imports allowed per month. However, implementation of these restrictions has been patchy. Exports are also restricted. Private traders remain (mostly) barred from exporting rice, teak and minerals. In 1998 the junta extended the state monopoly on exports to include other commodities, such as sugar and pulses. In 2003 exports of some commodities were liberalised, but the SPDC backtracked in early 2004, imposing a six-month ban on exports of rice and other commodities.

Foreign exchange

In 1995 private money-changers were licensed to deal in foreign exchange. But in 1998 the junta imposed a new limit of US$50,000 per month on access to foreign exchange for repatriation, subsequently reduced steadily to only US$10,000 per month by August 2000. Foreign-exchange licences were withdrawn from private banks in 1998. Foreign-exchange markets are often closed at times of severe pressure on the currency. The junta has indicated that it cannot realign the grossly overvalued official exchange rate without external support.

The SPDC�s medium-term economic aims are likely to remain focused on boosting output of key domestic staples, such as rice, as well as raising output of �import substitution� crops such as edible oils. However, the junta may do little to support these policy goals. The SPDC also talks often of its desire to upgrade the country�s transport and communications infrastructure. Again, however, the junta is not likely to do much to encourage investment in these sectors. Indeed, the junta�s own policies may work against it.

Privatisation of the remaining SOEs is expected to remain a long-term goal. After years with little progress, there were some signs in 2006 that the junta intends to pick up the pace. For example, according to press reports in mid-2006, the junta sold minority stakes (up to 49%) in 11 factories run by the Ministry of Industry-1. Looking at the external sector, Myanmar is committed to an ASEAN tariff-reduction programme until 2008. However, implementation is likely to remain patchy, and the SPDC is also likely to continue to impose ad-hoc non-tariff restrictions on both imports and exports.

Economic performance

Gross domestic product (% real change; fiscal years)

Annual average 2003/04 2001/02-03/04GDP 13.8 12.4

Source: IMF, International Financial Statistics.

The SPDC initially forecast a slowdown in real GDP growth during its 2001/02-2005/06 five-year plan, to an annual average of 6%, compared with 8.4% in the previous five-year period. However, the SPDC has since claimed that the economy has been growing at double-digit rates since fiscal year 1999/2000 (April-March). According to the latest data from the Central Statistical Organisation (CSO), real GDP growth averaged 12.4% a year in

Longer-term policy aims lack clarity

Official figures may overstate GDP growth rates

Myanmar (Burma) 25

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

1999/00 to 2003/04, reaching 13.8% in 2003/04. Some sectors have been performing well. For example, the energy and mining sectors have recorded an upturn since the late 1990s as important oil and gas projects have come on stream. Services have also shown solid growth, driven by several years of double-digit growth in the transport, communications and financial services sectors. Anecdotal evidence suggests that there has been an upturn in private investment in transport and communications in recent years, and that the financial sector expanded following the lifting of controls on private-sector activity during the early 1990s.

Nevertheless, the SPDC�s claims of double-digit growth appear questionable, particularly in 2003/04. A banking crisis erupted in early 2003, causing a severe tightening of credit to the private sector during much of that year and into 2004, and this is likely to have slowed investment sharply and caused severe disruption to the financial sector. At the same time, the garment manu-facturing sector suffered a major setback in 2003 when the US imposed sanctions on all imports from Myanmar. Proxy indicators such as electricity consumption and output by SOEs tend to suggest that the GDP growth rates claimed by the junta are overstated. For example, electricity bought by industry fell by 10.8% in 2003/04, to 1,264m kwh, undermining the junta�s claims that manufacturing, construction and electric power all rose at double-digit rates.

It is probable that economic growth picked up in 2004/05 and 2005/06, boosted by strong gas exports and a modest recovery in investment as the credit squeeze eased. However, a number of factors are likely to have kept GDP growth below the high rates claimed by the junta in recent press reports. Problems such as repeated power cuts, feeble domestic demand, weak foreign investment inflows and a continued lack of imported inputs persisted throughout 2004/05 and 2005/06.

Fixed investment growth slowed steadily in the late 1990s, constrained by short-ages of capital for the private sector and a slump in foreign direct investment. Fixed investment growth slowed to only 6.1% year on year in 2002/03, half the rate of overall GDP growth. However, CSO data then show fixed investment rising by 28% year on year in 2003/04. This seems improbable, given that credit extended to the private sector fell by 43.9% year on year in 2003 (although credit to the public sector continued to expand). No official data are produced on private consumption (the junta publishes total consumption data, which group together public and private consumption). Real incomes have been eroded in recent years by high inflation, and consumer confidence remains poor.

Myanmar typically experiences high inflation, owing to rapid money supply growth, high import price pressures and erratic supplies of staples such as rice. However, consumer price inflation slowed to single digits in 2004-05. According to the Yangon consumer price index (the main measure of inflation used by the government), inflation averaged 4.5% in 2004, and 9.4% in 2005. The main factor that drove inflation down to single digits was easing food prices (food prices have the heaviest weighting in the index and rice is the main staple). The junta imposed new restrictions on rice exports for the first six months of 2004,

Investment and consumption have slumped

Inflation is far higher than official figures suggest

26 Myanmar (Burma)

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

resulting in a drop in domestic rice prices. In addition, the tightening of credit in 2003 following the banking crisis dampened already weak demand-side pressures and brought a sharp slowdown in money supply growth in 2003, which may have had a knock-on impact on reducing inflation in 2004.