Embed Size (px)

Citation preview

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 1/56

Nabard offers CSR schemes to corporates

in Jharkhand

Arindam Sinha

Posted: Tuesday, Mar 09, 2010 at 0055 hrs IST

Tags: Nabard | CSR Schemes

The National Bank for Agriculture & Rural Development (Nabard) is looking for corporates in Jharkhand who are willing to take up its livelihood-enhancing schemes for

rural areas in the state while fulfilling their own corporate social responsibility (CSR)

obligations.

Although around 12 to 14 corporates are engaged in CSR activities in the state, a majorityof them are not focused on improving the livelihood of the beneficiaries of their schemes.

Nabard with its various developmental initiatives and resources thinks that forging an

alliance with like-minded individuals and organizations would give a boost to itslivelihood earning schemes.

“Some of them (CSR projects) are not moving towards livelihood activities; they are

either concentrating only on health or education; so, we wanted them to take a holistic

approach to be adopted while having a strategy for CSR activity,” said Nabard Jharkhandregional office chief general manager (CGM) M V Ashok.

This is Nabard’s first move in Jharkhand to try to woo the corporate sector into taking up

its tested projects through their CSR activities as they are said to ensure livelihood

generation.

Speaking at the inauguration here of a “consultative meet for coporates to devise

Jharkhand-specific strategy under CSR initiatives of corporates” operating in Jharkhand,

Nabard executive director P L Behera expected corporates in the state to come forward in

collaborating with Nabard, especially as Jharkhand had a poor developmental index.

Nabard is currently disseminating amongst corporates in Jharkhand information about the

schemes and programmes it has, particularly in terms of the financial grants and loans

associated with them, so that they could take advantage of them. Thus, Nabard, which is

currently associated with some of the CSR initiatives taken up by Krishi Gram VikasKendra (KGVK) of the Usha Martin group and the Tata Steel Rural Development Society

(TSRDS) of Tata Steel, is looking forward to more such relationships with corporates in

Jharkhand.

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 2/56

While KGVK is running several livelihood related projects in Jharkhand today including

at Rukka near Ranchi where farmers/technicians are trained to later transfer the

knowledge on the field, TDRDS, among many of its initiatives, is currently doing jointlywith Nabard and Pune-based Bharatiya Agro Industries Foundation, a tribal development

project at Seraikela in Seraikela-Kharswan district.

Under Nabard’s ‘tribal development model’ an NGO/CSR unit is required to identify

around 100 to 500 acres of land belonging to several tribal farmers, with each tribalfarmer having plantation crop at least on an acre of land, water storage structures and

some allied income-generating activity like diary/poultry/goatery, with Nabard providing

for the community as a whole facilities such common processing centres, etc. Nabard isseeking to establish at least 20 tribal groups during 2010-11 under its “tribal development

model” which involves a total disbursement of grant money between Rs 55-Rs 60 lakh to

each such project, at various stages of their completion in five to seven years.

Similarly, under its grant-based rural entrepreneurship development programme, which

has so far been taken advantage of by several groups each comprising of 20-25individuals, the agricultural bank is targeting to train & launch at least 50 such groups of

rural entrepreneurs in the next fiscal in areas such as garment making, mushroomcultivation, vermin-compost making, silk weaving, etc.

As for its watershed projects each of which requires coming together of five to six

villages involving around 500 to 1,000 hectares of land, Nabard is keeping a target of

funding 50 new projects during 2010-11

Introduction

NABARD is set up as an apex Development Bank with a mandate for facilitating credit

flow for promotion and development of agriculture, small-scale industries, cottage andvillage industries, handicrafts and other rural crafts. It also has the mandate to support all

other allied economic activities in rural areas, promote integrated and sustainable rural

development and secure prosperity of rural areas. In discharging its role as a facilitator

for rural prosperity NABARD is entrusted with 1. Providing refinance to lendinginstitutions in rural areas 2. Bringing about or promoting institutional development and

3. Evaluating, monitoring and inspecting the client banks Besides this pivotal role,

NABARD also: • Acts as a coordinator in the operations of rural credit institutions •Extends assistance to the government, the Reserve Bank of India and other organizations

in matters relating to rural development • Offers training and research facilities for

banks, cooperatives and organizations working in the field of rural development •Helps the state governments in reaching their targets of providing assistance to eligible

institutions in agriculture and rural development Acts as regulator for cooperative

banks and RRBs

Some of the milestones in NABARD's activities are:

• Refinance disbursement under ST-Agri & Others and MT-Conversion/ Liquidity

support aggregated Rs.16952.83 crore during 2007-08. • Refinance disbursement under

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 3/56

Investment Credit to commercial banks, state cooperative banks, state cooperative

agriculture and rural development banks, RRBs and other eligible financial institutions

during 2007-08 aggregated Rs.9046.27 crore. •Through the Rural Infrastructure Development Fund (RIDF) Rs.8034.93 crores were

disbursed during 2007-08. With this, a cumulative amount of Rs.74073.41 crore has been

sanctioned for 280227 projects as on 31 March 2008 covering irrigation, rural roads and bridges, health and education, soil conservation, drinking water schemes, flood

protection, forest management etc.

• Under Watershed Development Fund with a corpus of Rs.613.71 crore as on 31March 2008, 416 projects in 94 districts of 14 states have benefited. • Farmers now

enjoy hassle free access to credit and security through 714.68 lakh Kisan Credit Cards

that have been issued through a vast rural banking network. • Under the Farmers' Club

Programme, a total of 28226 clubs covering 61789 villages in 555 districts have beenformed, helping f

Genesis and Historical Background The Committee to Review Arrangements for Institutional Credit for Agriculture and

Rural Development (CRAFICARD) set up by the RBI under the Chairmanship of

Shri B Sivaraman in its report submitted to Governor, Reserve Bank of India on

November 28, 1979 recommended the establishment of NABARD. The Parliamentthrough the Act 61 of 81, approved its setting up.

The Committee after reviewing the arrangements came to the conclusion that a newarrangement would be necessary at the national level for achieving the desired focus and

thrust towards integration of credit activities in the context of the strategy for Integrated

Rural Development. Against the backdrop of the massive credit needs of ruraldevelopment and the need to uplift the weaker sections in the rural areas within a given

time horizon the arrangement called for a separate institutional set-up. Similarly. The

Reserve Bank had onerous responsibilities to discharge in respect of its many basicfunctions of central banking in monetary and credit regulations and was not therefore in a

position to devote undivided attention to the operational details of the emerging complex

credit problems. This paved the way for the establishment of NABARD.

CRAFICARD also found it prudent to integrate short term, medium term and long-term

credit structure for the agriculture sector by establishing a new bank. NABARD is the

result of this recommendation. It was set up with an initial capital of Rs 100 crore, whichwas enhanced to Rs 2,000 crore, fully subscribed by the Government of India and the

RBI.

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 4/56

armers get aMission

Promoting sustainable and equitable agriculture and rural development through effective

credit support, related services, institution building and other innovative initiatives.

In pursuing this mission, NABARD focuses its activities on: Credit functions,involving preparation of potential-linked credit plans annually for all districts of the

country for identification of credit potential, monitoring the flow of ground level

rural credit, issuing policy and operational guidelines to rural financing institutions

and providing credit facilities to eligible institutions under various programmesDevelopment functions, concerning reinforcement of the credit functions and making

credit more productive Supervisory functions, ensuring the proper functioning of

cooperative banks and regional rural bankccess to c

ObjectivesNABARD was established in terms of the Preamble to the Act, "for providing credit for

the promotion of agriculture, small scale industries, cottage and village industries,

handicrafts and other rural crafts and other allied economic activities in rural areas with aview to promoting IRDP and securing prosperity of rural areas and for matters connected

therewith in incidental thereto". The main objectives of the NABARD as stated in the

statement of objectives while placing the bill before the Lok Sabha were categorized asunder : 1. The National Bank will be an apex organisation in respect of all matters

relating to policy, planning operational aspects in the field of credit for promotion of

Agriculture, Small Scale Industries, Cottage and Village Industries, Handicrafts and other

rural crafts and other allied economic activities in rural areas. 2. The Bank will serve asa refinancing institution for institutional credit such as long-term, short-term for the

promotion of activities in the rural areas. 3. The Bank will also provide direct lending to

any institution as may approved by the Central Government. 4. The Bank will haveorganic links with the Reserve Bank and maintain a close link with in.redit, technology

and exten

National Seminar

on

Agricultural Credit

Silver Jubilee

Celebrations

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 5/56

NABARD

25 YEARS OF DEDICATION

TO RURAL PROSPERITY NABARD completed 25 years of its eventful and trailblazingexistence on 12 July 2007. Established in 1982, by an Act of

Parliament, NABARD's mandate was to provide focused and

undivided attention to the development of rural India by facilitatingcredit flow for promotion of agriculture and rural non farm sector.

Emphasizing this in no uncertain terms, its mission statement

underscores NABARD's goal to "promote sustainable and equitable

agriculture and rural prosperity through effective credit support,

related services, institution development and other innovativeinitiatives".

NABARD's functions can be classified into 4 major categories viz.Credit Planning, Financial Services, Promotion and Development, and

Supervision. Under Credit Planning NABARD prepares Potential

Linked Credit Plan (PLP) annually for each district of the country by

assessing potential available in agriculture and rural sector. This servesas a guide for banks and Government agencies to prepare their own

investment and credit plans in the district and state. Under its Financial

services, it refinances commercial, co-operative and regional rural

banks for lending to on farm and non-farm activities. This includesfarm activities like minor irrigation, animal husbandry, farm

mechanization, forestry, fisheries, land development, horticulture, plantation and medicinal crops and non-farm like rural industries,

artisans, handicrafts, handlooms, rural housing, rural tourism and agro

processing. Refinance is provided by NABARD for both long term

investment credit as well as short term production credit for crop loansand working capital for non-farm activities. A nationwide network of

28 regional offices at the state capitals, a sub-office at Port Blair and

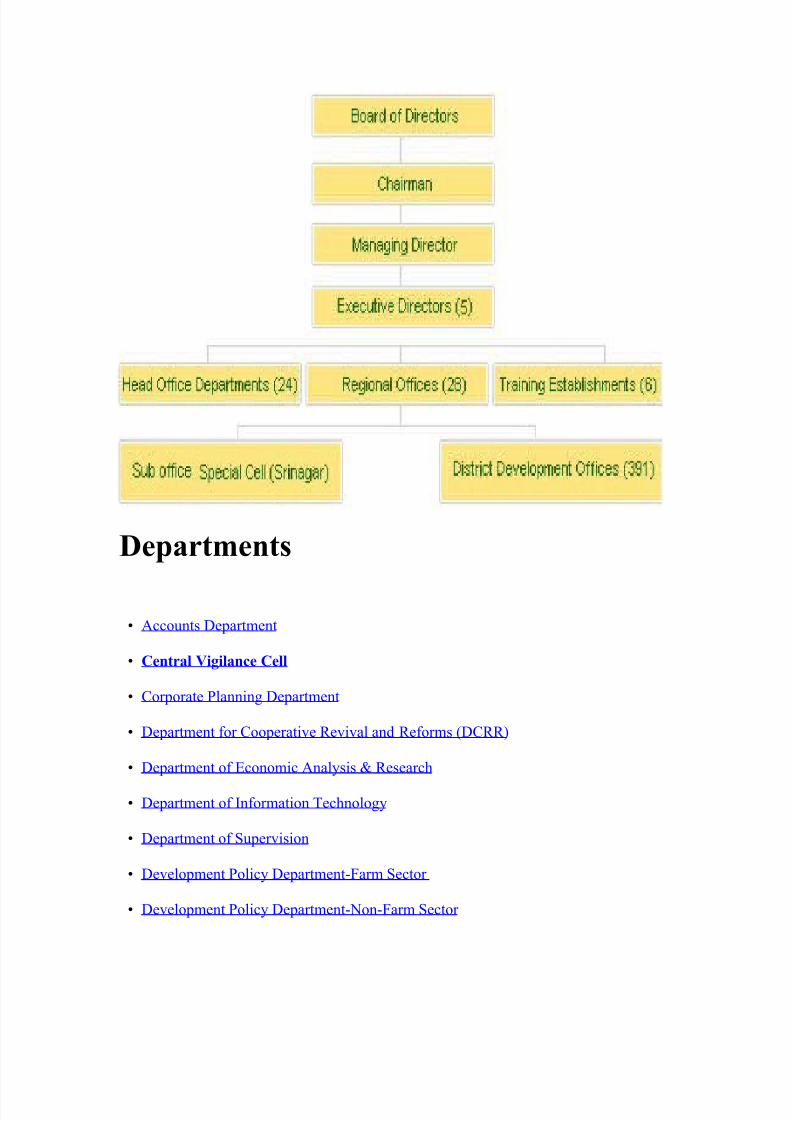

391 district development offices are at hand to cater to this awesometask.

Clearly NABARD's benevolent hand has been silently at work in

supporting rural resurgence in various ways and its stakes are quite

enormous. A glance at the figures will give a fair idea. It haschannelised a whopping Rs. 1,21,000 crore under its investment credit

programme and RIDF since inception, which includes Rs. 8795 crore

disbursed during 2006-07. Under production credit the Bank

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 6/56

sanctioned limits of Rs. 12570 crore during 2006-07.

NABARD has effectively brought in a number of innovations in the

rural credit domains. To quote a few: Formation and Linkage of Self

Help Groups, Farmers Clubs, Rural Infrastructure Development Fund,Watershed Development, Kisan Credit Card, District Rural Industries

Project, Cluster Development Programme and Rural Innovation Fund.

Self Help Groups (SHGs)

Farmers Clubs

Rural Infrastructure Development Fund (RIDF)

Watershed Development

Tribal Development and WADI approach

Women and Development

District Rural Industries Project (DRIP)

Rural Entrepreneurship Development Programme (REDP)

Rural Marketing

Revival of Short-Term Rural Co-operative Structure (STCCS)

Rural Innovation Fund

NABARD Consultancy Services (NABCONS)

Co-Financing

Self Help Groups (SHGs):

One of the major success stories of NABARD, the SHG Bank linkage

programme started as a pilot project in 1992 with 500 SHGs. SHGscomprise homogeneous groups of poor people who have voluntarily

come together mainly with the idea of overcoming their common

problems of low social and economic status. SHGs enable the poor,

especially the women from the poor households, to collectivelyidentify, prioritize and tackle the problems they face in their socio

economic environment. By pooling their meager resources and using

them for lending among themselves, they develop the habit of thrift

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 7/56

and the skill of credit appraisal, before getting mature enough to access

a loan from banks, which is called credit linkage. Starting with small

loans for consumption they soon graduate to bigger loans for settingup of income generating micro-enterprises. Today, NABARD's SHG

Bank Linkage Programme boasts of over 26 lakh SHGs and 3.9 crore

households influencing the lives of over 16 crore poor population.During the year 2006-07 alone, as many as 458591 groups were credit

linked.

go to top

Farmers Clubs

A popular intervention among both farmers and Bankers, the farmersClub concept was envisaged as an experiment in social engineering, a

forum to bring the rural banker and the borrower closer and to

propagate the principles of development through credit. Farmers Clubis an informal group of 15-20 farmers, one per village, which acts as amedium for accessing and disseminating awareness of modern

methods of farming and technological advancements in agriculture in

its area. Financial support is provided by NABARD for opening andmaintenance of Clubs as well as for organizing training programmes in

the respective villages. With corporates and food chains looking for

supply chain linkages of farm produce, Farmers Clubs may have animportant role to play in joint production and marketing of farm

produce. As on 31 March 2007 , there were Farmers Clubs in 534

districts covering 48763 villages.

Rural Infrastructure Development Fund (RIDF):

Deficient Rural infrastructure hinders both social and economic

development. Economists have explicitly emphasized on the directcorrelation between the index of infrastructure development and rural

development. NABARD's support to State Governments through

RIDF since 1995-96 has brought about a sea change in the shape of

upgraded infrastructure in rural areas. Rural roads and bridges under RIDF have improved market access to farmers; check dams and

irrigation structures have augmented their water resources. Even

drinking water projects and health centres have been supported under the Fund. NABARD so far has sanctioned Rs. 61539 crore for

2,44,025 projects under the Fund. A cumulative position of sector-wise

sanctions as on 31 st March 2007 : Irrigation: Rs. 20637 crore, Ruralconnectivity: Rs. 26935 crore for rural road network and bridges,

Power: Rs. 1434 crore Social Sector: Rs. 6988 crore Others: Rs. 5547

crore. A separate window has been created for rural connectivity withvillages of population less than 500, with a corpus of Rs. 4,000 crore

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 8/56

to support the Bharat Nirman project.

go to top

Watershed Development:

In a comprehensive effort to enhance productivity of dryland through

conserving soil, rainwater and irrigation, NABARD embarked on perfecting its experiments in creating a sustainable cost effective

solution to the water harvesting techniques in rural areas. Building on

its experience with the KFW funded watershed development programme in Maharashtra , NABARD established a Watershed

Development Fund with an initial corpus of Rs. 200 crore in 1999-

2000 which now stands at Rs. 602.76 crore. The programme is now being replicated in 124 districts of 14 States.

Tribal Development and WADI approach :

With over 8% of the population comprising tribals largely dependenton forests, livestock and agriculture, NABARD found a holistic

approach by addressing production, processing and marketing of the

produce with WADI as the core of the programme. WADI (smallorchard) was found to be an effective tool for arresting migration of

tribals from their native habitat. The WADI model evolved out of

concerted efforts made in association with Bhartiya Agro Industries

Foundation (BAIF). The project also envisages other developmentinterventions like environment, gender and health. Having completed

10 years in Gujarat and 5 years in Maharashtra , the programme hastouched 275111 families in 410 villages.

go to top

Women and Development

Women constitute one third of the labour force. In order to give focus

to women in various development activities and increase their access

to Bank credit, schemes like Assistance to Rural women in Non-farmDevelopment (ARWIND), Assistance for Marketing of Non- Farm

Products of Rural Women (MAHIMA), Development of Women

through Area Programme (DEWTA) have been designed to provideexclusive support to women in rural areas.

District Rural Industries Project (DRIP):

NABARD launched DRIP, an integrated area-based creditintensification programme, in collaboration with Government, banks

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 9/56

and other development agencies with district specific focus. It was

introduced in 1993-94 with the objective of creating sustainable

employment opportunities in 106 districts all over the country.

go to top

Rural Entrepreneurship Development Programme (REDP):

In order to generate employment in rural areas, it was felt necessary to

develop the entrepreneurial skills of the rural youth. REDP is a

promotional programme supported by NABARD to motivate and traineducated unemployed rural youth, to set up their own enterprises. So

far, 2.32 lakh persons have been trained under the programme under

7792 REDPs.

Rural Marketing:

A number of marketing interventions have been made for marketing of

rural non-farm products since marketing is a key factor in thesustainability of any such endeavour. With the financial support of

NABARD under its promotional programmes like Rural Haats, Rural

Marts, participation in fairs, exhibitions and marketing melas, ruralartisans and entrepreneurs can get a larger market for their produce

and showcase their talent to urban and upcountry markets.

go to top

Revival of Short-Term Rural Co-operative Structure (STCCS)

NABARD is the implementing agency for the Revival package for the

STCCS which mean the State Coop. Banks, District Coop. Banks andthe Primary Agricultural Coop. Societies. (PACS). The revival

package has been approved by the Govt. of India based on the

recommendations of the Vaidyanathan Committee. NABARD has haddialogues with State Govts. and so far 10 states have executed MOU

with GoI and NABARD. Apart from being on the national, state and

district level implementing committees, NABARD has designedguidelines and training manuals for the special audit of PACS under

the Package.

Rural Innovation Fund:

In association with Swiss Agency for Development and Cooperation

(SDC), NABARD has constituted the “NABARD SDC Rural

Innovation Fund (RIF)” to support innovative projects in Farm, Non-Farm and Micro-Finance Sectors leading to creation of livelihood

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 10/56

opportunities for the poor. Government and Non-GovernmentInstitutions, corporate bodies, financial institutions and individuals can

avail funding support for activities involved in development of new

products, processes, prototypes, technology etc. which have the poor in their focus.

go to top

NABARD Consultancy Services (NABCONS)

NABCONS is a wholly owned subsidiary of NABARD, which has

established itself as a dependable and professional consultancyservices provider in agriculture and allied activities. As on 31 March

2007 , it has cumulatively contracted 487 national and international

sion services. Major Activities

• Preparing of Potential Linked Credit Plans for identification of exploitable potentialsunder agriculture and other activities available for development through bank credit. •

Refinancing banks for extending loans for investment and production purpose in rural

areas. • Providing loans to State Government/Non Government Organizations(NGOs)/Panchayati Raj Institutions (PRIs) for developing rural infrastructure. •

Supporting credit innovations of Non Government Organizations (NGOs) and other non-

formal agencies. • Extending formal banking services to the unreached rural poor by

evolving a supplementary credit delivery strategy in a cost effective manner by promoting Self Help Groups (SHGs) • Promoting participatory watershed development

for enhancing productivity and profitability of rainfed agriculture in a sustainable

manner. • On-site inspection of cooperative banks and Regional Rural Banks (RRBs)and iff-site surveillance over health of cooperatives andRRBs.

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 11/56

Departments

• Accounts Department

• Central Vigilance Cell

• Corporate Planning Department

• Department for Cooperative Revival and Reforms (DCRR)

• Department of Economic Analysis & Research

• Department of Information Technology

• Department of Supervision

• Development Policy Department-Farm Sector

• Development Policy Department-Non-Farm Sector

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 12/56

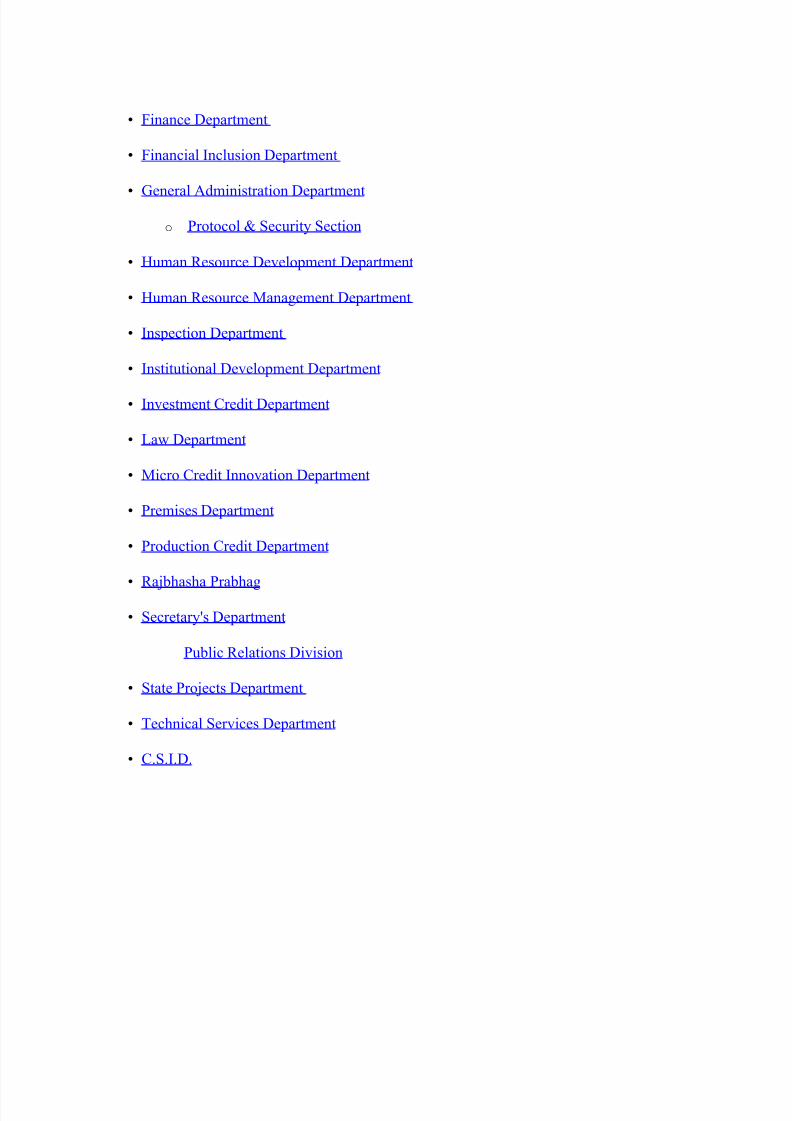

• Finance Department

• Financial Inclusion Department

• General Administration Department

o Protocol & Security Section

• Human Resource Development Department

• Human Resource Management Department

• Inspection Department

• Institutional Development Department

• Investment Credit Department

• Law Department

• Micro Credit Innovation Department

• Premises Department

• Production Credit Department

• Rajbhasha Prabhag • Secretary's Department

Public Relations Division

• State Projects Department

• Technical Services Department

• C.S.I.D.

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 13/56

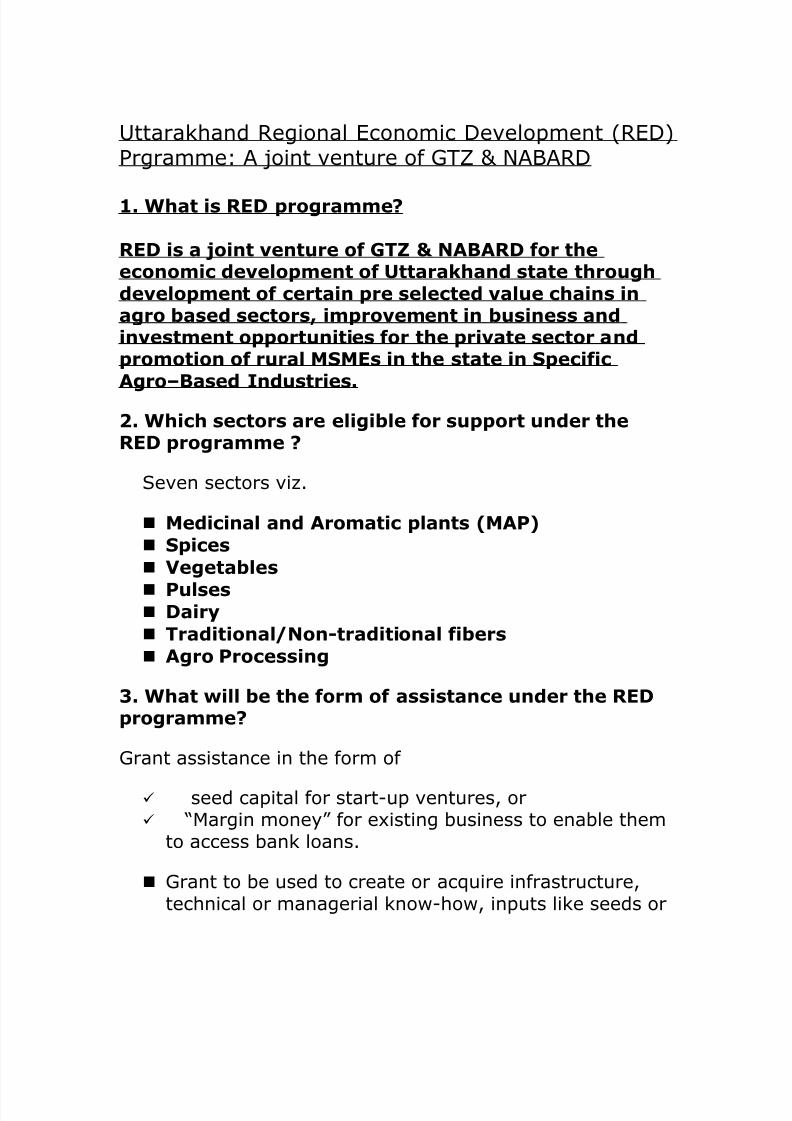

Uttarakhand Regional Economic Development (RED)Prgramme: A joint venture of GTZ & NABARD

1. What is RED programme?

RED is a joint venture of GTZ & NABARD for theeconomic development of Uttarakhand state throughdevelopment of certain pre selected value chains inagro based sectors, improvement in business andinvestment opportunities for the private sector andpromotion of rural MSMEs in the state in SpecificAgro–Based Industries.

2. Which sectors are eligible for support under theRED programme ?

Seven sectors viz.

Medicinal and Aromatic plants (MAP)

Spices

Vegetables

Pulses Dairy

Traditional/Non-traditional fibers

Agro Processing

3. What will be the form of assistance under the REDprogramme?

Grant assistance in the form of

seed capital for start-up ventures, or “Margin money” for existing business to enable them

to access bank loans.

Grant to be used to create or acquire infrastructure,technical or managerial know-how, inputs like seeds or

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 14/56

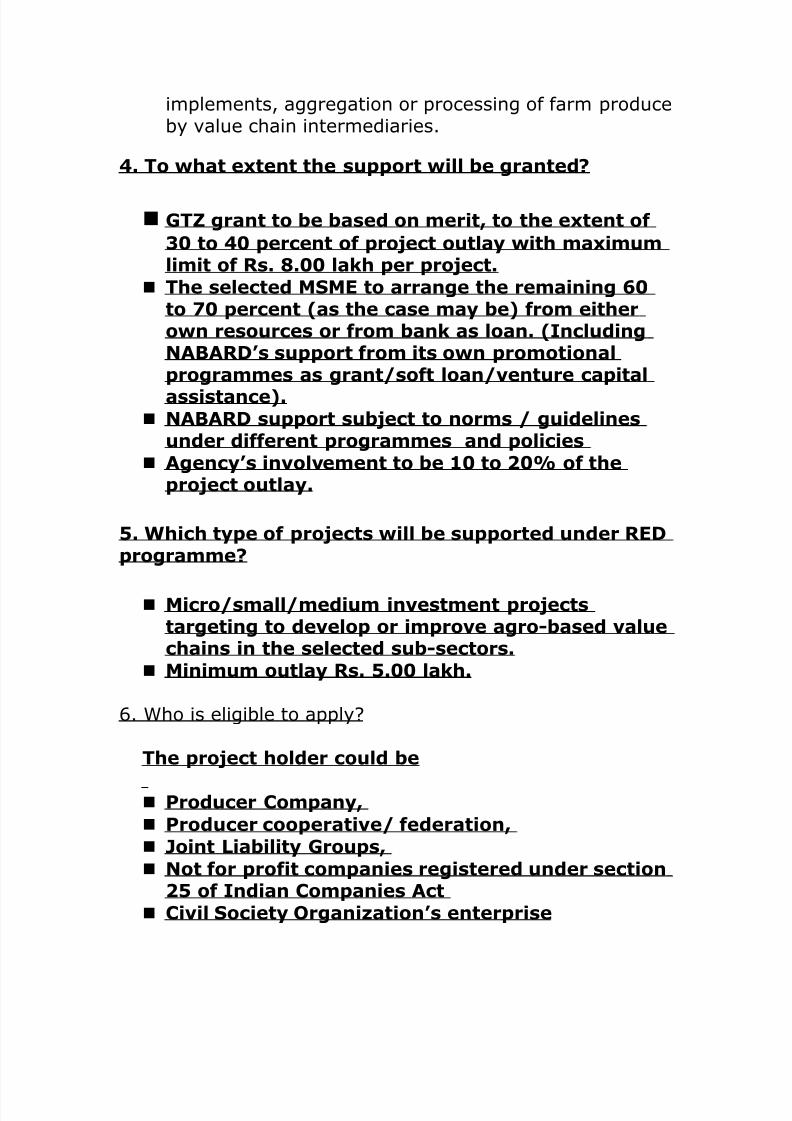

implements, aggregation or processing of farm produceby value chain intermediaries.

4. To what extent the support will be granted?

GTZ grant to be based on merit, to the extent of

30 to 40 percent of project outlay with maximumlimit of Rs. 8.00 lakh per project.

The selected MSME to arrange the remaining 60to 70 percent (as the case may be) from eitherown resources or from bank as loan. (IncludingNABARD’s support from its own promotionalprogrammes as grant/soft loan/venture capital

assistance). NABARD support subject to norms / guidelines

under different programmes and policies

Agency’s involvement to be 10 to 20% of theproject outlay.

5. Which type of projects will be supported under REDprogramme?

Micro/small/medium investment projectstargeting to develop or improve agro-based valuechains in the selected sub-sectors.

Minimum outlay Rs. 5.00 lakh.

6. Who is eligible to apply?

The project holder could be

Producer Company,

Producer cooperative/ federation,

Joint Liability Groups,

Not for profit companies registered under section25 of Indian Companies Act

Civil Society Organization’s enterprise

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 15/56

Societies registered under Soc. Registration Act

1860

Trusts registered under Indian Trusts Act 1880

7. How to apply?Approach the District Development Manager (DDM) of NABARD in the district or the Regional Office of NABARD at State Capital, Dehradun. For detail of address of the Regional Office, please see relevantsection of the NABARD web-site. The proposals canalso be directly emailed to NABARD RO, Dehradun([email protected] [email protected]).

8. What is the application format?

In view of the fact that there will be different types of proposals expected to be received, no format has beenprescribed. The Institutions eligible to avail assistanceunder the RED programme may submit their proposalscontaining adequate information / data as indicated inquestion 12 below about the competence of theproposer to implement the project, how the projectwill impact the life of the target population etc.The project should have positive economic impact onthe rural masses; it should be implement able andreplicable in a reasonable time frame of , say 1 to 3years.

9.What is the prima facie competence of the proposer

to apply under RED programme?NGO’s/CBO’s Peoples Based Organizations should beduly registered under relevant Acts, have a minimumof 3 years’ audited A/cs, should have a good trackrecord and relevant experience in the field. Theyshould not have been blacklisted by GoI /State Govt/other Donor / Financing Agencies and should not have

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 16/56

political affiliations and their activities should notdiscriminate on the basis of caste, creed or religion.

10. What will be the general procedure followed by

NABARD in dealing with the proposals?

On receipt of the proposals, NABARD (Office of DDM /Regional Office/Head Office) will issue anacknowledgment of the receipt of the proposal.Within a month, further information’s/details if anyrequired for processing will be called for.In case the proposal is sanctioned, the proposer willbe informed of the sanction of the proposal and the

terms and conditions of sanction.

Further details of implementation, monitoring andreview will be contained in the terms and conditionsof sanction. In case of rejection, the reasons forrejection will be intimated to the proposer.

In the sanction letter the monitoring process andindicators will be stipulated, in relation to the specific

nature of the proposal.

11. Who would be the Implementing Agency?The Agency submitting the proposal will have toimplement the proposal.

12. Check-list for submitting proposals for assistancefrom RED

The proposals received will be subjected to scrutinyby the Regional Office of NABARD. The Regional Officewill verify whether information on the following isavailable in the proposal or not (the list is illustrativeand not exhaustive). Therefore, the proposer shouldensure that information together with supporting

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 17/56

documents, wherever deemed necessary, is furnishedto avoid repeated correspondence.

The following is the checklist:

Details of the Initiator of the Proposal• Name of the Agency/individual

• Address

• Past experience if any (Specific details ontypes of projects undertaken, supportreceived from NABARD or any otherInstitution/ Body/ authority.)

• Financial stake in the proposal; to whatextent? Item wise financial details,

contribution of the proposer, other partners/stakeholders, their role and contribution, if any

• Whether the Proposer’s role is limited toconceptualization of the idea only or is it upto implementation stage

• Track Record: What has been the record ininitiating similar project(s) / ideas in thepast?

• The audited balance sheet of the agency,registration details if any, copy of bye-laws/Memorandum & Article of Associationas the case may be, may be submitted

About the project/ proposalThe project proposal should contain

• Details of the proposed project/purpose and

expected outcome• Financial costs (component wise)

• Cost benefit analysis (including social costbenefit) wherever necessary

• Profitability/break even wherever necessary

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 18/56

For any further information contact:

NABARD, Dehradun Regional Office,

113/2 Hotel Sunrise Building,

Rajpur Road,

Dehradun.

Tel. No.- 0135-6601092

Email – [email protected]

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 19/56

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 20/56

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 21/56

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 22/56

NABARD is an apex institution, accredited with all matters concerning policy, planning and

operations in the field of credit for agriculture and other economic activities in rural areas in India.

The Committee to Review Arrangements for Institutional Credit for Agriculture and Rural

Development (CRAFICARD), set up by the Reserve Bank of India (RBI) under the Chairmanship of

Shri B. Sivaraman, conceived and recommended the establishment of the National Bank for Agriculture and Rural Development (NABARD). The Indian Parliament through the Act 61 of 1981,

approved the setting up of NABARD. The Bank which came into existence on 12 July, 1982, was

dedicated to the service of the Nation by the Hon’ble Prime Minister, Smt Indira Gandhi on 5

November, 1982.

NABARD is established as a development Bank, in terms of the Preamble of the Act, "for providing

and regulating Credit and other facilities for the promotion and development of agriculture, small

scale industries, cottage and village industries, handicrafts and other rural crafts and other allied

economic activities in rural areas with a view to promoting integrated rural development and securing

prosperity of rural areas and for matters connected therewith or incidental thereto."

NABARD took over the functions of the erstwhile Agricultural Credit Department (ACD) and Rural

Planning and Credit Cell (RPCC) of RBI and Agricultural Refinance and Development Corporation

(ARDC). Its subscribed and paid-up Capital was Rs.100 crore which was enhanced to Rs. 500 crore,

contributed by the Government Of India (GOI) and RBI in equal proportions. Currently it is Rs. 2000

crore, contibuted by GoI (Rs.550 crore) and RBI (Rs.1450 crore).

NABARD: (i) serves as an apex financing agency for the institutions providing investment and

production credit for promoting the various developmental activities in rural areas; (ii) takes measures

towards institution building for improving absorptive capacity of the credit delivery system, including

monitoring, formulation of rehabilitation schemes, restructuring of credit institutions, training of

personnel, etc. ; (iii) co-ordinates the rural financing activities of all institutions engaged in

developmental work at the field level and maintains liaison with Government of India, State

Governments, Reserve Bank of India (RBI) and other national level institutions concerned with policy

formulation; and (iv) undertakes monitoring and evaluation of projects refinanced by it.

NABARD’s refinance is available to State Co-operative Agriculture and Rural Development Banks

(SCARDBs), State Co-operative Banks (SCBs), Regional Rural Banks (RRBs), Commercial Banks

(CBs) and other financial institutions approved by RBI. While the ultimate beneficiaries of investment

credit can be

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 23/56

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 24/56

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 25/56

NABARD is an apex institution, accredited with all matters concerning policy, planning and

operations in the field of credit for agriculture and other economic activities in rural areas in India.

The Committee to Review Arrangements for Institutional Credit for Agriculture and Rural

Development (CRAFICARD), set up by the Reserve Bank of India (RBI) under the Chairmanship of

Shri B. Sivaraman, conceived and recommended the establishment of the National Bank for

Agriculture and Rural Development (NABARD). The Indian Parliament through the Act 61 of 1981,

approved the setting up of NABARD. The Bank which came into existence on 12 July, 1982, was

dedicated to the service of the Nation by the Hon’ble Prime Minister, Smt Indira Gandhi on 5

November, 1982.

NABARD is established as a development Bank, in terms of the Preamble of the Act, "for providing

and regulating Credit and other facilities for the promotion and development of agriculture, small

scale industries, cottage and village industries, handicrafts and other rural crafts and other alliedeconomic activities in rural areas with a view to promoting integrated rural development and securing

prosperity of rural areas and for matters connected therewith or incidental thereto."

NABARD took over the functions of the erstwhile Agricultural Credit Department (ACD) and Rural

Planning and Credit Cell (RPCC) of RBI and Agricultural Refinance and Development Corporation

(ARDC). Its subscribed and paid-up Capital was Rs.100 crore which was enhanced to Rs. 500 crore,

contributed by the Government Of India (GOI) and RBI in equal proportions. Currently it is Rs. 2000

crore, contibuted by GoI (Rs.550 crore) and RBI (Rs.1450 crore).

NABARD: (i) serves as an apex financing agency for the institutions providing investment and

production credit for promoting the various developmental activities in rural areas; (ii) takes measures

towards institution building for improving absorptive capacity of the credit delivery system, including

monitoring, formulation of rehabilitation schemes, restructuring of credit institutions, training of

personnel, etc. ; (iii) co-ordinates the rural financing activities of all institutions engaged in

developmental work at the field level and maintains liaison with Government of India, State

Governments, Reserve Bank of India (RBI) and other national level institutions concerned with policy

formulation; and (iv) undertakes monitoring and evaluation of projects refinanced by it.

NABARD’s refinance is available to State Co-operative Agriculture and Rural Development Banks

(SCARDBs), State Co-operative Banks (SCBs), Regional Rural Banks (RRBs), Commercial Banks

(CBs) and other financial institutions approved by RBI. While the ultimate beneficiaries of investmentcredit can be

Kisan Credit Card

Genesis • Honorable Union Finance Minister announced in his budget speech for

1998-99 that NABARD would formulate a Model scheme for issue of Kisan Credit Cards

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 26/56

to farmers, on the basis of their land holdings, for uniform adoption by banks, so that the

farmers may use them to readily purchase agricultural inputs such as seeds, fertilisers,

pesticides, etc. and also draw cash for their production needs'. • NABARD formulated aModel Kisan Credit Card Scheme in consultation with major banks. • Model Scheme

circulated by RBI to commercial banks and by NABARD to Cooperative. • Banks and

RRBs in August 1998, with instructions to introduce the same in their respective area of operation. Objectives As a pioneering credit delivery innovation, Kisan Credit Card

Scheme aims at provision of adequate and timely support from the banking system to the

farmers for their cultivation needs including purchase of inputs in a flexible and costeffective manner. Contents of Credit Card • Beneficiaries covered under the

Scheme are issued with a credit card and a pass book or a credit card cum pass book

incorporating the name, address, particulars of land holding, borrowing limit, validity

period, a passport size photograph of holder etc., which may serve both as an identitycard and facilitate recording of transactions on an ongoing basis. • Borrower is required

to produce the card cum pass book whenever he/she operates the account. Salient

features of the Kisan Credit Card (KCC) Scheme

• Eligible farmers to be provided with a Kisan Credit Card and a pass book or card-cum-pass book.

• Revolving cash credit facility involving any number of drawals and repayments

within the limit.

• Limit to be fixed on the basis of operational land holding, cropping pattern and

scale of finance.

• Entire production credit needs for full year plus ancillary activities related to crop

production to be considered while fixing limit.

• Sub-limits may be fixed at the discretion of banks.

• Card valid for 3 years subject to annual review. As incentive for good

performance, credit limits could be enhanced to take care of increase in costs,change in cropping pattern, etc.

• Each drawal to be repaid within a maximum period of 12 months.

• Conversion/reschedulement of loans also permissible in case of damage to cropsdue to natural calamities.

• Security, margin, rate of interest, etc. as per RBI norms.

• Operations may be through issuing branch (and also PACS in the case of Cooperative Banks) through other designated branches at the discretion of bank.

• Withdrawals through slips/cheques accompanied by card and passbook.

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 27/56

go to top

Advantages of the Kisan Credit Card Scheme

•

Advantages to farmers

• Access to adequate and timely credit to farmers

• Full year's credit requirement of the borrower taken care of.

• Minimum paper work and simplification of documentation for drawal of funds

from the bank.

• Flexibility to draw cash and buy inputs.

• Assured availability of credit at any time enabling reduced interest burden for the

farmer.

• Sanction of the facility for 3 years subject to annual review and satisfactory

operations and provision for enhancement.

• Flexibility of drawals from a branch other than the issuing branch at the discretionof the bank.

Benefits of the Scheme to the Banks

• Reduction in work load for branch staff by avoidance of repeat appraisal and

processing of loan papers under Kisan Credit Card Scheme.

• Minimum paper work and simplification of documentation for drawal of fundsfrom the bank.

• Improvement in recycling of funds and better recovery of loans.

• Reduction in transaction cost to the banks.

• Better Banker - Client relationships.

Refinance Support for ST(SAO) Loans disbursed under KCC Scheme - Operationalguidelines

SCBs/DCCBs and RRBs were advised operational guidelines governing provision of

refinance for their ST(SAO) disbursements under the KCC Scheme vide Circular letter

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 28/56

No. NB.PCD(OPR)/662/A137(Spl.)/99-2000 dt.26.05.99 and Circular letter No.

NB.PCD(OPR)/662-A/A137(Spl.)/99-2000 dt. 26.05.99 respectively.

The same are summarised below:

•

Instructions on computation of Demand, Collection and Balance (DCB) position,maintenance of Non-overdue Cover (NODC), financing of small/marginal

farmers, etc, conveyed in circular letter No.NB.PCD(OPR)/5980/A.135/90-91

dated 17 December 1990 addressed to RCS and in circular letter No.NB.PCD(OPR)/1271/ 334/95-96 dated 02 November 1995 addressed to RRBs

will also be, mutatis mutandis, applicable for advances made under the KCC

Scheme by SCBs/DCCBs and RRBs respectively. although under the KCC

Scheme, production credit for SAO, advances for allied activities, non-farmactivities and consumption purposes can be covered, only the production credit

for SAO is eligible for refinance from NABARD under the ST(SAO) credit

limits. banks required to maintain separate details of sanctions and accounts for

operations on credit limits for SAO purposes under the KCC Scheme to facilitatesubmission of drawal applications for obtaining refinance from NABARD in

respect of eligible loans and reporting such loans in the monthly NODCstatements for ST(SAO) loans and advances. short-term loans outstanding for

financing ancillary activities relating to crop production such as maintenance of

agricultural machinery/implements, electricity charges, etc. under the KCCScheme also eligible for refinance from NABARD under ST(SAO) credit limits.

• Applicable to Cooperatives only

Seasonality discipline: In view of flexibility and discretion provided to the

farmers in both drawals and repayments, it has been decided not to insist, for the present, on compliance with the seasonality discipline in respect of KCC accounts

for the purpose of allowing drawals on the ST(SAO) credit limits.• Financing of Small Farmers(SF)/Marginal Farmers(MF) : For compliance on

financing of SF/MF, maximum outstanding under production credit for SAO

reached in KCC accounts of such farmers during the year(April-March) would be

reckoned as loans issued to SF/MF. Thus, for compliance in regard to coverage of SF/MF, the aggregate of maximum outstanding in KCC accounts of SF/MF as

well as normal cash credit accounts together with the aggregate of crop loans

issued to SF/MF under the normal loaning system, worked out as percentage to

the maximum outstanding reached under all KCC (including normal Cash Credit)accounts and the total ST(SAO) loans issued during the year (April-March) will

be reckoned.

• Applicable to Both Cooperatives and RRBsComputation of Demand, Collection and Balance (DCB) position : Maximum

outstandings under ST(SAO) loans in KCC accounts reached during the year

(July-June) be treated as demand, and outstandings in unrenewed KCC accountsmay be reckoned as overdues. Percentage of overdues to demand calculated

accordingly.

• Maintenance of Non Overdue Cover(NODC) : Outstanding in KCC accounts

against PACS/Branches for financing SAO excluding amount outstanding under

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 29/56

unrenewed KCC accounts will be reckoned as NODC for purpose of borrowings

from NABARD. Thus, for purpose of working out the aggregate NODC for

borrowings from NABARD for SAO, non-overdue short-term agricultural loansoutstanding under normal loan accounts plus non-overdue outstanding under

normal cash credit accounts and those under KCC Scheme will constitute NODC.

Revised formats of NODC to be submitted by DCCBs/RRBs given as Annexureto our circular letter No.NB.PCD (OPR)/662 & 662A/A.137(Spl)/ 1999-2000

dated 26 May 1999.

go to top

Coverage of Crop Loans disbursed under KCC

Under the Reshtriya Krishi Bima Yojna (RKBY)

GIC has agreed that the crop loans disbursed for eligible crops under the Crop Insurance

Scheme will be covered under the CCIS, now under Rashtriya Krishi Bima Yojna.

However, the banks are expected to maintain all back up records relating to compliance

with "RKBY" and its seasonality discipline, cut-off date for submitting declarations andend use, etc. as in the case of normal crop loans.

Objectives of the Scheme :

• To provide insurance coverage and financial support to the farmers in the event of

failure of crops as a result of natural calamities, pests and diseases.

• To encourage farmers to adopt progressive farming practices, high value inputsand higher technology in agriculture.

• To help stabilise farm incomes, particularly in disaster years.

• To support and stimulate primarily production of food crops and oilseeds.

• Farmers to be covered : All farmers (both loanee and non-loanee irrespective of

their size of holdings) including sharecroppers, tenant farmers growing insurablecrops covered.

• Sum insured : The sum insured extends upto the value of threshold yield of the

crop, with an option to cover upto 150% of average yield of the crop on payment

of extra premium.

• Premium subsidy : 50% subsidy in premium allowed to Small and MarginalFarmers, to be shared equally by the Government of India and State

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 30/56

Government/Union Territory. Premium subsidy to be phased out over a period of

5 years.

go to top

Budget 2001-02 announcement - Follow up :

• Hon'ble Union Finance Minister in his Budget Speech for the year 2001-02 set the

future agenda for the Scheme as under :

" The innovation of KCC is proved to be very successful. Since the year of its

introduction in 1998-99, almost 110 lakh KC cards have been issued. I am asking our

banks to accelerate this programme and cover all eligible agricultural farmers within the

next 3 years .

I am also asking the banks to provide a personal insurance package to the KCC holders as

is often done with other credit cards to cover them against accidental death or permanentdisability, upto maximum amount of Rs.50,000/ and Rs.25,000/- respectively. The

premium burden will be shared by the card issuing institutions. "

Coverage of farmers - Future strategy

• Banks, vide our Circular letter No.NB.PCD(KCC)/29/ 2001-02 dated 10 April

2001, requested to draw up an action plan immediately in consultation with our

Regional Office concerned, based on their past performance and experience in

implementing the scheme, to ensure the coverage of all the eligible agriculturalfarmers under the KCC Scheme within the next three years i.e. by 31 March 2004.

• Banks to ensure that targets fixed for 2001-02, 2002-03 and 2003-04 include newagricultural farmers likely to become eligible for their KC cards after 31 March

2001 also.

• Targets fixed for issue of KC Cards be disaggregated month-wise and

branch/PACS-wise to facilitate close monitoring of progress vis-a-vis target andalso advised to RO concerned.

• In order to ensure achievement of the targets so fixed, banks requested to follow

strategies suggested by NABARD from time to time. Towards this end, banks tolaunch a campaign approach to accelerate pace of implementation of the Scheme.

Following specific steps may be taken by the banks :

• Conduct of Sensitisation/training programmes for the officers of controllingoffices of banks, branch managers and field level functionaries as also district

level functions for distribution of cards.

• Holding Banker-Farmers' Meets, as part of the Kharif 2001 campaign, in each

block to identify the ground level constraints in the smooth implementation of theScheme and to initiate remedial measures therefor.

• Use of VVV Clubs fora for propagation of the scheme.

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 31/56

• Placement of hoardings/banners etc. at prominent places, such as branch

premises, Panchayat buildings, Mandis, etc.

• Use of audio-video media, bringing out KCC literature in local language to create better awareness about KCC Scheme among farmers.

• Issue of plastic/laminated cards to serve as Identity Cards.

•

Monitoring of progress in implementation of the Scheme in Board meetings asalso through various state/ district and block level fora with the participation of

Government functionaries, bankers, farmers etc.

Personal Accident Insurance Scheme -Salient features :

• Designated insurance company will nominate one office at district level to

function as nodal office for co-ordinating implementation of personal accidentinsurance scheme for KCC holders in the district.

• Nominated office of insurance company to issue a Master Insurance Policy to

each DCCB/RRB covering all its KCC holders.

• Premium payable Rs.15/- for a one year policy while Rs.45/- for a 3-year policy.

• Insurance coverage available under Policy only from date of receipt of premiumat insurance company

.

• Banks to ensure to incorporate name of Nominee in Kisan Credit Card-cum-Pass

Book.

• Simplified claim settlement procedure evolved under Scheme whereby anEnquiry-cum-Verification Committee comprising Branch Manager of

implementing bank, Lead Bank Officer and representative of insurance company

to certify nature of accident causing disability/death and recommend settlement of

insurance claims.

• Scheme covers risk of KCC holders against death or permanent disability

resulting from accidents caused by external, violent and visible means, as under:

• Death due to accident (within 12 months of the accident)

caused by outward, violent and visible means -- Rs.50,000/-

Permanent total disability -- Rs.50,000/-

Loss of two limbs or two eyes or one limb and one eye -- Rs.50,000/-Loss of one limb or one eye -- Rs.25,000/-

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 32/56

Major Steps taken by NABARD:

• A Brochure on KCC Scheme highlighting the salient features, advantages and

other relevant information about the Scheme was brought out by Head Office andROs were asked to circulate the brochure to State govt. departments, Commercial

Banks, Cooperative Banks, RRBs and other concerned agencies/officers so as togenerate wider awareness about the Scheme.

• Floor limit of Rs.5000/- for issue of KC Cards stands withdrawn.

• Studies on KCC Scheme have been entrusted to BIRD and NABARD Staff

College to facilitate feed back on the ground level issues/problems so that

changes, where necessary, could be considered.

• Studies on the implementation of the Scheme undertaken by NABARD periodically.

• On the lines of instructions of RBI to Commercial Banks, Cooperative Banks andRRBs have been advised that they may, at their discretion, pay interest at a rate

based on their perception and other relevant factors on the minimum credit

balances in the cash credit accounts under the Kisan Credit Cards of farmersduring the period from 10th to the last day of each calendar month.

• Regional Rural Banks (RRBs) were advised to initiate innovative publicity

campaign in each area of operation in order to cater all eligible farmers under

KCC.

Progress in implementation of the Scheme

• Since launching in August 1998, around 2.38 crore Kisan Credit Cards issuedupto 31 March 2002 by Cooperative Banks, Regional Rural Banks and

Commercial Banks put together.

• Scheme implemented in all States and Union Territories (except Chandigarh,

Daman & Diu and Dadra & Nagar Haveli) with all Cooperative Banks, RRBs andCommercial Banks participating.

• Agency-wise/State-wise progress in issue of cards by all banks during 2001-02

and since inception of Scheme.

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 33/56

Special Projects

• Maharashtra Rural Credit Project

The project was under implementation since January 1994 and covers 1483 villages in

twelve districts of Maharashtra. The primary objective is poverty alleviation throughincreased access to bank credit for the rural poor. It envisages formation and promotionof Self Help Groups through NGOs. The project has been completed. As against a target

of promoting 2600 SHGs, 9000 groups have been promoted, of which 7027 groups have

been credit linked with banks. MRCP has provided a window of opportunities, particularly to the poor rural women to enhance their skill and secure credit for income

generating activities. The project has helped in empowerment of rural women in addition

to providing access to bank credit.

• Adivasi Development programme in Gujarat

The programme has been under implementation with grant support from KfW, Germany,since 1994-95 in Dharampur Taluka of Valsad district through BAIF Development

Research Foundation, Pune. The focus is on development of wadi (small orchard) while

other supportive interventions viz, water resource development, agriculture development,women development, health and sanitation are also addressed. Small and marginal

farmers, including women, are selected under the programme. The landless are supported

by providing them micro-enterprises in farm and non-farm sectors and employmentopportunities in processing units. The establishment of village level people's

organisations (POs) called Village Ayojan Samitis (VAS) have been the strongest tool

and nuclei for planning and implementation of the programme. The programme has beena great success in converting 5,140 ha wastelands into orchards of cashew, mango and

forestry plants by 13,663 adivasi families from 162 villages.

• Adivasi Development Programme in Tribal Areas of Maharashtra

The successful implementation of Wadi model in Gujarat is being replicated in

Maharashtra (Nasik and Thane districts) with grant support from KfW, Germany throughMaharashtra Institute of Technology Transfer for Rural Areas (MITTRA), Nasik, an

NGO promoted by BAIF, Pune. The programme with a project period of ten years (2000-

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 34/56

2010), aims to support 15,000 tribal families by developing wadis on their marginally

productive lands. The project which was launched in September, 2000 has covered an

area of 2076 ha under wadis belonging to 5676 families from the 160 villages and has been instrumental in bringing about an overall improvement in the quality of life of the

families in the project area.

• Transfer of Technologies for Sustainable Development

The project assisted by CEC is under implementation since 1996-97 through BAIF, Pune.It aims at achieving sustainable development of selected small and marginal farmers and

landless families by promoting income generating activities and by adopting simple but

appropriate technologies. The major activities are orchard development, livestock

development, sericulture, watershed, Jana Utthan (basket of activities), health &sanitation and other suitable off-farm activities. The programme covers 217 villages of 11

districts spread over 5 States of Gujarat, Karnataka, Maharashtra, Rajasthan and Uttar

Pradesh. The programme has led to drudgery reduction , improvement in the standard of

living, better health and hygiene and confidence building of the assisted families

Development and Promotional Functions

Swarojgar Credit Card Overview

Swarojgar Credit Card Scheme (SCC Scheme) was introduced in September 2003

consequent upon the announcement made by Honorable Prime Minister in hisIndependent Day Speech on 15 August 2003.

Objective

• SCC Scheme aims at providing adequate and timely credit ie. working capital or block capital or both to small artisans, handloom weavers, service sector,

fishermen, self employed persons, rickshaw owners, other micro-entrepreneures,SHGs, etc from the banking system in a flexible, hassle free and cost effectivemanner.

• Borrowers in urban areas can be covered under SCC Scheme. Small business

covered under priority sector is also eligible under SCC Scheme.

• Any scheme/project that are income generating/ employment generating may be

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 35/56

covered under the scheme. The facility may also include a reasonable component

for consumption needs.

• Farm sector activities like fisheries, dairy, etc. can also be covered under thescheme. Generally such of the self-employment activities which have regular turn

over/income stream on short-interval basis can be covered under SCC scheme.

SCC is a credit delivery mode and not a purpose. Coverage of SCC will not make a unit

ineligible for subsidy. Banks can issue SCCs to target borrowers of SCC scheme for disbursing credit under any schemes whether they are covered under subsidy or not.

Credit Card

• SCC to SHGs

• Nature of financial accommodation

• Quantum of limit

• Renewal of SCC limits

• Interest on credit balance

• Validity

• Issue of cards

• Operation of the scheme

• Insurance

• Security/Margin/Rate of interest /Prudential norms

• NABARD refinance

• Monitoring

• Promotional Support from NABARD

SCC to SHGs

Self Help Groups (SHGs) can also be issued SCC and members will be liable jointly and

severally for repayment. As the Groups mature, some members may graduate to

entrepreneurs and start their own micro- enterprises with or without the support of the

SHGs. In such cases, SCC may be issued to members in individual capacity.

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 36/56

go to top

Nature of financial accommodation

The credit facility extended under the Scheme is in the nature of a composite loan

including term loan / cash credit or both.

go to top

Quantum of limit

Upto R s. 25,000/ per borrower as composite loan. This is indicative. Banks may consider

higher limits on the merits of the case. A component for consumption credit could be

built in keeping in view the value of the family labour in the productive activity. The totallimit would have a relationship with the projected net earning and the repayment capacityof the borrower.

go to top

Renewal of SCC limits

Limits will be renewed annually based on the amount credited to the cash credit

account /repayments.

go to top

Interest on credit balance

Interest as applicable to SB A/c may be paid to the borrowers on the credit balance under the account.

go to top

Validity

SCC is normally valid for 5 years subject to satisfactory operation of the account and

renewed on a yearly basis through simple review process.

go to top

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 37/56

Issue of cards

The beneficiaries under the scheme will be issued with a laminated credit card and a pass

book. This will serve as an identity card and facilitate recording of the transactions on an

ongoing basis. Banks may modify the format keeping in view the relevant data/information required. A passport size photograph of the holder will be affixed on the card

at the space provided for .The card holder would be required to produce the card and the

pass book for operations in the account.As far as possible cluster approach may be followed in implementing the scheme.

In case smart cards are issued, fees towards issue of card/processing may not exceed Rs

50/- per card.

go to top

Operation of the scheme

The banks may at their discretion permit operations through the designated branches,taking into account the convenience of the clientele.

Opening of SB A/c should not be a precondition for issue of SCC.

go to top

Insurance

Beneficiaries under the scheme would automatically be covered under the group

insurance scheme and the premium would be shared by the bank and the borrower equally. Each bank may negotiate the terms of insurance with a company of its choice on

a national or regional basis. Further, as advised by General Insurers’ (Public Sector)

Association of India (GIPSA), it would be advisable for the banks to take up the matter of Personal Accident Insurance linked with SCC scheme individually with the Insurance

Companies. Since many banks have tie-ups for bancassurance agreement with General

Insurance Companies they may decide to include SCC scheme also under their tie-ups.

go to top

Security/Margin/Rate of interest /Prudential norms

Security, Margin, Rate of interest and Prudential norms are applicable as per RBI/NABARD norms. The interest rate would not exceed that for comparable farm

loans. However banks may follow RBI instructions in this regard. Interest linked

incentives may be given for timely repayment. Women borrowers may be given

preference. Joint liability groups could be encouraged as a collateral substitute.

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 38/56

go to top

NABARD refinance

NABARD refinance will be provided for advances under SCC Scheme to eligible banks

against their lendings to the borrowers in rural areas as per norms under the Enterprise

Loan Scheme.

go to top

Monitoring

NABARD has been nominated by Govt. of India as the nodal agency for monitoring the

scheme. Banks are required to report monthly progress to concerned Regional Offices of

NABARD to facilitates monitoring.

go to top

Promotional Support from NABARD

NABARD has introduced a pilot scheme for supporting a total of 90 select RRBs and

Cooperative Banks in their efforts to promote SCC scheme. The objective is to generate

greater awareness about the scheme and cover maximum number of borrowers, educatethe cardholders to use the cash credit facility optimally and effectively, and improve

credit flow at ground level. The pilot scheme would facilitate the identified banks to issue

more SCCs and would be in operation upto 31 March 2007. The identified banks(RRBs/SCBs/SCARDBs) would be reimbursed the expenditure incurred on publicity of

SCC scheme on a cost sharing basis of 60:40, subject to a maximum of Rs.1 lakh.

NABARD has published brochures on SCC scheme in English, Hindi and various

regional languages. Regional Offices of NABARD conduct familiarisation progr ammesfor bankers on the schem

Development and

Promotional Functions

Farmer's Club Programme

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 39/56

Farmer's Club Programme Overview

Agriculture is the backbone of the Indian Economy as nearly 60% of

the population of the country depends on agriculture and it contributes18% to the GDP. Tenth Five Year Plan and National Agriculture

Policy documents envisage a growth level of 4% in Agriculture asagainst the average growth of less than 2% in the last 50 years. The

last decade commencing from 1990s was marked by post-Green

Revolution fatigue and plateauing yield levels in many parts of thecountry. For sustained 4% growth in agriculture there is need to

improve productivity and cut down on costs by improving efficiency.

There is, therefore, an urgent need to provide package of initiatives for

transfer of technology, improving input use efficiency, promoting

investments in agriculture both in private and in public sectors andcreating a favourable and enabling economic environment. Theemerging needs in agriculture sector now are adoption of location

specific skill and knowledge based technologies, promote greater

value addition to agriculture produce, forge new partnerships between public institutions, technology users and the corporate sector, harness

IT more effectively to realise financial sustainability and compete in

the international market.

For transmitting the latest agriculture techniques to the Farmers’ field,

orienting them to establish better relationship with banks, adoption of

latest post-harvest handling technology, value addition, etc. and enjoythe benefits of collective bargaining power both for procuring inputs

and select their produce the Farmers’ Club Programme is an

appropriate and most suitable strategy initiated by NABARD in late1982.

Mission

Development in rural areas through credit, technology transfer,

awareness and capacity building.

What is Farmers' Club Programme

National Bank for Agriculture and Rural Development (NABARD)encourages banks to promote Farmers' Clubs in rural areas under the

Farmers’ Club Programme, earlier known as “Vikas Volunteer Vahini

(VVV) Programme”. The Programme was launched by NABARD in November 1982 to propagate the five principles of “ Development

through Credit”.

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 40/56

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 41/56

in a village/ cluster of villages, generally in the Operational Area of a

Bank. While Farmers’ Club should have minimum of 10 members, no

upper limit in the membership is envisaged. Every Club would havethree office bearers - One 'Chief Coordinator/Volunteer/ President, the

other 'Associate Coordinator/Volunteer/Vice President. The office bearers would be elected by Club Members on a democratic basis for a

term to be decided by the Club. The office bearers should be residentsof the area of the operation of the club. No NGO/FC promoting agency

representative can be office bearer of the club.

Functions of the Office bearers:

The main functions of the office bearers would be to convene

meetings, to arrange meetings with experts, maintenance of Books of Accounts, coordination with Bank, Line Departments of the State

Governments, maintaining proper liaison with all concerned.

Membership

All villagers except willful defaulters can become members of the

club. The club must make endeavour to raise their own resources byway of contribution from members, undertaking certain business

services such as bulk procurement of inputs and collective marketing

of agricultural produce, functioning as Business Facilitators (BFs),

agents for insurance and other services etc.

Steps in the formation of Farmers’ Clubs

• Bank branch can promote the clubs directly or engage Farmers’Club promoting agencies like Krishi Vigyan Kendras (KVKs),

Agriculture Universities, NGOs, Corporates, etc.

• All grassroot level organisations (NGOs, PRIs, StateAgricultural Universities, KVKs, ATMA, Post Offices etc.) are

eligible to form Farmers’ Clubs

• Select a village/ cluster of villages suitable for launching Clubs

in the operational area of the bank branch.• Identify a few progressive farmers and borrowers with good

track record of proper loan utilisation, aptitude and capacity for

team work. (Success of the Club hinges on the right choice of members).

• Encourage the members to select a Chief

Coordinator/Volunteer/President and an AssociateCoordinator/Volunteer/Vice President and a Cashier. This will

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 42/56

ensure collective leadership and continuance of the Club.

• Provide orientation training to them with the help of NABARD

(Regional Office / DDM or trained officers from the bank) before launching.

• Encourage members to convene monthly meeting regularly,

guide them to have meaningful discussion and take necessaryfollow up action.

• Motivate members them to identify credit and non-credit needs

(training, socio-economic, village infrastructure, etc.), preparea plan of action and accordingly arrange for expert talks,

counselling, need-based activities, etc. with the help of

Government Departments and other agencies concerned.

• Ensure that the members maintain Membership Register,Meeting Register, Minutes Book and Books of accounts .

• Evolve a performance parameter and measure the Clubs’

contribution annually.

•

Use Club as a tool in aid of branch not only in the matter of credit and recovery but also in facilitating promotion of SHGs,

micro credit, Financial Inclusion and convergence of services.

Consent Letter:

NABARD provides financial support to FCs for an initial period of 3

years. Sponsoring Banks/Agencies are expected to give a consent letter

for supporting the clubs for a period of two years beyond the initial

period of 3 years of NABARD assistance.

No. of Clubs to be promoted by a Single Agency:

There is no restriction on the number of clubs to be formed a single

agency.

Rating of Farmers; Clubs

To facilitate the graduation of farmers’ Clubs into Federations of Farmers’ Clubs or Producers’ Groups/Companies, it would be

desirable for the sponsoring agencies to rate the Farmers’ Clubs as per

prescribed parameters. However, the rating of the clubs is not linked to

any releases to be made out of the assistance under the new policy.

Awards to Best Working Clubs:

Awards would be given to be provided to best working clubs at the

district, state and national levels, based on the rating norms.

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 43/56

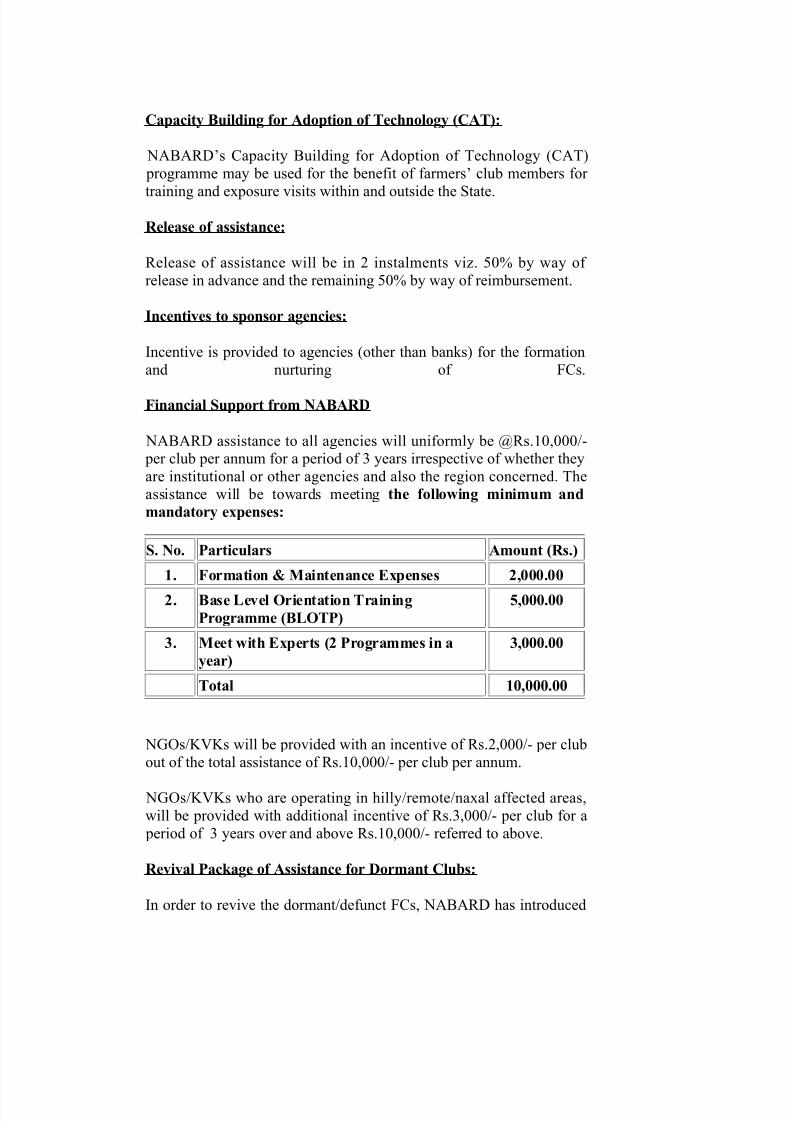

Capacity Building for Adoption of Technology (CAT):

NABARD’s Capacity Building for Adoption of Technology (CAT)

programme may be used for the benefit of farmers’ club members for

training and exposure visits within and outside the State.

Release of assistance:

Release of assistance will be in 2 instalments viz. 50% by way of

release in advance and the remaining 50% by way of reimbursement.

Incentives to sponsor agencies:

Incentive is provided to agencies (other than banks) for the formation

and nurturing of FCs.

Financial Support from NABARD

NABARD assistance to all agencies will uniformly be @Rs.10,000/- per club per annum for a period of 3 years irrespective of whether they

are institutional or other agencies and also the region concerned. The

assistance will be towards meeting the following minimum and

mandatory expenses:

S. No. Particulars Amount (Rs.)

1. Formation & Maintenance Expenses 2,000.00

2. Base Level Orientation Training

Programme (BLOTP)

5,000.00

3. Meet with Experts (2 Programmes in a

year)

3,000.00

Total 10,000.00

NGOs/KVKs will be provided with an incentive of Rs.2,000/- per club

out of the total assistance of Rs.10,000/- per club per annum.

NGOs/KVKs who are operating in hilly/remote/naxal affected areas,

will be provided with additional incentive of Rs.3,000/- per club for a

period of 3 years over and above Rs.10,000/- referred to above.

Revival Package of Assistance for Dormant Clubs:

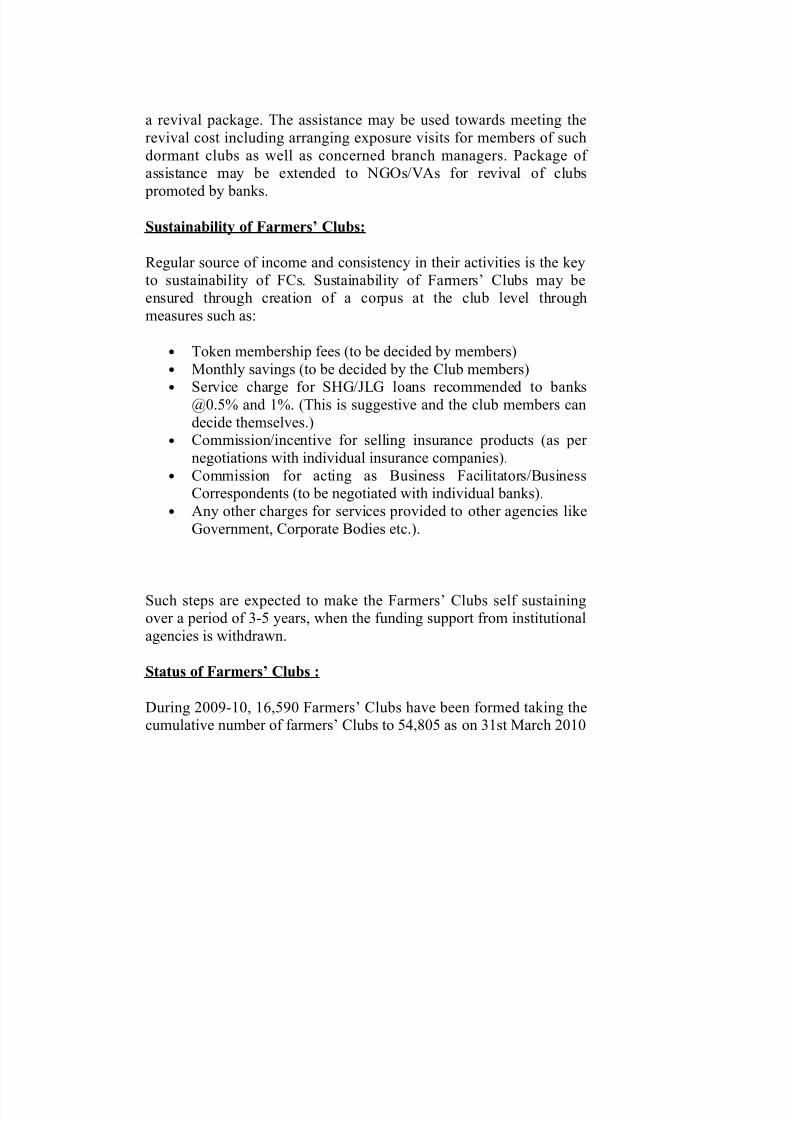

In order to revive the dormant/defunct FCs, NABARD has introduced

8/7/2019 Nabard offers CSR schemes to corporates in Jharkhand

http://slidepdf.com/reader/full/nabard-offers-csr-schemes-to-corporates-in-jharkhand 44/56

a revival package. The assistance may be used towards meeting the

revival cost including arranging exposure visits for members of such

dormant clubs as well as concerned branch managers. Package of assistance may be extended to NGOs/VAs for revival of clubs

promoted by banks.

Sustainability of Farmers’ Clubs:

Regular source of income and consistency in their activities is the key