Embed Size (px)

Citation preview

NAFTA: FROM A CANADIAN

PERSPECTIVE

61st Annual EDCO Conference

Toronto February 7, 2018

AGENDA

• Welcome

• Session Introduction

• Speaker Introduction

• Hugo Cameron, Executive Lead for U.S. Trade Engagemnt at the Ontario Ministry of International Trade

• John Holmes, Emeritus Professor of Geography and Planning at Queen’s University and an Academic Partner with the Automotive Policy Research Centre

• Question and Answer Period

• Closing Remarks

Ministry of International Trade

Update on the North

American Free Trade

Agreement (NAFTA)

Renegotiations

4

Ontario is the U.S.’ #1 Customer

02/02/2018

• 20 states rank Ontario

as their #1 export

destination and 8 states

rank Ontario as #2.

• Two-way trade between

Ontario and the U.S.

totaled US$299 billion.

• In 2016, Ontario

imported more than

US$141 billion in U.S.

goods.

• Our economies are

deeply integrated

through our industries

and people – nearly 9

million U.S. jobs

depend on Canada.

5

A Strong, Integrated Economic Relationship

02/02/2018

6

Ontario’s Trade in the NAFTA Region

Ontario is a critical economic force in the NAFTA region.

• Ontario accounts for 30% (or $426 billion) of the $1.4 trillion in trade in

goods that takes place within the NAFTA region.

• Total Ontario-U.S. trade in goods was $395.6 billion in 2016 – 59% of the

Canadian total, and nearly twice as much as the next three provinces

combined (Alberta: $84.5 billion, Quebec: $80.9 billion, B.C.: $40.9 billion).

Ontario is the largest exporter within the NAFTA region of any U.S. state or

province.

• In 2016, Ontario exported $206.5 billion in goods to the U.S. (52% of

Canada’s total exports). No other province had more than 17% of

Canada’s total exports to the U.S.

• No U.S. state, including Texas ($148 billion) and California ($55 billion),

surpassed Ontario’s goods exports to NAFTA Parties.

02/02/2018

7

View from Ontario

After 24 years, NAFTA renegotiation presents an opportunity to

consider how the existing agreement could be modernized. For

example:

• Addressing new issues, such as digital trade.

• Updating chapters on government procurement, temporary entry

for business persons and regulatory and customs cooperation.

• Incorporating new chapters on labour and the environment.

Canada has jurisdiction over signing international treaties, including

free trade agreements.

Provinces and territories engage regularly – including during

negotiating rounds – with Global Affairs Canada to forward their

interests.

• Strong ‘Team Canada’ approach since the start of negotiations.

02/02/2018

8

Progress in the Negotiations

Accelerated negotiating schedule: Six Rounds and one Intersessional have

been held since talks began in August 2017. Two chapters ‘parked’ thus far.

Approximately 28 negotiating tables.

Negotiations proceeding on two broad tracks:

Less contentious, more technical issues – i.e. SPS, TBT, Telecoms

U.S. unconventional proposals – i.e. Government Procurement, Autos,

Dairy, Dispute Settlement

Unlike more ‘traditional’ trade negotiation due to U.S. Administration seeking

rebalancing. Focus on trade deficits as key metric.

Context of threat of U.S. withdrawal. U.S. Congress, Governors, business, agriculture stakeholders all supportive of

maintaining or improving NAFTA.

Highly uncertain outcome.

02/02/2018

9

Perspectives on Canada’s Position With market access to the U.S. already secured under the existing NAFTA, Canada

remains open to modernizing the Agreement where it makes sense.

Canada has been fully engaged across the 28 negotiating tables, and continues to

undertake broad consultations with key sectors and stakeholders.

Canada has publicly raised concerns with the unconventional proposals tabled by the

U.S.

Canada has stressed its commitment to remain at the table.

Key negotiating interests include:

• Modernizing the Agreement’s provisions.

• Incorporating progressive elements (e.g. chapters on labour, environment, gender).

• Regulatory cooperation.

• Securing a freer market for government procurement.

• Improving temporary entry for business persons.

• Upholding and preserving key existing elements of the Agreement, such as Chapter

19, the exception to preserve Canadian culture, and Canada’s system of supply

management.

02/02/2018

10

Perspectives on U.S. and Mexican Positions

U.S.

• Looking to re-orient NAFTA towards domestic interests (e.g.

eliminating Chapter 19, reconfiguring autos rules of origin to favour

U.S. production).

• Open to modernizing new provisions into the Agreement, such as a

chapter on digital trade.

• Congress will need to approve the final Agreement, and will have

significant influence on U.S. positions.

Mexico

• Focused on ensuring there is no roll-back of trade liberalization.

• Concerns around economic uncertainty associated with the

renegotiation impacting on new investment.

• Canada and Mexico have common views on a number of key

negotiating areas, including opposing unconventional U.S.

proposals.

02/02/2018

11 02/02/2018

Coming up…

Rounds scheduled for late-February (Mexico)

and late-March (U.S.).

Mexican election on July 1st 2018.

U.S. midterm elections in November 2018 (full

House, 1/3 Senate, 34/50 Governorships).

NAFTA and the Automotive Industry

John Holmes

Queen’s University

Academic Partner, APRC

61st Annual EDCO Conference

Toronto, February 7, 2018

★ FIRST, I will announce my intention to renegotiate NAFTA or withdraw from the deal under Article 2205. ★ SECOND, I will announce our withdrawal from the Trans-Pacific Partnership. ★ THIRD, I will direct the Secretary of the Treasury to label China a currency manipulator. ★ FOURTH, I will direct the Secretary of Commerce and U.S. Trade Representative to identify all foreign trading abuses that unfairly impact American workers and direct them to use every tool under American and international law to end those abuses immediately.

Trump’s 100-day Action Plan to “Make America Great Again”

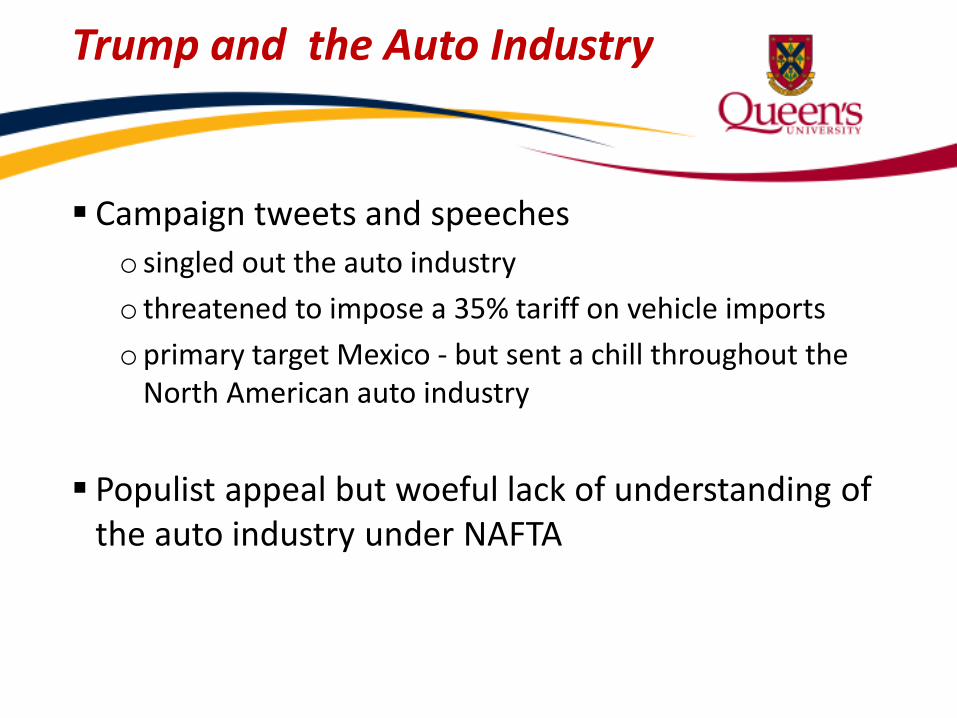

Trump and the Auto Industry

Campaign tweets and speeches

o singled out the auto industry

o threatened to impose a 35% tariff on vehicle imports

oprimary target Mexico - but sent a chill throughout the North American auto industry

Populist appeal but woeful lack of understanding of the auto industry under NAFTA

NAFTA 2.0: Sticking Points

Auto Industry Rules of Origin (complicated by CPTPP)

BUT, it’s about more than the auto industry!

o Dispute Resolution – Chapters 11,19 & 20

oSunset Clause

o Procurement

o IP

o Agricultural sectors

o Etc.

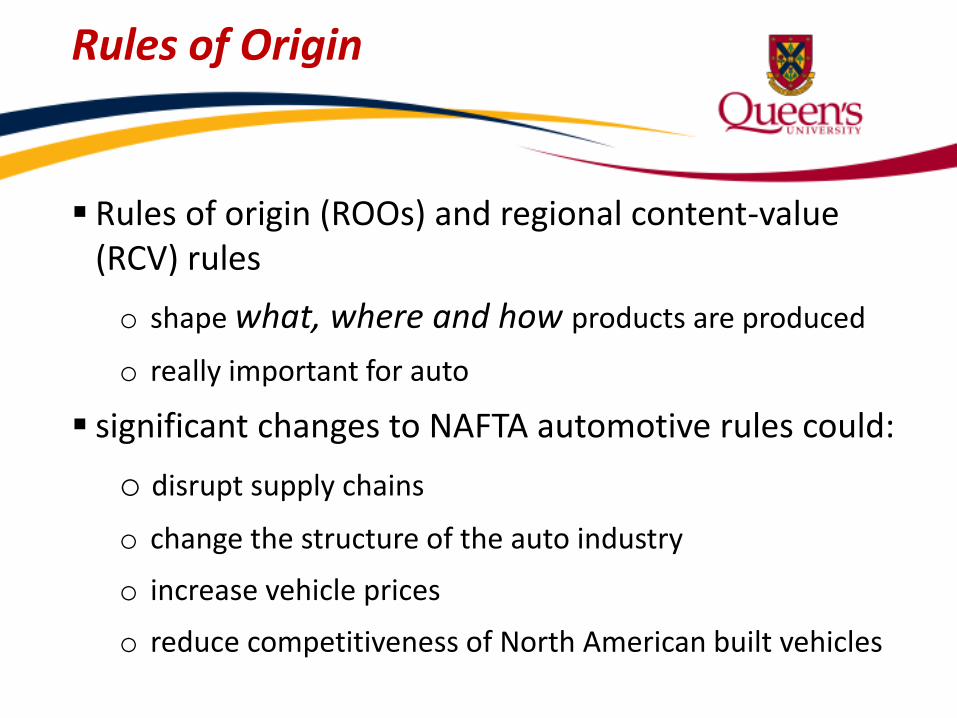

Rules of Origin

Rules of origin (ROOs) and regional content-value (RCV) rules

o shape what, where and how products are produced

o really important for auto

significant changes to NAFTA automotive rules could:

o disrupt supply chains

o change the structure of the auto industry

o increase vehicle prices

o reduce competitiveness of North American built vehicles

Outline

Canadian Auto Industry: Overview

Current NAFTA Automotive Trade

US NAFTA Automotive Demands

Potential Impact on Automakers and Suppliers in Canada

Canada’s Automotive Industry

• 126,000 direct jobs

• $9.6 billion in wages

• $18.2 billion in GDP

• $86.5 billion in exports

• Importance to Ontario

Canada’s Automotive Industry

5 OEMs (Toyota, FCA, GM, Honda, Ford) • 2.3 million vehicles; Toyota + Honda = 43% of total • ~ 2.0 million exported to US

700+ suppliers

• Canadian-owned global suppliers • Subsidiaries of Japanese, US, European global suppliers • Large number of smaller Canadian-owned firms • Tooling industry

Heavily concentrated in Windsor to Oshawa corridor Integral part of Great Lakes Auto Region (MI,OH,IN)

Canadian Automotive Industry Employment: 2014

Source: Sweeney APRC

Challenges

Technological Change

oNew engine/drive train technologies

oVehicle lightweighting

oVehicle electrification

Supplier Logistics

o Southern US

oMexico

Trade Agreements

oCKFTA, CETA

oCPTPP

oNAFTA 2.0?

Percentage Shares (by value), Total Vehicle Trade, Canada: 2016

United States 97%

Mexico 1%

Rest of World

2%

United States 71% Mexico

12%

Rest of World 17%

VEHICLE EXPORTS: $62.87 billion

VEHICLE IMPORTS: $47.64 billion

Source: Industry Canada, Strategis Online Trade Database

NAFTA Vehicle Production and Trade Flows: 2016 (Units)

Percentage Shares (by value), Total Automotive Parts Trade, Canada: 2016

United States 90%

Mexico 6%

Rest of World

4%

United States 65%

Mexico 13%

Rest of World 22%

PARTS EXPORTS: $21.1 billion

PARTS IMPORTS: $47.8 billion

Source: Industry Canada, Strategis Online Trade Database

NAFTA Automotive Parts Trade Flows: 2016 ($US Billions)

Canada Automotive Trade Balances Within NAFTA: 1992-2016

-15,000.00

-10,000.00

-5,000.00

0.00

5,000.00

10,000.00

15,000.00

20,000.00

25,000.00

30,000.00

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Mill

ion

s C

$ (

curr

en

t)

United States Mexico NAFTA

Source: Industry Canada, Strategis Online Trade Data

Canada Automotive Parts Trade within NAFTA: 2016

Great Lakes 70%

U.S. Mid-

South 10%

South U.S. 8%

Other U.S. 6%

Mexico 6%

Parts Exports 2016

Great Lakes 56%

US Mid-South 12%

South U.S. 9%

Other U.S. 6%

Mexico 17%

Parts Imports 2016

Not Just About Trade Balances….

NAFTA countries interdependent in automotive production

high levels of integration, specialization, and intra-industry trade

US imported vehicles from Canada and Mexico contain significant US parts content

keeps the North American auto industry globally competitive (cf. Japan; Europe)

benefited automakers, consumers, and attracted investment

USTR NAFTA 2.0 Objectives (July 2017)

Trade in Goods:

Improve the U.S. trade balance and reduce the trade deficit with the NAFTA countries.

Rules of Origin:

Update and strengthen the rules of origin, as necessary, to ensure that the benefits of NAFTA go to products genuinely made in the United States and North America.

Ensure the rules of origin incentivize the sourcing of goods and materials from the United States and North America.

Current NAFTA Automotive ROO and RCV

To qualify for preferential tariff treatment

oVehicle or part must “originate” in the NAFTA region

oTo “originate” must contain a specified minimum RCV

• 62.5% for vehicles, engines and transmissions

• 60% for automotive parts on “tracing list”

• 50% for some other parts

Tracing list (29 categories of parts)

o for listed components, non-originating value must be tracked through all stages of assembly and included as non-originating when vehicle RCV is calculated

Current Non-Preferential Import Tariffs

Canada

o6.1% on vehicles

o0% on parts destined for OEM assembly

United States

o2.5% on cars

o25.0% on pickup trucks

o3.1% (avg.) on automotive parts

US NAFTA 2.0 Automotive Demands

Increase NAFTA RCV

ofrom 62.5% to 85% for vehicles, engines and transmissions

ofrom 60% to 85% for parts on current tracing list

ofrom 50% to 72.5% for certain other parts

Require 50% US content-value for vehicles built in Canada/Mexico imported to US (i.e. “85/50” ROO)

Tracing list: include all parts and materials incl. steel, aluminum and textiles

Possible Outcomes

Scenario A: NAFTA 2.0

Higher NAFTA RCV and expanded tracing list

• could benefit Canadian parts suppliers

50% US content rule

• would disadvantage smaller Canadian suppliers

• how much rejigging of supply chains needed?

Increase cost of North American-built vehicles

Expanded tracing list: more cost effective to just pay the MFN tariff?

Possible Outcomes

Scenario B: US Withdraws from NAFTA; CUSFTA remains suspended Canadian-built cars face 2.5% tariff entering US – offset by

depreciated C$??

GM Oshawa hit by 25% US tariff on pickup trucks

US-built vehicles face 6.1% tariff entering Canada (cf. Japanese and European vehicle imports 0% under CETA and CPTPP)

No longer need to meet NAFTA RCV – OEMs could substitute lower-cost parts and negatively impact parts production in Canada and US

Summary

High levels of integration, specialization, and intra-industry trade keeps the North American auto industry globally competitive

Allows automakers to take advantage of best cost production and manage supply chain risk

US-demanded changes to automotive rules would disrupt existing supply chains, undermine competitiveness of the North American auto industry, and create unintended consequences for the US

Thank you John Holmes [email protected] Presentation from ongoing research by John Holmes and Brendan Sweeney supported by the APRC

QUESTION AND ANSWER

PERIOD

QUESTION:

What do you see as some of

the biggest stumbling blocks

to getting to a final deal?

QUESTION:

What role do sub-national

governments, particularly provinces

and territories, play in this

negotiation?

QUESTION: Besides the ongoing NAFTA renegotiations,

Canada has recently concluded trade

agreements with Korea and the EU and

there is still the possibility of an 11-country

Trans Pacific Partnership deal that will

include Canada but not the USA. What will

be the impact of these other trade

agreements have on Canada’s automotive

industry?

QUESTION: In addition to the uncertainties around

the future NAFTA, what other

challenges currently face Ontario

automotive suppliers?

Thank You Reminders:

• Complete the session evaluation form on

your mobile app

• Up Next: Lunch in the Osgoode Ballroom

• Next sessions: Breakout sessions

commencing at 1:45pm

Check for your room locations