Embed Size (px)

Citation preview

National Broadband Network Strategies in Turkey

Hamdi AYHAN

Network Directorate

AGENDA

• Türk Telekom Facts and Figures

• Evolution of Broadband in Turkey

• Türk Telekom’ s Experience

• Fibercitty

• Conclusion

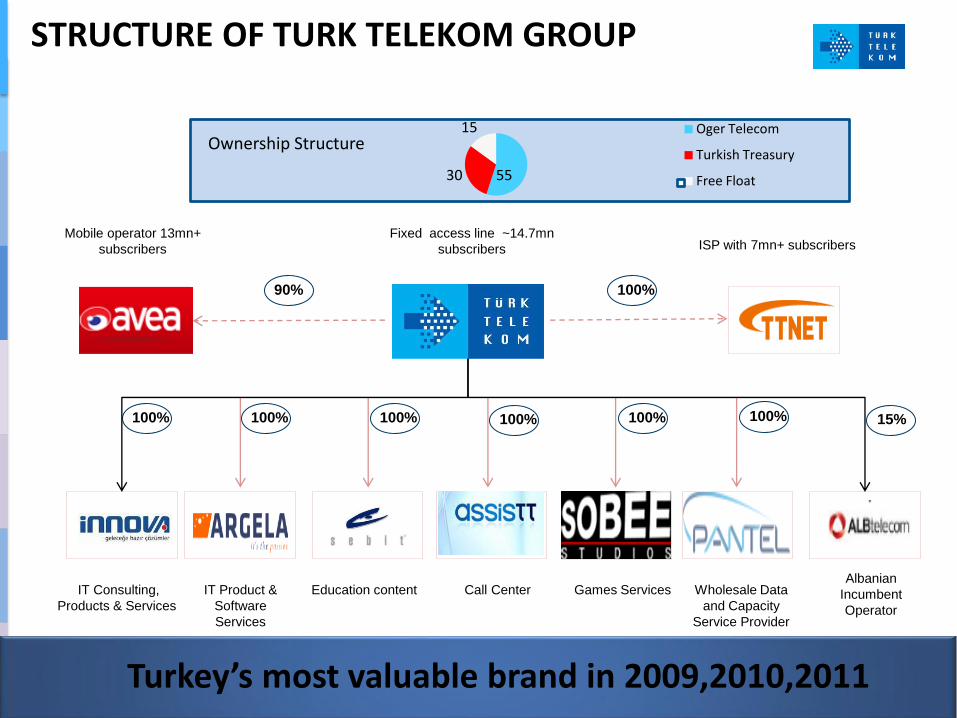

Ownership Structure

55 30

15 Oger Telecom

Turkish Treasury

Free Float

Turkey’s most valuable brand in 2009,2010,2011

IT Consulting,

Products & Services

IT Product &

Software

Services

Education content Call Center Games Services Albanian

Incumbent

Operator

ISP with 7mn+ subscribers Mobile operator 13mn+

subscribers

Fixed access line ~14.7mn

subscribers

90% 100%

100% 100% 100% 100% 100% 15%

Wholesale Data

and Capacity

Service Provider

100%

STRUCTURE OF TURK TELEKOM GROUP

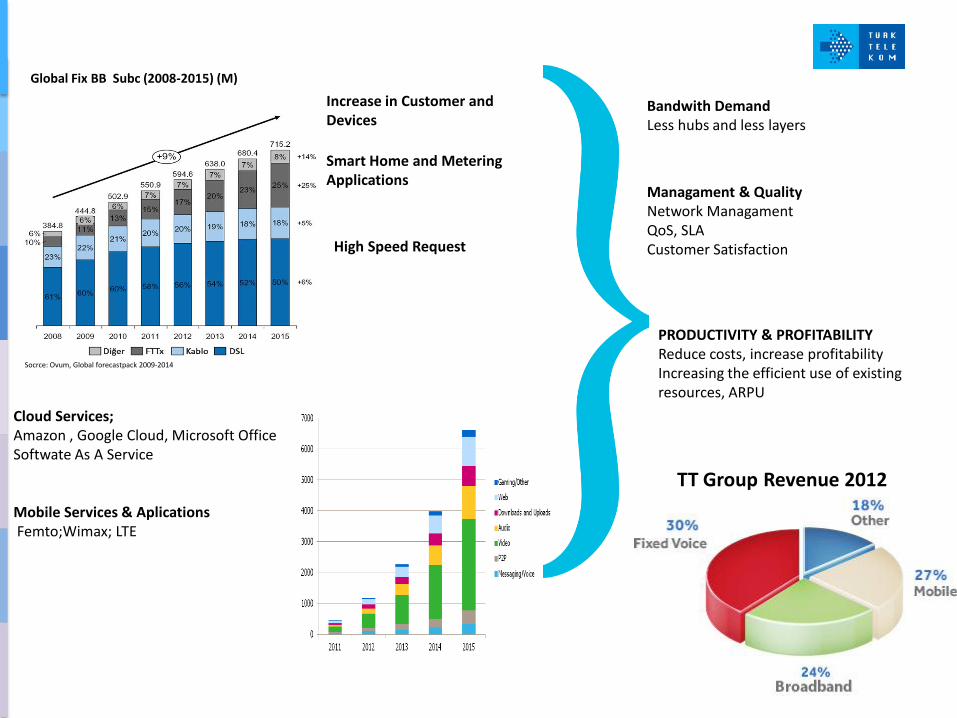

PRODUCTIVITY & PROFITABILITY Reduce costs, increase profitability Increasing the efficient use of existing resources, ARPU

Managament & Quality Network Managament QoS, SLA Customer Satisfaction

Bandwith Demand Less hubs and less layers

Increase in Customer and Devices

High Speed Request

Cloud Services; Amazon , Google Cloud, Microsoft Office Softwate As A Service

Smart Home and Metering Applications

Mobile Services & Aplications Femto;Wimax; LTE

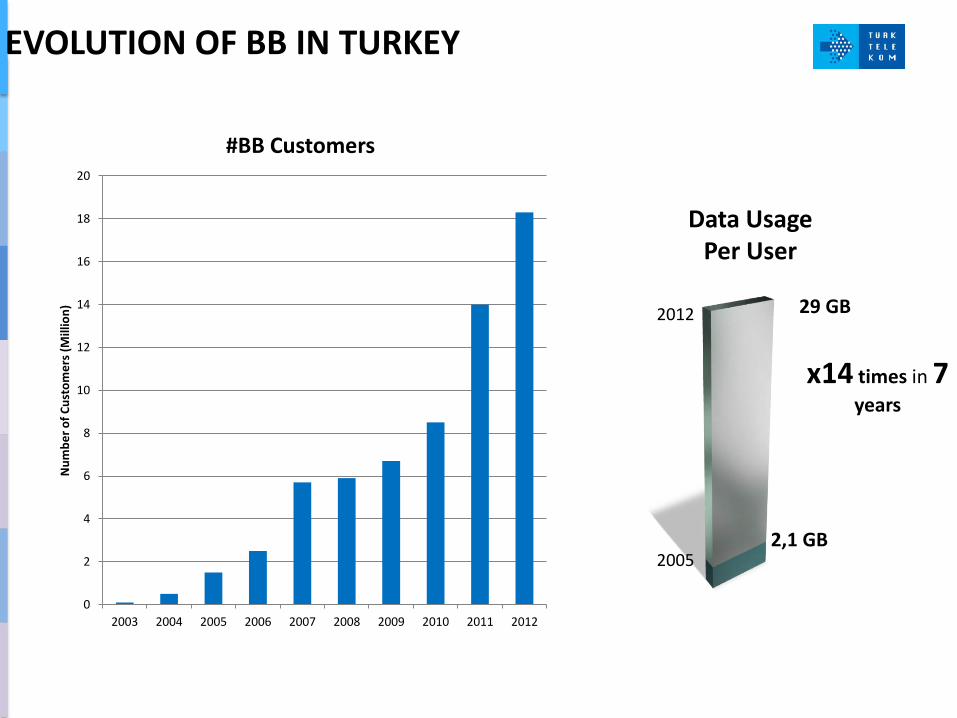

Global Fix BB Subc (2008-2015) (M)

Socrce: Ovum, Global forecastpack 2009-2014

TT Group Revenue 2012

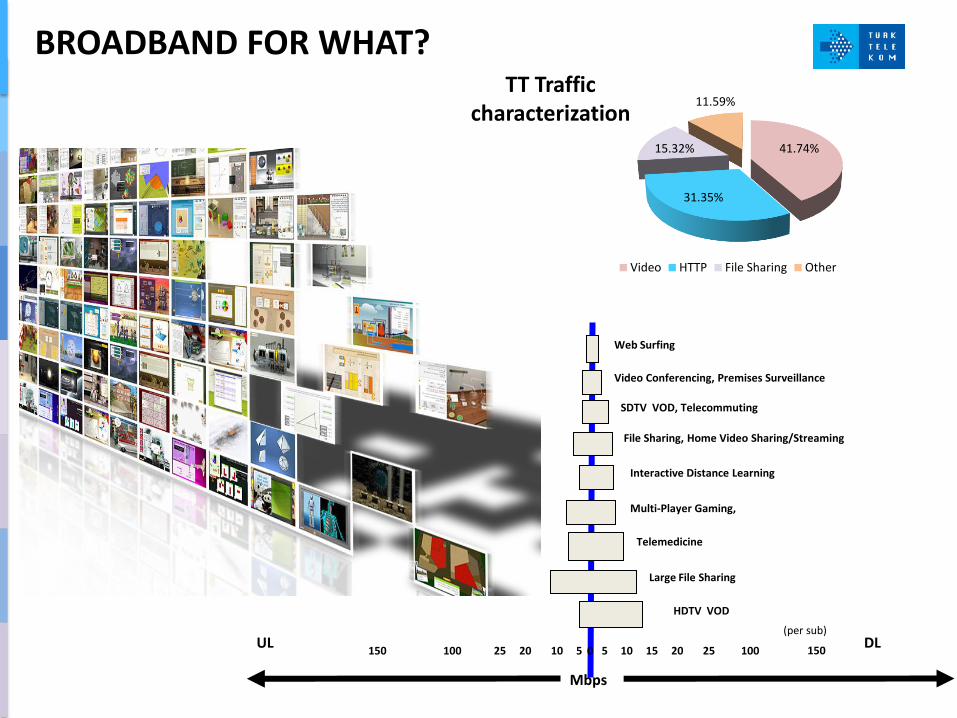

UL DL

Mbps

150 100 25 20 10 5 0 5 10 20 25 100 150 15

HDTV VOD

Large File Sharing

Telemedicine

Multi-Player Gaming,

Interactive Distance Learning

File Sharing, Home Video Sharing/Streaming

SDTV VOD, Telecommuting

Video Conferencing, Premises Surveillance

Web Surfing

(per sub)

41.74%

31.35%

15.32%

11.59%

Video HTTP File Sharing Other

TT Traffic characterization

BROADBAND FOR WHAT?

Data Usage Per User

29 GB

2,1 GB

2012

2005

x14 times in 7 years

0

2

4

6

8

10

12

14

16

18

20

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Nu

mb

er

of

Cu

sto

me

rs (

Mill

ion

)

#BB Customers

EVOLUTION OF BB IN TURKEY

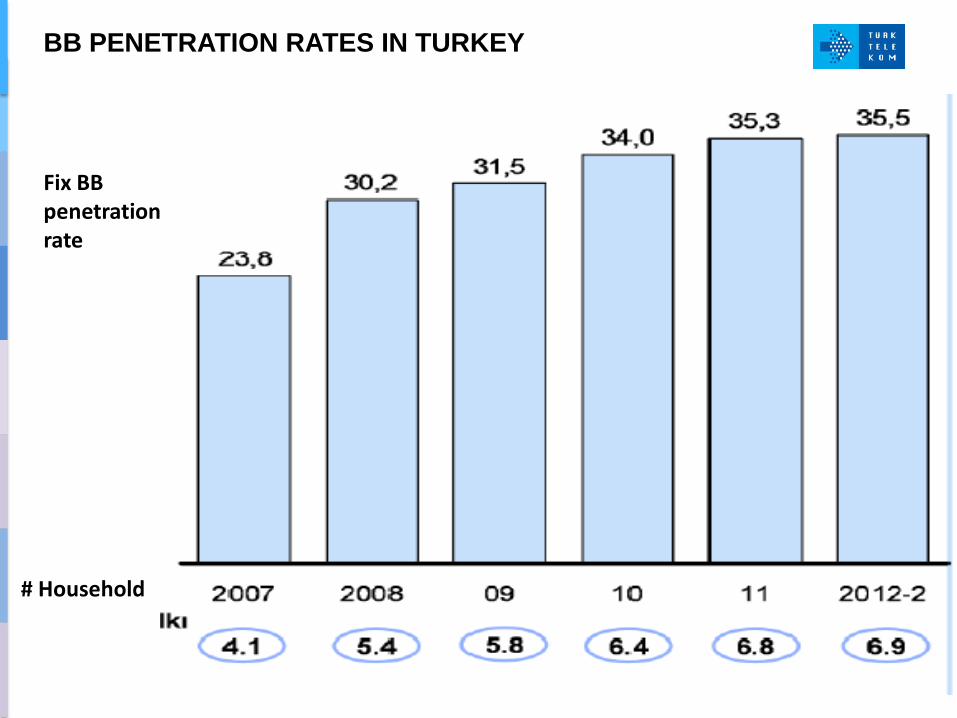

BB PENETRATION RATES IN TURKEY

Fix BB penetration rate

# Household

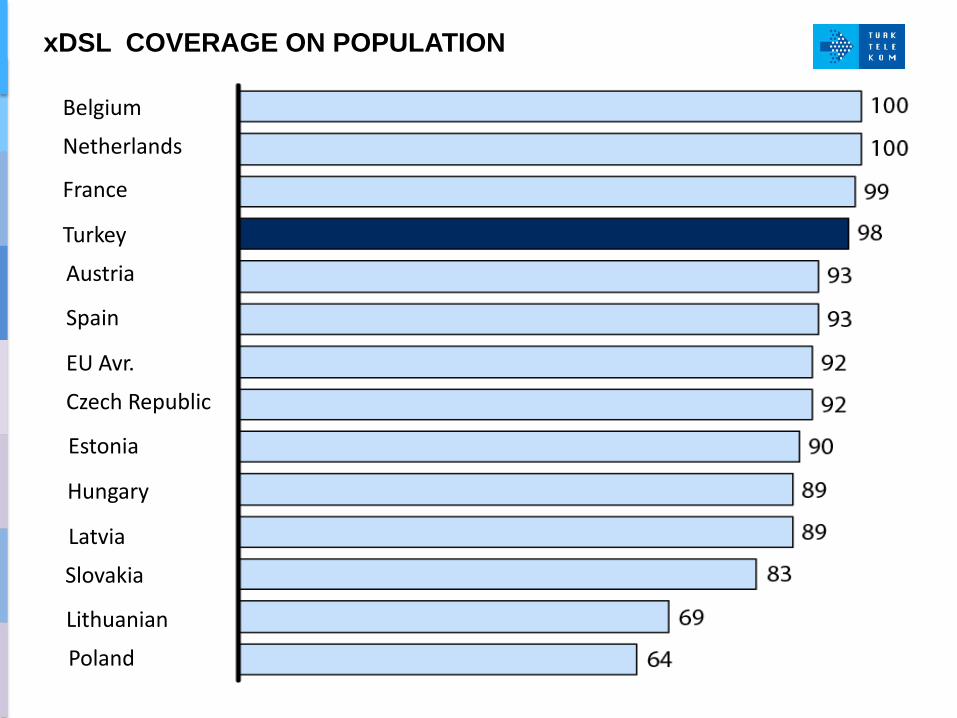

xDSL COVERAGE ON POPULATION

Belgium

Netherlands

France

Turkey

Austria

Spain

EU Avr.

Czech Republic

Estonia

Hungary

Latvia

Slovakia

Lithuanian

Poland

FIBER BLAST: DOING EVERYTHING AT THE SAME TIME

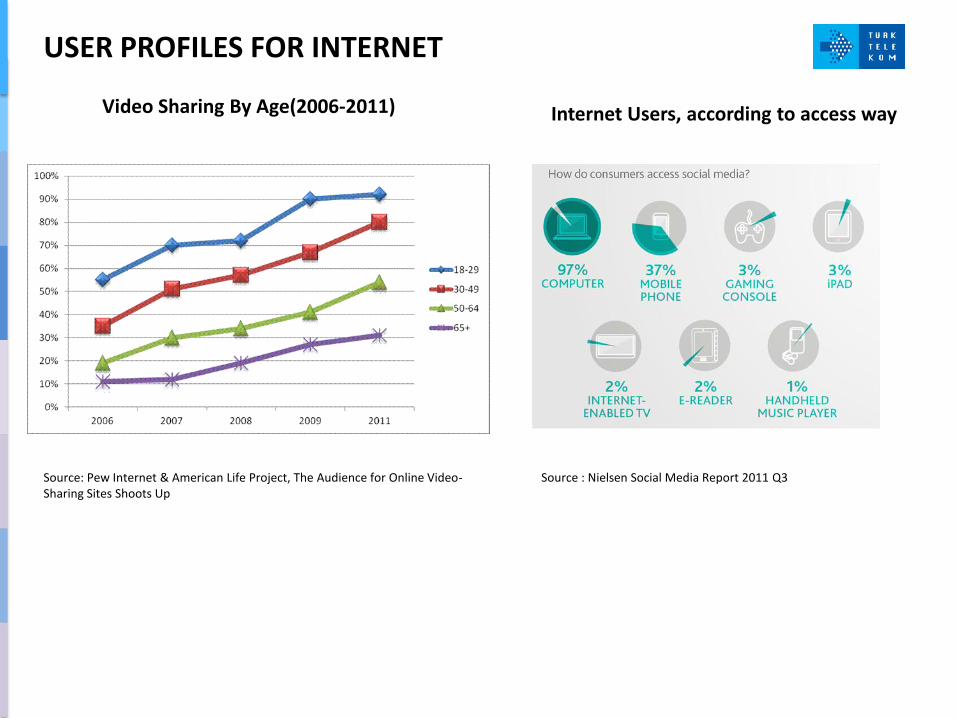

Source: Pew Internet & American Life Project, The Audience for Online Video-Sharing Sites Shoots Up

USER PROFILES FOR INTERNET

Video Sharing By Age(2006-2011) Internet Users, according to access way

Source : Nielsen Social Media Report 2011 Q3

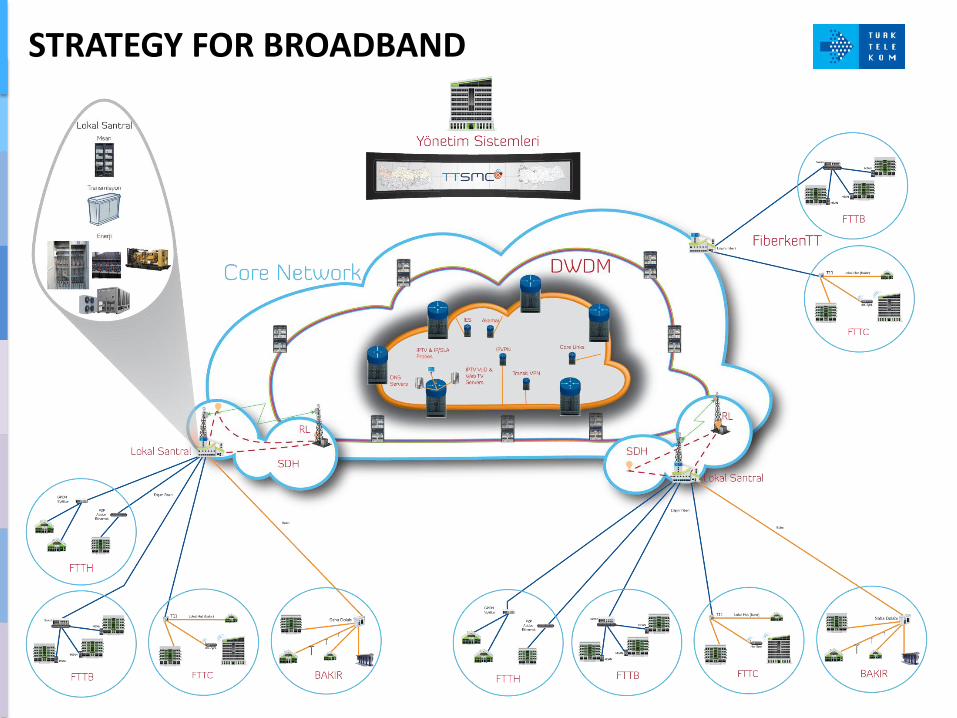

STRATEGY FOR BROADBAND

FIBERCITTY Internet for Everybody

Access for Whole Country

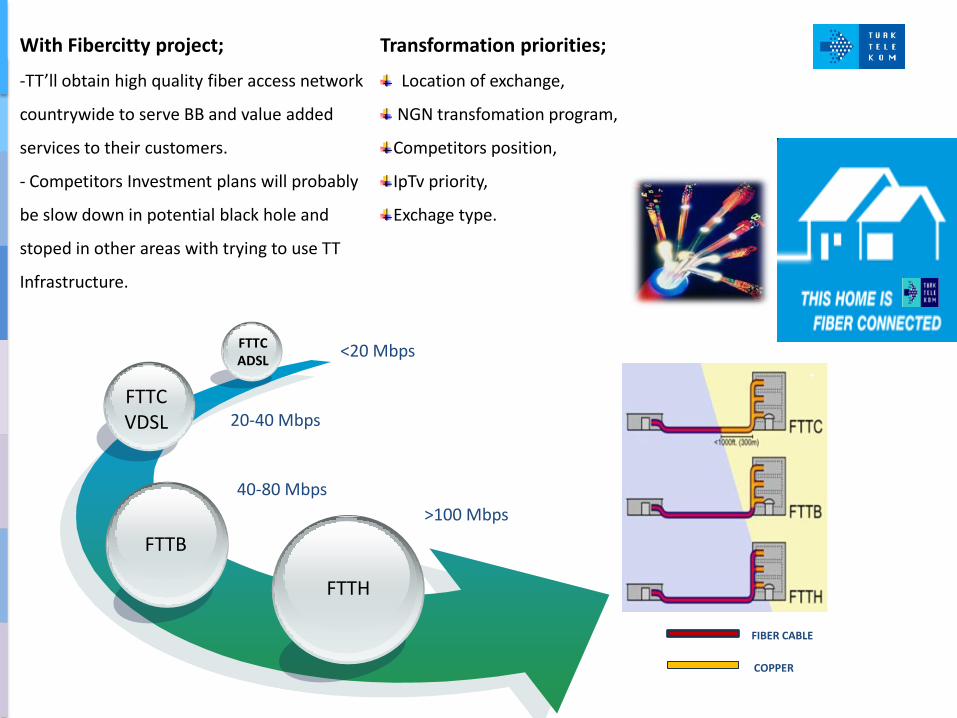

With Fibercitty project;

-TT’ll obtain high quality fiber access network

countrywide to serve BB and value added

services to their customers.

- Competitors Investment plans will probably

be slow down in potential black hole and

stoped in other areas with trying to use TT

Infrastructure.

Transformation priorities;

Location of exchange,

NGN transfomation program,

Competitors position,

IpTv priority,

Exchage type.

FTTH

FTTB

FTTC VDSL

FTTC ADSL

>100 Mbps

40-80 Mbps

20-40 Mbps

<20 Mbps

FIBER CABLE

COPPER

Target :

Much more bandwidth and speed to the customers

Ability of serving the value added services

Description:

Transformation of the existing copper access infrastructure into fiber optical access infrastructure.

Scope:

Replacement of copper cables between CO and street cabinets/ Costumer buildings with

Fiber Optic cables

Depending on the type of area, income level, topology and conditions of competition, FTTH,

FTTB or FTTC solutions could be implemented.

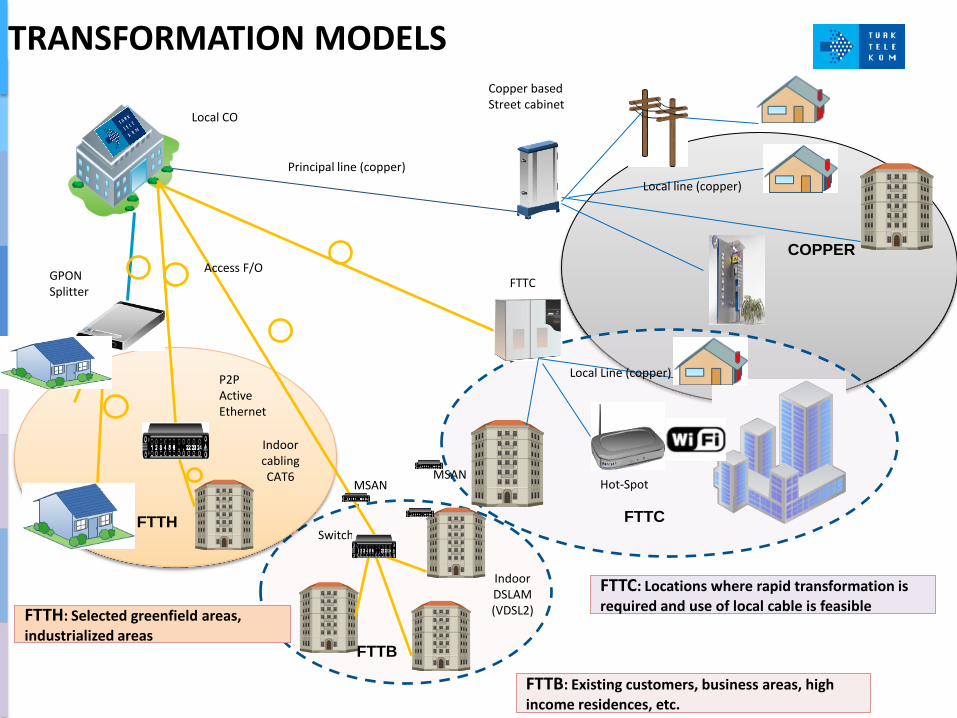

PROJECT DESCRIPTION AND SCOPE

Local CO

Copper based Street cabinet

FTTC

Principal line (copper)

FTTC

COPPER

GPON Splitter

FTTH

P2P Active Ethernet

Indoor cabling CAT6

Local line (copper)

Hot-Spot

Local Line (copper)

Access F/O

Switch

Indoor DSLAM (VDSL2)

FTTB

FTTH: Selected greenfield areas, industrialized areas

FTTB: Existing customers, business areas, high income residences, etc.

FTTC: Locations where rapid transformation is required and use of local cable is feasible

TRANSFORMATION MODELS

MSAN MSAN

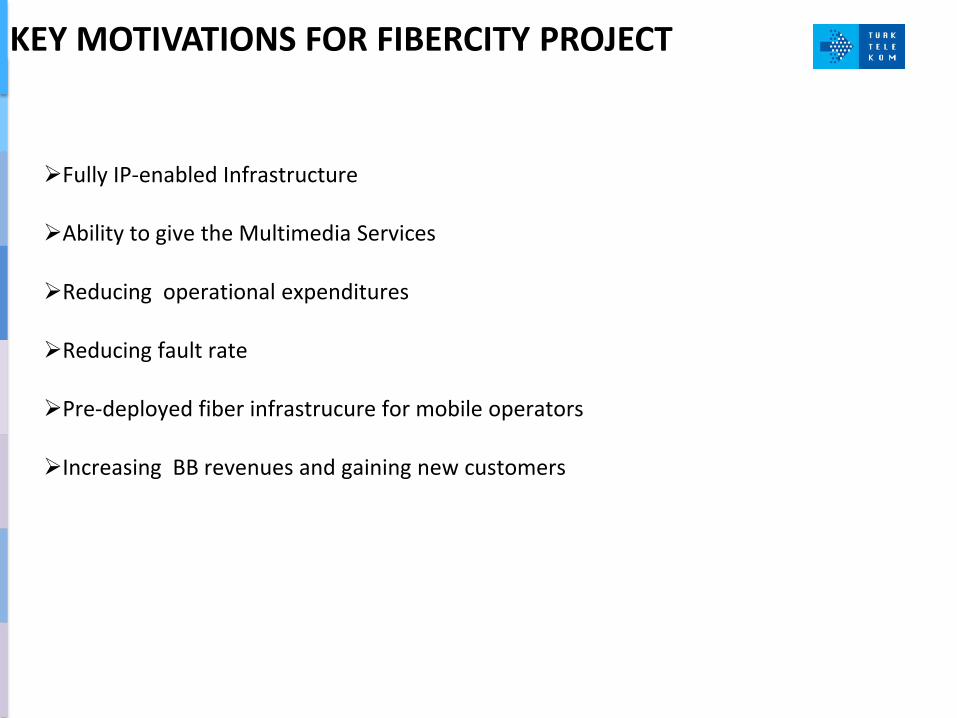

KEY MOTIVATIONS FOR FIBERCITY PROJECT

Fully IP-enabled Infrastructure

Ability to give the Multimedia Services

Reducing operational expenditures

Reducing fault rate

Pre-deployed fiber infrastrucure for mobile operators

Increasing BB revenues and gaining new customers

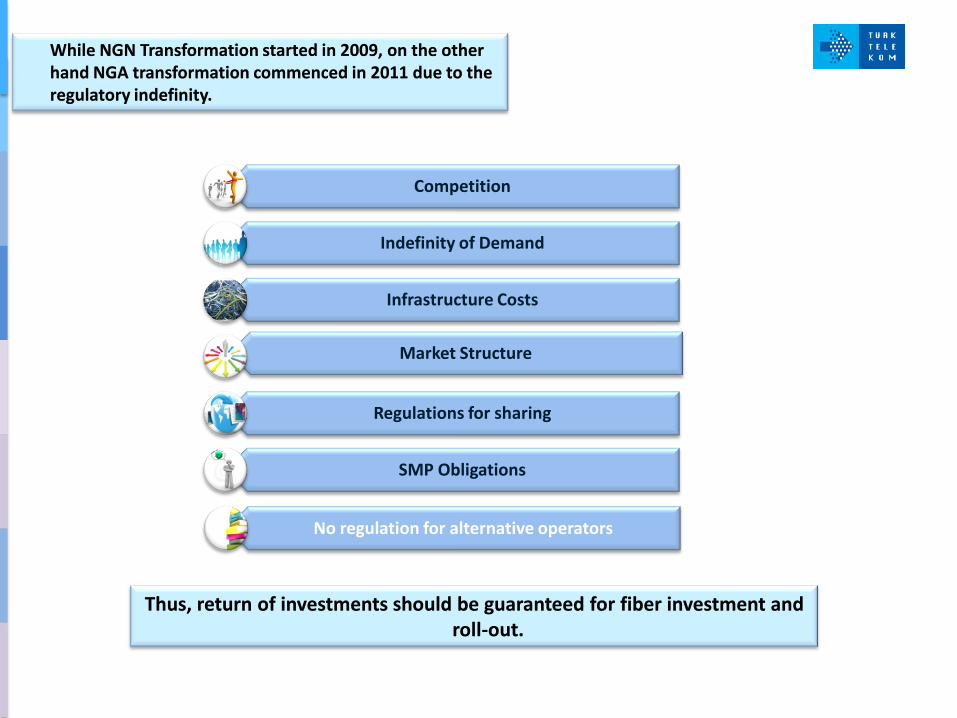

Competition

Indefinity of Demand

Infrastructure Costs

Market Structure

Regulations for sharing

SMP Obligations

No regulation for alternative operators

Thus, return of investments should be guaranteed for fiber investment and roll-out.

While NGN Transformation started in 2009, on the other hand NGA transformation commenced in 2011 due to the regulatory indefinity.

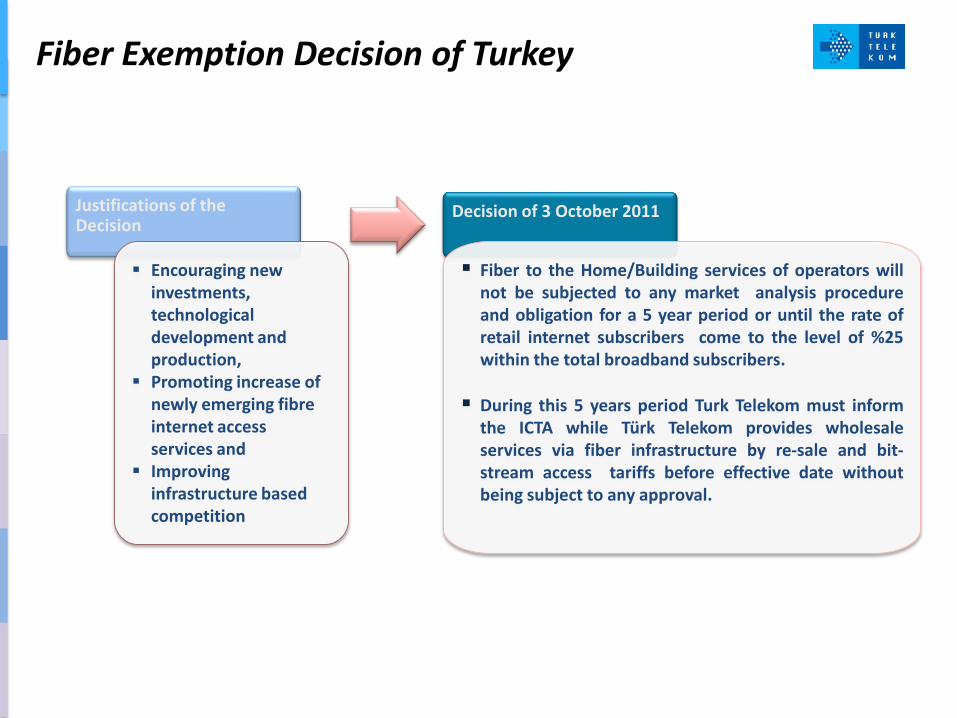

Justifications of the Decision

Encouraging new investments, technological development and production,

Promoting increase of newly emerging fibre internet access services and

Improving infrastructure based competition

Decision of 3 October 2011

Fiber to the Home/Building services of operators will not be subjected to any market analysis procedure and obligation for a 5 year period or until the rate of retail internet subscribers come to the level of %25 within the total broadband subscribers.

During this 5 years period Turk Telekom must inform the ICTA while Türk Telekom provides wholesale services via fiber infrastructure by re-sale and bit-stream access tariffs before effective date without being subject to any approval.

Fiber Exemption Decision of Turkey

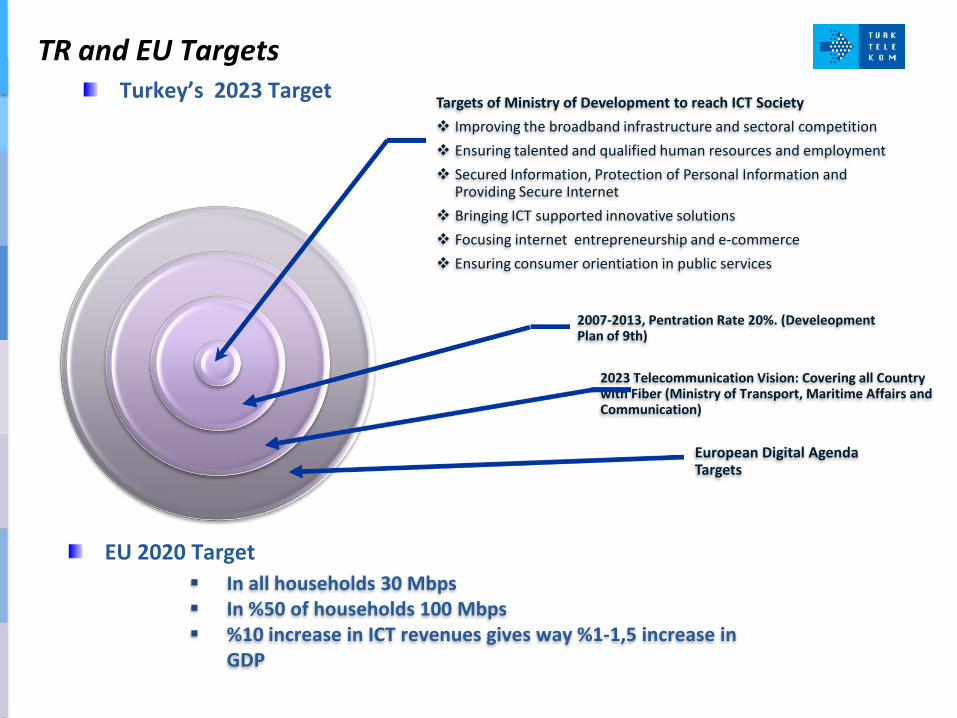

TR and EU Targets

Targets of Ministry of Development to reach ICT Society

Improving the broadband infrastructure and sectoral competition

Ensuring talented and qualified human resources and employment

Secured Information, Protection of Personal Information and Providing Secure Internet

Bringing ICT supported innovative solutions

Focusing internet entrepreneurship and e-commerce

Ensuring consumer orientiation in public services

2007-2013, Pentration Rate 20%. (Develeopment Plan of 9th)

2023 Telecommunication Vision: Covering all Country with Fiber (Ministry of Transport, Maritime Affairs and Communication)

European Digital Agenda Targets

EU 2020 Target

Turkey’s 2023 Target

In all households 30 Mbps In %50 of households 100 Mbps %10 increase in ICT revenues gives way %1-1,5 increase in

GDP

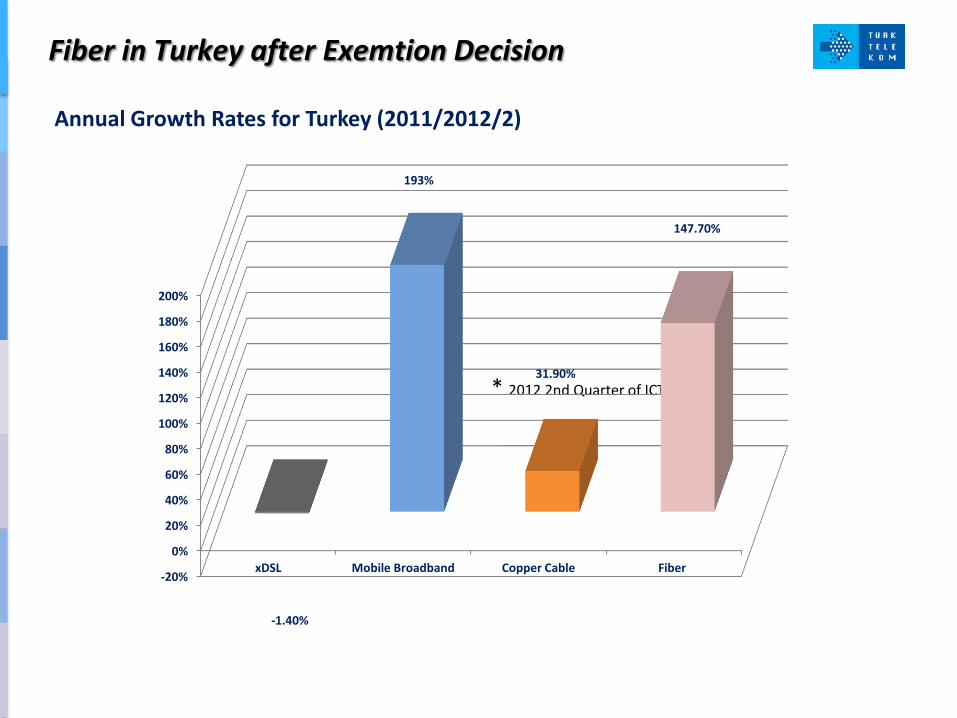

Fiber in Turkey after Exemtion Decision

* 2012 2nd Quarter of ICTA Report

-20%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

xDSL Mobile Broadband Copper Cable Fiber

-1.40%

193%

31.90%

147.70%

Annual Growth Rates for Turkey (2011/2012/2)

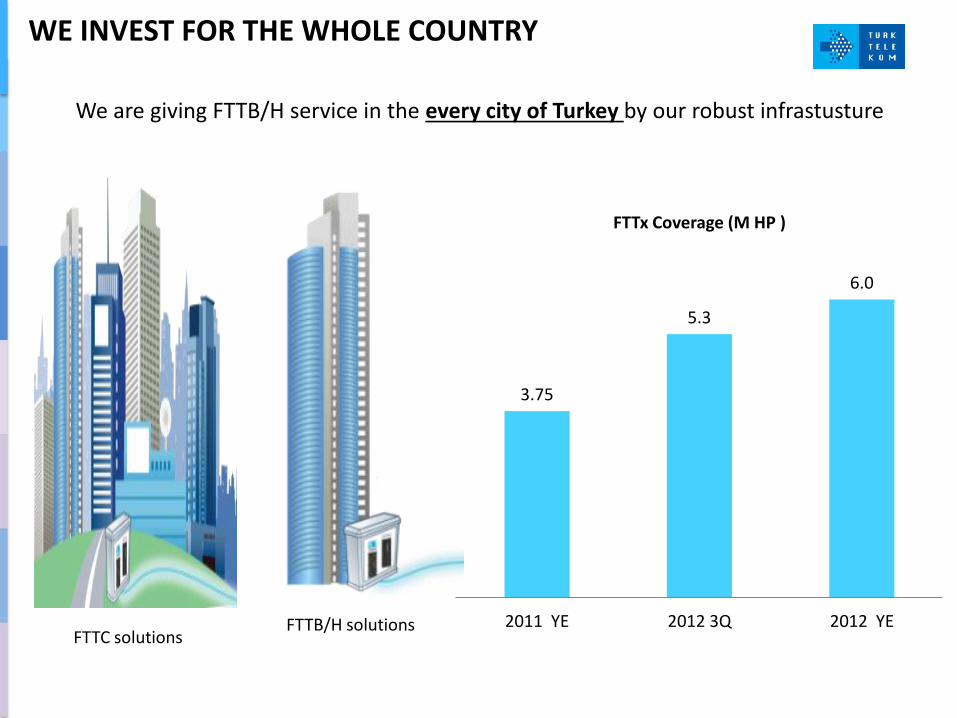

WE INVEST FOR THE WHOLE COUNTRY

FTTC solutions FTTB/H solutions

3.75

5.3

6.0

2011 YE 2012 3Q 2012 YE

FTTx Coverage (M HP )

We are giving FTTB/H service in the every city of Turkey by our robust infrastusture

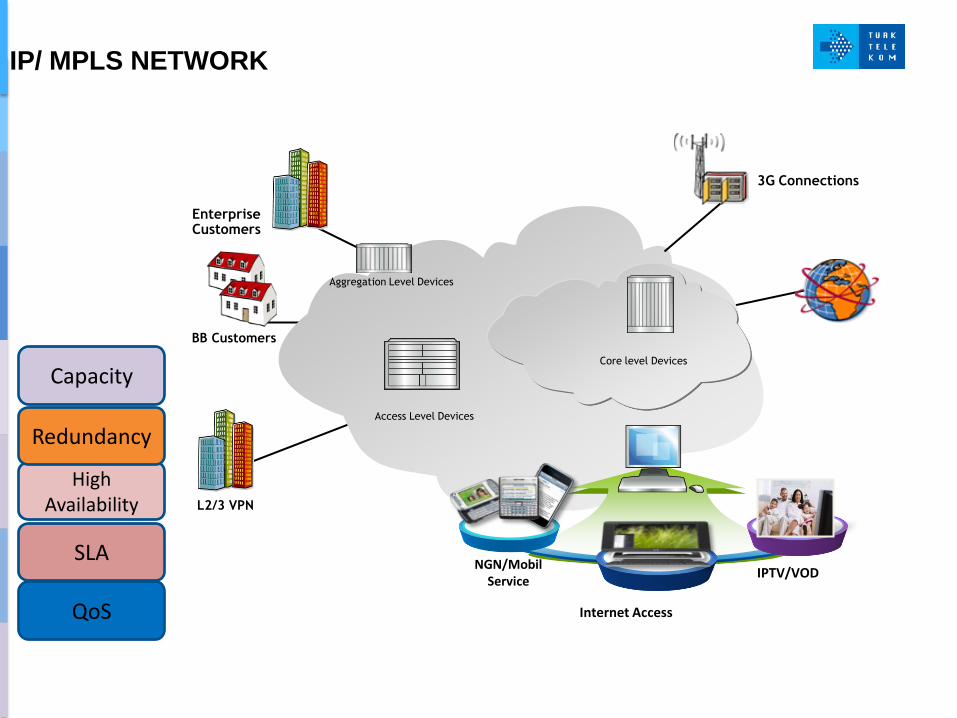

MANAGEMENT

ACCESS NETWORK

TRANSMISSION IP/MPLS NETWORK

BB STRATEGY IN TURK TELEKOM

BB Customers

Enterprise Customers

3G Connections

Core level Devices

Aggregation Level Devices

Access Level Devices

NGN/Mobil Service

Internet Access

IPTV/VOD

L2/3 VPN

QoS

SLA

High Availability

Redundancy

Capacity

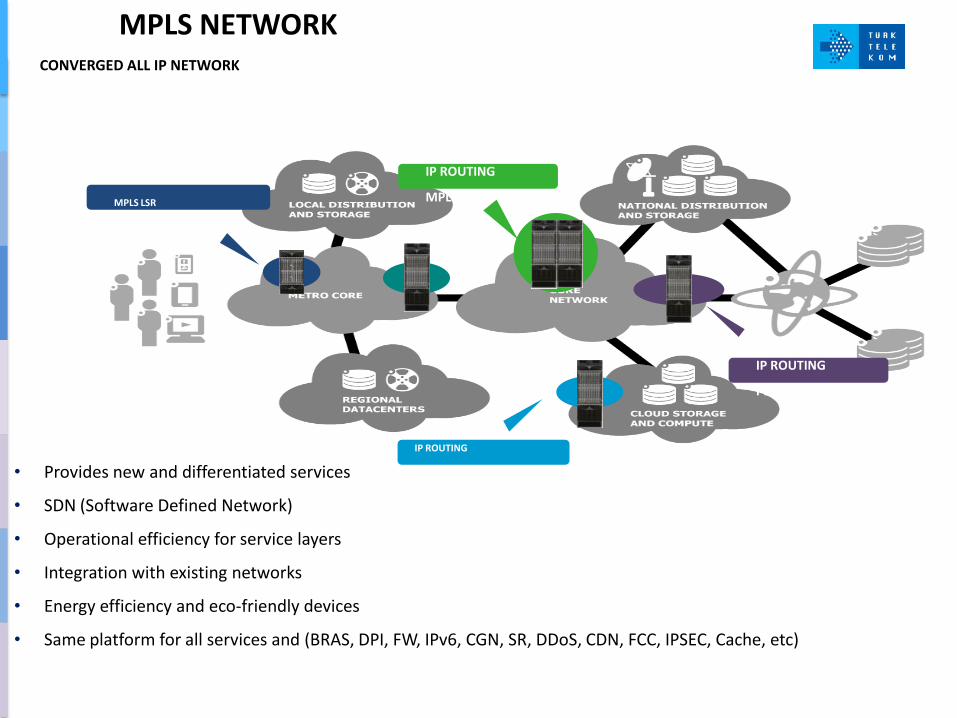

IP/ MPLS NETWORK

MPLS NETWORK CONVERGED ALL IP NETWORK

IP ROUTING

MPLS LSR

IP ROUTING

MPLS LSR

INFRASTRUCTURE

SERVICES

IP ROUTING

PEERING

IP ROUTING

DC INTERCONNECT • Provides new and differentiated services

• SDN (Software Defined Network)

• Operational efficiency for service layers

• Integration with existing networks

• Energy efficiency and eco-friendly devices

• Same platform for all services and (BRAS, DPI, FW, IPv6, CGN, SR, DDoS, CDN, FCC, IPSEC, Cache, etc)

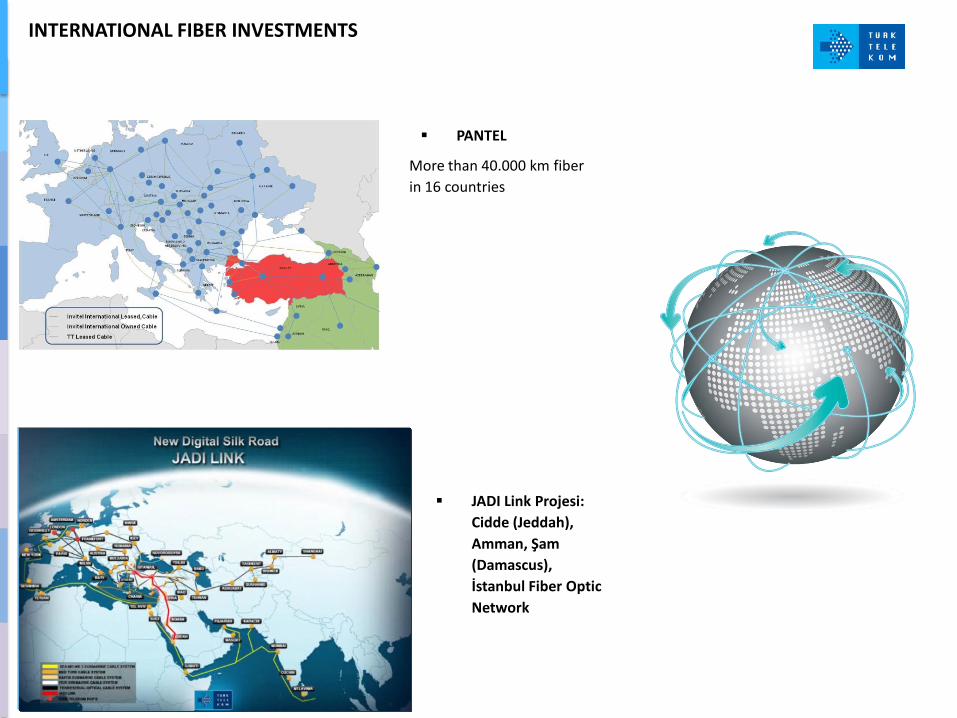

More than 40.000 km fiber

in 16 countries

JADI Link Projesi:

Cidde (Jeddah),

Amman, Şam

(Damascus),

İstanbul Fiber Optic

Network

INTERNATIONAL FIBER INVESTMENTS

PANTEL

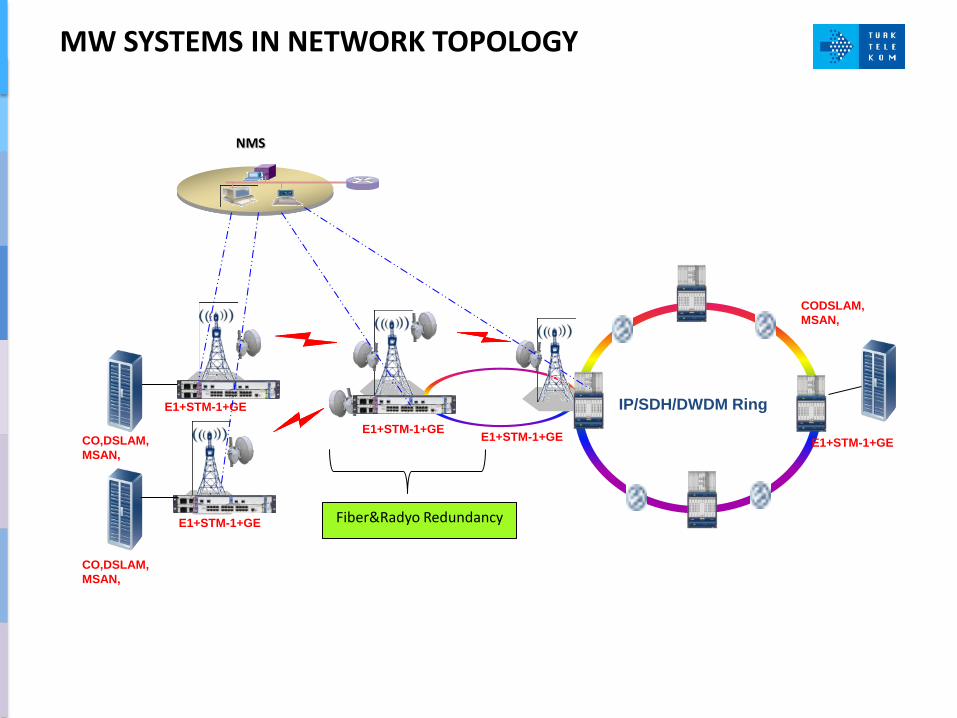

MW SYSTEMS IN NETWORK TOPOLOGY

IP/SDH/DWDM Ring

E1+STM-1+GE

E1+STM-1+GE

E1+STM-1+GE

NMS

E1+STM-1+GE CO,DSLAM,

MSAN,

CO,DSLAM,

MSAN,

Fiber&Radyo Redundancy

E1+STM-1+GE

CODSLAM,

MSAN,

UNIVERSAL SERVICE PROJECT

• Covers rural areas where there is not adequate telecommunication infrastructure

• Provisioning of fixed telephone and broadband internet services

• Scope: 2300 villages will be covered

CONCLUSION

Bandwidth Requirements are increasing

Close to customer

Indoor Outdoor Transformation necessary

FIBERCITY Project will «provide Distrubuted IP enabled Infrastructure», «Increase the Bandwidth», «Reduce the OPEX», «Reduce the network fault rate»

Access Network is not enough itself, Transmission, IP/MPLS Network and Management should be considered together.

Thank you for your attention … [email protected] www.turktelekom.com.tr