Embed Size (px)

Citation preview

http://pesd.stanford.edu/

Natural Gas and GeopoliticsNatural Gas and Geopolitics

CeSSACeSSA

David G. VictorDavid G. VictorProgram on Energy & Sustainable DevelopmentProgram on Energy & Sustainable Development

Stanford UniversityStanford University

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 2

Overview of the StudyOverview of the Study

• Collaboration between the James A. Baker III Institute for Public Policy, Rice University and Program on Energy and Sustainable Development, Stanford University

• Research partners conducted seven historical case studies

• New book fromCambridge University Press �

• New study: demand for gas in China and India

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 3

Gas Resources and Potential Demand

White: where the lights are on, satellite imageryBlue ���� Red : Gas resources, with increasing size (USGS)

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 4

Overview of this PresentationOverview of this Presentation

1. Changing roles for governments

• Winning suppliers are rich in gas and governance

2. Supply security and gas cartels• Few interruptions• Gas cartel unlikely

3. Gas markets in the future

• Chinese and Indian demand

• Major regulatory and political risks

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 5

Atlantic LNGQatargas LNG

Arun LNG

TransMed

YABOG

GasBol

GasAndes

The Belarus Connector

Bluestream

KKKTurkmenistan Export Routes

0 3,000 6,0001,500 Kilometers

ExistingProposed

International Gas Trade Projects: Lessons from Hist ory

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 6

1. 1. Changing Roles for GovernmentsChanging Roles for Governments

• “Old World”

• State-owned enterprises

• Tightly regulated monopolies

• Oil-indexed gas prices

• “New World”

• Private operators, financing, and contracting

• Contestable, multiple markets

• Gas-on-gas competition

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 7

From States to MarketsFrom States to Markets

1970 2000

State

Hybrid

Private

Yabog(Bolivia�Argentina)

1972

Arun(Indonesia

LNG� Japan)1978

Transmed(Algeria� Italy)

1983

QatargasLNG�

Japan1996

Belarus Connector

1996

GasBol1998

Turkmenistan ���� Iran

1997

Trinidad LNG1999

Bluestream(Russia�Turkey)

2002

GasAndes1997

Con

trol

ove

r ke

y ga

s en

terp

rises

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 8

^

Hibiscus

South Seg

Dolphin

Loran

Teak

Caribbean Sea

Venezuela

Trinidad

Tobago

AtlanticOcean

Gulf of Paria

Columbus Channel

Point Fortin

62°W

62°W

61°W

61°W

60°W

60°W

10°N 10°N

11°N 11°N

^ LNG Facilities

Gas PipelinesExisting

Proposed

Gas_Fields ]0 50 10025 Kilometers

Confidence for Investors:The Success of Trinidad and Failure of Venezuela

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 9

-2,000

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

2006 2010 2014 2018 2022 2026 2030 2034 2038

BC

M

Central, South America North America Europe Russia

Other FSU Middle East North Africa Other Africa

South Asia China Asia Pacific Importers Asia Pacific Exporters

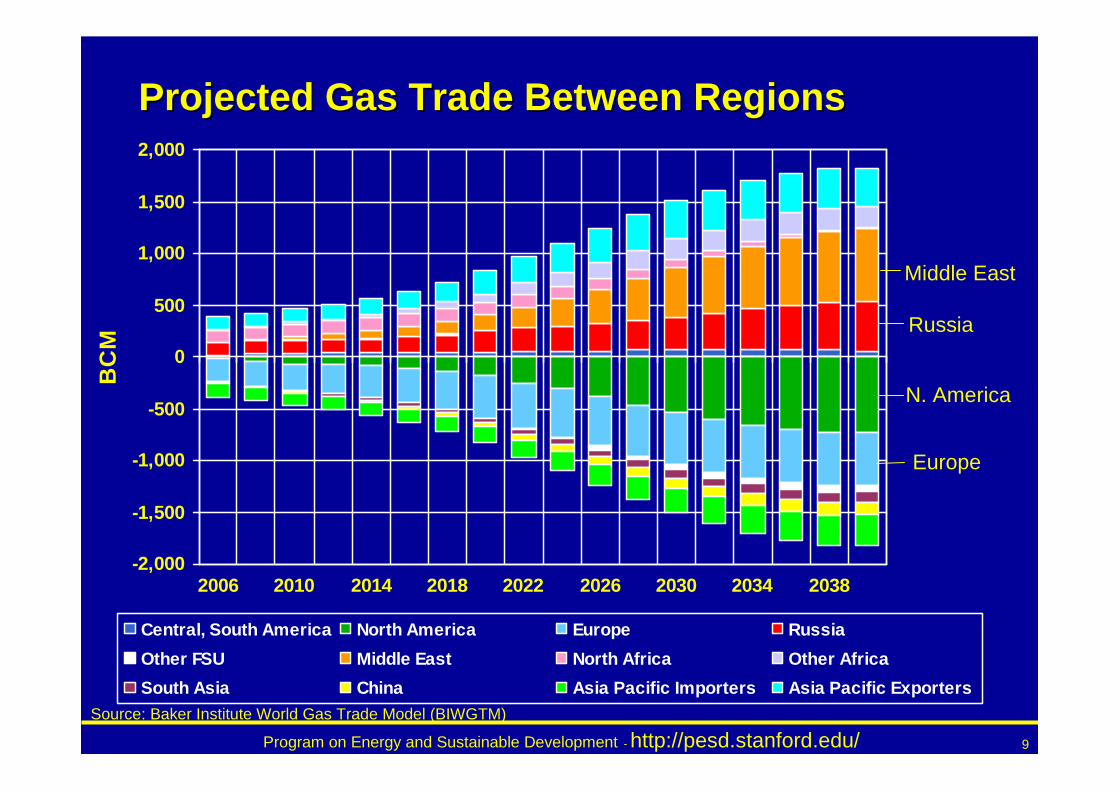

Projected Gas Trade Between RegionsProjected Gas Trade Between Regions

Source: Baker Institute World Gas Trade Model (BIWGTM)

Russia

Middle East

N. America

Europe

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 10

0

20

40

60

80

100

120

140

BC

M

2004 2012 2020

U.S.Europe

Projected US and European LNG ImportsProjected US and European LNG Imports

Source: BIWGTM, Base Case Results

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 11

2. 2. Supply SecuritySupply Security

• Rising attention to “gas security”

• How many interruptions? And by whom?

• Could a gas cartel form?

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 12

Gas Trade InterruptionsGas Trade Interruptions

1. U.S. Govt. (1981) disallows Algerian shipments in retaliation to price demands.2. YABOG (1987). Argentina refuses to take or pay for full Bolivian shipments.3. GasBol (2001). Brazil refuses full volumes contracted from Bolivia 4. Qatargas (1998). Japan demands price reductions.5. Bluestream (2002). Turkey demands price and volume reductions for Russian gas.

User

1. Russia (1997-1998). Gazprom refuses to transport Turkmen gas to Europe.2. Ukraine (mid-1990s) disputes with Gazprom over volumes and payments for gas

shipments.3. Gazprom (2004) cuts supplies to Belarus (and to Europe via Belarus Connector) in

pricing dispute with Belarus.4. Gazprom (2005-2006) cuts supplies to Ukraine during a pricing dispute but tries to

keep supplies flowing to Europe through cross-Ukraine pipelines.

Transit Country

1. Algeria (1981 to 1983). “Gas Battle” with Italy, the United States and others.2. Arun (2001). Civil unrest in Aceh disrupts shipments.3. GasAndes (2004). Argentine government curtails shipments to Chile.

Supplier

Examples from 7 Case StudiesInitiating Party

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 13

A Gas Cartel Is UnlikelyA Gas Cartel Is Unlikely

Others35%

UAE4%

Saudi Arabia4%

Qatar7%

Iran15%

Russia32%

United States3%

Distribution of Proved Gas Reserves Implies Concentration

US EIA; Proved gas reserves (2002)

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 14

3. 3. Gas Markets in the FutureGas Markets in the Future

• Will supplies materialize?

• Incredible governments, politicized resources

• Will demand materialize?

• Will CO2 regulation help gas? • Emerging gas markets in China and India

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 15

Uncertain Supplies: The Russian CaseUncertain Supplies: The Russian Case

0

100

200

300

400

500

600

700

1974 1978 1982 1986 1990 1994 1998 2002 2006 2010 2014 2018

BC

M

Urengoyskoye

YamburgskoyeMedvezh'yeZapalyarnoe

DeficitTotal Production

Source: IEA 2002, Stern, J.P. 2005

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 16

Credibility: The ‘Commitment Problem’Credibility: The ‘Commitment Problem’

1. State supplies credibility• “Old World” : state provides capital, enforcer, gua rantor

(e.g. Transmed)

• “New World”: credibility through transparency, rep utation

• “Real” World: one-off deals, erratic credibility

2. Realign incentives• Partner with locals ���� political leverage AND exposure

3. Engage international institutions?• Provide capital and leverage broader relationship ( e.g.

GasBol)

• External accounts

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 17

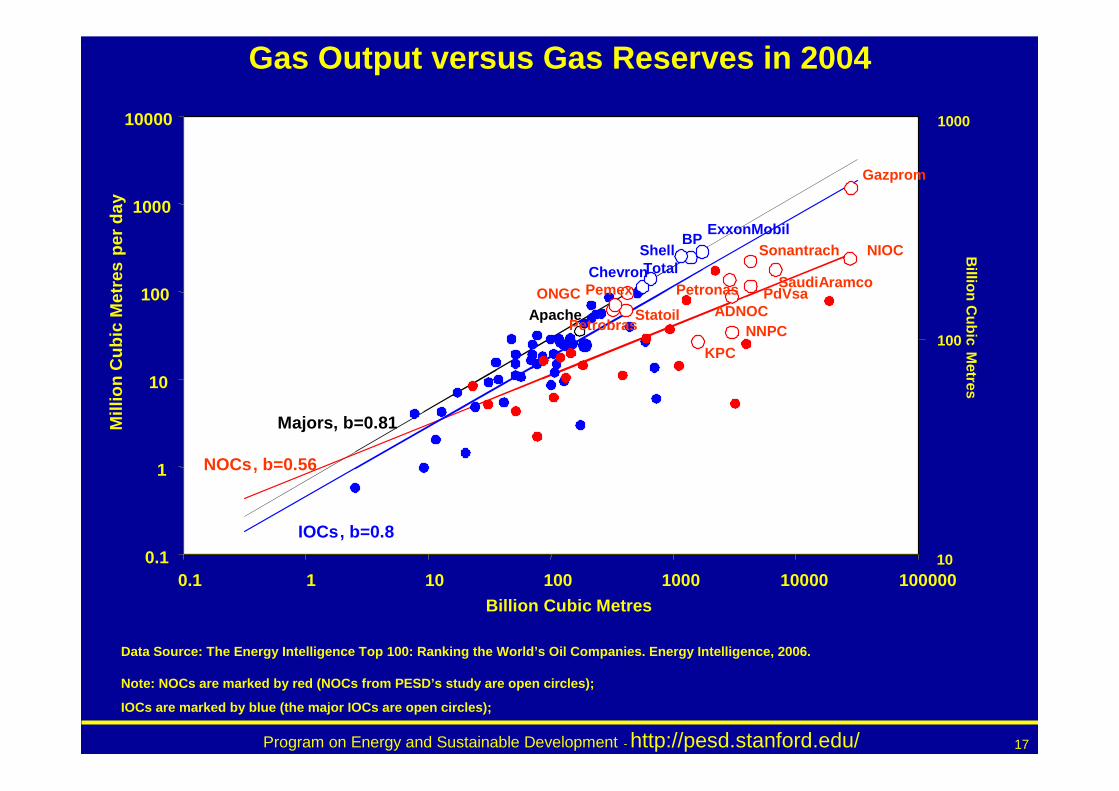

Gas Output versus Gas Reserves in 2004

10

100

1000

Billion C

ubic Metres

0.1

1

10

100

1000

10000

0.1 1 10 100 1000 10000 100000Billion Cubic Metres

Mill

ion

Cub

ic

Met

res

per

day

Chevron

ExxonMobilShellTotal

Apache

Gazprom

Pemex

Petrobras

PdVsaONGCSaudiAramcoPetronas

Statoil ADNOC

Sonantrach

NNPC

BP

KPC

NIOC

NOCs, b=0.56

IOCs, b=0.8

Majors, b=0.81

Data Source: The Energy Intelligence Top 100: Ranki ng the World’s Oil Companies. Energy Intelligence, 2006.

Note: NOCs are marked by red (NOCs from PESD’s study are open circles);

IOCs are marked by blue (the major IOCs are open circ les);

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 18

NOCs: “Dead” Gas versus Country’s Gas Reserves per capit a, 2004

Data Source: PIW (2006), BP (2006), WB (2006). Note : “Dead” oil was estimated on the base of regressio n equation for IOC’s Majors (PESD, 2007);

Average share of "dead" gas in total gas reserves f or NOCs is 46% and median is 65%. In 2004 Gazprom own s 68% of the gas stock and produced

93% of total gas in Russia, while the independent p roducers own only 30% of the gas stock and 7% of the production.

1

10

100

1,000

10,000

100,000

1,000,000

0.1 1.0 10.0 100.0 1000.0 10000.0

Country's Gas Reserves per Capita, Mcm per capita

"Dea

d" G

as, M

illio

ns B

arre

ls o

f oil

equi

vale

nt

ADNOC

CPC

EGPC

INOC

Kazmunaigas

KPC

NIOC

PdVSA

Pertamina

Qatar Petroleum

RosneftSaudi Aramco

Gazprom

CNOOC

PetroChina

Sinopec

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 19

0

100

200

300

400

500

600

700

2002 2010 2020 2030

BC

M

Will Demand Materialize?Will Demand Materialize?

Projected European Gas Consumption

Source: IEA-WEO 2004

ElectricPower

Residential /Commercial

Industry

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 20

Changing Projections for the Total Energy Changing Projections for the Total Energy Mix in 2020Mix in 2020

0%

20%

40%

60%

80%

100%

EIA 2002 EIA 2004 EIA 2006

Other

Nuclear

Gas

Oil

Coal

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 21

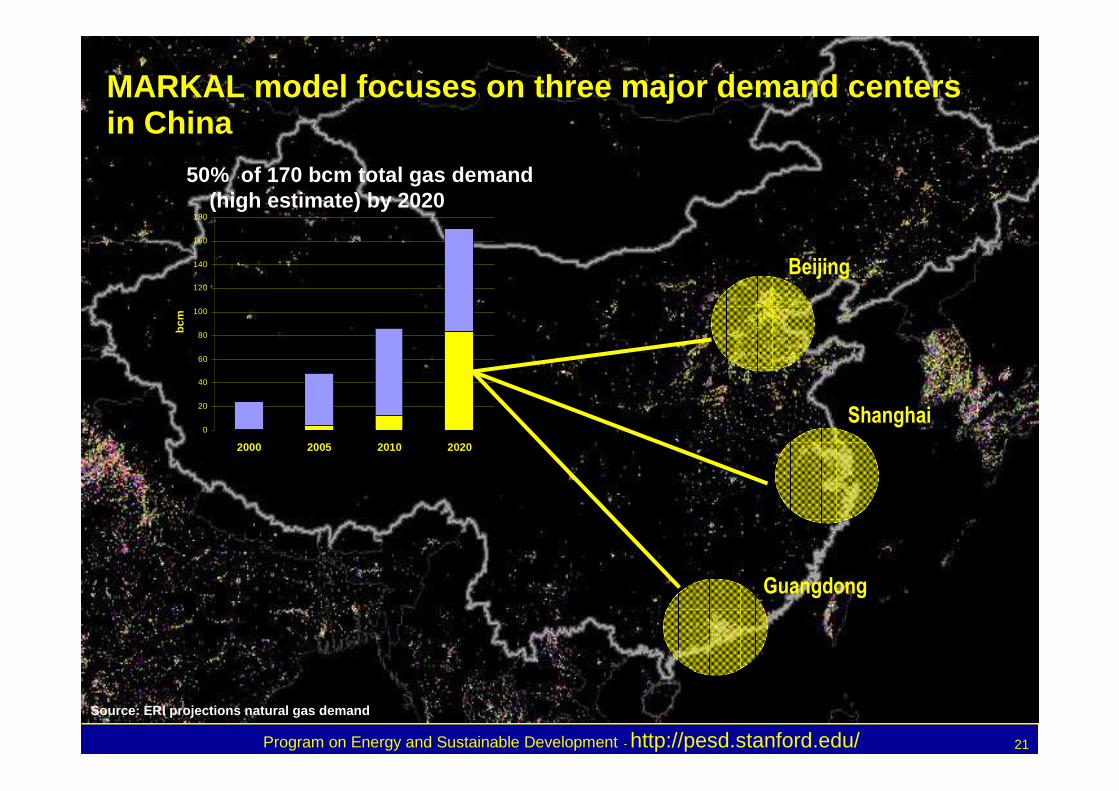

MARKAL model focuses on three major demand centers MARKAL model focuses on three major demand centers in Chinain China

Beijing

Shanghai

Guangdong

0

20

40

60

80

100

120

140

160

180

2000 2005 2010 2020

bcm

Source: ERI projections natural gas demand

50% of 170 bcm total gas demand (high estimate) by 2020

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 22

Demand for natural gas in the three regions is Demand for natural gas in the three regions is highly sensitive to environmental constrainthighly sensitive to environmental constraint

R= Reference case

P = Plausible scenario, imposed 40% decrease in SO 2

A = Aggressive scenario, 75% decrease in SO2

83 bcm

35 bcm

R P A R P A R P A R P A0

10

20

30

40

50

60

70

80

90

BC

M

Guangdong

Beijing

Shanghai

R P A2000 2005 2010 2015 2020

R= Reference case

P = Plausible scenario, imposed 40% decrease in SO 2

A = Aggressive scenario, 75% decrease in SO2

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 23

0

50000

100000

150000

200000

250000

300000

350000

400000

kt

Guangdong CO 2emissions by sector

R P A

2000 2005 2010 2015 2020

R P A R P A R P A

=1082816Aggressive

431511Plausible

202020152010Million tons

CO2 emissions savings

Transportation Residential Industrial Power plants

R P A

ReferencePlausible

Aggressive

Implications for COImplications for CO 22: : Do CODo CO22 emissions decrease?emissions decrease?

Program on Energy and Sustainable Development - http://pesd.stanford.edu/ 24

Conclusions:Conclusions:

• Governance drives investment

• “Real” world is a hybrid market

• A fungible, global market delivers security?

• Where governments aren’t credible, gas is left in the ground

• Gas-to-power highly uncertain

• Gas could help address the CO2 problem, even in markets where there are no CO2 regulations