Embed Size (px)

Citation preview

1

Papalote Ventures LLC Mike Reed

10Nov16

Natural Gas, Power, & Crude Fundamentals

Highlights Natural Gas • Natural gas price down (-$0.16) MMBtu week on week. • Temperature –

o U.S. Climate Prediction Center confirmed today that a weak La Nina is underway. It has the potential to bring the coldest U.S. winter since the “polar vortex” that sent gas prices surging across the U.S. in 2014, bullish sentiment.

o U.S. Climate Prediction Center U.S. 8-14 day outlook, bearish sentiment;

• Stocks – Storage inject +54 BCF last week, compared to my forecast +56 BCF, compared to

market expectation +51 BCF, bearish sentiment. Storage injections averaging +1 BCF/week more than prior year over past 4 weeks, bearish sentiment. o Natural gas stocks set a new record of 4,017 BCF, besting the prior record of 4,009 BCF

set 20Nov15, bearish sentiment.

2

o Forecast flipping from 108 consecutive weeks year on year surplus to year on year deficit 1Jan17, 1st year on year deficit since 5Dec14, 2.1 year glut is ending, bullish sentiment.

• Supply/Demand – Demand down (-11) BCF week year on year, supply down (-11) BCF week year on year, neutral sentiment. o Storage release confirming supply down trend started 5 weeks ago with supply down

(-15) BCF week average over prior 5 weeks, bullish sentiment. o Warm fall temperatures are masking supply drop, which I don’t think the market fully

understands yet. When winter temperatures normalize, the market will be surprised at how fast storage is drawn down to replace lost production. If we have a colder winter year on year, the market will be shocked at how fast storage is drawn down to replace lost production.

• Price – Apr-17 price forecast $2.97 - $3.22 range, compared to futures $2.79. Crude • Crude price up +$0.10 BBL week on week, US dollar caused down (-$5.80) BBL,

supply/demand caused up +$5.90 BBL. • US Dollar – Up +1.8% week on week, bearish sentiment.

o US Dollar – Up to the strongest level since February as investors adjusted to the reality of a Trump administration and increased inflation expectations. Benchmark Treasury 10-year yields exceeded 2 percent for the first time since January as Trump’s win fueled expectations of looser fiscal policy and quicker inflation. Trump’s proposals, including pledges to cut taxes and spend as much as $500 billion on infrastructure, are seen by economists as inflationary and leading to higher U.S. interest rates.

o Euro – Down on Trump’s ascendancy could arguably increase political uncertainty in the European Union, slow Eurozone growth and complicate the job of the European Central Bank which could therefore undermine the Euro going forward.

o Japanese Yen – Down on decision by the Bank of Japan to anchor the long end of the curve by fixing the 10-year Japanese Government Bond at zero means that in a global market where rate curves are steepening (U.S. inflation) and Japanese rate curves are anchored, then Japanese interest rates will remain comparatively low, weakening the Yen.

• Supply/Demand – o Crude stocks up +2,432,000 BBL, compared to my forecast +2,600,000, compared to

market expectation +2,000,000, compared to 5-year average +667,000, bearish sentiment.

o U.S. crude imports normalized at 7.0 MM BBLS/day, compared to Hurricane Matthew delay 8.9 MM BBLS/day last week, compared to 6.9 MM BBLS/day 4-week average prior to last week, bullish sentiment.

o U.S. refinery utilization normalized at 87.1%, compared to 85.2% prior week, compared to 5-year average 87.4%. Despite refinery utilization jumping +1.9% week on week, gasoline stocks were still down (-1.3%) week on week, distillate stocks were down (-1.3%), and total stocks were down (-0.3%), bullish sentiment.

3

o Total stocks, since peaking 28 weeks ago at 911 MM BBLS, are down (-56) MM BBLS, down (-6%), down 20 of 27 weeks since, and down recent 7 of 8 weeks, bullish sentiment.

o U.S. crude production jumped +2.0% week on week, the largest % and BBL jump in 77 weeks, jumped from 8,522,000 BBLS/day to 8,692,000 BBLS/day, up +170,000 BBLS/day, bearish sentiment.

4

Natural Gas U.S. Temperature U.S. population weighted average temperature last week warmer +1.3 degrees F YoY, last week 62.0 degrees F compared to prior year 60.7 degrees F U.S. Industrial Demand • Industrial demand last week up +1.3% YoY • Refinery utilization last week dn (-2.4%) YoY • Steel utilization dn (-1.1%) YoY U.S. Coal • Coal production last week 16.9 MM NT/week, up +0.4 MM NT/week YoY, up +2% YoY • Coal inventories end Aug 162.6 MM NT, up +6.0 MM NT YoY, up +4% YoY, dn (-9.1) MM NT

MoM, dn (-5.3%) MoM, 42nd percentile • West PRB 8800 price $11.80 NT, unchanged MoM, up +15% YoY • East CSX 1% price $63.25 NT, up +12.9% MoM, up +70% YoY U.S. Nuclear Nuclear generation last week up +2.1% YoY U.S. Hydro Hydro generation last week up +1.0% YoY U.S. Wind/Solar • Wind generation 637,270 MWh/d, dn (-2.8%) YoY • Solar generation 82,740 MWh/d, up +30.9% YoY • Wind + solar generation 720,010 MWh/d, up +0.2% YoY U.S. Exports Mexico U.S. exports to Mexico last week 3.33 BCF/d, up +1.8% WoW, up +13% YoY U.S. LNG Imports/Exports Aug-16 • Imports 1.82 BCF/week, up +40% MoM, dn (-28%) YoY • Exports (-6.04) BCF/week, up +70% MoM, up +870% YoY • Net Exports (-4.22) BCF/week, up (-1.97) BCF/week MoM, up +87% MoM, up (-6.13)

BCF/week YoY, up +321% YoY U.S. Crude Production (associated natural gas) Crude production last week 8,692,000 barrels/day, up +2.0% WoW, up +2.7% MoM, dn (-5%) YoY

5

North American Natural Gas Rigs • Rigs up +1 last week vs. up +1 same week last year • Rigs now 194, dn (-111) YoY, dn (-36%) YoY U.S. Natural Gas Storage Storage inject +54 BCF last week • vs. my forecast +56 BCF, bullish sentiment • vs. market expectation +51 BCF, bearish sentiment • vs. 5-year average +36 BCF, bearish sentiment • vs. inject +54 BCF same week last year, 0 BCF YoY variance • Total demand dn (-11) BCF/week YoY, total supply dn (-11) BCF/week YoY Variance breakdown view

YoY • Storage now 4,017 BCF, up +32 BCF YoY, up +1% YoY • Storage same week 5-year average 3,832 BCF • Storage now 84% full vs. 83% full same week last year Storage and price view

Temperature variance this year continues Prior 4 weeks’ storage has averaged +1 BCF per week compared to same 4 weeks last year, if unchanged, then:

• Storage inject season ends 11/18/16 at 4,043 BCF (84% full) o vs. prior year ending 11/20/15 at 4,009 BCF (84% full) o vs. Nov 18th five year average 3,799 BCF (79% full) o Apr-17 natural gas price forecast $2.97 compared to natural gas futures $2.79

VarianceDemand Temperature 9 BCFDemand Industrial (1) BCFDemand Nuclear 2 BCFDemand Hydro 0 BCFDemand Wind/Solar 0 BCFDemand Coal Plants Retired 0 BCFDemand Gas to Coal Switching 9 BCFDemand Mexico Exports (3) BCF VarianceDemand LNG Import/Export Net (6) BCF Total Demand 11 BCFSupply Gas Rig Count (19) BCFSupply Gas Rig Efficiency 1 BCFSupply Associated/Shut-in/Reclassify/EIA Error 7 BCF Total Supply (11) BCF

Total Variance This Year 0 BCF Total Variance 0 BCFSubtract Temperature Variance 9 BCFTotal Variance Last Year (9) BCF

6

Temperature variance last year continues Prior 4 weeks’ storage has averaged (-9) BCF per week compared to same 4 weeks last year, if unchanged, then:

• Storage inject season ends 11/18/16 at 4,024 BCF (84% full) o vs. prior year ending 11/20/15 at 4,009 BCF (84% full) o vs. Nov 18th five year average 3,799 BCF (79% full) o Apr-17 natural gas price forecast $3.22 compared to natural gas futures $2.79

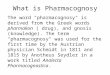

Technical • Fast moving 9 day moving average crossed under 20 day moving average 27Oct16; bearish

sentiment • Slow moving 50 day moving average crossed over 200 day moving average 20Jun16; bullish

sentiment

1.50 1.70 1.90 2.10 2.30 2.50 2.70 2.90 3.10 3.30 3.50

4/1/

16

4/22

/16

5/13

/16

6/3/

16

6/24

/16

7/15

/16

8/5/

16

8/26

/16

9/16

/16

10/7

/16

10/2

8/16

$MM

Btu

Prom

pt M

onth

Fut

ures

50 Days20 Days9 Days1 Day200 Days

7

Power Generation Type • Nuclear up +4% YoY last week, compared to up +2% YoY two weeks ago • Coal up +14% YoY last week, compared to up +14% two weeks ago • Natural Gas dn (-8%) YoY last week, compared to dn (-13%) YoY two weeks ago • Wind dn (-11%) YoY last week, compared to unchanged YoY two weeks ago • Hydro up +44% YoY last week, compared to up +41% YoY two weeks ago • Industrial Gas up +9% YoY last week, compared to up +7% YoY two weeks ago • Other dn (-2%) YoY last week, compared to dn (-19%) YoY two weeks ago • Total up +4% YoY last week, compared to up +2% YoY two weeks ago

Natural Gas Henry Hub Henry Hub prompt month natural gas $2.61 MMBtu, dn (-5.7%) WoW, up +15% YoY Natural Gas Basis • Columbia TCO prompt month basis (-$0.159) MMBtu, up +$0.027 WoW, dn (-$0.004) YoY • ERCOT Houston prompt month basis (-$0.008) MMBtu, up +$0.013 WoW, up +$0.057 YoY • SoCal Gas prompt month basis $0.203 MMBtu, up +$0.065 WoW, up +$0.029 YoY

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

Last

Wee

k M

Wh/

Day

Aver

age

2015 2016

8

Natural Gas Delivered • Delivered prompt month Columbia TCO $2.45 MMBtu, dn (-5.1%) WoW, up +16% YoY • Delivered prompt month ERCOT Houston $2.60 MMBtu, dn (-5.3%) WoW, up +18% YoY • Delivered prompt month SoCal Gas $2.81 MMBtu, dn (-3.2%) WoW, up +15% YoY Heat Rate • PJM West on-peak prompt month 12.2 MMBtu/MWh, dn (-2.6%) WoW, dn (-16%) YoY • ERCOT Houston on-peak prompt month 9.4 MMBtu/MWh, dn (-0.9%) WoW, dn (-12%) YoY • CAISO SP15 on-peak prompt month 12.3 MMBtu/MWh, up +0.2% WoW, dn (-5%) YoY Spark Spread • PJM West on-peak prompt month

o 11.0 heat rate peaker $2.96 MWh, dn (-25.2%) WoW, down (-60%) YoY o 7.2 heat rate combined cycle $12.27 MWh, dn (-10.9%) WoW, dn (-21%) YoY

• ERCOT on-peak prompt month o 11.0 heat rate peaker (-$4.18) MWh o 7.2 heat rate combined cycle $5.71 MWh, dn (-8.7%) WoW, dn (-24%) YoY

• CAISO SP15 on-peak prompt month o 11.0 heat rate peaker $3.66 MWh, dn (-1.8%) WoW, dn (-24%) YoY o 7.2 heat rate combined cycle $14.35 MWh, dn (-2.9%) WoW, up +2% YoY

Power • PJM West on-peak prompt month $29.92 MWh vs. $30.64 same day last year, dn (-$0.72)

MWh YoY variance • ERCOT Houston on-peak prompt month $24.45 MWh vs. $23.35 same day last year, up

+$1.10 YoY variance • CAISO SP15 on-peak prompt month $34.60 MWh vs. $31.65 same day last year, up +$2.95

YoY variance Variance breakdown view

PJM WestERCOT Houston

CAISO SP15

Variance Variance VarianceCost Natural Gas Henry $5.04 $3.68 $4.51 MWhCost Natural Gas Basis ($0.06) $0.60 $0.38 MWhCost Natural Gas Delivered $4.99 $4.28 $4.88 MWhReserve Margin Heat Rate ($5.71) ($3.18) ($1.93) MWh

Total Variance ($0.72) $1.10 $2.95 MWh

9

Crude US Dollar • DXY index (Euro weighted) 98.91 this week, up +1.8% WoW, up +1% MoM, unchanged YoY,

bearish sentiment o Each +/- 1% USD change = -/+ $3.30 BBL change

• US trade weighted broad dollar index (Yuan weighted) 123.12 last week, dn (-0.4%) WoW, up +1% MoM, up +3% YoY, bullish sentiment o Each +/- 1% USD change = -/+ $3.72 BBL change

70

80

90

100

110

120

130$20

$40

$60

$80

$100

$120

$140

$160

Jan-

08Se

p-08

May

-09

Jan-

10Se

p-10

May

-11

Jan-

12Se

p-12

May

-13

Jan-

14Se

p-14

May

-15

Jan-

16Se

p-16 US

Tra

de W

eigh

ted

Broa

d Do

llar (

Reve

rse

Orde

r)

Prom

pt W

TI C

rude

$BB

L

Crude Price US Dollar

10

Stocks • US crude 485 MM BBL, up +0.5% WoW, up +2% MoM, up +7% YoY, tanks 83% full, 90th

percentile o Crude stocks up +2,432,000 BBL last week vs. my forecast +2,600,000, bullish sentiment vs. market expectation +2,000,000, bearish sentiment vs. 5-year average +667,000, bearish sentiment vs. same week last year +3,981,000, bullish sentiment

• Each +/- 1% crude stocks change = -/+ $1.80 BBL change • US gasoline 221 MM BBL, dn (-1.3%) WoW, dn (-2%) MoM, up +4% YoY, 53rd percentile • US distillate 149 MM BBL, dn (-1.3%) WoW, dn (-5%) MoM, up +5% YoY, 79th percentile • US total 855 MM BBL, dn (-0.3%) WoW, unchanged MoM, up +6% YoY, 84th percentile • Cushing stocks 58.5 MM BBL, unchanged WoW, dn (-5%) MoM, up +6% YoY, tanks 78% full,

68th percentile

-

100

200

300

400

500

600$20

$40

$60

$80

$100

$120

$140

$160

Jan-

08Au

g-08

Mar

-09

Oct-0

9M

ay-1

0De

c-10

Jul-1

1Fe

b-12

Sep-

12Ap

r-13

Nov-

13Ju

n-14

Jan-

15Au

g-15

Mar

-16

Oct-1

6

Crud

e St

ocks

Milli

on B

arre

ls (R

ever

se O

rder

)

Crude Price Stocks

11

275 300 325 350 375 400 425 450 475 500 525 550 575 600

Oct-1

0

Mar

-11

Aug-

11

Jan-

12

Jun-

12

Nov-

12

Apr-1

3

Sep-

13

Feb-

14

Jul-1

4

Dec-

14

May

-15

Oct-1

5

Mar

-16

Aug-

16

Milli

on B

arre

ls

Crude Stocks Capacity

12

Refinery utilization 87.1%, dn (-2.4%) YoY, vs. 5-year average 87.4%, dn (-0.3%);

65

70

75

80

85

90

95

100Ja

n-08

Jul-0

8Ja

n-09

Jul-0

9Ja

n-10

Jul-1

0Ja

n-11

Jul-1

1Ja

n-12

Jul-1

2Ja

n-13

Jul-1

3Ja

n-14

Jul-1

4Ja

n-15

Jul-1

5Ja

n-16

Jul-1

6

Refin

ery

Utiliz

atio

n Pe

rcen

t

Weekly 5-Year Avg

13

Crude stocks change seasonality last week was week 46; • 5-year average up +667,000 BBL compared to actual stocks change up +2,432,000 BBL

(6,000)

(4,000)

(2,000)

0

2,000

4,000

6,000

8,000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53

Last

5 Y

ears

201

0-20

15 U

.S. C

rude

Sto

cks

Avg

WoW

Cha

nge

(000

) BBL

S

Week

Crude Stocks Change Seasonality

14

• World crude stocks Aug-16 1,180 MM BBL, dn (-2.2%) MoM, up +4% YoY, 83rd percentile • US crude stocks Aug-16 42% of world crude stocks (excluding Strategic Petroleum Reserve)

-

200

400

600

800

1,000

1,200

1,400

Oct-1

0Fe

b-11

Jun-

11Oc

t-11

Feb-

12Ju

n-12

Oct-1

2Fe

b-13

Jun-

13Oc

t-13

Feb-

14Ju

n-14

Oct-1

4Fe

b-15

Jun-

15Oc

t-15

Feb-

16Ju

n-16

Milli

on B

arre

ls

World Crude Stocks US Crude Stocks

15

World Supply/Demand Balance • IEA Q216 world crude supply 95.9 MM BBL/day, dn (-0.7%) QoQ, dn (-1%) YoY • IEA Q216 world crude demand 95.6 MM BBL/day, up +0.3% QoQ, up +2% YoY • IEA Q216 world crude balance +0.3 MM BBL/day surplus, dn (-77.4%) QoQ, dn (-87%) YoY • EIG Sep-16 world crude supply 99.2 MM BBL/day, up +1.3% MoM, up +2% YoY • EIG Sep-16 world crude demand 97.6 MM BBL/day, dn (-0.7%) MoM, up +1% YoY • EIG Sep-16 world crude balance +1.6 MM BBL/day surplus, vs. (-0.4) MM BBL/day deficit

previous month, vs. +0.8 MM BBL/day surplus same month last year

(5.0)

(4.0)

(3.0)

(2.0)

(1.0)

-

1.0

2.0

3.0

4.0

5.0

Jan-

08Ju

l-08

Jan-

09Ju

l-09

Jan-

10Ju

l-10

Jan-

11Ju

l-11

Jan-

12Ju

l-12

Jan-

13Ju

l-13

Jan-

14Ju

l-14

Jan-

15Ju

l-15

Jan-

16Ju

l-16

Bala

nce

Milli

on B

BLS/

Day

IEA EIG

16

Crude Oil Production Mar-2016

0 2000 4000 6000 8000 10000 12000

RussiaSaudi Arabia

U.SIraq

ChinaCanada

IranVenezuela

BrazilMexicoNigeriaAngola

KazakhstanNorway

QatarAlgeriaOman

U.K.ColombiaArgentina

EgyptLibyaSyria

(000) BBLS/Day

Crude Oil Production

17

Import Export Arb WTI discount to Brent (-$1.20) BBL, narrow (-29%) WoW, narrow (-33%) MoM, narrow (-58%) YoY

Ethanol

• Stocks 19.2 MM BBL, dn (-2.6%) WoW, dn (-1%) MoM, up +2% YoY, 52nd percentile • Prompt month RIN $0.65 gallon, unchanged WoW, unchanged MoM

BRIC Real GDP

• Brazil Q216 GDP dn (-0.6%) vs. Q116, dn (-3.8%) vs. Q215 • Russia Q216 GDP up +7.0% vs. Q116, dn (-0.6%) vs. Q215 • India Q216 GDP up +1.9% vs. Q116, up +7.3% vs. Q215 • China Q316 GDP up +1.8% vs. Q216, up +6.7% vs. Q315

(30)

(25)

(20)

(15)

(10)

(5)

-

5

10

15

20

Jan-

08Ju

l-08

Jan-

09Ju

l-09

Jan-

10Ju

l-10

Jan-

11Ju

l-11

Jan-

12Ju

l-12

Jan-

13Ju

l-13

Jan-

14Ju

l-14

Jan-

15Ju

l-15

Jan-

16Ju

l-16

WTI

min

us B

rent

$BB

L

Export Arb <(-$5) BBL

Import Arb >(-$5) BBL

18

U.S. Oil Rigs • Permian 218 rigs, up +6 WoW, up +2.8% WoW, up +7% MoM, dn (-4%) YoY • Eagle Ford 30 rigs, up +1 WoW, up +3.4% WoW, dn (-6%) MoM, dn (-51%) YoY • Williston 37 rigs, up +2 WoW, up +5.7% WoW, up +23% MoM, dn (-42%) YoY • Other 165 rigs, unchanged WoW, up +1% MoM, dn (-25%) YoY • Total 450 rigs, up +9 WoW, up +2.0% WoW, up +5% MoM, dn (-21%) YoY

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Feb-

11Ju

n-11

Oct-1

1Fe

b-12

Jun-

12Oc

t-12

Feb-

13Ju

n-13

Oct-1

3Fe

b-14

Jun-

14Oc

t-14

Feb-

15Ju

n-15

Oct-1

5Fe

b-16

Jun-

16Oc

t-16

OthersWillistonEagle FordPermian

19

U.S. Production Crude production last week 8,692,000 barrels/day, up +2.0% WoW, up +2.7% MoM, dn (-5%) YoY

0

2,000

4,000

6,000

8,000

10,000

12,000

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800Ja

n-08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Jan-

15

Jan-

16

U.S.

Cru

de P

rodu

ctio

n (0

00) B

BLS/

Day

U.S.

Oil

Rig

Coun

t Rigs Production

20

OPEC Unplanned Crude Production Outages Aug-16 • Iran 0.000 MM BBL/day, unchanged MoM, 0.800 MM BBL/day same month last year • Libya 0.990 MM BBL/day, dn (-6%) MoM, dn (-6%) YoY • Nigeria 0.646 MM BBL/day, dn (-5%) MoM, up +119% YoY • Indonesia 0.000 MM BBL/day, unchanged MoM, unchanged YoY • Iraq 0.158 MM BBL/day, dn (-12%) MoM, up +100% YoY • Kuwait 0.250 MM BBL/day, dn (-4%) MoM, unchanged YoY • Saudi Arabia 0.250 MM BBL/day, unchanged MoM, unchanged YoY • Total 2.294 MM BBL/day, dn (-5%) MoM, dn (-16%) YoY

Geopolitical Risk USO OVX VIX index 42.08 infers risk up +1.4% WoW, up +15% MoM, unchanged YoY

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan-

11M

ay-1

1Se

p-11

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14M

ay-1

4Se

p-14

Jan-

15M

ay-1

5Se

p-15

Jan-

16M

ay-1

6Se

p-16

MM

BBL

S/Da

y ArabiaKuwaitIraqIndonesiaNigeriaLibyaIran

21

U.S. Imports • Total 7.0 MM BBL/day, dn (-18.1%) WoW, dn (-5%) MoM, up +2% YoY

o U.S. crude production last week 55.1% of crude demand (imports 44.9%); compared to 57.6% same week last year (imports 42.4%)

• Canada 3.2 MM BBL/day, dn (-2.3%) WoW, unchanged MoM, up +6% YoY o Canada 46% of total imports compared to 44% same week last year

• Saudi Arabia 1.3 MM BBL/day, up +10.7% WoW, up +36% MoM, up +16% YoY • Venezuela 0.5 MM BBL/day, dn (-36.2%) WoW, dn (-25%) MoM, dn (-44%) YoY • Mexico 0.5 MM BBL/day, dn (-25.1%) WoW, up +8% MoM, dn (-19%) YoY • Colombia 0.0 MM BBL/day, dn (-94.5%) WoW, dn (-89%) MoM, dn (-88%) YoY • Iraq 0.4 MM BBL/day, dn (-33.8%) WoW, dn (-28%) MoM, up +6% YoY • Other 1.0 MM BBL/day, dn (-25.3%) WoW, dn (-11%) MoM, up +105% YoY

0

2

4

6

8

10

12

Jun-

10No

v-10

Apr-

11Se

p-11

Feb-

12Ju

l-12

Dec-

12M

ay-1

3Oc

t-13

Mar

-14

Aug-

14Ja

n-15

Jun-

15No

v-15

Apr-

16Se

p-16

4-W

eek

Mov

ing

Aver

age

MM

BBL

S/Da

y

Other Iraq Colombia Mexico Venezuela Saudi Arabia Canada

22

U.S. Exports Total 0.410 MM BBL/day, up +1.5% WoW, dn (-15%) MoM, dn (-19%) YoY

-

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Jun-

10No

v-10

Apr-

11Se

p-11

Feb-

12Ju

l-12

Dec-

12M

ay-1

3Oc

t-13

Mar

-14

Aug-

14Ja

n-15

Jun-

15No

v-15

Apr-

16Se

p-16

Milli

on B

BLS/

Day

Other Canada

23

Exports by destination August-16;

Canada 50%

Netherlands 15%

Italy 6%

Colombia 5%

China 5%

Switzerland 4%

United Kingdom 3%

Sing

apor

e 3%

Cu

raca

o 3%

Lib

eria

2%

So

uth

Afric

a 2%

Spai

n 2%

24

Gulf Coast Refining Profit • 321 crack spread $5.78 BBL, dn (-33.8%) WoW, dn (-29%) MoM, dn (-20%) YoY • EBITDA $2.05 BBL, dn (-154.1%) WoW, dn (-53%) MoM, up +219% YoY

(20)

(10)

-

10

20

30

40

50

Jan-

08Ju

l-08

Jan-

09Ju

l-09

Jan-

10Ju

l-10

Jan-

11Ju

l-11

Jan-

12Ju

l-12

Jan-

13Ju

l-13

Jan-

14Ju

l-14

Jan-

15Ju

l-15

Jan-

16Ju

l-16

$BBL

Crack 321 EBITDA

25

Gulf Coast Light LLS minus Heavy Maya Differential $6.65 BBL, dn (-6.1%) WoW, dn (-21%) MoM, dn (-27%) YoY

-

5

10

15

20

25

30Ja

n-08

Jul-0

8Ja

n-09

Jul-0

9Ja

n-10

Jul-1

0Ja

n-11

Jul-1

1Ja

n-12

Jul-1

2Ja

n-13

Jul-1

3Ja

n-14

Jul-1

4Ja

n-15

Jul-1

5Ja

n-16

Jul-1

6

LLS

min

us M

aya

$BBL

Heavy Unprofitable <$4 BBL

Heavy Profitable >$4 BBL Differential

26

WTI Price WTI $44.82 BBL vs. $42.93 BBL same day last year, up +$1.89 BBL YoY variance Variance breakdown view

Price view Each variance attribute prior 20 trading days trended forward

VarianceSupply US Dollar ($5.95) BBLSupply Geopolitical Risk $32.41 BBLSupply WTI Discount $1.68 BBLSupply/Demand Stocks ($14.97) BBLDemand BRIC GDP ($11.27) BBL

Total Variance $1.89 BBL

$0

$10

$20

$30

$40

$50

$60

14-N

ov-1

6

14-D

ec-1

6

14-J

an-1

7

14-F

eb-1

7

14-M

ar-1

7

14-A

pr-1

7

14-M

ay-1

7

14-J

un-1

7

14-J

ul-1

7

14-A

ug-1

7

14-S

ep-1

7

14-O

ct-1

7

$BBL

View Futures

27

Technical • Fast moving 9 day moving average crossed under 20 day moving average 1Nov16; bearish

sentiment • Slow moving 50 day moving average crossed over 200 day moving average 11May16;

bullish sentiment

30

35

40

45

50

554/

1/16

4/22

/16

5/13

/16

6/3/

16

6/24

/16

7/15

/16

8/5/

16

8/26

/16

9/16

/16

10/7

/16

10/2

8/16

$BBL

Pro

mpt

Mon

th F

utur

es

20 Days50 Days9 Days1 Day200 Days