Embed Size (px)

Citation preview

Natural Resource Partners L.P.

FRIEDMAN BILLINGS RAMSEY

2005 Investor Conference

New York

November 2005

Forward-Looking Statements

The statements made by representatives of Natural Resource Partners L.P. (“NRP”) during the course of this presentation that are not historical facts are forward-looking statements. Although NRP believes that the assumptions underlying these statements are reasonable, investors are cautioned that such forward-looking statements are inherently uncertain and necessarily involve risks that may affect NRP’s business prospects and performance, causing actual results to differ from those discussed during the presentation.

Such risks and uncertainties include, by way of example and not of limitation: general business and economic conditions; decreases in demand for coal; changes in our lessees’ operating conditions and costs; changes in the level of costs related to environmental protection and operational safety; unanticipated geologic problems; problems related to force majeure; potential labor relations problems; changes in the legislative or regulatory environment; and lessee production cuts.

These and other applicable risks and uncertainties have been described more fully in NRP’s 2004 Annual Report on Form 10-K. NRP undertakes no obligation to publicly update any forward-looking statements, whether as a result of new information or future events.

What is 3 years old and weighs over 2 billion tons?

What MLP has increased: Production by ~70%

Reserves by ~85% Lessees by ~115% Leases by ~185%

and

has a reserve life of over 38 years

What MLP has….?

Grown its distribution 44% in the last 3 years

Increased its distribution nine consecutive quarters

Over two full quarters of distributions in cash in the bank

A distribution coverage of 1.37x

Natural Resource Partners L.P.

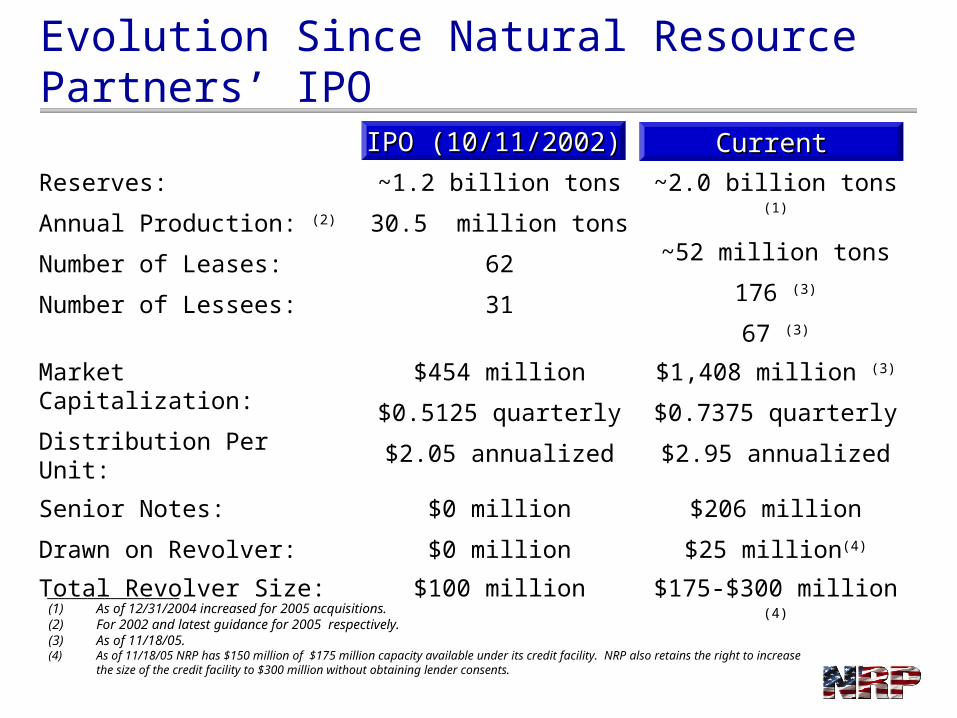

Evolution Since Natural Resource Partners’ IPO

Reserves:

Annual Production: (2)

Number of Leases:

Number of Lessees:

~1.2 billion tons

30.5 million tons

62

31

~2.0 billion tons (1)

~52 million tons

176 (3)

67 (3)

Market Capitalization:

Distribution Per Unit:

$454 million

$0.5125 quarterly

$2.05 annualized

$1,408 million (3)

$0.7375 quarterly

$2.95 annualized

Senior Notes:

Drawn on Revolver:

$0 million

$0 million

$206 million

$25 million(4)

Total Revolver Size: $100 million $175-$300 million (4)

_______________________(1) As of 12/31/2004 increased for 2005 acquisitions.(2) For 2002 and latest guidance for 2005 respectively.(3) As of 11/18/05.(4) As of 11/18/05 NRP has $150 million of $175 million capacity available under its credit facility. NRP also retains the right to increase

the size of the credit facility to $300 million without obtaining lender consents.

IPO (10/11/2002)IPO (10/11/2002) CurrentCurrent

Overview of Natural Resource Partners

Own and manage coal properties in the three major coal producing regions of the United States:

Appalachia, Illinois Basin and Western US

Eleven States Lease reserves to experienced mine operators under long-term

leases in exchange for royalty payments

Royalty payments based on percentage of sales price or fixed price, with periodic minimum payments

Lessees provide coal to diverse group of utilities, steel companies and industrial users

Coal Producing Basins in U.S.

States in which NRP has Coal Reserves

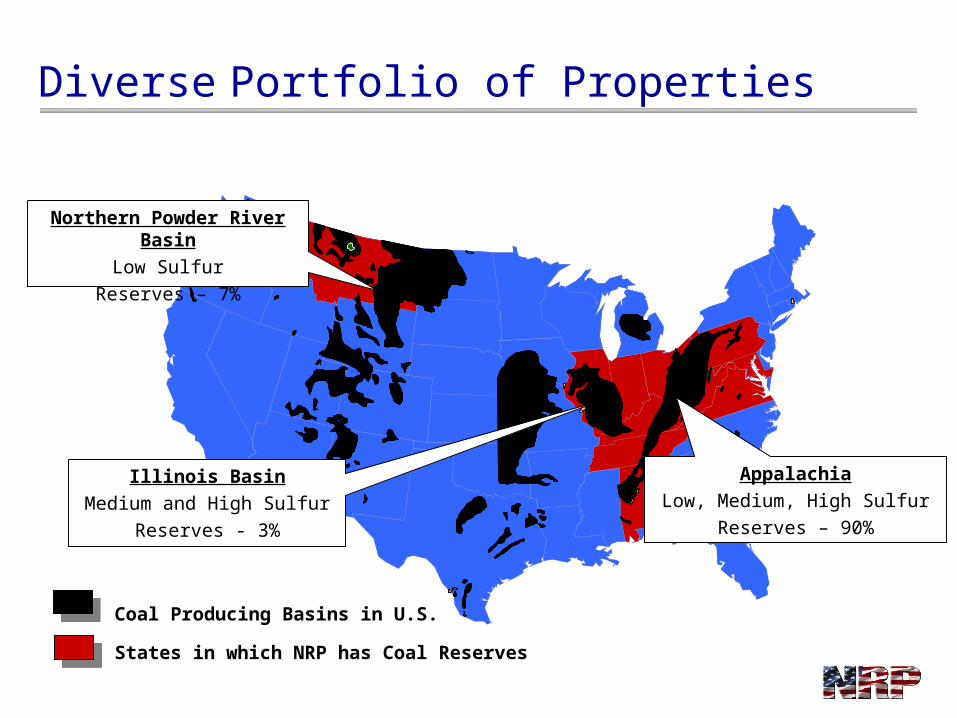

Diverse Portfolio of Properties

Northern Powder River Basin

Low Sulfur

Reserves – 7%

Illinois Basin

Medium and High Sulfur

Reserves - 3%

Appalachia

Low, Medium, High Sulfur

Reserves – 90%

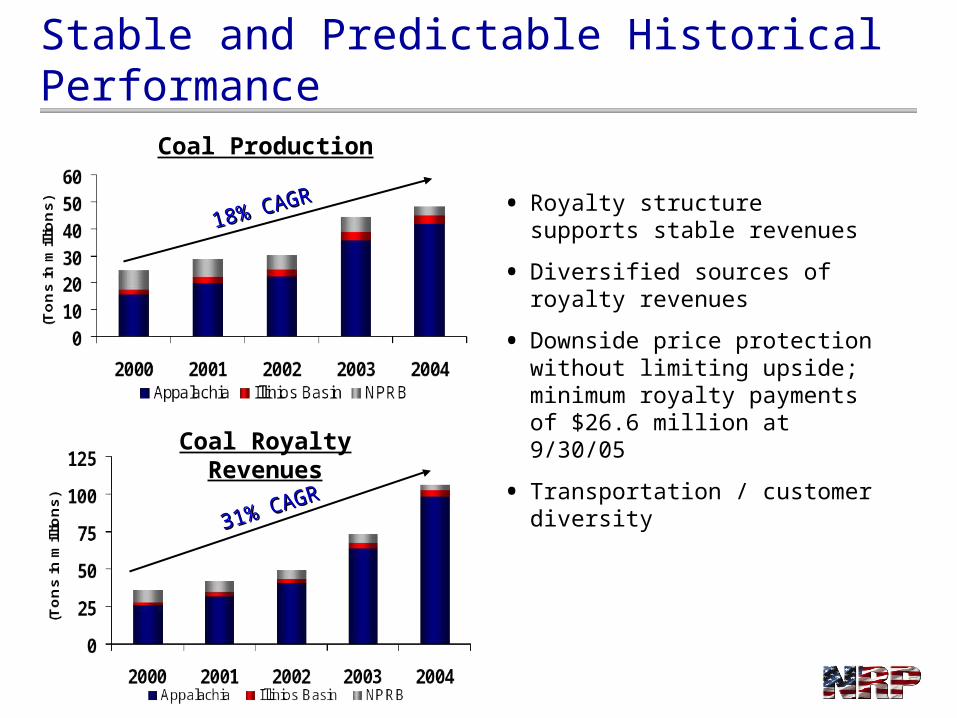

Stable and Predictable Historical PerformanceCoal Production

• Royalty structure supports stable revenues

• Diversified sources of royalty revenues

• Downside price protection without limiting upside; minimum royalty payments of $26.6 million at 9/30/05

• Transportation / customer diversity

Coal Royalty Revenues

18% CAGR18% CAGR

31% CAGR31% CAGR

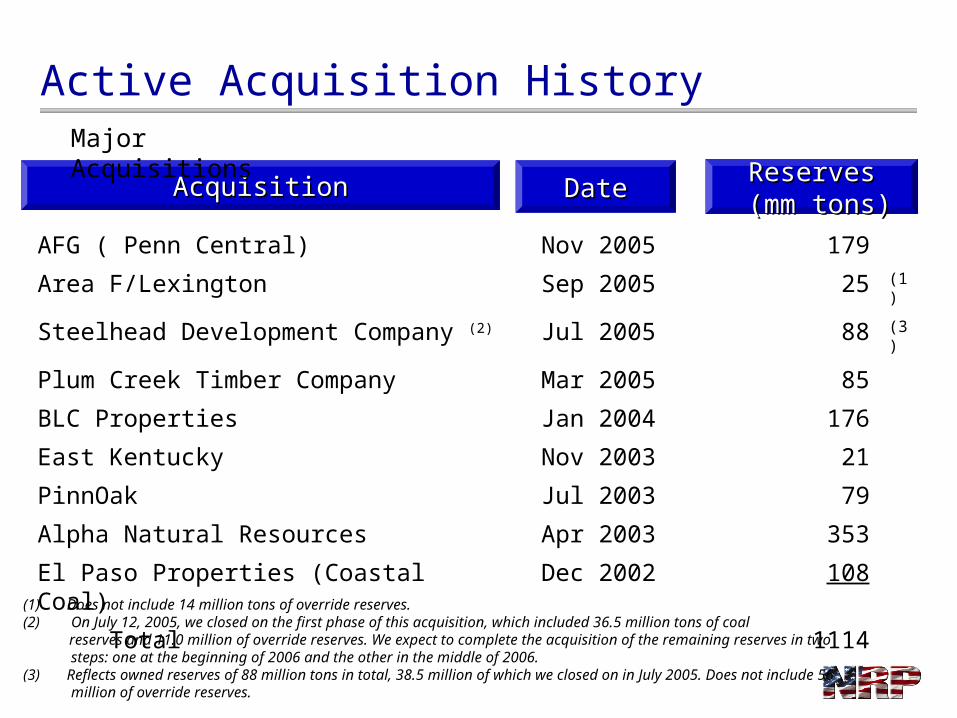

Active Acquisition History

AcquisitionAcquisition DateDate ReservesReserves (mm tons)(mm tons)

(1) Does not include 14 million tons of override reserves.(2) On July 12, 2005, we closed on the first phase of this acquisition, which included 36.5 million tons of coal reserves and 11.0 million of override reserves. We expect to complete the acquisition of the remaining reserves in

two steps: one at the beginning of 2006 and the other in the middle of 2006.(3) Reflects owned reserves of 88 million tons in total, 38.5 million of which we closed on in July 2005. Does not include

56 million of override reserves.

Major Acquisitions

AFG ( Penn Central) Nov 2005 179

Area F/Lexington Sep 2005 25 (1)

Steelhead Development Company (2) Jul 2005 88 (3)

Plum Creek Timber Company Mar 2005 85

BLC Properties Jan 2004 176

East Kentucky Nov 2003 21

PinnOak Jul 2003 79

Alpha Natural Resources Apr 2003 353

El Paso Properties (Coastal Coal) Dec 2002 108

Total 1114

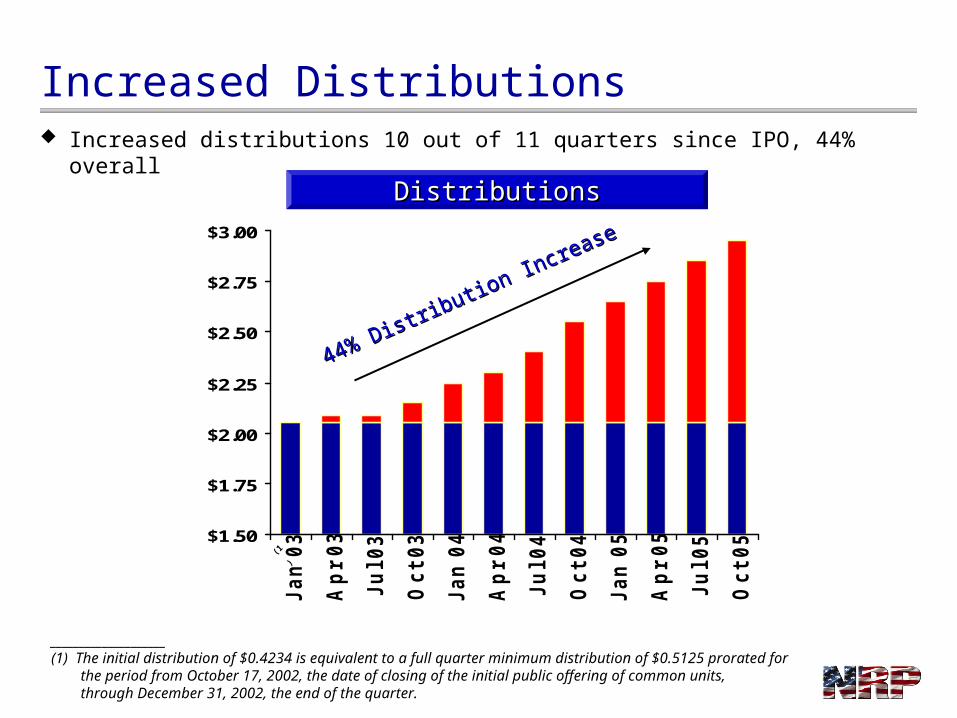

Increased Distributions Increased distributions 10 out of 11 quarters since IPO, 44% overall

DistributionsDistributions

$1.50

$1.75

$2.00

$2.25

$2.50

$2.75

$3.00

Ja

n 0

3

Ap

r 0

3

Ju

l 0

3

Oc

t 0

3

Ja

n 0

4

Ap

r 0

4

Ju

l 0

4

Oc

t 0

4

Ja

n 0

5

Ap

r 0

5

Ju

l 0

5

Oc

t 0

5

44% Distribution Increase

44% Distribution Increase

(1)

____________________(1) The initial distribution of $0.4234 is equivalent to a full quarter minimum distribution of $0.5125 prorated for the

period from October 17, 2002, the date of closing of the initial public offering of common units, through December 31, 2002, the end of the quarter.

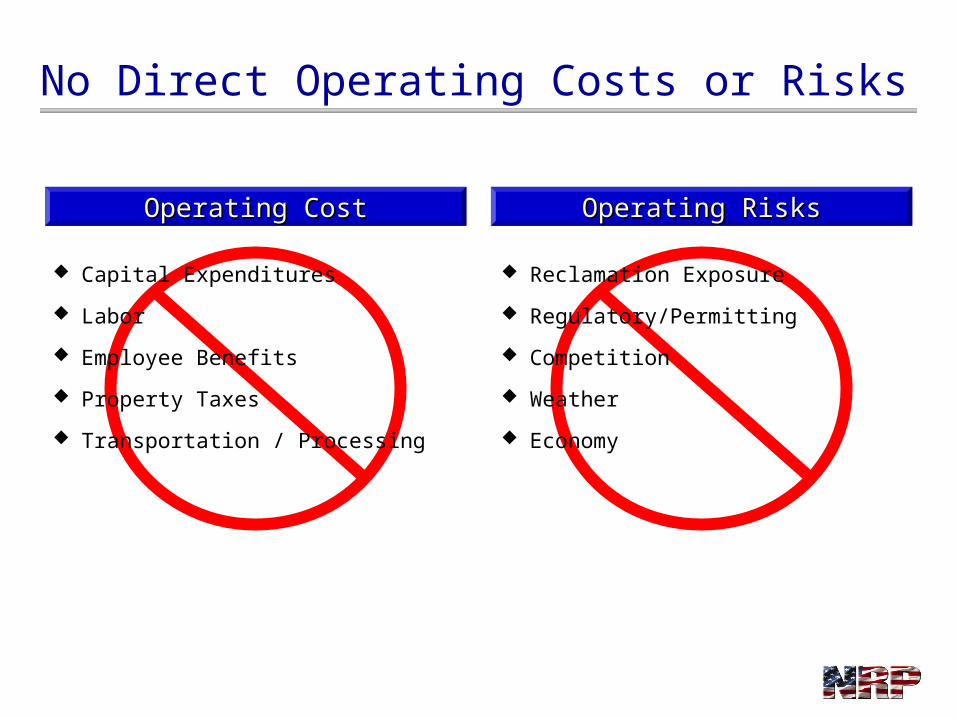

Capital Expenditures

Labor

Employee Benefits

Property Taxes

Transportation / Processing

No Direct Operating Costs or Risks

Operating CostOperating Cost Operating RisksOperating Risks

Reclamation Exposure

Regulatory/Permitting

Competition

Weather

Economy

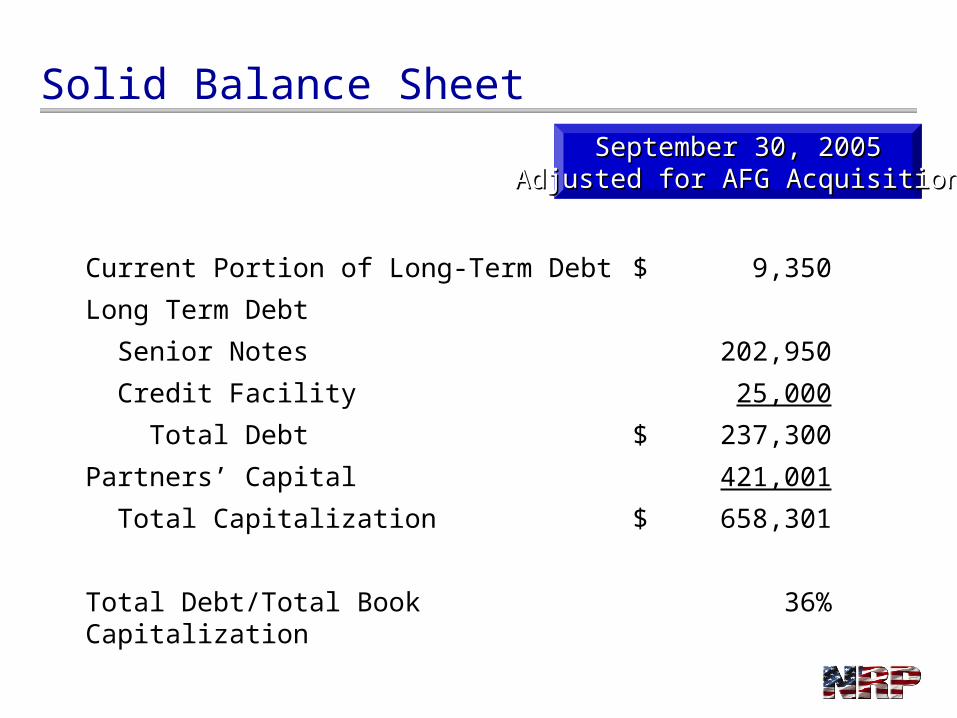

Solid Balance SheetSeptember 30, 2005September 30, 2005

Adjusted for AFG AcquisitionAdjusted for AFG Acquisition

Current Portion of Long-Term Debt $ 9,350

Long Term Debt

Senior Notes 202,950

Credit Facility 25,000

Total Debt $ 237,300

Partners’ Capital 421,001

Total Capitalization $ 658,301

Total Debt/Total Book Capitalization 36%

Attractive Tax Structure

Distributions are treated as return of capital

Unit holders are taxed on the income generated by the partnership

Coal royalty revenues are taxed as long term capital gains

Approximately 60% of the revenue generated is sheltered by depletion deductions

Depletion does not have to be recaptured upon sale of the units

If units are held for more than one year, receive capital gains treatment on the sale

Industry Highlights

Favorable Current Coal Fundamentals

Growing economy and demand for electricity

High natural gas prices

Low stockpile levels at utilities

Coal-fired equipment has become cleaner

Increase in plans to build new coal-fired plants

Increased U.S. export market

Favorable exchange rate with European Union

Increased demand due to explosion of Chinese economy

Domestic DemandDomestic Demand

Global DemandGlobal Demand

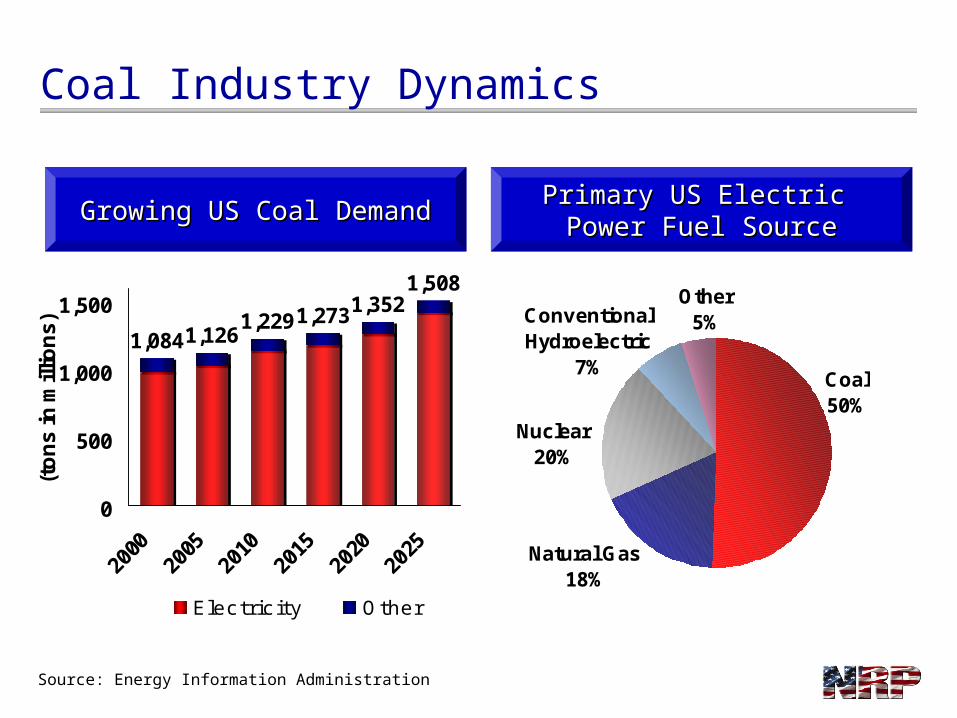

Coal Industry Dynamics

Growing US Coal DemandGrowing US Coal Demand Primary US Electric Primary US Electric Power Fuel SourcePower Fuel Source

Nuclear20%

Natural Gas18%

Coal50%

Other5%Conventional

Hydroelectric7%

Source: Energy Information Administration

1,0841,1261,2291,2731,352

1,508

0

500

1,000

1,500

(to

ns

in m

illio

ns

)

Electric ity Other

NRP – A Proxy for the Coal Industry

Over 2 Billion tons of low, medium and high sulfur coal reserves

67 lessees produce approximately 5% of the US production from our 176 leases

Three major coal producing regions in eleven states Appalachia

– Northern– Central– Southern

Illinois Basin Powder River Basin

Production - Metallurgical Coal – 28% Steam Coal – 72%

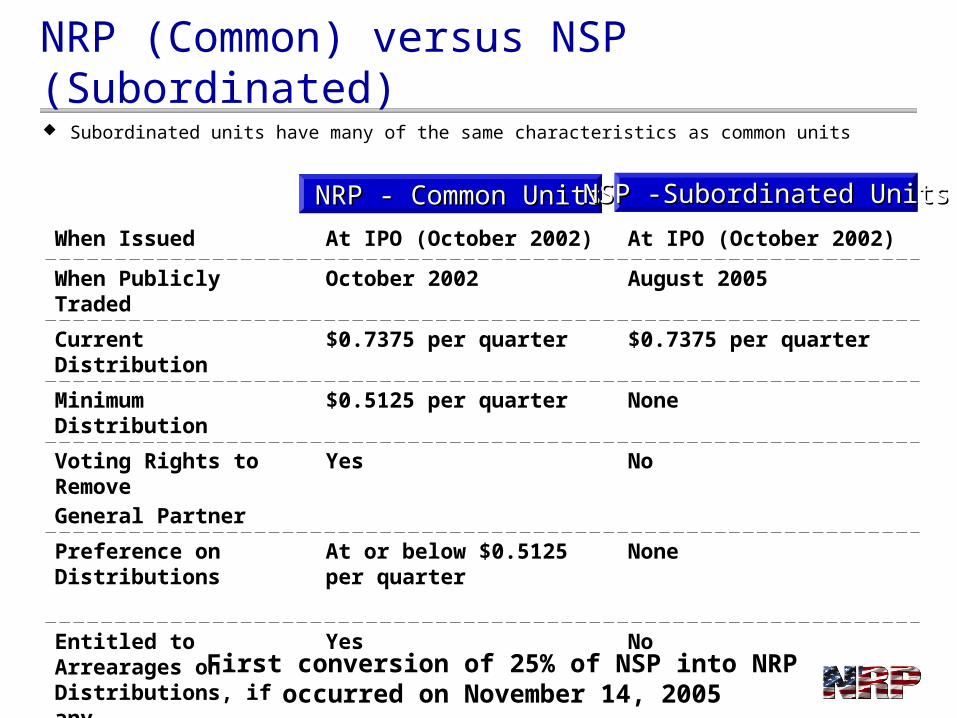

Subordinated units have many of the same characteristics as common units

NRP (Common) versus NSP (Subordinated)

NRP - Common UnitsNRP - Common Units NSP -Subordinated UnitsNSP -Subordinated Units

When Issued At IPO (October 2002) At IPO (October 2002)

When Publicly Traded October 2002 August 2005

Current Distribution $0.7375 per quarter $0.7375 per quarter

Minimum Distribution $0.5125 per quarter None

Voting Rights to RemoveGeneral Partner

Yes No

Preference on Distributions

At or below $0.5125 per quarter

None

Entitled to Arrearages on Distributions, if any

Yes No

First conversion of 25% of NSP into NRP occurred on November 14, 2005

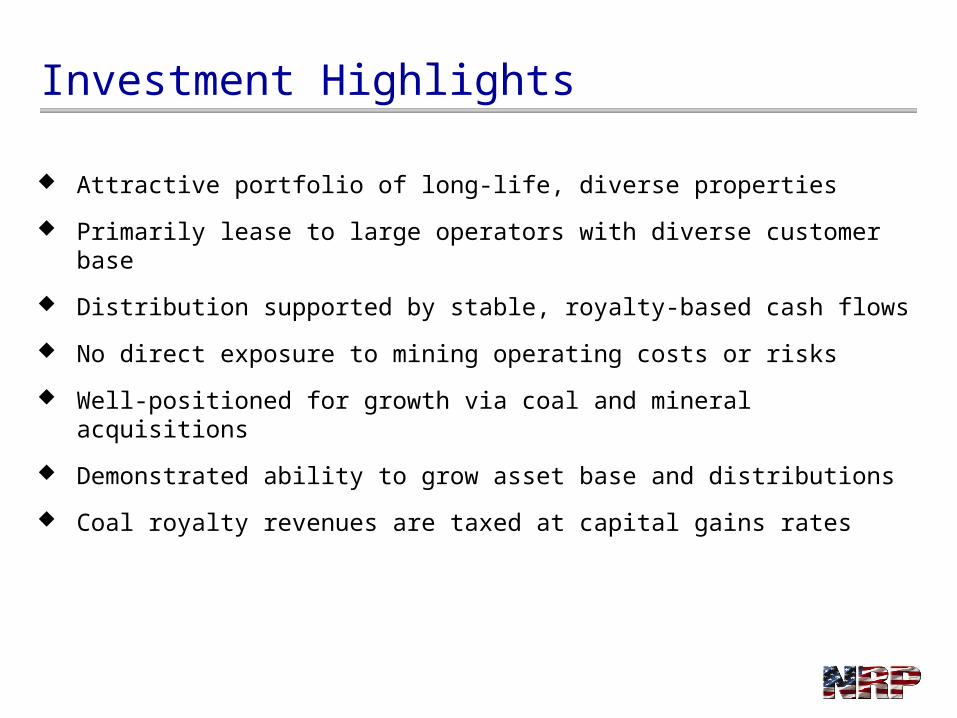

Investment Highlights

Attractive portfolio of long-life, diverse properties

Primarily lease to large operators with diverse customer base

Distribution supported by stable, royalty-based cash flows

No direct exposure to mining operating costs or risks

Well-positioned for growth via coal and mineral acquisitions

Demonstrated ability to grow asset base and distributions

Coal royalty revenues are taxed at capital gains rates

Natural Resource Partners L.P.