Embed Size (px)

Citation preview

Refiners in Europe should benefit from

margin recovery, weaker currencies and lower gas price in 2015…

…and maybe more so from economic growth in selective regions

Initiate coverage of Hellenic Petroleum and PKN Orlen (both at Buy); establish Buy ratings for MOL Group (from OW) and Petro Rabigh (from OW(V)), Hold rating for Tupras (from N under our previous rating system)

Refiners in Europe have managed to make money in a

challenging environment and finally appear to be

benefiting from lower oil and gas prices and a stronger

US dollar: Greenfield refineries in the Middle East remain a

source of threat from H2 2015 but, on the positive side, we

expect 5-6% lower refining runs in Russia this year.

Although we still expect the recent strength in benchmark

margins to reverse soon, we believe the factors that have

helped the sector to weather the headwinds over the past few

years will remain in place.

The sector’s earnings are much more stable than one might

assume when looking at the refining margin charts. Over the

past five to six years it has often been the pace of economic

growth in the domestic markets and fuel consumption trends

that have had more impact on refiners’ earnings in the

region. As HSBC expects 2015 GDP growth in Hungary,

Czech Republic, Poland and Turkey of 2.8%, 2.2%, 3.4%

and 3.0% respectively, we expect stronger fuel demand in

these countries to benefit the refiners.

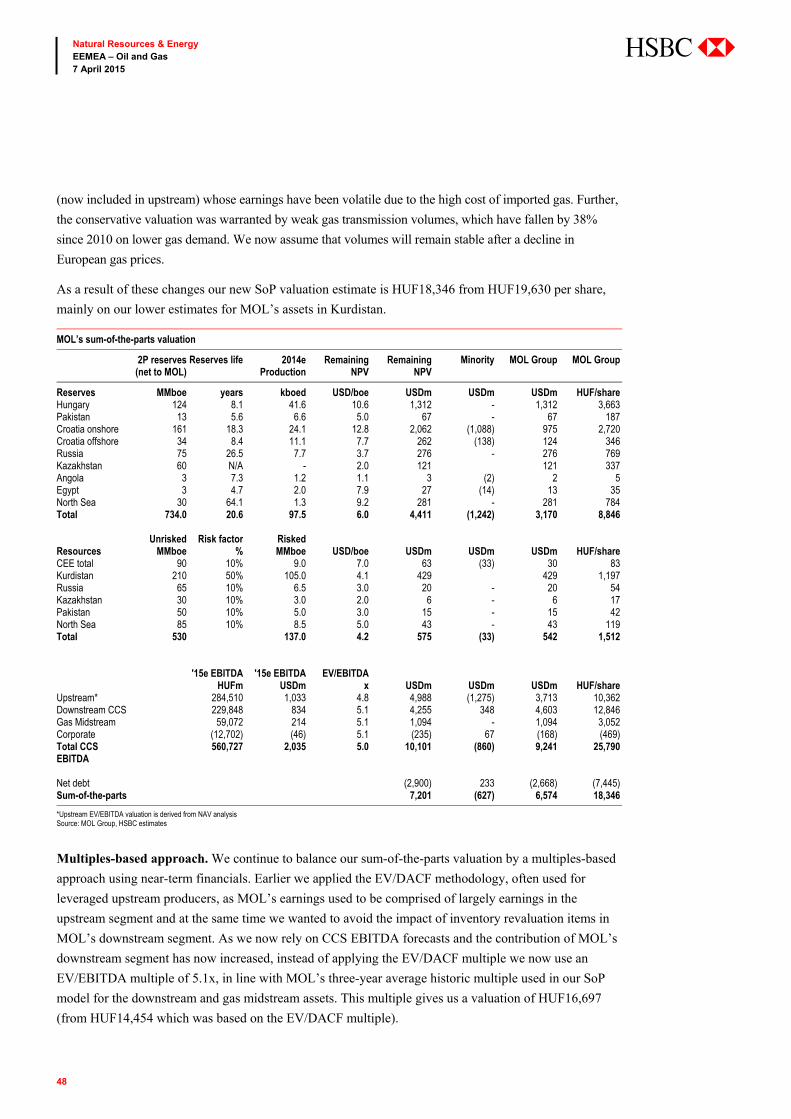

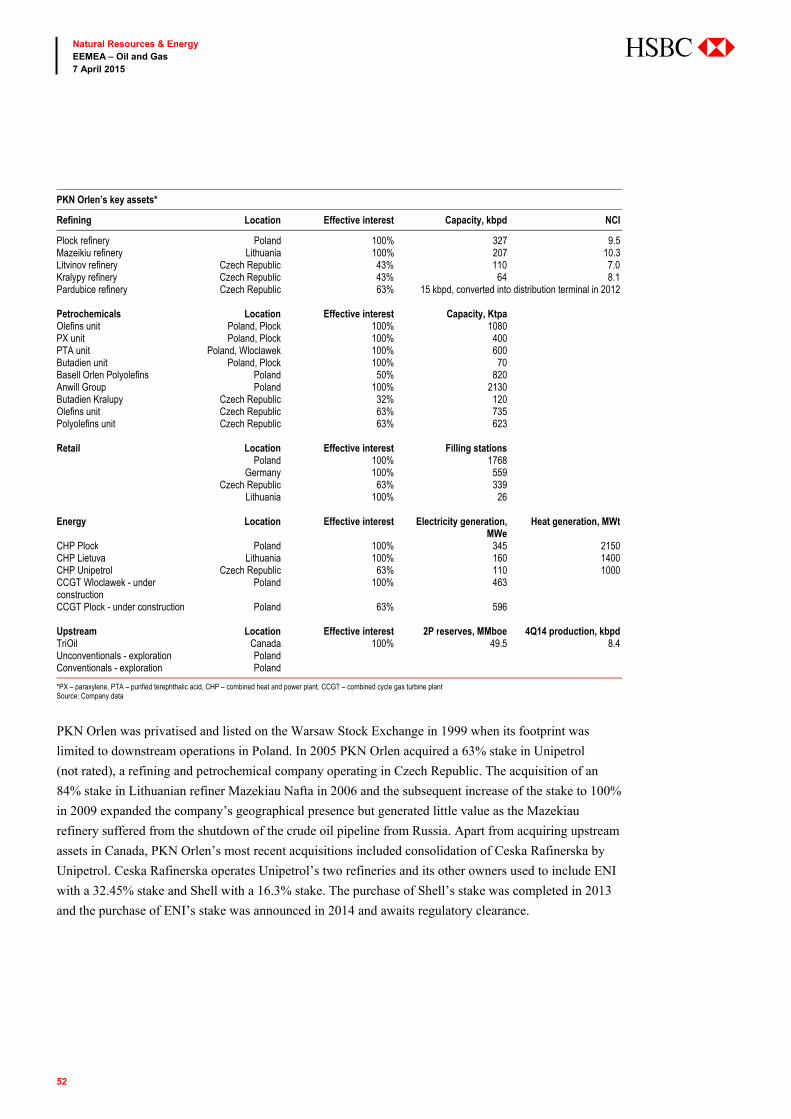

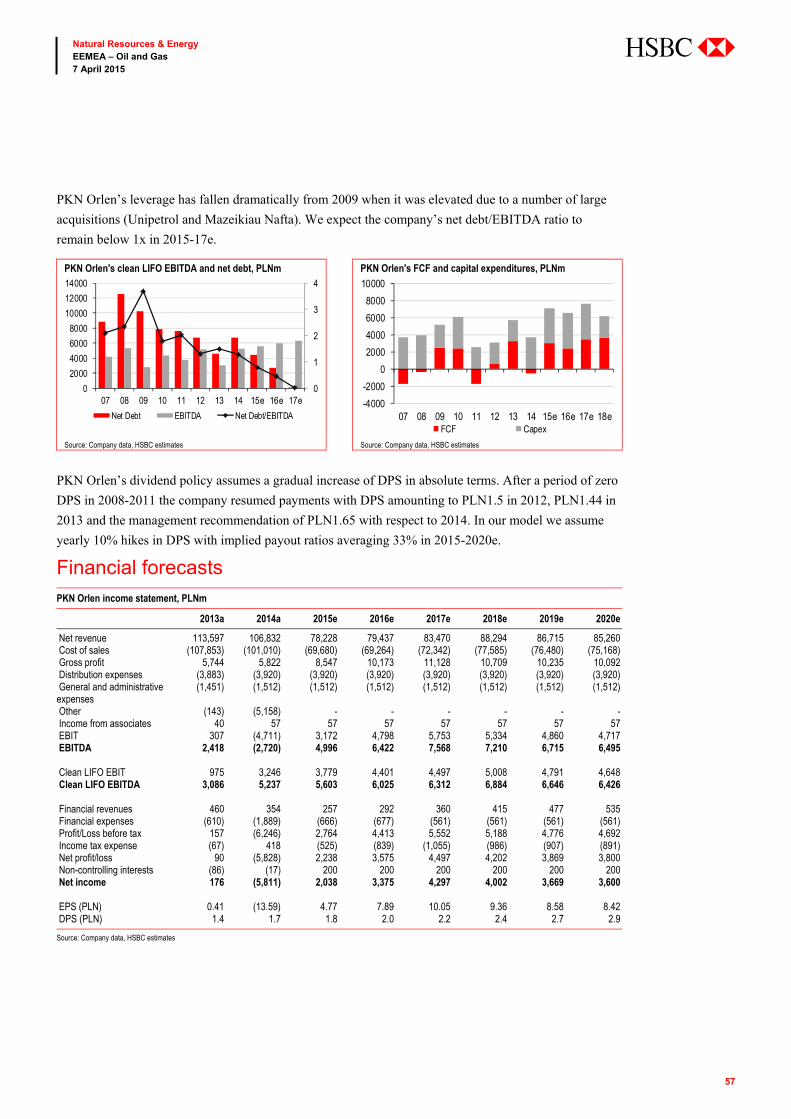

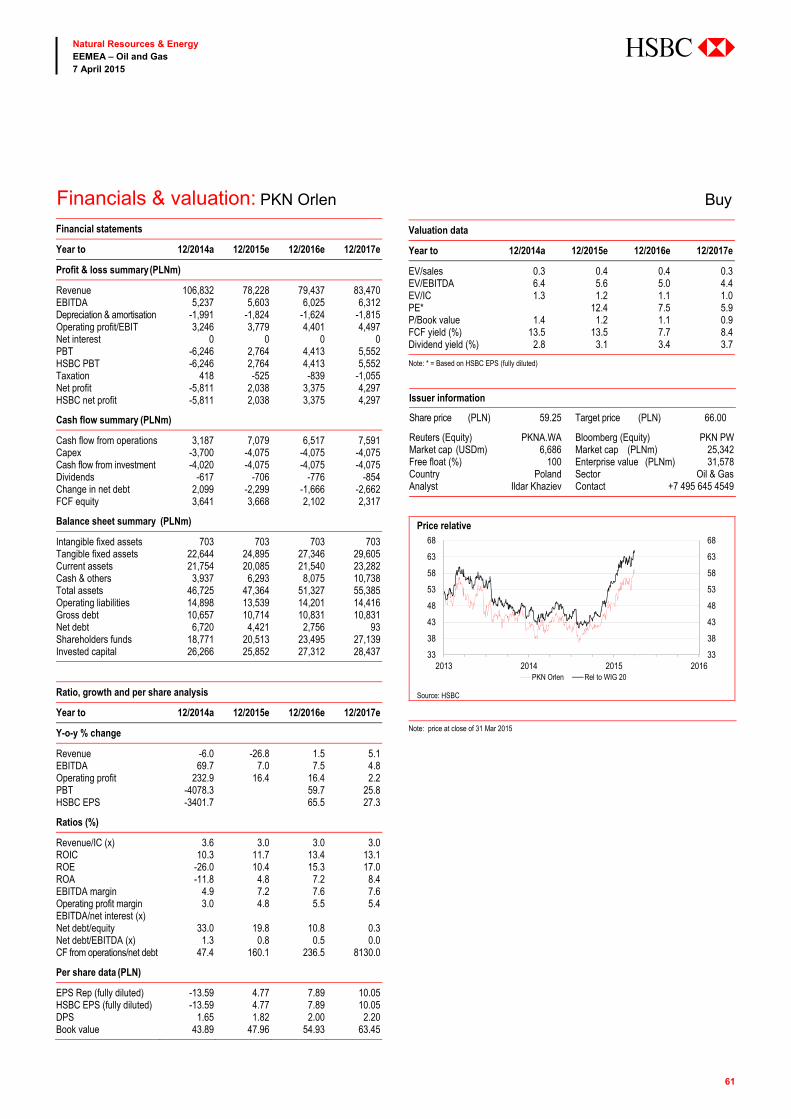

With this report we initiate coverage of PKN Orlen (Buy)

and Hellenic Petroleum (Buy) which together with MOL

Group (Buy) and Tupras (Hold) account for 78% of refining

throughput in the above countries and Greece together. We

like PKN Orlen for its high quality diversified portfolio and

scope for moderate dividend growth, Hellenic Petroleum for

its attractive valuation and we continue to like MOL Group,

whose downstream segment returns are in the spotlight and

the valuation is attractive. In Saudi Arabia we like Petro

Rabigh (Buy), which remains a multi-leg growth story.

Natural Resources & Energy EEMEA – Oil and Gas

EEMEA Refiners

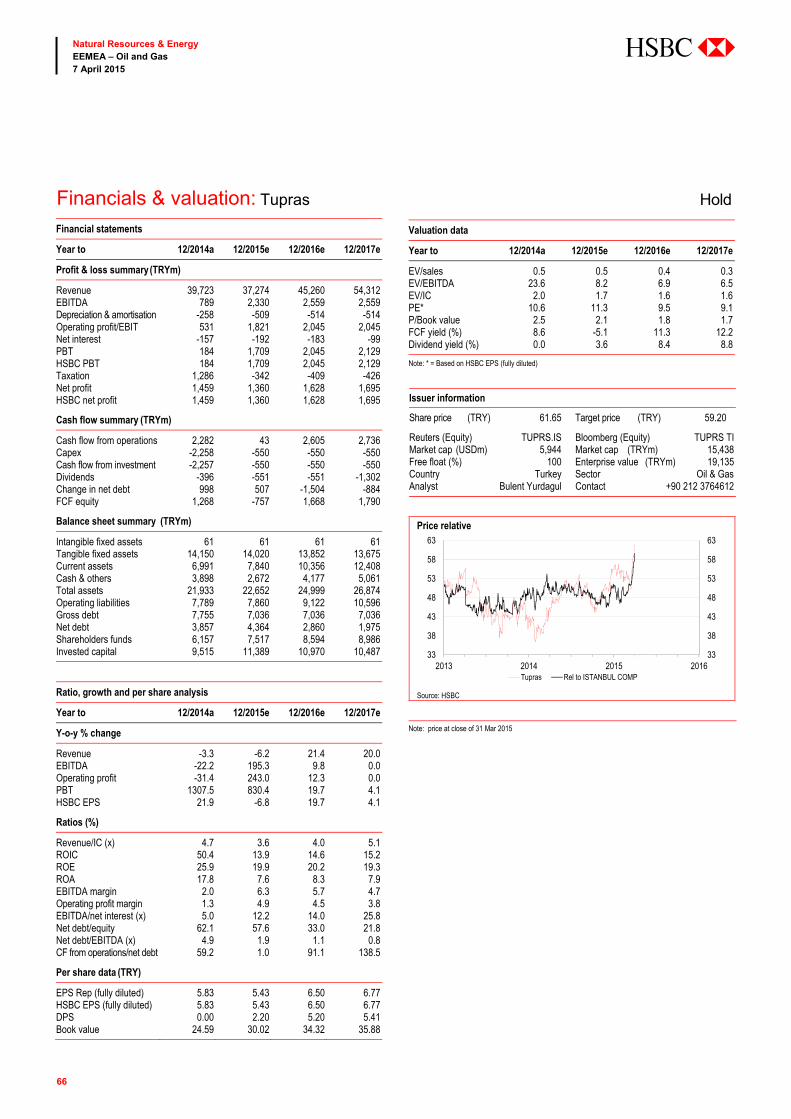

Rating and target price summary

Stock Ticker Curr Price Target price

Rating Upside/downside

Hellenic Petroleum

ELPE GA EUR 3.55 5.6 Initiate at Buy 57.7%

MOL Group MOL HB HUF 12120 17500 Buy (from OW) 44.4%PKN Orlen PKN PW PLN 59.25 66.0 Initiate at Buy 11.4%Tupras TUPRS TI TRY 61.65 59.2 Hold (from N) -4.1%Petro Rabigh PETROR AB SAR 21.36 29.0 Buy (from OW(V)) 35.8%

Prices as of close of 27 March 2015. Source: Bloomberg and HSBC estimates

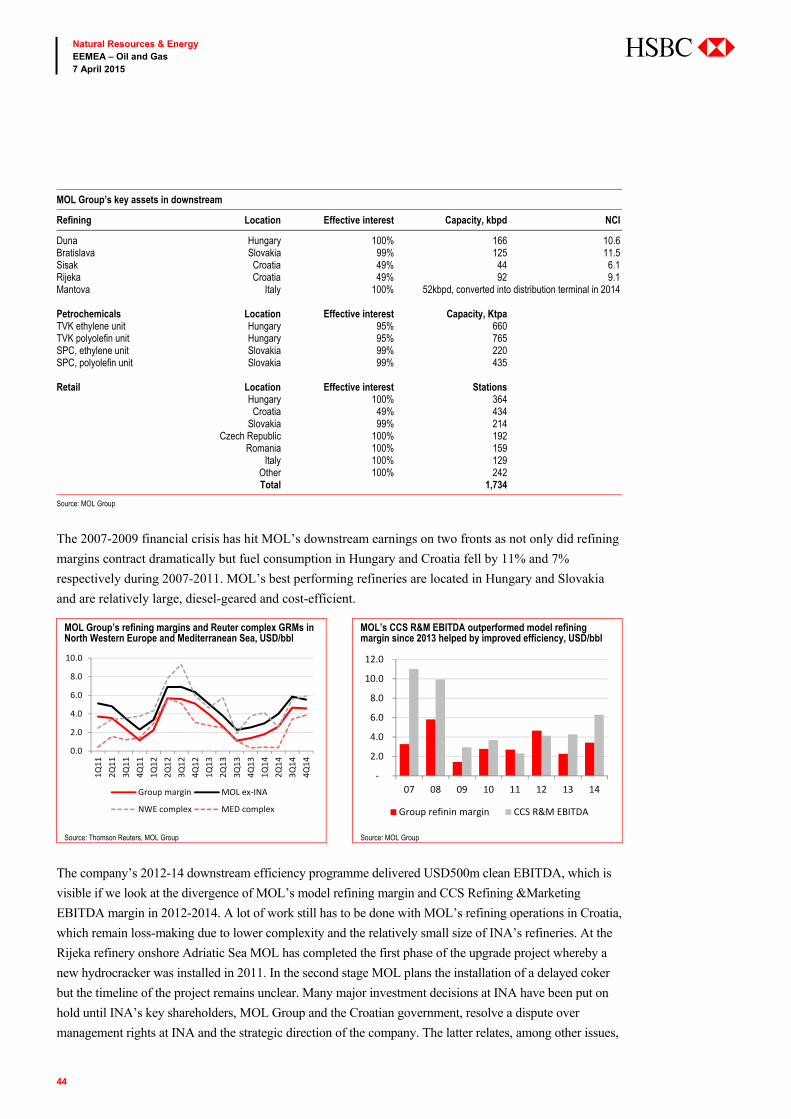

Look beyond refining margins

7 April 2015 Ildar Khaziev*, CFA Analyst OOO HSBC Bank (RR) +7 495 645 4549 [email protected]

Bulent Yurdagul* Analyst HSBC Yatırım Menkul Değerler A.Ş. +90 212 3764612 [email protected]

Sriharsha Pappu* Analyst HSBC Bank Middle East Ltd +971 4223 9624 [email protected]

Govinder Kumar*

Associate, Bangalore

View HSBC Global Research at: http://www.research.hsbc.com

*Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/qualified pursuant to FINRA regulations

Issuer of report: OOO HSBC Bank (RR) (Limited Liability Company)

Disclaimer & Disclosures This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it

Extel Survey 2015 runs from March 23rd through to April 30th. If you value our service and insight please vote for HSBC at

www.extelsurveys.com/quickvote

2

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

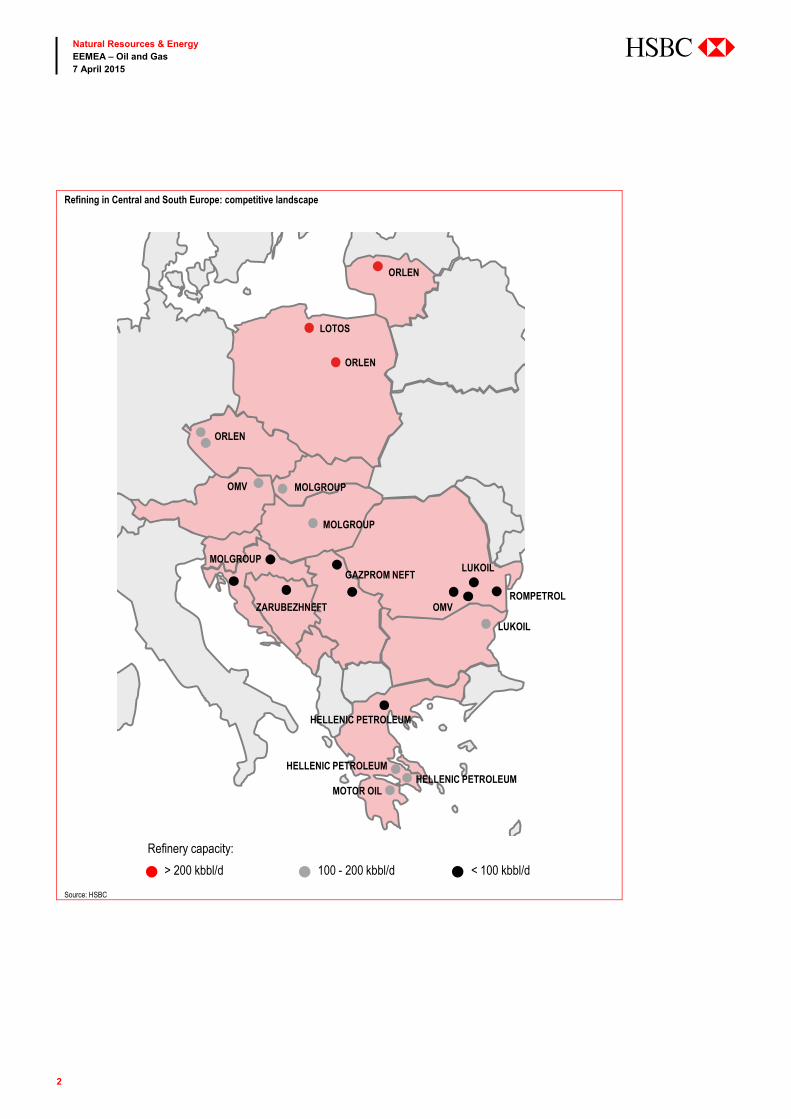

abc

Refining in Central and South Europe: competitive landscape

Source: HSBC

Refinery capacity:

> 200 kbbl/d 100 - 200 kbbl/d < 100 kbbl/d

ORLEN

LOTOS

ORLEN

ORLEN

OMV MOLGROUP

MOLGROUP

MOLGROUP

GAZPROM NEFTLUKOIL

ROMPETROL

LUKOIL

OMVZARUBEZHNEFT

MOTOR OIL

HELLENIC PETROLEUM

HELLENIC PETROLEUMHELLENIC PETROLEUM

3

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

Summary 4

European refining sector challenges 8 European refining margins are the weakest globally 8

Weak demand and diesel/output mismatch is a part

of the story 9

Energy and other cost disadvantages are another factor 11

Finally, some tailwinds in 2015 14 Why lower oil price have improved refining margins 14

Conflicting factors to drive margins further in 2015 16

Weaker currencies to support earnings 19

What if the oil price stays low? Watch Russian refining runs 20

How refiners (some) make money in CEEMEA 24 Benchmark margins ignore regional pricing specifics 24

Fuel marketing 26

Petrochemicals 27

Refining margin assumptions 27

Historical performance: 2007-2014 28

Competitive landscape 31

Hellenic Petroleum 32

MOL Group 42

PKN Orlen 51

Tupras 62

Petro Rabigh 67

Disclosure appendix 71

Disclaimer 75

Contents

4

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

Competitive pressures coming from Russia and the Middle East, a mismatch between demand and

production capacity across products, weak demand for motor fuels and high energy costs in Europe have

been the key threats to European refiners. European refining margins remain the lowest globally.

However, some refiners have managed to make money in the challenging environment and finally appear

to be benefiting from lower oil and gas prices and a stronger US dollar. Although we expect the recent

strength in benchmark margins to reverse soon, we believe the factors that have helped them to weather

the headwinds over the past few years will remain in place.

On a global scale, we expect refining utilisation rates to remain flat to positive at least until 2017, based

on our demand-supply forecasts. In a regional context, the sector has faced potential threats from

greenfield refineries in the Middle East and growing refining runs in Russia. The former will materialise

from Q2 2015 after the ramp-up of two new refineries in Saudi Arabia and UAE but we note that they

will compete not only in Europe but also in Asia where margins are more attractive. The Russian refining

sector may not be a source of risk in 2015 at all. This is because the recent tax reform and weaker oil

prices have sent the Russian average refining margins to nearly zero since February 2015 and we see

scope for a 5-6% cut in the Russian refining runs this year – this would imply less competition for the

European refiners.

We expect European benchmark refining margins to remain volatile in 2015-2016 but in reality the

refining sector’s earnings are much more stable than one may think when looking at the refining margin

charts. We observe that the benchmark margins oscillate around the refining costs and where the refiners

are really making money is the delivery of fuels to their customers with regional price mark-ups protected

by logistical advantages from importers. Over the past five to six years it has often been the pace of

economic growth in the domestic markets and fuel consumption trends that have had more impact on the

refiners’ earnings in the region. As HSBC expects 2015 GDP growth in Hungary, Czech Republic,

Poland and Turkey of 2.8%, 2.2%, 3.4% and 3.0% respectively, we expect stronger fuel demand in these

countries to benefit the refiners. With this report we initiate coverage of PKN Orlen and Hellenic

Summary

Refiners should benefit from margin recovery, weaker currencies

and lower gas price in 2015…

…and maybe more so from economic growth in selective regions

Initiate coverage of Hellenic Petroleum and PKN Orlen (both at

Buy), establish Buy ratings for MOL Group (from OW) and Petro

Rabigh (from OW(V)) and Hold for Tupras (from Neutral)

5

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

Petroleum, which together with MOL Group and Tupras account for 78% of refining throughput in the

above countries and Greece together. HSBC introduced a new stock rating system on 23 March 2015.

For details, please see our published research or our Global Research website.

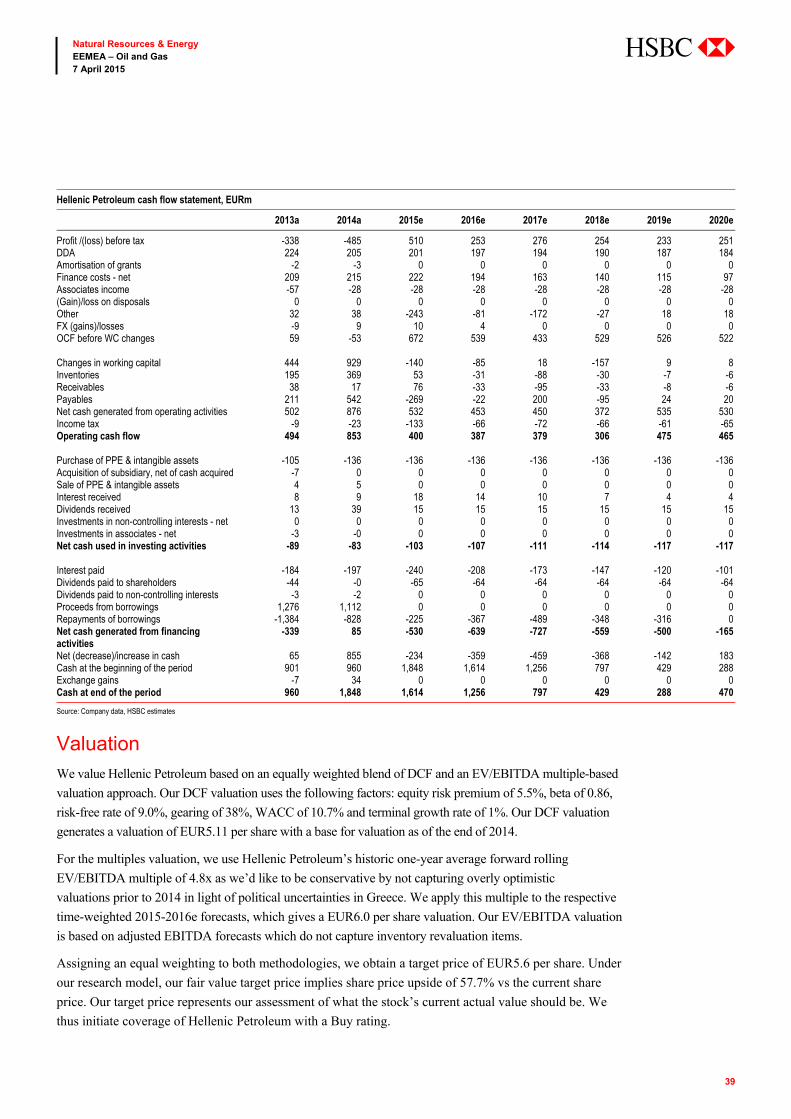

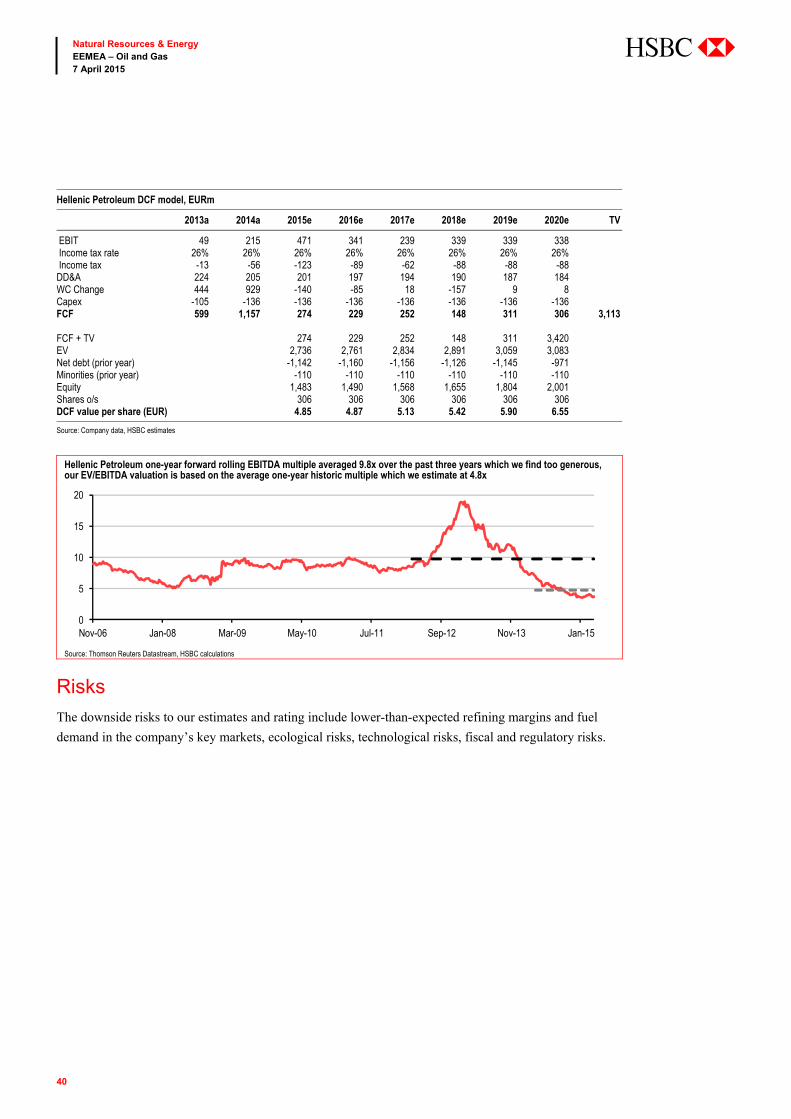

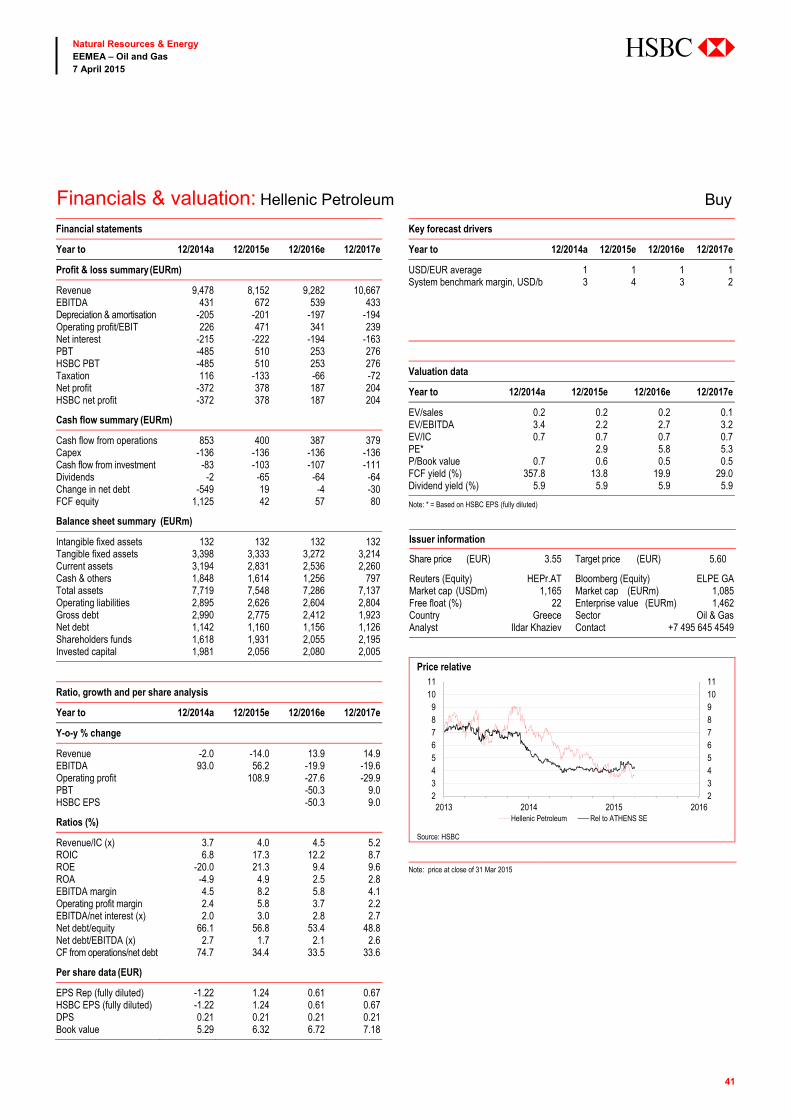

Hellenic Petroleum

Initiate with a Buy rating and set a fair value target price of EUR5.6

After completion of the Elefsina upgrade project the company has entered the delivery phase, which

should be supported by a recovery in refining margins and weaker EUR. Although there are medium-term

risk coming from the additional supply of diesel to the region from 2017, Hellenic Petroleum’s margins

should be supported by its close proximity to the strongly growing fuel market of Turkey in 2015-16e.

The company’s EUR1.85bn cash position and EUR250-350m yearly FCF generation during the period

leaves the company with enough resources to service its debt schedule in 2015-2018. The resumption of

dividend payments (5.9% dividend yield with respect to the 2014 results) underscores the improved

financial position of the company and makes the stock an attractive value play despite the political

uncertainties in Greece.

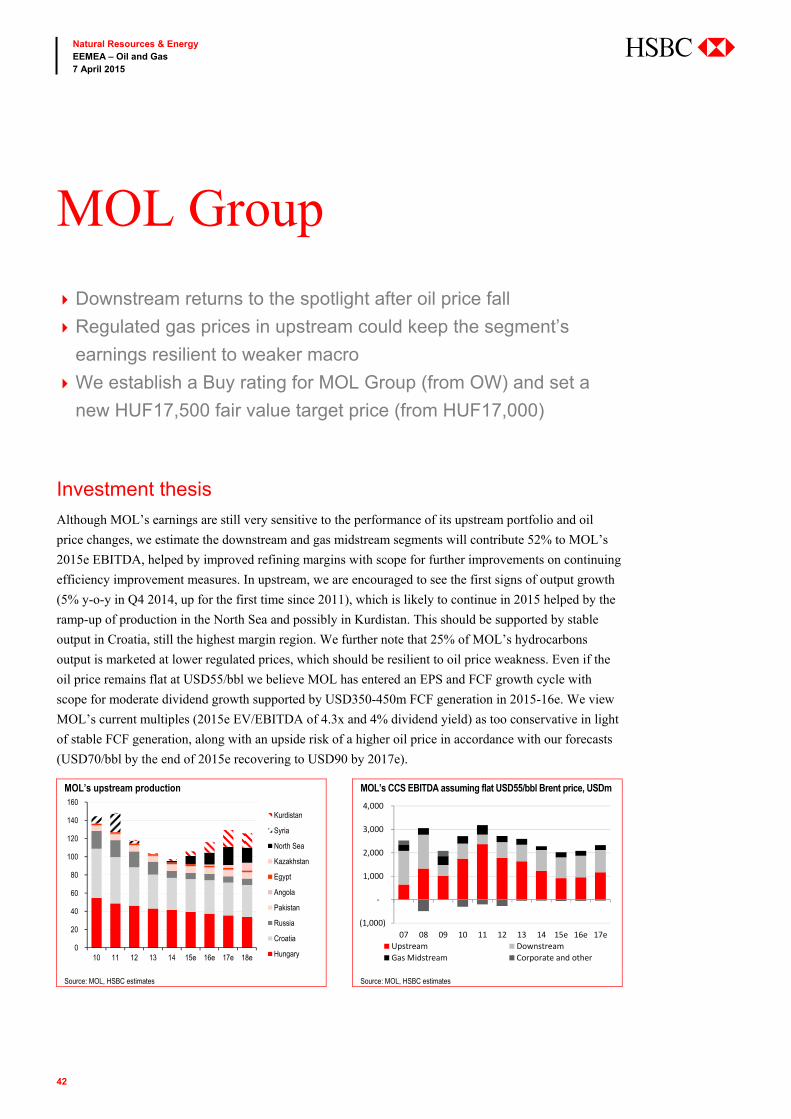

MOL Group

Establish a Buy rating (from Overweight) and set a fair value target price of HUF17,500

(vs HUF17,000)

Although MOL’s earnings are still very sensitive to the performance of its upstream portfolio and oil

price changes, we estimate the downstream and gas midstream segments will contribute 52% to MOL’s

2015e EBITDA, helped by improved refining margins with scope for further improvements on continuing

efficiency improvement measures. In upstream, we are encouraged to see the first signs of output growth

(+5% y-o-y in Q4 2014, for the first time since 2011), which is likely to continue in 2015 helped by the

ramp-up of production in the North Sea and possibly in Kurdistan. This should be supported by stable

output in Croatia, still the highest margin region. We further note that 25% of MOL’s hydrocarbons

output is marketed at lower regulated prices, which should be resilient to oil price weakness. Even if the

oil price remains flat at USD55/bbl, we believe MOL has entered an EPS and FCF growth cycle with

scope for moderate dividend growth supported by USD350-450m FCF generation in 2015-16e. We view

MOL’s current multiples (2015e EV/EBITDA of 4.3x and 4% dividend yield) as too conservative in light

of stable FCF generation along with an upside risk of a higher oil price in accordance with our forecasts

(USD70/bbl by end of 2015e, recovering to USD90 by 2017e).

PKN Orlen

Initiate with a Buy rating and set a fair value target price of PLN66

PKN Orlen’s key attractions include a diversified portfolio of downstream assets and exposure to regions

with strong economic growth. The company’s two key segments, refining and petrochemicals,

complement each other nicely as their returns are negatively correlated. In 2015 we expect the

petrochemical segment to post a 43% decline on a weaker EUR but most of the decline will be offset by

higher EBITDA in the refining segment. We see scope for moderate dividend growth as the company is

approaching the end of its deleveraging cycle. As PKN Orlen operates largely in Poland and Czech

Republic we view it as relatively well protected from the potential inflow of imported diesel from the

new greenfield refineries in the Middle East, which is likely to affect mostly the Mediterranean region

6

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

from H2 2015. Although the stock doesn’t look cheap currently, it still trades at a 9% discount to its

mid-cycle average EV/EBITDA multiple.

Tupras

Establish a Hold rating (from Neutral) and set a fair value target price of TRY59.2 (from TRY61)

Tupras has completed the construction of the residuum upgrade project (RUP), the biggest investment

project in the company’s history. The USD3bn project is expected to start operating towards the end of

March or the beginning of April, according to management guidance. We expect RUP to contribute

USD500m annually towards Tupras’ EBITDA (vs company guidance of USD550m), even on a low crude

price and consequently narrower diesel-HSFO spread. Our estimates indicate Tupras’ EBITDA will rise

by 195% y-o-y in 2015e to TRY2,330m. Next year will be the first full year of RUP’s operation and we

forecast 2016e EBITDA to rise further by 10% y-o-y to TRY2,559m. Our estimates are largely in line

with the IBES consensus EBITDA forecasts of TRY2,369m and TRY2,587m for 2015-16e. The

consensus is therefore also assuming a similar amount of RUP-related benefits. We think that the rally in

Tupras’ share price since H2 2014 is also in part driven by the completion and subsequent start-up of

RUP and its benefits are reflected in the company’s share price as well as in consensus estimates. Tupras’

stock, therefore, has only limited further upside, in our view, and hence we establish a Hold rating on the

stock.

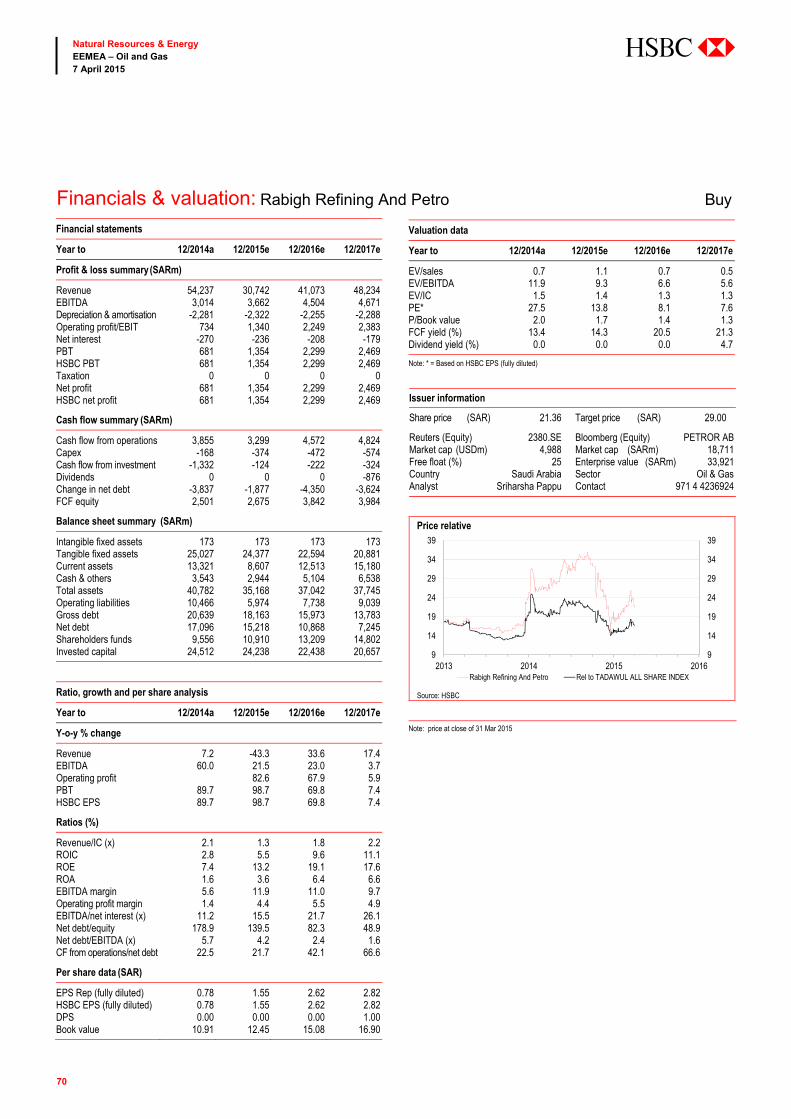

Petro Rabigh

Establish Buy rating (from Overweight (V)) and set a fair value target price of SAR29 (vs SAR31)

Petro Rabigh remains a multi-leg equity story set to play out in several phases over the 2015-16

timeframe. In the last 18 months, the company has addressed issues related to its loss-making refinery,

taken a big step towards improving operations at its chemical unit and provided greater clarity around

growth opportunities related to Rabigh 2. None of these factors – improvement in chemical operations or

growth from Rabigh 2 – is correlated to the oil price. We expect to see continued positive news flow

around Rabigh 2 and better operating performance from Rabigh 1 over the next 12-18 months, driving the

next leg of equity upside from current levels. We establish a Buy rating (Overweight (V) earlier) and set a

target price of SAR29 (SAR31 earlier).

7

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

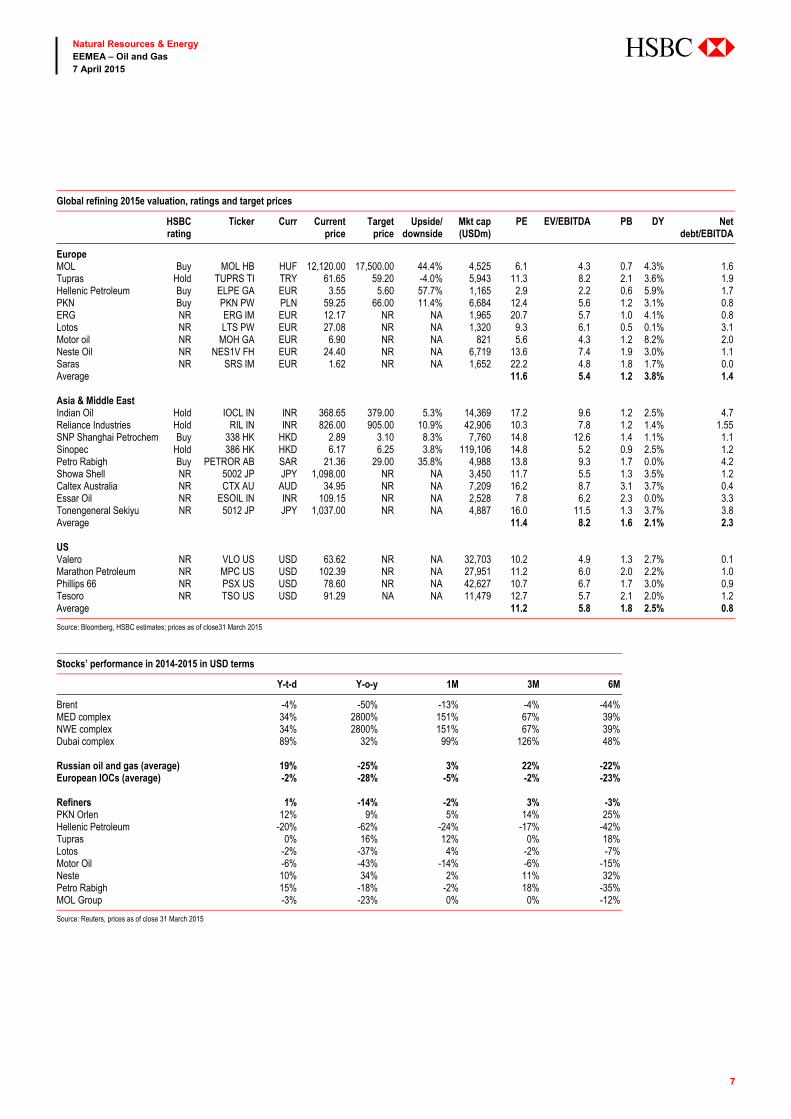

Global refining 2015e valuation, ratings and target prices

HSBC rating

Ticker Curr Current price

Target price

Upside/downside

Mkt cap (USDm)

PE EV/EBITDA PB DY Net debt/EBITDA

Europe MOL Buy MOL HB HUF 12,120.00 17,500.00 44.4% 4,525 6.1 4.3 0.7 4.3% 1.6Tupras Hold TUPRS TI TRY 61.65 59.20 -4.0% 5,943 11.3 8.2 2.1 3.6% 1.9Hellenic Petroleum Buy ELPE GA EUR 3.55 5.60 57.7% 1,165 2.9 2.2 0.6 5.9% 1.7PKN Buy PKN PW PLN 59.25 66.00 11.4% 6,684 12.4 5.6 1.2 3.1% 0.8ERG NR ERG IM EUR 12.17 NR NA 1,965 20.7 5.7 1.0 4.1% 0.8Lotos NR LTS PW EUR 27.08 NR NA 1,320 9.3 6.1 0.5 0.1% 3.1Motor oil NR MOH GA EUR 6.90 NR NA 821 5.6 4.3 1.2 8.2% 2.0Neste Oil NR NES1V FH EUR 24.40 NR NA 6,719 13.6 7.4 1.9 3.0% 1.1Saras NR SRS IM EUR 1.62 NR NA 1,652 22.2 4.8 1.8 1.7% 0.0Average 11.6 5.4 1.2 3.8% 1.4 Asia & Middle East Indian Oil Hold IOCL IN INR 368.65 379.00 5.3% 14,369 17.2 9.6 1.2 2.5% 4.7Reliance Industries Hold RIL IN INR 826.00 905.00 10.9% 42,906 10.3 7.8 1.2 1.4% 1.55SNP Shanghai Petrochem Buy 338 HK HKD 2.89 3.10 8.3% 7,760 14.8 12.6 1.4 1.1% 1.1Sinopec Hold 386 HK HKD 6.17 6.25 3.8% 119,106 14.8 5.2 0.9 2.5% 1.2Petro Rabigh Buy PETROR AB SAR 21.36 29.00 35.8% 4,988 13.8 9.3 1.7 0.0% 4.2Showa Shell NR 5002 JP JPY 1,098.00 NR NA 3,450 11.7 5.5 1.3 3.5% 1.2Caltex Australia NR CTX AU AUD 34.95 NR NA 7,209 16.2 8.7 3.1 3.7% 0.4Essar Oil NR ESOIL IN INR 109.15 NR NA 2,528 7.8 6.2 2.3 0.0% 3.3Tonengeneral Sekiyu NR 5012 JP JPY 1,037.00 NR NA 4,887 16.0 11.5 1.3 3.7% 3.8Average 11.4 8.2 1.6 2.1% 2.3 US Valero NR VLO US USD 63.62 NR NA 32,703 10.2 4.9 1.3 2.7% 0.1Marathon Petroleum NR MPC US USD 102.39 NR NA 27,951 11.2 6.0 2.0 2.2% 1.0Phillips 66 NR PSX US USD 78.60 NR NA 42,627 10.7 6.7 1.7 3.0% 0.9Tesoro NR TSO US USD 91.29 NA NA 11,479 12.7 5.7 2.1 2.0% 1.2Average 11.2 5.8 1.8 2.5% 0.8

Source: Bloomberg, HSBC estimates; prices as of close31 March 2015

Stocks’ performance in 2014-2015 in USD terms

Y-t-d Y-o-y 1M 3M 6M

Brent -4% -50% -13% -4% -44% MED complex 34% 2800% 151% 67% 39% NWE complex 34% 2800% 151% 67% 39% Dubai complex 89% 32% 99% 126% 48% Russian oil and gas (average) 19% -25% 3% 22% -22% European IOCs (average) -2% -28% -5% -2% -23% Refiners 1% -14% -2% 3% -3% PKN Orlen 12% 9% 5% 14% 25% Hellenic Petroleum -20% -62% -24% -17% -42% Tupras 0% 16% 12% 0% 18% Lotos -2% -37% 4% -2% -7% Motor Oil -6% -43% -14% -6% -15% Neste 10% 34% 2% 11% 32% Petro Rabigh 15% -18% -2% 18% -35% MOL Group -3% -23% 0% 0% -12%

Source: Reuters, prices as of close 31 March 2015

8

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

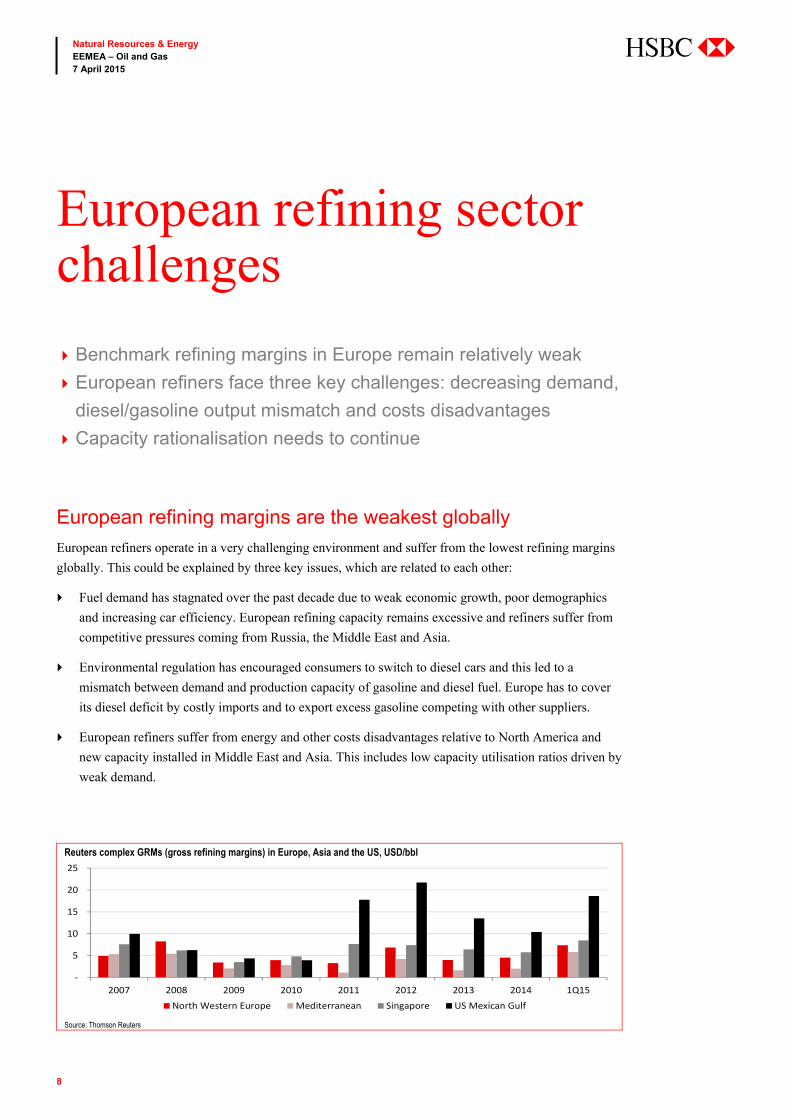

European refining margins are the weakest globally

European refiners operate in a very challenging environment and suffer from the lowest refining margins

globally. This could be explained by three key issues, which are related to each other:

Fuel demand has stagnated over the past decade due to weak economic growth, poor demographics

and increasing car efficiency. European refining capacity remains excessive and refiners suffer from

competitive pressures coming from Russia, the Middle East and Asia.

Environmental regulation has encouraged consumers to switch to diesel cars and this led to a

mismatch between demand and production capacity of gasoline and diesel fuel. Europe has to cover

its diesel deficit by costly imports and to export excess gasoline competing with other suppliers.

European refiners suffer from energy and other costs disadvantages relative to North America and

new capacity installed in Middle East and Asia. This includes low capacity utilisation ratios driven by

weak demand.

European refining sector challenges

Benchmark refining margins in Europe remain relatively weak

European refiners face three key challenges: decreasing demand,

diesel/gasoline output mismatch and costs disadvantages

Capacity rationalisation needs to continue

Reuters complex GRMs (gross refining margins) in Europe, Asia and the US, USD/bbl

Source: Thomson Reuters

-

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014 1Q15North Western Europe Mediterranean Singapore US Mexican Gulf

9

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

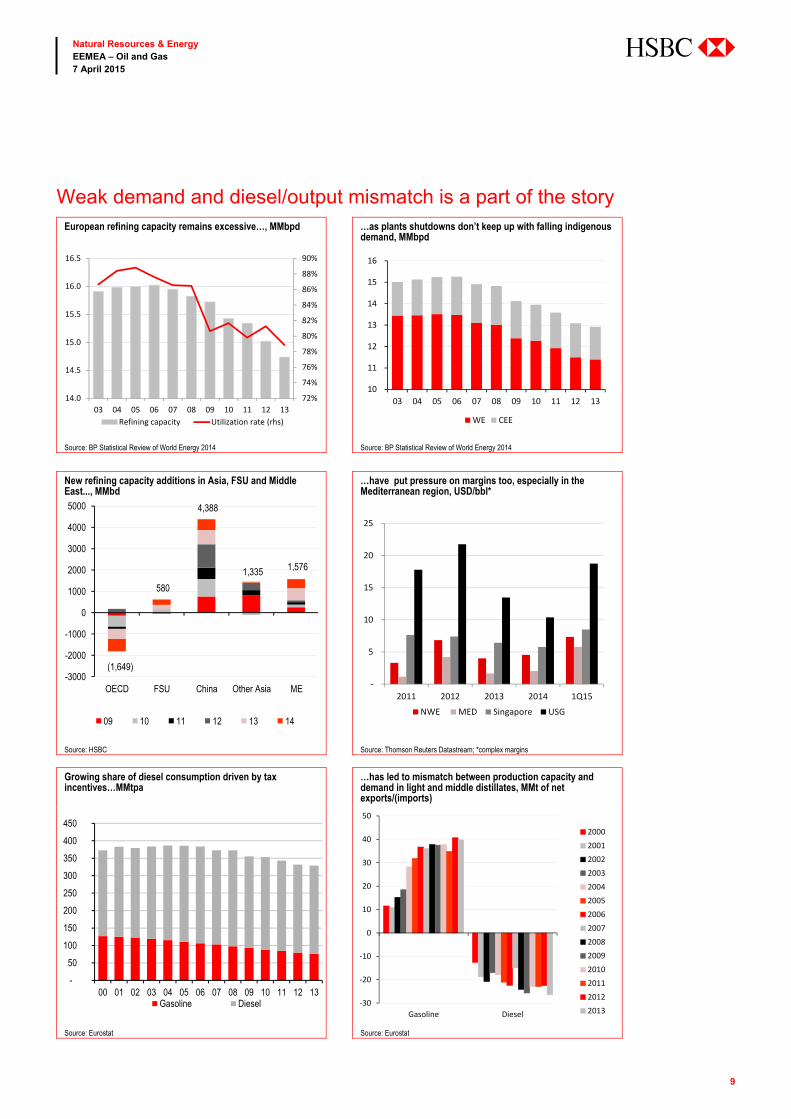

Weak demand and diesel/output mismatch is a part of the story European refining capacity remains excessive…, MMbpd …as plants shutdowns don’t keep up with falling indigenous

demand, MMbpd

Source: BP Statistical Review of World Energy 2014 Source: BP Statistical Review of World Energy 2014

New refining capacity additions in Asia, FSU and Middle East..., MMbd

…have put pressure on margins too, especially in the Mediterranean region, USD/bbl*

Source: HSBC Source: Thomson Reuters Datastream; *complex margins

Growing share of diesel consumption driven by tax incentives…MMtpa

…has led to mismatch between production capacity and demand in light and middle distillates, MMt of net exports/(imports)

Source: Eurostat Source: Eurostat

72%

74%

76%

78%

80%

82%

84%

86%

88%

90%

14.0

14.5

15.0

15.5

16.0

16.5

03 04 05 06 07 08 09 10 11 12 13Refining capacity Utilization rate (rhs)

10

11

12

13

14

15

16

03 04 05 06 07 08 09 10 11 12 13

WE CEE

(1,649)

580

4,388

1,335 1,576

-3000

-2000

-1000

0

1000

2000

3000

4000

5000

OECD FSU China Other Asia ME

09 10 11 12 13 14

-

5

10

15

20

25

2011 2012 2013 2014 1Q15

NWE MED Singapore USG

-

50

100

150

200

250

300

350

400

450

00 01 02 03 04 05 06 07 08 09 10 11 12 13Gasoline Diesel -30

-20

-10

0

10

20

30

40

50

Gasoline Diesel

20002001200220032004200520062007200820092010201120122013

10

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

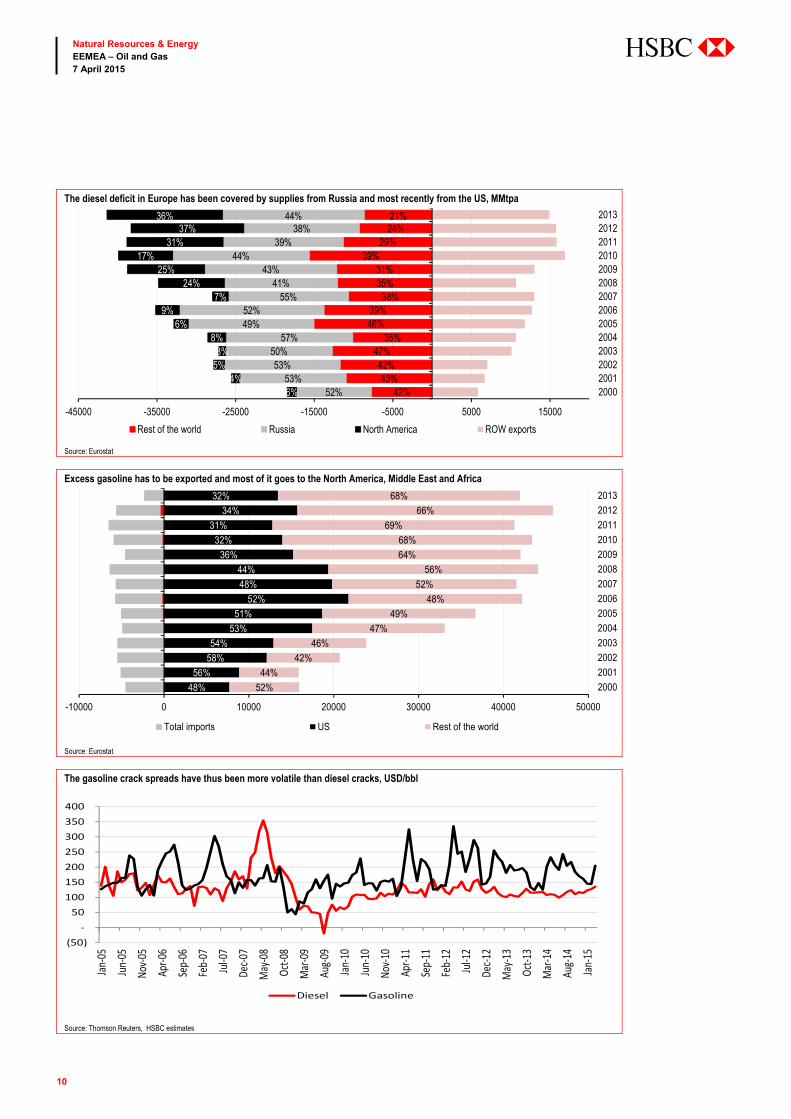

The diesel deficit in Europe has been covered by supplies from Russia and most recently from the US, MMtpa

Source: Eurostat

Excess gasoline has to be exported and most of it goes to the North America, Middle East and Africa

Source: Eurostat

The gasoline crack spreads have thus been more volatile than diesel cracks, USD/bbl

Source: Thomson Reuters, HSBC estimates

42%43%

42%47%

35%46%39%

38%35%31%

39%29%

24%21%

52%53%

53%50%

57%49%52%

55%41%

43%44%

39%38%

44%

6%4%

5%3%

8%6%

9%7%

24%25%

17%31%

37%36%

-45000 -35000 -25000 -15000 -5000 5000 15000

20002001200220032004200520062007200820092010201120122013

Rest of the world Russia North America ROW exports

48%

56%

58%

54%

53%

51%

52%

48%

44%

36%

32%

31%

34%

32%

52%

44%

42%

46%

47%

49%

48%

52%

56%

64%

68%

69%

66%

68%

-10000 0 10000 20000 30000 40000 50000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Total imports US Rest of the world

(50) -

50100150200250300350400

Jan-0

5Ju

n-05

Nov-0

5Ap

r-06

Sep-

06Fe

b-07

Jul-0

7De

c-07

May

-08Oc

t-08

Mar

-09Au

g-09

Jan-1

0Ju

n-10

Nov-1

0Ap

r-11

Sep-

11Fe

b-12

Jul-1

2De

c-12

May

-13Oc

t-13

Mar

-14Au

g-14

Jan-1

5

Diesel Gasoline

11

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

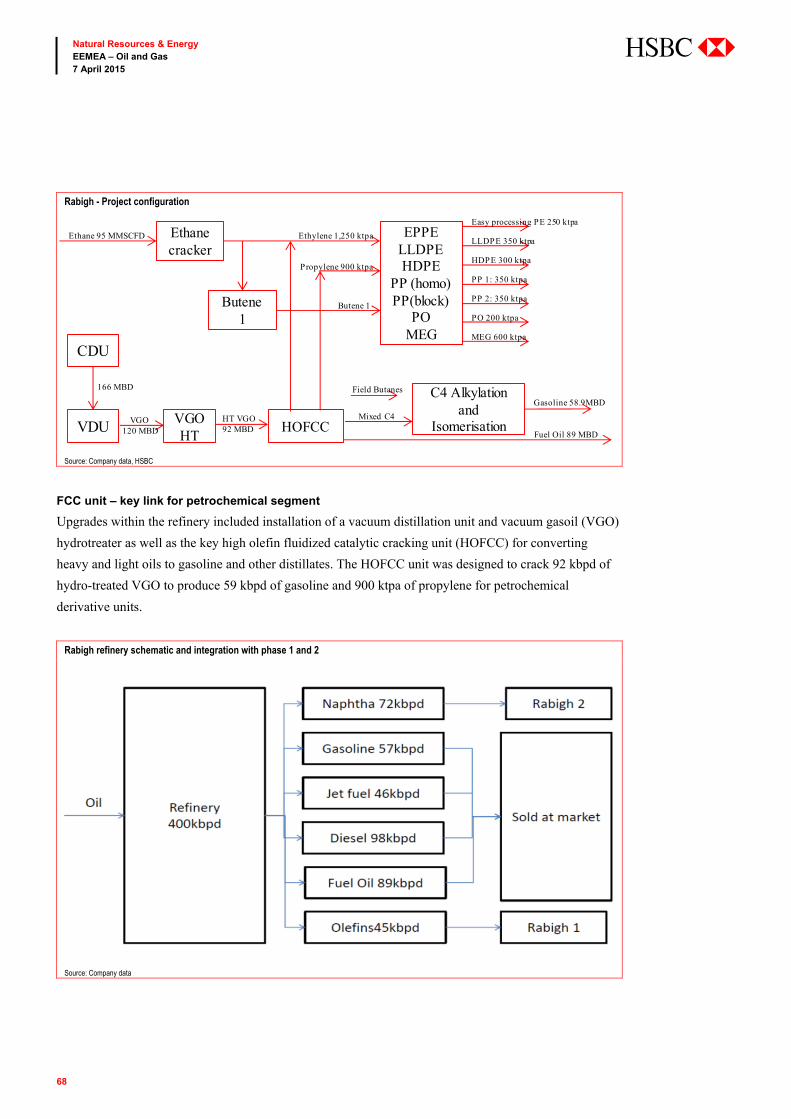

Energy and other cost disadvantages are another factor

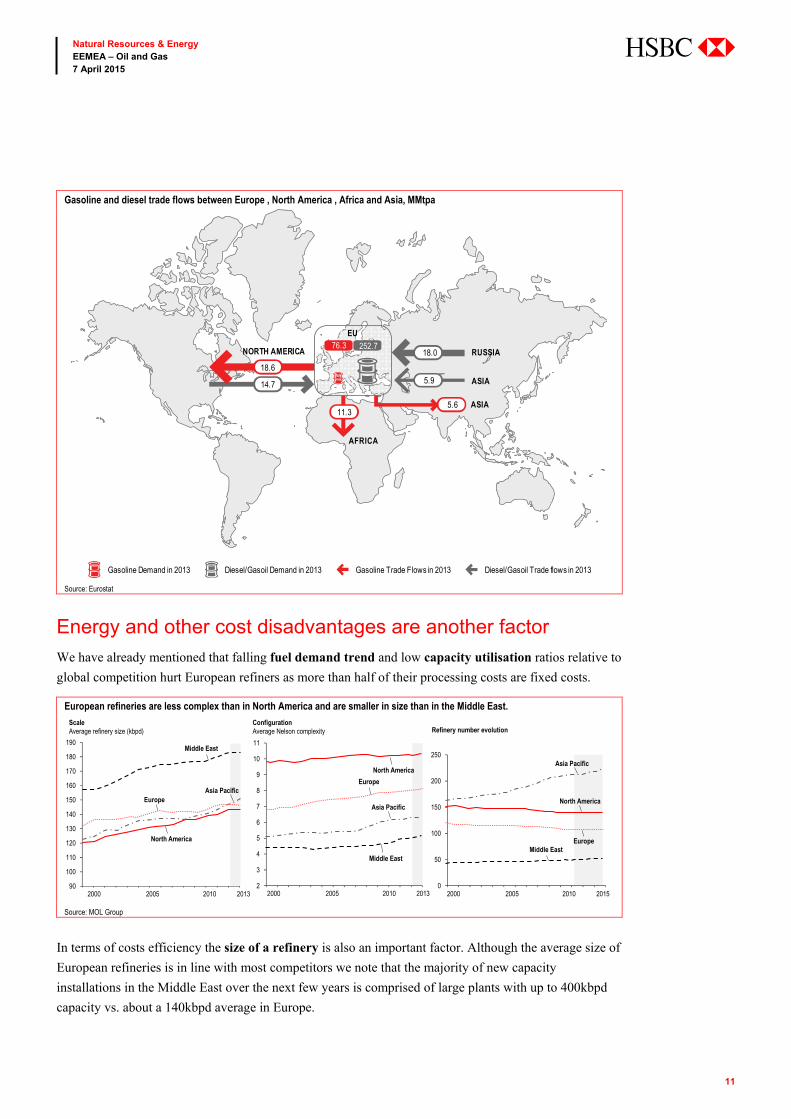

We have already mentioned that falling fuel demand trend and low capacity utilisation ratios relative to

global competition hurt European refiners as more than half of their processing costs are fixed costs.

European refineries are less complex than in North America and are smaller in size than in the Middle East.

Source: MOL Group

In terms of costs efficiency the size of a refinery is also an important factor. Although the average size of

European refineries is in line with most competitors we note that the majority of new capacity

installations in the Middle East over the next few years is comprised of large plants with up to 400kbpd

capacity vs. about a 140kbpd average in Europe.

90

100

110

120

130

140

150

160

170

180

190

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20132000 2005 2010 2013

Middle East

EuropeAsia Pacific

North America

2

3

4

5

6

7

8

9

10

11

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

North America

Europe

Asia Pacific

Middle East

2000 2005 2010 20130

50

100

150

200

250

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20132000 2005 2010 2015

Asia Pacific

North America

EuropeMiddle East

ScaleAverage refinery size (kbpd)

Configuration Average Nelson complexity Refinery number evolution

Gasoline and diesel trade flows between Europe , North America , Africa and Asia, MMtpa

Source: Eurostat

EU

RUSSIA

ASIA

ASIA

AFRICA

NORTH AMERICA76.3 252.7

18.6

14.7

18.0

5.9

5.611.3

Gasoline Trade Flows in 2013 Diesel/Gasoil Trade flows in 2013Gasoline Demand in 2013 Diesel/Gasoil Demand in 2013

12

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

Generally, there are two principal ways to improve the competitiveness of a refinery: investing in higher

complexity and higher energy efficiency. The former enhances the yield of higher value-added products

and could improve capacity utilisation while the latter cuts operating costs.

In simple terms a higher complexity generally indicates higher light and middle distillates yields

(naphtha, gasoline, jet and diesel fuels) and lower heavy distillates yield (fuel and heating oils, bitumen).

More complex refineries generally have higher variable operating costs but generate higher refining

margins. Such refineries can also enjoy the benefit of being able to refine heavier and sourer crude oils,

fuel and heating oils, thus extracting a premium as such feedstock normally trades at a discount.

EU demand is best matched by complex diesel-geared refineries

Source: Fuels Europe, Eurostat

Energy efficiency is another important driver which affects the profitability of refineries as cost of

energy accounts for about half of a refinery’s operating costs. When processing crude oil and other

feedstock a refinery burns a part of its output to heat feedstock flows at its processing units, generate

steam and sometimes electric power. Depending on its configuration, a refinery burns 3% to 10% of its

gross product output, normally heating and fuel oil. More efficient heaters and combustion units thus

consume less fuel and improve the profitability of refineries. For Central and Eastern European refineries,

however, a more important factor in terms of energy efficiency is often the physical size of the refinery,

or rather the distances between the plant units. Most of these refineries were designed and built using the

former USSR construction standards, which dictated larger distances between units as a means of

improving the security of operations in case of fires or explosions. It is not uncommon for a refinery or

any other plant which was built in the USSR under such standards to cover an area of 100 square

kilometres. Although improving the security of operations, such standards led to lower energy efficiency

as longer distance refinery flows generate large amounts of heat losses (distillation and cracking units

operate at temperatures of up to 400 C). There are things which can be done and things which can’t be

done about this but most refiners continue to focus on energy efficiency of their operations. For instance,

MOL’s 2012-2014 downstream efficiency programme delivered cUSD400m savings, 30% of which came

from energy efficiency improvement.

0%

2%

4%

6%

8%

10%

0%

20%

40%

60%

80%

100%

2013 Demand Simple refinery High gasoline High diesel

HFO/Other products Diesel Kero/Jet GasolineNaphtha LPG Losses

13

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

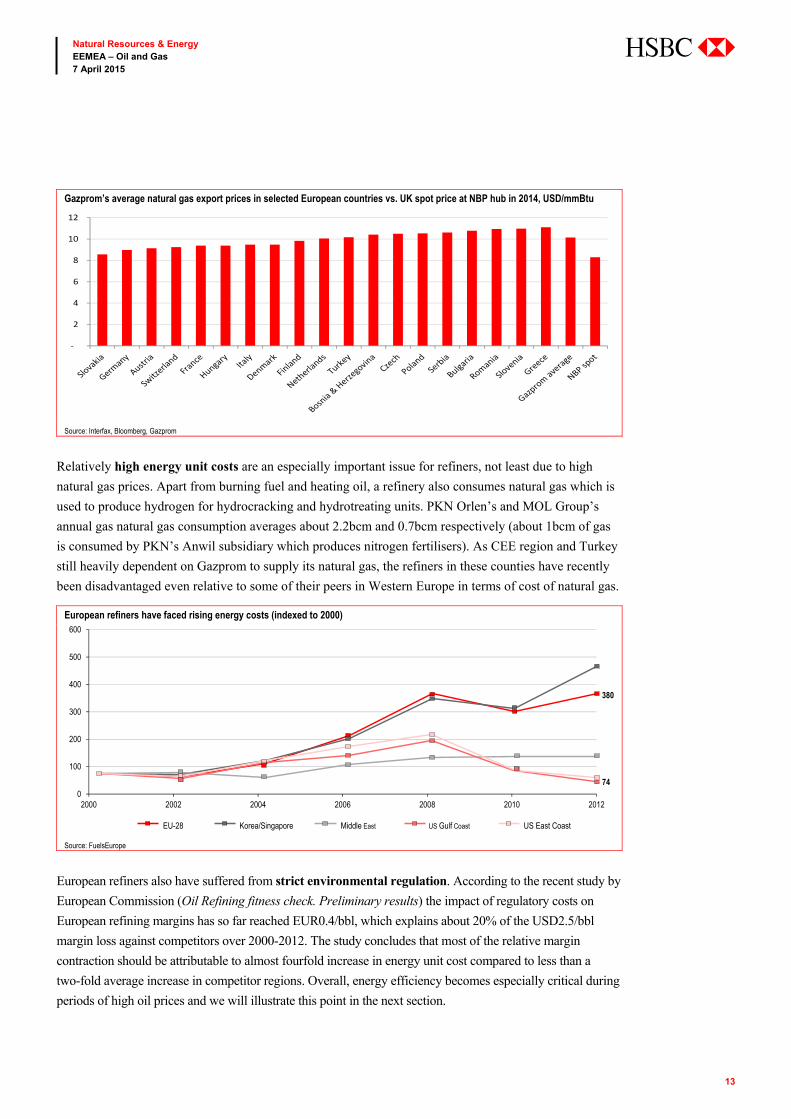

Gazprom’s average natural gas export prices in selected European countries vs. UK spot price at NBP hub in 2014, USD/mmBtu

Source: Interfax, Bloomberg, Gazprom

Relatively high energy unit costs are an especially important issue for refiners, not least due to high

natural gas prices. Apart from burning fuel and heating oil, a refinery also consumes natural gas which is

used to produce hydrogen for hydrocracking and hydrotreating units. PKN Orlen’s and MOL Group’s

annual gas natural gas consumption averages about 2.2bcm and 0.7bcm respectively (about 1bcm of gas

is consumed by PKN’s Anwil subsidiary which produces nitrogen fertilisers). As CEE region and Turkey

still heavily dependent on Gazprom to supply its natural gas, the refiners in these counties have recently

been disadvantaged even relative to some of their peers in Western Europe in terms of cost of natural gas.

European refiners have faced rising energy costs (indexed to 2000)

Source: FuelsEurope

European refiners also have suffered from strict environmental regulation. According to the recent study by

European Commission (Oil Refining fitness check. Preliminary results) the impact of regulatory costs on

European refining margins has so far reached EUR0.4/bbl, which explains about 20% of the USD2.5/bbl

margin loss against competitors over 2000-2012. The study concludes that most of the relative margin

contraction should be attributable to almost fourfold increase in energy unit cost compared to less than a

two-fold average increase in competitor regions. Overall, energy efficiency becomes especially critical during

periods of high oil prices and we will illustrate this point in the next section.

-

2

4

6

8

10

12

0

100

200

300

400

500

600

2000 2002 2004 2006 2008 2010 2012

EU-28 Korea/Singapore Middle East US Gulf Coast US East Coast

380

74

14

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

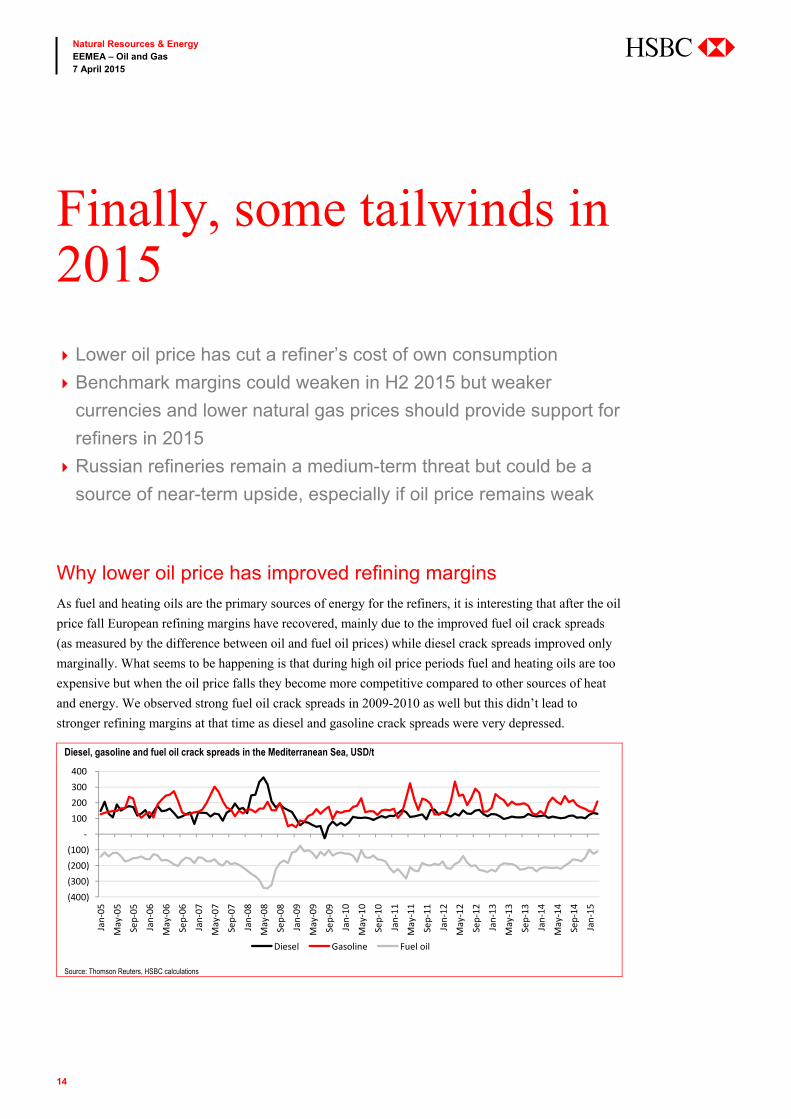

Why lower oil price has improved refining margins

As fuel and heating oils are the primary sources of energy for the refiners, it is interesting that after the oil

price fall European refining margins have recovered, mainly due to the improved fuel oil crack spreads

(as measured by the difference between oil and fuel oil prices) while diesel crack spreads improved only

marginally. What seems to be happening is that during high oil price periods fuel and heating oils are too

expensive but when the oil price falls they become more competitive compared to other sources of heat

and energy. We observed strong fuel oil crack spreads in 2009-2010 as well but this didn’t lead to

stronger refining margins at that time as diesel and gasoline crack spreads were very depressed.

Diesel, gasoline and fuel oil crack spreads in the Mediterranean Sea, USD/t

Source: Thomson Reuters, HSBC calculations

(400) (300) (200) (100)

- 100 200 300 400

Jan-

05

May

-05

Sep-

05

Jan-

06

May

-06

Sep-

06

Jan-

07

May

-07

Sep-

07

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

May

-14

Sep-

14

Jan-

15

Diesel Gasoline Fuel oil

Finally, some tailwinds in 2015

Lower oil price has cut a refiner’s cost of own consumption

Benchmark margins could weaken in H2 2015 but weaker

currencies and lower natural gas prices should provide support for

refiners in 2015

Russian refineries remain a medium-term threat but could be a

source of near-term upside, especially if oil price remains weak

15

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

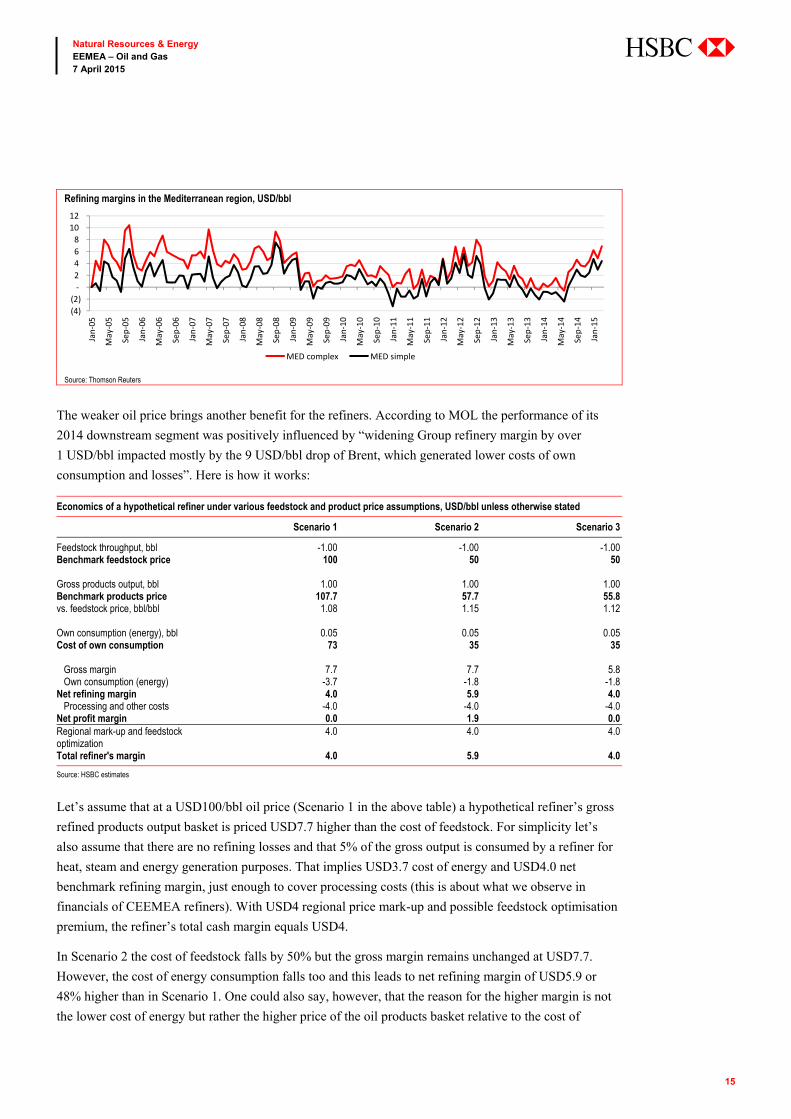

Refining margins in the Mediterranean region, USD/bbl

Source: Thomson Reuters

The weaker oil price brings another benefit for the refiners. According to MOL the performance of its

2014 downstream segment was positively influenced by “widening Group refinery margin by over

1 USD/bbl impacted mostly by the 9 USD/bbl drop of Brent, which generated lower costs of own

consumption and losses”. Here is how it works: Economics of a hypothetical refiner under various feedstock and product price assumptions, USD/bbl unless otherwise stated

Scenario 1 Scenario 2 Scenario 3

Feedstock throughput, bbl -1.00 -1.00 -1.00 Benchmark feedstock price 100 50 50 Gross products output, bbl 1.00 1.00 1.00 Benchmark products price 107.7 57.7 55.8 vs. feedstock price, bbl/bbl 1.08 1.15 1.12 Own consumption (energy), bbl 0.05 0.05 0.05 Cost of own consumption 73 35 35 Gross margin 7.7 7.7 5.8 Own consumption (energy) -3.7 -1.8 -1.8 Net refining margin 4.0 5.9 4.0 Processing and other costs -4.0 -4.0 -4.0 Net profit margin 0.0 1.9 0.0 Regional mark-up and feedstock optimization

4.0 4.0 4.0

Total refiner's margin 4.0 5.9 4.0

Source: HSBC estimates

Let’s assume that at a USD100/bbl oil price (Scenario 1 in the above table) a hypothetical refiner’s gross

refined products output basket is priced USD7.7 higher than the cost of feedstock. For simplicity let’s

also assume that there are no refining losses and that 5% of the gross output is consumed by a refiner for

heat, steam and energy generation purposes. That implies USD3.7 cost of energy and USD4.0 net

benchmark refining margin, just enough to cover processing costs (this is about what we observe in

financials of CEEMEA refiners). With USD4 regional price mark-up and possible feedstock optimisation

premium, the refiner’s total cash margin equals USD4.

In Scenario 2 the cost of feedstock falls by 50% but the gross margin remains unchanged at USD7.7.

However, the cost of energy consumption falls too and this leads to net refining margin of USD5.9 or

48% higher than in Scenario 1. One could also say, however, that the reason for the higher margin is not

the lower cost of energy but rather the higher price of the oil products basket relative to the cost of

(4) (2)

- 2 4 6 8

10 12

Jan-

05

May

-05

Sep-

05

Jan-

06

May

-06

Sep-

06

Jan-

07

May

-07

Sep-

07

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

May

-14

Sep-

14

Jan-

15

MED complex MED simple

16

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

feedstock (at 1.15 on a bbl per bbl basis compared to 1.08 in Scenario 1). If the product basket was priced

12% higher than the cost of feedstock (Scenario 3), that would generate a net refining margin equivalent

to that in Scenario 1. However, the level of the basket premium over the crude oil price is a derivative of

individual crack spreads, which are driven by individual product supply/demand balances and the

respective refining costs, that is refiners are price-takers when it comes to benchmark prices.

Conflicting factors to drive margins further in 2015

We expect the Brent oil price to recover gradually to USD70/bbl by the end of 2015 and average

USD75/bbl in 2016. We continue to believe the current price environment will have the effect intended

by OPEC in curbing non-OPEC output and preserving its market share in the longer term. Between 2014

and 2020, we expect global oil demand to rise by 6mbd, with the effect of weakening economic activity

offset to some degree by positive effects on developed world demand from price elasticity. If our

forecasts prove to be correct, the benefit of the lower oil price on the cost of own consumption for refiners

may thus start fading soon. At the same time, HSBC believes that near-term downside risks to oil prices

remain very real due to a rise in US stockpiles and a possible increase in Iranian exports (for more details

see HSBC report Crude oil market insights – March 2015 published on 23 March 2015).

HSBC crude oil and natural gas forecast

2013 2014 Q1 2015e Q2 2015e Q3 2015e Q4 2015e 2015e 2016e 2017e 2018e

Brent USD/bbl 108.8 98.9 55.0 60.0 65.0 70.0 62.5 75.0 90.0 95.0 WTI USD/bbl 97.9 93.1 48.0 53.0 58.0 63.0 55.5 70.0 85.0 90.0 UK spot gas GBp/th 68.2 50.2 8.0 42.0 42.0 45.0 44.3 48.3 56.3 61.8

Source: Bloomberg, HSBC estimates

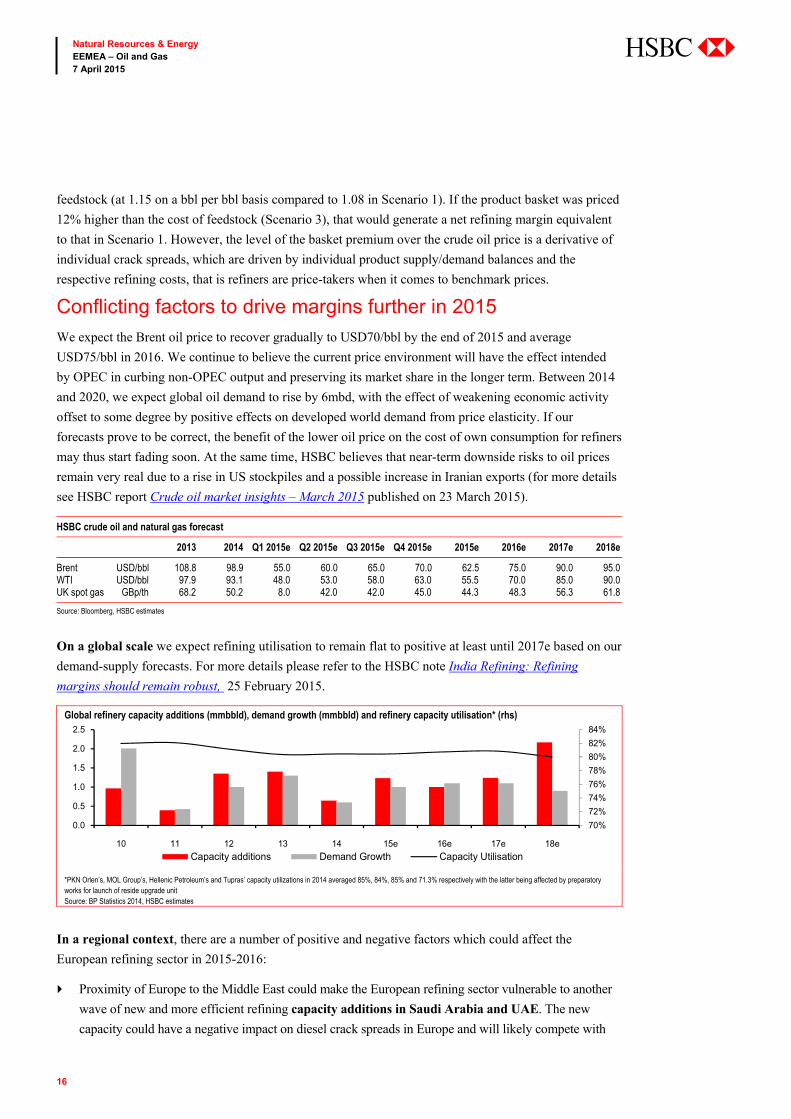

On a global scale we expect refining utilisation to remain flat to positive at least until 2017e based on our

demand-supply forecasts. For more details please refer to the HSBC note India Refining: Refining

margins should remain robust, 25 February 2015.

Global refinery capacity additions (mmbbld), demand growth (mmbbld) and refinery capacity utilisation* (rhs)

*PKN Orlen’s, MOL Group’s, Hellenic Petroleum’s and Tupras’ capacity utilizations in 2014 averaged 85%, 84%, 85% and 71.3% respectively with the latter being affected by preparatory works for launch of reside upgrade unit Source: BP Statistics 2014, HSBC estimates

In a regional context, there are a number of positive and negative factors which could affect the

European refining sector in 2015-2016:

Proximity of Europe to the Middle East could make the European refining sector vulnerable to another

wave of new and more efficient refining capacity additions in Saudi Arabia and UAE. The new

capacity could have a negative impact on diesel crack spreads in Europe and will likely compete with

70%

72%

74%

76%

78%

80%

82%

84%

0.0

0.5

1.0

1.5

2.0

2.5

10 11 12 13 14 15e 16e 17e 18e

Capacity additions Demand Growth Capacity Utilisation

17

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

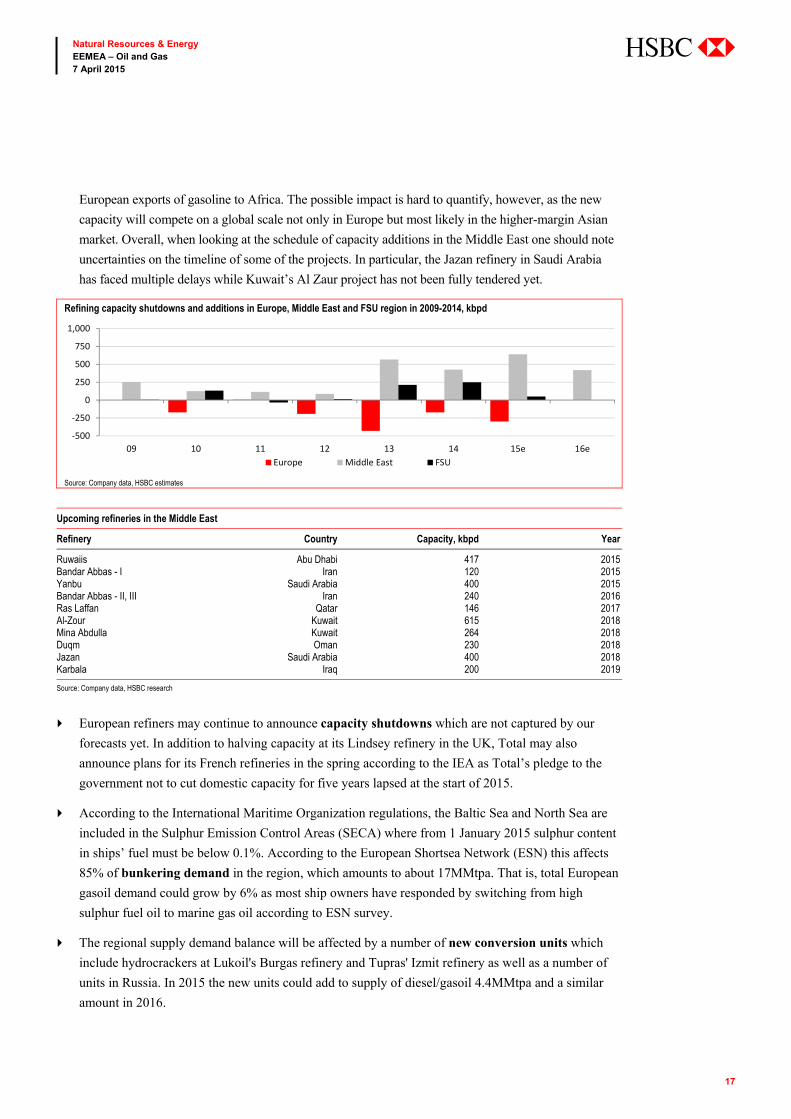

European exports of gasoline to Africa. The possible impact is hard to quantify, however, as the new

capacity will compete on a global scale not only in Europe but most likely in the higher-margin Asian

market. Overall, when looking at the schedule of capacity additions in the Middle East one should note

uncertainties on the timeline of some of the projects. In particular, the Jazan refinery in Saudi Arabia

has faced multiple delays while Kuwait’s Al Zaur project has not been fully tendered yet.

Refining capacity shutdowns and additions in Europe, Middle East and FSU region in 2009-2014, kbpd

Source: Company data, HSBC estimates

Upcoming refineries in the Middle East

Refinery Country Capacity, kbpd Year

Ruwaiis Abu Dhabi 417 2015 Bandar Abbas - I Iran 120 2015 Yanbu Saudi Arabia 400 2015 Bandar Abbas - II, III Iran 240 2016 Ras Laffan Qatar 146 2017 Al-Zour Kuwait 615 2018 Mina Abdulla Kuwait 264 2018 Duqm Oman 230 2018 Jazan Saudi Arabia 400 2018 Karbala Iraq 200 2019

Source: Company data, HSBC research

European refiners may continue to announce capacity shutdowns which are not captured by our

forecasts yet. In addition to halving capacity at its Lindsey refinery in the UK, Total may also

announce plans for its French refineries in the spring according to the IEA as Total’s pledge to the

government not to cut domestic capacity for five years lapsed at the start of 2015.

According to the International Maritime Organization regulations, the Baltic Sea and North Sea are

included in the Sulphur Emission Control Areas (SECA) where from 1 January 2015 sulphur content

in ships’ fuel must be below 0.1%. According to the European Shortsea Network (ESN) this affects

85% of bunkering demand in the region, which amounts to about 17MMtpa. That is, total European

gasoil demand could grow by 6% as most ship owners have responded by switching from high

sulphur fuel oil to marine gas oil according to ESN survey.

The regional supply demand balance will be affected by a number of new conversion units which

include hydrocrackers at Lukoil's Burgas refinery and Tupras' Izmit refinery as well as a number of

units in Russia. In 2015 the new units could add to supply of diesel/gasoil 4.4MMtpa and a similar

amount in 2016.

-500

-250

0

250

500

750

1,000

09 10 11 12 13 14 15e 16eEurope Middle East FSU

18

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

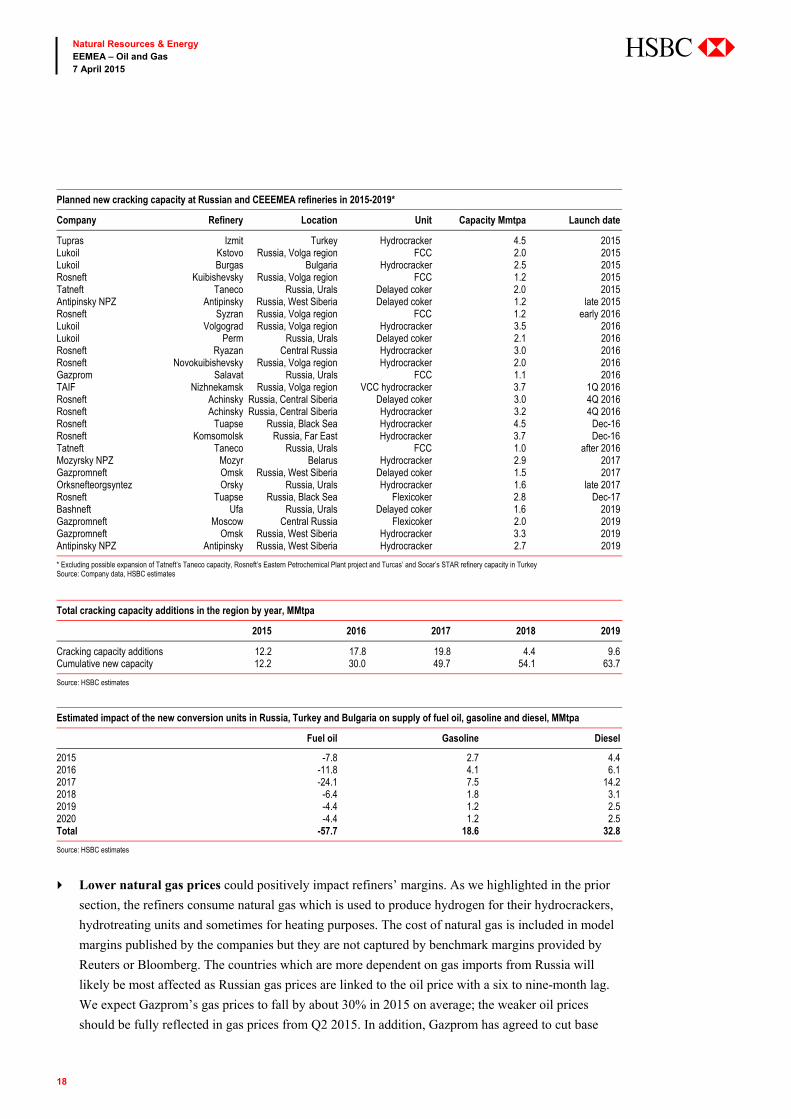

Planned new cracking capacity at Russian and CEEEMEA refineries in 2015-2019*

Company Refinery Location Unit Capacity Mmtpa Launch date

Tupras Izmit Turkey Hydrocracker 4.5 2015 Lukoil Kstovo Russia, Volga region FCC 2.0 2015 Lukoil Burgas Bulgaria Hydrocracker 2.5 2015 Rosneft Kuibishevsky Russia, Volga region FCC 1.2 2015 Tatneft Taneco Russia, Urals Delayed coker 2.0 2015 Antipinsky NPZ Antipinsky Russia, West Siberia Delayed coker 1.2 late 2015 Rosneft Syzran Russia, Volga region FCC 1.2 early 2016 Lukoil Volgograd Russia, Volga region Hydrocracker 3.5 2016 Lukoil Perm Russia, Urals Delayed coker 2.1 2016 Rosneft Ryazan Central Russia Hydrocracker 3.0 2016 Rosneft Novokuibishevsky Russia, Volga region Hydrocracker 2.0 2016 Gazprom Salavat Russia, Urals FCC 1.1 2016 TAIF Nizhnekamsk Russia, Volga region VCC hydrocracker 3.7 1Q 2016 Rosneft Achinsky Russia, Central Siberia Delayed coker 3.0 4Q 2016 Rosneft Achinsky Russia, Central Siberia Hydrocracker 3.2 4Q 2016 Rosneft Tuapse Russia, Black Sea Hydrocracker 4.5 Dec-16 Rosneft Komsomolsk Russia, Far East Hydrocracker 3.7 Dec-16 Tatneft Taneco Russia, Urals FCC 1.0 after 2016 Mozyrsky NPZ Mozyr Belarus Hydrocracker 2.9 2017 Gazpromneft Omsk Russia, West Siberia Delayed coker 1.5 2017 Orksnefteorgsyntez Orsky Russia, Urals Hydrocracker 1.6 late 2017 Rosneft Tuapse Russia, Black Sea Flexicoker 2.8 Dec-17 Bashneft Ufa Russia, Urals Delayed coker 1.6 2019 Gazpromneft Moscow Central Russia Flexicoker 2.0 2019 Gazpromneft Omsk Russia, West Siberia Hydrocracker 3.3 2019 Antipinsky NPZ Antipinsky Russia, West Siberia Hydrocracker 2.7 2019

* Excluding possible expansion of Tatneft’s Taneco capacity, Rosneft’s Eastern Petrochemical Plant project and Turcas’ and Socar’s STAR refinery capacity in Turkey Source: Company data, HSBC estimates

Total cracking capacity additions in the region by year, MMtpa

2015 2016 2017 2018 2019

Cracking capacity additions 12.2 17.8 19.8 4.4 9.6 Cumulative new capacity 12.2 30.0 49.7 54.1 63.7

Source: HSBC estimates

Estimated impact of the new conversion units in Russia, Turkey and Bulgaria on supply of fuel oil, gasoline and diesel, MMtpa

Fuel oil Gasoline Diesel

2015 -7.8 2.7 4.4 2016 -11.8 4.1 6.1 2017 -24.1 7.5 14.2 2018 -6.4 1.8 3.1 2019 -4.4 1.2 2.5 2020 -4.4 1.2 2.5 Total -57.7 18.6 32.8

Source: HSBC estimates

Lower natural gas prices could positively impact refiners’ margins. As we highlighted in the prior

section, the refiners consume natural gas which is used to produce hydrogen for their hydrocrackers,

hydrotreating units and sometimes for heating purposes. The cost of natural gas is included in model

margins published by the companies but they are not captured by benchmark margins provided by

Reuters or Bloomberg. The countries which are more dependent on gas imports from Russia will

likely be most affected as Russian gas prices are linked to the oil price with a six to nine-month lag.

We expect Gazprom’s gas prices to fall by about 30% in 2015 on average; the weaker oil prices

should be fully reflected in gas prices from Q2 2015. In addition, Gazprom has agreed to cut base

19

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

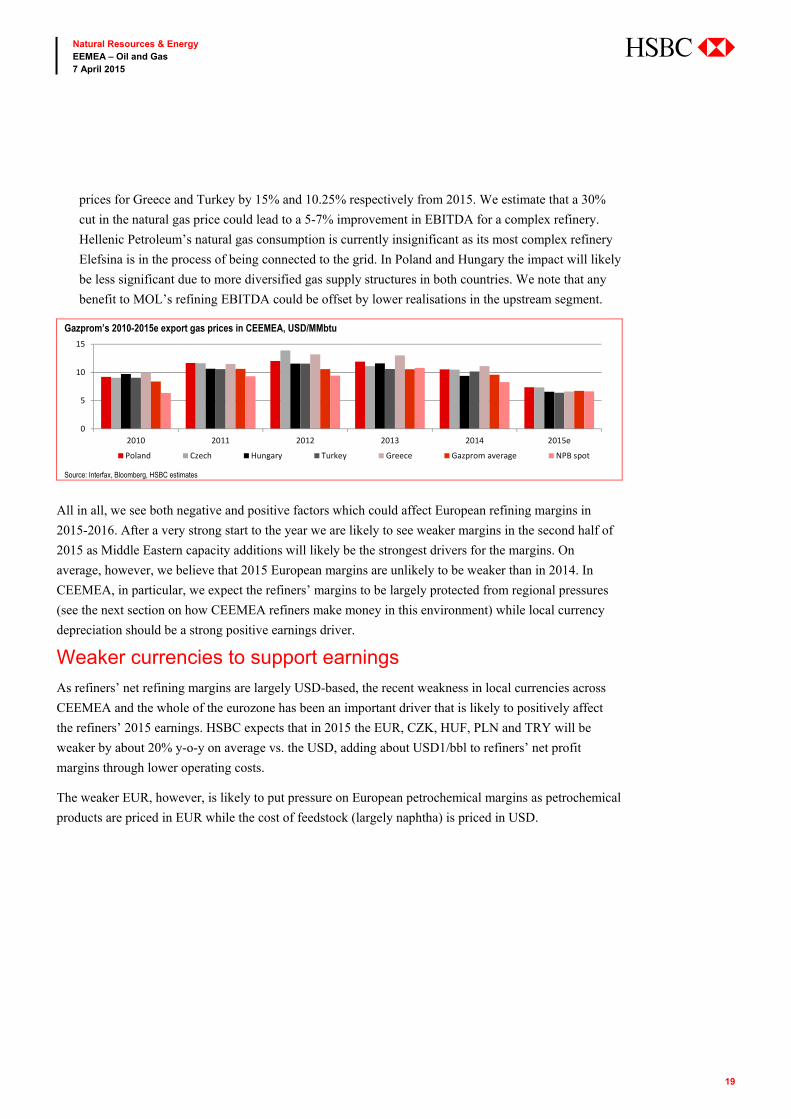

prices for Greece and Turkey by 15% and 10.25% respectively from 2015. We estimate that a 30%

cut in the natural gas price could lead to a 5-7% improvement in EBITDA for a complex refinery.

Hellenic Petroleum’s natural gas consumption is currently insignificant as its most complex refinery

Elefsina is in the process of being connected to the grid. In Poland and Hungary the impact will likely

be less significant due to more diversified gas supply structures in both countries. We note that any

benefit to MOL’s refining EBITDA could be offset by lower realisations in the upstream segment.

Gazprom’s 2010-2015e export gas prices in CEEMEA, USD/MMbtu

Source: Interfax, Bloomberg, HSBC estimates

All in all, we see both negative and positive factors which could affect European refining margins in

2015-2016. After a very strong start to the year we are likely to see weaker margins in the second half of

2015 as Middle Eastern capacity additions will likely be the strongest drivers for the margins. On

average, however, we believe that 2015 European margins are unlikely to be weaker than in 2014. In

CEEMEA, in particular, we expect the refiners’ margins to be largely protected from regional pressures

(see the next section on how CEEMEA refiners make money in this environment) while local currency

depreciation should be a strong positive earnings driver.

Weaker currencies to support earnings

As refiners’ net refining margins are largely USD-based, the recent weakness in local currencies across

CEEMEA and the whole of the eurozone has been an important driver that is likely to positively affect

the refiners’ 2015 earnings. HSBC expects that in 2015 the EUR, CZK, HUF, PLN and TRY will be

weaker by about 20% y-o-y on average vs. the USD, adding about USD1/bbl to refiners’ net profit

margins through lower operating costs.

The weaker EUR, however, is likely to put pressure on European petrochemical margins as petrochemical

products are priced in EUR while the cost of feedstock (largely naphtha) is priced in USD.

0

5

10

15

2010 2011 2012 2013 2014 2015e

Poland Czech Hungary Turkey Greece Gazprom average NPB spot

20

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

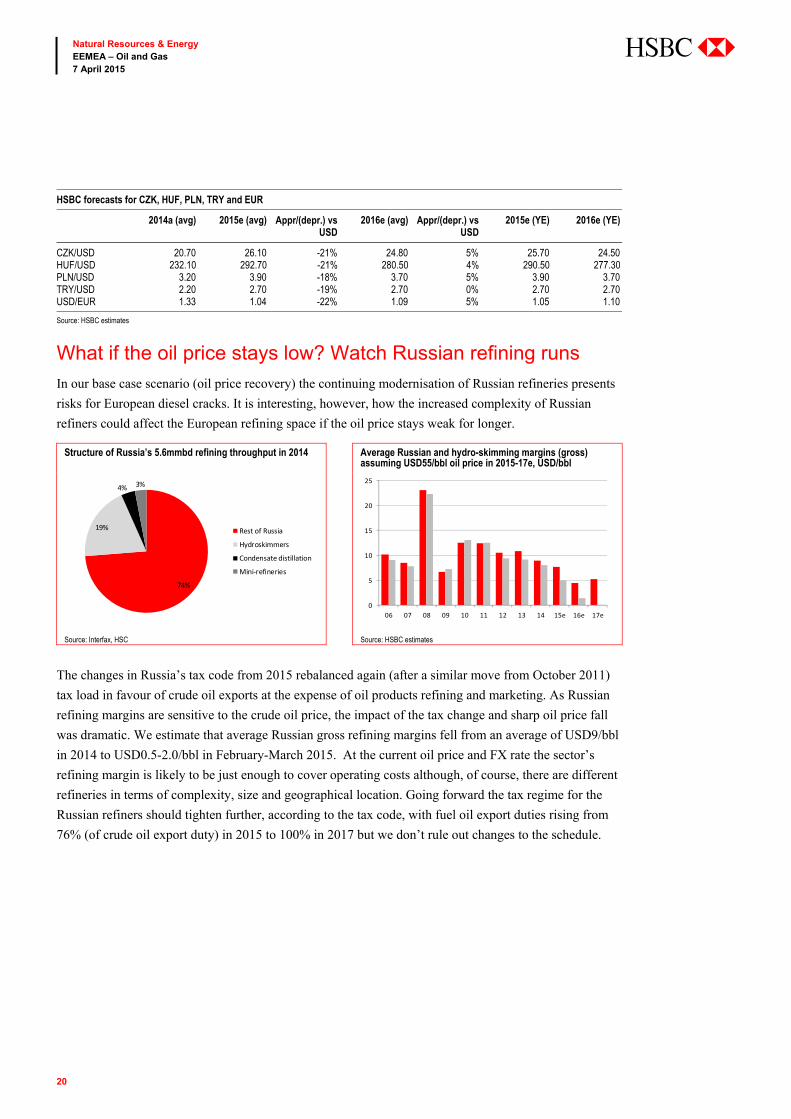

HSBC forecasts for CZK, HUF, PLN, TRY and EUR

2014a (avg) 2015e (avg) Appr/(depr.) vs USD

2016e (avg) Appr/(depr.) vs USD

2015e (YE) 2016e (YE)

CZK/USD 20.70 26.10 -21% 24.80 5% 25.70 24.50 HUF/USD 232.10 292.70 -21% 280.50 4% 290.50 277.30 PLN/USD 3.20 3.90 -18% 3.70 5% 3.90 3.70 TRY/USD 2.20 2.70 -19% 2.70 0% 2.70 2.70 USD/EUR 1.33 1.04 -22% 1.09 5% 1.05 1.10

Source: HSBC estimates

What if the oil price stays low? Watch Russian refining runs

In our base case scenario (oil price recovery) the continuing modernisation of Russian refineries presents

risks for European diesel cracks. It is interesting, however, how the increased complexity of Russian

refiners could affect the European refining space if the oil price stays weak for longer.

Structure of Russia’s 5.6mmbd refining throughput in 2014 Average Russian and hydro-skimming margins (gross) assuming USD55/bbl oil price in 2015-17e, USD/bbl

Source: Interfax, HSC Source: HSBC estimates

The changes in Russia’s tax code from 2015 rebalanced again (after a similar move from October 2011)

tax load in favour of crude oil exports at the expense of oil products refining and marketing. As Russian

refining margins are sensitive to the crude oil price, the impact of the tax change and sharp oil price fall

was dramatic. We estimate that average Russian gross refining margins fell from an average of USD9/bbl

in 2014 to USD0.5-2.0/bbl in February-March 2015. At the current oil price and FX rate the sector’s

refining margin is likely to be just enough to cover operating costs although, of course, there are different

refineries in terms of complexity, size and geographical location. Going forward the tax regime for the

Russian refiners should tighten further, according to the tax code, with fuel oil export duties rising from

76% (of crude oil export duty) in 2015 to 100% in 2017 but we don’t rule out changes to the schedule.

74%

19%

4% 3%

Rest of Russia

Hydroskimmers

Condensate distillation

Mini-refineries

0

5

10

15

20

25

06 07 08 09 10 11 12 13 14 15e 16e 17e

21

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

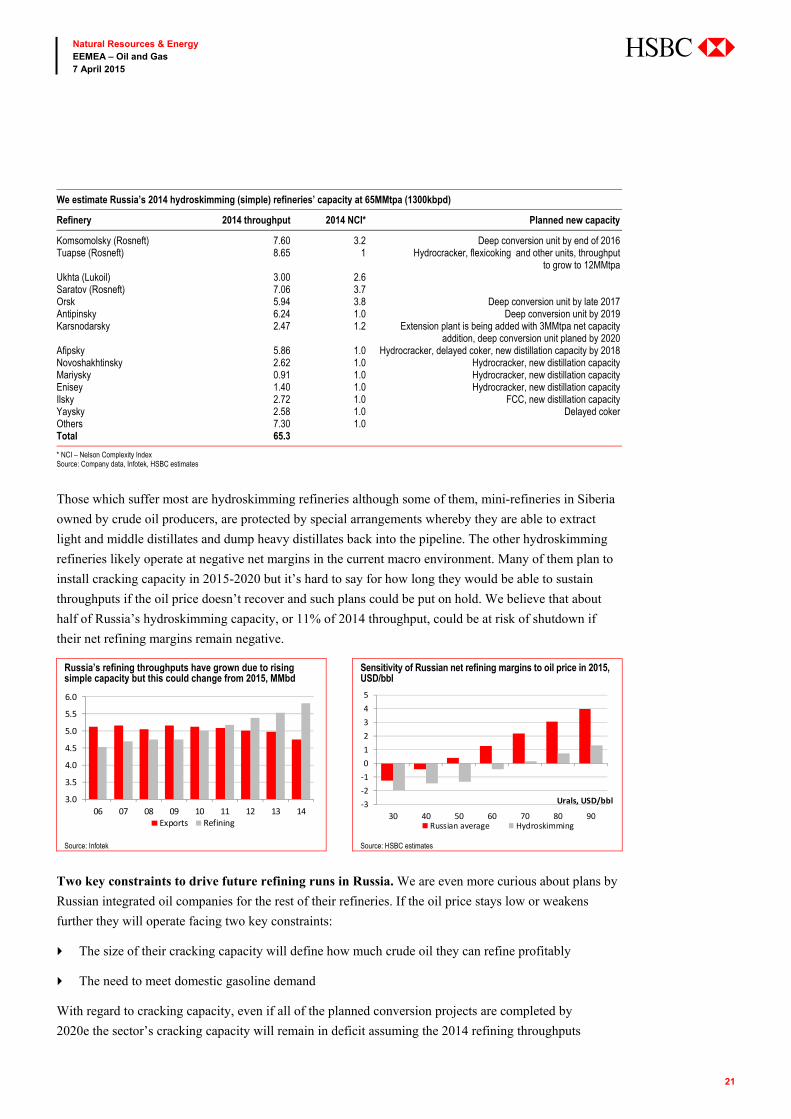

We estimate Russia’s 2014 hydroskimming (simple) refineries’ capacity at 65MMtpa (1300kbpd)

Refinery 2014 throughput 2014 NCI* Planned new capacity

Komsomolsky (Rosneft) 7.60 3.2 Deep conversion unit by end of 2016 Tuapse (Rosneft) 8.65 1 Hydrocracker, flexicoking and other units, throughput

to grow to 12MMtpa Ukhta (Lukoil) 3.00 2.6 Saratov (Rosneft) 7.06 3.7 Orsk 5.94 3.8 Deep conversion unit by late 2017 Antipinsky 6.24 1.0 Deep conversion unit by 2019 Karsnodarsky 2.47 1.2 Extension plant is being added with 3MMtpa net capacity

addition, deep conversion unit planed by 2020 Afipsky 5.86 1.0 Hydrocracker, delayed coker, new distillation capacity by 2018 Novoshakhtinsky 2.62 1.0 Hydrocracker, new distillation capacity Mariysky 0.91 1.0 Hydrocracker, new distillation capacity Enisey 1.40 1.0 Hydrocracker, new distillation capacity Ilsky 2.72 1.0 FCC, new distillation capacity Yaysky 2.58 1.0 Delayed coker Others 7.30 1.0 Total 65.3

* NCI – Nelson Complexity Index Source: Company data, Infotek, HSBC estimates

Those which suffer most are hydroskimming refineries although some of them, mini-refineries in Siberia

owned by crude oil producers, are protected by special arrangements whereby they are able to extract

light and middle distillates and dump heavy distillates back into the pipeline. The other hydroskimming

refineries likely operate at negative net margins in the current macro environment. Many of them plan to

install cracking capacity in 2015-2020 but it’s hard to say for how long they would be able to sustain

throughputs if the oil price doesn’t recover and such plans could be put on hold. We believe that about

half of Russia’s hydroskimming capacity, or 11% of 2014 throughput, could be at risk of shutdown if

their net refining margins remain negative.

Russia’s refining throughputs have grown due to rising simple capacity but this could change from 2015, MMbd

Sensitivity of Russian net refining margins to oil price in 2015, USD/bbl

Source: Infotek Source: HSBC estimates

Two key constraints to drive future refining runs in Russia. We are even more curious about plans by

Russian integrated oil companies for the rest of their refineries. If the oil price stays low or weakens

further they will operate facing two key constraints:

The size of their cracking capacity will define how much crude oil they can refine profitably

The need to meet domestic gasoline demand

With regard to cracking capacity, even if all of the planned conversion projects are completed by

2020e the sector’s cracking capacity will remain in deficit assuming the 2014 refining throughputs

3.0

3.5

4.0

4.5

5.0

5.5

6.0

06 07 08 09 10 11 12 13 14Exports Refining

-3-2-1012345

30 40 50 60 70 80 90

Urals, USD/bbl

Russian average Hydroskimming

22

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

(fuel oil output was 78MMtpa on the top of about 10MMtpa vacuum gasoil). That is, even if all of these

projects were completed and there were no other constraints, the refiners would be tempted to cut their

runs to a level where marginal refined barrel margin breaks even. The Energy Ministry expects that

Russia’s refining runs will fall by 12% by 2020 but this estimate is sensitive to oil prices, in our view. Estimated impact of the new conversion units in Russia on supply of fuel oil, gasoline and diesel, MMtpa

Fuel oil Gasoline Diesel

2015 -2.3 1.0 0.6 2016 -10.6 3.7 5.3 2017 -24.1 7.5 14.2 2018 -6.4 1.8 3.1 2019 -4.4 1.2 2.5 2020 -4.4 1.2 2.5 Total -52.1 16.5 28.3

Source: HSBC estimates

In a scenario where there is some excessive gasoline capacity, a refiner which lacks cracking capacity

could be tempted to cut its runs at least to the level where gasoline demand is matched. We estimate that

the sector’s gasoline output capacity could grow by 1.0MMtpa, 3.7MMtpa and 7.5MMtpa in 2015-2017e

respectively. Gasoline supply in Russia was nearly identical to the total sector’s output in 2011 but 2014

production of gasoline exceeded demand by 4MMtpa and a similar surplus is expected in 2015 according

to Russia’s Energy Ministry, although likely more than half of this gasoline is exported to FSU countries

and can be considered as consumed domestically for the purposes of our analysis. Theoretically, marginal

supply of 1MMtpa of gasoline can allow the sector to cut throughputs by 5MMtpa or by about 2%.

In our view, there is scope for a 5-6% cut in 2015 refining runs. Based on 1MMt gasoline supply

addition this year, likely lower consumption (HSBC expects Russia’s GDP to fall by 3% in 2015) and

some room to cut exports we believe that in 2015 the scope for cuts in refining throughput is limited to

some 5-6% but marginal production of gasoline will rise dramatically from 2016.

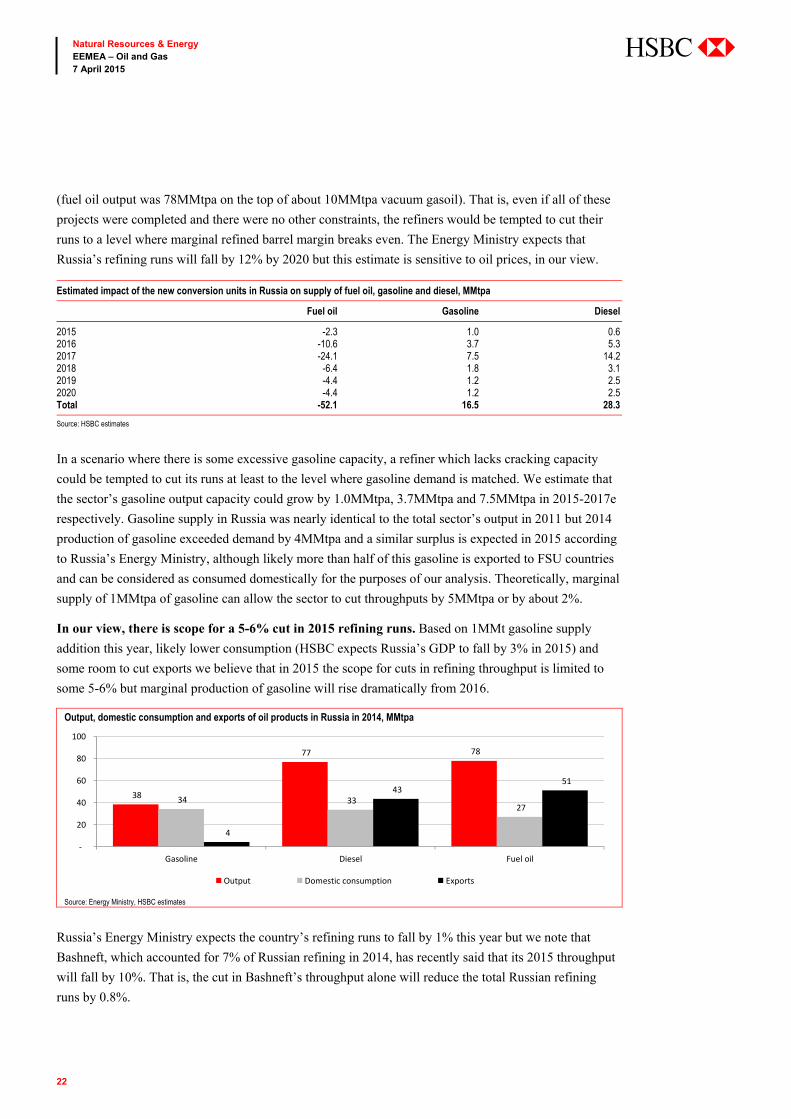

Output, domestic consumption and exports of oil products in Russia in 2014, MMtpa

Source: Energy Ministry, HSBC estimates

Russia’s Energy Ministry expects the country’s refining runs to fall by 1% this year but we note that

Bashneft, which accounted for 7% of Russian refining in 2014, has recently said that its 2015 throughput

will fall by 10%. That is, the cut in Bashneft’s throughput alone will reduce the total Russian refining

runs by 0.8%.

38

77 78

34 33 27

4

43 51

-

20

40

60

80

100

Gasoline Diesel Fuel oil

Output Domestic consumption Exports

23

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

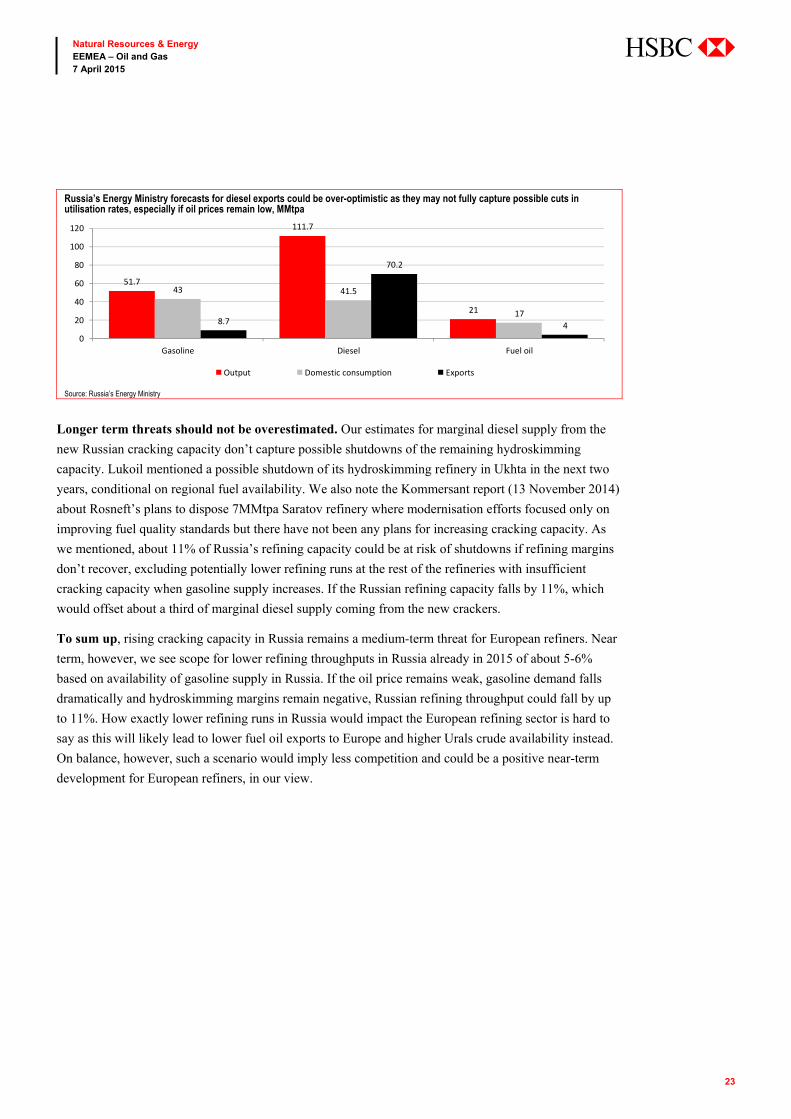

Russia’s Energy Ministry forecasts for diesel exports could be over-optimistic as they may not fully capture possible cuts in utilisation rates, especially if oil prices remain low, MMtpa

Source: Russia’s Energy Ministry

Longer term threats should not be overestimated. Our estimates for marginal diesel supply from the

new Russian cracking capacity don’t capture possible shutdowns of the remaining hydroskimming

capacity. Lukoil mentioned a possible shutdown of its hydroskimming refinery in Ukhta in the next two

years, conditional on regional fuel availability. We also note the Kommersant report (13 November 2014)

about Rosneft’s plans to dispose 7MMtpa Saratov refinery where modernisation efforts focused only on

improving fuel quality standards but there have not been any plans for increasing cracking capacity. As

we mentioned, about 11% of Russia’s refining capacity could be at risk of shutdowns if refining margins

don’t recover, excluding potentially lower refining runs at the rest of the refineries with insufficient

cracking capacity when gasoline supply increases. If the Russian refining capacity falls by 11%, which

would offset about a third of marginal diesel supply coming from the new crackers.

To sum up, rising cracking capacity in Russia remains a medium-term threat for European refiners. Near

term, however, we see scope for lower refining throughputs in Russia already in 2015 of about 5-6%

based on availability of gasoline supply in Russia. If the oil price remains weak, gasoline demand falls

dramatically and hydroskimming margins remain negative, Russian refining throughput could fall by up

to 11%. How exactly lower refining runs in Russia would impact the European refining sector is hard to

say as this will likely lead to lower fuel oil exports to Europe and higher Urals crude availability instead.

On balance, however, such a scenario would imply less competition and could be a positive near-term

development for European refiners, in our view.

51.7

111.7

21

43 41.5

178.7

70.2

40

20

40

60

80

100

120

Gasoline Diesel Fuel oil

Output Domestic consumption Exports

24

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

Benchmark margins ignore regional pricing specifics

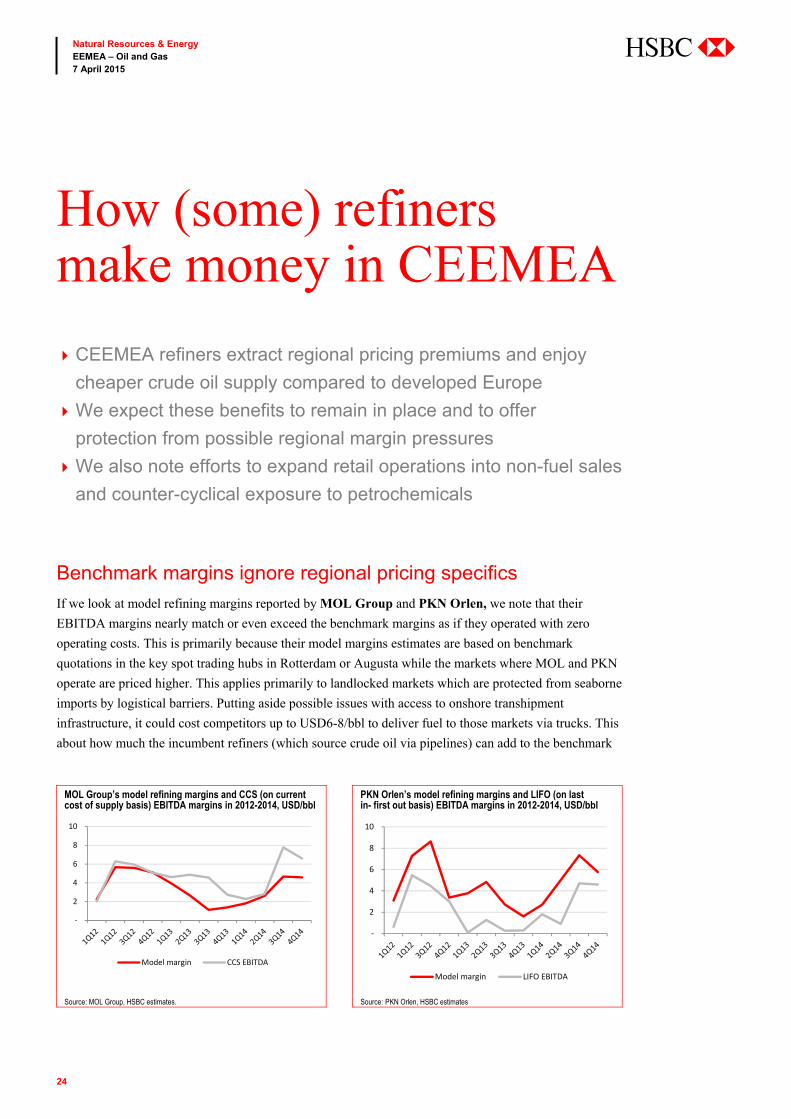

If we look at model refining margins reported by MOL Group and PKN Orlen, we note that their

EBITDA margins nearly match or even exceed the benchmark margins as if they operated with zero

operating costs. This is primarily because their model margins estimates are based on benchmark

quotations in the key spot trading hubs in Rotterdam or Augusta while the markets where MOL and PKN

operate are priced higher. This applies primarily to landlocked markets which are protected from seaborne

imports by logistical barriers. Putting aside possible issues with access to onshore transhipment

infrastructure, it could cost competitors up to USD6-8/bbl to deliver fuel to those markets via trucks. This

about how much the incumbent refiners (which source crude oil via pipelines) can add to the benchmark

How (some) refinersmake money in CEEMEA

CEEMEA refiners extract regional pricing premiums and enjoy

cheaper crude oil supply compared to developed Europe

We expect these benefits to remain in place and to offer

protection from possible regional margin pressures

We also note efforts to expand retail operations into non-fuel sales

and counter-cyclical exposure to petrochemicals

MOL Group’s model refining margins and CCS (on current cost of supply basis) EBITDA margins in 2012-2014, USD/bbl

PKN Orlen’s model refining margins and LIFO (on last in- first out basis) EBITDA margins in 2012-2014, USD/bbl

Source: MOL Group, HSBC estimates. Source: PKN Orlen, HSBC estimates

-

2

4

6

8

10

Model margin CCS EBITDA

-

2

4

6

8

10

Model margin LIFO EBITDA

25

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

prices when selling their products in their markets. The opposite, of course, applies to products which

they have to export.

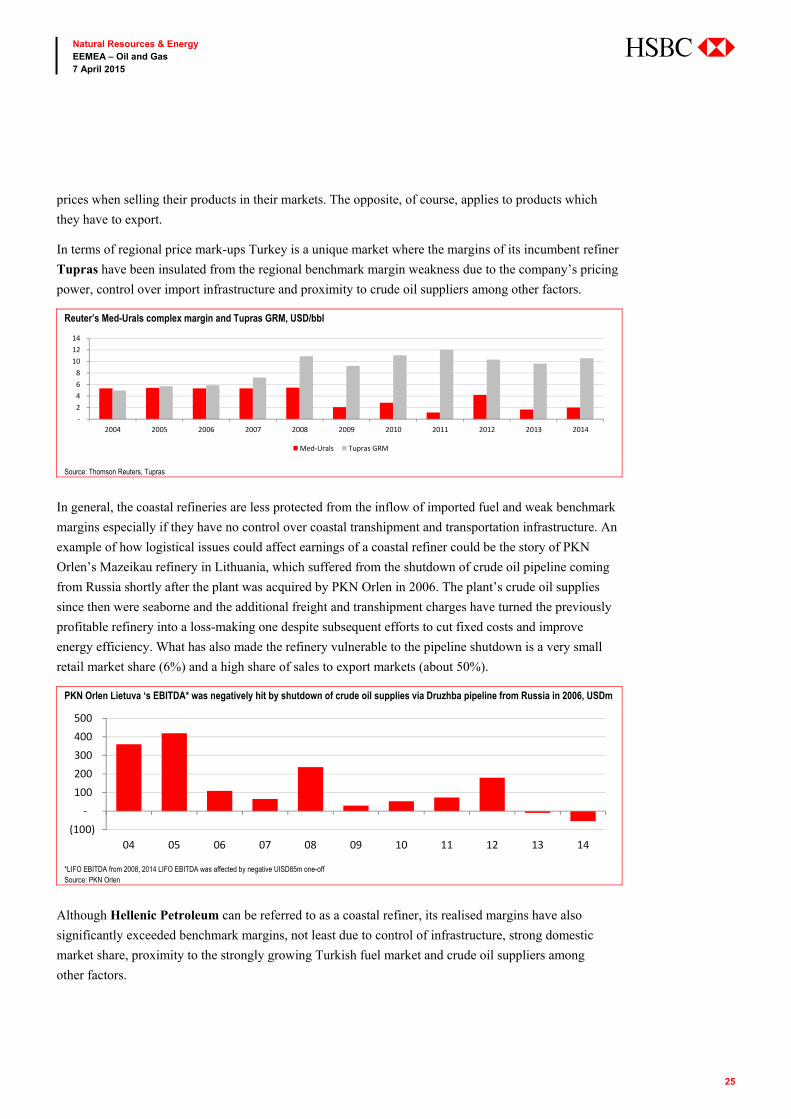

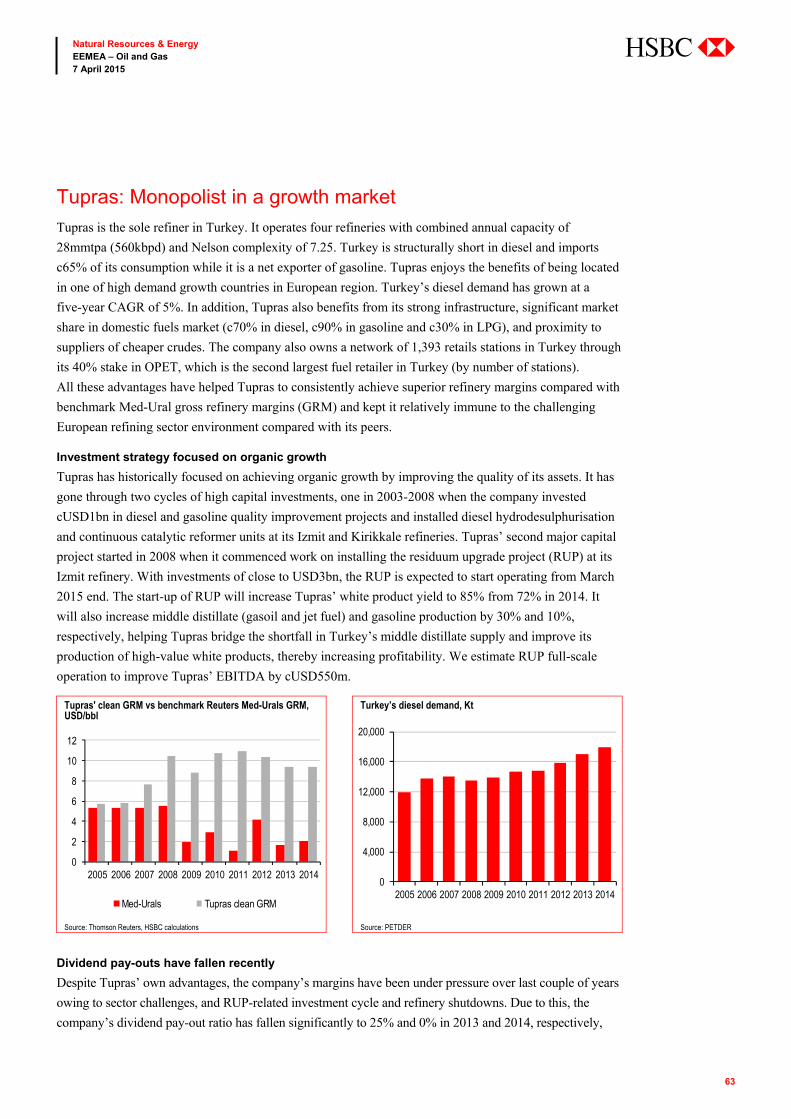

In terms of regional price mark-ups Turkey is a unique market where the margins of its incumbent refiner

Tupras have been insulated from the regional benchmark margin weakness due to the company’s pricing

power, control over import infrastructure and proximity to crude oil suppliers among other factors.

Reuter’s Med-Urals complex margin and Tupras GRM, USD/bbl

Source: Thomson Reuters, Tupras

In general, the coastal refineries are less protected from the inflow of imported fuel and weak benchmark

margins especially if they have no control over coastal transhipment and transportation infrastructure. An

example of how logistical issues could affect earnings of a coastal refiner could be the story of PKN

Orlen’s Mazeikau refinery in Lithuania, which suffered from the shutdown of crude oil pipeline coming

from Russia shortly after the plant was acquired by PKN Orlen in 2006. The plant’s crude oil supplies

since then were seaborne and the additional freight and transhipment charges have turned the previously

profitable refinery into a loss-making one despite subsequent efforts to cut fixed costs and improve

energy efficiency. What has also made the refinery vulnerable to the pipeline shutdown is a very small

retail market share (6%) and a high share of sales to export markets (about 50%).

PKN Orlen Lietuva ‘s EBITDA* was negatively hit by shutdown of crude oil supplies via Druzhba pipeline from Russia in 2006, USDm

*LIFO EBITDA from 2008, 2014 LIFO EBITDA was affected by negative UISD85m one-off Source: PKN Orlen

Although Hellenic Petroleum can be referred to as a coastal refiner, its realised margins have also

significantly exceeded benchmark margins, not least due to control of infrastructure, strong domestic

market share, proximity to the strongly growing Turkish fuel market and crude oil suppliers among

other factors.

- 2 4 6 8

10 12 14

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Med-Urals Tupras GRM

(100) -

100 200 300 400 500

04 05 06 07 08 09 10 11 12 13 14

26

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

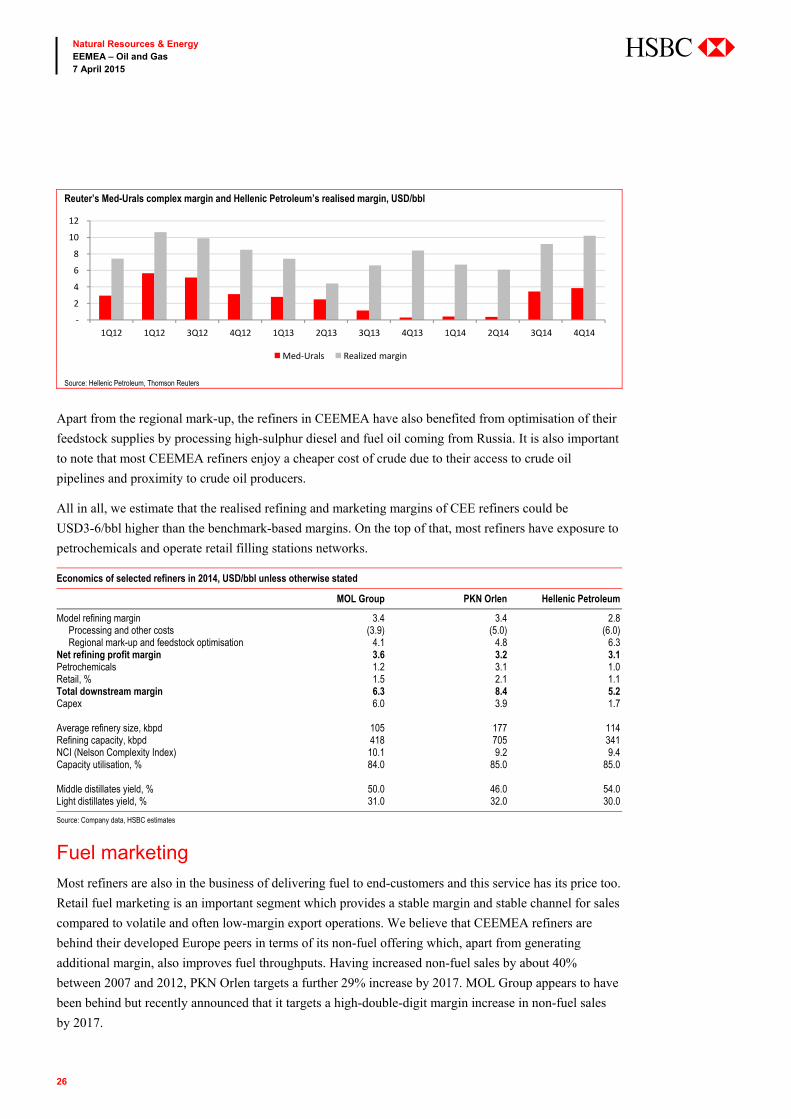

Reuter’s Med-Urals complex margin and Hellenic Petroleum’s realised margin, USD/bbl

Source: Hellenic Petroleum, Thomson Reuters

Apart from the regional mark-up, the refiners in CEEMEA have also benefited from optimisation of their

feedstock supplies by processing high-sulphur diesel and fuel oil coming from Russia. It is also important

to note that most CEEMEA refiners enjoy a cheaper cost of crude due to their access to crude oil

pipelines and proximity to crude oil producers.

All in all, we estimate that the realised refining and marketing margins of CEE refiners could be

USD3-6/bbl higher than the benchmark-based margins. On the top of that, most refiners have exposure to

petrochemicals and operate retail filling stations networks.

Economics of selected refiners in 2014, USD/bbl unless otherwise stated

MOL Group PKN Orlen Hellenic Petroleum

Model refining margin 3.4 3.4 2.8 Processing and other costs (3.9) (5.0) (6.0) Regional mark-up and feedstock optimisation 4.1 4.8 6.3 Net refining profit margin 3.6 3.2 3.1 Petrochemicals 1.2 3.1 1.0 Retail, % 1.5 2.1 1.1 Total downstream margin 6.3 8.4 5.2 Capex 6.0 3.9 1.7 Average refinery size, kbpd 105 177 114 Refining capacity, kbpd 418 705 341 NCI (Nelson Complexity Index) 10.1 9.2 9.4 Capacity utilisation, % 84.0 85.0 85.0 Middle distillates yield, % 50.0 46.0 54.0 Light distillates yield, % 31.0 32.0 30.0

Source: Company data, HSBC estimates

Fuel marketing

Most refiners are also in the business of delivering fuel to end-customers and this service has its price too.

Retail fuel marketing is an important segment which provides a stable margin and stable channel for sales

compared to volatile and often low-margin export operations. We believe that CEEMEA refiners are

behind their developed Europe peers in terms of its non-fuel offering which, apart from generating

additional margin, also improves fuel throughputs. Having increased non-fuel sales by about 40%

between 2007 and 2012, PKN Orlen targets a further 29% increase by 2017. MOL Group appears to have

been behind but recently announced that it targets a high-double-digit margin increase in non-fuel sales

by 2017.

-

2

4

6

8

10

12

1Q12 1Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14

Med-Urals Realized margin

27

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

Fuel retailing is just one important segment of this activity as refiners also compete in aviation and

bunkering fuel segments and the latter is common not only for coastal refiners but also for those with

links to important river corridors, of which the best example is the Danube, Europe’s second-longest river

navigable from the Black Sea to Bavaria in Germany with access to Austria, Slovakia, Hungary, Croatia,

Serbia, Bulgaria, Romania, Moldova and Ukraine.

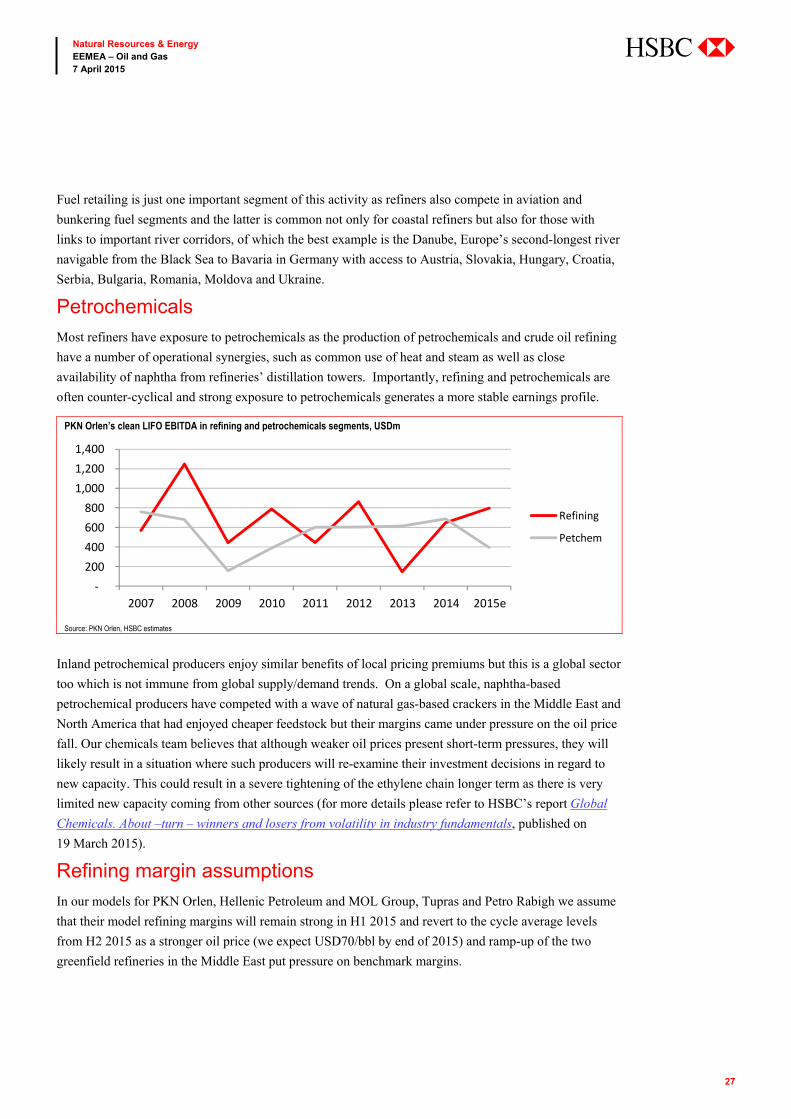

Petrochemicals

Most refiners have exposure to petrochemicals as the production of petrochemicals and crude oil refining

have a number of operational synergies, such as common use of heat and steam as well as close

availability of naphtha from refineries’ distillation towers. Importantly, refining and petrochemicals are

often counter-cyclical and strong exposure to petrochemicals generates a more stable earnings profile.

PKN Orlen’s clean LIFO EBITDA in refining and petrochemicals segments, USDm

Source: PKN Orlen, HSBC estimates

Inland petrochemical producers enjoy similar benefits of local pricing premiums but this is a global sector

too which is not immune from global supply/demand trends. On a global scale, naphtha-based

petrochemical producers have competed with a wave of natural gas-based crackers in the Middle East and

North America that had enjoyed cheaper feedstock but their margins came under pressure on the oil price

fall. Our chemicals team believes that although weaker oil prices present short-term pressures, they will

likely result in a situation where such producers will re-examine their investment decisions in regard to

new capacity. This could result in a severe tightening of the ethylene chain longer term as there is very

limited new capacity coming from other sources (for more details please refer to HSBC’s report Global

Chemicals. About –turn – winners and losers from volatility in industry fundamentals, published on

19 March 2015).

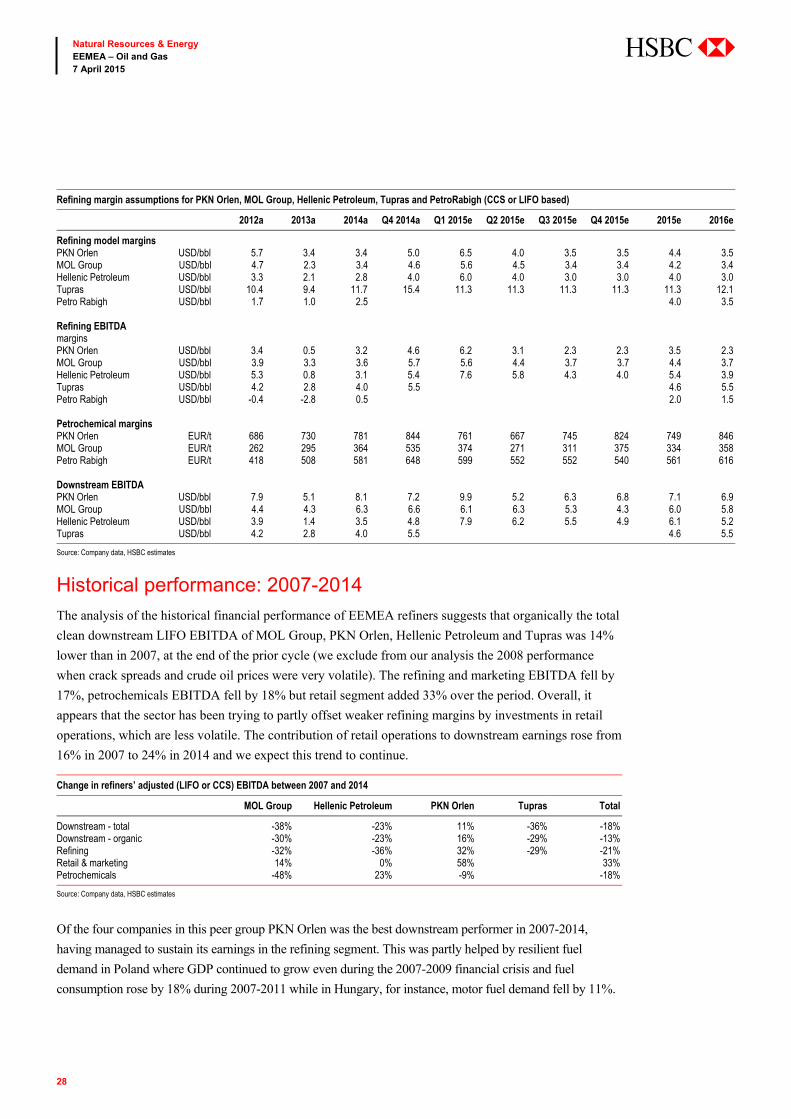

Refining margin assumptions

In our models for PKN Orlen, Hellenic Petroleum and MOL Group, Tupras and Petro Rabigh we assume

that their model refining margins will remain strong in H1 2015 and revert to the cycle average levels

from H2 2015 as a stronger oil price (we expect USD70/bbl by end of 2015) and ramp-up of the two

greenfield refineries in the Middle East put pressure on benchmark margins.

- 200 400 600 800

1,000 1,200 1,400

2007 2008 2009 2010 2011 2012 2013 2014 2015e

Refining

Petchem

28

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

Refining margin assumptions for PKN Orlen, MOL Group, Hellenic Petroleum, Tupras and PetroRabigh (CCS or LIFO based)

2012a 2013a 2014a Q4 2014a Q1 2015e Q2 2015e Q3 2015e Q4 2015e 2015e 2016e

Refining model margins PKN Orlen USD/bbl 5.7 3.4 3.4 5.0 6.5 4.0 3.5 3.5 4.4 3.5 MOL Group USD/bbl 4.7 2.3 3.4 4.6 5.6 4.5 3.4 3.4 4.2 3.4 Hellenic Petroleum USD/bbl 3.3 2.1 2.8 4.0 6.0 4.0 3.0 3.0 4.0 3.0 Tupras USD/bbl 10.4 9.4 11.7 15.4 11.3 11.3 11.3 11.3 11.3 12.1 Petro Rabigh USD/bbl 1.7 1.0 2.5 4.0 3.5 Refining EBITDA margins

PKN Orlen USD/bbl 3.4 0.5 3.2 4.6 6.2 3.1 2.3 2.3 3.5 2.3 MOL Group USD/bbl 3.9 3.3 3.6 5.7 5.6 4.4 3.7 3.7 4.4 3.7 Hellenic Petroleum USD/bbl 5.3 0.8 3.1 5.4 7.6 5.8 4.3 4.0 5.4 3.9 Tupras USD/bbl 4.2 2.8 4.0 5.5 4.6 5.5 Petro Rabigh USD/bbl -0.4 -2.8 0.5 2.0 1.5 Petrochemical margins PKN Orlen EUR/t 686 730 781 844 761 667 745 824 749 846 MOL Group EUR/t 262 295 364 535 374 271 311 375 334 358 Petro Rabigh EUR/t 418 508 581 648 599 552 552 540 561 616 Downstream EBITDA PKN Orlen USD/bbl 7.9 5.1 8.1 7.2 9.9 5.2 6.3 6.8 7.1 6.9 MOL Group USD/bbl 4.4 4.3 6.3 6.6 6.1 6.3 5.3 4.3 6.0 5.8 Hellenic Petroleum USD/bbl 3.9 1.4 3.5 4.8 7.9 6.2 5.5 4.9 6.1 5.2 Tupras USD/bbl 4.2 2.8 4.0 5.5 4.6 5.5

Source: Company data, HSBC estimates

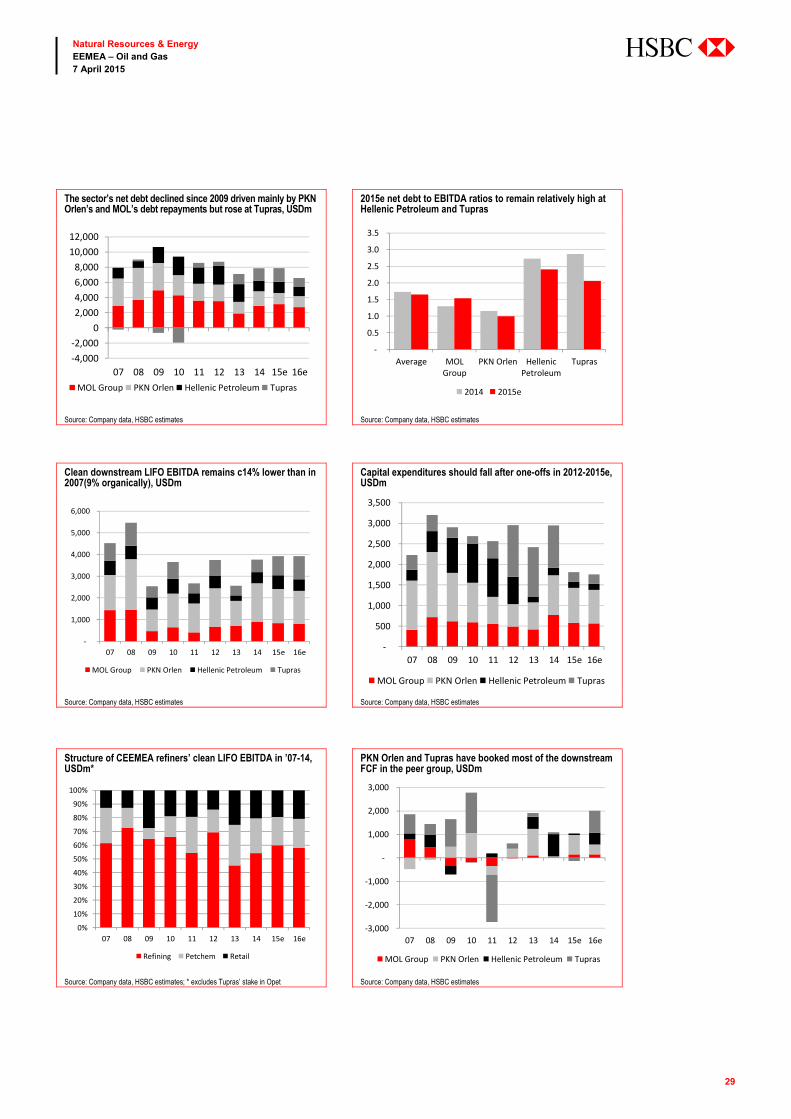

Historical performance: 2007-2014

The analysis of the historical financial performance of EEMEA refiners suggests that organically the total

clean downstream LIFO EBITDA of MOL Group, PKN Orlen, Hellenic Petroleum and Tupras was 14%

lower than in 2007, at the end of the prior cycle (we exclude from our analysis the 2008 performance

when crack spreads and crude oil prices were very volatile). The refining and marketing EBITDA fell by

17%, petrochemicals EBITDA fell by 18% but retail segment added 33% over the period. Overall, it

appears that the sector has been trying to partly offset weaker refining margins by investments in retail

operations, which are less volatile. The contribution of retail operations to downstream earnings rose from

16% in 2007 to 24% in 2014 and we expect this trend to continue.

Change in refiners’ adjusted (LIFO or CCS) EBITDA between 2007 and 2014

MOL Group Hellenic Petroleum PKN Orlen Tupras Total

Downstream - total -38% -23% 11% -36% -18% Downstream - organic -30% -23% 16% -29% -13% Refining -32% -36% 32% -29% -21% Retail & marketing 14% 0% 58% 33% Petrochemicals -48% 23% -9% -18%

Source: Company data, HSBC estimates

Of the four companies in this peer group PKN Orlen was the best downstream performer in 2007-2014,

having managed to sustain its earnings in the refining segment. This was partly helped by resilient fuel

demand in Poland where GDP continued to grow even during the 2007-2009 financial crisis and fuel

consumption rose by 18% during 2007-2011 while in Hungary, for instance, motor fuel demand fell by 11%.

29

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

The sector’s net debt declined since 2009 driven mainly by PKN Orlen’s and MOL’s debt repayments but rose at Tupras, USDm

2015e net debt to EBITDA ratios to remain relatively high at Hellenic Petroleum and Tupras

Source: Company data, HSBC estimates Source: Company data, HSBC estimates

Clean downstream LIFO EBITDA remains c14% lower than in 2007(9% organically), USDm

Capital expenditures should fall after one-offs in 2012-2015e, USDm

Source: Company data, HSBC estimates Source: Company data, HSBC estimates

Structure of CEEMEA refiners’ clean LIFO EBITDA in ’07-14, USDm*

PKN Orlen and Tupras have booked most of the downstream FCF in the peer group, USDm

Source: Company data, HSBC estimates; * excludes Tupras’ stake in Opet Source: Company data, HSBC estimates

-4,000-2,000

02,0004,0006,0008,000

10,00012,000

07 08 09 10 11 12 13 14 15e 16eMOL Group PKN Orlen Hellenic Petroleum Tupras

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Average MOLGroup

PKN Orlen HellenicPetroleum

Tupras

2014 2015e

-

1,000

2,000

3,000

4,000

5,000

6,000

07 08 09 10 11 12 13 14 15e 16e

MOL Group PKN Orlen Hellenic Petroleum Tupras

-

500

1,000

1,500

2,000

2,500

3,000

3,500

07 08 09 10 11 12 13 14 15e 16e

MOL Group PKN Orlen Hellenic Petroleum Tupras

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

07 08 09 10 11 12 13 14 15e 16e

Refining Petchem Retail

-3,000

-2,000

-1,000

-

1,000

2,000

3,000

07 08 09 10 11 12 13 14 15e 16e

MOL Group PKN Orlen Hellenic Petroleum Tupras

30

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

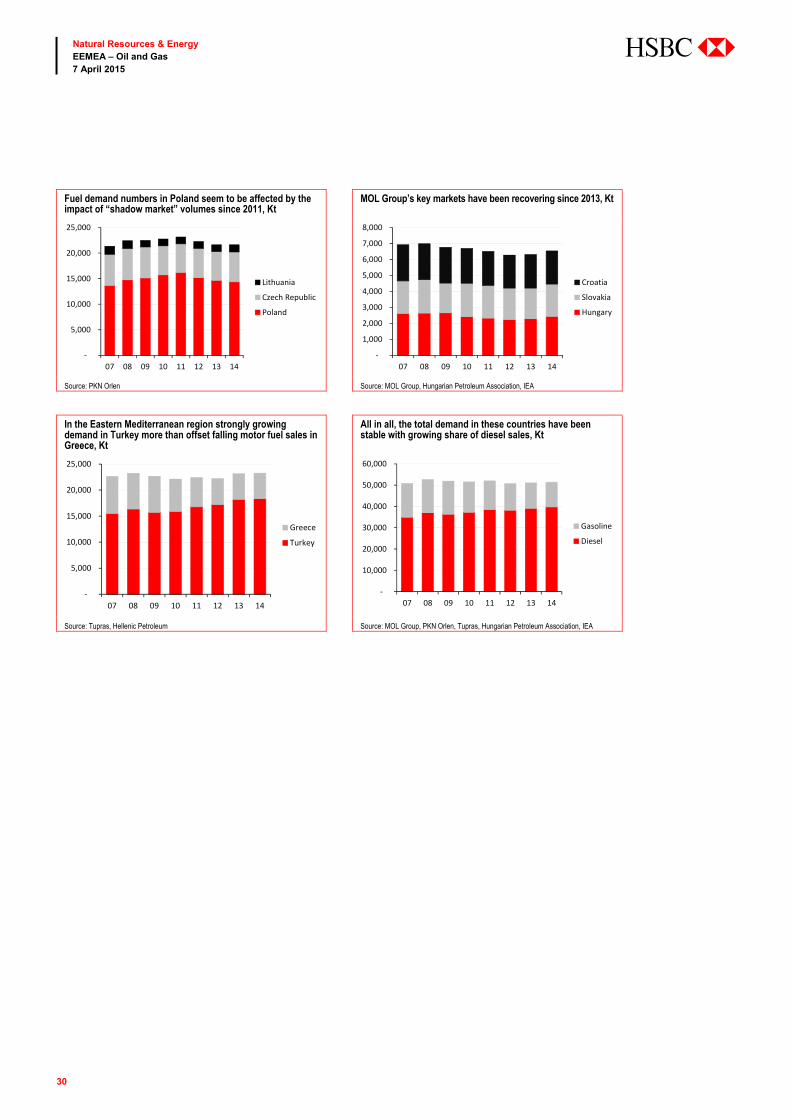

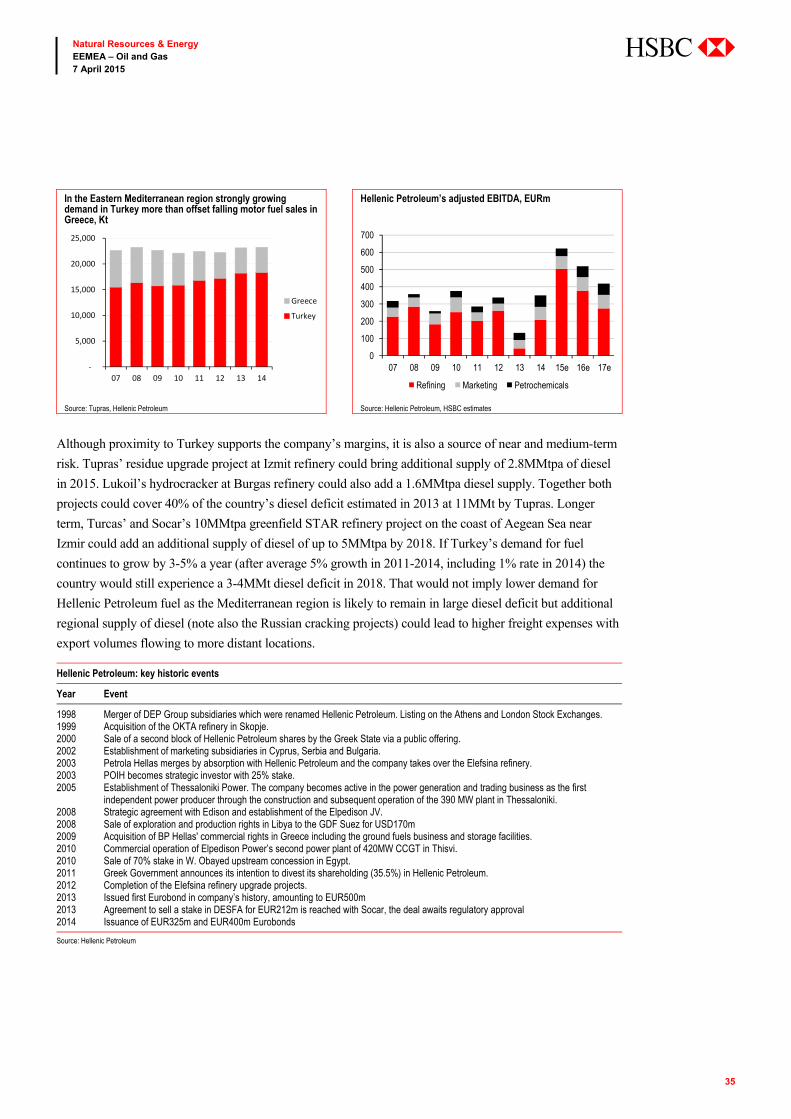

In the Eastern Mediterranean region strongly growing demand in Turkey more than offset falling motor fuel sales in Greece, Kt

All in all, the total demand in these countries have been stable with growing share of diesel sales, Kt

Source: Tupras, Hellenic Petroleum Source: MOL Group, PKN Orlen, Tupras, Hungarian Petroleum Association, IEA

-

5,000

10,000

15,000

20,000

25,000

07 08 09 10 11 12 13 14

Greece

Turkey

-

10,000

20,000

30,000

40,000

50,000

60,000

07 08 09 10 11 12 13 14

Gasoline

Diesel

Fuel demand numbers in Poland seem to be affected by the impact of “shadow market” volumes since 2011, Kt

MOL Group’s key markets have been recovering since 2013, Kt

Source: PKN Orlen Source: MOL Group, Hungarian Petroleum Association, IEA

-

5,000

10,000

15,000

20,000

25,000

07 08 09 10 11 12 13 14

Lithuania

Czech Republic

Poland

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

07 08 09 10 11 12 13 14

Croatia

Slovakia

Hungary

31

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

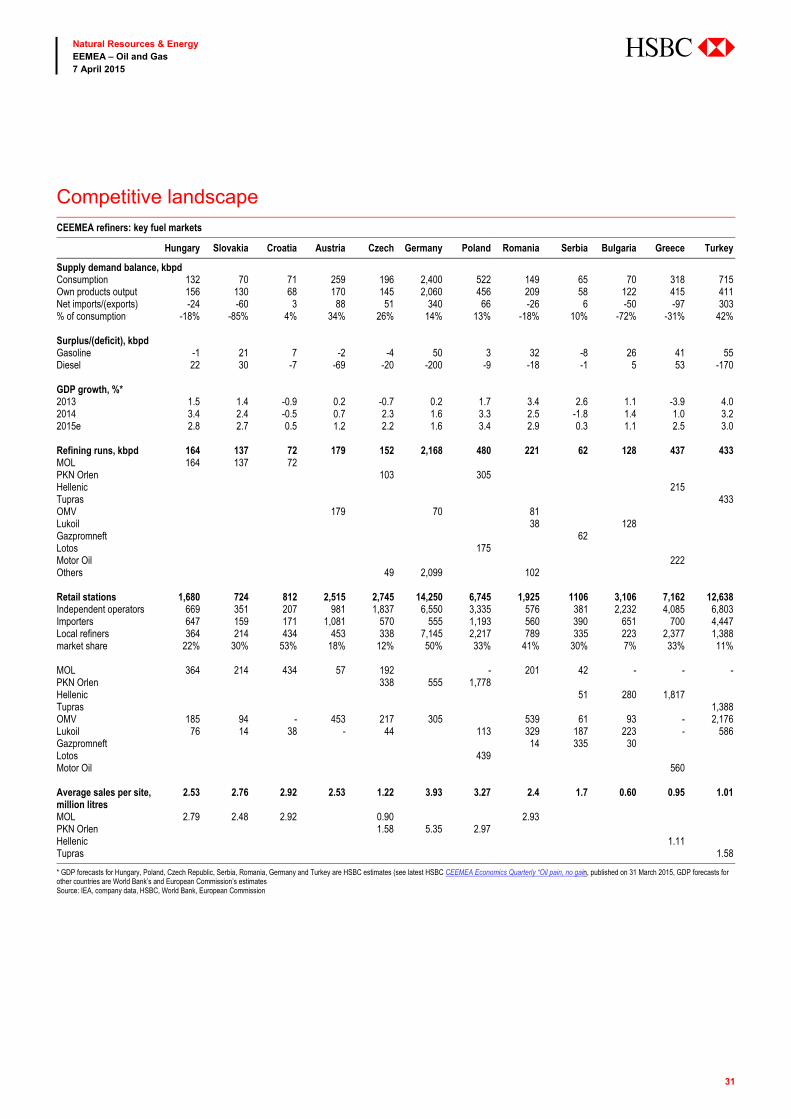

Competitive landscape CEEMEA refiners: key fuel markets

Hungary Slovakia Croatia Austria Czech Germany Poland Romania Serbia Bulgaria Greece Turkey

Supply demand balance, kbpd Consumption 132 70 71 259 196 2,400 522 149 65 70 318 715Own products output 156 130 68 170 145 2,060 456 209 58 122 415 411Net imports/(exports) -24 -60 3 88 51 340 66 -26 6 -50 -97 303% of consumption -18% -85% 4% 34% 26% 14% 13% -18% 10% -72% -31% 42% Surplus/(deficit), kbpd Gasoline -1 21 7 -2 -4 50 3 32 -8 26 41 55Diesel 22 30 -7 -69 -20 -200 -9 -18 -1 5 53 -170 GDP growth, %* 2013 1.5 1.4 -0.9 0.2 -0.7 0.2 1.7 3.4 2.6 1.1 -3.9 4.02014 3.4 2.4 -0.5 0.7 2.3 1.6 3.3 2.5 -1.8 1.4 1.0 3.22015e 2.8 2.7 0.5 1.2 2.2 1.6 3.4 2.9 0.3 1.1 2.5 3.0 Refining runs, kbpd 164 137 72 179 152 2,168 480 221 62 128 437 433 MOL 164 137 72 PKN Orlen 103 305 Hellenic 215 Tupras 433 OMV 179 70 81 Lukoil 38 128 Gazpromneft 62 Lotos 175 Motor Oil 222 Others 49 2,099 102 Retail stations 1,680 724 812 2,515 2,745 14,250 6,745 1,925 1106 3,106 7,162 12,638 Independent operators 669 351 207 981 1,837 6,550 3,335 576 381 2,232 4,085 6,803 Importers 647 159 171 1,081 570 555 1,193 560 390 651 700 4,447 Local refiners 364 214 434 453 338 7,145 2,217 789 335 223 2,377 1,388 market share 22% 30% 53% 18% 12% 50% 33% 41% 30% 7% 33% 11% MOL 364 214 434 57 192 - 201 42 - - -PKN Orlen 338 555 1,778 Hellenic 51 280 1,817 Tupras 1,388 OMV 185 94 - 453 217 305 539 61 93 - 2,176 Lukoil 76 14 38 - 44 113 329 187 223 - 586 Gazpromneft 14 335 30 Lotos 439 Motor Oil 560 Average sales per site, million litres

2.53 2.76 2.92 2.53 1.22 3.93 3.27 2.4 1.7 0.60 0.95 1.01

MOL 2.79 2.48 2.92 0.90 2.93 PKN Orlen 1.58 5.35 2.97 Hellenic 1.11 Tupras 1.58

* GDP forecasts for Hungary, Poland, Czech Republic, Serbia, Romania, Germany and Turkey are HSBC estimates (see latest HSBC CEEMEA Economics Quarterly “Oil pain, no gain, published on 31 March 2015, GDP forecasts for other countries are World Bank’s and European Commission’s estimates Source: IEA, company data, HSBC, World Bank, European Commission

32

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

Investment thesis

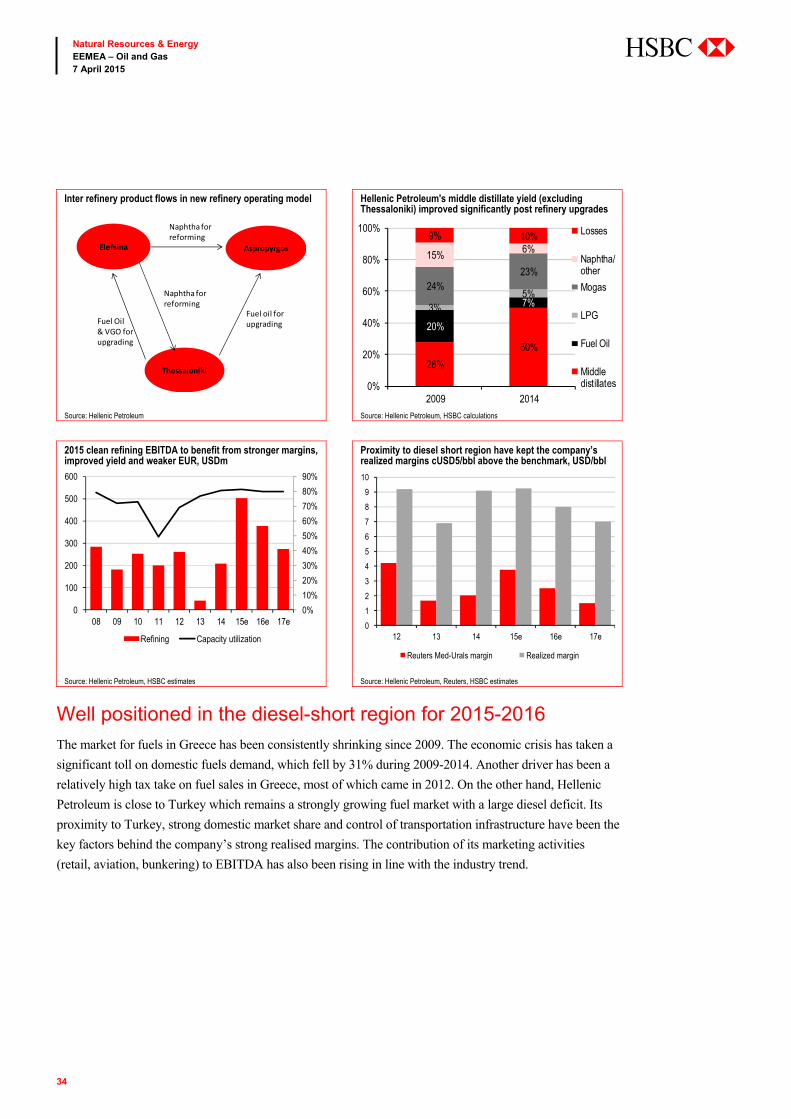

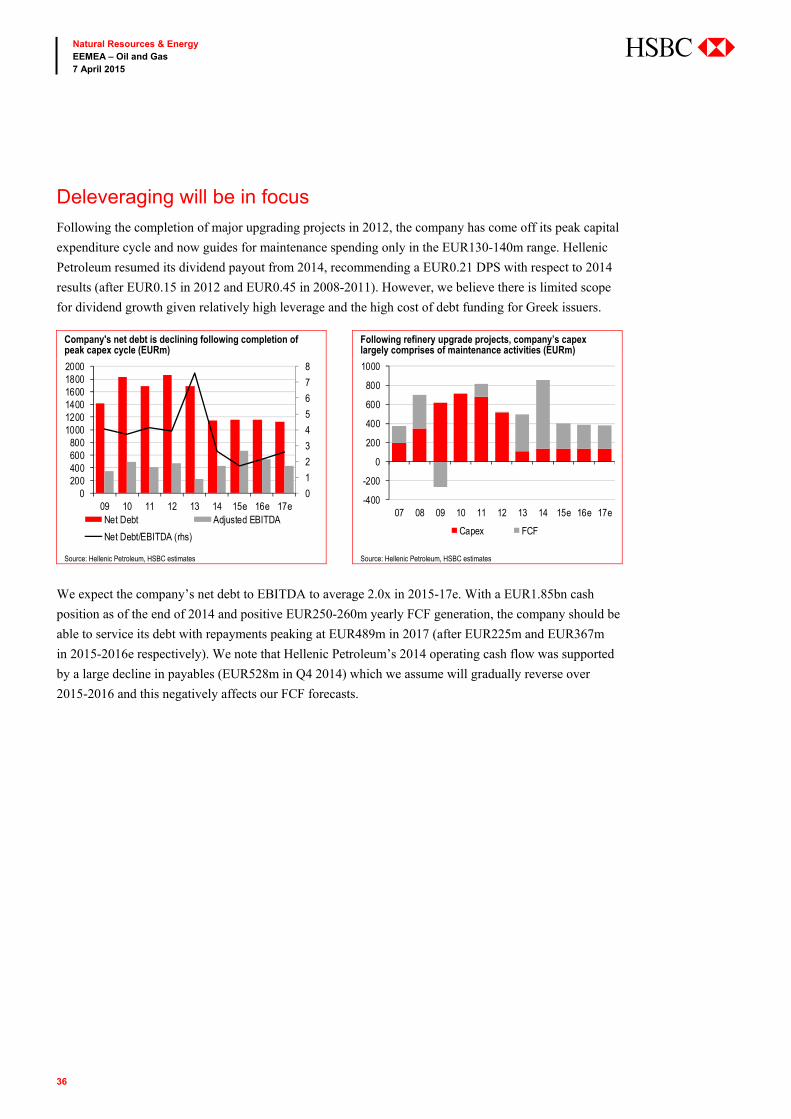

After completion of the Elefsina upgrade project the company has entered the delivery phase, which should

be supported by a recovery in refining margins and a weaker EUR. Although there are medium-term risks

from the additional supply of diesel to the region from 2017, Hellenic Petroleum’s margins should be

supported by its close proximity to the strongly growing fuel market of Turkey in 2015-16e. The company’s

EUR1.85bn cash position and EUR250-350m yearly FCF generation during the period leaves it with enough

resources to service its debt schedule in 2015-2018. The resumption of dividend payments (5.9% dividend

yield with respect to 2014 results) underscores the improved financial position of the company and makes

the stock an attractive value play, in our view, despite the political uncertainties in Greece,

Introducing Hellenic Petroleum

The largest refiner in Greece. Hellenic Petroleum is the largest refiner in Greece. The Greek

government owns a 35.5% stake and a 42.6% stake belongs to Pan-European Oil & Industrial Holdings

(POIH) owned by Spiro Latsis. The Greek government has mentioned plans to privatise its stake in the

company in the past and overhang risks should be mentioned but the timeline of the possible transaction

is very unclear.

The company operates three of the country’s four refineries that constitute 66% of Greece’s total refining

capacity. Two of Hellenic most complex and largest refineries in the south of the country – Aspropyrgos

and Elefsina – are located close to each other and are operated as an integrated “South Hub” with over

100% capacity utilisation in H2 2014. Its third refinery in Thessaloniki has no cracking capacity and

operates only when there is a favourable external environment with average capacity utilisation of 37% in

2014 (60% in Q4 2014). With a market share of c65%, Hellenic Petroleum has a leadership position in

the domestic fuel market where it competes with Motor Oil (not rated), which operates Greece’s largest

refinery (172kbpd). As Greek domestic demand has fallen by 42% since 2009, the country’s refining

sector has been increasingly export-oriented with Hellenic Petroleum’s export sales volumes reaching

50% in 2014 from 18% in 2009. Hellenic Petroleum also operates a 220Kpta polypropylene plant which

exports 50-60% of its output.

Hellenic Petroleum

The company is in the delivery phase following completion of the

Elefsina upgrade project, deleveraging will now be in focus

Weak domestic demand has been offset by growing export

supplies to the diesel short region but beware of mid-term risks

Initiate with Buy rating and EUR5.6 fair value target price

33

Natural Resources & Energy EEMEA – Oil and Gas 7 April 2015

abc

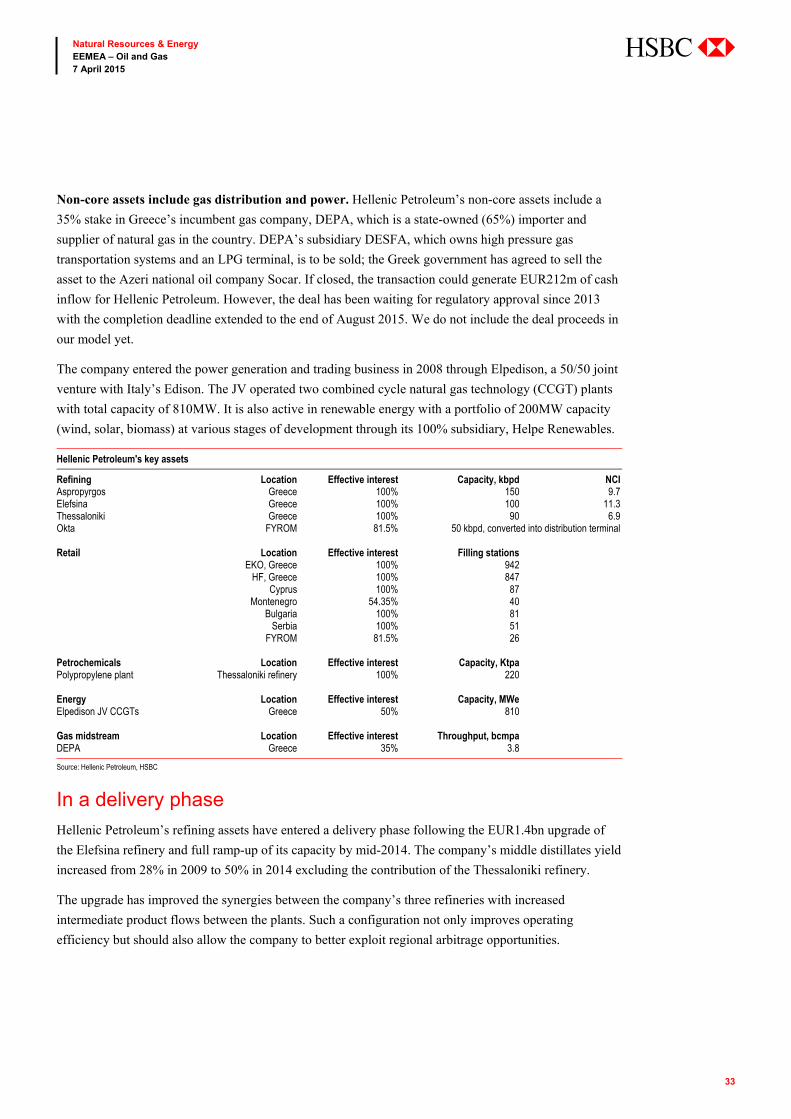

Non-core assets include gas distribution and power. Hellenic Petroleum’s non-core assets include a

35% stake in Greece’s incumbent gas company, DEPA, which is a state-owned (65%) importer and

supplier of natural gas in the country. DEPA’s subsidiary DESFA, which owns high pressure gas

transportation systems and an LPG terminal, is to be sold; the Greek government has agreed to sell the

asset to the Azeri national oil company Socar. If closed, the transaction could generate EUR212m of cash

inflow for Hellenic Petroleum. However, the deal has been waiting for regulatory approval since 2013

with the completion deadline extended to the end of August 2015. We do not include the deal proceeds in

our model yet.

The company entered the power generation and trading business in 2008 through Elpedison, a 50/50 joint

venture with Italy’s Edison. The JV operated two combined cycle natural gas technology (CCGT) plants