Embed Size (px)

DESCRIPTION

NCBFAA Government Affairs Conference September 24, 2007. Vessel Operators and Non-Vessel Operators: Partners or Adversaries in Contract Negotiation? Tim Perry APL, Ltd. AGENDA. Trade Outlook We’re in This Together Successes & Challenges Summary. Trade Outlook. - PowerPoint PPT Presentation

Citation preview

NCBFAA Government Affairs ConferenceSeptember 24, 2007

Vessel Operators and Non-Vessel Operators:

Partners or Adversariesin Contract Negotiation?

Tim PerryAPL, Ltd.

AGENDA

1. Trade Outlook2. We’re in This Together3. Successes & Challenges4. Summary

Trade Outlook

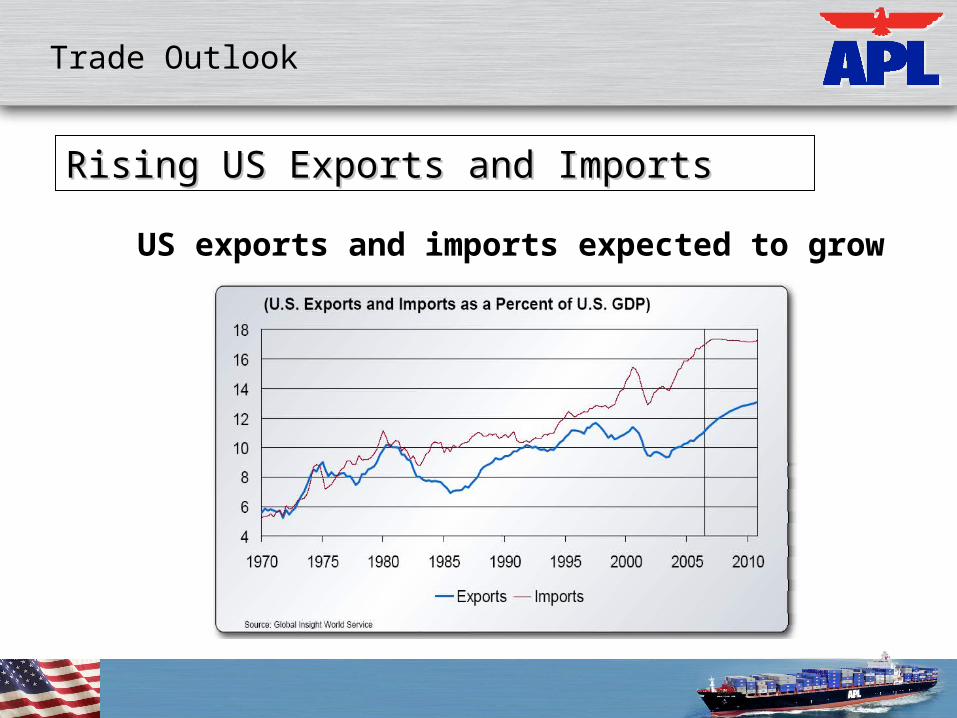

Rising US Exports and ImportsRising US Exports and Imports

US exports and imports expected to grow

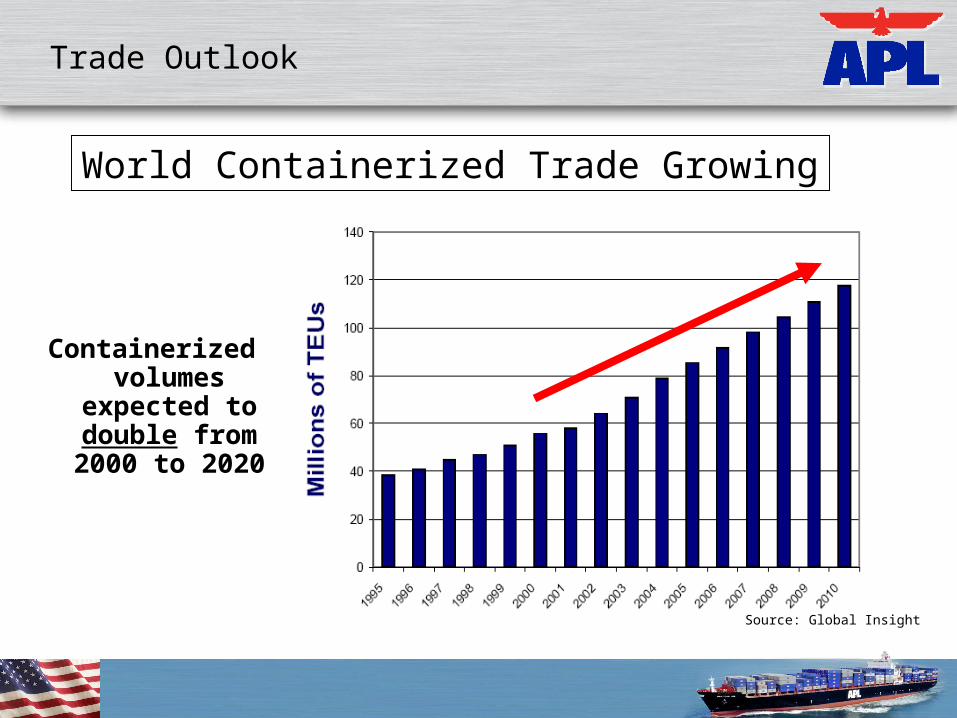

Trade Outlook

Containerized volumes expected

to double from 2000 to 2020

Source: Global Insight

World Containerized Trade Growing

Trade Outlook

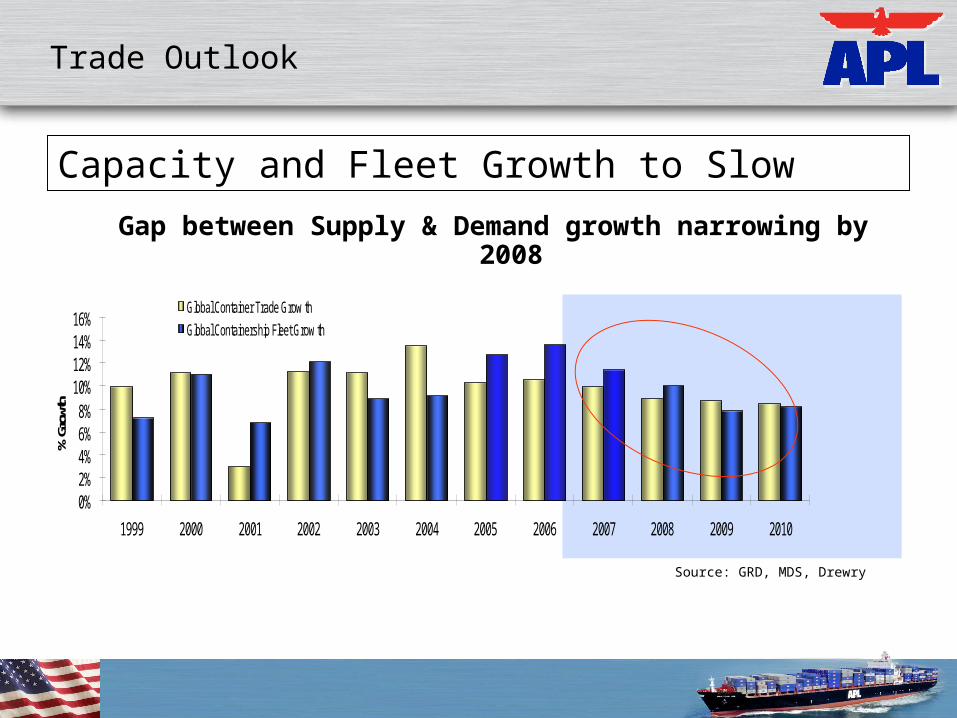

Capacity and Fleet Growth to Slow

Gap between Supply & Demand growth narrowing by 2008

Source: GRD, MDS, Drewry

0%2%4%6%8%

10%12%14%16%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

% Gr

owth

Global Container Trade Grow th

Global Containership Fleet Grow th

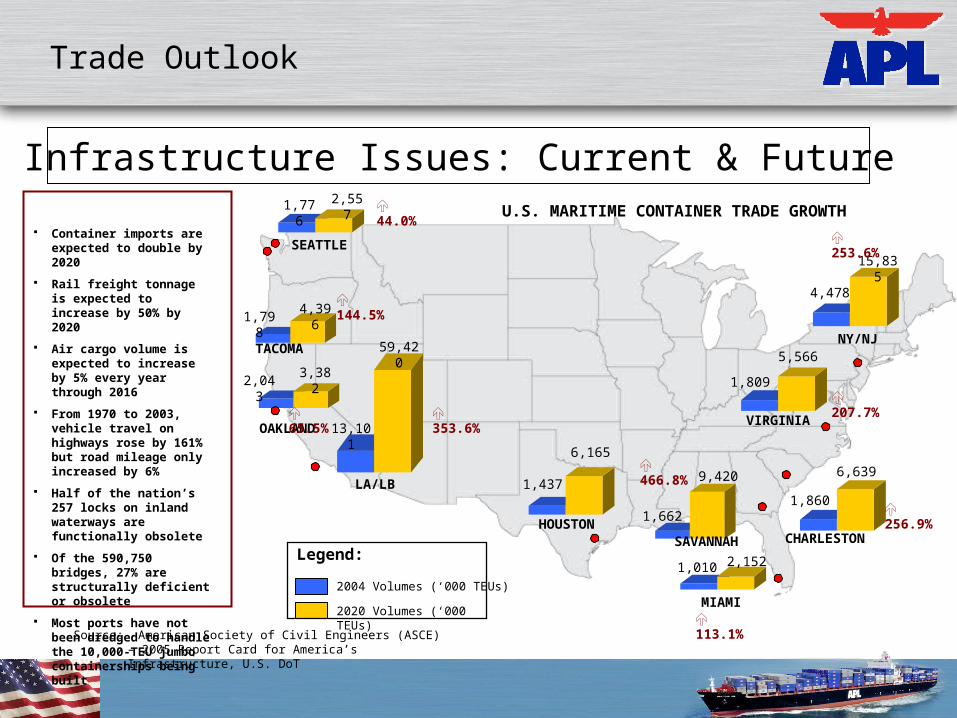

Trade Outlook

TACOMA

1,776 2,557

SEATTLE

1,7984,396

Container imports are expected to double by 2020

Rail freight tonnage is expected to increase by 50% by 2020

Air cargo volume is expected to increase by 5% every year through 2016

From 1970 to 2003, vehicle travel on highways rose by 161% but road mileage only increased by 6%

Half of the nation’s 257 locks on inland waterways are functionally obsolete

Of the 590,750 bridges, 27% are structurally deficient or obsolete

Most ports have not been dredged to handle the 10,000-TEU jumbo containerships being built

OAKLAND

2,0433,382

LA/LB

13,101

59,420

HOUSTON

1,437

6,165

2,1521,010

MIAMI

SAVANNAH

1,662

9,420

CHARLESTON

1,860

6,639

VIRGINIA

1,809

5,566NY/NJ

4,478

15,835

2004 Volumes (‘000 TEUs)

2020 Volumes (‘000 TEUs)

Legend:

U.S. MARITIME CONTAINER TRADE GROWTH

Source: American Society of Civil Engineers (ASCE) – 2005 Report Card for America’s Infrastructure, U.S. DoT

44.0%

144.5%

65.5% 353.6%

113.1%

256.9%

253.6%

207.7%

466.8%

Trade Outlook

Infrastructure Issues: Current & Future

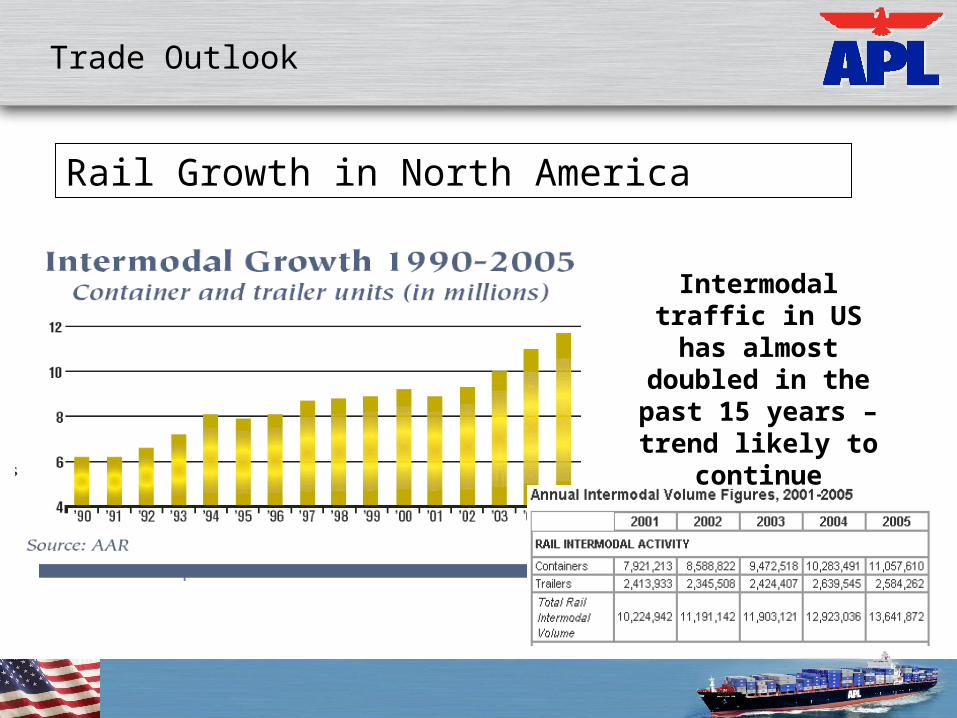

Rail Growth in North America

Intermodal traffic in US has almost

doubled in the past 15 years – trend likely to continue

Trade Outlook

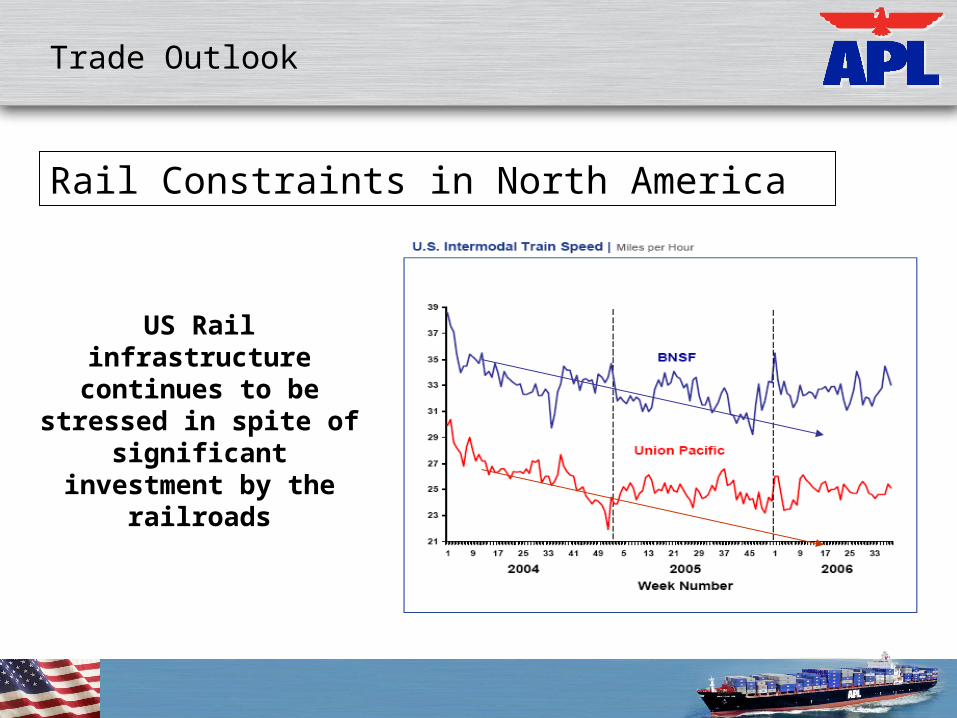

Rail Constraints in North America

US Rail infrastructure continues to be stressed

in spite of significant investment by the

railroads

Trade Outlook

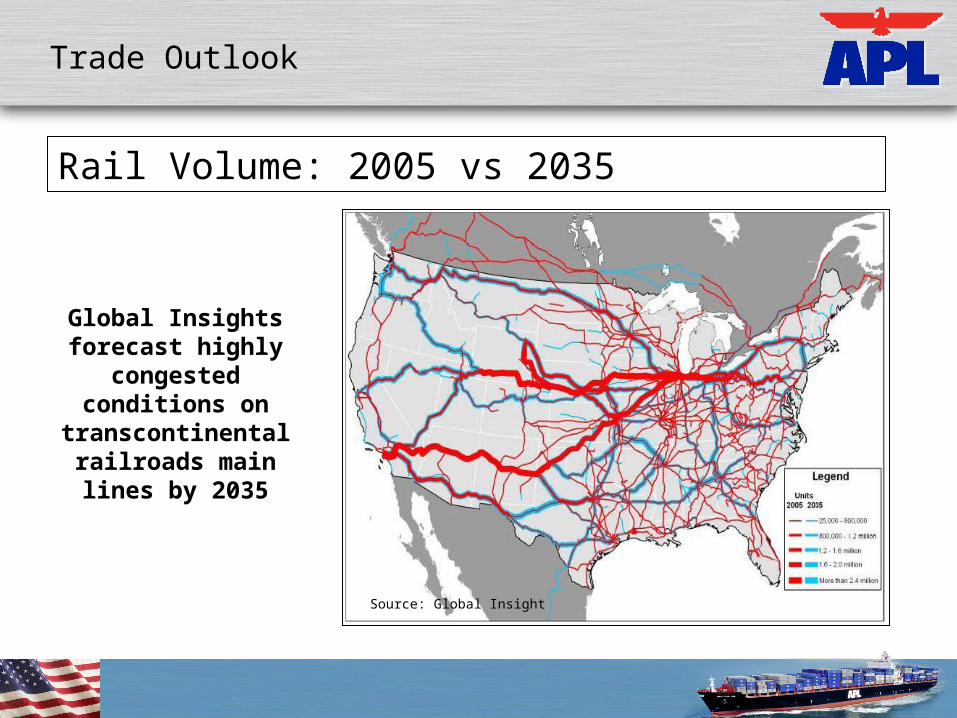

Global Insights forecast highly

congested conditions on

transcontinental railroads main lines

by 2035

Rail Volume: 2005 vs 2035

Source: Global Insight

Trade Outlook

Trade Outlook

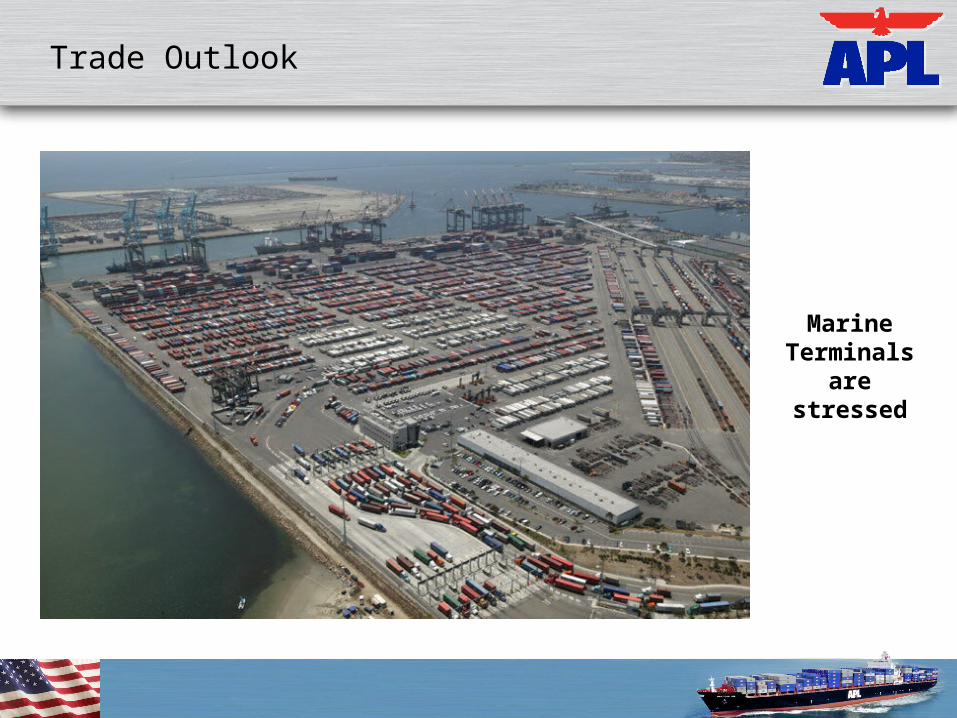

Marine Terminals are

stressed

Port of Long Beach

2004

Trade Outlook

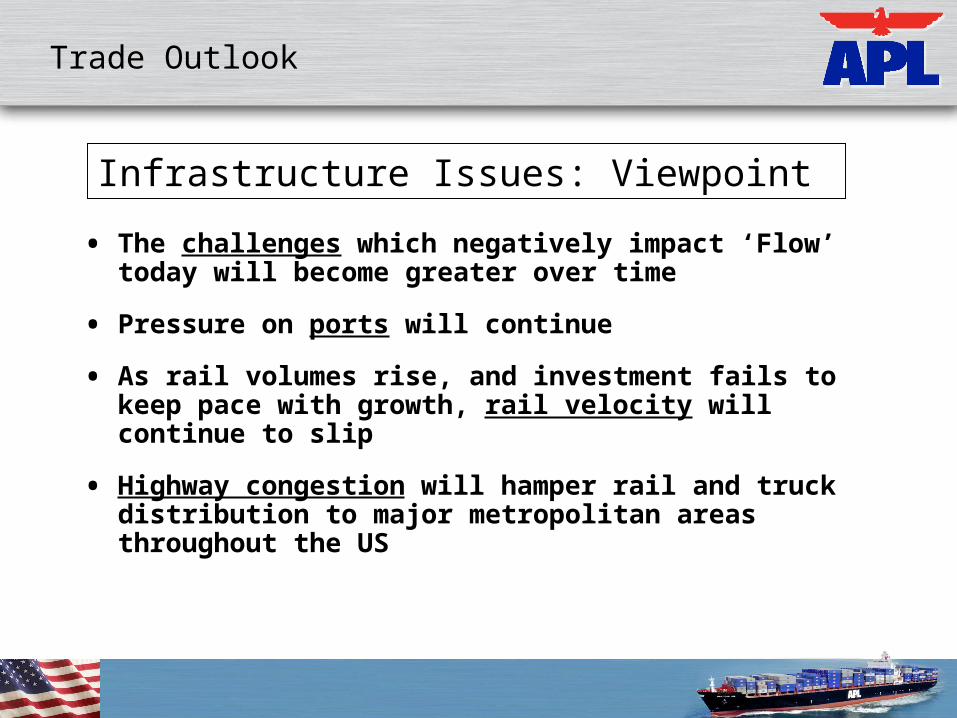

Infrastructure Issues: Viewpoint

• The challenges which negatively impact ‘Flow’ today will become greater over time

• Pressure on ports will continue

• As rail volumes rise, and investment fails to keep pace with growth, rail velocity will continue to slip

• Highway congestion will hamper rail and truck distribution to major metropolitan areas throughout the US

Trade Outlook

We’re All In This Together

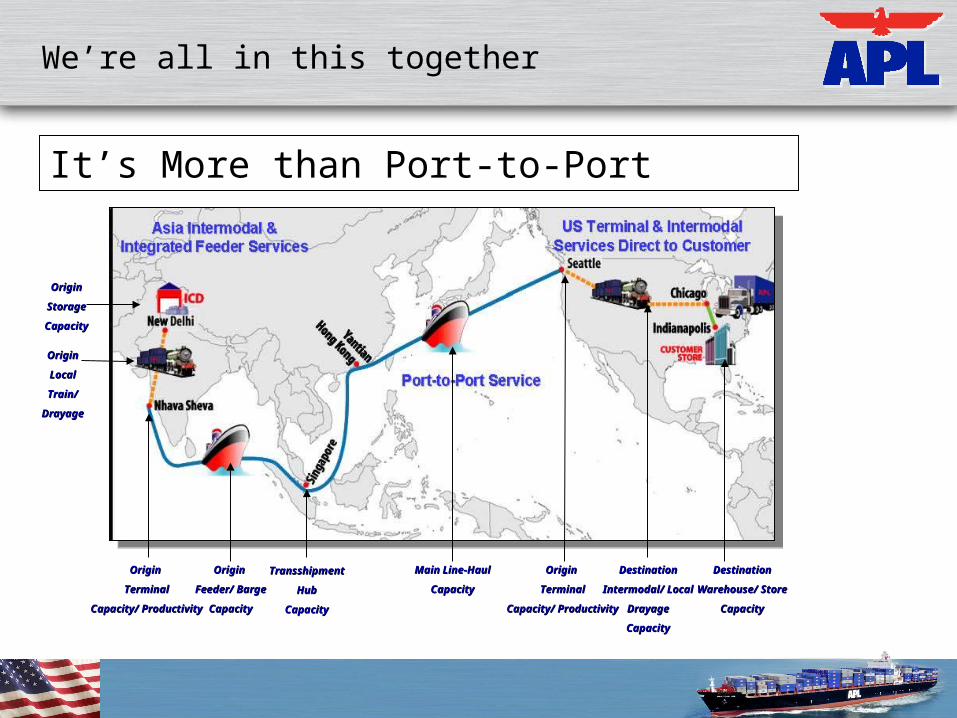

It’s More than Port-to-Port

OriginOrigin

LocalLocal

Train/Train/

DrayageDrayage

Origin Origin

Feeder/ BargeFeeder/ Barge

CapacityCapacity

Main Line-HaulMain Line-Haul

CapacityCapacity

DestinationDestination

Intermodal/ LocalIntermodal/ Local

DrayageDrayage

CapacityCapacity

Origin Origin

TerminalTerminal

Capacity/ ProductivityCapacity/ Productivity

Origin Origin

TerminalTerminal

Capacity/ ProductivityCapacity/ Productivity

DestinationDestination

Warehouse/ StoreWarehouse/ Store

CapacityCapacity

TransshipmentTransshipment

HubHub

CapacityCapacity

OriginOrigin

StorageStorage

CapacityCapacity

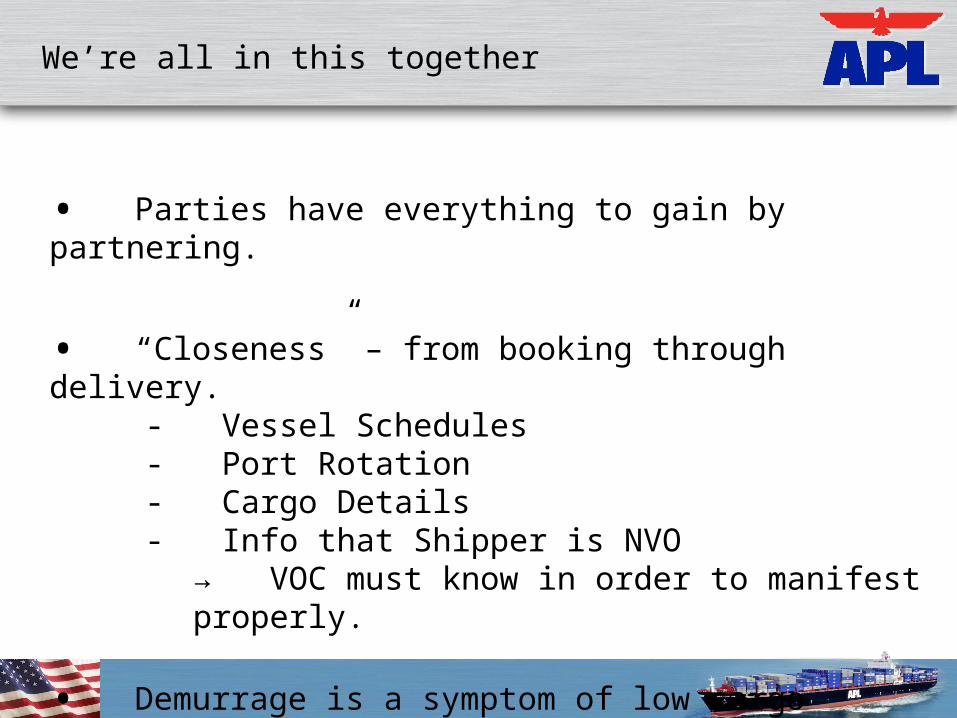

We’re all in this together

• Parties have everything to gain by partnering.

• “Closeness” – from booking through delivery.- Vessel Schedules- Port Rotation- Cargo Details- Info that Shipper is NVO

→ VOC must know in order to manifest properly.

• Demurrage is a symptom of low cargo velocity.

We’re all in this together

Successes and Challenges

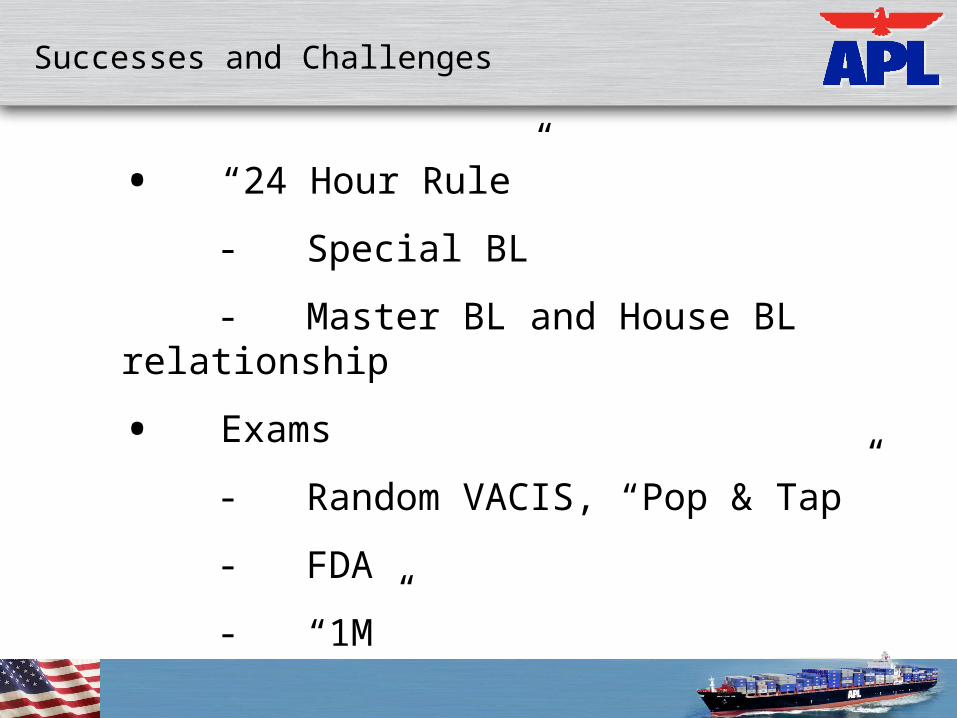

• “24 Hour Rule”

- Special BL

- Master BL and House BL relationship

• Exams

- Random VACIS, “Pop & Tap”

- FDA

- “1M”

Successes and Challenges

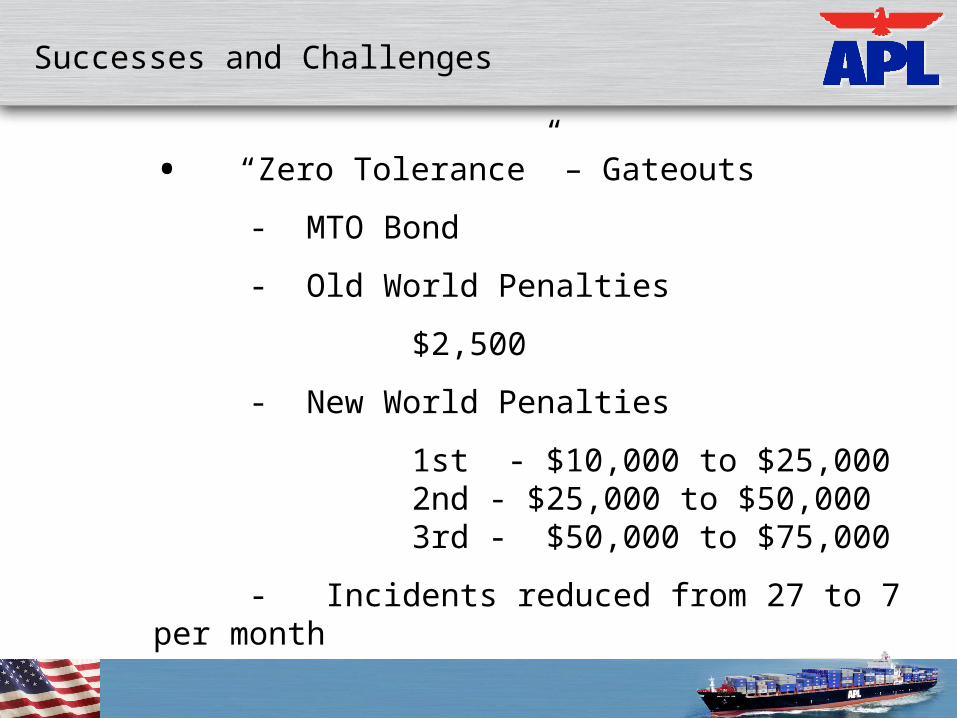

• “Zero Tolerance” – Gateouts

- MTO Bond

- Old World Penalties

$2,500

- New World Penalties

1st - $10,000 to $25,000 2nd - $25,000 to $50,000 3rd - $50,000 to $75,000

- Incidents reduced from 27 to 7 per month

Successes and Challenges

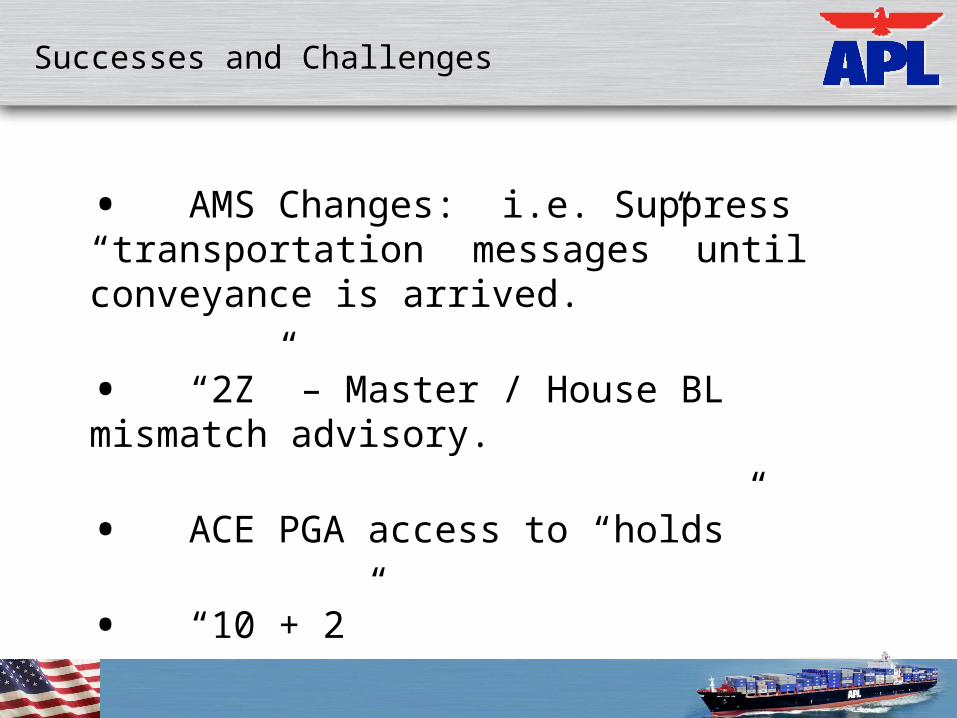

• AMS Changes: i.e. Suppress “transportation messages” until conveyance is arrived.

• “2Z” – Master / House BL mismatch advisory.

• ACE PGA access to “holds”

• “10 + 2”

Successes and Challenges

Summary

• Know your partners

• Communicate

- CESAC

- NCBFAA Customs Committee

- NCBFAA Legislative Advocacy

- Ocean Carrier Best Practice Committee

- COAC

- Trade Support Network

- TOPAS

Thank you.

Tim PerryAPL, Ltd.1667 K Street NW, Suite 400Washington, DC 20006

[email protected] 202.496.2482

NCBFAA Government Affairs ConferenceSeptember 24, 2007