Embed Size (px)

Citation preview

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the

instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-

926-7926 ext. 10.

Presenting a live 90-minute webinar with interactive Q&A

Negotiating Covenants and Closing Conditions

in M&A Transactions: Practical Tactics and Techniques Crafting Provisions that Protect Buyer and Seller Interests and Minimize Legal Disputes

Today’s faculty features:

WEDNESDAY, SEPTEMBER 9, 2015

Martin B. Robins, Esq., Member, FisherBroyles, Chicago

Samuel M. Shafner, Member, FisherBroyles, Boston

Michael M. Sullivan, Member, Taylor English Duma, Atlanta

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-888-450-9970 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your participation in this

webinar by completing and submitting the Attendance Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email that you will receive

immediately following the program.

For additional information about CLE credit processing call us at 1-800-926-7926 ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-hand column on your

screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's

program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

NEGOTIATING COVENANTS AND CLOSING CONDITIONS IN M&A TRANSACTIONS: PRACTICAL TACTICS AND TECHNIQUES

We d ne s d ay, S e ptember 9 , 2 0 1 5

00623964.PPTX 5

Faculty Martin B. Robins, Esq., Member

FisherBroyles, Chicago

Mr. Robins practices extensively in the general corporate and corporate governance, M&A, finance, intellectual property (including licensing, compliance and DMCA) and information technology/data security areas.

He represents public and private clients of all sizes and in all industries ranging from Fortune 50 multinational firms to substantial private companies to start-ups to individual executives.

His work encompasses transactions of all sizes and covers a wide array of transactions including business acquisitions, shareholder buy/sell agreements bank and similar financing, software licenses and computer/telecom hardware procurements, joint ventures, equipment and real estate leases, patent licenses, outsourcing and managed service contracts.

He also publishes extensively in a number of legal journals and presents at legal conferences.

Contact Information: FisherBroyles 203 N. LaSalle Street, Suite 2100, Chicago, IL 60010 Direct: 847.277.2580 Email: [email protected] Web: www.fisherbroyles.com

6 00623964.PPTX

Faculty Samuel M. Shafner, Member

FisherBroyles, Boston

Mr. Shafner is a business, corporate and securities lawyer for over 25 years.

His clients range from young startups to major publicly traded companies, counseling them in both routine and extraordinary business transactions, as well as in launching new businesses, strategic partnerships and investments, acquisitions and divestitures, securities law, corporate governance, and all manner of business and transactional legal work.

A large portion of his clients are international, located in Canada, Western Europe and Israel.

He is a frequent writer and public speaker at conferences all over the world on M&A and finance topics.

Contact Information: FisherBroyles 470 Atlantic Avenue, 4th Floor, Boston, MA 02210 Direct: 781.821.0410 Email: [email protected] Web: www.fisherbroyles.com

7 00623964.PPTX

Faculty Michael M. Sullivan, Member

Taylor English Duma, Atlanta

Mr. Sullivan’s principal areas of concentration include general corporate, commercial and business matters, family-business law, financial matters, and mergers and acquisitions.

He assist clients in negotiating all forms of complex corporate and commercial agreements and contracts, shareholder and buy-sell agreements, customer and vendor agreements, employment, independent contractor and work for hire agreements, non-compete agreements, and non-disclosure agreements.

He advises U.S. clients on their legal structure and other matters when entering new International markets, and has negotiated numerous cross-border transactions for U.S. clients.

Contact Information: Taylor English Duma LLP 1600 Parkwood Circle, Suite 400 Atlanta, GA 30339 Direct: 770.434.1567 Email: [email protected] Web: www.taylorenglish.com

8 00623964.PPTX

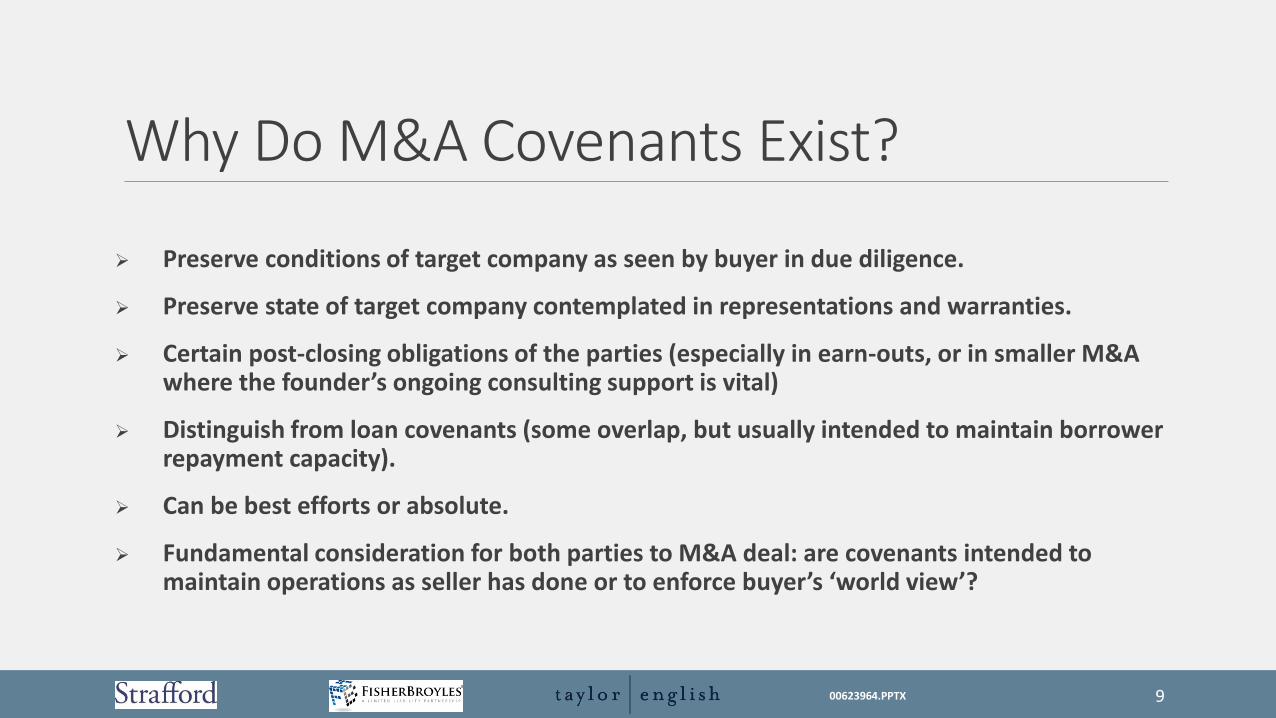

Why Do M&A Covenants Exist?

Preserve conditions of target company as seen by buyer in due diligence.

Preserve state of target company contemplated in representations and warranties.

Certain post-closing obligations of the parties (especially in earn-outs, or in smaller M&A where the founder’s ongoing consulting support is vital)

Distinguish from loan covenants (some overlap, but usually intended to maintain borrower repayment capacity).

Can be best efforts or absolute.

Fundamental consideration for both parties to M&A deal: are covenants intended to maintain operations as seller has done or to enforce buyer’s ‘world view’?

9 00623964.PPTX

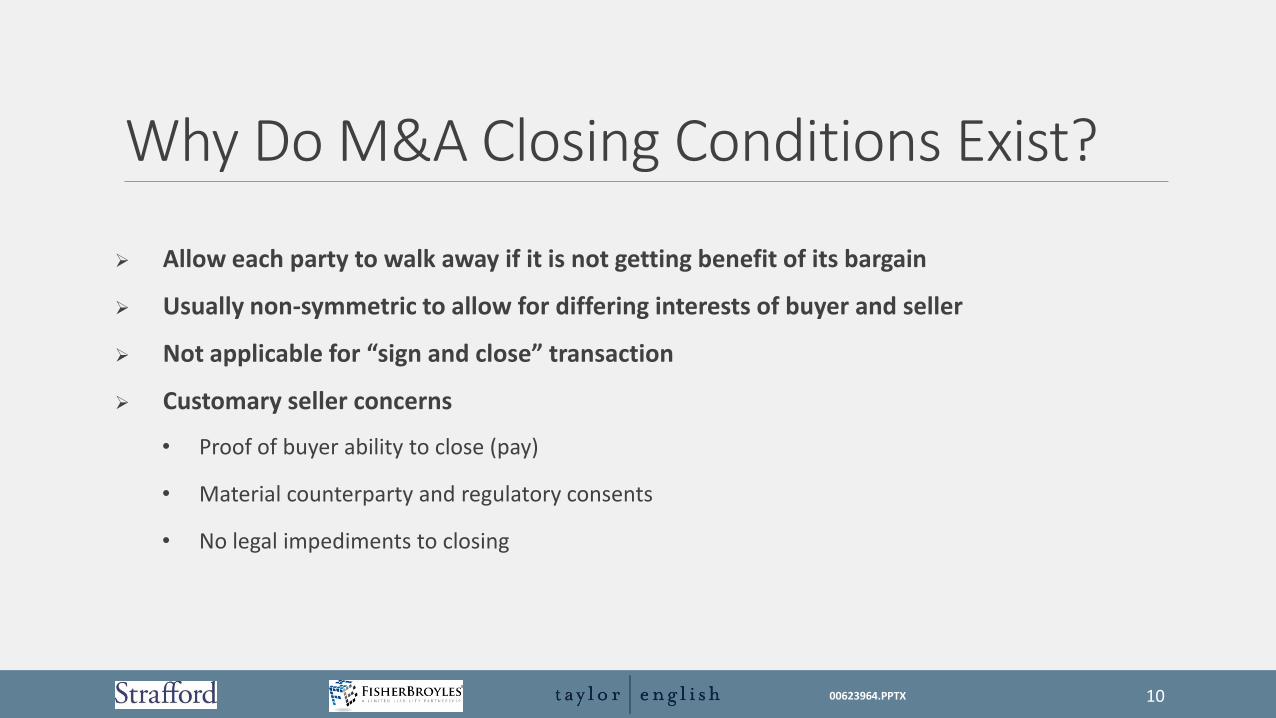

Why Do M&A Closing Conditions Exist?

Allow each party to walk away if it is not getting benefit of its bargain

Usually non-symmetric to allow for differing interests of buyer and seller

Not applicable for “sign and close” transaction

Customary seller concerns

• Proof of buyer ability to close (pay)

• Material counterparty and regulatory consents

• No legal impediments to closing

10 00623964.PPTX

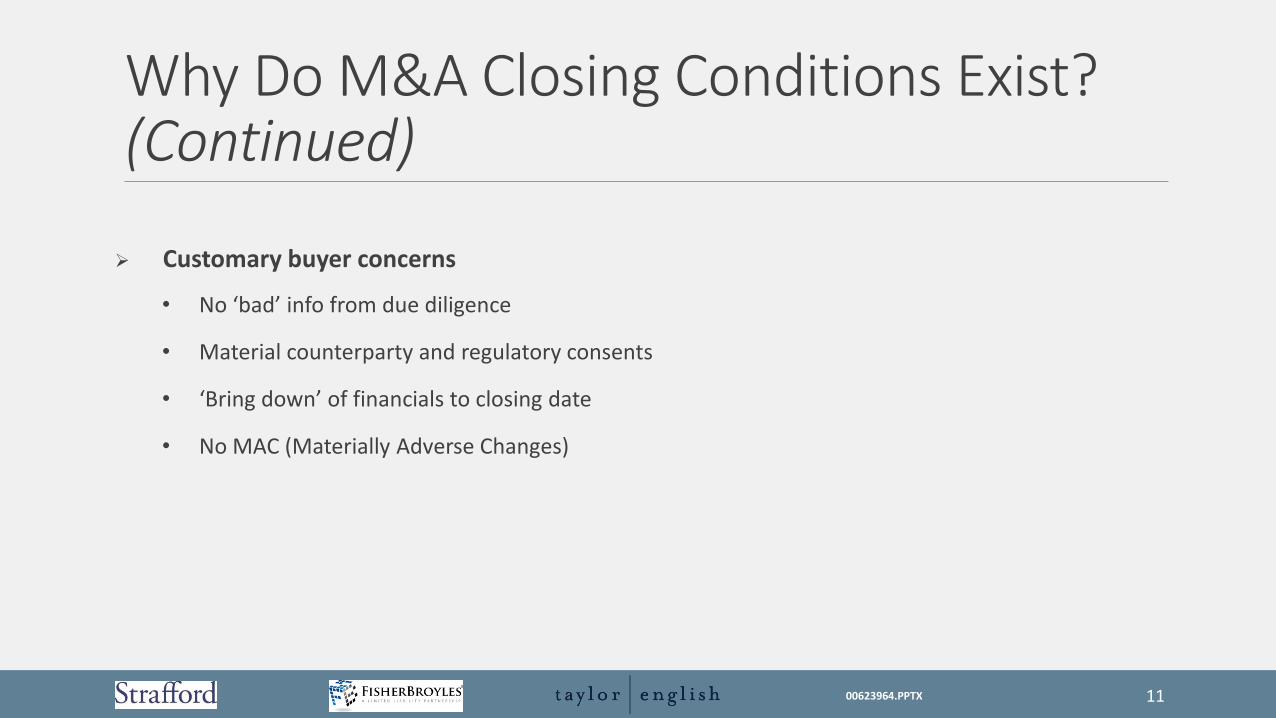

Why Do M&A Closing Conditions Exist? (Continued)

Customary buyer concerns

• No ‘bad’ info from due diligence

• Material counterparty and regulatory consents

• ‘Bring down’ of financials to closing date

• No MAC (Materially Adverse Changes)

00623964.PPTX 11

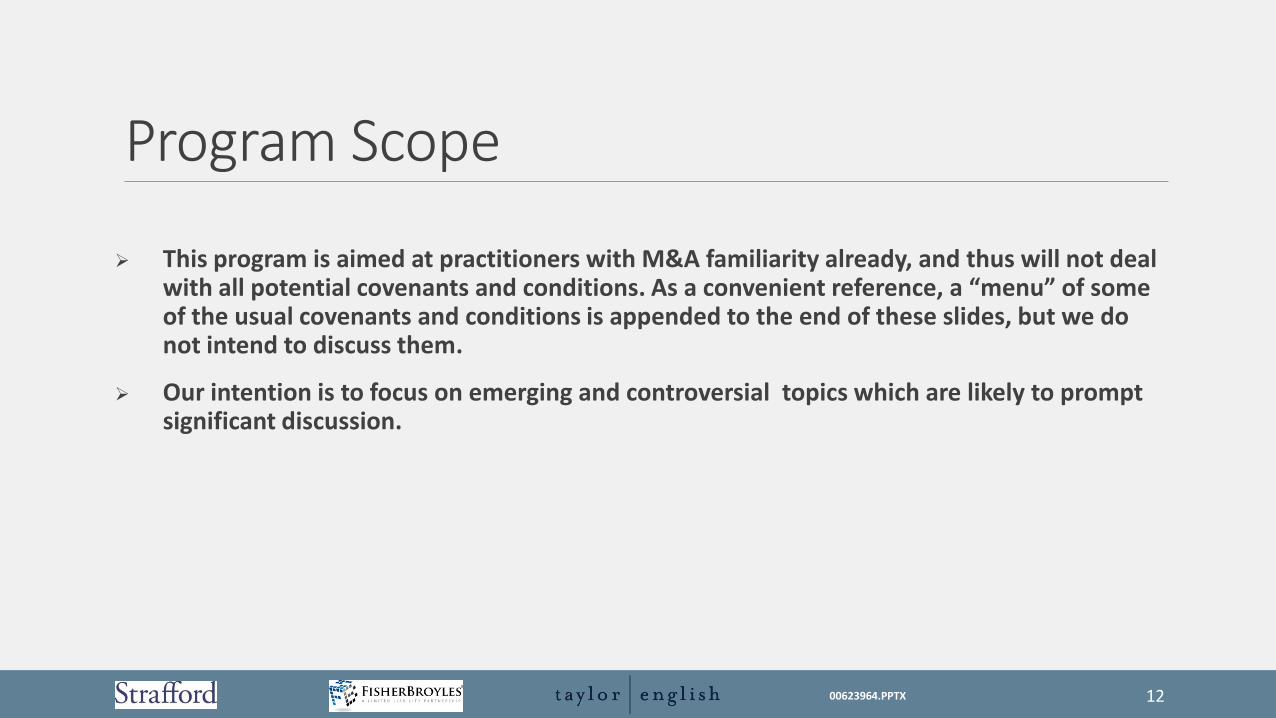

Program Scope

This program is aimed at practitioners with M&A familiarity already, and thus will not deal with all potential covenants and conditions. As a convenient reference, a “menu” of some of the usual covenants and conditions is appended to the end of these slides, but we do not intend to discuss them.

Our intention is to focus on emerging and controversial topics which are likely to prompt significant discussion.

12 00623964.PPTX

Public vs Private Company Distinctions

‘34 Act compliance, substantive and procedural (review by buyer during gap period?)

‘33 Act compliance if new financings permitted at all (incl. S-8’s)

Exchange and NASDAQ obligations

Corporate obligations, substantive and procedural including potential fiduciary outs (‘go shop’ and ‘no shop’) to allow consideration of other offers which may be preferable for shareholders

00623964.PPTX 13

One Holder or Very Closely Held Targets vs “Diffuse” Private Targets

Procedural compliance with statute and organic documents/corporate mechanics matters more, the more diffuse is the target

Ability to consider other offers more important for more diffuse ownership situations

If any private Reg D or other financings have been done within six months of proposed closing, this may trigger discussion of need for covenants or closing conditions aimed at preventing inadvertent public offering for which buyer could be liable

00623964.PPTX 14

Covenants:

1. Post-Closing Consulting:

For small companies, often the cooperation of the founder is key to its continuing success.

The buyer depends upon a smooth handoff. Yet the founder is selling precisely because he wants out!

How do you make the commitment real and concrete, without violating the 13th Amendment (slavery)?

What consequences make sense to impose?

15 00623964.PPTX

Covenants:

2. Transitional Services Agreement for Purchases of Divisions and Subsidiaries:

Where the buyer is buying a division of the seller, and both buyer and seller are ongoing businesses, delicate issues can arise where transitional services are needed.

Confidentiality can be an issue, as can pricing, especially beyond a certain point in time.

Most of all, how can the buyer protect itself from leakage of confidential knowledge into the service provider, which then can be used to advantage by the seller.

Obviously this is especially problematic where buyer and seller are to some extent competitive (e.g., where buyer buys one geographic market from seller).

16 00623964.PPTX

Covenants:

3. Ongoing Accounting, Tax and Financial Covenants:

Between signing and closing (and, where seller’s business is ongoing, even after the closing), to what extent may buyer decide for seller how the financial data will be presented, and tax elections will be made?

17 00623964.PPTX

Covenants:

4. Intellectual Property Maintenance:

Especially for tech companies.

Is seller required to continue R&D operations prior to closing?

Must seller file patents then (especially dealing with provisionals whose 12 month period ends between signing and closing)?

If so, who pays?

Similar issue with other forms of IP.

18 00623964.PPTX

Covenants:

5. Intellectual Property Rights and Duties:

If buyer or seller innovate post-signing (or even post-closing), are there grants-back of IP rights?

If so, how do the parties divide the rights, and who pays for what (both in terms of R&D expense sharing, and legal and other costs of IP filing etc.)?

Notification of R&D advances; when?

Notification of infringing parties?

Must patent holder join with its licensee to enforce the patent against infringers?

Who pays?

If damages are awarded, how are they shared?

19 00623964.PPTX

Covenants:

6. Registration Rights and Rule 144 Covenants:

Where stock is part of the consideration, how do we keep it meaningful and give the seller the liquidity it needs?

After all, the seller is an “unwilling investor” in the buyer, and so should have his investment risk as moderate as possible.

What consequences if Rule 144 is unavailable because the buyer fails to file his ’34 Act reports on time or is not public?

20 00623964.PPTX

Covenants:

6. Registration Rights and Rule 144 Covenants (Continued):

Seller needs to understand the risk of taking back stock in a private buyer as part of the sale consideration, without the assurance of liquidity:

If buyer is a private company and seller is receiving substantial buyer stock as all or part of the consideration, seller should consider demanding a "registration covenant" forcing buyer to go public to allow liquidity to seller.

If buyer is or is, or will be going, public, and new shares granted to seller as consideration are restricted, seller should consider a Rule 144 compliance covenant, assuring seller of legal right to sell shares in public market.

Alternatively, seller could have a “put clause” in the transaction documents under which seller may put buyer’s stock back to buyer at appraised value or on some other value basis:

− There can be a holding period during which seller cannot exercise the “put”.

− Seller needs to address buyer’s financial capability to perform put.

21 00623964.PPTX

Conditions

1. Verification of Key Customer Relationships; Termination of Disadvantageous Ones:

When a key part of the sales pitch has been the seller’s ongoing business with a few key customers/distributors, the buyer wants to be sure that the relationship with these folks is sound.

But the seller naturally does not want to allow those customers/distributors to know that the seller is for sale, lest the sale fall through and the relationship be damaged.

How can such a condition be negotiated to satisfy both parties’ needs?

22 00623964.PPTX

Conditions

1. Verification of Key Customer Relationships; Termination of Disadvantageous Ones (Continued):

Also, on the flip side of that, if a buyer doesn’t like a distributorship or franchisee situation, can the seller agree to user his best efforts terminate it post-closing, if the seller otherwise has the right to do so, or might arguably have that right?

Or does “tortious interference with a contractual relationship” prevent this?

How does one deal with pre-existing baggage that the buyer wants to avoid?

23 00623964.PPTX

Conditions

2. Absence of Material Adverse Change:

At what point, when deviation from representations gets too wide, can buyer instead decide to not buy?

And at what point can seller decide not to sell?

How to factor out intervening market conditions, which may provide an “ulterior motive” for either?

How is “MAC” defined: with reference to the seller, its industry, the national or global economy, or some combination of all of them?

24 00623964.PPTX

Conditions

3. Key Employees Staying: When are they told?

What about buyer wanting to interview them?

What conditions can be crafted to anticipate their responses, and to classify them in terms of degree of willingness to stay on?

What consequence to seller if they leave within a given time after the closing?

25 00623964.PPTX

Conditions

4. Financing Contingency:

How to keep it fair, so that it doesn’t amount to a unilateral “escape clause” for the buyer, but still cover the buyer for bona fide financing problems (think October 2008).

Obligation to pursue with due diligence and accept proffered financing meeting specified criteria – e.g., interest rate or preferred dividend, terms and amortization schedule, limitations on voting, etc.

26 00623964.PPTX

Conditions

5. Fiduciary Out:

With very large public companies, the obligations of Revlon and progeny are well known.

But with a smaller public company, is there a different standard as to when the company is truly “in play”?

How far does the Board need to go, in terms of seeking bids?

How do we keep the buyer’s advantage meaningful?

27 00623964.PPTX

Conditions

6. Stockholder Approval Threshold:

How high is high enough?

Appraisal rights concern.

Possible solutions: special escrow for dissenters?

28 00623964.PPTX

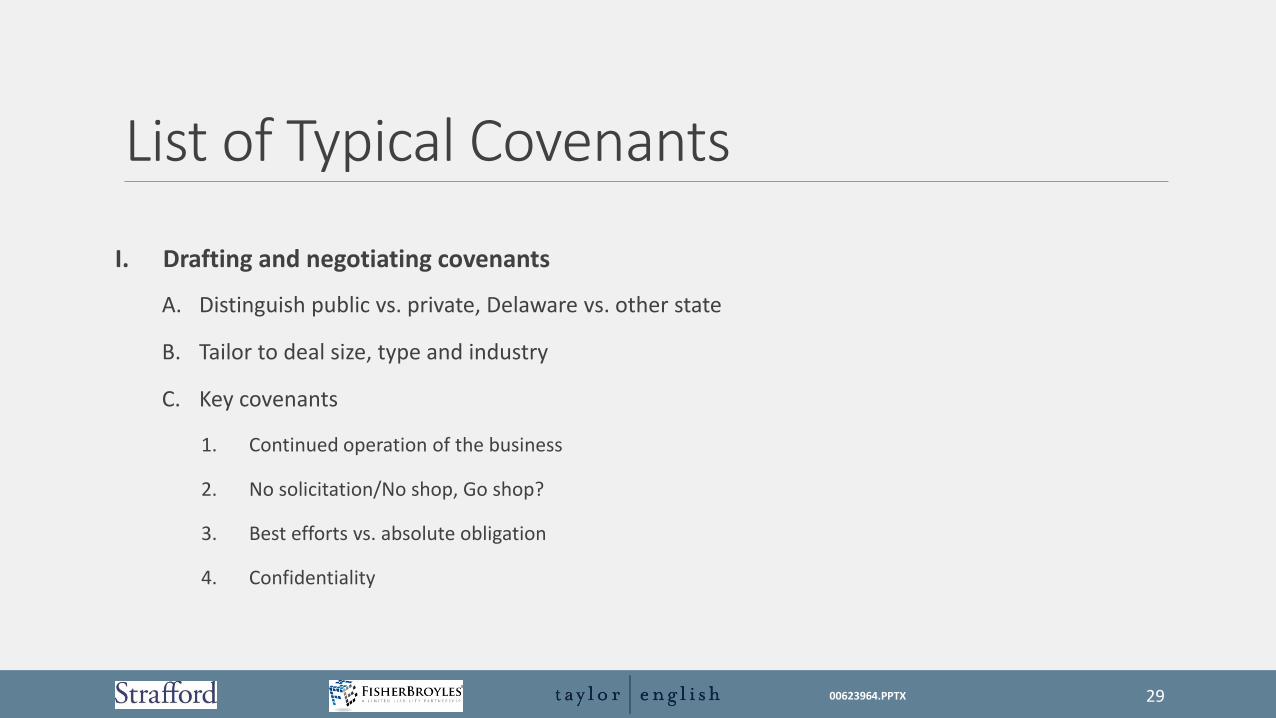

List of Typical Covenants

I. Drafting and negotiating covenants

A. Distinguish public vs. private, Delaware vs. other state

B. Tailor to deal size, type and industry

C. Key covenants

1. Continued operation of the business

2. No solicitation/No shop, Go shop?

3. Best efforts vs. absolute obligation

4. Confidentiality

29 00623964.PPTX

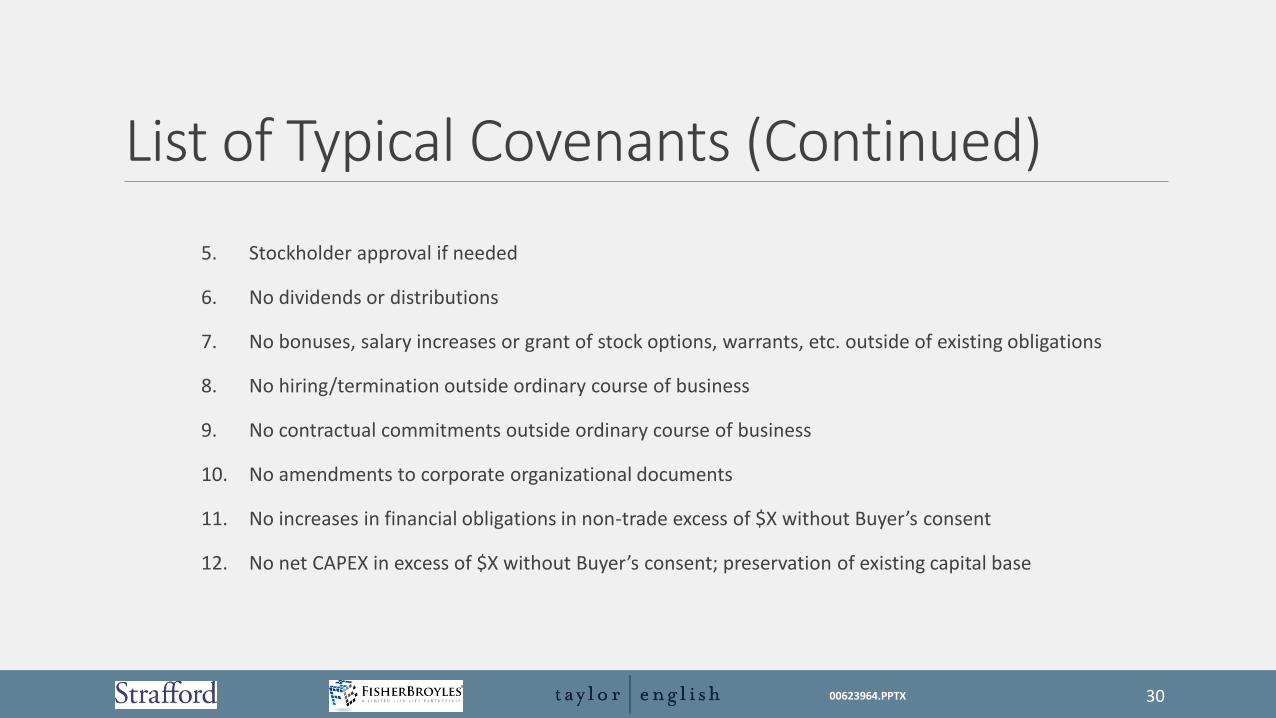

List of Typical Covenants (Continued)

5. Stockholder approval if needed

6. No dividends or distributions

7. No bonuses, salary increases or grant of stock options, warrants, etc. outside of existing obligations

8. No hiring/termination outside ordinary course of business

9. No contractual commitments outside ordinary course of business

10. No amendments to corporate organizational documents

11. No increases in financial obligations in non-trade excess of $X without Buyer’s consent

12. No net CAPEX in excess of $X without Buyer’s consent; preservation of existing capital base

30 00623964.PPTX

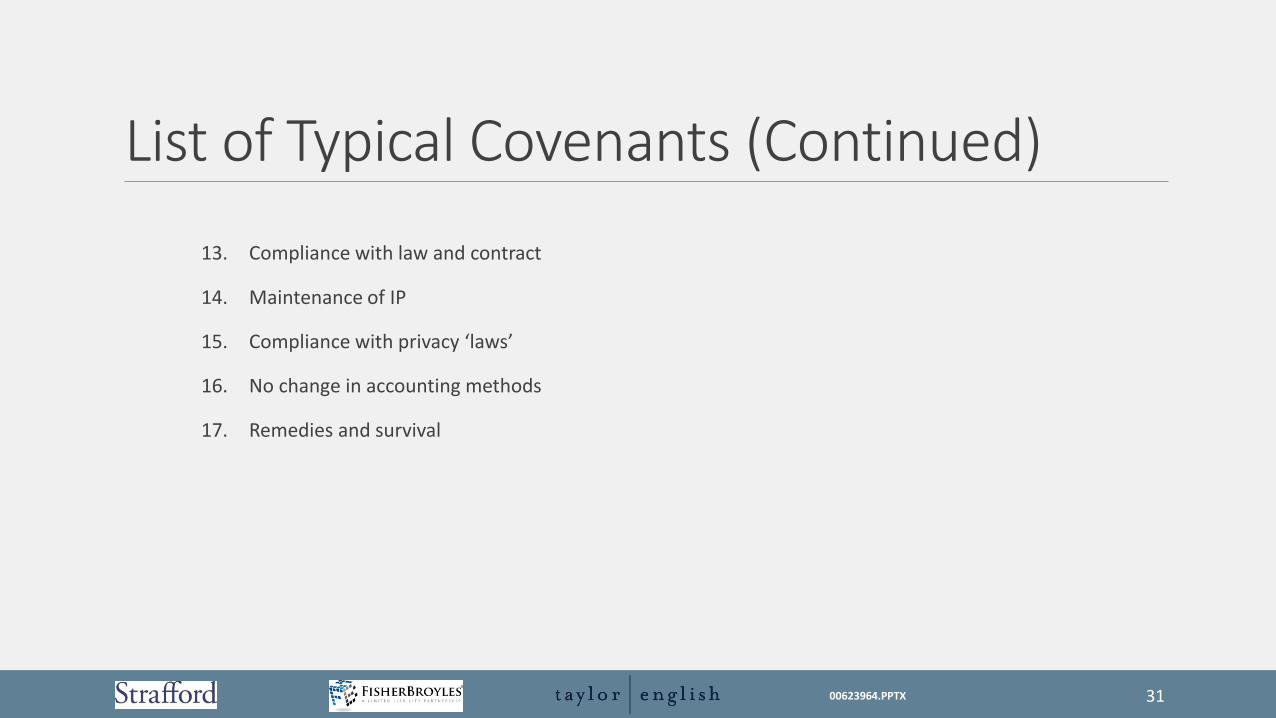

List of Typical Covenants (Continued)

13. Compliance with law and contract

14. Maintenance of IP

15. Compliance with privacy ‘laws’

16. No change in accounting methods

17. Remedies and survival

31 00623964.PPTX

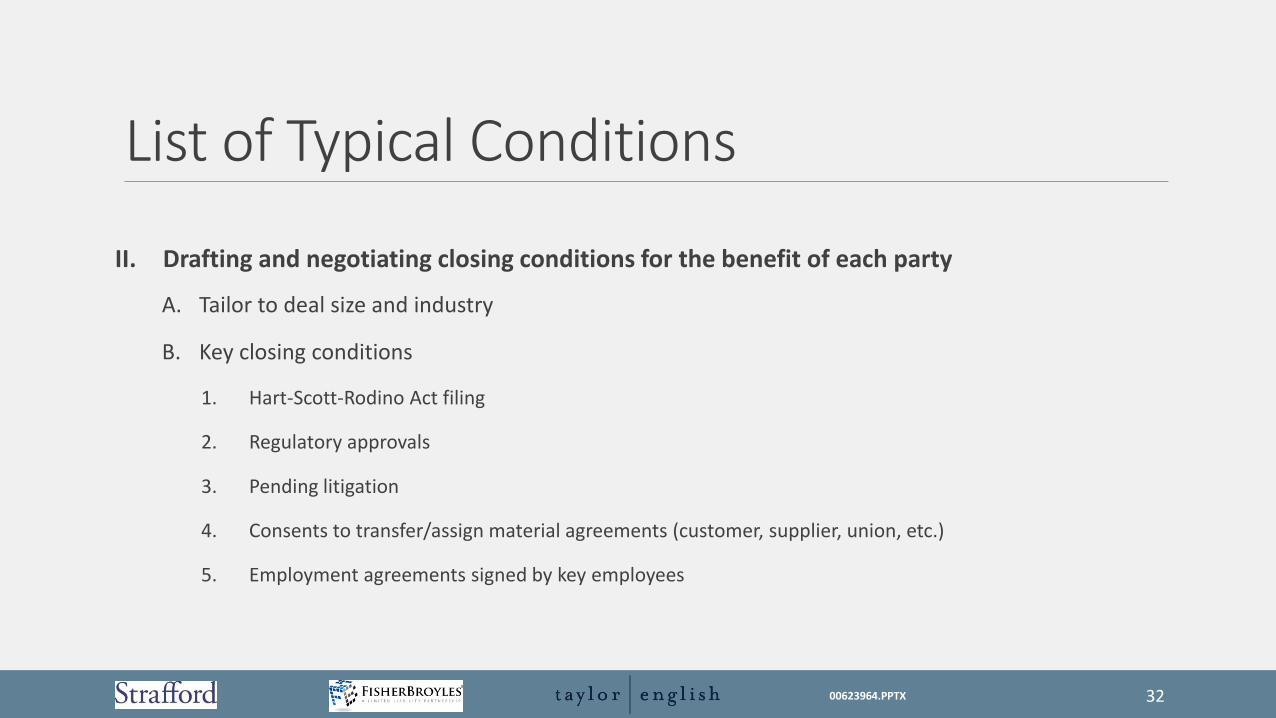

List of Typical Conditions

II. Drafting and negotiating closing conditions for the benefit of each party

A. Tailor to deal size and industry

B. Key closing conditions

1. Hart-Scott-Rodino Act filing

2. Regulatory approvals

3. Pending litigation

4. Consents to transfer/assign material agreements (customer, supplier, union, etc.)

5. Employment agreements signed by key employees

32 00623964.PPTX

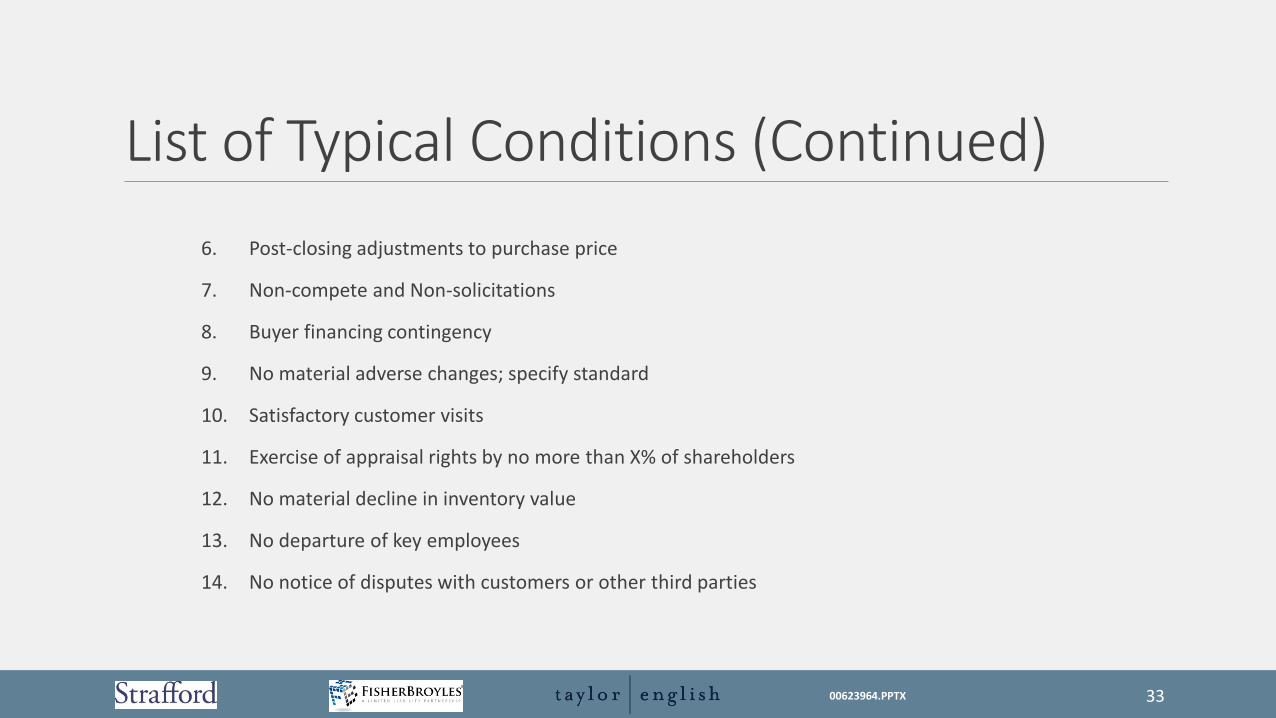

List of Typical Conditions (Continued)

6. Post-closing adjustments to purchase price

7. Non-compete and Non-solicitations

8. Buyer financing contingency

9. No material adverse changes; specify standard

10. Satisfactory customer visits

11. Exercise of appraisal rights by no more than X% of shareholders

12. No material decline in inventory value

13. No departure of key employees

14. No notice of disputes with customers or other third parties

33 00623964.PPTX