Embed Size (px)

Citation preview

1

Chapter 11: Net Investment Income Tax (NIIT)

Page 159-172

11: Net Investment Income Tax (NIIT)

Upon completion of this seminar, participants should be able to—

Learning Objectives

2

• Calculate the 3.8% Net Investment Income Tax (NIIT).• Apply strategies to reduce the NIIT.

Page 159-172

11: Net Investment Income Tax (NIIT)

3

Key Developments

• Determining whether an activity is an IRC 162 business activity is a challenge.

Page 159-172

11: Net Investment Income Tax (NIIT)

Page 159

To review how we calculate the tax

III. The Calculation

11: Net Investment Income Tax (NIIT)4

Page 159-160

To review how we calculate the tax

There is very few questions regarding to what exactly is:

MAGI orThreshold

So what exactly constitutes Net Investment Income – What do we keep and what do we Flush?

III. The Calculation

11: Net Investment Income Tax (NIIT)5

Page 160

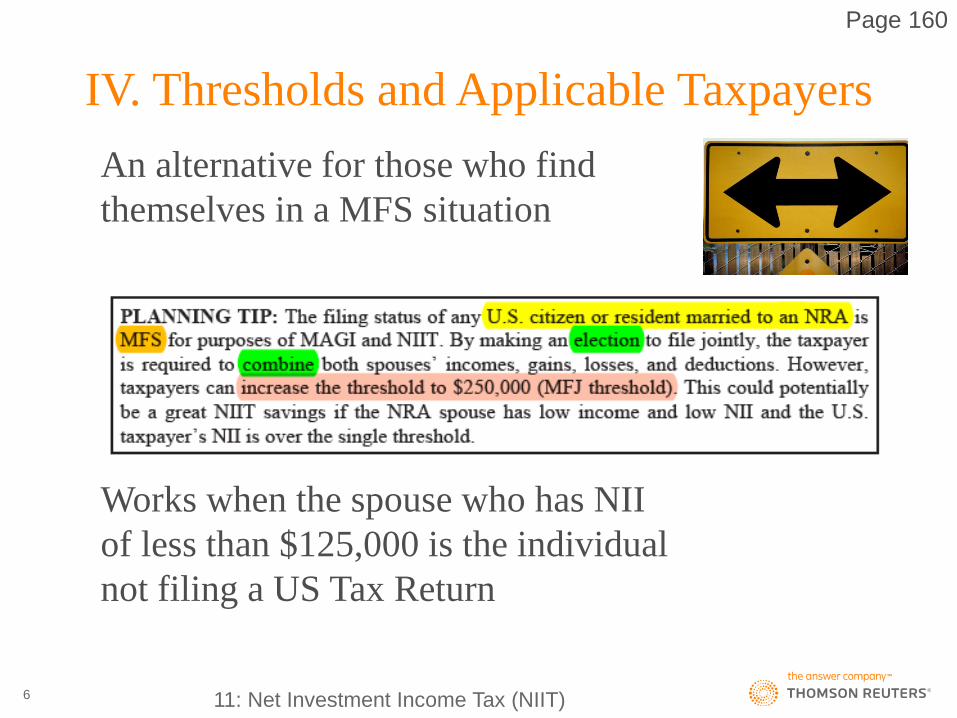

An alternative for those who find themselves in a MFS situation

Works when the spouse who has NII of less than $125,000 is the individual not filing a US Tax Return

IV. Thresholds and Applicable Taxpayers

11: Net Investment Income Tax (NIIT)6

Page 161

Lots of deductions – Look to software or line adjustment on Form 8960.A. Investment Interest Expense.B. Allocated State and Local Income Taxes.C. Investment Expenses.D. Deductions allocable to (Passive & Certain)

Business Activities. Rental Royalty Passive Business Activity Expense Financial Instruments and Commodities

VI. Allocable Deductions forNII (Reg. 1.1411-4(f))

11: Net Investment Income Tax (NIIT)7

Page 162

Lots of deductions – Look to software or line adjustment on Form 8960.E. Early Withdrawal Penalties.F. Foreign Taxes Paid.G. IRC 1411 NOL Amounts.H. Annuity remaining basis on final year.I. Estate taxes allocable to investment income

from the estate.J. Associated expenses of NIIT Income

VI. Allocable Deductions forNII (Reg. 1.1411-4(f))

11: Net Investment Income Tax (NIIT)8

Page 162

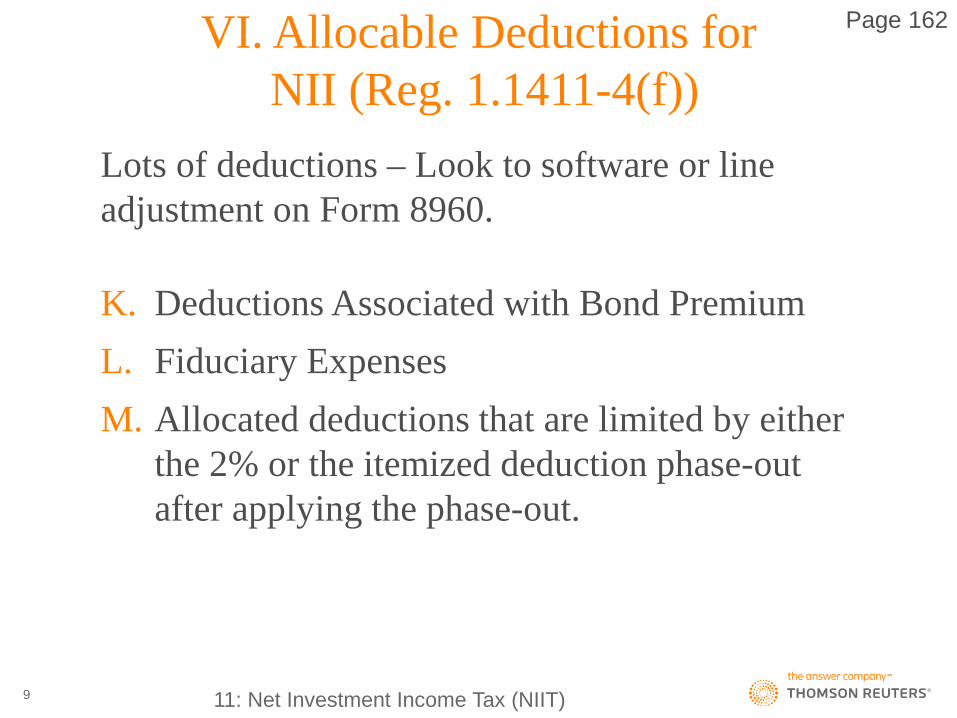

Lots of deductions – Look to software or line adjustment on Form 8960.

K. Deductions Associated with Bond PremiumL. Fiduciary ExpensesM. Allocated deductions that are limited by either

the 2% or the itemized deduction phase-out after applying the phase-out.

VI. Allocable Deductions forNII (Reg. 1.1411-4(f))

11: Net Investment Income Tax (NIIT)9

Page 163

What can I always throw out?A. Wages and SE Income Except – Trading Financial Instruments and

CommoditiesB. Non-Passive Business IncomeC. Retirement Plan Distributions BUT

VII. Income Exemptedfrom NII (Regs. 1.1411-4, -5, -8, and -9)

11: Net Investment Income Tax (NIIT)10

Page 163

What can I always throw out?D. Tax ExclusionsE. Tax DeferralsF. Non-Investment Income Such As: Social Security Alimony Unemployment

G. Pass-Through Income (Gains and Losses) –When the shareholder or partner materially participates

VII. Income Exemptedfrom NII (Regs. 1.1411-4, -5, -8, and -9)

11: Net Investment Income Tax (NIIT)11

Page 163

First the Basics:A. NII will include the net gain if the gain/loss is

taken into account for regular tax.B. The net gain from property dispositions is

reduced but not below ZERO.C. Gain from the disposition of business property

will be excluded from NIIT – Exception financial instruments and commodities

D. Gains from the investment of working capital are includable in NIIT.

VIII. Net Gains and Losses for NIIT Purposes

11: Net Investment Income Tax (NIIT)12

Page 164

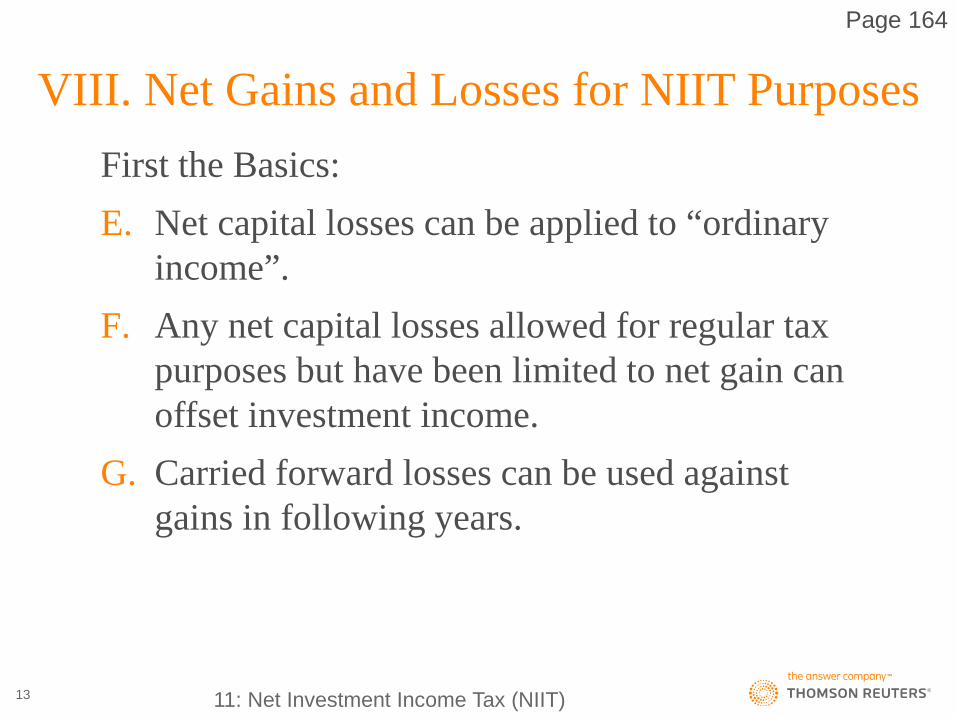

First the Basics:E. Net capital losses can be applied to “ordinary

income”.F. Any net capital losses allowed for regular tax

purposes but have been limited to net gain can offset investment income.

G. Carried forward losses can be used against gains in following years.

VIII. Net Gains and Losses for NIIT Purposes

11: Net Investment Income Tax (NIIT)13

Page 24

This is how it works:

The bucket of income/loss will stay together – the capital loss first offsets the capital gain

VIII. Net Gains and Losses for NIIT Purposes

11: Net Investment Income Tax (NIIT)14

Page 164

As we used all the loss for regular tax we get the same for NII as any amount used for regular tax that is NII will be included:

VIII. Net Gains and Losses for NIIT Purposes

11: Net Investment Income Tax (NIIT)16

Page 164-165

Proposed Reg. 1.1411-4(d)(4)(iii) – What happens if we have a non-NII item that cannot be applied to NII and is carried forward – it is GONE:

VIII. Net Gains and Losses for NIIT Purposes

11: Net Investment Income Tax (NIIT)17

18

With the ACA taxpayers are subject to the NIIT

Taxpayers who have multiple business activities must determine if their interest is a business activity and if they are material to that activity.By a show of hands:A. Determination of trade or business activities is made

at the entity level.B. Whether the taxpayer is a material participant is made

at the taxpayer level.C. If the activity is not a business activity or the taxpayer

is not material may subject the taxpayer to an additional tax.

D.All of the above. 11: Net Investment Income Tax (NIIT)

Page 165

Determination can happen at either the entity or shareholder/partner level.

Income and gains from the investment of working capital is included for NIIT purposes.Determination of whether the income, gain and related deductions are non-passive is made at the owner level.Whether a S-Corp or Partnership is engaged in a business activity is determined at entity level.

IX. Business, Passive and Rental Activities

11: Net Investment Income Tax (NIIT)19

Page 165

Some Examples:

Look to the source of the income

IX. Business, Passive and Rental Activities

11: Net Investment Income Tax (NIIT)20

Page 166

Additional Caution:IRC 1411 v. IRC 162 Example – NIIA restaurant while an IRC 162 activity but the taxpayer is not a material participant will be subject NIITExample - PALFor PAL purposes simply the allowance per the 7 rules of IRC 469 will make it non-passive

IX. Business, Passive and Rental Activities

11: Net Investment Income Tax (NIIT)21

Page 166

The problems with gains on a C-CorporationIncome from the C Corporation not subject to NIIT Wages. Personal Goodwill on Sale – This has not been tested

by the courts and some disagree.

Income from the C Corporation subject to NII. Dividends Liquidation Gains Sale of Stock

XI. C Corporation

11: Net Investment Income Tax (NIIT)22

Page 166

A. A trust is subject to NIIT to the extent of the lesser of:1. AGI in excess of the top fiduciary bracket

($12,500) for 2017 or2. Undistributed Net Investment Income

XII. Estate & Trust Rules

11: Net Investment Income Tax (NIIT)23

Page 167

Additional Issues:Caution - Simple Trusts while required to distribute current income may be subject to capital gains.C. IRD can be reduced by applicable expenses.D. Direct expenses are allocated to NII to which it

relates.E. The Undistributed NII is reduced by any

allowable income distribution deduction.

XII. Estate & Trust Rules

11: Net Investment Income Tax (NIIT)24

Page 167

The Problem: AGI of $1 million which comprisesWages - $ 600,000Muni Interest- $ 30,000S-Corp K-1- $ 100,000Interest Income- $ 100,000Dividends- $ 50,000NQ Annuity- $ 70,000Capital Loss- $ 30,000Rental Income- $ 83,000AGI- $1,000,000

XIII. Comprehensive NIITCalculation Example

NII$100,000$ 50,000$ 70,000

-$ 3,000$ 83,000$300,000

11: Net Investment Income Tax (NIIT)25

Page 168

Type Here

XIII. Comprehensive NIIT Calculation ExampleDescription AGI/TI NIITotal $1,000,000Investment Int. Exp.D. Investment ExpenseC. State Income TaxNet

$40,000

$18,000

$300,000

$30,000

$212,000

11: Net Investment Income Tax (NIIT)27

Page 174

Type Here

XIV. Form 8960 Cheat Sheet

11: Net Investment Income Tax (NIIT)28

Page 172

Tax Saving Moves:

Reduce MAGI

Tax Exempts

Defer Income

Tax Favored Investments

Watch the Timing

Life Insurance Products

Retirement Programs

Trust Planning

XV. Planning Checklist

11: Net Investment Income Tax (NIIT)29