Embed Size (px)

Citation preview

IV.MONETARY DEVELOPMENT

4.1. Money supply and credit

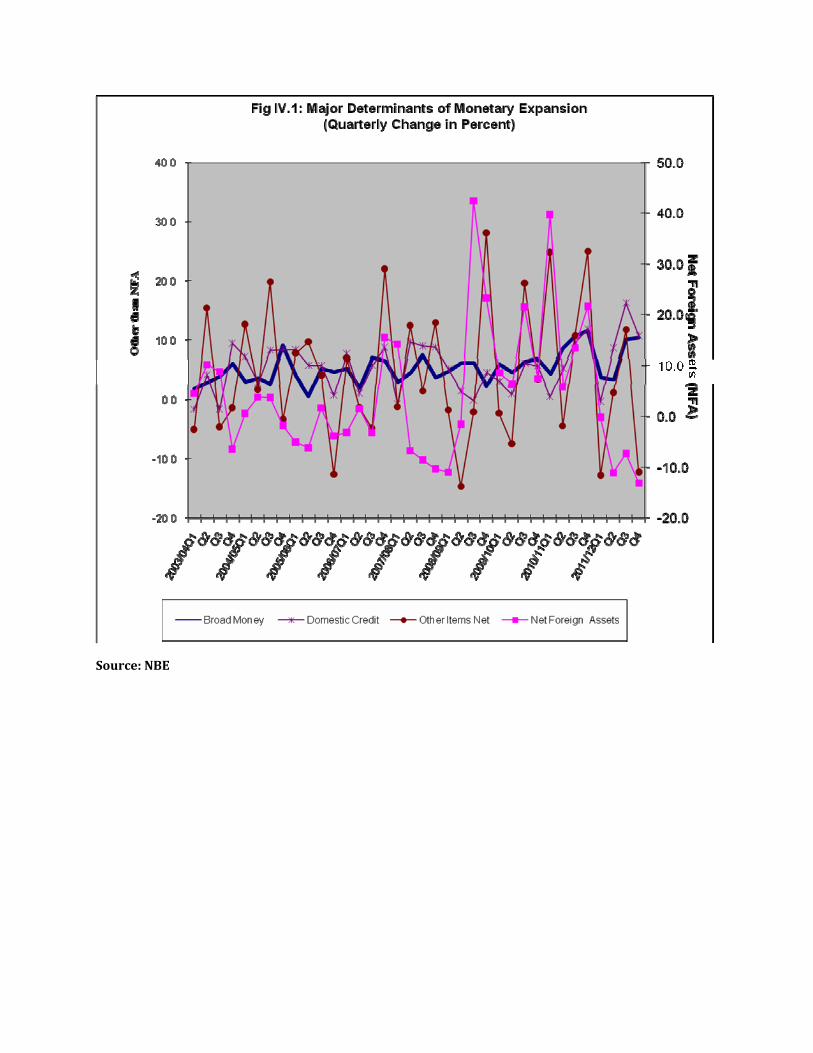

Broad money supply (m2) reached birr 189.4 billion at the end of the fourth quarter

showing annual growth rate of 30.3 percent. This was due to high domestic credit,

which expanded by 39.5 percent, mainly due to 56.7 percent increase in credit to non-

central government sector. On the other hand, claims on government went down by 24.8

percent.

Meanwhile, net foreign assets declined by 28.4 percent on annual bases, and reached

birr 39.8 billion at the end of the fourth quarter (Table 4.1).

Table 4.1: Factors Influencing Broad Money (In Millions of Birr)

2011

Qtr. IV Qtr. III Qtr. IV(Jun. 11) (Mar. 12) (June. 12)

A B C

1. External Assets (net) 55,534.7 45,771.8 39,787.7 -28.4 -13.1 -35.8 -33.42. Domestic Credit 135,553.9 170,731.8 189,080.8 39.5 10.7 121.6 102.5 . Claims on Central Gov't (net) 28,651.7 15,673.9 21,557.4 -24.8 37.5 -16.1 32.9 . Claims on Non-Central Gov't 106,902.2 155,057.9 167,523.4 56.7 8.0 137.7 69.7 . Financial Institutions 6,250.0 11,870.0 12,502.0 100.0 5.3 14.2 3.5 . Others 100,652.2 143,187.9 155,021.4 54.0 8.3 123.5 66.13. Other Items (net) 45,711.6 44,999.4 39,469.7 -13.7 -12.3 -14.2 -30.94. Broad Money (M2) 145,377.0 171,504.3 189,398.8 30.3 10.4 100.0 100.0

Particulars

Percentage Change

Contibutions of Each Component to Broad Money

Growth

C/A C/B Annual Quarterly

2012

Source:NBE

Source:NBE

Source:NBE

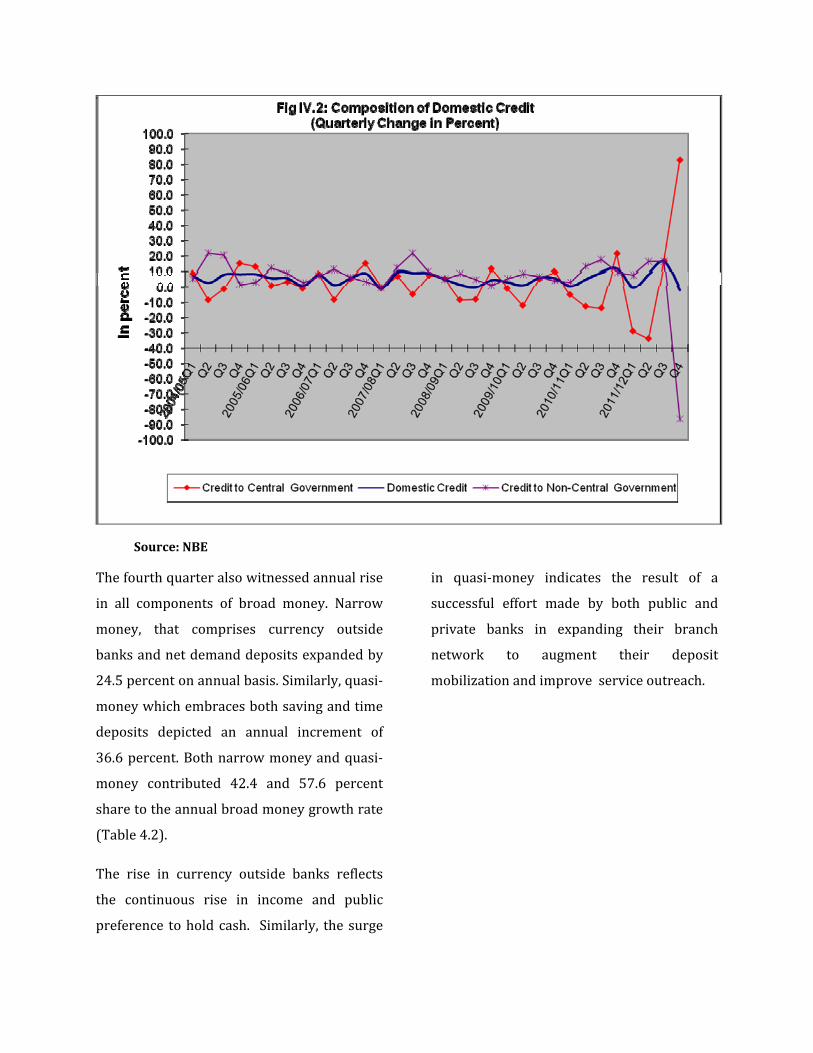

Thefourthquarteralsowitnessedannualrise

in all components of broad money. Narrow

money, that comprises currency outside

banksandnetdemanddepositsexpandedby

24.5percentonannualbasis.Similarly,quasi‐

moneywhichembracesbothsavingandtime

deposits depicted an annual increment of

36.6percent.Bothnarrowmoneyandquasi‐

money contributed 42.4 and 57.6 percent

sharetotheannualbroadmoneygrowthrate

(Table4.2).

The rise in currency outside banks reflects

the continuous rise in income and public

preference toholdcash. Similarly, thesurge

in quasi‐money indicates the result of a

successful effort made by both public and

private banks in expanding their branch

network to augment their deposit

mobilizationandimproveserviceoutreach.

Table 4.2: Components of Broad Money

(In Millions of Birr)

2011

Qtr. IV Qtr. III Qtr. IV(Jun. 11) (Mar. 12) (June. 12)

A B C

1. Narrow Money Supply 76,171.0 84,974.1 94,849.9 24.5 11.6 42.4 55.2 . Currency outside banks 32,574.9 37,727.7 38,537.1 18.3 2.1 13.5 4.5 . Demand Deposits (net) 43,596.1 47,246.4 56,312.7 29.2 19.2 28.9 50.72. Quasi-Money 69,206.0 86,530.1 94,548.9 36.6 9.3 57.6 44.8 . Savings Deposits 64,539.6 76,393.8 82,487.8 27.8 35.8 40.8 34.1 . Time Deposits 4,666.4 10,136.4 12,061.1 158.5 19.0 16.8 10.83. Broad Money Supply 145,377.0 171,504.3 189,398.8 30.3 10.4 100.0 100.0

Contibution of Each Component to Broad Money

Growth

C/A C/B Annual Quarter

ly

Percentage Change

2012

Particulars

Source:NBE

SOURCE:NBE

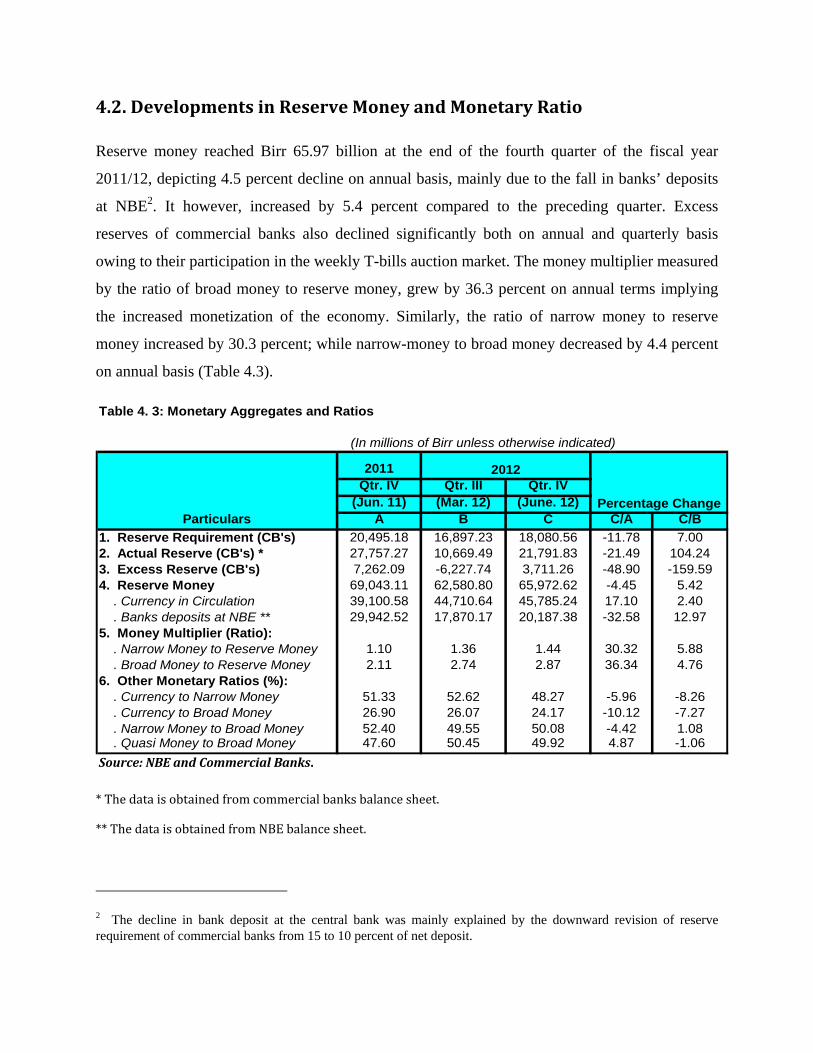

4.2.DevelopmentsinReserveMoneyandMonetaryRatio

Reserve money reached Birr 65.97 billion at the end of the fourth quarter of the fiscal year

2011/12, depicting 4.5 percent decline on annual basis, mainly due to the fall in banks’ deposits

at NBE2. It however, increased by 5.4 percent compared to the preceding quarter. Excess

reserves of commercial banks also declined significantly both on annual and quarterly basis

owing to their participation in the weekly T-bills auction market. The money multiplier measured

by the ratio of broad money to reserve money, grew by 36.3 percent on annual terms implying

the increased monetization of the economy. Similarly, the ratio of narrow money to reserve

money increased by 30.3 percent; while narrow-money to broad money decreased by 4.4 percent

on annual basis (Table 4.3).

Table 4. 3: Monetary Aggregates and Ratios

(In millions of Birr unless otherwise indicated)

2011Qtr. IV Qtr. III Qtr. IV

(Jun. 11) (Mar. 12) (June. 12)Particulars A B C C/A C/B

1. Reserve Requirement (CB's) 20,495.18 16,897.23 18,080.56 -11.78 7.002. Actual Reserve (CB's) * 27,757.27 10,669.49 21,791.83 -21.49 104.243. Excess Reserve (CB's) 7,262.09 -6,227.74 3,711.26 -48.90 -159.594. Reserve Money 69,043.11 62,580.80 65,972.62 -4.45 5.42 . Currency in Circulation 39,100.58 44,710.64 45,785.24 17.10 2.40 . Banks deposits at NBE ** 29,942.52 17,870.17 20,187.38 -32.58 12.975. Money Multiplier (Ratio): . Narrow Money to Reserve Money 1.10 1.36 1.44 30.32 5.88 . Broad Money to Reserve Money 2.11 2.74 2.87 36.34 4.766. Other Monetary Ratios (%): . Currency to Narrow Money 51.33 52.62 48.27 -5.96 -8.26 . Currency to Broad Money 26.90 26.07 24.17 -10.12 -7.27 . Narrow Money to Broad Money 52.40 49.55 50.08 -4.42 1.08 . Quasi Money to Broad Money 47.60 50.45 49.92 4.87 -1.06

Percentage Change

2012

Source:NBEandCommercialBanks.

*Thedataisobtainedfromcommercialbanksbalancesheet.

**ThedataisobtainedfromNBEbalancesheet.

2 The decline in bank deposit at the central bank was mainly explained by the downward revision of reserve requirement of commercial banks from 15 to 10 percent of net deposit.

Source:NBE

‐10,000.0

‐5,000.0

0.0

5,000.0

10,000.0

15,000.0

20,000.0

25,000.0

30,000.0

2004/05Q1

Q2

Q3

Q4

2005/06Q1

Q2

Q3

Q4

2006/07Q1

Q2

Q3

Q4

2007/08Q1

Q2

Q3

Q4

2008/09Q1

Q2

Q3

Q4

2009/10Q1

Q2

Q3

Q4

2010/11Q1

Q2

Q3

Q4

2011/12Q1

Q2

Q3

Q4

In millions of Birr

Fig IV.5: Monetary Aggregates(Fourth Quarter of 2011/12)

Required Reserve

Actual Reserve

Excess Reserve

Source:NBE

4.3.InterestRateDevelopments

Average saving deposit rate and average

lending rates remained at 5.4 and 11.88

percent, respectively, on quarterly and

annual basis. Weighted average time

deposit rate, however, registered annual

decline of 5.6 percent. On the other hand,

the weighted yearly average yield on T-

bills increased from 1.067 to 1.621

percent. However, considering annual

headline inflation of 20.9 percent during

the quarter under review, all deposit rates,

lending rates and T-bill yields remained

negative in real terms (Table 4.4).

Table4.4:‐InterestRateStructureofCommercialBanks(Percentperannum)

2010/11 2011/12PercentageChanges

QIV QIII QIV Annual Quarterly

1.SavingsDepositRate

Minimum 5 5 5 0.0 0.0

Maximum 5.75 5.75 5.75 0.0 0.0

AverageSavingRate 5.4 5.4 5.4 0.0 0.0

2.TimeDeposits

Upto1yr 5.71 5.61 5.65 ‐1.0 0.7

1‐2years 5.85 5.71 5.74 ‐1.8 0.5

Over2yrs 5.91 5.76 5.79 ‐2.1 0.5

AverageTimeDep.Rate(Weighted) 5.82 5.70 5.73 ‐1.6 0.6

3.DemandDeposit(Weighted) 0.04 0.03 0.03 ‐27.4 ‐1.9

4.LendingRate

Minimum 7.5 7.5 7.5 0.0 0.0

Maximum 16.25 16.25 16.25 0.0 0.0

AverageLendingRate 11.88 11.88 11.88 0.0 0.0

5.T‐billsRate(Weighted) 1.067 1.935 1.621 51.9 ‐16.2

6.BondYield(SimpleAverage) 3.67 3.67 3.67 0.0 0.0

7.HeadlineInflation 38.10 32.50 20.90 ‐45.1 ‐35.7

8.FoodInflation 45.30 40.90 21.50 ‐52.5 ‐47.4

9.Core/non‐foodInflation 27.90 20.40 19.80 ‐29.0 ‐2.9

Source:NBEandcommercialbanks

Source:NBEandCommercialBank

Source:NBEstaffcompilation

4.4. Developments in the Financial Sector

Banks, insurance companies and

microfinance institutions are the main

financial institutions in Ethiopia. The

number of banks operating in the country

reached 17 at the end of June 2012 of which

14 banks were privately owned.

During the review quarter, 108 new bank

branches were opened, raising the total

number of bank branches to 1289. As a

result, the ratio of total bank branch to total

population went down to 62,063 from

67,739 in the preceding quarter, reflecting

an improvement in financial service

outreach.

About 33.4 percent of the total bank

branches were located in Addis Ababa,

depicting relatively high concentration of

branches in the capital. Of the total bank

branches, the share of private banks

decreased to 47.6 percent from 48.6 percent

in the preceding quarter due to the opening

of 68 new branches by public banks during

the review quarter.

Computedbasedontheassumptionthattotalpopulationwas80million

Meanwhile, the total capital of the banking

system reached Birr 18.0 billion at the end

of the fourth quarter of the fiscal year

2011/12, of which private banks together

accounted for49.3 percent. Commercial

Bank of Ethiopia, the biggest state owned

bank, has 34.6 percent of the total capital of

the banking system. (Table 4.5)

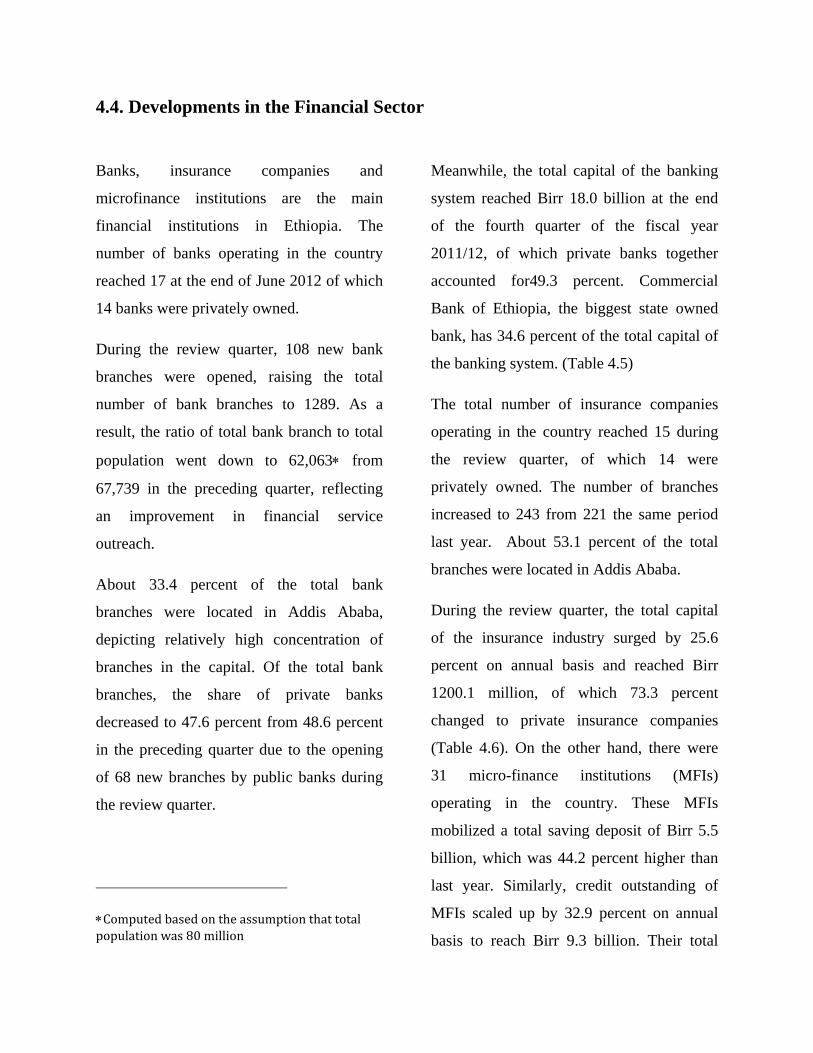

The total number of insurance companies

operating in the country reached 15 during

the review quarter, of which 14 were

privately owned. The number of branches

increased to 243 from 221 the same period

last year. About 53.1 percent of the total

branches were located in Addis Ababa.

During the review quarter, the total capital

of the insurance industry surged by 25.6

percent on annual basis and reached Birr

1200.1 million, of which 73.3 percent

changed to private insurance companies

(Table 4.6). On the other hand, there were

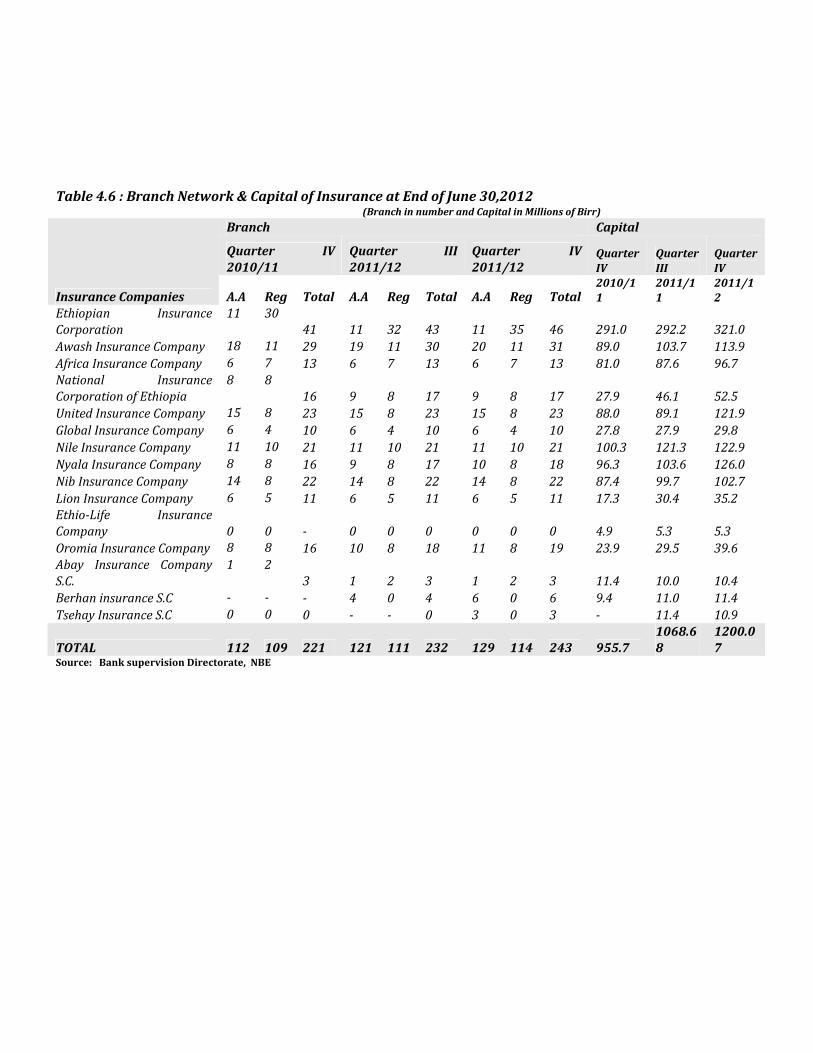

31 micro-finance institutions (MFIs)

operating in the country. These MFIs

mobilized a total saving deposit of Birr 5.5

billion, which was 44.2 percent higher than

last year. Similarly, credit outstanding of

MFIs scaled up by 32.9 percent on annual

basis to reach Birr 9.3 billion. Their total

assets also increased by 31.0 percent to Birr

13.3 billion by the end of June 2012 (Table

4.7). The top five largest MFIs (Amhara

Credit & Saving, Dedebit Credit & Saving,

Oromia Credit & Saving, Omo Credit &

Saving institute and Addis credit & savings)

alone accounted for 86.6 percent of the total

capital, 94.0 percent of the savings, 89.7

percent of the credit and 90.3 percent of the

total assets of the industry.

Source:BanksupervisionDirectorate,NBE

3 Although, Zemen Bank follows a “one brach” strategy, it also includes (comprise) banking kiosk network in different locations.

Table4.5:CapitalandBranchNetworkofBankingSystematEndofJune30,2012(BranchinNumberandCapitalinMillionsofBirr)

BranchNetwork Capital

2010/11 2011/122010/11 2011/12

QuarterIV QuarterIII QuarterIVBanks

Reg. A.A Total %Share

Reg A.A Total %Share

Reg. A.A Total %Share

QuarterIV

QuarterIII

QuarterIV

1.PublicBanks CommercialBankofEthiopia 323 94 417 43.0 395 103 498 42.2 448 111 559 43.4 6,262.0 6,231.0 6,231.0Construction&BusinessBank 17 17 34 3.5 48 29 77 6.5 53 31 84 6.5 277.0 364.0 363.0DevelopmentBankofEthiopia 31 1 32 3.3 31 1 32 2.7 31 1 32 2.5 2,179.0 2,454.0 2,540.0TotalPublicBanks 371 112 483 49.8 474 133 607 51.4 532 143 675 52.4 8718 9049 91342.PrivateBanks

AwashIntern.Bank 36 34 70 7.2 37 44 81 6.9 39 47 86 6.7 1,104.0 1,254.0 1,257.0DashenBank 31 34 65 6.7 36 37 73 6.2 38 37 75 5.8 1,152.0 1,157.0 1,381.0

AbyssiniaBank 25 32 57 5.9 29 32 61 5.2 29 32 61 4.7 532.0 687.0 691.0

WegagenBank 29 24 53 5.5 33 27 60 5.1 33 27 60 4.7 1,093.0 1,267.0 1,269.0

UnitedBank 18 32 50 5.2 26 36 62 5.2 29 40 69 5.4 748.0 785.0 785.0

NibIntern.Bank 19 32 51 5.3 19 34 53 4.5 20 38 58 4.5 983.0 1,241.0 1,242.0

CooperativeBankofOromiya

38 5 43 4.4 44 6 50 4.2 45 6 51 4.0 207.0 287.0 338.0

LionIntern.Bank 17 13 30 3.1 17 13 30 2.5 19 17 36 2.8 318.0 341.0 357.0

OromiaInternationalBank

25 11 36 3.7 28 11 39 3.3 29 12 41 3.2 265.0 374.0 393.0

ZemenBank3 0 3 3 0.3 2 4 6 0.5 3 4 7 0.5 193.0 290.0 290.0

BunaInternationalBank

2 9 11 1.1 11 10 21 1.8 14 11 25 1.9 220.0 236.0 257.0

BerhanIntern.Bank 3 7 10 1.0 6 8 14 1.2 7 8 15 1.2 138.0 170.0 211.0

AbayBank 7 1 8 0.8 18 2 20 1.7 21 4 25 1.9 161.0 204.0 250.0AddisInterationalBank

n/a n/a 0 0.0 1 3 4 0.0 1 4 5 0.4 117.0 137.0 155.0

TotalPrivateBanks

250 237 487 50.2 307 267 574 48.6 327 287 614 47.6 7,231.0 8,430.0 8,876.0

3.GrandTotalBanks

621 349 970 100.0 781 400 1181 100.0 859 430 1289 100.0 15,949.0 17,479.0 18,010.0

Table4.6:BranchNetwork&CapitalofInsuranceatEndofJune30,2012(BranchinnumberandCapitalinMillionsofBirr)

Branch Capital

Quarter IV2010/11

Quarter III2011/12

Quarter IV2011/12

QuarterIV

QuarterIII

QuarterIV

InsuranceCompanies A.A Reg Total A.A Reg Total A.A Reg Total2010/11

2011/11

2011/12

Ethiopian InsuranceCorporation

11 3041 11 32 43 11 35 46 291.0 292.2 321.0

AwashInsuranceCompany 18 11 29 19 11 30 20 11 31 89.0 103.7 113.9AfricaInsuranceCompany 6 7 13 6 7 13 6 7 13 81.0 87.6 96.7National InsuranceCorporationofEthiopia

8 816 9 8 17 9 8 17 27.9 46.1 52.5

UnitedInsuranceCompany 15 8 23 15 8 23 15 8 23 88.0 89.1 121.9GlobalInsuranceCompany 6 4 10 6 4 10 6 4 10 27.8 27.9 29.8NileInsuranceCompany 11 10 21 11 10 21 11 10 21 100.3 121.3 122.9NyalaInsuranceCompany 8 8 16 9 8 17 10 8 18 96.3 103.6 126.0NibInsuranceCompany 14 8 22 14 8 22 14 8 22 87.4 99.7 102.7LionInsuranceCompany 6 5 11 6 5 11 6 5 11 17.3 30.4 35.2Ethio‐Life InsuranceCompany 0 0 ‐ 0 0 0 0 0 0 4.9 5.3 5.3OromiaInsuranceCompany 8 8 16 10 8 18 11 8 19 23.9 29.5 39.6Abay Insurance CompanyS.C.

1 23 1 2 3 1 2 3 11.4 10.0 10.4

BerhaninsuranceS.C ‐ ‐ ‐ 4 0 4 6 0 6 9.4 11.0 11.4TsehayInsuranceS.C 0 0 0 ‐ ‐ 0 3 0 3 ‐ 11.4 10.9

TOTAL 112 109 221 121 111 232 129 114 243 955.71068.68

1200.07

Source:BanksupervisionDirectorate,NBE

Source:BankSupervisionDirectorate,NBE

BN=denotesbranchnetworkandC=Capital

SOURCE:MICROFINANCESUPERVISIONDIRECTORATE,NBE

BN=denotesbranchnetworkandC=Capital

Table4.7:MicrofinanceInstitutionsPerformanceasofJune30,2012(InThousandsofBirr)

2010/11 2011/12

Qtr.IV Qtr.III Qtr.IV %Change

Particulars

A B C C/A C/B

TotalCapital 2,945,970.0 3,491,468.0 3755479.9 27.5 7.6

Saving 3,779,089.0 4,903,920.0 5450593.5 44.2 11.1

Credit 6,991,986.0 7,514,288.0 9289642.6 32.9 23.6

TotalAssets 10,156,387.0 12,048,730.0 13308200.1 31.0 10.5

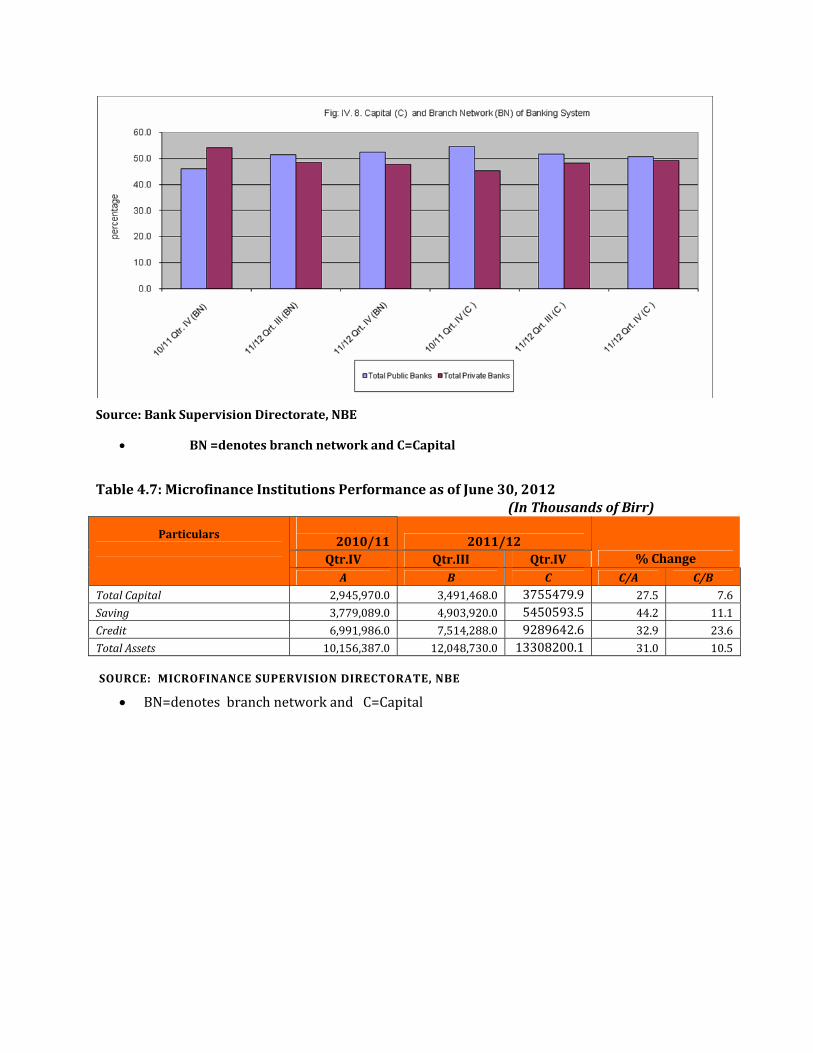

4.5ACTIVITIESOFTHEBANKINGSYSTEM

4.5.1RESOURCEMOBILIZATION

Total resource mobilized by banking System

(as measured by the sum of net change in

deposit, loans collected and net Change in

borrowings) went down by14.2 Percent

against last year the same period due to

higher net deposit (Table 4.8).

Table4.8:SummaryofResourceMobilizationandDisbursementofBankingSystemduringtheFourthQuarterof2011/12

(InMillionsofBirr)PublicBanks PrivateBanks GrandTotal

1 2 (3)=(1)+(2)

ParticularsQtr.IV2010/11

Qtr.III2011/12

Qtr.IV2011/12 %Change

Qtr.III2011/12

Qtr.IV2011/12

Qtr.III2011/12

Qtr.IV2011/12 A B C C/A C/B

1.Deposits(netchange) 15,749.9 8,859.0 1,408.5 3,541.3 10,964.5 17,158.3 12,400.3 13.1 ‐27.7

‐Demand 7,925.9 3,149.0 ‐543.5 1,242.8 6,360.1 7,382.3 4,391.8 ‐30.9 ‐40.5

‐Saving 3,478.4 4,174.0 1,338.8 1,910.7 4,380.5 4,817.3 6,084.7 38.9 26.3

‐Time 4,345.5 1,536.0 613.2 387.8 223.9 4,958.7 1,923.8 759.2 ‐61.2

2.Borrowing(netchange) 1,389.0 1,003.2 0.0 0.0 2,246.7 1,389.0 1,003.2 ‐55.3 ‐27.8

‐Local 1,407.4 923.8 0.0 0.0 2,224.9 1,407.4 923.8 ‐58.5 ‐34.4

‐Foreign ‐18.4 79.4 0.0 0.0 21.8 ‐18.4 79.4 264.3 ‐

3.CollectionofLoans 2,917.8 6,527.4 4,150.9 4,610.9 8,286.8 7,068.7 11,138.3 34.4 57.6

4.TotalResourcesMobilized(1+2+3) 20,056.7 16,389.5 5,559.4 8,152.2 21,498.0 25,616.1 24,541.8 14.2 ‐4.2

5.Disbursement 10,940.8 13,540.2 3,663.8 2,947.4 12,687.7 14,604.6 16,487.6 29.9 12.9

6.ChangeinLiquidity(4‐5) 9,115.9 2,849.4 1,895.6 5,204.8 8,810.3 11,011.4 8,054.2 ‐8.6 ‐26.9

MemorandumItem:

A.OutstandingCredit* 68,054.3 75250.1 35,071.9 34950.5 77,690.5 103,126.2 110,200.6 41.8 6.9

B.OutstandingInterbankLending 98.4 276.4 0.0 0.0 12.9 98.4 276.4 2,038.3 180.8

Source:CommercialBanksandstaffcomputation Notes:*ExcludesgovernmentborrowingintheformofbondsandtreasurybillsfromcommercialbanksandothersectorsotherthanNBE

Source:NBE

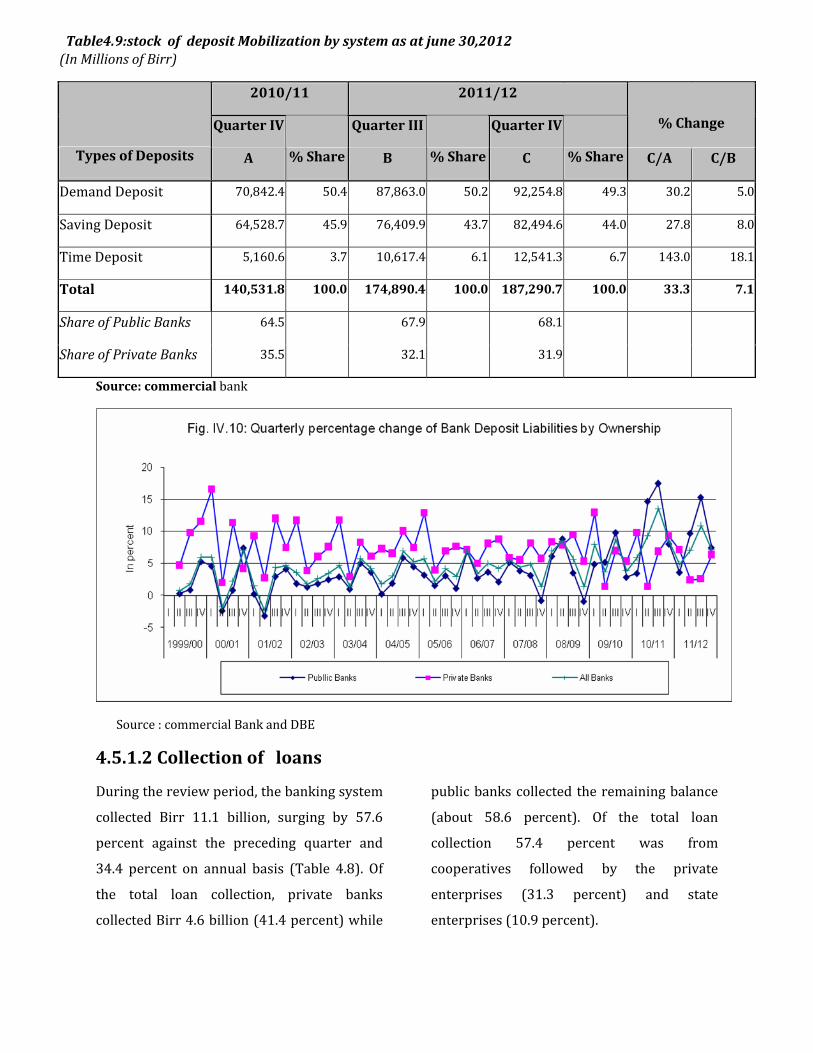

4.5.1.1 Deposit Mobilization

Total deposit liabilities of the banking

system reached Birr 187.3billion at the end

of the fourth quarter of the fiscal year

2011/12, indicating a quarterly and annual

growth rate of 7.1 and 33.3 percent,

respectively. The growth in deposit

mobilization was partly attributed to the rise

in the number of bank branches opened by

commercial banks and improvements in

economic activities. Component wise,

demand deposits, which accounted for 49.3

percent of the total deposits, reached Birr

92.3 billion, showing quarterly and annual

growth rates of 5.0 and 30.2 percent,

respectively. Similarly, saving deposits, with

44.0 percent share in total deposits increased

by 8.0 and 27.8 percent during same period.

Time deposits, which constituted 6.7 percent

of the total deposit liabilities surged by

143.0 percent over same period last year.

The share of public banks in total deposits

mobilization increased marginally to 68.1

percent from 64.5 percent last year, while

the share of private banks decreased from

35.5 to 31.9 percent (Table 4.9).

Source:commercialbank

Source:commercialBankandDBE

4.5.1.2Collectionofloans

Duringthereviewperiod,thebankingsystem

collected Birr 11.1 billion, surging by 57.6

percent against the preceding quarter and

34.4 percent on annual basis (Table 4.8). Of

the total loan collection, private banks

collectedBirr4.6billion(41.4percent)while

publicbankscollectedtheremainingbalance

(about 58.6 percent). Of the total loan

collection 57.4 percent was from

cooperatives followed by the private

enterprises (31.3 percent) and state

enterprises(10.9percent).

Table4.9:stockofdepositMobilizationbysystemasatjune30,2012(InMillionsofBirr)

2010/11 2011/12

QuarterIV QuarterIII QuarterIV %Change

TypesofDeposits A %Share B %Share C %Share C/A C/B

DemandDeposit 70,842.4 50.4 87,863.0 50.2 92,254.8 49.3 30.2 5.0

SavingDeposit 64,528.7 45.9 76,409.9 43.7 82,494.6 44.0 27.8 8.0

TimeDeposit 5,160.6 3.7 10,617.4 6.1 12,541.3 6.7 143.0 18.1

Total 140,531.8 100.0 174,890.4 100.0 187,290.7 100.0 33.3 7.1

ShareofPublicBanks 64.5 67.9 68.1

ShareofPrivateBanks 35.5 32.1 31.9

4.5.1.3.Borrowing

Total outstanding borrowing of the banking

system reached Birr 16.9 billion, up by 74.8

percent,onannualbasisduetothegrowthin

domestic borrowings (83.5 percent). Of the

total borrowing, Birr 15.9 billion (93.9

percent) came from domestic and Birr 1.0

billion(6.1percent)wasfromforeignsources

(Table4.10).

Table4.10:OutstandingBorrowingofBankingSystembySourcesasatJune30,2012

(InMillionsofBirr)

Source:CommercialBanksandDBE

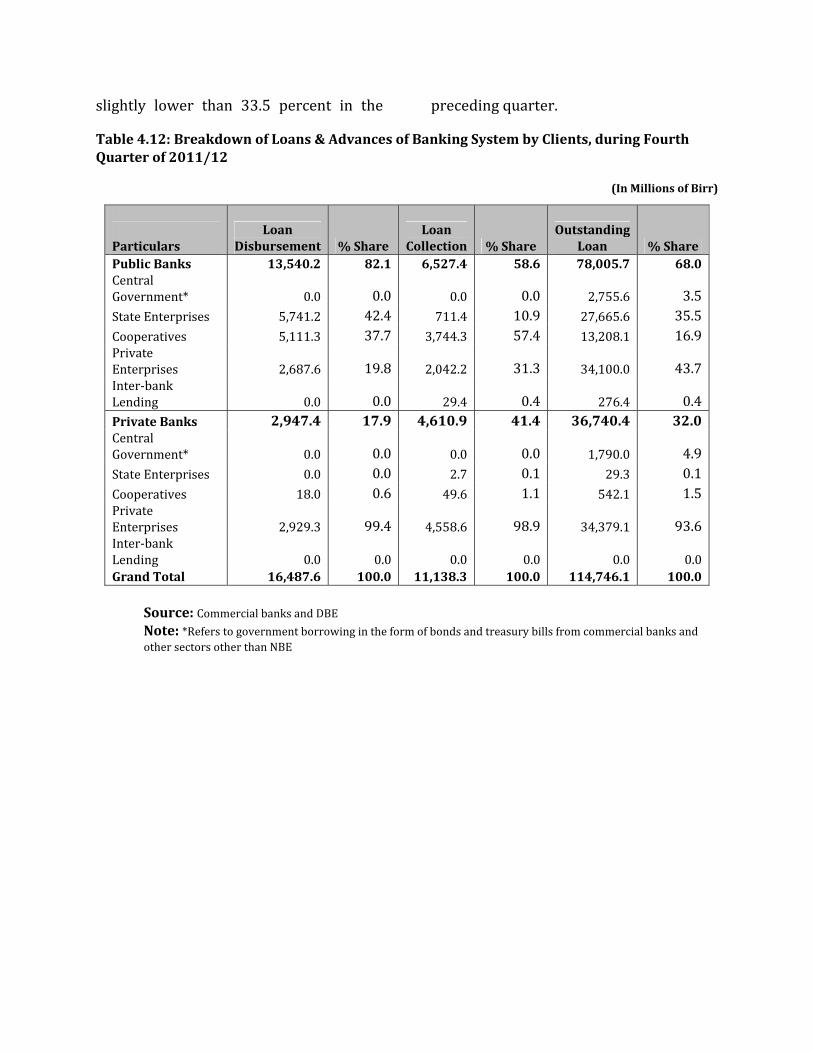

4.5.2.Disbursementoffreshloan

During the fourth quarter of the fiscal year,

total fresh loan disbursement reached Birr

16.5billion, indicatinganincreaseofpercent

over the same period of last year (Table

4.8).Public banks disbursed Birr 13.5 billion

(or 82.1percent) and private banks the

remaining balance (Table 4.12). About 99.4

percentofnewloandisbursementbyprivate

banks went to finance private enterprises

while public banks financed 57.5 percent

(Table 4.12). Sector wise, industry was the

largest beneficiary (43.4 percent), followed

byagriculture(33.1percent)andhousingand

construction(7.9percent)(Table4.11).

2010/11 2011/12QuarterIV QuarterIII QuarterIV Percentagechange

Banks A B C C/B C/ADomesticBorrowing 8,666.5 14,975.1 15,898.9 6.2 83.5ForeignBorrowing 1,019.4 954.8 1,034.1 8.3 1.4

Total 9,686.0 15,929.9 16,933.1 6.3 74.8

Source:CommercialBankandDBE

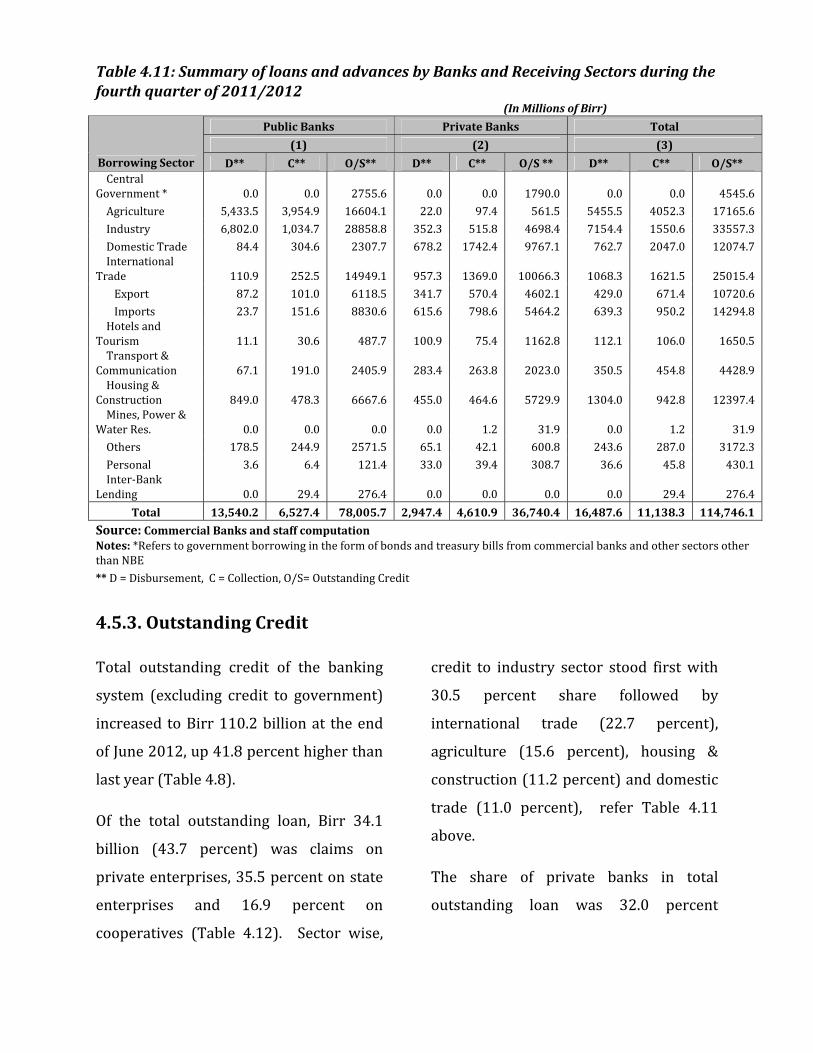

4.5.3.OutstandingCredit

Total outstanding credit of the banking

system (excluding credit to government)

increased toBirr110.2billionat theend

ofJune2012,up41.8percenthigherthan

lastyear(Table4.8).

Of the total outstanding loan, Birr 34.1

billion (43.7 percent) was claims on

privateenterprises,35.5percentonstate

enterprises and 16.9 percent on

cooperatives (Table 4.12). Sector wise,

credit to industry sector stood firstwith

30.5 percent share followed by

international trade (22.7 percent),

agriculture (15.6 percent), housing &

construction(11.2percent)anddomestic

trade (11.0 percent), refer Table 4.11

above.

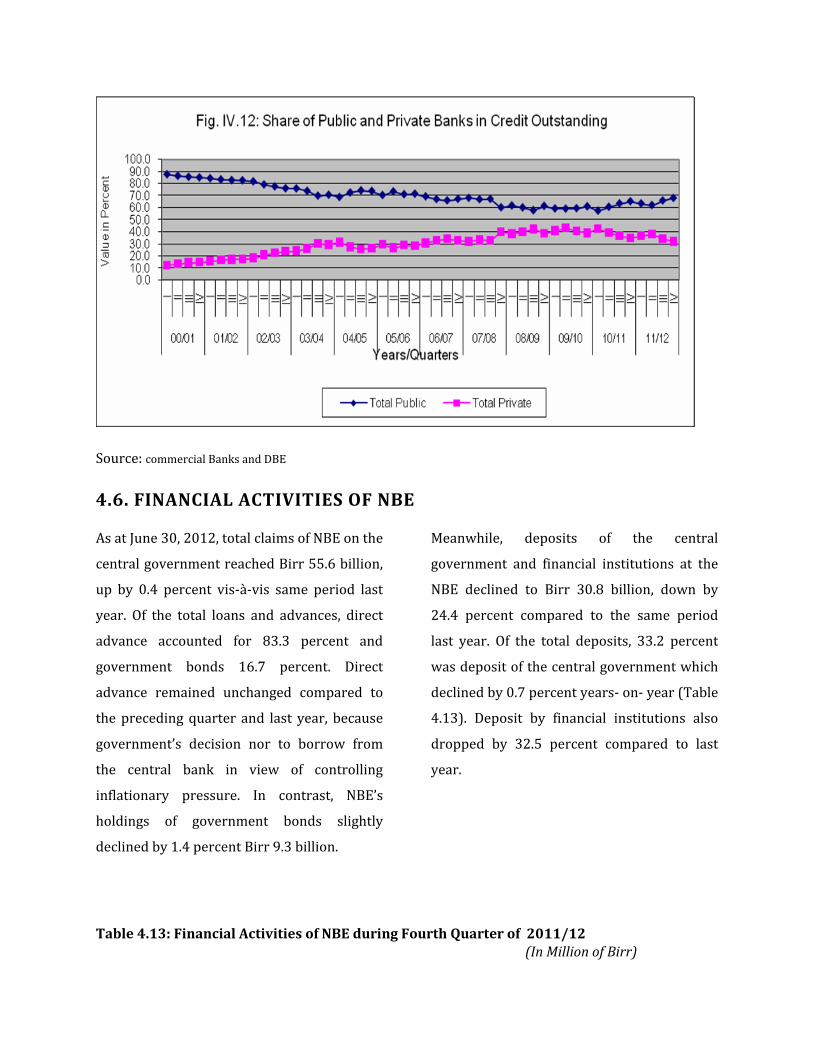

The share of private banks in total

outstanding loan was 32.0 percent

Table4.11:SummaryofloansandadvancesbyBanksandReceivingSectorsduringthefourthquarterof2011/2012(InMillionsofBirr)

PublicBanks PrivateBanks Total

(1) (2) (3)

BorrowingSector D** C** O/S** D** C** O/S** D** C** O/S**CentralGovernment* 0.0 0.0 2755.6 0.0 0.0 1790.0 0.0 0.0 4545.6

Agriculture 5,433.5 3,954.9 16604.1 22.0 97.4 561.5 5455.5 4052.3 17165.6

Industry 6,802.0 1,034.7 28858.8 352.3 515.8 4698.4 7154.4 1550.6 33557.3

DomesticTrade 84.4 304.6 2307.7 678.2 1742.4 9767.1 762.7 2047.0 12074.7InternationalTrade 110.9 252.5 14949.1 957.3 1369.0 10066.3 1068.3 1621.5 25015.4

Export 87.2 101.0 6118.5 341.7 570.4 4602.1 429.0 671.4 10720.6

Imports 23.7 151.6 8830.6 615.6 798.6 5464.2 639.3 950.2 14294.8HotelsandTourism 11.1 30.6 487.7 100.9 75.4 1162.8 112.1 106.0 1650.5Transport&Communication 67.1 191.0 2405.9 283.4 263.8 2023.0 350.5 454.8 4428.9Housing&Construction 849.0 478.3 6667.6 455.0 464.6 5729.9 1304.0 942.8 12397.4Mines,Power&WaterRes. 0.0 0.0 0.0 0.0 1.2 31.9 0.0 1.2 31.9

Others 178.5 244.9 2571.5 65.1 42.1 600.8 243.6 287.0 3172.3

Personal 3.6 6.4 121.4 33.0 39.4 308.7 36.6 45.8 430.1Inter‐BankLending 0.0 29.4 276.4 0.0 0.0 0.0 0.0 29.4 276.4

Total 13,540.2 6,527.4 78,005.7 2,947.4 4,610.9 36,740.4 16,487.6 11,138.3 114,746.1

Source:CommercialBanksandstaffcomputationNotes:*ReferstogovernmentborrowingintheformofbondsandtreasurybillsfromcommercialbanksandothersectorsotherthanNBE

**D=Disbursement,C=Collection,O/S=OutstandingCredit

slightly lower than 33.5 percent in the precedingquarter.

Table4.12:BreakdownofLoans&AdvancesofBankingSystembyClients,duringFourthQuarterof2011/12

(InMillionsofBirr)

Source:CommercialbanksandDBENote:*ReferstogovernmentborrowingintheformofbondsandtreasurybillsfromcommercialbanksandothersectorsotherthanNBE

Particulars

LoanDisbursement %Share

LoanCollection %Share

OutstandingLoan %Share

PublicBanks 13,540.2 82.1 6,527.4 58.6 78,005.7 68.0CentralGovernment* 0.0 0.0 0.0 0.0 2,755.6 3.5StateEnterprises 5,741.2 42.4 711.4 10.9 27,665.6 35.5Cooperatives 5,111.3 37.7 3,744.3 57.4 13,208.1 16.9PrivateEnterprises 2,687.6 19.8 2,042.2 31.3 34,100.0 43.7Inter‐bankLending 0.0 0.0 29.4 0.4 276.4 0.4PrivateBanks 2,947.4 17.9 4,610.9 41.4 36,740.4 32.0CentralGovernment* 0.0 0.0 0.0 0.0 1,790.0 4.9StateEnterprises 0.0 0.0 2.7 0.1 29.3 0.1Cooperatives 18.0 0.6 49.6 1.1 542.1 1.5PrivateEnterprises 2,929.3 99.4 4,558.6 98.9 34,379.1 93.6Inter‐bankLending 0.0 0.0 0.0 0.0 0.0 0.0GrandTotal 16,487.6 100.0 11,138.3 100.0 114,746.1 100.0

Source:commercialBanksandDBE

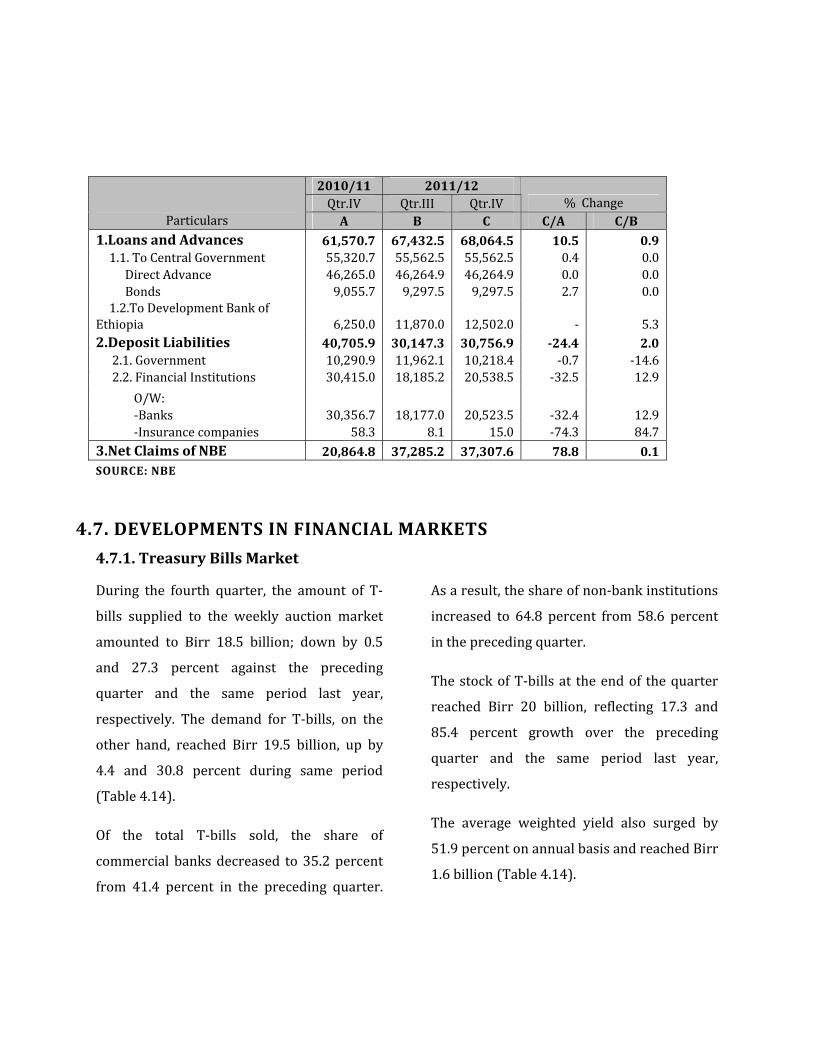

4.6.FINANCIALACTIVITIESOFNBE

AsatJune30,2012,totalclaimsofNBEonthe

centralgovernmentreachedBirr55.6billion,

up by 0.4 percent vis‐à‐vis same period last

year. Of the total loans and advances, direct

advance accounted for 83.3 percent and

government bonds 16.7 percent. Direct

advance remained unchanged compared to

theprecedingquarter and last year, because

government’s decision nor to borrow from

the central bank in view of controlling

inflationary pressure. In contrast, NBE’s

holdings of government bonds slightly

declinedby1.4percentBirr9.3billion.

Meanwhile, deposits of the central

government and financial institutions at the

NBE declined to Birr 30.8 billion, down by

24.4 percent compared to the same period

last year. Of the total deposits, 33.2 percent

wasdepositofthecentralgovernmentwhich

declinedby0.7percentyears‐on‐year(Table

4.13). Deposit by financial institutions also

dropped by 32.5 percent compared to last

year.

Table4.13:FinancialActivitiesofNBEduringFourthQuarterof2011/12

(InMillionofBirr)

SOURCE:NBE

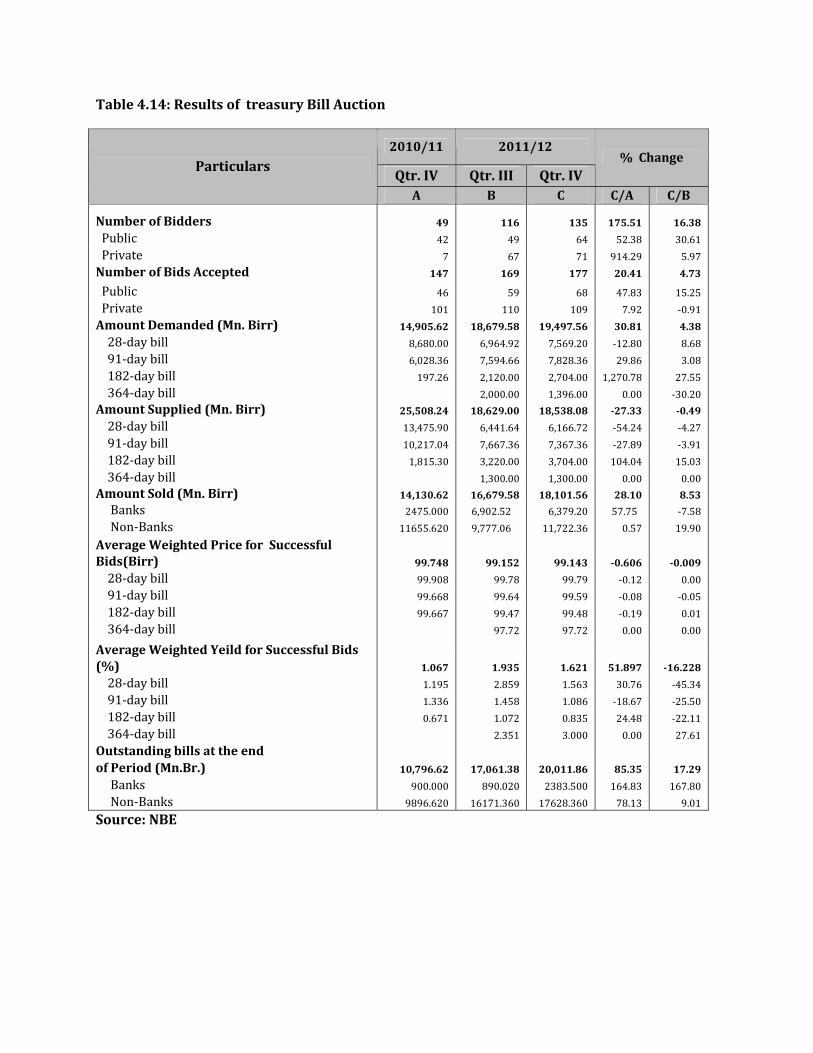

4.7.DEVELOPMENTSINFINANCIALMARKETS

4.7.1.TreasuryBillsMarket

During the fourth quarter, the amount of T‐

bills supplied to the weekly auction market

amounted to Birr 18.5 billion; down by 0.5

and 27.3 percent against the preceding

quarter and the same period last year,

respectively. The demand for T‐bills, on the

other hand, reached Birr 19.5 billion, up by

4.4 and 30.8 percent during same period

(Table4.14).

Of the total T‐bills sold, the share of

commercialbanksdecreased to35.2percent

from 41.4 percent in the preceding quarter.

Asaresult,theshareofnon‐bankinstitutions

increased to 64.8 percent from 58.6 percent

intheprecedingquarter.

ThestockofT‐billsat theendof thequarter

reached Birr 20 billion, reflecting 17.3 and

85.4 percent growth over the preceding

quarter and the same period last year,

respectively.

The average weighted yield also surged by

51.9percentonannualbasisandreachedBirr

1.6billion(Table4.14).

2010/11 2011/12Qtr.IV Qtr.III Qtr.IV %Change

Particulars A B C C/A C/B1.LoansandAdvances 61,570.7 67,432.5 68,064.5 10.5 0.91.1.ToCentralGovernment 55,320.7 55,562.5 55,562.5 0.4 0.0

DirectAdvance 46,265.0 46,264.9 46,264.9 0.0 0.0Bonds 9,055.7 9,297.5 9,297.5 2.7 0.01.2.ToDevelopmentBankof

Ethiopia 6,250.0 11,870.0 12,502.0 ‐ 5.32.DepositLiabilities 40,705.9 30,147.3 30,756.9 ‐24.4 2.02.1.Government 10,290.9 11,962.1 10,218.4 ‐0.7 ‐14.62.2.FinancialInstitutions 30,415.0 18,185.2 20,538.5 ‐32.5 12.9

O/W: ‐Banks 30,356.7 18,177.0 20,523.5 ‐32.4 12.9‐Insurancecompanies 58.3 8.1 15.0 ‐74.3 84.73.NetClaimsofNBE 20,864.8 37,285.2 37,307.6 78.8 0.1

Table4.14:ResultsoftreasuryBillAuction

Source:NBE

2010/11 2011/12

Qtr.IV Qtr.III Qtr.IV%Change

Particulars

A B C C/A C/B

NumberofBidders 49 116 135 175.51 16.38

Public 42 49 64 52.38 30.61

Private 7 67 71 914.29 5.97

NumberofBidsAccepted 147 169 177 20.41 4.73

Public 46 59 68 47.83 15.25

Private 101 110 109 7.92 ‐0.91

AmountDemanded(Mn.Birr) 14,905.62 18,679.58 19,497.56 30.81 4.38

28‐daybill 8,680.00 6,964.92 7,569.20 ‐12.80 8.68

91‐daybill 6,028.36 7,594.66 7,828.36 29.86 3.08

182‐daybill 197.26 2,120.00 2,704.00 1,270.78 27.55

364‐daybill 2,000.00 1,396.00 0.00 ‐30.20

AmountSupplied(Mn.Birr) 25,508.24 18,629.00 18,538.08 ‐27.33 ‐0.49

28‐daybill 13,475.90 6,441.64 6,166.72 ‐54.24 ‐4.27

91‐daybill 10,217.04 7,667.36 7,367.36 ‐27.89 ‐3.91

182‐daybill 1,815.30 3,220.00 3,704.00 104.04 15.03

364‐daybill 1,300.00 1,300.00 0.00 0.00

AmountSold(Mn.Birr) 14,130.62 16,679.58 18,101.56 28.10 8.53

Banks 2475.000 6,902.52 6,379.20 57.75 ‐7.58

Non‐Banks 11655.620 9,777.06 11,722.36 0.57 19.90

AverageWeightedPriceforSuccessfulBids(Birr) 99.748 99.152 99.143 ‐0.606 ‐0.009

28‐daybill 99.908 99.78 99.79 ‐0.12 0.00

91‐daybill 99.668 99.64 99.59 ‐0.08 ‐0.05

182‐daybill 99.667 99.47 99.48 ‐0.19 0.01

364‐daybill 97.72 97.72 0.00 0.00

AverageWeightedYeildforSuccessfulBids(%) 1.067 1.935 1.621 51.897 ‐16.228

28‐daybill 1.195 2.859 1.563 30.76 ‐45.34

91‐daybill 1.336 1.458 1.086 ‐18.67 ‐25.50

182‐daybill 0.671 1.072 0.835 24.48 ‐22.11

364‐daybill 2.351 3.000 0.00 27.61

Outstandingbillsattheend

ofPeriod(Mn.Br.) 10,796.62 17,061.38 20,011.86 85.35 17.29

Banks 900.000 890.020 2383.500 164.83 167.80

Non‐Banks 9896.620 16171.360 17628.360 78.13 9.01

4.7.3.CorporateBondMarket

Corporate bond market is not developed in

Ethiopia; the big players are few public

institutions and regional governments. The

purchaserofthesebondsistheCommercialBank

ofEthiopia(CBE).

Duringthequarterunderreview,CBEpurchased

corporatebondsworthBirr6.6billion,ofwhich

76.3 percent were issued by public enterprises

and the rest by the Addis Ababa City

Administrationtofinancehousingproject.

At the end of June 31, 2012, the stock of

corporate bonds held by the CBE stood at Birr

61.8billion,ofwhich82.2percentwasclaimson

publicenterprisesandtheremainingbalance,on

regional states (Table 4.15). Corporate bonds

issued by EEPCO accounted for 79.1 percent of

thetotaloutstandingcorporatebondbalanceand

96.3 percent of the bonds issued by public

enterprises.

2010/11 2011/12

QIV QIII QIVIssueroftheBond

NP Red O/S NP Red O/S NP Red O/S

1.PuplicEnterprises 2,800.0 4,318.6 31,400.0 6,100.0 0.0 45,800.0 5,000.0 4,318.6 50,770.9

EEPCO 2,600.0 0.0 29,600.0 6,000.0 0.0 43,900.0 5,000.0 0.0 48,900.0

ETC 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

DBE 200.0 4,318.6 1,800.0 100.0 0.0 1,900.0 0.0 4,318.6 1,870.9

2.RegionalGovernments

1,091.0 451.5 8,858.3 1,350.0 449.5 10,222.5 1,550.0 753.9 11,015.8

Oromia 164.0 25.6 2,004.2 0.0 0.0 1993.3 0.0 0.4 1993.0

Amhara 169.0 31.4 1,393.1 0.0 213.0 1080.0 0.0 329.0 751.1

Tigray 85.0 15.0 774.0 0.0 34.1 724.1 0.0 2.4 721.7

SNNPRS 23.0 52.2 988.8 0.0 38.3 821.0 0.0 29.5 791.5

DireDawa 40.0 16.2 213.7 0.0 4.8 216.0 0.0 5.6 210.4

Harari 10.0 16.2 148.9 0.0 12.8 109.6 0.0 14.7 94.8

AddiaAbaba 600.0 294.9 3,335.6 1350.0 146.5 5278.5 1550.0 372.3 6453.4

3.GrandTotal(1+2) 3,891.0 4,770.1 40,258.3 7,450.0 449.5 56,022.5 6,550.0 5,072.5 61,786.7

Source: NBE Note:NP=NewPurchase,Red.=Redemption,O/S=outstanding