Embed Size (px)

Citation preview

New Concession Agreement and Business Plan 2013-2016

Investor PresentationAudio Conference

Fiumicino, February 6th 2013

1

OPENING(Gemina Chairman, Fabrizio Palenzona)

1. 2012 HIGHLIGHTS(ADR Chief Executive Officer, Lorenzo Lo Presti)

2. NEW CONCESSION AGREEMENT (Gemina Chief Executive Officer, Carlo Bertazzo)

3. DEVELOPMENT OUTLOOK AND BUSINESS PLAN 2013-2016 HIGHLIGHTS(ADR Chief Executive Officer, Lorenzo Lo Presti)

4. RATIONALE OF THE POTENTIAL INTEGRATION WITH ATLANTIA(Gemina Chairman, Fabrizio Palenzona)

5. CLOSING REMARKS(Gemina Chairman, Fabrizio Palenzona)

Q&A SESSION

Agenda

2

OPENING(Gemina Chairman, Fabrizio Palenzona)

3

1. 2012 HIGHLIGHTS(ADR Chief Executive Officer, Lorenzo Lo Presti)

4

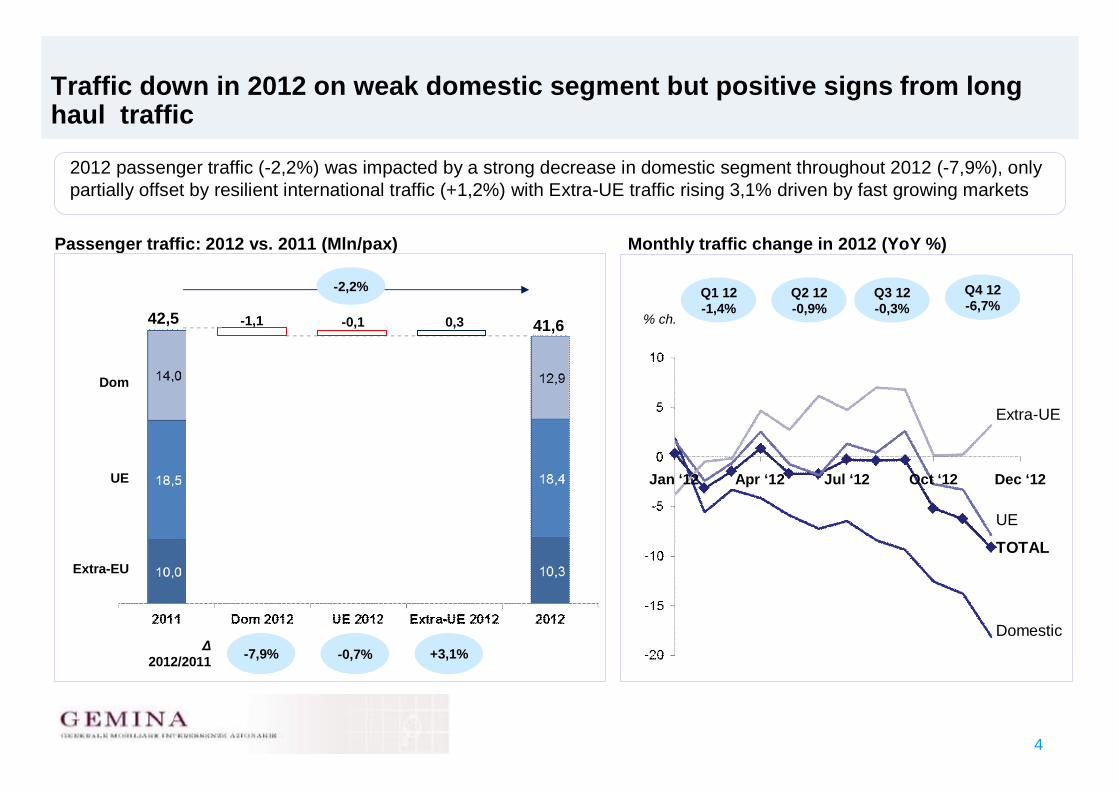

Traffic down in 2012 on weak domestic segment but positive signs from long haul traffic

2012 passenger traffic (-2,2%) was impacted by a strong decrease in domestic segment throughout 2012 (-7,9%), only partially offset by resilient international traffic (+1,2%) with Extra-UE traffic rising 3,1% driven by fast growing markets

Passenger traffic: 2012 vs. 2011 (Mln/pax) Monthly traffic change in 2012 (YoY %)

-7,9% -0,7% +3,1%

42,5 41,6

Extra-EU

Dom

UE

Δ2012/2011

Dec ‘12Oct ‘12Jul ‘12Apr ‘12Jan ‘12

Q1 12-1,4%

Q2 12-0,9%

Q3 12-0,3%

Q4 12-6,7%

% ch.

TOTAL

UE

Extra-UE

Domestic

-1,1 -0,1 0,3

-2,2%

5

Alitalia and other domestic carriers had a negative year…

• 2012 weak Italian GDP (-2,3%) affected performance of domestic traffic (33% of total traffic) and in particular Fiumicino's hub-carrier that boasts a 55% share of total Italian traffic

• Domestic traffic was also hit by the consequences of Wind Jet's bankruptcy in August 2012 and Blue Panorama's procedure for composition with creditors

Monthly traffic change in 2012 at Fiumicino (YoY %)

Pax: 16,7 Mln Mkt share: 45,8%

Pax: 20,3 Mln Mkt share: 54,9%

-4,6DomesticUEExtra-UE

Total-6,4-6,5+2,1

-808-663 -254 +79

+0,9DomesticUEExtra-UE

Total-16,0+3,6+4,6

+177-500+397+280

Other carriers

Blue PanoramaMeridianaeasyJetWind JetTotal:

-138.000 pax-56.700 pax-15.900 pax

-276.000 pax-486.600 pax

Pax 2012(mln)

9,33,63,8

Mkt share (%)

55,621,622,8

Δ2012/2011

(%)

Δ2012/2011(000/pax)

16,7

Traffic performance of Alitalia and other carriers

45,8---

---

20,3 54,92,6

11,46,3

12,856,231,0

AugAprFeb JulMayMar NovJun Sep DecOctJan

Other carriers

6

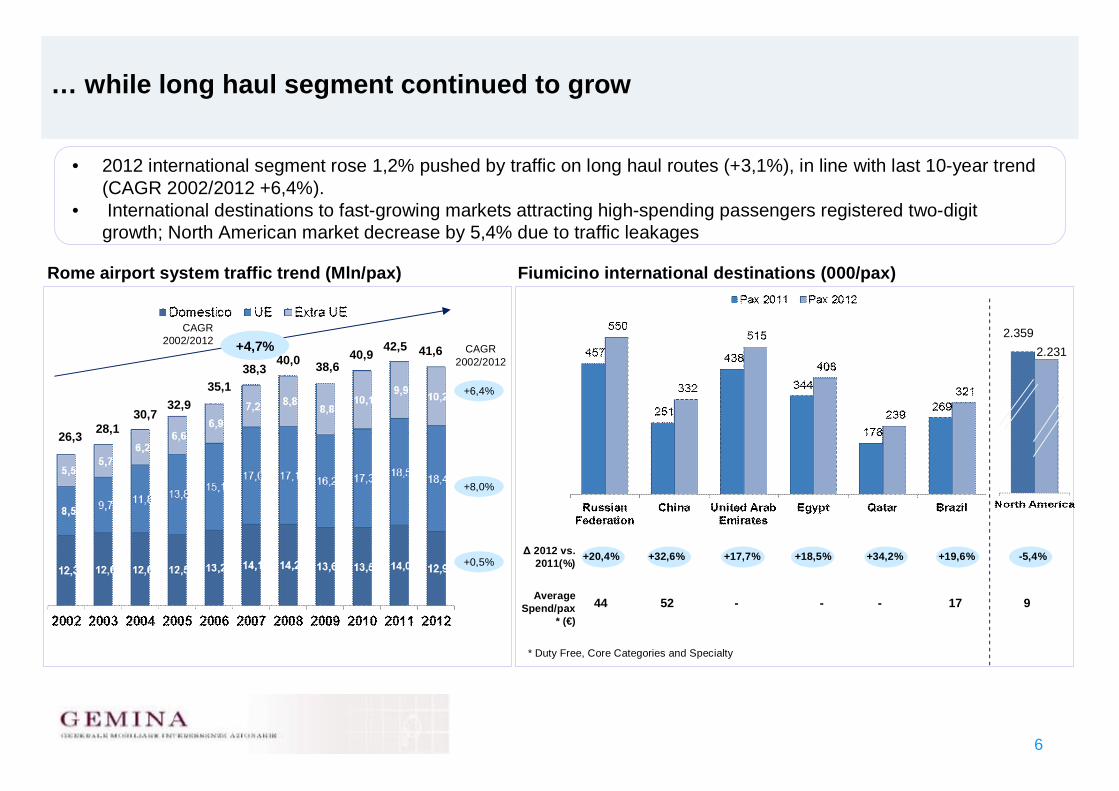

… while long haul segment continued to grow

• 2012 international segment rose 1,2% pushed by traffic on long haul routes (+3,1%), in line with last 10-year trend (CAGR 2002/2012 +6,4%).

• International destinations to fast-growing markets attracting high-spending passengers registered two-digit growth; North American market decrease by 5,4% due to traffic leakages

Fiumicino international destinations (000/pax)Rome airport system traffic trend (Mln/pax)

+20,4% +32,6% +17,7% +18,5% +19,6%+34,2%Δ 2012 vs. 2011(%)

2.3592.231

-5,4%

AverageSpend/pax

* (€)44 52 - - 17- 9

* Duty Free, Core Categories and Specialty

26,3 28,130,7

32,935,1

38,340,0 38,6

40,9 42,5 41,6+4,7%

+0,5%

+8,0%

+6,4%

CAGR 2002/2012

CAGR 2002/2012

7

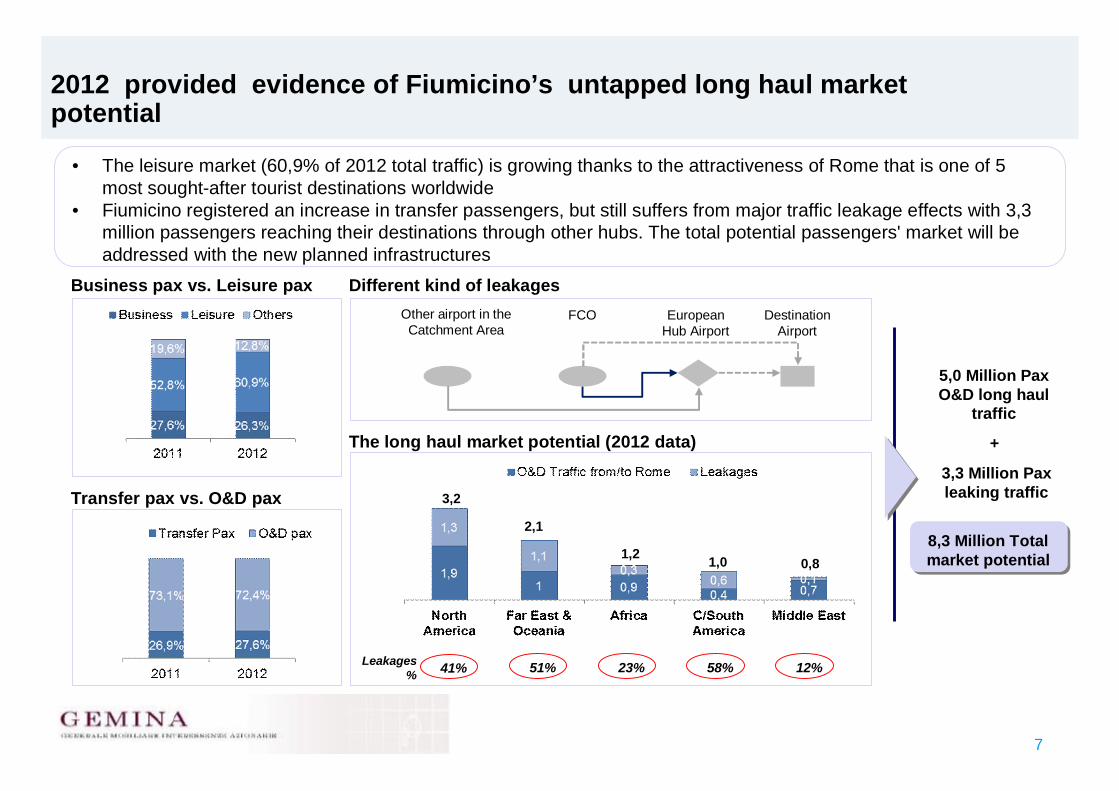

2012 provided evidence of Fiumicino’s untapped long haul market potential

• The leisure market (60,9% of 2012 total traffic) is growing thanks to the attractiveness of Rome that is one of 5 most sought-after tourist destinations worldwide

• Fiumicino registered an increase in transfer passengers, but still suffers from major traffic leakage effects with 3,3 million passengers reaching their destinations through other hubs. The total potential passengers' market will be addressed with the new planned infrastructures

Different kind of leakages

5,0 Million Pax O&D long haul

traffic

3,3 Million Pax leaking traffic

8,3 Million Total market potential

+

Transfer pax vs. O&D pax

Business pax vs. Leisure pax

41% 51% 23% 58% 12%

3,2

2,1

1,2 1,0 0,8

Leakages %

Other airport in the Catchment Area

FCO European Hub Airport

Destination Airport

The long haul market potential (2012 data)

8

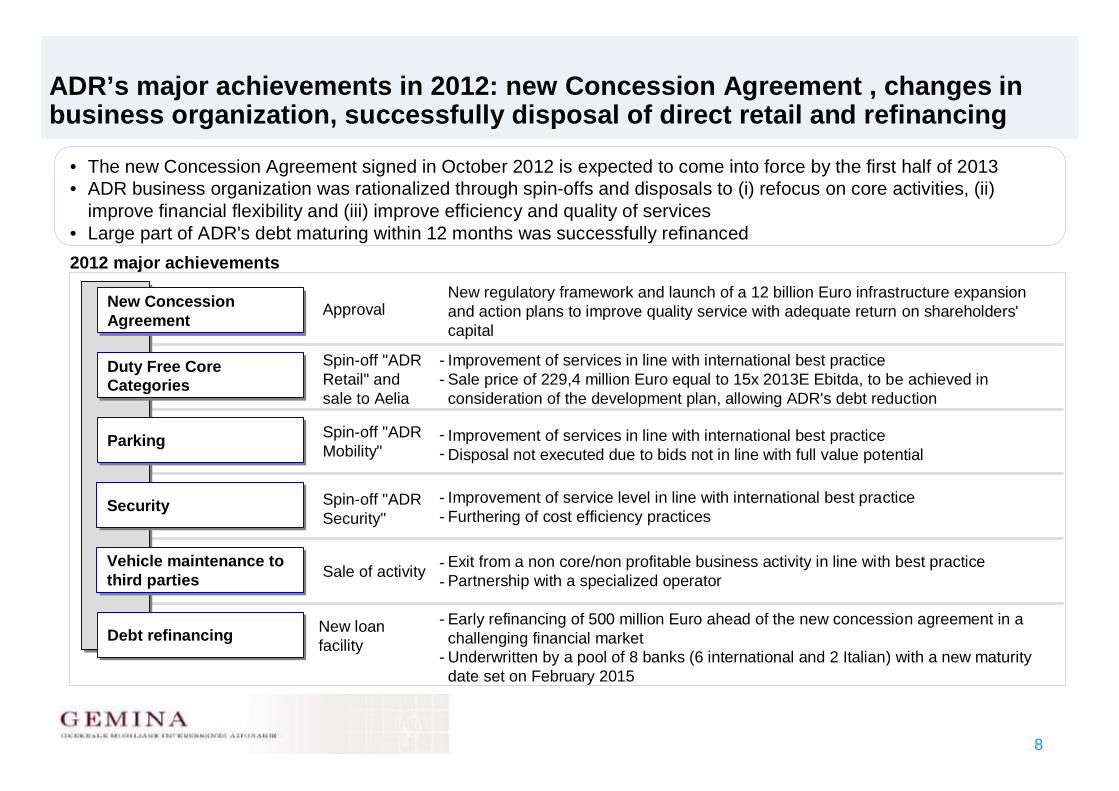

ADR’s major achievements in 2012: new Concession Agreement , changes in business organization, successfully disposal of direct retail and refinancing

• The new Concession Agreement signed in October 2012 is expected to come into force by the first half of 2013• ADR business organization was rationalized through spin-offs and disposals to (i) refocus on core activities, (ii)

improve financial flexibility and (iii) improve efficiency and quality of services• Large part of ADR's debt maturing within 12 months was successfully refinanced

Spin-off "ADR Retail" and sale to Aelia

Improvement of services in line with international best practiceSale price of 229,4 million Euro equal to 15x 2013E Ebitda, to be achieved in consideration of the development plan, allowing ADR's debt reduction

Spin-off "ADR Mobility"

Spin-off "ADR Security"

Sale of activity

Improvement of services in line with international best practiceDisposal not executed due to bids not in line with full value potential

Improvement of service level in line with international best practiceFurthering of cost efficiency practices

Exit from a non core/non profitable business activity in line with best practicePartnership with a specialized operator

2012 major achievements

Duty Free Core CategoriesDuty Free Core Categories

ParkingParking

SecuritySecurity

Vehicle maintenance to third partiesVehicle maintenance to third parties

New Concession AgreementNew Concession Agreement

Debt refinancingDebt refinancing

New regulatory framework and launch of a 12 billion Euro infrastructure expansion and action plans to improve quality service with adequate return on shareholders' capital

Approval

--

--

--

New loan facility

Early refinancing of 500 million Euro ahead of the new concession agreement in a challenging financial market Underwritten by a pool of 8 banks (6 international and 2 Italian) with a new maturity date set on February 2015

--

-

-

9

2. NEW CONCESSION AGREEMENT (Gemina Chief Executive Officer, Carlo Bertazzo)

10

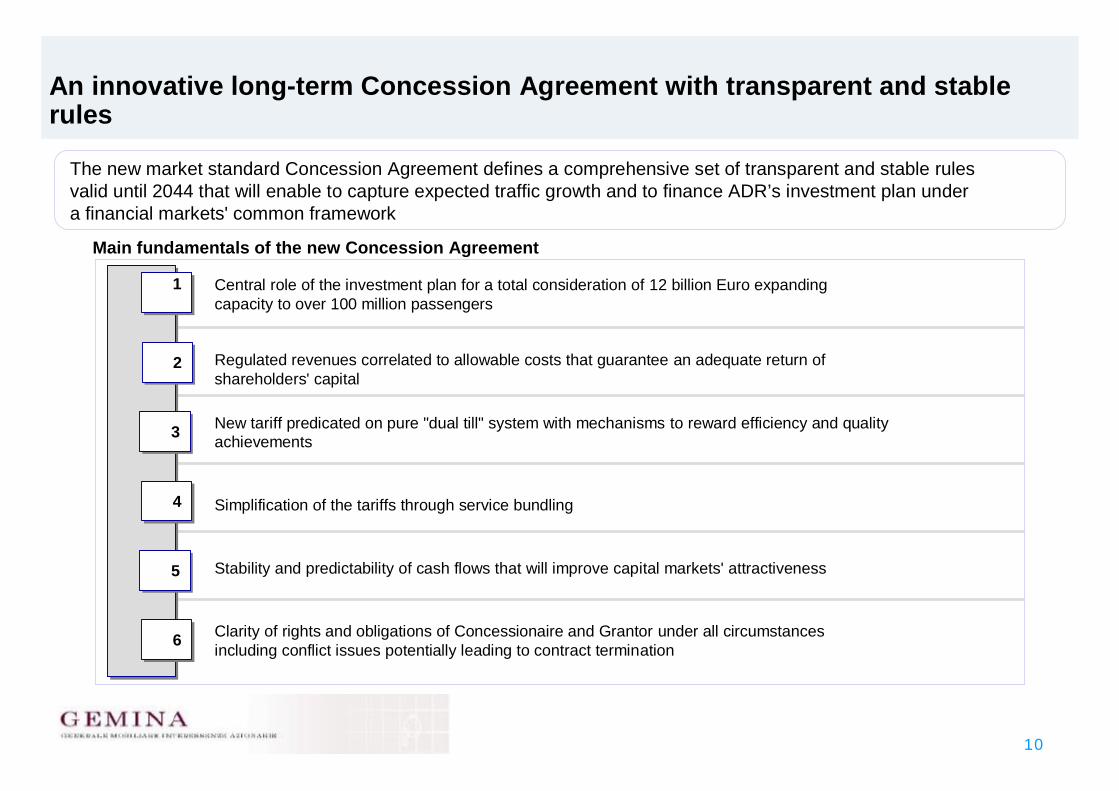

An innovative long-term Concession Agreement with transparent and stable rules

The new market standard Concession Agreement defines a comprehensive set of transparent and stable rules valid until 2044 that will enable to capture expected traffic growth and to finance ADR’s investment plan under a financial markets' common framework

Main fundamentals of the new Concession Agreement

11

22

33

44

55

66

Central role of the investment plan for a total consideration of 12 billion Euro expanding capacity to over 100 million passengers

Regulated revenues correlated to allowable costs that guarantee an adequate return of shareholders' capital

New tariff predicated on pure "dual till" system with mechanisms to reward efficiency and quality achievements

Simplification of the tariffs through service bundling

Clarity of rights and obligations of Concessionaire and Grantor under all circumstances including conflict issues potentially leading to contract termination

Stability and predictability of cash flows that will improve capital markets' attractiveness

11

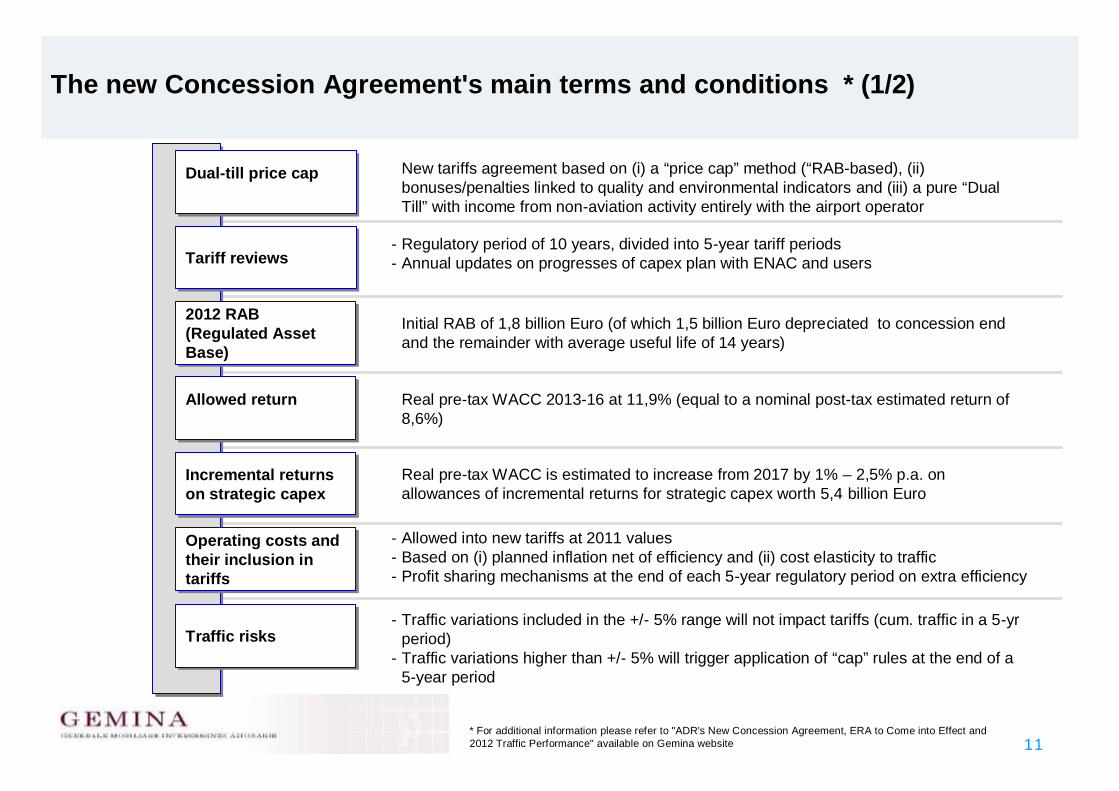

New tariffs agreement based on (i) a “price cap” method (“RAB-based), (ii) bonuses/penalties linked to quality and environmental indicators and (iii) a pure “Dual Till” with income from non-aviation activity entirely with the airport operator

Regulatory period of 10 years, divided into 5-year tariff periodsAnnual updates on progresses of capex plan with ENAC and users

Initial RAB of 1,8 billion Euro (of which 1,5 billion Euro depreciated to concession end and the remainder with average useful life of 14 years)

Real pre-tax WACC 2013-16 at 11,9% (equal to a nominal post-tax estimated return of 8,6%)

--

Dual-till price capDual-till price cap

Tariff reviewsTariff reviews

2012 RAB (Regulated Asset Base)

2012 RAB (Regulated Asset Base)

Allowed returnAllowed return

* For additional information please refer to "ADR's New Concession Agreement, ERA to Come into Effect and 2012 Traffic Performance" available on Gemina website

Real pre-tax WACC is estimated to increase from 2017 by 1% – 2,5% p.a. on allowances of incremental returns for strategic capex worth 5,4 billion Euro

Allowed into new tariffs at 2011 valuesBased on (i) planned inflation net of efficiency and (ii) cost elasticity to trafficProfit sharing mechanisms at the end of each 5-year regulatory period on extra efficiency

Traffic variations included in the +/- 5% range will not impact tariffs (cum. traffic in a 5-yr period)Traffic variations higher than +/- 5% will trigger application of “cap” rules at the end of a 5-year period

Incremental returns on strategic capex Incremental returns on strategic capex

Operating costs and their inclusion in tariffs

Operating costs and their inclusion in tariffs

Traffic risksTraffic risks

---

The new Concession Agreement's main terms and conditions * (1/2)

-

-

12

The new Concession Agreement's main terms and conditions (2/2)

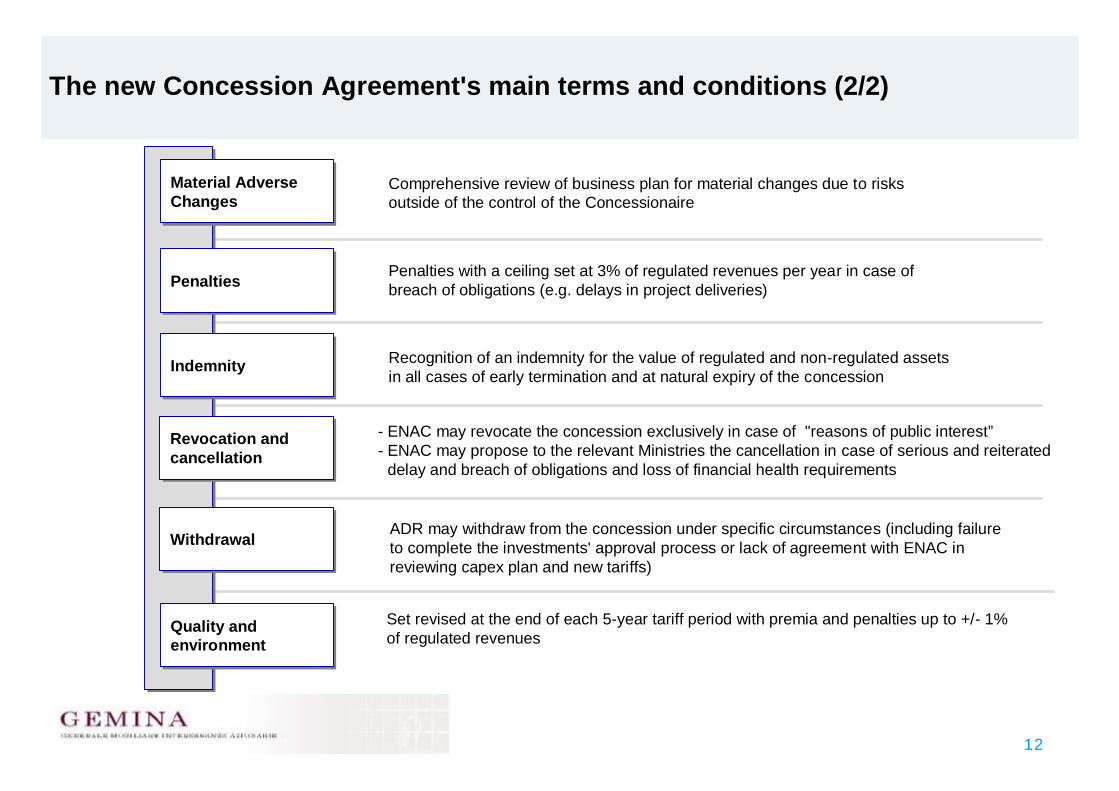

Comprehensive review of business plan for material changes due to risks outside of the control of the Concessionaire

ADR may withdraw from the concession under specific circumstances (including failure to complete the investments' approval process or lack of agreement with ENAC in reviewing capex plan and new tariffs)

Material Adverse ChangesMaterial Adverse Changes

Revocation and cancellation Revocation and cancellation

WithdrawalWithdrawal

PenaltiesPenalties Penalties with a ceiling set at 3% of regulated revenues per year in case of breach of obligations (e.g. delays in project deliveries)

Recognition of an indemnity for the value of regulated and non-regulated assets in all cases of early termination and at natural expiry of the concessionIndemnityIndemnity

ENAC may revocate the concession exclusively in case of "reasons of public interest”ENAC may propose to the relevant Ministries the cancellation in case of serious and reiterated delay and breach of obligations and loss of financial health requirements

--

Quality and environmentQuality and environment

Set revised at the end of each 5-year tariff period with premia and penalties up to +/- 1% of regulated revenues

13

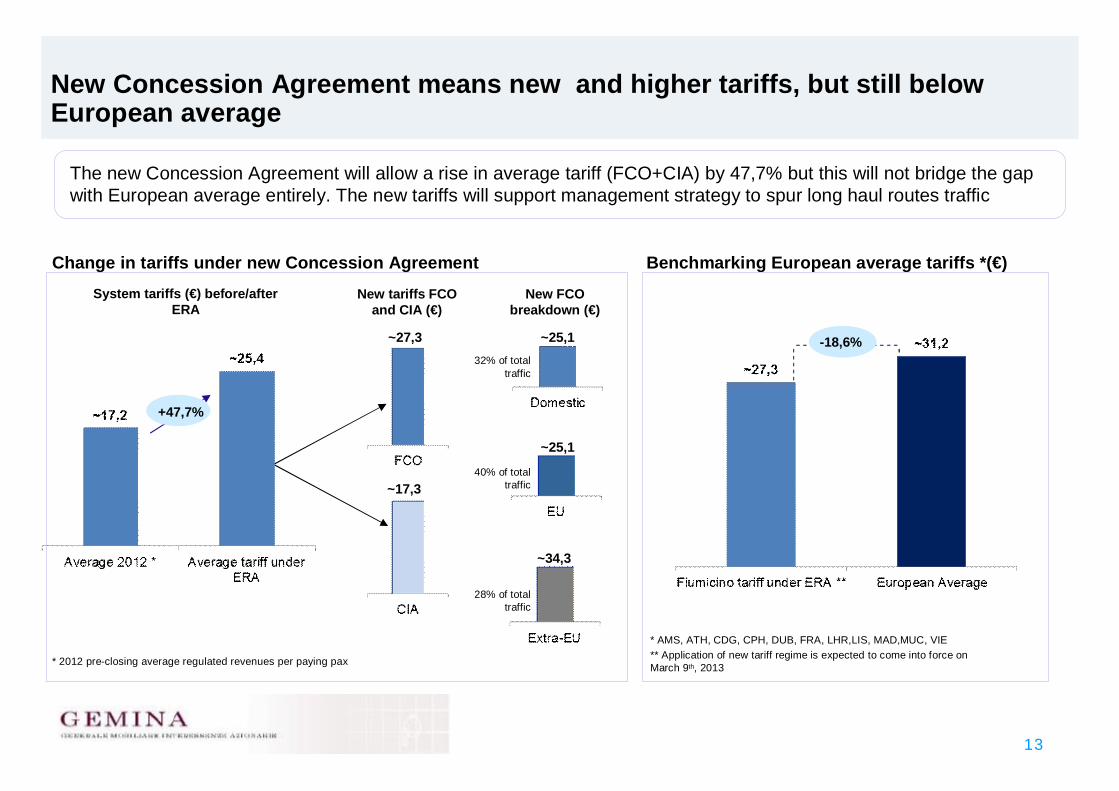

New Concession Agreement means new and higher tariffs, but still below European average

System tariffs (€) before/after ERA

Benchmarking European average tariffs *(€)

New tariffs FCO and CIA (€)

New FCO breakdown (€)

* 2012 pre-closing average regulated revenues per paying pax

The new Concession Agreement will allow a rise in average tariff (FCO+CIA) by 47,7% but this will not bridge the gap with European average entirely. The new tariffs will support management strategy to spur long haul routes traffic

+47,7%

Change in tariffs under new Concession Agreement

* AMS, ATH, CDG, CPH, DUB, FRA, LHR,LIS, MAD,MUC, VIE** Application of new tariff regime is expected to come into force on March 9th, 2013

~27,3

~17,3

~25,1

~25,1

~34,3

32% of total traffic

40% of total traffic

28% of total traffic

-18,6%

14

3. DEVELOPMENT OUTLOOK AND BUSINESS PLAN 2013-2016 HIGHLIGHTS(ADR Chief Executive Officer, Lorenzo Lo Presti)

15

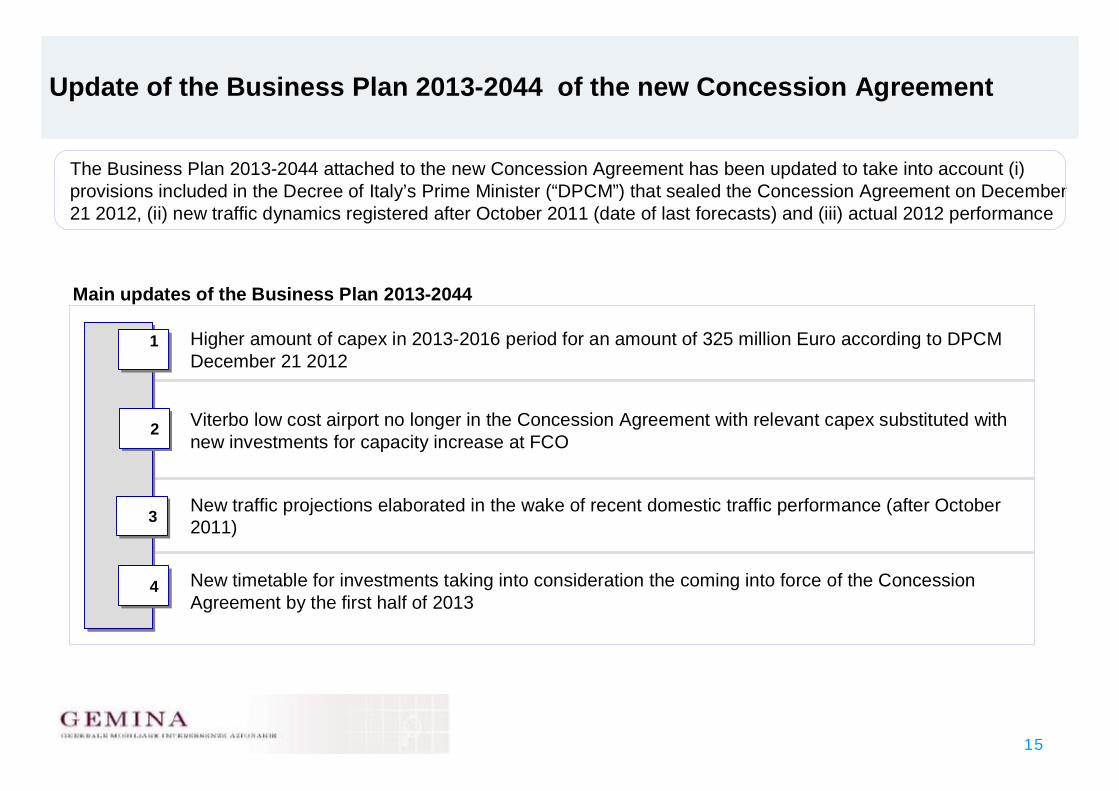

Update of the Business Plan 2013-2044 of the new Concession Agreement

Main updates of the Business Plan 2013-2044

Viterbo low cost airport no longer in the Concession Agreement with relevant capex substituted withnew investments for capacity increase at FCO

Higher amount of capex in 2013-2016 period for an amount of 325 million Euro according to DPCM December 21 2012

New timetable for investments taking into consideration the coming into force of the Concession Agreement by the first half of 2013

11

22

33

44

The Business Plan 2013-2044 attached to the new Concession Agreement has been updated to take into account (i) provisions included in the Decree of Italy’s Prime Minister (“DPCM”) that sealed the Concession Agreement on December 21 2012, (ii) new traffic dynamics registered after October 2011 (date of last forecasts) and (iii) actual 2012 performance

New traffic projections elaborated in the wake of recent domestic traffic performance (after October 2011)

16

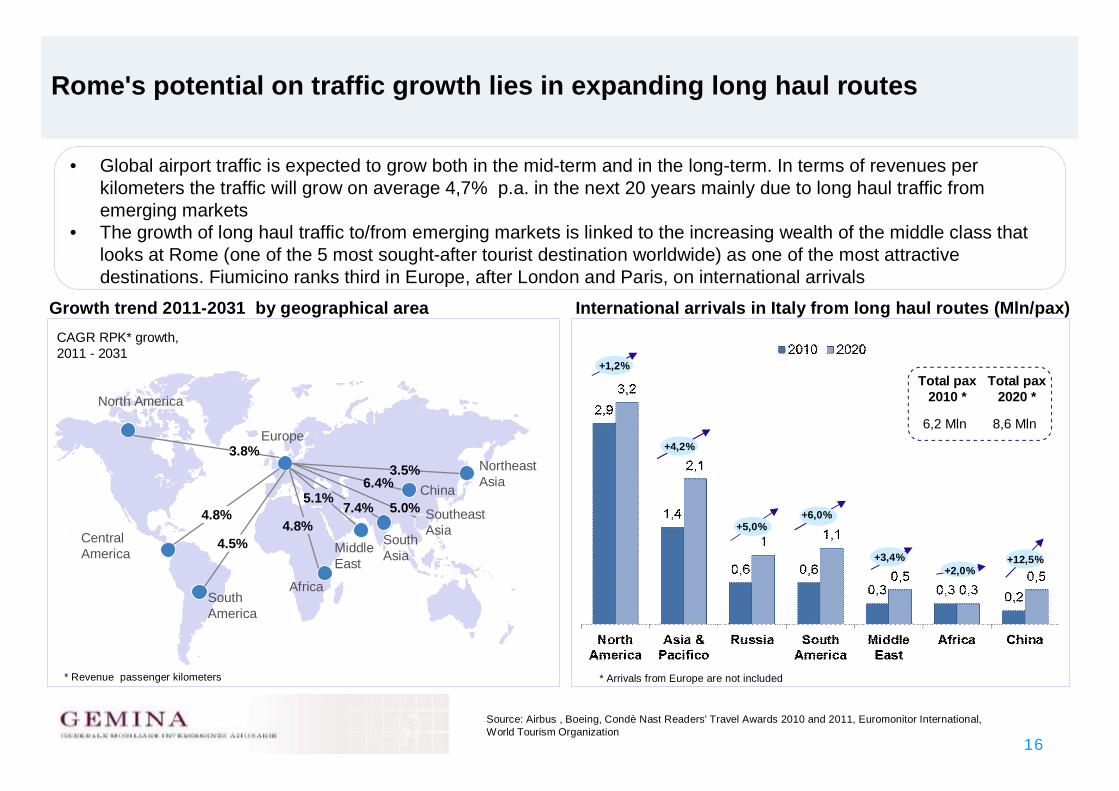

Rome's potential on traffic growth lies in expanding long haul routes

• Global airport traffic is expected to grow both in the mid-term and in the long-term. In terms of revenues per kilometers the traffic will grow on average 4,7% p.a. in the next 20 years mainly due to long haul traffic from emerging markets

• The growth of long haul traffic to/from emerging markets is linked to the increasing wealth of the middle class that looks at Rome (one of the 5 most sought-after tourist destination worldwide) as one of the most attractive destinations. Fiumicino ranks third in Europe, after London and Paris, on international arrivals

Source: Airbus , Boeing, Condè Nast Readers' Travel Awards 2010 and 2011, Euromonitor International, World Tourism Organization

Growth trend 2011-2031 by geographical area

North America

Europe

MiddleEast

SouthAmerica

Africa

CentralAmerica

4.8%4.8%

3.8%

4.5%

5.1%5.0%

SouthAsia

SoutheastAsia

7.4%

NortheastAsia

3.5%China6.4%

CAGR RPK* growth, 2011 - 2031

* Revenue passenger kilometers

International arrivals in Italy from long haul routes (Mln/pax)

+1,2%

+4,2%

+5,0%+6,0%

+3,4%+2,0%

+12,5%

Total pax 2010 *

Total pax 2020 *

6,2 Mln 8,6 Mln

* Arrivals from Europe are not included

17

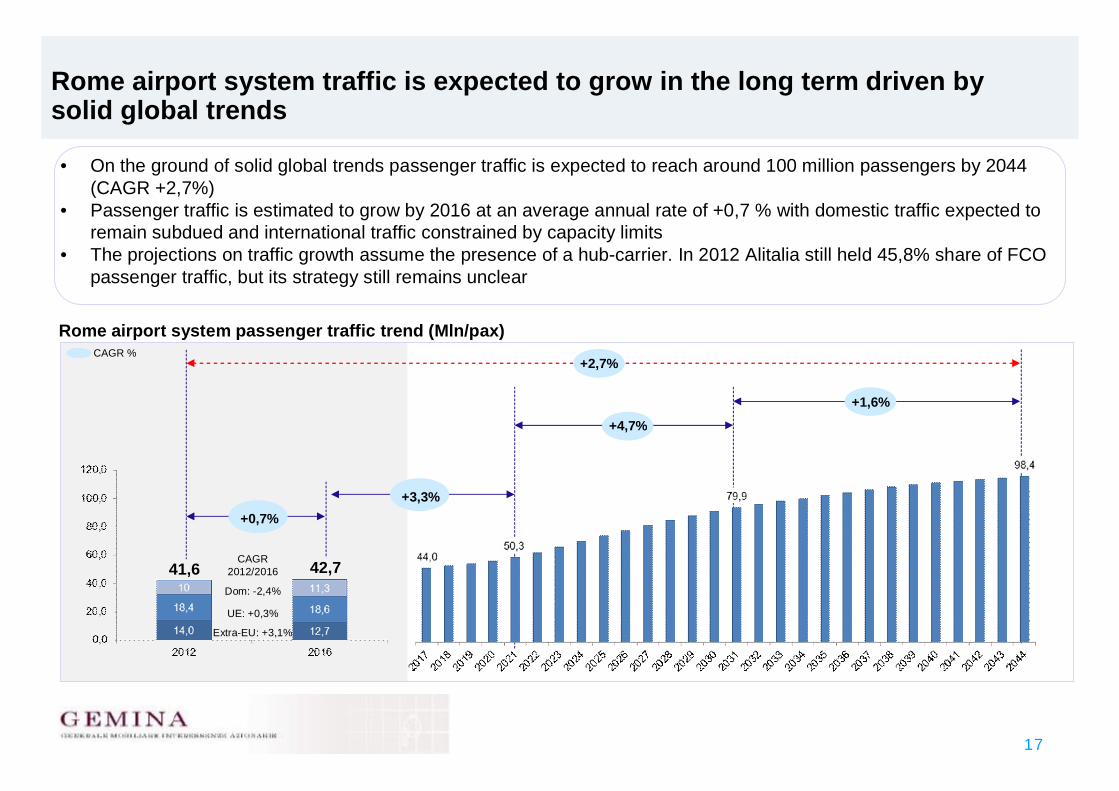

Rome airport system passenger traffic trend (Mln/pax)

• On the ground of solid global trends passenger traffic is expected to reach around 100 million passengers by 2044 (CAGR +2,7%)

• Passenger traffic is estimated to grow by 2016 at an average annual rate of +0,7 % with domestic traffic expected to remain subdued and international traffic constrained by capacity limits

• The projections on traffic growth assume the presence of a hub-carrier. In 2012 Alitalia still held 45,8% share of FCO passenger traffic, but its strategy still remains unclear

Rome airport system traffic is expected to grow in the long term driven by solid global trends

41,6

+4,7%

+1,6%

+2,7%

42,7

+0,7%

Extra-EU: +3,1%

Dom: -2,4%

UE: +0,3%

+3,3%

CAGR %

CAGR 2012/2016

18

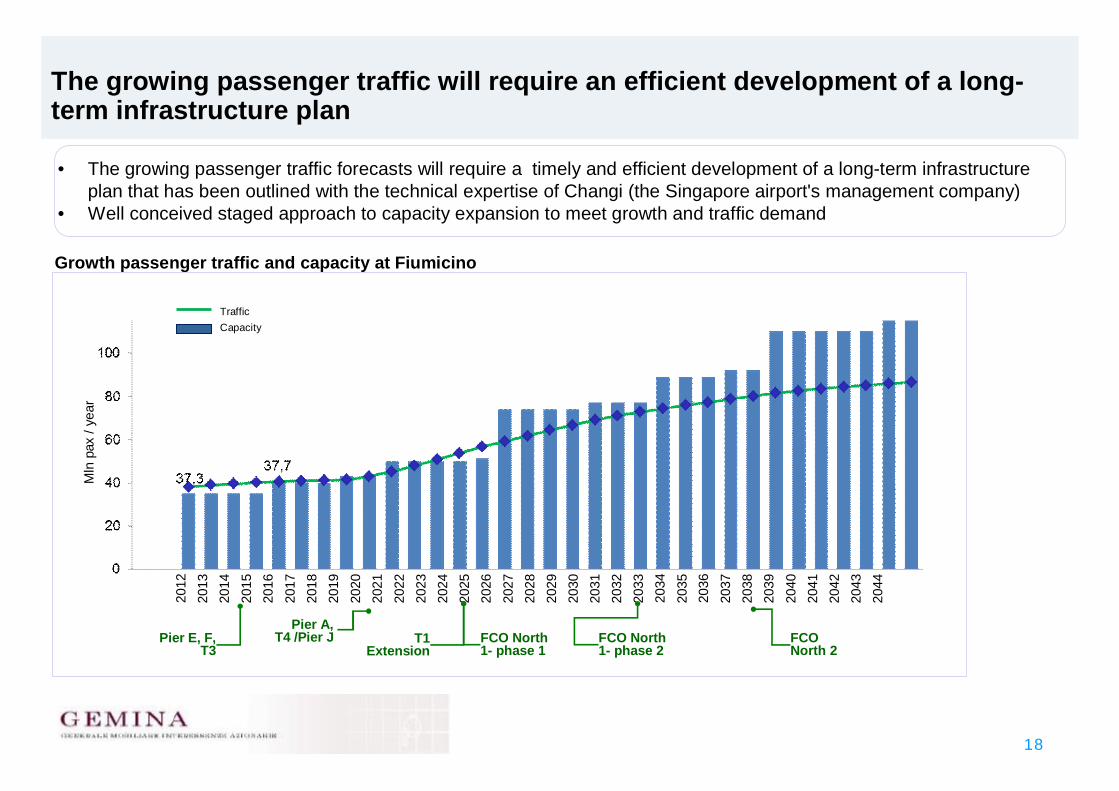

The growing passenger traffic will require an efficient development of a long-term infrastructure plan

Growth passenger traffic and capacity at Fiumicino

• The growing passenger traffic forecasts will require a timely and efficient development of a long-term infrastructure plan that has been outlined with the technical expertise of Changi (the Singapore airport's management company)

• Well conceived staged approach to capacity expansion to meet growth and traffic demand

2032

2044

2033

2039

2038

2036

2035

2043

2042

2037

2041

2040

2034

2031

2030

2029

2028

2027

2026

2025

2024

2023

2022

2021

2020

2019

2018

2017

2013

2016

2014

2015

2012

Mln

pax

/ ye

ar

Pier E, F, T3

Pier A, T4 /Pier J T1

ExtensionFCO North 1- phase 1

FCO North 1- phase 2

FCO North 2

TrafficCapacity

19

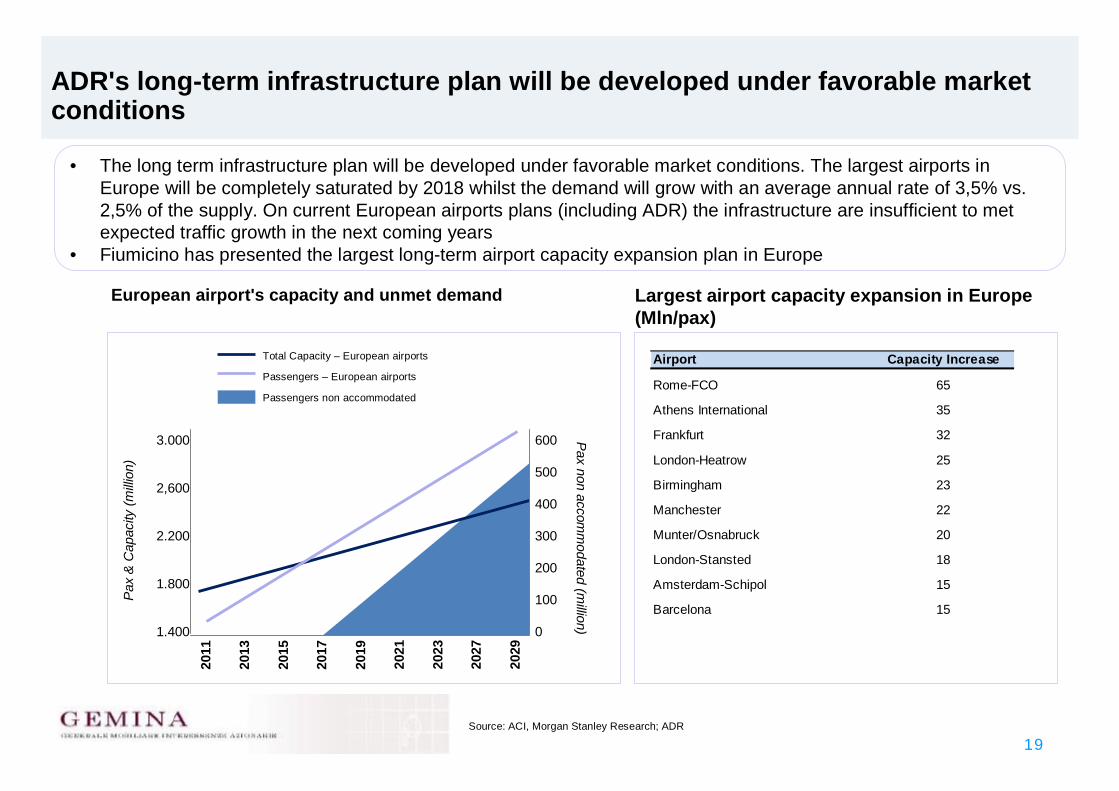

ADR's long-term infrastructure plan will be developed under favorable market conditions

• The long term infrastructure plan will be developed under favorable market conditions. The largest airports in Europe will be completely saturated by 2018 whilst the demand will grow with an average annual rate of 3,5% vs. 2,5% of the supply. On current European airports plans (including ADR) the infrastructure are insufficient to met expected traffic growth in the next coming years

• Fiumicino has presented the largest long-term airport capacity expansion plan in Europe

European airport's capacity and unmet demand

Source: ACI, Morgan Stanley Research; ADR

Largest airport capacity expansion in Europe (Mln/pax)

3.000

2,600

2.200

1.800

1.400

2011

2013

2015

2019

2017

2021

2027

2023

2029

600

500

400

300

200

100

0

Pax

& C

apac

ity (m

illion

)

Pax non accom

modated (m

illion)

Total Capacity – European airports

Passengers – European airports

Passengers non accommodated

Airport Capacity Increase

Rome-FCO 65

Athens International 35

Frankfurt 32

London-Heatrow 25

Birmingham 23

Manchester 22

Munter/Osnabruck 20

London-Stansted 18

Amsterdam-Schipol 15

Barcelona 15

20

At the onset of the 12 billion Euro infrastructure development plan capex will step up vs. historical level

Mid-term investment plan (Mln/€)

• ADR has projected a long-term infrastructure development plan for a total consideration of 12 billion Euro, of which (i) 4,4 billion Euro Fiumicino South, (ii) 7,2 billion Euro new Fiumicino North, (iii) 0,2 billion Euro to convert Ciampino into a city airport and (iv) and 0,2 billion Euro of remaining investment

• The long-term infrastructure development plan will trigger total job growth of 230.000, of which around 30.000 in the first ten years

• Until 2016 capex is estimated to grow at an average annual amount more than 6x 2012 figure

Renovation of land side terminal and facilities, e.g. area international arrivals and toilettes (by 2013)

New pavement in front of the airport (by 2013)

Construction of new Pier C and expansion of Terminal 3 (within the next 4 years)

New baggage sorting system (by 2015)

Extension of parking areas for aircraft (by 2016)

Renovation of runways and "people mover" to efficiently connect airport facilities (within the next 4 years)

-

-

-

-

-

-

Main capex

Cumulative capex2012-2016:

~ 1.260

21

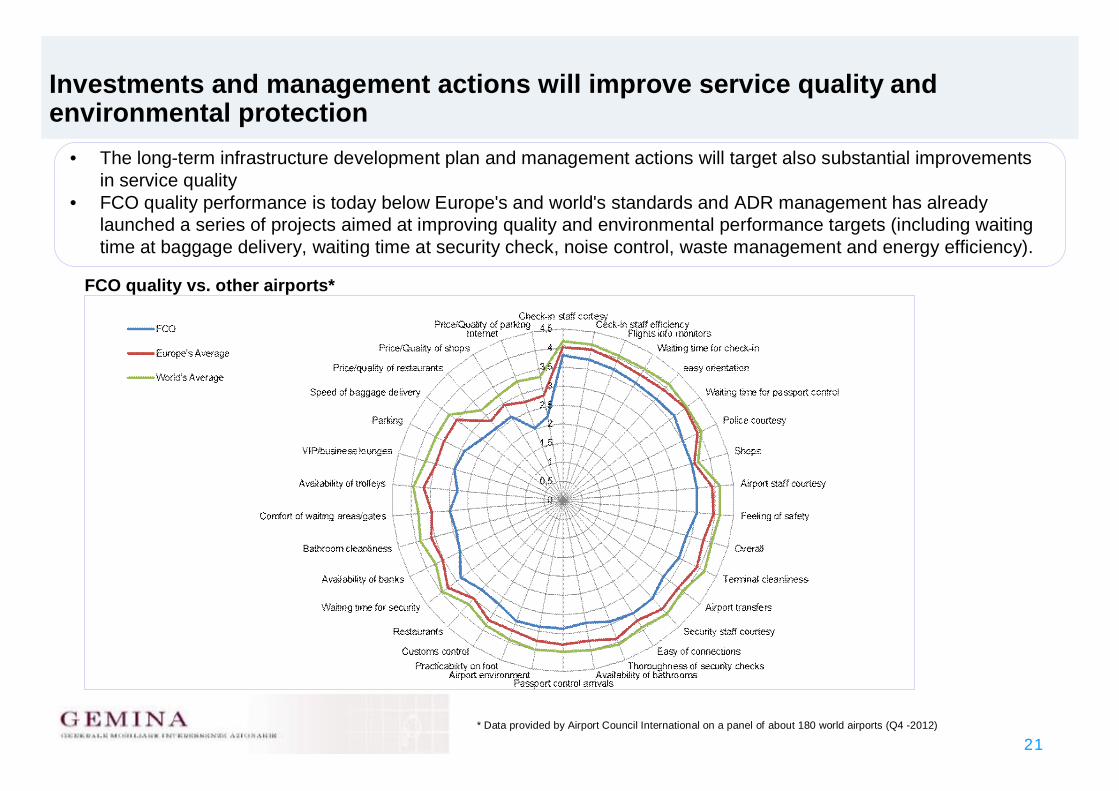

Investments and management actions will improve service quality and environmental protection

FCO quality vs. other airports*

• The long-term infrastructure development plan and management actions will target also substantial improvements in service quality

• FCO quality performance is today below Europe's and world's standards and ADR management has already launched a series of projects aimed at improving quality and environmental performance targets (including waiting time at baggage delivery, waiting time at security check, noise control, waste management and energy efficiency).

* Data provided by Airport Council International on a panel of about 180 world airports (Q4 -2012)

22

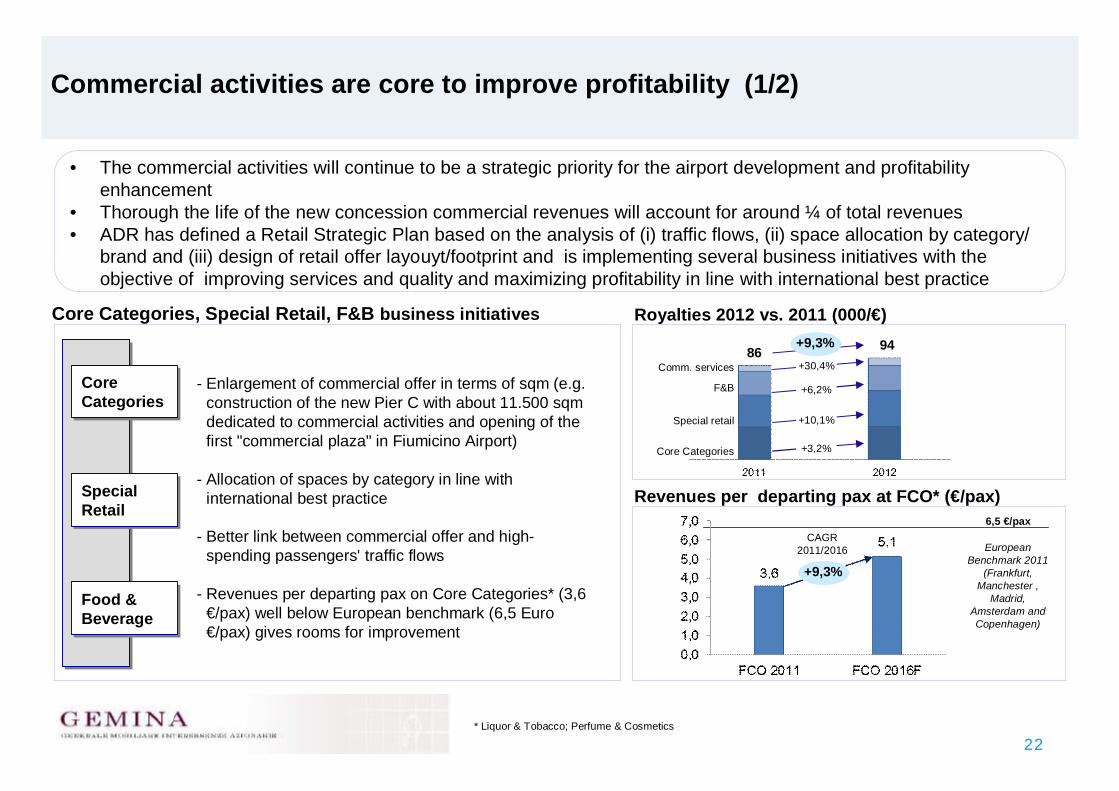

Commercial activities are core to improve profitability (1/2)

Core Categories, Special Retail, F&B business initiatives

• The commercial activities will continue to be a strategic priority for the airport development and profitability enhancement

• Thorough the life of the new concession commercial revenues will account for around ¼ of total revenues• ADR has defined a Retail Strategic Plan based on the analysis of (i) traffic flows, (ii) space allocation by category/

brand and (iii) design of retail offer layouyt/footprint and is implementing several business initiatives with the objective of improving services and quality and maximizing profitability in line with international best practice

Special RetailSpecial Retail

Enlargement of commercial offer in terms of sqm (e.g. construction of the new Pier C with about 11.500 sqm dedicated to commercial activities and opening of the first "commercial plaza" in Fiumicino Airport)

Allocation of spaces by category in line with international best practice

Better link between commercial offer and high-spending passengers' traffic flows

Revenues per departing pax on Core Categories* (3,6 €/pax) well below European benchmark (6,5 Euro €/pax) gives rooms for improvement

Core CategoriesCore Categories

Food & BeverageFood & Beverage

European Benchmark 2011

(Frankfurt, Manchester ,

Madrid, Amsterdam and Copenhagen)

Revenues per departing pax at FCO* (€/pax)

Royalties 2012 vs. 2011 (000/€)

-

-

-

-

+3,2%

+10,1%

+6,2%

+30,4%

Core Categories

Special retail

F&B

Comm. services86 94

6,5 €/pax

* Liquor & Tobacco; Perfume & Cosmetics

+9,3%

+9,3%

CAGR 2011/2016

23

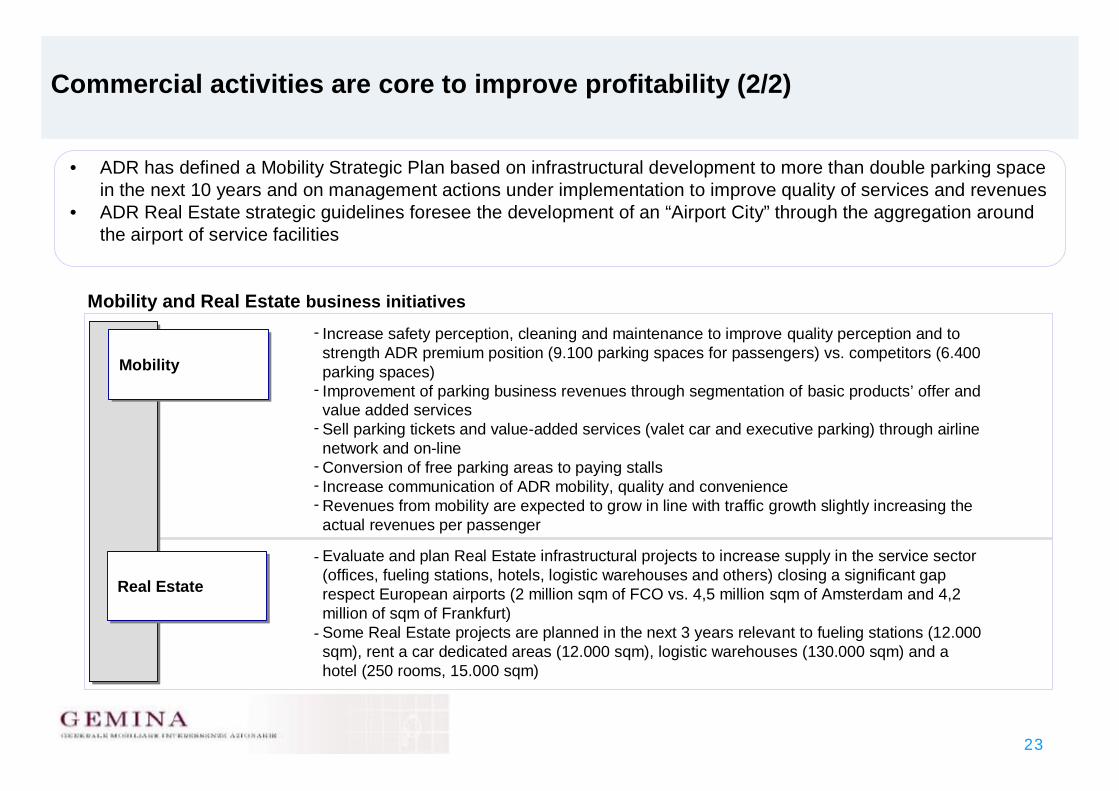

Commercial activities are core to improve profitability (2/2)

Mobility and Real Estate business initiatives

MobilityMobility

Increase safety perception, cleaning and maintenance to improve quality perception and to strength ADR premium position (9.100 parking spaces for passengers) vs. competitors (6.400 parking spaces)Improvement of parking business revenues through segmentation of basic products’ offer and value added servicesSell parking tickets and value-added services (valet car and executive parking) through airlinenetwork and on-lineConversion of free parking areas to paying stallsIncrease communication of ADR mobility, quality and convenienceRevenues from mobility are expected to grow in line with traffic growth slightly increasing the actual revenues per passenger

-

-

-

---

• ADR has defined a Mobility Strategic Plan based on infrastructural development to more than double parking space in the next 10 years and on management actions under implementation to improve quality of services and revenues

• ADR Real Estate strategic guidelines foresee the development of an “Airport City” through the aggregation around the airport of service facilities

Real EstateReal Estate

Evaluate and plan Real Estate infrastructural projects to increase supply in the service sector (offices, fueling stations, hotels, logistic warehouses and others) closing a significant gap respect European airports (2 million sqm of FCO vs. 4,5 million sqm of Amsterdam and 4,2 million of sqm of Frankfurt)Some Real Estate projects are planned in the next 3 years relevant to fueling stations (12.000 sqm), rent a car dedicated areas (12.000 sqm), logistic warehouses (130.000 sqm) and a hotel (250 rooms, 15.000 sqm)

-

-

24

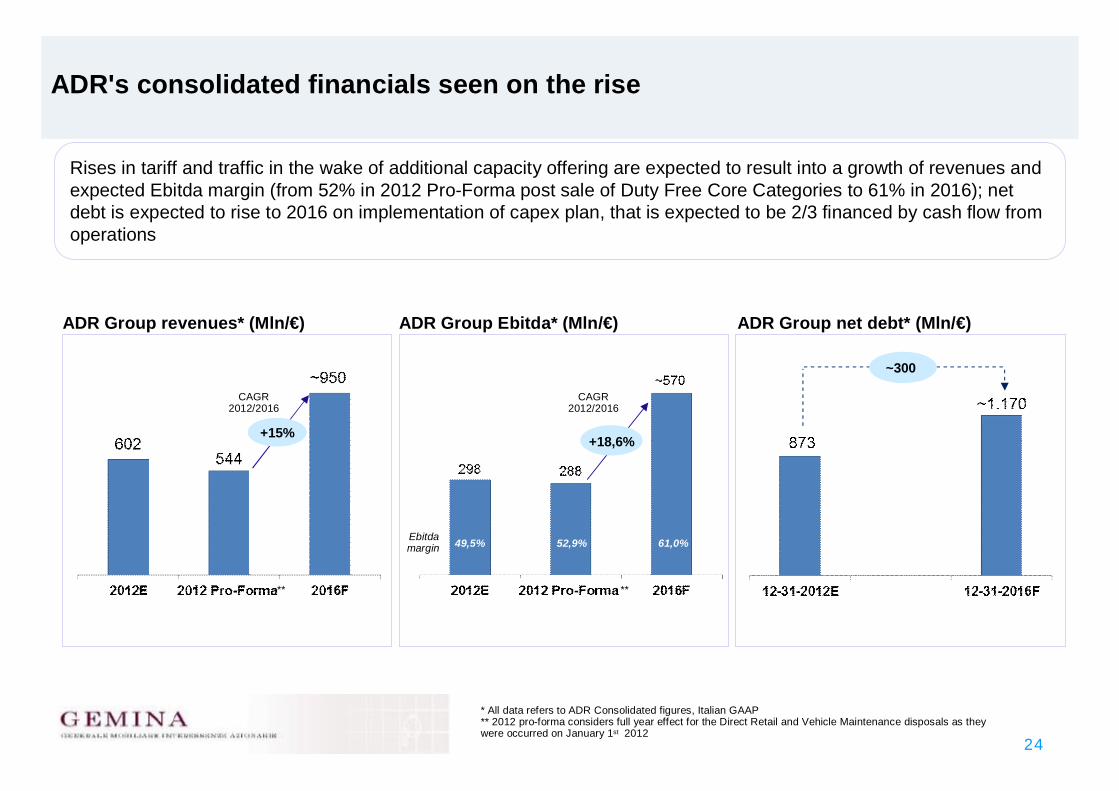

ADR's consolidated financials seen on the rise

+15%

ADR Group revenues* (Mln/€) ADR Group Ebitda* (Mln/€)

+18,6%

ADR Group net debt* (Mln/€)

Rises in tariff and traffic in the wake of additional capacity offering are expected to result into a growth of revenues and expected Ebitda margin (from 52% in 2012 Pro-Forma post sale of Duty Free Core Categories to 61% in 2016); net debt is expected to rise to 2016 on implementation of capex plan, that is expected to be 2/3 financed by cash flow from operations

**

Ebitda margin 49,5% 52,9% 61,0%

CAGR 2012/2016

CAGR 2012/2016

~300

* All data refers to ADR Consolidated figures, Italian GAAP** 2012 pro-forma considers full year effect for the Direct Retail and Vehicle Maintenance disposals as they were occurred on January 1st 2012

**

25

Gemina-ADR's promising future with some challenges in the near term

Result-oriented management culture to be strengthen. The overall support of Gemina's shareholder Changi will be crucial to achieve highest quality standards

To execute timely and efficiently an highly concentrated investment plan and in an amount significantly higher than historical levels, with an "investment machine" almost stuck for the last 10 years

To secure long-term funding to a significant investment plan at competitive terms and conditions

While Gemina-ADR is confident on the capabilities to attract new airlines, the presence of a Hub-carrier remains a crucial element for the full development of the business plan

Unique long-term traffic potentialUnique long-term traffic potential

Biggest development project in EuropeBiggest development project in Europe

Value-oriented long-term concession agreement

Value-oriented long-term concession agreement

Main opportunities Main challenges

Service quality improvementService quality improvement

CapexCapex

Financial resourcesFinancial resources

Traffic developmentTraffic development

Growing commercial businessGrowing commercial business

26

4. RATIONALE OF THE POTENTIAL INTEGRATION WITH ATLANTIA(Gemina Chairman, Fabrizio Palenzona)

27

Rationale of the potential integration with Atlantia

Gemina-ADR will develop the biggest airport project in Europe allowing to meet the growing demand of global traffic, supported by a long-term regulatory framework

Looking ahead, aware of our strengths and responsibilities, Gemina started an analysis of industrial, operating and financial merits of a potential integration with Atlantia, aimed at creating value for all stakeholders

In this context, Gemina is evaluating Atlantia’s strengths in terms of (i) management skills in executing large investment programs on critical infrastructures, also considering the capabilities of the group's engineering and construction companies and (ii) experience in securing funding at competitive costs in the international capital markets

Relevant analyses are expected to be completed by mid March 2013

Gemina-ADR will develop the biggest airport project in Europe allowing to meet the growing demand of global traffic, supported by a long-term regulatory framework

Looking ahead, aware of our strengths and responsibilities, Gemina started an analysis of industrial, operating and financial merits of a potential integration with Atlantia, aimed at creating value for all stakeholders

In this context, Gemina is evaluating Atlantia’s strengths in terms of (i) management skills in executing large investment programs on critical infrastructures, also considering the capabilities of the group's engineering and construction companies and (ii) experience in securing funding at competitive costs in the international capital markets

Relevant analyses are expected to be completed by mid March 2013

28

5. CLOSING REMARKS(Gemina Chairman, Fabrizio Palenzona)

29

Q&A SESSION

30

Disclaimer

This presentation has been prepared by and is the sole responsibility of GEMINA S.p.A. (the “Company”) for the sole purpose described herein. In no case may it or any other statement (oral or otherwise) made at any time in connection herewith be interpreted as an offer or invitation to sell or purchase any security issued by the Company or its subsidiaries, nor shall it or any part of it nor the fact of its distribution form the basis of, or be relied on in connection with, any contract or investment decision in relation thereto. This presentation is not for distribution in, nor does it constitute an offer of securities for sale in Canada, Australia, Japan or in any jurisdiction where such distribution or offer is unlawful. Neither the presentation nor any copy of it may be taken or transmitted into the United States of America, its territories or possessions, or distributed, directly or indirectly, in the United States of America, its territories or possessions or to any U.S. person as defined in Regulation S under the US Securities Act 1933.The content of this document has a merely informative and provisional nature and is not to be construed as providing investment advice. The statements contained herein have not been independently verified. No representation or warranty, either express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness, correctness or reliability of the information contained herein. Neither the Company nor any of its representatives shall accept any liability whatsoever (whether in negligence or otherwise) arising in any way in relation to such information or in relation to any loss arising from its use or otherwise arising in connection with this presentation. The Company is under no obligation to update or keep current the information contained in this presentation and any opinions expressed herein are subject to change without notice. This document is strictly confidential to the recipient and may not be reproduced or redistributed, in whole or in part, or otherwise disseminated, directly or indirectly, to any other person.The information contained herein and other material discussed at the presentation may include forward-looking statements that are not historical facts, including statements about the Company’s beliefs and current expectations. These statements are based on current plans, estimates and projections, and projects that the Company currently believes are reasonable but could prove to be wrong. However,forward-looking statements involve inherent risks and uncertainties. We caution you that a number of factors could cause the Company’s actual results to differ materially from those contained or implied in any forward-looking statement. Such factors include, but are not limited to: trends in company’s business, its ability to implement cost-cutting plans, changes in the regulatory environment, its ability to successfully diversify and the expected level of future capital expenditures. Therefore, you should not place undue reliance on such forward-looking statements. Past performance of the Company cannot be relied on as a guide to future performance. No representation is made that any of the statements or forecasts will come to pass or that any forecast results will be achieved.By attending this presentation or otherwise accessing these materials, you agree to be bound by the foregoing limitations.

![APPENDIX Appendix A, D 'Arcy Concession Agreement …978-3-658-00093-6/1.pdf · APPENDIX Appendix A, D 'Arcy Concession Agreement [Persia] The D'Arcy Concession Agreement May 28,1901](https://img.pdfslide.net/doc/110x75/5addb0787f8b9a9d4d8d808c/appendix-appendix-a-d-arcy-concession-agreement-978-3-658-00093-61pdfappendix.jpg)