Embed Size (px)

Citation preview

New Jersey Natural Gas Market Update

Presentation to:

SNJDC Natural Gas Seminar

Tom KileyNortheast Gas Association

March 25, 2015Mullica Hill, NJ

Issues

Regional Market Developments

New Jersey Gas Market

Demand & Supply

Continued on NGA web site…

http://www.northeastgas.org/about-nga/antitrust-guidelines

About NGA

Non-profit trade association

Local gas utilities (LDCs) serving New England, New York, and New Jersey

Several interstate pipeline companies

LNG importers (Distrigas, Repsol) and LNG trucking companies

Over 200 “associate member” companies, from industry suppliers and contractors to electric grid operators

www.northeastgas.org

A Cold 2015…

• Coldest February in over 2 decades, and 3rd coldest February in NJ since 1895.

• Average temp. of 22 degrees, more than 11 degrees colder than average.

• Monthly cold record remains Feb. 1934 at 17.9 degree average.

• Consistent throughput, esp. Jan-Feb

• High demand on system infrastructure

1200 2200 3200 4200

New Eng. Actual

New Eng. Normal

Mid-Atl. Actual

Mid-Atl. Normal

Source: U.S. NOAA. Data thru Feb. 28, 2015.

Heating Degree Days,Nov. 2014 - Feb. 2015

New Peak Day Set by Gas Utilities in Feb.

• South Jersey Gas – new sendoutrecord on Feb. 15, 2015

• New Jersey Natural Gas – new sendout record on Feb. 15, 2015

• PSE&G – 2nd highest sendout on Feb. 15, 2015

• New England natural gas utilities combined – new sendout record on Feb. 15, 2015

2‐5 2‐31‐28 1‐8

2‐2

1‐13 1‐7

18 of Top 25 Days on Algonquin Pipeline Set this Winter

Chart: Spectra Energy

New Records for Pipeline Throughput: AGT

Market Prices Less Volatile than Last Winter – but still higher than national average

Chart: U.S. FERC, March 2015

Short-Term Price Outlook: EIA

Source: U.S. EIA, March 2015

0

2

4

6

8

10

12

Jan 2014 Jul 2014 Jan 2015 Jul 2015 Jan 2016 Jul 2016

Henry Hub Natural Gas Pricedollars per million Btu

Historical spot price

STEO forecast price

Source: Short-Term Energy Outlook, March 2015.

Note: Confidence interval derived from options market information for the 5 trading days ending Mar. 5, 2015. Intervals not calculated for months with sparse trading in near-the-money options contracts.

Natural Gas Retains a Price Advantage

0

500

1,000

1,500

2,000

2,500

2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

Source: U.S. EIA, Mar. 10, 2015. Natural gas data is for Northeast states of CT, ME, MA, NH, NJ, NY, PA, RI, VT. Heating oil is U.S. average.

Average Consumer Expenditures for Heating Fuels, $, 2008-2015

Natural Gas

Heating Oil

New Jersey Natural Gas Market

Overview

Natural Gas Use in NJ

Primary energy: 30%

Electric generation capacity: 54%

% of households with gas as main heating fuel: 74%

Annual consumption: 681 billion cubic feet (Bcf) of natural gas.

Demand Outlook andSupply Opportunities

Home Heating Market

• New Jersey statewide has strong gas share for home heating: 74% (compared to 56% in NY and 38% in New England).

• NJ home heating shares: gas, 74%; oil, 10%; electric, 12%

• Still potential for further residential sector growth– notably in southern part of state

Proposed Power Plants by Fuel, Northeast

Source: ISO-NE

Natural Gas, 63

Other, 1

Wind, 36GENERATOR PROPOSALS IN THE

ISO NEW ENGLAND QUEUEPercentage, 2015

NEW YORK ISO SYSTEM, 2014Proposed Power Projects by Fuel Type

Megawatts

Source: NY ISO

95

0.6 4 0.40

20

40

60

80

100

NaturalGas

Wind Solar Other

NEW JERSEY, 2014Queued Capacity by Fuel Type,

Percentage (In-State Only)Approx. 7,776 MW

Source: PJM, March 2015

63%

70%95%

Interstate Pipelines

· Algonquin Gas Transmission and Texas Eastern Transmission, subsidiaries of Spectra Energy. · Columbia Transmission, a subsidiary of NiSource. · Dominion Transmission· Tennessee Gas Pipeline Company, a subsidiary of Kinder Morgan. · Transcontinental Pipeline, a subsidiary of Williams.

Source: U.S. EIA, 7-14

Marcellus Shale Production:Still Robust

Source: U.S. EIA, 3-15

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Marcellus Production, 2007-2015, Mcf/d

Prepared by NGA, based on publicly available information. Project locations approximate. As of 3-15.

VERMONT

Proposed Pipeline Projects

Spectra, “AIM”

National Fuel / Empire,

“Tuscarora Lateral”

Williams, “Rockaway Lateral”

Williams & Cabot,

“Constitution Pipeline”

Tennessee, “Northeast

Energy Direct”

Iroquois, “Wright

Interconnect”

Columbia, “East Side Expansion

Project”

PNGTS, “C2C”

Spectra, “Atlantic Bridge”

Tennessee, “ConnecticutExpansion”

Iroquois, “South to North”

National Fuel / Empire, “Northern

Access 2015 & 2016”

Dominion, “New Market

Project”

Tennessee, “Niagara

Expansion”

PennEastProject

Williams/Transco, “Garden State

Expansion Project”

Spectra/ Eversource

Energy/National Grid, “Access

Northeast”

Millennium, “Corning to Rockland”

East Side Expansion Project:Columbia Gas / NiSource

Project Scope: The project will involve the installation

of two natural gas pipelines with approximately 9.5 miles of pipeline in Chester County, PA and 9.5 miles of pipeline in Gloucester County, NJ. Provides up to 312,000 Dth/d.

Customers:• Cabot Oil & Gas Corporation, • New Jersey Natural Gas Company, • Southwestern Energy

Services Company, • South Jersey Gas Company, and• South Jersey Resources Group, LLC

Project Status: Received FERC Certificate, Dec. 2014 Planned In-Service Date

– November 2015

Map: Columbia Gas Transmission

Garden State Expansion: Transco/Williams

Project Scope: Provide up to 180,000 dekatherms

per day of natural gas service in two phases to a new delivery point with New Jersey Natural Gas in Burlington County, N.J. Installation of new compression and

meter/regulation station; no pipeline expansion required.

Customer:New Jersey Natural Gas

Project Status: FERC filing, Feb., 2015 Est. Phase I in-service: Nov. 2016 Est. Phase 2 in-service: Nov. 2017

Map: Transco/Williams

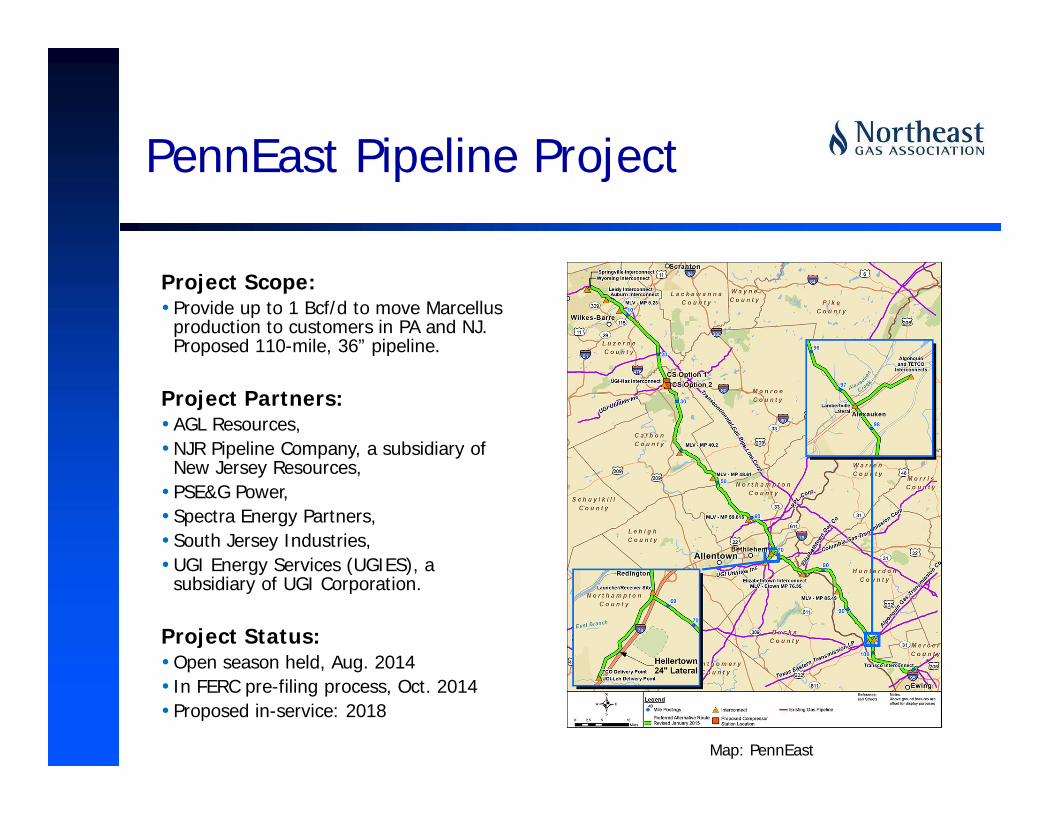

PennEast Pipeline Project

Project Scope: Provide up to 1 Bcf/d to move Marcellus

production to customers in PA and NJ. Proposed 110-mile, 36” pipeline.

Project Partners: AGL Resources,NJR Pipeline Company, a subsidiary of

New Jersey Resources, PSE&G Power, Spectra Energy Partners, South Jersey Industries,UGI Energy Services (UGIES), a

subsidiary of UGI Corporation.

Project Status:Open season held, Aug. 2014 In FERC pre-filing process, Oct. 2014 Proposed in-service: 2018

Map: PennEast

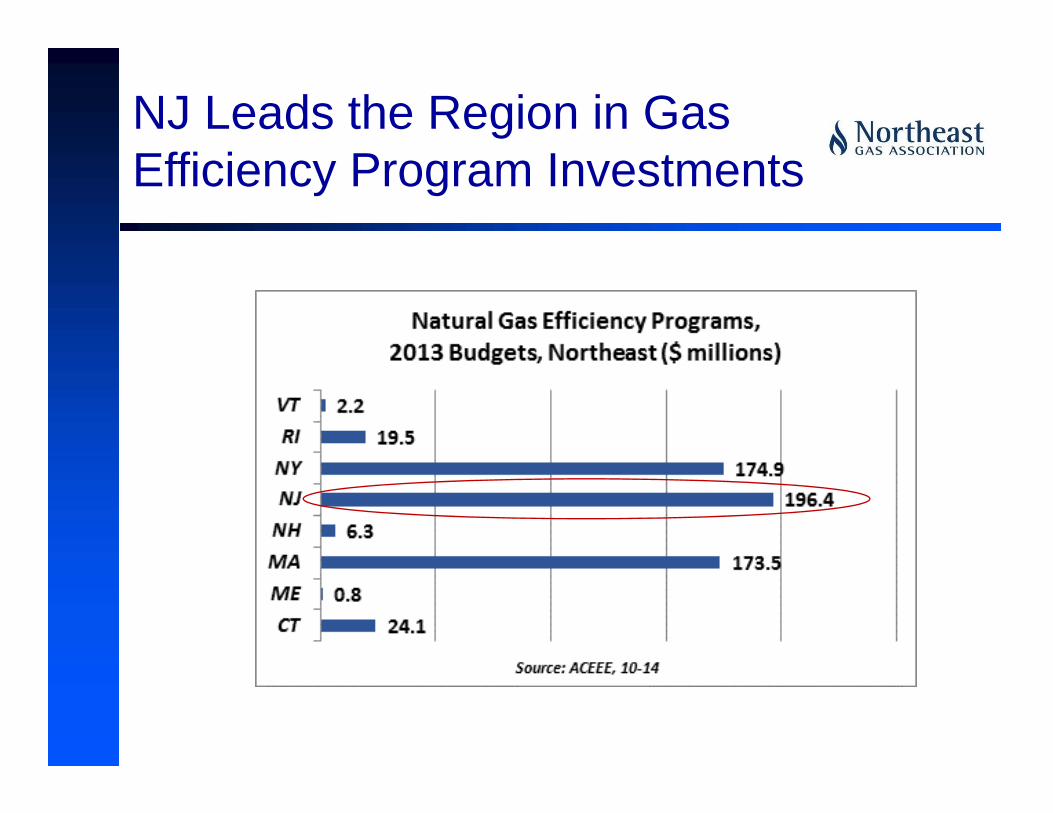

NJ Leads the Region in GasEfficiency Program Investments

System Safety / Infrastructure Enhancements

• Primary focus of federal and state oversight agencies, along with addressing methane emissions.

• NJ gas utilities working with BPU to implementstorm resilience programs and acceleratereplacement of older pipeline system components.

Northeast Market Opportunity• Northeast region remains highest-priced U.S. region for energy

• Traditionally at a distance from gas resource fields – now very close thanks to Marcellus

• Market demand remains strong for gas for home heating, power gen – and potentially transportation

• Pipeline capacity constraints in Northeast are leading to numerous infrastructure proposals, to increase access to Marcellus gas.

April is “Safe Digging Month”

Questions?

30.