Embed Size (px)

Citation preview

The New Brownfield Cleanup Program

Effective Post July 1, 2015

L inda S haw, E sq .

K nauf S haw LLP

1400 C rossroads B u ild ing

2 S ta te S tree t

R ocheste r, N Y, 14614

585-546-8430

lshaw @ nyenv law.com

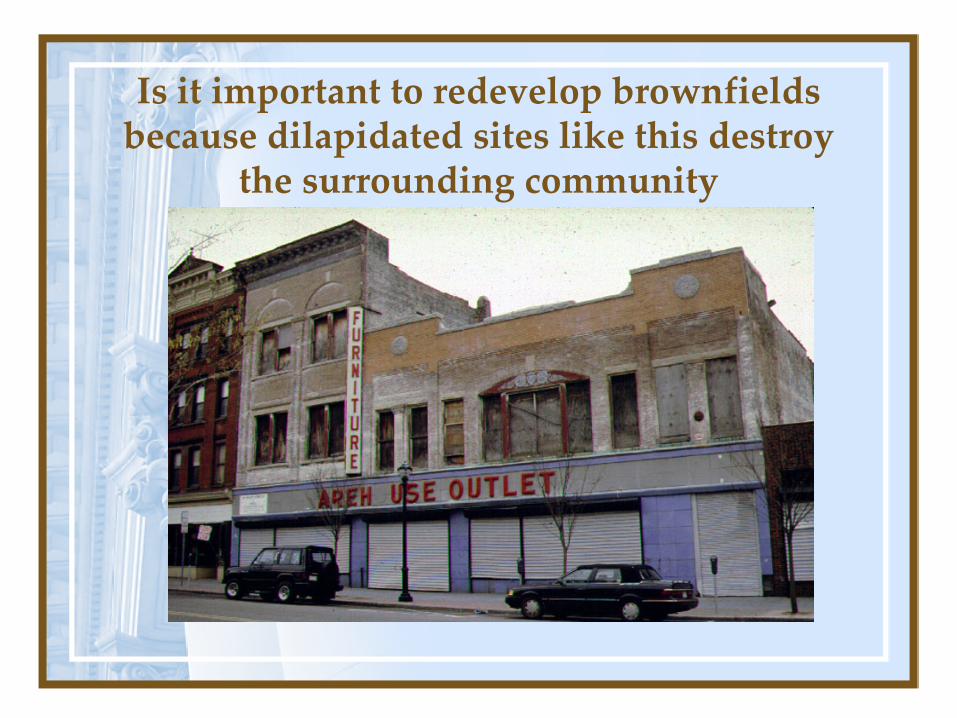

Is it important to redevelop brownfields because dilapidated sites like this destroy

the surrounding community

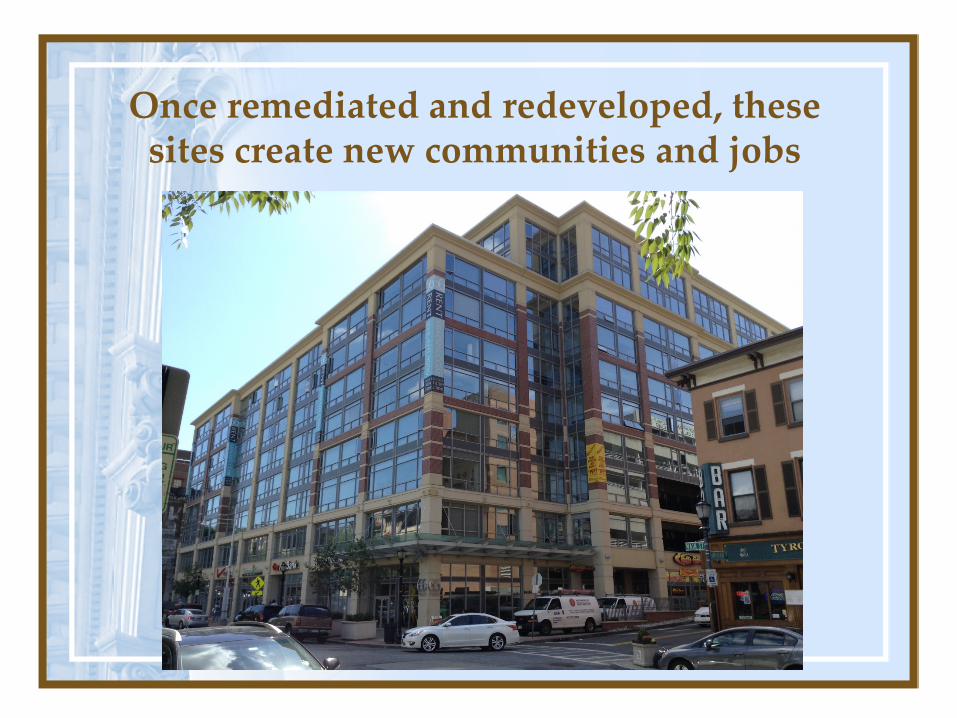

Once remediated and redeveloped, these sites create new communities and jobs

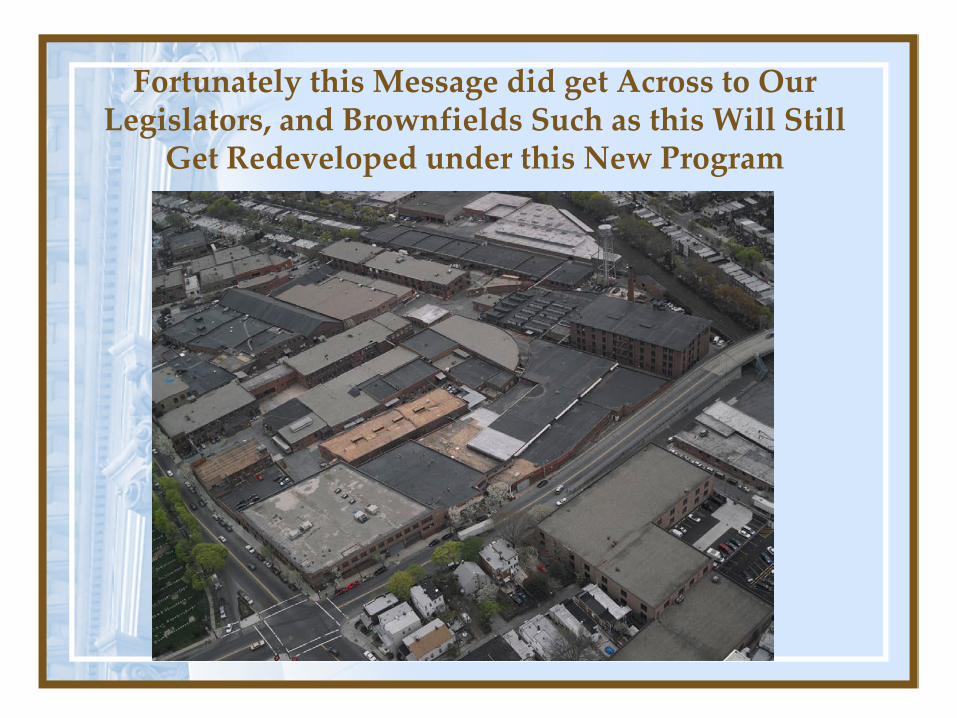

Fortunately this Message did get Across to Our Legislators, and Brownfields Such as this Will Still

Get Redeveloped under this New Program

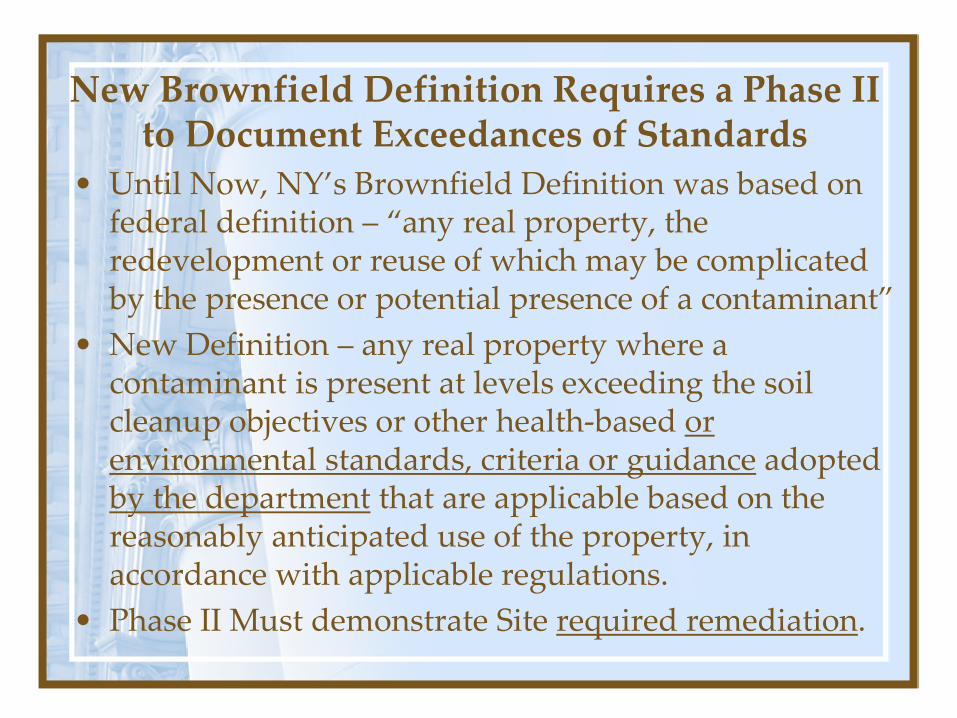

New Brownfield Definition Requires a Phase II to Document Exceedances of Standards

• Until Now, NY’s Brownfield Definition was based on federal definition – “any real property, the redevelopment or reuse of which may be complicated by the presence or potential presence of a contaminant”

• New Definition – any real property where a contaminant is present at levels exceeding the soil cleanup objectives or other health-based or environmental standards, criteria or guidance adopted by the department that are applicable based on the reasonably anticipated use of the property, in accordance with applicable regulations.

• Phase II Must demonstrate Site required remediation.

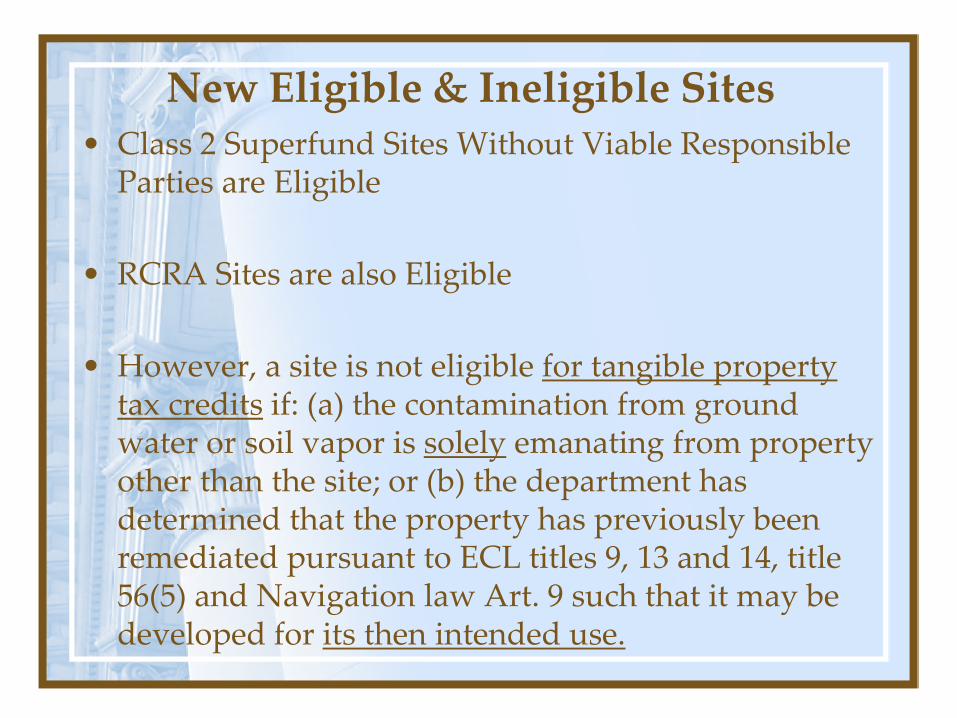

New Eligible & Ineligible Sites • Class 2 Superfund Sites Without Viable Responsible

Parties are Eligible

• RCRA Sites are also Eligible • However, a site is not eligible for tangible property

tax credits if: (a) the contamination from ground water or soil vapor is solely emanating from property other than the site; or (b) the department has determined that the property has previously been remediated pursuant to ECL titles 9, 13 and 14, title 56(5) and Navigation law Art. 9 such that it may be developed for its then intended use.

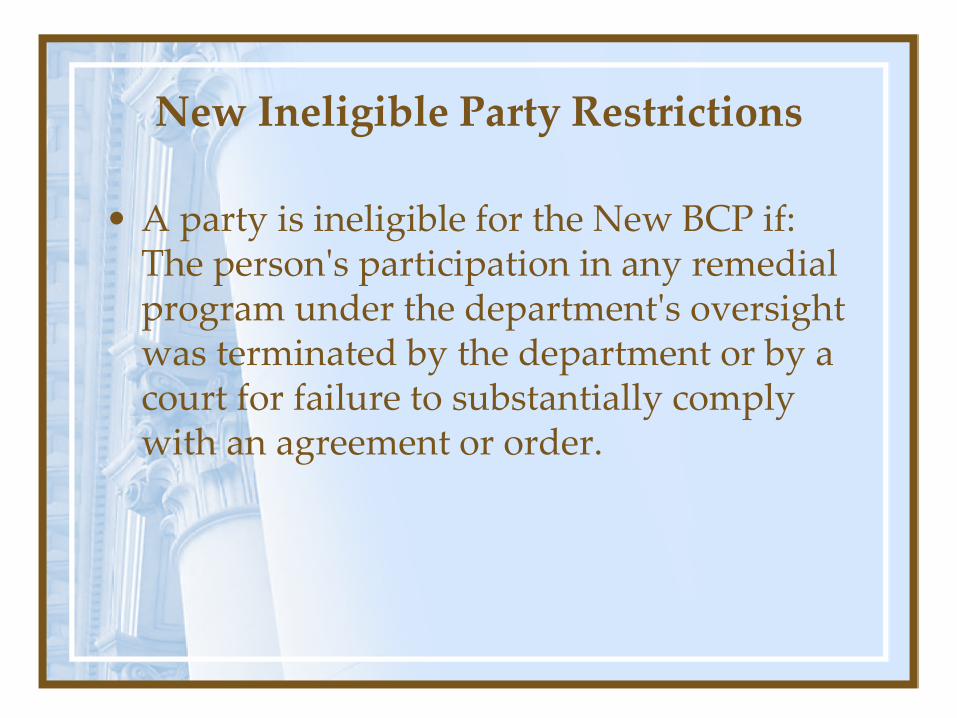

New Ineligible Party Restrictions

• A party is ineligible for the New BCP if: The person's participation in any remedial program under the department's oversight was terminated by the department or by a court for failure to substantially comply with an agreement or order.

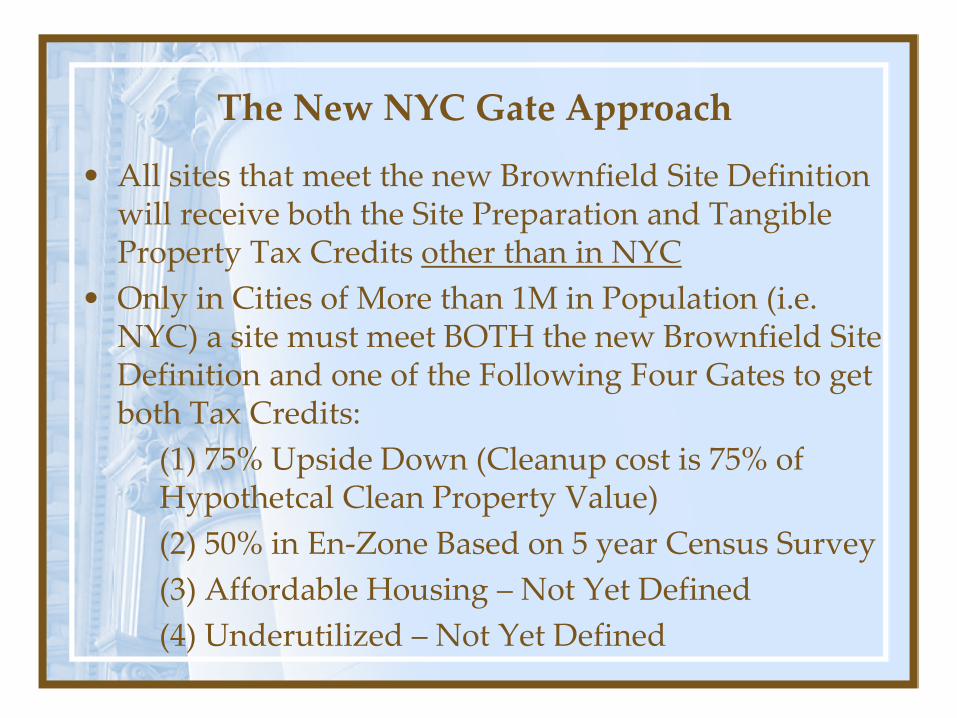

The New NYC Gate Approach

• All sites that meet the new Brownfield Site Definition will receive both the Site Preparation and Tangible Property Tax Credits other than in NYC

• Only in Cities of More than 1M in Population (i.e. NYC) a site must meet BOTH the new Brownfield Site Definition and one of the Following Four Gates to get both Tax Credits: (1) 75% Upside Down (Cleanup cost is 75% of

Hypothetcal Clean Property Value) (2) 50% in En-Zone Based on 5 year Census Survey (3) Affordable Housing – Not Yet Defined (4) Underutilized – Not Yet Defined

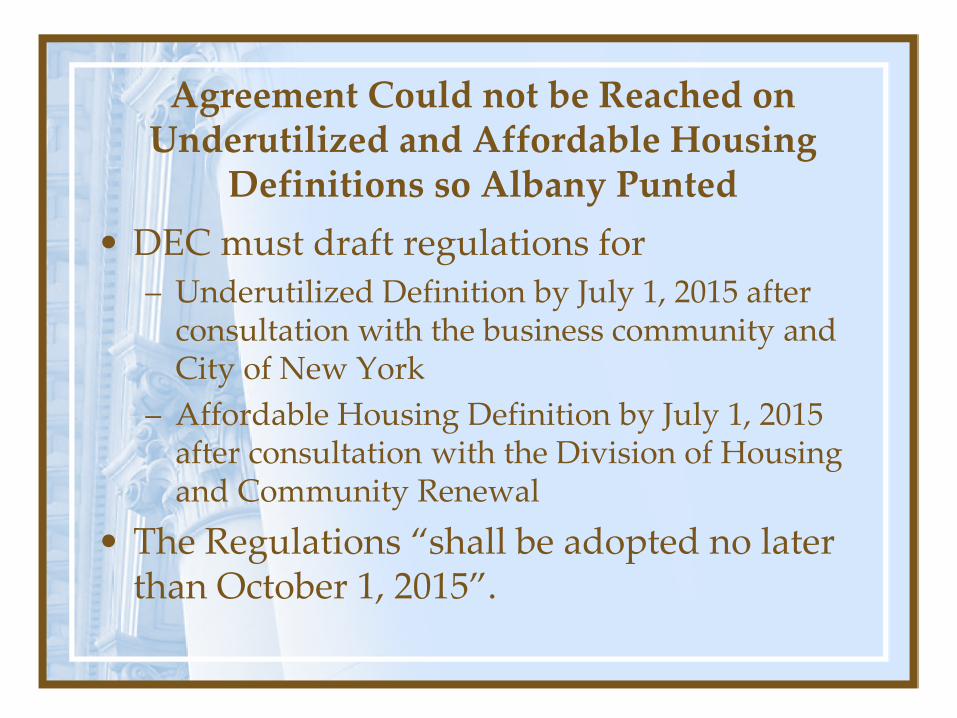

Agreement Could not be Reached on Underutilized and Affordable Housing

Definitions so Albany Punted • DEC must draft regulations for

– Underutilized Definition by July 1, 2015 after consultation with the business community and City of New York

– Affordable Housing Definition by July 1, 2015 after consultation with the Division of Housing and Community Renewal

• The Regulations “shall be adopted no later than October 1, 2015”.

What do the New Tax Credits Look like? • The new tax credits are very similar to the existing

Post June 2008 tax credits • The formulas for the site preparation tax credits of

22% (for lowest level Track 4) up to 50% (for highest level Track 1) have not been changed but some eligible costs have been cut (e.g. only foundation cost needed for a cover system)

• The formulas for the tangible property tax credit are: – 10% base credit plus five 5% “bump ups”(up to maximum

24%) described below or 3x’s the cost of the new site preparation costs, whichever of these two numbers is LOWER, up to the current $35M cap for non-Manufacturing Projects/$45M for Manufacturing

Slightly Cut Site Preparation Cost Categories Eligible for These Tax Credits

• Foundation Costs Limited to Cover System Regulatory Definition – i.e. 6 inches of asphalt or concrete

• Related Parties Service Fees – These costs will only apply for Tangible Property Credits and Not Site Preparation Credits and must be based on costs actually incurred

• New Long List of Defined Site Prep Costs that are eligible

New Site Preparation Costs Definition • Costs …necessary to implement a site's investigation,

remediation, or qualification for a COC, and shall include costs of: excavation; demolition; activities DOL /DOH supervised asbestos, lead or PCB work or; environmental consulting; engineering; legal costs; transportation, disposal, treatment or containment of contaminated soil; remediation measures taken to address contaminated soil vapor; cover systems consistent with applicable regulations; physical support of excavation; dewatering and other work to facilitate or enable remediation activities; sheeting, shoring, and other engineering controls required to prevent off-site migration of contamination from the qualified site or migrating onto the qualified site; and the costs of fencing, temporary electric wiring, scaffolding, and security facilities.

New Tangible Property Formula Percentages

• Cap is Still $35M non-Manufacturing Projects & $45M for Manufacturing Projects

• Formula is 3x Site Preparation costs or 10% of Tangible Property Capital Costs (so no 12% for C-Corps) PLUS

• Bump Ups with Maximum Credit of 24% – Affordable Housing -5% – En-Zone – 5% – Brownfield Opportunity Area Compliant – 5% – Manufacturing – 5% – Track 1 – 5%

BOA Plans are Being Put on DOS Website Soon So Developers Can Find the BOA Sites

B O A M ap P rov ided by

D ept o f S ta te

Other Tax Credits Eliminated Post July 1, 2015

• The real property tax credit that was earned if jobs were created was eliminated.

• The insurance tax credit was eliminated. • Therefore, only the revised site preparation

and tangible property tax credits remain.

Grandfathering Provisions • Pre-2008 Projects have until 12/31/17 to finish

or the post 7/1/15 tax credit gates, costs + formulas will apply. Good news is that site will not be terminated but need to meet gate.

• Post-2008 Projects Have until 12/31/19 to finish or new post 7/1/15 tax credit gates, cut costs & formulas apply.

• New Sites Program effective 7/1/15 unless there is no underutilized definition promulgated; sites have until 12/22 to apply and 12/26 to finish.

New Process Timeframes / Deadlines • Application Approval Timeframe: DEC now has 30

days instead of 10 to review an application • Work Implementation Deadlines Based on Schedule:

Governor’s Proposal that Work plans must be implemented within 90 days was amended:

An applicant shall include with every report submitted to the department a schedule for the submission of any subsequent work plan required to meet the requirements of this title. There is a new FER applicant certification that the remediation requirements have been or will be achieved in accordance with the schedules provided in reports.

New Timeframes / Deadlines Cont’d

• Easement Filing Deadline: Governor’s proposal mandated filing easement within 180 days of work commencement, which was amended to require filing within 180 days of commencement of the remedial design or three months prior to the date of the anticipated issuance of COC.

New COC Transfer & Termination Provisions

• COC can be transferred to a successor to a real property interest, including legal title, equitable title or leasehold, in all or a part of the brownfield site, but cannot be transfer to a responsible party.

• COC may be modified or revoked if applicant made a misrepresentation of a material fact tending to demonstrate that: (i) it was a volunteer; or (ii) met one of the new “gates” for receiving the tangible property tax credits.

• NOTE: There already was a very broad reopener: “There is good cause for such modification or revocation.”

New DEC Oversight Cost Provisions

• Only a participant not a volunteer applicant will have to pay for state costs, including the recovery of state costs incurred before the effective date of such agreement; provided, however, that such costs may be based on a reasonable flat-fee for oversight, which shall reflect the projected future state costs incurred in negotiating and overseeing implementation of such agreement

New DEC Access to Site for Post-Remediation SMP Requirements

• to inspect for compliance with the site management plan approved by the department, including (i) inspection of the performance of maintenance, monitoring and operational activities required as part of the remedial program for the site, (ii) inspection for the purpose of ascertaining current uses of the site, and (iii) taking samples in accordance with paragraph (a) of this subdivision.

New Non-Tax Credit Voluntary Cleanup Program - BCP-EZ

• Devil will be in the Details of Future Regulations since this new Program is supposed to provide for expedited investigation and remediation

• No Significant Threat Sites • No Tax Credits • Must still satisfy BCP Remedial and CPP

Requirements • Can use “Background” Data to Demonstrate a

Track 4 cleanup • COC is provided but Liability Release is not

Specified

Only “Brownfield Sites” can enter New BCP-EZ

• BCP-EZ applies to “Brownfield Sites”, which suggests the same new brownfield site definition must be met to get in (exceedances of standards and need for remediation; not just suspect contamination);

• Sites earn no tax credits but a COC; however, the COC provision does not reference a liability release.

• Liability Release is earned by operation of law under ECL 27-1421“after the department has issued a certificate of completion for a brownfield site”.

• Until regulations come out for this program, be cognizant of “brownfield site” definitional issue because if you meet the definition, why use BCP-EZ?

The New BCP Law Should Still Encourage Brownfield Development

• For all parts of the State other than NYC, the new BCP Law is still very lucrative and only a more detailed Phase II investigation will be required to get in, which documents contamination above standards that require remediation

• For NYC, sites can still get in until the new Underutilized and Affordable Housing definitions are promulgated; eligibility afterwards will be contingent on language finalized in regulations and focused on sites in an En-zone since 75% upside down test will be hard to meet. Stay tuned for definitions!