Embed Size (px)

Citation preview

MOODYS.COM

5 OCTOBER 2017

NEWS & ANALYSIS Corporates 2 » Toshiba Memory Sale Is Credit Negative for WDC, Positive

for Seagate » Carlisle Companies’ Purchase of Accella Performance Materials

Is Credit Positive » National Vision’s Proposed IPO Is Credit Positive » For Reliance Communications, Cancellation of Aircel Merger Is

Credit Negative

Banks 6 » US Regulators’ Proposal to Increase Allowance of DTAs and

MSAs in Bank Capital Is Credit Negative » Groupe Credit Mutuel-CM-11 and Credit Mutuel Nord Europe’s

Merger of Insurance Units Is Credit Positive » Nordea and DNB Baltic Operations Merger Creates Efficiencies

and Strengthens Local Presence, a Credit Positive » Indian Banks’ Sale of Stakes in Insurance Subsidiaries Will

Strengthen Their Loss-Absorbing Buffers

Insurers 11 » Rescission of AIG’s SIFI Designation Is Credit Negative

Asset Managers 13 » Invesco’s Acquisition of Guggenheim ETFs Is Credit Positive

US Public Finance 15 » State and Local Government Delays in Capital Expenditures

Push Costs into the Future

RECENTLY IN CREDIT OUTLOOK

» Articles in Last Monday’s Credit Outlook 17 » Go to Last Monday’s Credit Outlook

Click here for Weekly Market Outlook, our sister publication containing Moody’s Analytics’ review of market activity, financial predictions, and the dates of upcoming economic releases.

NEWS & ANALYSIS Credit implications of current events

2 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017 8

Corporates

Toshiba Memory Sale Is Credit Negative for WDC, Positive for Seagate Last Thursday, Toshiba Corporation (Caa1 negative) announced that it had reached a definitive agreement to sell about 60% of Toshiba Memory Corporation (TMC) to a consortium of financial and strategic investors led by Bain Capital for ¥2.0 trillion (about $17.8 billion). Seagate Technology plc, which issues debt through Seagate HDD Cayman (Baa3 negative), then confirmed that it is a participant in the consortium and has the right to purchase up to ¥139.5 billion in non-convertible 5% preferred equity to be issued by KK Pangea, the newly formed company that is buying Toshiba Memory.

The sale is credit negative for Western Digital Corporation (WDC, Ba1 stable), which owns 49.9% of three joint ventures (Flash Ventures) with Toshiba that are housed in TMC. Flash Ventures, which we estimate accounts for about 40% of TMC’s business, produces NAND memory chips for Toshiba and WDC. The companies split the output evenly and either sell it to their customers as raw NAND capacity or use it to manufacture solid-state storage drives (SSDs). Having access to a captive supply of NAND is important to WDC as it battles the secular decline of its legacy hard disk drive (HDD) products.

The buying consortium includes two of WDC’s direct competitors, Seagate and SK Hynix Inc. (Ba1 positive). WDC currently has a cost and technology advantage over its competitors’ products, but that differential likely will shrink if Seagate and SK Hynix get direct access to TMC’s NAND output. As part of its investment in KK Pangea, Seagate will negotiate with TMC a long-term supply agreement of NAND flash, which it currently procures in the spot market and through short-term agreements with various NAND suppliers at much higher prices. Having a captive source of NAND supply benefits Seagate, which will gain the cost and supply clarity it needs to make incremental investments to grow the SSD side of its business to reduce pressure on declining HDD sales.

WDC participated in a separate investor consortium seeking to buy TMC. Since May, it has been pursuing legal remedies under the terms of the joint venture agreement to prevent the transfer of Flash Ventures and TMC assets without its consent. Arbitrators and the courts have sided with WDC in several prior motions it filed during the protracted sale process. WDC now expects the injunctive relief it is seeking to be resolved in early 2018. An extended regulatory and antitrust review of the sale also is likely, given that SK Hynix also manufactures storage and memory chips.

In the meantime, WDC will continue to build up cash on its balance sheet from its operations, aided by the achievement of planned synergies following its purchase over the past three years of Hitachi and SanDisk. The company had about $6.4 billion of cash as of 30 June 2017, the end of its fiscal year, because it delayed paying down debt in order to build capacity for a possible TMC bid. With Toshiba having selected another bidder, we expect WDC’s cash balances to grow to about $7.5 billion by the end of 2017, giving it the capacity to resume paying down debt, if it so chooses.

Seagate, for its part, is financially capable of making the TMC investment. The company had $2.5 billion of cash and investments as of 30 June 2017. We expect cash balances to increase by about $500 million by year-end, giving Seagate more capacity to make the investment from available cash and minimize additional borrowings.

The buying consortium’s agreement is the latest step in Toshiba’s protracted sale of its memory unit. Toshiba seeks to shore up its finances following a bankruptcy filing by its energy unit and to avoid a delisting from the Tokyo stock exchange.

Gerald Granovsky Senior Vice President +1.212.553.4198 [email protected]

NEWS & ANALYSIS Credit implications of current events

3 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017

Carlisle Companies’ Purchase of Accella Performance Materials Is Credit Positive On Monday, Carlisle Companies Incorporated (Baa2 stable) said that it would buy Accella Performance Materials (unrated), a provider of polyurethane foam for building applications, from private-equity firm Arsenal Capital Partners for $670 million in cash. The purchase of Accella, which Carlisle will fund entirely from its revolving credit line, is credit positive, expanding the company’s roofing product offerings without substantially increasing leverage.

We estimate that Carlisle’s adjusted balance sheet debt will increase by $670 million to about $1.5 billion, and its pro forma adjusted debt/EBITDA ratio will deteriorate to 2.0x from 1.1x at 30 June, which is still suitable for the company’s Baa2 rating. Our estimates exclude lease adjustments for Accella, or any cost synergies, but we believe neither would significantly change debt leverage.

Carlisle’s pro forma capital structure at 30 June would have consisted of a $1 billion senior unsecured revolving credit facility, with $780 million outstanding, and two unsecured notes totaling $600 million. Consistent with our standard adjustments, we added an additional $100 million to balance-sheet debt for pension liabilities and operating lease commitments. We expect that most revolver usage will be termed out later this year, possibly with one or both notes, freeing up liquidity under the revolving loan and taking advantage of low interest rates.

Upon the acquisition’s close, Scottsdale, Arizona-based Carlisle will be one of the largest North American providers of roofing materials to the domestic construction market. Accella will merge into the company’s Carlisle Construction Materials (CCM) business, making CCM a more significant driver of future earnings and cash flow. The addition of Accella’s approximately $430 million a year in revenue would bring CCM’s combined pro forma revenue for the 12 months through 30 June to approximately $2.6 billion. The division now will contribute slightly more than 60% of Carlisle’s total pro forma revenue, up from around 56% for 2016. Cash on hand at 30 June was about $140 million, but foreign subsidiaries held most of Carlisle’s cash.

CCM generates operating margins in excess of 20%, the highest among Carlisle’s businesses. CCM benefits from sound fundamentals in commercial roofing repair, which is less volatile than new construction demand and is the main driver of CCM’s revenue and earnings. Storm damage and aging roofs provide steady demand for the company because the upfront costs associated with roof repair or replacement are worth the investment compared with the time and potential costs associated with repairing water damage and replacing damaged property.

Our forward view considers trends in the American Institute of Architects’ Architecture Billings Index, an industry survey that gauges planned non-residential construction activity over the next nine to 12 months. The index rose to 53.7 in August from 51.9 in July. The index’s past seven readings have all been above 50, meaning the majority of those surveyed believe market conditions are expanding.

Peter Doyle Vice President - Senior Analyst +1.212.553.4475 [email protected]

NEWS & ANALYSIS Credit implications of current events

4 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017

National Vision’s Proposed IPO Is Credit Positive Last Friday, National Vision Holdings Inc., the parent company of discount optical retailer National Vision, Inc. (B2 stable), filed plans to sell shares of its common stock in an initial public offering (IPO). In an S-1 IPO registration statement filed with the US Securities and Exchange Commission, National Vision Holdings Inc. disclosed plans to use IPO proceeds to repay its $125 million second-lien term loan and a portion of its $804 million first-lien term loan. The proposed IPO is credit positive because, if completed, it would meaningfully reduce debt.

The company has performed largely in line with our expectations since a $170 million dividend recapitalization in February 2017. Excluding the benefit of any prospective debt repayment, we expect National Vision to continue to de-lever through revenue growth from same-store sales in the high-single to low-double digits from mid-single digits and the addition of 70-80 stores per year.

If National Vision completes the IPO and reduces outstanding debt by a sufficient amount, we could upgrade the company’s corporate family and probability of default ratings. Our current upgrade trigger requires a commitment to a conservative financial policy, such that debt/EBITDA remains below 5x and EBIT/interest expense remains above 2x. An upgrade also would require stronger liquidity, but it is not yet clear if the IPO would substantially benefit liquidity beyond reducing interest payments.

At present earnings, if National Vision were to pay down $250 million of debt ($125 million of first-lien debt and the $125 million second lien), we estimate that its Moody’s-adjusted financial leverage would fall to 5.0x debt/EBITDA from 6.2x as of 1 July 2017. EBIT/interest expense was 1.3x as of 1 July 2017. Meeting the interest-coverage upgrade trigger would require National Vision to pay down about $350 million of first-lien debt, in addition to the $125 million second-lien repayment, pro forma for the full-year effect of the dividend recapitalization.

Financial sponsor KKR & Co.’s ownership of National Vision will not change after the proposed IPO. The buyout firm bought a majority stake in National Vision in March 2014. Duluth, Georgia-based National Vision sells low price-point eyeglasses and contacts through 980 retail locations, including 227 located within Wal-Mart stores.

Raya Sokolyanska Vice President - Senior Analyst +1.212.553.7415 [email protected]

NEWS & ANALYSIS Credit implications of current events

5 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017

For Reliance Communications, Cancellation of Aircel Merger Is Credit Negative On Sunday, Reliance Communications Limited (RCOM, Ca negative) announced that an agreement involving the merger of its mobile business with Aircel Limited had lapsed owing to legal and regulatory uncertainties, objections by interested parties and delays in receiving relevant approvals. Cancellation of the merger is credit negative for RCOM because the merger was crucial to a debt reduction plan the company agreed to with its lenders and which also included disposal of tower assets. RCOM and Aircel signed a binding agreement in September 2016 to merge their mobile businesses. The company continues to pursue a sale of its tower assets, although it did not provide an update on the process.

In conjunction with the merger, RCOM expected its debt to decline by INR140 billion with the transfer of bank debt and INR60 billion of spectrum liabilities to the new merged entity. Because the merger has failed, RCOM’s debt levels will remain elevated and leverage, as measured by adjusted debt/EBITDA, will remain above 9.0x.

RCOM’s reported debt totaled INR457 billion at 31 March 2017, including a $300 million senior secured bond due on 6 November 2020 and a $350 million senior secured bond issued by its 100%-owned subsidiary, GCX Limited (B3 negative) that is due on 1 August 2019. Because GCX is not a restricted subsidiary under RCOM’s $300 million bond indenture, GCX assets and cash flows are ring-fenced from RCOM creditors.

In June, RCOM’s lenders agreed to consider a strategic debt restructuring. As part of this process, the company received a standstill on its obligations’ debt servicing through 31 December 2017, by which time the merger with Aircel and sale of 100% of its tower assets were to have been completed. If the transactions are not completed, the lenders can exercise their right to convert their debt into equity and take over management of the company. RCOM has stated that it has since extended the standstill deadline to 31 December 2018. The company did not provide a status update of its agreement to sell 100% of its tower assets and related infrastructure to Brookfield Infrastructure Partners LP for INR110 billion.

Our negative outlook on RCOM’s rating reflects the ongoing uncertainty regarding the company’s ability to generate cash flow, corporate and debt-restructuring progress and the resultant recovery prospects for both lenders and bondholders. Additionally, failure to meet the proposed restructuring timetable or to remain current on the interest payable on RCOM’s $300 million bond or GCX’s $350 million bond will adversely pressure ratings. According to management, these bonds are excluded from the debt standstill agreement in place.

Annalisa Di Chiara Vice President - Senior Credit Officer +852.3758.1537 [email protected]

Nidhi Dhruv Vice President - Senior Analyst +65.6398.8315 [email protected]

NEWS & ANALYSIS Credit implications of current events

6 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017

Banks

US Regulators’ Proposal to Increase Allowance of DTAs and MSAs in Regulatory Capital Is Credit Negative On 27 September, US regulators proposed a number of regulatory capital changes for US banks. These include increasing the limit of deferred tax assets (DTAs) and mortgage servicing assets (MSAs)1 that can be included in the calculation of common equity Tier 1 (CET1) for US banks with less than $250 billion in assets. The existing capital rules limit the inclusion of DTAs and MSAs each to 10% of CET1 capital, with a combined limit of 15%.

The proposed rule would raise the limit to 25% for both DTAs and MSAs and eliminate the combined limit. Such changes would allow for more esoteric assets to make up a bank’s capital structure, which is credit negative. However, the proposed changes do not materially affect rated US banks given their limited holdings of DTAs and MSAs. According to regulatory filings, none of the large US regional banks with less than $250 billion in assets currently has DTAs or MSAs in excess of the 10% threshold.

We consider DTAs to be a relatively low-quality asset, and thus a low-quality source of capital, compared with most other components of tangible common equity (TCE), the measure of capital we use in our bank methodology. The recoverability of DTAs typically depends on a bank’s ability to generate taxable income in future periods. As such, it is uncertain whether DTA amounts can be realized, especially in times of stress. For this reason, our bank rating methodology limits the amount of DTAs included in our calculation of a bank’s TCE to a maximum of 10% of total TCE.

A DTA is recognized when there is a temporary difference between the carrying amount of an asset or liability for tax reporting and for financial reporting under applicable accounting standards. A meaningful portion of DTAs are the result of loan-loss provisioning. When a bank records an allowance for loan losses, the carrying amount of its net loans normally will be higher under tax reporting than under financial reporting because such losses typically are deducted for tax reporting purposes only when the loans are charged off, which happens later. In this case, the bank would report a DTA in its financial statements equal to the tax savings that it may realize in a future period when its taxable income falls as a result of charging off the loans. The other uncertainty with DTAs is that a change in the tax rate changes the value of the DTA.

Although we do not exclude MSAs from our TCE calculation, we recognize that MSA valuations can be volatile because most US homeowners can refinance their mortgage at any time without incurring a prepayment penalty. As a result, MSAs are highly sensitive to mortgage rates. A decline in mortgage rates can lead to an increase in mortgage prepayments, causing a sharp reduction in MSA valuations. MSAs also can be difficult to hedge. Consequently, if a bank’s capital structure was 25% composed of MSAs, which would be allowed under the regulatory proposal, it would heighten risks regarding a bank’s business concentration and its reliance on one asset for its capital structure.

1 An MSA is the present value of the projected future income stream from mortgage servicing.

Megan Fox Analyst +1.212.553.4986 [email protected]

NEWS & ANALYSIS Credit implications of current events

7 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017

Groupe Credit Mutuel-CM-11 and Credit Mutuel Nord Europe’s Merger of Insurance Units Is Credit Positive Last Friday, Groupe Credit Mutuel-CM11 (CM-CM11, unrated2), the largest member of the large French mutualist bancassurance group Groupe Credit Mutuel (GCM, unrated), announced that CM-CM11 and Credit Mutuel Nord Europe (CMNE, unrated), another GCM member, will merge their insurance businesses. The merger is credit positive because the combination will enhance the business’ efficiency through cost synergies, reinforce CM-CM11’s position in the domestic insurance market and create business opportunities outside of France, particularly in Belgium.

The size of CM-CM11’s insurance operations is approximately 10x that of CMNE’s insurance operations. We estimate that the merger will increase CM-CM11’s market share to 6.3% from around 5.6% currently in the life insurance segment, and to 6.1% from 5.8% in the non-life insurance segment. Such growth is material in a highly fragmented domestic insurance market, where most players have less than a 10% market share, and at a time when all large French banks are enhancing their insurance franchises.

As part of the merger, Groupe des Assurances du Credit Mutuel (GCAM, unrated), CM-CM11’s insurance subsidiary, will absorb Nord Europe Assurance SA (NEA, unrated), CMNE’s insurance subsidiary. GACM and NEA provide their respective parents’ retail banking networks with insurance products and back-office services. Merging their resources will allow economies of scale, while reducing the number of regulated entities will lower regulatory costs. We expect the combined entity to benefit from lower reinsurance costs.

Insurance is a core business at CM-CM11 and has strong synergies with CM-CM11’s banking activities. It is an important source of earnings and currently contributes around 30% of net profit. Business growth and improved efficiency at GACM will benefit CM-CM11, all the more so since its retail banking and investment revenue are under pressure in the current low interest rate environment.

The merger between GACM and NEA also is strategically important for CM-CM11 because it reinforces its leading position within GCM. CM-CM11 has a strategy of fostering its influence on GCM by pooling resources with, or providing support to, other member banks. CM-CM11 is keen on consolidating its position amid increasing tension with GCM’s other main subgroup, Credit Mutuel Arkea (Aa3 negative, a2), which since mid-2016 has expressed its intention to separate from the rest of the group.

2 The rated entities within CM11-CM are Banque Federative du Credit Mutuel (Aa3/Aa3 stable, a2) and Credit Industriel et

Commercial (Aa3/Aa3 stable, a2). The bank ratings shown in this report are the bank’s deposit rating, senior unsecured debt rating (where available) and adjusted baseline credit assessment.

Yasuko Nakamura Vice President - Senior Credit Officer +33.1.5330.1030 [email protected]

NEWS & ANALYSIS Credit implications of current events

8 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017

Nordea and DNB Baltic Operations Merger Creates Efficiencies and Strengthens Local Presence, a Credit Positive On Sunday, Nordea Bank AB (Aa3/Aa3 stable, a33) and DNB Bank ASA (Aa2/Aa2 negative, a3) announced that they had closed the transaction that created a joint venture of the banks’ operations in the Baltics. The new entity will operate as Luminor, with Nordea controlling 56% of the economic rights and DNB controlling 44%, and both banks each holding 50% of the voting rights. Although the transaction’s financial effect will be limited for both banks, we expect that the merger will create cost synergies and strengthen the banks’ local presence, both credit positive.

Nordea’s and DNB’s operations in the Baltic region are complementary. Nordea had a strong market position in the large corporate market segment (corporate lending constituted 52% of total lending at the end of June 2017), while DNB was more focused on retail lending (52% of its total lending). Also, DNB’s corporate lending (39% of its book) was more focused on small and midsize enterprises. Luminor’s loan book is around €12 billion, versus €14 billion if Nordea had transferred its entire Baltic portfolios to the joint venture. Nevertheless, Luminor will be the third-largest lender in the Baltic region behind Swedbank AB (Aa3/Aa3 stable, a3) and SEB (Aa3/Aa3 stable, a3), as Exhibit 1 shows.

EXHIBIT 1

Baltic Countries’ Largest Banks by Loan Market Share as of June 2017

Sources: Estonian Financial Supervision Authority, Association of Latvian Commercial Banks, Association of Lithuanian Banks and Moody’s Investors Service

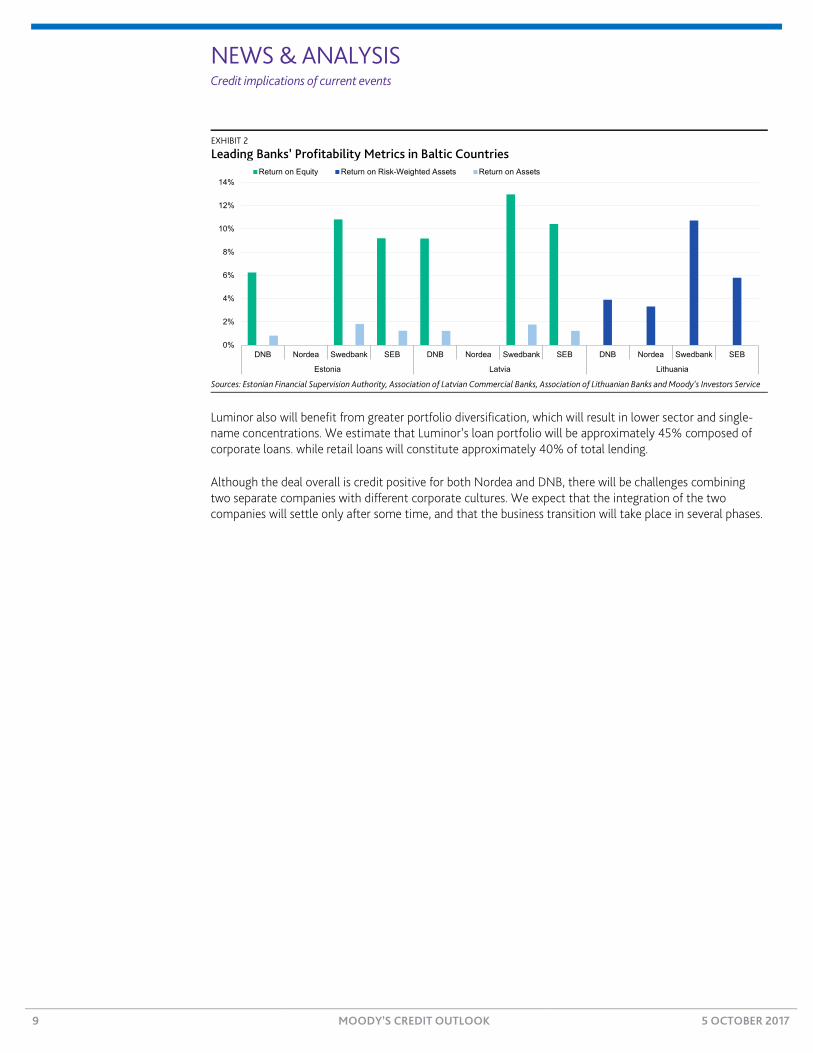

We expect Luminor to improve operational efficiencies in markets where Nordea and DNB each had historically subpar returns (see Exhibit 2). Whereas Nordea previously worked through branches, DNB over time will benefit from one legal structure, versus previously having operated through three subsidiaries. Large and costly branch networks partly explain DNB’s and Nordea’s low profitability in the Baltic countries. Although we do not expect to see a material effect on the banks’ consolidated financial statements, we expect over the next 24-36 months that rationalisation will lead to higher profitability as the newly created joint venture reduces costs and improves its pricing power.

3 The bank ratings shown in this report are the bank’s deposit rating, senior unsecured debt rating and baseline credit assessment.

0%

5%

10%

15%

20%

25%

30%

Luminor (DNB-Nordea) Swedbank SEB

DNB Nordea

Effie Tsotsani Analyst +44.20.7772.1712 [email protected]

Louise Lundberg Vice President - Senior Credit Officer +46.850.256.568 [email protected]

NEWS & ANALYSIS Credit implications of current events

9 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017

EXHIBIT 2

Leading Banks’ Profitability Metrics in Baltic Countries

Sources: Estonian Financial Supervision Authority, Association of Latvian Commercial Banks, Association of Lithuanian Banks and Moody’s Investors Service

Luminor also will benefit from greater portfolio diversification, which will result in lower sector and single-name concentrations. We estimate that Luminor’s loan portfolio will be approximately 45% composed of corporate loans. while retail loans will constitute approximately 40% of total lending.

Although the deal overall is credit positive for both Nordea and DNB, there will be challenges combining two separate companies with different corporate cultures. We expect that the integration of the two companies will settle only after some time, and that the business transition will take place in several phases.

0%

2%

4%

6%

8%

10%

12%

14%

DNB Nordea Swedbank SEB DNB Nordea Swedbank SEB DNB Nordea Swedbank SEB

Estonia Latvia Lithuania

Return on Equity Return on Risk-Weighted Assets Return on Assets

NEWS & ANALYSIS Credit implications of current events

10 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017

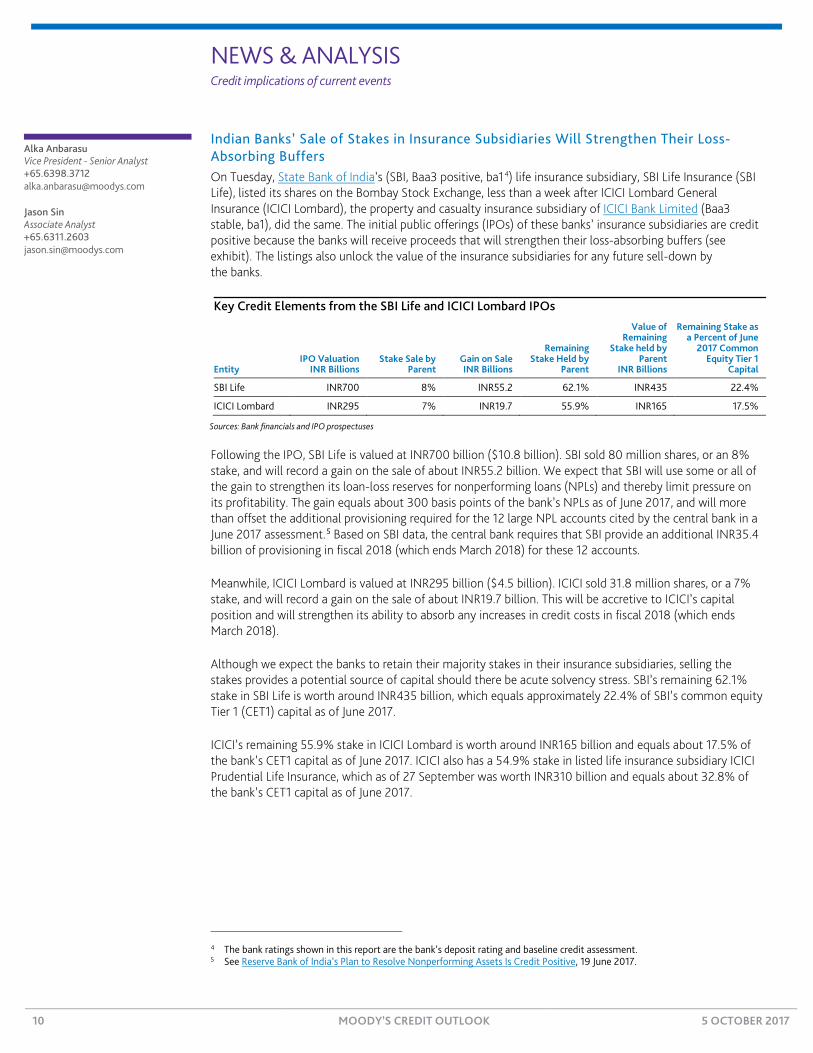

Indian Banks’ Sale of Stakes in Insurance Subsidiaries Will Strengthen Their Loss-Absorbing Buffers On Tuesday, State Bank of India’s (SBI, Baa3 positive, ba14) life insurance subsidiary, SBI Life Insurance (SBI Life), listed its shares on the Bombay Stock Exchange, less than a week after ICICI Lombard General Insurance (ICICI Lombard), the property and casualty insurance subsidiary of ICICI Bank Limited (Baa3 stable, ba1), did the same. The initial public offerings (IPOs) of these banks’ insurance subsidiaries are credit positive because the banks will receive proceeds that will strengthen their loss-absorbing buffers (see exhibit). The listings also unlock the value of the insurance subsidiaries for any future sell-down by the banks.

Key Credit Elements from the SBI Life and ICICI Lombard IPOs

Entity IPO Valuation

INR Billions Stake Sale by

Parent Gain on Sale INR Billions

Remaining Stake Held by

Parent

Value of Remaining

Stake held by Parent

INR Billions

Remaining Stake as a Percent of June

2017 Common Equity Tier 1

Capital

SBI Life INR700 8% INR55.2 62.1% INR435 22.4%

ICICI Lombard INR295 7% INR19.7 55.9% INR165 17.5%

Sources: Bank financials and IPO prospectuses

Following the IPO, SBI Life is valued at INR700 billion ($10.8 billion). SBI sold 80 million shares, or an 8% stake, and will record a gain on the sale of about INR55.2 billion. We expect that SBI will use some or all of the gain to strengthen its loan-loss reserves for nonperforming loans (NPLs) and thereby limit pressure on its profitability. The gain equals about 300 basis points of the bank’s NPLs as of June 2017, and will more than offset the additional provisioning required for the 12 large NPL accounts cited by the central bank in a June 2017 assessment.5 Based on SBI data, the central bank requires that SBI provide an additional INR35.4 billion of provisioning in fiscal 2018 (which ends March 2018) for these 12 accounts.

Meanwhile, ICICI Lombard is valued at INR295 billion ($4.5 billion). ICICI sold 31.8 million shares, or a 7% stake, and will record a gain on the sale of about INR19.7 billion. This will be accretive to ICICI’s capital position and will strengthen its ability to absorb any increases in credit costs in fiscal 2018 (which ends March 2018).

Although we expect the banks to retain their majority stakes in their insurance subsidiaries, selling the stakes provides a potential source of capital should there be acute solvency stress. SBI’s remaining 62.1% stake in SBI Life is worth around INR435 billion, which equals approximately 22.4% of SBI’s common equity Tier 1 (CET1) capital as of June 2017.

ICICI’s remaining 55.9% stake in ICICI Lombard is worth around INR165 billion and equals about 17.5% of the bank’s CET1 capital as of June 2017. ICICI also has a 54.9% stake in listed life insurance subsidiary ICICI Prudential Life Insurance, which as of 27 September was worth INR310 billion and equals about 32.8% of the bank’s CET1 capital as of June 2017.

4 The bank ratings shown in this report are the bank’s deposit rating and baseline credit assessment. 5 See Reserve Bank of India’s Plan to Resolve Nonperforming Assets Is Credit Positive, 19 June 2017.

Alka Anbarasu Vice President - Senior Analyst +65.6398.3712 [email protected]

Jason Sin Associate Analyst +65.6311.2603 [email protected]

NEWS & ANALYSIS Credit implications of current events

11 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017

Insurers

Rescission of AIG’s SIFI Designation Is Credit Negative Last Friday, the US Financial Stability Oversight Council (FSOC) announced its rescission of its systemically important financial institution (SIFI) designation of American International Group, Inc. (AIG, Baa1 stable). The decision is credit negative because it ends the US Federal Reserve’s supervision of AIG, which we viewed as beneficial to creditors. AIG’s insurance operations continue to be regulated by state-based regulators in the US and various national regulators outside the US, which are developing mechanisms to provide group-wide supervision.

The FSOC designated AIG a nonbank SIFI in July 2013, based on its view that financial distress at AIG could pose a threat to US financial stability. The designation followed AIG’s liquidity crunch during the financial crisis of 2008-09, with adverse effects on its many creditors and counterparties. The SIFI designation, per the Dodd-Frank Act of 2010, provided for the Federal Reserve to regulate AIG on a consolidated basis with enhanced prudential standards. The Federal Reserve is developing rigorous tests for capital adequacy, liquidity and risk management of nonbank SIFIs, although it has not finalized these rules. Such group-wide supervision enhances the credit quality of an insurer such as AIG, which has operations spanning multiple business lines and jurisdictions. However, the heightened regulatory costs associated with SIFI status partly offset the credit benefits.

The FSOC vote, which just met the two-thirds majority required for rescission, reflects the changing composition of the FSOC under the Trump administration, as well as AIG’s considerable de-risking over the past several years. De-risking actions that began during the financial crisis included the unwinding of AIG Financial Products Corp. (AIGFP) and AIG’s securities lending program. AIGFP had a broad array of derivatives, including credit default swaps that insured structures with residential mortgage-backed securities (RMBS). As part of AIG’s securities lending program, booked mainly in its life insurance subsidiaries, the company invested a large portion of the cash proceeds in RMBS. These derivative and securities lending activities caused the bulk of AIG’s liquidity problems during the financial crisis, prompting the Federal Reserve Bank of New York to purchase for prices well below par AIG’s RMBS and related securities through special-purpose vehicles. This sped the unwinding of these activities, while locking in substantial losses for AIG. In other de-risking actions, AIG has divested sizable business units to narrow its focus and simplify the organization.

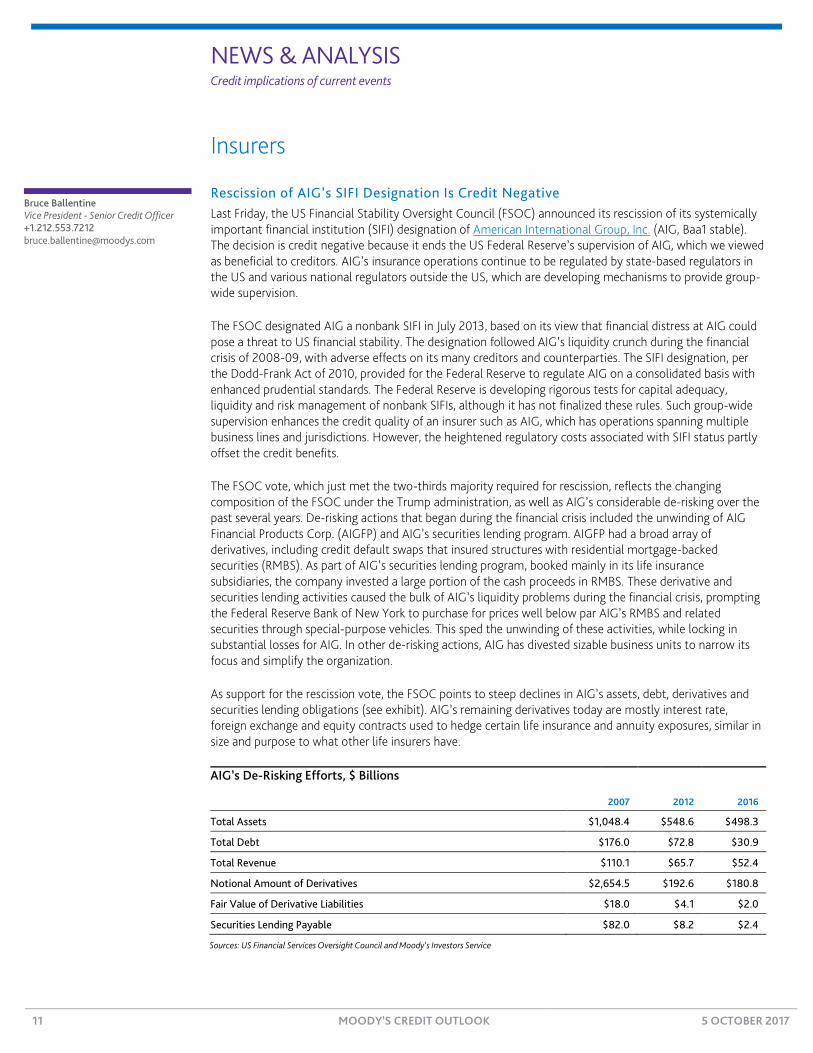

As support for the rescission vote, the FSOC points to steep declines in AIG’s assets, debt, derivatives and securities lending obligations (see exhibit). AIG’s remaining derivatives today are mostly interest rate, foreign exchange and equity contracts used to hedge certain life insurance and annuity exposures, similar in size and purpose to what other life insurers have.

AIG’s De-Risking Efforts, $ Billions

2007 2012 2016

Total Assets $1,048.4 $548.6 $498.3

Total Debt $176.0 $72.8 $30.9

Total Revenue $110.1 $65.7 $52.4

Notional Amount of Derivatives $2,654.5 $192.6 $180.8

Fair Value of Derivative Liabilities $18.0 $4.1 $2.0

Securities Lending Payable $82.0 $8.2 $2.4

Sources: US Financial Services Oversight Council and Moody’s Investors Service

Bruce Ballentine Vice President - Senior Credit Officer +1.212.553.7212 [email protected]

NEWS & ANALYSIS Credit implications of current events

12 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017

Further de-risking actions since the 2013 SIFI designation include AIG’s sales of aircraft lessor International Lease Finance Corporation in May 2014 and mortgage guarantor United Guaranty Corporation in December 2016. Within its property and casualty business, AIG has sharply reduced writings of US casualty lines, where it has a history of adverse loss development and poor returns. The FSOC cites the reduced commercial lines’ market share as another indication of lower systemic risk at AIG.

The FSOC’s rescission vote stems from a yearly reevaluation of AIG’s SIFI status, as called for in the Dodd-Frank Act. The FSOC began the latest reevaluation in early 2016. After some correspondence through the year, AIG notified the FSOC in late 2016 that it was not contesting the SIFI designation. In May 2017, AIG appointed a new CEO, Brian Duperreault, a seasoned insurance executive who raised questions about the SIFI designation. In July 2017, AIG submitted additional materials to the FSOC, and formally requested a rescission of the SIFI designation. After years of de-risking and shrinking, we expect that AIG will return to growth mode under Mr. Duperreault’s leadership, with enhanced risk controls developed in the wake of the financial crisis.

We believe the rescission vote with respect to AIG raises the likelihood that the FSOC will rescind the SIFI designation of the one remaining nonbank SIFI, Prudential Financial, Inc. (Baa1 stable). It also raises the likelihood that the US Department of Justice, acting on behalf of the FSOC, will drop its appeal of a March 2016 US District Court ruling that rescinded the SIFI designation of MetLife, Inc. (A3 stable).

NEWS & ANALYSIS Credit implications of current events

13 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017

Asset Managers

Invesco’s Acquisition of Guggenheim ETFs Is Credit Positive Last Thursday, Invesco Ltd. ((P)A2 stable), the parent and guarantor of Invesco Finance PLC (A2 stable), announced that it would acquire the exchange-traded fund (ETF) business of Guggenheim Investments for $1.2 billion of cash, receiving 79 ETFs with $37 billion of assets under management (AUM). Although expensive, the acquisition is credit positive for Invesco because it will help the company keep pace with the fast-growing ETF market. The acquired funds will add to Invesco’s considerable range of 281 ETFs with $159.4 billion of AUM. The parties expect to close the transaction in second-quarter 2018.

At $1.2 billion, the cost of the acquisition is quite high, approaching 17x EBITDA on the basis of 2018 projected earnings.6 Invesco’s motivation to acquire a known, fast-growing ETF franchise reflects competition at the smaller end of the ETF market, where fund sponsors are struggling to differentiate themselves. Invesco’s broadening range of differentiated ETFs will compete against the massive capitalization-weighted ETFs that dominate the market.

To close the transaction, Invesco will borrow approximately $1 billion from its line of credit, raising its Moody’s-adjusted leverage multiple to approximately 2x EBITDA from 1.6x as of second-quarter 2017. With free cash flow of $1 billion, we believe Invesco will be able to restore its leverage to pre-deal levels within a year and a half, assuming the markets remain stable. Invesco maintains $1 billion of cash in excess of regulatory requirements, and the outstanding balance on its $1.25 billion credit facility was zero as of 30 June 2017. Invesco also suspended share repurchases in anticipation of the August acquisition of Source, a UK-based ETF provider with 88 ETFs with $25 billion of AUM, which had consumed approximately $550 million of cash per year in 2016 and 2015. The company also announced that it will not resume share buybacks until late 2018 at the soonest.

The Guggenheim funds provide Invesco a broad range of investment categories. Many of the funds have AUM of at least $100 million, average inception dates exceeding 10 years and annualized trading in excess of 100%.

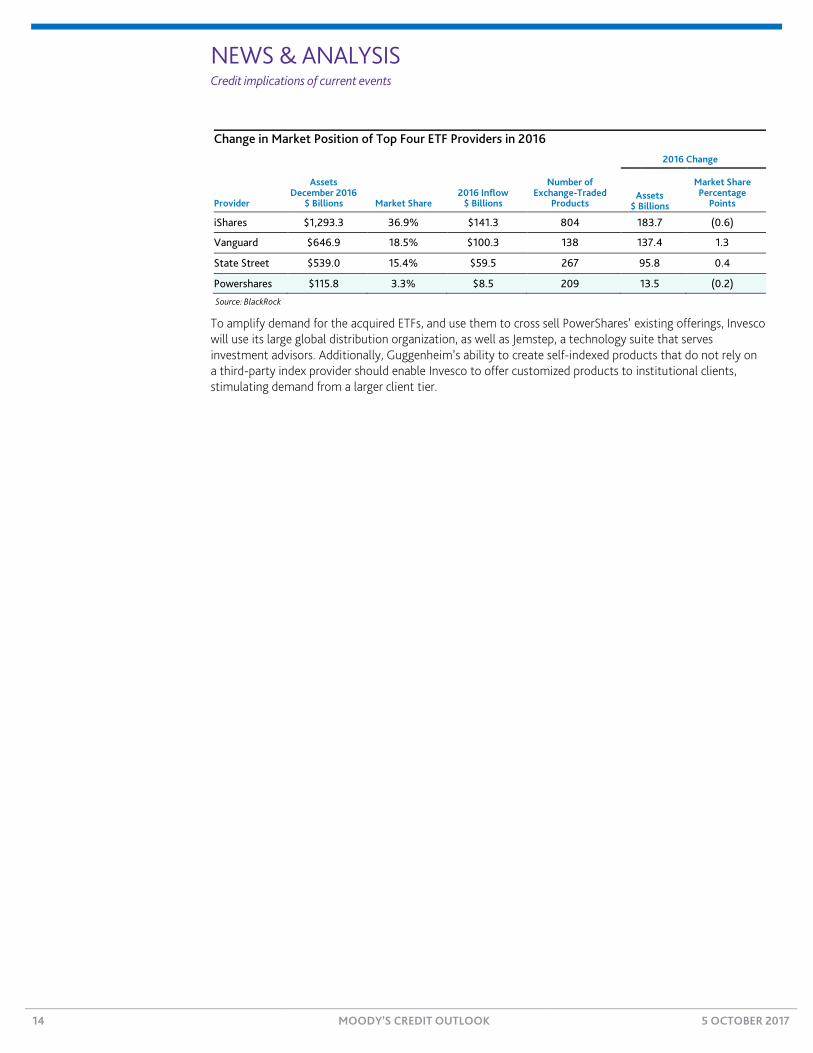

Although the ETF market has grown rapidly, leading players such as BlackRock, Inc. (A1 positive) and The Vanguard Group, Inc. (unrated) garnered most of that growth, attracting more than $100 billion each in 2016 (see exhibit). Invesco’s PowerShares ETF franchise, whose market share was less than 4% last year, has been under pressure to grow inorganically. Guggenheim’s ETFs have grown at a 17% compound annual growth rate since 2014, nearly matching the 18% annual growth of the global market.

6 Invesco stated that the present value of the tax shield from the amortization of acquisition intangibles would ultimately save it

$360 million (assuming a 40% tax rate), and therefore the “net” multiple would be 11.7x EBITDA. Given the significant intangibles created, Invesco expects to have $30 million of tax amortization for 15 years from the transaction.

Neal M. Epstein, CFA Vice President - Senior Credit Officer +1.212.553.3700 [email protected]

NEWS & ANALYSIS Credit implications of current events

14 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017

Change in Market Position of Top Four ETF Providers in 2016

2016 Change

Provider

Assets December 2016

$ Billions Market Share 2016 Inflow

$ Billions

Number of Exchange-Traded

Products Assets

$ Billions

Market Share Percentage

Points

iShares $1,293.3 36.9% $141.3 804 183.7 (0.6)

Vanguard $646.9 18.5% $100.3 138 137.4 1.3

State Street $539.0 15.4% $59.5 267 95.8 0.4

Powershares $115.8 3.3% $8.5 209 13.5 (0.2)

Source: BlackRock

To amplify demand for the acquired ETFs, and use them to cross sell PowerShares’ existing offerings, Invesco will use its large global distribution organization, as well as Jemstep, a technology suite that serves investment advisors. Additionally, Guggenheim’s ability to create self-indexed products that do not rely on a third-party index provider should enable Invesco to offer customized products to institutional clients, stimulating demand from a larger client tier.

NEWS & ANALYSIS Credit implications of current events

15 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017

US Public Finance

State and Local Government Delays in Capital Expenditures Push Costs into the Future Last Thursday, the Bureau of Economic Analysis released its second-quarter gross domestic product report, which showed that state and local governments continue to cut back on capital expenditures. The report suggests an ongoing buildup of deferred infrastructure maintenance that will eventually prove expensive and credit negative for the sector.

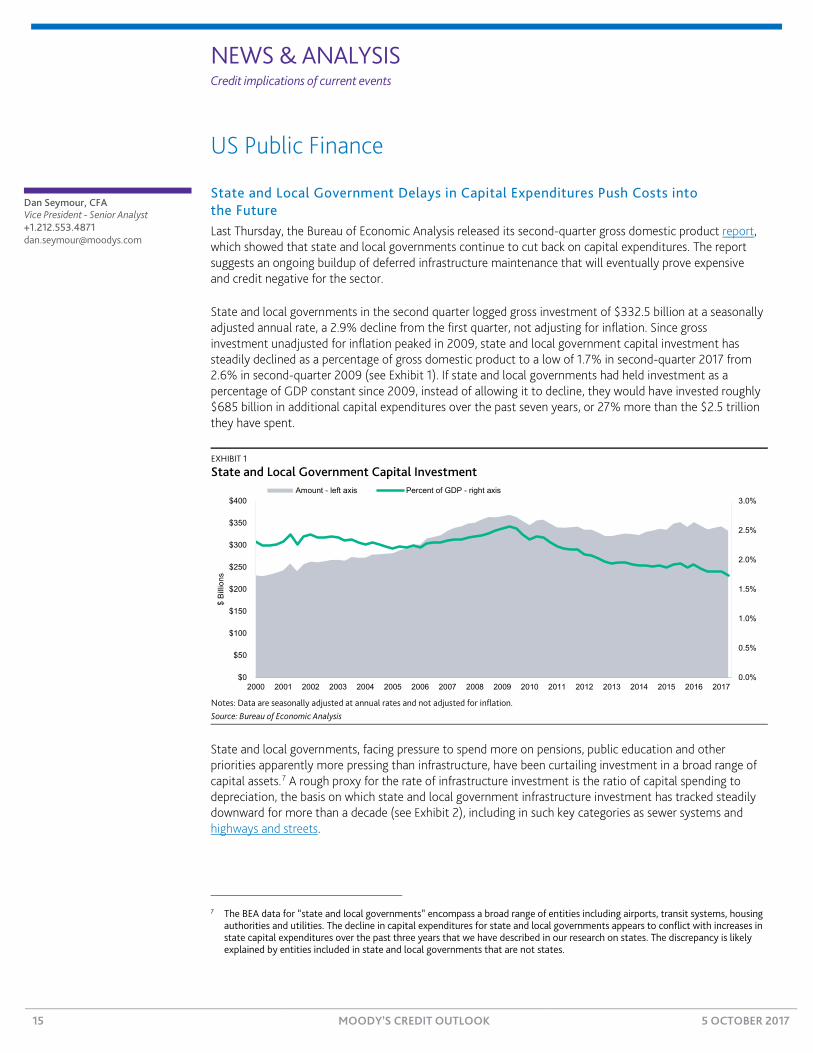

State and local governments in the second quarter logged gross investment of $332.5 billion at a seasonally adjusted annual rate, a 2.9% decline from the first quarter, not adjusting for inflation. Since gross investment unadjusted for inflation peaked in 2009, state and local government capital investment has steadily declined as a percentage of gross domestic product to a low of 1.7% in second-quarter 2017 from 2.6% in second-quarter 2009 (see Exhibit 1). If state and local governments had held investment as a percentage of GDP constant since 2009, instead of allowing it to decline, they would have invested roughly $685 billion in additional capital expenditures over the past seven years, or 27% more than the $2.5 trillion they have spent.

EXHIBIT 1

State and Local Government Capital Investment

Notes: Data are seasonally adjusted at annual rates and not adjusted for inflation. Source: Bureau of Economic Analysis

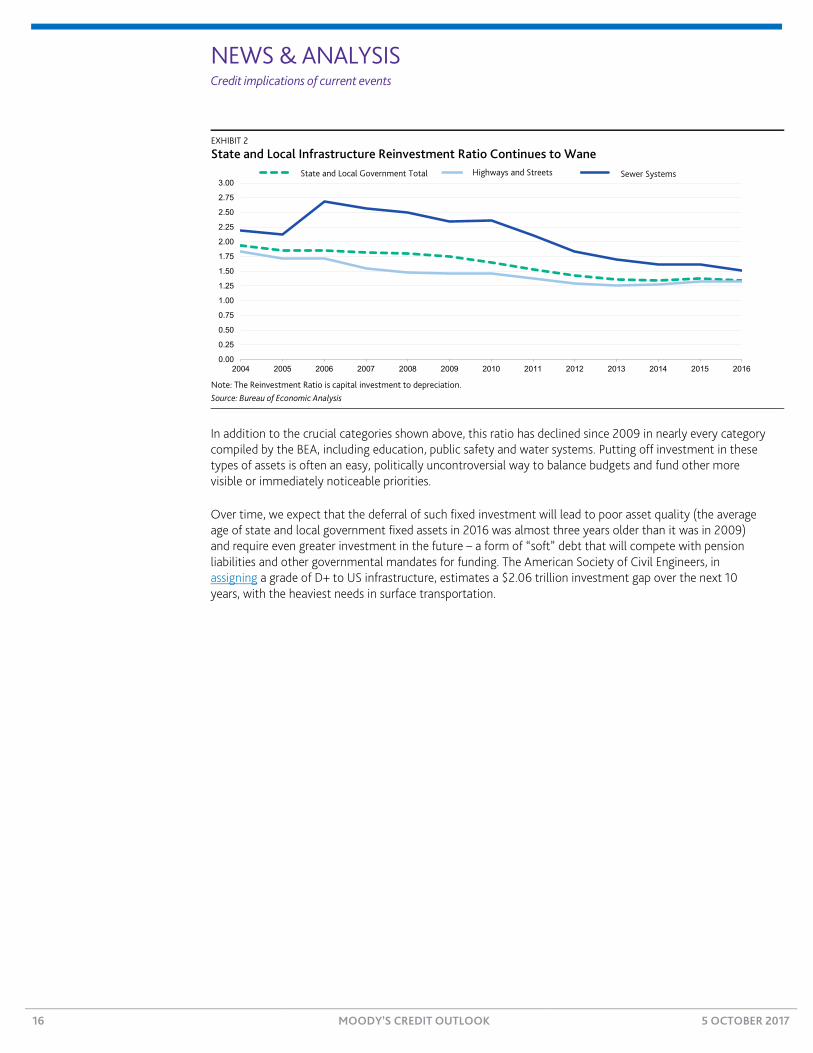

State and local governments, facing pressure to spend more on pensions, public education and other priorities apparently more pressing than infrastructure, have been curtailing investment in a broad range of capital assets.7 A rough proxy for the rate of infrastructure investment is the ratio of capital spending to depreciation, the basis on which state and local government infrastructure investment has tracked steadily downward for more than a decade (see Exhibit 2), including in such key categories as sewer systems and highways and streets.

7 The BEA data for “state and local governments” encompass a broad range of entities including airports, transit systems, housing

authorities and utilities. The decline in capital expenditures for state and local governments appears to conflict with increases in state capital expenditures over the past three years that we have described in our research on states. The discrepancy is likely explained by entities included in state and local governments that are not states.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

$0

$50

$100

$150

$200

$250

$300

$350

$400

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

$ Bi

llion

s

Amount - left axis Percent of GDP - right axis

Dan Seymour, CFA Vice President - Senior Analyst +1.212.553.4871 [email protected]

NEWS & ANALYSIS Credit implications of current events

16 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017

EXHIBIT 2

State and Local Infrastructure Reinvestment Ratio Continues to Wane

Note: The Reinvestment Ratio is capital investment to depreciation. Source: Bureau of Economic Analysis

In addition to the crucial categories shown above, this ratio has declined since 2009 in nearly every category compiled by the BEA, including education, public safety and water systems. Putting off investment in these types of assets is often an easy, politically uncontroversial way to balance budgets and fund other more visible or immediately noticeable priorities.

Over time, we expect that the deferral of such fixed investment will lead to poor asset quality (the average age of state and local government fixed assets in 2016 was almost three years older than it was in 2009) and require even greater investment in the future – a form of “soft” debt that will compete with pension liabilities and other governmental mandates for funding. The American Society of Civil Engineers, in assigning a grade of D+ to US infrastructure, estimates a $2.06 trillion investment gap over the next 10 years, with the heaviest needs in surface transportation.

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

State and local government total Highways and streets Sewer systemsState and Local Government Total Highways and Streets Sewer Systems

RECENTLY IN CREDIT OUTLOOK Select any article below to go to last Monday’s issue of Credit Outlook

17 MOODY’S CREDIT OUTLOOK 5 OCTOBER 2017 8

NEWS & ANALYSIS Corporates 2 » Siemens' Merger of Mobility Unit with Alstom Is

Credit Positive » Alstom's Tie-Up with Siemens' Rail Operations Creates

Global Number 2, a Credit Positive » For Bouygues, an Alstom-Siemens Mobility Merger Is

Credit Positive » Air Berlin Liquidation Will Hasten Airline Consolidation, a

Credit Positive for the Sector » Deutsche Wohnen's €800 Million Convertible-Bond Issue

Will Increase Leverage » Scania's Antitrust Fine Is Credit Negative for

Parent Volkswagen » APT Pipelines Will Benefit from Increasing Demand for

Gas Transportation » Indika Will Gain Control of Indonesia’s Third-Largest Coal

Producer, a Credit Positive

Banks 13 » Brazil's Lower Payroll Loan Rates for Retirees Are Credit

Negative for Banco Mercantil do Brasil » Grupo Financiero Galicia's Capital Raise Is Credit Positive » European Banking Authority Strengthens Banks' Corporate

Governance Rules, a Credit Positive » German Banks’ Deposit Protection Fund Reforms Are Credit

Negative for Smaller Private Banks » Portugal's Largest Banks Team Up to Manage Problem Loans,

a Credit Positive » Guaranty's Planned Bond Buyback Will Boost Net

Interest Income » The Commercial Bank Enters Negotiations to Sell Stake in

United Arab Bank, a Credit Positive » Thailand's Additional Capital Requirement for Systemically

Important Banks Is Credit Positive

Insurers 27 » Pacific Life Sells 20% of Its Aircraft Leasing Subsidiary, a

Credit Positive

Sovereigns 28 » US President Trump's Proposed Tax Framework Is Likely

Credit Negative for US, Positive for Most Sectors » Foreign Investment in Jamaica's Alpart Alumina Refinery Is

Credit Positive for the Sovereign » Swiss Voters Reject Proposal to Increase Pension Funding, a

Credit Negative » Turkey's Fiscal Program Portends More Borrowing as

Spending Rises, a Credit Negative

Sub-sovereigns 35 » Russian Regions Will Benefit from Programme Restructuring

Budget Loans

MOODYS.COM

Report: 197584

© 2017 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating, agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be reckless and inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or other professional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a Nationally Recognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an entity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registered with the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it fees ranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

EDITORS SENIOR PRODUCTION ASSOCIATE Jay Sherman and Elisa Herr Amanda Kissoon