Embed Size (px)

Citation preview

NEWSLETTER

December 2014NEWSLETTER

December 2014

Preface

Private & Confidential2 | Nov. 2014

Talati & Talati wishes you and your family a Merry Christmas & a very Happy, Prosperous, Healthy, Wealthy & Fruitful New Year 2015. Let the New Year bring peace and tranquility and let the world prospers in all fronts for humanity. Christmas is celebrated on the 25th December every year with great pomp and show. Christmas is not just a day, an event to be observed and speedily forgotten but it is a spirit which should permeate every part of our lives.

November and December months are periods where time is spent on reviewing what has been done in the past three quarters and planning and scheduling for the last quarter and training and education. It is the right time to give a changed look to all aspiration. It is said that change is the only thing that is constant. Time change, year change, trends change, generation pass but knowledge endures.

This month newsletter consist of topics on Company Law Settlement Scheme (CLSS) with a circular, Goods & Service Tax with few Highlights, Implementation of New Accounting Standards with a press release issued by MCA and a important judgement of the Hon’ble CESTAT, Delhi in the case of Bharat Sanchar Nigam Ltd. Vs. Commissioner of Central Excise, Jaipur (2014).

Once again, we wish you a Happy Christmas & Prosperous New Year 2015.

Looking forward for your reviews, feedbacks & suggestions.

Enjoy Reading.....

Many Thanks!!!!!

Regards,Editorial Team

Talati & Talati

Private & Confidential3 |

The Ministry of Corporate Affairs, in order to give an opportunity to companies who have failed to file annual statutory documents (Annual Return and Financial Statements), has launched Company Settlement Scheme, 2014 (CLSS – 2014), vide General Circular no. 34/2014 dated 12.08.2014.

The Company Law Settlement Scheme, 2014 (CLSS-2014) gives an opportunity to the defaulting companies to enable them to make their default good by filing belated documents. Corporates can avail the following benefits:

1. Immunity from prosecution for delayed filing

2. A reduced additional fee of 25% of the actual additional fees payable

3. Escape for directors disqualified under section 164(2) of Companies Act, 2013

Company Law Settlement Scheme CLSS 2014

The Companies Act, 2013 lays down more stringent penal consequences for defaulting companies. For example, section 451 prescribes twice the fine for repeated second default within a period of three years. Further the provisions of section 164(2) disqualify a directors from being appointed re-appointed in case the company has not filed financial statements or annual returns for any continuous period of three financial years.Despite that it was observed that a large percentage of companies have not filed their statutory documents which makes them liable for penalties and prosecution for such non-compliance. Also there are large number of companies which after

Nov. 2014

Company Law Settlement Scheme

Private & Confidential

the Registrar for declaring such companies as “dormant company”. The provisions of section 455 enable such inactive companies to remain on the Register of Companies with minimal compliance requirements.

Silent Features/Procedure/Consequences of Non-Compliances for CLSS-2014

A. Documents covered under this scheme

The scheme CLSS-2014 shall apply to the following belated documents only:

1. Form 20B - Form for filing Annual Return by a company having Share Capital.

2. Form 21A - Particulars of Annual Return for the company not having Share Capital.

3. Form 23AC, 23ACA, 23AC - XBRL and 23ACA - XBRL - Forms for filing Balance Sheet and Profit & Loss Account.

4. Form 66 - Form for filing Compliance Certificate with the ROC.

5. Form 238 - Form for Intimation for Appointment of Auditors.

B. Cases not covered by the scheme

The scheme does not apply to:

1. To companies against which action for striking off the name {section 560(5) Companies Act, 1956} has already been initiated by the Registrar of Companies.

2. Where any application has already been filed by the companies for action of striking off name.

3. Where applications have been filed for obtaining Dormant Status under

4 | Nov. 2014

Private & Confidential

section 455 of the Companies Act, 2013.

4. To vanishing companies.

C. Applicability

Any defaulting company can apply for annual documents which were due for filing up to 30th June, 2014.

D. Benefits:

1. Condonation of the delay in filing the Annual Returns or financial statements.

2. Grant of the immunity for prosecution.

3. Reduced charging of additional fee @ 25% of the actual additional fees payable.

4. Non applicability of disqualification of directors u/s 164(2) (a).

5. Opportunity to Inactive companies to get their companies declared as 'dormant company' in a simple application at reduced fee.

E. What will happen to existing appeals filed by company against prosecution launched?

The applicant company before filing application under the scheme is required to withdraw the appeal and furnish proof of such withdrawal along with the application.

5 | Nov. 2014

Private & Confidential

The defaulting inactive companies, while filing ClSS-2014 can, simultaneously, either:

1. Apply to get themselves declared as Dormant Company by filing e-form MSC-1 at 25% of the fee for the said form; or

2. Apply for striking off the name of the company by filing e- Form FTE at 25% of the fee payable on form FTE.

G. Application and grant of Immunity

After filing of belated documents, the application seeking immunity in respect of such documents filed under the Scheme is to be made electronically in the e-Form CLSS-2014. The said e-form shall be available on the MCA21 portal from 1st September, 2014. The CLSS-2014 should be filed not later than three months from the date of closure of the Scheme. There shall not be any fee payable on this Form. The ROC shall consider the application and upon being satisfied shall grant the Immunity certificate In respect of documents filed under this Scheme.

H. Penal and Prosecution

Section 92 of the Companies Act 2013 provides for penalty at Rs. 1000 per day extending up to Rs. 10 Lacs and also Imprisonment of directors up-to a term of 6 months.

I. Disqualification of Directors

Also Section 164(2) provides for Disqualification of Director if the company has not filed annual returns for 3 or more consecutive years. The disqualification which was earlier only restricted to public companies is now also extended to

F. Options for inactive companies:

6 | Dec. 2014

General Circular No. 44/2014Dated: 14.11.2014

Subject: COMPANY LAW SETTLEMENT SCHEME, 2014 (CLSS-2014)

In continuation to the Ministry’s General Circular No. 34/2014 dated 12.08.2014 and 40/2014 dated 15/10/2014 on the subject cited above, this Ministry has, on consideration of requests received from various stakeholders, has decided to extend the Company Law Settlement Scheme (CLSS 2014) upto 31st December, 2014.

Private & Confidential8 |

One of the biggest taxation reforms in India the Goods and Service Tax (GST) is all set to integrate State economies and boost overall growth. GST will create a single, unified Indian market to make the economy stronger. The implementation of GST will lead to the abolition of other taxes such as octroi, central sales tax, state-level sales tax, entry tax, stamp duty, telecom license fees, turnover tax, tax on consumption or sale of electricity, taxes on transportation of goods and services thus avoiding multiple layers of taxation that currently exist in India.Goods and Services Tax is a comprehensive tax levy on manufacture, sale and consumption of goods and services at a national level. Through a tax credit mechanism, this tax is collected on value-added goods and services at each stage of sale or purchase in the supply chain. The system allows the set-off of GST paid on the procurement of goods and services against the GST which is payable on the supply of goods or services. However, the end consumer bears this tax as he is the last person in the supply chain.Under GST, the taxation burden will be divided equitably between manufacturing and services, through a lower tax rate by increasing the tax base and minimizing exemptions. It is expected to help build a transparent and

Private & Confidential| Dec. 2014

Goods & Service Tax

corruption-free tax administration. GST will be levied only at the destination point, and not at various points. It is estimated that India will gain $15 billion a year by implementing the Goods and Services Tax as it would promote exports, raise employment and boost growth. It will divide the tax burden equitably between manufacturing and services. In the GST system, both Central and State taxes will be collected at the point of sale. Both components (the Central and State GST) will be charged on the manufacturing cost. This will benefit individuals as prices are likely to come down. Lower prices will lead to more consumption, thereby helping companies.India is planning to implement a dual GST system. Under dual GST, a Central Goods and Services Tax (CGST) and a State Goods and Services Tax (SGST) will be levied on the taxable value of a transaction. All goods and services, barring a few exceptions, will be brought into the GST base. There will be no distinction between goods and services. Almost 140 countries have already implemented the GST. Most of the countries have a unified GST system. Brazil and Canada follow a dual system where GST is levied by both the Union and the State governments. It will not be an additional tax. CGST will include central excise duty (Cenvat), service tax, and additional duties of customs at the central level; and value-added tax, central sales tax, entertainment tax, luxury tax, octroi, lottery taxes, electricity duty, state surcharges related to supply of goods and services and purchase tax at the State level.The combined GST rate is being discussed by government. The rate is expected around 14-16 per cent. After the total GST rate is arrived the States and the Centre will decide on the CGST and SGST rates. Currently, services are taxed at 10 per cent and the combined charge indirect taxes on most goods is around 20 per cent. The prices are expected to fall in the long term as dealers might pass on the benefits of the reduced tax to consumers. Alcohol, tobacco, petroleum products are likely to be out of the GST regime.

Private & Confidential9 | Dec. 2014

Private & Confidential10 |

Highlights of New Proposed Goods & Service Tax (GST)1. The basic principal governing behind GST is to have single Taxation System for Goods and Services across the country. Currently Indian economy has various taxes on Goods and services such as VAT, Service Tax, Excise, Entertainment Tax, Luxury Tax Etc. now in the new Proposal of GST; we will be having only two taxes on all goods and Services as follows: a) State Level GST(SGST) b) Central Level GST (CGST)

2. In case of Central GST, following Taxes will be subsumed with CGST which are at presently levied separately on goods and services by Central government: a) Central Excise Duty b) Additional Excise Duty c) The Excise Duty levied under Medicinal and toiletries preparation Act d) Service Tax e) Additional Custom Duty (CVD) f) Special Additional Duty g) Surcharge h) Education Cess and Secondary and Higher Secondary education Cess3. In case of State GST, following taxes will be subsumed with SGST; which are

priestly levied on goods and services by State Governments : a) VAT/ Sales Tax b) Entertainment Tax (unless it is levied by local bodies) c) Luxury Tax d) Tax on lottery e) State Cess and Surcharge to the extend related to supply of goods and

services.a) The basic principal for subsuming of taxes in GST is provided as follows:

b) Those taxes which commences with import / manufacture /production of

Nov. 2014

Private & Confidential11 | Dec. 2014

goods or provision of services at one end and the consumption of goods and services at other end.

c) The taxes, levies and fees which are not related to supply of goods & services should not be subsumed under GST.

4. Taxes on items containing alcohol and petroleum product are kept out of GST. They will continue to be taxed as per existing practices.

5. Tax on Tobacco products will be subject to GST. But government can levy the extra Excise duty over and above GST.

6. The Small Taxpayer: The small taxpayers whose gross annual turnover is less than 1.5 Crore are exempted from CGST and SGST.

7. Input Tax Credit (ITC): Taxes Paid against CGST allowed as ITC against CGST. Taxes paid against SGST allowed as ITC against SGST.

8. Cross utilization of ITC between the Central GST and State GST would not be allowed. Exception: Inter State Supply of goods and services.

9. PAN based identification number will be allowed to each taxpayer to have integration of GST with Direct Tax

10.IGST Model and ITC: a) Center would levy IGST levy ( CGST + SGST) b) The ITC will be allowed in this transaction will be SGST, IGST, CGST as

applicable. c) Appropriate provision will be provided for consignment or Stock transfer..11.GST Rate Structure: a) Two Rate Structure b) A lower rate for necessary items and goods of basic importance c) Standard rate for goods in General d) Special Rate12.Exports are fully exempted with Zero rates.

Private & Confidential12 | Dec. 2014

Final report on new accounting norms likely within 15 daysThe National Advisory Committee on Accounting Standards (NACAS) is set to submit its final report on new accounting standards to the government within 15 days, paving the way for Indian companies to voluntarily adopt the International Financial Reporting Standards or IFRS from April next year.

The report will specify certain carve outs or exceptions since India is only converging with IFRS and not adopting the norms entirely. NACAS is also ironing out differences between the definition specified in the accounting standards and the Companies Act including the definition of related party transaction, the section which is also being considered by the corporate affairs ministry for amendment.

As announced by finance minister Arun Jaitley in his budget speech in July, the adoption of new Indian Accounting Standards (Ind-AS), converged with IFRS, by domestic companies is scheduled to start from 2015-16 and will be mandatory from 2016-17. NACAS is also working towards clearing several accounting standards recommended by the Chartered Accountants Institute including the one on financial instruments, which addresses the issue of recognition of loan losses that banks and financial institutions in developed countries faced during the 2008 global financial crisis, besides fair value measurement and employee benefits.

The new standards are likely to increase global acceptance of financial statements

of Indian companies. The government shall keep the carve outs to the bare minimum to ensure that there is global acceptability for financial statements prepared. Banks and insurance companies are expected to have a separate set of Ind-AS.The corporate services ministry, which is implementing the companies law, had in September reconstituted NACAS to advise the central government on the formulation of accounting policies and accounting standards. The body will be in place till the National Financial Reporting Authority (NFRA), proposed under the Companies Act 2013, is set up.

Press Information BureauGovernment of India

Ministry of Corporate Affairs

25-November-2014 15:59 IST

Implementation of New Accounting Standards

In accordance with the announcement in the Budget Speech 2014-15, the Indian Accounting Standards (Ind-AS), based on the International Financial Reporting Standards (IFRS), will be notified for voluntary adoption from the financial year 2015-16 and mandatorily from financial year 2016-17. Banks, Financial Institutions and Insurance Companies may be brought under the purview of the standards at a later date. The class of companies to which these standards will apply are being finalized and would be notified along with the Ind-AS.

This was stated by Shri Arun Jaitley, Minister of Corporate Affairs in written reply to a question in the Rajya Sabha.

Private & Confidential13 | Dec. 2014

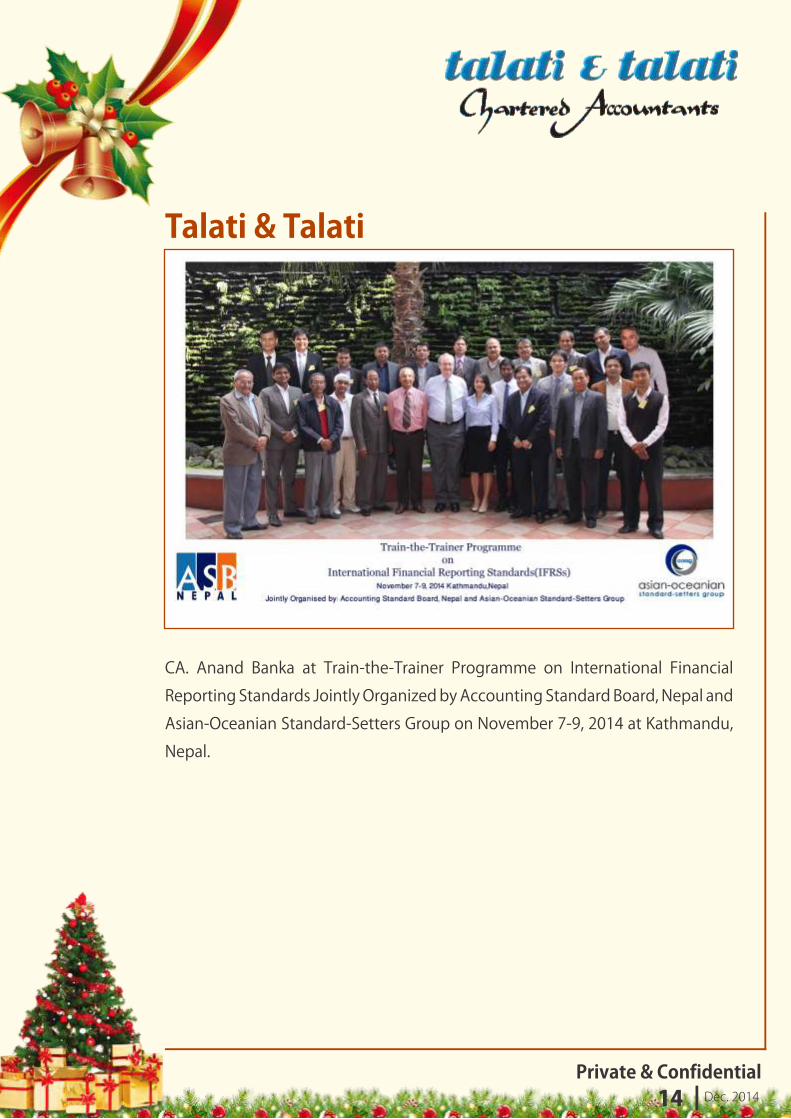

CA. Anand Banka at Train-the-Trainer Programme on International Financial Reporting Standards Jointly Organized by Accounting Standard Board, Nepal and Asian-Oceanian Standard-Setters Group on November 7-9, 2014 at Kathmandu, Nepal.

Private & Confidential14 | Dec. 2014

Talati & Talati

Important judgement of the Hon’ble CESTAT, Delhi in the case of Bharat Sanchar Nigam Ltd. Vs. Commissioner of Central Excise, Jaipur [(2014) 51 taxmann.com 10 (New Delhi - CESTAT)]on following issue:Issue:

Whether Department can adjust unconfirmed demand against refund payable to the Assessee?

Facts & Background:

Bharat Sanchar Nigam Ltd. (“the Appellant”) filed refund claim of Rs. 11, 79,720/- for the excess amount paid. The Appellant was issued a Show Cause Notice dated January 17, 2007 (“SCN”) to show cause as to why their refund claim of Rs. 11,79,720/- should not be rejected. The Appellant submitted their reply dated May 25, 2007 and was sanctioned entire refund claim by the Assistant Commissioner vide Order-in-Original No. 44/R/2007.However, the Assistant Commissioner later issued a corrigendum dated July 17, 2007 to the SCN stating that as the Appellant had taken Cenvat credit to the tune of Rs. 11, 18,182/- on the strength of the invoices for Capital goods issued by their Head Office, the same was not admissible as their Head Office was not registered as a registered dealer and therefore asking why their refund claim should not be rejected to the extent of Rs. 11, 18,182/-.Later, the Commissioner (Appeals) also upheld the adjustment of Rs. 11,18,182/- out of the total refund of Rs. 11,79,720/-and the Appellant was refunded only the net (remaining) amount of Rs. 61,538/- in form of Cenvat credit. Being aggrieved,

Private & Confidential15 | Dec. 2014

Case Law-1

the Appellant preferred an appeal before the Hon’ble CESTAT, Delhi.

Held:

The Hon’ble CESTAT, Delhi observed that there has been no Show Cause Notice given to the Appellant for showing cause as to why Cenvat credit amount of Rs.11, 18,182/- (adjusted from the amount of refund sanctioned) was inadmissible to them and even if the corrigendum issued on July 17, 2007 is an attempt to be treated as a Show Cause Notice, the said corrigendum falls fatally short of the requirement of a notice under Section 73 of the Finance Act, 1994.

Accordingly, it was held by the Hon’ble Tribunal that while confirmed demand can be adjusted from the amount of refund, there is no provision to adjust unconfirmed demand from the amount of refund and in the instant case, Rs. 11,18,182/- cannot be held to be a confirmed demand. Hence, the Department was directed to refund back Rs. 11, 18,182/- to the Appellant along with applicable interest.

Private & Confidential16 | Dec. 2014

17 |

December

20th

21st

5th Service TaxService tax Payment by Companies for November

6th Central ExciseDue Date for payment of Excise Duty for all Asssessee (including SSI Units)

MVAT

E.S.I.C

MVAT*

TDS Payment of November

E.S.I.C. Payment for November

Monthly payment of NovemberMVAT Monthly Returns for October.(TAX>1000000)

P.F. Payment for November

10th Central ExciseFilling ER-1 Return(Other than SSI Units)Filling Quarterly Return ER-2 by 100% EOUs.Filling monthly ER-6 Returns by specified class of Assessees regarding principal inputs

15th P.F.

Prof.TaxPayment for November

*If payment of MVAT made as per time prescribed, additional 10 days are given for uploading e-return

7th Income taxTDS Payment of November

31st

Important Dates

Private & ConfidentialDec. 2014

Private & ConfidentialDec. 2014|

Disclaimer: With respect to information available herein, Talati & Talati Chartered Accountants do not make any warranty, express or implied, including the warranty of merchantability and fitness for a particular purpose or assume any liability or responsibility for the accuracy, completeness, or usefulness of such information.

You acknowledge and agree that all proprietary rights in the information received shall remain the property of Talati & Talati Chartered Accountants. Reproduction, redistribution and transmission of any information contained herein are strictly prohibited. Talati & Talati Chartered Accountants shall not be liable for any claims or losses of any nature, arising indirectly or directly from use of the data or material or otherwise howsoever arising.

TALATI & TALATI GROUPwww.talatiandtalati.com

AHMEDABAD HEAD OFFICEAmbica Chambers,

Nr. Old High Court, Navrangpura,

Ahmedabad-380 009.

E-mail: [email protected]

Tel: +91 79 2754 4571-72

Fax: +91 79 2754 2233

SURAT BRANCH4008, World Trade Centre,

Nr. Udhana Darwaja,

Ring Road, Surat - 395002

E-Mail: [email protected]

Tel: 0261 2361236, +919824644423

VADODARA BRANCH501, Race Course Tower,

Race Course South,

Vadodara-390 007.

E-mail: [email protected]

Tel: +91 265 305 8025-26

Fax: +91 265 305 8027

ANAND BRANCH127, Sardar Nagar Co-operative

Housing Society, Nr. Swami Marble,

Karamsad, Anand

E-mail: [email protected]

Tel: + 91 269 265 6405

MUMBAI BRANCH233, 2nd Floor,

Kaliandas Udyog Bhavan,

Near Century Bazaar, Prabhadevi,

Mumbai- 400 025, India

E-mail: [email protected]

Tel: +91 22 4004 3747

DELHI BRANCH15, Birbal Road,

Jangpura Extension,

New Delhi-110 014.

E-mail: [email protected]

Tel: +91 11 4182 4199 | +91 11 3255 3900

Fax: +91 11 4182 3900

Designed by: eggfirst.com

We can be found on facebookPlease our facebook page to get regular updates.

SCAN THIS CODEto know more

18