Embed Size (px)

Citation preview

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 1

OVERVIEW

Catalyst

Personalization is an emerging trend whereby food and drink products are more closely aligned with consumers’ individual

nutritional requirements, lifestyle aspirations and taste preferences. It reflects a crossover between the health and

individualism mega-trends: the coming together of intensifying health concerns and a ‘just for me’ ethos driving a desire for

products, services, and experiences that cater to specific needs and identities.

Summary • Personalized nutrition is an emerging yet potentially influential trend as intensifying health concerns drive

interest in more sophisticated and effective forms of nutrition.

• Personalized nutrition overlaps with a number of other food and beverage trends and themes but is now evolving

with complex nutritional science focusing on genetics.

• Consumers are attracted by the prospect of custom solutions but the desire for personalized benefits is

secondary to most other aspects influencing dietary choices.

• Many consumers appear skeptical about personalized nutrition, especially nutrigenomics. Another potential

inhibitor is that the desire for personalized choices conflicts with the desire for choice simplification, a less

complicated lifestyle and value conscious purchasing.

• Manufacturers can capitalize by developing a broad range of functional food and beverage products offering

antidotes to the myriad health problems faced by consumers. Developing age, gender and occasion targeted

food and beverage solutions is also a key innovation platform. Datamonitor also encourages industry players to

be future focused and invest in the opportunities presented by developments in nutritional science such as

nutrigenomics.

NEW CONSUMER INSIGHT (NCI) SERIES

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition Profiting by aligning food and drink products more closely with consumers’ individual nutritional requirements, aspirations and preferences

Reference Code: DMCM4650

Publication Date: November 2008

Table of Contents

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 2

TABLE OF CONTENTS

Overview 1 Catalyst 1 Summary 1

THE FUTURE DECODED 8 INTRODUCTION: Personalized nutrition is an emerging yet potentially influential trend 8 TREND: Intensifying health concerns are driving interest in more sophisticated and effective forms of nutrition9 TREND: Personalized nutrition overlaps with a number of other food and beverage trends and themes but is now evolving with complex nutritional science focusing on genetics 16 INSIGHT: Consumers are attracted by the prospect of custom solutions but the desire for personalized benefits is secondary to most other aspects influencing dietary choices 32 INSIGHT: Many consumers appear skeptical about personalized nutrition, especially nutrigenomics 39 INSIGHT: The desire for personalized choices conflicts with the desire for simplified choices, a less complicated lifestyle and value conscious purchasing 48

ACTION POINTS 54 ACTION: Develop a broad range of functional food and beverage products offering antidotes to the myriad health problems facing consumers 54 ACTION: Develop age, gender and occasion targeted food and beverage solutions 80 ACTION: Be future focused and invest in the opportunities presented by developments in nutritional science such as nutrigenomics 91

APPENDIX 94 Definitions 94 Methodology 94 Further reading and references 95 Ask the analyst 96 Datamonitor consulting 96 Disclaimer 96

Table of Contents

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 3

TABLE OF FIGURES

Figure 1: Personalized nutrition reflects a crossover between the health and individualism mega-trends 8

Figure 2: More than three quarters of consumers consider diet and nutrition to be an important factor in creating a feeling of wellbeing 10

Figure 3: Diet and nutrition is one of six dimensions associated with the broader notion of wellness 10

Figure 4: Health considerations have a significant amount of influence on food and beverage choices 12

Figure 5: Consumers demonstrate a high level of interest, at least attitudinally, towards label information 14

Figure 6: Intensifying health concerns lead to more considered choices governed by a heightened reliance on food labels which in turn is likely to fuel the demand for more personalized choices 15

Figure 7: Personalized nutrition encompasses four specific sub-trends and associated product benefits 17

Figure 8: Functional food and drinks are formulated to offer specific health and wellness benefits to targeted consumers and consumer needs, and are therefore central to personalized nutrition 19

Figure 9: A high proportion of consumers have no concern over gluten 20

Figure 10: Nutrigenomics is geared towards understanding the response of the body to diets and food factors through various ''omics'' technologies such as transcriptomics, proteomics, and metabolomics 24

Figure 11: Identity based consumption is driven by the importance that shoppers place on ‘brand attitude’ 29

Figure 12: Enjoying small indulgences to escape everyday pressures has remained a theme in global consumer behavior in 2008 30

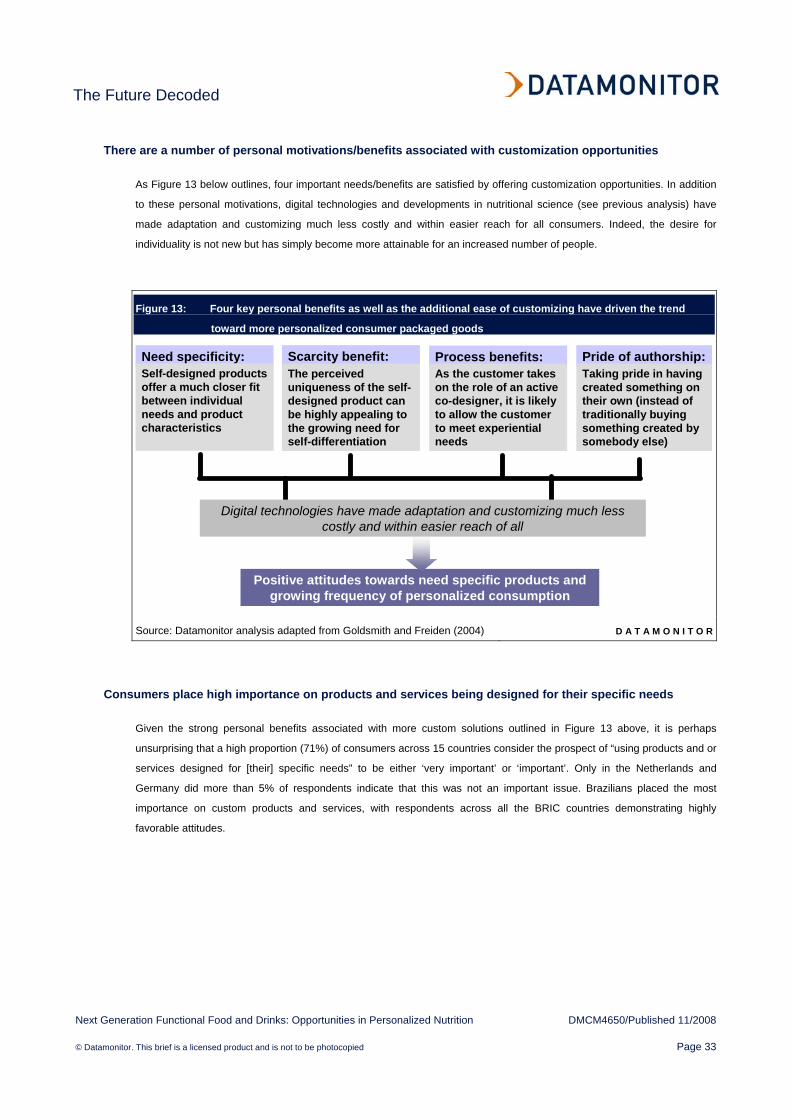

Figure 13: Four key personal benefits as well as the additional ease of customizing have driven the trend toward more personalized consumer packaged goods 33

Figure 14: Consumers are attracted to the idea of using products and or services designed for specific needs 34

Table of Contents

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 4

Figure 15: When considering a wider set of food and beverage considerations, customization/personalization benefits are less important to global consumers 37

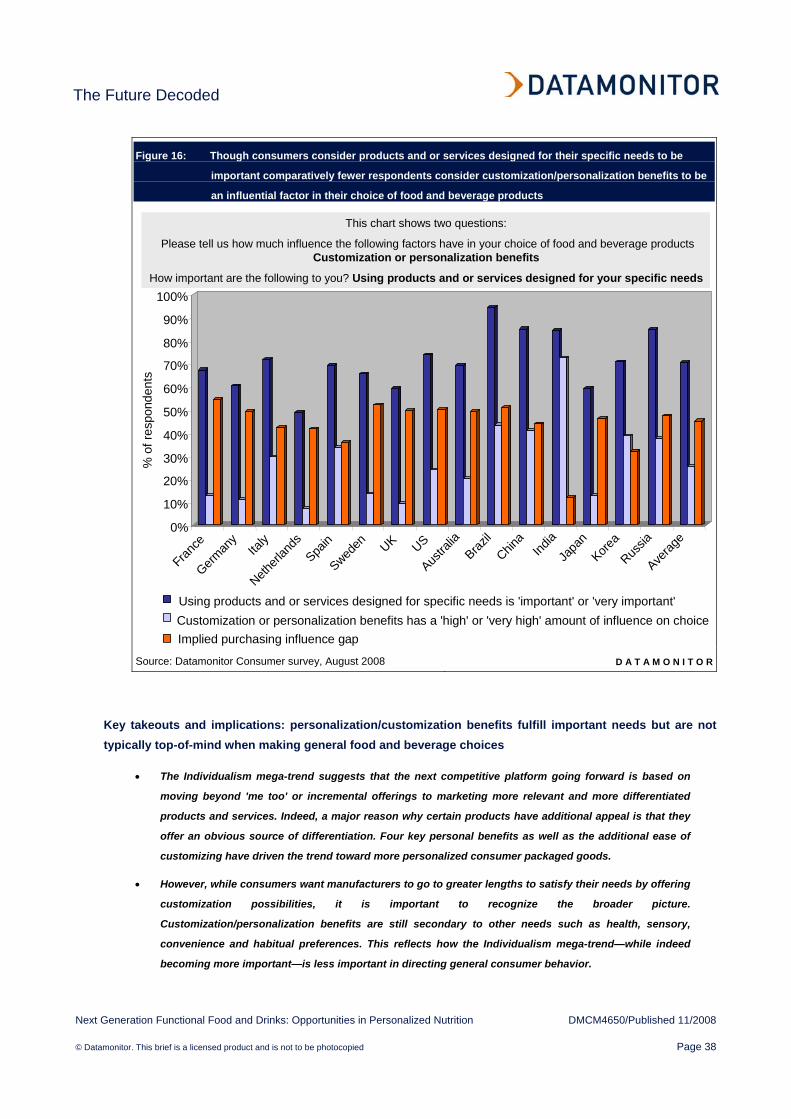

Figure 16: Though consumers consider products and or services designed for their specific needs to be important comparatively fewer respondents consider customization/personalization benefits to be an influential factor in their choice of food and beverage products 38

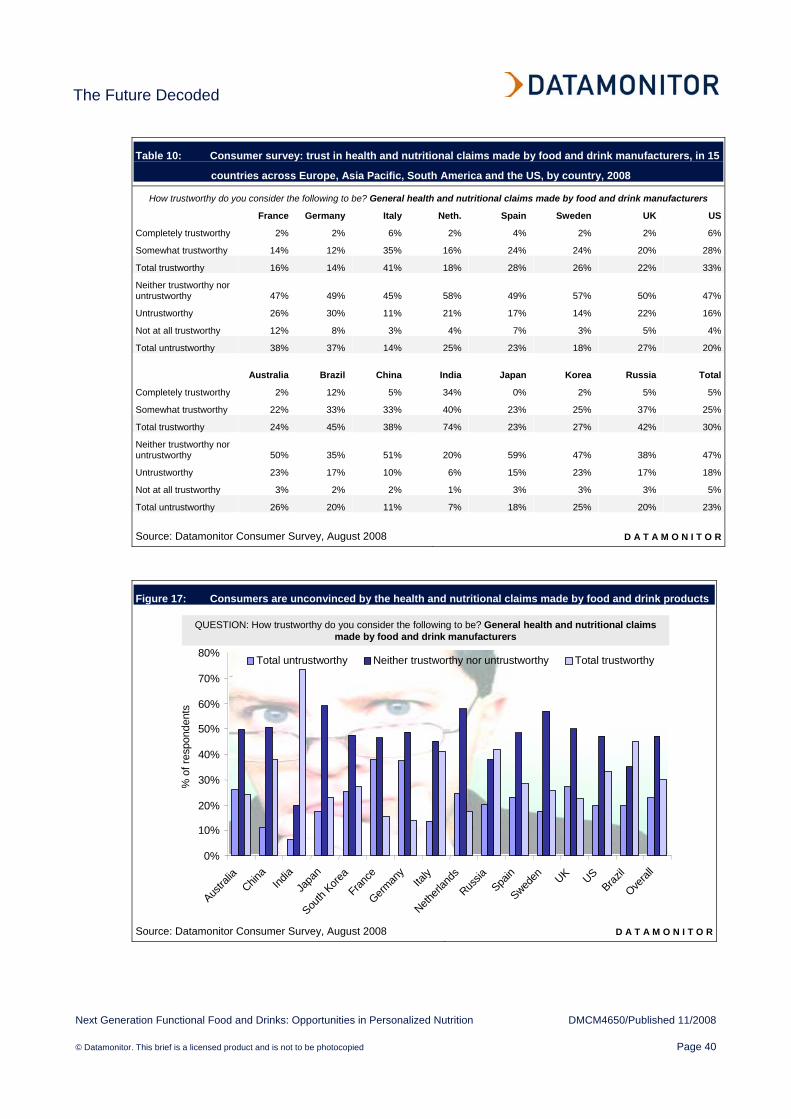

Figure 17: Consumers are unconvinced by the health and nutritional claims made by food and drink products 40

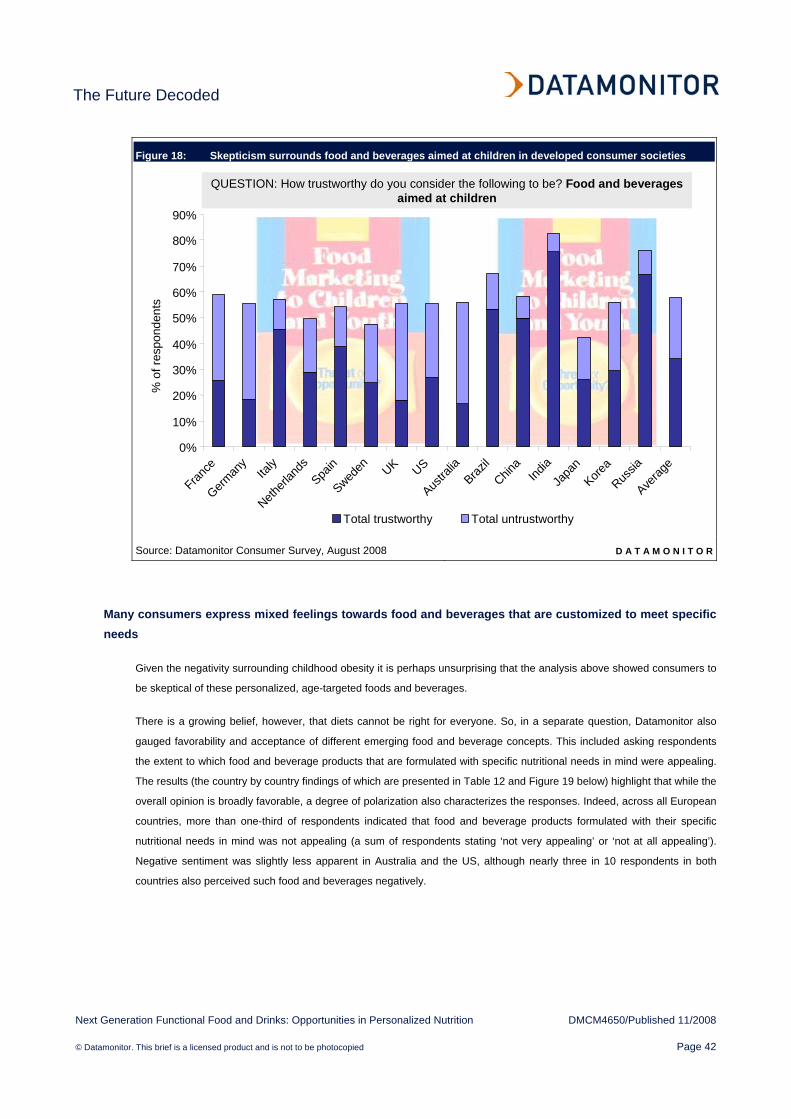

Figure 18: Skepticism surrounds food and beverages aimed at children in developed consumer societies 42

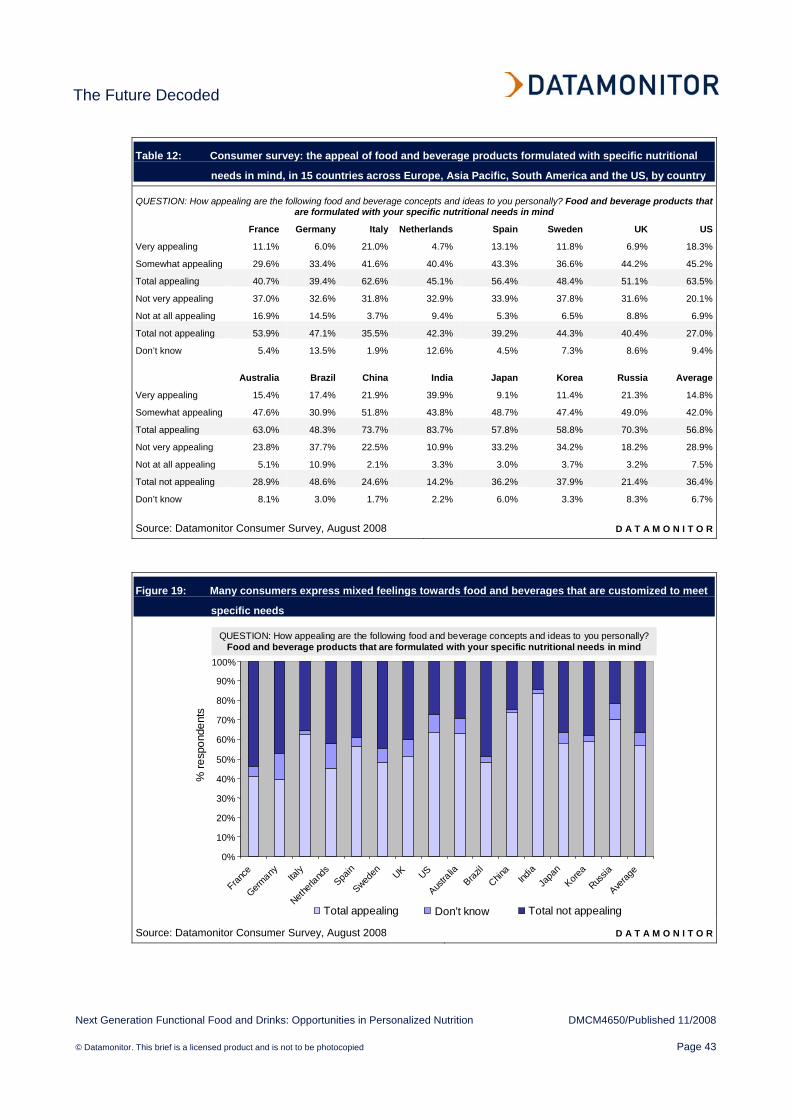

Figure 19: Many consumers express mixed feelings towards food and beverages that are customized to meet specific needs 43

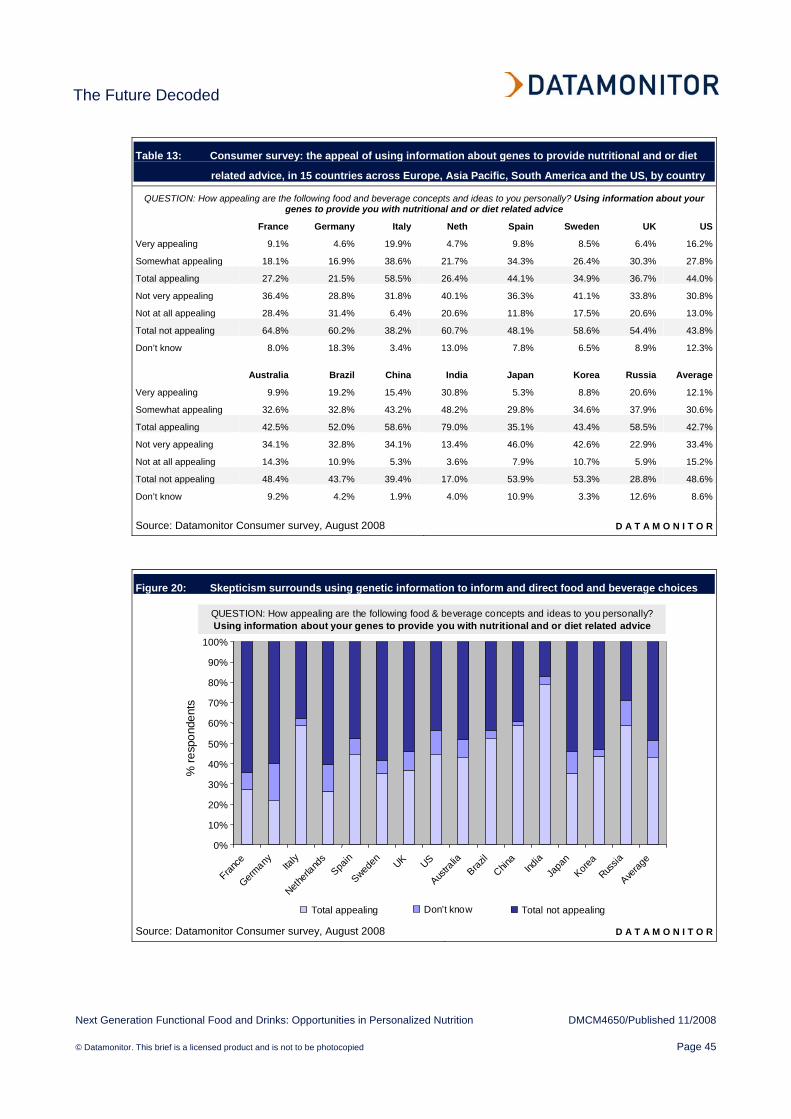

Figure 20: Skepticism surrounds using genetic information to inform and direct food and beverage choices 45

Figure 21: The desire for personalized choices conflicts with the desire for simplified choices, a less complicated lifestyle and value conscious purchasing 48

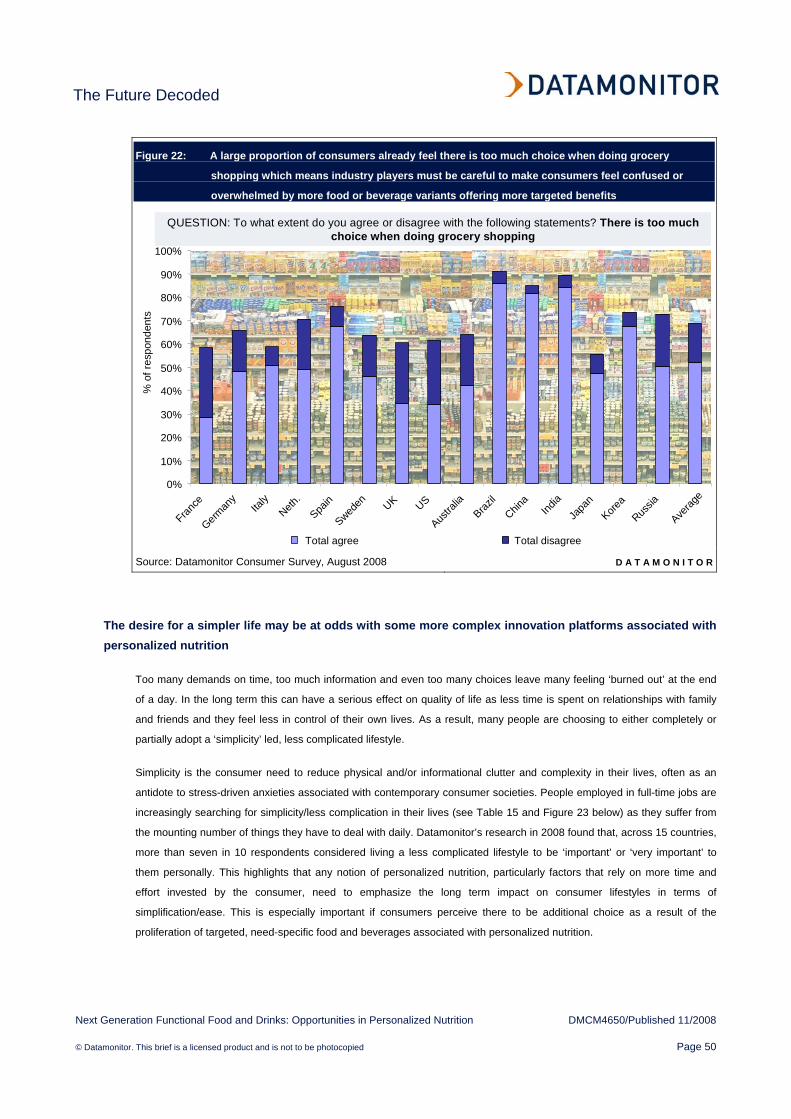

Figure 22: A large proportion of consumers already feel there is too much choice when doing grocery shopping which means industry players must be careful to make consumers feel confused or overwhelmed by more food or beverage variants offering more targeted benefits 50

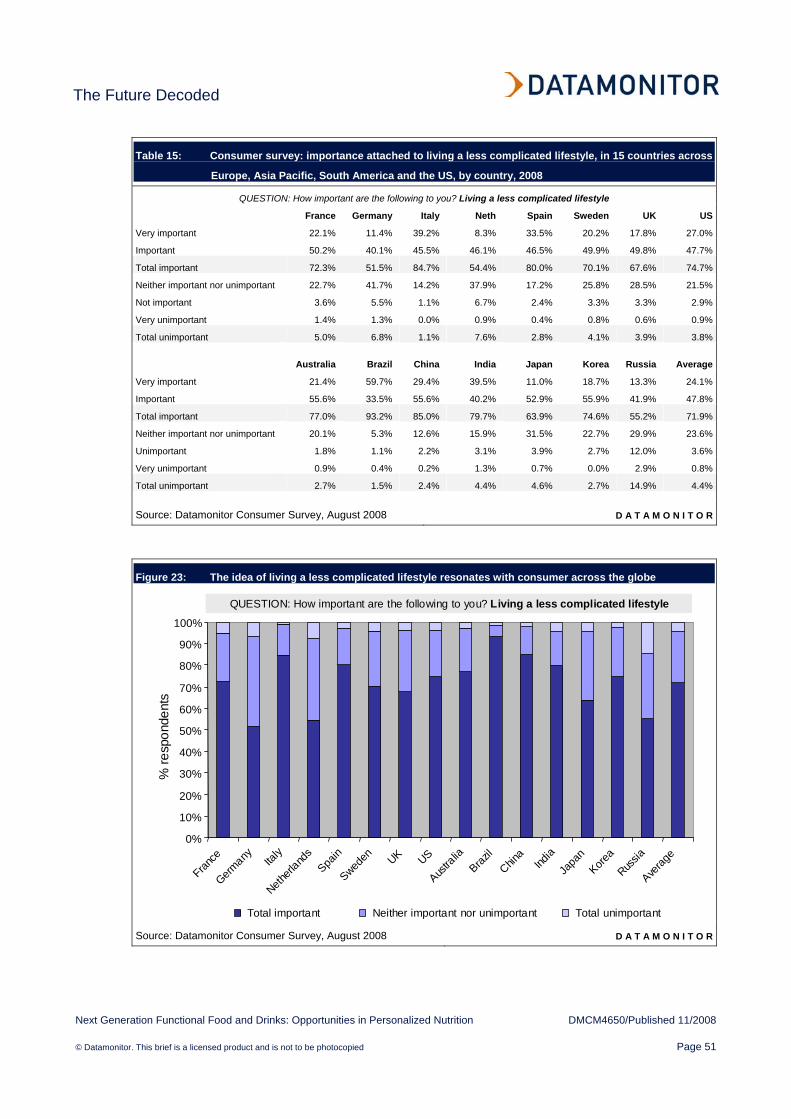

Figure 23: The idea of living a less complicated lifestyle resonates with consumer across the globe51

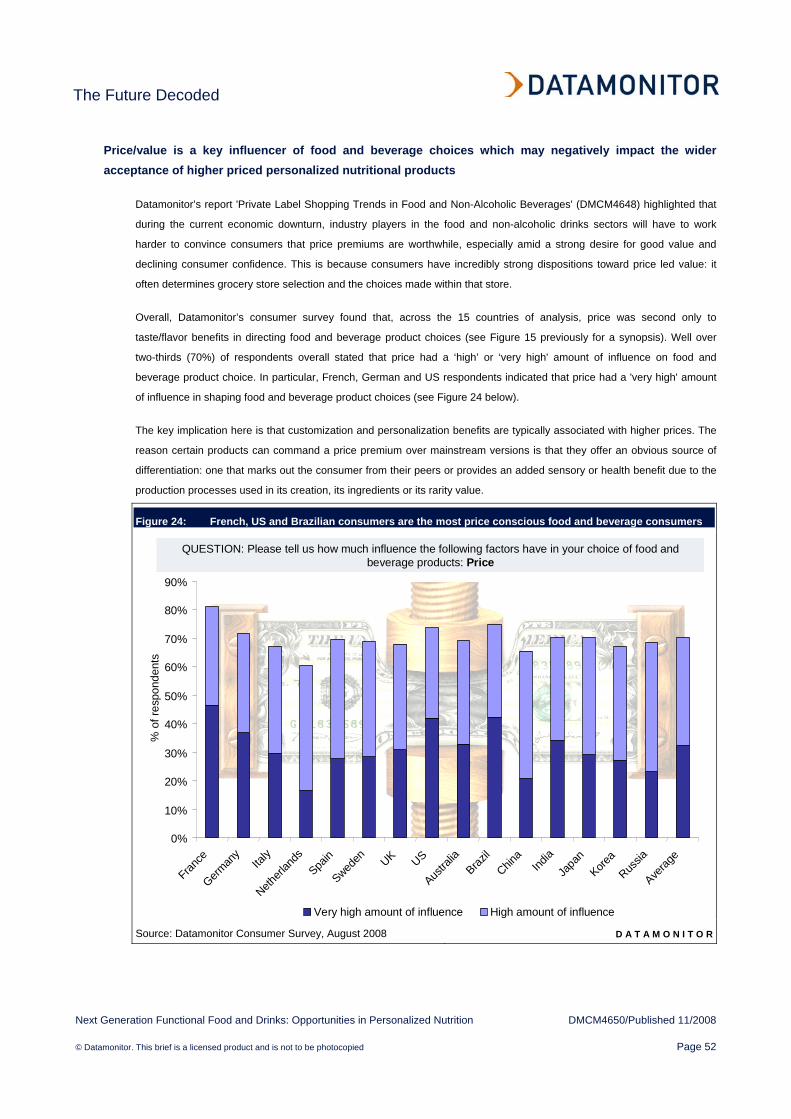

Figure 24: French, US and Brazilian consumers are the most price conscious food and beverage consumers 52

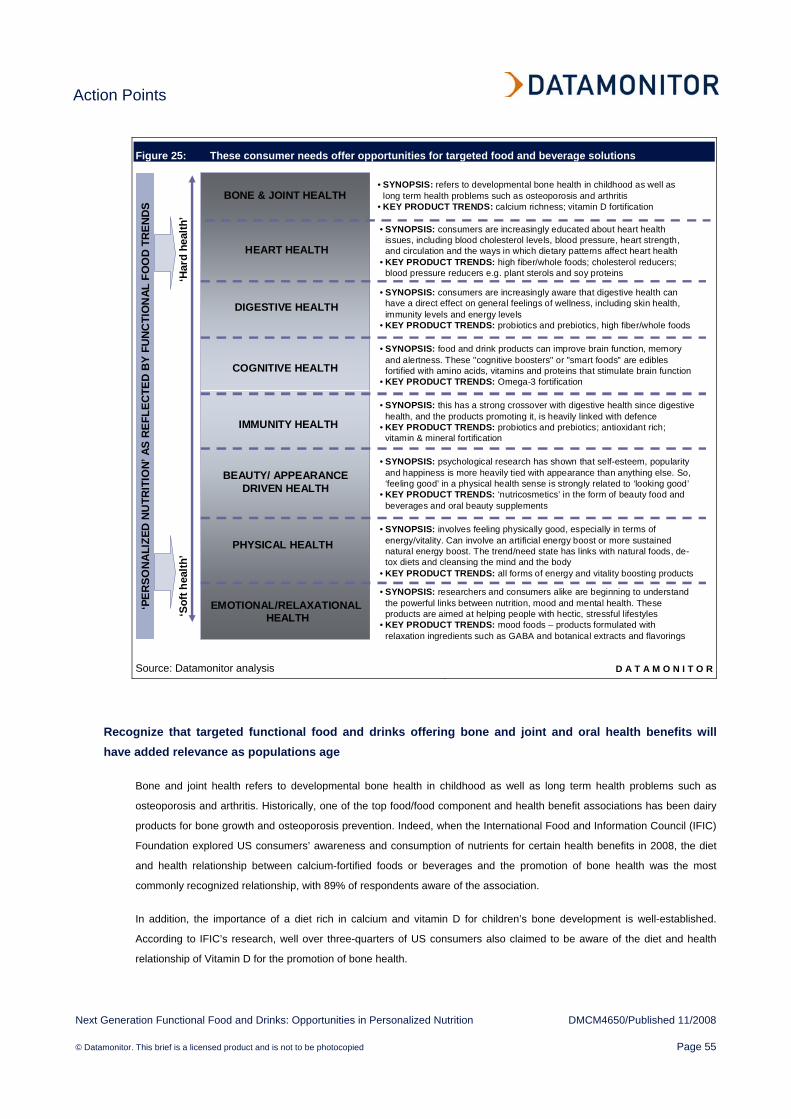

Figure 25: These consumer needs offer opportunities for targeted food and beverage solutions 55

Figure 26: Bone, joint and tooth strengthening food and beverages are all forms personalized nutrition through targeted functional products 57

Figure 27: Heart health products are prevalent across sectors and categories and range in claim specificity 60

Figure 28: Probiotics and prebiotics are being offered in tandem and across a broader range of product formats 62

Figure 29: Omega-3 DHA is typically the core ingredient for the proliferating lines of brain nourishing food and beverages 65

Table of Contents

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 5

Figure 30: Antioxidant rich ingredients and probiotics are being used to boost immunity health 68

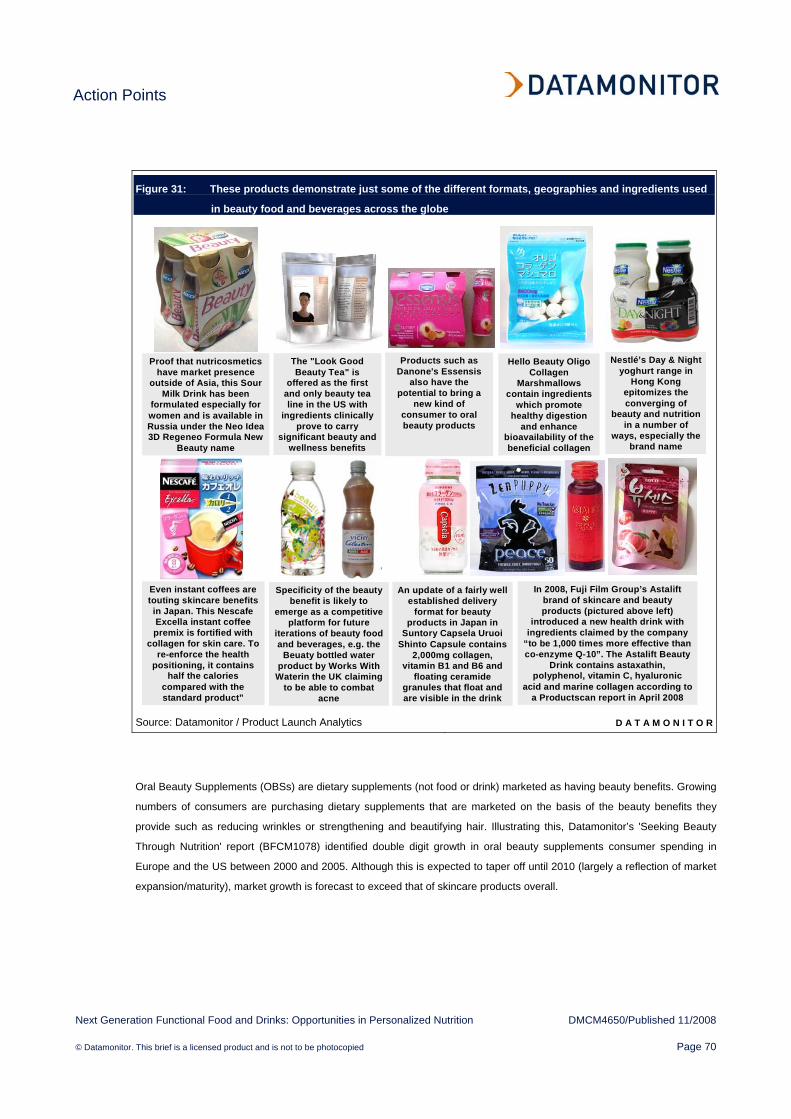

Figure 31: These products demonstrate just some of the different formats, geographies and ingredients used in beauty food and beverages across the globe 70

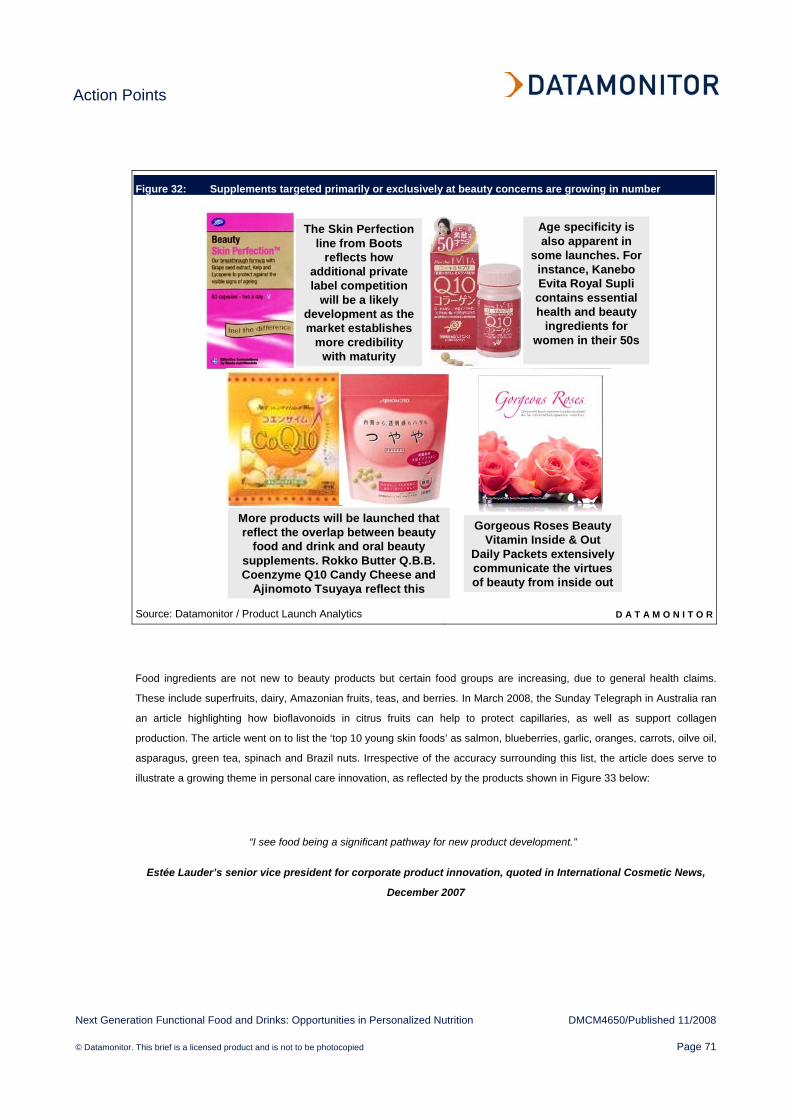

Figure 32: Supplements targeted primarily or exclusively at beauty concerns are growing in number 71

Figure 33: Traditional cosmetic companies are increasingly investigating how food ingredients can be beneficial to the skin and hair 72

Figure 34: Targeting the desire for energy and vitality is being done with more intensity and sophistication 74

Figure 35: Mood foods reflect the growing array of products targeting emotional wellbeing 77

Figure 36: Many brands are delivering ‘multi-faceted health’ by developing product ranges with variants that cater to the differing health needs of consumers 79

Figure 37: Gender specific products are well placed to capitalize on the personalized nutrition trend 83

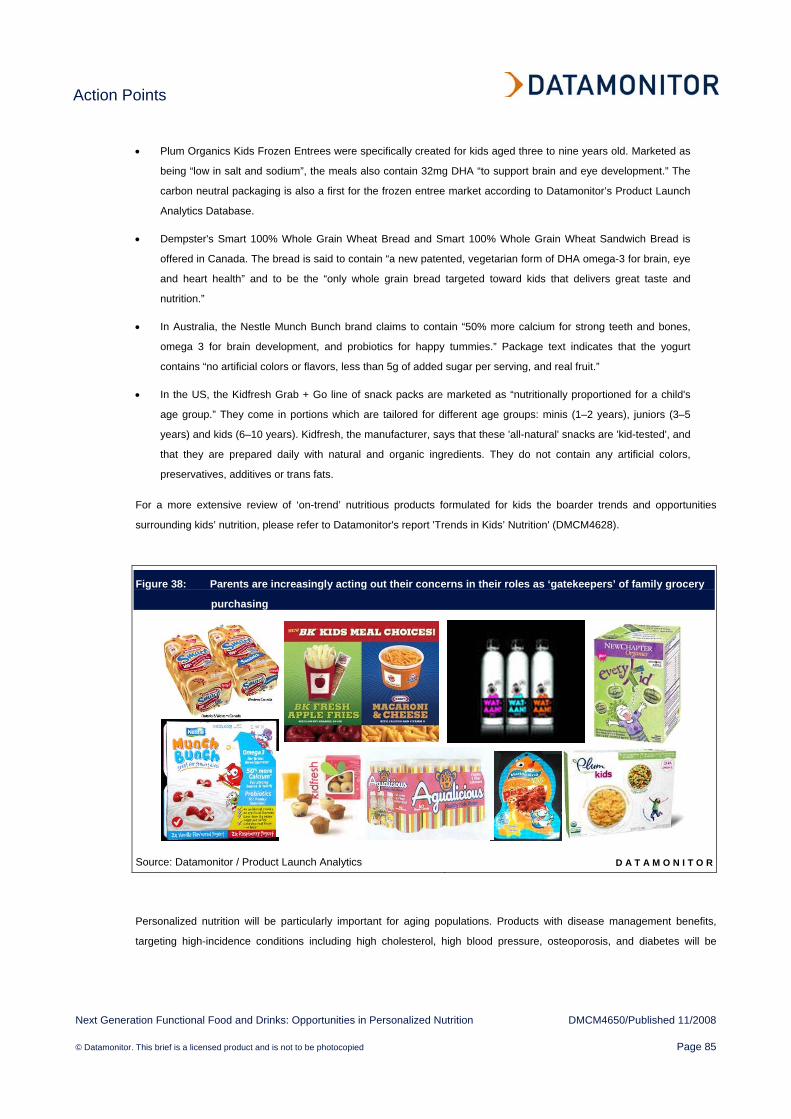

Figure 38: Parents are increasingly acting out their concerns in their roles as ‘gatekeepers’ of family grocery purchasing 85

Figure 39: Personalized nutrition will be particularly important for aging populations 87

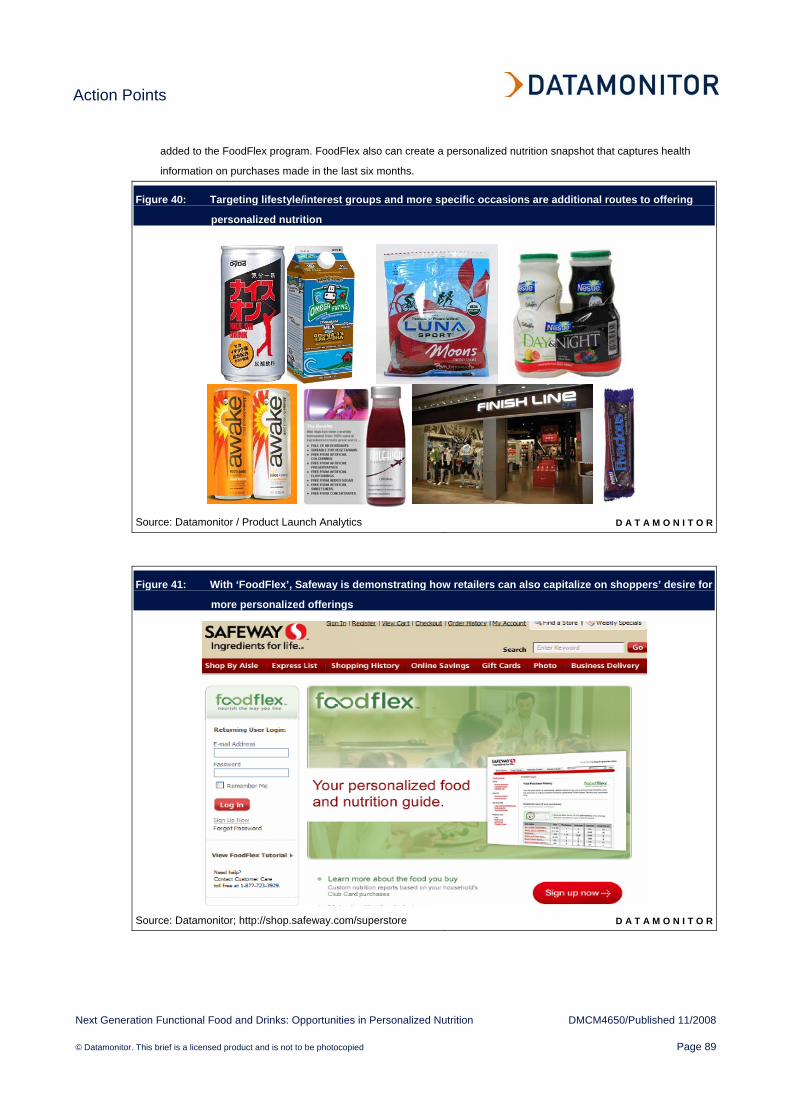

Figure 40: Targeting lifestyle/interest groups and more specific occasions are additional routes to offering personalized nutrition 89

Figure 41: With ‘FoodFlex’, Safeway is demonstrating how retailers can also capitalize on shoppers’ desire for more personalized offerings 89

Figure 42: Developing and clearly signposting gluten and lactose free products will become an increasing feature of food and drink product development in the coming years 91

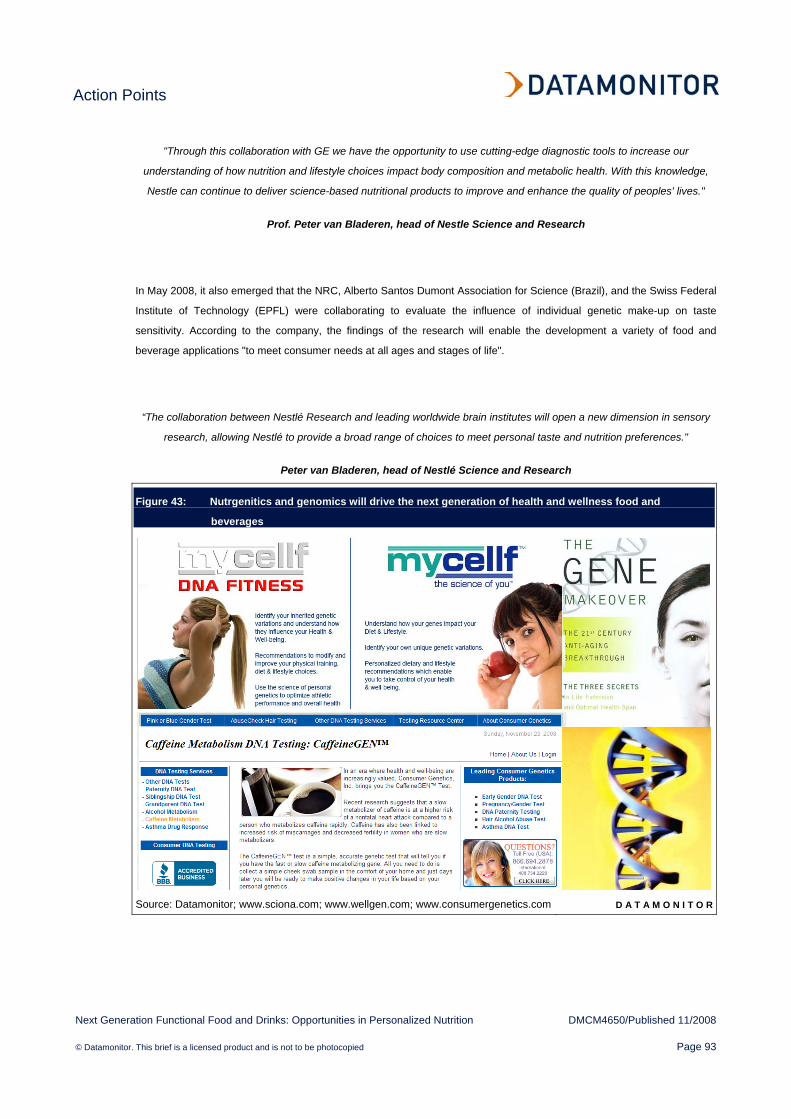

Figure 43: Nutrgenitics and genomics will drive the next generation of health and wellness food and beverages 93

Table of Contents

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 6

TABLE OF TABLES

Table 1: Consumer survey: the importance that individuals attach to diet and nutrition in creating a feeling of wellbeing or wellness, in 15 countries across Europe, Asia Pacific, South America and the US, by country, 2008 9

Table 2: Consumer survey: the influence of health on food and beverage product choices, in 15 countries across Europe, Asia Pacific, South America and the US, by country, 2008 11

Table 3: Consumer survey: the propensity to take active steps to eat more healthily more or less often, in 15 countries across Europe, Asia Pacific, South America and the US, by country, 2008 13

Table 4: Functional food and drink market value in Europe, the US and Asia Pacific ($ millions), by country, 2002–12 18

Table 5: Consumer survey: the importance that individuals attach to diet and nutrition in creating a feeling of wellbeing or wellness, in 15 countries across Europe, Asia Pacific, South America and the US, by country and gender, by country, 2008 21

Table 6: Consumer survey: the importance consumers attach to individuality and self-expression, in 15 countries across Europe, Asia Pacific, South America and the US, by country, 2008 27

Table 7: Consumer survey: the importance attached to brands which match their attitudes and outlook on life, in 15 countries across Europe, Asia Pacific, South America and the US, by country, 2008 29

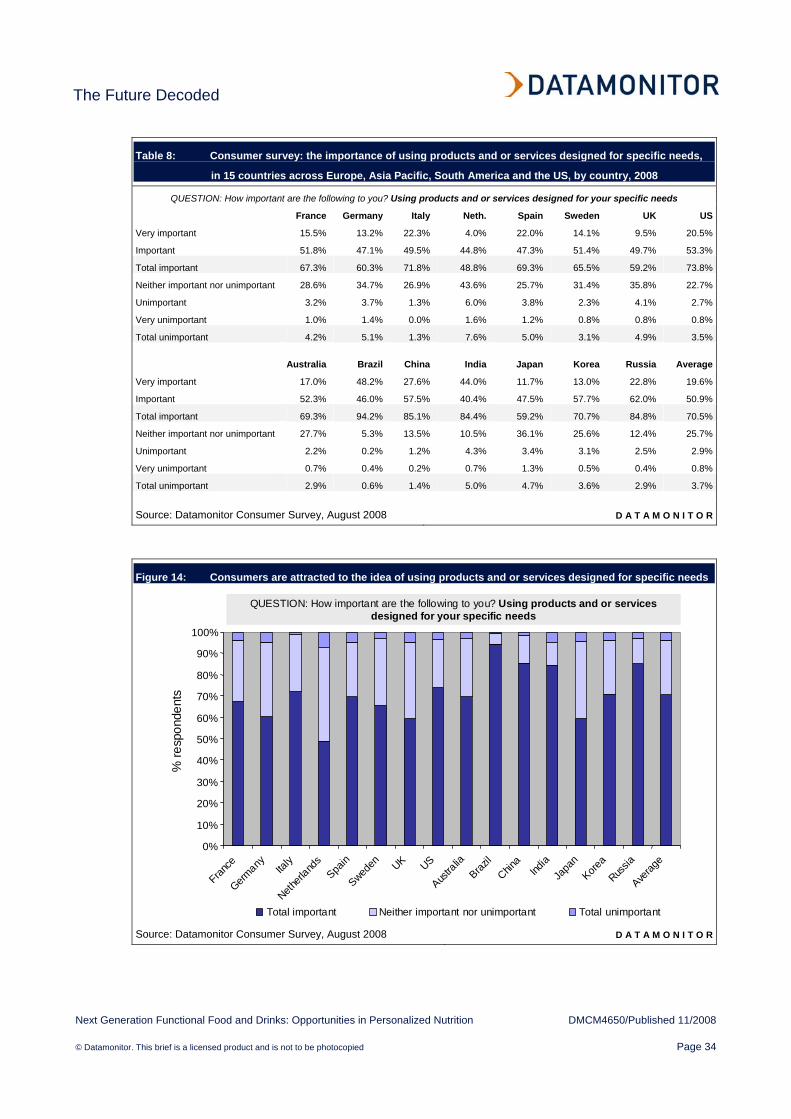

Table 8: Consumer survey: the importance of using products and or services designed for specific needs, in 15 countries across Europe, Asia Pacific, South America and the US, by country, 2008 34

Table 9: Consumer survey: the perceived influence of customization or personalization benefits on food and beverage product choices, in 15 countries across Europe, Asia Pacific, South America and the US, by country, 2008 36

Table 10: Consumer survey: trust in health and nutritional claims made by food and drink manufacturers, in 15 countries across Europe, Asia Pacific, South America and the US, by country, 2008 40

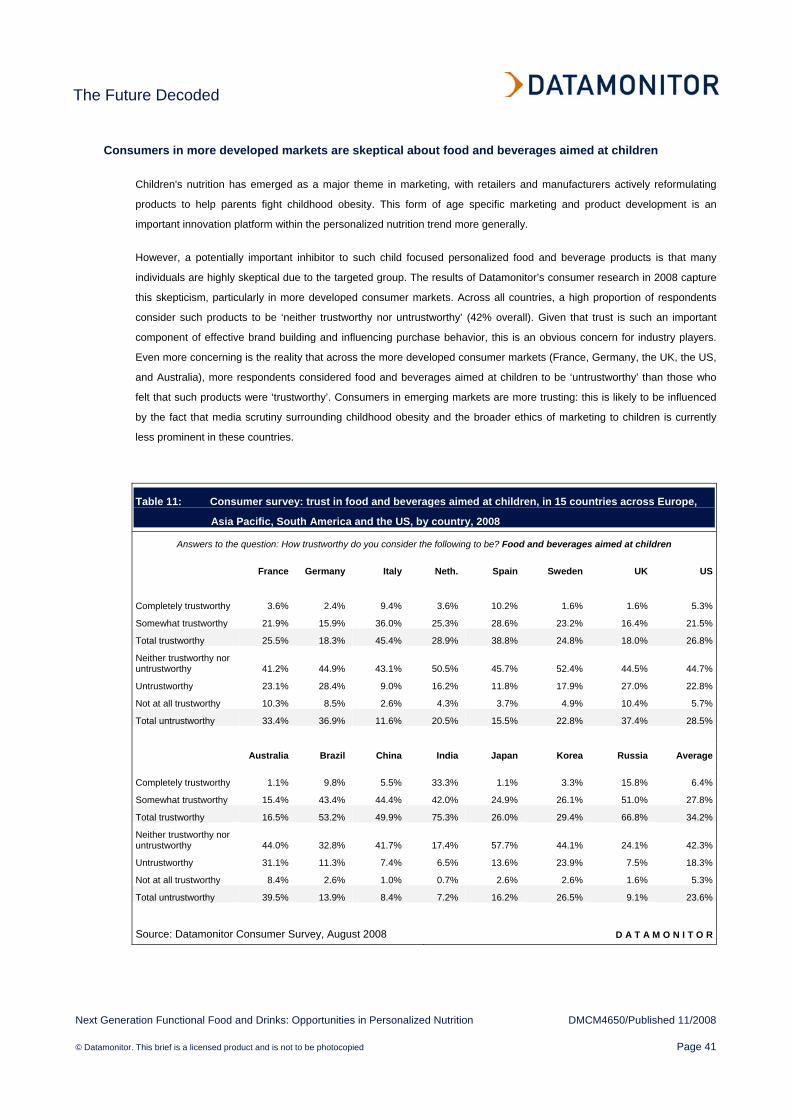

Table 11: Consumer survey: trust in food and beverages aimed at children, in 15 countries across Europe, Asia Pacific, South America and the US, by country, 2008 41

Table 12: Consumer survey: the appeal of food and beverage products formulated with specific nutritional needs in mind, in 15 countries across Europe, Asia Pacific, South America and the US, by country 43

Table of Contents

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 7

Table 13: Consumer survey: the appeal of using information about genes to provide nutritional and or diet related advice, in 15 countries across Europe, Asia Pacific, South America and the US, by country 45

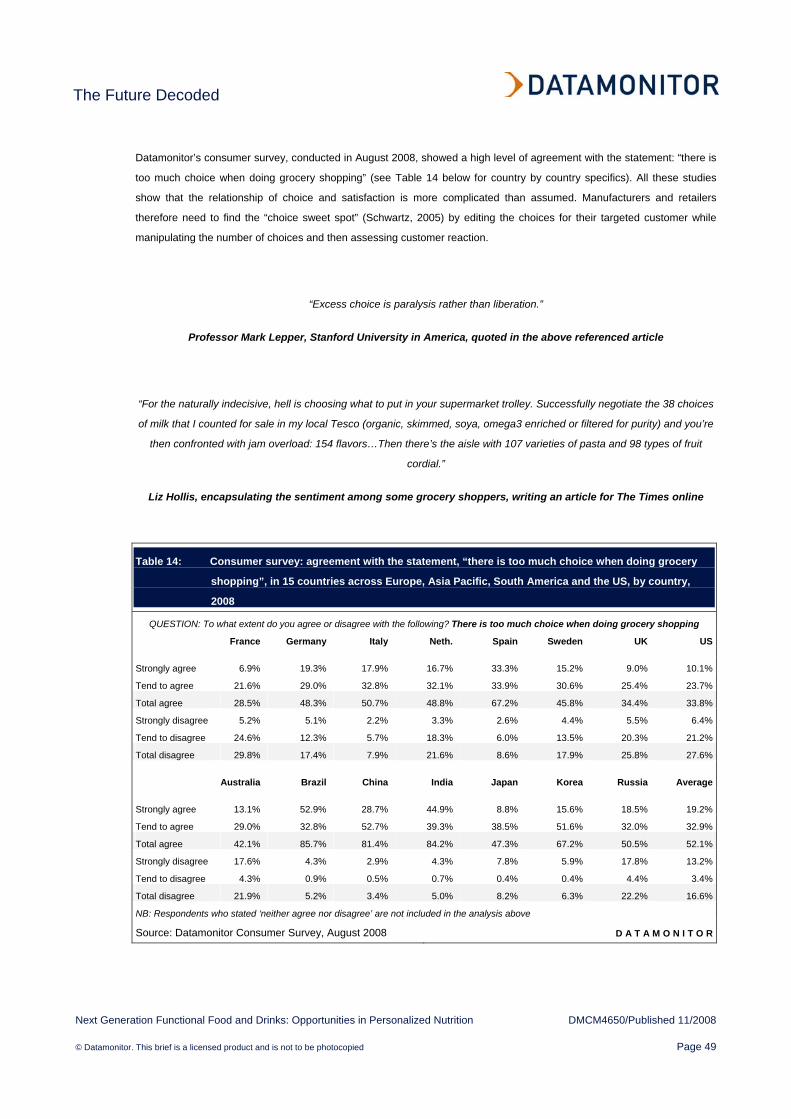

Table 14: Consumer survey: agreement with the statement, “there is too much choice when doing grocery shopping”, in 15 countries across Europe, Asia Pacific, South America and the US, by country, 2008 49

Table 15: Consumer survey: importance attached to living a less complicated lifestyle, in 15 countries across Europe, Asia Pacific, South America and the US, by country, 2008 51

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 8

THE FUTURE DECODED

INTRODUCTION: Personalized nutrition is an emerging yet potentially influential trend

Personalization is an emerging trend whereby food and drink products are more closely aligned with consumers’ individual

nutritional requirements, lifestyle aspirations and taste preferences. It reflects a crossover between the health and

individualism mega-trends: the coming together of intensifying health concerns and a ‘just for me’ ethos driving a desire for

products, services, and experiences that cater to specific needs and identities. Indeed, “‘personalized diets’ will have

replaced 20th century mass consumerism by 2030,” according to speakers at the Perspectives for Food conference, held by

the European Commission's Directorate-General for Research in Brussels in April 2007. There is a growing belief that diets

cannot be right for everyone. As a result, personalization, whether based on lifestyle, ethnicity, blood type or genetics, will

become an important component of dietary regimes going forward.

If successful branding is developing and marketing a product which the consumer perceives as possessing unique added

values which match their needs more closely, then personalized nutrition can also be viewed as an important component of

future focused food and beverage branding more generally. This report focuses on the differing components of

personalized nutrition, ranging from the choice of products to express self identity through to science-led nutritional

developments such as nutrigenomics. Before examining the specifics, Figure 1 below serves to highlight the key issues

surrounding developments in personalized nutrition. The remainder of this report explores these issues in detail.

Figure 1: Personalized nutrition reflects a crossover between the health and individualism mega-trends

HEALTH & WELLBEING

INDUSTRY PUSH

DRIVERS INHIBITORSECONOMIC DOWNTURN

LACK OF TRUST & AWARENESS

INDIVIDUALISM/NEED SPECIFICITY

Personalized nutrition reflects a

cross-over between the health and individualism

megatrends. These powerful drivers will

generate an intensifying focus on how nutritional benefits can be

tailored to meet the individual needs of

consumers

However, the longer-term

commercialization of personalized nutrition will be dependant on overcoming a

number of inhibitors

• Intensifying health concerns and a better understanding understand of the relationship between food and health

• Aging populations and escalating concerns about diet related illnesses related to aging

• A rejection of the one size fits all" approach to nutrition; dieters know from experience that not every diet works for everybody

• Increased self-responsibility for one’s health and wellness

• The importance of the self and the desire for products that protect/reinforce self identity

• The recognition that science has a major role to play in the fight against many of the diseases prevalent in society

• The growth of functional food and drinks which are scientifically formulated to address consumers’ individual nutritional needs

• Producing foods based on an individual’s genetic make up is at the cutting edge of current nutritional research

• Changing consumer priorities; economic wellbeing takes precedence over dietary wellbeing

• Personalized solutions are typically more expensive and are thus potentially less appealing to consumers who are trying to maximize their discretionary incomes

• Nutrigenomic science – the latest cutting edge approach to facilitating personalized nutrition – is still in its infancy

• So far, evidence on the interaction of nutrients, genetic variations and health implications is uncertain and controversial

• There is also evidence to suggest that consumer opinion is polarized. Some find the science-led approach to nutrition to be at odds with ‘normal’ food culture

• Consumer preference for a simpler choice and the desire for a less complication lifestyle moreover

A DESIRE FOR SIMPLICITY

Source: Datamonitor analysis D A T A M O N I T O R

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 9

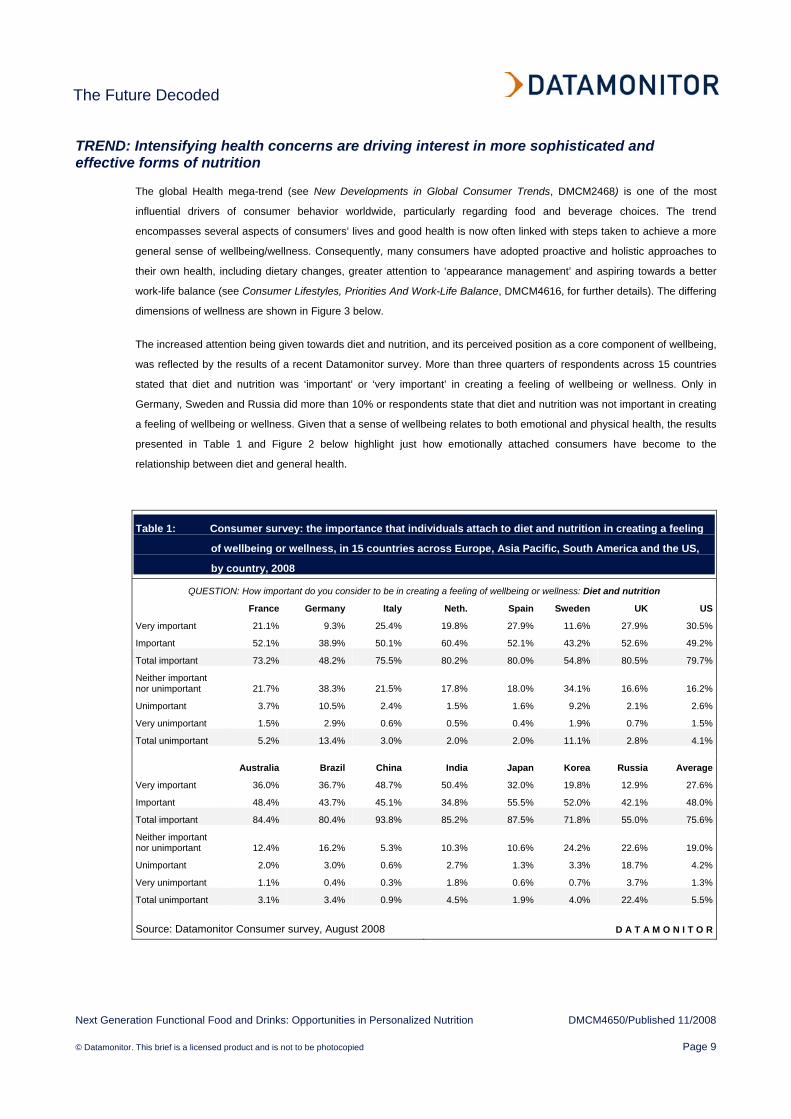

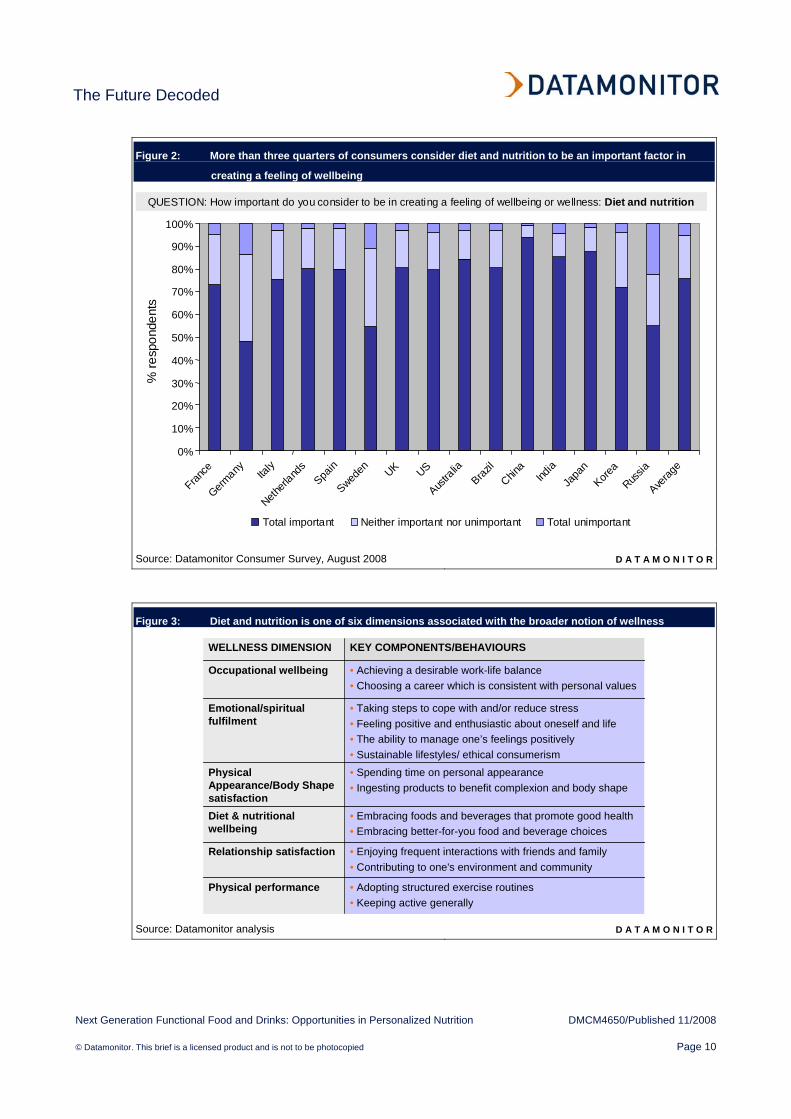

TREND: Intensifying health concerns are driving interest in more sophisticated and effective forms of nutrition

The global Health mega-trend (see New Developments in Global Consumer Trends, DMCM2468) is one of the most

influential drivers of consumer behavior worldwide, particularly regarding food and beverage choices. The trend

encompasses several aspects of consumers’ lives and good health is now often linked with steps taken to achieve a more

general sense of wellbeing/wellness. Consequently, many consumers have adopted proactive and holistic approaches to

their own health, including dietary changes, greater attention to ‘appearance management’ and aspiring towards a better

work-life balance (see Consumer Lifestyles, Priorities And Work-Life Balance, DMCM4616, for further details). The differing

dimensions of wellness are shown in Figure 3 below.

The increased attention being given towards diet and nutrition, and its perceived position as a core component of wellbeing,

was reflected by the results of a recent Datamonitor survey. More than three quarters of respondents across 15 countries

stated that diet and nutrition was ‘important’ or ‘very important’ in creating a feeling of wellbeing or wellness. Only in

Germany, Sweden and Russia did more than 10% or respondents state that diet and nutrition was not important in creating

a feeling of wellbeing or wellness. Given that a sense of wellbeing relates to both emotional and physical health, the results

presented in Table 1 and Figure 2 below highlight just how emotionally attached consumers have become to the

relationship between diet and general health.

Table 1: Consumer survey: the importance that individuals attach to diet and nutrition in creating a feeling

of wellbeing or wellness, in 15 countries across Europe, Asia Pacific, South America and the US,

by country, 2008

QUESTION: How important do you consider to be in creating a feeling of wellbeing or wellness: Diet and nutrition

France Germany Italy Neth. Spain Sweden UK US

Very important 21.1% 9.3% 25.4% 19.8% 27.9% 11.6% 27.9% 30.5%

Important 52.1% 38.9% 50.1% 60.4% 52.1% 43.2% 52.6% 49.2%

Total important 73.2% 48.2% 75.5% 80.2% 80.0% 54.8% 80.5% 79.7%

Neither important nor unimportant 21.7% 38.3% 21.5% 17.8% 18.0% 34.1% 16.6% 16.2%

Unimportant 3.7% 10.5% 2.4% 1.5% 1.6% 9.2% 2.1% 2.6%

Very unimportant 1.5% 2.9% 0.6% 0.5% 0.4% 1.9% 0.7% 1.5%

Total unimportant 5.2% 13.4% 3.0% 2.0% 2.0% 11.1% 2.8% 4.1%

Australia Brazil China India Japan Korea Russia Average

Very important 36.0% 36.7% 48.7% 50.4% 32.0% 19.8% 12.9% 27.6%

Important 48.4% 43.7% 45.1% 34.8% 55.5% 52.0% 42.1% 48.0%

Total important 84.4% 80.4% 93.8% 85.2% 87.5% 71.8% 55.0% 75.6%

Neither important nor unimportant 12.4% 16.2% 5.3% 10.3% 10.6% 24.2% 22.6% 19.0%

Unimportant 2.0% 3.0% 0.6% 2.7% 1.3% 3.3% 18.7% 4.2%

Very unimportant 1.1% 0.4% 0.3% 1.8% 0.6% 0.7% 3.7% 1.3%

Total unimportant 3.1% 3.4% 0.9% 4.5% 1.9% 4.0% 22.4% 5.5%

Source: Datamonitor Consumer survey, August 2008 D A T A M O N I T O R

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 10

Figure 2: More than three quarters of consumers consider diet and nutrition to be an important factor in

creating a feeling of wellbeing

QUESTION: How important do you consider to be in creating a feeling of wellbeing or wellness: Diet and nutrition

% re

spon

dent

s

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

France

Germany Ita

ly

Netherl

ands

Spain

Sweden UK US

Austra

liaBraz

ilChin

aInd

iaJa

pan

Korea

Russia

Averag

e

Total important Neither important nor unimportant Total unimportant

Source: Datamonitor Consumer Survey, August 2008 D A T A M O N I T O R

Figure 3: Diet and nutrition is one of six dimensions associated with the broader notion of wellness

KEY COMPONENTS/BEHAVIOURSWELLNESS DIMENSION

• Adopting structured exercise routines• Keeping active generally

Physical performance

• Enjoying frequent interactions with friends and family• Contributing to one's environment and community

Relationship satisfaction

• Embracing foods and beverages that promote good health• Embracing better-for-you food and beverage choices

Diet & nutritional wellbeing

• Spending time on personal appearance• Ingesting products to benefit complexion and body shape

Physical Appearance/Body Shape satisfaction

• Taking steps to cope with and/or reduce stress• Feeling positive and enthusiastic about oneself and life • The ability to manage one’s feelings positively• Sustainable lifestyles/ ethical consumerism

Emotional/spiritual fulfilment

• Achieving a desirable work-life balance• Choosing a career which is consistent with personal values

Occupational wellbeing

KEY COMPONENTS/BEHAVIOURSWELLNESS DIMENSION

• Adopting structured exercise routines• Keeping active generally

Physical performance

• Enjoying frequent interactions with friends and family• Contributing to one's environment and community

Relationship satisfaction

• Embracing foods and beverages that promote good health• Embracing better-for-you food and beverage choices

Diet & nutritional wellbeing

• Spending time on personal appearance• Ingesting products to benefit complexion and body shape

Physical Appearance/Body Shape satisfaction

• Taking steps to cope with and/or reduce stress• Feeling positive and enthusiastic about oneself and life • The ability to manage one’s feelings positively• Sustainable lifestyles/ ethical consumerism

Emotional/spiritual fulfilment

• Achieving a desirable work-life balance• Choosing a career which is consistent with personal values

Occupational wellbeing

Source: Datamonitor analysis D A T A M O N I T O R

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 11

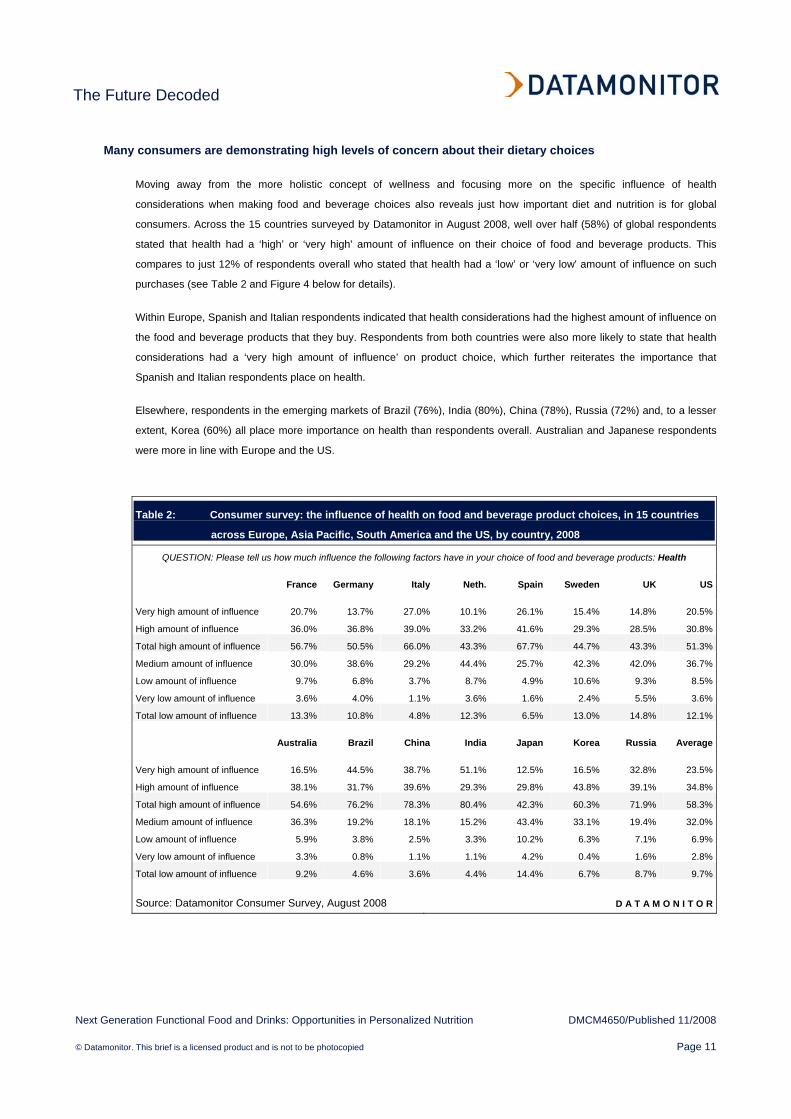

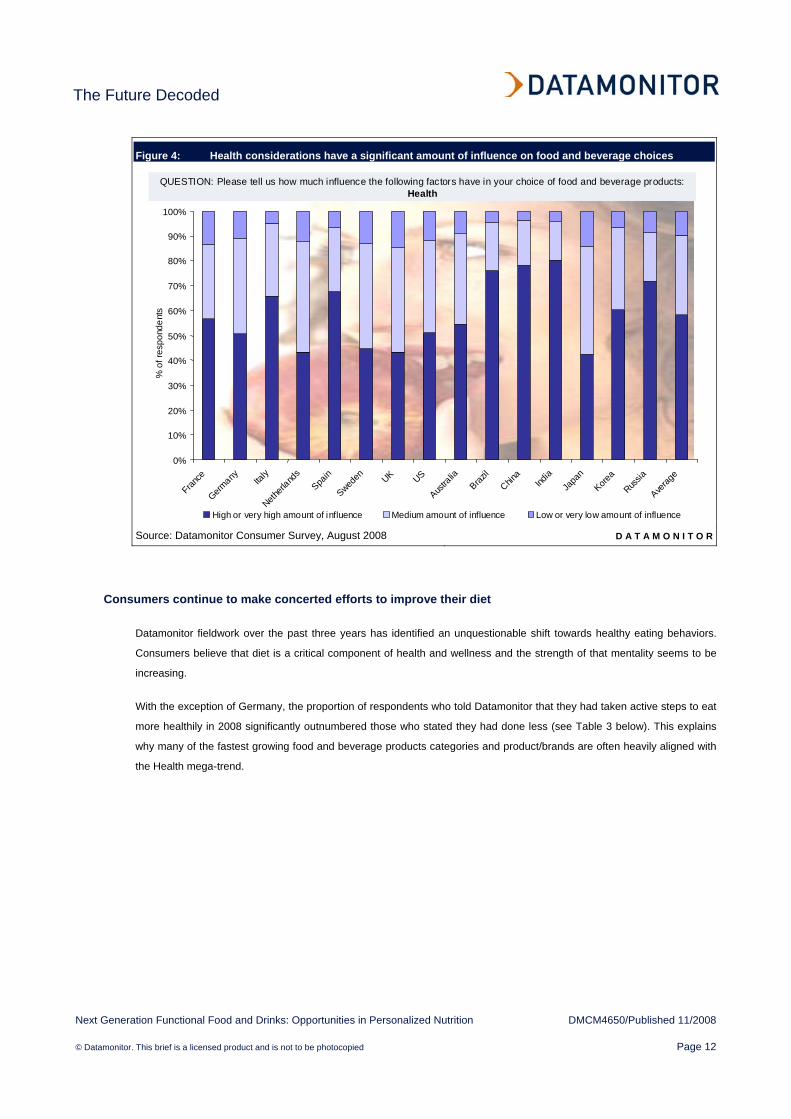

Many consumers are demonstrating high levels of concern about their dietary choices

Moving away from the more holistic concept of wellness and focusing more on the specific influence of health

considerations when making food and beverage choices also reveals just how important diet and nutrition is for global

consumers. Across the 15 countries surveyed by Datamonitor in August 2008, well over half (58%) of global respondents

stated that health had a ‘high’ or ‘very high' amount of influence on their choice of food and beverage products. This

compares to just 12% of respondents overall who stated that health had a ‘low’ or ‘very low' amount of influence on such

purchases (see Table 2 and Figure 4 below for details).

Within Europe, Spanish and Italian respondents indicated that health considerations had the highest amount of influence on

the food and beverage products that they buy. Respondents from both countries were also more likely to state that health

considerations had a ‘very high amount of influence’ on product choice, which further reiterates the importance that

Spanish and Italian respondents place on health.

Elsewhere, respondents in the emerging markets of Brazil (76%), India (80%), China (78%), Russia (72%) and, to a lesser

extent, Korea (60%) all place more importance on health than respondents overall. Australian and Japanese respondents

were more in line with Europe and the US.

Table 2: Consumer survey: the influence of health on food and beverage product choices, in 15 countries

across Europe, Asia Pacific, South America and the US, by country, 2008

QUESTION: Please tell us how much influence the following factors have in your choice of food and beverage products: Health

France Germany Italy Neth. Spain Sweden UK US

Very high amount of influence 20.7% 13.7% 27.0% 10.1% 26.1% 15.4% 14.8% 20.5%

High amount of influence 36.0% 36.8% 39.0% 33.2% 41.6% 29.3% 28.5% 30.8%

Total high amount of influence 56.7% 50.5% 66.0% 43.3% 67.7% 44.7% 43.3% 51.3%

Medium amount of influence 30.0% 38.6% 29.2% 44.4% 25.7% 42.3% 42.0% 36.7%

Low amount of influence 9.7% 6.8% 3.7% 8.7% 4.9% 10.6% 9.3% 8.5%

Very low amount of influence 3.6% 4.0% 1.1% 3.6% 1.6% 2.4% 5.5% 3.6%

Total low amount of influence 13.3% 10.8% 4.8% 12.3% 6.5% 13.0% 14.8% 12.1%

Australia Brazil China India Japan Korea Russia Average

Very high amount of influence 16.5% 44.5% 38.7% 51.1% 12.5% 16.5% 32.8% 23.5%

High amount of influence 38.1% 31.7% 39.6% 29.3% 29.8% 43.8% 39.1% 34.8%

Total high amount of influence 54.6% 76.2% 78.3% 80.4% 42.3% 60.3% 71.9% 58.3%

Medium amount of influence 36.3% 19.2% 18.1% 15.2% 43.4% 33.1% 19.4% 32.0%

Low amount of influence 5.9% 3.8% 2.5% 3.3% 10.2% 6.3% 7.1% 6.9%

Very low amount of influence 3.3% 0.8% 1.1% 1.1% 4.2% 0.4% 1.6% 2.8%

Total low amount of influence 9.2% 4.6% 3.6% 4.4% 14.4% 6.7% 8.7% 9.7%

Source: Datamonitor Consumer Survey, August 2008 D A T A M O N I T O R

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 12

Figure 4: Health considerations have a significant amount of influence on food and beverage choices

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

France

Germany Ita

ly

Netherl

ands

Spain

Sweden UK US

Austra

liaBraz

ilChin

aInd

iaJa

pan

Korea

Russia

Averag

e

High or very high amount of influence Medium amount of influence Low or very low amount of influence

QUESTION: Please tell us how much influence the following factors have in your choice of food and beverage products: Health

% o

f res

pond

ents

Source: Datamonitor Consumer Survey, August 2008 D A T A M O N I T O R

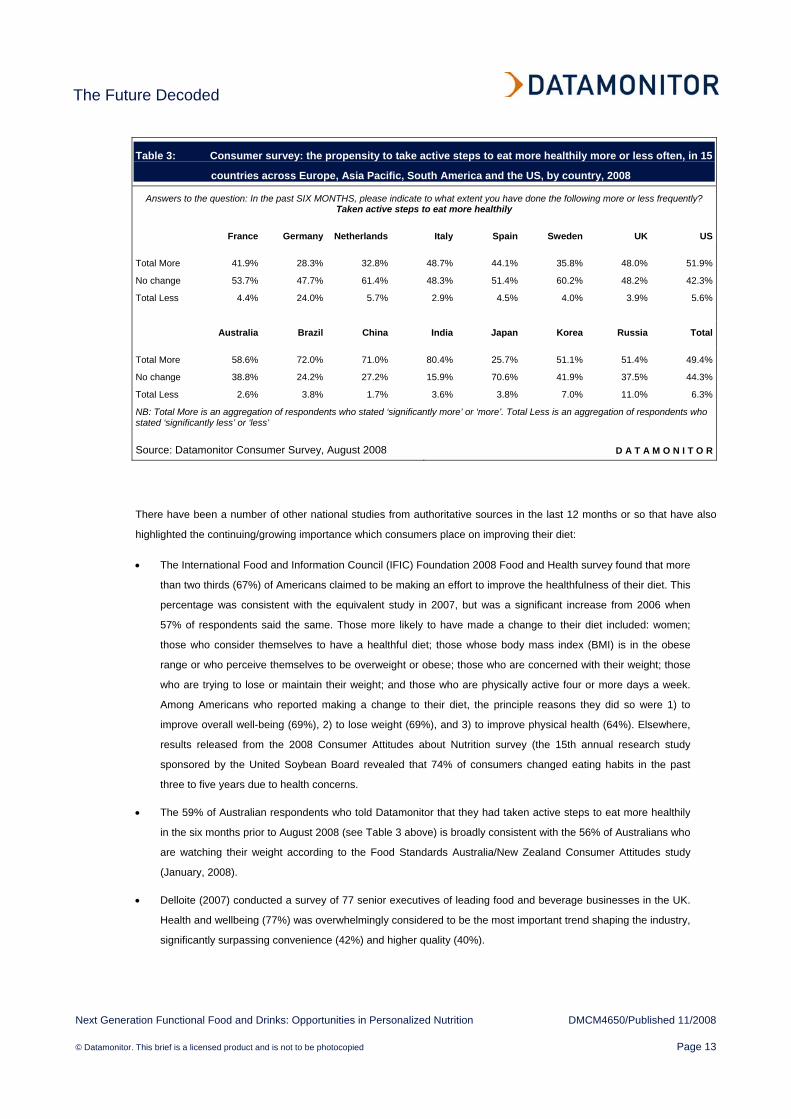

Consumers continue to make concerted efforts to improve their diet

Datamonitor fieldwork over the past three years has identified an unquestionable shift towards healthy eating behaviors.

Consumers believe that diet is a critical component of health and wellness and the strength of that mentality seems to be

increasing.

With the exception of Germany, the proportion of respondents who told Datamonitor that they had taken active steps to eat

more healthily in 2008 significantly outnumbered those who stated they had done less (see Table 3 below). This explains

why many of the fastest growing food and beverage products categories and product/brands are often heavily aligned with

the Health mega-trend.

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 13

Table 3: Consumer survey: the propensity to take active steps to eat more healthily more or less often, in 15

countries across Europe, Asia Pacific, South America and the US, by country, 2008

Answers to the question: In the past SIX MONTHS, please indicate to what extent you have done the following more or less frequently? Taken active steps to eat more healthily

France Germany Netherlands Italy Spain Sweden UK US

Total More 41.9% 28.3% 32.8% 48.7% 44.1% 35.8% 48.0% 51.9%

No change 53.7% 47.7% 61.4% 48.3% 51.4% 60.2% 48.2% 42.3%

Total Less 4.4% 24.0% 5.7% 2.9% 4.5% 4.0% 3.9% 5.6%

Australia Brazil China India Japan Korea Russia Total

Total More 58.6% 72.0% 71.0% 80.4% 25.7% 51.1% 51.4% 49.4%

No change 38.8% 24.2% 27.2% 15.9% 70.6% 41.9% 37.5% 44.3%

Total Less 2.6% 3.8% 1.7% 3.6% 3.8% 7.0% 11.0% 6.3%

NB: Total More is an aggregation of respondents who stated ‘significantly more’ or ‘more’. Total Less is an aggregation of respondents who stated ‘significantly less’ or ‘less’

Source: Datamonitor Consumer Survey, August 2008 D A T A M O N I T O R

There have been a number of other national studies from authoritative sources in the last 12 months or so that have also

highlighted the continuing/growing importance which consumers place on improving their diet:

• The International Food and Information Council (IFIC) Foundation 2008 Food and Health survey found that more

than two thirds (67%) of Americans claimed to be making an effort to improve the healthfulness of their diet. This

percentage was consistent with the equivalent study in 2007, but was a significant increase from 2006 when

57% of respondents said the same. Those more likely to have made a change to their diet included: women;

those who consider themselves to have a healthful diet; those whose body mass index (BMI) is in the obese

range or who perceive themselves to be overweight or obese; those who are concerned with their weight; those

who are trying to lose or maintain their weight; and those who are physically active four or more days a week.

Among Americans who reported making a change to their diet, the principle reasons they did so were 1) to

improve overall well-being (69%), 2) to lose weight (69%), and 3) to improve physical health (64%). Elsewhere,

results released from the 2008 Consumer Attitudes about Nutrition survey (the 15th annual research study

sponsored by the United Soybean Board revealed that 74% of consumers changed eating habits in the past

three to five years due to health concerns.

• The 59% of Australian respondents who told Datamonitor that they had taken active steps to eat more healthily

in the six months prior to August 2008 (see Table 3 above) is broadly consistent with the 56% of Australians who

are watching their weight according to the Food Standards Australia/New Zealand Consumer Attitudes study

(January, 2008).

• Delloite (2007) conducted a survey of 77 senior executives of leading food and beverage businesses in the UK.

Health and wellbeing (77%) was overwhelmingly considered to be the most important trend shaping the industry,

significantly surpassing convenience (42%) and higher quality (40%).

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 14

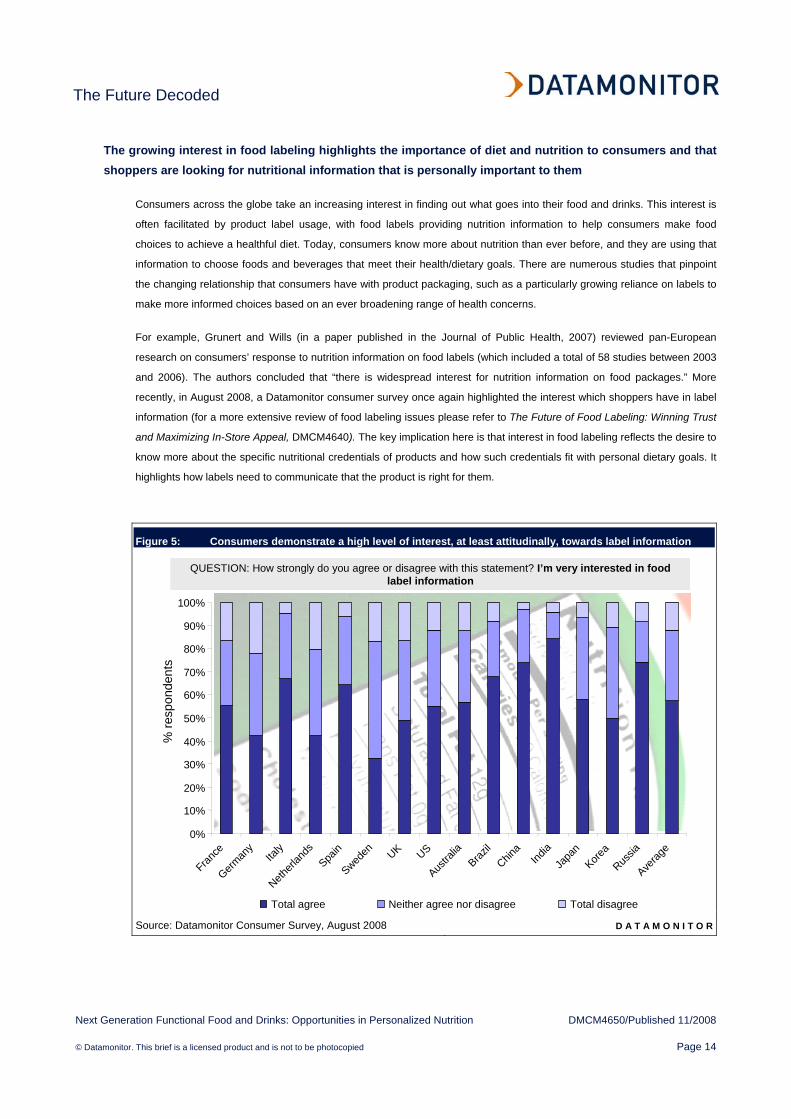

The growing interest in food labeling highlights the importance of diet and nutrition to consumers and that shoppers are looking for nutritional information that is personally important to them

Consumers across the globe take an increasing interest in finding out what goes into their food and drinks. This interest is

often facilitated by product label usage, with food labels providing nutrition information to help consumers make food

choices to achieve a healthful diet. Today, consumers know more about nutrition than ever before, and they are using that

information to choose foods and beverages that meet their health/dietary goals. There are numerous studies that pinpoint

the changing relationship that consumers have with product packaging, such as a particularly growing reliance on labels to

make more informed choices based on an ever broadening range of health concerns.

For example, Grunert and Wills (in a paper published in the Journal of Public Health, 2007) reviewed pan-European

research on consumers’ response to nutrition information on food labels (which included a total of 58 studies between 2003

and 2006). The authors concluded that “there is widespread interest for nutrition information on food packages.” More

recently, in August 2008, a Datamonitor consumer survey once again highlighted the interest which shoppers have in label

information (for a more extensive review of food labeling issues please refer to The Future of Food Labeling: Winning Trust

and Maximizing In-Store Appeal, DMCM4640). The key implication here is that interest in food labeling reflects the desire to

know more about the specific nutritional credentials of products and how such credentials fit with personal dietary goals. It

highlights how labels need to communicate that the product is right for them.

Figure 5: Consumers demonstrate a high level of interest, at least attitudinally, towards label information

QUESTION: How strongly do you agree or disagree with this statement? I’m very interested in food label information

% re

spon

dent

s

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

France

German

yIta

ly

Netherl

ands

Spain

Sweden UK US

Austra

liaBraz

il

China

India

Japa

nKore

a

Russia

Averag

e

Total agree Neither agree nor disagree Total disagree

Source: Datamonitor Consumer Survey, August 2008 D A T A M O N I T O R

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 15

Figure 6: Intensifying health concerns lead to more considered choices governed by a heightened reliance

on food labels which in turn is likely to fuel the demand for more personalized choices

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Austra

liaChin

aInd

iaJa

pan

South

Korea

France

Germany Ita

ly

Netherl

ands

Russia

Spain

Sweden UK US

Brazil

Overal

l

More often Significantly more often

% o

f res

pond

ents

QUESTION: In the past SIX MONTHS, I have used nutritional information on product packaging to help make food and drinks choices…

Source: Datamonitor Consumer Survey, August 2008 D A T A M O N I T O R

Key takeouts and implications: as general health concerns engulf the mass population, dietary concerns will evolve to become more specific

• Health continues to have a growing impact on consumer lifestyles and dietary choices. As the trend

evolves it is natural that concerns and behavior become more sophisticated. This is why new dietary

and nutritional trends are emerging, such as personalized nutrition (and related sub-trends which are

discussed in the next section).

• Food and drink in particular is becoming a more important way of living more healthily. This creates

significant opportunities for functional food and beverage manufacturers as consumers are now

demonstrating a real desire and willingness to understand how they can eat more nutritiously or

compensate for the lifestyle habits that contribute to poor dietary habits. Accordingly, companies are

looking increasingly to market food and drinks on a health platform, and the trend is expected to

continue to develop in the foreseeable future. Enhanced nutritional benefits are emerging as the main

means of differentiating food and beverage brands. Health is a major NPD battleground.

• The growing reliance on food labeling information is symptomatic of both general and specific health

concerns. Regarding the latter, consumers are increasingly relying on label information to make

informed decisions about the nutritional profile of food and beverage products that matter most to them.

This represents a potentially important development for industry players looking to offer more

personalized nutritional solutions. This is because shoppers are more likely to take the time out to really

understand the benefits associated with such product variants.

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 16

• Given the growth of aging populations, escalating levels of obesity and associated lifestyle illnesses,

the personalization trend offers manufacturers a significant growth opportunity to market targeted food

and drinks products to a wide range of consumers. In recognition of this, it is likely that manufacturers

will begin to meet the growing demand for personalized food and drinks products which offer more

targeted health benefits.

TREND: Personalized nutrition overlaps with a number of other food and beverage trends and themes but is now evolving with complex nutritional science focusing on genetics

The following analysis explores the nutritional and science based developments associated with personalized nutrition. It

highlights that food and nutrition science has moved from identifying and correcting nutritional deficiencies to the

development of products that promote optimal health for the individual and reduce the risk of disease. The understanding of

human dietary requirements is aided by developments in many scientific disciplines, including food science, nutrition,

chemistry, biochemistry, physiology, and genetics. In particular, new research in proteomics, nutrigenomics, metabolomics,

and other disciplines look set to further identify the biological basis by which food components promote health and

wellness.

Personalized nutrition is a relatively broad concept and it is not focused solely on health and nutrition

Figure 7 below highlights that personalized nutrition encompasses four specific sub-trends and associated product benefits:

• lifestyle supporting/expressive food and beverage products;

• occasion, demographic and dietary specificity;

• functional food and drinks;

• nutrigenomics.

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 17

Figure 7: Personalized nutrition encompasses four specific sub-trends and associated product benefits

Degree of personalization and manufacturer investment

Targ

ets

spec

ific

nutr

ition

al n

eeds

/ sci

ence

bas

ed in

nova

tion

LIFESTYLE/ EXPRESSIVE PRODUCTS

FUNCTIONAL FOOD & DRINKS

NUTRIGENOMICS

• Consumers are now seeking to optimize their performance and reduce the risk, or delay the onset of diseases with functional food and drink products

• Includes: bone health, digestive health, heart health, cognitive health, physical health and emotional health

• Progressive nutritional science suggests diets can be customized according to genetic make-up.

• This science is expected to fuel the growth of the nutritional supplement and functional food industries

OCCASION & DEMOGRAPHIC SPECIFICITY• Targeted food and beverage solutions catering to

specific occasion, age group and gender needs is an ongoing theme of innovation in FMCGs

• Self-definition is partly reliant on consumption and the symbolic meaning of brands

• Consumers prefer products and brands with symbolic meanings consistent with their self-concept

• Self indulgence is also loosely aligned with a personal approach to eating

Source: Datamonitor analysis D A T A M O N I T O R

Growing consumption of functional food and drinks reflects the demand for more personalized, targeted dietary solutions

Consumers have moved beyond consuming food simply to maintain everyday health. They are now seeking to optimize

their performance and reduce the risk, or delay the onset of diseases with functional food and drink products. Globally,

there is an ever increasing amount of scientific evidence on the positive contribution that a balanced diet, rich in nutrients—

particularly micronutrients and bioactive compounds—can have on a consumer's overall wellbeing. Widespread interest in

select foods that promote health has resulted in the use of the term 'functional foods'.

The definition of functional food and beverages is a contentious issue, especially as regulatory agencies do not recognize

'functional food' as a nutritional entity. Even in Japan, where functional foods originated, the term was not adopted as it was

deemed that all foods are functional in that they provide the energy and nutrients necessary for survival. A lack of

legislation means that there are several different definitions of functional foods, and this lack of consistency explains why

market valuations on the size of the industry can vary dramatically between sources.

Datamonitor defines functional foods and drinks as “everyday packaged food and beverage products that contain specific

physiologically active components that provide health and wellbeing benefits beyond basic nutritional functions (the term

‘nutraceuticals’ is interchangeable with the term ‘functional food and drinks’).” Functional products contribute a higher

nutritional value than standard products in that they deliver targeted health benefits. For example, products that provide a

natural bioactive substance may be enhanced to increase the level present in the food (e.g. eggs with increased levels of

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 18

omega-3 fatty acids or tomatoes with enhanced lycopene levels). Products can also be fortified to provide consumers with

a broader selection of food types that contain components with a particular health benefit (e.g. calcium-fortified orange

juice). Functional products can be further defined by the type of benefits provided (e.g. gut and heart health).

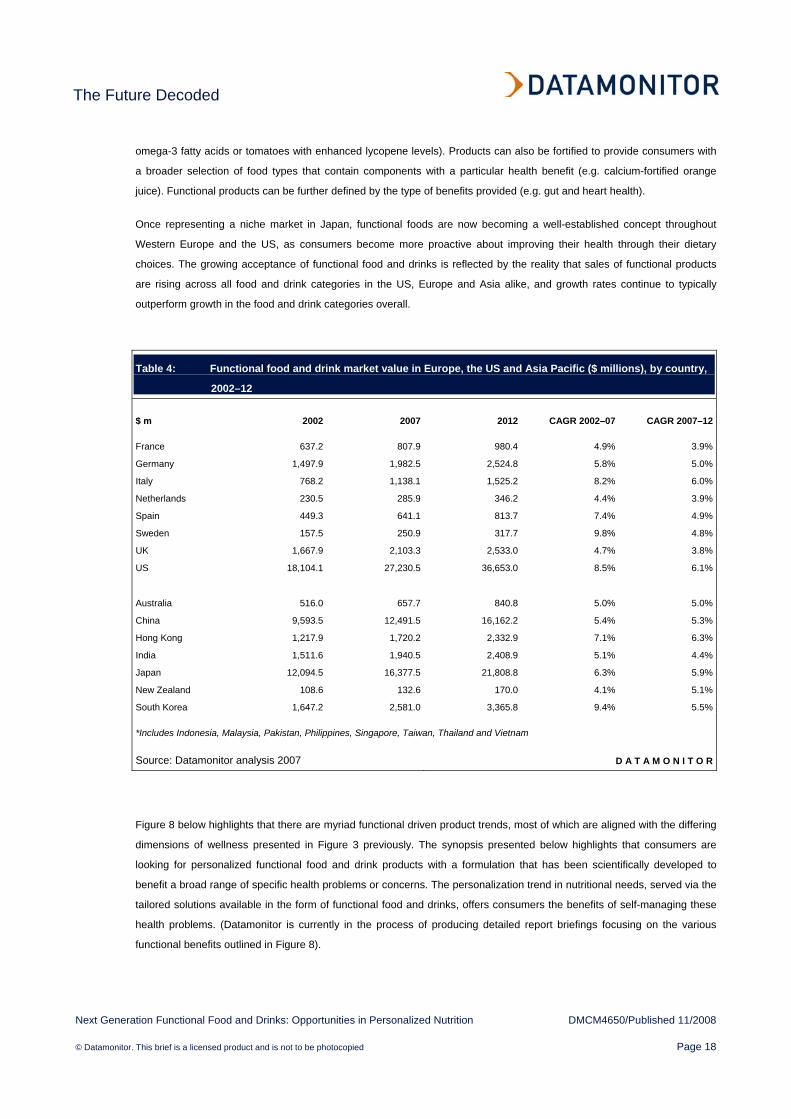

Once representing a niche market in Japan, functional foods are now becoming a well-established concept throughout

Western Europe and the US, as consumers become more proactive about improving their health through their dietary

choices. The growing acceptance of functional food and drinks is reflected by the reality that sales of functional products

are rising across all food and drink categories in the US, Europe and Asia alike, and growth rates continue to typically

outperform growth in the food and drink categories overall.

Table 4: Functional food and drink market value in Europe, the US and Asia Pacific ($ millions), by country,

2002–12

$ m 2002 2007 2012 CAGR 2002–07 CAGR 2007–12

France 637.2 807.9 980.4 4.9% 3.9%

Germany 1,497.9 1,982.5 2,524.8 5.8% 5.0%

Italy 768.2 1,138.1 1,525.2 8.2% 6.0%

Netherlands 230.5 285.9 346.2 4.4% 3.9%

Spain 449.3 641.1 813.7 7.4% 4.9%

Sweden 157.5 250.9 317.7 9.8% 4.8%

UK 1,667.9 2,103.3 2,533.0 4.7% 3.8%

US 18,104.1 27,230.5 36,653.0 8.5% 6.1%

Australia 516.0 657.7 840.8 5.0% 5.0%

China 9,593.5 12,491.5 16,162.2 5.4% 5.3%

Hong Kong 1,217.9 1,720.2 2,332.9 7.1% 6.3%

India 1,511.6 1,940.5 2,408.9 5.1% 4.4%

Japan 12,094.5 16,377.5 21,808.8 6.3% 5.9%

New Zealand 108.6 132.6 170.0 4.1% 5.1%

South Korea 1,647.2 2,581.0 3,365.8 9.4% 5.5%

*Includes Indonesia, Malaysia, Pakistan, Philippines, Singapore, Taiwan, Thailand and Vietnam

Source: Datamonitor analysis 2007 D A T A M O N I T O R

Figure 8 below highlights that there are myriad functional driven product trends, most of which are aligned with the differing

dimensions of wellness presented in Figure 3 previously. The synopsis presented below highlights that consumers are

looking for personalized functional food and drink products with a formulation that has been scientifically developed to

benefit a broad range of specific health problems or concerns. The personalization trend in nutritional needs, served via the

tailored solutions available in the form of functional food and drinks, offers consumers the benefits of self-managing these

health problems. (Datamonitor is currently in the process of producing detailed report briefings focusing on the various

functional benefits outlined in Figure 8).

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 19

Figure 8: Functional food and drinks are formulated to offer specific health and wellness benefits to targeted

consumers and consumer needs, and are therefore central to personalized nutrition ‘S

oft h

ealth

’‘H

ard

heal

th’

DIGESTIVE HEALTH

HEART HEALTH

PHYSICAL HEALTH

BEAUTY/ APPEARANCE DRIVEN HEALTH

EMOTIONAL/RELAXATIONALHEALTH

BONE & JOINT HEALTH• SYNOPSIS: refers to developmental bone health in childhood as well as

long term health problems such as osteoporosis and arthritis• KEY PRODUCT TRENDS: calcium richness; vitamin D fortification

• SYNOPSIS: consumers are increasingly aware that digestive health can have a direct effect on general feelings of wellness, including skin health, immunity levels and energy levels

• KEY PRODUCT TRENDS: probiotics and prebiotics, high fiber/whole foods

‘PER

SON

ALI

ZED

NU

TRIT

ION’

AS R

EFLE

CTE

D B

Y FU

NC

TIO

NAL

FO

OD

TR

END

S

• SYNOPSIS: consumers are increasingly educated about heart health issues, including blood cholesterol levels, blood pressure, heart strength, and circulation and the ways in which dietary patterns affect heart health

• KEY PRODUCT TRENDS: high fiber/whole foods; cholesterol reducers; blood pressure reducers e.g. plant sterols and soy proteins

IMMUNITY HEALTH

• SYNOPSIS: this has a strong crossover with digestive health since digestive health, and the products promoting it, is heavily linked with defence

• KEY PRODUCT TRENDS: probiotics and prebiotics; antioxidant rich; vitamin & mineral fortification

• SYNOPSIS: psychological research has shown that self-esteem, popularity and happiness is more heavily tied with appearance than anything else. So, ‘feeling good’ in a physical health sense is strongly related to ‘looking good’

• KEY PRODUCT TRENDS: ‘nutricosmetics’ in the form of beauty food and beverages and oral beauty supplements

• SYNOPSIS: involves feeling physically good, especially in terms of energy/vitality. Can involve an artificial energy boost or more sustained natural energy boost. The trend/need state has links with natural foods, de-tox diets and cleansing the mind and the body

• KEY PRODUCT TRENDS: all forms of energy and vitality boosting products

• SYNOPSIS: researchers and consumers alike are beginning to understand the powerful links between nutrition, mood and mental health. These products are aimed at helping people with hectic, stressful lifestyles

• KEY PRODUCT TRENDS: mood foods – products formulated with relaxation ingredients such as GABA and botanical extracts and flavorings

COGNITIVE HEALTH

• SYNOPSIS: food and drink products can improve brain function, memory and alertness. These "cognitive boosters" or "smart foods" are edibles fortified with amino acids, vitamins and proteins that stimulate brain function

• KEY PRODUCT TRENDS: Omega-3 fortification

Source: Datamonitor analysis D A T A M O N I T O R

Usage occasion and demographic specificity, and catering to specific dietary requirements, are also important platforms for personalized nutrition

As Figure 7 previously highlighted, personalized nutrition also involves tailoring product formulations according to the

specific nutritional and sensory preferences of consumer groups and consumer occasions. The following analysis explores

this is in more detail:

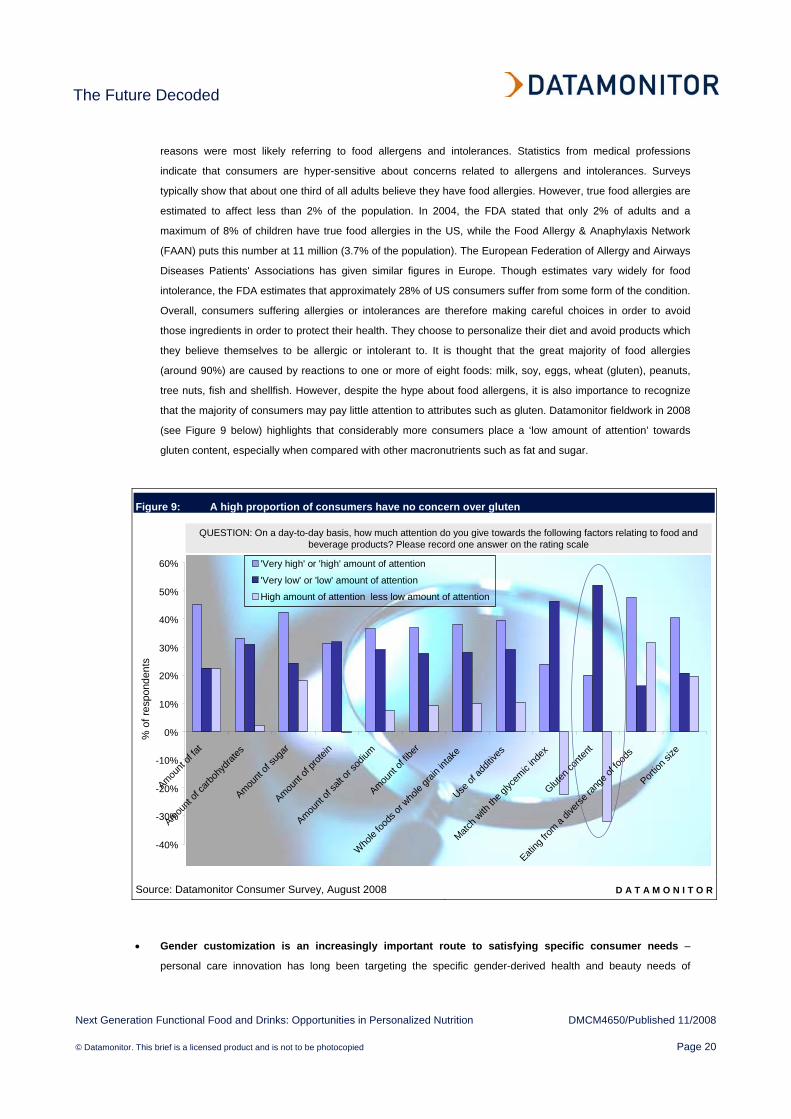

• A number of consumers have specific dietary requirements, even if some are hyper-sensitive about this

– the UK’s Food Standards Agency Consumer Attitudes report (FSA, 2008) asked whether respondents had any

specific dietary requirements using a prompted list. A substantial proportion of the UK sample (40%, taking all

the categories together) claimed they avoided certain foods for some reason. The largest single group did so for

medical reasons (15%), followed by those on a diet to lose weight (13%). The respondents citing medical

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 20

reasons were most likely referring to food allergens and intolerances. Statistics from medical professions

indicate that consumers are hyper-sensitive about concerns related to allergens and intolerances. Surveys

typically show that about one third of all adults believe they have food allergies. However, true food allergies are

estimated to affect less than 2% of the population. In 2004, the FDA stated that only 2% of adults and a

maximum of 8% of children have true food allergies in the US, while the Food Allergy & Anaphylaxis Network

(FAAN) puts this number at 11 million (3.7% of the population). The European Federation of Allergy and Airways

Diseases Patients' Associations has given similar figures in Europe. Though estimates vary widely for food

intolerance, the FDA estimates that approximately 28% of US consumers suffer from some form of the condition.

Overall, consumers suffering allergies or intolerances are therefore making careful choices in order to avoid

those ingredients in order to protect their health. They choose to personalize their diet and avoid products which

they believe themselves to be allergic or intolerant to. It is thought that the great majority of food allergies

(around 90%) are caused by reactions to one or more of eight foods: milk, soy, eggs, wheat (gluten), peanuts,

tree nuts, fish and shellfish. However, despite the hype about food allergens, it is also importance to recognize

that the majority of consumers may pay little attention to attributes such as gluten. Datamonitor fieldwork in 2008

(see Figure 9 below) highlights that considerably more consumers place a ‘low amount of attention’ towards

gluten content, especially when compared with other macronutrients such as fat and sugar.

Figure 9: A high proportion of consumers have no concern over gluten

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Amount

of fat

Amount

of ca

rbohy

drates

Amount

of su

gar

Amount

of pro

tein

Amount

of sa

lt or s

odium

Amount

of fib

er

Who

le foo

ds or

who

le gra

in int

ake

Use of

addit

ives

Match w

ith th

e glyc

emic

index

Gluten

conte

nt

Eating

from a

divers

e ran

ge of

food

s

Portion

size

'Very high' or 'high' amount of attention

'Very low' or 'low' amount of attention

High amount of attention less low amount of attention

% o

f res

pond

ents

QUESTION: On a day-to-day basis, how much attention do you give towards the following factors relating to food and beverage products? Please record one answer on the rating scale

Source: Datamonitor Consumer Survey, August 2008 D A T A M O N I T O R

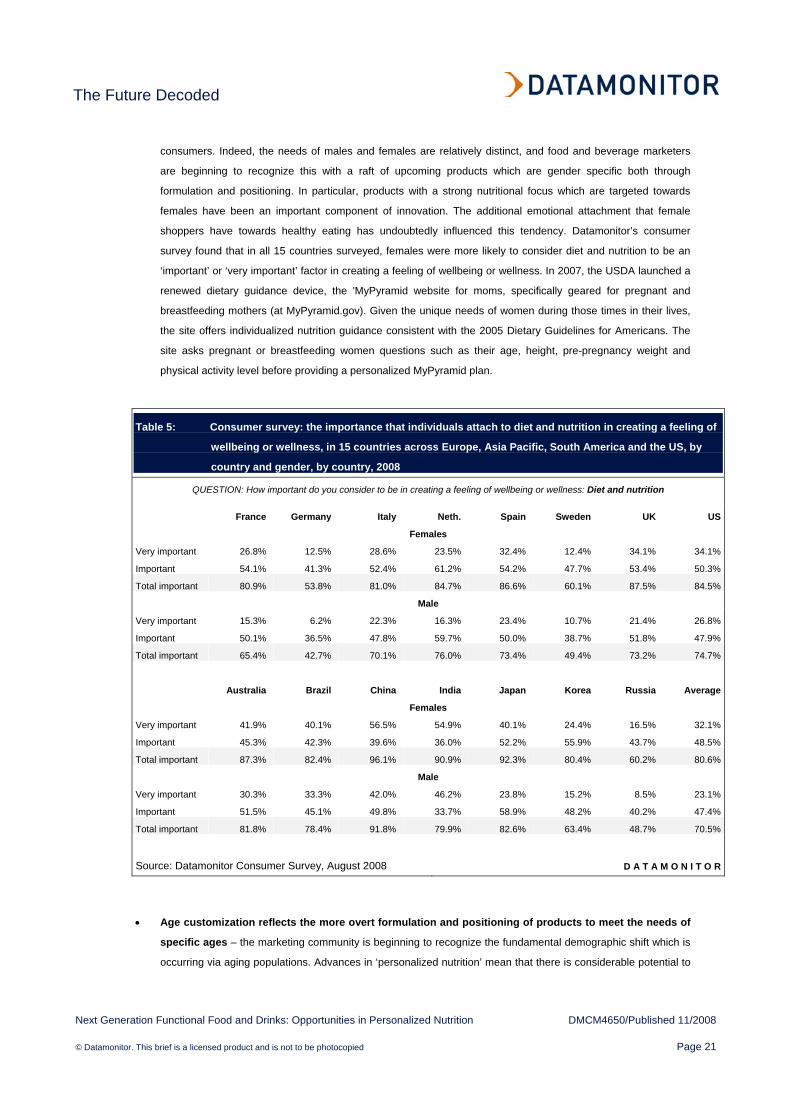

• Gender customization is an increasingly important route to satisfying specific consumer needs –

personal care innovation has long been targeting the specific gender-derived health and beauty needs of

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 21

consumers. Indeed, the needs of males and females are relatively distinct, and food and beverage marketers

are beginning to recognize this with a raft of upcoming products which are gender specific both through

formulation and positioning. In particular, products with a strong nutritional focus which are targeted towards

females have been an important component of innovation. The additional emotional attachment that female

shoppers have towards healthy eating has undoubtedly influenced this tendency. Datamonitor’s consumer

survey found that in all 15 countries surveyed, females were more likely to consider diet and nutrition to be an

‘important’ or ‘very important’ factor in creating a feeling of wellbeing or wellness. In 2007, the USDA launched a

renewed dietary guidance device, the 'MyPyramid website for moms, specifically geared for pregnant and

breastfeeding mothers (at MyPyramid.gov). Given the unique needs of women during those times in their lives,

the site offers individualized nutrition guidance consistent with the 2005 Dietary Guidelines for Americans. The

site asks pregnant or breastfeeding women questions such as their age, height, pre-pregnancy weight and

physical activity level before providing a personalized MyPyramid plan.

Table 5: Consumer survey: the importance that individuals attach to diet and nutrition in creating a feeling of

wellbeing or wellness, in 15 countries across Europe, Asia Pacific, South America and the US, by

country and gender, by country, 2008

QUESTION: How important do you consider to be in creating a feeling of wellbeing or wellness: Diet and nutrition

France Germany Italy Neth. Spain Sweden UK US

Females

Very important 26.8% 12.5% 28.6% 23.5% 32.4% 12.4% 34.1% 34.1%

Important 54.1% 41.3% 52.4% 61.2% 54.2% 47.7% 53.4% 50.3%

Total important 80.9% 53.8% 81.0% 84.7% 86.6% 60.1% 87.5% 84.5%

Male

Very important 15.3% 6.2% 22.3% 16.3% 23.4% 10.7% 21.4% 26.8%

Important 50.1% 36.5% 47.8% 59.7% 50.0% 38.7% 51.8% 47.9%

Total important 65.4% 42.7% 70.1% 76.0% 73.4% 49.4% 73.2% 74.7%

Australia Brazil China India Japan Korea Russia Average

Females

Very important 41.9% 40.1% 56.5% 54.9% 40.1% 24.4% 16.5% 32.1%

Important 45.3% 42.3% 39.6% 36.0% 52.2% 55.9% 43.7% 48.5%

Total important 87.3% 82.4% 96.1% 90.9% 92.3% 80.4% 60.2% 80.6%

Male

Very important 30.3% 33.3% 42.0% 46.2% 23.8% 15.2% 8.5% 23.1%

Important 51.5% 45.1% 49.8% 33.7% 58.9% 48.2% 40.2% 47.4%

Total important 81.8% 78.4% 91.8% 79.9% 82.6% 63.4% 48.7% 70.5%

Source: Datamonitor Consumer Survey, August 2008 D A T A M O N I T O R

• Age customization reflects the more overt formulation and positioning of products to meet the needs of

specific ages – the marketing community is beginning to recognize the fundamental demographic shift which is

occurring via aging populations. Advances in ‘personalized nutrition’ mean that there is considerable potential to

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 22

develop more tailored solutions to help consumers overcome age related ailments and nutritional deficiencies. At

the other end of the scale, there is currently a huge focus on children's nutrition, in light of escalating childhood

obesity. As a result, age formulated products are proving to be a prominent feature of new product development

plans, with particular focus on the two extremes of the age spectrum. For instance, as children's nutrition

emerges as a major theme in marketing, manufacturers are actively reformulating products to help parents fight

childhood obesity. Simultaneously, aging populations have been a key target for more personalized solutions,

particularly functional food and drinks.

• Occasion specific products are being used as a way of helping consumers to maximize enjoyment while

creating a ‘just for the moment’ positioning – there are a number of interesting concepts that reinforce the

idea that a product is to be consumed during a specific occasion. While this is not an entirely new marketing

approach, it is evident that manufacturers and retailers have been embracing this approach across a broader

range of categories. Datamonitor’s report, On-Trend’ Innovation & Marketing Concepts: The Individualism Mega-

Trend(DMCM4627) highlighted that product categories which are less associated with food or beverages are

now seeking to cross-merchandize by reinforcing the association, and this is being done with ever increasing

detail and sophistication. In addition, food and beverage marketers are targeting more niche and specific

occasions: Awake Good Morning Energy Drink in the US, for example, is touted as "the only energy juice

specially formulated for morning consumption.” Niche vending concepts are likely to emerge to satisfy unmet

needs for foods hard to come by when away from home. In the US, Kosher Vending Industries (KVI) introduced

Hot Nosh 24/6, “the first certified kosher on-demand hot food available through vending machines.” The concept

was spawned when its co-founders identified the challenges that kosher travelers face when visiting locations

that have no available kosher hot food.

Consumers are empowered by additional choice and the new possibilities to adjust and adapt the taste/flavor benefits

Empowerment is an important word associated with individualistic behaviors. Consumers want more control, both in the

way that they use brands (which can be referred to as ‘adaptive customization’) and in how brands are created in the first

place. In particular, personalization in tastes and flavors, whereby a consumer can adapt flavors to their own personal

tastes, is an emerging trend.

• Programmable and adjustable packaging now allows food, beverage and even tobacco consumers to

customize efficacy and taste benefits – food and beverage manufacturers are offering more impressive

personalized benefits through packaging that offer a form of taste/flavor customization. For example, Ipifini's

Programmable Liquid Container technology employs buttons on the container's surface that release additives

(flavors, colors, fragrances) into the liquid. Additive buttons allow for the consumer to choose variations of the

liquid in the container at the point of consumption. For example, a programmable cola bottle with buttons for

lemon, lime, vanilla, and cherry flavors, as well as a caffeine button, allows for thirty-two potential choices of

soda. Similarly, IntelligentWater products are offered in a plastic 'genie' bottle, with a patented ‘TwistRelease’

cap, which dispenses the concentrated vitamin mixture into the pure spring water. Interestingly, the varieties are

also user specific, including Mother&Baby (with folic acid for expectant mothers), Mature&Wise (for individuals

over 50), Body&Beauty (for physically active people) and Spirit&Mind (for mental concentration). Elsewhere,

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 23

Tetley's Twistea Tea offers taste customization benefits via the innovative packaging format. It features a Tetley

teabag locked into a plastic cup to which the consumer simply adds boiling water, twisting the lid to achieve the

required strength of flavor. The teabag remains inside the unit and does not need to be disposed of separately.

• ‘Taste customized vending’ is an emerging concept in offering convenient, yet personalized food and

beverages – a UK company has developed a system that allows soft drinks to be packed in situ within vending

machines. Branded plastic pouches, from 250ml to 500ml, are stored on a roll in the Pouchlink system, created

by Waterwerkz, before being separated and filled using just-in-time flash chilling technology at the point of sale.

Machines can hold up to 2,000 interlinked resealable, spouted pouches of varying sizes, which are then filled on

demand using filtered main water and flavored syrups. WaterWerkz is launching its own brand of juice-based

drinks, under the brand name Froobee, which it has designed to meet the new health standards of UK schools.

Overall, Datamonitor believes there is a big opportunity in the vending market as people look for healthy, on-the-

go refreshments in convenient formats. Offering customers the novelty of creating their own distinct mixes is a

possible reflection of the future of vending.

Nutrigenomics facilitates dietary customization according to an individual’s genetic make-up

Until relatively recently, nutrition studies often assumed that all individuals have average dietary requirements. However,

nutritional science advancements have led to researchers recognizing how different mindsets, genes and genetics all play

a role in the types of food that are most effective for different people in the areas of weight management, nutrition and

general health. In particular, nutrigenomics explores how genetic variation and ‘epigenetic events’ alter individual

requirements for, and responses to, nutrients. There are two aspects to this:

• how dietary patterns affects the genome;

• how genetics determine individual nutritional requirements to prevent diseases.

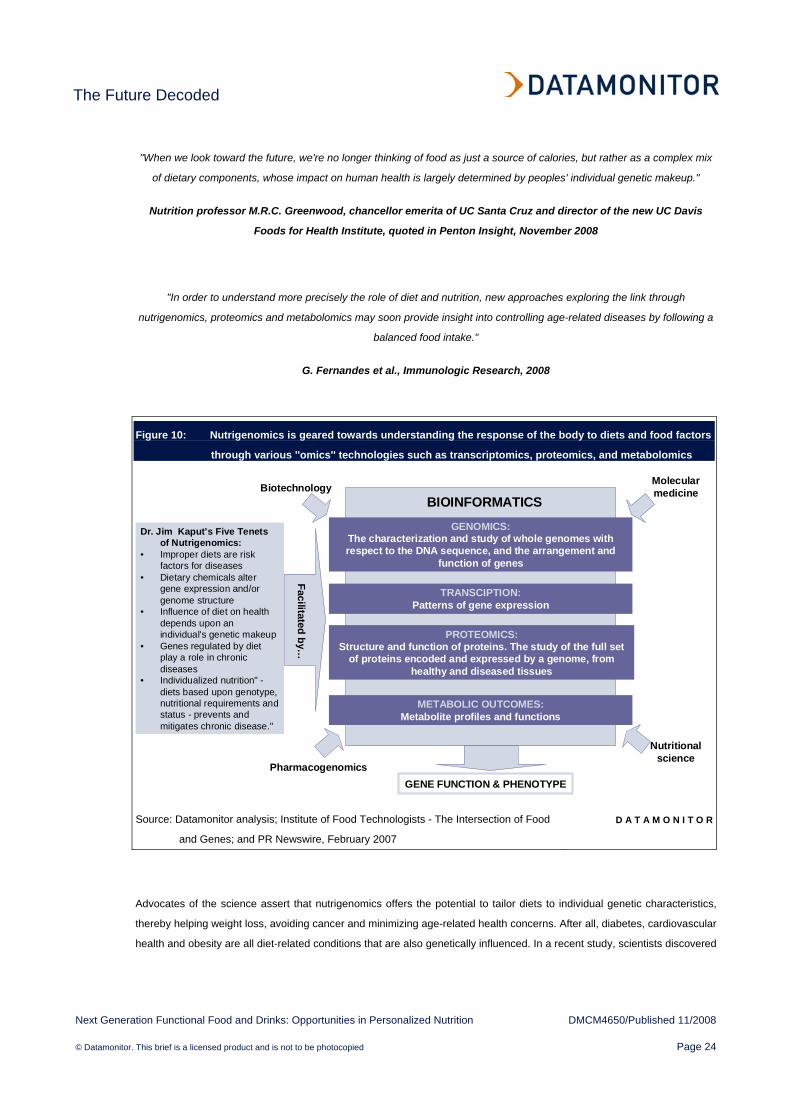

The US-based Institute of Food Technologists defines nutrigenomics as the “the interaction of dietary components that are

nutritive (vitamins, minerals, fatty acids), bioactive (phytochemicals), or metabolites of food components (retinoic acid,

eicosanoids) with genes to result in gene expression.” Essentially, nutrigenomics is geared towards understanding the

response of the body to diets and food factors through various ''omics'' technologies such as transcriptomics, proteomics,

and metabolomics (see Figure 10 below for synopsis). This knowledge has led to a growing interest in the commercial

opportunity for innovative nutritional products that influence gene expression:

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 24

"When we look toward the future, we're no longer thinking of food as just a source of calories, but rather as a complex mix

of dietary components, whose impact on human health is largely determined by peoples' individual genetic makeup."

Nutrition professor M.R.C. Greenwood, chancellor emerita of UC Santa Cruz and director of the new UC Davis

Foods for Health Institute, quoted in Penton Insight, November 2008

"In order to understand more precisely the role of diet and nutrition, new approaches exploring the link through

nutrigenomics, proteomics and metabolomics may soon provide insight into controlling age-related diseases by following a

balanced food intake."

G. Fernandes et al., Immunologic Research, 2008

Figure 10: Nutrigenomics is geared towards understanding the response of the body to diets and food factors

through various ''omics'' technologies such as transcriptomics, proteomics, and metabolomics

GENOMICS:The characterization and study of whole genomes with respect to the DNA sequence, and the arrangement and

function of genes

TRANSCIPTION:Patterns of gene expression

PROTEOMICS:Structure and function of proteins. The study of the full set

of proteins encoded and expressed by a genome, from healthy and diseased tissues

METABOLIC OUTCOMES:Metabolite profiles and functions

Molecular medicine

Nutritional science

BIOINFORMATICSBiotechnology

PharmacogenomicsGENE FUNCTION & PHENOTYPE

Dr. Jim Kaput’s Five Tenets of Nutrigenomics:

• Improper diets are risk factors for diseases

• Dietary chemicals alter gene expression and/or genome structure

• Influence of diet on health depends upon an individual's genetic makeup

• Genes regulated by diet play a role in chronic diseases

• Individualized nutrition" -diets based upon genotype, nutritional requirements and status - prevents and mitigates chronic disease."

Facilitated by…

Source: Datamonitor analysis; Institute of Food Technologists - The Intersection of Food

and Genes; and PR Newswire, February 2007

D A T A M O N I T O R

Advocates of the science assert that nutrigenomics offers the potential to tailor diets to individual genetic characteristics,

thereby helping weight loss, avoiding cancer and minimizing age-related health concerns. After all, diabetes, cardiovascular

health and obesity are all diet-related conditions that are also genetically influenced. In a recent study, scientists discovered

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 25

that 16% of the population has inherited two copies of a variant of a gene called FTO, which makes them 70% more likely

to be obese.

While 99.9% of human genes are the same, genetic variations occur that can impact things like an individual's

predisposition to certain dietary components. Indeed, gene variations may offer the only plausible explanation for why two

people can eat roughly the same amount of food but have vastly different body shapes. This is because interactions

between an individual's genetic make-up and various nutrients can lead to subtle changes in DNA when particular

nutritional factors are increased or decreased in their diet. As the genome is recognized and understood, nutrigenomics

aims to individually prescribe particular levels of nutritional supplements to minimize DNA damage. According to Dr Jim

Kaput of the Centre of Excellence in Nutritional Genomics in California, a pioneer of nutrigenomics, genes play a huge part

in obesity and type 2 diabetes. He asserts that we “have about 30,000 genes in our DNA and maybe about 100 of them will

be mis-expressed because of food consumed. This ‘mis-expression’ forces a bodily response which can lead to weight

gain." (Source: UBIC-CONSULTING)

Overall, it is believed that developments in nutrigenomics and nutrigenetics could change clinical practice in nutrition as

reflected by the Perspectives for Food conference, held by the European Commission's Directorate-General for Research

in Brussels in April 2007:

“There is currently a revolution in genomics. The sequencing of the genome of humans, animals, plants and bacteria is a

huge technological leap forward with enormous potential for human health and disease. Knowledge of the genomes is

helping to uncover unprecedented information about the way our bodies react to food and medicines and this is a huge

scientific challenge for the food industry. Producing foods based on an individual’s genetic make up will be a development

of this in the future… A number of scientists have made alliances with companies that are active in developing personalized

nutrition. Consumers in the future will expect to be able to make choices regarding their food. When they desire to, they will

be able to select foods and diets with functionality and wellbeing aspects consistent with their lifestyle.”

Research Food 2030, Conference Report, European Commission

Other authoritative studies and sources have also highlighted the potential significance of personalized nutrition through

nutrigenomics:

• The Foresight report, entitled "Tackling Obesities: Future Choices," is a two year study conducted in the UK by

about 250 experts and scientists. It examined the causes of obesity and mapped future trends to help the

government develop new health strategies. The report predicted that more than half the population of Great

Britain will be "extremely overweight" by 2050, resulting in an estimated cost of £45 billion for public health

services and lost working hours. The study identified nutrigenomics as a possible means for alleviating this

situation by gaining an understanding of how nutrients and genes interact, and how genetic variations can cause

people to respond differently to food nutrients. However, the study notes there is a shortage of evidence

regarding how successful this approach may be in achieving sustainable weight loss, particularly because there

are more than 600 genes currently associated with obesity.

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 26

• In mid-November 2008, more than 100 nutritionists, food scientists, plant researchers, engineers, and medical

and veterinary scientists from Denmark, Finland, Korea, New Zealand, Sweden, and the US gathered at the

University of California, Davis, to chart future research directions in the area of foods, nutrition and human

health. Top of the agenda were presentations on obesity, nutrigenomics and improving human health.

• H Kato and colleagues from the University of Tokyo (in a study published in the Asia Pacific Journal of Clinical

Nutrition, 2008) concluded: "the 'omics' data accumulated by our group and others strongly support the promise

of the systems biology approach to food and nutrition science."

However, a sizeable number of skeptics are also apparent when it comes to the both the evidence and commercial viability

surrounding nutrigenomics and nutrigenetics. This includes both consumers (as analysis elsewhere in this report shows),

and experts within the nutritional community. While genes undoubtedly contribute to obesity (and wider nutrition problems)

other substantive factors include higher consumption of kilojoules, coupled with a sedentary lifestyle.

Dutch researcher Amber Ronteltap recently interviewed 29 experts from trade and industry, civil organizations,

government, media and science for her doctoral research. These interviews revealed that there is poor consensus on

important questions such as what exactly defines nutrigenomics, within what time frame it will be usable in practice, and

how acceptance by consumers is determined. Based on interviews with experts and extensive study, Ronteltap developed

different future scenarios to put to the general public. A representative random sample generated a number of conditions

that consumers would require before accepting nutrigenomics. The most important is freedom of choice: the guarantee that

it would not be compulsory to register a genetic profile. Consumers also believe that the products being developed should

provide proven (health) benefits and that their use should not disrupt the routine of daily life. The general public also wants

to see clear scientific agreement about the usefulness of the possibilities provided by nutrigenomics, according to a release

from the Netherlands Organization for Scientific Research (NWO).

"Commercialization of genetics tests at this stage is premature."

Stuart Hogarth, a fellow at the Institute for Science and Society at the University of Nottingham, England, quoted in

the Wall Street Journal Asia, December 2007

“Given the current state of genetic knowledge—in which there often aren't clear-cut associations between genes and

disease—[it] sounds like a genetic horoscope.”

Gail Javitt, who leads a genetic-testing quality initiative at the Genetics and Public Policy Center at Johns Hopkins

University quoted in the Wall Street Journal Asia, December 2007

Thus far, nutrigenetics based dietary products marketed as personalized nutrition products have been designed to

complement genetic test kits and to provide individuals with dietary solutions that combat specific health issues growing out

The Future Decoded

Next Generation Functional Food and Drinks: Opportunities in Personalized Nutrition DMCM4650/Published 11/2008

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 27

of genetic variation. In contrast to nutrigenetics, nutrigenomics products will rely on the science of genomics to support

efficacy. Examples of companies and researchers capitalizing on the opportunities apparent through this science-led

approach to personalized nutrition are presented in the Action Points chapter.

Personalized nutrition, and the mega-trend it is aligned with, is also linked to self identity, self-expression and self indulgence

The definition of personalized nutrition can also be expanded to include the targeting of lifestyle and personal aspirations.

The Individualism mega-trend represents consumers’ desires to express themselves (self definition in consumer societies

is at least partially reliant on consumption), and to be recognized as having personal needs rather than being part of the

mass market.

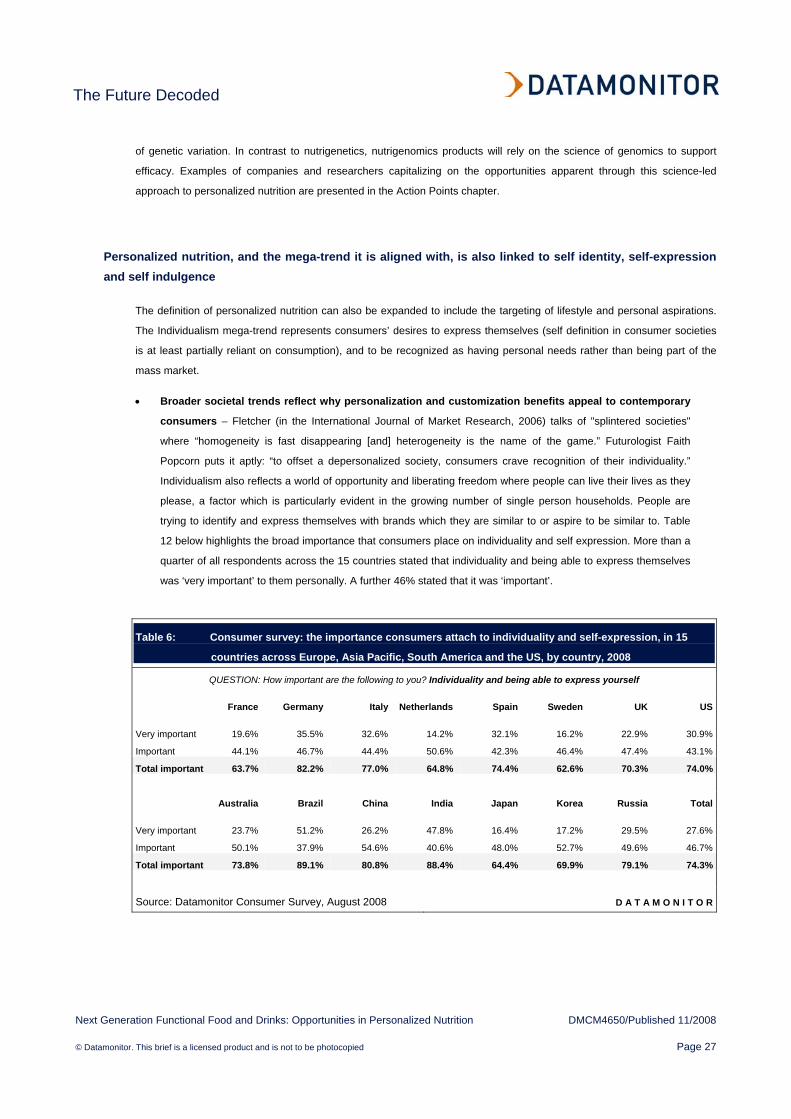

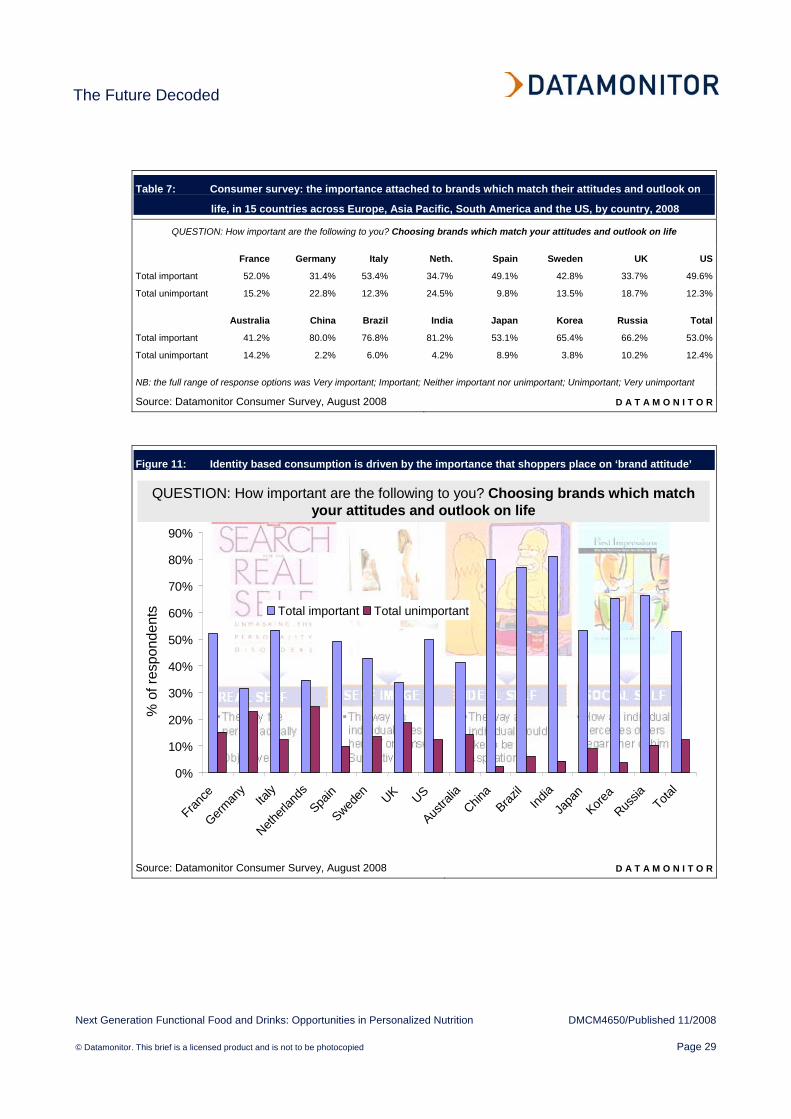

• Broader societal trends reflect why personalization and customization benefits appeal to contemporary

consumers – Fletcher (in the International Journal of Market Research, 2006) talks of "splintered societies"

where “homogeneity is fast disappearing [and] heterogeneity is the name of the game.” Futurologist Faith

Popcorn puts it aptly: “to offset a depersonalized society, consumers crave recognition of their individuality.”

Individualism also reflects a world of opportunity and liberating freedom where people can live their lives as they

please, a factor which is particularly evident in the growing number of single person households. People are

trying to identify and express themselves with brands which they are similar to or aspire to be similar to. Table

12 below highlights the broad importance that consumers place on individuality and self expression. More than a

quarter of all respondents across the 15 countries stated that individuality and being able to express themselves

was ‘very important’ to them personally. A further 46% stated that it was ‘important’.

Table 6: Consumer survey: the importance consumers attach to individuality and self-expression, in 15

countries across Europe, Asia Pacific, South America and the US, by country, 2008