Embed Size (px)

DESCRIPTION

NextGen Energy Board Meeting Lending Observations Jim Jones August 30, 2007. Overview. Farm Credit System – Ethanol Background Sources of Debt Capital Underwriting Considerations. AgriBank Overview. - PowerPoint PPT Presentation

Citation preview

NextGen Energy Board Meeting

Lending Observations

Jim Jones

August 30, 2007

Overview

Farm Credit System – Ethanol Background

Sources of Debt Capital

Underwriting Considerations

Comprised of 18 Farm Credit Associations that provide financial products to agricultural producers and agricultural related business within 15 states (See map)

$49.6 billion in assets Wells Fargo $415.8 billion

US Bank $205.9 billion

Farm Credit System (inc. AgriBank) $130.0 billion

AgriBank Overview

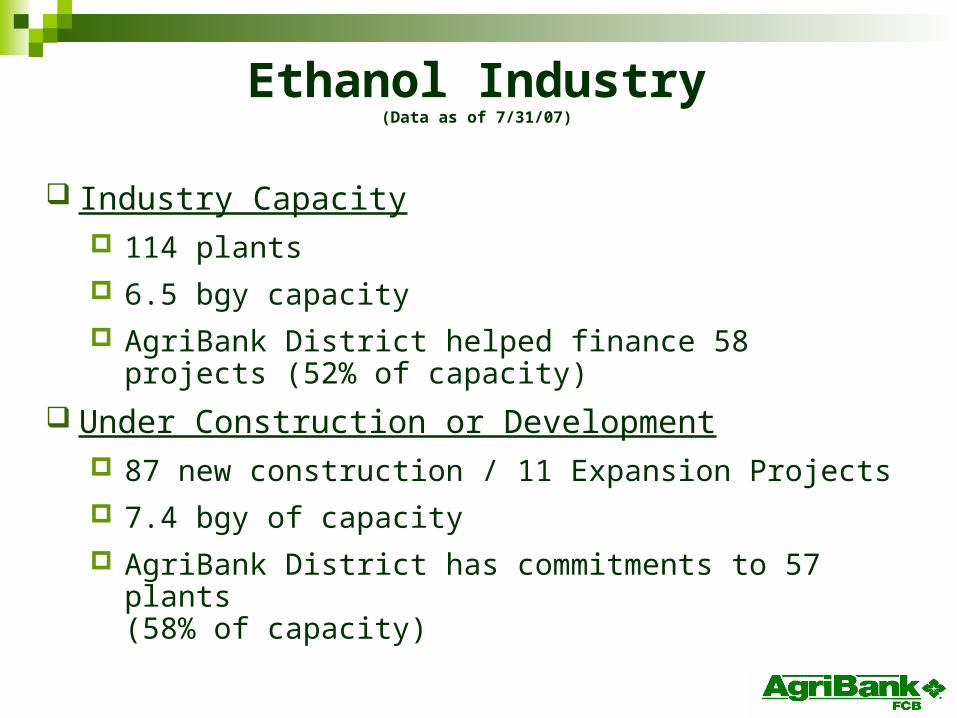

Ethanol Industry(Data as of 7/31/07)

Industry Capacity 114 plants

6.5 bgy capacity

AgriBank District helped finance 58 projects (52% of capacity)

Under Construction or Development 87 new construction / 11 Expansion Projects

7.4 bgy of capacity

AgriBank District has commitments to 57 plants (58% of capacity)

Farm Credit System Ethanol Portfolio

(as of June 30, 2007)

AgriBank District: $1.7 billion

Other Farm Credit

System Lenders: $1.8 billion*

Total System

Ethanol Commitments: $3.5 billion

* Includes Farmer Mac commitments and guarantees

Current Sources of Debt

Farm Credit System (since 1992) Provided approximately 2/3’s of debt capital prior to

2005

Commercial Banks: First National Bank of Omaha, Home Federal Savings & Loan, Community Banks

Insurance Companies

Foreign Banks: West LB, Society Generale

Future Sources of Debt

Issues Farm Credit is Full: little remaining loan capacity to

finance additional ethanol projects unless existing volume is paid down rapidly. (Hold Limits)

Blender Wall: Rate of growth exceeding blender capacity results in: Ethanol priced at variable cost of production. Idling of ethanol plants. Portfolio stress and slow rate of debt pay down. Reduced industry enthusiasm and capital investment.

Why the concern about Blender Wall?

Historical Ethanol Demand

-

1

2

3

4

5

6

7

8

9

10

11

12

13

145/

7/04

7/7/

049/

7/04

11/7

/04

1/7/

053/

7/05

5/7/

057/

7/05

9/7/

0511

/7/0

51/

7/06

3/7/

065/

7/06

7/7/

069/

7/06

11/7

/06

1/7/

073/

7/07

5/7/

077/

7/07

Bil

lio

ns

of

Gal

lon

s/Y

ear_

MTBE SubstitutionMay/June 2006

Since MTBE has been replaced Ethanol demand has been relatively flat.

Source: Houston BioFuels Consultants

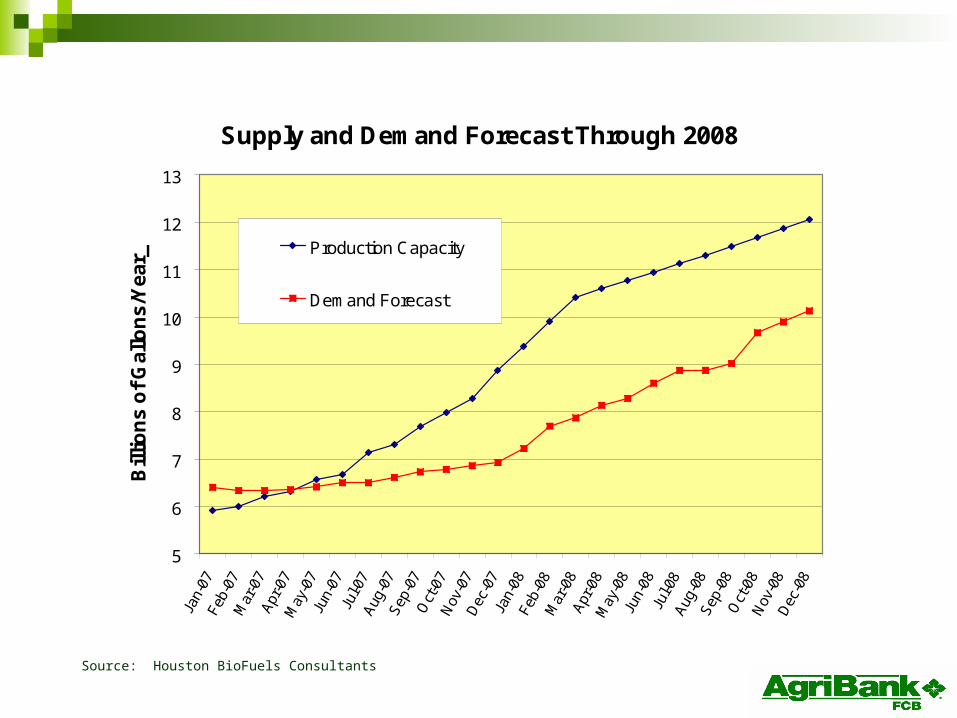

Supply and Demand Forecast Through 2008

5

6

7

8

9

10

11

12

13Ja

n-07

Feb-

07M

ar-0

7A

pr-0

7M

ay-0

7Ju

n-07

Jul-0

7A

ug-0

7S

ep-0

7O

ct-0

7N

ov-0

7D

ec-0

7Ja

n-08

Feb-

08M

ar-0

8A

pr-0

8M

ay-0

8Ju

n-08

Jul-0

8A

ug-0

8S

ep-0

8O

ct-0

8N

ov-0

8D

ec-0

8

Bil

lio

ns

of

Gal

lon

s/Y

ear_

Production Capacity

Demand Forecast

If Supply out paces demand…

Price of ethanol will drop to incent more blending capacity and/or less capacity utilization until equilibrium is satisfied

Contribution Margin = net revenues less variable costs (corn, utilities, chemicals)

Contribution Margin is the signal to producers on whether to vary production rate or stop production

In oversupplied commoditized markets, pricing typically reverts to a variable cost-plus basis. A value-added basis (gasoline related) only arises when negotiating leverage is more balanced between buyers and sellers.

Variable Costs = cash costs incurred to produce an incremental amount of product.

Underwriting Guidelines

Historical – Dry Mill Plant Equity: 50% for start up/ 40% existing

Mitigators: Experienced Management/ Construction Cash Sweeps/ Retention of Earnings Debt per gallon (less than $0.90)

Working Capital: 5% of sales or $0.15 /gallon Repayment Capacity: 115% (Net income + Interest + Depreciation divided

by Principal + Interest + Capital Expenditure + Dividends) Limitations on Dividends Loan Term: 7 to 10 years (May include cash sweeps to reduce

debt faster) Feasibility Study: Corn procurement, marketing, permitting, rail

access, infrastructure, technology, etc.

Underwriting Guidelines

Cellulosic Ethanol: No current guidelines but…

Similar to Dry Mill Ethanol Plant with following Equity: 50%

Working Capital: 10% to 15% of sales

Repayment Capacity: 115%

Dividend Limitations

Cash Sweep Provisions

Loan term 7 to 10 years

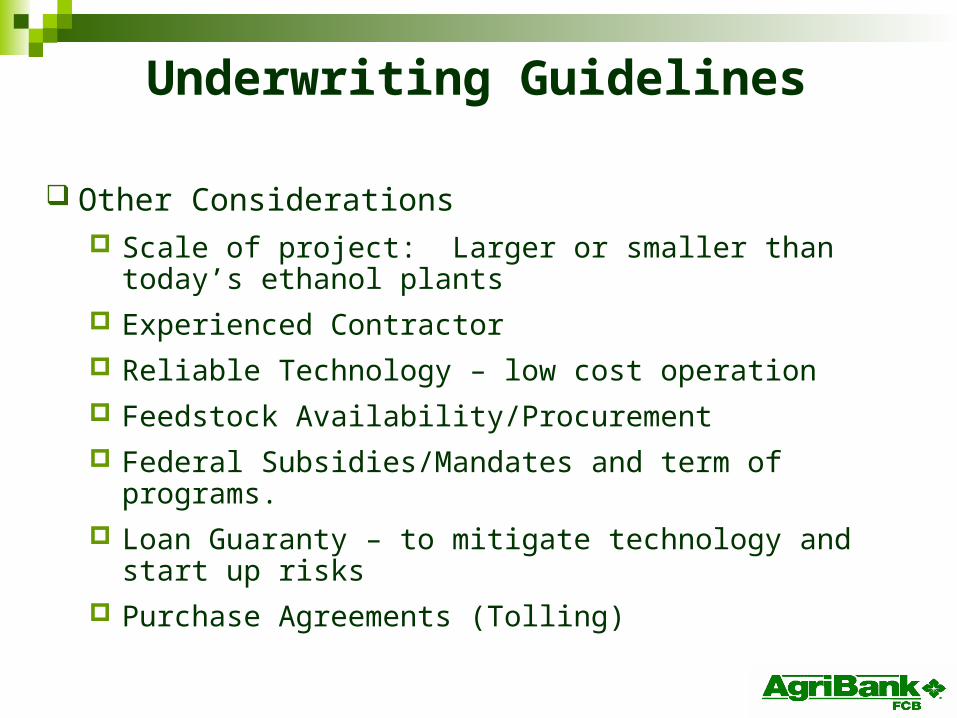

Underwriting Guidelines

Other Considerations Scale of project: Larger or smaller than today’s

ethanol plants

Experienced Contractor

Reliable Technology – low cost operation

Feedstock Availability/Procurement

Federal Subsidies/Mandates and term of programs.

Loan Guaranty – to mitigate technology and start up risks

Purchase Agreements (Tolling)

Federal IncentivesLenders Perspective

Federal Incentives (CCC production credit, Production credit) are typically not relied upon in the underwriting process.

Federal Subsidies and Mandates: Important but ultimately industry must be financially viable without Federal support to attract lenders. Large Commercial Banks have avoided the industry due to political risk.

Loan Guarantees: Best credit enhancement Issue: size of guaranty relative to cellulosic projects Typically do not guaranty lender during construction

phase