Embed Size (px)

Citation preview

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 1/224

Business Plan

RII0-GD1

NoticeSmall sections o this

document have been

redacted or reasons

o condentiality.

NoticeSmall sections o this

document have been

redacted or reasons

o condentiality.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 2/224

This document is the business plan o Northern

Gas Networks (NGN) or the period rom April 2013

to March 2021.

Its primary purpose is to demonstrate to NGN’s

customers and other stakeholders that the

company has an eective and ecient business

plan or the eight years o the price control. The

plan sets out how NGN will continue to maintain the

physical network in optimal condition, how we will

invest wisely to ensure its continued saety, how we

will meet our customers’ expectations and continue

to deliver value or money. The plan meets therequirements o our economic regulator, Ogem, to

provide a high level o detail to support our business

case.

This price review period is the rst or gas

distribution which is based upon the principles

o RIIO (Revenue = Incentives + Innovation +

Outputs) and is known as RIIO-GD1. The RIIO

model replaces the previous RPI-X regime and

is designed to better meet the investment and

innovation challenge by placing more emphasis on

incentives to drive the innovation needed to deliver

a sustainable energy network, at value or money,

or existing and uture customers.

The document is divided into the ollowing sections.

Section 1 – Executive summary

This is a high-level overview o the entire document,

summarising the contents o each section.

Section 2 – Northern Gas Networks

NGN was created in June 2005 with the sale o

our o the eight gas distribution networks owned

by National Grid. This section explains how NGN

works to a corporate vision which is supported by

a range o perormance measures. It details how

NGN has perormed against these measures or

the past six years, delivering natural gas in the most

cost-ecient way to 2.6m users across Northern

England.

Section 3 – Business and operatingenvironment

NGN must operate within a legal and regulatory

ramework which dictates required perormance

levels. This brings with it a range o challenges:

some are specic to the gas distribution industry;

some are as a result o the economic situation; and

some are geographic issues. This section details

these challenges and NGN’s approach to managing

them.

Section 4 – Innovation strategy

Innovation allows a company to adapt the way in

which it delivers its services, reacting to a changing

environment to ensure it continues to deliver optimal

perormance. When NGN was created it chose to

operate a unique asset management model, which

it is now changing as the company reacts to the

challenges o a new price control period and the

move to a low carbon economy in the UK. This

section explains how NGN has and will continue to

use innovation.

Section 5 – Stakeholder engagement

The views o customers and other stakeholders are

important to NGN. They provide a vital direction

and ocus to improve our service delivery. For this

price control period we implemented an enhanced

engagement programme to ensure all stakeholders

were given an opportunity to engage with us and

their eedback has delivered a reduction in our initial

expenditure plans. This section explains how NGN

has historically gathered stakeholders’ views, what

we did or this business plan and our plans or the

uture.

Section 6 – RIIO-GD1 output forecasts

NGN has detailed 56 output measures in six

business activity areas in this business plan,

covering the eight years o the RIIO-GD1 price

control period. Section 6 contains detailed orecasts

o how NGN expects to perorm in these areas.

A guide to this document

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 3/224

Section 7 – Expenditure forecasts

NGN needs to make signicant levels o investmentin the gas distribution network during

RIIO-GD1 to ensure we continue to deliver gas to

homes and businesses across the North o England

in a sae and ecient manner. Our expenditure

plans are explained in detail in this Section.

Section 8 – Revenue and nancialforecasts

I NGN is to continue to operate a sae and

secure gas distribution network it needs levelso revenue to match its expenditure plans. We

must attract the investment which is essential to

nance the business and balance the requirements

o customers. This section explains how we will

achieve this balance and the level o revenue we

need to operate.

Section 9 – Impact on customer bills

NGN’s business plan is based upon the principle

o continuing to deliver value or money or the

network’s customers whilst maintaining high

standards o saety, customer service and

environmental responsibility. The nancial impact o

this business plan on customers’ bills is detailed in

this section.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 4/224

Contents1

2

3

4 8

5

7

6Executivesummary 7

NorthernGasNetworks 13

2.1 Key Facts 15

2.2 Corporate vision 17

2.3 Perormance since 2005 18

Businessandoperatingenvironment 27

3.1 Background 29

3.2 Legal and regulatory ramework 29

3.3 RIIO 29

3.4 Longer term challenges 30

3.5 Regional economic outlook 32

3.6 The demand or gas on NGN’s network 33

3.7 Regional actors 35

Innovationstrategy 37

4.1 Background 39

4.2 NGN’s innovation strategy 40

4.3 Integrated business model 43

4.4 Total Network Management 46

4.5 Innovation investment programme 55

4.6 Benchmarking and best practice 65

4.7 Summary 69

Stakeholderengagement 71

5.1 Background 73

5.2 Key messages 74

5.3 Stakeholder engagement since 2005 79

5.4 Stakeholder input to RIIO-GD1business plan 80

RIIO-GD1outputorecasts 85

6.1 Background 87

6.2 Saety 88

6.3 Reliability 97

6.4 Customer service 107

6.5 Environment 112

6.6 Social obligations 120

6.7 Connections 124

Expenditureorecasts 129

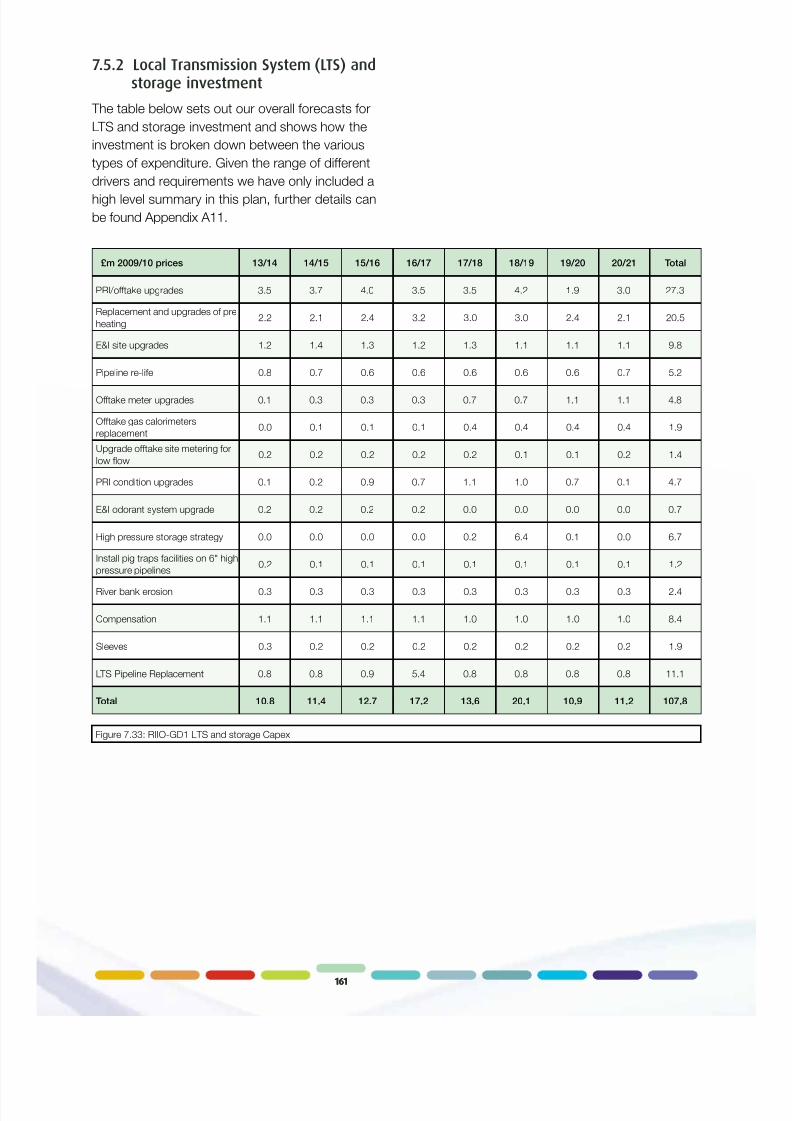

7.1 Background 131

7.2 Key assumptions 132

7.3 Investment plans 139

7.4 Replacement expenditure 140

7.5 Capital expenditure 159

7.6 Operating expenditure 174

Revenueandfnancialorecasts 191

8.1 RIIO-GD1 revenue and nancialorecasts 193

8.2 Financial outcomes 194

8.3 Key nancial modelling assumptions 196

8.4 Requirement or transitionalarrangements 204

8.5 Proposed transitional arrangements 209

8.6 Rewards or rontier perormance 214

Page No. Page No.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 5/224

9

A

Impactoncustomerbills 217

9.1 Background 219

9.2 RIIO-GD1 revenue 219

9.3 Customer bills 219

9.4 Charging volatility and predictability 220

Appendicestothisdocument

A1 ENA Gas Futures scenarios

A2 TPA report on medium term economicoutlook

A3 Benchmarking and testing

A4 Innovation projects

A5 Stakeholder engagement

A6 EC Harris report on Real Price Eects

A7 First Economics report on productivity

A8 Expenditure orecast plan and tablereconciliation

A9 Pensions-Redacted

A10 Repex tier two risk threshold methodology

A11 Capex and asset health-Redacted

A12 NTS NGN capacity interaction

A13 Oxera report on cost o equity

A14 Oxera report on cash fow betas andcost o equity

A15 Oxera report on debt indexation

A16 Oxera report on long term equity returns

A17 Uncertainty and risk

A18 Regional actors

Page No.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 6/224

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 7/224

7

Executivesummary 1

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 8/224

8

Northern Gas Networks is thefrontier gas distribution networkin the UK.

For the past six years we have been consistently

measured by Ogem as the most cost-ecient o

the eight networks (GDNs), delivering industry-leading value or money or our 2.6m customers.

At the same time we have delivered signicant

improvements in our saety, customer service and

environmental perormance and have established

excellent levels o network reliability.

Our aim is to continue with this pace-setting

perormance as we transition rom the GDPCR1

period into RIIO-GD1. Our corporate vision is to be

consistently measured by Ogem and the Healthand Saety Executive (HSE) as a top two perormer

or saety, eciency and customer service. We are

achieving this vision and want to go urther - we

want to be measured as the best in class.

Our business plan or RIIO-GD1 is based upon

the most solid o oundations, our unrivalled track

record since 2005. But we are ambitious and plan

to set ever-improving benchmark perormances

by relentlessly improving saety, delivering better

customer service, reducing our impact upon the

environment and, most importantly, continuing to

provide excellent value or money.

We have made huge reductions in the level o risk

to our customers rom our network assets and are

the only GDN to have internationally recognised

accreditation or both saety and environmental

perormance. We are the clear leader or cost

eciency, saely delivering gas to homes and

businesses across Yorkshire, the North Eastand northern Cumbria around the clock without

interruption, even in the worst weathers. We have

also reduced the number o customer complaints

by 74% in recent years as we are committed to

getting the job right rst time, every time.

When the our GDNs were sold in 2005, Ogem

predicted a 15% reduction in controllable operating

expenditure (Opex) over the ollowing two regulatory

periods. This was on the basis o new ownersmoving into the sector and the introduction o

comparative competition.

At Northern Gas Networks (NGN) we have already

delivered an 18% saving in controllable Opex since

2005. This represents an early delivery o the ulldemerger dividend with customers beneting rom

2013/14 rather than the predicted 2018/19.

This demonstrable cost benet, together with

signicant improvements in saety and customer

service, has been delivered or the benet o gas

distribution customers across the UK, creating

signicant levels o long term value. This has been

achieved in spite o some unique challenges to our

business.

Unlike the other GDNs, or the last three years we

have not held major contracts to carry out domestic

metering work. This has resulted in an annual

stranded resource cost o around £10m, which we

have proactively managed down to £4m per year

o recurrent costs. No other GDN aces this cost

pressure and we believe this unique position should

be recognised in the setting o nancial allowances

and benchmarks.

Similarly, we ace specic regional actors which

add extra costs to our service delivery. These

include the Pennine bedrock which makes

working in our West Yorkshire conurbation more

challenging; and the engineering anomaly o double

rail secondary mains, traditionally laid in the rear

gardens o our mill towns, which increase our mains

replacement costs.

Additionally, whilst our geographic area contains

two o the six largest UK conurbations, our region

has the lowest level o population density outside

Scotland. This mixture o dense urban areas with

outlying rural centres o population at the edge o

our network adds a signicant cost burden to our

operational perormance.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 9/224

9

There are challenges to be aced rom the

Government’s desire to move to a low carbon

energy mix. We strongly believe that gas distribution

has a pivotal role to play as we transition to a low

carbon economy. The capability o our network will

be maintained – it is in the UK’s interest to retain

a strong and ecient gas distribution capability –to ensure we can meet any challenges which are

posed and to support the Government’s agenda.

This business plan is based upon what our

stakeholders have told us. Their views can largely

be broken down into three main subject areas: cost,

saety and impact upon the environment.

We have always engaged with our customers and

wider stakeholder audiences. For us it is not just

about listening to their views, it’s about involvingstakeholders.

We believe we have achieved this in developing

this business plan through one-to-one and one-

to-several conversations and meetings; not just

by asking a customer to ll in a survey orm or to

attend a public meeting. We have delivered a multi-

level engagement strategy to ensure we captured all

points o view.

Our stakeholders told us what was important tothem: delivering sae and reliable supplies o gas to

their homes and businesses at the lowest possible

price, without jeopardising saety, minimising our

eect on the environment and with high levels o

customer ocus.

When they suggested new ways o doing things

we costed them out, then went back and asked i

they wanted us to incorporate the suggestions into

our business operations. Sometimes it was yes,sometimes no. But they were involved, they made

the decisions.

We will continue with this approach, involving our

stakeholders in the decision-making processes o

our business.

We involved our stakeholders in the setting o our

overall nancial orecasts. When we presented

our initial proposals they told us they were too

expensive and highlighted the areas upon which

we should ocus. As a result, our plans have been

reduced by c.£30m a year, or c.£250m over the

RIIO-GD1 timerame. This will deliver improvementsin saety, eciency, customer service and in the

way in which we impact on the environment,

representing enhanced levels o value or money or

the users o our network.

Our stakeholders told us what they wanted us to

improve and what they were happy to maintain

at current perormance levels. Our business plan

contains 56 output measures. Based on what our

stakeholders told us, we plan to improve our current

perormance in 35 and to maintain current levels in

the remaining 21. We are proposing six voluntary

measures based upon what our stakeholders told

us was important to them, so they can track how

we perorm.

We are committed to delivering and maintaining

high levels o perormance in the most cost-ecient

way. Our stakeholders’ requirement or value or

money is directly refected in our overall expenditure

plans.

To achieve this we are taking a new approach to

network management: the Total Cost o Ownership.

This innovation will allow us to prioritise our expenditure

to manage risk and deliver the key outputs our

stakeholders demand. It will drive a higher level o

inormed decision-making about the most ecient way

o working, aligning geographic and asset perormance

data to give a greater ocus on when and where to

maintain, enhance and replace our assets.

Making this change is a natural progression rom

the strategic asset management model which

worked so successully or us in the past. A new

approach is needed to meet the resh challenges o

RIIO-GD1 and the move to a low carbon economy.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 10/224

10

We are already reshaping our organisation to

enable the Total Cost o Ownership approach to

be ully unctional ahead o the implementation o

RIIO. This integrated, customer-ocused business

model connects asset integrity management with

customer operations and programme investment.

They are intrinsically linked, working seamlesslyto place asset management and asset health at

the centre o the business, underpinning all our

investment decisions.

A new asset health model has been developed

which provides essential inormation on all the

types o asset we own, their condition and the risk

and consequence o ailure. This allows us to make

timely and ecient investment decisions and the

ability to assess the range o options available to

manage the identied risk. Our rst ull network-

wide analysis o asset health has been built into our

uture investment plans.

In order to deliver this holistic approach we are

giving a greater geographic ocus to our rontline

customer operations. This will drive higher levels o

perormance at a local level, closer to our assets

and customers, ensuring we have the right resource

available in the right place and at the right time.

To do all this requires our business to remain on

rm nancial oundations. This is a major challenge

as we move rom GDPCR1 into RIIO-GD1.

The nancial package which is required must

balance the critical nanceability actors with the

impact on customers’ bills.

We believe the nancial package contained within

this business plan achieves that balance between

customers and investors, including shareholders.

Our plan prioritises the need to minimise

customers’ exposure to signicant uture

increases in bills as a result o the capitalisation

o replacement expenditure and the move to

international nancial reporting standards (IFRS).

The transitional arrangements which we are

proposing will ensure customers are given longer

term assurances on the stability and transparency

o the costs they will incur.

Importantly, we believe our proposals will deliver

the stable regulatory ramework which is required

to attract the appropriate levels o investment

into our business in the RIIO-GD1 period and

beyond. There is also an appropriate balance to

be struck between risk and reward or customers

and investors. Shareholders continue to absorb asignicant element o risk in RIIO-GD1.

In developing the overall nancial package which

is required to deliver our business plan, we have

ensured that our proposals are compliant with

the RIIO principles including: the cost o equity;

the cost o debt; capitalisation policy; and asset

lives and depreciation. We broadly agree with the

regulator’s proposals or these parameters.

We strongly believe that as the GDN setting theeciency rontier, there will be an element o reward

or our past perormance. This has delivered

signicant cost savings or the users o our own

network and or gas distribution customers across

the UK as we have already moved the eciency

rontier beyond what was predicted at the time

o network sale. We see a sum o at least £10m

per year as being appropriate recognition or the

customer benets which we have delivered since

2005.

The key nancial parameters we have assumed

within this plan include: notional gearing at 62.5%;

a cost o equity o 7.2%; a cost o debt o 2.8%

(average); a notional equity return on Regulatory

Asset Value (RAV) o 5%; transitional arrangements

to maintain credit metrics; and a depreciation

prole based upon a sum o digits methodology.

Our revenue requirements are broadly in line with

those o GDPCR1 (excluding the impact o IFRS),

averaging c.£342m per year over the eight years o

the price control. Our overall nancial package will

support the investment o more than £1.2bn in the

network over the eight years o RIIO-GD1. (These

are in 2009/10 prices.)

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 11/224

11

Our plan will see more than 4,100km o ageing

metal gas mains replaced with new, saer

plastic pipes; a reduction in carbon emissions

equivalent to 500,000 tonnes o carbon dioxide;

the recruitment o more than 250 apprentices

into our business; 6,500 homes connected to

the gas network and removed rom uel poverty;£25m invested in innovation; the removal o all

the gasholders in the North o England; and a 1%

per year improvement in the productivity o our

workorce.

This will demonstrably deliver better value or our

customers and signicant levels o investment in

the economy o the North o England. It will provide

a saer gas distribution network with ewer leaks,

reduced risk, improvements in customer service,

enhanced levels o innovation, reduced levels o uel

poverty and a signicant shit towards the low carbon

economy which the Government has committed to.

Our network is already driven by what our

customers tell us. That will increase in the

uture as we develop new ways o involving our

stakeholders. Our expenditure plans or RIIO-GD1

are derived rom our existing industry-leading levels

o eciency. We are committed to continuing to

deliver real improvements in productivity and cost-eciency.

Our nancial proposals balance the requirements

o all the stakeholders in our network: customers,

shareholders and other providers o nance who all

have a vested interest in ensuring risk and reward

are equalised, in the short, medium and longer term.

With the balancing o revenue and expenditure,

as proposed in this business plan, we will make

signicant improvements in our physical network,

enhancing its health, integrity and saety and

ensuring it is capable o playing its role in the UK’s

transition towards a low carbon economy. This

will be supported by our strategy or investment

in research and the development o innovative

technologies, processes and commercial

arrangements which will enable NGN, and the

wider gas distribution sector, to meet the signicant

challenges o the uture.

All these increased outputs can be delivered,

saely, eciently and sustainably, or a one penny

a day increase in our customers’ bills. In return, we

will continue to drive innovation in managing our

network; we will build upon our rontier position,

working closely with our stakeholders to ensure our

customers continue to get value or money; and wewill do this saely, eciently and sustainably.

Customers will receivesignicantly more value for anincrease in gas bills of one pennyper day. We believe this plandelivers tremendous value formoney for customers.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 12/224

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 13/224

13

NorthernGasNetworks 2NGN was created in June 2005 with the sale of four of the eight gas

distribution networks owned by National Grid. This section explains

how NGN works to a corporate vision which is supported by a range of

performance measures. It details how NGN has performed against these

measures for the past six years, delivering natural gas in the most

cost-efcient way to 2.6m users across northern England.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 14/224

14

Executive summaryNGN is the most ecient gas distribution network

in the UK.

This is evident rom the benchmarking o the

nancial perormance o the eight GDNs since

2005/6 and has delivered signicant benet or gasdistribution customers across the North o England,

and or gas users across the UK as a whole. We

deliver a high value, cost-ecient service to our

customers.

The reductions in the cost o operating our network

total 18%, which represents early delivery o the

demerger dividend which was predicted at the time

o network sales in 2005. It was expected to take

two ull regulatory periods to deliver cost savings

o 15%, through the introduction o new network

owners and comparative competition. We have

delivered the benet in one regulatory period.

At the same time we have taken massive steps

orward in improving saety in our network,

removing the risk rom ageing metallic mains and

reducing the number o accidents in our network.

Customer service perormance has also seen a

signicant improvement, with a reduction in the

number o complaints o c.74% when compared

to 2007. Excellent levels o network asset reliability

underpin this perormance.

This level o perormance has been achieved

through the implementation o a challenging

network vision, which refects the primary

objectives o the business to be a top perormer

in eciency, saety and customer service while

at the same time recognising our environmental

responsibilities. That vision is being achieved.

We have a strong track record in delivering our

commitments to customers and have an industry

leading perormance which will continue to provide

a value or money service through the RIIO-GD1

period.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 15/224

15

2.1 Key factsNorthern Gas Networks is the licensed gas

transporter or the North o England. We are

responsible or the sae and ecient delivery o gas

to homes and businesses in West, East and North

Yorkshire, the North East and northern Cumbria.

• Our network

- has 37,000km o pipeline

- covers 25,000km2

- serves 2.6m customers.

• 50% o our customers are located in two o thelargest conurbations in the UK.

• The remainder are in sparsely populated rural

areas taking in our national parks.

• Our network transports 82,000 GWh o energy

annually.

• We are a signicant regional employer with a

highly skilled workorce o more than 1,200 sta

and 800 contractors.

• We invest £120m annually in the inrastructure o

the region.

Figure 2.1: The geographic area served by NGN

Workington

Carlisle

Newcastle-upon-Tyne

Berwick-upon-Tweed

Sunderland

Middlesbrough

Scarborough

York

Leeds

Hudderseld

Hull

< 23

148 - 322

323 - 866

867 - 2,337

> 2,337Key: Population density -number o people per km2 per local authority district.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 16/224

16

NGN is owned by a consortium o three partners.

The consortium constitutes a robust, well

capitalised shareholder group which has signicant

global experience in the ownership and operation

o utility and inrastructure businesses.

We have sought to exploit the synergies and

benets that come rom being part o this large,

multi-national group o companies and will continue

to leverage these commercial relationships to

deliver ongoing eciencies and productivity.

The strong, stable regulatory ramework in the UK

has been a key actor in attracting investors o the

stature o NGN’s ownership group. Such investors,

with signicant experience in international utilities

and inrastructure assets, who look to invest or

the longer term, will be key players in delivering thenecessary investment required to meet the UK’s

uture energy and environmental challenges.

All three owners are committed to building on the

network’s inheritance o providing sae and reliable

operations and to maintaining NGN as a socially

responsible corporate citizen in the region. These

will continue to be key elements o our business

plan as we meet the uture challenges over the

short, medium and longer term.

Figure 2.2: NGN’s ownership structure

Power Assets Holdings

Limited

NORTHERN GAS NETWORKS LIMITED

Northern Gas Networks

Holdings Limited

SAS Trustee Corporation

Northern Gas Networks

Finance Plc

Northern Gas Networks

Operations Limited

Cheung Kong Inrastructure

Holdings Limited

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 17/224

17

2.2 Corporate vision

A corporate vision was introduced in 2005,

refecting the primary objectives o the business:

saely, eciently and sustainably delivering a secure

supply o gas to our customers.

The vision is based rmly within the scope o NGN’s

role as a monopoly utility service provider and has

provided a robust basis against which we have

successully addressed the challenges aced since

June 2005. This vision remains appropriate as NGN

adapts to the additional challenges that a changing

energy market will present as the UK moves towards

a low carbon economy.

Our corporate vision is supported directly by

our business values which refect the way our

employees deliver their roles and activities. The

consistent demonstration o our values in our dayto day business activities has helped build a culture

that drives sustainable business perormance.

• Believing in a workplace ree o accidents and

injuries.

• Valuing and rewarding our employees or their

contribution to the business.

• Motivating our contractor partners to

continuously improve perormance or mutualbenet.

• Treating customers as we would wish to be

treated.

• Maintaining high standards o corporate

governance.

• Taking pride in being a respected part o the

community.

• Achieving the expectations o our owners.

To be benchmarked by Ofgem andthe HSE consistently in the top twocomparable utilities for safety, efciencyand customer service.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 18/224

18

2.3 Performance since 2005

We have a strong record o industry leading

perormance since 2005.

• Set new benchmark standards or cost eciency

to drive increasing value or our customers.

• Improved saety perormance has reduced

the number o people injured in our network to

record low levels.

• Customer service perormance has improved

year on year as we drive down the number o

complaints.

2.3.1 NGN has already delivered the

demerger dividend

An assessment o our perormance since 2005

provides a very good benchmark o the eectiveness

o our corporate strategy and, importantly, NGN’s

ability to deliver the commitments set out in this

business plan or RIIO-GD1.

It was predicted that the sale o the gas networks

by National Grid in 2005 would result in signicant

reductions in controllable operating expenditure

(Opex) over two regulatory periods through new

ownership and comparative competition, reerred

to as the demerger dividend.

NGN has delivered this benet in just one

regulatory period, through driving consistent yearon year eciencies whilst improving customer

service and saety.

This represents early delivery o the ull demerger

dividend as the benet to customers o network sale.

Customers benet rom lower transportation

charges immediately and will continue to benet

rom 2013/14 instead o waiting until 2018/19.

This equates to an industry leading 18% real

reduction in controllable Opex since 2005.

Figure 2.3: Controllable operating expenditure (Opex)

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 19/224

19

2.3.2 Efciency

At the start o GDPCR1 NGN was assessed to be

the most ecient GDN. By setting these rontier

levels o perormance, we have enabled Ogem

to set the benchmark or all GDNs, so delivering

signicant levels o value or all gas distribution

customers.

We have continued to set rontier levels o

perormance and provide the standard by which

other GDNs should be assessed. In using this

approach Ogem will be able to return urther

signicant amounts o value to customers during

RIIO-GD1.

Our perormance over the last six years has

demonstrated how the company has successullydeveloped a culture o continual improvement,

clearly driving corporate initiatives to improve

eciency.

2005/6 2006/7 2007/8 2008/9 2009/10 2010/11

Opex

Repex

Totex

Figure 2.4: Ogem’s eciency analysis o NGN

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 20/224

20

R

e p e x a n d C a p e x

Top 25% National Grid - West MidlandsWales and West Utilities

Between

25% - 50%

National Grid - East o England

National Grid - North West

National Grid - North West

Wales and West Utilities

Between

50% - 75% National Grid - East o England National Grid - West Midlands

Scotland Gas Networks

Scotland Gas Networks

Bottom

25%National Grid - London

National Grid - London

Southern Gas Networks

Southern Gas Networks

Key

2009/10 perormance

2008/09 perormance

Bottom

25%

Between

50% - 75%

Between

25% - 50%Top 25%

Total Opex

Figure 2.5: Ogem’s total cost benchmarking

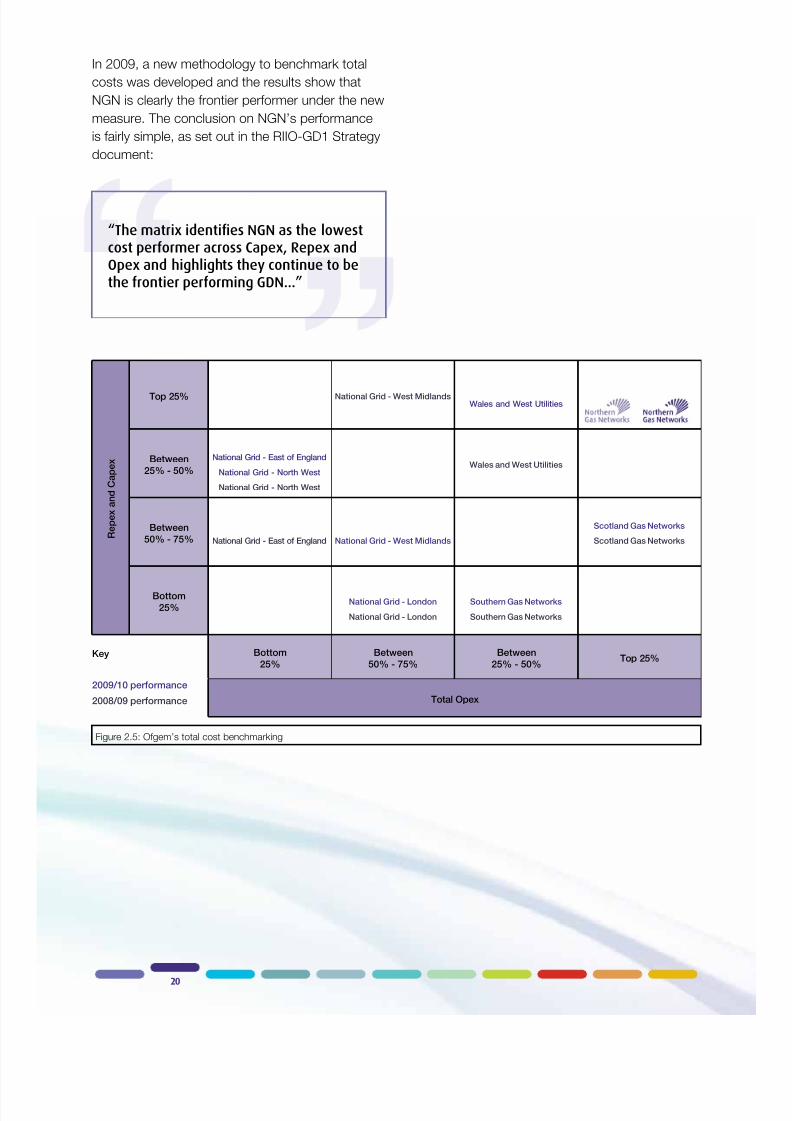

In 2009, a new methodology to benchmark total

costs was developed and the results show that

NGN is clearly the rontier perormer under the new

measure. The conclusion on NGN’s perormance

is airly simple, as set out in the RIIO-GD1 Strategy

document:

“The matrix identies NGN as the lowestcost performer across Capex, Repex andOpex and highlights they continue to bethe frontier performing GDN...”

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 21/224

21

NGN’s rontier perormance allows the regulatory

ramework to create enormous benet or gas

customers across the UK by moving all companies

to the benchmarked rontier level o eciency.

Setting all GDN expenditure allowances in line

with NGN’s rontier levels o eciency will reduce

costs or gas customers right across the RIIO-GD1period.

Based on a range o techniques, we can be seen

to have delivered signicant value or customers

through extending the rontier. This benet could

total in excess o £200m in RIIO-GD1. Rewards or

rontier perormers creates the correct incentive

ramework both within and across regulatory

periods. As an example, the graph below shows

the aggregate annual industry cost savings (using

2008/09 and 2009/10 industry costs) that NGN

has driven through operating as the most ecient

GDN rather than an average GDN.

In addition to Ogem’s analysis we have

corroborated NGN’s perormance throughout

this business plan with our own benchmarking,

including international benchmarking exercises with

gas distribution operators in the US and Japan,

and comparative assessment o various parts o

NGN’s operations. These conrm our status as a

rontier perormer within gas distribution and also in

comparison to other sectors.

2.3.3 Customer service

The importance o customer service to NGN is

demonstrated by our corporate vision. Together

with saety and cost-eciency, customer service

is prioritised as being a business-critical activity

which is crucial to the continued success o the

company.

Number of complaints

We have reduced the number o complaints

received by the business by c.74% since 2007.

We believe reducing the number o complaints is

a key perormance indicator. It is a measure o the

quality o our operational (ront line) delivery andcustomer service.

Reducing the number o complaints we receive will

continue to be a key ocus and a key indicator o

our customers’ overall satisaction with the service

we are providing.

Figure 2.6 : Value created by NGN rontier per ormance Figure 2.7: Number o complaints received

0

5

10

1520

25

30

35

40

Opex Repex Totex

A g g r e g a t e i n d u s t r y

a n n u a l c o s t s a v i n g s

( £ m 2

0 0 9 /

1 0 p r i c e s )

Annual value for customers created by

NGN’s frontier performance

14

23

37

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 22/224

22

Customer satisfaction surveys (CSS)

Undertaking quarterly surveys o customers’

opinions was started in 2005, or customers

who had experienced an unplanned gas supply

interruption (repair and emergency) and or those

who had experienced a planned supply interruption

(replacement).

A survey o connections customers was started

in 2008. NGN’s customer service scores in the

surveys since 2008/9 are set out below.

Standards o customer service across the GDNs

are consistently high with customers rating

perormance across the three categories at an

average o 7.7 out o 10. The average ‘spread’

between the highest and lowest scoring GDNs is

typically less than one point.

Since 2008/9 (when scoring was introduced on

a consistent 1 - 10 basis) NGN has achieved

scores at or above the industry average or repair

and replacement. Whilst our perormance in

connections was initially below average, this hasimproved signicantly to where we are well above

average in 2010/11 and are now a consistent upper

quartile perormer.

We remain committed to consistently achieving

a top two level o perormance in the customer

service surveys.

Figure 2.8: Ogem CSS Repair & Emergency Figure 2.9: Ogem CSS Replacement

Figure 2.10: Ogem CSS Connections

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 23/224

23

2.3.4 Health and safety

The importance o saety is highlighted by eedback

rom stakeholders, where it is consistently ranked

as an important element o our activities. NGN

is committed to protecting the saety, health and

welare o our employees, those who work directly

or us and on our behal. We believe it is our

responsibility to deliver our operations in a way

which protects public saety at all times.

In 2007 NGN achieved certication to the

Occupational Health and Saety Standard, OHSAS

18001, and we have an integrated health, saety

and environmental management system. OHSAS

18001 demonstrates NGN’s commitment to health

and saety including, amongst others, to:

• Lower or eliminate the risk o ill health or injury

to our employees, contractors, visitors and

members o the public;

• Comply with applicable laws, regulations and

other requirements;

• Continually improve our health and saety

perormance through the development o targets

and objectives; and

• Conorm to national health and saety best

practice.

Working to OHSAS 18001 means that NGN

can manage risk, demonstrate diligence, gain

assurance, prevent downtime, and potentially

reduce liability claims and insurance premiums.

We believe that all work-related injuries and

illnesses are preventable. We have integrated saety

and occupational health considerations into all our

business decisions to help ensure the saety o our

workorce and the public.

These principles, allied to a strong management

commitment to saety and a nancial incentive

ramework or all employees and contracting

partners, have resulted in a demonstrable

improvement in saety perormance.

Operational safety

Since taking ownership o the network we have

signicantly reduced the number o lost time

injuries (LTIs) within our workorce, both our direct

employees and those o our contract partners.

We have also signicantly reduced the number o

members o the public (MOP) injured as a result o

our works.

We have successully introduced initiatives such asthe It’s Your Call scheme that encourages sta and

members o the public to report to us directly any

incidents or practices that they believe pose a risk

to operational saety.

We have an overall objective to reduce the number

o LTIs and MOPs on our network to zero. We have

set ourselves stretching targets over the RIIO-GD1

period to achieve this objective.

Figure 2.12: Number o LTIs

Figure 2.11: Number o injuries to MOP

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 24/224

24

Asset safety

Additionally, since 2006 we have almost halved the

amount o risk in the distribution network rom our

iron mains. By targeting our replacement programme

to address those iron mains that pose the greatest

risk to the public we have succeeded in removing a

higher percentage o risk per km o main.

We have ranked consistently in the top two

perormers in the percentage o repairs completedwithin 12 hours. Direct eedback rom HSE

representatives strongly indicates that NGN is

regarded as one o the best perorming networks

by the HSE across all gas distribution activities.

2.3.5 Environmental impact

NGN is ully aware o the impact that our

operations have upon the wider environment and

the local communities we serve. We are committed

to operating our business in an environmentally

responsible and sustainable manner, ensuring at all

times that any potential adverse impact upon the

environment is minimised.

We hold ISO 14001 certication. This internationally

recognised environmental management standard

delivers a ocus on the ollowing.

• Reducing adverse environmental impacts.

• Delivering continual environmental perormance

improvements.

• Complying with all applicable environmental

requirements.

• Conorming to national environmental best

practice.

Natural gas emissions

Methane, the main constituent o the natural gas

we transport, is a potent greenhouse gas. The

principal contribution we can make to improve the

environment is to reduce leakage rom our network.

This leakage occurs through pipeline joints, seams

and other assets as gas is transported through the

gas distribution network and represents around

0.06% o total throughput.

Since 2005, we have reduced leakage by more

than 10%, approximately 185,000 tonnes o carbon

equivalent (tCO2e). We have achieved this througha programme o pipeline replacement, reducing

system operating pressures, treatment o pipeline

joints and seals, the capture o gas vented during

street works and managing gas escapes within the

agreed standards o service.

Figure 2.14: Percentage o repairs completed within 12 hours

Figure 2.13: Target population and total risk remaining (normalised)

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 25/224

25

Carbon emissions

We also actively measure, monitor and manage

our non-leakage business carbon ootprint

which in 2010/11 equated to 11,376 tCO2e. This

is the amount o carbon which we emit to the

atmosphere through the operation o our vehicle

feet, the energy we use in our oces and depots

and in the day-to-day operations o our business.

We have made signicant progress in reducing our

impact on the environment since 2005. There is

more we need to do over the next decade. We are

committed to making urther signicant progress inthe uture.

NGN has a strong track record of delivering its commitments since 2005. This businessplan is built directly upon the industry leading performance detailed above and deliversadditional and continual improvement across RIIO-GD1.

Figure 2.15: NGN’s business carbon emissions 2010/11

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 26/224

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 27/224

27

3Businessandoperatingenvironment

NGN must operate within a legal and regulatory framework which dictates

required performance levels. This brings with it a range of challenges:

some are specic to the gas distribution industry; some are as a result

of the economic situation; and some are geographic issues. This section

details these challenges and NGN’s approach to managing them.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 28/224

28

Executive summaryNGN’s purpose is to deliver natural gas to 2.6m

users across the North o England, saely, cost-

eciently and sustainably, at all times meeting the

legal and regulatory demands on our business.

The role o gas distribution will change as the UK transitions towards a low carbon economy, but

we believe that gas has a signicant role to play

in the uture energy mix. It is in the UK’s interest

to maintain strong and ecient gas distribution

networks in order to meet the Government’s

environmental objectives, at signicantly lower cost

than other alternatives.

Demand or gas has been reducing in our region

or several years and we orecast that this trend will

continue during RIIO-GD1. However, there will be

a need to reinorce the network to meet localised

organic changes in customers’ demand patterns

and to maintain a ocus on saety, reliability and

value or money.

The economic outlook presents a gloomy picture

in the short and medium term. Economic growth

in our region has remained below the UK average

since 1990 and the impact o the recession was,

and continues to be, more markedly elt in the

North. These key economic elements have been

included in our business plan. Additionally, there

are a range o unique regional actors which impact

upon NGN and add an additional cost burden to

the delivery o our operations. These include the

act that we have the lowest customer density

with the greatest network coverage o all the eight

GDNs. While we have two o the UK’s largest six

conurbations within our region, we have the lowest

population density o anywhere in England or

Wales.

We believe these additional costs should be

recognised and refected in our benchmarking and

cost allowances.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 29/224

29

3.1 BackgroundNGN has a unique role in the business environment

o the North o England. We are responsible or

the sae, continual delivery o natural gas to users,

transporting the uel over long distances, through

towns and cities, into the homes and businesses

o 2.6m customers. We are largely invisible, even

unrecognised, yet our role is o great importance to

those who rely on us or uninterrupted supplies o

gas or their daily use.

We are a critical element in the region’s

inrastructure and are the primary delivery route

or energy in the North o England. During periods

o peak demand our network is transporting up

to our times as much energy as the electricity

networks in our region.

The energy industry in the UK aces signicant

challenges i the issues o the environment,

sustainability and consumer energy requirements

are to be eectively addressed while maintaining

the historical ocus on reliability, saety and value or

money.

This plan takes ull consideration o the business

environment in which we operate, recognises the

key drivers or change in the short, medium and

longer term and the stern challenges which we ace

at regional and national level.

3.2 Legal and regulatoryframeworkNGN operates in a legislative and regulatory

ramework determined by three elements o

primary legislation: the Gas Act (1986), the

Health and Saety at Work Act (1974) and the

Environmental Protection Act (1990). We operate

under a Gas Transporter’s Licence granted by

Ogem which denes the broad range o licensed

activities and responsibilities and sets out the rules

and standards to which the company must adhere.

This ramework ocuses our obligations on quality

o service to customers, ensures the sae operation

o the network and regulates prices to ensure that

we carry out our activities in an ecient,

non-discriminatory manner.

3.3 RIIOIn 2009, the traditional RPI-X approach to network

price controls was updated with the introduction o

the RIIO principles. This provides a broader toolkit

with which networks and Ogem can address the

uture energy and environmental challenges aced

by the UK. These key principles are ully embeddedin our plan or RIIO-GD1 and beyond.

• Outputs ocused – at the heart o our plan is the

commitment to the ecient delivery o specied

outputs in RIIO-GD1.

• Stakeholder led – outputs, levels o expenditure

and the impact upon customer bills refect the

views expressed by our stakeholders.

• Strong incentives or ecient delivery – theplan is based upon industry leading levels o

eciency and signicant continuing productivity

and service improvements.

• Requirement or innovation – the plan includes

a strategy or innovation to address the key

challenges in RIIO-GD1 and into the uture.

• Ensuring investment is nanceable – the plan

includes a ully justied and nanceable package

that maintains strong investment grade creditratings.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 30/224

30

3.4 Longer term challenges The need or change in the energy industry has

been embraced by the Government and the extent

o the challenge rom climate change is widely

accepted. Legislation was introduced in 2008 to

create a legally binding, long term ramework to cut

greenhouse gas emissions. This means that the UK

cannot continue to produce and consume energy

into the uture as we do currently.

These policy developments raise the question o

what role gas has to play in the uture energy mix.

To help inorm this debate, NGN along with all other

GDNs and National Grid Gas Transmission, via the

Energy Networks Association Gas Futures Group

(ENA GFG), undertook a long-range scenario

based modelling study o the uture utilisation o gas to 2050, and the consequential impacts o

this or gas networks. The study analysed our key

scenarios with each identiying a separate pathway

to delivering the Government’s policy objectives to

cut greenhouse gas emissions by 2020 and urther

by 2050.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 31/224

31

Alongside these issues, international market

developments such as the discovery o large

resources o shale gas, have the potential toundamentally change the economics o the

energy mix in the UK and deliver reductions in

energy costs in the longer term. Additionally, there

are renewed uncertainties about the uture role

o nuclear energy in the UK. Given the level o

uncertainty that exists on all these issues, there

appears to be signicant value in retaining the

option or a ‘high gas’ uture both in the transition

to a low carbon economy and also as part o the

longer term energy mix.

This plan is based upon a core assumption that

gas and the gas distribution networks have a

signicant role to play in the transition to a low

carbon economy and a potentially signicant role

in the energy mix o the uture. Consequently, the

capabilities o the gas distribution networks must

be retained i the benets identied above are to be

delivered.

The key messages rom this analysis are as

detailed below.

• An ongoing role or gas is ully compatible with

achieving the Government’s environmental

objectives.

• Gas could oer a cost-eective solution or a low

carbon transition whilst meeting the signicant

peak heat demand (more than £700bn lower

than electrical revolution over the 2010 to 2050

period).

• All potential pathways to a low carbon uture will

require signicant investment in new technology,

including carbon capture and storage, bio-

methane injection, dual uel and/or district

heating systems.

• Maintaining gas will enhance the diversity o

the energy supply mix and provide necessary

fexibility at times o low renewable output.

Commercialisation o electricity and heat storage technologies

Low/slow High/rapid

C o m m e r c i a l i s a t i o

n o f c a r b o n c a p t u r e a n d s t o r a g e t e c h n o

l o g i e s

High/rapid

Green gas

Transmission-delivered gas 2050: HIGH

•Gas+CarbonCapture&Storage(CCS)•Someunabatedgasforbalancing

Distribution-delivered gas 2050: HIGH

•DualFuelfordomesticheating

•Bio-methanegridinjection

•Districtheating+CCS

•SomeuseofCompressedNaturalGas

(CNG) in transport

Storage solution

Transmission-delivered gas 2050: HIGH•Gas+CCS

•Smallamountofunabatedgas

•Additionalbalancingviaelectricitystorageand

demand side response

Distribution-delivered gas 2050: HIGH

•Heatingandtransportlargelyelectried

•Heatstorageusedtobalanceseasonalheat

Low/slow

Gas versatility

Transmission-delivered gas 2050: LOW

•Renewables/nucleardominate

•Someunabatedgasforbalancing

Distribution-delivered gas 2050: HIGH

•Bio-methaneatmaxpotential

•SomeuseofCNGintransport

Electrical revolution

Transmission-delivered gas 2050: NONE

•Renewables/nucleardominate

•Balancingviaelectricitystorage,exiblenuclear•interconnectionanddemand-sideresponse

Distribution-delivered gas 2050: NONE

•Heatingandtransportlargelyelectried

•Heatstorageusedtobalanceseasonalheat

Figure 3.1: Gas Futures Group scenario analysis

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 32/224

32

3.5 Regional economic outlookDuring 2008/9 and 2009/10 the UK economy

experienced the most severe economic recession

since the 1930s, with six consecutive quarters o

negative GDP growth beore a nal return to growth

in 2010. The economic recovery in the period since

then has been ragile with output alling back during

late 2010. This period o tentative economic recovery

has also been characterised by a period o high

infation, uelled extensively by high energy and

commodity prices which have acted as a signicant

brake on urther recovery as disposable incomes

have allen in real terms.

Changes in national and regional economic

conditions have a direct and sometimes signicant

impact upon key aspects o our activities and thewider gas distribution network. The economic

downturn during 2009 and 2010 led directly to a

signicant reduction in the demand or gas with

throughput on our system alling by around 4%

in 2009 compared to 2008 beore recovering

modestly during 2010. Likewise, applications or

new connections to our network ell sharply during

2008, 2009 and 2010 as the impact o recession

slowed the development o new housing; high

energy prices seemingly deerring decisions toswitch to gas.

At the time o writing, the likely period o transition

rom recession to more sustained economic

growth is still highly uncertain. The Bank o England

projections o GDP growth are very widely spread

and to some degree refect the recent dip in the

economy. They could be viewed as presenting a

not overly optimistic picture in the very short term.

The key economic assumptions underlying this

plan include the ollowing.

• Gross Value Added (GVA) growth or our

network is assumed to remain fat at last year’s

rate (1.49%) or a urther two years as Britainstruggles to recover rom the recession. It is

then anticipated to return to the same three

year economic cycle that has been experienced

with an average rate equal to the long term

non-recessionary average. GVA growth in our

region has been below the average or Britain in

the period 1990 to 2009, with the impact o the

recession being marginally more severe in both

2008 and 2009.

• Gas prices have shown signicant increases

since 2002 or households and eectively rom

1999 in the non-domestic market. These have

been driven by the wholesale gas price, which

has in turn been driven by rising oil prices. Prices

are orecast to maintain 2011 levels (in real terms)

across the plan period.

• Ater a period o relative low increases in the

Retail Price Index (RPI), Consumer Price Index

(CPI) and RPIX (RPI minus mortgage payments)

during the rst three quarters o 2009, all indices

rose sharply in the last quarter o 2009 and

continued to rise during 2010 and into 2011. RPI

in this plan is orecast to remain above 4.5%

during 2011, alling to 3.3% by 2013 and settling

at 2.5% rom 2018 onwards.

Our region has one o the highest levels o uel

poverty in England with approximately 24% (660k)o all households in our region being classed as

uel poor. The current economic climate is likely

to see this rise. In partnership with a number o

parties, we help by providing access to lower cost

gas heating.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 33/224

33

3.6 The demand for gas onNGN’s network

The amount o gas being delivered through NGN’s

network has allen signicantly in recent years. Total

annual demand or gas was 14% lower in 2010/11

when compared to 2005/6. These reductions have

been driven largely by sustained high energy prices

and the economic recession which have stimulated

increased energy eciency and changes in the

patterns o usage o gas.

Peak demand, while estimated to have allen

over the same period, has been more resilient to

the drivers o change in annual throughput. Cold

winters in 2009/10 and 2010/11 in particular have

demonstrated that the relationship between annual

and peak demand is not linear and that periods o

very cold weather will see demand or gas increase

accordingly.

Our orecasts o throughput or the period to 2021

are based upon the likely economic scenario and

take account o the impact o continued high

energy prices and the wider environmental agenda

on the demand or gas on the network. Annual

throughput is orecast to continue to all over the

period as consumers continue to change the wayin which they consume energy, despite relatively

strong growth in underlying economic drivers. This

is shown below.

Figure 3.2: NGN orecast annual throughput Figure 3.3: NGN orecast peak day 1 in 20 demand

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 34/224

34

Our demand orecasts have been derived against

three economic and energy eciency scenarios.

Each represents a valid background against which

to assess uture levels o demand across the

period, taking into consideration the large range o

uture uncertainties that surround key economic

drivers. We have chosen the central scenario asthe basis o our demand orecasts in RIIO-GD1.

These scenarios are set out in Appendix A2.

Annual demand is orecast to all a urther 5%

during the RIIO-GD1 timerame, largely driven by

reductions in the domestic sector as consumers

become more ecient in how they consume

their energy. The industrial and commercial

(I&C) and manuacturing sectors also expect

to see reductions in demand. This is against a

background o nationally increasing demand or

energy over the whole period.

Peak day demand (1:20) is orecast to all by only

3% over the period. Recent history has shown

that demand proles are becoming more ‘peaky’

in nature as consumers respond to economic

conditions and high energy prices. This trend is

orecast to continue over the next 10 years with

peak demand orecasts being more resilient than

average annual demand as consumers reversetheir more rugal behaviour during the periods o

coldest weather.

The investment programme set out within this

plan has been tested directly against the range

o peak demand orecasts outlined above. A key

point to consider is that none o the three scenarios

provides a requirement or any general network

reinorcement to support growth in demand.

However, the plan does refect a requirementor small localised, reinorcements to overcome

specic constraints on the network.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 35/224

35

3.7 Regional factorsOur operating environment contains a range o

geographic, social and commercial actors which

infuence the level, type and costs o activities we

carry out. These ‘regional actors’ can be identied

as those which impact upon NGN in a manner that

is not consistent with other GDNs and must be

addressed when drawing any direct comparisons

within the industry.

These include the ollowing.

• Geography and demographics Our network has the lowest customer density

with the greatest network coverage o all the

GDNs. We are also impacted by having some

o the largest conurbations in the UK on the

periphery o our region, in particular on the east

coast. This results in a requirement to provide a

higher level o resource and acilities to serve the

more remote regions. This imposes additional

operating costs to maintain the our ‘rural’

depots in the network. The NGN region has two

o the UK’s top six conurbations yet 97% o the

region has the lowest population density outside

Scotland and contains our national parks. We

calculate that maintaining higher resource levels

and depots to service these areas is equivalent

to a urther c.£4m per year, impacting our

operating costs.

• West Yorkshire There are unique combinations o actors in this

region, including ‘steel rail’ services (secondary

mains usually ound in back gardens). Pennine

bedrock and the street design o our mill towns

have added a clear premium to mains and

service replacement costs which can be clearlyseen in contractor rates when compared to

the north o our region. This equates to c.£3m

additional annual costs.

• Loss of meterworkMeterwork has been used historically by

the GDNs to oset the standing time o the

emergency response workorce. In 2008, NGN

was not successul in retaining these contractual

arrangements, leading to the stranding o

resource costs o c.£10m annually within the

regulated business. We have reduced these by

more than 60% by 2010/11 to ecient levels.

However NGN still aces c.£4m o recurring

costs annually. No other GDN has yet aced this

issue and can still allocate large elements o cost

rom the regulated business into non-regulated

activities.

Further details on these regional actors can beound in Appendix A18.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 36/224

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 37/224

37

4Innovationstrategy

Innovation allows a company to adapt the way in which it provides its

services, reacting to a changing environment to ensure it continues to

deliver optimal performance. When NGN was created it chose to operate

a unique asset management model, which it is now changing as the

company reacts to the challenges of a new price control period and the

move to a low carbon economy in the UK. This section explains how NGN

has and will continue to use innovation.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 38/224

38

Executive summaryInnovation is the lieblood o a successul

organisation. It delivers the incremental and

sustainable changes in business perormance to

keep the organisation at the leading edge o its

capabilities.

NGN’s industry leading perormance over the last

six years was built upon our innovative approach

to setting the benchmark or ecient, sae and

customer-ocused service delivery. The way in

which we historically operated the business, using

the strategic asset management model, was a rst

in the gas industry. Now we ace the challenges

o moving to a low carbon economy against the

backdrop o a turbulent economic situation, we will

innovate to ensure we continue to manage a cost-ecient and customer-driven business.

Our organisation is evolving to give a clear ocus

on the Total Cost o Ownership (TCO). We are

implementing an integrated business model, taking

an holistic view o asset management to meet

the complex perormance challenges and cost

pressures o the uture. It will be driven by Total

Network Management (TNM) which provides a

deeper approach to asset management. Thiswill drive investment decisions across single and

multiple output measures to inorm expenditure

based upon providing the best value or money.

We will work inclusively with business and industry

partners, our employees and other stakeholders,

to benchmark ourselves against other leading

international businesses and ensure we remain the

most cost ecient, saest and customer ocused

GDN in the UK.

Our new business model and approach to

managing the network are wholly consistent with

the principles o RIIO. We will use innovation as a

tool to research, evaluate and implement new ways

o doing things, sustaining our rontier position

and driving increasing levels o value or our

stakeholders.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 39/224

39

4.1 BackgroundNGN has a strong track record in developing

and implementing targeted innovation. This is a

product o the unique challenges we ace in the

provision o our core services. Innovation has

encompassed corporate, commercial, technical

and process developments which have all delivered

signicant benets to customers and stakeholders

since 2005. This includes delivering the ‘demerger

dividend’ early and generating an 18% reduction in

controllable operating expenditure.

Time Period Pre - 2005 2005 to 2010 2011 to 2013 RIIO-GD1

Key business

challenges

•Day to daymanagement

o the network.

•Step change incommercialisation andeciencies to meetdemerger expectations.

•Disciplined control o demerger cost anddelivery o step changes inoperational perormance.

•Continue to meetstakeholder expectations.

•Continue to driveproductivity and value ormoney.

•Ensure the network cantransition to a low carboneconomy.

•Responding to new andsmarter technology.

•Other sources o gas in thenetwork.

•Potentially changing usagepattern o energy.

Key innovations•PE pipes.

•Insertion.

•Market-tested strategicasset managementmodel underpinned by acommercial asset servicesagreement.

•Partnering with a strongutility provider.

• Total Cost o Ownershipapproach.

•New business model.

•Measurable asset health.

• Total Network Management.

•International benchmarking.

• A variety o technology-ledsolutions.

•Potential new approachesto using smarter data anddistributed sources o gas.

I n n o v a t i o n

National Grid

Transco

Driving commercial value

Total Cost o Ownership

Smarterinvestment...

Figure 4.1: Innovation track record

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 40/224

40

4.2 NGN’s innovation strategy-Total Cost of Ownership (TCO)

Innovation and the ability to respond eectively to

the evolving requirements o our customers and

stakeholders is and will remain, a key element o

the continued success o NGN.

As part o our business model we have a clear

perormance challenge or increased innovation

across the organisation. This perormance

challenge and the delivery o new innovative

solutions will become part o the process by which

we measure the eectiveness o our business, sta

and contracting partners.

A key element in the delivery o this strategy is a

thorough understanding and appreciation o the

range and variety o challenges that NGN as a

business must respond to in the short, medium

and longer term. Summarised below are the key

challenges that we will ace in the RIIO-GD1 period.

These will enable us to identiy the new technology,

commercial arrangements, processes and services

which will be required to address them.

Working in partnership to putinnovation at the heart of ourbusiness, to deliver our stakeholders’expectations in the short, medium andlong term.

The unique strategic asset management

business model which was implemented when

NGN acquired the network in 2005 was itsel a

signicant innovation in the UK’s energy sector.

It was specically targeted at managing the cost

pressures, uncertainties and service obligations

through a period o signicant change ollowingnetwork sales. Additionally, within this perormance

based ramework there existed strong incentive

arrangements to develop innovative responses

to these key challenges. These were a signicant

stimulus or challenging existing practices within the

business.

However, we recognise the signicant challenges

that the wider energy industry in the UK will ace

in the short, medium and long term. We have a

signicant role in ensuring our gas distribution

network can ully play its part in the move to a

low carbon economy. We must also maintain our

ocus on the continuing challenges o improving

overall levels o service, meeting our stakeholders’

expectations and delivering urther improvements

in eciency and productivity.

We also recognise that a step change is required

across the industry and within NGN in the scope

and level o innovation necessary to meet thesechallenges.

The changes we have already made to our

business model, and the approach we are taking

to our management o the network, (which are

described elsewhere in this plan), are clear

indications o how we are proposing to respond to

these challenges as part o our innovation strategy.

This strategy dovetails with NGN’s new approach

o Total Cost o Ownership by having a balancedportolio o projects which are reviewed and tested

prior to potential implementations.

This section sets out NGN’s innovation strategy

and also demonstrates how the use o unding,

research and development, trialling and

implementation, will be employed in RIIO-GD1.

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 41/224

41

These challenges have been identied and

evaluated in partnership with a wide range o

stakeholders, including employees, customers,

contracting partners, suppliers, consumer groups

and local and national government representatives.

It is only by maintaining this level o dialogue

across all our stakeholder groups that we can be

certain that we are ully evaluating the issues and

identiying potential responses to these challenges.

This principle will orm a key element o ourstakeholder engagement strategy across RIIO-GD1.

To meet these challenges we have developed a

new approach: Total Cost o Ownership (TCO).

The TCO approach is at the heart o our innovation

strategy and has our main building blocks,

overlea.

• More ecient delivery o the replacement programme

• Emergency service

• Reduce gas escapes

• Reduce injuries rom our operations

• Comply with saety legislation

• Reduce carbon ootprint

• Reduce use o natural resources

• Facilitate connections o low carbon

sources o gas

• Maintain reliability o network

• Ensure security o supply

• Better investment decisions

• Risk based approach

• Deliver operational eciency

• Respond to changing requirements o the network

• Improve delivery o services

• Remain aware o changing customer and stakeholder

requirements

• Be more responsive to customer and stakeholder

requirements

• Ensure delivery o value or money

• Understand the impact o investment decisions on

customer bills (short and longer term)

• Identiy market developments and requirements o

the gas network

• Ensure the network maintains fexibility to deliver

energy requirements in the long term

• Respond to changing patterns o demand and input

to our system

Innovation

Saety

Environment

Asset & network

management

Customer

service

Value or

money

Future role

or gas

Figure 4.2: NGN’s key strategic challenges RIIO-GD1

7/22/2019 Ngn Business Plan

http://slidepdf.com/reader/full/ngn-business-plan 42/224

42

NGN’s TCO approach has provided the ocus or

our innovation strategy to support the challenges

in RIIO–GD1. This approach embraces the

management and operation o network assets and

drives inormed decisions to deliver in the most

ecient way the required outputs or customersand other stakeholders. TCO delivers an holistic

approach to asset stewardship which is necessary

to meeting the increasingly complex challenges

and cost-pressures GDNs will ace over the next

decade. In particular the business has to deliver:

• better customer service;

• a reduction in saety risks;

• ewer gas leaks and service interruptions;

• less impact on the environment;

• improved sustainability;

• improved asset health;

• urther operating cost eciencies; and

• investment in processes, skills and workorce

renewal.

The remainder o this section describes each

element o the TCO approach.

Figure 4.3: NGN’s innovation strategy – TCO approach

Integrated business modelFully integrated business model that

allows unctions to work together.

Total Network Management A deeper approach to assetmanagement using health indices.

Innovation investment programmeDetailed innovation plans including new ways o working,

new technologies and new processes.

Benchmarking An understanding o best practice

internationally and in other industries.

NGN’s innovation strategy is TCO, which assesses expenditure on the whole assetlife impact across the investment stream to ensure an overall holistic benet tooperations. By balancing our innovation investment across network integrity,customer operations and replacement activities we will ensure the greatest value isobtained.

7/22/2019 Ngn Business Plan