Embed Size (px)

Citation preview

Copyright 2011 IHS Herold Inc. Herold Regional Play Assessment 1

Key Implications

Successful horizontal development of Niobrara oil limited to handful of E&Ps and fields

Early entry and development of the Niobrara introduces risks, as time is needed to delineate the play

Established producers with access to pre-existing seismic and well data, will have an advantage

Well performance to date is variable, and has yet to demonstrate resource play predictability

Despite this variability, some are citing the play’s best wells as indicative of future results

E&Ps anticipate experience will enhance both well performance and predictability

Acreage should be heavily risked, and low-cost entry into large acreage plots is the key to success

E&Ps and investors are growing more optimistic about unlocking the emerging Niobrara horizontal oil play’s

resource potential with the aid of experience and technology. The shale formation’s vast expanse from Wyoming

and Colorado into Nebraska and Kansas makes it possible for even small E&Ps to assemble large, contiguous

leaseholds. The Niobrara is situated at various depths and has diverse rock properties as it spans multiple

basins, making it very risky to generalize about prospectivity at this early stage.

Niobrara Has Not Yet Proven to be a Resource Play

21 March 2011

Sven Del Pozzo, CFA

Source: IHS

Niobrara Acreage Holders

Unrisked* Unrisked

('000)

Net Acres Shares Share Price Basin

DBLE 70,000 11,178 6,262 31.42 $8.32 378% Washakie

WRES 80,000 71,348 1,121 5.61 $4.15 135% Washakie

REXX 45,000 44,312 1,016 5.08 $11.31 45% Denver Julesburg (DJ)

PETD 74,000 23,465 3,154 15.77 $44.66 35% Denver Julesburg (DJ)

KWK 140,000 170,316 822 4.11 $14.07 29% Greater Green River

CRZO 61,000 35,000 1,743 8.71 $33.94 26% Denver Julesburg (DJ)

BBG 90,800 46,876 1,937 9.69 $37.93 26% Wind River

VOG 14,200 52,400 271 1.35 $5.40 25% DJ, Weld Cty.

SSN 14,000 83,300 168 0.84 $3.65 23% DJ, Goshen Cty.

NBL 630,000 175,750 3,585 17.92 $92.63 19% Denver Julesburg (DJ)

APC 1,260,000 496,000 2,540 12.70 $77.06 16% DJ & Powder

CHK 536,000 658,000 815 4.07 $34.00 12% DJ & Powder

QEP 139,000 176,300 788 3.94 $38.91 10% Denver Julesburg (DJ)

GPOR 24,500 44,590 549 2.75 $31.30 9% NW Colorado

MDU 65,000 188,750 344 1.72 $21.68 8% Denver Julesburg (DJ)

EOG 300,000 254,250 1,180 5.90 $108.68 5% Denver Julesburg (DJ)

SGY 10,000 49,000 204 1.02 $27.91 4% Hanna

CLR 72,000 170,400 423 2.11 $66.81 3% Denver Julesburg (DJ)

MRO 170,000 710,280 239 1.20 $49.54 2% Denver Julesburg (DJ)

WLL 73,000 236,230 309 1.55 $67.29 2% DJ, Carbon Cty.

CNOOC 264,000 44,669,200 6 0.03 $2.19 1% DJ & Powder

ECA 40,000 736,250 54 0.27 $33.49 1% Denver Julesburg (DJ)

*Valued at $5,000/acre, essentially representing CNOOC-CHK Niobrara/Frontier Deal Value or NPV@10% & $90 oil of well with 600 b/d

24HR IP tracking EOG's "Jake" well production profile (see bottom of p. 8). Does not Discount for Geological Risk or Pace of Development.

Acres per

MM Shares

Niobrara Value,

$/Share

as % of

Share Price

Copyright 2011 IHS Herold Inc. Herold Regional Play Assessment 2

0

100

200

300

400

500

600

CORE BAKKEN SINCE 2009 ALL NIOBRARA Since 2008 Top 5 Niobrara

Bb

l of O

il P

er

Da

y

Horizontal Niobrara Oil Declines Faster (Outside of Silo) Than Core Bakken

60 Day Avg. 180 Day Avg. 365 Day Avg. Avg. in Month 6 Avg. in Month 12

0

150

300

450

600

750

JAK

E

(2

4-O

ct-0

9)

ELM

ER

(23-M

ar-

10)

PO

LL R

ED

(2

5-M

ar-

10)

GA

RD

EN

CR

EEK 6

-11H

(30-J

un-1

0)

CR

ITTER

CR

EEK

4-0

9H

(7-J

ul-

10)

Lo

ng

horn

B 3

-36H

(2-S

ep

-10

Cri

tter C

reek

6-1

2H

(8-S

ep

-10)

Cri

tter C

reek

08-1

4H

(10-O

ct-1

0)

Cri

tter C

reek

13-7

H

(24-O

ct-1

0)

Gard

en C

reek

09-1

6H

(25-O

ct-1

0)

Cri

tter C

reek

09-1

5H

(28-O

ct-1

0)

Cri

tter C

reek

1-0

2H

(13-N

ov-1

0)

Els

ie 7

-34H

*

(6-D

ec-

10)

Cri

tter C

reek

17-2

1H

(26-D

ec-

10)

bb

ls o

il/d

EOG-Hereford Ranch-First 30 Days vs. Latest Month

Oldest to Newest Completions (Oct-09 to Dec-10)

Latest 30 days First 30 days

Note: () denotes completion date

Critter Creek 2-03H confidential status

*Elsie may be confidential status

Oil resource play optimism is likely driven by repeated success in discovering new, US gas resource plays.

Extrapolating success with oil resource plays from gas resource plays may prove an improper assumption. Oil

flows with greater difficulty than gas, and often needs artificial lift to produce, raising operating costs. EOG

Resources (EOG) has recently alluded to this, citing higher downtime in oil wells than in gas wells. Neither do

we have long-term production histories for oilier, “liquids-rich” plays, so the larger the estimated ultimate

recovery (EUR) per well, the riskier the estimate, since it likely depends on lengthy well-life. For our analysis,

we have limited our investment return analysis to a 20-year well life, which may seem short compared with

some E&P estimates, but captures the lion’s share of a well’s present value.

Some of the Niobrara’s positive outlook may also be tied to the success of the Bakken/Three Forks play. We

stress that definitive conclusions can’t be made at this early stage, as fewer than 20 modern horizontal Niobrara

wells (D-J & North Park Basin) have 365 days of IHS production history, of which less than 10 have a

meaningful oil cut. Initial 180 and 365 day production rates for a select handful of the Niobrara’s best

horizontal, oil-weighted wells averaged about 95% and 70% (respectively) of the median Bakken well in the

core of the play highlighting faster decline rates in the Niobrara (see page 11 for production profiles).

The median Bakken horizontal well completed since 2009 in the core of the play averaged about 230 b/d of oil

in its sixth month online. Two modern Niobrara horizontal wells matched or bested that, with the remaining 10

wells ranging between 10 and 190 b/d of oil. In their sixth month, five of these wells produced 70 b/d or less of

oil; three produced between 100-125 b/d, and the remaining two produced about 185 b/d. The Bakken’s

production is also predictable over a wide area, compared with Niobrara well performance that still varies

considerably, even in the same field.

Source: IHS

Source: IHS

Copyright 2011 IHS Herold Inc. Herold Regional Play Assessment 3

The Niobrara’s strong, early-month IPs that decline relatively rapidly, beg the questions of whether it is mainly

induced fractures that contribute to IP rates, and whether the horizontal oil play can evolve into a resource play

like the Bakken. In the large, horizontally developed Niobrara Silo field, notice that early-month IP rates have

little if any correlation to EUR (see page 12, Silo chart). The answer to the “resource play debate” depends upon

the potential contribution of matrix porosity to production, which if present would increase production and

reserves, slow decline rates, and enhance the possibility of down-spacing from a typical 640 acres. E&Ps are

confident early on, but if matrix contribution is not material, then successful Niobrara development will continue

to be limited to fractured and faulted fields.

Most E&Ps are in the early stages of shooting and analyzing 3D seismic to better identify faulting and fracturing.

When establishing leaseholds, E&Ps have consulted existing vertical well data, formation thickness, and

resistivity, among other factors, and may target anticlinal structures in the hope of encountering natural

fractures. We believe patience is a virtue for investors seeking profit as this early-stage play evolves. Operators

with the most experience and data to consult will have a leg up on the competition and produce more consistent

results earlier in the play’s evolution.

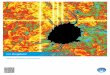

DJ Basin: To date, successful horizontal development of Niobrara oil has mainly been limited to the DJ Basin in

several naturally fractured fields east and north of Denver, Colorado. These include Wattenberg, just north of

Denver in southern Weld County, Colorado; Silo (see page 4, yellow well spots with second-month average oil

production enumerated) in Laramie County, southeastern Wyoming; and Hereford Ranch (see page 4, lime

green well spots), about 30 miles south of Silo in northern Weld County, on Wyoming’s southeastern border.

The Niobrara is situated at 7,500-8,800 feet of depth at Silo, compared with 7,000-7,500 feet deep at Hereford

Ranch, where the Jake and the Critter Creek 4-09H and 9-15H wells were drilled. These are some of the best

wells in the field with a reliable production history.

Silo was horizontally developed in the early- to mid-1990s, mainly by Union Pacific Resources (acquired by

Anadarko) before the advent of multistage hydraulic fracturing. Many Silo wells were noteworthy for sustained

production rates over several years. SM Energy and Rex Energy (REXX) are in the early stages of drilling

modern wells at Silo. A few modern Silo wells have been reported thus far with mixed results, and time will tell

how modern completion technique can affect a partially depleted field. E&Ps have also mentioned geological

similarities between Silo and southeastern Wyoming / northeastern Colorado, but at this early stage, we would

exercise caution in drawing parallels with Silo to more recently developed fields, as it seems somewhat unique.

About one-third of Silo’s horizontal wells sustained 100-300 bo/d production rates for over two years, compared

with 100-200 bo/d rates sustained for six months to a year for the best oil-weighted modern horizontal wells in

the Niobrara play, most of which are EOG’s at Hereford Ranch.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

bb

l o

f o

il

First Year Cumulative Oil Production: Silo Field Seems Unique

Silo Niobrara (Ex-Silo) EOG CHK (Spillman Draw Deep)

Source: IHS

Copyright 2011 IHS Herold Inc. Herold Regional Play Assessment 4

Source: IHS

Southern DJ & North Park Basin Niobrara Completions with 2nd Month Average Oil Production

Copyright 2011 IHS Herold Inc. Herold Regional Play Assessment 5

EOG’s early success at Hereford Ranch late in 2009 likely spurred a nearby land grab by E&Ps, including Carrizo

Oil and Gas (CRZO), REXX, Continental Resources (CLR), Whiting Petroleum (WLL) and QEP Resources (QEP).

Continental already has experience developing the Niobrara at the Silo field, and will be drilling the play’s first

long lateral on 1,280-acre spacing as it transfers its knowledge as one of the Bakken’s most efficient operators

to the Niobrara in northeast Colorado. Notwithstanding what appears to be a lengthening trend of variability in

well performance at Hereford Ranch based on recent one-month average IP rates (see page 2, chart), EOG

recently expressed increasing confidence about the possibility of matrix porosity contributing to production.

EOG is experimenting with restricted choke sizes to enhance EUR (Elsie 7- 34H and Critter Creek 13-17H),

which could make early-month IP rates even less meaningful, and future decline rates and EUR more relevant,

to valuation.

Noble, another premier Rockies operator, is focusing on its Wattenberg leasehold (see page 5, sky blue well

spots), and suggested possible matrix contributions based on the few modern wells it has drilled north of

Wattenberg. Potential contribution from matrix porosity would increase reserves per well and expand the play

beyond naturally fractured fields and convert it into a true resource play. However, widespread matrix

contribution is far from proven, despite some early optimism in the industry.

EOG is also responsible for the only horizontally developed Niobrara oil field to date west of the Front Range,

developed in 2007-2008, in the North Park Basin in northwestern Colorado, where the Niobrara is also naturally

fractured and situated at approximately 7,000 feet. We would imagine such fields to be somewhat unique,

considering the geological complexity of the region.

About 12 miles to the southeast of Chugwater, Wyoming, is EOG’s next region of Niobrara exploration, dubbed Silvertip. This is in the northern DJ Basin (north of Silo), where the northern border of Laramie County meets the southern border of Wyoming’s Platte and Goshen counties. Results of EOG’s first well, Silvertip 5-34H in Goshen County, are highly anticipated, as EOG has been actively permitting and drilling in the area. In this

region, logs indicate the Niobrara’s depth is similar to that at Silo.

Wattenberg Field, Southern Weld County, CO:

The Niobrara is a shallower secondary target of

vertical gas wells in the field that primarily targeted

the deeper J-sand and Codell pay zones. Based only

on publicly stated IP rates, Noble Energy (NBL) seems

to benefit greatly from having extensive vertical well

and seismic data to consult when horizontally exploring

and developing the Niobrara at Wattenberg, which may

help explain reportedly more consistent results. NBL

has indicated minimal interference between vertical and

horizontal wells, which bodes well for down-spacing.

Given the variability in well performance witnessed to

date in different parts of the play, NBL’s development

approach resonates with us. The company states that it

will first focus on exploring the Niobrara within the

existing Wattenberg field area, which it understands

best and where it has infrastructure, before focusing on

delineating its extensive leaseholdin northeastern Weld

County, Colorado, and in Laramie and Goshen County,

Wyoming (see acreage, page 7). NBL’s announced one-

month average Niobrara IP rates seem to be the most

consistent thus far in the play, with 20 horizontal wells

averaging over 500 boe/d. It also says its Niobrara

liquids cut rises from 45%-75% when moving from the

central core of the field to its oiler, cooler, periphery.

This higher gas cut may help to lift the oil, lowering

operating costs, versus a90% oil cut at Silo and Hereford Ranch. NBL is in the early stages of developing

acreage to the north (Grover area) and northeast of Wattenberg, where it has had mixed results on several

wells. NBL estimates 1.7 billion Boe of unrisked resource potential on its 830,000 net acres in the play. That

Noble Wattenberg Field Acreage

Source: Noble

Copyright 2011 IHS Herold Inc. Herold Regional Play Assessment 6

appears more conservative than Chesapeake Energy’s (CHK) estimates on its acreage, which is more heavily

weighted to the earlier stage Powder River Basin. Anadarko (APC) also has a large position at Wattenberg.

Southern Powder River Basin: In addition to DJ

Basin Niobrara, where CHK has not yet publicly

announced results, and moving north from Silo, CHK

is developing the Southern Powder River Basin

Niobrara, which is an even earlier-stage play that is

geologically distinct, much deeper (12,500 feet), less

porous, and under greater pressure than in the DJ. CHK has publicized one definitive success thus far, Spillman

Draw Deep (87% oil), completed in mid-October 2009 in Converse County, Wyoming. It is one of the best wells

in the play and of great interest because it suggests a northern extension of the Niobrara play, but we await a

number of follow-up wells. It averaged about 470 b/d of oil production in its first month of substantial oil

production, and after a year declined about 75% to roughly 120 b/d. In nearly its first year online, production

averaged about 195 b/d of oil. CHK has also reported some results of the Spillman Draw Deep Unit State 16-

1H, drilled to 12,600-foot vertical depth with nearly a 5,000-foot lateral, with a publicly stated IP of about 650

bbl of oil over an undetermined period. CHK has reported 3 billion boe of resource potential on its 535,000 net

acres in the Niobrara after selling down its interest to CNOOC, which appears to be a more aggressive estimate

than NBL’s. CHK has publicly stated that it operates over 16 producing wells in the DJ and Powder River Basins

that have tested at IP rates of up to 1,000 bbl of oil and 3.0 MMcf of natural gas per day, but we can’t specify

the testing parameters.

Chesapeake Niobrara Acreage Noble Niobrara Acreage

Source: Noble

Source: Chesapeake

Copyright 2011 IHS Herold Inc. Herold Regional Play Assessment 7

Wind River Basin: Bill Barret Corp. (BBG) has a large legacy Niobrara acreage position in the middle of

Wyoming with no well data to report thus far, and did mention some geological similarities between the Wind

River and southern Powder River Basin Niobrara, with Niobrara depths varying from 4,000 to 14,000 feet. BBG

has 3D seismic to consult and its first well will be completed in the summer of 2011.

Washakie Basin: Located in the middle of Wyoming’s southern border with Colorado, due south of the Wind

River Basin, Anadarko Petroleum (APC), and minnows Warren Resources (WRES) and Double Eagle Petroleum

(DBLE) all develop Atlantic Rim coalbed methane, which may help secure development rights to the deep

Niobrara.

Valuation: IHS data suggests publicized industry Niobrara-type curves and EURs mimic EOG’s Jake 2-01H well

completed in late October 2009 at Hereford Ranch, whose early success incited the region’s land grab. The

“Jake” well is one of the field’s best oil wells to date, along with Critter Creek 4-09H and 9-15H (see page 2).

We caution against using the Jake well as a type-well, because it is one of the best wells, not an average well.

Results are highly variable even within the Hereford Ranch field, where the Jake well was drilled. We ran an oil

price scenario analysis around the Jake well, purposely selected to reflect a best-case outcome ( see results

tabulated on page 8). We conclude that NPV-based acreage values can conceivably attain non-core Bakken-like

metrics on a one-off basis, but until the Niobrara play can demonstrate the predictability of a resource play, the

industry and investors alike must risk acreage heavily, ensuring cheap entry into large leaseholds, relative to

unrisked NPV-based values. Similarly, if an E&P’s leasehold is relatively small, and it is a newcomer to the area,

the chance of discovering new Niobrara fields is more remote, based on the data we have analyzed to date. Our

modeling applies Jake well percentage declines to initial 24-hour production rates, concluding that at $90 oil, a

minimum 24-hour initial flow rate of 375 bo/d is needed to have NPVat a 10% break-even. In its first calendar

month online, the Jake well averaged 680 bo/d. Note that for investment performance to be attractive, even at

$80 oil, the 24-hour IP rate needs to be at least 500 bo/d. Inputs: Completed Well Cost (CWC): $4.2MM (top of the industry guidance range)

Lifting Costs per BOE: $13.00/boe (water disposal $3-$4/bbl)

Severance tax: 13%

Royalty: 18%

Oil/Gas Split: 90% oil / 10% gas

Differentials: Oil ($10); Gas ($1.50) or $3.10 flat at well-head

Gross EUR: 300,000 Boe at $90/bbl oil reference price ($80 at well-head) with 24HR 800 boe/d IP, 20 Year life

Decline Rates: Shown Beneath Table

Source: IHS

Northern DJ Niobrara Completions with 2nd Month Average Oil Production

Copyright 2011 IHS Herold Inc. Herold Regional Play Assessment 8

Comparing our best case investment metrics with M&A deal values, CNOOC’s acquisition of CHK’s acreage in

both the Powder River Basin and the D-J Basin looks like it was overly aggressive, as does CHK’s acquisition of

acreage from Samson Oil (albeit a much smaller deal), both seen in the table on the next page. CNOOC’s near-

$4,750/acre deal value closely corresponds to the NPV of a well drilled on 640-acre spacing, with a 700 boe/d,

24-hour IP rate at $90 oil, without even considering further deductions to NPV for lead times to full

development of acquired acreage, geological or execution risk. CNOOC entered the play early, but could have

paid up later, for better delineated acreage tracts. But we would note similarly aggressive investment decisions

generally being made by other Asian buyers. ITOCHU Corp. acquired 22,000 net DJ Niobrara acres from MDU

Resources for an undisclosed price late in 2010.

Based on results to date, and without the advent of down-spacing that the industry thinks likely, CNOOC did not

add value for shareholders in this deal, while CHK did.

Sven Del Pozzo, CFA [email protected]

IRR $50 Oil $60 Oil $70 Oil $80 Oil $90 Oil $100 Oil $110 Oil $120 Oil $130 Oil

24 Hour IP Rate, b/d oil

800 24% 39% 55% 71% 88% 106% 124% 142% 160%

700 15% 27% 40% 54% 69% 84% 99% 114% 130%

600 6% 16% 27% 38% 50% 62% 75% 87% 101%

500 -9% 3% 12% 22% 31% 41% 51% 62% 72%

400 NM -12% -2% 6% 14% 21% 29% 37% 45%

NPV@10%, $ '000s

800 1,188 2,378 3,569 4,759 5,950 7,140 8,331 9,521 10,712

700 408 1,450 2,491 3,533 4,575 5,617 6,658 7,700 8,742

600 (368) 521 1,414 2,307 3,200 4,093 4,986 5,879 6,772

500 (1,295) (565) 174 920 1,670 2,422 3,175 3,927 4,680

400 (2,040) (1,473) (893) (305) 288 885 1,484 2,086 2,688

Payout Period, Quarters

800 9 6 4 3 3 2 2 1 1

700 13 8 6 4 3 3 2 2 2

600 25 12 8 6 5 4 3 3 2

500 160 31 14 9 7 5 4 4 3

400 160 160 160 22 13 9 7 6 5

NPV, $/Acre (640s)

800 $1,856 $3,716 $5,576 $7,436 $9,297 $11,157 $13,017 $14,877 $16,738

700 $638 $2,265 $3,893 $5,521 $7,148 $8,776 $10,404 $12,031 $13,659

600 -$575 $815 $2,210 $3,605 $5,000 $6,395 $7,790 $9,186 $10,581

500 -$2,023 -$883 $273 $1,438 $2,609 $3,785 $4,961 $6,136 $7,312

400 -$3,187 -$2,302 -$1,396 -$477 $450 $1,383 $2,319 $3,259 $4,200

Sum of 2 Yrs of Cash Flow / Completed Well Cost

800 0.9x 1.1x 1.3x 1.5x 1.7x 1.9x 2.1x 2.3x 2.5x

700 0.8x 1.0x 1.1x 1.3x 1.5x 1.6x 1.8x 2.0x 2.1x

600 0.7x 0.8x 1.0x 1.1x 1.3x 1.4x 1.5x 1.7x 1.8x

500 0.6x 0.7x 0.8x 0.9x 1.0x 1.2x 1.3x 1.4x 1.5x

400 0.4x 0.5x 0.6x 0.7x 0.8x 0.9x 1.0x 1.1x 1.2x

YR 1 YR 2 YR 3 YR 4 YR 5 YR 6 YR 7 YR 8 YR 9

Decline Rate from 24 HR IP 81% 37% 37% 27% 18% 14% 10% 8% 8%

Niobrara Shale: Jake Well (Horizontal Well, Weld County, CO, Hereford Ranch Field)

Copyright 2011 IHS Herold Inc. Herold Regional Play Assessment 9

Niobrara Shale Transactions

ANNC'D

DATE BUYERS SELLERS

DEAL

LEVEL

Total

Transact.

Value

US$MM

KEY

CHARACTER

ACREAGE

VALUE

US$MM

Net

Undevel.

Acreage US$/Acre

Undevel.

Acreage

Asset

Value KEY ASSETS PRIMARY LOCATIONS

PRIMARY

BASINS

DEAL

TYPE

WTI

SPOT

DAY

PRIOR

ANNC'D

US$

NYMEX

OIL 12

MO.

STRIP

DAY

PRIOR

ANNC'D

US$

HENRY

HUB

GAS

SPOT

DAY

PRIOR

ANNC'D

US$

NYMEX

GAS 12

MO.

STRIP

DAY

PRIOR

ANNC'D

US$

1-Mar-11 Recovery

Energy

Wapiti Oil &

Gas

Asset $12.3 Oil Shale $12.3 8,060 $1,526.05

31-Jan-11 CNOOC

Limited

Chesapeake Asset $1,267.0 Oil Shale $1,267.0 266,400 $4,756.01 1,267.0 266,400 net

acres in

Niobrara

shale

focused

project

Niobrara Shale (U.S.)

U.S.-Rcky Mtns

Niobrara

Shale (U.S.)

Acquis. $89.34 $95.246 $4.29 $4.611

26-Jan-11 Halliburton Samson Oil

Undiscl.

private co.

Asset $9.2 Oil Shale $9.2 2,819 $3,275.00 9.2 25% stake

in farm-in

area

(2,819 net

acres)

Denver-Julesburg (U.S.)

Wyoming

U.S.-Rcky Mtns

Niobrara Shale (U.S.)

Denver-

Julesburg

(U.S.)

Niobrara

Shale (U.S.)

Farm In $85.14 $91.431 $4.45 $4.691

30-Jun-10 Rex Energy

Corp

Undiscl.

private co.

Asset $18.7 Oil Shale $18.7 18,700 $1,000.00 18.7 Niobrara

Shale

acreage

Denver-Julesburg (U.S.)

Laramie County (WY)

Wyoming

Niobrara Shale (U.S.)

U.S.-Rcky Mtns

Niobrara

Shale (U.S.)

Denver-

Julesburg

(U.S.)

Acquis. $75.94 $78.107 $4.68 $5.054

28-Jun-10 Voyager Oil

& Gas

Slawson

Exploration

Asset $7.5 Oil Shale $7.5 24,000 $312.50 7.5 50%

working

interest in

48,000-acre

block

Denver-Julesburg (U.S.)

Weld County (CO)

Colorado

U.S.-Rcky Mtns

Niobrara Shale (U.S.)

Denver-

Julesburg

(U.S.)

Niobrara

Shale (U.S.)

Acquis. $78.61 $81.257 $4.84 $5.296

25-Jun-10 Chesapeake Samson Oil

& Gas Ltd

Asset $73.7 Oil Shale $73.7 23,766 $3,099.93 73.7 23,766

acres in

Goshen

County

Project

Wyoming

U.S.-Rcky Mtns

Niobrara Shale (U.S.)

Niobrara

Shale (U.S.)

Acquis. $76.16 $78.835 $4.90 $5.213

13-May-10 Gulfport

Energy

Undisclosed

private

Asset $7.8 Oil Shale $7.8 24,468 $316.74 Niobrara

Shale assets

Colorado

Niobrara Shale (U.S.)

U.S.- Rcky Mtns

Niobrara

Shale (U.S.)

Acquis. $75.65 $84.244 $4.17 $5.079

26-Feb-10 Chesapeake American

O&G

North Finn

Asset $49.4 Oil Shale $49.4 53,000 $932.79 49.4 Fetter and

Krejci

projects

Powder River (U.S.)

Wyoming

U.S.-Rcky Mtns

Niobrara Shale (U.S.)

Powder

River (U.S.)

Niobrara

Shale (U.S.)

Acquis. $77.92 $80.019 $4.84 $5.363

Totals $1,396.2 368,213 $3,791.70

Copyright 2011 IHS Herold Inc. Herold Regional Play Assessment 10

0

100

200

300

400

500

EO

G

EO

G

EO

G

EO

G

CH

K

EO

G

EO

G

EO

G

NB

L

EO

G

NB

L

NB

L

EO

G

APC

(K

MG

)

EO

G

East R

es.

EO

G

EC

A

No

rth F

inn

EC

A

EC

A

EC

A

APC

(H

WL)

bb

l/d

First 180 Days Average Oil Production Daily AverageAll Niobrara Horizontals Since '07 w/180 Days History Outside of Silo

0

50

100

150

200

250

300

EO

G

CH

K

EO

G

EO

G

EO

G

EO

G

NB

L

APC

(K

MG

)

EC

A

EC

A

APC

(H

WL)

EC

A

EC

A

EC

A

Ro

sew

ood

EP

EP

bb

l/d

First 365 Days Oil Production Daily AverageAll Niobrara Horizontals Since '07 w/365 Days of History Outside of Silo Field

Source: IHS

Source: IHS

0

100

200

300

400

500

600

700

800

900

EO

G

EO

G

EO

G

EO

G

EO

G

EO

G

EO

G

EO

G

EO

G

NB

L

EO

G

EO

G

CH

K

EO

G

EO

G

EO

G

EO

G

NB

L

NB

L

EO

G

EO

G

EO

G

EO

G

APC

(K

MG

)

EO

G

EO

G

EA

ST R

es.

EC

A

No

rth F

inn

WLL

EC

A

APC

(H

WL)

EC

A

bb

l/d

First 60 Day Daily Avg. Oil ProductionAll Niobrara Horizontals Since '07 w/60 Days of History Outside of Silo

Source: IHS

Copyright 2011 IHS Herold Inc. Herold Regional Play Assessment 11

0

100

200

300

400

500

600

2 Mo. 3 Mo. 4 Mo. 5 Mo. 6 Mo. 7 Mo. 8 Mo. 9 Mo. 10 Mo. 11 Mo. 12 Mo. 13 Mo. 14 Mo. 15 Mo. 16 Mo. 17 Mo.

bb

l/d

ay o

nlin

e

Daily Oil Production: Only a Handful of Outstanding Modern Niobrara Oil Wells

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

0 100 200 300 400 500 600 700 800 900 1000

4 Y

ea

r C

um

ula

tive

Pro

du

cti

on

, bb

l of O

il

Monthly Average IP Rate, bbl of Oil

Silo Field-80 Horizontals - Early IP Rates Mean Little to Reserves

Source: IHS

Source: IHS

Copyright 2011 IHS Herold Inc. Herold Regional Play Assessment 12

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

0% 20% 40% 60% 80% 100% 120%

Cu

mu

lati

ve

bo

e

% Oil

Niobrara Horiz. Wells-Cumulative BOE vs. % Oil

The analyst that prepared this report has a long position in the securities of Stone Energy Corporation mentioned in this report. This analyst is contractually prohibited from purchasing or selling the securities of this company during the blackout period implemented by IHS Herold for this type of report.

The research analysts who prepared this report certify that the views expressed herein accurately reflect their professional opinions, are consistent with established Herold methodologies and standards and that no part of their compensation was, is or will be directly or indirectly related to specific views contained in this report. Copyright © 2011 IHS Herold Inc. All rights reserved. Herold Regional Play Assessment is published by IHS Herold Inc., 200 Connecticut Avenue, Suite 3A, Norwalk, CT 06854, USA for the exclusive use of IHS Herold clients. Reproduction of this report, even for internal distribution, is strictly prohibited. The information contained herein has been obtained from sources believed to be reliable, but IHS Herold does not guarantee their accuracy or completeness. No information or opinions contained herein constitutes a representation or solicitation for the purchase of any securities of the companies mentioned herein. From time to time, IHS Herold and/or its officers and employees may have long or short positions in the securities mentioned herein or during the past year may have transacted in securities of the companies mentioned.

Source: IHS