Embed Size (px)

Citation preview

DBS Group Research • October 2015DBS Asian Insights16n

um

ber

SECTOR BRIEFING

E-Commerce In AsiaNew Retail Strategy to

Counter Digital Disruption

DBS Asian Insights SECTOR BRIEFING 1602

E-Commerce In Asia New Retail Strategy to Counter Digital DisruptionThematic co-ordinator

Sachin MITTAL +65 6682 3699 [email protected]

Analysts

Carol WU +852 2863 8841 [email protected]

Mavis HUI +852 2863 8879 [email protected]

Andy SIM CFA +65 6682 3718 [email protected]

Derek TAN +65 6682 3716 [email protected]

Jeff YAU CFA +852 2820 4912 [email protected]

Danielle WANG CFA +852 2820 4915 [email protected]

Mervin SONG CFA +65 6682 3715 [email protected]

Alfie YEO +65 6682 3717 [email protected]

Rachael TAN +65 6682 3713 [email protected]

Steve CHOW +852 2820 4611 [email protected]

Mark LI +852 2971 1935 [email protected]

Production and additional research by:Asian Insights Office • DBS Group Research

go.dbs.com/research @dbsinsights [email protected]

Chien Yen Goh Editor in ChiefGeraldine Tan EditorMartin Tacchi Art Director

DBS Asian Insights SECTOR BRIEFING 16

03

0405

13

17

Introduction

O2O Readiness in China and the US

Battlefield 1: Company Website/E-Shop

Battlefield 2: O2O Integration

Battlefield 3: Mobile Apps

Impact of O2O on Commercial Property Value and Management

China

Hong Kong

Singapore

Conclusion

Introduction -commerce is gaining momentum in Asia, albeit at different paces and under different circumstances in each market. One thing that is true across all markets is the fact that online commerce is adversely affecting sales in physical stores. This not only has an impact on revenues, but can also disrupt the way commercial

property is valued and managed.

We have identified three key strategies for traditional retailers and commercial property managers to mitigate the negative impact of e-commerce:

Raise exposure to segments that are less likely to be sold or bought online: Food & beverage, entertainment, lifestyle, and luxury.

Implement online-to-offline (O2O) offerings in key shopping areas to help retailers raise their offline sales.

Focus on large malls in strategic locations where events and flagship stores can be hosted.

Of these three strategies, the O2O approach seems to us the most likely to lead to durable and viable synergies between traditional retailers and online marketplaces. By directing online customers to offline stores, O2O combines the ease and traceability of online payments for customers with the guarantee of offline foot traffic and purchases for merchants.

In Asia, O2O offerings are still at a nascent stage of development, which is precisely why an early adoption of successful practices can help overcome some of the most pressing challenges brought on by a disruptive digital environment. This report examines some of these challenges and explores the many potential opportunities created by a sound, forward-thinking O2O strategy.

E

DBS Asian Insights SECTOR BRIEFING 1604

DBS Asian Insights SECTOR BRIEFING 16

05

O2O Readiness in China and the USnline-to-offline commerce (O2O) is a means to direct online users to offline physical stores. With O2O, the customer can (1) buy products from the shop after conducting online research; (2) pay online and collect the products from the shop to save on delivery charges; and (3) find out-of-stock products that

may not be displayed or marketed in the physical store.

Macy’s, the largest department store operator in the US in terms of sales, has seen a big improvement in online sales as well as same-store performance after introducing O2O retailing. Online sales have grown to 14% of total revenues, from 4% in 2011. Same-store sales have grown from 1.9% to 5.3% over the past three years, while Macy’s peers have seen it decline during the same period.

From a sales and marketing point of view, O2O has many advantages:

Higher impulse sales than online retailers. When a customer receives a product delivery at home, he or she is unlikely to buy anything else. However, when a product is collected from the shop, the customer also comes across other products and promotions and is likely to buy other associated products.

Lower discounts than pure brick-and-mortar retailers. In brick-and-mortar retailing, a product that is difficult to sell in a particular store in the region is sold via heavy discounting. An O2O approach allows the retailer to sell the product to other stores in different regions at the full price.

Better brand building than online retailers. Brick-and-mortar stores in town centres and expensive malls provide high visibility and act as custodians of the brand.

The main challenges that come from O2O are related to practical and logistical obstacles: Large investments are required to integrate the in-store and online inventories of an entire retail chain. Retailers must also be able to build a nimble fleet of smaller vans carrying items from store to store on the same day. This is quite different from the conventional fleet of a few large trucks with fixed delivery points and schedules.

We have compared various e-commerce and O2O initiatives, including online sites, mobile apps, online-offline integration and marketing strategies of some Chinese operators with selected overseas retailers. Our findings suggest that China is significantly lagging behind in e-commerce and O2O development. In our view, Chinese retailers could take at least one to two years to more fully realise their O2O potential before benefitting from it.

Most retailers in China including department stores, hypermarkets, and supermarkets, and those in the luxury segment still see limited or no contribution from e-commerce and O2O despite robust growth potential. One key reason is that retailers have been

O

China is significantly

lagging behind in e-commerce

and O2O development

DBS Asian Insights SECTOR BRIEFING 1606

too reliant on virtual marketplaces. There is also a lack of specialised talent currently available in China to best implement multi-dimensional e-commerce and O2O solutions. Another obstacle may be the inadequate amount of merchandise suitable or available for online sales, especially in the case of department stores, shopping malls and grocery retail formats.

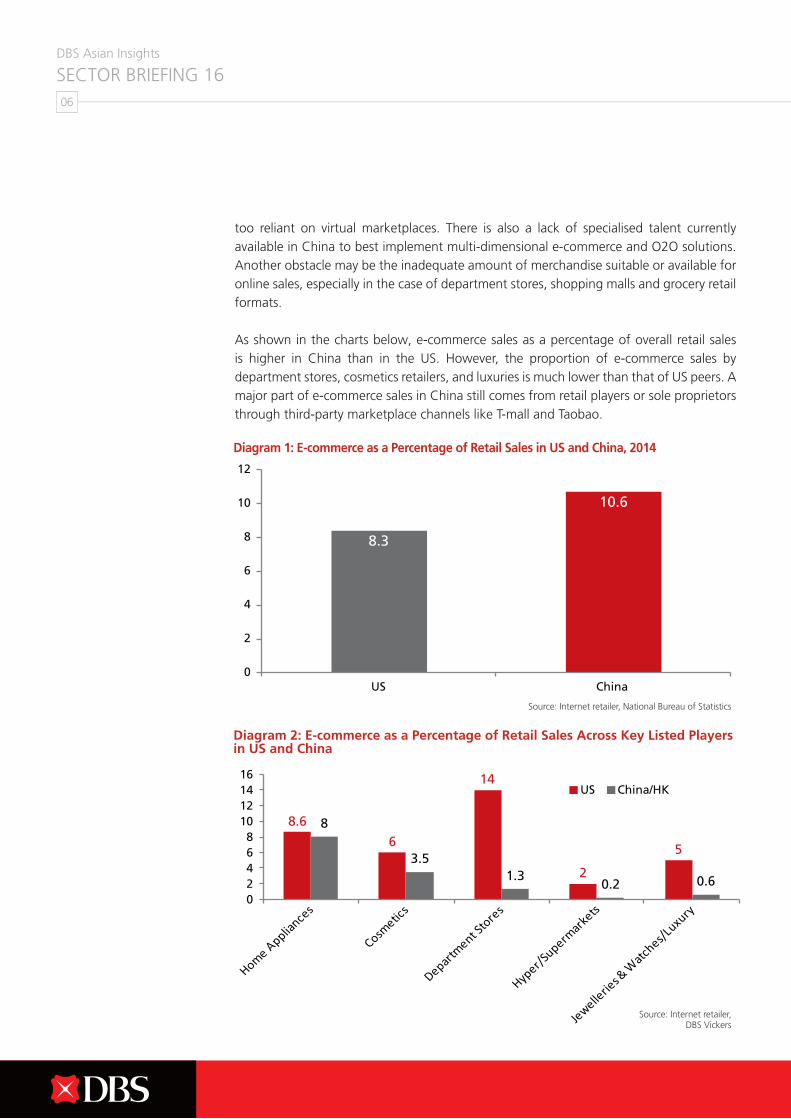

As shown in the charts below, e-commerce sales as a percentage of overall retail sales is higher in China than in the US. However, the proportion of e-commerce sales by department stores, cosmetics retailers, and luxuries is much lower than that of US peers. A major part of e-commerce sales in China still comes from retail players or sole proprietors through third-party marketplace channels like T-mall and Taobao.

Source: Internet retailer, National Bureau of Statistics

Source: Internet retailer, DBS Vickers

Diagram 1: E-commerce as a Percentage of Retail Sales in US and China, 2014

Diagram 2: E-commerce as a Percentage of Retail Sales Across Key Listed Players in US and China

DBS Asian Insights SECTOR BRIEFING 16

07

While Chinese online spending mainly targets low-end products, a China Internet Network Information Centre survey states that, in 2013, online buyers in China were the most active in the apparel and footwear segment. Other popular segments for e-commerce include digital (computer, communication, and consumer electronics) products, as well as handbags and luggage. On the other hand, e-commerce demand for luxury items has been unnoticeable.

Retail stores in tier-3 or lower-tier cities in China do not have well-developed retail infrastructure. As such, people in tier-3 cities go online to buy a wide range of products and brands that are unavailable locally. The E-commerce Index across the top 100 cities in China reached 15.4 on average in 2013, lower than the average of 17.4 across the top 100 counties in China.

By cross-referencing the index level in Jiangsu and Zhejiang provinces, the e-commerce indices of their capital cities (i.e. Nanjing and Hangzhou, respectively) were also lower than selected counties in their regions. This could suggest that the lower-tier cities generally have more active online customers, likely due to the lack of physical stores offering an adequate variety of merchandise and offline shopping experiences.

Diagram 3: Percentage of Online Consumers Buying Various Products in China (2013)

Source: China Internet Network Information Centre

Chinese online spending mainly targets low-end

products

DBS Asian Insights SECTOR BRIEFING 1608

Battlefield 1: Company Website/E-Shop

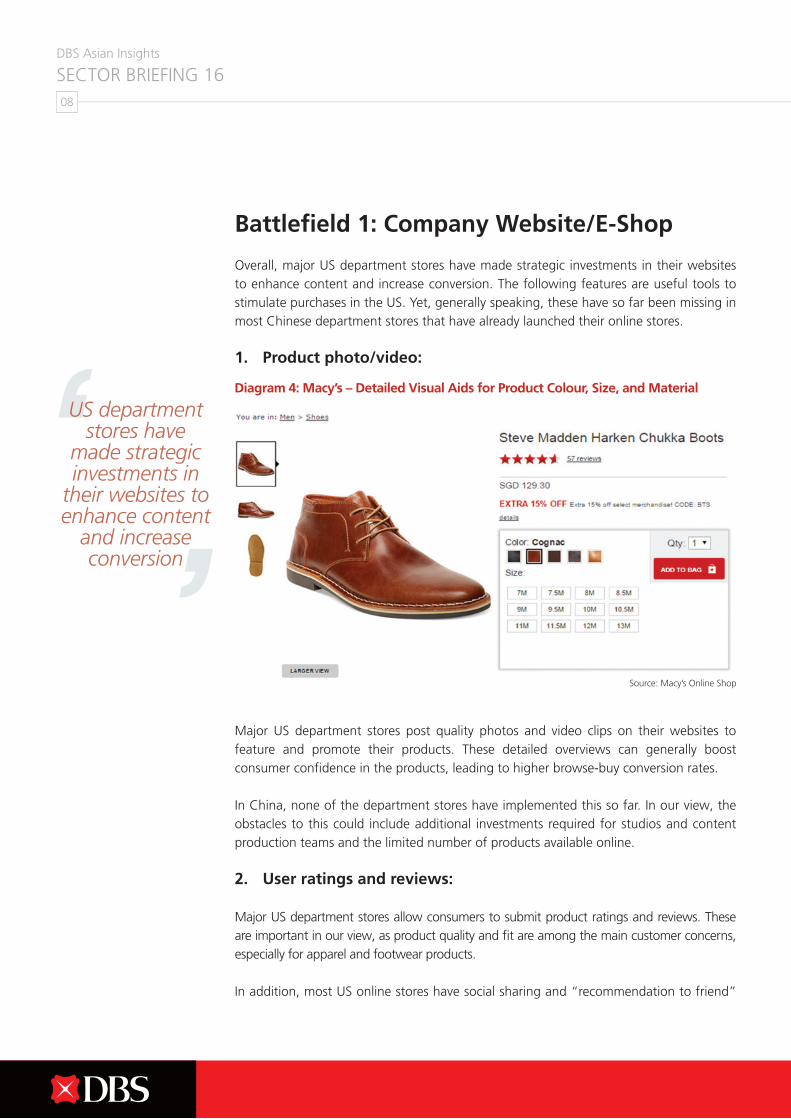

Overall, major US department stores have made strategic investments in their websites to enhance content and increase conversion. The following features are useful tools to stimulate purchases in the US. Yet, generally speaking, these have so far been missing in most Chinese department stores that have already launched their online stores.

1. Product photo/video:

Major US department stores post quality photos and video clips on their websites to feature and promote their products. These detailed overviews can generally boost consumer confidence in the products, leading to higher browse-buy conversion rates.

In China, none of the department stores have implemented this so far. In our view, the obstacles to this could include additional investments required for studios and content production teams and the limited number of products available online.

2. User ratings and reviews:

Major US department stores allow consumers to submit product ratings and reviews. These are important in our view, as product quality and fit are among the main customer concerns, especially for apparel and footwear products.

In addition, most US online stores have social sharing and “recommendation to friend”

Diagram 4: Macy’s – Detailed Visual Aids for Product Colour, Size, and Material

US department stores have

made strategic investments in

their websites to enhance content

and increase conversion

Source: Macy’s Online Shop

DBS Asian Insights SECTOR BRIEFING 16

09

features to increase their customer base. Some even allow photo reviews and video reviews to enhance the richness of customer feedback.

In China, select department stores such as Rainbow and New World Department Store offer these features, but user participation is generally low, with no reviews for many products.

3. Live chat with customer service:

Live chat with customer service is available on some US department store websites to enhance consumer confidence. This is not a feature that has been commonly implemented by Chinese department stores yet.

4. Search visibility:

Overall, we view department stores’ search visibility – in popular search engines such as Google and Baidu – as an important indicator of their brand awareness among online

Diagram 5: Nordstorm – User Rating Summary

Source: Nordstrom Online Shop

DBS Asian Insights SECTOR BRIEFING 1610

shoppers. In our view, this should be particularly important for Chinese department stores as high search visibility helps expand the customer base beyond their home markets.

In the US and Europe, major department stores such as Saks, John Lewis, and Nordstorm have been using paid ads to increase their search visibility. We find that major players such as Nordstorm, Macy’s, and Sears generally appear on the front pages of search results for common keywords such as “men shirt” and “ladies’ shoe”.

In China, however, search visibility is generally weak among department stores. We performed a series of searches on Baidu, China’s most popular search engine, using common apparel keywords and could not find any department store links in the search results. This indicates that department store operators in China need to implement an effective online marketing strategy to enhance their overall brand awareness among online shoppers.

Battlefield 2: O2O Integration

In recent years, major US department stores such as Bloomingdale’s and Macy’s have added “click-and-collect” services, which allows consumers to order online and pick up purchased items in physical stores or kiosks. In addition, some department stores offer an in-store return service and provide real-time inventory information to customers.

“Click-and-collect” has proven to be effective so far. According to a survey by UPS, about half of online shoppers choose the “click-and-collect” service, while about 40% make additional in-store purchases when they pick up the merchandise.

Prompted by the initial success, more US and European retailers are expanding their pick-up locations beyond their existing stores to enhance overall convenience to customers. For example, UK department store John Lewis has partnered with grocery store Waitrose to expand the number of pick-up locations to 300, against its own network of only 40 stores. Marks & Spencer is also partnering with Collect+ to leverage its network of more than 5,500 pick-up points in the UK.

Diagram 6: Click-and-Collect Pick Up Lockers

Source: AFP

DBS Asian Insights SECTOR BRIEFING 16

11

Such a “click-and-collect” business model remains uncommon in China, as O2O is still at an early stage of development.

Among major listed department stores in the country, only Rainbow has recently launched a “click-and-collect” service across about 400 pick-up points in Shenzhen through partnerships with Catic Property, GuoDa Drugstore, Sposter, and Chang Cheng Property, to name but a few.

In our view, a successful implementation of “click-and-collect” services in China could potentially boost department stores’ online and offline sales by mitigating customer concerns over the reliability of deliveries as well as lifting in-store traffic.

Battlefield 3: Mobile Apps

In addition to e-commerce, department stores are also moving into the mobile commerce, or m-commerce, space through the launch of their mobile apps. In the US and Europe, most major department stores including Sears, Macy’s, and Nordstrom have developed mobile apps in the iOS and Android platforms. In China, currently only a handful of operators such as Intime and Golden Eagle offer this.

Diagram 7: Sears – Click-and-Collect Service

Source: Sears Online Shop

a successful implementation of “click-and-

collect” services in China could

potentially boost department

stores’ online and offline sales

DBS Asian Insights SECTOR BRIEFING 1612

We also find that mobile apps of US and UK department stores generally offer more comprehensive functions than those offered by their Chinese peers.

For example, shoppers of most US department stores can use their mobile apps to view and write product ratings and reviews. In addition, operators like JCPenney and Nordstorm will show app users which products are available at stores within driving distance.

These functions are generally unavailable among major Chinese department stores. For example, Golden Eagle’s mobile app currently only provides basic promotional information for its stores. No e-commerce or O2O functions have been implemented yet. Intime offers a more comprehensive mobile app with e-commerce functions, but still lacks useful features such as user reviews and inventory checks.

Sears Macy's Nordstrom JC Penney Intime Golden Eagle

Social sharing Y Y Y Y Y Y

E commerce Y Y Y Y Y N

Wish list Y Y Y Y Y N

Geo-location N N Y Y N N

Rating and review Y Y Y Y N N

Coupons Y Y Y Y Y Y

Inventory check Y Y Y Y N N

Diagram 8: China and US Department Stores Mobile App Function Comparison

Source: DBS Vickers

Diagram 9: JCPenney – Comprehensive Features in Its Mobile App

Source: JCPenney Shopping App

DBS Asian Insights SECTOR BRIEFING 16

13

Impact of O2O on Commercial Property Value and Management ChinaMany developers are growing their commercial property exposure despite the e-commerce challenge. Chinese developers’ main revenue source is still property sales, while more are gradually building up their investment property portfolios. These include Wanda, CR Land, Cofco Land, Longfor, Sino Ocean, and Powerlong.

In terms of malls recently opened or under construction, Wanda and Powerlong are focusing more on tier 3 and 4 cities, while others are targeting tier 1 and 2 cities. In terms of brand names, CR Land aims to house most of the high-end international brands while others are focusing on mid- to high-end brand names.

Most Hong Kong property companies that operate in China, such as SHKP, Wharf, Swire Properties, Hang Lung, and Kerry Properties, are still the main players in the luxury mall segment in tier 1 and 2 cities. All are experiencing or foresee the e-commerce disruption. Fast-growing online shopping platforms are driving developers to adjust their tenant mix more toward catering, experiential services, entertainment, education and social activities.

Wanda Commercial – in collaboration with internet giants Tencent and Baidu – has established and owns a 35% equity stake in Wanda E-commerce, with the ambition of building it into the world’s biggest O2O business platform. Cofco Land is also working with Alibaba to drive its O2O initiatives in order to mitigate the impact from e-commerce disruption. Longfor has also developed an O2O and big data system to provide Wi-Fi, smart parking, customer traffic analysis, a payment system, etc. Yet, these efforts are only at the early stage of development and a successful model has yet to be built.

Hong Kong

Online shopping is not very popular in Hong Kong as it is very convenient to physically walk out to buy whatever is needed. Most local shoppers are able to get to regional malls, which house a mix of diversified branded retailers, within 20 minutes by subway. Online shopping tends to appeal to local shoppers only if the items cost less or are unavailable locally.

From the perspective of traditional branded retailers, online retailing has yet to become mainstream in Hong Kong. Indeed, the Hong Kong retail industry has received a strong boost from cross-border spending over the past decade. Wealthy Mainland tourists have indeed been key purchasers of hard luxuries (expensive watches and jewellery), a durable trend that has lessened the incentive for existing branded retailers to explore online retailing opportunities.

Supermarket sizes are decreasing with stores of more than 30,000 square feet becoming rarer and rarer.However, the local retail market landscape could change if locals are able to buy branded products via online retailers at cheaper prices as a result of price differentials.

Fast-growing online shopping

platforms are driving developers

to adjust their tenant mix

DBS Asian Insights SECTOR BRIEFING 1614

This may lead to adjustments in global pricing or store strategy by these established traditional retailers. Over the long-term, general products should be more easily sold via online e-platforms than other goods, as shoppers need not visit the physical store to see the items and to get the shopping experience before making purchase decisions.

Some supermarket items fall into this category. A growing number of locals are buying these items through the supermarkets’ own websites at cheaper prices with delivery services provided. This, in turn, explains why supermarkets in Hong Kong have been downsizing in recent years.

Going forward, malls where large supermarkets serve as anchor tenants to draw foot traffic may face challenges brought about by the popularity of internet retailing for general products. This is especially true for malls catering to middle-class consumers who are more likely to shop online. Kornhill Plaza in Quarry Bay could be a case in point. But concerns should not be overstated as Hong Kong’s renowned retail landlords excel in rejuvenating their malls through repositioning or trade mix reconfiguration, if needed.

“Click-and-Collect” is not yet popular in Hong Kong. So far, “click-and-collect” services have yet to gain popularity among traditional retailers offering O2O solutions. But if this proves to be effective in the future, we do not rule out the possibility that these retailers will adjust their store strategies.

Major shopping malls in strategic locations should be more resilient. Malls such as Wharf’s Harbour City and Times Square should be able to weather the competition from online retailing. These must-go-to shopping malls have diversified retail and entertainment offerings, with superb retail management in place. This has enabled them to provide a good shopping experience that online shopping is unable to match.

Diagram 10: Retail as a Percentage of Gross Asset Value in Hong Kong

Source: Companies, DBS Vickers

DBS Asian Insights SECTOR BRIEFING 16

15

Though not yet very popular, online retailing could have implications on the trade mix of shopping malls in Hong Kong over the long-term.

Singapore

Singapore retailers are grappling with a “new reality.” With retail sales stagnating over the past year and consumers moving toward online shopping, the impact on retail brick-and-mortar shops is very real.

Landlords are also adjusting their marketing strategies and repositioning their properties to offer more entertainment and food & beverage outlets, aiming to remain relevant in the midst of changing consumer preferences.

Key characteristics that make a mall more resilient to the threat of e-commerce, in our view, are:

Location, where malls that are located in or close to transportation hubs will likely see more pedestrian traffic and visibility, and thus enjoy better sales.

Mall size and the operator’s scale, which mean a larger tenant reach.

Mall positioning, where To-Meet Malls and Pass-Through Malls are likely to perform better as they cater largely to food & beverage and entertainment services, which are less likely to be affected.

We have identified some of the shopping malls which could face rising challenges. These would be To-Go-To Malls in the electronics sector and small Pass-Through malls which are not very conveniently located.

O2O has not yet been widely adopted in Singapore. Shopping malls concentrating all types of services and retail activities are still quite popular, which means there is little added value for consumers to move away from their deeply-seated habits.

Source: Kantar Retail, DBS Bank

Diagram 11: Segmenting Singapore’s Malls Based on Their Key Characteristics

Type of Mall Characteristic Risk from E-Commerce

Pass-Through Malls

Fulfil shoppers’ specific needs or provide convenient access en-route to final

destination

More resilient but could be impacted if operational scale is small, if offering limited mix of tenants and if not

conveniently located

To-Go-To Malls Typically have high concentration of tenants from a particular trade category

Benefit from “clustering effect” but lack range. Malls that focus on electronics, fashion, sports, etc. are feeling the heat

To-Meet Malls Designed for shoppers to meet and socialise, typically for leisure and lifestyle-

oriented activities

Scale is usually large so tenants and shoppers like to meet there. Risk of commoditisation due to limited range of

tenants

DBS Asian Insights SECTOR BRIEFING 1616

DBS Asian Insights SECTOR BRIEFING 16

17

Conclusion2O is still a work in progress in most of the places in which it has been implemented. In Asia, it is safe to say that most retailers are

not completely ready to adopt O2O. For the digital economy to truly take off in Asia, both physical retailers and e-commerce sites will need to be able to respond to the changing dynamics of consumers’ purchase journeys. This is particularly true in parts of Asia where the rise of online channels and the decline of the number and the size of physical stores make it urgent for retailers to at least examine their options before it is too late to recover.

O2O is indeed the ideal way to employ mobile devices, the web, and related technologies to make buying products more convenient, efficient, and even fun. But O2O is no longer only about searching online and purchasing offline, buying online and picking up in-store, or getting an online or mobile coupon to redeem in-store. It’s now about buying offline, going online, and then buying again.

O2O cannot, however, be a remedy for all physical stores, especially for those in less strategic locations; divesting them could be a good move in the long term. Businesses, investors, and policy-makers alike must thus balance the long-term strategic advantages of e-commerce practice versus near-term gains.

O

DBS Asian Insights SECTOR BRIEFING 1618

DBS Asian Insights SECTOR BRIEFING 09

19

Disclaimers and Important Notices

The information herein is published by DBS Bank Ltd (the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee.

The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof.

The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies.

The information herein is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation.

www.dbs.com

Living, Breathing Asia

![INSIS Road Map Forum2013.ppt [Read-Only] - fadata · Reinsurance - Simplification of ... accounts, their purposes, assignment of these accounts to ... Pre‐configured commercial](https://img.pdfslide.net/doc/110x75/5b0199ff7f8b9a6a2e8e7593/insis-road-map-read-only-fadata-simplification-of-accounts-their-purposes.jpg)