Embed Size (px)

Citation preview

Meng Teck August 22, 2015

No Bullshit Guide To Investing

Investing Handbook, Page �1

Meng Teck August 22, 2015

!

Investing Handbook, Page �2

Meng Teck August 22, 2015

Disclaimer: This handout contains the ideas and opinions of the author. While utmost care has been made to provide the most accurate and updated information, no guarantee is given regarding the reliability, accuracy or completeness of the information provided herein. The ideas provided are used with the understanding that the author is not engaged in rendering legal,accounting,investment or professional services. The author disclaims any responsibility for any liability, loss or risk, personal or otherwise, incurred as a result either directly or indirectly from the use of any ideas, strategies or techniques used in this program. No recommendation is given to buy or to sell any securities, businesses or investment discussed herein. For professional investment advice, please refer your stockbroker or registered investment advisers.

Copyright Notice: Savwee Investment. All rights reserved. Any unauthorised use,sharing,reproduction or distribution of these material by any means,electronic,mechanical,or otherwise is strictly prohibited. No portion of these materials may be reproduced in any manner whatsoever, without the expressed or written consent of the publisher

Summary: This is a handout that contains the important points on what you should be looking for in a business and when you should buy or sell the business. It should help in assisting you to refresh what is being covered in the course as it only highlights the main points.

Investing Handbook, Page �3

Meng Teck August 22, 2015

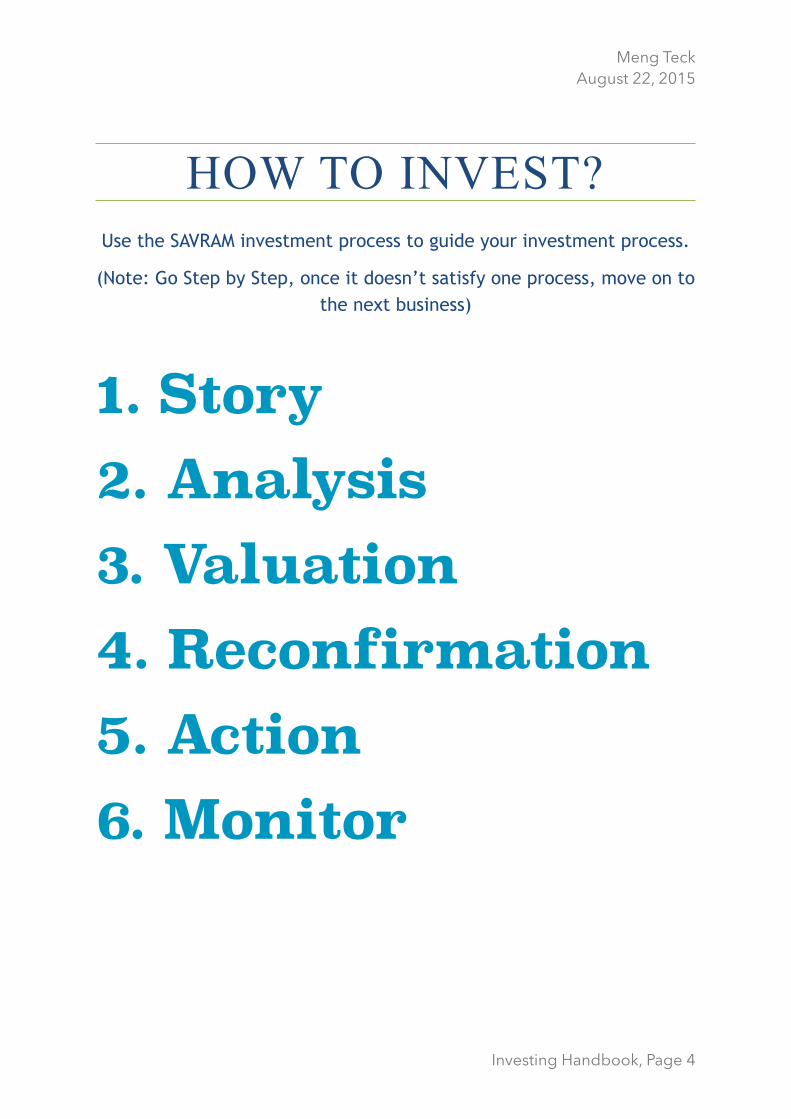

HOW TO INVEST? Use the SAVRAM investment process to guide your investment process.

(Note: Go Step by Step, once it doesn’t satisfy one process, move on to the next business)

1. Story 2. Analysis 3. Valuation 4. Reconfirmation 5. Action 6. Monitor

Investing Handbook, Page �4

Meng Teck August 22, 2015

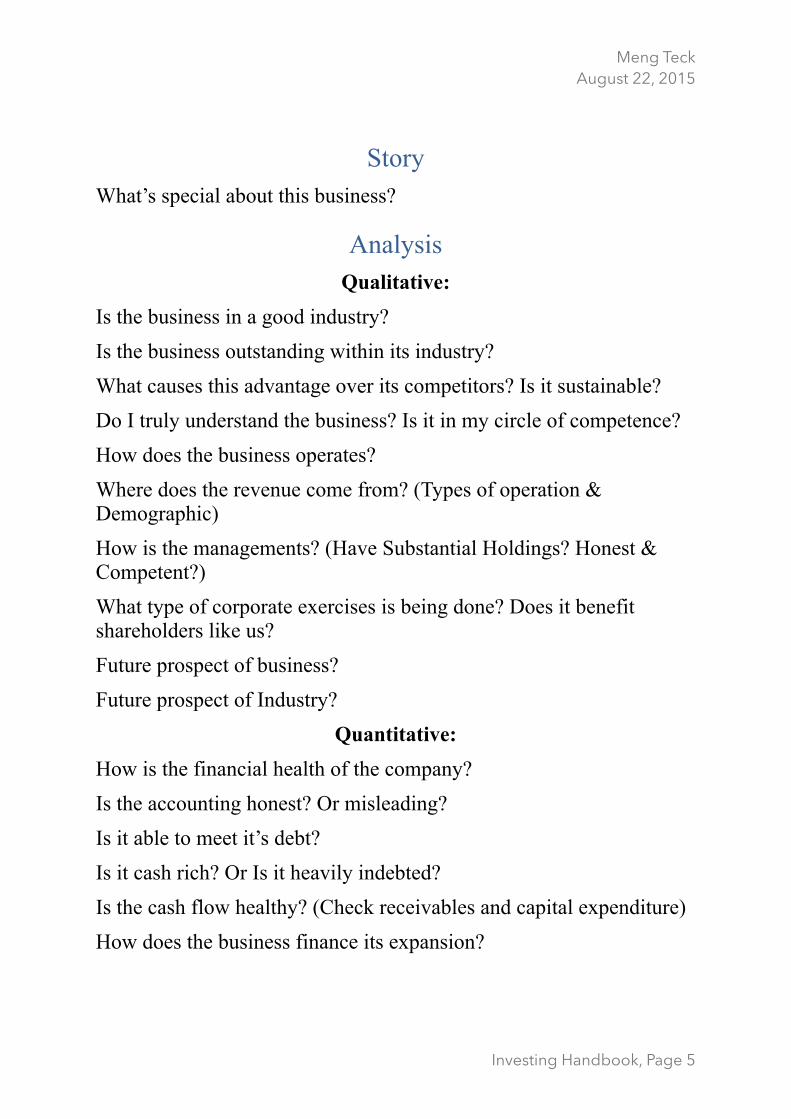

Story What’s special about this business?

Analysis Qualitative:

Is the business in a good industry? Is the business outstanding within its industry? What causes this advantage over its competitors? Is it sustainable? Do I truly understand the business? Is it in my circle of competence? How does the business operates? Where does the revenue come from? (Types of operation & Demographic) How is the managements? (Have Substantial Holdings? Honest & Competent?) What type of corporate exercises is being done? Does it benefit shareholders like us? Future prospect of business? Future prospect of Industry?

Quantitative: How is the financial health of the company? Is the accounting honest? Or misleading? Is it able to meet it’s debt? Is it cash rich? Or Is it heavily indebted? Is the cash flow healthy? (Check receivables and capital expenditure) How does the business finance its expansion?

Investing Handbook, Page �5

Meng Teck August 22, 2015

Valuation Is this a growth company? or Asset rich? or Turnaround? or Stalwart? Is there any one off item that may have caused the earnings to spike up? (Sometimes earnings can be misleading due to a one off gain from the sale of assets). Is the market price undervalued or overvalued?

Reconfirmation Have I missed out anything? Why is it so cheap? What could possibly go wrong? Is my valuation conservative? Is my facts & reasoning correct? Is emotion of greed/fear involved? IMPORTANT: If this business is offered privately to me in full, would I buy it?

Action Set up investment strategy (Determine entry point & exit point) What price to buy? What price to sell? How many shares to buy? (Minimum purchase is 1 lot = 100 Shares) Amount to invest = (Price per share * Number of shares) Key in buy order (Example: Buy: 100 lots at RM1.78 = RM17800) Check buy status (Whether In Market or Completed)

Monitor Is the earning power of the business still there? Is my prediction correct?

Investing Handbook, Page �6

Meng Teck August 22, 2015

WHAT STOCKS TO SELECT? (PUDOG STOCK SELECTION CRITERIA)

(Note: At least 3 characteristics must be met to be a good buy)

Predictability

( Is there consistent earnings with little fluctuations? If so, why? Is it because of its competitive advantage & economic moat)

Undervalued

(Is the price cheap compared to it’s worth?)

Dividend Yielding

( Is the company paying out dividend? It is okay for high growth company to not pay dividend in order to fund growth.)

*Please note that at time when market is over bullish like this, you should start to collect dividend paying shares to protect yourself and

to provide cash flow during market crash

Opportunity

(Buy During Panic, buy during support pending reversal or support in an uptrend)

Growth

(Is there any sustainable & predictable growth rate due to competitive advantage?)

Investing Handbook, Page �7

Meng Teck August 22, 2015

INVESTOR VS SPECULATOR

4 KEYSTONE TO VALUE INVESTING

INVESTOR & SPECULATOR CAN BE EASILY DIFFERENTIATED BY ASKING THE FOLLOWING 4

QUESTION WHICH THE LATTER WILL NOT BE ABLE TO ANSWER.

1. Is the business model good?

2. Is the business run by good management?

3. Is the business having strong financial health?

4. Is the business undervalued?

Investing Handbook, Page �8

Meng Teck August 22, 2015

BUSINESS MODEL ANALYSIS:

What to look for? We are looking for a great business in a good industry or a boring industry. Good industry means the industry is able to enjoy relatively “high profit margin” compared to other industries. Ideally, we are looking for industries that are not easily disrupted by new technology (disruptive invention that will kill the industry, example: Kodak films) and is not easy for new entrants. Also, we try to look for industries that don’t need to reinvest much of their profit to maintain their competitive advantage. (Can be studied from the Cash Flow Statement) “It is not fun to be in the horse business when the car business come along.” That is why we try to avoid airlines, manufacturing (without design) & steel industries. Also, we try to avoid ‘hot’ industries. A business model is like a system that churns out cash when you inject resources into it.

Investing Handbook, Page �9

Meng Teck August 22, 2015

Ideally, we want a business to have

Competitive Advantage ; is like a force that the business possesses to protect itself against competitors, to be scalable and to be able to increase profit margin, this includes but not limited to: Have a product that is desirable, very different from the competitors and it is difficult to be copied. (iPhone when it is first released) Habit Product (tobacco,alcohol,etc) Involves high switching cost (Very difficult to switch to competitor, Telcos many years ago) Economies of Scale (Having lower cost due to size, therefore, able to offer cheaper price than competitor) Having a strong branding (Gucci,high profit margin) Having government license (Casino,toll,mrts)

All said, make sure it is sustainable and growth is powered by these competitive advantages. Businesses that have strong competitive advantages that is sustainable is destined to do well,even if run by less competent management. Therefore, much attention has to be put into this area. A business having good competitive advantage is easily reflected by its high profit margin. (Compared to its peers)

Investing Handbook, Page �10

Meng Teck August 22, 2015

Before you even look at the financial statements of the company, you need to ask these questions to test if you truly understand the business:

What kind of industry is this business in? What is the business involved in? Is it a market leader in its industry? (30% above market share.) Who are their competitors? How does the business operate? What economic factors will affect it substantially? Why is this business profitably? (Competitive advantage) Where is the revenue from? Which segment contributes the most? Which area is the most significant? This way, you will be able to analyse the risk involved better. If you do not understand the business, please do not touch. Many people overestimate their circle of competence. Unless you are able to tell clearly how the business earn it’s profit, you do not understand the business. Complexity has no relation with profitability.

Investing Handbook, Page �11

Meng Teck August 22, 2015

How to understand a business?

Read the annual report (Chairman’s message)

Go to its website

Visit the point of sale (Go to the store; Padini)

Go to the AGMs

Ask the customers, employee, ex-employees, rivals, supplier, experts,etc.

Investing Handbook, Page �12

Meng Teck August 22, 2015

Good business is like a good cash churning machine, but if run by incompetent and dishonest management, it wouldn’t be too good for the owner too.

MANAGEMENT ANALYSIS

Look for honest & competent management.

How to gauge?

Act like owner

Diversify not diworsify

Think long term

Passionate about their work

Admit mistakes (Read the annual report, there will be clue)

No accounting gimmickry

Share buybacks when undervalued not otherwise

Management collects shares

Dividends or bonuses to employees?

Debt or Right issues?

Preferably owns a big portion of the business (our goals are aligned)

Thrifty or spending like crazy on big offices?

Good marketing skills

Corporate exercises don’t negatively affect shareholders.

Investing Handbook, Page �13

Meng Teck August 22, 2015

ANNUAL REPORT:

Frankly speaking, every page of the Annual Report matters. However, annual report are not user friendly at all! Languages and terms used may be quick difficult to understand. But do not worry, there are 5 most important parts of an annual report. As long as you are able to

have a fairly good grasp of these parts, you should be fine.

What are they?

Chairman’s Message

MD/CEO’s Message

Income Statement

Balance Sheet

Cash Flow Statement

You might want to pay attention to what they say because this will show whether they are honest and if they are planning long term

Investing Handbook, Page �14

Meng Teck August 22, 2015

FINANCIAL STATEMENTS 3 PARTS OF FINANCIAL STATEMENTS:

Income Statement

Balance Sheet

Cash Flow Statement

Investing Handbook, Page �15

Meng Teck August 22, 2015

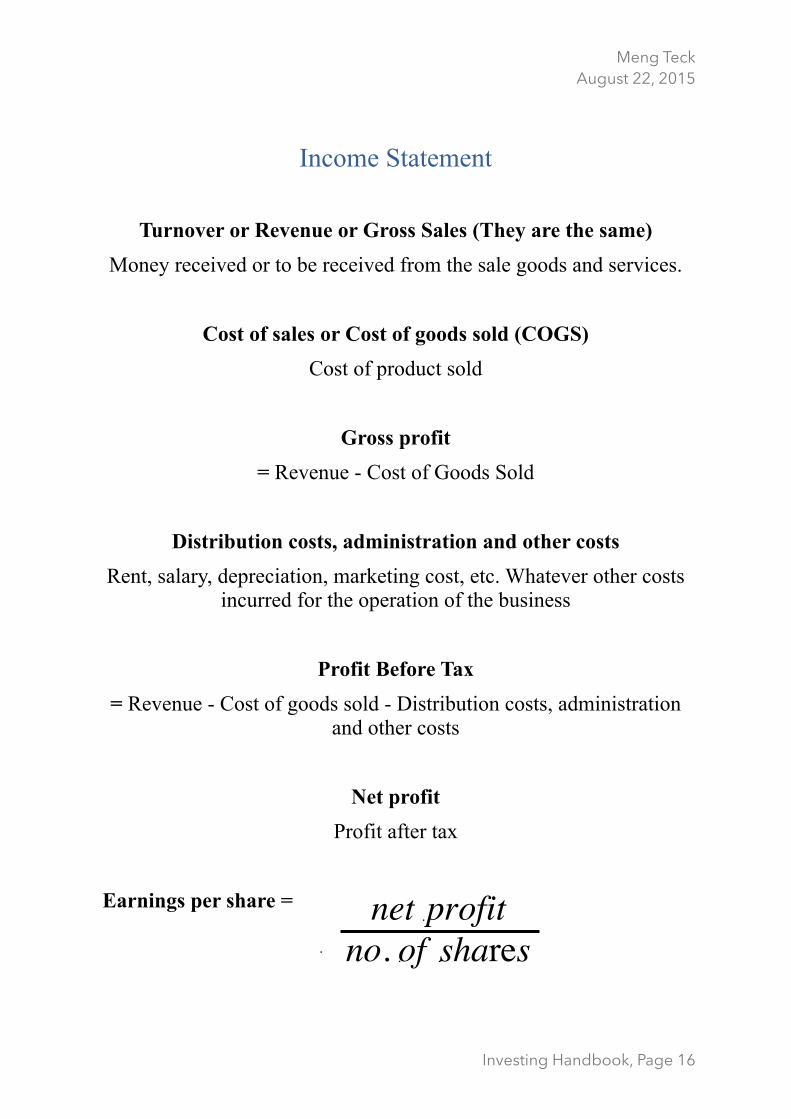

Income Statement

Turnover or Revenue or Gross Sales (They are the same) Money received or to be received from the sale goods and services.

Cost of sales or Cost of goods sold (COGS) Cost of product sold

Gross profit = Revenue - Cost of Goods Sold

Distribution costs, administration and other costs Rent, salary, depreciation, marketing cost, etc. Whatever other costs

incurred for the operation of the business

Profit Before Tax = Revenue - Cost of goods sold - Distribution costs, administration

and other costs

Net profit Profit after tax

Earnings per share =

Investing Handbook, Page �16

Meng Teck August 22, 2015

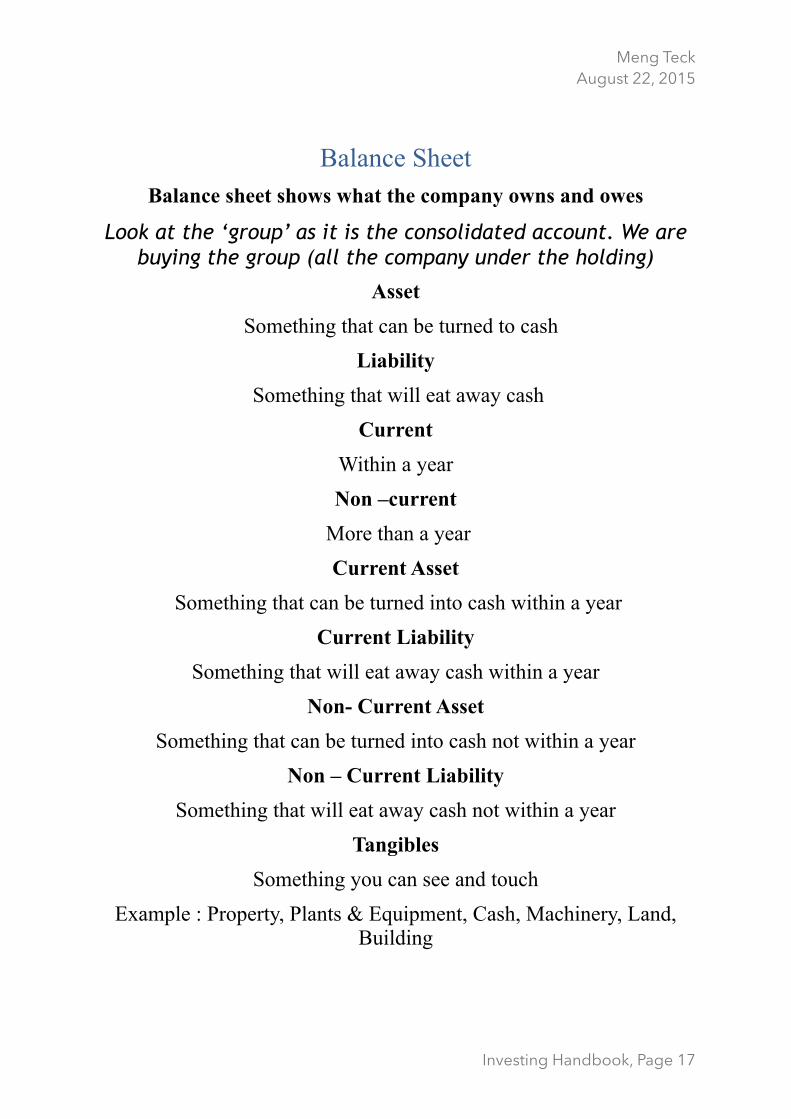

Balance Sheet Balance sheet shows what the company owns and owes

Look at the ‘group’ as it is the consolidated account. We are buying the group (all the company under the holding)

Asset Something that can be turned to cash

Liability Something that will eat away cash

Current Within a year Non –current

More than a year Current Asset

Something that can be turned into cash within a year Current Liability

Something that will eat away cash within a year Non- Current Asset

Something that can be turned into cash not within a year Non – Current Liability

Something that will eat away cash not within a year Tangibles

Something you can see and touch Example : Property, Plants & Equipment, Cash, Machinery, Land,

Building

Investing Handbook, Page �17

Meng Teck August 22, 2015

Intangibles Something you can’t see or touch. Example: Branding, Patents,

Goodwill, Trademarks, Publishing rights Property, plants & equipments

Things used by the business to operate (Spaces, Tools, Etc) Cash & cash equivalents

Cash in banks & Cash Deposits Investment properties

Properties bought not for use but for investment purposes either to collect rent or for capital appreciation

Investment in Subsidiaries Investment made in the subsidiaries of the holding (More than 30%

holding) Investment Securities

Second thing to as good as cash. However, may be much more volatile. This is actually the shares of other public listed companies

held by the group Deferred Tax Assets-

Credit the company has with the the federal government that can be used to reduce taxes.

Receivables Money owed to this group by others

Stock/Inventory Goods/Stocks of the company ready to be sold (Written as cost value)

Prepaid Expenses Amount of money paid in advance of getting the services.

Investing Handbook, Page �18

Meng Teck August 22, 2015

Depreciation,Depletion,Amortisation Accumulated loss as a result of the lowering of the durability or quality of an asset. (Example : Car has a lifespan of 10 years in Singapore, therefore, the value depreciates by 10% every year

Liabilities: Deferred Tax Liabilities

Money that the corporation owes the federal government but does not have to pay immediately.

Creditors/Trade payables Money owed to supplier (Different than money borrowed) Payables

are usually very short term and carries no interest. Debts & Borrowings

Money loaned from banks or bonds Equity

Total Asset - Total Liabilities Issued & Paid Up Capital

Capital being gathered to start the business + being gathered during IPO

Reserves Money earned that has been retained in the business

Net Asset Value or Book Value Total Asset – Intangible assets – Loss in value of asset due to

liquidation– Total Liabilities.

Investing Handbook, Page �19

Meng Teck August 22, 2015

Cash Flow Statement This is where most novices get tricked! Due to accrual accounting, earnings numbers can be manipulated. Often time, earnings are not reflected in the cash received. A company can show massive earnings and still face liquidation issue due to cash flow problem. Cash flow is the lifeline of the company. Cash is King!

Cash flows from operating activities Cash obtained or (Lost) due to business operations. Most of the earnings and cash should come from here. Good business should show a very strong cash flow in this section.

Cash flows from investing activities Cash obtained or (Lost) due to investing activities. This may be acquisition of businesses or land, purchase of new plants & equipments and opening of new stores. Beware of businesses that need to constantly infuse back earning to sustain competitive advantage.

Cash flows from financing activities Cash obtained or (Lost) due to financing activities. This includes giving out of dividend, paying back or debt or borrowing from banks.

Ideally,we want to see very high positive cash flow from operation , with very little need to reinvest back into investing activities and is able to retain some cash after paying back debt and giving out dividends. Measured by the amount of Free Cash Flow. The higher the better. Free Cash Flow = Cash Flow from Operating Activities - Cash Flow Used in Investing Activities

Investing Handbook, Page �20

Meng Teck August 22, 2015

Key Ratios: Market Capitalization :

(Market Cap means how much it will cost to buy the whole business)

Earnings Per Share (EPS) :

Price to Earning Ratio (PE) :

Indicates if the business is priced with a premium or is being sold cheaply. The higher the more expensive.

Return On Equity (ROE) :

Indicates the ability to generate cash for every dollar infused into the business Current Ratio :

Should be more than 1. Ideally around 1.5-2. Less than 1 means it might have liquidation issue whereas more than 2 might mean inefficient capital management.

Investing Handbook, Page �21

Meng Teck August 22, 2015

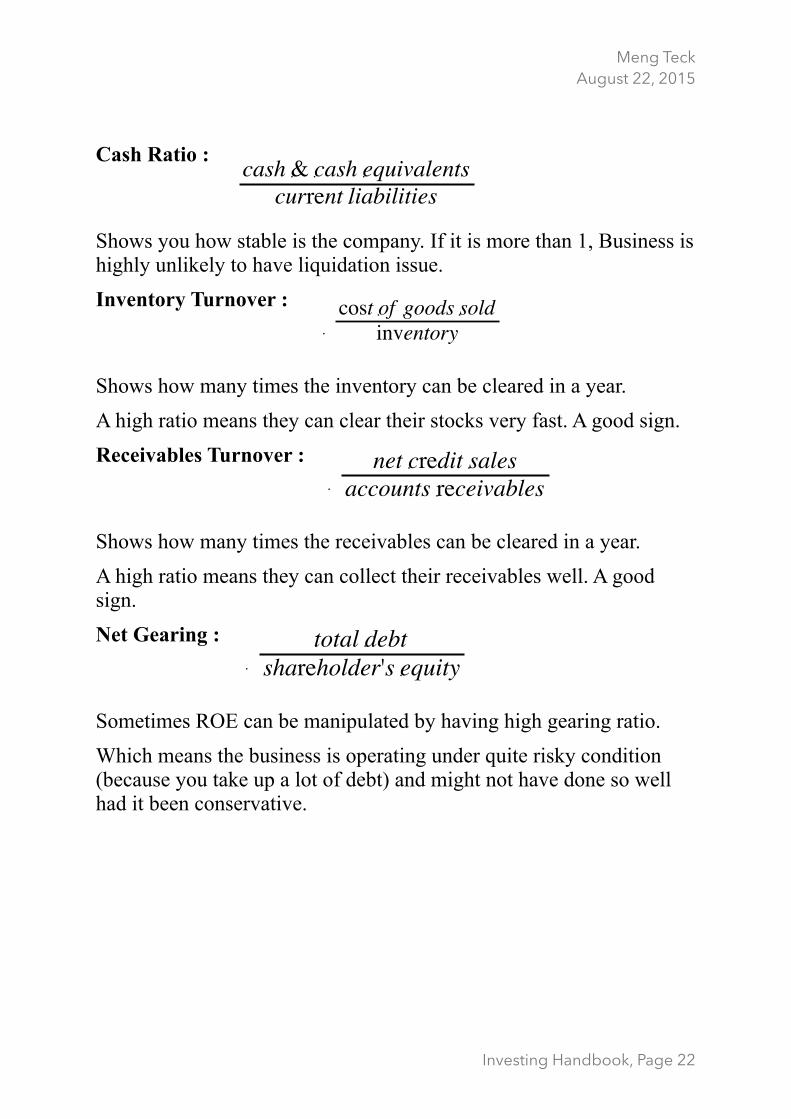

Cash Ratio :

Shows you how stable is the company. If it is more than 1, Business is highly unlikely to have liquidation issue. Inventory Turnover :

Shows how many times the inventory can be cleared in a year. A high ratio means they can clear their stocks very fast. A good sign. Receivables Turnover :

Shows how many times the receivables can be cleared in a year. A high ratio means they can collect their receivables well. A good sign. Net Gearing :

Sometimes ROE can be manipulated by having high gearing ratio. Which means the business is operating under quite risky condition (because you take up a lot of debt) and might not have done so well had it been conservative.

Investing Handbook, Page �22

Meng Teck August 22, 2015

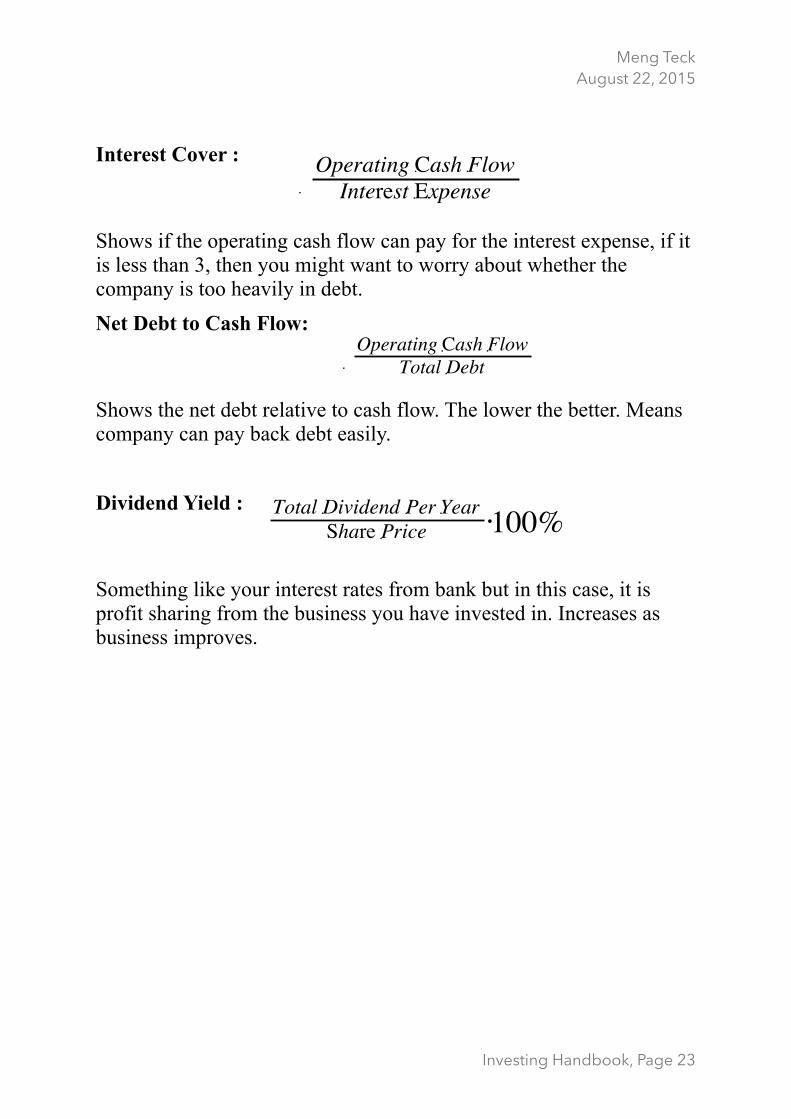

Interest Cover :

Shows if the operating cash flow can pay for the interest expense, if it is less than 3, then you might want to worry about whether the company is too heavily in debt. Net Debt to Cash Flow:

Shows the net debt relative to cash flow. The lower the better. Means company can pay back debt easily. Dividend Yield :

Something like your interest rates from bank but in this case, it is profit sharing from the business you have invested in. Increases as business improves.

Investing Handbook, Page �23

Meng Teck August 22, 2015

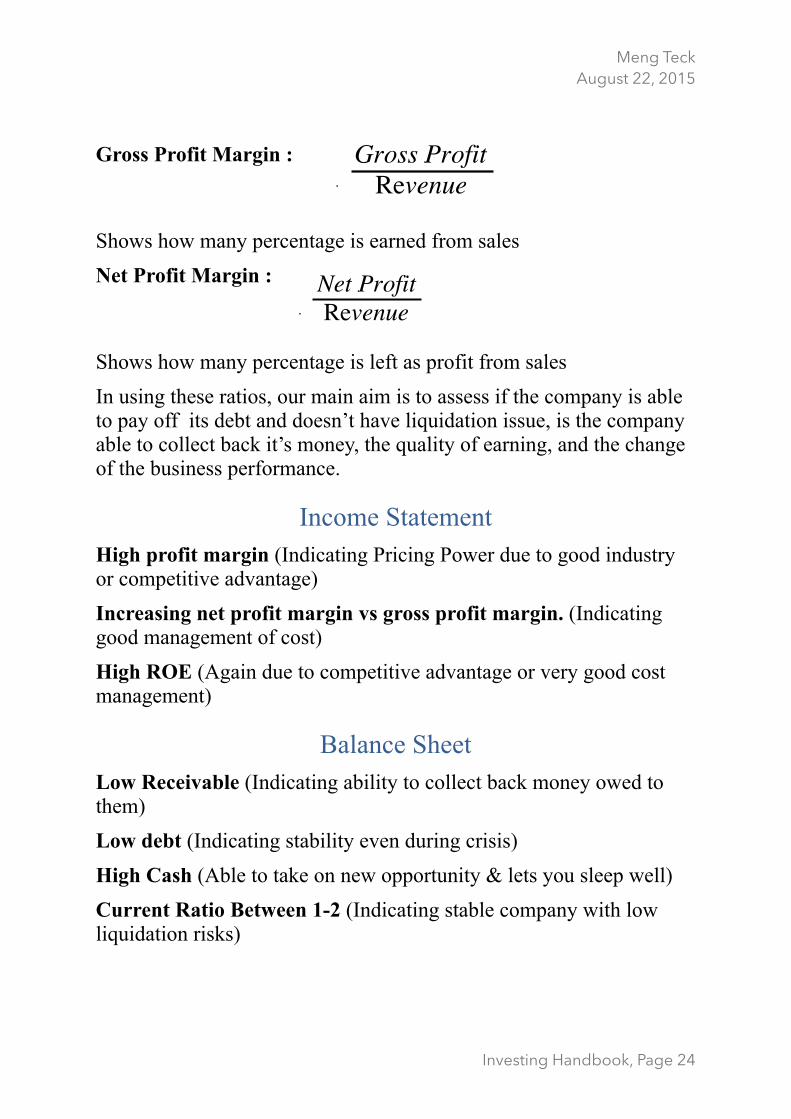

Gross Profit Margin :

Shows how many percentage is earned from sales Net Profit Margin :

Shows how many percentage is left as profit from sales In using these ratios, our main aim is to assess if the company is able to pay off its debt and doesn’t have liquidation issue, is the company able to collect back it’s money, the quality of earning, and the change of the business performance.

Income Statement High profit margin (Indicating Pricing Power due to good industry or competitive advantage) Increasing net profit margin vs gross profit margin. (Indicating good management of cost) High ROE (Again due to competitive advantage or very good cost management)

Balance Sheet Low Receivable (Indicating ability to collect back money owed to them) Low debt (Indicating stability even during crisis) High Cash (Able to take on new opportunity & lets you sleep well) Current Ratio Between 1-2 (Indicating stable company with low liquidation risks)

Investing Handbook, Page �24

Meng Teck August 22, 2015

Once you have a good business in a good industry with honest & competent management and you have found out that the company’s

financial health is very strong and is improving, you know you have got a good share! I’ve got to be very frank with you, 99% of the time, when

you discover a business that has all the features above, the factors have already been priced in (Sometimes over priced). You will notice that their PE is already at 20+( Due to so many analyst covering on it. Remember Mr.Market is very intelligent). Remember, A great share can

be a bad investment if you overpaid for it.

PRICE IS WHAT YOU PAY, VALUE IS WHAT YOU GET – WARREN

BUFFET However, Mr. Market has low EQ, therefore, a truly intelligent investor

needs to be patient and wait for Opportunity. When the market is acting foolishly, that’s your chance. You will be handsomely rewarded

for your patience.

Investing Handbook, Page �25

Meng Teck August 22, 2015

HOW TO VALUE A BUSINESS?

Ideally we want at least 15% discount relative to the biz value for outstanding businesses and 50% or more discounts for good businesses.

(Predictability is the most important thing here)

4 types of Valuation There are many other more valuation but they tend to be complex and is not necessarily very helpful. Remember, complexity has no relation

with profitability. Different Valuation should be used for different types of companies

Growth companies – PEG

(High Growth Companies with more than 15% Growth Rate)

Stalwarts – PEG or PE comparison

(Growth Companies with more than 10% Growth rates and is well established, has some strong competitive advantage and high ROE

(above 15%) )

Strong Companies- DCF

(Companies with low growth rate but greater than inflation, has high ROE and have very strong competitive advantage)

Ordinary – PE Comparison

(Companies with no special competitive advantage & Low Growth Rate (<5%))

Dying – Asset Play or Turnaround

(Companies making loss or very little profit, better dead than alive)

Investing Handbook, Page �26

Meng Teck August 22, 2015

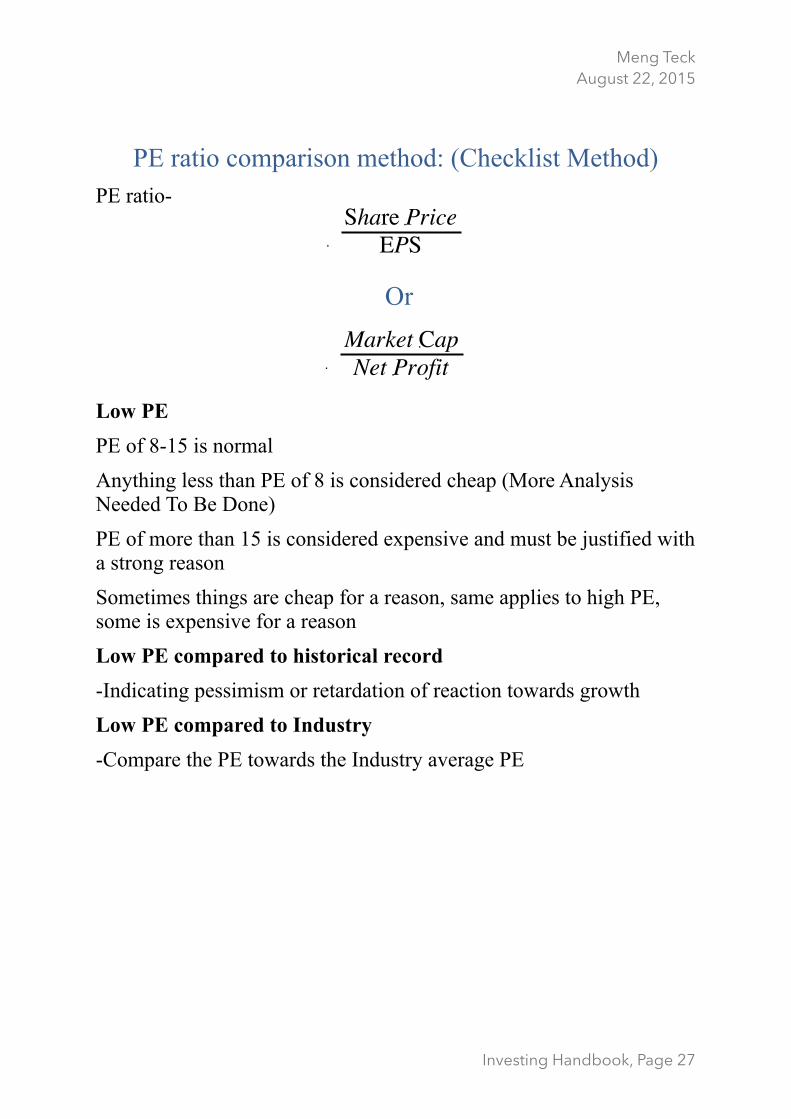

PE ratio comparison method: (Checklist Method) PE ratio-

Or

Low PE PE of 8-15 is normal Anything less than PE of 8 is considered cheap (More Analysis Needed To Be Done) PE of more than 15 is considered expensive and must be justified with a strong reason Sometimes things are cheap for a reason, same applies to high PE, some is expensive for a reason Low PE compared to historical record -Indicating pessimism or retardation of reaction towards growth Low PE compared to Industry -Compare the PE towards the Industry average PE

Investing Handbook, Page �27

Meng Teck August 22, 2015

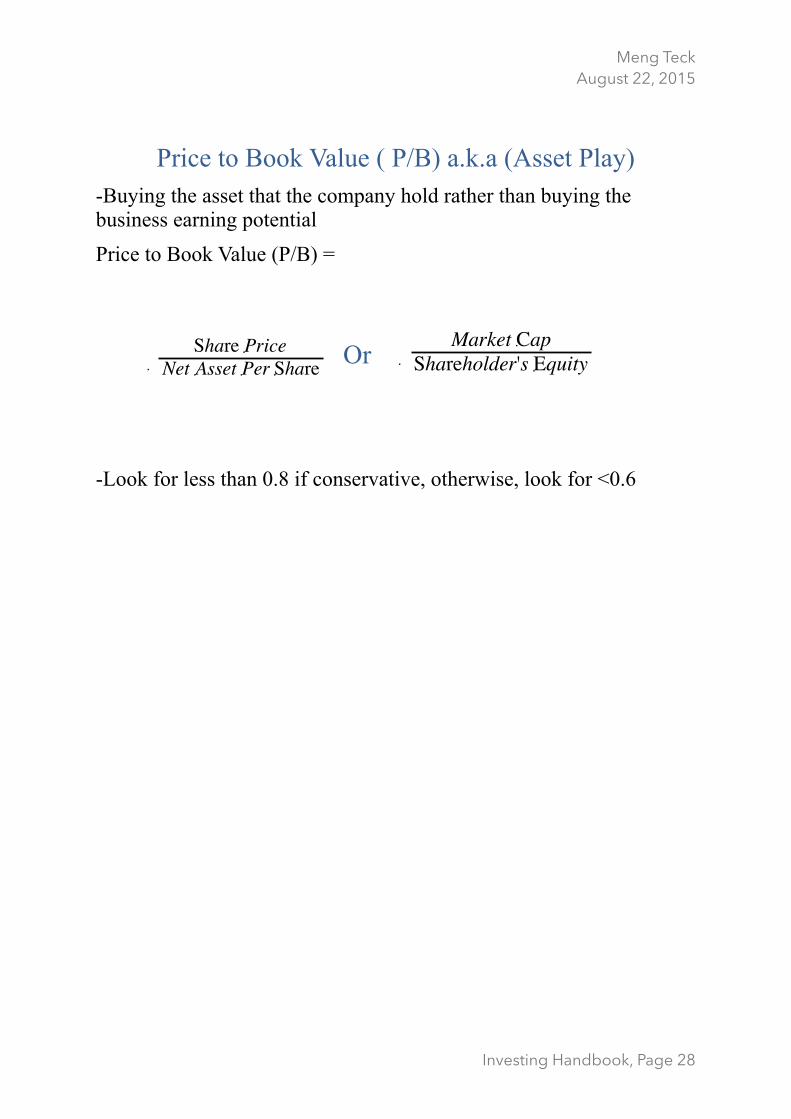

Price to Book Value ( P/B) a.k.a (Asset Play) -Buying the asset that the company hold rather than buying the business earning potential Price to Book Value (P/B) =

Or

-Look for less than 0.8 if conservative, otherwise, look for <0.6

Investing Handbook, Page �28

Meng Teck August 22, 2015

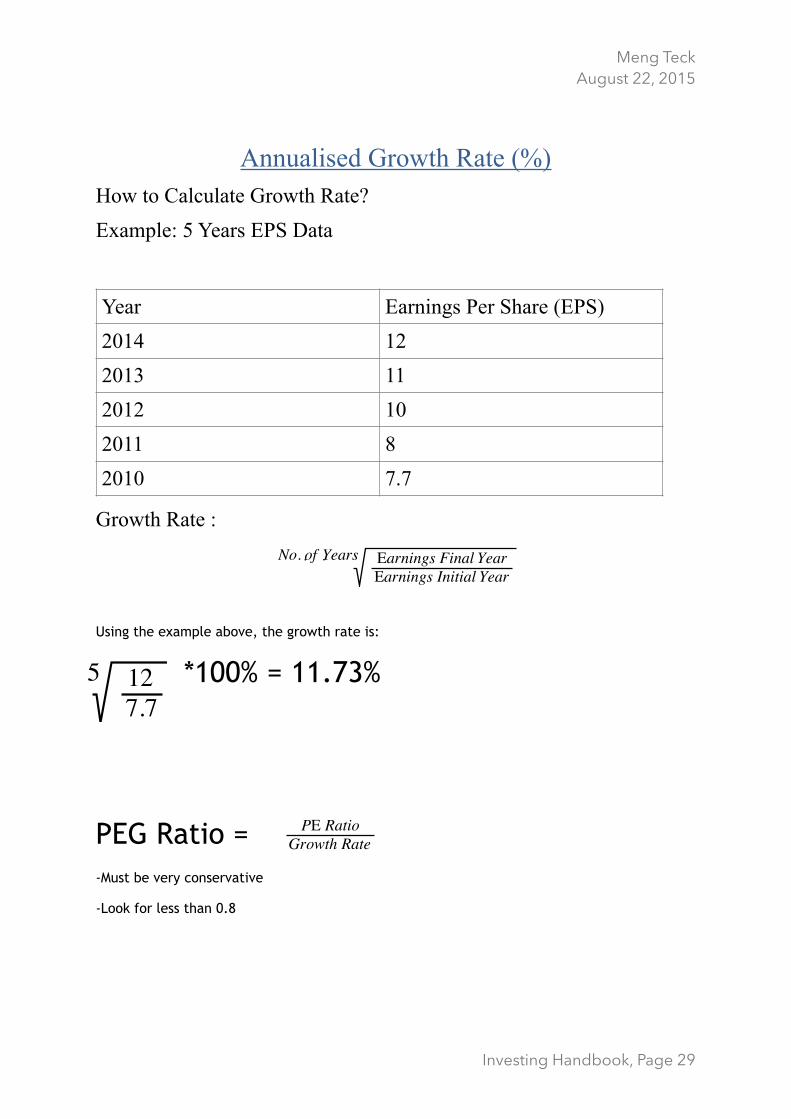

Annualised Growth Rate (%) How to Calculate Growth Rate? Example: 5 Years EPS Data

Growth Rate :

Using the example above, the growth rate is:

*100% = 11.73%

PEG Ratio = -Must be very conservative

-Look for less than 0.8

Year Earnings Per Share (EPS)2014 122013 112012 102011 82010 7.7

Investing Handbook, Page �29

Meng Teck August 22, 2015

10 Years Discounted Cash Flow (DCF)

Intrinsic Value :

a = EPS N = No. of Years , in this case, 10 years. R = 1 – Inflation Rate + Growth Rate – Risk Premium Inflation Rate = 6% or 0.06 Risk Premium = 4% or 0.04 Growth Rate = As calculated previously.

There are plenty of different version for this. You could use different number of year or inflation rate or risk premium or instead of using EPS, you can use the Free Cash Flow. But if you’re using the Free Cash Flow, you need to divide the answer by number of shares to determine how much to pay for the share price.

Investing Handbook, Page �30

Meng Teck August 22, 2015

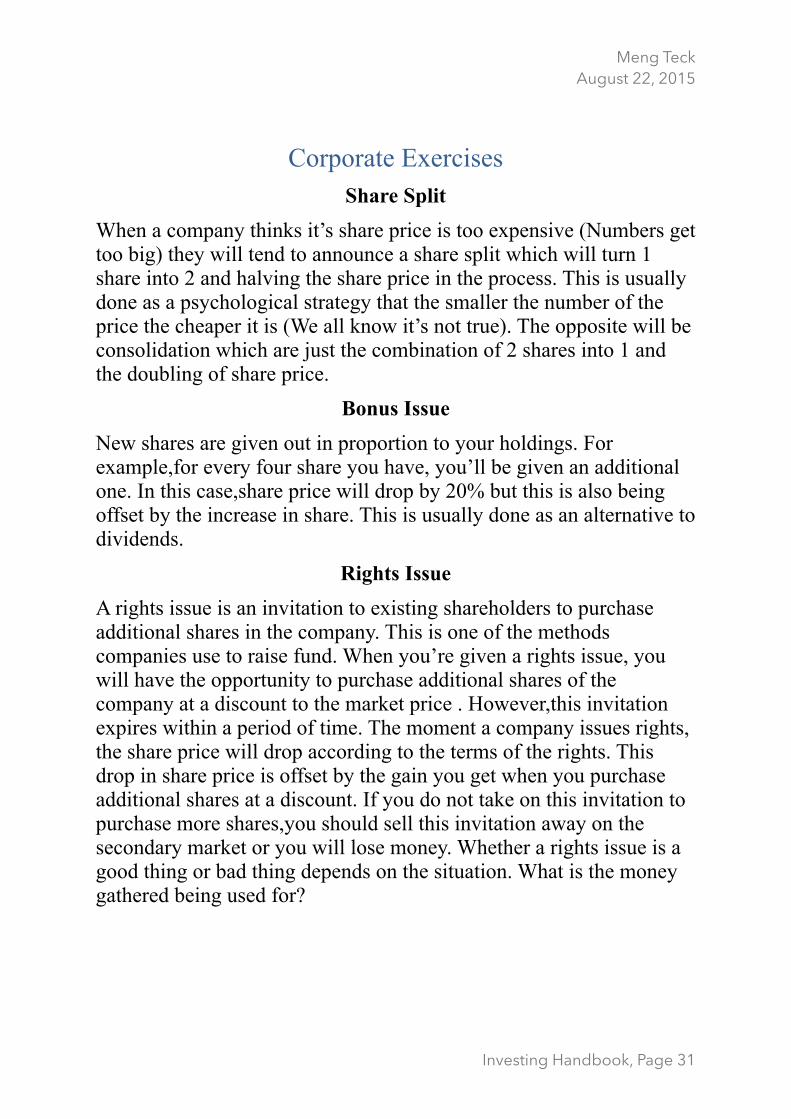

Corporate Exercises Share Split

When a company thinks it’s share price is too expensive (Numbers get too big) they will tend to announce a share split which will turn 1 share into 2 and halving the share price in the process. This is usually done as a psychological strategy that the smaller the number of the price the cheaper it is (We all know it’s not true). The opposite will be consolidation which are just the combination of 2 shares into 1 and the doubling of share price.

Bonus Issue New shares are given out in proportion to your holdings. For example,for every four share you have, you’ll be given an additional one. In this case,share price will drop by 20% but this is also being offset by the increase in share. This is usually done as an alternative to dividends.

Rights Issue A rights issue is an invitation to existing shareholders to purchase additional shares in the company. This is one of the methods companies use to raise fund. When you’re given a rights issue, you will have the opportunity to purchase additional shares of the company at a discount to the market price . However,this invitation expires within a period of time. The moment a company issues rights, the share price will drop according to the terms of the rights. This drop in share price is offset by the gain you get when you purchase additional shares at a discount. If you do not take on this invitation to purchase more shares,you should sell this invitation away on the secondary market or you will lose money. Whether a rights issue is a good thing or bad thing depends on the situation. What is the money gathered being used for?

Investing Handbook, Page �31

Meng Teck August 22, 2015

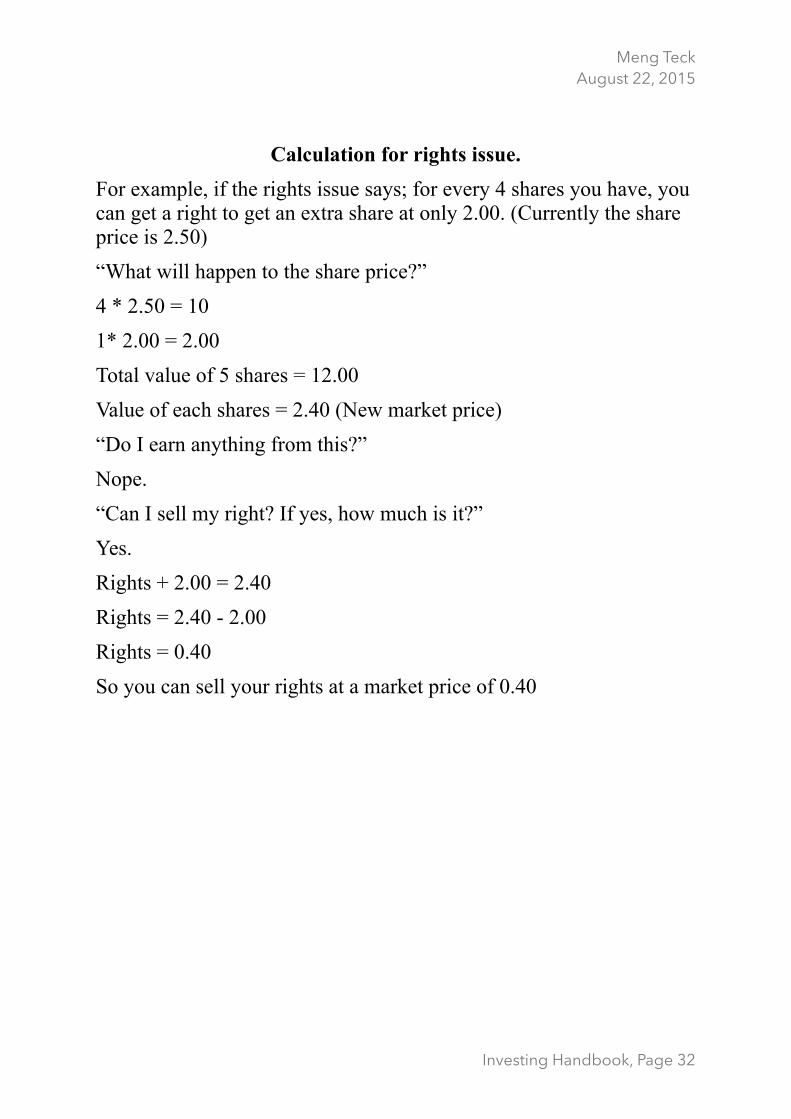

Calculation for rights issue. For example, if the rights issue says; for every 4 shares you have, you can get a right to get an extra share at only 2.00. (Currently the share price is 2.50) “What will happen to the share price?” 4 * 2.50 = 10 1* 2.00 = 2.00 Total value of 5 shares = 12.00 Value of each shares = 2.40 (New market price) “Do I earn anything from this?” Nope. “Can I sell my right? If yes, how much is it?” Yes. Rights + 2.00 = 2.40 Rights = 2.40 - 2.00 Rights = 0.40 So you can sell your rights at a market price of 0.40

Investing Handbook, Page �32

Meng Teck August 22, 2015

“RISK IS IN NOT KNOWING WHAT YOU DO.”

WITH THIS, I WOULD LIKE TO REMIND YOU OF THREE QUOTES BY WARREN BUFFETT

“IT IS FAR BETTER TO BUY A GREAT BUSINESS AT A FAIR PRICE THAN A FAIR BUSINESS AT A CHEAP

PRICE.”

“PRICE IS WHAT YOU PAY,VALUE IS WHAT YOU GET.”

“BE GREEDY WHEN OTHERS ARE FEARFUL, BE FEARFUL WHEN OTHERS ARE GREEDY”

Investing Handbook, Page �33

Meng Teck August 22, 2015

“IN THE SHORT TERM,MARKET IS A VOTING MACHINE, IN THE LONG TERM, MARKET IS A WEIGHING MACHINE.” – BENJAMIN GRAHAM

If you follow this sound investment framework and do not leave these principles (it may seem tempting to speculate gamble on the market but history has shown that people like these will get burnt ), you will be handsomely rewarded if you can FOCUS ON THE LONG TERM .

I hope you will achieve your financial goals much easier by following this method. When you have reached your goals, please do not forget how fortunate we are to be living in a free country that allows us to generate wealth in this relatively easy way. Many, otherwise, ordinary people have attained massive wealth by following these principles, I have seen many of them face to face! Not only will you be able to invest profitably, but you have also picked up the correct mentality and knowledge that is crucial and extremely useful to propel you to be a good businessman should you wish to start your own business. Please do not squander your wealth on meaningless things and do give back to the society. I believe everyone deserve equal chances in life, therefore, please help the less fortunate ones to uplift their lives when you have succeeded.

Happy Investing, See you at the top.

Meng Teck

Investing Handbook, Page �34