Embed Size (px)

Citation preview

No-Shops & Fiduciary Outs:A Survey of 2012 Public Merger Agreements

Robert Little, Travis Souza and Rachel HarrisonDecember 11, 2012

<Presentation Title/Client Name>

2

Precedent Examined

• 53 public company merger agreements

• Signed in 2012 (on or before November 30, 2012)

• Transactions valued at $1 billion or more

<Presentation Title/Client Name>

Go-Shop

Eight agreements—or 15% of the agreements reviewed—provide for a go-shop period.

3

<Presentation Title/Client Name>

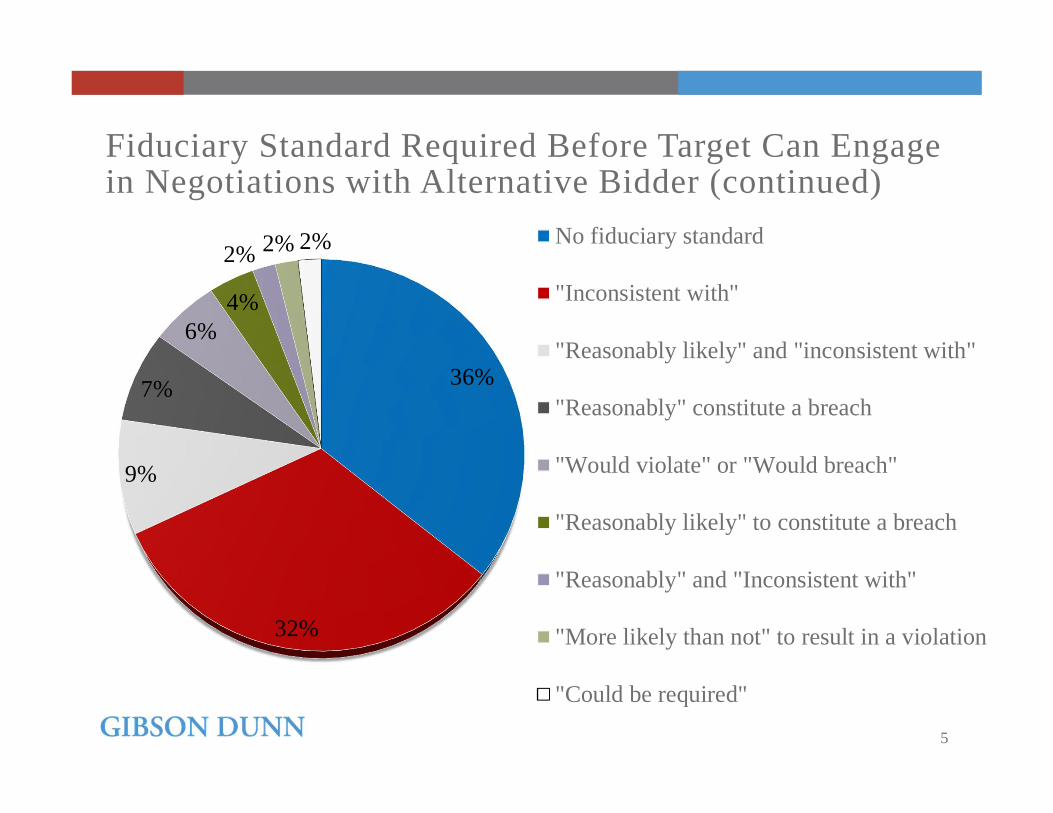

Fiduciary Standard Required Before Target Can Engage in Negotiations with Alternative Bidder• Examples:

– “would be a breach of the Board’s fiduciary duties”– “would be reasonably likely to be inconsistent with the directors’

fiduciary duties”– “would be reasonably likely to result in a breach of the Board’s

fiduciary duties”– “would be inconsistent with the Board’s fiduciary duties”– “could be required by the directors’ fiduciary duties”

4

<Presentation Title/Client Name>

Fiduciary Standard Required Before Target Can Engage in Negotiations with Alternative Bidder (continued)

36%

32%

9%

7%

6%4%

2% 2% 2% No fiduciary standard

"Inconsistent with"

"Reasonably likely" and "inconsistent with"

"Reasonably" constitute a breach

"Would violate" or "Would breach"

"Reasonably likely" to constitute a breach

"Reasonably" and "Inconsistent with"

"More likely than not" to result in a violation

"Could be required"

5

<Presentation Title/Client Name>

Acceptable Confidentiality Agreement with an Alternative Bidder

6

Standard Number (Percentage)“No less favorable” to the target or “not less restrictive” 26 (49.1%)Must permit target to comply with the merger agreement 12 (22.6%)“Customary” 12 (22.6%)Does not have to restrict alternative buyer from making an unsolicited bid 10 (18.9%)Standstill explicitly required 8 (15.1%)“No less favorable in any material respect” 7 (13.2%)“No less favorable in the aggregate” 6 (11.3%)Cannot provide for exclusivity 3 (5.7%)“Substantially similar” 3 (5.7%)“No less favorable in any substantive respect” 2 (3.8%)“Not materially less favorable” to the target 1 (1.9%)“Not materially less restrictive in the aggregate” 1 (1.9%)Standstill provisions not taken into account for purposes of determining whether agreement is acceptable 1 (1.9%)

If less favorable terms, company must offer to amend the parties’ agreement 1 (1.9%)

Standstill provision may be less favorable but, if so, such provision in the parties’ agreement is deemed amended to include such less favorable provision

1 (1.9%)

<Presentation Title/Client Name>

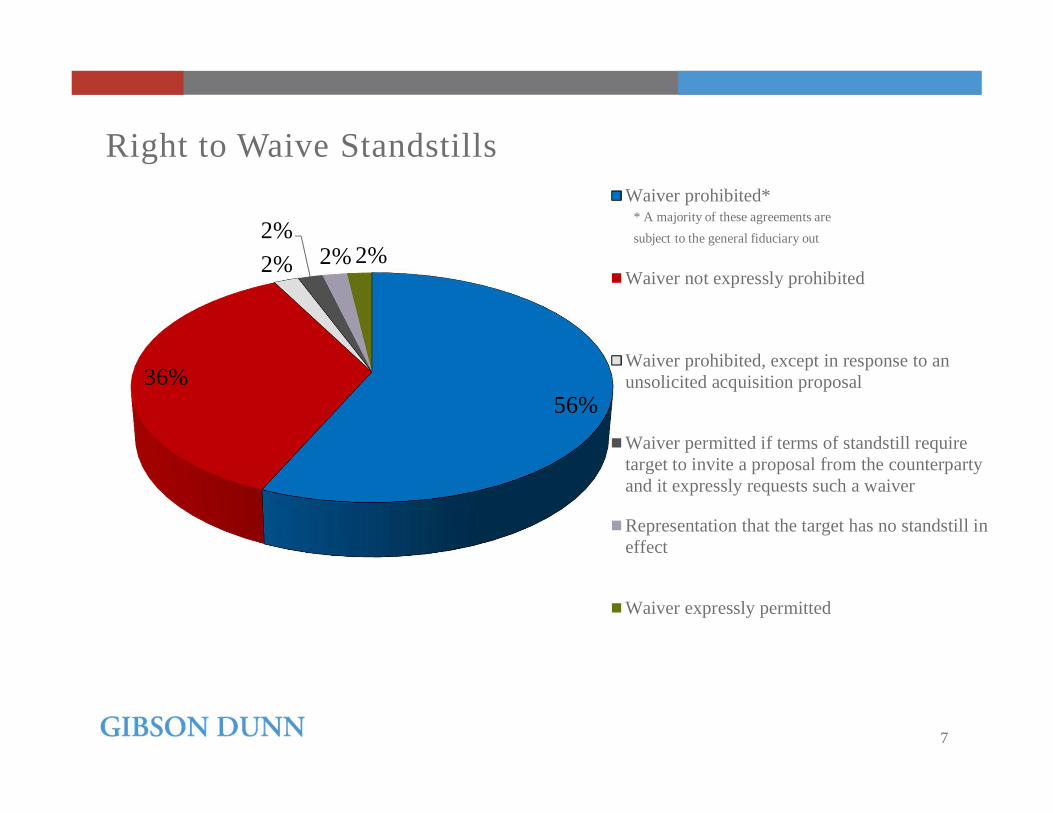

Right to Waive Standstills

7

56%36%

2%2%

2% 2%

Waiver prohibited*

Waiver not expressly prohibited

Waiver prohibited, except in response to anunsolicited acquisition proposal

Waiver permitted if terms of standstill requiretarget to invite a proposal from the counterpartyand it expressly requests such a waiver

Representation that the target has no standstill ineffect

Waiver expressly permitted

* A majority of these agreements are subject to the general fiduciary out

<Presentation Title/Client Name>

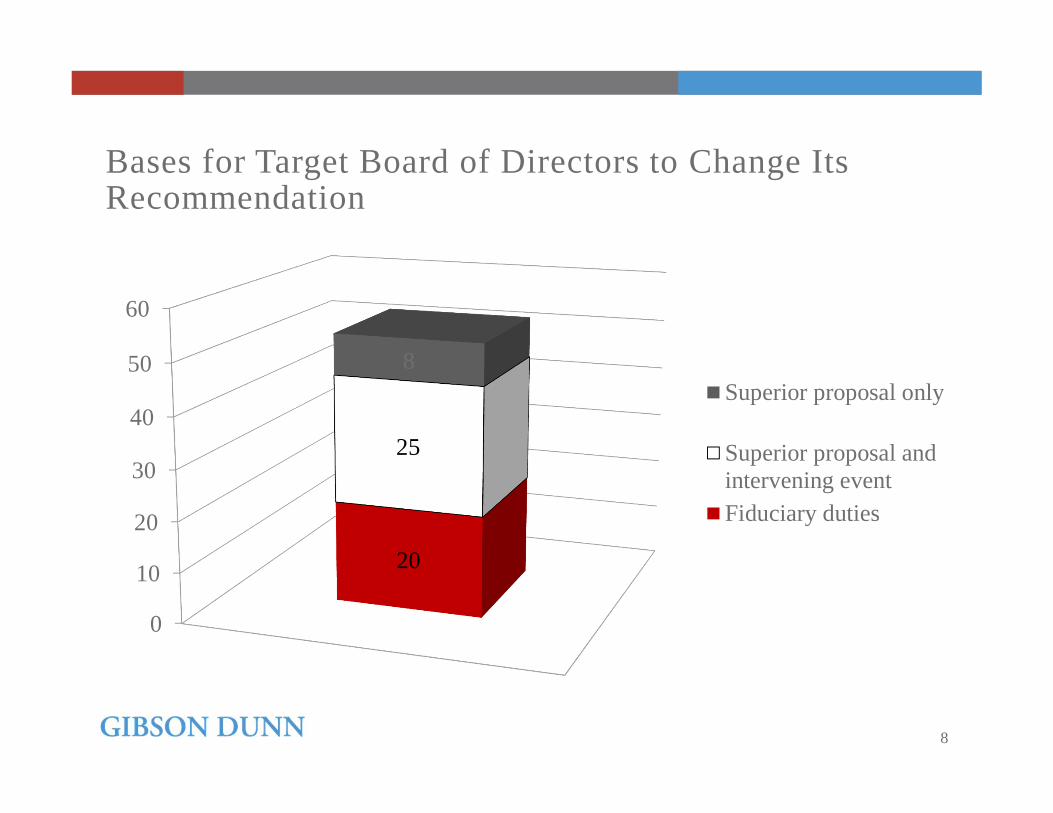

Bases for Target Board of Directors to Change Its Recommendation

8

0

10

20

30

40

50

60

20

25

8Superior proposal only

Superior proposal andintervening eventFiduciary duties

<Presentation Title/Client Name>

Definition of Intervening Event

9

27

17

13

6

20

5

10

15

20

25

30

Was not known bythe target's board as

of the date of theagreement

Is material Was not reasonablyforeseeable

Occurs or arises afterthe date of the

merger agreement

Was not known bythe target's

management as ofthe date of the

agreement

<Presentation Title/Client Name>

Definition of Intervening Event: Exclusions

Exclusions for circumstances relating to: Number (Percentage)

Any acquisition proposal 22 (41.5%)

Federal merger regulations 5 (9.4%)

An increase in the target’s trading price or decrease in the acquiror’s trading price 5 (9.4%)

The acquiror 4 (7.5%)

Actions taken pursuant to or relating to the merger agreement 4 (7.5%)

Changes in markets 2 (3.8%)

A breach by target 1 (1.9%)

Changes in the industry 1 (1.9%)

Announcement of the merger agreement 1 (1.9%)

Changes in law 1 (1.9%)

Failure to meet projections 1 (1.9%)

10

<Presentation Title/Client Name>

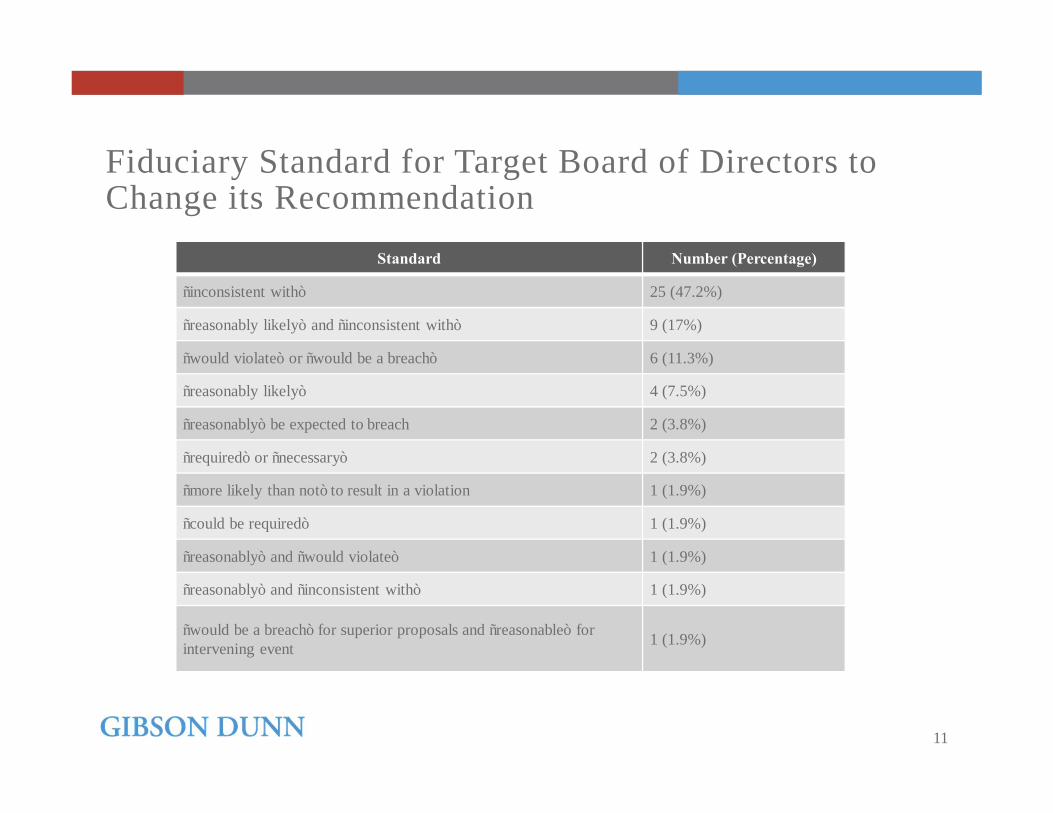

Fiduciary Standard for Target Board of Directors to Change its Recommendation

Standard Number (Percentage)

“inconsistent with” 25 (47.2%)

“reasonably likely” and “inconsistent with” 9 (17%)

“would violate” or “would be a breach” 6 (11.3%)

“reasonably likely” 4 (7.5%)

“reasonably” be expected to breach 2 (3.8%)

“required” or “necessary” 2 (3.8%)

“more likely than not” to result in a violation 1 (1.9%)

“could be required” 1 (1.9%)

“reasonably” and “would violate” 1 (1.9%)

“reasonably” and “inconsistent with” 1 (1.9%)

“would be a breach” for superior proposals and “reasonable” for intervening event 1 (1.9%)

11

<Presentation Title/Client Name>

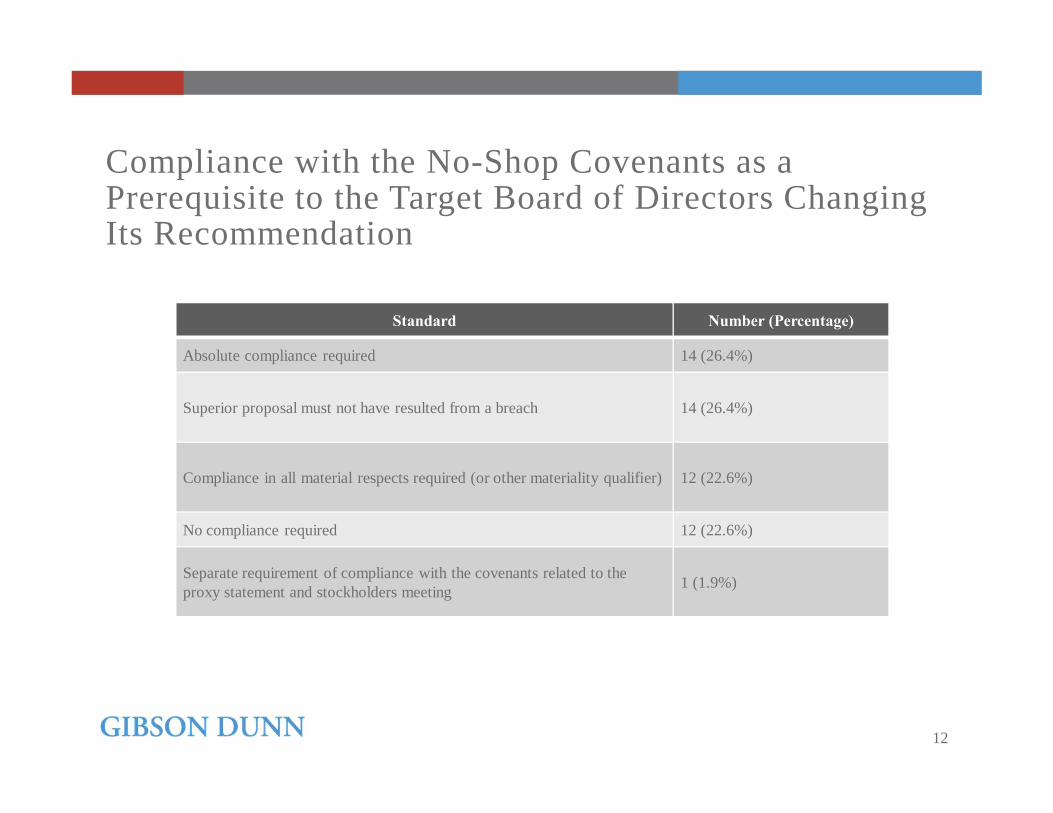

Compliance with the No-Shop Covenants as a Prerequisite to the Target Board of Directors Changing Its Recommendation

Standard Number (Percentage)

Absolute compliance required 14 (26.4%)

Superior proposal must not have resulted from a breach 14 (26.4%)

Compliance in all material respects required (or other materiality qualifier) 12 (22.6%)

No compliance required 12 (22.6%)

Separate requirement of compliance with the covenants related to the proxy statement and stockholders meeting 1 (1.9%)

12

<Presentation Title/Client Name>

Trigger for “Acquisition Proposal”

13

05

101520253035

25% 20% 15% for thetarget; 20%

for eachsubsidiary

15% 10% ofequity

securities orvoting

power; 15%of assets

3

32

1

16

1

<Presentation Title/Client Name>

Trigger for “Superior Proposal”

61%10%

11%

2% 6%

4% 2%2%

2%

50%

75%

50% of equity securities or votingpower; all or a substantially allassets50.10%

80%

Majority of outstanding commonstock

Majority of common stock or assets

All outstanding equity securities

All outstanding common stock; allor substantially all assets

14

<Presentation Title/Client Name>

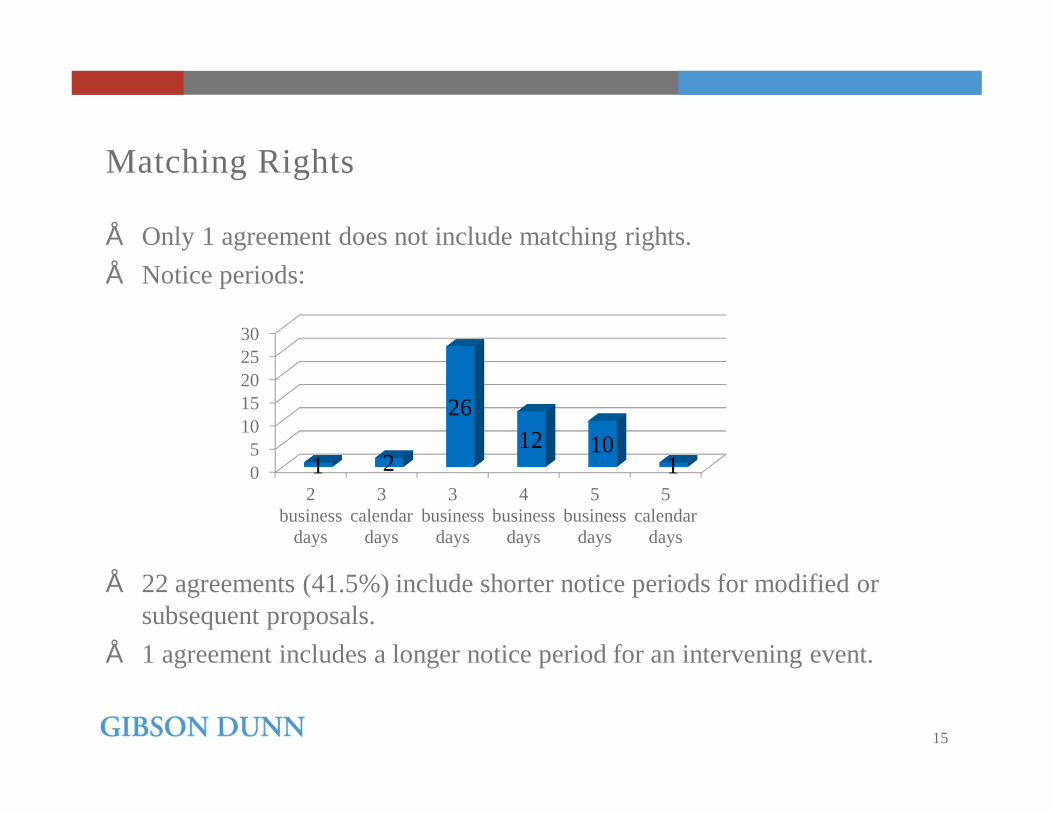

Matching Rights

• Only 1 agreement does not include matching rights.• Notice periods:

• 22 agreements (41.5%) include shorter notice periods for modified or subsequent proposals.

• 1 agreement includes a longer notice period for an intervening event.

15

05

1015202530

2business

days

3calendar

days

3business

days

4business

days

5business

days

5calendar

days

1 2

2612 10

1

<Presentation Title/Client Name>

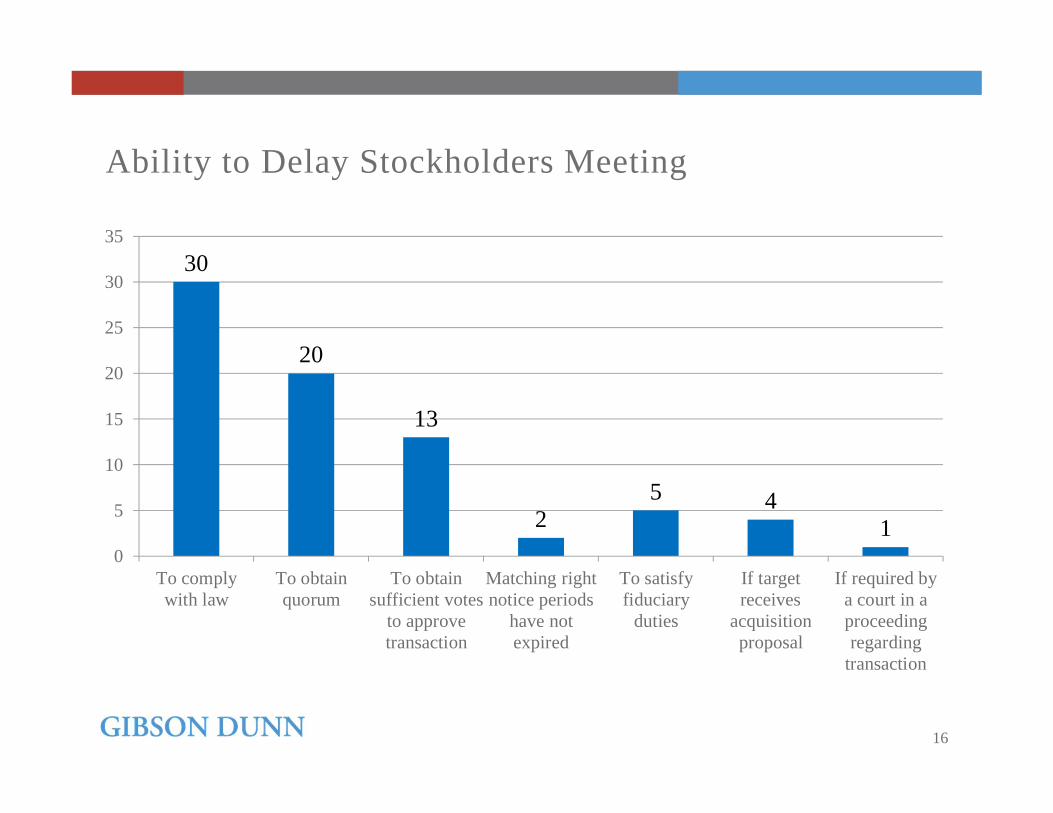

Ability to Delay Stockholders Meeting

16

30

20

13

25 4

10

5

10

15

20

25

30

35

To complywith law

To obtainquorum

To obtainsufficient votes

to approvetransaction

Matching rightnotice periods

have notexpired

To satisfyfiduciary

duties

If targetreceives

acquisitionproposal

If required bya court in aproceedingregarding

transaction

<Presentation Title/Client Name>

Force the Vote

• 4 agreements include force the vote provisions (i.e., the target is not permitted to terminate to enter into a superior proposal).

• 49 agreements do not include force the vote provisions (i.e., the target is permitted to terminate to enter into a superior proposal).

17

<Presentation Title/Client Name>

Force the Vote (continued)

In agreements that do not include force the vote provisions:

18

22

16

1 10

5

10

15

20

25

Ability to terminatesubject to absolute

compliance with no-shopcovenants

Ability to terminatesubject to material

compliance with no-shopcovenants

Superior proposal mustnot have resulted from a

breach of the no-shopcovenants

Separate requirement ofcompliance with the proxy

statement andstockholders meeting

covenants

<Presentation Title/Client Name>

Acquiror’s Separate Right to Terminate for the Target’s Breach of the No-Shop Covenants

19

• 17 agreements did not include a separate right to terminate.• The remaining agreements included a right to terminate for:

31

8

1 1 10

5

10

15

20

25

30

35

Breach of the no-shop covenants in

any materialrespect*

Breach of the proxystatement and

stockholder meetingcovenants in anymaterial respect

Any willful breachof no-shopcovenants

Any knowing andwillful breach of no-

shop covenants

Any breach of theno-shop covenants

* Of such 31, two require willfulness, two require intent, and one requires knowledge and willfulness

<Presentation Title/Client Name>

Triggers for Break-Up Fee

• All 53 agreements require the payment of a break-up fee if the acquiror terminates the agreement because the target board of directors changes its recommendation.

• 49 agreements require the payment of a break-up fee if the target terminates in order to enter into a superior proposal.

• Other break-up fee triggers include:– Target’s breach of the no-shop covenants—28 (53%)– Target’s breach of the proxy statement and stockholders meeting covenants—

12 (22.7%)– Target’s stockholders fail to approve the transaction—2 (3.8%)– The outside date passes at a time when the acquiror is entitled to terminate

because of target’s change in recommendation—1 (1.9%)– A tender offer is initiated—1 (1.9%)– A related party breaches a support agreement—1 (1.9%)

20

<Presentation Title/Client Name>

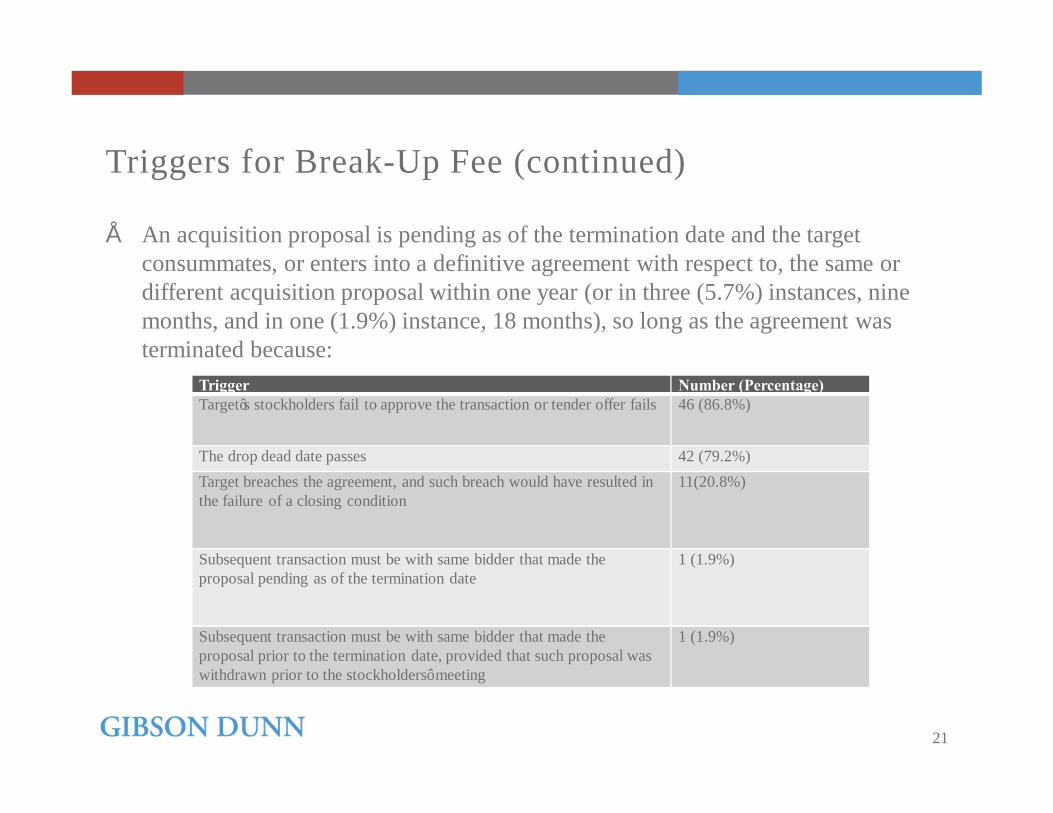

Triggers for Break-Up Fee (continued)

• An acquisition proposal is pending as of the termination date and the target consummates, or enters into a definitive agreement with respect to, the same or different acquisition proposal within one year (or in three (5.7%) instances, nine months, and in one (1.9%) instance, 18 months), so long as the agreement was terminated because:

21

Trigger Number (Percentage)Target’s stockholders fail to approve the transaction or tender offer fails 46 (86.8%)

The drop dead date passes 42 (79.2%)Target breaches the agreement, and such breach would have resulted in the failure of a closing condition

11(20.8%)

Subsequent transaction must be with same bidder that made the proposal pending as of the termination date

1 (1.9%)

Subsequent transaction must be with same bidder that made the proposal prior to the termination date, provided that such proposal was withdrawn prior to the stockholders’ meeting

1 (1.9%)

<Presentation Title/Client Name>

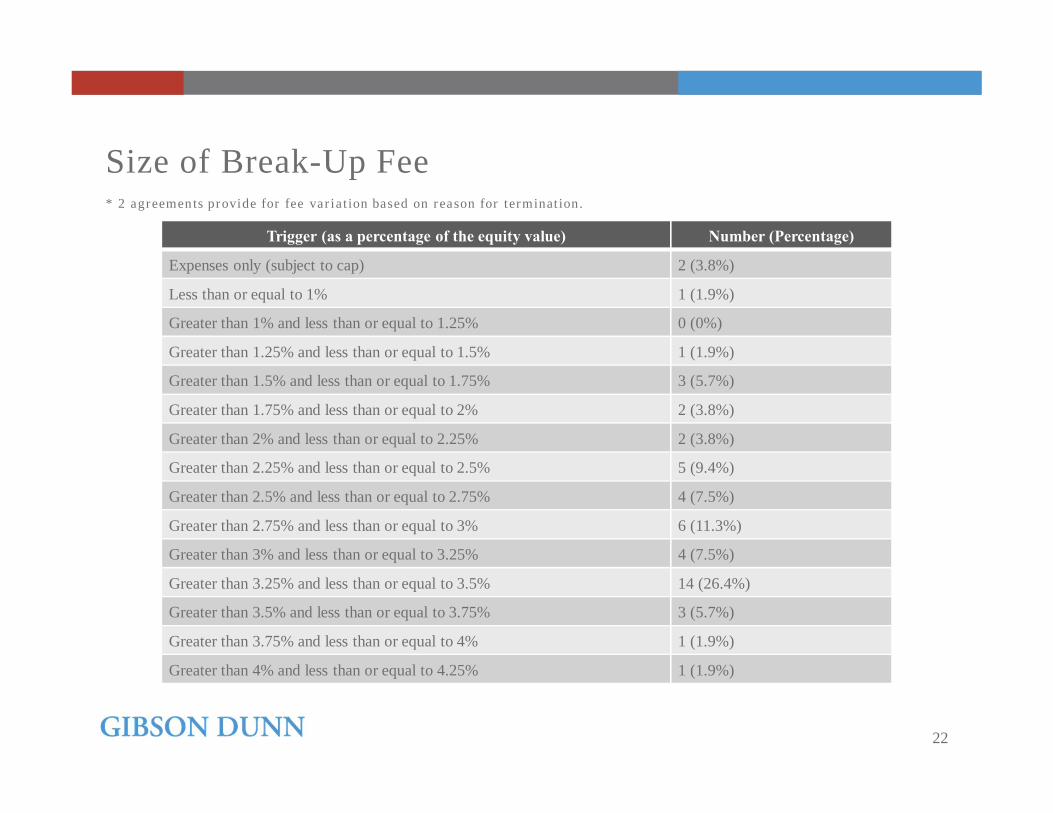

Size of Break-Up Fee* 2 agreemen ts provide for fee var ia t ion based on r eason for terminat ion.

22

Trigger (as a percentage of the equity value) Number (Percentage)

Expenses only (subject to cap) 2 (3.8%)

Less than or equal to 1% 1 (1.9%)

Greater than 1% and less than or equal to 1.25% 0 (0%)

Greater than 1.25% and less than or equal to 1.5% 1 (1.9%)

Greater than 1.5% and less than or equal to 1.75% 3 (5.7%)

Greater than 1.75% and less than or equal to 2% 2 (3.8%)

Greater than 2% and less than or equal to 2.25% 2 (3.8%)

Greater than 2.25% and less than or equal to 2.5% 5 (9.4%)

Greater than 2.5% and less than or equal to 2.75% 4 (7.5%)

Greater than 2.75% and less than or equal to 3% 6 (11.3%)

Greater than 3% and less than or equal to 3.25% 4 (7.5%)

Greater than 3.25% and less than or equal to 3.5% 14 (26.4%)

Greater than 3.5% and less than or equal to 3.75% 3 (5.7%)

Greater than 3.75% and less than or equal to 4% 1 (1.9%)

Greater than 4% and less than or equal to 4.25% 1 (1.9%)

<Presentation Title/Client Name>

Expense Reimbursement

• 30 (56.6%) agreements provide for expense reimbursement.• 9 (17%) agreements provide for mutual expense reimbursement.• 19 (35.8%) agreements provide for expense reimbursement paid solely by

target.• 2 (3.8%) agreements provide for expense reimbursement paid solely by

acquiror.

23

<Presentation Title/Client Name>

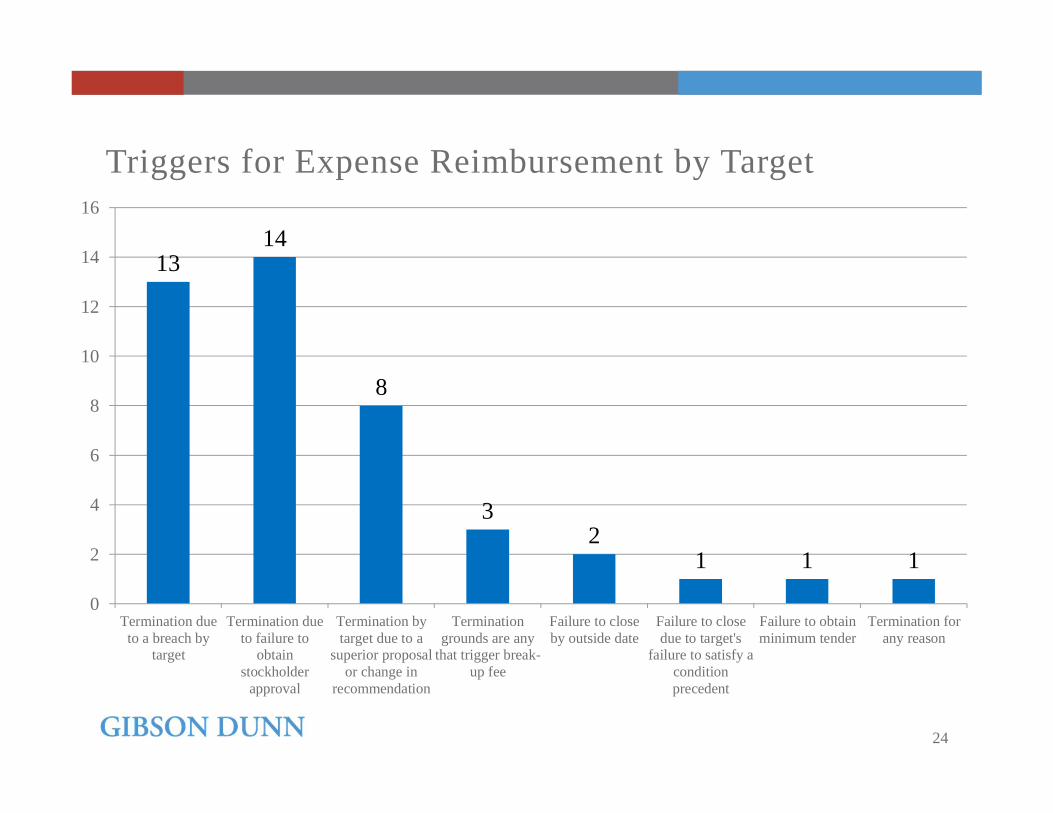

Triggers for Expense Reimbursement by Target

1314

8

32

1 1 1

0

2

4

6

8

10

12

14

16

Termination dueto a breach by

target

Termination dueto failure to

obtainstockholder

approval

Termination bytarget due to a

superior proposalor change in

recommendation

Terminationgrounds are any

that trigger break-up fee

Failure to closeby outside date

Failure to closedue to target's

failure to satisfy aconditionprecedent

Failure to obtainminimum tender

Termination forany reason

24

<Presentation Title/Client Name>

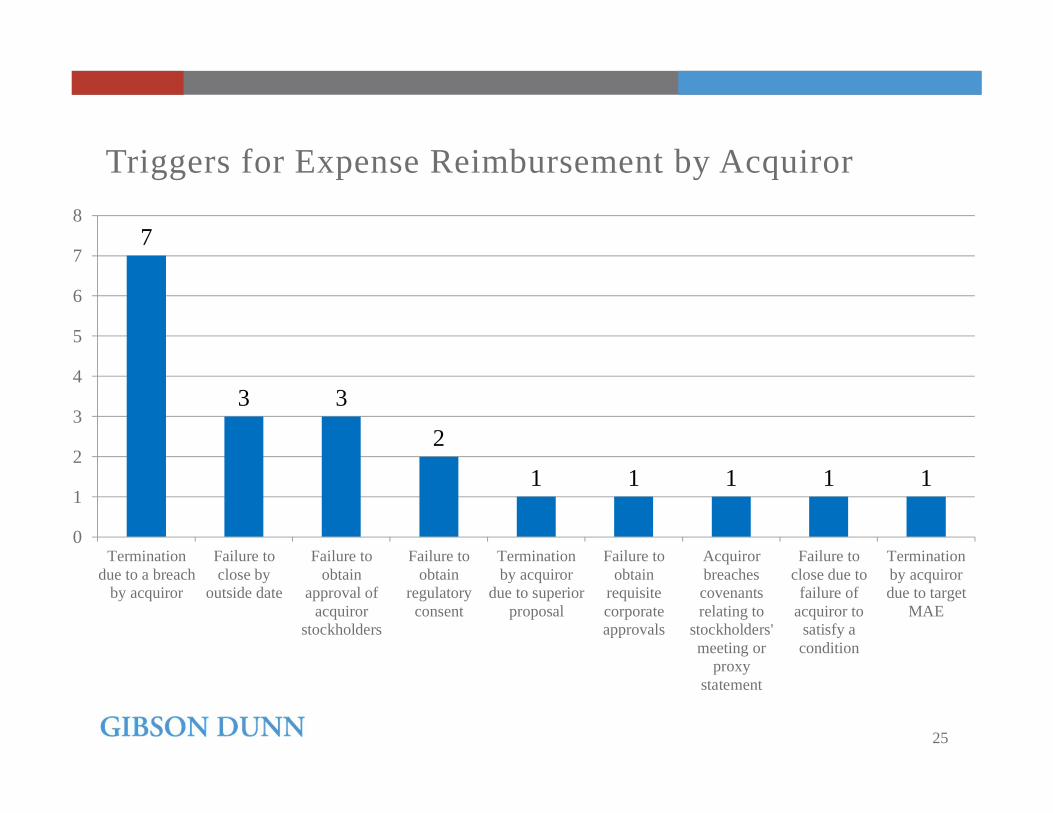

Triggers for Expense Reimbursement by Acquiror

7

3 3

2

1 1 1 1 1

0

1

2

3

4

5

6

7

8

Terminationdue to a breach

by acquiror

Failure toclose by

outside date

Failure toobtain

approval ofacquiror

stockholders

Failure toobtain

regulatoryconsent

Terminationby acquiror

due to superiorproposal

Failure toobtain

requisitecorporateapprovals

Acquirorbreachescovenantsrelating to

stockholders'meeting or

proxystatement

Failure toclose due to

failure ofacquiror to

satisfy acondition

Terminationby acquirordue to target

MAE

25

<Presentation Title/Client Name>

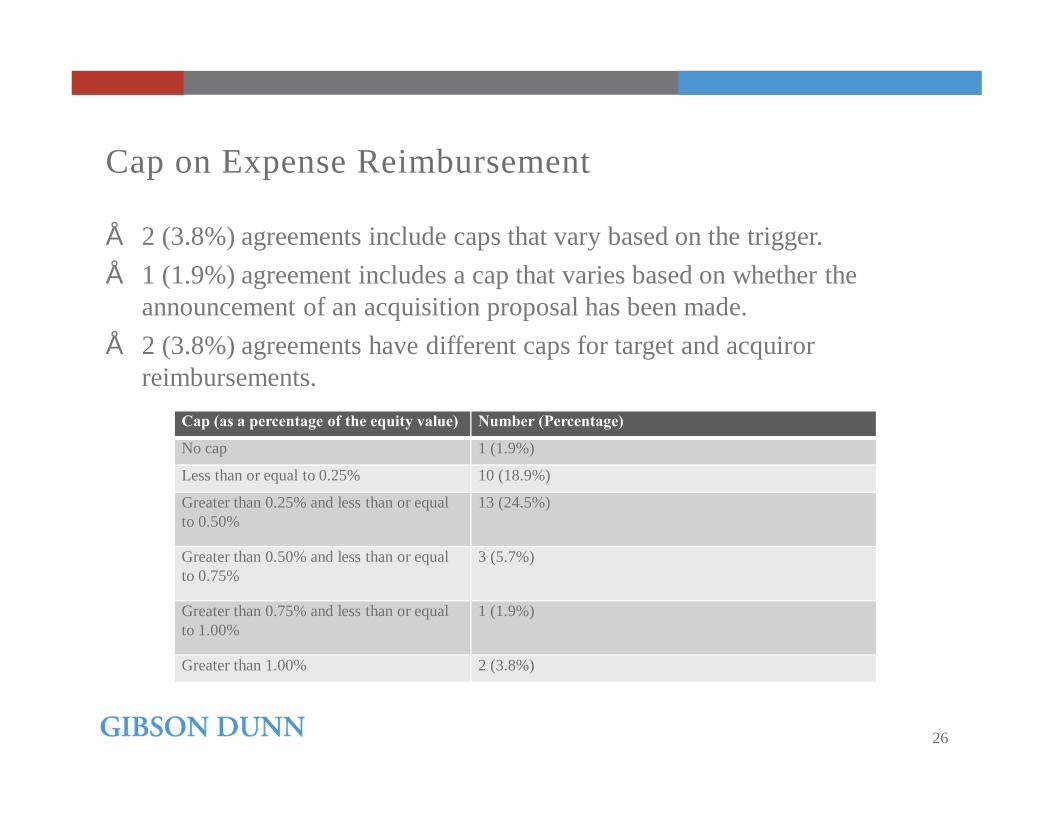

Cap on Expense Reimbursement

• 2 (3.8%) agreements include caps that vary based on the trigger.• 1 (1.9%) agreement includes a cap that varies based on whether the

announcement of an acquisition proposal has been made.• 2 (3.8%) agreements have different caps for target and acquiror

reimbursements.

26

Cap (as a percentage of the equity value) Number (Percentage)

No cap 1 (1.9%)

Less than or equal to 0.25% 10 (18.9%)

Greater than 0.25% and less than or equal to 0.50%

13 (24.5%)

Greater than 0.50% and less than or equal to 0.75%

3 (5.7%)

Greater than 0.75% and less than or equal to 1.00%

1 (1.9%)

Greater than 1.00% 2 (3.8%)

<Presentation Title/Client Name>

Professional Profile

Rob Little is a partner in Gibson, Dunn & Crutcher’s Dallas office. He is a member of the firm’s Mergers and Acquisitions, Capital Markets, Energy and Infrastructure, Private Equity, Securities Regulation and Corporate Governance, Global Finance, and Corporate Transactions practice groups. Mr. Little serves on the Gibson Dunn Hiring Committee and is the hiring partner for theDallas office.Consistently recognized as a “Rising Star” by Texas Monthly, Mr. Little’s practice focuses on corporate transactions, including mergers and acquisitions, securities offerings, joint ventures, investments in public and private entities, and commercial transactions. He also advises business organizations regarding matters such as securities law disclosure, corporate governance, and fiduciary obligations. In addition, he represents investment funds and their sponsors along with investors in such funds. Mr. Little has represented clients in a variety of industries, including energy, retail, technology, transportation, manufacturing, and financial services. Mr. Little received his law degree in 1998 with highest honors from The University of Texas School of Law, where he was named a Chancellor and a member of Order of the Coif and served as Articles Editor of the Texas Law Review. He also holds a B.A. from Baylor University, where he graduated summa cum laude in 1995.Prior to joining Gibson Dunn in 2011, Mr. Little was a partner in the Dallas office of Vinson & Elkins. He previously served as a law clerk to The Honorable Patrick Higginbotham of the U.S. Court of Appeals for the Fifth Circuit.Mr. Little is a member of the Dallas Bar Association and is admitted to practice in Texas. He is a frequent speaker on corporate law matters.

27

Contact:2100 McKinney AvenueDallas, Texas 75201Tel: [email protected]

Robert B. Little

<Presentation Title/Client Name>

Professional Profile

Travis Souza is an associate in the Dallas office of Gibson, Dunn & Crutcher LLP. He is a member of the firm's Corporate Transactions, Mergers and Acquisitions, Securities Regulation and Corporate Governance, Energy and Infrastructure and PrivateEquity practice groups. Mr. Souza also serves on the Gibson Dunn Hiring Committee.

Mr. Souza’s practice focuses on corporate transactions, including mergers and acquisitions, private equity investments, and joint ventures. He advises public and private clients in connection with complex asset and equity transactions ranging across a variety of industries. He also assists these clients with securities law, corporate governance, and general corporate matters.

Mr. Souza earned his law degree, magna cum laude, from Duke University School of Law in 2008, where he was a member of the Order of the Coif and an editor for the Duke Law Journal. While at Duke he participated in the Community Enterprise Clinic, providing assistance to non-profit organizations and low-wealth entrepreneurs working to improve the quality of life in low-wealth communities. He also holds a Bachelor of Arts degree in Accounting from Michigan State University where he graduated with high honors.

Mr. Souza is admitted to practice in the State of Texas.

28

Contact:2100 McKinney AvenueDallas, Texas 75201Tel: [email protected]

Travis S. Souza

<Presentation Title/Client Name>

Professional Profile

Rachel Harrison is an associate in the Dallas office of Gibson, Dunn & Crutcher LLP. She is a member of the firm’s Corporate Department and practices in the Capital Markets, Mergers and Acquisitions, and Energy and Infrastructure Practice Groups.

Prior to joining the firm, Ms. Harrison was an associate at Thompson & Knight, where she focused her practice on oil and gas transactions. Ms. Harrison also served as a stagiaire in the cabinet of M. le juge Allan Rosas at the European Court of Justice. Prior to law school, Ms. Harrison was an intern for the United States Attorney for the Western District of Louisiana.

Ms. Harrison received her law degree magna cum laude in 2010 from the SMU Dedman School of Law, where she was a member of the Order of the Coif. While in law school, she served as an editor of the SMU Law Review and then president of the SMU Law Review Association. She earned her Bachelor of Arts in history from Duke University.

A member of the Dallas Bar Association and the American Bar Association, Ms. Harrison is admitted to practice in Texas.

Ms. Harrison serves on the Alumni Admissions Advisory Committee for Duke University and is a member of the Dallas World Affairs Council.

29

Contact:2100 McKinney AvenueDallas, Texas 75201Tel: [email protected]

Rachel F. Harrison

<Presentation Title/Client Name>

3030

What Legal Industry Observers are Saying…

Gibson Dunn is ranked in the Top 10 Law Firms nationally by general counsel at major corporations

when asked which firms they would most want to represent their companies on national matters by

Corporate Board Member Magazine.

The Best Lawyers in America 2012 identified 105 Gibson Dunn partners as leading in 44 practice areas.

Eight Gibson Dunn partners were named 2012 Lawyer of the Year in their respective practice area.

PLC Which Lawyer? – Global 50 named Gibson Dunn one of the Global 50 firms in its most recent Yearbook.

Gibson Dunn also achieved 58 individual lawyer endorsements in various practice areas.

The American Lawyer has once again named Gibson Dunn the winner of its sixth biennial “Litigation

Department of the Year” competition. This honor represents a back-to-back win for Gibson Dunn, and

marks the first time a law firm has won the competition twice. In selecting Gibson Dunn as the “Litigation

Department of the Year,” The American Lawyerrecognized the Firm’s “stack of victories in some of the country’s thorniest cases” and noted the “brains, bench

strength, and bravado” of its top litigators.

Gibson Dunn received 35 practice category rankings, including six top-tier rankings, in the 2012 edition of The Legal 500 -- United States, and 11 partners were

recognized as Leading Lawyers in their respective practices.

<Presentation Title/Client Name>

Mergers & Acquisitions Practice

Gibson Dunn is consistently ranked among the Top 10 US Corporate Law Firms by Corporate Board Member.

Gibson Dunn is one of the leading international law firms representing companies, financial sponsors and financial advisors in complex M&A transactions. Gibson Dunn has been involved in many high-profile acquisitions and divestitures representing both acquirers and targets, as well as financial sponsors and investment banking firms and other financial advisors worldwide.

Depth. The firm’s practice has more than 60 partners and a total of nearly 250 lawyers specializing in M&A transactions spread across our 9 domestic and 8 foreign offices. Gibson Dunn’s size and geographic diversity is a distinct advantage when assisting our M&A clients.

Transactional Expertise. We handle all types of M&A transactions, including mergers of public and private companies, stock and asset purchases, tender and exchange offers, restructurings and acquisitions out of bankruptcy, leveraged buyouts and private equity investments, strategic investments and joint ventures, and cross-border M&A transactions. We have been involved in all aspects of both friendly and hostile transactions, including the structuring of acquisitions, divestitures and spin-offs, advising regarding anti-takeover defenses and proxy contests, and representing special committees of boards of directors.

Practice Integration. Our M&A lawyers work seamlessly with our capital markets, finance, tax, antitrust, employment, environmental, intellectual property, governmental and other experts to ensure that our client’s transaction is given the benefit of all the firm’s resources and collective knowledge.

31

<Presentation Title/Client Name>

BrusselsAvenue Louise 4801050 BrusselsBelgium+32 2 554 70 00

Century City2029 Century Park EastLos Angeles, CA 90067-3026United States+1 310 552 8500

Dallas2100 McKinney AvenueDallas, TX 75201-6912United States+1 214 698 3100

Denver1801 California StreetDenver, CO 80202-2642United States+1 303 298 5700

DubaiThe Exchange Building 5, Level 4Dubai International Finance CentreP.O. Box 506654Dubai, United Arab Emirates+971 4 370 0311

Hong KongRoom 3302, 33/FGloucester TowerThe Landmark15 Queen's Road CentralHong Kong +852 2214 3700

LondonTelephone House2-4 Temple AvenueLondon EC4Y 0HBEngland+44 20 7071 4000

Los Angeles333 South Grand AvenueLos Angeles, CA 90071-3197United States+1 213 229 7000

MunichWidenmayerstraße 10D-80538 MünchenGermany+49 89 189 33-0

New York200 Park AvenueNew York, NY 10166-0193United States+1 212 351 4000

Orange County3161 Michelson DriveIrvine, CA 92612-4412United States+1 949 451 3800

Palo Alto1881 Page Mill RoadPalo Alto, CA 94304-1125United States+1 650 849 5300

Paris166, rue du faubourg Saint Honoré75008 ParisFrance+33 1 56 43 13 00

São PauloRua Funchal, 418, 35°andarSao Paulo 04551-060Brazil+55 (11)3521-7160

San Francisco555 Mission StreetSan Francisco, CA 94105-2933United States+1 415 393 8200

SingaporeOne Raffles QuayLevel #37-01, North TowerSingapore 048583+65 6507 3600

Washington, D.C.1050 Connecticut Avenue, N. W.Washington, D.C. 20036-5306United States+1 202 955 8500

32

Our Offices